Custom MACD (Normalized by ATR)This is a modified version of the classic MACD indicator.

Instead of using just the difference between EMA(12) and EMA(26), this version normalizes the MACD line by ATR(26) and scales it by 100:

* 100

This adjustment makes the MACD relative to market volatility, allowing for easier comparison across assets and timeframes.

The idea of normalizing MACD with ATR comes from Alex Spioglou, who suggested this improvement to enhance signal consistency in volatile markets.

Plots include the ATR-normalized MACD line, the signal line, and the histogram, with rising/falling color cues and built-in alert conditions.

M-oscillator

CMC Macro Regime PanelOverview (what it is):

A macro‑regime gate built entirely from TradingView-native symbols (CRYPTOCAP, FRED, DXY/VIX, HYG/LQD). It aggregates central‑bank liquidity (Fed balance sheet − RRP − Treasury General Account), USD strength, credit conditions, stablecoin flows/dominance, tech beta and BTC–NDX co‑move into one normalized score (CLRC). The panel outputs Risk‑ON/OFF regimes, an Early 3/5 pre‑signal, and an automatic BTC vs ETH vs ALTs preference. It is intentionally scoped to Daily & Weekly reads (no intraday timing). Publish with a clean chart and a clear description as per TradingView rules.

TradingView

Why we also use other TradingView screens (and why that is compliant)

This script pulls data via request.security() from official TV symbols only; users often want to open the raw series on separate charts to sanity‑check:

CRYPTOCAP indices: TOTAL, TOTAL2, TOTAL3 (market cap aggregates) and dominance tickers like BTC.D, USDT.D. Helpful for regime & rotation (ALTs vs BTC). TradingView provides definitions for crypto market cap and dominance symbols.

TradingView

+3

TradingView

+3

TradingView

+3

FRED releases: WALCL (Fed assets, weekly), RRPONTSYD (ON RRP, daily), WTREGEN (TGA, weekly), M2SL (M2, monthly). These are the official macro sources exposed on TV.

FRED

+3

FRED

+3

FRED

+3

Risk proxies: TVC:DXY (USD index), TVC:VIX (implied vol), AMEX:HYG/AMEX:LQD (credit), NASDAQ:NDX (tech beta), BINANCE:ETHBTC. VIX/NDX relationship is well-documented; VIX measures 30‑day expected S&P500 vol.

TradingView

+2

TradingView

+2

Compliance note: Using multiple screens is optional for users, but it explains/justifies how components work together (a requirement for public scripts). Keep publication chart clean; use extra screens only to illustrate in the description.

TradingView

How it works (high level)

Liquidity block (Weekly/Monthly)

Net Liquidity = WALCL − RRPONTSYD − WTREGEN (YoY z‑score). WALCL is weekly (as of Wednesday) via H.4.1; RRP is daily; TGA is a Fed liability series. M2 YoY is monthly.

FRED

+3

FRED

+3

FRED

+3

Risk conditions (Daily)

DXY 3‑month momentum (inverted), VIX level (inverted), Credit (HYG/LQD ratio or HY OAS). VIX is a 30‑day constant‑maturity implied vol index per Cboe methodology.

Cboe

+1

Crypto‑internal (Daily)

Stablecoins (USDT+USDC+DAI 30‑day log change), USDT dominance (20‑day, inverted), TOTAL3 (63‑day momentum). Dominance symbols on TV follow a documented formula.

TradingView

Beta & co‑move (Daily)

NDX 63‑day momentum, BTC↔NDX 90‑day correlation.

All components become z‑scores (optionally clipped), weighted, missing inputs drop and weights renormalize. We never use lookahead; we confirm on bar close to avoid repainting per Pine docs (barstate.isconfirmed, multi‑TF).

TradingView

+2

TradingView

+2

What you see on the chart

White line (CLRC) = macro regime score.

Background: Green = Risk‑ON, Red = Risk‑OFF, Teal = Early 3/5 (pre‑signal).

Table: shows each component’s z‑score and the Preference: BTC / ETH / ALTs / Mixed.

Signals & interpretation

Designed for Daily (1D) and Weekly (1W) only.

Regime gates (default Fast preset):

Enter ON: CLRC ≥ +0.8; Hold ON while ≥ +0.5.

Enter OFF: CLRC ≤ −1.0; Hold OFF while ≤ −0.5.

0 / ±1 reading: CLRC is a standardized composite.

~0 = neutral baseline (no macro edge).

≥ +1 = strong macro tailwind (≈ +1σ).

≤ −1 = strong headwind (≈ −1σ).

Early 3/5 (teal): a fast pre‑signal when at least 3 of 5 daily checks align: USDT.D↓, DXY↓, VIX↓, HYG/LQD↑, ETHBTC↑ or TOTAL3↑. It often precedes a full ON flip—use for pre‑positioning rather than full sizing.

BTC/ETH/ALTs selector (only when ON):

ALTs when BTC.D↓ and (ETHBTC↑ or TOTAL3↑) ⇒ rotate down the risk curve.

BTC when BTC.D↑ and ETHBTC↓ ⇒ keep it concentrated.

ETH when ETHBTC↑ while BTC.D flat/up ⇒ add ETH beta.

(Dominance mechanics are documented by TV.)

TradingView

Dissonance (incompatibility) rules — when to stand down

Use these overrides to avoid false comfort:

CLRC > +1 but USDT.D↑ and/or VIX spikes day‑over‑day → downgrade to Neutral; wait for USDT.D to stabilize and VIX to cool (VIX is a fear gauge of 30‑day expectation).

Cboe Global Markets

CLRC > +1 but DXY↑ sharply (USD squeeze) → size below normal; require DXY momentum to roll over.

CLRC < −1 but Early 3/5 = true two days in a row → start reducing underweights; look for ON flip within a few bars.

NetLiq improving (W) but credit (HYG/LQD) deteriorating (D) → treat as mixed regime; prefer BTC over ALTs.

How to use (step‑by‑step)

A. Read on Daily (1D) — main regime

Open CRYPTOCAP:TOTAL3, 1D (panel applied).

Wait for bar close (use alerts on confirmed bar). Pine docs recommend barstate.isconfirmed to avoid repainting on realtime bars.

TradingView

If ON, check Preference (BTC / ETH / ALTs).

Then drop to 4H on your trading pair for micro entries (this indicator itself is not for intraday timing).

B. Confirm weekly macro (1W) — once per week)

Review WALCL/RRP/TGA after the H.4.1 release on Thursdays ~4:30 pm ET. WALCL is “Weekly, as of Wednesday”; M2 is Monthly—so do not expect daily responsiveness from these.

Federal Reserve

+2

FRED

+2

Recommended check times (practical schedule)

Daily regime read: right after your chart’s daily close (confirmed bar). For consistent timing across crypto, many users set chart timezone to UTC and read ~00:05 UTC; you can change chart timezone in TV’s settings.

TradingView

In‑day monitoring: optional spot checks 16:00 & 20:00 UTC (DXY/VIX move during US hours), but act only after the daily bar confirms.

Weekly macro pass: Thu 21:30–22:30 UTC (after H.4.1 4:30 pm ET) or Fri after daily close, to let weekly FRED series propagate.

Federal Reserve

Limitations & data latency (be explicit)

Higher‑TF data & confirmation: FRED weekly/monthly series will not reflect intraday risk in crypto; we aggregate them for regime, not for entry timing.

