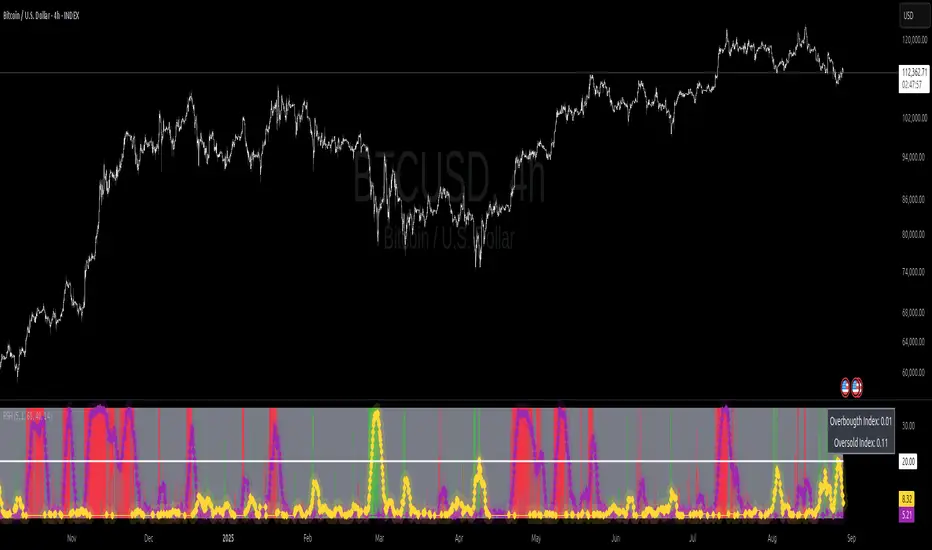

Relative Strength Heat [InvestorUnknown]The Relative Strength Heat (RSH) indicator is a relative strength of an asset across multiple RSI periods through a dynamic heatmap and provides smoothed signals for overbought and oversold conditions. The indicator is highly customizable, allowing traders to adjust RSI periods, smoothing methods, and visual settings to suit their trading strategies.

The RSH indicator is particularly useful for identifying momentum shifts and potential reversal points by aggregating RSI data across a range of periods. It presents this data in a visually intuitive heatmap, with color-coded bands indicating overbought (red), oversold (green), or neutral (gray) conditions. Additionally, it includes signal lines for overbought and oversold indices, which can be smoothed using RAW, SMA, or EMA methods, and a table displaying the current index values.

Features

Dynamic RSI Periods: Calculates RSI across 31 periods, starting from a user-defined base period and incrementing by a specified step.

Heatmap Visualization: Displays RSI strength as a color-coded heatmap, with red for overbought, green for oversold, and gray for neutral zones.

Customizable Smoothing: Offers RAW, SMA, or EMA smoothing for overbought and oversold signals.

Signal Lines: Plots scaled overbought (purple) and oversold (yellow) signal lines with a midline for reference.

Information Table: Displays real-time overbought and oversold index values in a table at the top-right of the chart.

User-Friendly Inputs: Allows customization of RSI source, period ranges, smoothing length, and colors.

How It Works

The RSH indicator aggregates RSI calculations across 31 periods, starting from the user-defined Starting Period and incrementing by the Period Increment. For each period, it computes the RSI and determines whether the asset is overbought (RSI > threshold_ob) or oversold (RSI < threshold_os). These states are stored in arrays (ob_array for overbought, os_array for oversold) and used to generate the following outputs:

Heatmap: The indicator plots 31 horizontal bands, each representing an RSI period. The color of each band is determined by the f_col function:

Red if the RSI for that period is overbought (>threshold_ob).

Green if the RSI is oversold (

Cari dalam skrip untuk " TABLE "

Straddle Charts - Live (Enhanced)Track options straddles with ease using the Straddle Charts - Live (Enhanced) indicator! Originally inspired by @mudraminer, this Pine Script v5 tool visualizes live call, put, and straddle prices for instruments like BANKNIFTY. Plotting call (green), put (red), and straddle (black) prices in a separate pane, it offers real-time insights for straddle strategy traders.

Key Features:

Live Data: Fetches 1-minute (customizable) option prices with error handling for invalid symbols.

Price Table: Displays call, put, straddle prices, and percentage change in a top-left table.

Volatility Alerts: Highlights bars with straddle price changes above a user-defined threshold (default 5%) with a yellow background and concise % labels.

Robust Design: Prevents plot errors with na checks and provides clear error messages.

How to Use: Input your call/put option symbols (e.g., NSE:NIFTY250814C24700), set the timeframe, and adjust the volatility threshold. Monitor straddle costs and volatility for informed trading decisions.

Perfect for options traders seeking a simple, reliable tool to track straddle performance. Check it out and share your feedback!

Money Risk Management with Trade Tracking

Overview

The Money Risk Management with Trade Tracking indicator is a powerful tool designed for traders on TradingView to simplify trade simulation and risk management. Unlike the TradingView Strategy Tester, which can be complex for beginners, this indicator provides an intuitive, beginner-friendly interface to evaluate trading strategies in a realistic manner, mirroring real-world trading conditions.

Built on the foundation of open-source contributions from LuxAlgo and TCP, this indicator integrates external indicator signals, overlays take-profit (TP) and stop-loss (SL) levels, and provides detailed money management analytics. It empowers traders to visualize potential profits, losses, and risk-reward ratios, making it easier to understand the financial outcomes of their strategies.

Key Features

Signal Integration: Seamlessly integrates with external long and short signals from other indicators, allowing traders to overlay TP/SL levels based on their preferred strategies.

Realistic Trade Simulation: Simulates trades as they would occur in real-world scenarios, accounting for initial capital, risk percentage, leverage, and compounding effects.

Money Management Dashboard: Displays critical metrics such as current capital, unrealized P&L, risk amount, potential profit, risk-reward ratio, and trade status in a customizable, beginner-friendly table.

TP/SL Visualization: Plots TP and SL levels on the chart with customizable styles (solid, dashed, dotted) and colors, along with optional labels for clarity.

Performance Tracking: Tracks total trades, win/loss counts, win rate, and profit factor, providing a clear overview of strategy performance.

Liquidation Risk Alerts: Warns traders if stop-loss levels risk liquidation based on leverage settings, enhancing risk awareness.

Benefits for Traders

Beginner-Friendly: Simplifies the complexities of the TradingView Strategy Tester, offering an intuitive interface for new traders to simulate and evaluate trades without confusion.

Real-World Insights: Helps traders understand the actual profit or loss potential of their strategies by factoring in capital, risk, and leverage, bridging the gap between theoretical backtesting and real-world execution.

Enhanced Decision-Making: Provides clear, real-time analytics on risk-reward ratios, unrealized P&L, and trade performance, enabling informed trading decisions.

Customizable and Flexible: Allows customization of TP/SL settings, table positions, colors, and sizes, catering to individual trader preferences.

Risk Management Focus: Encourages disciplined trading by highlighting risk amounts, potential profits, and liquidation risks, fostering better financial planning.

Why This Indicator Stands Out

Many traders struggle to translate backtested strategy results into real-world outcomes due to the abstract nature of percentage-based profitability metrics. This indicator addresses that challenge by providing a practical, user-friendly tool that simulates trades with real-world parameters like capital, leverage, and compounding. Its open-source nature ensures accessibility, while its integration with other indicators makes it versatile for various trading styles.

How to Use

Add to TradingView: Copy the Pine Script code into TradingView’s Pine Editor and add it to your chart.

Configure Inputs: Set your initial capital, risk percentage, leverage, and TP/SL values in the indicator settings. Select external long/short signal sources if integrating with other indicators.

Monitor Dashboards: Use the Money Management and Target Dashboard tables to track trade performance and risk metrics in real time.

Analyze Results: Review win rates, profit factors, and P&L to refine your trading strategy.

Credits

This indicator builds upon the open-source contributions of LuxAlgo and TCP , whose efforts in sharing their code have made this tool possible. Their dedication to the trading community is deeply appreciated.

Canuck Trading IndicatorOverview

The Canuck Trading Indicator is a versatile, overlay-based technical analysis tool designed to assist traders in identifying potential trading opportunities across various timeframes and market conditions. By combining multiple technical indicators—such as RSI, Bollinger Bands, EMAs, VWAP, MACD, Stochastic RSI, ADX, HMA, and candlestick patterns—the indicator provides clear visual signals for bullish and bearish entries, breakouts, long-term trends, and options strategies like cash-secured puts, straddles/strangles, iron condors, and short squeezes. It also incorporates 20-day and 200-day SMAs to detect Golden/Death Crosses and price positioning relative to these moving averages. A dynamic table displays key metrics, and customizable alerts help traders stay informed of market conditions.

