ES-VIX Daily Price Bands - Inner bands (80% and 50%)ES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Middle Inner upper band (green) at 80% of expected move

Middle Inner lower band (red) at 80% of expected move

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

Cari dalam skrip untuk "同花顺软件+美国+VIX+恐慌指数+行情代码"

ES-VIX Daily Price Bands - Inner bandsES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

ES-VIX Daily Price BandsES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

Ratchet Exit Trend Strategy with VIX FilterThis strategy is a trend-following system designed specifically for volatile markets. Instead of focusing solely on the "perfect entry," this script emphasizes intelligent trade management using a custom **"Ratchet Exit System."**

Additionally, it integrates a volatility filter based on the CBOE Volatility Index (VIX) to minimize risk during extreme market phases.

### 🎯 The Concept: Ratchet Exit

The "Ratchet" system operates like a mechanical ratchet tool: the Stop Loss can only move in one direction (up, for long trades) and "locks" into specific stages. The goal is to give the trade "room to breathe" initially to avoid being stopped out by noise, then aggressively reduce risk as the trade moves into profit.

The exit logic moves through 3 distinct phases:

1. **Phase 0 (Initial Risk):** At the start of the trade, a wide Stop Loss is set (Default: 10%) to tolerate normal market volatility.

2. **Phase 1 (Risk Reduction):** Once the trade reaches a specific floating profit (Default: +10%), the Stop Loss is raised and "pinned" to a fixed value (Default: -8% from entry). This drastically reduces risk while keeping the trade alive.

3. **Phase 2 (Trailing Mode):** If the trend extends to a higher profit zone (Default: +15%), the Stop switches to a dynamic Trailing Mode. It follows the **Highest High** at a fixed percentage distance (Default: 8%).

### 🛡️ VIX Filter & Panic Exit

High volatility is often the enemy of trend-following strategies.

* **Entry Filter:** The system will not enter new positions if the VIX is above a user-defined threshold (Default: 32). This helps avoid entering "falling knife" markets.

* **Panic Exit:** If the VIX spikes above the threshold (32) while a trade is open, the position is closed immediately to protect capital (Emergency Exit).

### 📈 Entry Signals

The strategy trades **LONG only** and uses Simple Moving Averages (SMAs) to identify trends:

* **Golden Cross:** SMA 25 crosses over SMA 50.

* **3-Bar Breakouts:** A confirmation logic where the price must close above the SMA 50, 100, or 200 for 3 consecutive bars.

### ⚙️ Settings (Inputs)

All parameters are fully customizable via the settings menu:

* **SMAs:** Lengths for the trend indicators (Default: 25, 50, 100, 200).

* **VIX Filter:** Toggle the filter on/off and adjust the panic threshold.

* **Ratchet Settings:** Percentages for Initial Stop, Trigger Levels for Stages 1 & 2, and the Trailing Distance.

### ⚠️ Technical Note & Risk Warning

This script uses `request.security` to fetch VIX data. Please ensure you understand the risks associated with trading leveraged or volatile assets. Past performance is not indicative of future results.

India Vix based Strangle StrikesA clean Nifty–VIX dashboard that converts India VIX into expected daily moves, price ranges, and suggested strangle strikes. Includes VIX %, expanded 1.2× range, and smart rounded strike levels for options trading.

This script provides a professional on-chart dashboard that converts India VIX into actionable trading levels for Nifty. It calculates the VIX-based expected daily move, projected price ranges, expanded 1.2× ranges, and suggested strangle strike prices. Includes clean formatting, color-coded sections, and real-time updates.

Ideal for traders using straddles, strangles, intraday volatility models, range-bound setups, and options-based risk management.

1.2x expanded range is better success probability, may keep 20% of strangle value as stop loss.

The vix based system is intended to give approx. 70%+ success rate.

Market Sentiment Suite: PCCE + VIX + Signals📊 Market Sentiment Suite: PCCE + VIX + Signals

Identify fear, greed, and turning points in the market.

This script combines the CBOE Put/Call Ratio (PCCE) with the VIX volatility index percentile to visualize crowd sentiment and highlight potential market tops and bottoms.

