BasicVisibleChartBasic library for the visible range chart; with functions to allow plotting Fibs from body high/low as well as wick high/low

-Thanks to code from @PineCoders Visible Chart library (PineCoders/VisibleChart/4), which is a much more comprehensive library than this, but which does not include some functions that I find useful:

-Added the following exportable functions: highest/lowest body, highest/lowest close, highest/lowest open. These allow one to anchor fibs from bodies rather than wicks

-Added a Fib Box function in the example code

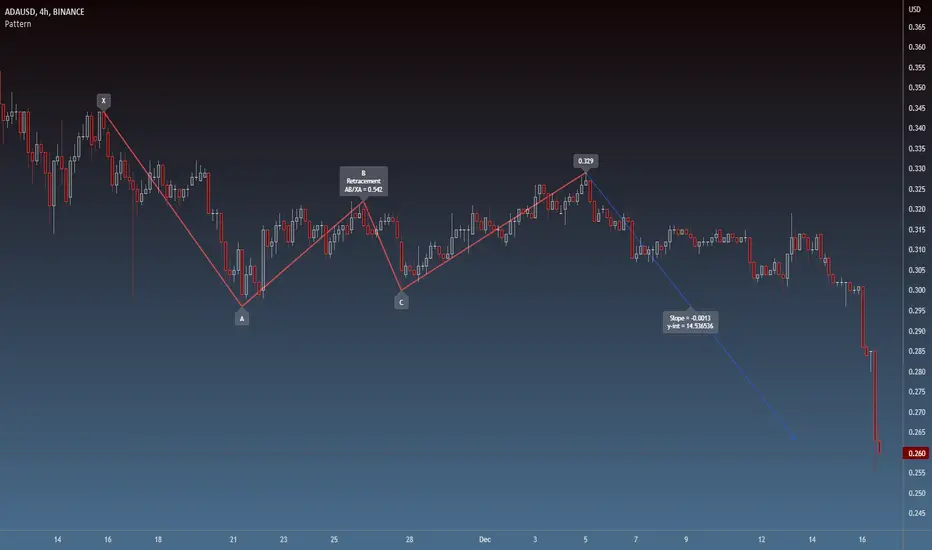

The above chart shows the example code plotting a Fib range drawn from bodies and a highlighted retracement zone (61.8 % - 78.6% )

~~All Exportable Functions~~

barIsVisible()

highestClose()

highestOpen()

highestBody()

lowestClose()

lowestOpen()

lowestBody()

high()

highBarTime()

low()

lowBarTime()

open()

close()

Penunjuk dan strategi

theme_presetsStyle Made Easy with 175 Reversable light/dark themes

Built on to of my theme engine, so any tools built with one

will work with the other.

getTheme(_input)

Get a theme by name. (see lib for copy/paste list)

Parameters:

_input : string Name of Theme to use.

apathy()

Theme preset -> "Apathy"

Returns: Theme object

apprentice()

Theme preset -> "Apprentice"

Returns: Theme object

ashes()

Theme preset -> "Ashes"

Returns: Theme object

atelier_cave()

Theme preset -> "Atelier Cave"

Returns: Theme object

atelier_dune()

Theme preset -> "Atelier Dune"

Returns: Theme object

atelier_estuary()

Theme preset -> "Atelier Estuary"

Returns: Theme object

atelier_forest()

Theme preset -> "Atelier Forest"

Returns: Theme object

atelier_heath()

Theme preset -> "Atelier Heath"

Returns: Theme object

atelier_lakeside()

Theme preset -> "Atelier Lakeside"

Returns: Theme object

atelier_plateau()

Theme preset -> "Atelier Plateau"

Returns: Theme object

atelier_savanna()

Theme preset -> "Atelier Savanna"

Returns: Theme object

atelier_seaside()

Theme preset -> "Atelier Seaside"

Returns: Theme object

atelier_sulphurpool()

Theme preset -> "Atelier Sulphurpool"

Returns: Theme object

atlas()

Theme preset -> "Atlas"

Returns: Theme object

ayu()

Theme preset -> "Ayu"

Returns: Theme object

ayu_mirage()

Theme preset -> "Ayu Mirage"

Returns: Theme object

bespin()

Theme preset -> "Bespin"

Returns: Theme object

black_metal()

Theme preset -> "Black Metal"

Returns: Theme object

black_metal_bathory()

Theme preset -> "Black Metal (bathory)"

Returns: Theme object

black_metal_burzum()

Theme preset -> "Black Metal (burzum)"

Returns: Theme object

black_metal_funeral()

Theme preset -> "Black Metal (dark Funeral)"

Returns: Theme object

black_metal_gorgoroth()

Theme preset -> "Black Metal (gorgoroth)"

Returns: Theme object

black_metal_immortal()

Theme preset -> "Black Metal (immortal)"

Returns: Theme object

black_metal_khold()

Theme preset -> "Black Metal (khold)"

Returns: Theme object

black_metal_marduk()

Theme preset -> "Black Metal (marduk)"

Returns: Theme object

black_metal_mayhem()

Theme preset -> "Black Metal (mayhem)"

Returns: Theme object

black_metal_nile()

Theme preset -> "Black Metal (nile)"

Returns: Theme object

black_metal_venom()

Theme preset -> "Black Metal (venom)"

Returns: Theme object

blue_forest()

Theme preset -> "Blue Forest"

Returns: Theme object

blueish()

Theme preset -> "Blueish"

Returns: Theme object

brewer()

Theme preset -> "Brewer"

Returns: Theme object

bright()

Theme preset -> "Bright"

Returns: Theme object

brogrammer()

Theme preset -> "Brogrammer"

Returns: Theme object

brush_trees()

Theme preset -> "Brush Trees"

Returns: Theme object

catppuccin()

Theme preset -> "Catppuccin"

Returns: Theme object

chalk()

Theme preset -> "Chalk"

Returns: Theme object

circus()

Theme preset -> "Circus"

Returns: Theme object

classic()

Theme preset -> "Classic"

Returns: Theme object

clrs()

Theme preset -> "Colors"

Returns: Theme object

codeschool()

Theme preset -> "Codeschool"

Returns: Theme object

cupcake()

Theme preset -> "Cupcake"

