BTC_Hull Suite StrategyOverview

BTC_Hull Suite Strategy is a trend-following system designed to keep drawdowns modest while staying exposed during genuine uptrends. It uses the Hull Moving Average (HMA) for fast, low-lag trend turns, a long-term SMA filter to avoid chop, and a percentage trailing stop to protect gains.

🔧 What the strategy includes

- Hull Moving Average (HMA) with configurable length (default 55)

- SMA filter (default 130) to trade only with higher-timeframe bias

- Trailing stop in percent (default 5%) based on the running peak of close

- Execution model: signals are evaluated on the previous bar and entries are placed at the next bar’s open (TradingView default)

📈 How it works:

✅ Entry (Long):

Detects a bullish Hull turn by comparing the current HMA to its value 3 bars ago:

h > h3 and h <= h3 → HMA just turned up on the prior bar

The SMA filter must confirm: close > sma

If both are true (and within the date window), a long is opened next bar at the open

❌ Exit:

Hull turn down: h < h3 and h >= h3 , or

Trailing stop: price closes below peak * (1 – trailingPct)

Either condition closes the position at the current bar’s close

Notes:

pyramiding = 1 → allows one add-on (maximum two concurrent long positions)

Position sizing defaults to 20% of equity per entry (adjustable in Properties)

Who is this for?

This strategy is tailored for Bitcoin traders (spot or perpetuals) who want a rules-based, low-lag trend system with built-in drawdown protection.

It works best on Daily or 4H charts, but parameters can be adapted for other timeframes.

⚠️ Disclaimer

This strategy is provided for educational and research purposes only.

It is not financial advice. Markets are risky — always test on your own data, include realistic fees/slippage, and forward-test before using real capital.

Penunjuk dan strategi

OPTIMAL super trend tripple confirm for leverage. Ai implemented for higher r:r still a work in progresss

Trend MasterOverview

The Strategy is a trend-following trading system designed for forex, stocks, or other markets on TradingView. It uses pivot points to identify support and resistance levels, combined with a 200-period Exponential Moving Average (EMA) to filter trades. The strategy enters long or short positions based on trend reversals during specific trading sessions (London or New York). It incorporates robust risk management, including position sizing based on risk percentage or fixed amount, trailing stop-losses, breakeven moves, and weekly/monthly profit/loss limits to prevent overtrading.

This script is ideal for traders who want a semi-automated approach with visual aids like colored session backgrounds, support/resistance lines, and a performance dashboard. It supports backtesting from a custom start date and can limit trades to one per session for discipline. Alerts are built-in for entries, exits, and stop-loss adjustments, making it compatible with automated trading bots.

Key Benefits:

Trend Reversal Detection: Spots higher highs/lows and lower highs/lows to confirm trend changes.

Session Filtering: Trades only during high-liquidity sessions to avoid choppy markets.

Risk Control: Automatically calculates position sizes to risk only a set percentage or dollar amount per trade.

Performance Tracking: Displays a table of weekly or monthly P&L (profit and loss) with color-coded heatmaps for easy review.

Customizable: Adjust trade direction, risk levels, take-profit ratios, and more via inputs.

The strategy uses a 1:1.2 risk-reward ratio by default but can be tweaked.

How It Works

Trend Identification:

The script calculates pivot highs and lows using left (4) and right (2) bars to detect swing points.

It identifies patterns like Higher Highs (HH), Higher Lows (HL), Lower Highs (LH), and Lower Lows (LL) to determine the trend direction (uptrend if above resistance, downtrend if below support).

Support (green dotted lines) and resistance (red dotted lines) are drawn dynamically and update on trend changes.

Bars are colored blue (uptrend) or black (downtrend) for visual clarity.

Entry Signals:

Long Entry: Price closes above the 200 EMA, trend shifts from down to up (e.g., breaking resistance), during an active session (London or NY), and no trade has been taken that session (if enabled).

Short Entry: Price closes below the 200 EMA, trend shifts from up to down (e.g., breaking support), during an active session, and no prior trade that session.

Trades can be restricted to "Long Only," "Short Only," or "Both."

Entries are filtered by a start date (e.g., from January 2022) and optional month-specific testing.

Position Sizing and Risk:

Risk per trade: Either a fixed dollar amount (e.g., $500) or percentage of equity (e.g., 1%).

Quantity is calculated as: Risk Amount / (Entry Price - Stop-Loss Price).

This ensures you never risk more than intended, regardless of market volatility.

Stop-Loss (SL) and Take-Profit (TP):

SL for Longs: Set below the recent support level, adjustable by a "reduce value" (e.g., tighten by 0-90%) and gap (e.g., add a buffer).

SL for Shorts: Set above the recent resistance level, with similar adjustments.

TP: Based on risk-reward ratio (default 1.2:1), so if SL is 100 pips away, TP is 120 pips in profit.

Visual boxes show SL (red) and TP (green) on the chart for the next 4 bars after entry.

Trade Management:

Trailing SL: Automatically moves SL to the new support (longs) or resistance (shorts) if it tightens the stop without increasing risk.

Breakeven Move: If enabled, SL moves to entry price once profit reaches a set ratio of initial risk (default 1:1). For example, if risk was 1%, SL moves to breakeven at 1% profit.