🔍 Key Features

Dual-indicator design: PCCE + normalized VIX percentile

Color-coded zones for Greed (<0.6) and Fear (>1.2)

Automatic alert signals when sentiment reaches extremes

Live sentiment table displaying real-time PCCE and VIX data

Works seamlessly on SPX, SPY, QQQ, or any major index

🧠 How to Use

When PCCE > 1.2 and VIX percentile > 80%, fear is extreme → possible market bottom

When PCCE < 0.6 and VIX percentile < 20%, greed is extreme → possible market top

Perfect for contrarian traders, sentiment analysts, and swing traders

✨ Best Timeframe: Daily

⚙️ Markets: SPX / SPY / QQQ / Global Indexes

📈 Type: Contrarian Sentiment Indicator

Inverse VIX / Custom Inverse Line🎯 Main Idea

This indicator creates a line that moves opposite to the VIX (Volatility Index) — or any symbol you choose.

When VIX rises (fear increases), → this line goes down.

When VIX falls (market calm), → this line goes up.

It helps you visually understand market sentiment — calm periods (bullish) vs fear periods (bearish).

⚙️ Input Settings

Setting Description

Symbol to invert The symbol to invert. Default is CBOE:VIX.

Inverse mode The method used to invert the values. There are 3 options:

① Negate Simply flips the sign (multiplies by -1). Very straightforward.

② Reciprocal Uses the mathematical inverse (1 ÷ value). High values become smaller, and vice versa.

③ Inverse Normalized The most useful mode 🔥 — normalizes values between 0–100 and flips them, similar to an RSI.

Normalization lookback How many bars to use for normalization (default 252 = roughly one trading year).

Smoothing (SMA) Number of bars for smoothing (makes the line smoother).

Use log for reciprocal Uses logarithmic scaling to stabilize big swings.

Plot color / width Customize the line’s color and thickness.

Show original source If enabled, shows the original VIX line for comparison.

📈 How It Works

The script fetches the close price of the VIX (or your chosen symbol).

It applies the selected inversion method.

The inverted line is plotted on the chart.

In “Inverse Normalized” mode:

The range is 0–100.

Values above 75 = high optimism (market often overheated).

Values below 25 = high fear (potential buying opportunity).

A middle line at 50 marks neutral sentiment.

⚠️ Alerts

The indicator includes two default alerts when using “Inverse Normalized” mode:

🔔 Above 75: Market showing strong optimism (potential top or correction zone).

🔔 Below 25: Market showing fear (potential bottom or buy signal).

🧠 How to Use It

Use it on daily or weekly charts for clearer signals.

Compare it with SPX or NASDAQ:

When the Inverse VIX line rises, markets often go up.

When it falls, markets usually drop or consolidate.

Combine it with other indicators (e.g., RSI, MACD) for confirmation.

Multi-Indicator Panel (RSI, Stoch, MACD, VIX Fix, MFI)A versatile single-pane oscillator panel combining RSI, Stochastic, MACD (scaled to 0–100), Williams VIX Fix (normalized & inverted: low value = high fear), and MFI. Each module is toggleable, with reference levels, background highlights, and ready-made alerts.

Key features

Per-indicator toggles: RSI, Stoch %K/%D, MACD (lines + optional histogram), inverted 0–100 VIX Fix, and MFI.

Standard levels & center line at 50; adjustable overbought/oversold thresholds.

Contextual background coloring (optional) for extreme conditions.

Built-in alerts: RSI/Stoch OB/OS, MACD–Signal cross, VIX Fix “High Fear/Low Fear,” and MFI OB/OS.

Unified scale: MACD mapped around 50 to align with other oscillators; VIX Fix normalized to 0–100.

How to use (quick)

Add the indicator → enable needed modules via “Indicator Toggles.”

Tune periods & levels (e.g., RSI 14, Stoch 14/3, MACD 12-26-9, VIX Fix 22/252, MFI 14).

(Optional) Turn on MACD histogram.

Create alerts from “Add alert on…” using the provided conditions.

Interpretation notes

Inverted VIX Fix: low values ⇒ high fear/volatility (potential bounces); high values ⇒ complacency.

Scaled MACD: lines around 50 ≈ MACD zero; line crosses remain valid despite scaling.

Disclaimer

Analysis tool, not financial advice. Test across timeframes/instruments and pair with risk management.

