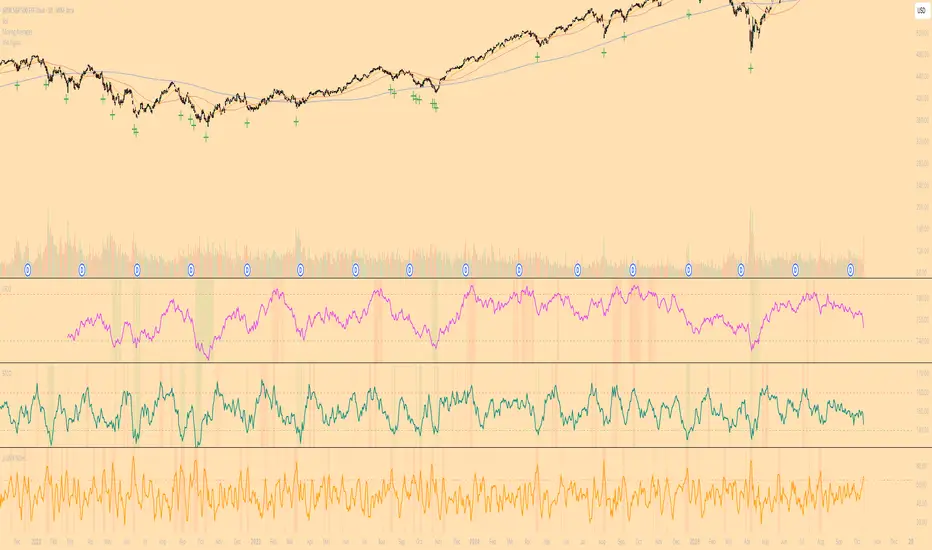

Diodato 'All Stars Align' SignalDescription:

This indicator is an overlay that plots the "All Stars Align" buy signal from Chris Diodato's 2019 CMT paper, "Making The Most Of Panic." It is designed to identify high-conviction, short-term buying opportunities by requiring a confluence of both price-based momentum and market-internal weakness.

What It Is

This script works entirely in the background, calculating three separate indicators: the 14-day Slow Stochastic, the Short-Term Capitulation Oscillator (STCO), and the 3-DMA of % Declining Issues. It then plots a signal directly on the main price chart only when the specific "All Stars Align" conditions are met.

How to Interpret

A green cross (+) appears below a price bar when a high-conviction buy signal is generated. This signal triggers only when two primary conditions are true:

The 14-day Slow Stochastic is in "oversold" territory (e.g., below 20).

AND at least one of the market internal indicators shows a state of panic:

Either the STCO is oversold (e.g., below 140).

Or the 3-DMA % Declines shows a panic spike (e.g., above 65).

This confluence signifies a potential exhaustion of sellers and can mark an opportune moment to look for entries.

Settings

Trigger Thresholds: You can customize the exact levels that define an "oversold" or "panic" state for each of the three underlying indicators.

Data Sources: Allows toggling the use of "Unchanged" data for the background calculations.

Stochastic Settings: You can adjust the parameters for the Slow Stochastic calculation.

Penunjuk Pine Script®