Returns: Theme object

cupertino()

Theme preset -> "Cupertino"

Returns: Theme object

da_one_black()

Theme preset -> "Da One Black"

Returns: Theme object

da_one_gray()

Theme preset -> "Da One Gray"

Returns: Theme object

da_one_ocean()

Theme preset -> "Da One Ocean"

Returns: Theme object

da_one_paper()

Theme preset -> "Da One Paper"

Returns: Theme object

da_one_sea()

Theme preset -> "Da One Sea"

Returns: Theme object

da_one_white()

Theme preset -> "Da One White"

Returns: Theme object

danqing()

Theme preset -> "Danqing"

Returns: Theme object

darcula()

Theme preset -> "Darcula"

Returns: Theme object

dark_violet()

Theme preset -> "Dark Violet"

Returns: Theme object

darkmoss()

Theme preset -> "Darkmoss"

Returns: Theme object

darktooth()

Theme preset -> "Darktooth"

Returns: Theme object

decaf()

Theme preset -> "Decaf"

Returns: Theme object

dirtysea()

Theme preset -> "Dirtysea"

Returns: Theme object

dracula()

Theme preset -> "Dracula"

Returns: Theme object

edge()

Theme preset -> "Edge"

Returns: Theme object

eighties()

Theme preset -> "Eighties"

Returns: Theme object

embers()

Theme preset -> "Embers"

Returns: Theme object

emil()

Theme preset -> "Emil"

Returns: Theme object

equilibrium()

Theme preset -> "Equilibrium"

Returns: Theme object

equilibrium_gray()

Theme preset -> "Equilibrium Gray"

Returns: Theme object

espresso()

Theme preset -> "Espresso"

Returns: Theme object

eva()

Theme preset -> "Eva"

Returns: Theme object

everforest()

Theme preset -> "Everforest"

Returns: Theme object

flat()

Theme preset -> "Flat"

Returns: Theme object

framer()

Theme preset -> "Framer"

Returns: Theme object

fruit_soda()

Theme preset -> "Fruit Soda"

Returns: Theme object

gigavolt()

Theme preset -> "Gigavolt"

Returns: Theme object

github()

Theme preset -> "Github"

Returns: Theme object

google()

Theme preset -> "Google"

Returns: Theme object

gotham()

Theme preset -> "Gotham"

Returns: Theme object

grayscale()

Theme preset -> "Grayscale"

Returns: Theme object

green_screen()

Theme preset -> "Green Screen"

Returns: Theme object

gruber()

Theme preset -> "Gruber"

Returns: Theme object

gruvbox_hard()

Theme preset -> "Gruvbox Dark, Hard"

Returns: Theme object

gruvbox_medium()

Theme preset -> "Gruvbox Dark, Medium"

Returns: Theme object

gruvbox_pale()

Theme preset -> "Gruvbox Dark, Pale"

Returns: Theme object

gruvbox_soft()

Theme preset -> "Gruvbox Dark, Soft"

Returns: Theme object

gruvbox_material_hard()

Theme preset -> "Gruvbox Material Dark, Hard"

Returns: Theme object

gruvbox_material_medium()

Theme preset -> "Gruvbox Material Dark, Medium"

Returns: Theme object

gruvbox_material_soft()

Theme preset -> "Gruvbox Material Dark, Soft"

Returns: Theme object

hardcore()

Theme preset -> "Hardcore"

Returns: Theme object

harmonic16()

Theme preset -> "Harmonic16"

Returns: Theme object

heetch()

Theme preset -> "Heetch"

Returns: Theme object

helios()

Theme preset -> "Helios"

Returns: Theme object

hopscotch()

Theme preset -> "Hopscotch"

Returns: Theme object

horizon()

Theme preset -> "Horizon"

Returns: Theme object

horizon_terminal()

Theme preset -> "Horizon Terminal"

Returns: Theme object

humanoid()

Theme preset -> "Humanoid"

Returns: Theme object

ia()

Theme preset -> "Ia"

Returns: Theme object

icy()

Theme preset -> "Icy"

Returns: Theme object

ir_black()

Theme preset -> "Ir Black"

Returns: Theme object

isotope()

Theme preset -> "Isotope"

Returns: Theme object

kanagawa()

Theme preset -> "Kanagawa"

Returns: Theme object

katy()

Theme preset -> "Katy"

Returns: Theme object

kimber()

Theme preset -> "Kimber"

Returns: Theme object

lime()

Theme preset -> "Lime"

Returns: Theme object

london_tube()

Theme preset -> "London Tube"

Returns: Theme object

macintosh()

Theme preset -> "Macintosh"

Returns: Theme object

marrakesh()

Theme preset -> "Marrakesh"

Returns: Theme object

materia()

Theme preset -> "Materia"

Returns: Theme object

material()

Theme preset -> "Material"

Returns: Theme object

materialdarker()

Theme preset -> "Material Darker"

Returns: Theme object

material_palenight()

Theme preset -> "Material Palenight"

Returns: Theme object

material_vivid()

Theme preset -> "Material Vivid"

Returns: Theme object

mellow_purple()

Theme preset -> "Mellow Purple"

Returns: Theme object

mocha()

Theme preset -> "Mocha"

Returns: Theme object

monokai()

Theme preset -> "Monokai"

Returns: Theme object

Nebula()

Theme preset -> "Nebula"

Returns: Theme object

nord()

Theme preset -> "Nord"

Returns: Theme object

nova()

Theme preset -> "Nova"

Returns: Theme object

ocean()

Theme preset -> "Ocean"

Returns: Theme object

oceanicnext()

Theme preset -> "Oceanicnext"

Returns: Theme object

onedark()

Theme preset -> "Onedark"

Returns: Theme object

outrun()

Theme preset -> "Outrun"

Returns: Theme object

pandora()

Theme preset -> "Pandora"

Returns: Theme object

papercolor()

Theme preset -> "Papercolor"

Returns: Theme object

paraiso()

Theme preset -> "Paraiso"

Returns: Theme object

pasque()

Theme preset -> "Pasque"

Returns: Theme object

phd()

Theme preset -> "Phd"

Returns: Theme object

pico()

Theme preset -> "Pico"

Returns: Theme object

pinky()

Theme preset -> "Pinky"

