Figma at 300x Earnings: Bubble Hype or the Next Great Compounder?

When I evaluate a company, I don't look at momentum charts or earnings surprises. I ask a more fundamental question: Would I want to own the entire business for the next 10 years? Not the stock. The business.

In that spirit, let's talk about Figma ![]() FIGthe company that Adobe

FIGthe company that Adobe ![]() ADBE tried to acquire for $20 billion in 2022, only to be blocked by regulators. The $20B Adobe acquisition wasn't just a headlineit was a validation. When the heavyweight in creative software offers a massive premium to eliminate a competitor, you know it sees something dangerous. And when regulators block the deal on antitrust grounds? That's not just a moat. That's a regulatory-confirmed threat.

ADBE tried to acquire for $20 billion in 2022, only to be blocked by regulators. The $20B Adobe acquisition wasn't just a headlineit was a validation. When the heavyweight in creative software offers a massive premium to eliminate a competitor, you know it sees something dangerous. And when regulators block the deal on antitrust grounds? That's not just a moat. That's a regulatory-confirmed threat.

Right after being listed, it was trading publicly with a market cap around $60 billion, and after a recent pullback, now trades around a $40 billion market cap, Figma offers a rare opportunity to own a generational software business at a more reasonable multiple. Figma has emerged as the category king in browser-based design collaboration. But this story isn't about hype. It's about fundamentalsand whether this beloved product has the staying power and economic muscle to justify its price tag.

Understanding What Figma Is

Figma builds browser-based tools for digital product design. Designers use it to create wireframes, prototypes, and UI/UX flows. Developers use it to inspect designs and export code. PMs and marketers comment directly inside shared files. No downloads. No version control nightmares. Just a seamless, multiplayer canvas in the cloud.

It started with interface design. But it didn't stop there. FigJam allows for collaborative whiteboarding. Dev Mode helps engineers ship faster. Figma Slides and Sites aim to replace presentation tools and even light web development. The roadmap is clear: become the operating system for digital product creation.

The product's simplicity hides its depth. Over 95% of the Fortune 500 has adopted Figma. Its viral, bottom-up go-to-market strategy turns one free user into an enterprise contract over time. Design teams start for free. Product managers join in. Developers get Dev Mode seats. Eventually, IT upgrades to an organization-wide license.

Figma monetizes by seat type: high-value creator seats for designers and discounted seats for collaborators and engineers. This tiered structure expands TAM and increases average revenue per customer. In Q1 2025, 70% of revenue came from Organization and Enterprise plansa clear sign that land-and-expand is working.

And it's not just usage growth. Figma's plugin ecosystem (with over 10,000 community-built extensions) makes it more valuable the more you use it. Want to add stock images? Charts? Sync to Jira? There's a plugin for that. These integrations create lock-inand reinforce Figma's moat.

A Financial Engine Hiding in a Design Tool

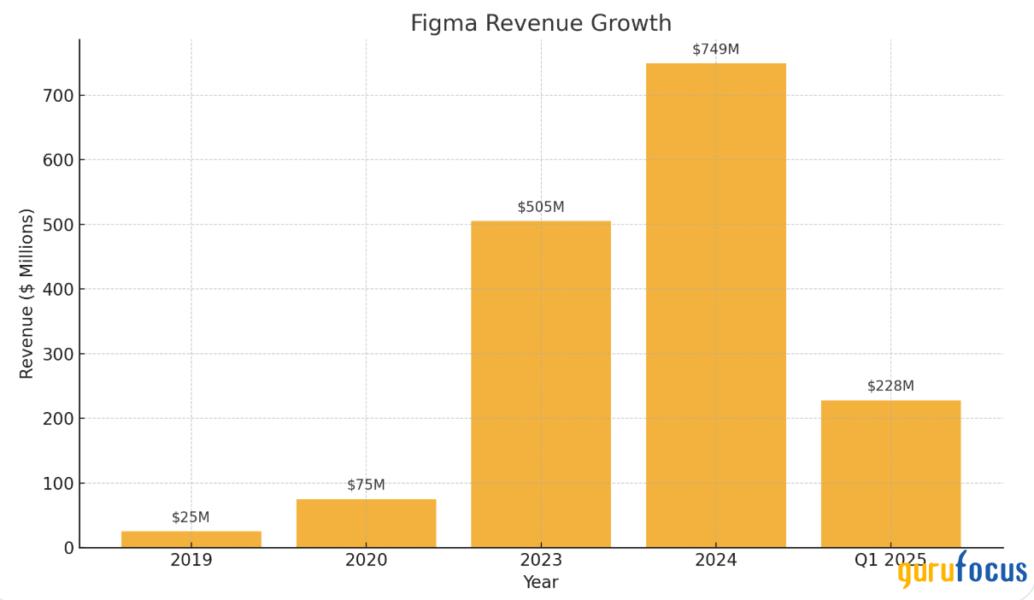

Let's look under the hood. Figma's revenue has grown at an extraordinary pace:

