Currency Strength v3.0Currency Strength v3.0

Summary

The Currency Strength indicator is a powerful tool designed to gauge the relative strength of major and emerging market currencies. By plotting the True Strength Index (TSI) of various currency indices, it provides a clear visual representation of which currencies are gaining momentum and which are losing it. This indicator automatically detects the currency pair on your chart and highlights the corresponding strength lines, simplifying analysis and helping you quickly identify potential trading opportunities based on currency dynamics.

Key Features

Comprehensive Currency Analysis: Tracks the strength of 19 currencies, including major pairs and several emerging market currencies.

Automatic Pair Detection: Intelligently identifies the base and quote currency of the active chart, automatically highlighting the relevant strength lines.

Dynamic Coloring: The base currency is consistently colored blue, and the quote currency is colored gold, making it easy to distinguish between the two at a glance.

Non-Repainting TSI Calculation: Uses the True Strength Index (TSI) for smooth and reliable momentum readings that do not repaint.

Customizable Settings: Allows for adjustment of the fast and slow periods for the TSI calculation to fit your specific trading style.

Clean Interface: Features a minimalist legend table that only displays the currencies relevant to your current chart, keeping your workspace uncluttered.

How It Works

The indicator pulls data from major currency indices (like DXY for the US Dollar and EXY for the Euro). For currencies that don't have a dedicated index, it uses their USD pair (e.g., USDCNY) and inverts the calculation to derive the currency's strength relative to the dollar. It then applies the True Strength Index (TSI) to this data. The TSI is a momentum oscillator that is less volatile than other oscillators, providing a more reliable measure of strength. The resulting values are plotted on the chart, allowing you to see how different currencies are performing against each other in real-time.

How to Use

Trend Confirmation: When the base currency's line is rising and above the zero line, and the quote currency's line is falling, it can confirm a bullish trend for the pair. The opposite would suggest a bearish trend.

Identifying Divergences: Look for divergences between the currency strength lines and the price action of the pair. For example, if the price is making higher highs but the base currency's strength is making lower highs, it could signal a potential reversal.

Crossovers: A crossover of the base and quote currency lines can signal a shift in momentum. A bullish signal occurs when the base currency line crosses above the quote currency line. A bearish signal occurs when it crosses below.

Overbought/Oversold Levels: The horizontal dashed lines at 0.5 and -0.5 can be used as general guides for overbought and oversold conditions, respectively. Strength moving beyond these levels may indicate an unsustainable move that is due for a correction.

Settings

Fast Period: The short-term period for the TSI calculation. Default is 7.

Slow Period: The long-term period for the TSI calculation. Default is 15.

Index Source: The price source used for the calculations (e.g., Close, Open). Default is Close.

Base Currency Color: The color for the base currency line. Default is Royal Blue.

Quote Currency Color: The color for the quote currency line. Default is Goldenrod.

Disclaimer

This indicator is intended for educational and analytical purposes only. It is not financial advice. Trading involves substantial risk, and past performance is not indicative of future results. Always conduct your own research and risk management before making any trading decisions.

Analisis Fundamental

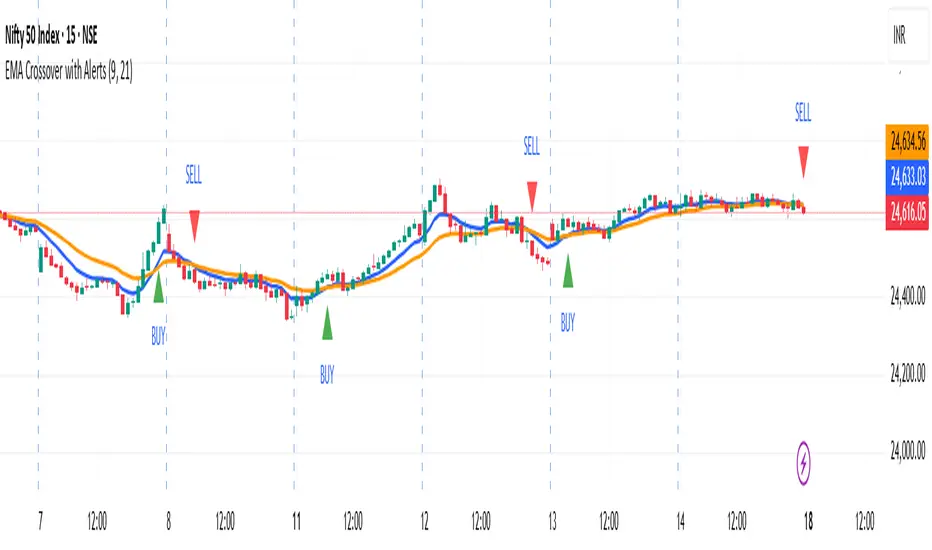

EMA Crossover with AlertsIndicator with Fast and Slow EMA Crossovers, includes alerts on such cross overs