Returns: Theme object

pop()

Theme preset -> "Pop"

Returns: Theme object

porple()

Theme preset -> "Porple"

Returns: Theme object

primer()

Theme preset -> "Primer"

Returns: Theme object

purpledream()

Theme preset -> "Purpledream"

Returns: Theme object

qualia()

Theme preset -> "Qualia"

Returns: Theme object

railscasts()

Theme preset -> "Railscasts"

Returns: Theme object

rebecca()

Theme preset -> "Rebecca"

Returns: Theme object

rose_pine()

Theme preset -> "Rosé Pine"

Returns: Theme object

rose_pine_dawn()

Theme preset -> "Rosé Pine Dawn"

Returns: Theme object

rose_pine_moon()

Theme preset -> "Rosé Pine Moon"

Returns: Theme object

sagelight()

Theme preset -> "Sagelight"

Returns: Theme object

sakura()

Theme preset -> "Sakura"

Returns: Theme object

sandcastle()

Theme preset -> "Sandcastle"

Returns: Theme object

seti_ui()

Theme preset -> "Seti Ui"

Returns: Theme object

shades_of_purple()

Theme preset -> "Shades Of Purple"

Returns: Theme object

shadesmear()

Theme preset -> "Shadesmear"

Returns: Theme object

shapeshifter()

Theme preset -> "Shapeshifter"

Returns: Theme object

silk()

Theme preset -> "Silk"

Returns: Theme object

snazzy()

Theme preset -> "Snazzy"

Returns: Theme object

solar_flare()

Theme preset -> "Solar Flare"

Returns: Theme object

solarized()

Theme preset -> "Solarized"

Returns: Theme object

spaceduck()

Theme preset -> "Spaceduck"

Returns: Theme object

spacemacs()

Theme preset -> "Spacemacs"

Returns: Theme object

stella()

Theme preset -> "Stella"

Returns: Theme object

still_alive()

Theme preset -> "Still Alive"

Returns: Theme object

summercamp()

Theme preset -> "Summercamp"

Returns: Theme object

summerfruit()

Theme preset -> "Summerfruit"

Returns: Theme object

synth_midnight_terminal()

Theme preset -> "Synth Midnight Terminal"

Returns: Theme object

tango()

Theme preset -> "Tango"

Returns: Theme object

tender()

Theme preset -> "Tender"

Returns: Theme object

tokyo_city()

Theme preset -> "Tokyo City"

Returns: Theme object

tokyo_city_terminal()

Theme preset -> "Tokyo City Terminal"

Returns: Theme object

tokyo_night()

Theme preset -> "Tokyo Night"

Returns: Theme object

tokyo_night_storm()

Theme preset -> "Tokyo Night Storm"

Returns: Theme object

tokyo_night_terminal()

Theme preset -> "Tokyo Night Terminal"

Returns: Theme object

tokyo_night_terminal_storm()

Theme preset -> "Tokyo Night Terminal Storm"

Returns: Theme object

tokyodark()

Theme preset -> "Tokyodark"

Returns: Theme object

tokyodark_terminal()

Theme preset -> "Tokyodark Terminal"

Returns: Theme object

tomorrow()

Theme preset -> "Tomorrow"

Returns: Theme object

tomorrow_night()

Theme preset -> "Tomorrow Night"

Returns: Theme object

tomorrow_night_eighties()

Theme preset -> "Tomorrow Night Eighties"

Returns: Theme object

twilight()

Theme preset -> "Twilight"

Returns: Theme object

unikitty()

Theme preset -> "Unikitty"

Returns: Theme object

unikitty_reversible()

Theme preset -> "Unikitty Reversible"

Returns: Theme object

uwunicorn()

Theme preset -> "Uwunicorn"

Returns: Theme object

vice()

Theme preset -> "Vice"

Returns: Theme object

vulcan()

Theme preset -> "Vulcan"

Returns: Theme object

windows_10()

Theme preset -> "Windows 10"

Returns: Theme object

windows_95()

Theme preset -> "Windows 95"

Returns: Theme object

windows_high_contrast()

Theme preset -> "Windows High Contrast"

Returns: Theme object

windows_nt()

Theme preset -> "Windows Nt"

Returns: Theme object

woodland()

Theme preset -> "Woodland"

Returns: Theme object

xcode_dusk()

Theme preset -> "Xcode Dusk"

Returns: Theme object

theme_engineLibrary "theme_engine"

Theme Builder and Structure for live generative themes

init(_name)

New theme object.

Parameters:

_name : (string) opptional name

Returns: a VAR theme (holds it's vals when updated if not overwritten)

globals(theme, _h1, _h2, _h3, _h4, _s, _val, _contrast)

Create light/dark theme globals

Parameters:

theme : (theme) Theme to add theses to

_h1 : (float) Hue #1 for Template

_h2 : (float) Hue #2 for Template

_h3 : (float) Hue #3 for Template

_h4 : (float) Hue #4 for Template

_s : (float) Saturation of theme

_val : (float) Luminosity (light/dark)

_contrast : (float) Contrast to apply

Returns: Theme wwith adjusted colors

setConfig(theme, setting)

Apply a Settings object to a theme

Parameters:

theme : Theme object to apply settings to.

setting : settings to apply

Returns: theme

Types :

settings

Settings for a theme

Fields:

h1 : (float) Hue #1 for Template

h2 : (float) Hue #2 for Template

h3 : (float) Hue #3 for Template

h4 : (float) Hue #4 for Template

sat : (float) Saturation of theme

lum : (float) Luminosity (light/dark)

vib : (float) Vibrance (Contrast)

r : (float) Hue of Red

o : (float) Hue of Orange

y : (float) Hue of Yellow

g : (float) Hue of Green

a : (float) Hue of Aqua

b : (float) Hue of Blue

i : (float) Hue of Indigo

v : (float) Hue of Violet

satvals : (settings) Array for use if desired to customize Saturation per color

lumvals : (settings) Array for use if desired to customize Luminancce per color

mods

Modifiers Item for Use if desired

Fields:

val : (float)

size : (float)

depth : (float)

hue : (float)

sat : (float)

alpha : (float)

mix : (float)

emit : (float)

ch : (float)

step : (int)

dist : (int)

holds : (mods)

isin : (mods)

track : (color)

varient

Light/Dark/Custom Theme Varients

Fields:

bg : (color) Bacckground Color

fg : (color) Foreground Color

accent : (color) Accccent Color

secondary : (color) Secondary Color

txt : (color) Text Color

theme

Theme Object

Fields:

name : (string) Theme name

dark : (varient) Theme dark Varient

light : (varient) Theme light Varient

red : (color) Color for red

orange : (color) Color for orange

yellow : (color) Color for yellow

green : (color) Color for green

aqua : (color) Color for aqua

blue : (color) Color for blue

purple : (color) Color for purple

pink : (color) Color for pink

tweaks : (mods) Modifiers UDT to use for adjusters

themedict

Fields:

names : (string ) Names of themes

themes : (theme ) Theme Items

MyLibraryLibrary "MyLibrary"

