Flux Power Dashboard (Updated and Renamed)Flux Power Dashboard is a compact market-state heads-up display for TradingView. It blends trend, momentum, and volume-flow into a single on-chart panel with color-coded cues and minimal lag. You get:

Clean visual trend via fast/slow MA with slope/debounce filters

MACD state and most recent cross (with “freshness” tint)

OBV confirmation and gating to reduce noise

Session awareness (Asia/London/New York + pre-sessions + overlap)

Optional HTF Regime row and regime gate to align signals to higher-timeframe bias

Context from VIX/VXN (volatility regime)

A single Flux Score (0–100) as a top-level read

It is deliberately “dashboard-first”: fast to read, consistent between symbols/timeframes, and designed to limit overtrading in chop.

What it can do (capabilities)

Signal gating: You can require multiple pillars to agree (Trend, MACD, OBV) before a “strong” bias is shown.

Debounced trend: Uses slope + confirmation bars to avoid flip-flopping.

Session presets: Auto-adjust the minimum confirmation bars by session (e.g., NY vs London vs Asia) to better match liquidity/volatility.

MACD presets: Quick switch between Scalp / Classic / Slow or roll your own custom speeds.

OBV confirmation: Volume flow must agree for trend/entries to “count” (optional).

HTF Regime awareness: Shows the higher-timeframe backdrop and (optionally) gates signals so you don’t fight the dominant trend.

Volatility context: VIX/VXN auto-colored cells based on your thresholds.

Top-center Session Title: Broadcasts the active session (or Overlap) with a matched background color.

Customizable UI: Column fonts, params font, transparency, dashboard corner, marker styles, colors, widths—tune it to your chart.

Practical use: Start with Flux Score + Summary for a snapshot, confirm with Trend & MACD, check OBV agreement (implicit in signal strength), glance at Regime to avoid counter-trend trades, and use Session + VIX/VXN for timing and risk context.

How it avoids common pitfalls

Repaint-aware: “Confirm on Close” can be enabled to read prior bar states, reducing intrabar noise.

Auto MA sanity: If fast ≥ slow length, it auto-swaps under the hood to keep calculations valid.

Debounce & confirm: Trend flips only after X bars satisfy conditions, cutting false flips in chop.

Freshness tint: New Cross/Signal rows tint slightly brighter for a few bars, so you can spot recency at a glance.

Every line of the dashboard (what it shows, how it’s colored)

Flux Score

What: Composite 0–100 built from three pillars: Trend (40%), MACD (30%), OBV (30%).

Read: ≥70 Bullish, ≤30 Bearish, else Neutral.

Use: Quick “state of play” gauge—stronger alignment pushes the score toward extremes.

Regime (optional row)

What: Higher-timeframe (your Regime TF) backdrop using the same MA pair with HTF slope/ATR buffer.

Values: Bull / Bear / Range.

Gate (optional): If Regime Gate is ON, Trend/Signals only go directional when HTF agrees.

Summary

What: One-line narrative combining the three pillars: MACD (up/down/flat), OBV (up/down/flat), Trend (up/down/flat).

Use: Human-readable cross-check; should rhyme with Flux Score.

Trend

What: Debounced MA relationship on the current chart.

Strict: needs fast > slow and slow rising (mirror for down) + slope debounce + confirmation bars.

Lenient: allows fast > slow or slow rising (mirror for down) with the same debounce/confirm.

Color: Green = UP, Red = DOWN, Gray = FLAT.

Use: Your structural bias on the trading timeframe.

MACD

What: Current MACD line vs signal, using your selected preset (or custom).

Values: Bull (line above), Bear (below), Flat (equal/indeterminate).

Color: Green/Red/Gray.

Cross

What: Most recent MACD cross and how many bars ago it occurred (e.g., “MACD XUP | 3 bars”).

Freshness: If the cross happened within Fresh Signal Tint bars, the cell brightens slightly.

Use: Timing helper for inflection points.

Signal

What: Latest directional shift (from short-bias to long-bias or vice versa) and age in bars.

Strength:

Strong = Trend + MACD + OBV all align

Weak = partial alignment (e.g., Trend + MACD, or Trend + OBV)

Color: Green for long bias, Red for short bias; fresh signals tint brighter.

Use: Action cue—treat Strong as higher quality; Weak as situational.

MA

What: Your slow MA type and length, plus slope direction (“up”/“down”).

Use: Context even when Trend is FLAT; slope often turns before full trend flips.

Session

What: Current market session by Eastern Time: New York / London / Asia, Pre- windows, Overlap, or Off-hours.

Logic: If ≥2 main sessions are active, shows Overlap (and grays the top title background).

Use: Timing and expectations for liquidity/volatility; also drives session-based confirmation presets if enabled.

VIX

What: Real-time CBOE:VIX on your chosen TF.

Auto-color (if on):

Calm (< Calm) → Green

Watch (< Watch) → Yellow

Elevated (< Elevated) → Orange

Very High (≥ Elevated) → Red

Use: Equity market–wide risk mood; higher = bigger moves, lower = quieter.

VXN

What: CBOE:VXN (Nasdaq volatility index) on your chosen TF.

Auto-color thresholds like VIX.

Use: Tech-heavy risk mood; helpful for growth/QQQ/NDX names.

Footer (params row, bottom-right)

What: Key live settings so you always know the context:

P= Trend Confirmation Bars

O= OBV Confirmation Bars

Strict/Lenient (trend mode)

MACD preset (or “Custom”)

swap if MA lengths were auto-swapped for validity

Regime gate if enabled

Candles for clarity

Use: Quick integrity check when comparing charts/screenshots or changing presets.

Recommended workflow

Start at Flux Score & Summary → snapshot of alignment.

Check Trend (color) and MACD (Bull/Bear).

Look at Signal (Strong vs Weak, and age).

Glance at Regime (and use gate if you’re trend-following).

Use Session + VIX/VXN to adjust expectations (breakout vs mean-revert, risk sizing, patience).

Keep Confirm on Close ON when you want stability; turn it OFF for faster (but noisier) reads.

Notes & limitations

Not advice: This is an informational tool; always combine with your own risk rules.

Repaint vs responsiveness: With “Confirm on Close” OFF you’ll see faster state changes but may get more churn intrabar.

Presets matter: Scalp MACD reacts fastest; Slow reduces whipsaw. Choose for your timeframe.

Session windows depend on the strings you set; adjust if your broker’s feed or DST handling needs tweaks.

Cari dalam skrip untuk "如何用wind搜索股票的发行价和份数"

Commodity Channel Index DualThe CCI Dual is a custom TradingView indicator built in Pine Script v5, designed to help traders identify potential buy and sell signals using two Commodity Channel Index (CCI) oscillators. It combines a shorter-period CCI (default: 14) for quick momentum detection with a longer-period CCI (default: 50) for confirmation, focusing on mean-reversion opportunities in overbought or oversold conditions.

This setup is particularly suited for volatile markets like cryptocurrencies on higher timeframes (e.g., 3-day charts), where it highlights reversals by requiring both CCIs to cross out of extreme zones within a short window (default: 3 bars).

The indicator plots the CCIs, customizable bands (inner: 100, OB/OS: 175, outer: 200), dynamic fills for visual emphasis, background highlights for signals, and alert conditions for notifications.

How It Works

The indicator calculates two CCIs based on user-defined lengths and source (default: close price):

CCI Calculation: CCI measures price deviation from its average, using the formula: CCI = (Typical Price - Simple Moving Average) / (0.015 * Mean Deviation). The short CCI reacts faster to price changes, while the long CCI provides smoother, trend-aware confirmation.

