ICOptimizerLibrary "ICOptimizer"

Library for IC-based parameter optimization

findOptimalParam(testParams, icValues, currentParam, smoothing)

Find optimal parameter from array of IC values

Parameters:

testParams (array) : Array of parameter values being tested

icValues (array) : Array of IC values for each parameter (same size as testParams)

currentParam (float) : Current parameter value (for smoothing)

smoothing (simple float) : Smoothing factor (0-1, e.g., 0.2 means 20% new, 80% old)

Returns: New parameter value, its IC, and array index

adaptiveParamWithStarvation(opt, testParams, icValues, smoothing, starvationThreshold, starvationJumpSize)

Adaptive parameter selection with starvation handling

Parameters:

opt (ICOptimizer) : ICOptimizer object

testParams (array) : Array of parameter values

icValues (array) : Array of IC values for each parameter

smoothing (simple float) : Normal smoothing factor

starvationThreshold (simple int) : Number of updates before triggering starvation mode

starvationJumpSize (simple float) : Jump size when in starvation (as fraction of range)

Returns: Updated parameter and IC

detectAndAdjustDomination(longCount, shortCount, currentLongLevel, currentShortLevel, dominationRatio, jumpSize, minLevel, maxLevel)

Detect signal imbalance and adjust parameters

Parameters:

longCount (int) : Number of long signals in period

shortCount (int) : Number of short signals in period

currentLongLevel (float) : Current long threshold

currentShortLevel (float) : Current short threshold

dominationRatio (simple int) : Ratio threshold (e.g., 4 = 4:1 imbalance)

jumpSize (simple float) : Size of adjustment

minLevel (simple float) : Minimum allowed level

maxLevel (simple float) : Maximum allowed level

Returns:

calcIC(signals, returns, lookback)

Parameters:

signals (float)

returns (float)

lookback (simple int)

classifyIC(currentIC, icWindow, goodPercentile, badPercentile)

Parameters:

currentIC (float)

icWindow (simple int)

goodPercentile (simple int)

badPercentile (simple int)

evaluateSignal(signal, forwardReturn)

Parameters:

signal (float)

forwardReturn (float)

updateOptimizerState(opt, signal, forwardReturn, currentIC, metaICPeriod)

Parameters:

opt (ICOptimizer)

signal (float)

forwardReturn (float)

currentIC (float)

metaICPeriod (simple int)

calcSuccessRate(successful, total)

Parameters:

successful (int)

total (int)

createICStatsTable(opt, paramName, normalSuccess, normalTotal)

Parameters:

opt (ICOptimizer)

paramName (string)

normalSuccess (int)

normalTotal (int)

initOptimizer(initialParam)

Parameters:

initialParam (float)

ICOptimizer

Fields:

currentParam (series float)

currentIC (series float)

metaIC (series float)

totalSignals (series int)

successfulSignals (series int)

goodICSignals (series int)

goodICSuccess (series int)

nonBadICSignals (series int)

nonBadICSuccess (series int)

goodICThreshold (series float)

badICThreshold (series float)

updateCounter (series int)

Penunjuk dan strategi

IC optimiser libLibrary "IC optimiser lib"

Library for IC-based parameter optimization

findOptimalParam(testParams, icValues, currentParam, smoothing)

Find optimal parameter from array of IC values

Parameters:

testParams (array) : Array of parameter values being tested

icValues (array) : Array of IC values for each parameter (same size as testParams)

currentParam (float) : Current parameter value (for smoothing)

smoothing (simple float) : Smoothing factor (0-1, e.g., 0.2 means 20% new, 80% old)

Returns: New parameter value, its IC, and array index

adaptiveParamWithStarvation(opt, testParams, icValues, smoothing, starvationThreshold, starvationJumpSize)

Adaptive parameter selection with starvation handling

Parameters:

opt (ICOptimizer) : ICOptimizer object

testParams (array) : Array of parameter values

icValues (array) : Array of IC values for each parameter

smoothing (simple float) : Normal smoothing factor

starvationThreshold (simple int) : Number of updates before triggering starvation mode

starvationJumpSize (simple float) : Jump size when in starvation (as fraction of range)

Returns: Updated parameter and IC

detectAndAdjustDomination(longCount, shortCount, currentLongLevel, currentShortLevel, dominationRatio, jumpSize, minLevel, maxLevel)

Detect signal imbalance and adjust parameters

Parameters:

longCount (int) : Number of long signals in period

shortCount (int) : Number of short signals in period

currentLongLevel (float) : Current long threshold

currentShortLevel (float) : Current short threshold

dominationRatio (simple int) : Ratio threshold (e.g., 4 = 4:1 imbalance)

jumpSize (simple float) : Size of adjustment

minLevel (simple float) : Minimum allowed level

maxLevel (simple float) : Maximum allowed level

Returns:

calcIC(signals, returns, lookback)

Parameters:

signals (float)

returns (float)

lookback (simple int)

classifyIC(currentIC, icWindow, goodPercentile, badPercentile)

Parameters:

currentIC (float)

icWindow (simple int)

goodPercentile (simple int)

badPercentile (simple int)

evaluateSignal(signal, forwardReturn)

Parameters:

signal (float)

forwardReturn (float)

updateOptimizerState(opt, signal, forwardReturn, currentIC, metaICPeriod)

Parameters:

opt (ICOptimizer)

signal (float)

forwardReturn (float)

currentIC (float)

metaICPeriod (simple int)

calcSuccessRate(successful, total)

Parameters:

successful (int)

total (int)

createICStatsTable(opt, paramName, normalSuccess, normalTotal)

Parameters:

opt (ICOptimizer)

paramName (string)

normalSuccess (int)

normalTotal (int)

initOptimizer(initialParam)

Parameters:

initialParam (float)

ICOptimizer

Fields:

currentParam (series float)

currentIC (series float)

metaIC (series float)

totalSignals (series int)

successfulSignals (series int)

goodICSignals (series int)

goodICSuccess (series int)

nonBadICSignals (series int)

nonBadICSuccess (series int)

goodICThreshold (series float)

badICThreshold (series float)

updateCounter (series int)

LIB_SDz_AucLibrary "LIB_SDz_Auc"

TODO: add library description here

getLineStyle(style)

Parameters:

style (string)

testLibLibrary "testLib"

TODO: add library description here

mySMA(x)

TODO: add function description here

Parameters:

x (int) : TODO: add parameter x description here

Returns: TODO: add what function returns

livremySMATestLibLibrary "livremySMATestLib"

TODO: add library description here

mySMA(x)

