Trend Engine [MMT]The Trend Engine is a versatile Pine Script indicator designed to identify trend direction, potential reversals, and key price levels using a combination of Exponential Moving Averages (EMAs), and Anchored Volume-Weighted Average Price (VWAP). This indicator provides traders with a clear visual representation of market bias, momentum, and key support/resistance levels, making it suitable for both trend-following and pullback trading strategies.

Key Features:

1. EMA Cloud System:

- Displays three customizable EMAs (Fast, Pullback, and Slow) with configurable lengths and visibility.

- Creates two cloud fills:

- Fast Cloud : Between the Fast EMA (default: 8) and Pullback EMA (default: 13).

- Slow Cloud : Between the Pullback EMA and Slow EMA (default: 21).

- Clouds are color-coded (green for bullish, red for bearish) based on EMA alignment, with adjustable transparency for clarity.

2. Bias EMA:

- A longer-term EMA (default: 35) indicates the overall market bias.

- Changes color based on whether the regular candle close is above (green) or below (red) the Bias EMA, providing a clear trend direction signal.

3. Heikin Ashi Signals:

- Utilizes Heikin Ashi candles to detect strong bullish or bearish momentum.

- Generates buy/sell signals when a Heikin Ashi candle confirms a trend (bullish HA candle closing above Bias EMA for buy, bearish HA candle closing below for sell).

- Signal arrows are currently disabled but can be enabled via settings for visual confirmation.

4. Anchored VWAP and Standard VWAP:

- Plots both a standard VWAP and an Anchored VWAP (anchored to the US RTH session, 09:30–16:00 EST).

- Customizable line styles (solid, cross, or circles) and colors for both VWAPs, aiding in identifying dynamic support/resistance levels.

5. Background and Candle Coloring:

- Optional background coloring reflects the market bias (green for bullish, red for bearish) based on the regular close relative to the Bias EMA.

- Optional Heikin Ashi candle coloring to visually distinguish bullish and bearish market conditions.

6. Regular Candle Close:

- Option to plot the regular (non-Heikin Ashi) close price with customizable styles (line, circles, or cross) for reference.

7. Alerts:

- Built-in alert conditions for bullish and bearish signals, allowing traders to receive notifications when a Heikin Ashi candle confirms a trend relative to the Bias EMA.

How to Use:

- Trend Identification : Use the Bias EMA and background color to determine the overall market direction.

- Pullback Trading : Monitor the EMA clouds for alignment (bullish or bearish) and use the Pullback EMA for entries during retracements.

- Support/Resistance : Leverage the VWAP and Anchored VWAP as dynamic levels for trade entries or exits.

- Signal Confirmation : Enable signal arrows (when fixed) to spot high-probability trend continuation or reversal setups.

- Customization : Adjust EMA lengths, colors, transparency, and visibility to suit your trading style and timeframe.

Settings:

- EMA Cloud : Customize lengths (default: 8, 13, 21), visibility, and cloud colors/transparency.

- Bias EMA : Adjust length (default: 35) and colors for above/below states.

- VWAP : Toggle standard and Anchored VWAP, with customizable styles and colors.

- Background/Candles : Enable/disable background and candle coloring for visual clarity.

- Regular Close : Show/hide the regular close price with style options.

Notes:

- Designed for use on any timeframe, but most effective on intraday (e.g., 5m, 15m) or daily charts.

- Best used in conjunction with other technical analysis tools for confirmation.

- Anchored VWAP is tailored for US markets (RTH session) but can be adjusted for other sessions by modifying the anchor time in the code.

Ideal For:

- Day traders and swing traders looking for trend direction and pullback opportunities.

- Traders using VWAP-based strategies for intraday support/resistance.

- Those seeking a clean, customizable visual aid for market bias and momentum.

This indicator is a powerful tool for traders aiming to capture trends and manage risk effectively, with extensive customization to adapt to various markets and trading styles.