Key Features

Multi-Timeframe Adaptability: Automatically adjusts parameters (e.g., ATR multiplier, ADX period, HMA length) based on the chart's timeframe (minute, hourly, daily, weekly, monthly) for optimal performance.

Comprehensive Signal Generation: Identifies short-term entries, breakouts, long-term bullish trends, and options strategies using a combination of momentum, trend, volatility, and candlestick patterns.

Candlestick Pattern Detection: Recognizes bullish/bearish engulfing, hammer, shooting star, doji, and strong candles for precise entry/exit signals.

Moving Average Analysis: Plots 20-day and 200-day SMAs, detects Golden/Death Crosses, and evaluates price position relative to these averages.

Dynamic Table: Displays real-time metrics, including zone status (bullish, bearish, neutral), RSI, MACD, Stochastic RSI, short/long-term trends, candlestick patterns, ADX, ROC, VWAP slope, and MA positioning.

Customizable Alerts: Over 20 alert conditions for entries, exits, overbought/oversold warnings, and MA crosses, with actionable messages including ticker, price, and suggested strategies.

Visual Clarity: Uses distinct shapes, colors, and sizes to plot signals (e.g., green triangles for bullish entries, red triangles for bearish entries) and overlays key levels like EMA, VWAP, Bollinger Bands, support/resistance, and HMA.

Options Strategy Signals: Suggests opportunities for selling cash-secured puts, straddles/strangles, iron condors, and capitalizing on short squeezes.

How to Use

Add to Chart: Apply the indicator to any TradingView chart by selecting "Canuck Trading Indicator" from the Pine Script library.

Interpret Signals:

Bullish Signals: Green triangles (short-term entry), lime diamonds (breakout), blue circles (long-term entry).

Bearish Signals: Red triangles (short-term entry), maroon diamonds (breakout).

Options Strategies: Purple squares (cash-secured puts), yellow circles (straddles/strangles), orange crosses (iron condors), white arrows (short squeezes).

Exits: X-cross shapes in corresponding colors indicate exit signals.

Monitor: Gray circles suggest holding cash or monitoring for setups.

Review Table: Check the top-right table for real-time metrics, including zone status, RSI, MACD, trends, and MA positioning.

Set Alerts: Configure alerts for specific signals (e.g., "Short-Term Bullish Entry" or "Golden Cross") to receive notifications via TradingView.

Adjust Inputs: Customize input parameters (e.g., RSI period, EMA length, ATR period) to suit your trading style or market conditions.

Input Parameters

The indicator offers a wide range of customizable inputs to fine-tune its behavior:

RSI Period (default: 14): Length for RSI calculation.

RSI Bullish Low/High (default: 35/70): RSI thresholds for bullish signals.

RSI Bearish High (default: 65): RSI threshold for bearish signals.

EMA Period (default: 15): Main EMA length (15 for day trading, 50 for swing).

Short/Long EMA Length (default: 3/20): For momentum oscillator.

T3 Smoothing Length (default: 5): Smooths momentum signals.

Long-Term EMA/RSI Length (default: 20/15): For long-term trend analysis.

Support/Resistance Lookback (default: 5): Periods for support/resistance levels.

MACD Fast/Slow/Signal (default: 12/26/9): MACD parameters.

Bollinger Bands Period/StdDev (default: 15/2): BB settings.

Stochastic RSI Period/Smoothing (default: 14/3/3): Stochastic RSI settings.

Uptrend/Short-Term/Long-Term Lookback (default: 2/2/5): Candles for trend detection.

ATR Period (default: 14): For volatility and price targets.

VWAP Sensitivity (default: 0.1%): Threshold for VWAP-based signals.

Volume Oscillator Period (default: 14): For volume surge detection.

Pattern Detection Threshold (default: 0.3%): Sensitivity for candlestick patterns.

ROC Period (default: 3): Rate of change for momentum.

VWAP Slope Period (default: 5): For VWAP trend analysis.

TradingView Publishing Compliance

Originality: The Canuck Trading Indicator is an original script, combining multiple technical indicators and custom logic to provide unique trading signals. It does not replicate existing public scripts.

No Guaranteed Profits: This indicator is a tool for technical analysis and does not guarantee profits. Trading involves risks, and users should conduct their own research and risk management.

Clear Instructions: The description and usage guide are detailed and accessible, ensuring users understand how to apply the indicator effectively.

No External Dependencies: The script uses only built-in Pine Script functions (e.g., ta.rsi, ta.ema, ta.vwap) and requires no external libraries or data sources.

Performance: The script is optimized for performance, using efficient calculations and adaptive parameters to minimize lag on various timeframes.

Visual Clarity: Signals are plotted with distinct shapes and colors, and the table provides a concise summary of market conditions, enhancing usability.

Limitations and Risks

Market Conditions: The indicator may generate false signals in choppy or low-liquidity markets. Always confirm signals with additional analysis.

Timeframe Sensitivity: Performance varies by timeframe; test settings on your preferred chart (e.g., 5-minute for day trading, daily for swing trading).

Risk Management: Use stop-losses and position sizing to manage risk, as suggested in alert messages (e.g., "Stop -20%").

Options Trading: Options strategies (e.g., straddles, iron condors) carry unique risks; consult a financial advisor before trading.

Feedback and Support

For questions, suggestions, or bug reports, please leave a comment on the TradingView script page or contact the author via TradingView. Your feedback helps improve the indicator for the community.

Disclaimer

The Canuck Trading Indicator is provided for educational and informational purposes only. It is not financial advice. Trading involves significant risks, and past performance is not indicative of future results. Always perform your own due diligence and consult a qualified financial advisor before making trading decisions.

PowerHouse SwiftEdge AI v2.10 with Custom Filters & AI AnalysisPowerHouse SwiftEdge AI v2.10 with Custom Filters & AI Analysis

Overview

PowerHouse SwiftEdge AI v2.10 is an advanced TradingView Pine Script indicator designed to identify high-probability trading setups by combining pivot-based structure analysis, multi-timeframe trend detection, and adaptive AI-driven signal filtering. The script integrates Change of Character (CHoCH) and Break of Structure (BOS) signals with customizable momentum, volume, breakout, and trend filters to enhance trade precision. Additionally, it offers an optional AI Market Analysis module that predicts future price trends across multiple timeframes, providing traders with a comprehensive market outlook.

The script is highly customizable, allowing users to tailor inputs to their trading style, whether for scalping, swing trading, or long-term strategies. It is suitable for all asset classes, including stocks, forex, crypto, and commodities, and performs optimally on timeframes ranging from 1-minute to daily charts.

Key Features

Pivot-Based Signal Generation:

Identifies pivot highs and lows to detect CHoCH (reversal patterns) and BOS (continuation patterns).

Signals are plotted as "Buy" or "Sell" labels with optional "Get Ready" pre-signals to prepare traders for potential setups.

Take-profit (TP) levels are automatically calculated based on user-defined points, with optional TP box visualization.

Multi-Timeframe Trend Analysis:

Analyzes trends across seven timeframes (1M, 5M, 15M, 30M, 1H, 4H, D) using EMA and VWAP to determine bullish, bearish, or neutral conditions.

Displays a futuristic AI-Trend Matrix dashboard showing trend direction, strength, and confidence levels for quick decision-making.

Customizable Signal Filters:

Momentum Filter: Ensures signals align with significant price changes, adjusted dynamically using ATR-based volatility.

Higher Timeframe Trend Filter: Requires signals to align with the trend of a user-selected higher timeframe (e.g., 1H).

Lower Timeframe Trend Filter: Prevents signals that conflict with the trend of a user-selected lower timeframe (e.g., 5M).

Volume Filter: Optionally requires above-average volume to confirm signals.

Breakout Filter: Optionally requires price to break previous highs/lows for signal validation.

Repeated Signal Restriction: Prevents consecutive signals in the same trend direction until the trend changes on a user-defined timeframe.

AI-Driven Adaptivity:

Incorporates Cumulative Volume Delta (CVD) to assess buying/selling pressure and classify market volatility (Low, Medium, High).

Uses ATR to dynamically adjust momentum thresholds, ensuring signals adapt to current market conditions.

Optional AI Market Analysis module predicts trends across multiple timeframes by combining trend, momentum, and volatility scores.

Visual Elements:

Plots CHoCH and BOS levels as horizontal lines with distinct colors (aqua for CHoCH sell, lime for CHoCH buy, fuchsia for BOS sell, teal for BOS buy).

Draws dynamic support and resistance trendlines based on short and long-term price action, colored by trend strength.

Displays TP levels and pivot highs/lows for easy reference.

How It Works

The script combines several technical analysis concepts to create a robust trading system:

Market Structure Analysis:

Pivot highs and lows are identified using a user-defined lookback period (Pivot Length).