Repainting 101: Realtime bars move until close. This script does not use lookahead and follows Pine guidance on multi‑TF series; still, always act on confirmed bars.

TradingView

+1

Public‑library compliance: Title EN‑only; description starts in EN; clean chart; justify component mash‑up; no lookahead; no unrealistic claims.

TradingView

Alerts you can use

“Macro Risk‑ON (entry)” — fires on ON flip (confirmed bar).

“Macro Risk‑OFF (entry)” — fires on OFF flip.

“Early 3/5” — fires when the teal pre‑signal appears (not a regime flip).

“Preference change” — BTC/ETH/ALTs toggles while ON.

Publish note: Alerts are fine; just avoid implying guaranteed accuracy/performance.

TradingView

Background research (why these inputs matter)

Liquidity → Crypto: Fed H.4.1 timing and series definitions (WALCL, RRP, TGA) formalize the “net liquidity” concept used here.

FRED

+3

Federal Reserve

+3

FRED

+3

Stablecoins ↔ Non‑stable crypto: empirical work shows bi‑directional causality between stablecoin market cap and non‑stable crypto cap; stablecoin growth co‑moves with broader crypto activity.

Global liquidity link: world liquidity positively relates to total crypto market cap; lagged effects are observed at monthly horizons.

VIX/Uncertainty effect: fear shocks impair BTC’s “safe haven” behavior; VIX is a meaningful risk‑off read.

Repulse OB/OS Z-Score (v3)🔹 What this script does

This indicator is an enhanced version of the Repulse, originally developed by Eric Lefort. The Repulse measures bullish and bearish pressure in the market by analyzing price momentum and crowd behavior.

In this version, I introduce a Z-Score transformation to the Repulse values. The Z-Score converts raw outputs into a standardized statistical scale, allowing traders to identify when pressure is abnormally high or low relative to historical conditions.

🔹 How it works

Repulse Core: The original Repulse calculation compares buying vs. selling pressure, highlighting shifts in momentum.

Z-Scoring Method: Repulse values are normalized around their mean and scaled by standard deviation. This transforms the indicator into a dimensionless metric, where:

Positive Z-Scores indicate stronger-than-usual bullish pressure.

Negative Z-Scores indicate stronger-than-usual bearish pressure.

Bands: Thresholds such as ±1 or ±2 Z-Scores can help detect when pressure is stretched, potentially signaling exhaustion or reversal points.

🔹 Why it’s useful

Statistical Clarity: Traders can instantly see whether current pressure is normal or extreme.

Cross-Asset Comparisons: Because Z-Scores are standardized, signals can be compared across different markets or timeframes.

Mean Reversion Tool: Extreme Z-Score values often precede turning points, making this a versatile addition to trend and momentum analysis.

🔹 How to use it

Apply the indicator to any chart and timeframe.

Watch for Z-Scores above +2 (possible overheated bullish pressure) or below –2 (possible oversold/exhaustion).

Use these levels as contextual signals, not standalone triggers. Best results come from combining with price structure, support/resistance, or volume analysis.

⚠️ Note: This script does not predict price. It highlights statistical extremes in pressure to support decision-making. Always use in combination with other tools and risk management practices.

RSI Crossover with Candlestick Patternsusing the RSI indicator levels 40 and 60, where the signal cuts above level 40 with a candlestick hammer or bull engulfing and cuts below level 60 with a candlestick inverter hammer or bearish engulfing.

Stochastic Divergence Indicatorshows bullish and bearish divergence with green and red candles. white border for double dip

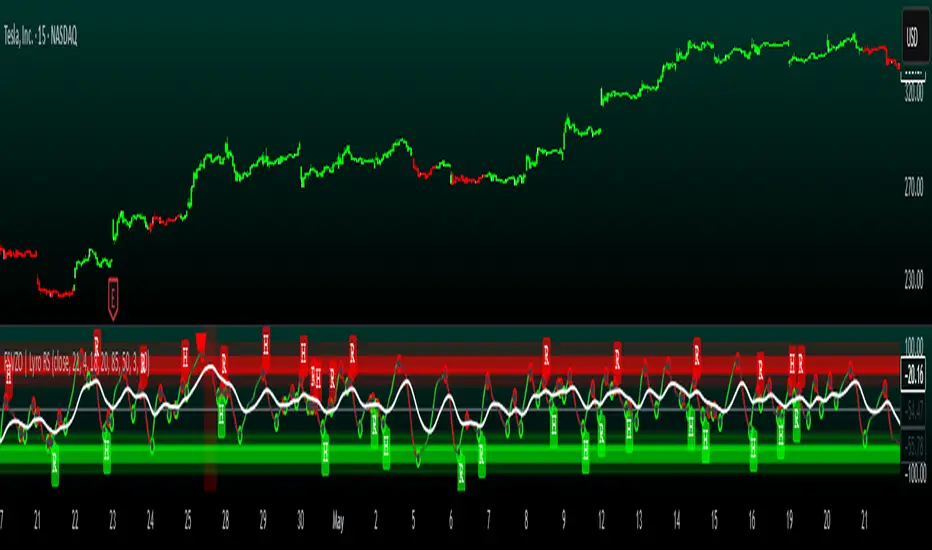

FSVZO | Lyro RSFSVZO | Lyro RS

This script is a technical analysis tool called the FSVZO, or Fourier Smoothed Volume Zone Oscillator. It is designed to analyze market momentum and trend strength by combining price and volume data with advanced smoothing techniques. The goal is to help identify potential trends, overbought/oversold conditions, and divergence signals in a clear visual format.

Understanding the Indicator's Components

The indicator plots a main oscillator line and several supporting elements on a separate pane below the chart.

The Main Oscillator: This is the primary, colored wave. Its movement and color are key to interpretation.

Trend Direction: The color shifts between bullish and bearish tones based on the momentum of the oscillator. This provides a quick visual reference for the prevailing short-term trend.

Key Levels: Horizontal lines mark significant levels such as +60, +85, -60, and -85. Movements above +60 or below -60 can indicate strong momentum, while approaches to the extreme levels (+85/-85) may suggest overbought or oversold conditions.

Divergence Detection: The indicator can plot labels ("ℝ" for Regular, "ℍ" for Hidden) on the oscillator to signal potential divergences. These occur when the indicator's direction differs from the price action on the main chart and can sometimes foreshadow reversals or continuations.

Moving Average (MA): A central moving average line, based on the oscillator, helps to smooth out the data further and can act as a dynamic support or resistance level within the indicator pane.

White Noise Filter (Optional): This feature displays a histogram that represents market noise. It can be toggled on or off. Analyzing the histogram's behavior may provide additional context on the stability or volatility of the current trend.

Dynamic Background: The background of the indicator pane can change color to highlight periods where the momentum is particularly strong, based on the position of the moving average.

Suggested Use and Interpretation

Traders might use this indicator in several ways:

Trend Identification: Observe the color and position of the main oscillator. A predominantly bullish-colored oscillator above the zero line may suggest an upward trend, while a bearish-colored one below zero may suggest a downward trend.

Signal Confirmation: Look for the oscillator to cross key levels (like +/-40 or +/-60) in the direction of a suspected trend as a confirmation signal.