Educational

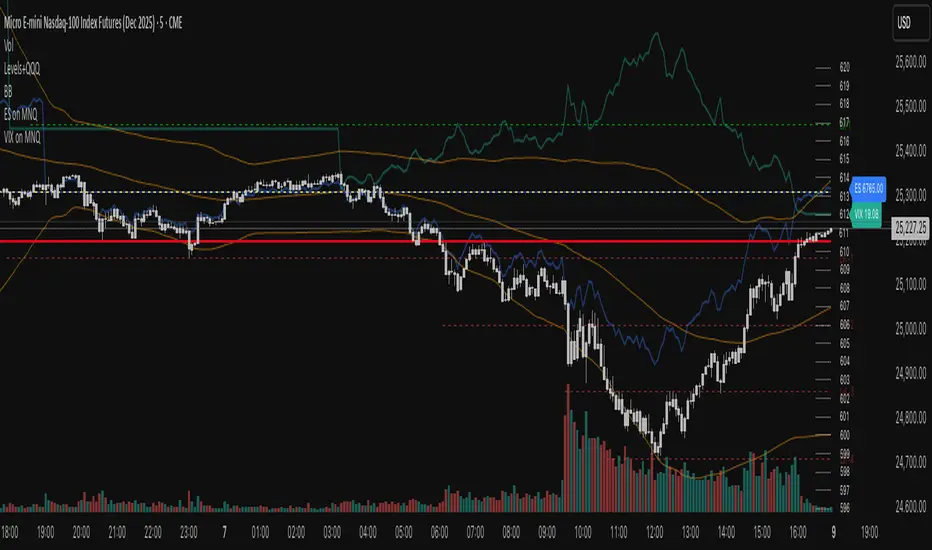

ES on MNQES on MNQ — ES percent-move overlay on the MNQ price scale.

Overview

This indicator projects the ES’s intraday percent change since session open onto the MNQ price scale. At the session start (18:00 chart time), it stores the ES open and the MNQ open, tracks ES’s percentage move from that anchor, and applies the same percent move to the MNQ open. The result is a single line that behaves like ES but is plotted in MNQ points—useful for spotting convergence/divergence, failed breaks, and mean-reversion setups between ES and MNQ.

How it works

1. Detects session open (18:00 on your chart).

2. Saves ES_open and MNQ_open.

3. Computes pct = (ES_close - ES_open) / ES_open.

4. Plots MNQ_open * (1 + pct) as the ES-on-MNQ line.

A label on the last bar shows the current ES value for quick reference.

Inputs

• ES Symbol: default ES1! (change if you use a different continuous).

• Line Color: color of the overlaid ES-on-MNQ line.

Works best on intraday timeframes and when your chart’s session aligns with ES.

Why it’s useful

• Highlights divergences (MNQ decoupling from ES baseline).

• Aids confirmation on pullbacks/breakouts when MNQ’s move disagrees with the ES-based projection.

• Helps risk control by flagging stretches likely to revert toward the ES-anchored path.

Notes & limitations

• This is a percent-rebasing overlay, not a hedge ratio, fair value, or spread model.

• Session/timezone settings matter; if your feed doesn’t print exactly at 18:00 on a higher timeframe, use a smaller TF or adjust session settings.

• Minor differences between ES (full) and MNQ (micro) and data latency can create small offsets.

Disclaimer

For educational use only. Not financial advice. Use proper risk management.

VIX on MNQVIX on MNQ — VIX percent-move overlay on the MNQ price scale (daily-open anchor, optional inversion)

Overview

This indicator projects the VIX’s intraday percent change from the daily open onto the MNQ price scale. It takes today’s open for both VIX and MNQ, measures the VIX’s percentage move since that open, optionally inverts it (given the typical inverse relationship), and applies a scale factor to fit that move onto MNQ’s price axis. The result is a single line that reflects VIX dynamics but is plotted in MNQ points—great for reading risk-on/risk-off tone, spotting divergences, and timing mean-reversion around volatility spikes.

