Range%This indicator displays the range of each candle i.e. High minus Low as a percentage of the previous closing price. It does not account for gaps, making it particularly useful for intraday trading. By tracking the volatility cycle of candles, this indicator helps identify periods of increased or decreased market volatility, allowing traders to pinpoint the best days to execute trades.

If the Range% is below low line candles will turn White and If Range% is above the High Line Candles will turn Red.

Options

Option Value/Time Value DifferenceThis indicator calculates and visualizes the difference between two option contracts (either their time value or option value) based on a user-selected underlying instrument (e.g., NIFTY 50). It fetches real-time data for the underlying and the two specified options, computes their intrinsic and time values, and plots either the time value or option value (ask price) along with their difference. A customizable table displays key details, including strike prices, option types (Call/Put), and the selected values, with a dark mode option for better visibility.

Key Features:

Flexible Plotting: Choose to plot and display either the Time Value (option price minus intrinsic value) or the Option Value (ask price) for two option strikes.

Difference Calculation: Plots the difference between the two options’ selected values (time value or option value) as a distinct line.

Dynamic Table: Shows strike prices, option types (CE/PE), and the selected values (time value or option value) for both options, plus their difference.

Dark Mode Support: Toggle between light and dark themes for the table display.

Real-Time Data: Uses TradingView’s request.security to fetch live prices for the underlying and options.

Use Case:

This script is ideal for options traders who want to compare two strikes (e.g., a Call and a Put, or two Calls/Puts at different strikes) and analyze their time value or option value differences in real-time. It’s particularly useful for strategies like spreads, straddles, or strangles.

How to Use

Add to Chart:

Open TradingView, go to the Pine Editor, paste this script, and click “Add to Chart.”

Configure Inputs:

Underlying Instrument: Enter the symbol of the underlying asset (e.g., NSE:NIFTY for NIFTY 50).

Option Instrument 1: Enter the symbol of the first option (e.g., NSE:NIFTY250327C24000 for a Call expiring March 27, 2025, at strike 24000).

Option Instrument 2: Enter the symbol of the second option (e.g., NSE:NIFTY250327C24500 for a Call at strike 24500).

Plot Type: Select either Time Value (default) or Option Value to determine what is plotted and displayed.

Dark Mode: Check this box to switch the table to a dark theme (default is light).

Interpret Outputs:

Chart Lines:

Blue Line: Value of the first option (time value or option value, based on selection).

Red Line: Value of the second option.

Purple Line: Difference between the two options’ values.

Table (Middle-Left Position):

Row 1: Strike price and type (CE/PE) of the first option.

Row 2: Strike price and type of the second option.

Row 3: Selected value (time value or option value) of the first option.

Row 4: Selected value of the second option.

Row 5: Difference between the two options’ values.

Adjust Settings:

Modify the input symbols or plot type via the indicator’s settings to suit your analysis needs.

Inputs

Underlying Instrument (Symbol, Default: NSE:NIFTY):

The ticker symbol of the underlying asset (e.g., NIFTY 50 index).

Option Instrument 1 (Symbol, Default: NSE:NIFTY250327C24000):

The ticker symbol of the first option contract. Must follow a format like NSE:NIFTY (e.g., Call at 24000).

Option Instrument 2 (Symbol, Default: NSE:NIFTY250327C24500):

The ticker symbol of the second option contract (e.g., Call at 24500).

Plot Type (String, Options: Time Value, Option Value, Default: Time Value):

Choose whether to plot and display the Time Value (option price minus intrinsic value) or the Option Value (ask price).

Dark Mode (Boolean, Default: false):

Enable for a dark-themed table; disable for a light theme.

Outputs

Plotted Lines:

Value 1 (Blue): Time value or option value of the first option, depending on the Plot Type.

Value 2 (Red): Time value or option value of the second option.

Difference (Purple): The difference between Value 1 and Value 2 (e.g., Time Value 1 - Time Value 2).

Table Display:

Strike prices and option types (Call/Put) for both options.

Selected values (time value or option value) for each option.

The difference between the two options’ selected values.

Ivan Gomes StrategyIG Signals+ - Ivan Gomes Strategy

This script is designed for scalping and binary options trading, generating buy and sell signals at the beginning of each candle. Although it is mainly optimized for short-term operations, it can also be used for medium and long-term strategies with appropriate adjustments.

How It Works

• The indicator provides buy or sell signals at the start of the candle, based on a statistical probability of candle patterns, depending on the timeframe.

• It is essential to enter the trade immediately after the signal appears and exit at the end of the same candle.

• If the first operation results in a loss (Loss), the script will send another trade signal at the start of the next candle. However, if the first trade results in a win (Gain), no new signal will be generated.

• The signals follow cycles of 3 candles, regardless of the timeframe. However, if a Doji candle appears, the cycle is interrupted, and no signals will be generated until the next valid cycle starts.

• The strategy consists of up to two trades per cycle: if the first trade is not successful, the second trade serves as an additional attempt to recover.

Key Points to Consider

1. Avoid trading in sideways markets – If price levels do not fluctuate significantly, the accuracy of the signals may decrease.

2. Trade in the direction of the trend – Using Ichimoku clouds or other trend indicators can help confirm trend direction and improve signal reliability. If the market is in an uptrend (bullish trend) and the indicator generates a sell signal, the most prudent decision would be to wait for a buy signal that aligns with the main trend. The same applies to downtrends, where buy signals may be riskier.

These decisions should be based on chart reading and supported by other technical analysis tools, such as support and resistance levels, which indicate zones where price might face obstacles or reverse direction. Additionally, Fibonacci retracement levels can help identify possible pullback points within a trend. Moving averages are also useful for visualizing the general market direction and confirming whether an indicator signal aligns with the overall price structure. Combining these tools can increase trade accuracy and prevent unnecessary trades against the main trend, reducing risks.

3. Works based on probability statistics – The algorithm analyzes candle formations and their statistical probabilities depending on the timeframe to optimize trade entries.

4. Best suited for scalping and binary options – This strategy performs best in 1-minute and 5-minute timeframes, allowing for multiple trades throughout the day.

Technical Details

• The script detects the candle cycle and assigns an index to each candle to identify patterns and possible reversals.

• It recognizes reference candles, stores their colors, and compares them with subsequent candles to determine if a signal should be triggered.

• Doji candle rules are implemented to avoid false signals in indecisive market conditions. When a Doji appears, the script does not generate signals for that cycle.

• The indicator displays visual alerts and notifications, ensuring fast execution of trades.

Disclaimer

The IG Signals+ indicator was created to assist traders who struggle to analyze the market by providing objective trade signals. However, no strategy is foolproof, and this script does not guarantee profits.

Trading involves significant financial risk, and users should test it in a demo account before trading with real money. Proper risk management is crucial for long-term success.

