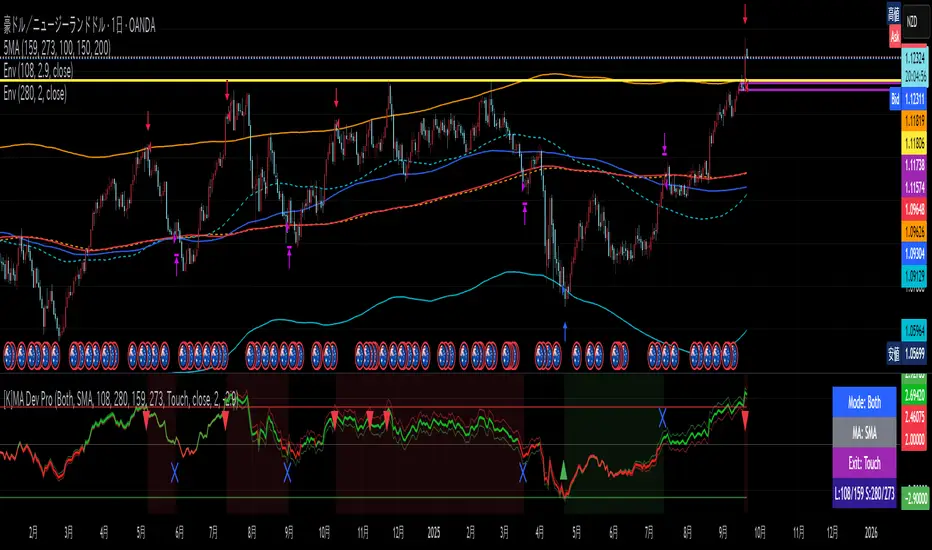

[K] MA Deviation Strategy Pro**This strategy is designed to demonstrate strength in sideways markets (range-bound), using envelope to determine entry and SMA to determine exit.**

**Key Points:**

• **Flexible optimization**: The strategy can be optimized by operating Long (buy) and Short (sell) positions with separate and independent settings.

• **Important risk management**: Since the maximum drawdown (maximum loss) can be significant, it is recommended to operate with low leverage.

**Strategy Summary:**

- **Entry signal**: Determined by the envelope indicator

- **Exit signal**: Determined by SMA (Simple Moving Average)

- **Ideal environment**: Range-bound (sideways) markets

- **Configuration**: Long and Short with independent parameters

- **Recommendation**: Use low leverage due to high drawdown risk

This is a strategy suitable for markets that oscillate within a defined price range, without a clear upward or downward trend.

Moving Averages

Extremum Range MA Crossover Strategy1. Principle of Work & Strategy Logic ⚙️📈

Main idea: The strategy tries to catch the moment of a breakout from a price consolidation range (flat) and the start of a new trend. It combines two key elements:

Moving Average (MA) 📉: Acts as a dynamic support/resistance level and trend filter.

Range Extremes (Range High/Low) 🔺🔻: Define the borders of the recent price channel or consolidation.

The strategy does not attempt to catch absolute tops and bottoms. Instead, it enters an already formed move after the breakout, expecting continuation.

Type: Trend-following, momentum-based.

Timeframes: Works on different TFs (H1, H4, D), but best suited for H4 and higher, where breakouts are more meaningful.

2. Justification of Indicators & Settings ⚙️

A. Moving Average (MA) 📊

Why used: Core of the strategy. It smooths price fluctuations and helps define the trend. The price (via extremes) must cross the MA → signals a potential trend shift or strengthening.

Parameters:

maLength = 20: Default length (≈ one trading month, 20-21 days). Good balance between sensitivity & smoothing.

Lower TF → reduce (10–14).

Higher TF → increase (50).

maSource: Defines price source (default = Close). Alternatives (HL2, HLC3) → smoother, less noisy MA.

maType: Default = EMA (Exponential MA).

Why EMA? Faster reaction to recent price changes vs SMA → useful for breakout strategies.

Other options:

SMA 🟦 – classic, slowest.

WMA 🟨 – weights recent data stronger.

HMA 🟩 – near-zero lag, but “nervous,” more false signals.

DEMA/TEMA 🟧 – even faster & more sensitive than EMA.

VWMA 🔊 – volume-weighted.

ZLEMA ⏱ – reduced lag.

👉 Choice = tradeoff between speed of reaction & false signals.

B. Range Extremes (Previous High/Low) 📏

Why used: Define borders of recent trading range.

prevHigh = local resistance.

prevLow = local support.

Break of these levels on close = trigger.

Parameters:

lookbackPeriod = 5: Searches for highest high / lowest low of last 5 candles. Very recent range.

Higher value (10–20) → wider, stronger ranges but rarer signals.

3. Entry & Exit Rules 🎯

Long signals (BUY) 🟢📈

Condition (longCondition): Previous Low crosses MA from below upwards.

→ Price bounced from the bottom & strong enough to push range border above MA.

Execution: Auto-close short (if any) → open long.

Short signals (SELL) 🔴📉

Condition (shortCondition): Previous High crosses MA from above downwards.

→ Price rejected from the top, upper border failed above MA.

Execution: Auto-close long (if any) → open short.

Exit conditions 🚪

Exit Long (exitLongCondition): Close below prevLow.

→ Uptrend likely ended, range shifts down.

Exit Short (exitShortCondition): Close above prevHigh.

→ Downtrend likely ended, range shifts up.

⚠️ Important: Exit = only on candle close beyond extremes (not just wick).

