These Analysts Increase Their Forecasts On Dycom Industries After Upbeat Q2 Earnings

Dycom Industries, Inc. ![]() DY reported better-than-expected second quarter FY25 results on Wednesday.

DY reported better-than-expected second quarter FY25 results on Wednesday.

Contract revenue increased 15.5% Y/Y to $1.203 billion, beating the consensus of $1.196 billion. Adjusted EBITDA increased to $158.3 million from $130.8 million a year ago. Adjusted EPS of $2.46 surpassed the street view of $2.26.

For the third quarter, Dycom anticipates a mid- to high single-digit percentage increase in total contract revenues, which included the company expectation of around $75 million of acquired contract revenues for the quarter.

In a separate release, Dycom revealed the acquisition of Black & Veatch's public carrier wireless telecom infrastructure business, expanding its reach into nine states and boosting its capabilities in wireless network modernization.

Dycom shares fell 2.4% to trade at $175.20 on Thursday.

These analysts made changes to their price targets on Dycom following earnings announcement.

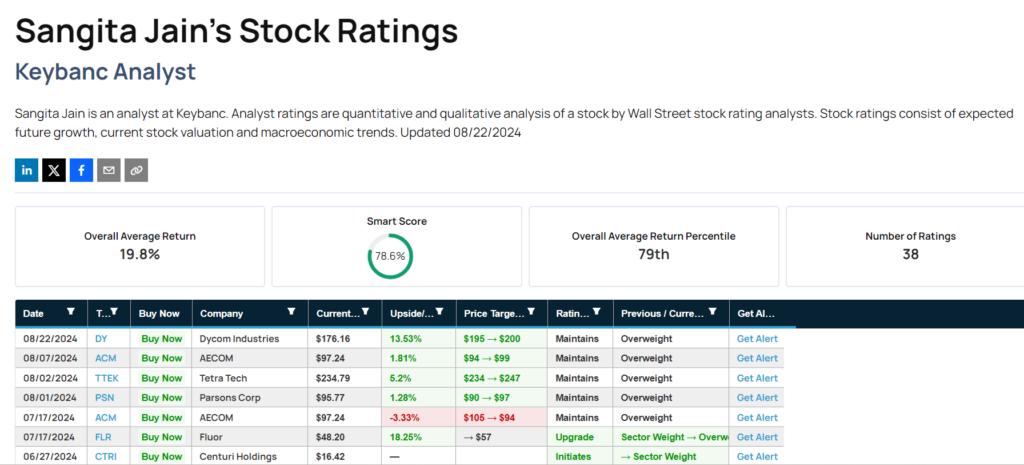

Keybanc analyst Sangita Jain maintained Dycom Industries with an Overweight and raised the price target from $195 to $200.

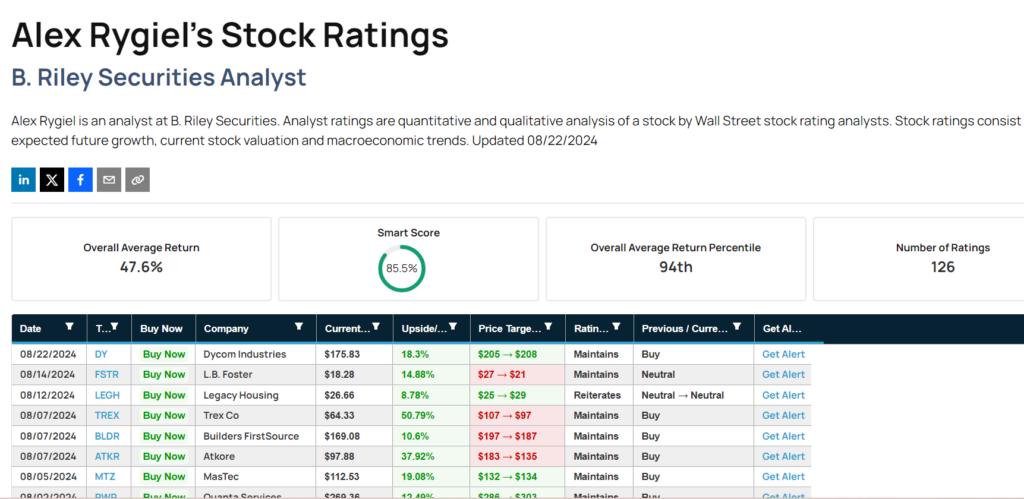

B. Riley Securities analyst Alex Rygiel maintained Dycom with a Buy and raised the price target from $205 to $208.

Read More:

- Toll Brothers To Rally Around 19%? Here Are 10 Top Analyst Forecasts For Thursday

Latest Ratings for DY

| Date | Firm | Action | From | To |

|---|---|---|---|---|

| Mar 2022 | Wells Fargo | Maintains | Overweight | |

| Jan 2022 | UBS | Initiates Coverage On | Buy | |

| Nov 2021 | B. Riley Securities | Maintains | Buy |

View More Analyst Ratings for DY

View the Latest Analyst Ratings

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.