Divergence Analysis: When the price makes a new high or low that is not confirmed by a new high or low on the FSVZO oscillator (a divergence), it can be a warning of potential weakness in the trend. The "ℝ" and "ℍ" labels help to identify these scenarios.

Extreme Readings: Readings near the +85 or -85 levels can indicate that a price move may be overextended, which could precede a pause or reversal.

Customization Options

The indicator includes settings groups that allow you to adjust its behavior and appearance:

FSVZO Settings: Adjust parameters like Length and Sensitivity to make the oscillator more or less responsive to market movements.

Signals & Display: Modify visual aspects such as Smooth Length and Glowing Amount, or toggle features like the dynamic background on and off.

Colors: Choose from several pre-set color palettes to suit your visual preferences.

⚠️Disclaimer

This indicator is a tool for technical analysis and does not provide guaranteed results. It should be used in conjunction with other analysis methods and proper risk management practices. The creators of this indicator are not responsible for any financial decisions made based on its signals.

VWAP Momentum Oscillator How It Works

Core Calculation Method

The oscillator combines four key market measurements into a single, normalized reading:

1. Price-VWAP Deviation: `(Close - VWAP) / VWAP × 100`

2. VWAP-MA Momentum: `(VWAP - MovingAverage) / MovingAverage × 100`

3. Anchored VWAP Strength: Average of high/low anchor deviations from rolling VWAP

4. Range Position: `(Close - PeriodLow) / (PeriodHigh - PeriodLow) × 100 - 50`

Dynamic Signal Line

The signal line uses an EMA that automatically adjusts its length based on your chart timeframe:

- Futures: Always covers 23 hours of trading (1,380 minutes)

- Stocks: Always covers 6.5 hours of trading (390 minutes)

- Examples: 276 periods on 5-min futures chart, 1,380 periods on 1-min futures chart

Trading Signals

🟢 Buy Signals

- Condition: Main oscillator crosses above signal line while below zero

- Logic: Momentum turning bullish from oversold conditions

- Visual: Green "BUY" label below price action

🔴 Sell Signals

- Condition: Main oscillator crosses below signal line while above zero

- Logic: Momentum turning bearish from overbought conditions

- Visual: Red "SELL" label above price action

⚠️ Extreme Warnings

- Extreme Overbought: Red triangle when oscillator crosses above +4.0

- Extreme Oversold: Green triangle when oscillator crosses below -4.0

- Purpose: Risk management alerts, not entry/exit signals

Oscillator Zones

Interpretation Guide

- Above +2.0: Strong bullish momentum zone (green background)

- 0 to +2.0: Mild bullish territory

- 0 to -2.0: Mild bearish territory

- Below -2.0: Strong bearish momentum zone (red background)

- Above +4.0: Extreme overbought (caution advised)

- Below -4.0: Extreme oversold (potential reversal zone)

Customization Options

Moving Average Settings

- EMA/SMA Toggle: Choose between exponential or simple moving average

- Color Customization: Adjust MA line color and width

Visual Controls

- Bullish/Bearish Colors: Customize momentum zone colors

- Signal Line: Toggle visibility and adjust color

- Line Widths: Control thickness of all plot lines

Anchor Modes

- NY Session Only: Anchors reset at NY market open (9:30 AM ET)

- 24H NY Day: Anchors reset at NY calendar day change (midnight ET)

Best Practices

Timeframe Selection

- Scalping: 1-5 minute charts for quick momentum changes

- Day Trading: 5-15 minute charts for clearer trend signals

- Swing Trading: 1-4 hour charts for major momentum shifts

Signal Confirmation

- Wait for crossovers: Don't trade on oscillator position alone

- Respect extreme levels: Exercise caution above +4 or below -4

- Use with price action: Combine with support/resistance levels

Risk Management

- Extreme zones: Reduce position size when oscillator is extended

- Failed signals: Exit quickly if momentum doesn't follow through

- Market context: Consider overall trend direction and market volatility

Technical Specifications

Calculation Components

- Base Length: 1,380 periods (futures) / 390 periods (stocks)

- Signal Line: Dynamic EMA covering one full trading day

- Smoothing: 3-period SMA on raw oscillator (adjustable)

- Update Frequency: Real-time on every price tick

Performance Notes

- Resource Efficient: Optimized calculations minimize CPU usage

- Memory Friendly: Uses incremental VWAP calculations

- Fast Loading: Minimal historical data requirements

Version History & Development

This oscillator evolved from advanced VWAP overlay strategies, transforming complex multi-line analysis into a single, actionable momentum gauge. The indicator maintains the sophistication of institutional VWAP analysis while providing the clarity needed for retail trading decisions.

Core Philosophy

Traditional VWAP indicators show where price is relative to volume-weighted averages, but they don't quantify momentum or provide clear entry/exit signals. This oscillator solves that problem by normalizing all VWAP relationships into a single, bounded indicator that works consistently across all timeframes and asset classes.

---

Open Source License: This indicator is provided free for the TradingView community. Feel free to modify and enhance according to your trading needs.

EMA Regime (9/20/50/100/200) — Stacked with 200 FilterEMA Regime (9/20/50/100/200) — Stacked Long/Short Box

Plots the 9, 20, 50, 100, and 200 EMAs on the chart.

Checks if price is above or below each EMA and whether the EMAs are stacked in order.

LONG signal: price above all selected EMAs and EMAs stacked 9 > 20 > 50 > 100 >(> 200 if strict mode on).

SHORT signal: price below all selected EMAs and EMAs stacked 9 < 20 < 50 < 100 (< 200 if strict mode on).

Shows a two-row table (LONGS / SHORTS) so you can quickly see which EMAs are aligned.

Optionally colors candles green/red when a full long/short regime is active.

Can show labels when a new LONG or SHORT condition appears.

Has alerts you can use for automated notifications when the regime flips.

“Use 200 EMA in the stack” lets you choose ultra-strict mode (9>20>50>100>200) or lighter mode (9>20>50>100 but price & 9 above 200).

Oscillator Matrix [Alpha Extract]A comprehensive multi-oscillator system that combines volume-weighted money flow analysis with enhanced momentum detection, providing traders with a unified framework for identifying high-probability market opportunities across all timeframes. By integrating two powerful oscillators with advanced confluence analysis, this indicator delivers precise entry and exit signals while filtering out market noise through sophisticated threshold-based regime detection.

🔶 Volume-Weighted Money Flow Analysis

Utilizes an advanced money flow calculation that tracks volume-weighted price movements to identify institutional activity and smart money flow. This approach provides superior signal quality by emphasizing high-volume price movements while filtering out low-volume market noise.

// Volume-weighted flows

up_volume = price_up ? volume : 0

down_volume = price_down ? volume : 0

// Money Flow calculation

up_vol_sum = ta.sma(up_volume, mf_length)

down_vol_sum = ta.sma(down_volume, mf_length)

total_volume = up_vol_sum + down_vol_sum

money_flow_ratio = total_volume > 0 ? (up_vol_sum - down_vol_sum) / total_volume : 0

🔶 Enhanced Hyper Wave Oscillator

Features a sophisticated MACD-based momentum oscillator with advanced normalization techniques that adapt to different price ranges and market volatility. The system uses percentage-based calculations to ensure consistent performance across various instruments and timeframes.