Line color best indices grouped by Artificial Intelligence

The script uses the best buy indicators, such as moving average crossovers, RSI, and others selected by AI. The idea is to determine whether the stock is classified as a strong buy (yellow line), a buy (green line), or a red (sell)

4 EMA Multi-Length / Abbas4 EMA Multi Length indicator

in case you need to make 4 different EMA/s for your chart

for swinging you'll need 50/100/150/200

for scalping perhaps 9/20/50

this indicator allows you to combine up to 4 EMAS in one indicator instead of 4 separate ones.

Trading bot gridsGuide: Price Lines – Arithmetic vs. Geometric

This script draws horizontal price lines (grids) between a start price and an end price.

You can choose whether the lines are distributed evenly (arithmetic) or by percentage (geometric).

🔧 Inputs

Start Price → Lower or upper boundary of the price range.

End Price → Opposite boundary of the price range.

Number of Lines → Total number of lines to be drawn between the start and end prices.

Distribution →

Arithmetic: Fixed USDT distance between each line.

Geometric: Fixed percentage distance between each line.

Grid Color → Color of the drawn lines.

📈 How it Works

The script calculates the lower (lo) and upper (hi) boundaries, regardless of which is entered first.

Arithmetic distribution: Each line is spaced by a fixed amount in USDT.

Geometric distribution: Each line is spaced by the same percentage difference from the previous one.

Lines are created only once at the first bar and remain on the chart.

All lines are extended across the entire visible chart.

💡 Tips

Useful for Grid Bot backtesting or visualizing price zones.

Works for both long and short price ranges.

In geometric mode, lines appear closer together near the lower price range and farther apart toward the upper range.

FVG + Bank Level Targeting w/ Alert TriggerDescription:

FVG + Bank Level Targeting w/ Alert Trigger is an intraday trading tool that combines Fair Value Gap (FVG) detection with dynamic institutional targeting using prior-day, weekly, and monthly high/low "Bank Levels." When a Fair Value Gap is detected, the script projects a logical target using the closest bank level in price's direction, and visually extends that level on your chart.

This tool is designed to help traders anticipate where price is most likely to move after an FVG appears — and alert them when price breaks through key target zones.

How It Works:

* Bank Level Calculation:

The indicator calculates Daily, Weekly, and Monthly high and low levels from the previous bar of each respective timeframe.

These are optionally plotted on the chart with a slight tick offset to avoid overlap with price.

* FVG Detection:

Bullish FVGs are defined by a gap between the low of the current candle and the high two candles prior, with a confirming middle candle.

Bearish FVGs follow the reverse pattern.

Once detected, the script finds the nearest unbroken institutional level (Bank Level) in the direction of the FVG and anchors a target line at that price level.

* Target Line Projection:

The script draws a persistent horizontal line (not just a plotted value) at the selected bank level.

These lines automatically extend a set number of bars into the future for clarity and trade planning.

* Breakout Detection:

When price crosses above a Bull Target or below a Bear Target, the script triggers a breakout condition.

These breakouts are useful for trade continuation or reversal setups.

* Alerts:

Built-in alert conditions notify you in real time when price crosses above or below a target.

These can be used to set TradingView alerts for your preferred Futures symbols or intraday pairs.

Parameters:

Tick Offset Multiplier: Adds distance between price and plotted levels.

Show Daily/Weekly/Monthly Levels: Toggle for each institutional level group.

FVG Extend Right (bars): Controls how far the target lines extend into the future.

Color Controls: Customize colors for FVG fill and target lines.