4. Trading Settings ⚒️

overlay = true → indicators shown on chart.

initial_capital = 10000 💵.

default_qty_type = strategy.cash, default_qty_value = 100 → trades fixed $100 per order (not lots). Can switch to % of equity.

commission_type = strategy.commission.percent, commission_value = 0.1 → default broker fee = 0.1%. Adjust for your broker!

slippage = 3 → slippage = 3 ticks. Adjust to asset liquidity.

currency = USD.

margin_long = 100, margin_short = 100 → no leverage (100% margin).

5. Visualization on Chart 📊

The strategy draws 3 lines:

🔵 MA line (thickness 2).

🔴 Previous High (last N candles).

🟢 Previous Low (last N candles).

Also: entry/exit arrows & equity curve shown in backtest.

Disclaimer ⚠️📌

Risk Warning: This description & code are for educational purposes only. Not financial advice. Trading (Forex, Stocks, Crypto) carries high risk and may lead to full capital loss. You trade at your own risk.

Testing: Always backtest & demo test first. Past results ≠ future profits.

Responsibility: Author of this strategy & description is not responsible for your trading decisions or losses.

2 of 3 Confluence StrategyA strategy created for swing and positional trading on stocks and index. Best to use on daily or minimum hourly time frame. It will also work in smaller time frames but there will be some noise.

Liquidation Strategy📈 It enters a long trade when long liquidation spikes above a set threshold.

📉 It enters a short trade when short liquidation drops below the negative threshold.

🧮 It optionally filters entries using an EMA multiplier.

🔁 It exits long when RSI crosses below its smoothed version.

🔄 It exits short when RSI crosses above its smoothed version.

🔗 It requires linking to the Liquidations indicator on Bybit or OKX charts.

Trend Strength Index Long Strategy📈 Trend Strength Index Long Strategy

This strategy combines the Trend Strength Index (TSI) with a Volume-Weighted Moving Average (VWMA) to identify high-probability long entries based on trend momentum and price confirmation.

📊 TSI Calculation : Measures correlation between price and time (bar index) over a user-defined period. Strong TSI values indicate trend momentum.

📏 VWMA Filter : Confirms bullish bias when price is above the VWMA.

🚀 Entry Condition : Long position is triggered when TSI crosses above -0.65 and price is above VWMA.

🔒 Exit Condition : Position is closed when TSI crosses above 0.65.

🎨 Visuals : Gradient fills highlight bullish and bearish zones. VWMA is plotted for trend context.

🧮 TSI Length: Adjustable (default 14)

📐 VWMA Length: Adjustable (default 55)

💸 Commission: 0.1% per trade

📊 Position Size: 75% of equity

⚙️ Slippage: 10 ticks

✅ Best used in trending markets with steady momentum.

⚠️ Avoid in choppy or range-bound conditions.

The Real Deal v3.0The Real Deal v3.0 blends multiple layers of market structure into a single adaptive framework. Using a Gaussian price channel as its backbone, it adds dynamic confirmation from EMA filters, cloud-style trend detection, and a proprietary “Secret Sauce” momentum engine. Flexible trade direction, optional TP/SL management, and configurable entry/exit triggers allow the strategy to adapt to changing conditions. The result is a system designed to identify high-probability trades while filtering out the noise—simple on the surface, but with deeper mechanics under the hood.

回撤再入场引擎This is a long-only, counter-trend strategy that aims to buy dips in a medium-term downtrend. The entry logic is based on a confluence of four filters:

1. **Trend Filter:** The price must be trading below the 60-period Simple Moving Average (SMA).

2. **Oversold Condition:** The WaveTrend Oscillator must first dip below -60 and then recover above -55.

3. **Momentum Confirmation:** The MACD must show sustained bullish momentum for at least 2 bars.

4. **Re-entry Filter:** A new trade is only allowed if the price is at least a certain percentage lower than the last trade's exit price.

The exit is based on a fixed Take Profit target. This version does not include a stop-loss.

Penguin Volatility State StrategyThe Penguin Volatility State Strategy is a comprehensive technical analysis framework designed to identify the underlying "state" or "regime" of the market. Instead of just providing simple buy or sell signals, its primary goal is to classify the market into one of four distinct states by combining trend, momentum, and volatility analysis.

The core idea is to trade only when these three elements align, focusing on periods of volatility expansion (a "squeeze breakout") that occur in the direction of a confirmed trend and are supported by strong momentum.

Key Components

The strategy is built upon two main engines

The Volatility Engine (Bollinger Bands vs. Keltner Channels)

This engine detects periods of rapidly increasing volatility. It measures the percentage difference (diff) between the upper bands of Bollinger Bands (which are based on standard deviation) and Keltner Channels (based on Average True Range). During a volatility "squeeze," both bands are close. When price breaks out, the Bollinger Band expands much faster than the Keltner Channel, causing the diff value to become positive. A positive diff signals a volatility breakout, which is the moment the strategy becomes active.

The Trend & Momentum Engine (Multi-EMA System)

This engine determines the market's direction and strength. It uses:

A Fast EMA (e.g., 12-period) and a Slow EMA (e.g., 26-period): The crossover of these two moving averages defines the primary, underlying trend (similar to a MACD).

An Ultra-Fast EMA (e.g., 2-period of ohlc4): This is used to measure the immediate, short-term momentum of the price.

The Four Market States

By combining the Trend and Momentum engines, the strategy categorizes the market into four visually distinct states, represented by the chart's background color. This is the most crucial aspect of the system.

💚 Green State: Strong Bullish

The primary trend is UP (Fast EMA > Slow EMA) AND the immediate momentum is STRONG (Price > Fast EMA).

Interpretation: This represents a healthy, robust uptrend where both the underlying trend and short-term price action are aligned. It is considered the safest condition for taking long positions.

❤️ Red State: Strong Bearish

Condition: The primary trend is DOWN (Fast EMA < Slow EMA) AND the immediate momentum is WEAK (Price < Fast EMA).