RSI and EMA crossover with big candlesThis TradingView indicator identifies big bullish and bearish candles using RSI, EMA crossovers, and wick analysis. It helps traders spot potential trend continuation or reversal points by labeling significant price movements and providing real-time alerts.

NOTE: THIS WORKS BEST ON 2 MINS TIME FRAME ONLY

Key Features:

✅ Big Candle Detection:

Detects large candles based on body size and recent price action.

Differentiates between bullish (green) and bearish (red) candles.

✅ Wick Analysis & RSI Filtering:

Ensures candles have relatively small wicks for stronger signals.

RSI confirmation:

Bullish signals require RSI above 59.

Bearish signals require RSI below 40.

✅ Candle Counting & Labeling:

Labels bullish and bearish candles with sequential numbers.

Adds PUTS and CALLS labels when an 8 EMA crosses the 21 EMA.

Adjusts label positioning for better visibility.

✅ Configurable Alerts for #2 Candle:

Alerts trigger when the second bullish or bearish candle is detected.

Users can enable/disable alerts from the script settings.

✅ EMA Crossover Signals:

Bullish crossover (8 EMA above 21 EMA): Displays a "CALLS" label below the candle.

Bearish crossover (8 EMA below 21 EMA): Displays a "PUTS" label above the candle.

Usage:

📊 Trend Confirmation: Use the big candle signals + EMA crossover for stronger trade setups.

🔔 Alerts: Get notified when the second big candle forms.

📉 Reversals & Continuation Patterns: Identify shifts in momentum early.

This script is perfect for traders looking for a clean and powerful price action-based indicator with automated alerts. 🚀

Combined Options IndicatorCombined Options Indicator

Indicator combines 2 option charts value with an operator.In the example, It combines 48600 strike call and put of banknifty, effectievely giving straddle price.

Features:

Combine any two option instruments (calls or puts) with customizable parameters

Support for different underlying instruments (NIFTY, BANKNIFTY, etc.)

Apply various operators: addition, subtraction, multiplication, division, or exponentiation

Visualize results as either candlesticks or a line chart

Customizable colors for bullish and bearish movements

Information panel displaying individual and combined values

Usage:

Input all components of each option symbol separately including instrument name, expiry details (year, month, day), option type (call/put), and strike price. The indicator automatically constructs the symbols, retrieves their data, and applies your selected operation to display the combined values.

Ideal for option traders looking to track custom spreads, analyze volatility, or create tailored trading indicators based on option price relationships.

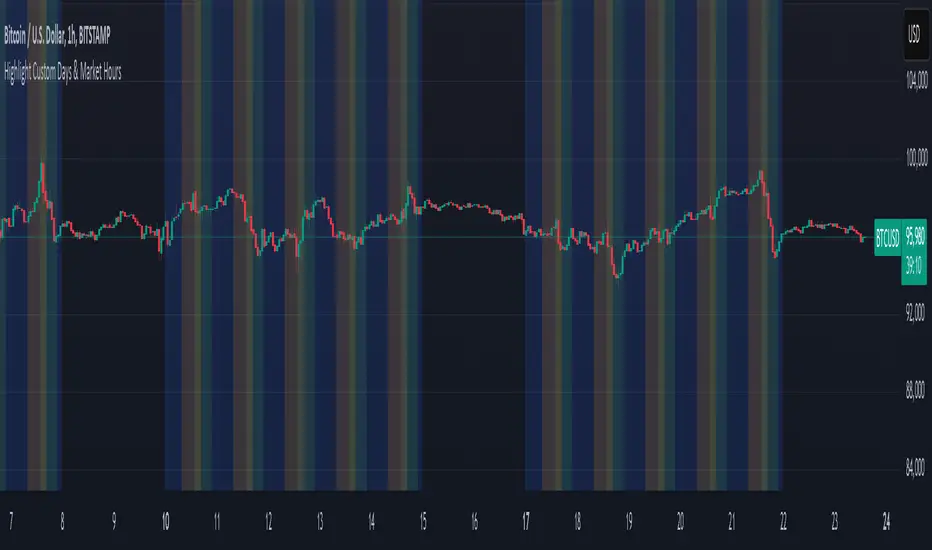

Mon to Fri + LSE and NYSE📌 Highlight Custom Days & Market Hours Indicator 📌

🔹 Overview:

This script allows traders to visually highlight specific weekdays and market sessions directly on their TradingView charts. With customizable checkboxes, you can choose which days of the week to highlight, along with session times for the New York Stock Exchange (NYSE) and London Stock Exchange (LSE).

🔹 Features:

✅ Select individual weekdays (Monday–Friday) to highlight in blue

✅ Highlight NYSE open hours (2:30 PM – 9:30 PM UK time) in green

✅ Highlight LSE open hours (8:00 AM – 4:30 PM UK time) in orange

✅ Ensures NYSE & LSE sessions are only highlighted on weekdays (no weekends)

✅ Clean and simple visualization for enhanced market awareness

🔹 How to Use:

1️⃣ Add the indicator to your TradingView chart

2️⃣ Use the settings panel to enable/disable specific weekdays

3️⃣ Toggle NYSE or LSE session highlights based on your trading preference

🚀 Perfect for traders who follow institutional sessions and want better time-based confluence in their strategies!

NSE: 2in1 Options-Index (Nifty-Bank-MID-Fin)

1. Using Two Charts in One Indicator with Buy and Sell Signals on Both Charts

Dual-Chart Functionality: This indicator allows you to monitor two charts simultaneously – the main chart (Options) and the underlying index chart (NIFTY, BANKNIFTY, etc.).

The index chart (below the main chart) shows the underlying index movement.

The main chart displays the Options data (e.g., NIFTY options, BANKNIFTY options).

Buy/Sell Signals on Both Charts:

Buy and sell signals are generated on both the options chart and the index chart, ensuring you don’t miss any trading opportunities.

This dual-chart setup helps you correlate the movement of the index with the options data for better decision-making.

2. Works Across Major Indices (NIFTY, BANKNIFTY, FINNIFTY, etc.)

Automatic Index Detection: The script automatically detects the underlying index based on the chart symbol. It supports:

NIFTY, BANKNIFTY, FINNIFTY, MIDCPNIFTY, SENSEX

Flexibility: Whether you’re trading NIFTY options or BANKNIFTY options, the indicator adapts to the selected index and provides accurate signals.

3. Helps You Select ATM, ITM, and OTM Strikes (Ideal for Beginners and Advanced Traders)

ATM (At-The-Money) Strike Calculation:

The script calculates the ATM strike price based on the current spot price of the underlying index.

ITM (In-The-Money) and OTM (Out-Of-The-Money) Strikes:

Users can adjust the strike price using a slider to select ITM or OTM strikes.