Use Case:

This indicator is designed for traders who want to:

Trade continuation or reversal moves around institutional price zones

Integrate Fair Value Gap concepts with more logical, historically anchored price targets

Trigger alerts when market structure evolves around key levels

It is especially useful for intraday Futures traders on the 15-minute chart or lower, but adapts well to any instrument with strong reactionary behavior at prior session highs/lows.

US Macro Cycle (Z-Score Model)US Macro Cycle (Z-Score Model)

This indicator tracks the US economic cycle in real time using a weighted composite of seven macro and market-based indicators, each converted into a rolling Z-score for comparability. The model identifies the current phase of the cycle — Expansion, Peak, Contraction, or Recovery — and suggests sector tilts based on historical performance in each phase.

Core Components:

Yield Curve (10y–2y): Positive & steepening = growth; inverted = slowdown risk.

Credit Spreads (HYG/LQD): Tightening = risk-on; widening = risk-off.

Sector Leadership (Cyclicals vs. Defensives): Measures market leadership regime.

Copper/Gold Ratio: Higher copper = growth signal; higher gold = defensive.

SPY vs. 200-day MA: Equity trend strength.

SPY/IEF Ratio: Stocks vs. bonds relative strength.

VIX (Inverted): Low/falling volatility = supportive; high/rising = risk-off.

Methodology:

Each series is transformed into a rolling Z-score over the selected lookback period (optionally using median/MAD for robustness and winsorization to clip outliers).

Z-scores are combined using user-defined weights and normalized.

The smoothed composite is compared against phase thresholds to classify the macro environment.

Features:

Customizable Weights: Emphasize the indicators most relevant to your strategy.

Adjustable Thresholds: Fine-tune cycle phase definitions.

Background Coloring: Visual cue for the current phase.

Summary Table: Displays composite Z, confidence %, and individual Z-scores.

Alerts: Trigger when the phase changes, with details on the composite score and recommended tilt.

Use Cases:

Align sector rotation or relative strength strategies with the macro backdrop.

Identify favorable or defensive phases for tactical allocation.

Monitor macro turning points to manage portfolio risk.

It's doesn't fill nan gaps so there is quite a bit of zeroes, non-repainting.

EPS QoQ % ChangeThis indicator calculates and displays the quarter-over-quarter (QoQ) percentage change in earnings per share (EPS) directly on your chart, aligned with each earnings event.

It is designed to quickly highlight EPS growth or decline without the need to open an earnings report, providing traders and investors with instant, visual performance context.

Features :

- Automatic Earnings Detection: Identifies earnings bars and calculates QoQ % change.

- Color-Coded Text: Positive changes are shown in your chosen “up” color, declines in your “down” color, and flat results in a neutral color.

- Customizable Appearance: Choose text size and colors to match your chart style.

- Tooltip Support: Optional detailed tooltip showing reported EPS, previous EPS, and calculated QoQ change.

- Compact Layout: Displays in its own pane to avoid cluttering price action.

Use Cases :

- Quickly assess EPS growth trends over time.

- Spot significant earnings beats or misses without reading earnings transcripts.

- Use alongside other technical or fundamental tools for better decision-making.

VRD-5: Volume Reversal Detector (5 Bars)Overview

This Pine Script indicator detects potential trend reversals based on volume patterns over a 5-bar period. It identifies accumulation (bullish) and distribution (bearish) patterns using volume analysis combined with price action.

Key Features

Volume Analysis:

Compares current volume to a 34-period SMA

Identifies strong/weak volume using configurable thresholds

Calculates volume "energy" as a 5-bar average ratio

Pattern Detection:

Bearish Signal: Looks for decreasing volume after a strong volume bar

Bullish Signal: Looks for increasing volume after weak volume bars

Visualization:

Colored volume histogram (bullish/bearish/neutral)

SMA volume line

Labels for detected signals

Customization Options:

Adjustable lookback period (3-10 bars)

Configurable thresholds for volume strength

Strict mode requiring confirming price action

Suggested Improvements

Performance Optimization:

Reduce the max_labels_count (currently 500) to improve performance

Consider using barstate.isconfirmed for more efficient calculations

Enhanced Visualization:

Add arrows on price chart for better visibility

Include a background color highlight for signal periods

Add option to display the energy level as a separate line

Additional Features:

Incorporate RSI or MACD for confirmation

Add multi-timeframe analysis capability

Include a strategy version for backtesting

Code Structure:

Separate the logic into distinct functions for better readability

Add more detailed comments for complex calculations

Consider using varip for real-time updates if needed

User Experience:

Add input options for label text size/position

Include sound options for alerts

Add a toggle for the information table

This indicator provides a solid foundation for volume-based reversal detection that could be further enhanced with these improvements while maintaining its core functionality.