Interpretation: This represents a strong, confirmed downtrend. It is considered the safest condition for taking short positions.

💛 Yellow State: Weakening Bullish / Pullback

Condition: The primary trend is UP (Fast EMA > Slow EMA) BUT the immediate momentum is WEAK (Price < Fast EMA).

Interpretation: This is a critical warning signal for bulls. While the larger trend is still up, the short-term price action is showing weakness. This could be a minor pullback, a period of consolidation, or the very beginning of a trend reversal. Caution is advised.

💙 Blue State: Weakening Bearish / Relief Rally

Condition: The primary trend is DOWN (Fast EMA < Slow EMA) BUT the immediate momentum is STRONG (Price > Fast EMA).

Interpretation: This signals that a downtrend is losing steam. It often represents a short-covering rally (a "bear market rally") or the first potential sign of a market bottom. Bears should be cautious and consider taking profits.

How the Strategy Functions

The strategy uses these four states as its foundation for making trading decisions. The entry and exit arrows (Long, Short, Close) are generated based on a set of rules that can be customized by the user. For instance, a trader can configure the strategy to

Only take long trades during the Green State.

Require a confirmed volatility breakout (diff > 0) before entering a trade.

Use the "RSI on Diff" indicator to ensure that the breakout is supported by accelerating momentum.

Summary

In essence, the Penguin Volatility State Strategy provides a powerful "dashboard" for viewing the market. It moves beyond simple indicators to offer a contextual understanding of price action. By waiting for the alignment of Trend (the State), Volatility (the Breakout), and Momentum (the Acceleration), it helps traders to identify higher-probability setups and, just as importantly, to know when it is better to stay out of the market.

License / disclaimer

© waranyu.trkm — MIT License. Educational use only; not financial advice.

VWAP Trend Strategy (Intraday) [KedarArc Quant]Description:

An intraday strategy that anchors to VWAP and only trades when a local EMA trend gate and a volume participation gate are both open. It offers two entry templates—Cross and Cross-and-Retest—with an optional Momentum Exception for impulsive moves. Exits combine a TrendBreak (structure flips) with an ATR emergency stop (risk cap).

Updates will be published under this script.

Why this merits a new script

This is not a simple “VWAP + EMA + ATR” overlay. The components are sequenced as gates and branches that *change the trade set* in ways a visual mashup cannot:

1. Trend Gate first (EMA fast vs. slow on the entry timeframe)

Counter-trend VWAP crosses are suppressed. Many VWAP scripts fire on every cross; here, no entry logic even evaluates unless the trend gate is open.

2. Participation Gate second (Volume SMA × multiplier)

This gate filters thin liquidity moves around VWAP. Without it, the same visuals would produce materially more false triggers.

3. Branching entries with structure awareness

* Cross: Immediate VWAP cross in the trend direction.

* Cross-and-Retest: Requires a revisit to VWAP vicinity within a lookback window (recent low near VWAP for longs; recent high for shorts). This explicitly removes first-touch fakeouts that a plain cross takes.

* Momentum Exception (optional): A quantified body% + volume condition can bypass the retest when flow is impulsive—intentional risk-timing, not “just another indicator.”

4. Dual exits that reference both anchor and structure

* TrendBreak: Close only when price loses VWAP and EMA alignment flips.

* ATR stop: Placed at entry to cap tail risk.

These exits complement the entry structure rather than being generic stop/target add-ons.

What it does

* Trades the session’s fair value anchor (VWAP), but only with local-trend agreement (EMA fast vs. slow) and sufficient participation (volume filter).

* Lets you pick Cross or Cross-and-Retest entries; optionally allow a fast Momentum Exception when candles expand with volume.

* Manages positions with a structure exit (TrendBreak) and an emergency ATR stop from entry.

How it works (concepts & calculations)

* VWAP (session anchor):

Standard VWAP of the active session; entries reference the cross and the retest proximity to VWAP.

* Trend gate:

Long context only if `EMA(fast) > EMA(slow)`; short only if `EMA(fast) < EMA(slow)`.

A *gate*, not a trigger—entries aren’t considered unless this is true.

* Participation (volume) gate:

Require `volume > SMA(volume, volLen) × volMult`.

Screens out low-participation wiggles around VWAP.

Entries:

* Cross: Price crosses VWAP in the trend direction while volume gate is open.

* Cross-and-Retest: After crossing, price revisits VWAP vicinity within `lookback` (recent *low near VWAP* for longs; recent *high near VWAP* for shorts).

* Momentum Exception (optional): If body% (|close−open| / range) and volume exceed thresholds, enter without waiting for the retest.

Exits:

* TrendBreak (structure):

* Longs close when `price < VWAP` and `EMA(fast) < EMA(slow)` (mirror for shorts).

* ATR stop (risk):

* From entry: `stop = entry ± ATR(atrLen) × atrMult`.

How to use it ?

1. Select market & timeframe: Intraday on liquid symbols (equities, futures, crypto).

2. Pick entry mode:

* Start with Cross-and-Retest for fewer, more selective signals.

* Enable Momentum Exception if strong moves leave without retesting.

3. Tune guards:

* Raise `volMult` to ignore thin periods; lower it for more activity.

* Adjust `lookback` if retests come late/early on your symbol.

4. Risk:

* `atrLen` and `atrMult` set the emergency stop distance.

5. Read results per session: Optional panel (if enabled) summarizes Net-R, Win%, and PF for today’s session to evaluate

behavior regime by regime.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Liquidation Strategy💣 Liquidation Strategy (High-Level Overview + Usage)

This strategy is built to trade extreme liquidation events on crypto exchanges like Bybit or OKX, using TradingView’s Liquidations indicator as input.