Overbought/Oversold Levels: Customizable thresholds define extremes (Overbought at +175, Oversold at -175 by default). Bands are plotted at inner (±100), mid (±175 dashed), and outer (±200) levels, with gray fills for the outer zones.

Dynamic Fills: The longer CCI is used to shade areas beyond OB/OS levels in red (overbought) or green (oversold) for quick visual cues.

Signals:

Buy Signal: Triggers when both CCIs cross above the Oversold level (-175) within the signal window (3 bars). This suggests a potential upward reversal from an oversold state.

Sell Signal: Triggers when both cross below the Overbought level (+175) within the window, indicating a possible downward reversal.

Visuals and Alerts: Buy signals highlight the background green, sells red. Separate alertconditions allow setting TradingView alerts for buys or sells independently.

Customization: Adjust lengths, levels, and window via inputs to fit your timeframe or asset—e.g., higher OB/OS for crypto volatility.

This logic reduces noise by requiring dual confirmation, but like all oscillators, it can produce false signals in strong trends where prices stay extended.

To mitigate false signals (e.g., in trending markets), layer the CCI Dual with MACD (default: 12,26,9) and RSI (default: 14) for multi-indicator confirmation:

With MACD: Only take CCI buys if the MACD line is above the signal line (or histogram positive), confirming bullish momentum. For sells, require MACD bearish crossover. This filters counter-trend signals by aligning with trend strength—e.g., ignore CCI sells if MACD shows upward momentum.

With RSI: Confirm CCI oversold buys only if RSI is below 30 and rising (or shows bullish divergence). For overbought sells, RSI above 70 and falling. This adds overextension validation, reducing whipsaws in crypto trends.

I made this customizable for you to find what works best for your asset you are trading. I trade the 6 hour and 3 day timeframe mainly on major cryptocurrency pairs. I hope you enjoy this script and it serves you well.

Moving Average Adaptive RSI [BackQuant]Moving Average Adaptive RSI

What this is

A momentum oscillator that reshapes classic RSI into a zero-centered column plot and makes it adaptive. It builds RSI from two parts:

• A sensitivity window that scans several recent bars to capture the strongest up and down impulses.

• A selectable moving average that smooths those impulses before computing RSI.

The output ranges roughly from −100 to +100 with 0 as the midline, with optional extra smoothing and built-in divergence detection.

How it works

Impulse extraction

• For each bar the script inspects the last rsi_sen bars and collects upward and downward price changes versus the current price.

• It keeps the maximum upward change and maximum downward change from that window, emphasizing true bursts over single-bar noise.

MA-based averaging

• The up and down impulse series are averaged with your chosen MA over rsi_len bars.

• Supported MA types: SMA, EMA, DEMA, WMA, HMA, SMMA (RMA), TEMA.

Zero-centered RSI transform

• RS = UpMA ÷ DownMA, then mapped to a symmetric scale: 100 − 200 ÷ (1 + RS) .

• Above 0 implies positive momentum bias. Below 0 implies negative momentum bias.

Optional extra smoothing

• A second smoothing pass can be applied to the final oscillator using smoothing_len and smooth_type . Toggle with “Use Extra Smoothing”.

Visual encoding

• The oscillator is drawn as columns around the zero line with a gradient that intensifies toward extremes.

• Static bands mark 80 to 100 and −80 to −100 for extreme conditions.

Key inputs and what they change

• Price Source : input series for momentum.

• Calculation Period (rsi_len) : primary averaging window on up and down components. Higher = smoother, slower.

• Sensitivity (rsi_sen) : how many recent bars are scanned to find max impulses. Higher = more responsive to bursts.

• Calculation Type (ma_type) : MA family that shapes the core behavior. HMA or DEMA is faster, SMA or SMMA is slower.

• Smoothing Type and Length : optional second pass to calm noise on the final output.

• UI toggles : show or hide the oscillator, candle painting, and extreme bands.

Reading the oscillator

• Midline cross up (0) : momentum bias turning positive.

• Midline cross down (0) : momentum bias turning negative.

• Positive territory :

– 0 to 40: constructive but not stretched.

– 40 to 80: strong momentum, continuation more likely.

– Above 80: extreme risk of mean reversion grows.

• Negative territory : mirror the same levels for the downside.

Divergence detection

The script plots four divergence types using pivot highs and lows on both price and the oscillator. Lookbacks are set by lbL and lbR .

• Regular bullish : price lower low, oscillator higher low. Possible downside exhaustion.

• Hidden bullish : price higher low, oscillator lower low. Bias to trend continuation up.

• Regular bearish : price higher high, oscillator lower high. Possible upside exhaustion.

• Hidden bearish : price lower high, oscillator higher high. Bias to trend continuation down.

Labels: ℝ for regular, ℍ for hidden. Green for bullish, red for bearish.

Candle coloring

• Optional bar painting: green when the oscillator is above 0, red when below 0. This is for visual scanning only.

Strengths

• Adaptive sensitivity via a rolling impulse window that responds to genuine bursts.

• Configurable MA core so you can match responsiveness to the instrument.

• Zero-centered scale for simple regime reads with 0 as a clear bias line.

• Built-in regular and hidden divergence mapping.

• Flexible across symbols and timeframes once tuned.

Limitations and cautions

• Trends can remain extended. Treat extremes as context rather than automatic reversal signals.

• Divergence quality depends on pivot lookbacks. Short lookbacks give more signals with more noise. Long lookbacks reduce noise but add lag.

• Double smoothing can delay zero-line transitions. Balance smoothness and timeliness.

Practical usage ideas

• Regime filter : only take long setups from your separate method when the oscillator is above 0, shorts when below 0.

• Pullback confirmation : in uptrends, look for dips that hold above 0 or turn up from 0 to 40. Reverse for downtrends.

• Divergence as a heads-up : wait for a zero-line cross or a price trigger before acting on divergence.

• Sensitivity tuning : start with rsi_sen 2 to 5 on faster timeframes, increase slightly on slower charts.

Alerts

• MA-A RSI Long : oscillator crosses above 0.

• MA-A RSI Short : oscillator crosses below 0.

Use these as bias or timing aids, not standalone trade commands.

Settings quick reference

• Calculation : Price Source, Calculation Type, Calculation Period, Sensitivity.

• Smoothing : Smoothing Type, Smoothing Length, Use Extra Smoothing.

• UI : Show Oscillator, Paint Candles, Show Static High and Low Levels.

• Divergences : Pivot Lookback Left and Right, Div Signal Length, Show Detected Divergences.

Final thoughts

This tool reframes RSI by extracting strong short-term impulses and averaging them with a moving-average model of your choice, then presenting a zero-centered output for clear regime reads. Pair it with your structure, risk and execution process, and tune sensitivity and smoothing to the market you trade.

Volumetric Support and Resistance [BackQuant]Volumetric Support and Resistance

What this is

This Overlay locates price levels where both structure and participation have been meaningful. It combines classical swing points with a volume filter, then manages those levels on the chart as price evolves. Each level carries:

• A reference price (support or resistance)

• An estimate of the volume that traded around that price

• A touch counter that updates when price retests it

• A visual box whose thickness is scaled by volatility

The result is a concise map of candidate support and resistance that is informed by both price location and how much trading occurred there.

How levels are built

Find structural pivots uses ta.pivothigh and ta.pivotlow with a user set sensitivity. Larger sensitivity looks for broader swings. Smaller sensitivity captures tighter turns.

Require meaningful volume computes an average volume over a lookback period and forms a volume ratio for the current bar. A pivot only becomes a level when the ratio is at least the volume significance multiplier.