One Trade Per Session: Prevents multiple entries in the same London or NY session to avoid overtrading.

Sessions include optional weekend inclusion and are highlighted (blue for London, green for NY).

Risk Limits (Weekly/Monthly):

Monitors P&L for the current week or month.

Stops trading if losses hit a limit (e.g., -3%) or profits reach a target (e.g., +7%).

Resets at the start of each new week/month.

Alerts notify when limits are hit.

Exits:

Trades exit at TP, SL, or manually via alerts.

No time-based exits; relies on price action.

Performance Dashboard:

A customizable table (position, size, colors) shows P&L percentages for each week/month in a grid.

Rows = Years, Columns = Weeks (1-52) or Months (1-12).

Color scaling: Green for profits (darker for bigger wins), red for losses (darker for bigger losses).

Yearly totals in the last column.

Helps visualize strategy performance over time without manual calculations.

Input Parameters Explained

Here's a breakdown of the main inputs for easy customization:

Trade Direction: "Both" (default), "Long Only," or "Short Only" – Controls allowed trade types.

Test Only Selected Month: If true, backtests only the specified month from the start year.

Start Year/Month: Sets the backtest start date (default: Jan 2022).

Include Weekends: If true, sessions can include weekends (rarely useful for forex).

Only One Trade Per Session: Limits to one entry per London/NY session (default: true).

Risk Management Time Frame: "Weekly" or "Monthly" – For P&L limits.

Enable Limits: Toggle weekly/monthly stop trading on loss/profit thresholds.

Loss Limit (%)/Profit Target (%): Stops trading if P&L hits these (e.g., -3% loss or +7% profit).

London/New York Session: Enable/disable, with time ranges (e.g., London: 0800-1300 UTC).

Left/Right Bars: For pivot detection (default: 4 left, 2 right) – Higher values smooth signals.

Support/Resistance: Toggle lines, colors, style, width.

Change Bar Color: Colors bars based on trend.

TP RR: Take-profit risk-reward (default: 1.2).

Stoploss Reduce Value: Tightens SL (negative values widen it, 0-0.9 range).

Stoploss Gap: Adds a buffer to SL (e.g., 0.1% away from support).

Move to Breakeven: Enables SL move to entry at a profit ratio (default: true, 1:1).

Use Risk Amount $: If true, risks fixed $ (e.g., 500); else, % of equity (default: 1%).

EMA 3: The slow EMA period (default: 200) for trend filter.

Performance Display: Toggle table, location (e.g., Bottom Right), size, colors, scaling for heatmaps.

Setup and Usage Tips

Add to Chart: Copy the script into TradingView's Pine Editor, compile, and add to your chart.

Backtesting: Use the Strategy Tester tab. Adjust inputs and test on historical data.

Live Trading: Connect alerts to a broker or bot (e.g., via webhook). The script sends JSON-formatted alerts for entry, exit, SL moves, and limits.

Best Markets: Works well on crypto pairs like SOLUSD or RUNEUSD on 4H timeframes.

Risk Warning: This is not financial advice. Always use demo accounts first. Past performance doesn't guarantee future results. Commission is set to 0.05% by default – adjust for your broker.

Customization: Experiment with EMA length or RR ratio for your style.

J12Matic Builder by galgoomA flexible Renko/tick strategy that lets you choose between two entry engines (Multi-Source 3-way or QBand+Moneyball), with a unified trailing/TP exit engine, NY-time trading windows with auto-flatten, daily profit/loss and trade-count limits (HALT mode), and clean webhook routing using {{strategy.order.alert_message}}.

Highlights

Two entry engines

Multi-Source (3): up to three long/short sources with Single / Dual / Triple logic and optional lookback.

QBand + Moneyball: Gate → Trigger workflow with timing windows, OR/AND trigger modes, per-window caps, optional same-bar fire.

Unified exit engine: Trailing by Bricks or Ticks, plus optional static TP/SL.

Session control (NY time): Evening / Overnight / NY Session windows; auto-flatten at end of any enabled window.

Day controls: Profit/Loss (USD) and Trade-count limits. When hit, strategy HALTS new entries, shows an on-chart label/background.

Alert routing designed for webhooks: Every order sets alert_message= so you can run alerts with:

Condition: this strategy

Notify on: Order fills only

Message: {{strategy.order.alert_message}}

Default JSONs or Custom payloads: If a Custom field is blank, a sensible default JSON is sent. Fill a field to override.

How to set up alerts (the 15-second version)

Create a TradingView alert with this strategy as Condition.

Notify on: Order fills only.

Message: {{strategy.order.alert_message}} (exactly).

If you want your own payloads, paste them into Inputs → 08) Custom Alert Payloads.

Leave blank → the strategy sends a default JSON.

Fill in → your text is sent as-is.

Note: Anything you type into the alert dialog’s Message box is ignored except the {{strategy.order.alert_message}} token, which forwards the payload supplied by the strategy at order time.

Publishing notes / best practices

Renko users: Make sure “Renko Brick Size” in Inputs matches your chart’s brick size exactly.

Ticks vs Bricks: Exit distances switch instantly when you toggle Exit Units.