TODO: add function description here

Parameters:

x (int) : TODO: add parameter x description here

Returns: TODO: add what function returns

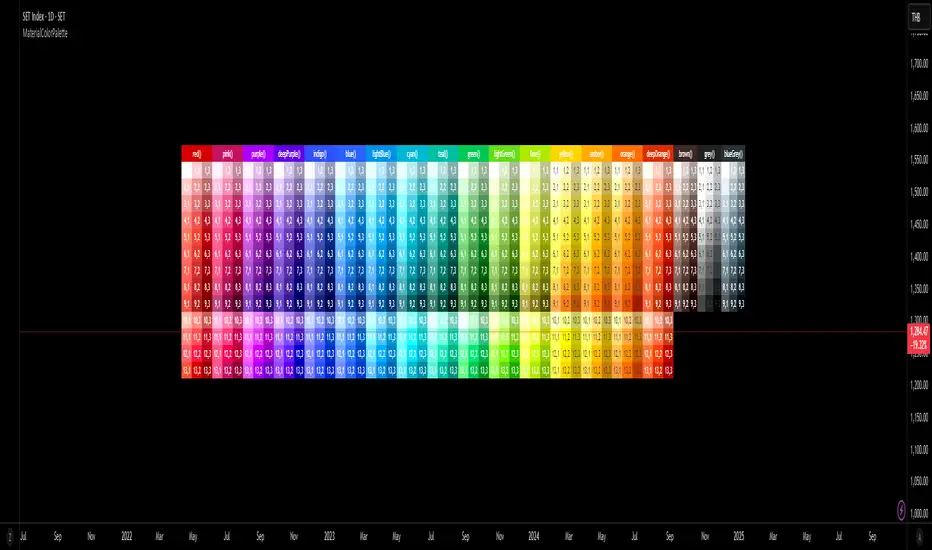

Material Color Palette Library█ OVERVIEW

Unlock a world of color in your Pine Script® projects with the Material Color Palette Library . This library provides a comprehensive and structured color system based on Google's Material Design palette, making it incredibly easy to create visually appealing and professional-looking indicators and strategies.

Forget about guessing hex codes. With this library, you have access to 19 distinct color families, each offering a wide range of shades. Every color can be fine-tuned with saturation, darkness, and opacity levels, giving you precise control over your script's appearance.

To make development even easier, the library includes a visual cheatsheet. Simply add the script to your chart to display a full table of all available colors and their corresponding parameters.

█ KEY FEATURES

Vast Spectrum: 19 distinct color families, from vibrant reds and blues to subtle greys and browns.

Fine-Tuned Control: Each color function accepts parameters for `saturationLevel` (1-13 or 1-9) and `darkLevel` (1-3) to select the perfect shade.

Opacity Parameter: Easily add transparency to any color for fills, backgrounds, or lines.

Quick Access Tones: A simple `tone()` function to grab base colors by name.

Visual Cheatsheet: An on-chart table displays the entire color palette, serving as a handy reference guide during development.

█ HOW TO USE

As a library, this script is meant to be imported into your own indicators or strategies.

1. Import the Library

Add the following line to the top of your script. Remember to replace `YourUsername` with your TradingView username.

import mastertop/ColorPalette/1 as colors

2. Call a Color Function

You can now use any of the exported functions to set colors for your plots, backgrounds, tables, and more.

The primary functions take three arguments: `functionName(saturationLevel, darkLevel, opacity)`

`saturationLevel`: An integer that controls the intensity of the color. Ranges from 1 (lightest) to 13 (most vibrant) for most colors, and 1-9 for `brown`, `grey`, and `blueGrey`.

`darkLevel`: An integer from 1 to 3 (1: light, 2: medium, 3: dark).

`opacity`: An integer from 0 (opaque) to 100 (invisible).

Example Usage:

Let's plot a moving average with a specific shade of teal.

// Import the library

import mastertop/ColorPalette/1 as colors

indicator("My Script with Custom Colors", overlay = true)

// Calculate a moving average

ma = ta.sma(close, 20)

// Plot the MA using a color from the library

// We'll use teal with saturation level 7, dark level 2, and 0% opacity

plot(ma, "MA", color = colors.teal(7, 2, 0), linewidth = 2)

3. Using the `tone()` Function

For quick access to a base color, you can use the `tone()` function.

// Set a red background with 85% transparency

bgcolor(colors.tone('red', 85))

█ VISUAL REFERENCE

To see all available colors at a glance, you can add this library script directly to your chart. It will display a comprehensive table showing every color variant. This makes it easy to pick the exact shade you need without guesswork.

This library is designed for fellow Pine Script® developers to streamline their workflow and enhance the visual quality of their scripts. Enjoy!

UTBotLibrary "UTBot"

is a powerful and flexible trading toolkit implemented in Pine Script. Based on the widely recognized UT Bot strategy originally developed by Yo_adriiiiaan with important enhancements by HPotter, this library provides users with customizable functions for dynamic trailing stop calculations using ATR (Average True Range), trend detection, and signal generation. It enables developers and traders to seamlessly integrate UT Bot logic into their own indicators and strategies without duplicating code.

Key features include:

Accurate ATR-based trailing stop and reversal detection

Multi-timeframe support for enhanced signal reliability

Clean and efficient API for easy integration and customization

Detailed documentation and examples for quick adoption

Open-source and community-friendly, encouraging collaboration and improvements

We sincerely thank Yo_adriiiiaan for the original UT Bot concept and HPotter for valuable improvements that have made this strategy even more robust. This library aims to honor their work by making the UT Bot methodology accessible to Pine Script developers worldwide.

This library is designed for Pine Script programmers looking to leverage the proven UT Bot methodology to build robust trading systems with minimal effort and maximum maintainability.

UTBot(h, l, c, multi, leng)

Parameters:

h (float) - high

l (float) - low

c (float)-close

multi (float)- multi for ATR

leng (int)-length for ATR

Returns:

xATRTS - ATR Based TrailingStop Value

pos - pos==1, long position, pos==-1, shot position

signal - 0 no signal, 1 buy, -1 sell

mt_elliott_coreLibrary "mt_elliott_core"

ewo(maFastLen, maSlowLen, smoothLen)

Parameters:

maFastLen (simple int)

maSlowLen (simple int)

smoothLen (simple int)

mt_phase_num(_len, _minGap)

Parameters:

_len (simple int)

_minGap (simple float)

mt_color_from_phase(_len, _minGap)

Parameters:

_len (simple int)

_minGap (simple float)

mt_phase_progress_pct(_len, _minGap)

Parameters:

_len (simple int)

_minGap (simple float)

anchor_p1_close(len, minGap)

Parameters:

len (simple int)

minGap (simple float)

anchor_p1_pivot(len, minGap)

Parameters:

len (simple int)

minGap (simple float)

row_group_from_ewo(ewoValue, atrValue, strongPct, neutralPct)

Parameters:

ewoValue (float)

atrValue (float)

strongPct (simple float)

neutralPct (simple float)

wave_event_pivot_aligned(ewoSeries, left, right, divTolPct, minBarsGap)

Parameters:

ewoSeries (float)

left (simple int)

right (simple int)

divTolPct (simple float)

minBarsGap (simple int)

DynLenLibLibrary "DynLenLib"

sum_dyn(src, len)

Parameters:

src (float)

len (int)

lag_dyn(src, len)

Parameters:

src (float)

len (int)

highest_dyn(src, len)

Parameters:

src (float)

len (int)

lowest_dyn(src, len)

Parameters:

src (float)

len (int)

var_dyn(src, len)

Parameters:

src (float)

len (int)

stdev_dyn(src, len)

Parameters:

src (float)

len (int)

hl2()

hlc3()

ohlc4()

sma_dyn(src, len)

Parameters:

src (float)

len (int)

ema_dyn(src, len)

Parameters:

src (float)

len (int)

rma_dyn(src, len)

Parameters:

src (float)

len (int)

smma_dyn(src, len)

Parameters:

src (float)

len (int)

wma_dyn(src, len)