// Enhanced MACD-based oscillator

fast_ma = ta.ema(src, hw_fast)

slow_ma = ta.ema(src, hw_slow)

macd_line = fast_ma - slow_ma

signal_line = ta.ema(macd_line, hw_signal)

// Proper normalization using percentage of price

price_base = ta.sma(close, 50)

macd_normalized = macd_line / price_base

hyper_wave = macd_range > 0 ? macd_normalized / macd_range : 0

🔶 Multi-Factor Confluence System

Implements an intelligent confluence scoring mechanism that combines signals from both oscillators to identify high-probability trading opportunities. The system assigns strength scores based on multiple confirmation factors, significantly reducing false signals.

🔶 Fixed Threshold Levels

Uses predefined threshold levels optimized for standard oscillator ranges to distinguish between normal market fluctuations and significant momentum shifts. The dual-threshold system provides clear visual cues for overbought/oversold conditions while maintaining consistent signal criteria across different market conditions.

🔶 Overflow Detection Technology

Advanced overflow indicators identify extreme market conditions that often precede major reversals or continuation patterns. These signals highlight moments when market momentum reaches critical levels, providing early warning for potential turning points.

🔶 Dual Oscillator Integration

The indicator simultaneously tracks volume-weighted money flow and momentum-based price action through two independent oscillators. This dual approach ensures comprehensive market analysis by capturing both institutional activity and technical momentum patterns.

// Multi-factor confluence scoring

confluence_bull = (mf_bullish ? 1 : 0) + (hw_bullish ? 1 : 0) +

(mf_overflow_bull ? 1 : 0) + (hw_overflow_bull ? 1 : 0)

confluence_bear = (mf_bearish ? 1 : 0) + (hw_bearish ? 1 : 0) +

(mf_overflow_bear ? 1 : 0) + (hw_overflow_bear ? 1 : 0)

confluence_strength = confluence_bull > confluence_bear ? confluence_bull / 4 : -confluence_bear / 4

🔶 Intelligent Signal Generation

The system generates two tiers of reversal signals: strong signals that require multiple confirmations across both oscillators, and weak signals that identify early momentum shifts. This hierarchical approach allows traders to adjust position sizing based on signal strength.

🔶 Visual Confluence Zones

Background coloring dynamically adjusts based on confluence strength, creating visual zones that immediately communicate market sentiment. The intensity of background shading corresponds to the strength of the confluent signals, making pattern recognition effortless.

🔶 Threshold Visualization

Color-coded threshold zones provide instant visual feedback about oscillator positions relative to key levels. The fill areas between thresholds create clear overbought and oversold regions with graduated color intensity.

🔶 Candle Color Integration

Optional candle coloring applies confluence-based color logic directly to price bars, creating a unified visual framework that helps traders correlate indicator signals with actual price movements for enhanced decision-making.

🔶 Overflow Alert System

Specialized circular markers highlight extreme overflow conditions on both oscillators, drawing attention to potential climax moves that often precede significant reversals or accelerated trend continuation.

🔶 Customizable Display Options

Comprehensive display controls allow traders to toggle individual components on or off, enabling focused analysis on specific aspects of the indicator. This modularity ensures the indicator adapts to different trading styles and analytical preferences.

1 Week

1 Day

15 Min

This indicator provides a complete analytical framework by combining volume analysis with momentum detection in a single, coherent system. By offering multiple confirmation layers and clear visual hierarchies, it empowers traders to identify high-probability opportunities while maintaining precise risk management across all market conditions and timeframes. The sophisticated confluence system ensures that signals are both timely and reliable, making it an essential tool for serious technical analysts.

Stochastic Divergence StrategyBackground bars:

Bearish

gradient from slightly bearish divergence to strong bearish divergence for red and a double bounce for pink

Bullish

gradient from slightly bearish divergence to strong bearish divergence for green and a double bounce for yellow

removable buy and sell signals in options

Stochastic [Paifc0de]Stochastic — clean stochastic oscillator with visual masking, neutral markers, and basic filters

What it does

This indicator plots a standard stochastic oscillator (%K with smoothing and %D) and adds practical quality-of-life features for lower timeframes: optional visual masking when %K hugs overbought/oversold, neutral K–D cross markers, session-gated edge triangles (K crossing 20/80), and simple filters (minimum %K slope, minimum |K–D| gap, optional %D slope agreement, mid-zone mute, and a cooldown between markers). Display values are clamped to 0–100 to keep the panel scale stable. The tool is for research/education and does not generate entries/exits or financial advice.

Default preset: 20 / 10 / 10

K Length = 20

Classic lookback used in many textbooks. On intraday charts it balances responsiveness and stability: short enough to react to momentum shifts, long enough to avoid constant whipsaws. In practice it captures ~the last 20 bars’ position of close within the high–low range.

K Smoothing = 10

A 10-period SMA applied to the raw %K moderates the “saw-tooth” effect that raw stochastic can exhibit in choppy phases. The smoothing reduces over-reaction to micro spikes while preserving the main rhythm of swings; visually, %K becomes a continuous path that is easier to read.

D Length = 10

%D is the moving average of smoothed %K. With 10, %D becomes a clearly slower guide line. The larger separation between %K(10-SMA) and %D(10-SMA of %K) produces cleaner crosses and fewer spurious toggles than micro settings (e.g., 3/3/3). On M5–M15 this pair often yields readable cross cycles without flooding the chart.

How the 20/10/10 trio behaves

In persistent trends, %K will spend more time near 20 or 80; the 10-period smoothing delays flips slightly and emphasizes only meaningful turn attempts.

In ranges, %K oscillates around mid-zone (40–60). With 10/10 smoothing, cross signals cluster less densely; combining with the |K–D| gap filter helps keep only decisive crosses.

If your symbol is unusually volatile or illiquid, reduce K Length (e.g., 14) or reduce K Smoothing (e.g., 7) to keep responsiveness. If crosses feel late, decrease D Length (e.g., 7). If noise is excessive, increase K Smoothing first, then consider raising D Length.

Visuals

OB/OS lines: default 80/20 reference levels and a midline at 50.

Masking near edges: %K can be temporarily hidden when it is pressing an edge, approaching it with low slope, or going nearly flat near the boundary. This keeps the panel readable during “stuck at the edge” phases.

Soft glow (optional): highlights %K’s active path; can be turned off.

Light/Dark palette: quick toggle to match your chart theme.

Scale safety: all plotted values (lines, fills, markers) are clamped to 0–100 to prevent the axis from expanding beyond the stochastic range.

Markers and filters

Neutral K–D cross markers: circles in the mid-zone when %K crosses %D.

Edge triangles: show when %K crosses 20 or 80; can be restricted to a session window (02:00–12:00 ET).

Filters (optional):

Min %K slope: require a minimum absolute slope so very flat crosses are ignored.

Min |K–D| gap: demand separation between lines at the cross moment.

%D slope agreement: keep crosses that align with %D’s direction.

Mid-zone mute: suppress crosses inside a user-defined 40–60 band (defaults).

Cooldown: minimum bars between successive markers.

Parameters (quick guide)

K Length / K Smoothing / D Length: core stochastic settings. Start with 20/10/10; tune K Smoothing first if you see too much jitter.

Overbought / Oversold (80/20): adjust for assets that tend to trend (raise to 85/15) or mean-revert (lower to 75/25).