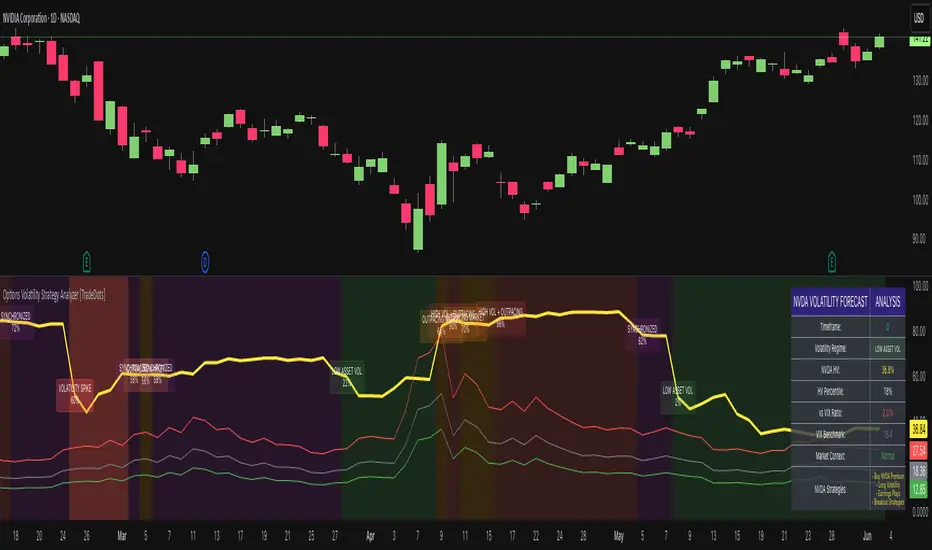

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

Monthly, Quarterly OPEX & Vix expirations

OPEX Indicator:

The OPEX indicator is designed to provide traders with a visual representation of key options expiration dates, particularly for monthly, quarterly, and VIX options expirations. This indicator can be particularly helpful for market participants who focus on options-based strategies or those who track the impact of options expiration on price action.

The indicator overlays vertical lines and labels on the chart to highlight three key types of expiration events:

Monthly Equity and Index Expiration (OPEX): This marks the standard monthly options expiration dates for equity and index options.

Quarterly Index Expiration (Q): This indicates the quarterly expiration dates for index options, which tend to have a larger impact on the market.

Monthly VIX Expiration (VIXEX): This marks the monthly expiration of VIX options and futures, which are important for volatility traders.

How to Use the OPEX Indicator:

Expiration Dates on the Chart: The OPEX indicator marks expiration dates with vertical lines and labels that appear on the chart. These are customizable, allowing you to adjust the line and label colors to suit your preferences. The lines and labels will appear at specific times, such as the closing of the market on expiration days, allowing traders to prepare for potential volatility or other market dynamics associated with these events.

Customizable Colors and Label Positions: The indicator offers flexibility in customizing the appearance of expiration lines and labels. For each expiration type (OPEX, Quarterly, and VIXEX), you can adjust the line color, label color, and label text color. Additionally, the label text size and position can be customized (e.g., above the bar, below the bar, top or bottom of the chart). This allows for a tailored display that suits your trading style and chart layout.

Visualizing Impact of Expiration Events: Traders who track the influence of expiration events can use this indicator to spot potential market moves around expiration dates. For example, significant price swings often occur near expiration days as options traders adjust their positions. With this indicator, you can visualize these dates on your chart and analyze market behavior in the lead-up to, during, and after the expirations.

Input Options:

Expiration Types:

Monthly Equity, Index Expiration (OPEX): Turn on or off the monthly equity expiration markers.

Quarterly Index Expiration (Q): Turn on or off the quarterly expiration markers.

Monthly VIX Expiration (VIXEX): Turn on or off the VIX expiration markers.

Line and Label Customization:

Line Color: Adjust the color of the vertical lines marking the expiration events.

Label Color: Customize the color of the expiration labels.

Label Text Color: Adjust the color of the text inside the labels.

Label Position: Choose the position of the labels (e.g., top, bottom, above bar, below bar).

Use Cases:

Options Traders: Track options expiration dates to assess potential price swings or liquidity changes.

Volatility Traders: Watch for patterns around VIX options expirations.

Index Traders: Monitor quarterly expirations for potential market-moving events.

Example Use:

As a trader, you can apply this indicator to your chart and observe how price action reacts near expiration dates. For instance, on the monthly OPEX expiration day, you might notice increased volatility or an uptick in options-related price moves. By observing this trend over time, you can align your trades to capitalize on predictable movements around key expiration days.

Additionally, you may use the quarterly expiration markers to assess whether there’s typically a market shift during these periods, providing insights for long-term traders.

This indicator can be a helpful tool for preparing and managing trades around critical options expiration dates, helping to forecast potential market behavior based on historical patterns.

TradingView Community Guidelines Compliance: This script complies with TradingView's community guidelines by offering a clear and valuable function for traders, providing customizable inputs for enhanced usability. The script is focused on chart visualizations without manipulating or misrepresenting market data. It serves as an educational tool and a functional indicator, with no claims or misleading functionality. The indicator does not promote financial products or services and focuses solely on charting for better trading decision-making.