Parameters:

src (float)

len (int)

vwma_dyn(price, vol, len)

Parameters:

price (float)

vol (float)

len (int)

hma_dyn(src, len)

Parameters:

src (float)

len (int)

dema_dyn(src, len)

Parameters:

src (float)

len (int)

tema_dyn(src, len)

Parameters:

src (float)

len (int)

kama_dyn(src, erLen, fastLen, slowLen)

Parameters:

src (float)

erLen (int)

fastLen (int)

slowLen (int)

mcginley_dyn(src, len)

Parameters:

src (float)

len (int)

median_price()

true_range()

atr_dyn(len)

Parameters:

len (int)

bbands_dyn(src, len, mult)

Parameters:

src (float)

len (int)

mult (float)

bb_percent_b(src, len, mult)

Parameters:

src (float)

len (int)

mult (float)

bb_bandwidth(src, len, mult)

Parameters:

src (float)

len (int)

mult (float)

keltner_dyn(src, lenEMA, lenATR, multATR)

Parameters:

src (float)

lenEMA (int)

lenATR (int)

multATR (float)

donchian_dyn(len)

Parameters:

len (int)

choppiness_index(len)

Parameters:

len (int)

vol_stop(lenATR, mult)

Parameters:

lenATR (int)

mult (float)

roc_dyn(src, len)

Parameters:

src (float)

len (int)

rsi_dyn(src, len)

Parameters:

src (float)

len (int)

stoch_dyn(kLen, dLen, smoothK)

Parameters:

kLen (int)

dLen (int)

smoothK (int)

stoch_rsi_dyn(rsiLen, stochLen, kSmooth, dLen)

Parameters:

rsiLen (int)

stochLen (int)

kSmooth (int)

dLen (int)

cci_dyn(src, len)

Parameters:

src (float)

len (int)

cmo_dyn(src, len)

Parameters:

src (float)

len (int)

trix_dyn(len)

Parameters:

len (int)

tsi_dyn(shortLen, longLen)

Parameters:

shortLen (int)

longLen (int)

ultimate_osc(len1, len2, len3)

Parameters:

len1 (int)

len2 (int)

len3 (int)

dpo_dyn(src, len)

Parameters:

src (float)

len (int)

willr_dyn(len)

Parameters:

len (int)

macd_dyn(src, fastLen, slowLen, sigLen)

Parameters:

src (float)

fastLen (int)

slowLen (int)

sigLen (int)

ppo_dyn(src, fastLen, slowLen, sigLen)

Parameters:

src (float)

fastLen (int)

slowLen (int)

sigLen (int)

aroon_dyn(len)

Parameters:

len (int)

dmi_adx_dyn(diLen, adxLen)

Parameters:

diLen (int)

adxLen (int)

vortex_dyn(len)

Parameters:

len (int)

coppock_dyn(rocLen1, rocLen2, wmaLen)

Parameters:

rocLen1 (int)

rocLen2 (int)

wmaLen (int)

rvi_dyn(len)

Parameters:

len (int)

price_osc_dyn(src, fastLen, slowLen)

Parameters:

src (float)

fastLen (int)

slowLen (int)

rci_dyn(src, len)

Parameters:

src (float)

len (int)

obv()

pvt()

cmf_dyn(len)

Parameters:

len (int)

adl()

chaikin_osc_dyn(fastLen, slowLen)

Parameters:

fastLen (int)

slowLen (int)

mfi_dyn(len)

Parameters:

len (int)

volume_osc_dyn(fastLen, slowLen)

Parameters:

fastLen (int)

slowLen (int)

up_down_volume()

cvd()

supertrend_dyn(atrLen, mult)

Parameters:

atrLen (int)

mult (float)

envelopes_dyn(src, len, pct)

Parameters:

src (float)

len (int)

pct (float)

linreg_line_slope(src, len)

Parameters:

src (float)

len (int)

lsma_dyn(src, len)

Parameters:

src (float)

len (int)

corrcoef_dyn(a, b, len)

Parameters:

a (float)

b (float)

len (int)

psar(step, maxStep)

Parameters:

step (float)

maxStep (float)

pivots_standard()

williams_alligator(src, jawLen, teethLen, lipsLen)

Parameters:

src (float)

jawLen (int)

teethLen (int)

lipsLen (int)

twap_dyn(src, len)

Parameters:

src (float)

len (int)

vwap_anchored(price, volume, reset)

Parameters:

price (float)

volume (float)

reset (bool)

performance_pct(len)

Parameters:

len (int)

AlgebraGeometryLabLibrary "AlgebraGeometryLab"

Algebra & 2D geometry utilities absent from Pine built-ins.

Rigorous, no-repaint, export-ready: vectors, robust roots, linear solvers, 2x2/3x3 det/inverse,

symmetric 2x2 eigensystem, orthogonal regression (TLS), affine transforms, intersections,

distances, projections, polygon metrics, point-in-polygon, convex hull (monotone chain),

Bezier/Catmull-Rom/Barycentric tools.

clamp(x, lo, hi)

clamp to

Parameters:

x (float)

lo (float)

hi (float)

near(a, b, atol, rtol)

approximately equal with relative+absolute tolerance

Parameters:

a (float)

b (float)

atol (float)

rtol (float)

sgn(x)

sign as {-1,0,1}

Parameters:

x (float)

hypot(x, y)

stable hypot (sqrt(x^2+y^2))

Parameters:

x (float)

y (float)

method length(v)

Namespace types: Vec2

Parameters:

v (Vec2)

method length2(v)

Namespace types: Vec2

Parameters:

v (Vec2)

method normalized(v)

Namespace types: Vec2

Parameters:

v (Vec2)

method add(a, b)

Namespace types: Vec2

Parameters:

a (Vec2)

b (Vec2)

method sub(a, b)

Namespace types: Vec2

Parameters:

a (Vec2)

b (Vec2)

method muls(v, s)

Namespace types: Vec2

Parameters:

v (Vec2)

s (float)

method dot(a, b)

Namespace types: Vec2

Parameters:

a (Vec2)

b (Vec2)

method crossz(a, b)

Namespace types: Vec2

Parameters:

a (Vec2)

b (Vec2)

method rotate(v, ang)

Namespace types: Vec2

Parameters:

v (Vec2)

ang (float)

method apply(v, T)

Namespace types: Vec2

Parameters:

v (Vec2)

T (Affine2)

affine_identity()

identity transform

affine_translate(tx, ty)

translation

Parameters:

tx (float)

ty (float)

affine_rotate(ang)

rotation about origin

Parameters:

ang (float)

affine_scale(sx, sy)

scaling about origin

Parameters:

sx (float)

sy (float)

affine_rotate_about(ang, px, py)

rotation about pivot (px,py)

Parameters:

ang (float)

px (float)

py (float)

affine_compose(T2, T1)

compose T2∘T1 (apply T1 then T2)

Parameters:

T2 (Affine2)

T1 (Affine2)

quadratic_roots(a, b, c)

Real roots of ax^2 + bx + c = 0 (numerically stable)

Parameters:

a (float)

b (float)

c (float)

Returns: with n∈{0,1,2}; r1<=r2 when n=2.

cubic_roots(a, b, c, d)

Real roots of ax^3+bx^2+cx+d=0 (Cardano; returns up to 3 real roots)