That makes Figma one of the rare high-growth SaaS companies that's already profitable. Its Rule of 40 score (growth rate + operating margin) was 63 in Q1well above the benchmark of 40. This isn't a grow-at-all-costs story. It's a business with real earnings power.

Capex is negligible. Free cash flow is strong. There's no debt. And the company exited Q1 2025 with $1.54 billion in cash. This is a self-funding, capital-light business with plenty of fuel.

Valuation in Context: Figma vs Other Competitors

Of course, all of this doesn't mean Figma is cheap. When it reached $60B market cap and projected ~$200M net income, Figma traded at roughly 300x forward earnings and 65x forward revenue. Now at a $38B market cap Figma trades at ~200x forward earnings and ~44x forward revenue. Still priceybut more grounded after the recent pullback. That puts it at the upper end of high-growth SaaS multiples.

So how does that compare?

- Adobe trades at ~15.9x forward earnings and ~6x forward sales. Gross margins: 89%. Growth: ~10% annually.

- Canva (private) was last valued at ~$26B with ~$2B in ARR. That's ~13x sales.

- Atlassian

TEAM trades at ~46x forward earnings and ~8x revenue. Gross margins: ~82%. Growth: 23%.

TEAM trades at ~46x forward earnings and ~8x revenue. Gross margins: ~82%. Growth: 23%. - Figma at the hype, trades at nearly 300x forward earnings and ~30x revenue. Gross margins: 88.3%. Growth: 48%.

In plain terms, Figma is much more expensive than Adobe, Canva, or Atlassian. But it's also growing faster, with higher margins and earlier-stage reinvestment opportunities.

WIX ![]() WIX apears to be one of the closest comparablescapital-light, sticky, and widely used. But WIX's ARPU (Average revenue per user) remains low because users log in infrequently. Adobe and Figma, by contrast, are deeply embedded into daily workflows. Designers, PMs, and developers live inside the product for hours every day. That kind of engagement drives much higher ARPU and makes Figma more comparable to Adobe or Atlassian in terms of monetization potential.

WIX apears to be one of the closest comparablescapital-light, sticky, and widely used. But WIX's ARPU (Average revenue per user) remains low because users log in infrequently. Adobe and Figma, by contrast, are deeply embedded into daily workflows. Designers, PMs, and developers live inside the product for hours every day. That kind of engagement drives much higher ARPU and makes Figma more comparable to Adobe or Atlassian in terms of monetization potential.

So how big is the market?

Take the ARPU of Adobe's most-used cloud productaround $300400 per yearand multiply that by the estimated 300 million users across design, product, and engineering teams (a proxy drawn from Atlassian's global user base). Even if Figma captures just 10% of that market, you're looking at $912 billion in annual revenue potential.

With a capital-light model and a path to 30% net margins, Figma could generate multi-billion-dollar earnings over time.

The real question isn't whether Figma is expensive today. It's whether it can grow into that valuationand whether its competitive advantages are durable enough to sustain long-term compounding.

Competitive Edge and Moat

What's stopping someone from cloning Figma? Technically, not much. But strategically? A lot.

Figma's moat comes from a few intertwined forces:

- Network effects: The more people inside a company use Figma, the more valuable it becomes. Teams standardize on it. New hires already know it. Switching tools would be painful.

- High switching costs: Enterprise customers build design systems, component libraries, and workflows directly inside Figma. Leaving would mean breaking all of that.

- Ecosystem lock-in: Thousands of plugins, tutorials, community-created templates. No rival offers that breadth.

- Brand dominance: Designers love Figma. PMs tolerate it. Developers respect it. That trifecta is rare.

Adobe failed to beat it with XD. Sketch has faded. Canva serves a different market. Miro, Notion, and others nibble at adjacent spaces but can't match Figma's depth in interface design.