How it works

• Fetches VIX close on your chart timeframe and today’s open for VIX and MNQ.

• Computes pct = (VIX_close − VIX_open) / VIX_open.

• Optionally multiplies by −1 (invert) and then by a Scale Factor to compress amplitude.

• Plots MNQ_open * (1 + pct * (invert? −1 : 1) * scaleFactor) as the VIX-on-MNQ line.

• Adds a last-bar label with the current VIX value and a small info panel (VIX, % change, scaled level).

Inputs

• VIX Symbol: VIX, CBOE:VIX, or TVC:VIX (pick the one that matches your data feed).

• VIX Line Color: color of the overlay line.

• Invert VIX: flip the sign to reflect inverse correlation with MNQ.

• Scale Factor (default 0.05): tune how much of the VIX move is mapped onto MNQ points.

Why it’s useful

• Surfaces volatility-led divergences: when MNQ’s path disagrees with VIX’s risk signal.

• Helps confirm/fade breakouts and pullbacks during volatility expansions/compressions.

• Provides a quick, visual “volatility baseline” directly on the MNQ chart without juggling two panes.

Notes & limitations

• This is a percent-rebased overlay, not a hedge ratio, fair value, or spread model.

• It anchors to the current day’s open; session/timezone settings and your VIX symbol choice (CBOE:VIX vs TVC:VIX) can affect exact prints.

• The scale factor is intentionally manual—adjust until the overlay’s swings are visually informative for your setup.

Disclaimer

For educational use only. Not financial advice. Always manage risk.

ES on MNQES on MNQ — ES percent-move overlay on the MNQ price scale

Overview

This indicator projects the ES’s intraday percent change since session open onto the MNQ price scale. At the session start (18:00 global chart time), it stores the ES open and the MNQ open, tracks ES’s percentage move from that anchor, and applies the same percent move to the MNQ open. The result is a single line that behaves like ES but is plotted in MNQ points—useful for spotting convergence/divergence, failed breaks, and mean-reversion setups between ES and MNQ.

How it works

1. Detects session open (18:00 on your chart).

2. Saves ES_open and MNQ_open.

3. Computes pct = (ES_close - ES_open) / ES_open.

4. Plots MNQ_open * (1 + pct) as the ES-on-MNQ line.

A label on the last bar shows the current ES value for quick reference.

Inputs

• ES Symbol: default ES1! (change if you use a different continuous).

• Line Color: color of the overlaid ES-on-MNQ line.

Works best on intraday timeframes and when your chart’s session aligns with ES.

Why it’s useful

• Highlights divergences (MNQ decoupling from ES baseline).

• Aids confirmation on pullbacks/breakouts when MNQ’s move disagrees with the ES-based projection.

• Helps risk control by flagging stretches likely to revert toward the ES-anchored path.

Notes & limitations

• This is a percent-rebasing overlay, not a hedge ratio, fair value, or spread model.

• Session/timezone settings matter; if your feed doesn’t print exactly at 18:00 on a higher timeframe, use a smaller TF or adjust session settings.

• Minor differences between ES (full) and MNQ (micro) and data latency can create small offsets.

Disclaimer

For educational use only. Not financial advice. Use proper risk management.

EMA 9/15/45 + MACD Confirm + SupertrendThis indicator uses EMA 9, 15, 45 days along with combination of MACD and Supertrend

BTST Trade - 3:15 PMOverview

This indicator is specifically designed for BTST (Buy Today, Sell Tomorrow) traders who want a clear directional signal at 3:15 PM, just before the market closes.

It identifies the active market trend and instantly shows whether the market is positioned for a BTST BUY or BTST SELL setup.

Its goal is simple — help you take a data-based end-of-day decision rather than relying on guesswork or emotion.