Real-Time FTFC Dashboard (Styled)Full Time Frame Continuity dashboard that monitors real-time market direction across multiple timeframes for any stock, ETF, or index. Uses green, red, and pause emojis to visually indicate bullish, bearish, or inactive periods, helping traders quickly assess overall market alignment.

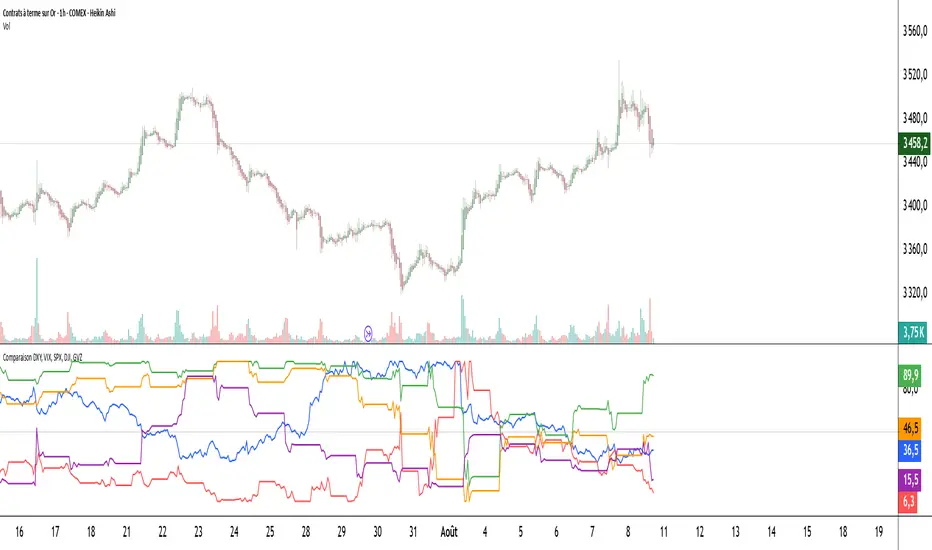

Comparaison DXY, VIX, SPX, DJI, GVZPine Script indicator compares the normalized values of DXY, VIX, SPX, DJI, and GVZ indices on a single scale from 0 to 100. Here's a breakdown of what it does:

Data Requests: Gets closing prices for:

US Dollar Index (DXY)

VIX Volatility Index

S&P 500 (SPX)

Dow Jones Industrial Average (DJI)

Gold Volatility Index (GVZ)

Normalization: Each index is normalized using a 500-period lookback to scale values between 0-100, making them comparable despite different price scales.

Visualization:

Plots each normalized index with distinct colors

Adds a dotted midline at 50 for reference

Uses thicker linewidth (2) for better visibility

Timeframe Flexibility: Works on any chart timeframe since it uses timeframe.period

This is useful for:

Comparing relative strength/weakness between these key market indicators

Identifying divergences or convergences in their movements

Seeing how different asset classes (currencies, equities, volatility) relate

You could enhance this by:

Adding correlation calculations between pairs

Including options to adjust the normalization period

Adding alerts when instruments diverge beyond certain thresholds

Including volume or other metrics alongside price

TSI Indicator with Trailing StopAuthor: ProfitGang

Type: Indicator (visual + alerts). No orders are executed.

What it does

This tool combines the True Strength Index (TSI) with a simple tick-based trailing stop visualizer.

It plots buy/sell markers from a TSI cross with momentum confirmation and, if enabled, draws a trailing stop line that “ratchets” in your favor. It also shows a compact info table (position state, entry price, trailing status, and unrealized ticks).

Signal logic (summary)

TSI is computed with double EMA smoothing (user lengths).

Signals:

Buy when TSI crosses above its signal line and momentum (TSI–Signal histogram) improves, with TSI above your Buy Threshold.

Sell when TSI crosses below its signal line and momentum weakens, with TSI below your Sell Threshold.

Confirmation: Optional “Confirm on bar close” setting evaluates signals on closed bars to reduce repaint risk.