Parameters:

a (float)

b (float)

c (float)

d (float)

Returns: (valid r2/r3 only if n>=2/n>=3)

det2(a, b, c, d)

det2 of

Parameters:

a (float)

b (float)

c (float)

d (float)

inv2(a, b, c, d)

inverse of 2x2; returns

Parameters:

a (float)

b (float)

c (float)

d (float)

solve2(a, b, c, d, e, f)

solve 2x2 * = via Cramer

Parameters:

a (float)

b (float)

c (float)

d (float)

e (float)

f (float)

det3(a11, a12, a13, a21, a22, a23, a31, a32, a33)

det3 of 3x3

Parameters:

a11 (float)

a12 (float)

a13 (float)

a21 (float)

a22 (float)

a23 (float)

a31 (float)

a32 (float)

a33 (float)

inv3(a11, a12, a13, a21, a22, a23, a31, a32, a33)

inverse 3x3; returns

Parameters:

a11 (float)

a12 (float)

a13 (float)

a21 (float)

a22 (float)

a23 (float)

a31 (float)

a32 (float)

a33 (float)

eig2_symmetric(a, b, d)

symmetric 2x2 eigensystem: [ , ]

Parameters:

a (float)

b (float)

d (float)

Returns: with unit eigenvectors

tls_line(xs, ys)

Orthogonal (total least squares) regression line through point cloud

Input arrays must be same length N>=2. Returns line in normal form n•x + c = 0

Parameters:

xs (array)

ys (array)

Returns: where (nx,ny) unit normal; (cx,cy) centroid.

orient(a, b, c)

orientation (signed area*2): >0 CCW, <0 CW, 0 collinear

Parameters:

a (Vec2)

b (Vec2)

c (Vec2)

project_point_line(p, a, d)

project point p onto infinite line through a with direction d

Parameters:

p (Vec2)

a (Vec2)

d (Vec2)

Returns: where proj = a + t*d

closest_point_segment(p, a, b)

closest point on segment to p

Parameters:

p (Vec2)

a (Vec2)

b (Vec2)

Returns: where t∈ on segment

dist_point_line(p, a, d)

distance from point to line (infinite)

Parameters:

p (Vec2)

a (Vec2)

d (Vec2)

dist_point_segment(p, a, b)

distance from point to segment

Parameters:

p (Vec2)

a (Vec2)

b (Vec2)

intersect_lines(p1, d1, p2, d2)

line-line intersection: L1: p1+d1*t, L2: p2+d2*u

Parameters:

p1 (Vec2)

d1 (Vec2)

p2 (Vec2)

d2 (Vec2)

Returns:

intersect_segments(s1, s2)

segment-segment intersection (closed segments)

Parameters:

s1 (Segment2)

s2 (Segment2)

Returns: where kind: 0=no, 1=proper point, 2=overlap (ix/iy=na)

circumcircle(a, b, c)

circle through 3 non-collinear points

Parameters:

a (Vec2)

b (Vec2)

c (Vec2)

intersect_circle_line(C, p, d)

intersections of circle and line (param p + d t)

Parameters:

C (Circle2)

p (Vec2)

d (Vec2)

Returns: with n∈{0,1,2}

intersect_circles(A, B)

circle-circle intersection

Parameters:

A (Circle2)

B (Circle2)

Returns: with n∈{0,1,2}

polygon_area(xs, ys)

signed area (shoelace). Positive if CCW.

Parameters:

xs (array)

ys (array)

polygon_centroid(xs, ys)

polygon centroid (for non-self-intersecting). Fallback to vertex mean if area≈0.

Parameters:

xs (array)

ys (array)

point_in_polygon(px, py, xs, ys)

point-in-polygon test (ray casting). Returns true if inside; boundary counts as inside.

Parameters:

px (float)

py (float)

xs (array)

ys (array)

convex_hull(xs, ys)

convex hull (monotone chain). Returns array of hull vertex indices in CCW order.

Uses array.sort_indices(xs) (ascending by x). Ties on x are handled; result is deterministic.

Parameters:

xs (array)

ys (array)

lerp(a, b, t)

linear interpolate between a and b

Parameters:

a (float)

b (float)

t (float)

bezier2(p0, p1, p2, t)

quadratic Bezier B(t) for points p0,p1,p2

Parameters:

p0 (Vec2)

p1 (Vec2)

p2 (Vec2)

t (float)

bezier3(p0, p1, p2, p3, t)

cubic Bezier B(t) for p0,p1,p2,p3

Parameters:

p0 (Vec2)

p1 (Vec2)

p2 (Vec2)

p3 (Vec2)

t (float)

catmull_rom(p0, p1, p2, p3, t, alpha)

Catmull-Rom interpolation (centripetal form when alpha=0.5)

t∈ , returns point between p1 and p2

Parameters:

p0 (Vec2)

p1 (Vec2)

p2 (Vec2)

p3 (Vec2)

t (float)

alpha (float)

barycentric(A, B, C, P)

barycentric coordinates of P wrt triangle ABC

Parameters:

A (Vec2)

B (Vec2)

C (Vec2)

P (Vec2)

Returns:

point_in_triangle(A, B, C, P)

point-in-triangle using barycentric (boundary included)

Parameters:

A (Vec2)

B (Vec2)

C (Vec2)

P (Vec2)

Vec2

Fields:

x (series float)

y (series float)

Line2

Fields:

p (Vec2)

d (Vec2)

Segment2

Fields:

a (Vec2)

b (Vec2)

Circle2

Fields:

c (Vec2)

r (series float)

Affine2

Fields:

a (series float)

b (series float)

c (series float)

d (series float)

tx (series float)

ty (series float)

ema 狀態機Library "ema_flow_lib"

ema_flow_state(e10, e20, e100, entanglePct, farPct, e10_prev, e20_prev)

Parameters:

e10 (float)

e20 (float)

e100 (float)

entanglePct (float)

farPct (float)

e10_prev (float)

e20_prev (float)

state_name(s)

Parameters:

s (int)

phx_liq_tlLibrary "phx_liq_tl"

new_state()

update(st, len, cup, cdn, space, proximity_pct, shs)

Parameters:

st (LTState)

len (int)

cup (color)

cdn (color)

space (float)

proximity_pct (float)

shs (bool)

LTState

Fields:

upln (array)

dnln (array)

upBroken (series bool)

dnBroken (series bool)

phx_kroLibrary "phx_kro"

compute(src, bandwidth, bbwidth, sdLook, sdMult, obos_mult)

Parameters:

src (float)

bandwidth (int)

bbwidth (float)

sdLook (int)

sdMult (float)

obos_mult (float)

start_flags(src, bandwidth, bbwidth)

Parameters:

src (float)

bandwidth (int)

bbwidth (float)

KROFeed

Fields:

Wave (series float)

is_green (series bool)

is_red (series bool)

band_width (series float)

band_width_sma (series float)

band_width_std (series float)

is_hyper_wide (series bool)

wave_sma (series float)

wave_std (series float)

wave_ob_threshold (series float)

wave_os_threshold (series float)

is_overbought (series bool)

is_oversold (series bool)

is_oversold_confirmed (series bool)

is_overbought_confirmed (series bool)

enhanced_os_confirmed (series bool)

enhanced_ob_confirmed (series bool)

triple_green_transition (series bool)

triple_red_transition (series bool)

startwave_bull (series bool)

startwave_bear (series bool)

phx_fvgfvg generator 4h and current time frame

library to import fvg from 4h with midle line and proximity support and resistance

JK_Traders_Reality_LibLibrary "JK_Traders_Reality_Lib"

This library contains common elements used in Traders Reality scripts

calcPvsra(pvsraVolume, pvsraHigh, pvsraLow, pvsraClose, pvsraOpen, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor, darkGreyCandleColor, lightGrayCandleColor)

calculate the pvsra candle color and return the color as well as an alert if a vector candle has apperared.