TODO: add library description here

isHammer(fib, colorMatch)

TODO: add function description here

Parameters:

fib

colorMatch

Returns: TODO: add what function returns

eHarmonicpatternsLogScaleLibrary "eHarmonicpatternsLogScale"

Library provides functions to scan harmonic patterns both or normal and log scale

getSupportedPatterns()

get_prz_range(x, a, b, c, patternArray, errorPercent, start_adj, end_adj, logScale)

Provides PRZ range based on BCD and XAD ranges

Parameters:

x : X coordinate value

a : A coordinate value

b : B coordinate value

c : C coordinate value

patternArray : Pattern flags for which PRZ range needs to be calculated

errorPercent : Error threshold

start_adj : - Adjustments for entry levels

end_adj : - Adjustments for stop levels

logScale : - calculate on log scale. Default is false

Returns: Start and end of consolidated PRZ range

get_prz_range_xad(x, a, b, c, patternArray, errorPercent, start_adj, end_adj, logScale)

Provides PRZ range based on XAD range only

Parameters:

x : X coordinate value

a : A coordinate value

b : B coordinate value

c : C coordinate value

patternArray : Pattern flags for which PRZ range needs to be calculated

errorPercent : Error threshold

start_adj : - Adjustments for entry levels

end_adj : - Adjustments for stop levels

logScale : - calculate on log scale. Default is false

Returns: Start and end of consolidated PRZ range

get_projection_range(x, a, b, c, patternArray, errorPercent, start_adj, end_adj, logScale)

Provides Projection range based on BCD and XAD ranges

Parameters:

x : X coordinate value

a : A coordinate value

b : B coordinate value

c : C coordinate value

patternArray : Pattern flags for which PRZ range needs to be calculated

errorPercent : Error threshold

start_adj : - Adjustments for entry levels

end_adj : - Adjustments for stop levels

logScale : - calculate on log scale. Default is false

Returns: Array containing start and end ranges

isHarmonicPattern(x, a, b, c, d, flags, defaultEnabled, errorPercent, logScale)

Checks for harmonic patterns

Parameters:

x : X coordinate value

a : A coordinate value

b : B coordinate value

c : C coordinate value

d : D coordinate value

flags : flags to check patterns. Send empty array to enable all

defaultEnabled

errorPercent : Error threshold

logScale : - calculate on log scale. Default is false

Returns: Array of boolean values which says whether valid pattern exist and array of corresponding pattern names

isHarmonicProjection(x, a, b, c, flags, defaultEnabled, errorPercent, logScale)

Checks for harmonic pattern projection

Parameters:

x : X coordinate value

a : A coordinate value

b : B coordinate value

c : C coordinate value

flags : flags to check patterns. Send empty array to enable all

defaultEnabled

errorPercent : Error threshold

logScale : - calculate on log scale. Default is false

Returns: Array of boolean values which says whether valid pattern exist and array of corresponding pattern names.

E5TradingLibrary

This library replaces the previous MetaWorldEngineFilterLibrary3.

Library "E5TradingLibrary"

GetCandleStickSize(_src_high, _src_low)

returns size of the candle

Parameters:

_src_high

_src_low

Returns: candlestick size

GetCandleStickBodySize(_src_open, _src_close)

returns size of the candle body

Parameters:

_src_open

_src_close

Returns: candlestick body size

FilterLongerLowerWickCandles(_src_open, _src_close, _src_low)

Alters Candlestick Value to Magnify Candles with Long Wicks

Parameters:

_src_open

_src_close

_src_low

Returns: Midpoint of the candle body less the lower wick. If value returned has a large delta from midpoint of the body, then it is short wick

IsBullish(_src_open, _src_close)

Determine if Candle is Bullish or Bearish

Parameters:

_src_open

_src_close

Returns: True is Bullish

IsDoji(_candleIndex, _precision)

Determine if Candle is a Doji

Parameters:

_candleIndex

_precision

Returns: True if a Doji

MACD(_src, _fastLength, _slowLength, _signalLength)

Computes MACD

Parameters:

_src

_fastLength

_slowLength

_signalLength

Returns: Returns MACD and Signal Line

isFastSlowCrossed(SeriesA, SeriesB)

Computes if SeriesA crosses SeriesB

Parameters:

SeriesA

SeriesB

Returns: if SeriesA crosses SeriesB then true else false

isReversalUpTrend(SeriesA, SeriesB)

Computes if SeriesA crosses over SeriesB to determine reversal uptrend

Parameters:

SeriesA

SeriesB

Returns: if SeriesA crosses over SeriesB then true else false

isReversalDownTrend(SeriesA, SeriesB)

Computes if SeriesA crosses over SeriesB to determine reversal uptrend

Parameters:

SeriesA

SeriesB

Returns: if SeriesA crosses over SeriesB then true else false

SSMA(_src, smalength)

Computes smoothed SMA

Parameters:

_src

smalength

Returns: a single concatenated string for evaluation

GetTimeFrame()

Get Current timeframe in minutes

Returns: an integer value in minutes

getMA(_src, length, maType)

Gets a Moving Average based on type

Parameters:

_src

length

maType

Returns: A moving average with the given parameters

ATRSwitch(_src, _ATRMult, _ATRLength)

Average True Range Trailing Stops by Sylvain Vervoort

Parameters:

_src

_ATRMult

_ATRLength

Returns: upper ATR Line, lower ATR Line and the switch point

FibRatiosLibrary "FibRatios"