Avoid clustering checks a minimum level distance (as a percent of price). If a candidate is too close to an existing level, it is skipped to keep the map readable.

Attach a volume strength to the level estimates volume strength by averaging the volume of recent bars whose high to low range spans that price. Levels with unusually high strength are flagged as high volume.

Store and draw levels are kept in an array with fields for price, type, volume, touches, creation bar, and a box handle. On the last bar, each level is drawn as a horizontal box centered at the price with a vertical thickness scaled by ATR. Borders are thicker when the level is marked high volume. Boxes can extend into the future.

How levels evolve over time

• Aging and pruning : levels are removed if they are too old relative to the lookback or if you exceed the maximum active levels.

• Break detection : a level can be removed when price closes through it by more than a break threshold set as a fraction of ATR. Toggle with Remove Broken Levels.

• Touches : when price approaches within the break threshold, the level’s touch counter increments.

Visual encoding

• Boxes : support boxes are green, resistance boxes are red. Box height uses an ATR based thickness so tolerance scales with volatility. Transparency is fixed in this version. Borders are thicker on high volume levels.

• Volume annotation : show the estimated volume inside the box or as a label at the right. If a level has more than one touch, a suffix like “(2x)” is appended.

• Extension : boxes can extend a fixed number of bars into the future and can be set to extend right.

• High volume bar tint : bars with volume above average × multiplier are tinted green if up and red if down.

Inputs at a glance

Core Settings

• Level Detection Sensitivity — pivot window for swing detection

• Volume Significance Multiplier — minimum volume ratio to accept a pivot

• Lookback Period — window for average volume and maintenance rules

Level Management

• Maximum Active Levels — cap on concurrently drawn levels

• Minimum Level Distance (%) — required spacing between level prices

Visual Settings

• Remove Broken Levels — drop a level once price closes decisively through it

• Show Volume Information on Levels — annotate volume and touches

• Extend Levels to Right — carry boxes forward

Enhanced Visual Settings

• Show Volume Text Inside Box — text placement option

• Volume Based Transparency and Volume Based Border Thickness — helper logic provided; current draw block fixes transparency and increases border width on high volume levels

Colors

• Separate colors for support, resistance, and their high volume variants

How it can be used

• Trade planning : use the most recent support and resistance as reference zones for entries, profit taking, or stop placement. ATR scaled thickness provides a practical buffer.

• Context for patterns : combine with breakouts, pullbacks, or candle patterns. A breakout through a high volume resistance carries more informational weight than one through a thin level.

• Prioritization : when multiple levels are nearby, prefer high volume or higher touch counts.

• Regime adaptation : widen sensitivity and increase minimum distance in fast regimes to avoid clutter. Tighten them in calm regimes to capture more granularity.

Why volume support and resistance is used in trading

Support and resistance relate to willingness to transact at certain prices. Volume measures participation. When many contracts change hands near a price:

• More market players hold inventory there, often creating responsive behavior on retests

• Order flow can concentrate again to defend or to exit

• Breaks can be cleaner as trapped inventory rebalances

Conditioning level detection on above average activity focuses attention on prices that mattered to more participants.

Alerts

• New Support Level Created

• New Resistance Level Created

• Level Touch Alert

• Level Break Alert

Strengths

• Dual filter of structure and participation, reducing trivial swing points

• Self cleaning map that retires old or invalid levels

• Volatility aware presentation using ATR based thickness

• Touch counting for persistence assessment

• Tunable inputs for instrument and timeframe

Limitations and caveats

• Volume strength is an approximation based on bars spanning the price, not true per price volume

• Pivots confirm after the sensitivity window completes, so new levels appear with a delay

• Narrow ranges can still cluster levels unless minimum distance is increased

• Large gaps may jump past levels and immediately trigger break conditions

Practical tuning guide

• If the chart is crowded: increase sensitivity, increase minimum level distance, or reduce maximum active levels

• If useful levels are missed: reduce volume multiplier or sensitivity

• If you want stricter break removal: increase the ATR based break threshold in code

• For instruments with session patterns: tailor the lookback period to a representative window

Interpreting touches and breaks

• First touch after creation is a validation test

• Multiple shallow touches suggest absorption; a later break may then travel farther

• Breaks on high current volume merit extra attention

Multi timeframe usage

Levels are computed on the active chart timeframe. A common workflow is to keep a higher timeframe instance for structure and a lower timeframe instance for execution. Align trades with higher timeframe levels where possible.

Final Thoughts

This indicator builds a lightweight, self updating map of support and resistance grounded in swings and participation. It is not a full market profile, but it captures much of the practical benefit with modest complexity. Treat levels as context and decision zones, not guarantees. Combine with your entry logic and risk controls.

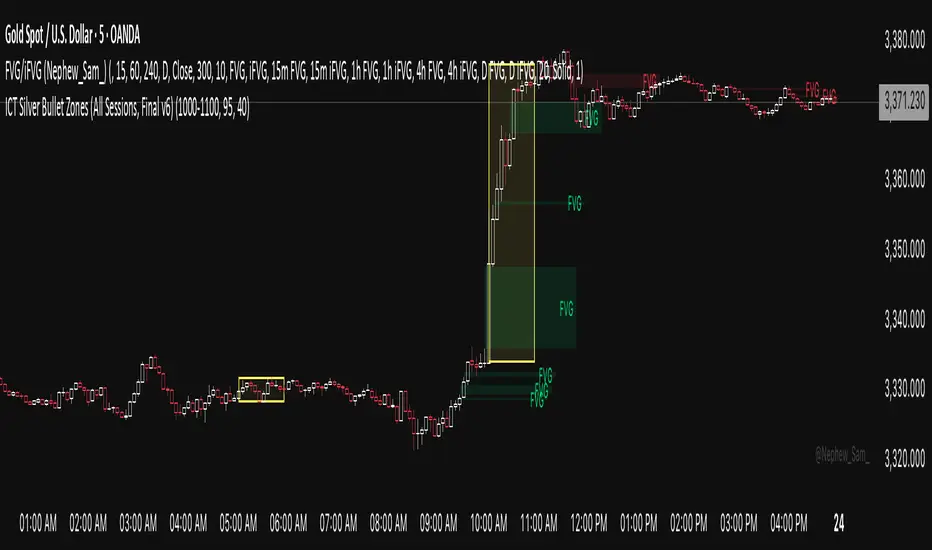

ICT Silver Bullet Zones (All Sessions)This Pine Script v6 indicator highlights the ICT Silver Bullet windows (10:00–11:00 local time) for all major forex/trading sessions: London, New York AM, New York PM, and Asia.

✅ Features:

Clearly visualizes Silver Bullet zones for each session.

Labels are centered inside each zone for easy identification.

Fully compatible with Pine Script v6 and TradingView.

Adjustable opacity and label size for better chart visibility.

Works on any timeframe and keeps historical zones visible.

Use Case:

Perfect for ICT strategy traders who want to identify high-probability trading windows during major market sessions. Helps in planning entries and understanding liquidity timing without cluttering the chart.

Instructions:

Add the script to your TradingView chart.

Adjust opacity and label size to suit your chart style.

Observe the SB zones for all sessions and plan trades according to ICT methodology.

VWAP For Loop [BackQuant]VWAP For Loop

What this tool does—in one sentence

A volume-weighted trend gauge that anchors VWAP to a calendar period (day/week/month/quarter/year) and then scores the persistence of that VWAP trend with a simple for-loop “breadth” count; the result is a clean, threshold-driven oscillator plus an optional VWAP overlay and alerts.