Slope & gap filters: increase on very noisy symbols; reduce if you miss too many crosses.

Session window (triangles only): use if you want edge markers only during active hours.

Marker size and offset: cosmetic; they do not affect calculations.

Alerts

K–D Cross Up (filtered) and K–D Cross Down (filtered): fire when a cross passes your filters/cooldown.

Edge Up / Edge Down: fire when %K crosses the 20/80 levels.

All alerts confirm on bar close.

Notes & attribution

Original implementation and integration by Paifc0de; no third-party code is copied.

This indicator is for research/education and does not provide entries/exits or financial advice.

Market Pressure Oscillator█ OVERVIEW

The Market Pressure Oscillator is an advanced technical indicator for TradingView, enabling traders to identify potential trend reversals and momentum shifts through candle-based pressure analysis and divergence detection. It combines a smoothed oscillator with moving average signals, overbought/oversold levels, and divergence visualization, enhanced by customizable gradients, dynamic band colors, and alerts for quick decision-making.

█ CONCEPT

The indicator measures buying or selling pressure based on candle body size (open-to-close difference) and direction, with optional smoothing for clarity and divergence detection between price action and the oscillator. It relies solely on candle data, offering insights into trend strength, overbought/oversold conditions, and potential reversals with a customizable visual presentation.

█ WHY USE IT?

- Divergence Detection: Identifies bullish and bearish divergences to reinforce signals, especially near overbought/oversold zones.

- Candle Pressure Analysis: Measures pressure based on candle body size, normalized to a ±100 scale.

- Signal Generation: Provides buy/sell signals via overbought/oversold crossovers, zero-line crossovers, moving average zero-line crossovers, and dynamic band color changes.

- Visual Clarity: Uses dynamic colors, gradients, and fill layers for intuitive chart analysis.

Flexibility: Extensive settings allow customization to individual trading preferences.

█ HOW IT WORKS?

- Candle Pressure Calculation: Computes candle body size as math.abs(close - open), normalized against the average body size over a lookback period (avgBody = ta.sma(body, len)). - Candle direction (bullish: +1, bearish: -1, neutral: 0) is multiplied by body weight to derive pressure.

- Cumulative Pressure: Sums pressure values over the lookback period (Lookback Length) and normalizes to ±100 relative to the maximum possible value.

- Smoothing: Optionally applies EMA (Smoothing Length) to normalized pressure.

- Moving Average: Calculates SMA (Moving Average Length) for trend confirmation (Moving Average (SMA)).

- Divergence Detection: Identifies bullish/bearish divergences by comparing price and oscillator pivot highs/lows within a specified range (Pivot Length). Divergence signals appear with a delay equal to the Pivot Length.

- Signals: Generates signals for:

Crossing oversold upward (buy) or overbought downward (sell).

Crossing the zero line by the oscillator or moving average (buy/sell).

Bullish/bearish divergences, marked with labels, enhancing signals, especially near overbought/oversold zones.

Dynamic band color changes when the moving average crosses MA overbought/oversold thresholds (green for oversold, red for overbought).

- Visualization: Plots the oscillator and moving average with dynamic colors, gradient fills, transparent bands, and labels, with customizable overbought/oversold levels.

Alerts: Built-in alerts for divergences, overbought/oversold crossovers, and zero-line crossovers (oscillator and moving average).

█ SETTINGS AND CUSTOMIZATION

- Lookback Length: Period for aggregating candle pressure (default: 14).

- Smoothing Length (EMA): EMA length for smoothing the oscillator (default: 1). Higher values smooth the signal but may reduce signal frequency; adjust overbought/oversold levels accordingly.

- Moving Average Length (SMA): SMA length for the moving average (default: 14, minval=1). Higher values make SMA a trend indicator, requiring adjusted MA overbought/oversold levels.

- Pivot Length (Left/Right): Candles for detecting pivot highs/lows in divergence calculations (default: 2, minval=1). Higher values reduce noise but add delay equal to the set value.

- Enable Divergence Detection: Enables divergence detection (default: true).

- Overbought/Oversold Levels: Thresholds for the oscillator (default: 30/-30) and moving average (default: 10/-10). For the moving average, no arrows appear; bands change color from gray to green (oversold) or red (overbought), reinforcing entry signals.

- Signal Type: Select signals to display: "None", "Overbought/Oversold", "Zero Line", "MA Zero Line", "All" (default: "Overbought/Oversold").

- Colors and Gradients: Customize colors for bullish/bearish oscillator, moving average, zero line, overbought/oversold levels, and divergence labels.

- Transparency: Adjust gradient fill transparency (default: 70, minval=0, maxval=100) and band/label transparency (default: 40, minval=0, maxval=100) for consistent visuals.

- Visualizations: Enable/disable moving average, gradients for zero/overbought/oversold levels, and gradient fills.

█ USAGE EXAMPLES

- Momentum Analysis: Observe the MPO Oscillator above 0 for bullish momentum or below 0 for bearish momentum. The SMA, being smoother, reacts slower and can confirm trend direction as a noise filter.

- Reversal Signals: Look for buy triangles when the oscillator crosses oversold upward, especially when the SMA is below the MA oversold threshold and the band turns green. Similarly, seek sell triangles when crossing overbought downward, with the SMA above the MA overbought threshold and the band turning red.

- Using Divergences: Treat bullish (green labels) and bearish (red labels) divergences as reinforcement for other signals, especially near overbought/oversold zones, indicating stronger potential trend reversals.

- Customization: Adjust lookback length, smoothing, and moving average length to specific instruments and timeframes to minimize false signals.

█ USER NOTES

Combine the indicator with tools like Fibonacci levels or pivot points to enhance accuracy.

Test different settings for lookback length, smoothing, and moving average length on your chosen instrument and timeframe to find optimal values.

Algorithmic Value Oscillator [CRYPTIK1]Algorithmic Value Oscillator

Introduction: What is the AVO? Welcome to the Algorithmic Value Oscillator (AVO), a powerful, modern momentum indicator that reframes the classic "overbought" and "oversold" concept. Instead of relying on a fixed lookback period like a standard RSI, the AVO measures the current price relative to a significant, higher-timeframe Value Zone .

This gives you a more contextual and structural understanding of price. The core question it answers is not just "Is the price moving up or down quickly?" but rather, " Where is the current price in relation to its recently established area of value? "

This allows traders to identify true "premium" (overbought) and "discount" (oversold) levels with greater accuracy, all presented with a clean, futuristic aesthetic designed for the modern trader.

The Core Concept: Price vs. Value The market is constantly trying to find equilibrium. The AVO is built on the principle that the high and low of a significant prior period (like the previous day or week) create a powerful area of perceived value.

The Value Zone: The range between the high and low of the selected higher timeframe.

Premium Territory (Distribution Zone): When the oscillator moves into the glowing pink/purple zone above +100, it is trading at a premium.

Discount Territory (Accumulation Zone): When the oscillator moves into the glowing teal/blue zone below -100, it is trading at a discount.

Key Features

1. Glowing Gradient Oscillator: The main oscillator line is a dynamic visual guide to momentum.

The line changes color smoothly from light blue to neon teal as bullish momentum increases.

It shifts from hot pink to bright purple as bearish momentum increases.

Multiple transparent layers create a professional "glow" effect, making the trend easy to see at a glance.