Trailing stop (visual only)

Units are ticks (uses the symbol’s min tick).

Start Trailing After (ticks): activates the trail only once price has moved in your favor by the set amount.

Trailing Stop (ticks): distance from price once active.

For longs: stop = close - trail; it never moves down.

For shorts: stop = close + trail; it never moves up.

Exits shown on chart when the trailing line is touched or an opposite signal occurs.

Note: This is a simulation for visualization and does not place, manage, or guarantee broker orders.

Inputs you can tune

TSI Settings: Long Length, Short Length, Signal Length, Buy/Sell thresholds, Confirm on Close.

Trailing Stop: Start Trailing After (ticks), Trailing Stop (ticks), Show/Hide trailing lines.

Display: Toggle chart signals, info table, and (optionally) TSI plots on the price chart.

Alerts included

TSI Buy / TSI Sell

Long/Short Trailing Activated

Long/Short Trail Exit

Tips for use

Timeframes/markets: Works on any symbol/timeframe that reports a valid min tick. If your market has large ticks, adjust the tick inputs accordingly.

TSI view: By default, TSI lines are hidden to avoid rescaling the price chart. Enable “Show TSI plots on price chart” if you want to see the oscillator inline.

Non-repainting note: With Confirm on bar close enabled, signals are evaluated on closed bars. Intrabar previews can change until the bar closes—this is expected behavior in TradingView.

Limitations

This is an indicator for education/research. It does not execute trades, and visuals may differ from actual broker fills.

Performance varies by market conditions; thresholds and trail settings should be tested by the user.

Disclaimer

Nothing here is financial advice. Markets involve risk, including possible loss of capital. Always do your own research and test on a demo before using any tool in live trading.

— ProfitGang

Institutional level Indicator V5Smart money concept indicator with added VWAP for better understanding for fair price with relation to movement of price.

ZoneShift+StochZ+LRO + AI Breakout Bands [Combined]This composite Pine Script brings together four powerful trend and momentum tools into a single, easy-to-read overlay:

ZoneShift

Computes a dynamic “zone” around price via an EMA/HMA midpoint ± average high-low range.

Flags flips when price closes convincingly above or below that zone, coloring candles and drawing the zone lines in bullish or bearish hues.

Stochastic Z-Score

Converts your chosen price series into a statistical Z-score, then runs a Stochastic oscillator on it and HMA-smooths the result.

Marks momentum flips in extreme over-sold (below –2) or over-bought (above +2) territory.

Linear Regression Oscillator (LRO)

Builds a bar-indexed linear regression, normalizes it to standard deviations, and shows area-style up/down coloring.

Highlights local reversals when the oscillator crosses its own look-back values, and optionally plots LRO-colored candles on price.

AI Breakout Bands (Kalman + KNN)

Applies a Kalman filter to price, smooths it further with a KNN-weighted average, then measures mean-absolute-error bands around that smoothed line.

Colors the Kalman trend line and bands for bullish/bearish breaks, giving you a data-driven channel to trade.

Composite Signals & Alerts

Whenever the ZoneShift flip, Stoch Z-Score flip, and LRO reversal all agree and price breaks the AI bands in the same direction, the script plots a clear ▲ (bull) or ▼ (bear) on the chart and fires an alert. This triple-confirmation approach helps you zero in on high-probability reversal points, filtering out noise and combining trend, momentum, and statistical breakout criteria into one unified signal.

CVDD Z-ScoreCumulative Value Days Destroyed (CVDD) - The CVDD was created by Willy Woo and is the ratio of the cumulative value of Coin Days Destroyed in USD and the market age (in days). While this indicator is used to detect bottoms normally, an extension is used to allow detection of BTC tops. When the BTC price goes above the CVDD extension, BTC is generally considered to be overvalued. Because the "strength" of the BTC tops has decreased over the cycles, a logarithmic function for the extension was created by fitting past cycles as log extension = slope * time + intercept. This indicator is triggered for a top when the BTC price is above the CVDD extension. For the bottoms, the CVDD is shifted upwards at a default value of 120%. The slope, intercept, and CVDD bottom shift can all be modified in the script.

Now with the automatic Z-Score calculation for ease of classification of Bitcoin's valuation according to this metric.

Created for TRW.