Williams Vix Fix BB + RVI & Squeeze (Keltner) filtered BBW + %BLegend:

- When line touches or crosses red band it is Top signal (Williams Vix Fix)

- When line touches or crosses blue band it is Bottom signal (Williams Vix Fix)

- Red dot at the top of indicator is a Top signal (Relative Volatility Index)

- Blue dot at the top of indicator is a Bottom signal (Relative Volatility Index)

- Gray dot at the bottom of indicator is a Keltner Squeeze signal (filtered by either BBW or %B)

- Silver dot at the bottom of indicator is a weaker Keltner Squeeze signal (Doesn't meet either BBW or %B filter)

- Purple is a 'Half Squeeze' only 1 Bollinger Band crossed the Keltner Channel

This is an attempt to make use of the main features of all 6 of these Volatility tools :

- Williams Vix Fix + Bollinger Bands

- Relative Volatility Index (RVI)

- The crossing of Keltner Channel by the Bollinger Bands (Squeeze)

Conditions to Help Filter Keltner Squeeze:

- When the Bollinger Bands Width (BBW) value is lower than the lowest value within a period plus a margin of error (percentage)

- When the %B value reaches the alert level detailed in LazyBears indicator. ()

If it meets one of these 2 filters and there is a Keltner Channel Squeeze than gray color or else if the squeeze doesn’t meet one of the 2 filters than silver color (weaker Squeeze).

The goal is to find the best tool to find bottoms and top relative to volatility and filter the squeeze.

The idea is that both Williams Vix Fix + Bollinger Bands and Relative Volatility Index both already give the main volatility bottom and top so combining them to compare and validate the signals makes sense. (Note: Bottom signal is more accurate than top). In addition, I added the squeeze to show the potential breakout pressure and to compliment bottom and top signals.

For ideas on how to continue this work :

I encourage ideas to combine the Williams Vix Fix and Relative Volatility Index for volatility top and bottom (with probability would be awesome)

And I encourage ideas to filter Keltner Channel Volatility Squeeze using both the BBW or %B or other volatility squeeze indicators or a combination of all of them.

Also, I encourage people to post their top parameters for the BBW and %B to filter the Keltner Squeeze in the comments or to send me them by chat relative to this indicator.

Half the battle is making the indicator, while the other half is tuning the parameters.

The current parameters are one of the least aggressive, and act as a mild filter.

Note: You can also change the threshold for RVI top and bottom.

And this work builds on my last indicator:

If you have ideas on this work or have ideas on potential combinations please message me, I always want to learn or get perspective on how it can be improved.

Sharing is how we get better (Parameter tuning, ideas, discussion)

I don’t reinvent the wheel, just trying to make the wheel better.

ES-VIX Expected Daily MoveThis indicator calculates the expected daily price movement for ES futures based on current volatility levels as measured by the VIX (CBOE Volatility Index).

Formula:

Expected Daily Move = (ES Price × VIX Price) / √252 / 100

The calculation converts the annualized VIX volatility into an expected daily move by dividing by the square root of 252 (the approximate number of trading days per year).

Features:

Real-time calculation using current ES futures price and VIX level

Histogram visualization in a separate pane for easy trend analysis

Information table displaying:

Current ES futures price

Current VIX level

Expected daily move in points

Expected daily move as a percentage

Dynamic Ratchet Trend Strategy [VIX Filter]Overview This strategy is a long-only trend-following system designed to capture major market moves while strictly managing downside risk through a state-machine based "Ratchet" exit logic. It incorporates a volatility filter using the CBOE VIX index to stay out of (or exit) the market during high-stress environments.

Key Features

1. Multi-Condition Entries The strategy looks for momentum shifts and trend breakouts using four Simple Moving Averages (25, 50, 100, 200).

Momentum Cross: SMA 25 crossover above SMA 50.

Trend Breakouts: A specific "3-Bar Breakout" logic above the SMA 50, 100, or 200. This requires the price to hold above the SMA for 3 consecutive bars after being below it, reducing false signals compared to simple closes.

2. VIX Volatility Filter Before entering any trade, the script checks the CBOE:VIX.

Filter: If VIX is above the threshold (default 32), new entries are blocked.

Panic Exit: If you are in a position and the VIX spikes above the threshold, the strategy executes an immediate "Panic Exit" to preserve capital during market crashes.

3. The "Ratchet" Exit System (3 Stages) Unlike a standard trailing stop, this strategy uses a 3-stage dynamic exit mechanism that tightens as profits grow:

Stage 0 (Initial Risk): Standard percentage-based Stop Loss from the entry price.