Detects the current market trend throughout the day.

At exactly 3:15 PM, it checks that trend and prints one clear signal:

🟢 BTST BUY → Trend is bullish.

🔴 BTST SELL → Trend is bearish.

The signal appears as a label on the chart, making it easy to spot and understand.

Only one signal per day, ensuring clarity and discipline.

How to Use

Apply the indicator on an intraday timeframe (recommended 5-min or 15-min).

Make sure your chart’s exchange timezone is set correctly (for NSE / BSE, use India Standard Time).

Observe the signal generated at 3:15 PM:

If you get a green BUY label, plan a BTST long trade for the next session.

If you get a red SELL label, consider a short-side opportunity or avoid longs.

Use it together with your own price-action or volume confirmation before entering a trade.

Best Practices

Works best on liquid stocks/indices where volume is strong near close.

Combine with Supertrend, EMA, or RSI for additional confirmation.

Avoid using on higher timeframes like 1 hour or daily (no 3:15 bar there).

Designed mainly for BTST and short-term traders.

Disclaimer

This indicator is created for educational purposes only.

It is not financial advice, and no outcome is guaranteed.

Always use proper risk management and confirm signals with your own analysis before taking any trade.

Credits

Created by Virendra Pandey

A simple, time-based approach to identify the BTST & STBT opportunity at 3:15 PM.

Time Range HighlighterThis indicator highlights up to two custom time ranges on your chart with fully adjustable settings:

🔧 Features:

Define two separate time sessions

Set custom start and end times (in any time zone)

Choose unique highlight colors and opacity for each session

Toggle each range on or off independently

Timezone input allows syncing sessions to any global market hours (e.g., UTC, Asia/Tehran, New York)

🕒 Example Use Cases:

Highlight market opening hours (e.g. NYSE: 0930–1600)

Track your personal trading hours or peak volatility sessions

Visualize specific algorithm time filters

📌 Usage:

Enter your desired timezone string (e.g., "Asia/Tehran" or "Etc/UTC")

Customize session times like "0930-1200" and "1500-1700"

Adjust colors and visibility to fit your strategy

Ideal for traders who rely on time-based setups or session overlays.

3HH/3LL → Next Bar Inside = Signal (Neon)Here’s a minimal, compile-ready Pine v5 indicator that does exactly this:

Detects 3 consecutive Higher Highs or 3 consecutive Lower Lows.

Signals only when the very next candle is an Inside Bar.

Uses your Neon Lime (HH case) and Neon Pink (LL case) colors.

Multi-Symbol Fib Zone Signal Scanner NSEMulti-Symbol Fib Zone Signal Scanner NSE

this indicator will suggest to buy or sell basis fib retracement

it is for educational purpose only.

3D Cube Projection - √3 Diagonal3D Cube Projection - √3 Diagonal

OVERVIEW

This indicator implements Bradley F. Cowan's cube projection methodology from his "Four Dimensional Stock Market Structures & Cycles" work. It visualizes a 3D cube projected onto the 2D price-time chart, using the √3 (square root of 3) body diagonal as the primary analytical tool for identifying market structure and potential cycle termination points.

METHODOLOGY

The cube is constructed by selecting two pivot points (A and E) which form the body diagonal - the longest diagonal running through the cube's interior from one corner to the diagonally opposite corner. According to Cowan's geometric approach:

- Point A = Starting pivot (low or high)

- Point E = Ending pivot (opposite extreme)

- Body Diagonal (A→E) = √3 × cube side length

- Face Diagonal (A→C) = √2 × cube side length

The script calculates the cube dimensions by:

1. Measuring the total price range from A to E

2. Dividing by √3 to determine the cube side length in price

3. Distributing the time component across three equal segments

4. Projecting the 3D structure onto the 2D chart plane

FEATURES

✓ Interactive date selection for points A and E

✓ Automatic UPLEG/DOWNLEG detection

✓ All 8 cube vertices labeled (A-H)