Plain-English overview

Instead of judging raw price alone, this indicator focuses on anchored VWAP —the market’s average price paid during your chosen institutional period. It then asks a simple question across a configurable set of lookback steps: “Is the current anchored VWAP higher than it was i bars ago—or lower?” Each “yes” adds +1, each “no” adds −1. Summing those answers creates a score that reflects how consistently the volume-weighted trend has been rising or falling. Extreme positive scores imply persistent, broad strength; deeply negative scores imply persistent weakness. Crossing predefined thresholds produces objective long/short events and color-coded context.

Under the hood

• Anchoring — VWAP using hlc3 × volume resets exactly when the selected period rolls:

Day → session change, Week → new week, Month → new month, Quarter/Year → calendar quarter/year.

• For-loop scoring — For lag steps i = , compare today’s VWAP to VWAP .

– If VWAP > VWAP , add +1.

– Else, add −1.

The final score ∈ , where N = (end − start + 1). With defaults (1→45), N = 45.

• Signal logic (stateful)

– Long when score > upper (e.g., > 40 with N = 45 → VWAP higher than ~89% of checked lags).

– Short on crossunder of lower (e.g., dropping below −10).

– A compact state variable ( out ) holds the current regime: +1 (long), −1 (short), otherwise unchanged. This “stickiness” avoids constant flipping between bars without sufficient evidence.

Why VWAP + a breadth score?

• VWAP aggregates both price and volume—where participants actually traded.

• The breadth-style count rewards consistency of the anchored trend, not one-off spikes.

• Thresholds give you binary structure when you need it (alerts, automation), without complex math.

What you’ll see on the chart

• Sub-pane oscillator — The for-loop score line, colored by regime (long/short/neutral).

• Main-pane VWAP (optional) — Even though the indicator runs off-chart, the anchored VWAP can be overlaid on price (toggle visibility and whether it inherits trend colors).

• Threshold guides — Horizontal lines for the long/short bands (toggle).

• Cosmetics — Optional candle painting and background shading by regime; adjustable line width and colors.

Input map (quick reference)

• VWAP Anchor Period — Day, Week, Month, Quarter, Year.

• Calculation Start/End — The for-loop lag window . With 1→45, you evaluate 45 comparisons.

• Long/Short Thresholds — Default upper=40, lower=−10 (asymmetric by design; see below).

• UI/Style — Show thresholds, paint candles, background color, line width, VWAP visibility and coloring, custom long/short colors.

Interpreting the score

• Near +N — Current anchored VWAP is above most historical VWAP checkpoints in the window → entrenched strength.

• Near −N — Current anchored VWAP is below most checkpoints → entrenched weakness.

• Between — Mixed, choppy, or transitioning regimes; use thresholds to avoid reacting to noise.

Why the asymmetric default thresholds?

• Long = score > upper (40) — Demands unusually broad upside persistence before declaring “long regime.”

• Short = crossunder lower (−10) — Triggers only on downward momentum events (a fresh breach), not merely being below −10. This combination tends to:

– Capture sustained uptrends only when they’re very strong.

– Flag downside turns as they occur, rather than waiting for an extreme negative breadth.

Tuning guide

Choose an anchor that matches your horizon

– Intraday scalps : Day anchor on intraday charts.

– Swing/position : Month or Quarter anchor on 1h/4h/D charts to capture institutional cycles.

Pick the for-loop window

– Larger N (bigger end) = stronger evidence requirement, smoother oscillator.

– Smaller N = faster, more reactive score.

Set achievable thresholds

– Ensure upper ≤ N and lower ≥ −N ; if N=30, an upper of 40 can never trigger.

– Symmetric setups (e.g., +20/−20) are fine if you want balanced behavior.

Match visuals to intent

– Enabling VWAP coloring lets you see regime directly on price.

– Background shading is useful for discretionary reading; turn it off for cleaner automation displays.

Playbook examples

• Trend confirmation with disciplined entries — On Month anchor, N=45, upper=38–42: when the long regime engages, use pullbacks toward anchored VWAP on the main pane for entries, with stops just beyond VWAP or a recent swing.

• Downside transition detection — Keep lower around −8…−12 and watch for crossunders; combine with price losing anchored VWAP to validate risk-off.

• Intraday bias filter — Day anchor on a 5–15m chart, N=20–30, upper ~ 16–20, lower ~ −6…−10. Only take longs while score is positive and above a midline you define (e.g., 0), and shorts only after a genuine crossunder.

Behavior around resets (important)

Anchored VWAP is hard-reset each period. Immediately after a reset, the series can be young and comparisons to pre-reset values may span two periods. If you prefer within-period evaluation only, choose end small enough not to bridge typical period length on your timeframe, or accept that the breadth test intentionally spans regimes.

Alerts included

• VWAP FL Long — Fires when the long condition is true (score > upper and not in short).

• VWAP FL Short — Fires on crossunder of the lower threshold (event-driven).

Messages include {{ticker}} and {{interval}} placeholders for routing.

Strengths

• Simple, transparent math — Easy to reason about and validate.

• Volume-aware by construction — Decisions reference VWAP, not just price.

• Robust to single-bar noise — Needs many lags to agree before flipping state (by design, via thresholds and the stateful output).

Limitations & cautions

• Threshold feasibility — If N < upper or |lower| > N, signals will never trigger; always cross-check N.

• Path dependence — The state variable persists until a new event; if you want frequent re-evaluation, lower thresholds or reduce N.

• Regime changes — Calendar resets can produce early ambiguity; expect a few bars for the breadth to mature.

• VWAP sensitivity to volume spikes — Large prints can tilt VWAP abruptly; that behavior is intentional in VWAP-based logic.

Suggested starting profiles

• Intraday trend bias : Anchor=Day, N=25 (1→25), upper=18–20, lower=−8, paint candles ON.

• Swing bias : Anchor=Month, N=45 (1→45), upper=38–42, lower=−10, VWAP coloring ON, background OFF.

• Balanced reactivity : Anchor=Week, N=30 (1→30), upper=20–22, lower=−10…−12, symmetric if desired.

Implementation notes

• The indicator runs in a separate pane (oscillator), but VWAP itself is drawn on price using forced overlay so you can see interactions (touches, reclaim/loss).

• HLC3 is used for VWAP price; that’s a common choice to dampen wick noise while still reflecting intrabar range.

• For-loop cap is kept modest (≤50) for performance and clarity.

How to use this responsibly

Treat the oscillator as a bias and persistence meter . Combine it with your entry framework (structure breaks, liquidity zones, higher-timeframe context) and risk controls. The design emphasizes clarity over complexity—its edge is in how strictly it demands agreement before declaring a regime, not in predicting specific turns.

Summary

VWAP For Loop distills the question “How broadly is the anchored, volume-weighted trend advancing or retreating?” into a single, thresholded score you can read at a glance, alert on, and color through your chart. With careful anchoring and thresholds sized to your window length, it becomes a pragmatic bias filter for both systematic and discretionary workflows.

Fibo Swing MFI by julzALGOOVERVIEW

Fibo Swing MFI by julzALGO blends MFI → RSI → Least-Squares smoothing to flag overbought/oversold swings and continuously plot Fibonacci retracements from the rolling high/low of the last 200 bars. It’s built to spot momentum shifts while giving you a clean, always-current fib map of the recent market range.

CORE PRINCIPLES

Hybrid Momentum Signal

- Uses MFI to integrate price and volume.

- Applies RSI to MFI for momentum clarity.

- Smooths the result with Least Squares regression to reduce noise.