CHoCH occurs when price crosses below a pivot high (bearish reversal) or above a pivot low (bullish reversal).

BOS occurs when price breaks a previous pivot low (bearish continuation) or pivot high (bullish continuation).

Trend and Momentum Integration:

Trends are determined by comparing price to EMA and VWAP on multiple timeframes.

Momentum is calculated as the percentage price change, with thresholds adjusted by ATR to account for volatility.

"Get Ready" signals appear when momentum approaches the threshold, preparing traders for potential CHoCH or BOS signals.

Signal Filtering:

Filters ensure signals align with user-defined criteria (e.g., trend direction, volume, breakouts).

The Restrict Repeated Signals option prevents over-signaling by requiring a trend change on a specified timeframe before generating a new signal in the same direction.

AI Market Analysis:

The optional AI module calculates a score for each timeframe based on trend direction, momentum, and volatility (ATR compared to its SMA).

Scores are translated into predictions (▲ for bullish, ▼ for bearish, — for neutral), displayed in a dedicated table.

CVD and Volatility Context:

CVD tracks buying vs. selling pressure by accumulating volume based on price direction.

Volatility is classified using CVD magnitude, influencing the script’s visual cues and signal sensitivity.

Why This Combination?

The integration of pivot-based structure analysis, multi-timeframe trend filtering, and AI-driven adaptivity addresses common trading challenges:

Precision: CHoCH and BOS signals focus on key market turning points, reducing noise from minor price fluctuations.

Context: Multi-timeframe analysis ensures trades align with broader market trends, improving win rates.

Adaptivity: ATR and CVD adjustments make the script responsive to changing market conditions, avoiding static thresholds that fail in volatile or quiet markets.

Customization: Extensive input options allow traders to adapt the script to their preferred markets, timeframes, and risk profiles.

Predictive Insight: The AI Market Analysis module provides forward-looking trend predictions, helping traders anticipate market moves.

This combination creates a self-contained system that balances responsiveness with reliability, making it suitable for both novice and experienced traders.

How to Use

Add to Chart:

Apply the indicator to your TradingView chart for any asset and timeframe.

Recommended timeframes: 5M to 1H for scalping/day trading, 4H to D for swing trading.

Configure Inputs:

Pivot Length: Adjust (default 5) to control sensitivity to pivot highs/lows. Lower values for faster signals, higher for stronger confirmations.

Momentum Threshold: Set the minimum price change (default 0.01%) for signals. Increase for stricter conditions.

Take Profit Points: Define TP distance (default 10 points). Adjust based on asset volatility.

Signal Filters: Enable/disable filters (momentum, trend, volume, breakout) to match your strategy.

Higher/Lower Timeframe: Select timeframes for trend alignment (e.g., 1H for higher, 5M for lower).

AI Market Analysis: Enable for predictive trend insights across timeframes.

Get Ready Signals: Enable to see pre-signals for potential setups.

Interpret Signals:

Buy/Sell Labels: Act on green "Buy" or red "Sell" labels, confirming with TP levels and trend direction.

Get Ready Labels: Yellow "Get Ready BUY" or orange "Get Ready SELL" indicate potential setups; prepare but wait for confirmation.

CHoCH/BOS Lines: Use aqua/lime (CHoCH) and fuchsia/teal (BOS) lines as key support/resistance levels.

AI-Trend Matrix: Check the top-right dashboard for trend strength (%), confidence (%), and timeframe-specific trends.

AI Market Analysis Table: If enabled, view predictions (▲/▼/—) for each timeframe to anticipate market direction.

Trading Tips:

Combine signals with other indicators (e.g., RSI, MACD) for additional confirmation.

Use higher timeframe trend alignment for higher-probability trades.

Adjust TP and signal distance based on asset volatility and trading style.

Monitor the AI-Trend Matrix for trend strength; values above 50% or below -50% indicate strong directional bias.

Originality

PowerHouse SwiftEdge AI v2.10 stands out due to its unique blend of:

Adaptive Signal Generation: ATR-based momentum thresholds and CVD-driven volatility context ensure signals remain relevant across market conditions.

Multi-Timeframe Synergy: The script’s ability to filter signals based on both higher and lower timeframe trends provides a rare balance of precision and context.

AI-Powered Insights: The AI Market Analysis module offers predictive capabilities not commonly found in traditional indicators, simulating institutional-grade analysis.

Visual Clarity: The futuristic dashboard and color-coded trendlines make complex data accessible, enhancing usability for all trader levels.

Unlike standalone pivot or trend indicators, this script integrates multiple layers of analysis into a cohesive system, reducing false signals and providing actionable insights without requiring external tools or research.

Limitations

False Signals: No indicator is foolproof; signals may fail in choppy or low-volume markets. Use filters to mitigate.

Timeframe Sensitivity: Performance varies by timeframe and asset. Test settings thoroughly.

AI Predictions: The AI Market Analysis is based on historical data and simplified scoring; it’s not a guaranteed forecast.

Resource Usage: Enabling all filters and AI analysis may slow performance on lower-end devices.

regressionUtilitiesLibrary "regressionUtilities"

get_linear_regression(bar_index_array, prices_array, stdDev_mult)

: Generates the linear regression channel for an array of values.

Parameters:

bar_index_array (array) : (array): Array with bar indexes

prices_array (array) : (array): Array with prices

stdDev_mult (float) : (float): Standard deviation multiple for the channels

Returns: : Returns x1, x2, y1_mid, y2_mid, y1_up, y2_up, y1_dn, y2_dn, m, b, R2, stdDev

get_optimal_linearRegression_channel(max_length, min_length, source, stdDev_mult, show_data_table, tableYpos, tableXpos, table_textSize, barsToRight, plot_labels, include_levels)

: Gets the best fitting linear regression using optimum length

Parameters:

max_length (int) : (int): Maximum bar length

min_length (int) : (int): Minimum bar length

source (float) : (float): Source for the regression

stdDev_mult (float) : (float): Array with prices

show_data_table (bool) : (bool): Activates and shows the data table

tableYpos (string)

tableXpos (string)

table_textSize (string)

barsToRight (int)

plot_labels (bool)

include_levels (bool)

Returns: : Returns three line objects that conform the regression channel, plus the optimal length and maximum r2

get_regressionChannel_data(max_length, min_length, source, stdDev_mult, plot_linearRegression, plot_labels, include_levels, barsToRight)

: Gets data for the linear regression channel

Parameters:

max_length (int) : (int): Maximum length for the linear regression.

min_length (int) : (int): Minimum length for the linear regression.

source (float) : (float): Source for the linear regression

stdDev_mult (float) : (float): Multiple for the standar deviations for the linear regression channel.

plot_linearRegression (bool)

plot_labels (bool)

include_levels (bool)

barsToRight (int)

Returns: : Returns a maps with the regression levels, the direction flag and the datatable map.

get_regressionChannel_data_v2(max_length, min_length, source, stdDev_mult, plot_linearRegression, plot_labels, include_levels, barsToRight)

Parameters:

max_length (int)

min_length (int)

source (float)

stdDev_mult (float)

plot_linearRegression (bool)

plot_labels (bool)

include_levels (bool)

barsToRight (int)

get_cuadratic_regression(x_array, y_array, bars_to_project, max_length)

: Gets the best fitting linear regression using optimum length

Parameters:

x_array (array) : (array): Maximum bar length

y_array (array) : (array): Minimum bar length

bars_to_project (int) : (int): Array with prices

max_length (int)

Returns: : Returns three line objects

NFP High/Low Levels PlusNFP High/Low Levels Plus

Description:

This indicator stores the 12 most recent NFP (Non-Farm-Payroll) days and their values.

Values are captured from 0830 (NFP Release) until close of market

The High and Low values for each NFP month are drawn on the chart with horizontal lines.

- Labels indicating the month's high or low line are placed after the line

- Optionally the high/low price can be displayed additionally

Support and Resistance boxes can be drawn at the closest NFP level above and below the

current price.

- Boxes will automatically update as prices cross the NFP value

Macro Indicator

- This option displays a small table in the top right corner that says "Up" or " Down"

- The Macro Indicator can be used to judge the potential direction for the current month

- Macro direction is calculated by the following:

- UP: If two consecutive days both open and close above the most recent NFP High level

- DOWN: If two consecutive days both open and close below the most recent NFP Low level

Micro Indicator

- This option displays a small table in the top right corner that says "Up" or " Down"

- The Micro Indicator can be used to judge the potential direction for low timeframes 1H or

lower

- Micro direction is calculated by the following:

- UP: If two consecutive 10m candles close above the 20EMA

- DOWN: If two consecutive 10m candles close below the 20EMA

NFP Session Bars

- This feature draws an arrow at the bottom of the chart for each candle that falls within the

NFP session day

- This is useful for identifying NFP Days

Support / Resistance Table

- This displays a table bottom center showing the nearest high and low NFP line level

What is an NFP Day and why is it useful to add to my chart?