Same-bar flips: If enabled, a new opposite signal will first close the open trade (with its exit payload), then enter the new side.

HALT mode: When day profit/loss limit or trade-count limit triggers, new entries are blocked for the rest of the session day. You’ll see a label and a soft background tint.

Session end flatten: Auto-closes positions at window ends; these exits use the “End of Session Window Exit” payload.

Bar magnifier: Strategy is configured for on-close execution; you can enable Bar Magnifier in Properties if needed.

Default JSONs (used when a Custom field is empty)

Open: {"event":"open","side":"long|short","symbol":""}

Close: {"event":"close","side":"long|short|flat","reason":"tp|sl|flip|session|limit_profit|limit_loss","symbol":""}

You can paste any text/JSON into the Custom fields; it will be forwarded as-is when that event occurs.

Input sections — user guide

01) Entries & Signals

Entry Logic: Choose Multi-Source (3) or QBand + Moneyball (pick one).

Enable Long/Short Signals: Master on/off switches for entering long/short.

Flip on opposite signal: If enabled, a new opposite signal will close the current position first, then open the other side.

Signal Logic (Multi-Source):

Single: any 1 of the 3 sources > 0

Dual: Source1 AND Source2 > 0

Triple (default): 1 AND 2 AND 3 > 0

Long/Short Signal Sources 1–3: Provide up to three series (often indicators). A positive value (> 0) is treated as a “pulse”.

Use Lookback: Keeps a source “true” for N bars after it pulses (helps catch late triggers).

Long/Short Lookback (bars): How many bars to remember that pulse.

01b) QBands + Moneyball (Gate -> Trigger)

Allow same-bar Gate->Trigger: If ON, a trigger can fire on the same bar as the gate pulse.

Trigger must fire within N bars after Gate: Size of the gate window (in bars).

Max signals per window (0 = unlimited): Cap the number of entries allowed while a gate window is open.

Buy/Sell Source 1 – Gate: Gate pulse sources that open the buy/sell window (often a regime/zone, e.g., QBands bull/bear).

Trigger Pulse Mode (Buy/Sell): How to detect a trigger pulse from the trigger sources (Change / Appear / Rise>0 / Fall<0).

Trigger A/B sources + Extend Bars: Primary/secondary triggers plus optional extension to persist their pulse for N bars.

Trigger Mode: Pick S2 only, S3 only, S2 OR S3, or S2 AND S3. AND mode remembers both pulses inside the window before firing.

02) Exit Units (Trailing/TP)

Exit Units: Choose Bricks (Renko) or Ticks. All distances below switch accordingly.

03) Tick-based Trailing / Stops (active when Exit Units = Ticks)

Initial SL (ticks): Starting stop distance from entry.

Start Trailing After (ticks): Start trailing once price moves this far in your favor.

Trailing Distance (ticks): Offset of the trailing stop from peak/trough once trailing begins.

Take Profit (ticks): Optional static TP distance.

Stop Loss (ticks): Optional static SL distance (overrides trailing if enabled).

04) Brick-based Trailing / Stops (active when Exit Units = Bricks)

Renko Brick Size: Must match your chart’s brick size.

Initial SL / Start Trailing After / Trailing Distance (bricks): Same definitions as tick mode, measured in bricks.

Take Profit / Stop Loss (bricks): Optional static distances.

05) TP / SL Switch

Enable Static Take Profit: If ON, closes the trade at the fixed TP distance.

Enable Static Stop Loss (Overrides Trailing): If ON, trailing is disabled and a fixed SL is used.

06) Trading Windows (NY time)

Use Trading Windows: Master toggle for all windows.

Evening / Overnight / NY Session: Define each session in NY time.

Flatten at End of : Auto-close any open position when a window ends (sends the Session Exit payload).

07) Day Controls & Limits

Enable Profit Limits / Profit Limit (Dollars): When daily net PnL ≥ limit → auto-flatten and HALT.

Enable Loss Limits / Loss Limit (Dollars): When daily net PnL ≤ −limit → auto-flatten and HALT.

Enable Trade Count Limits / Number of Trades Allowed: After N entries, HALT new entries (does not auto-flatten).

On-chart HUD: A label and soft background tint appear when HALTED; a compact status table shows Day PnL, trade count, and mode.

08) Custom Alert Payloads (used as strategy.order.alert_message)

Long/Short Entry: Payload sent on entries (if blank, a default open JSON is sent).

Regular Long/Short Exit: Payload sent on closes from SL/TP/flip (if blank, a default close JSON is sent).

End of Session Window Exit: Payload sent when any enabled window ends and positions are flattened.

Profit/Loss/Trade Limit Close: Payload sent when daily profit/loss limit causes auto-flatten.

Tip: Any tokens you include here are forwarded “as is”. If your downstream expects variables, do the substitution on the receiver side.

Known limitations

No bracket orders from Pine: This strategy doesn’t create OCO/attached brackets on the broker; it simulates exits with strategy logic and forwards your payloads for external automation.

alert_message is per order only: Alerts fire on order events. General status pings aren’t sent unless you wire a separate indicator/alert.

Renko specifics: Backtests on synthetic Renko can differ from live execution. Always forward-test on your instrument and settings.