Library with calculation logic for fib retracement, extension and ratios

retracement(a, b, ratio, logScale, precision)

Calculates the retracement for points a, b with given ratio and scale

Parameters:

a : Starting point a

b : Second point b

ratio : Ratio for which we need to calculate retracement c

logScale : Flag to get calculations in log scale. Default is false

precision : rounding precision. If set to netagive number, round_to_mintick is applied. Default is -1

Returns: retracement point c for points a,b with given ratio and scale

retracementRatio(a, b, c, logScale, precision)

Calculates the retracement ratio for points a, b, c with given scale

Parameters:

a : Starting point a

b : Second point b

c : Retracement point. c should be placed between a and b

logScale : Flag to get calculations in log scale. Default is false

precision : rounding precision. If set to netagive number, round_to_mintick is applied. Default is 3

Returns: retracement ratio for points a,b,c on given scale

extension(a, b, c, ratio, logScale, precision)

Calculates the extensions for points a, b, c with given ratio and scale

Parameters:

a : Starting point a

b : Second point b

c : Retracement point. c should be placed between a and b

ratio : Ratio for which we need to calculate extension d

logScale : Flag to get calculations in log scale. Default is false

precision : rounding precision. If set to netagive number, round_to_mintick is applied. Default is -1

Returns: extensoin point d for points a,b,c with given ratio and scale

extensionRatio(a, b, c, d, logScale, precision)

Calculates the extension ratio for points a, b, c, d with given scale

Parameters:

a : Starting point a

b : Second point b

c : Retracement point. c should be placed between a and b

d : Extension point. d should be placed beyond a, c. But, can be with b,c or beyond b

logScale : Flag to get calculations in log scale. Default is false

precision : rounding precision. If set to netagive number, round_to_mintick is applied. Default is 3

Returns: extension ratio for points a,b,c,d on given scale

DataCorrelationLibrary "DataCorrelation"

Implementation of functions related to data correlation calculations. Formulas have been transformed in such a way that we avoid running loops and instead make use of time series to gradually build the data we need to perform calculation. This allows the calculations to run on unbound series, and/or higher number of samples

🎲 Simplifying Covariance

Original Formula

//For Sample

Covₓᵧ = ∑ ((xᵢ-x̄)(yᵢ-ȳ)) / (n-1)

//For Population

Covₓᵧ = ∑ ((xᵢ-x̄)(yᵢ-ȳ)) / n

Now, if we look at numerator, this can be simplified as follows

∑ ((xᵢ-x̄)(yᵢ-ȳ))

=> (x₁-x̄)(y₁-ȳ) + (x₂-x̄)(y₂-ȳ) + (x₃-x̄)(y₃-ȳ) ... + (xₙ-x̄)(yₙ-ȳ)

=> (x₁y₁ + x̄ȳ - x₁ȳ - y₁x̄) + (x₂y₂ + x̄ȳ - x₂ȳ - y₂x̄) + (x₃y₃ + x̄ȳ - x₃ȳ - y₃x̄) ... + (xₙyₙ + x̄ȳ - xₙȳ - yₙx̄)

=> (x₁y₁ + x₂y₂ + x₃y₃ ... + xₙyₙ) + (x̄ȳ + x̄ȳ + x̄ȳ ... + x̄ȳ) - (x₁ȳ + x₂ȳ + x₃ȳ ... xₙȳ) - (y₁x̄ + y₂x̄ + y₃x̄ + yₙx̄)

=> ∑xᵢyᵢ + n(x̄ȳ) - ȳ∑xᵢ - x̄∑yᵢ

So, overall formula can be simplified to be used in pine as

//For Sample

Covₓᵧ = (∑xᵢyᵢ + n(x̄ȳ) - ȳ∑xᵢ - x̄∑yᵢ) / (n-1)

//For Population

Covₓᵧ = (∑xᵢyᵢ + n(x̄ȳ) - ȳ∑xᵢ - x̄∑yᵢ) / n

🎲 Simplifying Standard Deviation

Original Formula

//For Sample

σ = √(∑(xᵢ-x̄)² / (n-1))

//For Population

σ = √(∑(xᵢ-x̄)² / n)

Now, if we look at numerator within square root

∑(xᵢ-x̄)²

=> (x₁² + x̄² - 2x₁x̄) + (x₂² + x̄² - 2x₂x̄) + (x₃² + x̄² - 2x₃x̄) ... + (xₙ² + x̄² - 2xₙx̄)

=> (x₁² + x₂² + x₃² ... + xₙ²) + (x̄² + x̄² + x̄² ... + x̄²) - (2x₁x̄ + 2x₂x̄ + 2x₃x̄ ... + 2xₙx̄)

=> ∑xᵢ² + nx̄² - 2x̄∑xᵢ

=> ∑xᵢ² + x̄(nx̄ - 2∑xᵢ)

So, overall formula can be simplified to be used in pine as

//For Sample

σ = √(∑xᵢ² + x̄(nx̄ - 2∑xᵢ) / (n-1))

//For Population

σ = √(∑xᵢ² + x̄(nx̄ - 2∑xᵢ) / n)

🎲 Using BinaryInsertionSort library

Chatterjee Correlation and Spearman Correlation functions make use of BinaryInsertionSort library to speed up sorting. The library in turn implements mechanism to insert values into sorted order so that load on sorting is reduced by higher extent allowing the functions to work on higher sample size.

🎲 Function Documentation

chatterjeeCorrelation(x, y, sampleSize, plotSize)

Calculates chatterjee correlation between two series. Formula is - ξnₓᵧ = 1 - (3 * ∑ |rᵢ₊₁ - rᵢ|)/ (n²-1)

Parameters:

x : First series for which correlation need to be calculated

y : Second series for which correlation need to be calculated

sampleSize : number of samples to be considered for calculattion of correlation. Default is 20000

plotSize : How many historical values need to be plotted on chart.

Returns: float correlation - Chatterjee correlation value if falls within plotSize, else returns na

spearmanCorrelation(x, y, sampleSize, plotSize)

Calculates spearman correlation between two series. Formula is - ρ = 1 - (6∑dᵢ²/n(n²-1))

Parameters:

x : First series for which correlation need to be calculated

y : Second series for which correlation need to be calculated

sampleSize : number of samples to be considered for calculattion of correlation. Default is 20000

plotSize : How many historical values need to be plotted on chart.