🔧 Core Logic

Long entries: Triggered when long liquidation values spike above a set threshold.

Short entries: Triggered when short liquidation values drop below a negative threshold.

Optional EMA filter ensures liquidation values are significantly above/below their moving average.

RSI crossover logic is used to exit trades.

🛠️ Usage Instructions

Add the Liquidations Indicator: Go to TradingView → Indicators → Search for “Liquidations” under the Financials section.

Select the Correct Chart: Use a chart from Bybit or OKX, as these exchanges provide liquidation data.

Link the Data Sources: In the strategy settings, set: Long Liquidation Data to the long liquidation series from the indicator. Short Liquidation Data to the short liquidation series.

Overlay the Strategy: You can overlay this strategy directly on the Liquidations indicator for better visual alignment.

RSI Momentum Trend MM with Risk Per Trade [MTF]This is a comprehensive and highly customizable trend-following strategy based on RSI momentum. The core logic identifies strong directional moves when the RSI crosses user-defined thresholds, combined with an EMA trend confirmation. It is designed for traders who want granular control over their strategy's parameters, from signal generation to risk management and exit logic.

This script evolves a simple concept into a powerful backtesting tool, allowing you to test various money management and trade management theories across different timeframes.

Key Features

- RSI Momentum Signals: Uses RSI crosses above a "Positive" level or below a "Negative" level to generate trend signals. An EMA filter ensures entries align with the immediate trend.

- Multi-Timeframe (MTF) Analysis: The core RSI and EMA signals can be calculated on a higher timeframe (e.g., using 4H signals to trade on a 1H chart) to align trades with the larger trend. This feature helps to reduce noise and improve signal quality.

Advanced Money Management

- Risk per Trade %: Calculate position size based on a fixed percentage of equity you want to risk per trade.

- Full Equity: A more aggressive option to open each position with 100% of the available strategy equity.

Flexible Exit Logic: Choose from three distinct exit strategies to match your trading style

- Percentage (%) Based: Set a fixed Stop Loss and Take Profit as a percentage of the entry price.

- ATR Multiplier: Base your Stop Loss and Take Profit on the Average True Range (ATR), making your exits adaptive to market volatility.

- Trend Reversal: A true trend-following mode. A long position is held until an opposite "Negative" signal appears, and a short position is held until a "Positive" signal appears. This allows you to "let your winners run."

Backtest Date Range Filter: Easily configure a start and end date to backtest the strategy's performance during specific market periods (e.g., bull markets, bear markets, or high-volatility periods).

How to Use

RSI Settings

- Higher Timeframe: Set the timeframe for signal calculation. This must be higher than your chart's timeframe.

- RSI Length, Positive above, Negative below: Configure the core parameters for the RSI signals.

Money Management

Position Sizing Mode

- Choose "Risk per Trade" to use the Risk per Trade (%) input for precise risk control.

- Choose "Full Equity" to use 100% of your capital for each trade.

- Risk per Trade (%): Define the percentage of your equity to risk on a single trade (only works with the corresponding sizing mode).

SL/TP Calculation Mode

Select your preferred exit method from the dropdown. The strategy will automatically use the relevant inputs (e.g., % values, ATR Multiplier values, or the trend reversal logic).

Backtest Period Settings

Use the Start Date and End Date inputs to isolate a specific period for your backtest analysis.

License & Disclaimer

© waranyu.trkm — MIT License.

This script is for educational purposes only and should not be considered financial advice. Trading involves significant risk, and past performance is not indicative of future results. Always conduct your own research and risk assessment before making any trading decisions.

W Bottom Reversal Strategy W Bottom Reversal Strategy (15m-close entries; intrabar TP; daily MACD exit; JSON alerts v49.3-expire2)

Overview

A precision reversal strategy designed for 15-minute charts on liquid symbols. It detects a capitulation-and-stabilization “W” base using 1-hour (1H) context, confirms momentum improvement, then enters only on bar close to avoid early/“ghost” signals. Exits combine a fast intrabar take-profit (~2.7%) with a daily MACD risk-off exit that closes positions when higher-timeframe momentum turns against the setup.

How it works (high-level, matching code)

1H volatility + oversold gate (arming)

Compute 1H Bollinger-style bands (basis = SMA(close, bbLength=20), stdev multiplier bbMult=2.0).

Arm the setup when a 1H bar closes with price < 1H lower band and 1H RSI( rsiLength=14 ) < rsiThreshold (default 20.0).

1H momentum flip → pending entry

When a new 1H bar closes and 1H MACD line (EMA12−EMA26) crosses above 0 while armed and flat, set an entryPending flag.

This does not enter yet—it prepares a confirmed, bar-close entry on the lower timeframe.

Bar-close execution on the chart timeframe (15m)

On the next 15m bar close (or within N bars, see below) and still flat, fire the entry using a limit order at close × (1 − 0.00001) (≈ 0.001% below close) to reduce slippage and maintain chart/alert alignment.

Anti-late filter (no stale triggers)

If the pending entry doesn’t trigger within N chart bars (input: “Pending entry valid for N chart bars”, default 1, range 1–8), it expires and the arm state resets. This prevents late fills long after the 1H confirmation.

Exit logic

Primary: Standing intrabar take-profit at +2.7% from the average entry price (managed via strategy.exit limit).

Risk-off: On daily bar close, if Daily MACD line (EMA12−EMA26) crosses under 0, close the position (flat on daily momentum flip).