Swing Identification

- Marks potential swing highs when momentum is overbought.

- Marks potential swing lows when momentum is oversold.

Fixed-Window Fibonacci Mapping

- Always calculates fib levels from the highest high and lowest low of the last 200 bars.

- This keeps fib zones consistent, independent of swing point detection.

Visual Clarity & Non-Repainting Logic

- Clean labels for OB/OS zones.

- Lines and levels update only as new bars confirm changes.

Adaptability

- Works on any market and timeframe.

- Adjustable momentum length, OB/OS thresholds, and smoothing.

HOW IT WORKS

- Computes Money Flow Index (MFI) from price & volume.

- Applies RSI to the MFI for clearer OB/OS momentum.

- Smooths the hybrid with a Least Squares (linear regression) filter.

- Swing labels appear when OB/OS conditions are met (green = swing low, red = swing high).

- Fibonacci retracements are always drawn from the highest high and lowest low of the last 200 bars (rolling window), independent of swing labels.

HOW TO USE

- Watch for OB/OS flips to mark potential swing highs/lows.

- Use the 200-bar fib grid as your active map of pullback levels and reaction zones.

- Combine fib reactions with your price action/volume cues for confirmation.

- Works across markets and timeframes.

SETTINGS

- Length – Period for both MFI and RSI.

- OB/OS Levels – Overbought/oversold thresholds (default 70/30).

- Smooth – Least-Squares smoothing length.

- Fibonacci Window – Fixed at 200 bars in this version (changeable in code via fibLen).

NOTES

- Logic is non-repainting aside from standard bar/label confirmation.

- Increase Length on very low timeframes to reduce noise.

- Swing labels help context; fibs are always based on the most recent 200-bar high/low range.

SUMMARY

Fibo Swing MFI by julzALGO is a momentum-plus-price action tool that merges MFI → RSI → smoothing to identify overbought/oversold swings and automatically plot Fibonacci retracements based on the rolling high/low of the last 200 bars. It’s designed to help traders quickly see potential reversal points and pullback zones, offering visual confluence between momentum shifts and fixed-window price structure.

DISCLAIMER

For educational purposes only. Not financial advice. Trade responsibly with proper risk management.

Prev D/W/M + Asia & London Levels [Oeditrades]Prev D/W/M + Asia & London Levels

Author: Oeditrades

Platform: Pine Script® v6

What it does

Plots only the most recent, fully completed:

Previous Day / Week / Month highs & lows

Asia and London session highs & lows

Levels are drawn as true horizontal lines from the period/session start and extended to the right for easy confluence reading. The script is non-repainting.

How it works

Prev Day/Week/Month: Uses completed HTF candles (high / low ) so values are fixed for the entire next period.

Sessions (NY time): Asia (default 20:00–03:00) and London (default 03:00–08:00) are tracked in America/New_York time. High/low are locked when the session ends, and the line is anchored at that session’s start.

Inputs & customization

Visibility: toggle Previous Day/Week/Month, Asia, London, and labels.

Colors: highs default red; lows default green (user-configurable). Session highs default pink, lows aqua (also editable).

Style: line style (solid/dotted/dashed) and width.

Sessions: editable time windows for Asia and London (still interpreted in New York time).

Disclaimer: optional on-chart disclaimer panel with editable text.

Notes

Works on any timeframe. For intraday charts, the HTF values remain constant until the next HTF bar completes.

If your market’s overnight hours differ, simply adjust the session windows in Inputs.

Lines intentionally show only the latest completed period/session to keep charts clean.

Use cases

Quick view of PDH/PDL, PWH/PWL, PMH/PML for bias and liquidity.

Intraday planning around Asia/London range breaks, retests, and overlaps with prior levels.

Disclaimer

This tool is for educational purposes only and is not financial advice. Markets involve risk; past performance does not guarantee future results.

London & NY Session Markers + Pip MovementThis indicator visually marks the London and New York trading sessions on your chart and optionally calculates the pip range (high-low movement) during each session. It's specifically designed for Forex traders, helping you identify volatility windows and analyze market movement within major session times.

🔍 Key Features:

✅ Session Open/Close Markers

Draws vertical dotted lines at:

London Open (08:00 UK time)

London Close (11:00 UK time)

New York Open (14:00 UK time)

New York Close (17:00 UK time)

Each marker is labeled clearly ("London Open", "NY Close", etc.)

Uses color-coding for easy identification:

Aqua for London

Lime for New York

✅ Pip Range Display (Optional)

Measures the high-low price movement during each session.

Converts this movement into pips, using:

0.0001 pip size for most pairs

0.01 pip size for JPY pairs (auto-detected)

Displays a label (e.g., "London: 42.5 pips") above the candle at session close.

This feature can be toggled on/off via the settings panel.

✅ Time-Zone Aware

Session times are aligned to Europe/London time zone.

Adjusts automatically for Daylight Saving Time (DST).

✅ User Controls

Toggle visibility for:

London session markers

New York session markers

Pip range labels

📊 Use Cases:

Identify when liquidity and volatility increase, especially during session overlaps.

Analyze historical session-based volatility (e.g., compare NY vs. London pip ranges).

Combine with price action or indicator signals that work best in high-volume hours.

Optimize entry and exit timing based on session structure.

⚙️ Best Timeframes:

5-min to 1-hour charts for precise session tracking.

Works on Forex and CFD pairs with standard tick sizes.

⚠️ Notes:

This tool does not repaint and uses only completed bar data.

Pip calculation is based on the chart’s current symbol and tick size.

Designed for spot FX, not intended for cryptocurrencies or synthetic indices.

✅ Ideal For:

Forex Day Traders

Session-based Strategy Developers

London Breakout or NY Reversal Traders

Anyone analyzing volatility by session windows

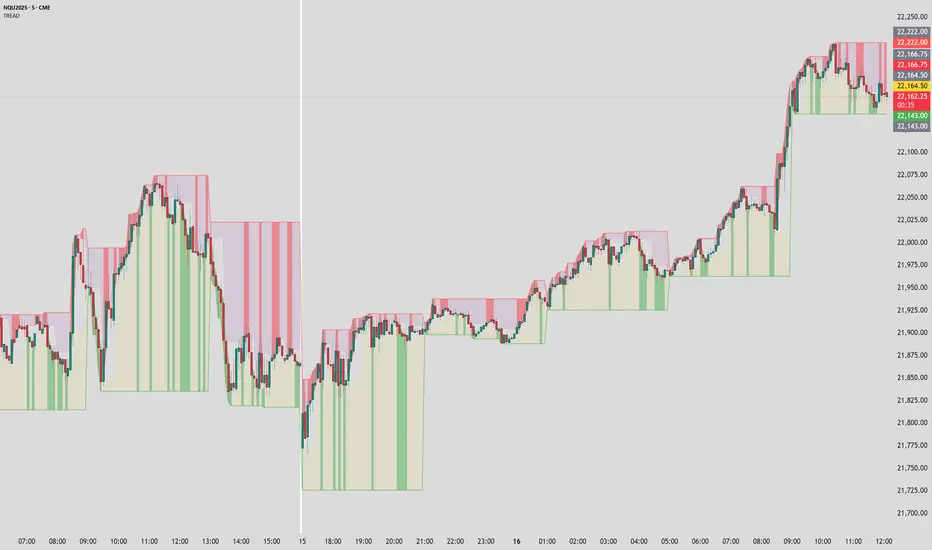

Timeframe Resistance Evaluation And Detection - CoffeeKillerTREAD - Timeframe Resistance Evaluation And Detection Guide