2. Dynamic Volatility Histogram: This histogram at the bottom of the indicator is a custom volatility meter. It has been engineered to be adaptive, ensuring that the visual differences between high and low volatility are always clear and dramatic, no matter your zoom level. It uses a multi-color gradient to visualize the intensity of market volatility.

3. Volatility Regime Dashboard: This simple on-screen table analyzes the histogram and provides a clear, one-word summary of the current market state: Compressing, Stable, or Expanding.

How to Use the AVO: Trading Strategies

1. Reversion Trading This is the most direct way to use the indicator.

Look for Buys: When the AVO line drops into the teal "Accumulation Zone" (below -100), the price is trading at a discount. Watch for the oscillator to form a bottom and start turning up as a signal that buying pressure is returning.

Look for Sells: When the AVO line moves into the pink "Distribution Zone" (above +100), the price is trading at a premium. Watch for the oscillator to form a peak and start turning down as a signal that selling pressure is increasing.

2. Best Practices & Settings

Timeframe Synergy: The AVO is most effective when your chart timeframe is lower than your selected "Value Zone Source." For example, if you trade on the 1-hour chart, set your Value Zone to "Previous Day."

Confirmation is Key: This indicator provides powerful context, but it should not be used in isolation. Always combine its readings with your primary analysis, such as market structure and support/resistance levels.

Premier Stochastic Oscillator [LazyBear, V2]This script builds on the well-known Premier Stochastic Oscillator (PSO) originally introduced by LazyBear, and adds a Z-Score extension to provide statistical interpretation of momentum extremes.

Features

Premier Stochastic Core: A smoothed stochastic calculation that highlights bullish and bearish momentum phases.

Z-Score Mapping: The PSO values are standardized into Z-Scores (from –3 to +3), quantifying the degree of momentum stretch.

Positive / Negative Z-Scores:

Positive Z values suggest momentum strength that can align with accumulation or favorable buying conditions.

Negative Z values indicate stronger bearish pressure, often aligning with selling or distribution conditions.

On-Chart Label: The current Z-Score is displayed on the latest bar for quick reference.

How to Use

Momentum Confirmation: Use the oscillator to confirm whether bullish or bearish momentum is intensifying.

Overextended Conditions: Extreme Z-Scores (±2 or beyond) highlight statistically stretched conditions, often preceding reversions.

Strategic Integration: Best applied in confluence with trend tools or higher-timeframe filters; not a standalone trading signal.

Originality

Unlike the standard PSO, this version:

Adds a Z-Score framework for objective statistical scaling.

Provides real-time labeling of Z values for clarity.

Extends the classic oscillator into a tool for both momentum detection and mean-reversion context.

RSI ScannerRSI Scanner

This script scans a custom list of symbols and displays their RSI values for a selected higher timeframe (default: 3M). It provides a quick way to monitor multiple markets in one place without switching charts.

Features:

Customizable timeframe for RSI calculation (default: 3M).

Adjustable RSI length and source input.

Flexible filter: display all symbols or only those with RSI above a chosen threshold.

Input your own list of symbols (stocks, forex, futures, crypto) via a text field.

Results displayed in a clean, table directly on the chart.

Automatic column split when the symbol list is long.

Table header shows selected timeframe and filter settings for clarity.

How to use:

Add the script to your chart.

Open the Inputs panel.

In Symbols List, enter the tickers you want to track, separated by commas (e.g. AAPL, TSLA, EURUSD, BTCUSD).

Set the desired Timeframe (e.g. 3M, 1M, W).

Adjust RSI Length and Source if needed.

Enable or disable filtering:

If filtering is enabled, only symbols with RSI ≥ the threshold will be shown.

If disabled, all entered symbols will be displayed.

The table in the top-right corner will update automatically on the last bar.

Use cases:

Monitor RSI across different asset classes on higher timeframes.

Quickly spot overbought symbols (e.g. RSI > 70) without switching charts.

Create a custom multi-market watchlist tailored to your strategy.

Katz Impact Wave 🚀Overview of the Katz Impact Wave 🚀

The Katz Impact Wave is a momentum oscillator designed to visualize the battle between buyers and sellers. Instead of combining bullish and bearish pressure into a single line, it separates them into two distinct "Impact Waves."

Its primary goal is to generate clear trade signals by identifying when one side gains control, but only when the market has enough volatility to be considered "moving." This built-in filter helps to avoid signals during flat or choppy market conditions.

Indicator Components: Lines & Plots

Impact Waves & Fill

Green Wave (Total Up Impulses): This line represents the cumulative buying pressure. When this line is rising, it indicates that bulls are getting stronger.

Red Wave (Total Down Impulses): This line represents the cumulative selling pressure. When this line is rising, it indicates that bears are getting stronger.

Colored Fill: The shaded area between the two waves provides an at-a-glance view of who is in control.

Lime Fill: Bulls are dominant (Green Wave is above the Red Wave).

Red Fill: Bears are dominant (Red Wave is above the Green Wave).

Background Color

The background color provides crucial context about the market state according to the indicator's logic.

Green Background: The market is in a bullish state (Green Wave is dominant) AND the Rate of Change (ROC) filter confirms the market is actively moving.

Red Background: The market is in a bearish state (Red Wave is dominant) AND the ROC filter confirms the market is actively moving.

Gray Background: The market is considered "not moving" or is in a low-volatility chop. Signals that occur when the background is gray should be viewed with extreme caution or ignored.

Symbols & Pivot Lines

▲ Blue Triangle (Up): This is your long entry signal. It appears on the bar where the Green Wave crosses above the Red Wave while the market is moving.

▼ Orange Triangle (Down): This is your short entry signal. It appears on the bar where the Red Wave crosses above the Green Wave while the market is moving.

Pivot Lines (Solid Green/Red/White Lines): These lines mark confirmed peaks of exhaustion in momentum, not price.

Green Pivot Line: Marks a peak in the Green Wave, signaling buying momentum exhaustion. This can be a warning that the uptrend is losing steam.

Red Pivot Line: Marks a peak in the Red Wave, signaling selling momentum exhaustion. This can be a warning that the downtrend is losing steam.

▼ Yellow Triangle (Compression): This rare signal appears when buying and selling exhaustion pivots happen at the same level. It signifies a point of extreme indecision or equilibrium that often occurs before a major price expansion.

Trading Rules & Strategy

This indicator provides entry signals but does not provide explicit Take Profit or Stop Loss levels. You must use your own risk management rules.

Long Trade Rules

Entry Signal: Wait for a blue ▲ triangle to appear at the top of the indicator panel.

Confirmation: Ensure the background color is green, confirming the market is in a bullish, moving state.

Action: Enter a long (buy) trade at the open of the next candle after the signal appears.

Short Trade Rules

Entry Signal: Wait for an orange ▼ triangle to appear at the bottom of the indicator panel.

Confirmation: Ensure the background color is red, confirming the market is in a bearish, moving state.

Action: Enter a short (sell) trade at the open of the next candle after the signal appears.

Take Profit (TP) & Stop Loss (SL) Ideas

You must develop and test your own exit strategy. Here are some common approaches:

Stop Loss:

Place a stop loss below the most recent significant swing low on the price chart for a long trade, or above the recent swing high for a short trade.

Use an ATR (Average True Range) based stop, such as 2x the ATR value below your entry for a long, to account for market volatility.