This feature is especially helpful for beginners who are learning about options trading and want to understand the difference between ITM, ATM, and OTM strikes.

Strike Price Display:

The selected strike price is displayed on the chart, making it easy to identify the right strike for your trades.

4. Double EMA Selection for Trading

Customizable EMAs:

The script uses two Exponential Moving Averages (EMAs) to generate signals:

Short EMA (Default: 21 periods)

Long EMA (Default: 34 periods)

Users can customize the EMA lengths based on their trading strategy.

5. Option Chart in the Main Chart with Index Chart Below for Easy Monitoring

Integrated Chart Setup:

The main chart displays the options data (e.g., NIFTY options, BANKNIFTY options).

The index chart (below the main chart) shows the underlying index movement.

Benefits:

This setup allows you to monitor both the options and the index in a single view, making it easier to:

Correlate the movement of the index with the options data.

Identify trading opportunities directly on the chart.

No need to switch between multiple charts – everything is in one place.

6. Targets and Stop-Loss When the Signal is Generated

Dynamic Targets and Stop-Loss:

The script calculates targets and stop-loss levels based on the Predicted Range (PR) bands.

Trailing Stop-Loss:

The stop-loss level adjusts dynamically as the price moves in your favor.

Target Levels:

Two target levels are provided (Target 1 and Target 2) based on the PR bands.

Visual Indicators:

Targets and stop-loss levels are plotted on the chart with labels and lines for easy reference.

Colors:

Trailing Stop: Light Pink

Target 1: Light Green

Target 2: Light Green

7. Various Other Options in One Indicator

Advanced Statistical Bands (KRO Settings):

The script includes Kernel Regression Oscillator (KRO) settings for advanced traders.

Plots upper and lower bands based on standard deviation and kernel regression.

Helps identify overbought and oversold conditions.

Customizable Alerts:

Users can enable/disable alerts for:

Buy/Sell signals.

Trailing stop-loss hits.

Target achievements.

Summary of Benefits

All-in-One Tool: Combines candlestick analysis, EMAs, options strike selection, targets, stop-loss, and advanced statistical bands in a single indicator.

Beginner-Friendly: Helps new traders understand ATM, ITM, and OTM strikes while providing clear buy/sell signals.

Advanced Features: Includes KRO settings, dynamic targets, and trailing stop-loss for experienced traders.

Dual-Chart Setup: Monitor options and the underlying index simultaneously for better decision-making.

Customizable: Adjust EMA lengths, strike prices, colors, and alerts to suit your trading style.

Put/Call RatioPut/Call Ratio Indicator

This indicator visualizes the Put/Call Ratio for various market symbols, helping traders assess market sentiment and potential reversals. It offers a dropdown menu to select from a range of Put/Call Ratios, including broad equities (CBOE), major indices (SPX, QQQ, IWM, VIX), and individual stocks (TSLA, GOOG, META, AMZN, MSFT, INTC).

The indicator plots the Put/Call Ratio with adjustable moving averages and standard deviation bands to highlight overbought or oversold conditions. A short-term moving average (default: 10 periods) is displayed with trend-based coloring, while longer-term moving averages (defaults: 30 and 200 periods) are calculated but hidden by default. Bands at 1, 1.5, and 2 standard deviations provide context for extreme readings.

Key Overbought/Oversold Signals:

Short-Term Extremes: The 10-day moving average moves beyond 1 standard deviation from the 200-day moving average, signaling potential overbought (above) or oversold (below) conditions. This will be highlighted by red or green background color.

Ratio Extremes: The Put/Call Ratio line itself crosses outside 2 standard deviations from the 200-day moving average, indicating stronger overbought or oversold zones.

Conditional coloring of the ratio line reflects its position relative to the bands, and background shading highlights when the short-term moving average crosses key levels.

Key Features:

Selectable Put/Call Ratio symbols.

Trend-colored moving averages.

Standard deviation bands for volatility analysis.

Dynamic line and background coloring for quick insights.

Usage:

Use this indicator to gauge market sentiment—high ratios may suggest bearish sentiment or oversold conditions, while low ratios may indicate bullish sentiment or overbought conditions. Combine with price action or other tools for confirmation.

IronCondor 10am 30TF by RMThe IronCondor 10am 30TF indicator shows Iron Condor trades win rate over a large number of days.

The default ETFs in this indicators are "QQQ", "SPY", "RUT" , "CBTX" and "SPX", other entries have not been tested.

Iron Condor quick explanation:

- Iron Condors trades have four options, generally, are based around a Midpoint price (Current Market Price Strike) and

- Two equally distances Strikes for the SELL components (called the Body of the Iron Condor)

- Further away from the two SELLs, another Two BUYs for protection (not considered in this indicator)

- Iron Condors are used for Passive Income based on small gains most of the time.

The IronCondor 10am 30TF has its logic created based on the premises that:

- Most days the market prices stay within a range.

- As example the S&P market prices would stay within 1% on about 80% of the time

- The moving markets (bullish or bearish) occur about 20% of the time

- The biggest market price volatility generally occurs before market opens and then around the first hour or so of trade in the day.

- After the first hour or so of the market the prices would be most likely to stay within a range.

The operation is simple:

- At the Trade Star time in the day (say 10:30 Hrs.) draws a vertical yellow line, then

- Creates two blue horizontal lines for the SELL limits in the Iron Condor Body, at +/- 1% price boundary (check Ticker list below for values)

- At the Trade End time (say 16:00 Hrs.) checks that none of the SELL limits have been broken by highs or lows during the trade day

(The check is done calculating at Trade End time the high/lows 10 bars back for 30 min TF - timeframe)

- There is a label at each Trade End time with Win/Loss and Body value.

- There is one final label with overall calculated past performance in Win percentage out of 'n' trades

Defaults and User Entries:

- The User can modify the Midpoint price called 'IronCondor Midpoint STRIKE' (default is the Candle Close at the selected time)

- The User can modify the Body value called 'IronCondor Body' (default is the Ticker's selected value as per list below)

"QQQ" or "SPY" Body = 5

"RUT" or "CBTX" Body = 20

"SPX" Body = 60

* Disclaimer: This is not a Financial tool, it cannot used as any kind of advice to invest or risk moneys in any market,

Markets are volatile in nature - with little or no warning - and will drain your account if you are not careful.

Use only as an academic demonstrator => * Use at your own risk *

Black-Scholes Probability Model with Time-Based VolatilityI developed this tool to automate probability calculations and to verify if Polymarkets accurately reflects Bitcoin's value. The indicator uses a modified Black-Scholes model to estimate the likelihood of Bitcoin exceeding or falling below a $97,000 strike price by a specified end date, providing a "fair value" probability.

Key Features:

- Timeframe Control: Displays data only between a defined start and end date, ensuring relevance during the prediction period.