Default Properties (used for this publication)

Timeframe: 15m (with 1H and Daily higher-timeframe confirmations via request.security)

Initial capital: $10,000

Position sizing: Percent of equity = 10% per trade (enters only when flat; no stacking while in a position)

Commission: 0.05% per side

Slippage: Recommend 1 tick in Strategy Properties for realistic fills

Inputs exposed:

BB Length: 20 • BB Multiplier: 2.0

RSI Length: 14 • RSI Threshold: 20.0

MACD: Short 12, Long 26, Signal 9 (signal kept for compatibility; logic uses MACD line vs 0)

Pending entry valid for N chart bars: default 1 (1–8)

Execution behavior (per code):

calc_on_every_tick = false (evaluates on bar close)

process_orders_on_close = true (orders placed at bar close)

Limit entry at close −0.001%

Intrabar TP (2.7%)

Daily risk-off exit on MACD<0 at daily bar close

Alerts (exact behavior in code)

Uses alert() function calls with standardized JSON.

Set your alert to “Only alert() function calls” and “Once per bar close.”

Two events are emitted:

LONG_CONFIRMED on entry fire (15m bar close)

EXIT_CONFIRMED_DAILY_MACD on daily MACD<0 (daily bar close)

JSON fields include: event, version ("v49.3-expire2"), symbol, interval, price, and time.

How to use

Apply on liquid tickers (tight spreads, healthy volume).

Keep defaults initially; run across a broad, liquid watchlist to gather a proper sample.

For automation, route bar-close alerts to your executor; confirm broker lot/route settings and that limit orders at close −0.001% are acceptable.

Expect fewer signals in powerful trends; the daily risk-off helps cut failed bases.

Methodology & expectations (results transparency)

Evaluate on a dataset yielding 100+ trades before drawing conclusions.

Keep commission & slippage enabled (see defaults).

Risk sizing: With 10% of equity per trade and flat-to-flat entries, exposure aligns with typical 5–10% guidance.

No performance guarantees—outcomes depend on symbol selection, volatility regime, news, and execution quality.

Originality & value (vendor justification)

While it uses familiar building blocks (BB/RSI/MACD), the edge comes from the 1H volatility + oversold arming, 1H momentum flip, strict 15m bar-close limit execution, and the N-bar pending expiry that prevents stale triggers—paired with a dual-exit design (intrabar TP + daily risk-off). The focus is on reducing premature fills, keeping alerts 1:1 with chart marks, and capturing the first impulse out of a W-base.

Disclaimers

For educational purposes only; not financial advice. Paper-test first. Verify alerts, fills, and symbol liquidity with your broker before live use.

Changelog: v49.3-expire2 — Bar-close limit entries; anti-late pending window; standardized JSON alerts; intrabar 2.7% TP; daily MACD risk-off exit.

7Lots v27Lots strategy

The strategy is a counter-trend with a return to the moving average. Based on the DCA strategy, but greatly simplified to 7 lots (limit orders) and using the default martingale x2.5

Strategy description

Two moving averages are used. The first MA can be used as a filter for opening a position and also closing if the second MA is disabled. If both are enabled, then the position is closed by the second MA, and the first is used as a filter. There is also a separate take profit and if the price does not reach it, the position will be closed when returning to the MA, which will act as a stop loss, but the risk of liquidation is still present since the strategy does not have a regular classic stop loss.

Main parameters

TP & SL - selection of closing a position only by MA or take profit + MA. If only MA is selected, the strategy ignores the take profit value and always closes the position by MA.

MA settings

MA length from 1 to 200

Sliding type ALMA, SMA, EMA, VWMA, WMA, RMA

MA data - Open, High, Low, Close, HL2, HL3, OHLC4, OC2

MA shift in %. The MA shift is set in % above or below the current prices. For the First MA, this function allows you to use it as a filter for opening a position. For example, if you specify a shift much lower, for example -1% or -2%, then there will be less noise for opening a position, but this affects the number of transactions.

DCA group settings

Take profit %. Set the take profit as usual, but if the price does not reach the take profit, then the closing will occur by MA when the price returns to its values.

Take profit from. There is a choice of take profit from the average position, or by closing the previous bar. The latter increases the profit factor, but also increases the risk of liquidation if the strategy is used on perpetual contracts or futures.

Position Entry % - specifies the condition for opening a position. 0% - opening will occur immediately. 2% - opening will occur when the price falls 2% below the bar closing if the Long mode is set. If Short, then vice versa.

Grid Scale - classic progressive grid step

Next comes the setup of lots as a percentage of the deposit. Simply specify how many percent of each lot will be used from the total deposit. By default, a percentage for each lot is already allocated according to Martingale with a multiplier of x2.5, but you can calculate your own. You can specify 0, then the lot will be disabled.

Leverage. By default, 1.

Extra lot. This is the 7th lot that I decided to allocate separately from the main grid, since it is not always really needed. And it is calculated from the last lot of the grid. You can set it to how much lower percentage of the last lot to set it for and also what percentage of the deposit it will use. If you trade futures, then this lot, as an auxiliary one, can greatly average the position in case of strong volatility in the market.

Next, you can specify the start and end dates of transactions.

The table displays the total percentage of the deposit involved in trading at the moment. By default, all lots and leverage are set to 100% deposit load. The table also shows the number of transactions of the last 5-6 lots and extra, so that you can understand how many of them there were throughout the history of trading and possibly draw some conclusions for yourself. Especially useful for extra lots. Max Historical Drawdown (%) shows the historical price drop at the moment from the average open position. This will make it possible to analyze what leverage this strategy could withstand over the entire trading history. The date of this drop is also indicated.

For novice traders, it is recommended to use only on spot without the risk of liquidation. It is also best to use large time frames to see the whole picture, but you can also use a minute chart, there are no restrictions, everything is in your hands.

