JD’s German retail bid has oddly compelling logic

JD.com’s ![]() 89618 possible push into Europe’s low-margin, slow-growth electronics-retail market looks unusual at first glance. The $53 billion Chinese e-commerce giant is in advanced talks to buy Düsseldorf-based Ceconomy

89618 possible push into Europe’s low-margin, slow-growth electronics-retail market looks unusual at first glance. The $53 billion Chinese e-commerce giant is in advanced talks to buy Düsseldorf-based Ceconomy ![]() CEC – the owner of the MediaMarkt and Saturn physical chain stores, which sell everything from TVs to washing machines. The upside for JD, founded and chaired by Richard Liu, lies in applying digital nous to lift online sales at the target, and gaining a foothold beyond a brutal Chinese home market.

CEC – the owner of the MediaMarkt and Saturn physical chain stores, which sell everything from TVs to washing machines. The upside for JD, founded and chaired by Richard Liu, lies in applying digital nous to lift online sales at the target, and gaining a foothold beyond a brutal Chinese home market.

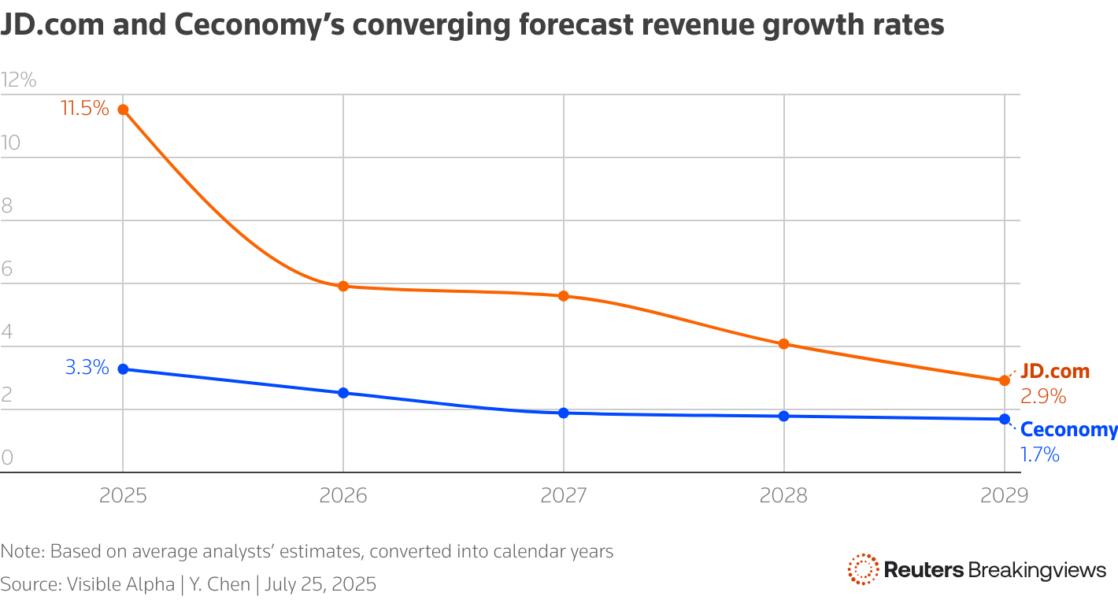

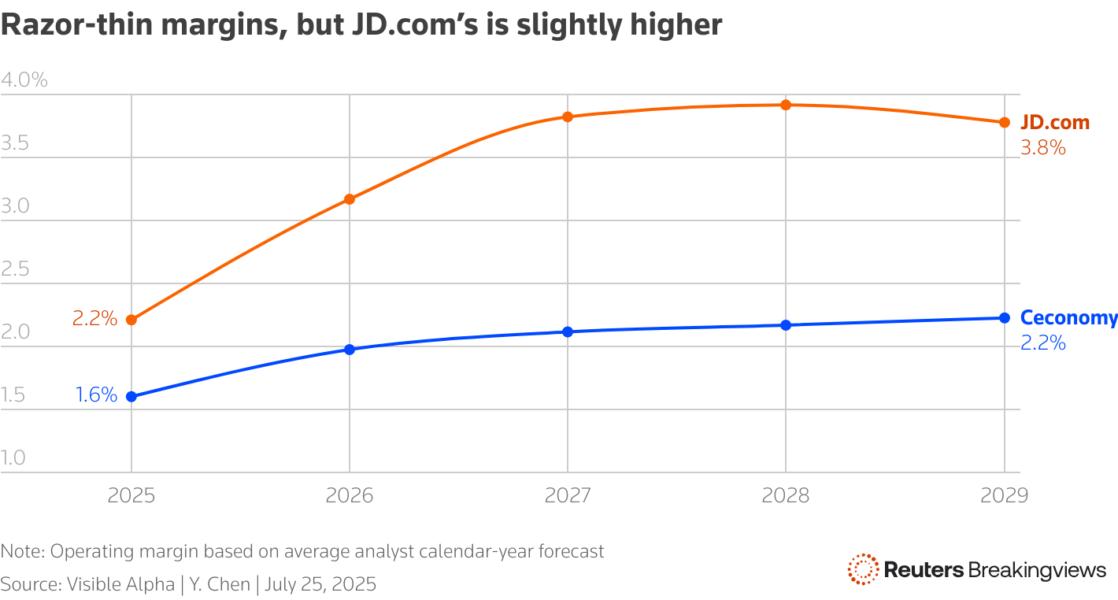

Ceconomy, perhaps unsurprisingly given its offline history, is a slow grower. Analysts are pencilling in a sales increase of 3.3% this calendar year and 2.5% next, estimates gathered by Visible Alpha show, with a slim operating profit margin of around 2%. Despite being Europe’s largest consumer electronics retailer with 1,000 stores across 11 countries, the company’s online journey looks slow given competition from Amazon.com. In other words, it’s not the most obvious target for a Chinese bidder that specialises in digital sales and e-commerce logistics.

The return, however, looks tolerable. JD’s possible offer of 4.6 euros a share in cash implies an enterprise value of just under 4 billion euros ($4.7 billion). By the 2028 fiscal year, analysts expect Ceconomy to make 524 million euros of operating profit, according to forecasts compiled by Visible Alpha. Taxed at 16%, that’s an 11% return on invested capital – only slightly below the German group’s 11.8% weighted average cost of capital as estimated by Kepler Cheuvreux. The return rises to 12.2% after five years, using average analysts’ forecasts for Ceconomy’s operating profit.