- Dynamic Volatility Calculation: Offers a choice between manual input and auto-calculated annualized volatility. The auto-calculation derives historical volatility from recent price data over a selected lookback period and adjusts it based on the time remaining until expiration. More time implies greater expected price movement; less time indicates a narrower expected range.

- Probability Estimation: Calculates an adjusted parameter (d1) and applies a normal cumulative distribution function (CDF) to determine:

- "Yes" (Green Line): Probability that Bitcoin will exceed $97,000.

- "No" (Red Line): Probability that Bitcoin will remain below $97,000.

When Bitcoin's price is exactly $97,000, the tool sets the probabilities to a balanced 50/50 split, indicating fair value.

- Fair Value Indicator: Includes a static white reference line at 50% probability. A 50/50 probability suggests Bitcoin is fairly valued at $97,000; deviations indicate potential overvaluation or undervaluation.

- Polymarkets Tracking & Trading Strategy: I use Polymarkets to access cost-effective, high-leverage long call options on Bitcoin. However, these options don't always mirror Bitcoin's price movements precisely. For instance, if I anticipate Bitcoin rising from $95,000 to $97,000 by day's end, the tool might show a fair value probability of 50%. If Polymarkets quotes a 50% chance, the alignment indicates a fair trade. In such cases, I can avoid an unfavorable trade or exploit the difference as an arbitrage opportunity.

- Personal Motivation: This indicator eliminates the need for manual calculations and ensures I can quickly assess when Polymarkets' pricing aligns with Bitcoin's actual value, leading to more informed trading decisions.

This tool automates probability and fair value assessments, serving as a practical resource for verifying and potentially capitalizing on discrepancies in Polymarkets' Bitcoin pricing. It helps identify when there's a mismatch between the market's implied probability and the calculated fair value, allowing me to avoid unnecessary premiums on high-leverage options.

VMA [Extreme Advanced Custom Table for BTCUSD]This indicator implements a Variable Moving Average (VMA) with a 33-period length—selected in homage to the Tesla 369 concept—to dynamically adjust to market conditions. It not only calculates the adaptive VMA but also displays a custom table of key metrics directly on the chart. Here’s how to use it:

Apply to Your Chart:

Add the indicator to your chart (optimized for BTCUSD, though it can be used on other symbols) and choose your desired source (e.g., close).

Customize Your Visuals:

Trend & Price Lines: Toggle the trend colors, price line, and bar coloring based on the VMA’s direction.

Channels & Slope: Enable the volatility channel and slope line to visualize market volatility and the VMA’s momentum.

Pivot Points & Super VMA: Activate pivot high/low markers for potential reversal points and a Super VMA (SMA of VMA) for an extra smoothing layer.

Table Customization: Adjust the table’s position, colors, and font sizes as needed for your viewing preference.

Monitor Key Metrics:

The dynamic table displays essential information:

VMA Value & Trend: See the current VMA and whether the trend is Bullish, Bearish, or Neutral.

Volatility Index (vI) & Slope: Quickly assess market volatility and the VMA’s slope (both absolute and percentage).

Price-VMA Difference & Correlation: Evaluate how far the price is from the VMA and its correlation.

Higher Timeframe VMA: Compare the current VMA with its higher timeframe counterpart (set via the “Higher Timeframe” input).

Alerts for Key Conditions:

Built-in alert conditions notify you when:

The trend changes (bullish/bearish).

The VMA slope becomes extreme.

The price and VMA correlation falls below a defined threshold.

The VMA crosses its higher timeframe average.

How to Use the Script:

Add to Your Chart:

Open TradingView and apply the indicator to your BTCUSD (or any other) chart.

The indicator will overlay on your chart, plotting the VMA along with optional elements such as the price line, volatility channels, and higher timeframe VMA.

Customize Your Settings:

Inputs:

Choose your data source (e.g., close price).

Adjust the VMA length (default is 33) if desired.

Visual Options:

Toggle trend colors, bar coloring, and additional visuals (price line, volatility channels, slope line, pivot points, and Super VMA) to suit your trading style.

Table Customization:

Set the table position, colors, border width, and font size to ensure key metrics are easily visible.

Higher Timeframe:

You can change the higher timeframe input (default is Daily) to better fit your analysis routine.

Interpret the Indicator:

Trend Analysis:

Watch the color-coded VMA line. A rising (orange) VMA suggests bullish momentum, while a falling (red) one indicates bearish conditions.

What Sets This Script Apart:

Dynamic Adaptation:

Unlike a fixed-period moving average, the VMA adjusts its sensitivity in real time by integrating a volatility measure, making it more adaptive to market swings.

Multi-Layered Analysis:

With integrated volatility channels, pivot points, slope analysis, and a higher timeframe VMA, this tool gives you a fuller picture of market dynamics.

Immediate Data at a Glance:

The real-time table consolidates multiple key metrics into one view, saving time and reducing the need for additional indicators.

Custom Alerts:

Pre-built alert conditions allow for timely notifications, ensuring you don’t miss critical market changes.

HTF EMA Pivot PointsHTF EMA Pivot Points - TradingView Indicator

📌 Overview

The HTF EMA Pivot Points indicator displays Exponential Moving Averages (EMAs) from higher timeframes (HTF) on your current chart. These EMAs act as dynamic support and resistance levels, helping traders identify key areas where price is likely to react.

⚡ Key Features

✅ Plots EMAs from multiple timeframes (1H, 4H, Daily)

✅ Works on any chart (1M, 5M, 15M, etc.)

✅ Acts as pivot points for price action, helping with trade entries & exits

✅ Customizable EMA lengths for flexibility

✅ Ideal for scalping, 0DTE options trading, and swing trading

🛠 How It Works

The script calculates EMAs from 1H, 4H, and Daily charts and overlays them on your current timeframe. These levels often act as support and resistance zones, where price tends to bounce or reject.

🎯 How to Use It for Trading

📍 Bullish Setup (Buy Calls)

• Price bounces off a higher timeframe EMA (e.g., 4H or Daily EMA)

• Confirmation with RSI or Fair Value Gaps (FVGs)

📍 Bearish Setup (Buy Puts)

• Price rejects from a higher timeframe EMA

• Confirmation with other indicators (RSI, MACD, Order Flow)

🚀 Why Use This Indicator?

• Filters out noise from lower timeframe EMAs

• Confirms trend direction using key moving averages

• Helps avoid false breakouts by identifying strong institutional levels

This is a must-have tool for traders who rely on higher timeframe confluence for scalping, options trading, or swing trading. 📈🔥

Monthly Options Expiration 2025Monthly Options Expiration 2025

Plots the monthly options expiration dates in advance for the year 2025.

Happy trading and all the best.