✓ All 6 cube faces with independent color/opacity controls

✓ √3 body diagonal (red line by default)

✓ √2 face diagonal (orange line by default)

✓ Customizable cube lines, fills, and labels

✓ Information table showing key measurements

VISUAL CUSTOMIZATION

- Front & Back faces: Box fills for the two square faces

- Side faces: Left and right vertical faces

- Top & Bottom faces: Horizontal connecting faces

- Each group has independent color and opacity settings

- Label size and transparency fully adjustable

- Cube line styles (solid, dashed, dotted) for depth perception

IMPORTANT LIMITATIONS & DISCLOSURES

This indicator works within the inherent constraints of projecting 3D geometry onto a 2D price-time chart:

⚠️ VISUAL APPROXIMATION: This is a visual projection tool, not a mathematically perfect 3D cube. True 3D geometry cannot be accurately represented on a 2D plane without distortion.

⚠️ TIME DISTRIBUTION: The script divides the time axis into three equal segments (total bars ÷ 3) for practical visualization. This is an approximation that prioritizes visual coherence over strict geometric accuracy.

⚠️ UNIT SCALING: Price and time use different units (dollars vs. bars), making true isometric projection impossible. The cube appears proportional on screen but the dimensions are not directly comparable.

⚠️ 2D CONSTRAINT: We only have X (time) and Y (price) axes available. The Z-axis (depth) is simulated through visual projection techniques (line styles, shading).

INTENDED USE

This tool is designed for traders and analysts who study Bradley Cowan's geometric market analysis methods. It helps visualize:

- Market structure in geometric terms

- Potential support/resistance zones at cube edges

- Cycle timing relationships using √2 and √3 ratios

- Harmonic price-time relationships

The cube projection should be used as one component of a comprehensive analysis approach, combined with other technical tools and fundamental analysis.

MATHEMATICAL FOUNDATION

While the visual representation involves approximations, the core √3 relationship is mathematically sound:

- For any cube, the body diagonal = √3 × side length

- The face diagonal = √2 × side length

- These ratios are preserved in the price dimension calculations

HOW TO USE

1. Select your starting date (Point A) - typically a significant low or high

2. Select your ending date (Point E) - the opposite extreme pivot

3. The indicator automatically constructs the cube geometry

4. Analyze the cube edges, diagonals, and faces for market structure insights

5. Adjust colors and opacity to suit your chart aesthetic

TECHNICAL NOTES

- Works on all timeframes and instruments

- Best viewed on charts with sufficient historical data

- Cube updates in real-time as new bars form

- Range selection is marked with vertical lines and shading

- Calculator table shows Point A, Point E, side length, and bar measurements

ACKNOWLEDGMENT

This indicator is based on the geometric market analysis principles developed by Bradley F. Cowan. Users are encouraged to study Cowan's original works for deeper understanding of the theoretical framework.

DISCLAIMER

This indicator is for educational and analytical purposes only. It does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research and risk management before making trading decisions.

The Capture - Wargame v2.0- Visualizes historical wargame session data by drawing time-based boxes on the chart showing when Low of Day (LOD) and High of Day (HOD) typically occur

- Calculates price levels as percentage distributions from the daily Globex open (18:00 EST) and positions boxes using actual timestamps in America/New_York timezone

- Supports four session types (Long True/False, Short True/False) with customizable colors, transparency, labels, and includes a configurable data table overlay

Midnight ET + Daily H/L True dayThis script divides each day from midnight EST to the next midnight opening price (True day). Full credits go to my mentor ICT for the idea behind the script

Midnight ET + Daily H/L (vertical midnight + HL lines)This script provides midnight EST dividers for each day and marks each daily high and low during each True day. Credits go to my mentor ICT for the idea behind this script.

12M SMA Timing (HTF-safe, 100% equity)Buy when S&P500 closes above 12M moving average. Sell when it closes below it. Monthly only.