🔔 Important Technical Limitation 🔔

**This indicator does NOT fetch true higher timeframe data.** Instead, it simulates higher timeframe levels by aggregating data from your current chart timeframe. This means:

- Results will vary depending on what chart timeframe you're viewing

- Levels may not match actual higher timeframe candle highs/lows

- You might miss important wicks or gaps that occurred between chart timeframe bars

- **Always verify levels against actual higher timeframe charts before trading**

Welcome traders! This guide will walk you through the TREAD (Timeframe Resistance Evaluation And Detection) indicator, a multi-timeframe analysis tool developed by CoffeeKiller that identifies support and resistance confluence across different time periods.(I am 50+ year old trader and always thought I was bad a teaching and explaining so you get a AI guide. I personally use this on the 5 minute chart with the default settings, but to each there own and if you can improve the trend detection methods please DM me. I would like to see the code. Thanks)

Core Components

1. Dual Timeframe Level Tracking

- Short Timeframe Levels: Tracks opening price extremes within shorter periods

- Long Timeframe Levels: Tracks actual high/low extremes within longer periods

- Dynamic Reset Mechanism: Levels reset at the start of each new timeframe period

- Momentum Detection: Identifies when levels change mid-period, indicating active price movement

2. Visual Zone System

- High Zones: Areas between long timeframe highs and short timeframe highs

- Low Zones: Areas between long timeframe lows and short timeframe lows

- Fill Coloring: Dynamic colors based on whether levels are static or actively changing

- Momentum Highlighting: Special colors when levels break during active periods

3. Customizable Display Options

- Multiple Plot Styles: Line, circles, or cross markers

- Flexible Timeframe Selection: Wide range of short and long timeframe combinations

- Color Customization: Separate colors for each level type and momentum state

- Toggle Controls: Show/hide different elements based on trading preference

Main Features

Timeframe Settings

- Short Timeframe Options: 15m, 30m, 1h, 2h, 4h

- Long Timeframe Options: 1h, 2h, 4h, 8h, 12h, 1D, 1W

- Recommended Combinations:

- Scalping: 15m/1h or 30m/2h

- Day Trading: 30m/4h or 1h/4h

- Swing Trading: 4h/1D or 1D/1W

Display Configuration

- Level Visibility: Toggle short/long timeframe levels independently

- Fill Zone Control: Enable/disable colored zones between levels

- Momentum Fills: Special highlighting for actively changing levels

- Line Customization: Width, style, and color options for all elements

Color System

- Short TF High: Default red for resistance levels

- Short TF Low: Default green for support levels

- Long TF High: Transparent red for broader resistance context

- Long TF Low: Transparent green for broader support context

- Momentum Colors: Brighter colors when levels are actively changing

Technical Implementation Details

How Level Tracking Works

The indicator uses a custom tracking function that:

1. Detects Timeframe Periods: Uses `time()` function to identify when new periods begin

2. Tracks Extremes: Monitors highest/lowest values within each period

3. Resets on New Periods: Clears tracking when timeframe periods change

4. Updates Mid-Period: Continues tracking if new extremes are reached

The Timeframe Limitation Explained

`pinescript

// What the indicator does:

short_tf_start = ta.change(time(short_timeframe)) != 0 // Detects 30m period start

= track_highest(open, short_tf_start) // BUT uses chart TF opens!

// What true multi-timeframe would be:

// short_tf_high = request.security(syminfo.tickerid, short_timeframe, high)

`

This means:

- On a 5m chart with 30m/4h settings: Tracks 5m bar opens during 30m and 4h windows

- On a 1m chart with same settings: Tracks 1m bar opens during 30m and 4h windows

- Results will be different between chart timeframes

- May miss important price action that occurred between your chart's bars

Visual Elements

1. Level Lines

- Short TF High: Upper resistance line from shorter timeframe analysis

- Short TF Low: Lower support line from shorter timeframe analysis

- Long TF High: Broader resistance context from longer timeframe

- Long TF Low: Broader support context from longer timeframe

2. Zone Fills

- High Zone: Area between long TF high and short TF high (potential resistance cluster)

- Low Zone: Area between long TF low and short TF low (potential support cluster)

- Regular Fill: Standard transparency when levels are static

- Momentum Fill: Enhanced visibility when levels are actively changing

3. Dynamic Coloring

- Static Periods: Normal colors when levels haven't changed recently

- Active Periods: Momentum colors when levels are being tested/broken

- Confluence Zones: Different intensities based on timeframe alignment

Trading Applications

1. Support/Resistance Trading

- Entry Points: Trade bounces from zone boundaries

- Confluence Areas: Focus on areas where short and long TF levels cluster

- Zone Breaks: Enter on confirmed breaks through entire zones

- Multiple Timeframe Confirmation: Stronger signals when both timeframes align

2. Range Trading

- Zone Boundaries: Use fill zones as range extremes

- Mean Reversion: Trade back toward opposite zone when price reaches extremes

- Breakout Preparation: Watch for momentum color changes indicating potential breakouts

- Risk Management: Place stops outside the opposite zone

3. Trend Following

- Direction Bias: Trade in direction of zone breaks

- Pullback Entries: Enter on pullbacks to broken zones (now support/resistance)

- Momentum Confirmation: Use momentum coloring to confirm trend strength

- Multiple Timeframe Alignment: Strongest trends when both timeframes agree

4. Scalping Applications

- Quick Bounces: Trade rapid moves between zone boundaries

- Momentum Signals: Enter when momentum colors appear

- Short-Term Targets: Use opposite zone as profit target

- Tight Stops: Place stops just outside current zone

Optimization Guide

1. Timeframe Selection

For Different Trading Styles:

- Scalping: 15m/1h - Quick levels, frequent updates

- Day Trading: 30m/4h - Balanced view, good for intraday moves

- Swing Trading: 4h/1D - Longer-term perspective, fewer false signals

- Position Trading: 1D/1W - Major structural levels

2. Chart Timeframe Considerations

**Important**: Your chart timeframe affects results

- Lower Chart TF: More granular level tracking, but may be noisy

- Higher Chart TF: Smoother levels, but may miss important price action

- Recommended: Use chart timeframe 2-4x smaller than short indicator timeframe

3. Display Settings

- Busy Charts: Disable fills, show only key levels

- Clean Analysis: Enable all fills and momentum coloring

- Multi-Monitor Setup: Use different color schemes for easy identification

- Mobile Trading: Increase line width for visibility

Best Practices

1. Level Verification

- Always Cross-Check: Verify levels against actual higher timeframe charts

- Multiple Timeframes: Check 2-3 different chart timeframes for consistency

- Price Action Confirmation: Wait for candlestick confirmation at levels

- Volume Analysis: Combine with volume for stronger confirmation

2. Risk Management

- Stop Placement: Use zones rather than exact prices for stops

- Position Sizing: Reduce size when zones are narrow (higher risk)

- Multiple Targets: Scale out at different zone boundaries

- False Break Protection: Allow for minor zone penetrations

3. Signal Quality Assessment

- Momentum Colors: Higher probability when momentum coloring appears

- Zone Width: Wider zones often provide stronger support/resistance

- Historical Testing: Backtest on your preferred timeframe combinations

- Market Conditions: Adjust sensitivity based on volatility

Advanced Features

1. Momentum Detection System

The indicator tracks when levels change mid-period:

`pinescript

short_high_changed = short_high != short_high and not short_tf_start

`

This identifies:

- Active level testing

- Potential breakout situations

- Increased market volatility

- Trend acceleration points

2. Dynamic Color System

Complex conditional logic determines fill colors:

- Static Zones: Regular transparency for stable levels

- Active Zones: Enhanced colors for changing levels

- Mixed States: Different combinations based on user preferences

- Custom Overrides: User can prioritize certain color schemes

3. Zone Interaction Analysis

- Convergence: When short and long TF levels approach each other

- Divergence: When timeframes show conflicting levels

- Alignment: When both timeframes agree on direction

- Transition: When one timeframe changes while other remains static

Common Issues and Solutions

1. Inconsistent Levels

Problem: Levels look different on various chart timeframes

Solution: Always verify against actual higher timeframe charts

2. Missing Price Action

Problem: Important wicks or gaps not reflected in levels

Solution: Use chart timeframe closer to indicator's short timeframe setting

3. Too Many Signals

Problem: Excessive level changes and momentum alerts

Solution: Increase timeframe settings or reduce chart timeframe granularity

4. Lagging Signals

Problem: Levels seem to update too slowly

Solution: Decrease chart timeframe or use more sensitive timeframe combinations

Recommended Setups

Conservative Approach

- Timeframes: 4h/1D

- Chart: 1h

- Display: Show fills only, no momentum coloring

- Use: Swing trading, position management

Aggressive Approach

- Timeframes: 15m/1h

- Chart: 5m

- Display: All features enabled, momentum highlighting

- Use: Scalping, quick reversal trades

Balanced Approach

- Timeframes: 30m/4h

- Chart: 15m

- Display: Selective fills, momentum on key levels

- Use: Day trading, multi-session analysis

Final Notes

**Remember**: This indicator provides a synthetic view of multi-timeframe levels, not true higher timeframe data. While useful for identifying potential confluence areas, always verify important levels by checking actual higher timeframe charts.

**Best Results When**:

- Combined with actual multi-timeframe analysis

- Used for confluence confirmation rather than primary signals

- Applied with proper risk management

- Verified against price action and volume

**DISCLAIMER**: This indicator and its signals are intended solely for educational and informational purposes. The timeframe limitation means results may not reflect true higher timeframe levels. Always conduct your own analysis and verify levels independently before making trading decisions. Trading involves significant risk of loss.

Killzones [Plug&Play]Highlight the most important institutional trading hours with precision.

The Setup Agent Killzones indicator automatically plots vertical lines to mark the key “Killzone” windows each day — London (08:00–09:00) and New York (15:00–16:00), shown in UK time. These timeframes represent periods of high volatility, where smart money activity is most likely to create the day’s major moves.

How it works:

Instantly visualise the London and New York Killzones with subtle vertical lines.

Customise which sessions to show to fit your trading style.

Stay focused on the windows where market makers are most active.

Perfect for intraday traders and anyone using session-based strategies.

Combine with our session indicator for a complete Plug&Play edge.

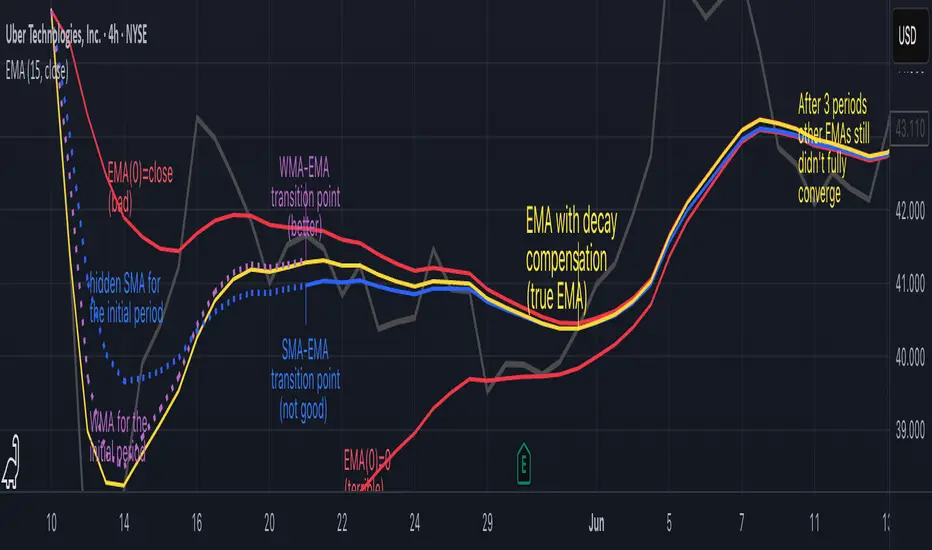

Why EMA Isn't What You Think It IsMany new traders adopt the Exponential Moving Average (EMA) believing it's simply a "better Simple Moving Average (SMA)". This common misconception leads to fundamental misunderstandings about how EMA works and when to use it.

EMA and SMA differ at their core. SMA use a window of finite number of data points, giving equal weight to each data point in the calculation period. This makes SMA a Finite Impulse Response (FIR) filter in signal processing terms. Remember that FIR means that "all that we need is the 'period' number of data points" to calculate the filter value. Anything beyond the given period is not relevant to FIR filters – much like how a security camera with 14-day storage automatically overwrites older footage, making last month's activity completely invisible regardless of how important it might have been.

EMA, however, is an Infinite Impulse Response (IIR) filter. It uses ALL historical data, with each past price having a diminishing - but never zero - influence on the calculated value. This creates an EMA response that extends infinitely into the past—not just for the last N periods. IIR filters cannot be precise if we give them only a 'period' number of data to work on - they will be off-target significantly due to lack of context, like trying to understand Game of Thrones by watching only the final season and wondering why everyone's so upset about that dragon lady going full pyromaniac.

If we only consider a number of data points equal to the EMA's period, we are capturing no more than 86.5% of the total weight of the EMA calculation. Relying on he period window alone (the warm-up period) will provide only 1 - (1 / e^2) weights, which is approximately 1−0.1353 = 0.8647 = 86.5%. That's like claiming you've read a book when you've skipped the first few chapters – technically, you got most of it, but you probably miss some crucial early context.

▶️ What is period in EMA used for?

What does a period parameter really mean for EMA? When we select a 15-period EMA, we're not selecting a window of 15 data points as with an SMA. Instead, we are using that number to calculate a decay factor (α) that determines how quickly older data loses influence in EMA result. Every trader knows EMA calculation: α = 1 / (1+period) – or at least every trader claims to know this while secretly checking the formula when they need it.

Thinking in terms of "period" seriously restricts EMA. The α parameter can be - should be! - any value between 0.0 and 1.0, offering infinite tuning possibilities of the indicator. When we limit ourselves to whole-number periods that we use in FIR indicators, we can only access a small subset of possible IIR calculations – it's like having access to the entire RGB color spectrum with 16.7 million possible colors but stubbornly sticking to the 8 basic crayons in a child's first art set because the coloring book only mentioned those by name.

For example:

Period 10 → alpha = 0.1818

Period 11 → alpha = 0.1667

What about wanting an alpha of 0.17, which might yield superior returns in your strategy that uses EMA? No whole-number period can provide this! Direct α parameterization offers more precision, much like how an analog tuner lets you find the perfect radio frequency while digital presets force you to choose only from predetermined stations, potentially missing the clearest signal sitting right between channels.

Sidenote: the choice of α = 1 / (1+period) is just a convention from 1970s, probably started by J. Welles Wilder, who popularized the use of the 14-day EMA. It was designed to create an approximate equivalence between EMA and SMA over the same number of periods, even thought SMA needs a period window (as it is FIR filter) and EMA doesn't. In reality, the decay factor α in EMA should be allowed any valye between 0.0 and 1.0, not just some discrete values derived from an integer-based period! Algorithmic systems should find the best α decay for EMA directly, allowing the system to fine-tune at will and not through conversion of integer period to float α decay – though this might put a few traditionalist traders into early retirement. Well, to prevent that, most traditionalist implementations of EMA only use period and no alpha at all. Heaven forbid we disturb people who print their charts on paper, draw trendlines with rulers, and insist the market "feels different" since computers do algotrading!