Tips. If you use minute charts, it is better to greatly increase the length of the MA from 20 and above. Hourly charts from 1-7. It is better to set up on spot and if you need futures, then use the same settings from spot, but with correction for futures. This strategy does not work well in Short, but shows excellent results for Long even when the market falls. When selecting settings, take into account sharp market fluctuations, Max Historical Drawdown (%) will show you this information in the table. You need to set up from the first MA, when you set up for the best result, then turn on the second MA and transfer the settings of the first MA to the second. Then fine-tune both MAs. The results can increase significantly, but this is not always the case. Sometimes just one MA is enough

The strategy is paid, tested with my own experience and money since 2022. Own development for opening a position.

Gann Fan Strategy [KedarArc Quant]Description

A single-concept, rule-based strategy that trades around a programmatic Gann Fan.

It anchors to a swing (or a manual point), builds 1×1 and related fan lines numerically, and triggers entries when price interacts with the 1×1 (breakout or bounce). Management is done entirely with the fan structure (next/previous line) plus optional ATR trailing.

What TV indicators are used

* Pivots: `ta.pivothigh/ta.pivotlow` to confirm swing highs/lows for anchor selection.

* ATR: `ta.atr` only to scale the 1×1 slope (optional) and for an optional trailing stop.

* EMA: `ta.ema` as a trend filter (e.g., only long above the EMA, short below).

No RSI/MACD/Stoch/Heikin/etc. The logic is one coherent framework: Gann price–time geometry, with ATR as a scale and EMA as a risk filter.

How it works

1. Anchor

* Auto: chooses the most recent *confirmed* pivot (you control Left/Right).

* Manual: set a price and bar index and the fan will hold that point (no re-anchoring).

* Optional Re-anchor when a newer pivot confirms.

2. 1×1 Slope (numeric, not cosmetic)

* ATR mode: `1×1 = ATR(Length) × Multiplier` (adapts to volatility).

* Fixed mode: `ticks per bar` (constant slope).

Because slope is numeric, it doesn’t change with chart zoom, unlike the drawing tool.

3. Fan Lines

Builds classic ratios around the 1×1: 1/8, 1/4, 1/3, 1/2, 1/1, 2/1, 3/1, 4/1, 8/1.

4. Signals

* Breakout: cross of price over/under the 1×1 in the EMA-aligned direction.

* Bounce (optional): touch + reversal across the 1×1 to reduce whipsaw.

5. Exits & Risk

* Take-profit at the next fan line; Stop at the previous fan line.

* If a level is missing (right after re-anchor), a fallback Risk-Reward (RR) is used.

* Optional ATR trailing stop.

Why this is unique

* True numeric fan: The 1×1 slope is calculated from ATR or fixed ticks—not from screen geometry—so it is scale-invariant and reproducible across users/timeframes.

* Deterministic anchor logic: Uses confirmed pivots (with your L/R settings). No look-ahead; anchors update only when the right bars complete.

* Fan-native trade management: Both entries and exits come from the fan structure itself (with a minimal ATR/EMA assist), keeping the method pure.

* Two entry archetypes: Breakout for momentum days; Bounce for range days—switchable without changing the core model.

* Manual mode: Lock a session’s bias by anchoring to a chosen swing (e.g., day’s first major low/high) and keep the fan constant all day.

Inputs (quick guide)

* Auto Anchor (Left/Right): pivot sensitivity. Higher values = fewer, stronger anchors.

* Re-anchor: refresh to newer pivots as they confirm.

* Manual Anchor Price / Bar Index: fixes the fan (turn Auto off).

* Scale 1×1 by ATR: on = adaptive; off = use ticks per bar.

* ATR Length / ATR Multiplier: controls adaptive slope; start around 14 / 0.25–0.35.

* Ticks per bar: exact fixed slope (match a hand-drawn fan by computing slope ÷ mintick).

* EMA Trend Filter: e.g., 50–100; trades only in EMA direction.

* Use Bounce: require touch + reverse across 1×1 (helps in chop).

* TP/SL at fan lines; Fallback RR for missing levels; ATR Trailing Stop optional.

* Transparency/Plot EMA: visual preferences.

Tips

* Range days: larger pivots (L/R 8–12), Bounce ON, ATR Multiplier \~0.30–0.40, EMA 100.

* Trend days: L/R 5–6, Breakout, Multiplier \~0.20–0.30, EMA 50, ATR trail 1.0–1.5.

* Match the TV Gann Fan drawing: turn ATR scale OFF, set ticks per bar = `(Δprice between anchor and 1×1 target) / (bars) / mintick`.

Repainting & testing notes

* Pivots require Right bars to confirm; anchors are set after confirmation (no look-ahead).

* Signals use the current bar close with TradingView strategy mechanics; real-time vs. bar-close can differ slightly, as with any strategy.

* Re-anchoring legitimately moves the structure when new pivots confirm—by design.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Hilly 2.0 Advanced Crypto Scalping Strategy - 1 & 5 Min ChartsHow to Use

Copy the Code: Copy the script above.

Paste in TradingView: Open TradingView, go to the Pine Editor (bottom of the chart), paste the code, and click “Add to Chart.”

Check for Errors: Verify no errors appear in the Pine Editor console. The script uses Pine Script v5 (@version=5).

Select Timeframe:

1-Minute Chart: Use defaults (emaFastLen=7, emaSlowLen=14, rsiLen=10, rsiOverbought=80, rsiOversold=20, slPerc=0.5, tpPerc=1.0, useCandlePatterns=false).

5-Minute Chart: Adjust to emaFastLen=9, emaSlowLen=21, rsiLen=14, rsiOverbought=75, rsiOversold=25, slPerc=0.8, tpPerc=1.5, useCandlePatterns=true.

Apply to Chart: Use a liquid crypto pair (e.g., BTC/USDT, ETH/USDT on Binance or Coinbase).