Stage 1 (The Lock-In): Triggered when profit hits 10% (configurable).

Unique Logic: Instead of trailing from the highest high, the stop is calculated based on the price at the exact moment this stage was triggered. It "steps up" once and holds, securing the initial move without being prematurely stopped out by normal volatility.

Stage 2 (Trailing Mode): Triggered when profit hits 15% (configurable).

The strategy switches to a classic Trailing Stop, following the percentage distance from the Highest High.

4. Emergency Backup A "Dead Cross" (SMA 25 crossing under SMA 50) acts as a final fail-safe to close positions if the trend reverses completely before hitting a stop.

Settings & Inputs

SMAs: Customize the lengths for all four moving averages.

VIX Filter: Toggle the filter on/off and set the panic threshold.

Exit Logic: Fully customizable percentages for Initial SL, Stage 1 Trigger/Distance, and Stage 2 Trigger/Trailing Distance.

Disclaimer This script is for educational purposes only. Past performance is not indicative of future results. Always manage your risk appropriately.

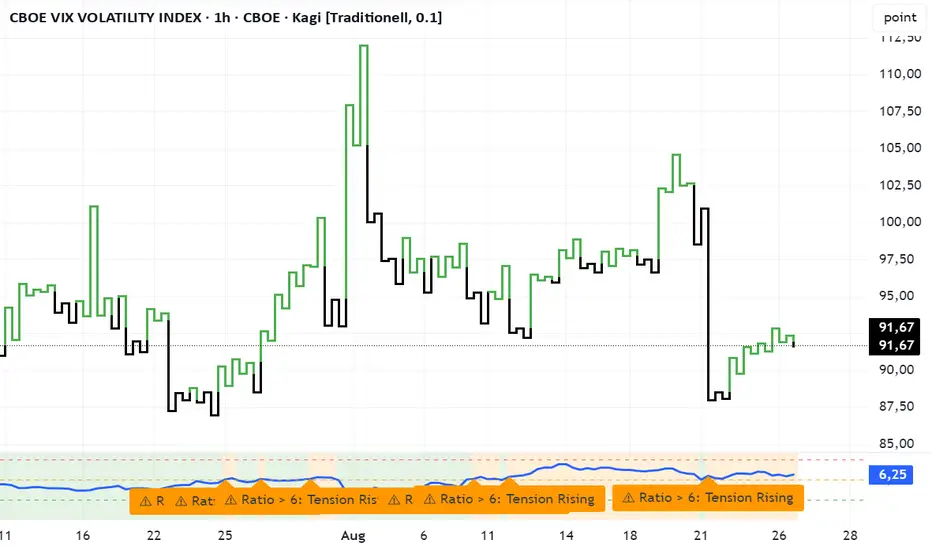

VVIX/VIX Ratio with Interpretation LevelsVVIX/VIX Ratio with Interpretation Levels

This indicator plots the ratio of VVIX (Volatility of Volatility Index) to VIX (CBOE Volatility Index) in a separate panel.

The ratio highlights when the options market is pricing unusually high volatility in volatility (VVIX) relative to the base volatility index (VIX).

Ratio < 5 → Complacency: Markets expect stability; often a pre-shock zone.

5–6 → Tension Building: Traders begin hedging volatility risk while VIX remains low.

6–7 → Elevated Risk: Divergence warns of potential regime change in volatility.

> 7 → High-Risk Zone: Options market pricing aggressive swings; can precede volatility spikes in equities.

The script also includes dashed interpretation lines (5, 6, 7) and automatic labels when key thresholds are crossed.

Background shading helps visualize current regime.

Use cases:

Detect hidden stress when VIX remains calm but VVIX rises.

Anticipate potential volatility regime shifts.

Support risk management and timing of long/short volatility strategies.

Mitsos4 RSI + BB + Dispersion + Trendlines + VIX Fix Mitsos4 RSI + BB + Dispersion + Trendlines + VIX Fix

This powerful custom indicator combines two analytical tools into one view:

RSI-based Bollinger Bands with Dispersion and the Vix Fix volatility spike detector.

It is designed for traders who want early volatility signals and precision RSI insights, all in a single pane.

🧩 What's Included:

✅ 1. RSI + BB (EMA) + Dispersion

RSI-Based Bollinger Bands: Tracks the RSI with Bollinger Bands using an EMA as the basis.

Dispersion Zone: A buffer zone around the moving average band for more sensitive overbought/oversold detection.

Dynamic RSI Coloring:

🟢 Green: RSI breaks above the dispersion zone.

🔴 Red: RSI breaks below the dispersion zone.