Quick checklist before you publish

✅ Brick size in Inputs matches your Renko chart

✅ Exit Units set to Bricks or Ticks as you intend

✅ Day limits/Windows toggled as you want

✅ Custom payloads filled (or leave blank to use defaults)

✅ Your alert uses Order fills only + {{strategy.order.alert_message}}

fero.Laplace + MA TP/SL Strategy (10m)//@version=5Labne is a good technique for generating logic or theory.

Optimised XAU/USD (Gold, IC Markets, 30m)The Illyad Strategy 1.0 optimised for XAU/USD (Gold) on the 30-minute timeframe (IC Markets feed).

📊 Backtest Results (Jan 2024 – Aug 2025):

✅ Total P&L: +30,143.28 USD (+30.14%)

📉 Max Drawdown: 3.60% (3,945.84 USD)

🔁 Total Trades: 57

📈 Win Rate: 42.11% (24/57 trades)

⚖️ Profit Factor: 1.91

This setup shows steady performance and low drawdown on Gold — ideal for traders wanting to capture volatility while maintaining consistency.

🔧 Optimisation Notes:

Works best on the 30m timeframe.

Each instrument (forex, indices, commodities, stocks) has unique behaviour.

To maximise results, always optimise the parameters per symbol — e.g., Gold requires a different configuration than GBP/USD or NASDAQ.

💡 Best Use Cases:

Prop firm challenges & scaling funded accounts.

Long-term compounding with low risk.

Automated execution via TradingView alerts → MT5 for hands-free trading.

⚠️ Disclaimer:

This strategy is for educational purposes only. Past results do not guarantee future performance. Always backtest and forward-test before going live.

📲 Next Steps:

This example demonstrates the Gold (XAU/USD) optimisation. The Illyad Strategy can be tuned for any forex pair, index, or commodity with proper optimisation.

👉 Visit my profile for full automation solutions.

Optimised GBP/USD (IC Markets, 30m)This is the Illyad Strategy 1.0 optimised for GBP/USD on the 30-minute timeframe (IC Markets feed).

📊 Backtest Results (Jan 2024 – Aug 2025):

✅ Total P&L: +19,501.97 USD (+19.50%)

📉 Max Drawdown: 3.57% (3,607.64 USD)

🔁 Total Trades: 37

📈 Win Rate: 51.35% (19/37 trades)

⚖️ Profit Factor: 2.08

This version shows steady profitability with controlled drawdown, making it highly effective for prop firm evaluations and scaling accounts.

🔧 Optimisation Notes:

Works best on the 30-minute timeframe.

Each symbol behaves differently — always optimise the algo per instrument (e.g. GBP/USD vs EUR/GBP vs Gold).

Parameters such as moving averages, risk, and SL/TP ratios can be tuned to maximise performance.

💡 Best Use Cases:

Prop firm challenges (FTMO, AquaFunded, MyForexFunds, etc.).

Scaling funded capital by trading multiple accounts simultaneously.

Full automation via TradingView alerts → MT5 integration.

⚠️ Disclaimer:

This script is for educational purposes only. Past results do not guarantee future performance. Always backtest and forward-test on demo before going live.

📲 Next Steps:

This setup demonstrates the GBP/USD optimisation. The Illyad Strategy can be adjusted to perform across any forex pair, index, or stock with proper optimisation.

👉 Check my profile for full automation solutions.

Optimised GBP/CAD (IC Markets, 30m) - Automated TradingHere’s the Illyad Strategy 1.0 optimised for GBP/CAD on the 30-minute timeframe (IC Markets feed).

📊 Backtest Results (Jan 2024 – Aug 2025):

✅ Total P&L: +28,529.35 CAD (+28.53%)

📉 Max Drawdown: 3.61% (3,822.27 CAD)

🔁 Total Trades: 38

📈 Win Rate: 50.00% (19/38 trades)

⚖️ Profit Factor: 2.49

This setup shows strong performance with low drawdown, making it well-suited for prop firm trading and long-term portfolio compounding.

🔧 Optimisation Notes:

Works best on the 30-minute timeframe.

Each symbol has unique volatility and structure. To maximise results, you must optimise the algo per symbol (e.g., GBP/CAD vs EUR/USD vs NASDAQ).

Parameters such as moving averages, signal intensity, and SL/TP levels should be tuned to the instrument.

💡 Best Use Cases:

Prop firm challenges (FTMO, AquaFunded, MyForexFunds alternatives).

Running across multiple accounts simultaneously for compounding.

Automated execution via TradingView alerts → MT5 integration.

⚠️ Disclaimer:

This script is provided for educational purposes only. Past results do not guarantee future performance. Always backtest and forward-test on demo before live trading.

📲 Next Steps:

This version demonstrates the GBP/CAD optimisation. The Illyad Strategy can be tuned to work on any symbol (forex, indices, or stocks).

👉 Visit my profile for full automation solutions (TradingView → MT5)

Optimised EURGBP (IC Markets, 30m)Illyad Strategy 1.0 – Optimised EURGBP (IC Markets, 30m)

Description:

This is the Illyad Strategy 1.0 optimised for EURGBP on the 30-minute timeframe (IC Markets feed).