Price Action IndicatorThis indicator is based on Price Action

Trend bar would be filled with Red/Green

Reversal bar would be tagged

📋 Trading Checklist – Precision Entry SystemTake your trading discipline to the next level with this Precision Trading Checklist for TradingView. Designed for intraday traders following liquidity, structure, and Smart Money Concepts (SMC) AKA ICT Concepts, this overlay ensures you never miss a key confirmation before entering a trade.

Features:

✅ Pre-Market Preparation: Track previous session highs/lows, AM/PM sessions, and key liquidity zones.

✅ Bias & Narrative Check: Quickly confirm daily trend, price position relative to daily open, and higher timeframe confluence.

✅ Session-Specific Rules: Focused sessions like Silver Bullet (10:00–11:30), Afternoon (13:30–15:00), and Final Hour (15:00–16:00).

✅ Structure & Setup Validation: Confirm liquidity sweeps, market structure shifts, expansion candles, fair value gaps, and order blocks.

✅ Risk Management Reminders: Stop-loss, target points, risk percentage, breakeven management, and pyramiding rules.

✅ Post-Trade Journaling: Document entries, session, setup type, trade outcome, and grading for continuous improvement.

✅ Golden Rules: Visual reminders to enforce discipline, avoid emotional trades, and respect session limits.

Why Use It:

This checklist is perfect for traders who want to stay consistent, minimise mistakes, and follow a disciplined routine. Displayed as an overlay on your chart, it provides all essential checks in one glance, keeping you focused on the setup rather than scrolling through notes or separate trackers.

How to use:

Add the indicator to your chart

Click the settings/gear icon

Check off items as you complete them

The checklist on your chart updates in real-time with green checkmarks!

The checkboxes will persist as long as the indicator is on your chart,

making it perfect for tracking your pre-trade and post-trade routines!

Follow the checklist items step by step before entering trades.

Use the session-specific guidelines to filter setups.

Journal your trades post-execution for growth and analysis.

Trend (5m & 1h) by Ben2010🧭 What it does:

✅ Checks 5 min and 1 hour timeframes (you can change them).

✅ Evaluates:

RSI: momentum

MACD: direction

VWAP: price vs fair value

Volume: buyers vs sellers

Price structure: Higher High or Lower Low

✅ Combines all into a qualitative strength label (Very Bullish → Very Bearish).

✅ Displays everything in a neat table at the top-right corner.

Trendy Bands + Reversal SignalsTrendy Bands + Reversal Signals

This is a versatile and powerful TradingView indicator that combines a dual Bollinger Bands system with momentum-based reversal signals. It's designed to help traders identify the prevailing trend, potential volatility expansions/contractions, and key reversal points in the market.

Core Concept: The indicator uses two sets of Bollinger Bands with different standard deviation settings to create a "band within a band" structure. This visual setup makes it easier to gauge trend strength and spot potential breakouts or breakdowns. Additionally, it calculates a custom momentum oscillator to generate early warnings for potential trend reversals.

EMAs 4/8/15 + Classic Pivots (clean v5)Here is a clean code for people to use, hope it works well for you. 4/8/15 are key indicators. You first got to be on the right side or upside of the 15 and then you need to see a detachment from the 4/8. You will see that is when upward movement happens. for shorting, you need to be below the 4/8 and usually on the under of 15.

Rotating Messages (Rules or Motivational)This lightweight utility indicator allows you to display rotating custom text messages directly on your TradingView chart — perfect for reminders, trading rules, motivational quotes, or session notes.

You can define multiple messages separated by semicolons (;) or new lines, and the indicator will automatically cycle through them based on time or bar count. Ideal for traders who want visual cues without cluttering the chart.

⚙️ Main Features

⏱ Time-based or bar-based rotation — switch messages every X seconds (real-time) or X bars (historical/backtest mode).