🟡 Yellow: RSI inside the zone (neutral).

Trendlines at RSI levels: 40 (green), 50 (yellow), 60 (red).

Alerts when RSI crosses dispersion zones.

✅ 2. CM_Williams_Vix_Fix

Designed to simulate VIX-like volatility spikes on non-VIX instruments.

Detects potential market bottoms by measuring price deviation from recent highs.

Includes:

Bollinger Band range on WVF.

Percentile high/low zones to detect significant volatility moves.

Histogram plot of WVF for quick visual alerts.

Color-coded spikes (green when above upper thresholds).

⚙️ User Controls:

Adjustable RSI, Bollinger Band, and dispersion settings.

Toggle options for:

Viewing high/low VIX percentiles.

Showing standard deviation bands for WVF.

Custom trendline display levels at RSI key areas.

📌 Best Use Cases:

Detect early market reversals and volatility spikes.

Combine RSI strength with volatility-based bottom signals.

Layer dispersion-based logic on top of classic RSI strategies.

Matrix Series and Vix Fix with VWAP CCI and QQE SignalsMatrix Series and Vix Fix with VWAP CCI and QQE Signals

Short Title: Advanced Matrix

Purpose

This Pine Script combines multiple technical analysis tools to create a comprehensive trading indicator. It incorporates elements like support/resistance zones, overbought/oversold conditions, Williams Vix Fix, QQE (Quantitative Qualitative Estimation) signals, VWAP CCI signals, and a 200-period SMA for trend filtering. The goal is to provide actionable buy and sell signals with enhanced visualization.

Key Features and Components

1. Matrix Series

Smoothing Input: Allows customization of EMA smoothing for the indicator (default: 5).

Support/Resistance Zones: Based on CCI (Commodity Channel Index) values.

Dynamic zones calculated with customizable parameters (SupResPeriod, SupResPercentage, PricePeriod).

Candlestick Visualization: Custom candlestick plots with colors indicating trends.

Dynamic levels for overbought/oversold conditions.

2. Overbought/Oversold Signals

Overbought and oversold levels are adjustable (ob and os).

Plots circles on the chart to highlight extreme conditions.

3. Williams Vix Fix

Identifies potential reversal points by analyzing volatility.

Uses Bollinger Bands and percentile thresholds to detect high-probability entries.

Includes two alert levels (alert1 and alert2) with customizable criteria for signal filtering.

4. QQE Signals

Based on the smoothed RSI and QQE methodology.

Detects trend changes using adaptive ATR bands (FastAtrRsiTL).

Plots long and short signals when specific conditions are met.

5. VWAP CCI Signals

Combines VWAP and CCI for additional trade signals.

Detects crossovers and crossunders of CCI levels (-200 and 200) to generate long and short signals.

6. 200 SMA

A 200-period simple moving average is plotted to act as a trend filter.

The script rules recommend buying only when the price is above the SMA200.

Customizable Inputs

General:

Smoothing, support/resistance periods, overbought/oversold levels.

Williams Vix Fix:

Lookback periods, Bollinger Band settings, percentile thresholds.

QQE:

RSI length, smoothing factor, QQE factor, and threshold values.

VWAP CCI:

Length for calculating deviations.

Visual Elements

Dynamic candlestick colors to indicate trend direction.

Overbought/oversold circles for extreme price levels.

Resistance and support lines.

Labels and shapes for buy/sell signals from Vix Fix, QQE, and VWAP CCI.

Alerts

Alerts are configured for the Matrix Series (e.g., "BUY MATRIX") and other components, ensuring traders are notified when significant conditions are met.

Intended Use

This indicator is designed for traders seeking a multi-faceted tool to analyze market trends, identify potential reversal points, and generate actionable trading signals. It combines traditional indicators with advanced techniques for comprehensive market analysis.

SVMKR_VIX_Based_LevelsThe "SVMKR_VIX_Based_Levels" script is a Pine Script indicator designed to assist intraday traders in identifying dynamic support and resistance levels based on the Volatility Index (VIX). Here's a breakdown of the script and its uses for intraday traders:

### Script Description:

1. **Data Retrieval**:

- The script fetches daily closing prices of the India VIX (volatility index) and a specified security using `request.security()`.

2. **Input Parameters**:

- Intraday traders can customize the indicator using input parameters such as the number of levels above and below the Pivot Day Close (PDC), line offset lengths, line extension options, and color and width settings for plotted lines.

3. **Plotting**:

- The script plots the PDC and VIX as hidden lines (`display=display.none`).

- Support and resistance levels are calculated based on the VIX and PDC, and plotted above and below the PDC with customizable colors and widths.