Take Profit:

Opposite Signal: The simplest exit is to close your trade when the opposite signal appears (e.g., close a long trade when a short signal ▼ appears).

Momentum Exhaustion: For a long trade, consider taking partial or full profit when a green Pivot Line appears, signaling that buying momentum is peaking.

Fixed Risk/Reward: Use a predetermined risk/reward ratio (e.g., 1:1.5 or 1:2).

Disclaimer

This indicator is a tool for analysis, not a financial advisor or a guaranteed profit system. All trading and investment activities involve substantial risk. You should not risk more than you are prepared to lose. Past performance is not an indication of future results. You are solely responsible for your own trading decisions, risk management, and for backtesting this or any other tool before using it in a live trading environment. This indicator is for educational purposes only.

Katz Exploding PowerBand FilterUnderstanding the Katz Exploding PowerBand Filter (EPBF) v2.4

1. Indicator Overview

The Katz Exploding PowerBand Filter (EPBF) is an advanced technical indicator designed to identify moments of expanding bullish or bearish momentum, often referred to as "power." It operates as a standalone oscillator in a separate pane below the main price chart.

Its primary goal is to measure underlying market strength by calculating custom "Bull" and "Bear" power components. These components are then filtered through a versatile moving average and a dual signal line system to generate clear entry and exit signals. This indicator is not a simple momentum oscillator; it uses a unique calculation based on exponential envelopes of both price and squared price to derive its values.

2. On-Chart Lines and Components

The indicator pane consists of five main lines:

Bullish Component (Thick Green/Blue/Yellow/Gray Line): This is the core of the indicator. It represents the calculated bullish "power" or momentum in the market.

Bright Green: Indicates a strong, active long signal condition.

Blue: Shows the bull component is above the MA filter, but the filter itself is still pointing down—a potential sign of a reversal or weakening downtrend.

Yellow: A warning sign that bullish power is weakening and has fallen below the primary signal lines.

Gray: Represents neutral or insignificant bullish power.

Bearish Component (Thick Red/Purple/Yellow/Gray Line): This line represents the calculated bearish "power" or downward momentum.

Bright Red: Indicates a strong, active short signal condition.

Purple: Shows the bear component is above the MA filter, but the filter itself is still pointing down—a sign of potential trend continuation.

Yellow: A warning sign that bearish power is weakening.

Gray: Represents neutral or insignificant bearish power.

MA Filter (Purple Line): This is the main filter, calculated using the moving average type and length you select in the settings (e.g., HullMA, EMA). The Bull and Bear components are compared against this line to determine the underlying trend bias.

Signal Line 1 (Orange Line): A fast Exponential Moving Average (EMA) of the stronger power component. It acts as the first level of dynamic support or resistance for the power lines.

Signal Line 2 (Lime/Gray Line): A slower EMA that acts as a confirmation filter.

Lime Green: The line turns lime when it is rising and the faster Signal Line 1 is above it, indicating a confirmed bullish trend in momentum.

Gray: Indicates a neutral or bearish momentum trend.

3. On-Chart Symbols and Their Meanings

Various characters are plotted at the bottom of the indicator pane to provide clear, actionable signals.

L (Pre-Long Signal): The first sign of a potential long entry. It appears when the Bullish Component rises and crosses above both signal lines for the first time.

S (Pre-Short Signal): The first sign of a potential short entry. It appears when the Bearish Component rises and crosses above both signal lines for the first time.

▲ (Post-Long Signal): A stronger confirmation for a long entry. It appears with the 'L' signal only if the momentum trend is also confirmed bullish (i.e., the slower Signal Line 2 is lime green).

▼ (Post-Short Signal): A stronger confirmation for a short entry. It appears with the 'S' signal only if the momentum trend is confirmed bullish.

Exit / Take-Profit Symbols:

These symbols appear when a power component crosses below a line, suggesting that momentum is fading and it may be time to take profit.

⚠️ (Exit Signal 1): The Bull/Bear component has crossed below the main MA Filter. This is the first and most sensitive take-profit signal.

☣️ (Exit Signal 2): The Bull/Bear component has crossed below the faster Signal Line 1. This is a moderate take-profit signal.

🚼 (Exit Signal 3): The Bull/Bear component has crossed below the slower Signal Line 2. This is the slowest take-profit signal, suggesting the trend is more definitively exhausted.

4. Trading Strategy and Rules

Long Entry Rules:

Initial Signal: Wait for an L to appear at the bottom of the indicator. This confirms that bullish power is expanding.

Confirmation (Recommended): For a higher-probability trade, wait for a green ▲ symbol to appear. This confirms the underlying momentum trend aligns with the signal.

Entry: Enter a long (buy) position on the opening of the next candle after the signal appears.

Short Entry Rules:

Initial Signal: Wait for an S to appear at the bottom of the indicator. This confirms that bearish power is expanding.

Confirmation (Recommended): For a higher-probability trade, wait for a maroon ▼ symbol to appear. This confirms the underlying momentum trend aligns with the signal.

Entry: Enter a short (sell) position on the opening of the next candle after the signal appears.

Take Profit (TP) Rules:

The indicator provides three levels of take-profit signals. You can choose to exit your entire position or scale out at each level.

For a long trade, exit when you see ⚠️, ☣️, or 🚼 appear below the Bullish Component.

For a short trade, exit when you see ⚠️, ☣️, or 🚼 appear below the Bearish Component.

Stop Loss (SL) Rules:

The indicator does not provide an explicit stop loss. You must use your own risk management rules. Common methods include:

Swing High/Low: For a long position, place your stop loss below the most recent significant swing low on the price chart. For a short position, place it above the most recent swing high.

ATR-Based: Use an Average True Range (ATR) indicator to set a volatility-based stop loss.

Fixed Percentage: Risk a fixed percentage (e.g., 1-2%) of your account on the trade.

5. Disclaimer

This indicator is a tool for technical analysis and should not be considered financial advice. All trading involves significant risk, and past performance is not indicative of future results. The signals generated by this indicator are probabilistic and can result in losing trades. Always use proper risk management, such as setting a stop loss, and never risk more than you are willing to lose. It is recommended to backtest this indicator and use it in conjunction with other forms of analysis before trading with real capital. The indicator should only be used for educational purposes.

Stochastic ExcessThe stochastic indicator is a technical analysis tool used in finance to assess the momentum of an asset’s price. It measures the current closing price relative to its price range over a specified period, usually a short one. This indicator helps identify overbought or oversold conditions, signaling when an asset might be about to reverse its trend.

SuperSmoother MA OscillatorSuperSmoother MA Oscillator - Ehlers-Inspired Lag-Minimized Signal Framework

Overview

The SuperSmoother MA Oscillator is a crossover and momentum detection framework built on the pioneering work of John F. Ehlers, who introduced digital signal processing (DSP) concepts into technical analysis. Traditional moving averages such as SMA and EMA are prone to two persistent flaws: excessive lag, which delays recognition of trend shifts, and high-frequency noise, which produces unreliable whipsaw signals. Ehlers’ SuperSmoother filter was designed to specifically address these flaws by creating a low-pass filter with minimal lag and superior noise suppression, inspired by engineering methods used in communications and radar systems.