AllDay Session TimesIndicator: Custom Session Times

This indicator is designed to assist traders by visualizing specific trading session times on the TradingView platform. It highlights two important trading sessions: the Day Session and the Evening Session, providing a visual aid that helps traders navigate the markets with greater accuracy.

Day Session Time Range:

Starts: 10:55 UTC+2

Ends: 13:30 UTC+2

Evening Session Time Range:

Starts: 16:55 UTC+2

Ends: 18:30 UTC+2

How It Works:

Colors and Backgrounds: This indicator uses background colors to differentiate the sessions. The green background appears during the Day Session, while the blue background indicates the Evening Session.

Lines: Session time ranges are also marked with clear lines on the chart, making it easier to identify the specific session periods.

Time Zone: The time zone is set to UTC+2 (Europe/Helsinki), but it can easily be adjusted to match your local time zone.

Why Use This Indicator?

This indicator is especially useful for traders who focus on specific market sessions. For example:

The Day Session might be when the market is more active, and trends are clearer.

The Evening Session could be a good time to observe market adjustments based on the events of the day and find potential trading opportunities.

By visualizing these specific time frames, the indicator helps reduce distractions and enables a more focused approach to trading.

Use Cases:

This indicator is ideal for:

Day traders and swing traders who want to focus on certain market sessions.

Technical analysts who prefer to visualize market behavior within specific time frames.

Strategy optimization and a more precise assessment of market conditions.

Features:

Visual session markers that help traders focus on key trading periods.

Easy customization of time zone and session time ranges.

Background colors and lines that improve chart readability and session tracking.

Made By AllDayEsa

Weekly Change(Green&Red) & Percentage Change(Blue&Yellow)Display bar chart of weekly price action. Use to determine the maximum price change in one week. It would be the possible strike price for a covered call option for weekly income.

WD Gann: Vertical Lines for Predefined Days/Bars AgoThis Pine Script draws vertical lines on the chart at specific time intervals, inspired by WD Gann’s theories of time cycles . WD Gann, a famous trader, believed that market movements were influenced by predictable time cycles. This script enables traders to visualize these key time cycles on the chart by placing vertical lines at predefined intervals (in bars ago), helping to identify potential turning points in the market.

The time intervals used in this script are inspired by Gann’s work, as well as astrological and numerological principles , which many traders believe influence market behavior . You can customize which time intervals (such as 3, 7, 9, 21, etc.) you want to track by enabling or disabling specific vertical lines on the chart.

Key Features:

Time Cycles Based on Gann’s Theory: Draws vertical lines at significant time intervals such as 3, 7, 9, 21, 27 bars ago, which are commonly used by Gann traders.

Astrological & Numerological Significance: The predefined intervals also align with key numerological and astrological values, allowing for a broader perspective on market cycles.

Customizable Intervals: You can choose which time intervals to display by enabling or disabling checkboxes for each cycle, allowing flexibility in chart analysis.

Visual Labels: Each vertical line is labeled with its corresponding "bars ago" value, providing clear reference points for the selected time cycles.

What Users Can Do:

Track and analyze market movements based on time cycles that are significant to Gann’s theory, as well as numerological and astrological influences.

Enable or disable vertical lines for specific cycles, like the 3-bar cycle, 9-bar cycle, or 365-bar cycle, depending on the intervals that align with your trading strategy.

Combine with other technical analysis tools and Gann techniques (e.g., Gann Angles, Gann Fans, or Square of Nine) for a more comprehensive trading approach.

This tool is designed for traders who believe in the power of time cycles to influence market behavior, and is especially useful for predicting turning points or key price movements based on these cycles.

Precision Trade Zone By KittisakThis indicator is designed for Money Management calculations, helping to facilitate risk management in trading, determining suitable leverage based on acceptable risk, and adjusting the Stop Loss level to align with the calculated leverage.

Abbreviation Descriptions

LR : Suitable Leverage.

EP : Entry Price.

BEP : Break-Even Point (a point where you can move your Stop Loss to prevent losses once the price reaches a certain level).

SL : Stop Loss (a recalculated Stop Loss level to match the leverage. You should use this as the Stop Loss price instead of the initial level you set).

TP : Take Profit (a point where you take profit based on the defined risk-reward ratio).

Note

When first activating the indicator, an error may occur, and no output will be displayed. This happens because you must first specify the Entry Price and Stop Loss in the indicator settings.

How Much Leverage Should You Use?

It may seem like a simple question but is difficult to answer.

Method for Calculating Suitable Leverage

Use the formula:

Leverage = Acceptable Loss / (Distance between Entry Price and Stop Loss + (Buy Fee + Sell Fee))

Calculating the Correct Stop Loss Point

(Stop Loss levels will be slightly adjusted or extended)

For Long Positions :

New Stop Loss = Entry Price * (1 - Acceptable Loss / (Calculated Leverage * 100))

For Short Positions :

New Stop Loss = Entry Price * (1 + Acceptable Loss / (Calculated Leverage * 100))

Calculating the Correct Take Profit Point

(Take Profit levels will be slightly adjusted or extended)

For Long Positions :

Take Profit = Entry Price * (1 + (Acceptable Loss / (Calculated Leverage * 100) * RR) + ((Buy Fee + Sell Fee) / 100))

For Short Positions :

Take Profit = Entry Price * (1 - (Acceptable Loss / (Calculated Leverage * 100) * RR) + ((Buy Fee + Sell Fee) / 100))

Benefits of This Calculation

1. Accurate Risk Assessment

The calculated leverage accounts for trading fees. For example, if you aim for a 2% loss, this method ensures the actual loss is exactly 2%, not more (e.g., 2% plus fees).

2. Eliminates Guesswork

Randomly setting leverage can lead to risks because the Stop Loss level may not align with your position. This calculation ensures that the leverage aligns precisely with your desired Stop Loss level.

3. Realistic Profit Targets

For example, with a 2% acceptable loss and a 1:2 RR, you expect a 4% profit. However, without this calculation, fees may reduce your profit below 4%. This method includes fees, ensuring your profit matches the intended target.

Caution

This indicator does not account for slippage or requotes. Use it with caution and allow a buffer for slippage in your calculations.