- NFP Days are one of the most important data releases monthly

- NFP (Non-Farm-Payroll) is the official release of 80% of the US workforce employed in

manufacturing, construction, and goods

- It does not include those who work on farms, private households, non-profit and

government workers

- Historically these high/low levels for the day create strong support and resistance levels

- Having them displayed on the chart can help identify potential strong levels and pivot points

Full Indicator with all options enabled and identified

Easily update NFP Release Days in the indicator settings

Modify various options: Show/Hide lines, labels, directional indicator tables, values tables

Adjust line width, offsets, colors, font sizes, box widths

Enable individual Directional Indicators and modify colors

Example of full indicator enabled

You can find a list of the NFP Release Schedule on the official US Bureau of Labor Statistics website. This is useful for updating the indicator settings with the correct dates

Line Break Chart StrategyHello All!

We should not pass this year without a gift!

My last publication in 2024 is Complete Line Break Chart Strategy with many features!

What is Line Break Chart?

" Line Break is a Japanese chart style that disregards time intervals and only focuses on price movements, similar to the Kagi and Renko chart styles. Line Break charts form a series of up and down bars (referred to as lines). Up lines represent rising prices, and down lines represent falling prices. New confirmed lines only form on the chart when closing prices break the range covered by previous lines. Users can control the number of past lines used in the calculation via the "Number of Lines" input in the chart settings. The typical "Number of Lines" setting is 3, meaning the chart forms a new up line when the closing price is above the high prices of the last three lines, and it forms a new down line when the closing price is below the past three lines' low prices. If the current price is higher, it is an up line and if it is lower, it is a down line. If the current closing price is the same or the move in the opposite direction is not large enough to warrant a reversal, l then no new line is draw n" by Tradingview. You can find it here

Now let's start examining the features of the indicator:

By using Line break reversals it shows trend on the main chart. You can create alert .

Moreover, you can decide which trade should be taken by using Risk Management in the indicator. You can set the " Maximum Risk " and then if the risk is more than you set then the trade is not taken. When trend changed it checks the distance between reversal level and open price and compare it with the Maximum Risk

Breakout:

It can find breakouts and shows on the chart. You can create alert for breakouts

It can show breakouts on the main chart:

Flip-Flops:

Upon looking at set of price break charts, the trader will notice that there are instances when uptrend blocks is followed by one reversal block, and then by a reversal to a series of uptrend blocks. The opposite is also possible: a series of downtrend blocks is followed by one reversal box and then by an immediate reversal to downtrend. This price action is called a " Flip-Flop ". This structure usually produces trend continuation signal. when we see this then we better use Buy/Sell stop order. lets see this on the chart:

Temporal Sequence Table:

Sequence frequency shows the frequency distribution of the number of sequential highs and the number of sequential lows that have been generated. This is quite important to the trader who is seeking to join a trend or put on a trade when the price break reverses into a new trend direction. For example, if the pattern over the past year has been that there never were more than nine consecutive high closes, it would make sense not to enter a position late into the sequence of new high closes.

also you can see market structure. I have tried to formalize it and show it under the table. so you can understand if it's choppy market.

"Number of Lines" has very important role. While using low time frames such seconds/minutes time frame you may want to choose higher number of lines such 5,6. ( this may minimize the risk of a whipsaw )

Gaps feature:

You can set Gaps on/off. if Gaps on then you can see how long it takes for each box

Reversal and Continuation Probability:

The script calculated Reversal level and Continuation probability of the trend by using Sequence frequency.

It also shows unconfirmed box and current closing price level:

Last but not least it has Overlay option for all items, and can show all items in the main chart!

P.S. I added alerts :)

Wish you all a happy new year!

Enjoy!

Machine Learning: Optimal RSI [YinYangAlgorithms]This Indicator, will rate multiple different lengths of RSIs to determine which RSI to RSI MA cross produced the highest profit within the lookback span. This ‘Optimal RSI’ is then passed back, and if toggled will then be thrown into a Machine Learning calculation. You have the option to Filter RSI and RSI MA’s within the Machine Learning calculation. What this does is, only other Optimal RSI’s which are in the same bullish or bearish direction (is the RSI above or below the RSI MA) will be added to the calculation.

You can either (by default) use a Simple Average; which is essentially just a Mean of all the Optimal RSI’s with a length of Machine Learning. Or, you can opt to use a k-Nearest Neighbour (KNN) calculation which takes a Fast and Slow Speed. We essentially turn the Optimal RSI into a MA with different lengths and then compare the distance between the two within our KNN Function.

RSI may very well be one of the most used Indicators for identifying crucial Overbought and Oversold locations. Not only that but when it crosses its Moving Average (MA) line it may also indicate good locations to Buy and Sell. Many traders simply use the RSI with the standard length (14), however, does that mean this is the best length?

By using the length of the top performing RSI and then applying some Machine Learning logic to it, we hope to create what may be a more accurate, smooth, optimal, RSI.

Tutorial:

This is a pretty zoomed out Perspective of what the Indicator looks like with its default settings (except with Bollinger Bands and Signals disabled). If you look at the Tables above, you’ll notice, currently the Top Performing RSI Length is 13 with an Optimal Profit % of: 1.00054973. On its default settings, what it does is Scan X amount of RSI Lengths and checks for when the RSI and RSI MA cross each other. It then records the profitability of each cross to identify which length produced the overall highest crossing profitability. Whichever length produces the highest profit is then the RSI length that is used in the plots, until another length takes its place. This may result in what we deem to be the ‘Optimal RSI’ as it is an adaptive RSI which changes based on performance.

In our next example, we changed the ‘Optimal RSI Type’ from ‘All Crossings’ to ‘Extremity Crossings’. If you compare the last two examples to each other, you’ll notice some similarities, but overall they’re quite different. The reason why is, the Optimal RSI is calculated differently. When using ‘All Crossings’ everytime the RSI and RSI MA cross, we evaluate it for profit (short and long). However, with ‘Extremity Crossings’, we only evaluate it when the RSI crosses over the RSI MA and RSI <= 40 or RSI crosses under the RSI MA and RSI >= 60. We conclude the crossing when it crosses back on its opposite of the extremity, and that is how it finds its Optimal RSI.

The way we determine the Optimal RSI is crucial to calculating which length is currently optimal.

In this next example we have zoomed in a bit, and have the full default settings on. Now we have signals (which you can set alerts for), for when the RSI and RSI MA cross (green is bullish and red is bearish). We also have our Optimal RSI Bollinger Bands enabled here too. These bands allow you to see where there may be Support and Resistance within the RSI at levels that aren’t static; such as 30 and 70. The length the RSI Bollinger Bands use is the Optimal RSI Length, allowing it to likewise change in correlation to the Optimal RSI.

In the example above, we’ve zoomed out as far as the Optimal RSI Bollinger Bands go. You’ll notice, the Bollinger Bands may act as Support and Resistance locations within and outside of the RSI Mid zone (30-70). In the next example we will highlight these areas so they may be easier to see.

Circled above, you may see how many times the Optimal RSI faced Support and Resistance locations on the Bollinger Bands. These Bollinger Bands may give a second location for Support and Resistance. The key Support and Resistance may still be the 30/50/70, however the Bollinger Bands allows us to have a more adaptive, moving form of Support and Resistance. This helps to show where it may ‘bounce’ if it surpasses any of the static levels (30/50/70).

Due to the fact that this Indicator may take a long time to execute and it can throw errors for such, we have added a Setting called: Adjust Optimal RSI Lookback and RSI Count. This settings will automatically modify the Optimal RSI Lookback Length and the RSI Count based on the Time Frame you are on and the Bar Indexes that are within. For instance, if we switch to the 1 Hour Time Frame, it will adjust the length from 200->90 and RSI Count from 30->20. If this wasn’t adjusted, the Indicator would Timeout.

You may however, change the Setting ‘Adjust Optimal RSI Lookback and RSI Count’ to ‘Manual’ from ‘Auto’. This will give you control over the ‘Optimal RSI Lookback Length’ and ‘RSI Count’ within the Settings. Please note, it will likely take some “fine tuning” to find working settings without the Indicator timing out, but there are definitely times you can find better settings than our ‘Auto’ will create; especially on higher Time Frames. The Minimum our ‘Auto’ will create is:

Optimal RSI Lookback Length: 90

RSI Count: 20

The Maximum it will create is:

Optimal RSI Lookback Length: 200

RSI Count: 30

If there isn’t much bar index history, for instance, if you’re on the 1 Day and the pair is BTC/USDT you’ll get < 4000 Bar Indexes worth of data. For this reason it is possible to manually increase the settings to say:

Optimal RSI Lookback Length: 500

RSI Count: 50

But, please note, if you make it too high, it may also lead to inaccuracies.