- Each level can be labeled with its corresponding price.

4. **Customization**:

- Intraday traders can choose to display or hide prices on the plotted lines.

- Colors and widths of plotted lines are customizable.

- Options to show minor and mild support levels provide additional flexibility.

5. **Labels**:

- Labels are added to indicate the PDC and the plotted levels, displaying corresponding prices if enabled.

### Uses for Intraday Traders:

1. **Dynamic Support and Resistance**: Intraday traders can benefit from dynamically adjusted support and resistance levels that respond to changes in market volatility, providing more accurate levels for trade planning.

2. **Market Sentiment Analysis**: By incorporating the VIX, a measure of market volatility and sentiment, the indicator provides insights into market sentiment, helping intraday traders gauge market mood and potential direction.

3. **Confirmation of Price Action**: The plotted support and resistance levels can serve as confirmation signals for intraday traders, helping validate trading decisions and enhance trading confidence.

4. **Adaptability to Changing Market Conditions**: Intraday traders often face rapidly changing market conditions. The indicator's ability to adapt to changes in volatility ensures that plotted levels remain relevant and responsive, aiding traders in adjusting their strategies accordingly.

5. **Trade Planning and Execution**: Intraday traders can use the plotted support and resistance levels to identify potential entry and exit points, set profit targets and stop-loss levels, and plan their trades more effectively.

Overall, the "SVMKR_VIX_Based_Levels" indicator provides intraday traders with a valuable tool for dynamic support and resistance identification, market sentiment analysis, confirmation of price action, and trade planning and execution, ultimately assisting them in making more informed and profitable trading decisions in the intraday timeframe.

Volatility Inverse Correlation CandleThis is an educational tool that can help you find direct or inverse relations between two assets.

In this case I am using VIX and SPX .

The way it works is the next one :

So I am looking at the current open value of VIX in comparison with the previous close ( if it either above or below) and after on the SPX I am looking into the history and see for example which type of candle we had in respect with the opening value from VIX .

So for example, lets imagine that today is monday, and the weekly open value from VIX was higher than previous friday close value. Now I am going to see with the inverse correlation , if based on this idea, the current weekly candle from SPX finished in a bear candle.

The same can be applied for the bearish situation, so if we had an open from VIX lower than previous close, we are looking to check the SPX bull candle accuracy.

At the same time, for a different type of calculation I have added an internal lookup into heikin ashi values.

If you have any questions please let me know !

Stock vs Index vs Vix (Adjusted)

Usually stocks move with Indexes and against Vix, so with this script you can compare and see how strong is the price movement of an asset.

Try to find what Index (e.g. SPY, QQQ, IWM) and Vix (e.g. VIX, VXN, RVX) fits better for selected symbol.

If price moving in the upper channel = price movement is strong.

If price moving in the lower channel = price movement is weak.

If price is stronger than Index and Vix = good sign.

If price is weaker than Index and Vix = bad sign.

Strong support and resistance lines are at 66.6 and 33.3

Disclaimer:

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitute professional and/or financial advice. You alone have the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

vix_roll_yieldShows the roll yield of the VX futures, which is the ratio of a continuously weighted average of the front two months to the VIX. The VX (VIX futures) contract expires on the third Tuesday of each month. On the next trading day, the front month will have full weighting, and the second month will have no weight. On the expiration day, the back month will have full weighting and the front month will have no weight. In between, the weight gradually shifts.

This weighted average is similar to the SPVIXSTR index that UVXY and several other funds track. When the average is below the VIX, the indicator is negative, and the front month contract will tend to gain value relatively more rapidly than the back month as it converges upward to the VIX spot price. Because funds whose NAV is tied up in VX contracts continuously roll from the (typically cheaper) front month to the back, in situations where the front month is more expensive than usual--or even more expensive than the back month--these products may have a "tailwind". In this case, they are selling expensive front month contracts to purchase cheap back month contracts.

Ordinarily, VIX funds have a "headwind." The roll yield is positive, the front month is cheap, and the back month is expensive. Day by day the funds sell cheap front month contracts and buy expensive back month contracts, which, in turn and over time, become the front month and converge with the VIX, losing value rapidly. This is a brief explanation about the decay of these products.