Indicator นี้มีไว้สำหรับคำนวณ Money Management ซึ่งจะช่วยอำนวยความสะดวกในการจัดการความเสี่ยงในการเทรด การคำนวณ Leverage ที่เหมาะสมกับความเสี่ยงที่คุณยอมรับได้ และจัดการจุด Stop Loss ให้เหมาะสมกับ Leverage นั้น

คำอธิบายเกี่ยวกับคำย่อ

LR หมายถึง Leverage ที่เหมาะสม

EP หมายถึง Entry Price หรือราคาเข้าซื้อ

BEP หมายถึง Break-Even Point หรือจุดคุ้มทุน (คุณสามารถย้าย Stop Loss มาที่จุดนี้เมื่อราคาไปถึงจุดหนึ่งเพื่อป้องกันการขาดทุนได้)

SL หมายถึง Stop Loss (ซึ่งเป็น Stop Loss ที่คำนวณใหม่เพื่อให้ตำแหน่งเหมาะสมกับ Leverage ที่คำนวณได้ คุณควรใช้จุดนี้เพื่อเป็นราคา Stop Loss แทนจุด Stop Loss ที่คุณกำหนดไว้ในตอนแรก)

TP หมายถึง Take Profit (เป็นจุดที่คุณจะขายทำกำไรตาม RR ที่กำหนดไว้)

* หมายเหตุ เมื่อเริ่มเปิด Indicator จะเกิด Error ขึ้น และไม่มีผลลัพท์ใด ๆ แสดงให้เห็น นั่นเป็นเพราะคุณต้องเข้าไปกำหนด Entry Price และ Stop Loss ในการตั้งค่าของ Indicator เสียก่อน

ต้องใช้ Leverage เท่าไหร่? มันเป็นคำถามที่ดูเหมือนง่าย แต่ตอบยาก

วิธีคำนวณ Leverage ที่เหมาะสม ใช้สมการคือ

Levarage = การขาดทุนที่ยอมรับได้ / (ระยะห่างระหว่าง Entry Price และ Stop Loss + (ค่าธรรมเนียมซื้อ + ค่าธรรมเนียมขาย))

นำผลลัพท์ Leverage ที่ได้มาคำนวณเพื่อหาจุด Stop Loss ที่ถูกต้อง (จุดของ Stop Loss จะมีการยืดขยายออกไปเล็กน้อย) โดยใช้สมการ

ตำแหน่ง Stop Loss ใหม่ = Entry Price * (1 - การขาดทุนที่ยอมรับได้ / (Leverage ที่คำนวณได้ * 100)) // สำหรับ Long

ตำแหน่ง Stop Loss ใหม่ = Entry Price * (1 + การขาดทุนที่ยอมรับได้ / (Leverage ที่คำนวณได้ * 100)) // สำหรับ Short

นำผลลัพท์ Leverage ที่ได้มาคำนวณเพื่อหาจุด Take Profit ที่ถูกต้อง (จุดของ Take Profit จะมีการยืดขยายออกไปเล็กน้อย) โดยใช้สมการ

ตำแหน่ง Take Profit = Entry Price * (1 + (การขาดทุนที่ยอมรับได้ / (Leverage ที่คำนวณได้ * 100) * RR) + ((ค่าธรรมเนียมซื้อ + ค่าธรรมเนียมขาย) / 100)) // สำหรับ Long

ตำแหน่ง Take Profit = Entry Price * (1 - (การขาดทุนที่ยอมรับได้ / (Leverage ที่คำนวณได้ * 100) * RR) + ((ค่าธรรมเนียมซื้อ + ค่าธรรมเนียมขาย) / 100)) // สำหรับ Short

ข้อดีของการคำนวณคือ

1. คุณจะได้ค่า Leverage ที่เหมาะสมกับความเสี่ยงที่คุณยอมรับได้โดยรวมค่าธรรมเนียมเข้าไปในนั้นแล้ว นั่นหมายความว่า ความสูญเสียจะเป็น 2% (ตามตัวอย่าง) จริง ๆ ไม่ใช่ 2% และถูกหักค่าธรรมเนียมเพิ่มอีก กลายเป็นสูญเสียมากกว่า 2%

2. การตั้ง Leverage มั่ว ๆ กลายเป็นความเสี่ยง นั่นเพราะตำแหน่งของ Stop Loss ไม่ได้อยู่ในจุดที่ควรจะเป็น การคำนวณนี้ช่วยให้คุณได้ Leverage ในตำแหน่ง Stop Loss ที่คุณต้องการโดยแท้จริง

3. ผลกำไรที่ได้รับตรงกับความต้องการจริง ๆ เช่น การขาดทุนที่ยอมรับได้ 2% และ RR 1:2 สิ่งที่คุณคิดคือกำไร 4% แต่จริง ๆ แล้วไม่ถึง 4% นั่นเพราะว่าโดนหักค่าธรรมเนียมไปส่วนหนึ่ง การคำนวณนี้ได้รวมค่าธรรมเนียมให้แล้ว คุณจึงได้กำไรที่ 4% อย่างถูกต้องตามต้องการ

ข้อควรระวัง

Indicator นี้ไม่ได้มีการควบคุมความเสี่ยงในเรื่องของ slippage หรือ requote โปรดใช้งานอย่างระมัดระวังและมีการเผื่อระยะสำหรับ slippage ด้วย

Best of Option Indicator - Manoj WadekarPlot this indicator for both CALL and PUT options and buy only when color of candle is YELLOW and above BLACK line.

Stop Loss & Take Profit LevelsCalculate and Plot Stop Loss (SL) Levels:

The indicator calculates the Stop Loss price level based on the account balance, risk percentage, and the trade's entry price.

For long positions, the SL is below the entry price.

For short positions, the SL is above the entry price.

Calculate and Plot Take Profit (TP) Levels:

The indicator calculates up to three Take Profit (TP) levels, each based on different Risk/Reward (R:R) ratios.

The R:R ratio determines how much reward (profit) you aim to achieve relative to the risk (the distance between the entry price and the stop loss).

These TP levels are plotted on the chart as lines above the entry price for long positions or below the entry price for short positions.

Manual Entry Price:

The user can input a manual entry price to simulate trades or plan trades before entering the market. This makes it useful for pre-trade analysis.

Dynamic Position Type:

Users can toggle between Long or Short positions:

Long Position: The trader expects the price to go up.

Short Position: The trader expects the price to go down.

The indicator adapts its calculations (SL and TP levels) based on the selected position type.

Risk Calculation Based on Account Balance:

The indicator calculates the amount of capital at risk (in €) based on the trader's account balance and the selected risk percentage.

For example:

If the account balance is €1,000 and the Stop Loss percentage is 1%, the risk amount is €10.

Visual Representation on the Chart:

The following levels are plotted on the chart:

Stop Loss Level (Red Line): The price level at which the trader would exit the trade to limit losses.

Take Profit Levels (Green Lines): Up to three price levels where the trader could take profits based on R:R ratios.

Entry Price (Blue Line): The price level where the trade begins.

These lines are dynamically updated as inputs are changed, providing instant feedback to the trader.

Rich's DikFat Money-Counter - ITM/OTM Options Price ViewerScript Overview

This Pine Script is a custom indicator designed for use on the TradingView platform. It analyzes options contracts, extracting key information from the options symbol, and then visualizes the relationship between the current price of the underlying asset and the option's strike price. Here’s a detailed explanation of the script and its components:

Key Features

Symbol Format Validation: The script checks whether the current symbol matches the expected format of an options symbol (like TSLA250131C400.0).