We will conclude our Tutorial here, hopefully this has given you some insight as to how calculating our Optimal RSI and then using it within Machine Learning may create a more adaptive RSI.

Settings:

Optimal RSI:

Show Crossing Signals: Display signals where the RSI and RSI Cross.

Show Tables: Display Information Tables to show information like, Optimal RSI Length, Best Profit, New Optimal RSI Lookback Length and New RSI Count.

Show Bollinger Bands: Show RSI Bollinger Bands. These bands work like the TDI Indicator, except its length changes as it uses the current RSI Optimal Length.

Optimal RSI Type: This is how we calculate our Optimal RSI. Do we use all RSI and RSI MA Crossings or just when it crosses within the Extremities.

Adjust Optimal RSI Lookback and RSI Count: Auto means the script will automatically adjust the Optimal RSI Lookback Length and RSI Count based on the current Time Frame and Bar Index's on chart. This will attempt to stop the script from 'Taking too long to Execute'. Manual means you have full control of the Optimal RSI Lookback Length and RSI Count.

Optimal RSI Lookback Length: How far back are we looking to see which RSI length is optimal? Please note the more bars the lower this needs to be. For instance with BTC/USDT you can use 500 here on 1D but only 200 for 15 Minutes; otherwise it will timeout.

RSI Count: How many lengths are we checking? For instance, if our 'RSI Minimum Length' is 4 and this is 30, the valid RSI lengths we check is 4-34.

RSI Minimum Length: What is the RSI length we start our scans at? We are capped with RSI Count otherwise it will cause the Indicator to timeout, so we don't want to waste any processing power on irrelevant lengths.

RSI MA Length: What length are we using to calculate the optimal RSI cross' and likewise plot our RSI MA with?

Extremity Crossings RSI Backup Length: When there is no Optimal RSI (if using Extremity Crossings), which RSI should we use instead?

Machine Learning:

Use Rational Quadratics: Rationalizing our Close may be beneficial for usage within ML calculations.

Filter RSI and RSI MA: Should we filter the RSI's before usage in ML calculations? Essentially should we only use RSI data that are of the same type as our Optimal RSI? For instance if our Optimal RSI is Bullish (RSI > RSI MA), should we only use ML RSI's that are likewise bullish?

Machine Learning Type: Are we using a Simple ML Average, KNN Mean Average, KNN Exponential Average or None?

KNN Distance Type: We need to check if distance is within the KNN Min/Max distance, which distance checks are we using.

Machine Learning Length: How far back is our Machine Learning going to keep data for.

k-Nearest Neighbour (KNN) Length: How many k-Nearest Neighbours will we account for?

Fast ML Data Length: What is our Fast ML Length? This is used with our Slow Length to create our KNN Distance.

Slow ML Data Length: What is our Slow ML Length? This is used with our Fast Length to create our KNN Distance.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

Technology Stocks RSPSTechnology Stocks RSPS Indicator - TradingView Description

Overview

The Technology Stocks RSPS (Relative Strength Portfolio System) indicator is a sophisticated portfolio allocation tool designed specifically for technology sector stocks. It calculates relative strength positions and provides dynamic allocation recommendations based on technical price momentum analysis.

Key Features

- Relative Strength Analysis: Compares 15 major technology stocks and the XLK sector ETF

against each other and gold as a baseline

- Dynamic Portfolio Allocation: Automatically calculates optimal position sizes based on relative

performance

- Visual Portfolio Performance: Tracks cumulative portfolio returns with color-coded

performance indicators

- Customizable Table Display: Shows real-time allocation percentages and optional cash values

for each position

- Technical Momentum Filtering: Uses normalized indicators to identify strength and filter out

weak positions

Included Assets

Sector ETF: XLK

Major Tech Stocks: AAPL, MSFT, NVDA, AVGO, CRM, ORCL, CSCO, ADBE, ACN, AMD, IBM, INTC, NOW, TXN

Benchmark: Gold (TVC:GOLD)

How It Works

The indicator calculates a relative strength score for each asset by comparing it against:

Gold (baseline commodity)

All other technology stocks in the pool

The XLK sector ETF

Assets with positive relative strength receive portfolio allocations proportional to their strength scores. Weak or negative performers are automatically filtered out (allocated 0%).

Visual Elements

Red Area: Aggregate strength of major technology stocks

Navy Blue Area: Overall technical positioning index (TPI)

Performance Line: Cumulative portfolio return (blue = cash-heavy, red = equity-heavy)

Allocation Table: Bottom-left display showing current recommended positions

Important Limitations

This indicator primarily uses technical data and has significant limitations:

❌ No fundamental economic data (ISM, CLI, etc.)

❌ Limited monetary data - missing critical components:

comprehensive monetary data

Funding rates

Detailed bond spreads analysis

Collateral data

❌ No sentiment indicators

❌ No options flow or derivatives data

❌ No earnings or valuation metrics

The indicator focuses purely on price-based relative strength and technical momentum. Users should combine this tool with fundamental analysis, economic data, and proper risk management for complete investment decisions.

Settings

Plot Table: Toggle allocation table visibility

Use Cash: Enable to display dollar amounts based on portfolio size

Cash Amount: Set your total portfolio value for cash allocation calculations

Use Cases

Sector rotation within technology stocks

Relative strength-based portfolio rebalancing

Technical momentum screening for tech sector

Dynamic position sizing based on price trends

Technical Notes

The script avoids for-loops to reduce calculation errors and noise

Uses semi-individual calculations for each asset

Requires the Unicorpus/NormalizedIndicators/1 library for normalized momentum calculations

Maximum lookback: 100 bars

Disclaimer: This indicator is a technical tool only and should not be used as the sole basis for investment decisions. It does not incorporate fundamental, economic, or comprehensive monetary data. Always conduct thorough research and consider your risk tolerance before making investment decisions.

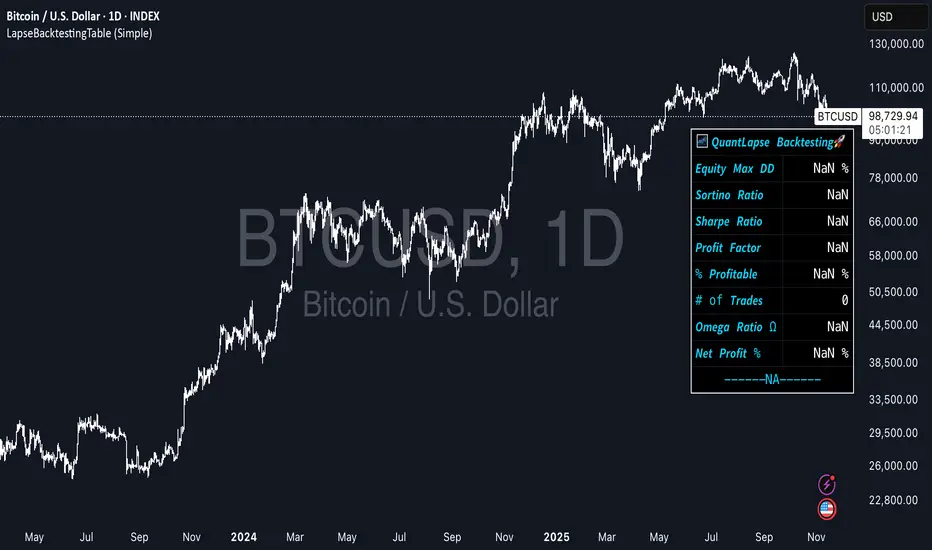

LapseBacktestingTableLibrary "LapseBacktestingMetrics"

This library provides a robust set of quantitative backtesting and performance evaluation functions for Pine Script strategies. It’s designed to help traders, quants, and developers assess risk, return, and robustness through detailed statistical metrics — including Sharpe, Sortino, Omega, drawdowns, and trade efficiency.

Built to enhance any trading strategy’s evaluation framework, this library allows you to visualize performance with the quantlapseTable() function, producing an interactive on-chart performance table.

Credit to EliCobra and BikeLife76 for original concept inspiration.

curve(disp_ind)

Retrieves a selected performance curve of your strategy.

Parameters:

disp_ind (simple string): Type of curve to plot. Options include "Equity", "Open Profit", "Net Profit", "Gross Profit".

Returns: (float) Corresponding performance curve value.

cleaner(disp_ind, plot)

Filters and displays selected strategy plots for clean visualization.