Situation "Climax"

Bars with volume >= 200% of the average volume of the 10 previous chart TFs, or bars

where the product of candle spread x candle volume is >= the highest for the 10 previous

chart time TFs.

Default Colors: Bull bars are green and bear bars are red.

Situation "Volume Rising Above Average"

Bars with volume >= 150% of the average volume of the 10 previous chart TFs.

Default Colors: Bull bars are blue and bear are violet.

Parameters:

pvsraVolume (float) : the instrument volume series (obtained from request.sequrity)

pvsraHigh (float) : the instrument high series (obtained from request.sequrity)

pvsraLow (float) : the instrument low series (obtained from request.sequrity)

pvsraClose (float) : the instrument close series (obtained from request.sequrity)

pvsraOpen (float) : the instrument open series (obtained from request.sequrity)

redVectorColor (simple color) : red vector candle color

greenVectorColor (simple color) : green vector candle color

violetVectorColor (simple color) : violet/pink vector candle color

blueVectorColor (simple color) : blue vector candle color

darkGreyCandleColor (simple color) : regular volume candle down candle color - not a vector

lightGrayCandleColor (simple color) : regular volume candle up candle color - not a vector

@return

adr(length, barsBack)

Parameters:

length (simple int) : how many elements of the series to calculate on

barsBack (simple int) : starting possition for the length calculation - current bar or some other value eg last bar

@return adr the adr for the specified lenght

adrHigh(adr, fromDo)

Calculate the ADR high given an ADR

Parameters:

adr (float) : the adr

fromDo (simple bool) : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adrHigh the position of the adr high in price

adrLow(adr, fromDo)

Parameters:

adr (float) : the adr

fromDo (simple bool) : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adrLow the position of the adr low in price

splitSessionString(sessXTime)

given a session in the format 0000-0100:23456 split out the hours and minutes

Parameters:

sessXTime (simple string) : the session time string usually in the format 0000-0100:23456

@return

calcSessionStartEnd(sessXTime, gmt)

calculate the start and end timestamps of the session

Parameters:

sessXTime (simple string) : the session time string usually in the format 0000-0100:23456

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

@return

drawOpenRange(sessXTime, sessXcol, showOrX, gmt)

draw open range for a session

Parameters:

sessXTime (simple string) : session string in the format 0000-0100:23456

sessXcol (simple color) : the color to be used for the opening range box shading

showOrX (simple bool) : boolean flag to toggle displaying the opening range

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

@return void

drawSessionHiLo(sessXTime, showRectangleX, showLabelX, sessXcolLabel, sessXLabel, gmt, sessionLineStyle)

Parameters:

sessXTime (simple string) : session string in the format 0000-0100:23456

showRectangleX (simple bool)

showLabelX (simple bool)

sessXcolLabel (simple color) : the color to be used for the hi/low lines and label

sessXLabel (simple string) : the session label text

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

sessionLineStyle (simple string) : the line stile for the session high low lines

@return void

calcDst()

calculate market session dst on/off flags

@return indicating if DST is on or off for a particular region

timestampPreviousDayOfWeek(previousDayOfWeek, hourOfDay, gmtOffset, oneWeekMillis)

Timestamp any of the 6 previous days in the week (such as last Wednesday at 21 hours GMT)

Parameters:

previousDayOfWeek (simple string) : Monday or Satruday

hourOfDay (simple int) : the hour of the day when psy calc is to start

gmtOffset (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

oneWeekMillis (simple int) : the amount if time for a week in milliseconds

@return the timestamp of the psy level calculation start time

getdayOpen()

get the daily open - basically exchange midnight

@return the daily open value which is float price

newBar(res)

new_bar: check if we're on a new bar within the session in a given resolution

Parameters:

res (simple string) : the desired resolution

@return true/false is a new bar for the session has started

toPips(val)

to_pips Convert value to pips

Parameters:

val (float) : the value to convert to pips

@return the value in pips

rLabel(ry, rtext, rstyle, rcolor, valid, labelXOffset)

a function that draws a right aligned lable for a series during the current bar

Parameters:

ry (float) : series float the y coordinate of the lable

rtext (simple string) : the text of the label

rstyle (simple string) : the style for the lable

rcolor (simple color) : the color for the label

valid (simple bool) : a boolean flag that allows for turning on or off a lable

labelXOffset (int) : how much to offset the label from the current position

rLabelOffset(ry, rtext, rstyle, rcolor, valid, labelOffset)

a function that draws a right aligned lable for a series during the current bar

Parameters:

ry (float) : series float the y coordinate of the lable

rtext (string) : the text of the label

rstyle (simple string) : the style for the lable

rcolor (simple color) : the color for the label

valid (simple bool) : a boolean flag that allows for turning on or off a lable

labelOffset (int)

rLabelLastBar(ry, rtext, rstyle, rcolor, valid, labelXOffset)

a function that draws a right aligned lable for a series only on the last bar

Parameters:

ry (float) : series float the y coordinate of the lable

rtext (string) : the text of the label

rstyle (simple string) : the style for the lable

rcolor (simple color) : the color for the label

valid (simple bool) : a boolean flag that allows for turning on or off a lable

labelXOffset (int) : how much to offset the label from the current position

drawLine(xSeries, res, tag, xColor, xStyle, xWidth, xExtend, isLabelValid, xLabelOffset, validTimeFrame)

a function that draws a line and a label for a series

Parameters:

xSeries (float) : series float the y coordinate of the line/label

res (simple string) : the desired resolution controlling when a new line will start

tag (simple string) : the text for the lable

xColor (simple color) : the color for the label

xStyle (simple string) : the style for the line

xWidth (simple int) : the width of the line

xExtend (simple string) : extend the line

isLabelValid (simple bool) : a boolean flag that allows for turning on or off a label

xLabelOffset (int)

validTimeFrame (simple bool) : a boolean flag that allows for turning on or off a line drawn

drawLineDO(xSeries, res, tag, xColor, xStyle, xWidth, xExtend, isLabelValid, xLabelOffset, validTimeFrame)

a function that draws a line and a label for the daily open series

Parameters:

xSeries (float) : series float the y coordinate of the line/label

res (simple string) : the desired resolution controlling when a new line will start

tag (simple string) : the text for the lable

xColor (simple color) : the color for the label

xStyle (simple string) : the style for the line

xWidth (simple int) : the width of the line

xExtend (simple string) : extend the line

isLabelValid (simple bool) : a boolean flag that allows for turning on or off a label

xLabelOffset (int)

validTimeFrame (simple bool) : a boolean flag that allows for turning on or off a line drawn

drawPivot(pivotLevel, res, tag, pivotColor, pivotLabelColor, pivotStyle, pivotWidth, pivotExtend, isLabelValid, validTimeFrame, levelStart, pivotLabelXOffset)