Extraction of Option Components: It extracts the base symbol (e.g., TSLA), expiration date (e.g., 250131), option type (C for call, P for put), and strike price (e.g., 400.0) from the options symbol.

Price Difference Calculation: It calculates the difference between the current price of the base asset (e.g., TSLA) and the option's strike price. Depending on whether the option is a call or put, the calculation is adjusted.

Visualization: The result is plotted on the chart, with color-coded filling to indicate whether the price difference is positive (ITM) or negative (OTM).

Detailed Explanation of Code Components

1. Indicator Definition

indicator("Rich's DikFat Money-Counter - In the Money/Out of the Money Options Price Viewer", shorttitle="Options Price Viewer", overlay=true)

This line defines the indicator's name, short title, and specifies that it should be plotted on the price chart (with overlay=true).

2. Symbol Detection

currentSymbol = syminfo.ticker

This retrieves the symbol of the current asset being analyzed. The script expects this symbol to be an options contract, for example, TSLA250131C400.0.

3. Symbol Format Validation

isOptionSymbol = str.length(currentSymbol) >= 9 and str.match(currentSymbol, "^ + {6} +(\. +)?$") != ""

This checks whether the current symbol matches the expected format for an option:

The symbol must have at least 9 characters.

It must follow a specific pattern: a base symbol (letters), a 6-digit expiration date, an option type (C for Call or P for Put), and a strike price that could include decimals.

[/list>

4. Extracting Option Components

If the symbol is a valid option symbol, the following code extracts the components:

baseSymbol := str.match(currentSymbol, "^ +")

expirationDate := str.substring(currentSymbol, str.length(baseSymbol), str.length(baseSymbol) + 6)

optionType := str.substring(currentSymbol, str.length(baseSymbol) + 6, str.length(baseSymbol) + 7)

strikePrice := str.substring(currentSymbol, str.length(baseSymbol) + 7, str.length(currentSymbol))

baseSymbol: Extracts the letters representing the stock symbol (e.g., TSLA).

expirationDate: Extracts the expiration date in the form of a 6-digit number (e.g., 250131).

optionType: Extracts the option type (C for Call, P for Put).

strikePrice: Extracts the strike price, which is the value after the option type (e.g., 400.0).

[/list>

5. Fetching the Base Symbol Price

baseSymbolClose = request.security(baseSymbol, "1", close)

This line uses the request.security() function to get the most recent close price of the base symbol (e.g., TSLA) on a 1-minute chart.

6. Converting the Strike Price to a Float

strikePriceFloat = na(strikePrice) ? na : str.tonumber(strikePrice)

Converts the strike price string to a numerical value (float). If the strike price is not available (i.e., na), it will not proceed with calculations.

7. Price Difference Calculation

priceDifference = baseSymbolClose - strikePriceFloat

This calculates the difference between the base symbol's close price and the strike price. For a Call option, this represents how much the stock price is above or below the strike price.

8. Adjusting for Put Options

if optionType == "P"

priceDifference := strikePriceFloat - baseSymbolClose

If the option is a Put, the price difference is reversed because a Put option becomes valuable when the stock price is below the strike price.

9. Plotting the Price Difference

priceDiffPlot = plot(priceDifference, title="Price Difference (Strike - Base)", color=color.blue, linewidth=2, style=plot.style_line, offset=0)

This line plots the calculated price difference as a blue line.

10. Zero Line Plot

zeroLinePlot = plot(0, "Zero Midline", color=color.white, linewidth=1, style=plot.style_line, offset=0)

This plots a white line at the zero level. This helps visually separate when the price difference is positive or negative.

11. Filling the Area Between the Price Difference and Zero Line

fill(priceDiffPlot, zeroLinePlot, color=color.new(priceDifference > 0 ? color.green : color.red, 70))

This fills the area between the price difference plot and the zero line:

Green if the price difference is positive (indicating the option is In the Money for Calls or Out of the Money for Puts).

Red if the price difference is negative (indicating the option is Out of the Money for Calls or In the Money for Puts).

Final Thoughts

This script is useful for traders and options investors who want to track the status of an option relative to the current price of the underlying asset. The green and red fill colors provide an immediate visual cue for whether the option is ITM or OTM. By applying this indicator on TradingView, users can easily see whether a particular option is valuable (ITM) or worthless (OTM) based on the current market price of the underlying asset. This makes it a valuable tool for quick decision-making in options trading.

Venta's DikFat Spread Visualizer & Dynamic Options Chain

**Venta's DikFat Spread Visualizer and Options Chain Strike Scanner** is a powerful trading tool designed to give users an immediate view of the nearest options strikes relative to the current price of the underlying asset. This script dynamically displays a selected number of call and put options strikes from the **options chain**, visualizing them directly on the chart for better decision-making.

By default, the script shows options strikes for the current chart’s price, but users have the flexibility to extend the view to include strikes on the opposite side of the market. The available options allow you to show either 3, 6, or 9 strikes on either side of the current price level.

This tool is essential for options traders who want to track strike prices in relation to the underlying asset's price movements. It provides key visual clues such as strike price distributions, volatility, and potential areas of market basing—all in a customizable and user-friendly interface.

---

█ CONCEPTS

This script pulls real-time **options strikes** directly from the **options chain**, providing traders with the ability to see call and put strikes as dynamic price markers on their chart. The concept revolves around understanding the proximity and distribution of strikes based on the current price and market conditions.

Key Features

**Dynamic Options Strike Display**: The script automatically identifies and displays the options strikes closest to the current market price of the underlying asset.

**Customizable Strike Range**: Choose between 3, 6, or 9 strikes on either side of the current price, giving flexibility in visualizing different strike ranges.

**Current Chart Focused by Default**: When added to the chart, the script focuses on the strikes closest to the current price. However, users can opt to include strikes on the opposite side of the market for a broader view.

**Instant Market Context**: The displayed

strikes offer a snapshot of the options market and how the current price relates to potential option expiration levels, helping traders understand key zones.

**Visual Clues on Spreads & Volatility**: This script not only displays the strikes but also provides instant visual clues that reflect the volatility and spread of the options market.

---

█ HOW IT WORKS

The script operates by accessing the **options chain** for the underlying asset, identifying the nearest call and put strikes, and plotting them as visual markers on the chart. This real-time strike data is dynamic, adjusting automatically as the market price moves.

Strike Calculation

The script uses the current price of the underlying asset as a base point and calculates the nearby **options strikes** from the **options chain**.

Depending on the user's settings, the script will plot up to 9 strikes on either side of the price level.

This calculation is performed using live market data, making sure the plotted strikes always reflect the most current market conditions.