And while AI is a potential disruptor, Figma is leaning into it. Figma Make (prototype from text prompt) and other AI tools are being built in-house. The goal: automate the boring parts of design without replacing the designer.

Management: Aligned and Focused

Dylan Field still leads the company. He owns ~50% of voting rights. His strategic moves post-IPO suggest discipline. Instead of splashy M&A, Figma doubled down on its core platform. It scaled responsibly. It expanded pricing tiers. It accelerated product cadence.

The one wart? In 2024, the failed Adobe acquisition triggered a massive $889M stock comp expense. But this was a one-off to retain talent. Strip it out, and Figma would've been profitable in 2024 too. Field also brought in heavyweights like Bill McDermott (ServiceNow CEO) to the board. That blend of youthful vision and enterprise wisdom is a good sign. And he's not the only one leaning in. Cathie Wood's ARK Investment Management has recently added to its position, purchasing 60,000 shares of Figma. That kind of vote of confidence from a high-conviction, innovation-focused investor tells you something. ARK isn't in the business of indexingthey're betting on exponential curves. If they believe Figma is still early in its compounding journey, it's worth paying attention.

Dylan built Figma from scratch, rejected early buyout offers, and steered through the Adobe drama. He's not optimizing for short-term optics. He's playing a longer game. Another key signal? Only 10% of total shares were sold during the IPO, and 30% of the capital raised was reinvested back into Figma. The limited float has fueled some of the post-IPO volatility, but it also tells you something else: the insiders didn't cash out. They held on. That kind of convictionespecially from a founder like Dylan Field with majority voting controlshouldn't be ignored. They're still playing the long game. That's exactly the kind of alignment I want to see.

Risks Worth Watching

Every great story has risks. For Figma, they include:

- Overpricing seats: As Figma adds roles and charges per seat, cost-sensitive customers might balk. CFOs could push back.

- Enterprise saturation: 95% of the Fortune 500 use Figma, but only ~1,000 pay $100k+. Can those accounts grow to $500k+?

- Complacency: If Figma slows innovation, competitors will catch up.

- AI disruption: If generative tools reduce the need for manual design, seat counts might shrink.

- Founder concentration: Dylan Field has majority voting control. Great if he stays sharp. Risky if he drifts.

That said, none of these risks are fatal. They simply require focus.

Riding the Volatility: Risk or Opportunity?

Figma's recent valuation haircutfrom $60B to $40Bwasn't about fundamentals. It was a reminder that even the best businesses can't escape short-term volatility. Short-term traders might flinch. But long-term investors should see the share price plunge as a potential gift. When price diverges from value, opportunity knocks. If the core business remains intactand it doesthe volatility is your entry point, not your exit sign.

So, Would I Buy the Whole Business?

If I could buy Figma outright for $40 billion, I'd be acquiring more than just a design tool. I'd be getting a $900 million-plus run-rate business growing at 45% a year, with 88% gross margins and real free cash flow. I'd be getting a product that dominates its category and is entrenched inside 95% of the Fortune 500. I'd be buying into a thriving ecosystemthousands of plugins, loyal users, and workflows that teams can't live without. I'd be backing a founder-CEO who still owns the mission, executes relentlessly, and plays long-term. And I'd be inheriting a pristine balance sheet with zero debt and over $1.6 billion in cash. In short: this isn't just softwareit's a compounding engine hiding in plain sight.

The only question is whether I'd be overpaying for perfection.

If Figma compounds at 50% a year for the next five years and settles at a 30% net margin, the math gets simple fast: a ~900 million revenue run-rate today grows to roughly $6.8$6.9 billion, which translates into about $2 billion in annual earnings at maturity. At today's ~$40 billion market cap, you're effectively paying ~20 those Year-5 earnings.

If the market still values a dominant, high-ROIC software franchise at 3540 earnings, that implies $70$80 billion of equity value; if it compresses to ~25, you're closer to $50 billion. In other words, at 50% compounding with 30% margins, today's price isn't euphoricit's a bet on execution and multiple durability. Deliver the growth and hold a sensible premium multiple, and this looks fair to attractive in hindsight; miss on either lever, and the upside tightens.

But one thing's clear: This is one of the best software businesses of the last decade. Whether you buy now or wait for a pullback, Figma deserves a spot on every long-term investor's radar. Because price is what you pay. Value is what you get. And in Figma's case, the value is real. The price? That's up to your risk tolerance.