draw a pivot line - the line starts one day into the past

Parameters:

pivotLevel (float) : series of the pivot point

res (simple string) : the desired resolution

tag (simple string) : the text to appear

pivotColor (simple color) : the color of the line

pivotLabelColor (simple color) : the color of the label

pivotStyle (simple string) : the line style

pivotWidth (simple int) : the line width

pivotExtend (simple string) : extend the line

isLabelValid (simple bool) : boolean param allows to turn label on and off

validTimeFrame (simple bool) : only draw the line and label at a valid timeframe

levelStart (int) : basically when to start drawing the levels

pivotLabelXOffset (int) : how much to offset the label from its current postion

@return the pivot line series

getPvsraFlagByColor(pvsraColor, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor, lightGrayCandleColor)

convert the pvsra color to an internal code

Parameters:

pvsraColor (color) : the calculated pvsra color

redVectorColor (simple color) : the user defined red vector color

greenVectorColor (simple color) : the user defined green vector color

violetVectorColor (simple color) : the user defined violet vector color

blueVectorColor (simple color) : the user defined blue vector color

lightGrayCandleColor (simple color) : the user defined regular up candle color

@return pvsra internal code

updateZones(pvsra, direction, boxArr, maxlevels, pvsraHigh, pvsraLow, pvsraOpen, pvsraClose, transperancy, zoneupdatetype, zonecolor, zonetype, borderwidth, coloroverride, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor)

a function that draws the unrecovered vector candle zones

Parameters:

pvsra (int) : internal code

direction (simple int) : above or below the current pa

boxArr (array) : the array containing the boxes that need to be updated

maxlevels (simple int) : the maximum number of boxes to draw

pvsraHigh (float) : the pvsra high value series

pvsraLow (float) : the pvsra low value series

pvsraOpen (float) : the pvsra open value series

pvsraClose (float) : the pvsra close value series

transperancy (simple int) : the transparencfy of the vecor candle zones

zoneupdatetype (simple string) : the zone update type

zonecolor (simple color) : the zone color if overriden

zonetype (simple string) : the zone type

borderwidth (simple int) : the width of the border

coloroverride (simple bool) : if the color overriden

redVectorColor (simple color) : the user defined red vector color

greenVectorColor (simple color) : the user defined green vector color

violetVectorColor (simple color) : the user defined violet vector color

blueVectorColor (simple color) : the user defined blue vector color

cleanarr(arr)

clean an array from na values

Parameters:

arr (array) : the array to clean

@return if the array was cleaned

calcPsyLevels(oneWeekMillis, showPsylevels, psyType, sydDST)

calculate the psy levels

4 hour res based on how mt4 does it

mt4 code

int Li_4 = iBarShift(NULL, PERIOD_H4, iTime(NULL, PERIOD_W1, Li_0)) - 2 - Offset;

ObjectCreate("PsychHi", OBJ_TREND, 0, Time , iHigh(NULL, PERIOD_H4, iHighest(NULL, PERIOD_H4, MODE_HIGH, 2, Li_4)), iTime(NULL, PERIOD_W1, 0), iHigh(NULL, PERIOD_H4,

iHighest(NULL, PERIOD_H4, MODE_HIGH, 2, Li_4)));

so basically because the session is 8 hours and we are looking at a 4 hour resolution we only need to take the highest high an lowest low of 2 bars

we use the gmt offset to adjust the 0000-0800 session to Sydney open which is at 2100 during dst and at 2200 otherwize. (dst - spring foward, fall back)

keep in mind sydney is in the souther hemisphere so dst is oposite of when london and new york go into dst

Parameters:

oneWeekMillis (simple int) : a constant value

showPsylevels (simple bool) : should psy levels be calculated

psyType (simple string) : the type of Psylevels - crypto or forex

sydDST (bool) : is Sydney in DST

@return

adrHiLo(length, barsBack, fromDO)

Parameters:

length (simple int) : how many elements of the series to calculate on

barsBack (simple int) : starting possition for the length calculation - current bar or some other value eg last bar

fromDO (simple bool) : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adr, adrLow and adrHigh - the adr, the position of the adr High and adr Low with respect to price

drawSessionHiloLite(sessXTime, showRectangleX, showLabelX, sessXcolLabel, sessXLabel, gmt, sessionLineStyle, sessXcol)

Parameters:

sessXTime (simple string) : session string in the format 0000-0100:23456

showRectangleX (simple bool)

showLabelX (simple bool)

sessXcolLabel (simple color) : the color to be used for the hi/low lines and label

sessXLabel (simple string) : the session label text

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

sessionLineStyle (simple string) : the line stile for the session high low lines

sessXcol (simple color) : - the color for the box color that will color the session

@return void

msToHmsString(ms)

converts milliseconds into an hh:mm string. For example, 61000 ms to '0:01:01'

Parameters:

ms (int) : - the milliseconds to convert to hh:mm

@return string - the converted hh:mm string

countdownString(openToday, closeToday, showMarketsWeekends, oneDay)

that calculates how much time is left until the next session taking the session start and end times into account. Note this function does not work on intraday sessions.

Parameters:

openToday (int) : - timestamps of when the session opens in general - note its a series because the timestamp was created using the dst flag which is a series itself thus producing a timestamp series

closeToday (int) : - timestamp of when the session closes in general - note its a series because the timestamp was created using the dst flag which is a series itself thus producing a timestamp series

@return a countdown of when next the session opens or 'Open' if the session is open now

showMarketsWeekends (simple bool)

oneDay (simple int)

countdownStringSyd(sydOpenToday, sydCloseToday, showMarketsWeekends, oneDay)

that calculates how much time is left until the next session taking the session start and end times into account. special case of intraday sessions like sydney

Parameters:

sydOpenToday (int)

sydCloseToday (int)

showMarketsWeekends (simple bool)

oneDay (simple int)

Market Structure Report Library [TradingFinder]🔵 Introduction

Market Structure is one of the most fundamental concepts in Price Action and Smart Money theory. In simple terms, it represents how price moves between highs and lows and reveals which phase of the market cycle we are currently in uptrend, downtrend, or transition.

Each structure in the market is formed by a combination of Breaks of Structure (BoS) and Changes of Character (CHoCH) :

BoS occurs when the market breaks a previous high or low, confirming the continuation of the current trend.

CHoCH occurs when price breaks in the opposite direction for the first time, signaling a potential trend reversal.

Since price movement is inherently fractal, market structure can be analyzed on two distinct levels :

Major / External Structure: represents the dominant macro trend.

Minor / Internal Structure: represents corrective or smaller-scale movements within the larger trend.

🔵 Library Purpose

The “Market Structure Report Library” is designed to automatically detect the current market structure type in real time.

Without drawing or displaying any visuals, it analyzes raw price data and returns a series of logical and textual outputs (Return Values) that describe the current structural state of the market.

It provides the following information :

Trend Type :

External Trend (Major): Up Trend, Down Trend, No Trend

Internal Trend (Minor): Up Trend, Down Trend, No Trend

Structure Type :

BoS : Confirms trend continuation

CHoCH : Indicates a potential trend reversal

Consecutive BoS Counter : Measures trend strength on both Major and Minor levels.