Visual Clues

**Spreads**: The space between the plotted call and put options strikes provides immediate insights into the current bid/ask spreads. If the spread between strike prices is wide, it suggests increased volatility or a higher level of uncertainty in the market. Conversely, narrow spreads often indicate market stability or a lack of price movement.

**Market Basing**: When options strikes form a concentrated group near a certain price level, it can indicate that the market is building up or basing at a key level. This might signal the potential for a breakout or a reversal.

**Volatility Insights**: Wider gaps between strikes, particularly on the call side versus the put side (or vice versa), can indicate an imbalance in options trading activity, often a reflection of higher volatility expectations. This visual clue can help traders assess when the market is pricing in significant movements.

Customization and User Settings

**Number of Strikes**: The number of options strikes shown is fully customizable, allowing users to display 3, 6, or 9 strikes on either side.

**Show Opposite Strikes**: By default, the script shows strikes on the current side of the market, but users can enable the option to show strikes on the opposite side to gain a more complete view of the market's options landscape.

**Strike Colors & Width**: Customize the visual appearance of the plotted strikes by adjusting the color and line width for better clarity and chart aesthetics.

---

█ POTENTIAL USE CASES

This indicator is especially valuable for **options traders**, **market analysts**, and anyone interested in gaining insights into the underlying options market. Here are some of the key use cases:

**Options Traders**: Quickly identify the nearest strike prices and understand the risk/reward potential for options positions. The ability to customize the number of strikes shown allows traders to focus on the most relevant price levels.

**Volatility Monitoring**: Use the visual clues from the spread between strike prices to assess the level of volatility in the options market. A wider spread suggests that options traders are expecting more significant price moves, while a narrow spread indicates less expected movement.

**Support and Resistance Identification**: The clustering of strike prices on one side of the market can indicate a potential support or resistance level. By monitoring these levels, traders can get a sense of where the market may reverse or consolidate.

**Market Sentiment Analysis**: A large concentration of call strikes above the current price level, or put strikes below, can be an indication of market sentiment, such as whether traders are generally bullish or bearish.

**Risk Management**: By tracking nearby options strikes, traders can adjust their strategies to minimize risk, especially when market price levels approach significant strike points.

---

█ FEATURES

**Real-Time Data**: The script pulls data from the **options chain**, ensuring that the plotted strikes are always up-to-date with the current market price.

**User-Friendly Interface**: Clear and customizable inputs allow users to easily adjust the number of strikes displayed and control visual settings such as colors and line widths.

**Visual Strike Indicators**: Instantly spot volatility, market basing, and spread imbalances through visual clues from the plotted strikes, enhancing your market analysis.

---

█ LIMITATIONS

**Accuracy Depends on Market Data**: This indicator relies on the available **options chain** data. While the data is updated in real-time, its accuracy may depend on the liquidity and availability of options contracts in the market.

**Not Suitable for Non-Options Traders**: If you don’t trade options, the relevance of this indicator may be limited as it is designed specifically to provide insight into the options market.

**Data Delays**: In fast-moving markets, there may be a slight delay in the updating of strike prices, depending on the data feed.

---

█ HOW TO USE

**Load the Script**: Add the **Venta's DikFat Spread Visualizer and Options Chain Strike Scanner** script to your TradingView chart.

**Adjust Settings**: Use the input options to select the number of strikes you want to display (3, 6, or 9). You can also choose whether to display only the current chart’s strikes or include strikes from the opposite side.

**Interpret the Strikes**: Look at the plotted strikes to gain insights into where the market is currently pricing options and where major strike prices are located. Pay attention to the spreads, concentrations, and volatility signals.

**Monitor the Market**: As the market moves, watch how the strikes shift and cluster, providing you with real-time information about market sentiment and potential volatility.

---

█ THANKS

We would like to extend our gratitude to the PineCoders community for their ongoing support and contributions to the TradingView Pine Script ecosystem. Special thanks to The Options Team.

Enhanced Spread MonitorThis indicator helps you monitor market spreads and identify potential trading opportunities by analyzing spread behavior, market liquidity, and volatility across multiple exchanges. It's particularly useful for crypto traders looking for market inefficiencies or arbitrage opportunities.

Visuals:

-Blue Line: The real-time spread, enhanced by market conditions

-Orange Line: A smoothed threshold that helps identify unusual spread levels

-Red Background: Appears when the spread exceeds the threshold, signaling a potential opportunity

Key Features:

Multi-Exchange Monitoring

-Can track up to 3 different exchanges/markets

-Option to view individual or aggregated spreads

-Useful for spotting arbitrage opportunities between venues

Enhanced Spread Detection

-Automatically amplifies the spread when liquidity is low

-Increases sensitivity during volatile periods

-Helps identify true trading costs beyond the simple bid-ask spread

How to Configure:

Symbol Settings

-Choose up to three markets to monitor

-Enable "Aggregate Multiple Symbols" to see a volume-weighted combined view

Market Impact Factor (Depth Settings)

-Default: 0.5

-Higher values (>1.0): More sensitive to low liquidity

-Lower values (<0.5): More conservative spread estimation

Volatility Settings

-Short-term Volatility: React to immediate market changes

-Long-term Volatility: Establish baseline market behavior

-Recommended: Keep long-term 3-5x larger than short-term

Threshold Settings

-Historical Lookback: How much history to consider (500 bars recommended)

-Threshold Smoothing: Stability of the threshold line (14 default)

-Std Dev Multiplier: How extreme spreads need to be for signals (2.0 default)

Trading Application:

-Watch for red background highlighting - these are potential opportunities

Consider trading when:

-Spread exceeds threshold significantly

-Multiple exchanges show similar patterns

-Market conditions suggest the spread is due to real inefficiencies

Be cautious when:

-High volatility is the main driver of spread increases

-Only one exchange shows unusual spread behavior

-Market depth is very low (might be hard to execute)

Risk Management:

-Large spreads during low liquidity might indicate difficult trading conditions

-Verify actual executable prices before trading

-Consider exchange fees and withdrawal costs for arbitrage

Previous Day High and Low by DRK TradingThe Previous Day High and Low Indicator is a simple yet powerful tool designed for traders who want to keep track of critical levels from the previous trading session. This indicator automatically marks the high and low of the previous day on your chart with dashed horizontal lines, making it easier to identify key support and resistance zones.

Features:

Horizontal Lines: Clearly marks the previous day's high and low levels.

Dynamic Updates: Automatically updates at the start of a new trading day.

Visual Clarity: Includes labels at the start of the day for quick reference.

Customizable: Works seamlessly across all timeframes and instruments.

Use Case:

Identify potential breakout and reversal zones.

Enhance intraday and swing trading strategies by focusing on key price levels.

Plan stop-loss and target levels based on historical price movements.

This indicator is perfect for price action traders, intraday scalpers, and swing traders who rely on past price behavior to make informed decisions.