Parameters:

disp_ind (simple string): Type of display.

plot (simple float): Strategy plot variable.

Returns: (float) Filtered plot value.

maxEquityDrawDown()

Calculates the maximum equity drawdown during the strategy’s lifecycle.

Returns: (float) Maximum equity drawdown percentage.

maxTradeDrawDown()

Computes the worst intra-trade drawdown among all closed trades.

Returns: (float) Maximum intra-trade drawdown percentage.

consecutive_wins()

Finds the highest number of consecutive winning trades.

Returns: (int) Maximum consecutive wins.

consecutive_losses()

Finds the highest number of consecutive losing trades.

Returns: (int) Maximum consecutive losses.

no_position()

Counts the maximum consecutive bars where no position was held.

Returns: (int) Maximum flat days count.

long_profit()

Calculates total profit generated by long positions as a percentage of initial capital.

Returns: (float) Total long profit %.

short_profit()

Calculates total profit generated by short positions as a percentage of initial capital.

Returns: (float) Total short profit %.

prev_month()

Measures the previous month’s profit or loss based on equity change.

Returns: (float) Monthly equity delta.

w_months()

Counts the number of profitable months in the backtest.

Returns: (int) Total winning months.

l_months()

Counts the number of losing months in the backtest.

Returns: (int) Total losing months.

checktf()

Returns the time-adjusted scaling factor used in Sharpe and Sortino ratio calculations based on chart timeframe.

Returns: (float) Annualization multiplier.

stat_calc()

Performs complete statistical computation including drawdowns, Sharpe, Sortino, Omega, trade stats, and profit ratios.

Returns: (array)

.

f_colors(x, nv)

Generates a color gradient for performance values, supporting dynamic table visualization.

Parameters:

x (simple string): Metric label name.

nv (simple float): Metric numerical value.

Returns: (color) Gradient color value for table background.

quantlapseTable(option, position)

Displays an interactive Performance Table summarizing all major backtesting metrics.

Includes Sharpe, Sortino, Omega, Profit Factor, drawdowns, profitability %, and trade statistics.

Parameters:

option (simple string): Table type — "Full", "Simple", or "None".

position (simple string): Table position — "Top Left", "Middle Right", "Bottom Left", etc.

Returns: (table) On-chart performance visualization table.

This library empowers advanced quantitative evaluation directly within Pine Script®, ideal for strategy developers seeking deeper performance diagnostics and intuitive on-chart metrics.

ka66: Symbol InformationThis shows a table of all current (Pine v6) `syminfo.` values.

Please note this is primarily of use to Pine Developers, or the curious trader.

There are a few of these around on TradingView, but many seem to focus on the use case they have. This script just dumps all values, in alphabetical order of properties.

You can use this to inspect the details of the symbol, which in turn, can be fed into various scripts covering tasks such as:

Position Sizing calculation (which requires things like tick, pointvalue, and currency details)

Recommendation engines (which use the recommendation_* properties)

Fundamentals on stocks (which may use share count information, and possibly employee information)

Note that not all table values are populated, as they depend on the instrument being introspected. For example, a share ticker will have some different details to a Forex pair. The `NaN` values (the "Not A Number" special value in programming parlance) are not a bug, they are simply Pine reporting that no value is set for it. I have opted to dump out values as-is as the focus is developers.

My motivation to create it was to write a position sizing tool. Additionally, the output of this script is cleanly formatted, with monospace fonts and conventional alignment for tables/forms with key and values. It also allows customising the table position. Ideally this feature is made part of the default TradingView customisation, but at this time, it is not, and tables don't auto-adjust their positions.

Zero Lag Trend Signals (MTF) [Quant Trading] V7Overview

The Zero Lag Trend Signals (MTF) V7 is a comprehensive trend-following strategy that combines Zero Lag Exponential Moving Average (ZLEMA) with volatility-based bands to identify high-probability trade entries and exits. This strategy is designed to reduce lag inherent in traditional moving averages while incorporating dynamic risk management through ATR-based stops and multiple exit mechanisms.

This is a longer term horizon strategy that takes limited trades. It is not a high frequency trading and therefore will also have limited data and not > 100 trades.

How It Works

Core Signal Generation:

The strategy uses a Zero Lag EMA (ZLEMA) calculated by applying an EMA to price data that has been adjusted for lag:

Calculate lag period: floor((length - 1) / 2)

Apply lag correction: src + (src - src )

Calculate ZLEMA: EMA of lag-corrected price

Volatility bands are created using the highest ATR over a lookback period multiplied by a band multiplier. These bands are added to and subtracted from the ZLEMA line to create upper and lower boundaries.

Trend Detection:

The strategy maintains a trend variable that switches between bullish (1) and bearish (-1):

Long Signal: Triggers when price crosses above ZLEMA + volatility band

Short Signal: Triggers when price crosses below ZLEMA - volatility band

Optional ZLEMA Trend Confirmation:

When enabled, this filter requires ZLEMA to show directional momentum before entry:

Bullish Confirmation: ZLEMA must increase for 4 consecutive bars

Bearish Confirmation: ZLEMA must decrease for 4 consecutive bars

This additional filter helps avoid false signals in choppy or ranging markets.

Risk Management Features:

The strategy includes multiple stop-loss and take-profit mechanisms:

Volatility-Based Stops: Default stop-loss is placed at ZLEMA ± volatility band

ATR-Based Stops: Dynamic stop-loss calculated as entry price ± (ATR × multiplier)

ATR Trailing Stop: Ratcheting stop-loss that follows price but never moves against position

Risk-Reward Profit Target: Take-profit level set as a multiple of stop distance

Break-Even Stop: Moves stop to entry price after reaching specified R:R ratio

Trend-Based Exit: Closes position when price crosses EMA in opposite direction

Performance Tracking:

The strategy includes optional features for monitoring and analyzing trades:

Floating Statistics Table: Displays key metrics including win rate, GOA (Gain on Account), net P&L, and max drawdown

Trade Log Labels: Shows entry/exit prices, P&L, bars held, and exit reason for each closed trade

CSV Export Fields: Outputs trade data for external analysis

Default Strategy Settings

Commission & Slippage:

Commission: 0.1% per trade

Slippage: 3 ticks

Initial Capital: $1,000

Position Size: 100% of equity per trade

Main Calculation Parameters:

Length: 70 (range: 70-7000) - Controls ZLEMA calculation period

Band Multiplier: 1.2 - Adjusts width of volatility bands

Entry Conditions (All Disabled by Default):

Use ZLEMA Trend Confirmation: OFF - Requires ZLEMA directional momentum

Re-Enter on Long Trend: OFF - Allows multiple entries during sustained trends

Short Trades:

Allow Short Trades: OFF - Strategy is long-only by default

Performance Settings (All Disabled by Default):

Use Profit Target: OFF

Profit Target Risk-Reward Ratio: 2.0 (when enabled)

Dynamic TP/SL (All Disabled by Default):

Use ATR-Based Stop-Loss & Take-Profit: OFF

ATR Length: 14

Stop-Loss ATR Multiplier: 1.5

Profit Target ATR Multiplier: 2.5

Use ATR Trailing Stop: OFF

Trailing Stop ATR Multiplier: 1.5

Use Break-Even Stop-Loss: OFF

Move SL to Break-Even After RR: 1.5

Use Trend-Based Take Profit: OFF

EMA Exit Length: 9

Trade Data Display (All Disabled by Default):

Show Floating Stats Table: OFF

Show Trade Log Labels: OFF

Enable CSV Export: OFF

Trade Label Vertical Offset: 0.5

Backtesting Date Range:

Start Date: January 1, 2018

End Date: December 31, 2069

Important Usage Notes

Default Configuration: The strategy operates in its most basic form with default settings - using only ZLEMA crossovers with volatility bands and volatility-based stop-losses. All advanced features must be manually enabled.

Stop-Loss Priority: If multiple stop-loss methods are enabled simultaneously, the strategy will use whichever condition is hit first. ATR-based stops override volatility-based stops when enabled.

Long-Only by Default: Short trading is disabled by default. Enable "Allow Short Trades" to trade both directions.

Performance Monitoring: Enable the floating stats table and trade log labels to visualize strategy performance during backtesting.

Exit Mechanisms: The strategy can exit trades through multiple methods: stop-loss hit, take-profit reached, trend reversal, or trailing stop activation. The trade log identifies which exit method was used.

Re-Entry Logic: When "Re-Enter on Long Trend" is enabled with ZLEMA trend confirmation, the strategy can take multiple long positions during extended uptrends as long as all entry conditions remain valid.

Capital Efficiency: Default setting uses 100% of equity per trade. Adjust "default_qty_value" to manage position sizing based on risk tolerance.