📊 Results (Jan 2024 – Aug 2025):

✅ Total P&L: +£31,032.15 (+31.03%)

📉 Max Drawdown: 2.86% (£3,576.85)

🔁 Total Trades: 39

📈 Win Rate: 58.97%

⚖️ Profit Factor: 2.92

This strategy focuses on controlled drawdown + consistent growth, making it ideal for prop trading challenges and long-term account compounding.

🔧 Optimisation:

Works best on the 30m timeframe.

Each symbol behaves differently — for maximum performance, you should optimise the parameters (MAs, SL/TP, intensity) to the instrument you want to trade.

Example: The EURGBP setup shown here differs from what you’d use on NASDAQ, XAUUSD, or stocks like Tesla.

💡 Best Use Cases:

Passing and scaling prop firm accounts (FTMO, AquaFunded, etc.).

Automated alerts → MT5 integration (hands-free trading).

Consistent, rule-based trading without emotion.

⚠️ Disclaimer:

This script is for educational purposes only. Past results don’t guarantee future performance. Always backtest and forward-test on demo before live trading.

📲 Next Steps:

This version shows the EURGBP optimisation. If you want to run it on other pairs, indices, or stocks → simply optimise parameters for that symbol.

👉 For full automation (TradingView → MT5 execution), check my profile for details.

Illyad Strategy 1.0 - Automate your alerts by connecting to MT5Illyad Strategy 1.0 – Automated Prop Trading System (30m Timeframe)

Description:

The Illyad Strategy 1.0 is a rule-based automated trading system designed for serious traders and prop-firm challenges.

🔑 Key Features:

Optimised to work best on the 30-minute timeframe.

Built-in money management to keep drawdown controlled.

Dynamic stop-loss / take-profit levels.

Works across forex, indices, and stocks.

Compatible with TradingView alerts → MT5 automation.

⚙️ Optimisation:

Each symbol has its own behaviour. For best results, you should optimise the parameters (moving averages, signal intensity, SL/TP ratios) on the symbol you want to trade. The algo adapts differently to EURUSD vs NASDAQ vs stocks like TSLA, so proper tuning is critical.

💡 Best Use Case:

Prop firm accounts (FTMO, MyForexFunds, AquaFunded, etc.).

Consistent returns without emotional decision-making.

Traders who want to scale multiple accounts at once.

⚠️ Disclaimer:

This script is for educational purposes. Past results do not guarantee future returns. Always backtest and forward test on demo before going live.

📲 Next Step:

This is the public version. If you’d like to connect it directly to MT5/MT4 for fully automated trading, visit my profile or contact me for details.

fero.karma algoUnderstand what stocks, currencies (forex), and cryptocurrencies are. Learn common terms like bull market, bear market, volatility, and liquidity.

Study Analysis: There are two main types of analysis:

THE BATATAH SAUCE BTC.PERP TRADING STRAT12hr hour is the sweet spot

great profit factor

decent risk management avg losing (back tested for 5 yrs and does alright till even 2018)trade 8.21% vs avg winning 174.87% (back tested for 5 yrs and does alright since even start2018)

Its alright on daily as well as 6hr but lower just gets more noisy

Breakout + Volume + HH/LL (Clean labels TP1-3)Breakout + Volume + HH/LL Strategy (Clean Labels)

This strategy combines breakout confirmation, volume strength, and market structure (Higher Highs / Lower Lows) to identify high-probability trade setups.

Breakout Filter: Uses a Donchian channel to detect price breakouts above resistance or below support.

Volume Confirmation: Requires volume to exceed the moving average of volume by a chosen multiplier, filtering out weak or false breakouts.

Market Structure: Long trades are only allowed if a Higher High (HH) has formed, and short trades only if a Lower Low (LL) has formed.

Trade Execution Rules:

For BUY trades: Entry at breakout, stop loss (SL) below the last pivot low, and three take profits (TP1–TP3) based on configurable risk-reward ratios.

For SELL trades: Entry at breakout, stop loss above the last pivot high, with TP1–TP3 levels set symmetrically below the entry.

Labels on Chart:

Each signal is marked with a clean label showing only:

Trade direction (BUY or SELL)

Entry price

Stop Loss

TP1, TP2, TP3

This makes the chart uncluttered while still providing all key trade information for execution or backtesting.

Energy Across TimePrivate Use-Only Version

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Sed euismod, lectus nec varius dictum, nibh arcu imperdiet augue, ac tristique odio nulla nec ligula. Vivamus ac odio nec lorem faucibus posuere. Proin sed sapien dignissim, laoreet velit vitae, vehicula justo. Curabitur et viverra lectus. Ut sit amet rhoncus ligula. Nullam nec posuere nisl. Morbi faucibus mattis sem, nec faucibus neque tristique vitae. Praesent malesuada nisl nec lectus congue, sit amet fringilla mauris vulputate. Ut quis felis vitae arcu varius ultrices non vel metus. Duis ac posuere nulla. Sed quis odio arcu. Etiam sodales eros libero, eget finibus elit bibendum nec. Cras ac justo sed justo facilisis suscipit. Nullam faucibus tortor vitae lorem eleifend, ut rhoncus lacus imperdiet.

