PepsiCo: A Great Long-Term Value Play

Introduction

In times of lots of uncertainty, when most investors are focused on high-growth industries like AI, it might make sense to diversify into more defensive companies in the case of an economic downturn. PepsiCo (NASDAQ: PEP) currently seems like an attractive investment in this space due to its comparably cheap valuation.

Fundamentals

Growth and Profitability

Pepsi currently shows above-average profitability at a gross profit margin of 54.74% vs. an industry average of only 37.56%. Furthermore, the company has higher than average EBITDA margins of 18.11%, while its biggest standout is the incredibly high ROE of 49.64%, almost 5 times that of its sector, indicating still great investment opportunities. This is further amplified by 0.87% forward ROE growth, which is not great but still higher than the otherwise stagnating industry. While forward revenue growth is only at 1.17% and forward EBITDA growth at 3.43%, that of the industry is slightly higher at 3.44% and 5.1%, respectively. While it would be nice to see some more growth, the most important factor for the beverage sector is valuation, as the sector is very unlikely to see high growth rates that could really move investment returns.

Valuation

When looking at valuation, PEP currently has an EV/EBITDA ratio of 13.71, above the industry average. The reason for this is likely the high quality of Pepsi as a company, which is why a peer group comparison is very important. The same can be said for the P/S and P/B ratios of 2.05 and 10.19, respectively. Nevertheless, the company's P/E ratio is currently at 20.07 with a forward P/E of 17.32. This is not under the industry average, but historically very low. When looking at Figure 1, one can see the P/E ratio of Pepsi over time. Interestingly, it has only been below the 20 level in 1 of the last 7 years, with the median level at 26.46 in 2019. This would indicate a potential 31.84% upside potential just to reach this level again.

#

Peer Group Comparison

When comparing Pepsi to other companies, some that instantly come to mind are Coca-Cola (NYSE: KO), Nestle (NSRGY), and Keurig Dr Pepper (NASDAQ: KDP). Figure 2 shows the valuation metrics of PEP and its peers combined with revenue growth and the gross profit margin to get a feeling for the company's quality. As can be seen, PEP is the cheapest of all the mentioned companies, having the lowest EV/EBITDA, P/S, and P/E ratio and trading at discounts between 10% and 60% to the peer group, depending on the ratio used. The only ratio where the company lags is the P/B ratio. However, even here, KO, Pepsi's biggest competitor, is still more expensive. While growth remains PEP's biggest weakness as all of its peers have higher forward growth rates, the biggest among the KDP at 4.3%, and current revenue growth rates, except for NSRGY at -1.75%. Nevertheless, the industry as a whole has low growth, which is why the difference should not be too high. Nevertheless, PEP remains one of the most profitable companies on the list. While the gross profit margin is average, the already mentioned ROE of almost 50% is unmatched with KO only having one of 40.98% and KDP at only 6.13%. Furthermore, return on capital is also the highest in the group at 13.53%, also higher than that of NSRGY at 10.14%. All of this shows that PEP is a great company, resulting in the thesis that the undervaluation to its peers is not justified.

The Reason Value Could Exceed Expectations

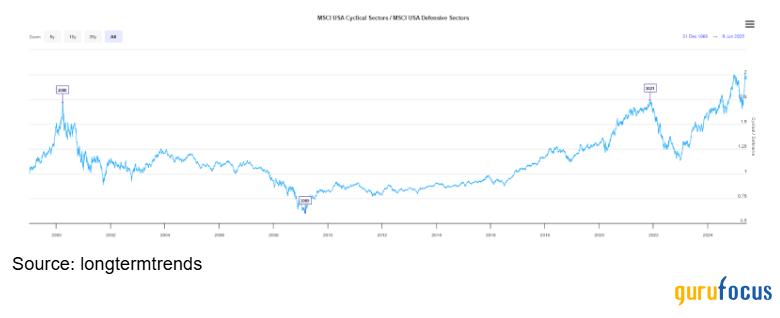

Figure 3 shows the ratio of cyclical to defensive stocks over time. As can be seen, cyclical stocks are at an all-time high, even exceeding the tech bubble in 2000. This generally suggests an undervaluation for more defensive companies like PEP and makes a good pick to diversify otherwise very cyclical-oriented investment portfolios. Furthermore, the Shiller P/E ratio of the US stock market, displayed in Figure 4, is also at one of the highest points it has ever been at. This increases the risk of a potential bubble and thereby the risk for high-growth stocks. Furthermore, at levels higher than 1929, it could initiate a huge sector shift from more aggressive assets to more defensive ones with low elasticity of demand that can also be a plus in a potential inflationary environment due to increased tariffs. All of this makes PEP an interesting bet, especially considering that it also pays a strong dividend of 4.02%.

At the moment, PEP does not have great momentum with a 6-month performance of only -8.83% and a 1-year performance of -16.09%. At the same time, KO has gained 14.83% and 11.98%, respectively. While this is rather bad in the short term, it can be seen as probable that the performance spread between the two companies will contract once again, as it has often done in the past. This might especially be true as it is a pair that often appears in statistical arbitrage algorithms due to its high correlation, low normalized spread difference, and similar business model, which could further push PEP up. Also, the stock has already been recently bought by Ken Fisher (Trades, Portfolio), one of the most famous hedge fund managers out there.

Conclusion

In total, PEP looks like an interesting buy at the moment. It remains a high-quality company at a low valuation compared to peers and its historic valuation. Furthermore, the company is a good hedge/diversification against increased uncertainty and potential overvaluation in the US market, while it should still show solid upside potential if the market continues to rise. This makes PEP an attractive investment for defensive and income-oriented investors and earns it a buy rating over the long term. Nevertheless, I would at first buy in tranches as we would see even lower prices in the short term.