📍 Flexible positioning — choose between Top Right, Bottom Right, or Bottom Center.

📏 Vertical offset — move text up or down for perfect placement on your chart.

🎨 Custom styling — set text color, background color, border visibility, and text size.

✍️ Simple message input — enter your rules or quotes in a text box with support for multi-line messages.

fpmanananaThis is a description of the indicator. It is a really good one that I think is really good.

Quantura - Session High/LowIntroduction

“Quantura – Session High/Low” is a professional-grade session mapping indicator that automatically identifies and visualizes the highs, lows, and ranges of key global trading sessions — London, New York, and Asia. It helps traders understand when and where liquidity tends to accumulate, allowing for better market structure analysis and session-based strategy alignment.

Originality & Value

This indicator unifies the three most influential global sessions into a single, adaptive visualization tool. Unlike typical session indicators, it dynamically updates live session highs and lows in real time while marking session boundaries and transitions. Its multi-session management system allows for immediate recognition of overlapping liquidity zones — a crucial feature for institutional and intraday traders.

The value and originality come from:

Real-time tracking of session highs, lows, and developing ranges.

Simultaneous visualization of multiple global sessions.

Optional vertical range lines for clearer visual segmentation.

Customizable session times, colors, and time zone offset for global accuracy.

Automatically extending and updating lines as each session progresses.

Functionality & Core Logic

Detects the start and end of each trading session (London, New York, Asia) using built-in time logic and user-defined UTC offsets.

Initializes session-specific high and low variables at the start of each new session.

Continuously updates session high/low levels as new candles form.

Draws color-coded horizontal lines for each session’s high and low.

Optionally adds vertical dotted lines to visually connect session range extremes.

Locks each session’s range once it ends, preserving historical structure for review.

Parameters & Customization

New York Session: Enable/disable, customize time (default 15:30–21:30), and set color.

London Session: Enable/disable, customize time (default 09:00–16:30), and set color.

Asia Session: Enable/disable, customize time (default 02:30–08:00), and set color.

Vertical Line: Toggle dotted vertical lines connecting session high and low levels.

UTC Offset: Adjust session timing to align with your chart’s local time zone.

Visualization & Display

Each session is color-coded for quick identification (default: blue for London, red for New York, green for Asia).

Horizontal lines track evolving session highs and lows in real time.

Once a session closes, the lines remain fixed to mark historical range boundaries.

Vertical dotted lines (optional) visually connect the session’s high and low for clarity.

Supports full overlay display without interfering with other technical indicators.

Use Cases

Identify liquidity zones and range extremes formed during active trading sessions.

Observe session overlaps (London–New York) to anticipate volatility spikes.

Combine with volume or market structure tools for session-based confluence.

Track how price interacts with prior session highs/lows to detect potential reversals.

Analyze session-specific performance patterns for algorithmic or discretionary systems.

Limitations & Recommendations

The indicator is designed for intraday analysis and may not provide meaningful output on daily or higher timeframes.

Adjust session times and UTC offset based on your broker’s or exchange’s timezone.

Does not provide trading signals — it visualizes session structure only.

Combine with liquidity and volatility indicators for full contextual understanding.

Markets & Timeframes

Compatible with all asset classes — including crypto, forex, indices, and commodities — and optimized for intraday timeframes (1m–4h). Particularly useful for traders analyzing session overlaps and volatility transitions.

Author & Access

Developed 100% by Quantura. Published as a Open-source script indicator. Access is free.

Compliance Note

This description fully complies with TradingView’s Script Publishing Rules and House Rules . It provides a detailed explanation of functionality, parameters, and realistic use cases without making any performance or predictive claims.

Inside Day FinderWhat is an Inside Day?

An inside day happens when:

Today’s high is lower than yesterday’s high, and

Today’s low is higher than yesterday’s low.

So, today’s candle is inside the previous day’s range — showing consolidation or indecision in the market.