Vestibulum ante ipsum primis in faucibus orci luctus et ultrices posuere cubilia curae; Integer sagittis mi ut leo efficitur, vel feugiat nibh suscipit. Morbi sed vulputate risus, eu volutpat massa. Vestibulum luctus, nisl non posuere vehicula, enim urna bibendum est, sit amet luctus libero sapien a massa. Nullam blandit nulla non massa pretium, nec fermentum turpis vestibulum. Pellentesque habitant morbi tristique senectus et netus et malesuada fames ac turpis egestas. Nam condimentum congue feugiat. Donec commodo, libero nec congue finibus, augue mi malesuada mi, sed suscipit erat sem ut orci. Phasellus dictum justo at ligula tincidunt, nec dictum libero scelerisque. Nulla et faucibus nulla, id aliquet magna. Fusce congue, justo in luctus iaculis, lectus dolor ultrices nunc, nec euismod lectus lorem ac lectus.

Pellentesque habitant morbi tristique senectus et netus et malesuada fames ac turpis egestas. Nam dictum sapien non mattis aliquet. Integer semper venenatis libero, sit amet posuere magna laoreet at. Aliquam erat volutpat. Aenean congue luctus felis, vel blandit velit posuere nec. Aenean feugiat, purus at vulputate posuere, ipsum nulla dignissim arcu, nec sollicitudin quam est sed purus. Aenean bibendum, ligula a luctus venenatis, erat nisl sagittis eros, id ultrices purus nibh ac nunc. Sed egestas sodales dui, vitae volutpat mauris facilisis vitae. Nam sit amet dolor ac lorem luctus luctus. Morbi iaculis fringilla bibendum. Mauris ut ullamcorper leo. Sed fringilla fermentum nunc, eget egestas orci porttitor a. Aenean sit amet mi ligula. Suspendisse sed efficitur odio. Quisque in turpis eget mauris ullamcorper faucibus. Sed euismod turpis ut arcu posuere tincidunt.

Simple SMA StrategySimple strategy to buy based on closing above SMA, and sell based on closing below SMA.

You can change the SMA value and your start date to customize the strategy for your initial entry date and SMA value. SMA is based on chart time frame.

SPX EMA 9/21 + VWAP Strategy1. Temporality: 2 minutes.

2. EMA 9 and EMA 21:

• Purchase Call: when EMA 9 crosses up EMA 21 and the price is > VWAP.

• Put : when EMA 9 crosses down EMA 21 and the price is < VWAP.

3. Stop and Take Profit:

• Stop: candle closure on the other side of the VWAP.

• TP: configurable in points (e.g. +10 pts, +20 pts) or up to the opposite crossing of EMAs.

• Long enters when EMA 9 crosses up 21 and the price is above VWAP.

• Short enters when the EMA 9 crosses down the 21 and the price is below VWAP.

• TP and SL in SPX points (configurable in inputs).

• You can run in 2 minutes on SPX.

EMA and BB Analysis for US100 V250829This TradingView strategy generates buy and sell signals based on exponential moving average (EMA) crossovers, limited by other factors such as Bollinger Bands, volume, and EMA distance.

It uses EMAs of 16, 24, 32, and 64 periods, as well as the angles of each of these EMAs.

Entry Conditions:

EMA Crossover Entry:

When EMA16 crosses EMA64 and the following conditions are met:

EMA16, EMA24, EMA32 are aligned — for a buy signal:

EMA16 > EMA24

EMA24 > EMA32

EMA32 > EMA48

(and the opposite for a sell signal)

EMA Angles:

The angles of the EMAs must also follow the same alignment.

Divergence Entry:

When the distance between EMAs 16, 24, 32, and 48 increases.

Entry Limitations:

Once an entry is detected, it is filtered by several conditions:

When the distance between the entry candle and EMA96 is more than two candles of the maximum size over three periods.

The stop loss is set as two candles of the maximum size over three periods. If this stop loss exceeds 6,000 points (adjustable parameter), the entry is invalid.

When the price is at the edge of the Bollinger Band with a 1200-period setting (equivalent to a 1-hour Bollinger Band).

When the Bollinger Band's middle line is descending and a buy signal is triggered (and vice versa).

When volume drops below a certain threshold.

When a sideways market movement is detected.

All these entry limitations are configurable parameters and can be enabled or disabled.

ORB FVG Strategy with telegram V6.1Summary

Intraday NY-session strategy with Opening-Range bias (09:30–10:00 NY), FVG entries (incl. optional HTF FVGs), momentum filters (LinReg slope & Williams %R), limit entries inside the zone, SL from FVG anchors, and TP via risk-reward. Includes session/trade caps, pending-order handling, auto-cancel at NY time, and optional Telegram webhook alerts.

Feature Overview

Opening Range & Bias: OR high/low built until 10:00 NY, then frozen. Bias from confirmed 5-minute candles (modes: Body Close, Complete Candle, Wick Only).

FVG Scanner: Bull/bear FVGs (choose wick or body gaps), min size, auto-extend, mitigation cleanup (touch or 50%).

HTF FVG (10 min): Optional – displayed after ≥ 2 consecutive FVGs; cleans up on touch/50%.

Entry/SL/TP: Entry at X% fill (+extra %) within the FVG; SL from FVG candle / FVG-1 / FVG-2 (smart) + buffer; TP via risk-reward.