Candle Type : Returns the current candle’s condition(Bullish, Bearish, Doji)

This library is specifically designed for use in Smart Money–based screeners, indicators, and algorithmic strategies.

It can analyze multiple symbols and timeframes simultaneously and return the exact structure type (BoS or CHoCH) and trend direction for each.

🔵 Function Outputs

The function MS() processes the price data and returns seven key outputs,

each representing a distinct structural state of the market. These values can be used in indicators, strategies, or multi-symbol screeners.

🟣 ExternalTrend

Type : string

Description : Represents the direction of the Major (External) market structure.

Possible values :

Up Trend

Down Trend

No Trend

This is determined based on the behavior of Major Pivots (swing highs/lows).

🟣 InternalTrend

Type : string

Description : Represents the direction of the Minor (Internal) market structure.

Possible values :

Up Trend

Down Trend

No Trend

🟣 M_State

Type : string

Description : Specifies the type of the latest Major Structure event.

Possible values :

BoS

CHoCH

🟣 m_State

Type : string

Description : Specifies the type of the latest Minor Structure event.

Possible values :

BoS

CHoCH

🟣 MBoS_Counter

Type : integer

Description : Counts the number of consecutive structural breaks (BoS) in the Major structure.

Useful for evaluating trend strength :

Increasing count: indicates trend continuation.

Reset to zero: typically occurs after a CHoCH.

🟣 mBoS_Counter

Type : integer

Description : Counts the number of consecutive structural breaks in the Minor structure.

Helps analyze the micro structure of the market on lower timeframes.

Higher value : strong internal trend.

Reset : indicates a minor pullback or reversal.

🟣 Candle_Type

Type : string

Description : Represents the type of the current candle.

Possible values :

Bullish

Bearish

Doji

import TFlab/Market_Structure_Report_Library_TradingFinder/1 as MSS

PP = input.int (5 , 'Market Structure Pivot Period' , group = 'Symbol 1' )

= MSS.MS(PP)

SequencerLibraryLibrary "SequencerLibrary"

SequencerLibrary v1 is a Pine Script™ library for identifying, tracking, and visualizing

sequential bullish and bearish patterns on price charts.

It provides a complete framework for building sequence-based trading systems, including:

• Automatic detection and counting of setup and countdown phases.

• Real-time tracking of completion states, perfected setups, and exhaustion signals.

• Dynamic support and resistance thresholds derived from recent price structure.

• Customizable visual highlighting for both setup and countdown sequences.

method doSequence(s, src, config, condition)

Updates the sequence state based on the source value, and user configuration.

Namespace types: Sequence

Parameters:

s (Sequence) : The sequence object containing bullish and bearish setups.

src (float) : The source value (e.g., close price) used for evaluating sequence conditions.

config (SequenceInputs) : The user-defined settings for sequence analysis.

condition (bool) : When true, executes the sequence logic.

Returns:

highlight(s, css, condition)

Highlights the bullish and bearish sequence setups and countdowns on the chart.

Parameters:

s (Sequence) : The sequence object containing bullish and bearish sequence states.

css (SequenceCSS) : The styling configuration for customizing label appearances.

condition (bool) : When true, the function creates and displays labels for setups and countdowns.

Returns:

SequenceState

A type representing the configuration and state of a sequence setup.

Fields:

setup (series int) : Current count of the setup phase (e.g., how many bars have met the setup criteria).

countdown (series int) : Current count of the countdown phase (e.g., bars meeting countdown criteria).

threshold (series float) : The price threshold level used as support/resistance for the sequence.

priceWhenCompleted (series float) : The closing price when the setup or countdown phase is completed.

indicatorWhenCompleted (series float) : The indicator value when the setup or countdown phase is completed.

setupCompleted (series bool) : Indicates if the setup phase has been completed (i.e., reached the required count).

countdownCompleted (series bool) : Indicates if the countdown phase has been completed (i.e., reached exhaustion).

perfected (series bool) : Indicates if the setup meets the "perfected" condition (e.g., aligns with strict criteria).

highlightSetup (series bool) : Determines whether the setup phase should be visually highlighted on the chart.

highlightCountdown (series bool) : Determines whether the countdown phase should be visually highlighted on the chart.

Sequence

A type containing bullish and bearish sequence setups.

Fields:

bullish (SequenceState) : Configuration and state for bullish sequences.

bearish (SequenceState) : Configuration and state for bearish sequences.

SequenceInputs

A type for user-configurable input settings for sequence-based analysis.

Fields:

showSetup (series bool) : Enables or disables the display of setup sequences.

showCountdown (series bool) : Enables or disables the display of countdown sequences.

setupFilter (series string) : A comma‐separated string containing setup sequence counts to be highlighted (e.g., "1,2,3,4,5,6,7,8,9").

countdownFilter (series string) : A comma‐separated string containing countdown sequence counts to be highlighted (e.g., "1,2,3,4,5,6,7,8,9,10,11,12,13").

lookbackSetup (series int) : Defines the lookback period for evaluating setup conditions (default: 4 bars).

lookbackCountdown (series int) : Defines the lookback period for evaluating countdown conditions (default: 2 bars).

lookbackSetupPerfected (series int) : Defines the lookback period to determine a perfected setup condition (default: 6 bars).

maxSetup (series int) : The maximum count required to complete a setup phase (default: 9).

maxCountdown (series int) : The maximum count required to complete a countdown phase (default: 13).

SequenceCSS

A type defining the visual styling options for sequence labels.

Fields:

bullish (series color) : Color used for bullish sequence labels.

bearish (series color) : Color used for bearish sequence labels.

imperfect (series color) : Color used for labels representing imperfect sequences.

GBB_lib_utilsLibrary "GBB_lib_utils"

gbb_moving_average_source(_source, _length, _ma_type)

gbb_moving_average_source

@description Calculates the moving average of a source series.

Parameters:

_source (float) : (series float)

_length (simple int) : (int)

_ma_type (string) : (string)

Returns: (series) Moving average series

gbb_tf_to_display(tf_minutes, tf_string)

gbb_tf_to_display

@description Converts minutes and TF string into a short standard label.

Parameters:

tf_minutes (float) : (float)

tf_string (string) : (string)

Returns: (string) Timeframe label (M1,H1,D1,...)

gbb_convert_bars(_bars)

gbb_convert_bars

@description Formats a number of bars into a duration (days, hours, minutes + bar count).

Parameters:

_bars (int) : (int)

Returns: (string)

gbb_goldorak_init(_tf5Levels_input)

gbb_goldorak_init

@description Builds a contextual message about the current timeframe and optional 5-level TF.

Parameters:

_tf5Levels_input (string) : (string) Alternative timeframe ("" = current timeframe).