Verify Signals:

Green “BUY” or “EMA BUY” labels and triangle-up arrows below candles.

Red “SELL” or “EMA SELL” labels and triangle-down arrows above candles.

Green/red background highlights for signal candles.

Arrows use size.normal for consistent visibility.

Backtest: Use TradingView’s Strategy Tester to evaluate performance over 1–3 months, checking Net Profit, Win Rate, and Drawdown.

Demo Test: Run on a demo account to confirm signal visibility and performance before trading with real funds.

Lavender Multi-Signal Momentum StrategyOverview

The Lavender strategy is a sophisticated momentum-based trading system specifically optimized for Tesla (TSLA) on the 15-minute timeframe. It combines multiple technical signals to identify high-probability long entries during strong trending conditions.

Key Features

🎯 Multi-Signal Entry System

The strategy uses 4 distinct signal types that can be enabled/disabled individually:

Supertrend Pullback (Default: ON)

Identifies pullbacks in uptrends using Supertrend (ATR: 9, Factor: 0.5)

Enters when price retests EMA9-20 zone during bullish Supertrend

Donchian Breakout + Z-Score Momentum (Default: ON)

53-period Donchian channel breakouts

Combined with 35-period Z-Score momentum filter

Only triggers with positive momentum confirmation

Keltner Squeeze Expansion (Default: OFF)

Detects volatility squeeze conditions

Enters on breakout above Keltner Channel after compression

Opening Range Breakout (ORB) (Default: ON)

Tracks first hour range (9:30-10:30 AM)

Triggers on breakout above opening range high

🧭 Trend Regime Filter

EMA Trend Filter: 20 EMA > 100 EMA (Default: ON)

ADX Strength Filter: ADX > 22 with 15/13 smoothing (Default: ON)

Only trades when both trend conditions align

💵 Advanced Risk Management

Risk per Trade: 2.0% of capital (Default)

ATR-Based Stop Loss: 15-period ATR × 1.6 multiplier

Risk/Reward Ratio: 4:1 (Default)

Position Sizing: Automatic based on stop distance

Capital Options: Dynamic equity or fixed capital ($200,000 default)

⚙️ Execution Control

Candle Close Entries: Prevents intrabar noise (Default: ON)

Candle Close Exits: Stop loss and take profit only at bar close (Default: ON)

Trading Session: 9:00 AM - 4:00 PM (Default)

Trading Days: Monday-Saturday (Default: 123456)

Default Settings Summary

ParameterDefault ValuePurposeRisk per Trade2.0%Capital risk percentageATR Length15Stop loss calculationATR Multiplier1.6Stop distance factorRisk/Reward4.0Take profit multiplierEMA Fast20Short-term trendEMA Slow100Long-term trendADX Threshold22Minimum trend strengthMin Signals Required1Entry trigger thresholdInitial Capital$200,000Backtesting capital

How It Works

Trend Confirmation: Checks EMA alignment and ADX strength

Signal Generation: Scans for active momentum signals

Entry Execution: Enters when minimum signal threshold is met

Risk Management: Calculates position size based on ATR stop

Exit Management: Manages trades with 4:1 risk/reward ratio

Best Use Cases

Tesla (TSLA) on 15-minute charts

Trending market conditions

Intraday momentum trading

Markets with clear directional bias

Visual Indicators

Blue Line: 100-period EMA (trend filter)

Green/Red Line: Supertrend indicator

Teal Line: Donchian channel high

Purple Triangles: Keltner breakout signals

Orange Arrows: Opening range breakouts

Green Dots: Combined entry signals

Red/Green Lines: Active stop loss and take profit levels

Risk Disclaimer

This strategy is optimized for Tesla's specific price behavior on 15-minute timeframes. Past performance does not guarantee future results. Always test thoroughly and manage risk appropriately.

Created by kevloewe - Specialized for TSLA 15M momentum trading

AI - Customizable EMA Offset Entry StrategyMoving average with offsets, such that buy indicators are above the MA and sell indicators are below the MA

Mikey’s Strategy (AutoEMA+)

⚙️ Core Idea:

A long-only EMA crossover strategy that automatically selects the optimal EMA length (5–25) based on historical performance using a custom scoring system.

🎯 Entry Conditions:

Price crosses above the selected EMA.

(Optional) Price is above HTF EMA200 (higher timeframe trend).

(Optional) ADX is above a minimum threshold.

(Optional) Volume is above average × multiplier.

A cooldown period has passed since the last exit.

❌ Exit Condition:

Price closes fully below the EMA (current candle: high, low, and close all below),

and the previous candle was above or touched the EMA.

🧠 Auto EMA Selection Logic:

Scans EMAs in the range (e.g., 8–21) every N bars.

Scores each EMA based on:

Time price spent above the EMA

Respect for EMA (touches)

Trend consistency

Distance from EMA (when above)

Picks the EMA with the highest valid score, and updates only if it’s significantly better.

🛡️ Risk Management:

No pyramiding (1 position max).

Cooldown period after exit.

No hard stop loss or take profit.

📊 Visuals & Alerts:

Plots the selected EMA and optional HTF EMA200.

Entry markers and info label on the chart.

Alerts for valid entries and filtered signals.

hh ema 2 (No TP)hi, my first strategy. Only btc. it will be idea for btc. and it can use for bot system.

EMA20 Cross Strategy with countertrades and signalsEMA20 Cross Strategy Documentation

Overview

The EMA20 Cross Strategy with Counter-Trades and Instant Signals is a Pine Script (version 6) trading strategy designed for the TradingView platform. It implements an Exponential Moving Average (EMA) crossover system to generate buy and sell signals, with optional trend filtering, session-based trading, instant signal processing, and visual/statistical feedback. The strategy supports counter-trades (closing opposing positions before entering new ones) and operates with a fixed trade size in EUR.