Returns: float correlation - Spearman correlation value if falls within plotSize, else returns na

covariance(x, y, include, biased)

Calculates covariance between two series of unbound length. Formula is Covₓᵧ = ∑ ((xᵢ-x̄)(yᵢ-ȳ)) / (n-1) for sample and Covₓᵧ = ∑ ((xᵢ-x̄)(yᵢ-ȳ)) / n for population

Parameters:

x : First series for which covariance need to be calculated

y : Second series for which covariance need to be calculated

include : boolean flag used for selectively including sample

biased : boolean flag representing population covariance instead of sample covariance

Returns: float covariance - covariance of selective samples of two series x, y

stddev(x, include, biased)

Calculates Standard Deviation of a series. Formula is σ = √( ∑(xᵢ-x̄)² / n ) for sample and σ = √( ∑(xᵢ-x̄)² / (n-1) ) for population

Parameters:

x : Series for which Standard Deviation need to be calculated

include : boolean flag used for selectively including sample

biased : boolean flag representing population covariance instead of sample covariance

Returns: float stddev - standard deviation of selective samples of series x

correlation(x, y, include)

Calculates pearson correlation between two series of unbound length. Formula is r = Covₓᵧ / σₓσᵧ

Parameters:

x : First series for which correlation need to be calculated

y : Second series for which correlation need to be calculated

include : boolean flag used for selectively including sample

Returns: float correlation - correlation between selective samples of two series x, y

HiveLibraryLibrary "HiveLibrary"

: Custom library

RoundDown(number, decimals)

RoundDown() rounds the specified number down to the given number

of decimal places.

Parameters:

number : is the argument for rounding down & decimals is the number of digits after dot

decimals

Returns: return is the rounded down value of the number

JeeSauceScriptsLibrary "JeeSauceScripts"

getupdnvol()

GetTotalUpVolume(upvolume)

Parameters:

upvolume

GetTotalDnVolume(downvolume)

Parameters:

downvolume

GetDelta(totalupvolume, totaldownvolume)

Parameters:

totalupvolume

totaldownvolume

GetMaxUpVolume(upvolume)

Parameters:

upvolume

GetMaxDnVolume(downvolume)

Parameters:

downvolume

Getcvd()

Getcvdopen(cvd)

Parameters:

cvd

Getcvdhigh(cvd, maxvolumeup)

Parameters:

cvd

maxvolumeup

Getcvdlow(cvd, maxvolumedown)

Parameters:

cvd

maxvolumedown

Getcvdclose(cvd, delta)

Parameters:

cvd

delta

CombineData(data1, data2, data3, data4, data5, data6)

Parameters:

data1

data2

data3

data4

data5

data6

FindData(data, find)

Parameters:

data

find

MyLibraryLibrary "MyLibrary"

TODO: add library description here

init(value)

Parameters:

value

set(source, value)

Parameters:

source

value

get(source)

Parameters:

source

Motion▮ FEATURES

Now as library version :)

String-based transition-effects

Performance optimization. Reduced memory consumption up to >90% by kicking the output to the "stdout".

Use marquee- or loader-effect on any possible string location.

Example: UI Price-Ticker

----------------------------------------------------------------------------

Library "Motion"

_getStringMono(_len, _str, _sep)

Parameters:

_len

_str

_sep

marquee(this, _extern, _ws, _subLen, _subStart)

Parameters:

this

_extern

_ws

_subLen

_subStart

transition(this, _subLen, _subStart)

Parameters:

this

_subLen

_subStart

hold(this)

Parameters:

this

keyframe

keyframe A keyframe object.

Fields:

seq

intv

step

length

update_no

frame_no

ltr

hold

Replica of TradingView's Backtesting Engine with ArraysHello everyone,

Here is a perfectly replicated TradingView backtesting engine condensed into a single library function calculated with arrays. It includes TradingView's calculations for Net profit, Total Trades, Percent of Trades Profitable, Profit Factor, Max Drawdown (absolute and percent), and Average Trade (absolute and percent). Here's how TradingView defines each aspect of its backtesting system:

Net Profit: The overall profit or loss achieved.

Total Trades: The total number of closed trades, winning and losing.

Percent Profitable: The percentage of winning trades, the number of winning trades divided by the total number of closed trades.

Profit Factor: The amount of money the strategy made for every unit of money it lost, gross profits divided by gross losses.

Max Drawdown: The greatest loss drawdown, i.e., the greatest possible loss the strategy had compared to its highest profits.

Average Trade: The sum of money gained or lost by the average trade, Net Profit divided by the overall number of closed trades.

Here's how each variable is defined in the library function:

_backtest(bool _enter, bool _exit, float _startQty, float _tradeQty)

bool _enter: When the strategy should enter a trade (entry condition)

bool _exit: When the strategy should exit a trade (exit condition)

float _startQty: The starting capital in the account (for BTCUSD, it is the amount of USD the account starts with)

float _tradeQty: The amount of capital traded (if set to 1000 on BTCUSD, it will trade 1000 USD on each trade)

Currently, this library only works with long strategies, and I've included a commented out section under DEMO STRATEGY where you can replicate my results with TradingView's backtesting engine. There's tons I could do with this beyond what is shown, but this was a project I worked on back in June of 2022 before getting burned out. Feel free to comment with any suggestions or bugs, and I'll try to add or fix them all soon. Here's my list of thing to add to the library currently (may not all be added):

Add commission calculations.

Add support for shorting

Add a graph that resembles TradingView's overview graph.

Clean and optimize code.

Clean up in a way that makes it easy to add other TradingView calculations (such as Sharpe and Sortino ratio).

Separate all variables, so they become accessible outside of calculations (such as gross profit, gross loss, number of winning trades, number of losing trades, etc.).

Thanks for reading,

OztheWoz

Library_SmoothersLibrary "Library_Smoothers"

CorrectedMA(Src, Len)

CorrectedMA The strengths of the corrected Average (CA) is that the current value of the time series must exceed a the current volatility-dependent threshold, so that the filter increases or falls, avoiding false signals when the trend is in a weak phase.