Bitcoin Logarithmic Growth Curve 2025 Z-Score"The Bitcoin logarithmic growth curve is a concept used to analyze Bitcoin's price movements over time. The idea is based on the observation that Bitcoin's price tends to grow exponentially, particularly during bull markets. It attempts to give a long-term perspective on the Bitcoin price movements.

The curve includes an upper and lower band. These bands often represent zones where Bitcoin's price is overextended (upper band) or undervalued (lower band) relative to its historical growth trajectory. When the price touches or exceeds the upper band, it may indicate a speculative bubble, while prices near the lower band may suggest a buying opportunity.

Unlike most Bitcoin growth curve indicators, this one includes a logarithmic growth curve optimized using the latest 2024 price data, making it, in our view, superior to previous models. Additionally, it features statistical confidence intervals derived from linear regression, compatible across all timeframes, and extrapolates the data far into the future. Finally, this model allows users the flexibility to manually adjust the function parameters to suit their preferences.

The Bitcoin logarithmic growth curve has the following function:

y = 10^(a * log10(x) - b)

In the context of this formula, the y value represents the Bitcoin price, while the x value corresponds to the time, specifically indicated by the weekly bar number on the chart.

How is it made (You can skip this section if you’re not a fan of math):

To optimize the fit of this function and determine the optimal values of a and b, the previous weekly cycle peak values were analyzed. The corresponding x and y values were recorded as follows:

113, 18.55

240, 1004.42

451, 19128.27

655, 65502.47

The same process was applied to the bear market low values:

103, 2.48

267, 211.03

471, 3192.87

676, 16255.15

Next, these values were converted to their linear form by applying the base-10 logarithm. This transformation allows the function to be expressed in a linear state: y = a * x − b. This step is essential for enabling linear regression on these values.

For the cycle peak (x,y) values:

2.053, 1.268

2.380, 3.002

2.654, 4.282

2.816, 4.816

And for the bear market low (x,y) values:

2.013, 0.394

2.427, 2.324

2.673, 3.504

2.830, 4.211

Next, linear regression was performed on both these datasets. (Numerous tools are available online for linear regression calculations, making manual computations unnecessary).

Linear regression is a method used to find a straight line that best represents the relationship between two variables. It looks at how changes in one variable affect another and tries to predict values based on that relationship.

The goal is to minimize the differences between the actual data points and the points predicted by the line. Essentially, it aims to optimize for the highest R-Square value.

Below are the results:

snapshot

snapshot

It is important to note that both the slope (a-value) and the y-intercept (b-value) have associated standard errors. These standard errors can be used to calculate confidence intervals by multiplying them by the t-values (two degrees of freedom) from the linear regression.

These t-values can be found in a t-distribution table. For the top cycle confidence intervals, we used t10% (0.133), t25% (0.323), and t33% (0.414). For the bottom cycle confidence intervals, the t-values used were t10% (0.133), t25% (0.323), t33% (0.414), t50% (0.765), and t67% (1.063).

The final bull cycle function is:

y = 10^(4.058 ± 0.133 * log10(x) – 6.44 ± 0.324)

The final bear cycle function is:

y = 10^(4.684 ± 0.025 * log10(x) – -9.034 ± 0.063)

The main Criticisms of growth curve models:

The Bitcoin logarithmic growth curve model faces several general criticisms that we’d like to highlight briefly. The most significant, in our view, is its heavy reliance on past price data, which may not accurately forecast future trends. For instance, previous growth curve models from 2020 on TradingView were overly optimistic in predicting the last cycle’s peak.

This is why we aimed to present our process for deriving the final functions in a transparent, step-by-step scientific manner, including statistical confidence intervals. It's important to note that the bull cycle function is less reliable than the bear cycle function, as the top band is significantly wider than the bottom band.

Even so, we still believe that the Bitcoin logarithmic growth curve presented in this script is overly optimistic since it goes parly against the concept of diminishing returns which we discussed in this post:

This is why we also propose alternative parameter settings that align more closely with the theory of diminishing returns."

Now with Z-Score calculation for easy and constant valuation classification of Bitcoin according to this metric.

Created for TRW

Martin Strategy - No Loss Exit v3Martin Strategy1.0 Martin Strategy1.0 Martin Strategy1.0 Martin Strategy1.0 Martin Strategy1.0 Martin Strategy1.0

Multi-Tool Nasdaq US100 IndikatorA combination of several tools such as moving averages (EMA 50, 100, 200), Fibonacci retracements, pivot points, RSI (Relative Strength Index), order blocks, fair value gaps, supply and demand zones, and a simple volume profile.