Williams Vix Fix + BB & RVI (Top/Bottom) & SqueezeLegend :

- When line touches or crosses red band it is Top signal (Williams Vix Fix)

- When line touches or crosses blue band it is Bottom signal (Williams Vix Fix)

- Red dot at the top of indicator is a Top signal (Relative Volatility Index)

- Blue dot at the top of indicator is a Bottom signal (Relative Volatility Index)

- Gray dot at the bottom of indicator is a Squeeze signal

This is an attempt to make use of the main features of all 4 of these very popular Volatility tools :

- Williams Vix Fix + Bollinger Bands (as per Larry Williams idea, link )

- Relative Volatility Index (RVI)

- The crossing of Keltner Channel by the Bollinger Bands (Squeeze)

The goal is to find the best tool to find bottoms and top relative to volatility . This is a simple combination, but I find it very useful personally

(no need to reinvent the wheel, just need to find what works best)

The idea is that Williams Vix Fix + Bollinger Bands already give the main volatility bottom and top (Bottom are more accurate).

So instead of trying to modify it, I chose to compliment it by mapping with points when the Relative Volatility Index (RVI) reached the

top/bottom thresholds (red dot means top and blue dot means bottom). That way we can easily see when both indicators find a top or bottom relative

to volatility (of course this needs to be then confirmed with a momentum indicator rally).

In addition, I added the squeeze because this quickly shows the potential breakouts.

For ideas on how to continue this work, it would be very interesting to be able to create a probability of a bottom and top relative to volatility using the

Williams Vix Fix + Bollinger Bands and "Relative Volatility Index" signals as both work well and give top or bottom the other doesn't see.

Bollinger Bands %B Compare VixThis imple script converts your chosen chart price and outputs it as a percentage in relation to the Vix percentage.

If price (Blue line) is higher than 0.60 and vix (Red Line) is lower than 0. 40 then there is lower volatility and this is good for buying.

If price (Blue line) is lower than 0. 40 and vix (Red Line) is higher than 0.60 then there is higher volatility and this is good for selling, exiting and cash only.

If you like risk you can enter as soon as the price and vix cross in either direction

This is my first script, please give me a lot of critique, I won't cry hahaha :)

For greater accuracy, you use these Vix products for their specific stocks/Indicies:

Apple - VXAPL

Google - VXGOG

Amazon - CBOE:VXAZN

IBM - CBOE:VXIBM

Goldman Sachs - CBOE:VXGS

NASDAQ 100 = CBOE:VXN

SP100 - CBOE:VXO

SP500 (3months) - VIX3M

XLE(energy sector) - CBOE:VXXLE

EWZ(brazil etf) - VXEWZ

EEM( emerging markets etf) - CBOE:VXEEM

EFA (MSCI ETF) - CBOE:VXEFA

FXI (Cina ETF) - CBOE:VXFXI

(JS)S&P 500 Volatility Oscillator For Options 2.0I am going to start taking requests to open source my indicators and they will also be updated to Version 4 of Pinescript.

I added some features to the original code such the ability to smooth the oscillator and select the look back periods for the historical volatility.

Link to original:

Original post:

"The idea for this started here: www.tradingview.com with the user @dime

This should only be used on SPX or SPY (though you could use it on other things for correlation I suppose) given that the instrument used to create this calculation is derived from the S&P 500 (thank you VIX ). There's a lot of moving parts here though, so allow me to explain...

First: The main signal is when Implied Volatility (from VIX ) drops beneath Historical Volatility - which is what you want to see so you aren't purchasing a ton of premium on long options. Green and above 0 means that IV% has dropped lower than Historical Volatility . (this signal, for example, would suggest using a Long Call or Put depending on your sentiment)

Second: The green line running underneath zero is the bottom portion of the "Average True Range" derived from the values used to create the oscillator. the closer the bottom histogram is to the green line, the more "normal" IV% is. Obviously, if this gets far away from the line then it could be setting up nicely to short options and sell the IV premium to someone else. (this signal, for example, would suggest using something like a Bull Put Spread)

Third: The red background along with the white line that drops down below zero signals when (and how far) the IV% from 3 months out (from VIX3M ) is less than the current IV%. This would signal the current environment has IV way too high, a signal to short options once again (and don't take any long option positions!).

Tried to make this simple, yet effective. If you trade options on SPX , SPY , even ES1! futures - this is a tool tailored specifically for you! As I said before, if you want you can use it for correlation on other securities. Any other ideas or suggestions surrounding this, please let me know! Enjoy!

Feb 17, 2019

Release Notes: Cosmetic update for a much cleaner look:

-Replaced the "HIGH IV" with a simlple "H"

-Now the white line is constantly showing you the relationship between VIX and VIX3M - when VIX is greater than VIX3M the background still goes red

-However, now when VIX drops below Historical Volatility, the background is bright green

-When both above are true - it's dark green

-The Average True Range on the bottom is now a series of crosses"