Parameters:

Src

Len

Returns: The Corrected source.

EHMA(src, len)

EMA Exponential Moving Average.

Parameters:

src : Source to act upon

len

Returns: EMA of source

FRAMA(src, len, FC, SC)

FRAMA Fractal Adaptive Moving Average

Parameters:

src : Source to act upon

len : Length of moving average

FC : Fast moving average

SC : Slow moving average

Returns: FRAMA of source

Jurik(src, length, phase, power)

Jurik A low lag filter

Parameters:

src : Source

length : Length for smoothing

phase : Phase range is ±100

power : Mathematical power to use. Doesn't need to be whole numbers

Returns: Jurik of source

SMMA(src, len)

SMMA Smoothed moving average. Think of the SMMA as a hybrid of its better-known siblings — the simple moving average (SMA) and the exponential moving average (EMA).

Parameters:

src : Source

len

Returns: SMMA of source

SuperSmoother(src, len)

SuperSmoother

Parameters:

src : Source to smooth

len

Returns: SuperSmoother of the source

TMA(src, len)

TMA Triangular Moving Average

Parameters:

src : Source

len

Returns: TMA of source

TSF(src, len)

TSF Time Series Forecast. Uses linear regression.

Parameters:

src : Source

len

Returns: TSF of source

VIDYA(src, len)

VIDYA Chande's Variable Index Dynamic Average. See www.fxcorporate.com

Parameters:

src : Source

len

Returns: VIDYA of source

VAWMA(src, len, startingWeight, volumeDefault)

VAWMA = VWMA and WMA combined. Simply put, this attempts to determine the average price per share over time weighted heavier for recent values. Uses a triangular algorithm to taper off values in the past (same as WMA does).

Parameters:

src : Source

len : Length

startingWeight

volumeDefault : The default value to use when a chart has no volume.

Returns: The VAWMA of the source.

WWMA(src, len)

WWMA Welles Wilder Moving Average

Parameters:

src : Source

len

Returns: The WWMA of the source

ZLEMA(src, len)

ZLEMA Zero Lag Expotential Moving Average

Parameters:

src : Source

len

Returns: The ZLEMA of the source

SmootherType(mode, src, len, fastMA, slowMA, offset, phase, power, startingWeight, volumeDefault, Corrected)

Performs the specified moving average

Parameters:

mode : Name of moving average

src : the source to apply the MA type

len

fastMA : FRAMA fast moving average

slowMA : FRAMA slow moving average

offset : Linear regression offset

phase : Jurik phase

power : Jurik power

startingWeight : VAWMA starting weight

volumeDefault : VAWMA default volume

Corrected

Returns: The MA smoothed source

HendrixLIBRARY - utilsLibrary "HendrixLIBRARY"

getVolumeData()

getLTF(customTimeframe, ltf)

Parameters:

customTimeframe

ltf

sumArray(a)

Parameters:

a

arrs2vals(upVolumeArray, downVolumeArray, volArr)

Parameters:

upVolumeArray

downVolumeArray

volArr

getVolumesFromUpDownArrays(upVolumeArray, downVolumeArray)

Parameters:

upVolumeArray

downVolumeArray

getDeltaFromVolumes(upVolume, downVolume)

Parameters:

upVolume

downVolume

getDeltaFromUpDownArrays(upVolumeArray, downVolumeArray)

Parameters:

upVolumeArray

downVolumeArray

getUpColor()

getDownColor()

getBlackColor()

getColors()

printTableTR(txt)

Parameters:

txt

printTableBR(txt)

Parameters:

txt

printTableMR(txt)

Parameters:

txt

print(txt, lbl)

Parameters:

txt

lbl

printSyminfo(sym)

Parameters:

sym

Profit EstimateLibrary "profitestimate"

Simple profit Estimatr. Engages when Position != 0

and holds until posittion is na/0...

if position changes sizes, it will update automatically and adjust.

it has an input for comission to estmate exit fees

update_avgprice(_sizewas, _delta, _pricewas, _newprice)

Get a new Average position Price

Parameters:

_sizewas : (float) the position prior

_delta : (float) the order amount

_pricewas : (float) the prior price

_newprice : (float) the price of order

Returns: New Avg Price

amount(_position, _close, _commission, _leverage, _fullqty)

Position Net Profit Net Commission, automatic on/off if position != 0

Parameters:

_position : (float) position size (total or margin size)

_close

_commission : (float) % where (0.1 = 0.1%)

_leverage : (float) optional if leveraged, default 1x

_fullqty : (bool) if position entered is tottal trade size default is margin qty (1/lev)

Returns: quote value of profit

percent(_position, _close, _commission, _leverage, _fullqty)

Position Net Profit, automatic on/off if position != 0

Parameters:

_position : (float) position size (total or margin size)

_close

_commission : (float) % where (0.1 = 0.1%)

_leverage : (float) optional if leveraged, default 1x

_fullqty : (bool) if position entered is tottal trade size, default is margin qty (1/lev)

Returns: percentage profit (1% = 1)

HeikinashiLibrary "Heikinashi"

This library calculates "Heikinashi".

calc(_o, _h, _l, _c, _my_close)

This function calculates "Heikinashi".

Parameters:

_o : open

_h : high

_l : low

_c : close

_my_close : Specify if you want to force only the closing price to a real value.