This oscillator extends Ehlers’ foundation by combining the SuperSmoother filter with multi-length moving average oscillation, ATR-based normalization, and dynamic color coding. The result is a tool that helps traders identify market momentum, detect reliable crossovers earlier than conventional methods, and contextualize volatility and phase shifts without being distracted by transient price noise.

Unlike conventional oscillators, which either oversimplify price structure or overload the chart with reactive signals, the SuperSmoother MA Oscillator is designed to balance responsiveness and stability. By preprocessing price data with the SuperSmoother filter, traders gain a signal framework that is clean, robust, and adaptable across assets and timeframes.

Theoretical Foundation

Traditional MA oscillators such as MACD or dual-EMA systems react to raw or lightly smoothed price inputs. While effective in some conditions, these signals are often distorted by high-frequency oscillations inherent in market data, leading to false crossovers and poor timing. The SuperSmoother approach modifies this dynamic: by attenuating unwanted frequencies, it preserves structural price movements while eliminating meaningless noise.

This is particularly useful for traders who need to distinguish between genuine market cycles and random short-term price flickers. In practical terms, the oscillator helps identify:

Early trend continuations (when fast averages break cleanly above/below slower averages).

Preemptive breakout setups (when compressed oscillator ranges expand).

Exhaustion phases (when oscillator swings flatten despite continued price movement).

Its multi-purpose design allows traders to apply it flexibly across scalping, day trading, swing setups, and longer-term trend positioning, without needing separate tools for each.

The oscillator’s visual system - fast/slow lines, dynamic coloration, and zero-line crossovers - is structured to provide trend clarity without hiding nuance. Strong green/red momentum confirms directional conviction, while neutral gray phases emphasize uncertainty or low conviction. This ensures traders can quickly gauge the market state without losing access to subtle structural signals.

How It Works

The SuperSmoother MA Oscillator builds signals through a layered process:

SuperSmoother Filtering (Ehlers’ Method)

At its core lies Ehlers’ two-pole recursive filter, mathematically engineered to suppress high-frequency components while introducing minimal lag. Compared to traditional EMA smoothing, the SuperSmoother achieves better spectral separation - it allows meaningful cyclical market structures to pass through, while eliminating erratic spikes and aliasing. This makes it a superior preprocessing stage for oscillator inputs.

Fast and Slow Line Construction

Within the oscillator framework, the filtered price series is used to build two internal moving averages: a fast line (short-term momentum) and a slow line (longer-term directional bias). These are not plotted directly on the chart - instead, their relationship is transformed into the oscillator values you see.

The interaction between these two internal averages - crossovers, separation, and compression - forms the backbone of trend detection:

Uptrend Signal : Fast MA rises above the slow MA with expanding distance, generating a positive oscillator swing.

Downtrend Signal : Fast MA falls below the slow MA with widening divergence, producing a negative oscillator swing.

Neutral/Transition : Lines compress, flattening the oscillator near zero and often preceding volatility expansion.

This design ensures traders receive the information content of dual-MA crossovers while keeping the chart visually clean and focused on the oscillator’s dynamics.

ATR-Based Normalization

Markets vary in volatility. To ensure the oscillator behaves consistently across assets, ATR (Average True Range) normalization scales outputs relative to prevailing volatility conditions. This prevents the oscillator from appearing overly sensitive in calm markets or too flat during high-volatility regimes.

Dynamic Color Coding

Color transitions reflect underlying market states:

Strong Green : Bullish alignment, momentum expanding.

Strong Red : Bearish alignment, momentum expanding.

These visual cues allow traders to quickly gauge trend direction and strength at a glance, with expanding colors indicating increasing conviction in the underlying momentum.

Interpretation

The oscillator offers a multi-dimensional view of price dynamics:

Trend Analysis : Fast/slow line alignment and zero-line interactions reveal trend direction and strength. Expansions indicate momentum building; contractions flag weakening conditions or potential reversals.

Momentum & Volatility : Rapid divergence between lines reflects increasing momentum. Compression highlights periods of reduced volatility and possible upcoming expansion.

Cycle Awareness : Because of Ehlers’ DSP foundation, the oscillator captures market cycles more cleanly than conventional MA systems, allowing traders to anticipate turning points before raw price action confirms them.

Divergence Detection : When oscillator momentum fades while price continues in the same direction, it signals exhaustion - a cue to tighten stops or anticipate reversals.

By focusing on filtered, volatility-adjusted signals, traders avoid overreacting to noise while gaining early access to structural changes in momentum.

Strategy Integration

The SuperSmoother MA Oscillator adapts across multiple trading approaches:

Trend Following

Enter when fast/slow alignment is strong and expanding:

A fast line crossing above the slow line with expanding green signals confirms bullish continuation.

Use ATR-normalized expansion to filter entries in line with prevailing volatility.

Breakout Trading

Periods of compression often precede breakouts:

A breakout occurs when fast lines diverge decisively from slow lines with renewed green/red strength.

Exhaustion and Reversals

Oscillator divergence signals weakening trends:

Flattening momentum while price continues trending may indicate overextension.

Traders can exit or hedge positions in anticipation of corrective phases.

Multi-Timeframe Confluence

Apply the oscillator on higher timeframes to confirm the directional bias.

Use lower timeframes for refined entries during compression → expansion transitions.

Technical Implementation Details

SuperSmoother Algorithm (Ehlers) : Recursive two-pole filter minimizes lag while removing high-frequency noise.

Oscillator Framework : Fast/slow MAs derived from filtered prices.

ATR Normalization : Ensures consistent amplitude across market regimes.

Dynamic Color Engine : Aligns visual cues with structural states (expansion and contraction).

Multi-Factor Analysis : Combines crossover logic, volatility context, and cycle detection for robust outputs.

This layered approach ensures the oscillator is highly responsive without overloading charts with noise.

Optimal Application Parameters

Asset-Specific Guidance:

Forex : Normalize with moderate ATR scaling; focus on slow-line confirmation.

Equities : Balance responsiveness with smoothing; useful for capturing sector rotations.

Cryptocurrency : Higher ATR multipliers recommended due to volatility.

Futures/Indices : Lower frequency settings highlight structural trends.

Timeframe Optimization:

Scalping (1-5min) : Higher sensitivity, prioritize fast-line signals.

Intraday (15m-1h) : Balance between fast/slow expansions.

Swing (4h-Daily) : Focus on slow-line momentum with fast-line timing.

Position (Daily-Weekly) : Slow lines dominate; fast lines highlight cycle shifts.

Performance Characteristics

High Effectiveness:

Trending environments with moderate-to-high volatility.

Assets with steady liquidity and clear cyclical structures.

Reduced Effectiveness:

Flat/choppy conditions with little directional bias.

Ultra-short timeframes (<1m), where noise dominates.

Integration Guidelines

Confluence : Combine with liquidity zones, order blocks, and volume-based indicators for confirmation.

Risk Management : Place stops beyond slow-line thresholds or ATR-defined zones.

Dynamic Trade Management : Use expansions/contractions to scale position sizes or tighten stops.

Multi-Timeframe Confirmation : Filter lower-timeframe entries with higher-timeframe momentum states.

Disclaimer

The SuperSmoother MA Oscillator is an advanced trend and momentum analysis tool, not a guaranteed profit system. Its effectiveness depends on proper parameter settings per asset and disciplined risk management. Traders should use it as part of a broader technical framework and not in isolation.