Momentum Filters: LinReg slope (MLL) + Williams %R with threshold/slope filters (individually switchable).

Intrabar Mode (optional): Immediate Open/intrabar entry on touch (calc_on_every_tick=true) or classic bar-close confirmation (toggle).

Trade Management: Max trades/day, pending cap, auto-cancel at defined NY time, pause after first winner (optional).

Telegram: Programmatic alerts via alert() with Telegram-ready JSON payload.

Parameters (compact)

Group Parameter Purpose

Sessions Trading session, Opening range Trading/OR window (internal NY TZ)

Bias Body Close / Complete Candle / Wick Only Bias confirmation relative to OR

Liquidity LQ session, lookback days, cleanup points, show lines Intraday liquidity marks & cleanup

FVG Min size, wick/body, colors, extend, cleanup Detection/visualization & validity

HTF FVG (10 m) Toggle/Display/Colors Conservative HTF filter/POI

Entry Fill %, extra %, max pending, validity (bars), cancel time, intrabar switch Execution timing, order caps, auto-cancel

Stop Loss Source: Candle / -1 / -2 (smart), buffer (points) SL anchor from FVG history + safety offset

Take Profit Risk-Reward (R:R) Target calculation

Momentum LinReg length/min slope, W%R length/min slope, HUD Trend/momentum filters

Trade Mgmt Max trades/day, pause after win Daily cap / risk cooldown

Telegram Enabled, tester, interval, channel id Webhook output & test signals

Debug & Info Debug panel, rejection reasons On-chart status/diagnostics

Alerts / Telegram Webhook (Quick Setup)

Create an alert with Condition: “Any alert() function call”.

Webhook URL: api.telegram.org

Message: leave empty (the strategy provides JSON via alert() – includes chat_id, parse_mode, text).

Ensure your bot can post to the channel and the chat_id is valid.

Repainting & Backtesting

HTF series via lookahead_off on closed higher-TF candles; FVG detection on confirmed bars (barstate.isconfirmed).

Intrabar/Open entries allow earlier fills but typically cause differences between backtest and live (tick granularity/slippage, limit touch on bar OHLC).

For reproducibility, trade without intrabar (bar-close only).

Limitations

No full tick simulation; limit fills rely on bar OHLC.

Liquidity “cleanup” is rule-based (not an orderbook).

Telegram depends on correct webhook configuration.

Tips

Timeframes: M5 (intrabar)

Start with modest R:R (e.g., 1.5–2.0) and tune filters carefully.

Disclaimer

No financial advice. Past results do not guarantee future performance. Use responsibly and follow Public Library rules.

License / Credits

© 2025 Lean Trading (Lennart Pomreinke). License: MPL-2.0.

Changelog

V06.1: Intrabar switch (Open/intrabar vs bar-close), Telegram sanitizer & tester, HTF-FVG cleanup, refined pending/cancel logic, debug panel (status & rejections).

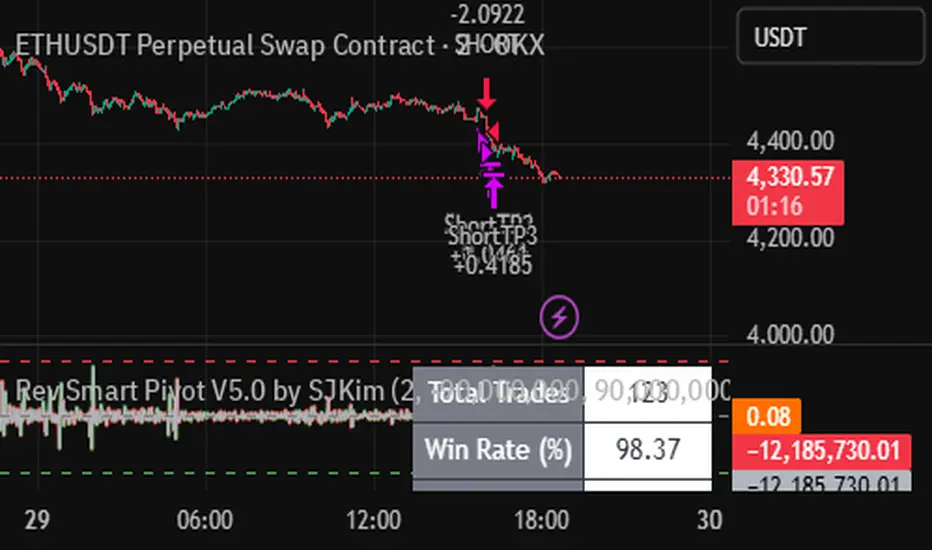

Std Smart Pivot V5.0 by SJKimStd Smart Pivot V5.0 by SJKim

Std Smart Pivot V5.0 by SJKim

Std Smart Pivot V5.0 by SJKim

Intraday Alpha Pro - ORB + Trend/MomentumOverview

This is a pure intraday trading strategy designed for active traders seeking to capitalize on short-term price movements using two complementary modules: Opening Range Breakout (ORB) and Trend/Momentum. The strategy operates strictly within a user-defined trading session, automatically flattening all positions at session end to avoid overnight carry. It employs a points-based exit system with a trailing stop that activates only after the target is reached, ensuring disciplined risk management. Optional Martingale position sizing is included for users who prefer aggressive scaling after losses.Key Features Pure Intraday, No Carry: Trades are confined to a user-defined session (default: 9:15 AM–3:25 PM, Monday–Sunday). All positions are closed at session end.