Realistic Backtesting: Strategy includes commission (0.1%) and slippage (3 ticks) to provide realistic performance expectations. These values should be adjusted based on your broker and market conditions.

Recommended Use Cases

Trending Markets: Best suited for markets with clear directional moves where trend-following strategies excel

Medium to Long-Term Trading: The default length of 70 makes this strategy more appropriate for swing trading rather than scalping

Risk-Conscious Traders: Multiple stop-loss options allow traders to customize risk management to their comfort level

Backtesting & Optimization: Comprehensive performance tracking features make this strategy ideal for testing different parameter combinations

Limitations & Considerations

Like all trend-following strategies, performance may suffer in choppy or ranging markets

Default 100% position sizing means full capital exposure per trade - consider reducing for conservative risk management

Higher length values (70+) reduce signal frequency but may improve signal quality

Multiple simultaneous risk management features may create conflicting exit signals

Past performance shown in backtests does not guarantee future results

Customization Tips

For more aggressive trading:

Reduce length parameter (minimum 70)

Decrease band multiplier for tighter bands

Enable short trades

Use lower profit target R:R ratios

For more conservative trading:

Increase length parameter

Enable ZLEMA trend confirmation

Use wider ATR stop-loss multipliers

Enable break-even stop-loss

Reduce position size from 100% default

For optimal choppy market performance:

Enable ZLEMA trend confirmation

Increase band multiplier

Use tighter profit targets

Avoid re-entry on trend continuation

Visual Elements

The strategy plots several elements on the chart:

ZLEMA line (color-coded by trend direction)

Upper and lower volatility bands

Long entry markers (green triangles)

Short entry markers (red triangles, when enabled)

Stop-loss levels (when positions are open)

Take-profit levels (when enabled and positions are open)

Trailing stop lines (when enabled and positions are open)

Optional ZLEMA trend markers (triangles at highs/lows)

Optional trade log labels showing complete trade information

Exit Reason Codes (for CSV Export)

When CSV export is enabled, exit reasons are coded as:

0 = Manual/Other

1 = Trailing Stop-Loss

2 = Profit Target

3 = ATR Stop-Loss

4 = Trend Change

Conclusion

Zero Lag Trend Signals V7 provides a robust framework for trend-following with extensive customization options. The strategy balances simplicity in its core logic with sophisticated risk management features, making it suitable for both beginner and advanced traders. By reducing moving average lag while incorporating volatility-based signals, it aims to capture trends earlier while managing risk through multiple configurable exit mechanisms.

The modular design allows traders to start with basic trend-following and progressively add complexity through ZLEMA confirmation, multiple stop-loss methods, and advanced exit strategies. Comprehensive performance tracking and export capabilities make this strategy an excellent tool for systematic testing and optimization.

Note: This strategy is provided for educational and backtesting purposes. All trading involves risk. Past performance does not guarantee future results. Always test thoroughly with paper trading before risking real capital, and adjust position sizing and risk parameters according to your risk tolerance and account size.

================================================================================

TAGS:

================================================================================

trend following, ZLEMA, zero lag, volatility bands, ATR stops, risk management, swing trading, momentum, trend confirmation, backtesting

================================================================================

CATEGORY:

================================================================================

Strategies

================================================================================

CHART SETUP RECOMMENDATIONS:

================================================================================

For optimal visualization when publishing:

Use a clean chart with no other indicators overlaid

Select a timeframe that shows multiple trade signals (4H or Daily recommended)

Choose a trending asset (crypto, forex major pairs, or trending stocks work well)

Show at least 6-12 months of data to demonstrate strategy across different market conditions

Enable the floating stats table to display key performance metrics

Ensure all indicator lines (ZLEMA, bands, stops) are clearly visible

Use the default chart type (candlesticks) - avoid Heikin Ashi, Renko, etc.

Make sure symbol information and timeframe are clearly visible

================================================================================

COMPLIANCE NOTES:

================================================================================

✅ Open-source publication with complete code visibility

✅ English-only title and description

✅ Detailed explanation of methodology and calculations

✅ Realistic commission (0.1%) and slippage (3 ticks) included

✅ All default parameters clearly documented

✅ Performance limitations and risks disclosed

✅ No unrealistic claims about performance

✅ No guaranteed results promised

✅ Appropriate for public library (original trend-following implementation with ZLEMA)

✅ Educational disclaimers included

✅ All features explained in detail

================================================================================

Tchwella Stocks Custom WatermarkThis Pine Script v5 indicator adds a customizable watermark to TradingView charts, displaying key stock information while allowing for flexible positioning and formatting.

📌 Features & Functionality:

✅ Custom Positioning:

• Fixed to the top-left corner.

• Adjustable spacing ensures the text is properly aligned.

✅ Displayed Information (Configurable):

• Company Name & Market Cap (Optional: Shows dynamically calculated market cap)

• Stock Ticker & Timeframe

• Industry & Sector

✅ Customization Options:

• Font Size: Huge, Large, Normal, Small

• Text Color & Transparency: Adjustable

• Proper Left Alignment for a clean, structured display

• Vertical Offset Tweaks to move text down for better visibility

✅ Optimized Table Layout:

• Uses table.new() for persistent placement.

• Added an empty row to fine-tune positioning, ensuring the watermark doesn’t overlap key chart areas.

🔧 Use Case:

Designed for traders who want a clear, customizable stock watermark to enhance their charting experience without obstructing price action.

Feb 1

Release Notes

Updated version: now you can decide your location for the watermark

Micha Stocks Custom Watermark (MSWM) – TradingView Script

This Pine Script v5 indicator adds a customizable watermark to TradingView charts, displaying key stock information while allowing for flexible positioning and formatting.

📌 Features & Functionality:

✅ Custom Positioning:

• Fixed to the top-left corner.

• Adjustable spacing ensures the text is properly aligned.

✅ Displayed Information (Configurable):

• Company Name & Market Cap (Optional: Shows dynamically calculated market cap)

• Stock Ticker & Timeframe

• Industry & Sector

✅ Customization Options:

• Font Size: Huge, Large, Normal, Small

• Text Color & Transparency: Adjustable

• Proper Left Alignment for a clean, structured display

• Vertical Offset Tweaks to move text down for better visibility

✅ Optimized Table Layout:

• Uses table.new() for persistent placement.

• Added an empty row to fine-tune positioning, ensuring the watermark doesn’t overlap key chart areas.

🔧 Use Case:

Designed for traders who want a clear, customizable stock watermark to enhance their charting experience without obstructing price action.

Feb 7

Release Notes

Micha Stocks Custom Watermark – Updated Version 🚀

This updated Micha Stocks Custom Watermark script enhances your TradingView experience by adding an ATR-based volatility signal alongside the existing customizable stock watermark.

🆕 New Features & Improvements:

✅ ATR (14-Day) with Dynamic Volatility Indicator

• Displays the ATR value and its percentage relative to price.

• Includes a color-coded volatility signal:

• 🔴 High Volatility (Above user-defined Red Threshold)

• 🟡 Moderate Volatility (Between Red & Yellow Thresholds)

• 🟢 Low Volatility (Below user-defined Yellow Threshold)

✅ Fully Customizable ATR Thresholds

• Users can set their own ATR % levels for Red, Yellow, and Green signals.

✅ Improved Watermark Customization

• Users can still adjust the position, size, and color of the watermark.

• Includes Company Name, Ticker, Market Cap, Industry, and Sector.

• ATR can be turned on/off in settings for flexibility.

🔧 How to Use:

1️⃣ Go to Indicator Settings → Enable or Disable ATR Display

2️⃣ Adjust ATR % Thresholds to fit your volatility preference

3️⃣ Customize Text Position, Color, and Size to match your chart setup

This update makes it easier to quickly assess market volatility while keeping a clean and professional chart layout.

💡 Why Use This Indicator?

• Effortlessly track key stock info without cluttering your chart.

• Quickly identify volatile conditions using ATR percentage signals.

• Adjust settings on the fly to match your trading strategy.

📢 Update Now & Enjoy a Smarter Charting Experience!

Extended CANSLIM Indicator❖ Extended CANSLIM Indicator.

The Extended CANSLIM indicator is an indicator that concentrates all the tools usually used by CANSLIM traders.

It shows a table where all the stock fundamental information is shown at once first for the last quarter and then up to 5 years back.

The fundamental data is checked against well known CANSLIM validation criteria and is shown over 4 state levels.

1. Good = Value is CANSLIM Compliant.

2. Acceptable = Value is not CANSLIM compliant but still good. value is shown with a lighter background color.

3. Warning = Value deserves special attention. Value is shown over orange background color.

3. Stop = Value is non CANSLIM compliant or indicates a stop trading condition. Value is shown over red background color.

The indicator has also a set of technical tools calculated on price or index and shown directly on the chart.