JD may hope that it can improve that figure by overhauling and scaling up the digital operations. Its prowess in running supply chains could in theory lift margins, while a bit of investment might see the stores double as e-commerce hubs. JD has the firepower to pull off such a facelift, with some 165 billion yuan ($23 billion) of net cash as of March.

More importantly, the move offers strategic relief. JD is under intense pressure at home, where price wars, regulatory scrutiny, and an uncertain consumer recovery have hit profitability. Analysts expect its growth rate to fall in the coming years, implying that diversifying away from China makes sense, even if Europe’s economy isn’t exactly booming.

The key risk to getting a deal done may lie in geopolitics. Europe’s relationship with China is under strain, from electric car tariffs to concerns over Beijing’s support for Russia. While a consumer electronics retailer doesn’t scream “national security”, the danger is that some in Berlin fear JD may use Ceconomy to dump Chinese-made products. JD’s Liu will have to navigate these hurdles to get his hands on a valuable European beachhead.

Follow Yawen Chen on Bluesky and LinkedIn.

CONTEXT NEWS

German electronics retailer Ceconomy confirmed on July 24 that it was in advanced negotiations about a potential cash takeover by China’s JD.com, at 4.6 euros per share.

The retailer, which owns electronics chains MediaMarkt and Saturn, said that no legally binding agreements had yet been signed and it was not certain whether a deal would happen.

Ceconomy shares were trading at 3.75 euros when the German stock market closed on July 23. They rose 12% to 4.2 euros as of market close on July 24, and traded 1% higher at 4.3 euros as of 0730 GMT on July 25.