The indicator is designed to enable high profitability by combining various established technical analysis approaches into one tool, facilitating decision-making regarding entry and exit points.

The script can be integrated and used directly in TradingView by creating a new indicator script and pasting the code there.

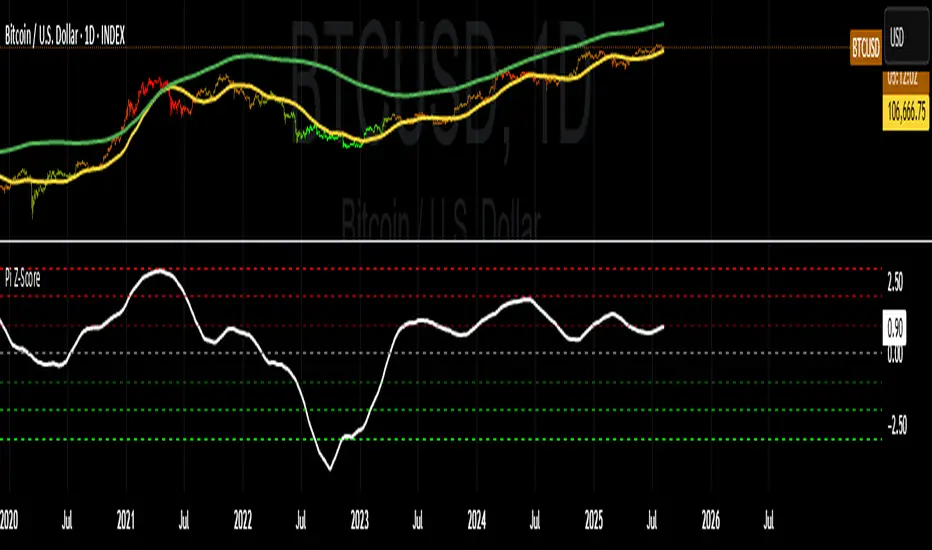

Bitcoin: Pi Cycle Top & Bottom Indicator Z ScoreIndicator Overview

The Pi Cycle Top Indicator has historically been effective in picking out the timing of market cycle highs within 3 days.

It uses the 111 day moving average (111DMA) and a newly created multiple of the 350 day moving average, the 350DMA x 2.

Note: The multiple is of the price values of the 350DMA, not the number of days.

For the past three market cycles, when the 111DMA moves up and crosses the 350DMA x 2 we see that it coincides with the price of Bitcoin peaking.

It is also interesting to note that 350 / 111 is 3.153, which is very close to Pi = 3.142. In fact, it is the closest we can get to Pi when dividing 350 by another whole number.

It once again demonstrates the cyclical nature of Bitcoin price action over long time frames. However, in this instance, it does so with a high degree of accuracy over Bitcoin's adoption phase of growth.

Bitcoin Price Prediction Using This Tool

The Pi Cycle Top Indicator forecasts the cycle top of Bitcoin’s market cycles. It attempts to predict the point where Bitcoin price will peak before pulling back. It does this on major high time frames and has picked the absolute tops of Bitcoin’s major price moves throughout most of its history.

How It Can Be Used

Pi Cycle Top is useful to indicate when the market is very overheated. So overheated that the shorter-term moving average, which is the 111-day moving average, has reached an x2 multiple of the 350-day moving average. Historically, it has proved advantageous to sell Bitcoin around this time in Bitcoin's price cycles.

It is also worth noting that this indicator has worked during Bitcoin's adoption growth phase, the first 15 years or so of Bitcoin's life. With the launch of Bitcoin ETF's and Bitcoin's increased integration into the global financial system, this indicator may cease to be relevant at some point in this new market structure.

Added the Z-Score metric for easy classification of the value of Bitcoin according to this indicator.

Created for TRW

Opening Range Breakout (9:30 - 9:45 EST)Here's a Pine Script (v5) for TradingView that plots the Opening Range Breakout (ORB) lines from 9:30 AM to 9:45 AM EST on a 15-minute chart.

It draws a green line at the high of the opening range and a red line at the low, both extending through the rest of the day.