Non-Repainting: Entries are evaluated only on confirmed bar closes (barstate.isconfirmed), ensuring no lookahead or repainting.

Dual Signal Modules: Opening Range Breakout (ORB): Captures breakouts above/below the high/low of a user-defined opening range (default: 9:15 AM–9:30 AM).

Trend/Momentum: Combines EMA (9/21) crossovers, RSI filters, volume confirmation, and an optional 200-period MA trend filter for robust trend-following signals.

Points-Based Exits: Uses fixed stop-loss (slPoints, default 16 points) and take-profit (tpPoints, default 32 points) distances. Once the take-profit level is reached, a trailing stop (trailDistPts, default 10 points) activates, ratcheting monotonically to lock in gains.

Martingale Sizing (Optional): Allows position size increases after losses (up to maxQtyInput) with a reset option after wins.

Cooldown Period: Prevents immediate re-entries after exits using a configurable cooldown (cooldownBars).

Flexible Inputs: Toggle long/short entries, enable/disable ORB or Trend/Momentum modules, and customize all parameters (e.g., MA lengths, RSI thresholds, volume multiplier).

Visuals & Alerts: Plots ORB high/low lines and moving averages (9, 21, 200). Includes alerts for long/short entries and end-of-day flattening.

How It Works Session Management: Trades only within the specified tradeSes (default: 9:15 AM–3:25 PM). The ORB module uses a separate orbSes (default: 9:15 AM–9:30 AM) to calculate breakout levels. Positions are closed automatically at session end.

Entry Conditions: ORB: Long when price closes above the ORB high after the ORB session ends; short when price closes below the ORB low.

Trend/Momentum: Long on fast MA (default EMA 9) crossing above slow MA (default EMA 21), with RSI above rsiBuy (default 55), volume exceeding volMult (default 1.5x prior bar), and price above the 200-period MA (if enabled). Shorts use the inverse.

Exit Logic: Stop-loss is set at entry price ± slPoints.

Take-profit is monitored using a running high/low since entry. Once price moves tpPoints in profit, the stop trails at trailDistPts behind the current price, adjusting only in the favorable direction (never loosening).

Exits use strategy.exit with stop only (no limit orders).

Position Sizing: Default size is baseQtyInput (minimum 1 contract). With useMartingale enabled, size increases by martingaleFactor after a loss, capped at maxQtyInput. If resetOnWin is true, size resets to baseQtyInput after a winning trade.

Cooldown: After an exit, no new trades are allowed for cooldownBars to prevent overtrading.

Futures-Safe Volume: Volume filter accommodates markets with missing or zero volume data (e.g., futures), ensuring signals aren’t blocked unnecessarily.

Inputs Trading Session: tradeSes (e.g., "0915-1525:1234567") and orbSes (e.g., "0915-0930:1234567").

Toggles: enableLong, enableShort, useORB, useTrendMom, useTrendFilter (200-MA).

Trend/Momentum: maType (EMA/SMA), fastLen (9), slowLen (21), trendLen (200), rsiLen (14), rsiBuy (55), rsiSell (45), volMult (1.5).

Exits: slPoints (16), tpPoints (32), trailDistPts (10).

Martingale: useMartingale, baseQtyInput, maxQtyInput, martingaleFactor, resetOnWin.

Cooldown: cooldownBars (1).

Legacy (Ignored): tp1RR, tp2RR, tp3RR, tp1Pct, tp2Pct, tp3Pct, stepTrail for backward compatibility.

Usage Notes Best suited for liquid, intraday markets (e.g., futures like ES, NQ, or forex pairs).

Adjust slPoints, tpPoints, and trailDistPts to match instrument volatility.

Use useMartingale cautiously, as it increases risk after losses.

Ensure tradeSes and orbSes align with your market’s trading hours.

Alerts can be set for long/short entries and EOD flattening.

The strategy avoids lookahead and repainting, ensuring reliability in live trading.

Risk Warning

Trading involves significant risk. Backtest thoroughly and use appropriate risk management. The Martingale option can amplify losses if not carefully monitored. Past performance is not indicative of future results.

BOLL Omakase 2.0testing own {

"symbol": "{{ticker}}",

"price": {{close}},

"time": "{{time}}"

}{

"symbol": "{{ticker}}",

"price": {{close}},

"time": "{{time}}"

}{

"symbol": "{{ticker}}",

"price": {{close}},

"time": "{{time}}"

}{

"symbol": "{{ticker}}",

"price": {{close}},

"time": "{{time}}"

}

Nor Smart Pivot V5.0 by SJKimNor Smart Pivot V5.0 by SJKim.

Nor Smart Pivot V5.0 by SJKim.

Nor Smart Pivot V5.0 by SJKim.

Golden Cross + Support/Resistance + SL/TP + SignalsGolden Cross + Support/Resistance + SL/TP + Signals

Golden Cross + Support/Resistance + SL/TP + Signals