Returns: (string, string, float)

CarolTradeLibLibrary "CarolTradeLib"

f_generateSignalID(strategyName)

Parameters:

strategyName (string)

f_buildJSON(orderType, action, symbol, price, strategyName, apiKey, additionalFields, indicatorJSON)

Parameters:

orderType (string)

action (string)

symbol (string)

price (float)

strategyName (string)

apiKey (string)

additionalFields (string)

indicatorJSON (string)

sendSignal(action, symbol, price, strategyName, apiKey, indicatorJSON)

Parameters:

action (string)

symbol (string)

price (float)

strategyName (string)

apiKey (string)

indicatorJSON (string)

marketOrder(action, symbol, price, strategyName, apiKey, stopLoss, takeProfit, rrRatio, size, indicatorJSON)

Parameters:

action (string)

symbol (string)

price (float)

strategyName (string)

apiKey (string)

stopLoss (float)

takeProfit (float)

rrRatio (float)

size (float)

indicatorJSON (string)

limitOrder(action, symbol, price, strategyName, apiKey, limitPrice, size, indicatorJSON)

Parameters:

action (string)

symbol (string)

price (float)

strategyName (string)

apiKey (string)

limitPrice (float)

size (float)

indicatorJSON (string)

stopLimitOrder(action, symbol, price, strategyName, apiKey, stopPrice, limitPrice, size, indicatorJSON)

Parameters:

action (string)

symbol (string)

price (float)

strategyName (string)

apiKey (string)

stopPrice (float)

limitPrice (float)

size (float)

indicatorJSON (string)

TrailingStopLossLibrary "TrailingStopLoss"

简易追踪止损; 未充分测试,欢迎提交issue

drawdown_percent(entry_bar_index, direction_long)

drawdown_percent: 回撤百分比

Parameters:

entry_bar_index (int)

direction_long (bool)

Returns: percentage: 回撤百分比 > 0

closure_needed(entry_bar_index, initial_sl_price, percentage_ts, num_bars_tolerance, extra_drawdown_distance)

closure_needed: 是否满足平仓条件

Parameters:

entry_bar_index (int)

initial_sl_price (float)

percentage_ts (float)

num_bars_tolerance (int)

extra_drawdown_distance (float)

Returns: do_closure: bool 是否平仓

PubLibPivotLibrary "PubLibPivot"

Pivot detection library for harmonic pattern analysis - Fractal and ZigZag methods with validation and utility functions

fractalPivotHigh(depth)

Fractal pivot high condition

Parameters:

depth (int)

Returns: bool

fractalPivotLow(depth)

Fractal pivot low condition

Parameters:

depth (int)

Returns: bool

fractalPivotHighPrice(depth, occurrence)

Get fractal pivot high price

Parameters:

depth (int)

occurrence (simple int)

Returns: float

fractalPivotLowPrice(depth, occurrence)

Get fractal pivot low price

Parameters:

depth (int)

occurrence (simple int)

Returns: float

fractalPivotHighBarIndex(depth, occurrence)

Get fractal pivot high bar index

Parameters:

depth (int)

occurrence (simple int)

Returns: int

fractalPivotLowBarIndex(depth, occurrence)

Get fractal pivot low bar index

Parameters:

depth (int)

occurrence (simple int)

Returns: int

zigzagPivotHigh(deviation, backstep, useATR, atrLength)

ZigZag pivot high condition

Parameters:

deviation (float)

backstep (int)

useATR (bool)

atrLength (simple int)

Returns: bool

zigzagPivotLow(deviation, backstep, useATR, atrLength)

ZigZag pivot low condition

Parameters:

deviation (float)

backstep (int)

useATR (bool)

atrLength (simple int)

Returns: bool

zigzagPivotHighPrice(deviation, backstep, useATR, atrLength, occurrence)

Get ZigZag pivot high price

Parameters:

deviation (float)

backstep (int)

useATR (bool)

atrLength (simple int)

occurrence (simple int)

Returns: float

zigzagPivotLowPrice(deviation, backstep, useATR, atrLength, occurrence)

Get ZigZag pivot low price

Parameters:

deviation (float)

backstep (int)

useATR (bool)

atrLength (simple int)

occurrence (simple int)

Returns: float

zigzagPivotHighBarIndex(deviation, backstep, useATR, atrLength, occurrence)

Get ZigZag pivot high bar index

Parameters:

deviation (float)

backstep (int)

useATR (bool)

atrLength (simple int)

occurrence (simple int)

Returns: int

zigzagPivotLowBarIndex(deviation, backstep, useATR, atrLength, occurrence)

Get ZigZag pivot low bar index

Parameters:

deviation (float)

backstep (int)

useATR (bool)

atrLength (simple int)

occurrence (simple int)

Returns: int

isValidPivotVolume(pivotPrice, pivotBarIndex, minVolumeRatio, volumeLength)

Validate pivot quality based on volume

Parameters:

pivotPrice (float)

pivotBarIndex (int)

minVolumeRatio (float)

volumeLength (int)

Returns: bool

isValidPivotATR(pivotPrice, lastPivotPrice, minATRMultiplier, atrLength)

Validate pivot based on minimum ATR movement

Parameters:

pivotPrice (float)

lastPivotPrice (float)

minATRMultiplier (float)

atrLength (simple int)

Returns: bool

isValidPivotTime(pivotBarIndex, lastPivotBarIndex, minBars)

Validate pivot based on minimum time between pivots

Parameters:

pivotBarIndex (int)

lastPivotBarIndex (int)

minBars (int)

Returns: bool

isPivotConfirmed(pivotBarIndex, depth)

Check if pivot is not repainting (confirmed)

Parameters:

pivotBarIndex (int)

depth (int)

Returns: bool

addPivotToArray(pivotArray, barArray, pivotPrice, pivotBarIndex, maxSize)

Add pivot to array with validation

Parameters:

pivotArray (array)

barArray (array)

pivotPrice (float)

pivotBarIndex (int)

maxSize (int)

Returns: array - updated pivot array

getPivotFromArray(pivotArray, barArray, index)

Get pivot from array by index

Parameters:

pivotArray (array)

barArray (array)

index (int)

Returns: tuple - (price, bar_index)

getPivotsInRange(pivotArray, barArray, startIndex, count)

Get all pivots in range

Parameters:

pivotArray (array)

barArray (array)

startIndex (int)

count (int)

Returns: tuple, array> - (prices, bar_indices)

pivotDistance(barIndex1, barIndex2)

Calculate distance between two pivots in bars

Parameters:

barIndex1 (int)

barIndex2 (int)

Returns: int - distance in bars

pivotPriceRatio(price1, price2)

Calculate price ratio between two pivots

Parameters:

price1 (float)

price2 (float)

Returns: float - price ratio

pivotRetracementRatio(startPrice, endPrice, currentPrice)

Calculate retracement ratio

Parameters:

startPrice (float)

endPrice (float)

currentPrice (float)

Returns: float - retracement ratio (0-1)

pivotExtensionRatio(startPrice, endPrice, currentPrice)

Calculate extension ratio

Parameters:

startPrice (float)

endPrice (float)

currentPrice (float)

Returns: float - extension ratio (>1 for extension)

isInFibZone(startPrice, endPrice, currentPrice, fibLevel, tolerance)

Check if price is in Fibonacci retracement zone

Parameters:

startPrice (float)

endPrice (float)

currentPrice (float)

fibLevel (float)

tolerance (float)

Returns: bool - true if in zone

getPivotType(pivotPrice, pivotBarIndex, lookback)

Get pivot type (high/low) based on surrounding prices

Parameters:

pivotPrice (float)

pivotBarIndex (int)

lookback (int)

Returns: string - "high", "low", or "unknown"

calculatePivotStrength(pivotPrice, pivotBarIndex, lookback)

Calculate pivot strength based on volume and price action

Parameters:

pivotPrice (float)

pivotBarIndex (int)

lookback (int)

Returns: float - strength score (0-100)