❖ Fundamental data shown in the table.

The table is arranged in 4 sets of data:

1. Table Header, showing Indicator and Company data.

2. CANSLIM.

3. 3Rs: RS Rating, Revenue and ROE.

4. Extra Data: Piotroski score, ATR, Trend Days, D to E, Avg Vol and Vol today.

Sets 3 and 4 can be hidden from the table.

❖ Indicator and Compay Data.

The table header shows, Indicator name and version.

It then displays Company Name, sector and industry, human size and its capitalization.

❖ CANSLIM Data.

Displays either genuine CANSLIM data from TradinView or custom data as best effort when that data cannot be obtained in TV.

C = EPS diluted growth, Quarterly YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

A = EPS diluted growth, Annual YoY.

>= 25% = Good, >= 0% = Acceptable, < 0% = Stop

N = New High as best effort (Cust).

Always Good

S = Float shares as best effort.

Always Good

L = One year performance relative to S&P 500 (Cust),

Positive : 0% .. 50% = Neutral, 50%+ = Leader, 80%+ = Leader+, 100%+ = Leader++

Negative : 0% .. -10% = Laggard, -10% .. -30% = Laggard+, -30%+ = Laggard++

>= 50% = Good, >= 0% = Acceptable, >= -10% Warning, < -10% = Stop

I = Accumulation/Distribution days over last 25 days as a clue for institutional support (Cust).

A delta is calculated by subtracting Distribution to Accumulation days.

> 0 = Good, = 0 = Acceptable, < 0 = Warning, < -5 = Stop

M = Market direction and exposure measured on S&500 closing between averages (Cust).

Varies from 0% Full Bear to 100% Full Bull

>= 80% = Good, >= 60% = Acceptable, >= 40% = Warning, < 40% = Stop

❖ Extra non CANSLIM Data.

RS = RS Rating.

>= 90 = Good, >= 80 = Accept, >= 50 = Warning, < 50 = Stop

Rev. = Revenue Growth Quarterly YoY.

>= 0% = Good, <0% = Stop

ROE = Return on Equity, Quarterly YoY.

>= 17% = Good, >= 0% = Acceptable, < 0% = Stop

Piotr. = Piotroski Score, www.investopedia.com (TV)

>= 7 = Good, >= 4 = Acceptable, < 4 = Stop

ATR = Average True Range over the last 20 days (Cust).

0% - 2% = Acceptable, 2% - 4% = Ideal, 4% - 6% = Warning, 5%+ = Stop.

Trend Days = Days since EMA150 is over EMA200 (Cust).

Always Good

D. to E. = Days left before Earnings. Maybe not a good idea buying just before earnings (Cust).

>= 28 = Good, >= 21 = Acceptable, >= 14 = Warning, < 14 = Stop

Avg Vol. = 50d Average Volume (Cust).

>= 100K = Good, < 100K = Acceptable

Vol. Today = Today's percentage volume compared to 50d average (Cust).

Always Good.

❖ Historical Data.

Optionally selectable historical data can be displayed for C, A, Revenue and ROE up to 20 quarters if available.

Quarterly numbers can also be displayed for A, C and Revenue.

Information can be shown in Chronological or Reverse Chronological order (default).

Increasing growth quarters are shown in white, while diminuing ones are shown in Yellow.

Transition from Losing to Profitable quarters are shown with an exclamation mark ‘!’

Finally, losing quarters are shown between parenthesis.

❖ MAs on chart.

Displays 200, 100, 50 and 20 days MAs on chart.

The MAs are also automatically scaled in the 1W time frame.

❖ New 52 Week High on chart.

A sun is shown on the chart the first time that a new 52 week high is reached.

The N cell shows a filled sun when a 52 week high is no older than a month, an lighter sun when it’s no older than a quarter or a moon otherwise.

❖ Pocket Pivots on chart.

Small triangles below the price are signaling pocket pivots.

❖ Bases on chart, formerly Darvas Boxes.

Draw bases as defined by Darvas boxes, both top or bottom of bases can be selected to be shown in order to only show resistance or support.

❖ Market exposure/direction indicator.

When charting S&P500 (SPX), Nasdaq 100 Index (NDX), Nasdaq composite (IXIC) or Dow Jownes Index (DJIA), the indicator switches to Market Exposure indicator, showing also Accumulation/Distribution days when volume information is available. This indication which varies from 0% to 100% is what is shown under the M letter in the CANSLIM table which is calculated on the S&P500.

❖ Follow Through Days indicator.

If you are an adept of the Low-cheat entry, then you will be highly interested by the Follow Through days indicator as measured in the S&P 500 and shown as diamonds on the chart.

The follow-through days are calculated on S&P500 but shown in current stock chart so you don’t need to chart the S&P 500 to know that a follow through day occurred.

Follow Through days show correctly on Daily time frame and most are also shown on the Weekly time frame as well.

They are also classified according to the market zone in which they occur:

0%-5% from peak = Pullback : FT day is not shown.

5%-10% from peak = Minor Correction : Minor FT days is shown.

10%-20% from peak = Correction : Intermediate FT days us shown

20+% from peak = Bear Market : Makor FT days is shown

❖ RS Line and Rating indicator.

A RS Line and Rating indicator can be added to the chart.

Relative Strength Rating Accuracy.

Please note that the RS Rating is not 100% accurate when compared to IBD values.

❖ Earning Line indicator.

An Earning Line indicator can be added to the chart.

❖ ATR Bands and ATR Trade calculator.

The motivation for this calculator came from my own need to enter trades on volatile stocks where the simple 7% Stop Loss rule doest not work.

It simply calculates the number of shares you can buy at any moment based on current stock price and using the lower ATR band as a stop loss.

A few words about the ATR Bands.

On this indicator the ATR bands are not drawn as a classical channel that follows the price.

The lower band is drawn as a support until it’s broken on a closing basis. It can’t be in a down trend.

The upper band is drawn as a resistance until it’s broken on a closing basis. It can’t be in an up trend.

The idea is that when price starts to fall down from a peak, it should not violate its lower band ATR and that means that we can use that level as a Stop Loss.

You must look back for the stock volatility and find out which ATR multiplier works well meaning that the ATR bands are not violated on normal pullbacks. By default, the indicator uses 5x multiplier.

❖ Extra things, visual features and default settings.

The first square cell of current quarter displays a check mark ‘V’ if the CANSLIM criteria is OK or acceptable or a cross ‘X’ otherwise.

The first square cell of historical C and Rev show respectively the count of last consecutive positive quarters.

There are different color themes from “Forest” to “Space” you can chose from to best fit your eyes.

You also have different table sizes going from “Micro” to “Huge” for better adjustment to the size of your display.

The default settings view show: Pocket Pivots, FT Days, MA50, RS Line and ATR Bands.

That's all, Enjoy!

MSFA_LibraryLibrary "MSFA_library"

TODO: add library description here

getDecimals()

Calculates how many decimals are on the quote price of the current market

Returns: The current decimal places on the market quote price

getPipSize(multiplier)

Calculates the pip size of the current market

Parameters:

multiplier (int) : The mintick point multiplier (1 by default, 10 for FX/Crypto/CFD but can be used to override when certain markets require)

Returns: The pip size for the current market

truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places

Parameters:

number (float) : The number to truncate

decimalPlaces (simple float) : (default=2) The number of decimal places to truncate to

Returns: The given number truncated to the given decimalPlaces

toWhole(number)

Converts pips into whole numbers

Parameters:

number (float) : The pip number to convert into a whole number

Returns: The converted number

toPips(number)

Converts whole numbers back into pips

Parameters:

number (float) : The whole number to convert into pips

Returns: The converted number

getPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period

Parameters:

value1 (float) : The first value to reference

value2 (float) : The second value to reference

lookback (int) : The lookback period to analyze

Returns: The percent change over the two values and lookback period

random(minRange, maxRange)

Wichmann–Hill Pseudo-Random Number Generator

Parameters:

minRange (float) : The smallest possible number (default: 0)

maxRange (float) : The largest possible number (default: 1)

Returns: A random number between minRange and maxRange

bullFib(priceLow, priceHigh, fibRatio)

Calculates a bullish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

bearFib(priceLow, priceHigh, fibRatio)

Calculates a bearish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

getMA(length, maType)

Gets a Moving Average based on type (! MUST BE CALLED ON EVERY TICK TO BE ACCURATE, don't place in scopes)

Parameters:

length (simple int) : The MA period

maType (string) : The type of MA

Returns: A moving average with the given parameters

barsAboveMA(lookback, ma)

Counts how many candles are above the MA

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to check

Returns: The bar count of how many recent bars are above the MA

barsBelowMA(lookback, ma)

Counts how many candles are below the MA

Parameters: