EMA Cross + RSI + ADX - Autotrade Strategy V2Overview

A versatile trend-following strategy combining EMA 9/21 crossovers with RSI momentum filtering and optional ADX trend strength confirmation. Designed for both cryptocurrency and traditional futures/options markets with built-in stop loss management and automated position reversals.

Key Features

Multi-Market Compatibility: Works on both crypto futures (Bitcoin, Ethereum) and traditional markets (NIFTY, Bank NIFTY, S&P 500 futures, equity options)

Triple Confirmation System: EMA crossover + RSI filter + ADX strength (optional)

Automated Risk Management: 2% stop loss with wick-touch detection

Position Auto-Reversal: Opposite signals automatically close and reverse positions

Webhook Ready: Six distinct alert messages for automation (Entry Buy/Sell, Close Long/Short, SL Hit Long/Short)

Performance Metrics

NIFTY Futures (15min): 50%+ win rate with ADX filter OFF

Crypto Markets: Requires extensive backtesting before live deployment

Optimal Timeframes: 15-minute to 1-hour charts (patience required for higher timeframes)

Strategy Logic

Entry Signals:

LONG: EMA 9 crosses above EMA 21 + RSI > 55 + ADX > 20 (if enabled)

SHORT: EMA 9 crosses below EMA 21 + RSI < 45 + ADX > 20 (if enabled)

Exit Signals:

Opposite EMA crossover (auto-closes current position)

Stop loss hit at 2% from entry price (tracks candle wicks)

Technical Indicators:

Fast EMA: 9-period (short-term trend)

Slow EMA: 21-period (primary trend)

RSI: 14-period with 55/45 thresholds (momentum confirmation)

ADX: 14-period with 20 threshold (trend strength filter - optional)

Market-Specific Settings

Traditional Markets (NIFTY, Bank NIFTY, S&P Futures, Options)

Recommended Settings:

ADX Filter: Turn OFF (less choppy, cleaner trends)

Timeframe: 15-minute chart

Win Rate: 50%+ on NIFTY Futures

Why No ADX: Traditional markets have more institutional participation and smoother price action, making ADX unnecessary

Cryptocurrency Markets (BTC, ETH, Altcoins)

Recommended Settings:

ADX Filter: Turn ON (ADX > 20)

Timeframe: 15-minute to 1-hour

Extensive backtesting required before live trading

Why ADX: Crypto markets are highly volatile and prone to false breakouts; ADX filters low-quality chop

Best Practices

✅ Backtest thoroughly on your specific instrument and timeframe

✅ Use larger timeframes (1H, 4H) for higher quality signals and better risk/reward

✅ Adjust RSI thresholds based on market volatility (try 52/48 for more signals, 60/40 for fewer but stronger)

✅ Monitor ADX effectiveness - disable for traditional markets, enable for crypto

✅ Proper position sizing - adjust default_qty_value based on your capital and instrument price

✅ Paper trade first - test for 2-4 weeks before risking real capital

Risk Management

Fixed 2% stop loss per trade (adjustable)

Stop loss tracks candle wicks for accurate execution

Positions auto-reverse on opposite signals (no manual intervention needed)

0.075% commission built into backtest (adjust for your broker)

Customization Options

All parameters are adjustable via inputs:

EMA periods (default: 9/21)

RSI length and thresholds (default: 14-period, 55/45 levels)

ADX length and threshold (default: 14-period, 20 threshold)

Stop loss percentage (default: 2%)

Webhook Automation

This strategy includes six distinct alert messages for automated trading:

"Entry Buy" - Long position opened

"Entry Sell" - Short position opened

"Close Long" - Long position closed on opposite crossover

"Close Short" - Short position closed on opposite crossover

"SL Hit Long" - Long stop loss triggered

"SL Hit Short" - Short stop loss triggered

Compatible with Delta Exchange, Binance Futures, 3Commas, Alertatron, and other webhook platforms.

Important Notes

⚠️ Crypto markets require extensive backtesting - volatility patterns differ significantly from traditional markets

⚠️ Higher timeframes = better results - 15min works but 1H/4H provide cleaner signals

⚠️ ADX toggle is critical - OFF for traditional markets, ON for crypto

⚠️ Not financial advice - always conduct your own research and use proper risk management

⚠️ Past performance ≠ future results - backtest results may not reflect live trading conditions

Disclaimer

This strategy is for educational and informational purposes only. Trading futures and options involves substantial risk of loss. Always backtest thoroughly, start with paper trading, and never risk more than you can afford to lose. The author assumes no responsibility for any trading losses incurred using this strategy.

Market

Full Swing Gold Vwap Macd SMO StrategyThis is a full strategy designed for gold market using 12h timeframe chart.

Its components are:

VWAP monthly

SMO oscillator

MACD histogram

Rules for entry:

For long: when enter when close of the candle is above vwap monthly, current histogram is higher than the previous one and SMO oscillator is above 0

For long: when enter when close of the candle is below vwap monthly, current histogram is lower than the previous one and SMO oscillator is below 0

Rules for exit:

We exit the trade if we get a reverse condition.

We also exit the trade based on a risk management system, both for SL and TP using % movements.

If you have any questions let me know !

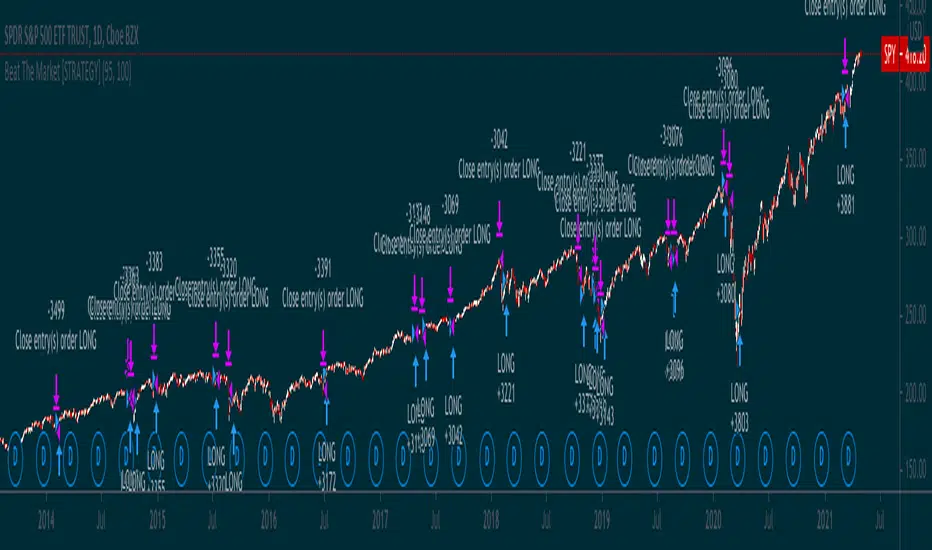

Simple way to BEAT the market [STRATEGY]This script has been created to demonstrate the effectiveness of using market regime filters in your trading strategy, and how they can improve your returns and lower your drawdowns

This strategy adds a simple filter (A historical volatility percentile filter, an implementation of which can be found on my trading profile) to a traditional buy and hold strategy of the index SPY.

Note, There are other filters that could also be added including a long-term moving average/percentile rank filter/ADX filter etc, to improve the returns further.

The filter closes our long position during periods of volatility that exceed the 95th percentile (or in the top 5% of volatile days) and buys back when the volatility is below 95% rank of the past 100 days

Have included the backtest results since 1993 which is 28 years of data at the time of writing. Comparison of traditional buy and hold with this modified strategy can be found below:

Traditional buy and hold:

Return per year: 7.95 % (ex Dividends)

Total return: 851.1 %

Max drawdown: 50.79 %

'Modified' buy and hold (this script):

Return per year: 9.92 % (ex Dividends)

Total return: 1412.2 %

Max drawdown: 31.57 %

Feel free to use some of the market filters in my trading profile to improve and refine your strategies further, or make a copy and play around with the code yourself. This is just a simple example for demo purposes.

Automated - Fibs with Market ordersThis script was recently shared for limit only orders here:

This version does not worry about keeping orders in the books and moving them around, instead it will simply market in and out.

I am sharing this to reveal the difference between the 2 setups.