Returns: TODO: add what function returns

String Extra FunctionsLibrary "string_extras"

Additional String shortcuts, unshift and pop return the string ~without~ the first or last, so in use will still require to extract first or last character prior to overwriting a string with the output.

can be imported "as str" to work side by side with regular pine

last(_string)

last char of a string

Parameters:

_string

Returns: last char of a string

shift(_string)

string without first char

Parameters:

_string

Returns: string without first char

pop(_string)

string without last char

Parameters:

_string

Returns: string without last char

get(_string, _position)

get specific char of a string

Parameters:

_string

_position

Returns: string _string

push(_string, _char)

push to end of a string

Parameters:

_string

_char

Returns: string _string

unshift(_string, _char)

unshift char to prepend string

Parameters:

_string

_char

Returns: string _string

HSupertrendLibrary "HSupertrend"

Supertrend implementation based on harmonic patterns

hsupertrend(zProperties, pProperties, errorPercent, showPatterns, patternColor)

derives supertrend based on harmonic patterns

Parameters:

zProperties : ZigzagProperties containing Zigzag length and source array

pProperties : PatternProperties used for calculation

errorPercent : Error threshold for scanning patterns

showPatterns : Draw identified patterns structure on chart

patternColor : Color of the pattern lines to be drawn

Returns:

ZigzagProperties

ZigzagProperties contains values required for zigzag calculation

Fields:

length : Zigzag length

source : Array containing custom OHLC. If not set, array.from(high, low) is used

PatternProperties

PatternProperties are essential pattern parameters used for calculation of bullish and bearish zones

Fields:

base : Base for calculating entry and stop of pattern. Can be CD, minmax or correction. Default is CD

entryPercent : Distance from D in terms of percent of Base in the direction of pattern

stopPercent : Distance from D in terms of percent of Base in the opposite direction of pattern

useClosePrices : When set uses close price for calculation of supertrend breakout

PatternLibrary "Pattern"

Pattern object definitions and functions. Easily draw and keep track of patterns, legs, and points.

Supported pattern types (as of Version 1):

Type Leg validation # legs

"xabcd" Direction 3 or 4 (point D not required)

"zigzag" Direction >= 2

"free" None >= 2

erase_label(this)

Delete the point label

Parameters:

this : Point

Returns: Void

draw_label(this, position, clr, transp, txt_clr, txt, tooltip, size)

Draw the point label

Parameters:

this : Point

position

clr

transp

txt_clr

txt

tooltip

size

Returns: line

leg_init(a, b, prev, next, line)

Initialize a pattern leg

Parameters:

a : Point A (required)

b : Point B (required)

prev : Previous leg

next : Next leg

line : Line

Returns: New instance of leg object

erase(this)

Delete the pattern leg

Parameters:

this : Leg

Returns: Void

erase(this)

Parameters:

this

draw(this, clr, style, transp, width)

Draw the pattern leg

Parameters:

this : Leg

clr : Color

style : Style ("solid", "dotted", "dashed", "arrowleft", "arrowright")

transp : Transparency

width : Width

Returns: line

draw(this, clr, style, transp, width)

Parameters:

this

clr

style

transp

width

leg_getLineTerms(this)

Get the slope and y-intercept of a leg

Parameters:

this : Leg

Returns:

leg_getPrice(this, index)

Get the price (Y) at a given bar index (X) within the leg

Parameters:

this : Leg

index : Bar index

Returns: Price (float)

pattern_init(legs, tp, name, subType, pid)

Initialize a pattern object from a given set of legs

Parameters:

legs : Array of pattern legs (required)

tp : Pattern type ("zigzag", "xabcd", or "free". dft = "free")

name : Pattern name

subType : Pattern subtype

pid : Pattern Identifier string

Returns: New instance of pattern object, if one was successfully created

pattern_init(points, tp, name, subType, pid)

Initialize a pattern object from a given set of points

Parameters:

points

tp : Pattern type ("zigzag", "xabcd", or "free". dft = "free")

name : Pattern name

subType : Pattern subtype

pid : Pattern Identifier string

Returns: New instance of pattern object, if one was successfully created

point

A point on the chart (x,y)

Fields:

x : Bar index (x coordinate)

y

label

leg

A pattern leg (point A to point B)

Fields:

a : Point A

b

deltaX

deltaY

prev

next

retrace

line

pattern

A pattern (set of at least 2 connected legs)

Fields:

legs

type

subType

name

pid

ChasinAlts_LibraryLibrary "ChasinAlts_Library"

rci(_BCgtg, _Tgtg, _close, _smaLen, _bar_index)

Parameters:

_BCgtg

_Tgtg

_close

_smaLen

_bar_index

printedBC(_time, _minPerc, _Tgtg, _lkbk)

Parameters:

_time

_minPerc

_Tgtg

_lkbk

form123(_ppLen, _BCgtg, _Tgtg, _high, _low, _close, _bar_index)

Parameters:

_ppLen

_BCgtg

_Tgtg

_high

_low

_close

_bar_index

obosCnt(_BCgtg, _Tgtg, _rci, _obosMin, _obosMax, _thresh)

Parameters:

_BCgtg

_Tgtg

_rci

_obosMin

_obosMax

_thresh

div(_thresh, _HLestLen, _Tgtg, _BCgtg, _rci, _time, _price, _LSL, _SSL, _LTP, _STP, _colorid, _long, _short)

Parameters:

_thresh

_HLestLen

_Tgtg

_BCgtg

_rci

_time

_price

_LSL

_SSL

_LTP

_STP

_colorid

_long

_short

tradeSim(_SL, _TP, _BCgtg, _Tgtg, _ppLen, _high, _low, _close, _bar_index, _time, _bull_rev, _bear_rev, _bull_obosCnt_gtg, _bear_obosCnt_gtg)

Parameters:

_SL

_TP

_BCgtg

_Tgtg

_ppLen

_high

_low

_close

_bar_index

_time

_bull_rev

_bear_rev

_bull_obosCnt_gtg

_bear_obosCnt_gtg

TrailingStopsLibrary "TrailingStops"

This library contains functions to output trailing stop lines.

f_marketStructureStop(_restartMode, _flipMode, _restartLowIn, _restartHighIn)

Parameters:

_restartMode - Defines how the stop lines persist. Allowed values are:

"Always On" - The stop lines are always present and they just reset when they're crossed.

"Flip" - The stop lines flip when they're crossed.

"Manual" - The stop lines turn off when they're crossed, and turn back on again when _restartLowIn or _restartHighIn are passed into the function as true.

_flipMode - Defines whether the stop lines are broken by wicks or closes. Allowed values are "Wick", and "Close".

_restartLowIn - If _restartMode is "Manual", passing this parameter as true restarts the Low stop line.

_restartHighIn - If _restartMode is "Manual", passing this parameter as true restarts the High stop line.

@returns - floats for the Low and High stop line.

SignalBuilderSignalBuilder

Utility for building a collection of signal values. Provides a default view for displaying signals.

Simplified API for aggregating signal values.

Flexible for use with indicators and strategies.

See the demo section for an example.