Features

EMA Crossover Mechanism:

Uses a short-term EMA (configurable length, default: 1) and a long-term EMA (default: 20) to detect crossovers.

A buy signal is generated when the short EMA crosses above the long EMA.

A sell signal is generated when the short EMA crosses below the long EMA.

Instant Signals:

If enabled (useInstantSignals), signals are based on the current price crossing the short EMA, rather than waiting for the candle close.

This allows faster trade execution but may increase sensitivity to price fluctuations.

Trend Filter:

Optionally filters trades based on the trend direction (useTrendFilter).

Long trades are allowed only when the short EMA (or price, for instant signals) is above the long EMA.

Short trades are allowed only when the short EMA (or price) is below the long EMA.

Session Filter:

Restricts trading to specific market hours (sessionStart, default: 09:00–17:00) if enabled (useSessionFilter).

Ensures trades occur only during active market sessions, reducing exposure to low-liquidity periods.

Customizable Timeframe:

The EMA calculations can use a higher timeframe (e.g., 5m, 15m, 1H, 4H, 1D, default: 1H) via request.security.

This allows the strategy to base signals on longer-term trends while operating on a shorter-term chart.

Trade Management:

Fixed trade size of €100,000 per trade (tradeAmount), with a maximum quantity cap (maxQty = 10,000) to prevent oversized trades.

Counter-trades: Closes short positions before entering a long position and vice versa.

Trades are executed with a minimum quantity of 1 to ensure valid orders.

Visualization:

EMA Lines: The short EMA is colored based on the last signal (green for buy, red for sell, gray for neutral), and the long EMA is orange.

Signal Markers: Displays buy/sell signals as arrows (triangles) above/below candles if enabled (showSignalShapes).

Background/Candle Coloring: Optionally colors the chart background or candles green (bullish) or red (bearish) based on the trend (useColoredBars).

Statistics Display:

If enabled (useStats), a label on the chart shows:

Total closed trades

Open trades

Win rate (%)

Number of winning/losing trades

Profit factor (gross profit / gross loss)

Net profit

Maximum drawdown

Configuration Inputs

EMA Short Length (emaLength): Length of the short-term EMA (default: 1).

Trend EMA Length (trendLength): Length of the long-term EMA (default: 20).

Enable Trend Filter (useTrendFilter): Toggles trend-based filtering (default: true).

Color Candles (useColoredBars): Colors candles instead of the background (default: true).

Enable Session Filter (useSessionFilter): Restricts trading to specified hours (default: false).

Trading Session (sessionStart): Defines trading hours (default: 09:00–17:00).

Show Statistics (useStats): Displays performance stats on the chart (default: true).

Show Signal Arrows (showSignalShapes): Displays buy/sell signals as arrows (default: true).

Use Instant Signals (useInstantSignals): Generates signals based on live price action (default: false).

EMA Timeframe (emaTimeframe): Timeframe for EMA calculations (options: 5m, 15m, 1H, 4H, 1D; default: 1H).

Strategy Logic

Signal Generation:

Standard Mode: Signals are based on EMA crossovers (short EMA crossing long EMA) at candle close.

Instant Mode: Signals are based on the current price crossing the short EMA, enabling faster reactions.

Trade Execution:

On a buy signal, closes any short position and opens a long position.

On a sell signal, closes any long position and opens a short position.

Position size is calculated as the minimum of €100,000 or available equity, divided by the current price, capped at 10,000 units.

Filters:

Trend Filter: Ensures trades align with the trend direction (if enabled).

Session Filter: Restricts trades to user-defined market hours (if enabled).

Visual Feedback

EMA Lines: Provide a clear view of the short and long EMAs, with the short EMA’s color reflecting the latest signal.

Signal Arrows: Large green triangles (buy) below candles or red triangles (sell) above candles for easy signal identification.

Chart Coloring: Highlights bullish (green) or bearish (red) trends via background or candle colors.

Statistics Label: Displays key performance metrics in a label above the chart for quick reference.

Usage Notes

Initial Capital: €100,000 (configurable via initial_capital).

Currency: EUR (set via currency).

Order Processing: Orders are processed at candle close (process_orders_on_close=true) unless instant signals are enabled.

Dynamic Requests: Allows dynamic timeframe adjustments for EMA calculations (dynamic_requests=true).

Platform: Designed for TradingView, compatible with any market supported by the platform (e.g., stocks, forex, crypto).

Example Use Case

Scenario: Trading on a 5-minute chart with a 1-hour EMA timeframe, trend filter enabled, and session filter set to 09:00–17:00.

Behavior: The strategy will:

Calculate EMAs on the 1-hour timeframe.

Generate buy signals when the short EMA crosses above the long EMA (and price is above the long EMA).

Generate sell signals when the short EMA crosses below the long EMA (and price is below the long EMA).

Execute trades only during 09:00–17:00.

Display green/red candles and performance stats on the chart.

Limitations

Instant Signals: May lead to more frequent signals, increasing the risk of false positives in volatile markets.

Fixed Trade Size: Does not adjust dynamically based on market conditions beyond equity and max quantity limits.

Session Filter: Simplified and may not account for complex session rules or holidays.

Statistics: Displayed on-chart, which may clutter the view in smaller charts.

Customization

Adjust emaLength and trendLength to suit different market conditions (e.g., shorter for scalping, longer for swing trading).

Toggle useInstantSignals for faster or more stable signal generation.

Modify sessionStart to align with specific market hours.

Disable useStats or showSignalShapes for a cleaner chart.

This strategy is versatile for both manual and automated trading, offering flexibility for various markets and trading styles while providing clear visual and statistical feedback.