▶️ Calculating EMAs Efficiently

The standard textbook formula for EMA is:

EMA = CurrentPrice × alpha + PreviousEMA × (1 - alpha)

But did you know that a more efficient version exists, once you apply a tiny bit of high school algebra:

EMA = alpha × (CurrentPrice - PreviousEMA) + PreviousEMA

The first one requires three operations: 2 multiplications + 1 addition. The second one also requires three ops: 1 multiplication + 1 addition + 1 subtraction.

That's pathetic, you say? Not worth implementing? In most computational models, multiplications cost much more than additions/subtractions – much like how ordering dessert costs more than asking for a water refill at restaurants.

Relative CPU cost of float operations :

Addition/Subtraction: ~1 cycle

Multiplication: ~5 cycles (depending on precision and architecture)

Now you see the difference? 2 * 5 + 1 = 11 against 5 + 1 + 1 = 7. That is ≈ 36.36% efficiency gain just by swapping formulas around! And making your high school math teacher proud enough to finally put your test on the refrigerator.

▶️ The Warmup Problem: how to start the EMA sequence right

How do we calculate the first EMA value when there's no previous EMA available? Let's see some possible options used throughout the history:

Start with zero : EMA(0) = 0. This creates stupidly large distortion until enough bars pass for the horrible effect to diminish – like starting a trading account with zero balance but backdating a year of missed trades, then watching your balance struggle to climb out of a phantom debt for months.

Start with first price : EMA(0) = first price. This is better than starting with zero, but still causes initial distortion that will be extra-bad if the first price is an outlier – like forming your entire opinion of a stock based solely on its IPO day price, then wondering why your model is tanking for weeks afterward.

Use SMA for warmup : This is the tradition from the pencil-and-paper era of technical analysis – when calculators were luxury items and "algorithmic trading" meant your broker had neat handwriting. We first calculate an SMA over the initial period, then kickstart the EMA with this average value. It's widely used due to tradition, not merit, creating a mathematical Frankenstein that uses an FIR filter (SMA) during the initial period before abruptly switching to an IIR filter (EMA). This methodology is so aesthetically offensive (abrupt kink on the transition from SMA to EMA) that charting platforms hide these early values entirely, pretending EMA simply doesn't exist until the warmup period passes – the technical analysis equivalent of sweeping dust under the rug.

Use WMA for warmup : This one was never popular because it is harder to calculate with a pencil - compared to using simple SMA for warmup. Weighted Moving Average provides a much better approximation of a starting value as its linear descending profile is much closer to the EMA's decay profile.

These methods all share one problem: they produce inaccurate initial values that traders often hide or discard, much like how hedge funds conveniently report awesome performance "since strategy inception" only after their disastrous first quarter has been surgically removed from the track record.

▶️ A Better Way to start EMA: Decaying compensation

Think of it this way: An ideal EMA uses an infinite history of prices, but we only have data starting from a specific point. This creates a problem - our EMA starts with an incorrect assumption that all previous prices were all zero, all close, or all average – like trying to write someone's biography but only having information about their life since last Tuesday.

But there is a better way. It requires more than high school math comprehension and is more computationally intensive, but is mathematically correct and numerically stable. This approach involves compensating calculated EMA values for the "phantom data" that would have existed before our first price point.

Here's how phantom data compensation works:

We start our normal EMA calculation:

EMA_today = EMA_yesterday + α × (Price_today - EMA_yesterday)

But we add a correction factor that adjusts for the missing history:

Correction = 1 at the start

Correction = Correction × (1-α) after each calculation

We then apply this correction:

True_EMA = Raw_EMA / (1-Correction)

This correction factor starts at 1 (full compensation effect) and gets exponentially smaller with each new price bar. After enough data points, the correction becomes so small (i.e., below 0.0000000001) that we can stop applying it as it is no longer relevant.

Let's see how this works in practice:

For the first price bar:

Raw_EMA = 0

Correction = 1

True_EMA = Price (since 0 ÷ (1-1) is undefined, we use the first price)

For the second price bar:

Raw_EMA = α × (Price_2 - 0) + 0 = α × Price_2

Correction = 1 × (1-α) = (1-α)

True_EMA = α × Price_2 ÷ (1-(1-α)) = Price_2

For the third price bar:

Raw_EMA updates using the standard formula

Correction = (1-α) × (1-α) = (1-α)²

True_EMA = Raw_EMA ÷ (1-(1-α)²)

With each new price, the correction factor shrinks exponentially. After about -log₁₀(1e-10)/log₁₀(1-α) bars, the correction becomes negligible, and our EMA calculation matches what we would get if we had infinite historical data.

This approach provides accurate EMA values from the very first calculation. There's no need to use SMA for warmup or discard early values before output converges - EMA is mathematically correct from first value, ready to party without the awkward warmup phase.

Here is Pine Script 6 implementation of EMA that can take alpha parameter directly (or period if desired), returns valid values from the start, is resilient to dirty input values, uses decaying compensator instead of SMA, and uses the least amount of computational cycles possible.

// Enhanced EMA function with proper initialization and efficient calculation

ema(series float source, simple int period=0, simple float alpha=0)=>

// Input validation - one of alpha or period must be provided

if alpha<=0 and period<=0

runtime.error("Alpha or period must be provided")

// Calculate alpha from period if alpha not directly specified

float a = alpha > 0 ? alpha : 2.0 / math.max(period, 1)

// Initialize variables for EMA calculation

var float ema = na // Stores raw EMA value

var float result = na // Stores final corrected EMA

var float e = 1.0 // Decay compensation factor

var bool warmup = true // Flag for warmup phase

if not na(source)

if na(ema)

// First value case - initialize EMA to zero

// (we'll correct this immediately with the compensation)

ema := 0

result := source

else

// Standard EMA calculation (optimized formula)

ema := a * (source - ema) + ema

if warmup

// During warmup phase, apply decay compensation

e *= (1-a) // Update decay factor

float c = 1.0 / (1.0 - e) // Calculate correction multiplier

result := c * ema // Apply correction

// Stop warmup phase when correction becomes negligible

if e <= 1e-10

warmup := false

else

// After warmup, EMA operates without correction

result := ema

result // Return the properly compensated EMA value

▶️ CONCLUSION

EMA isn't just a "better SMA"—it is a fundamentally different tool, like how a submarine differs from a sailboat – both float, but the similarities end there. EMA responds to inputs differently, weighs historical data differently, and requires different initialization techniques.

By understanding these differences, traders can make more informed decisions about when and how to use EMA in trading strategies. And as EMA is embedded in so many other complex and compound indicators and strategies, if system uses tainted and inferior EMA calculatiomn, it is doing a disservice to all derivative indicators too – like building a skyscraper on a foundation of Jell-O.

The next time you add an EMA to your chart, remember: you're not just looking at a "faster moving average." You're using an INFINITE IMPULSE RESPONSE filter that carries the echo of all previous price actions, properly weighted to help make better trading decisions.

EMA done right might significantly improve the quality of all signals, strategies, and trades that rely on EMA somewhere deep in its algorithmic bowels – proving once again that math skills are indeed useful after high school, no matter what your guidance counselor told you.

TLC sessionA Professional Intraday Session Tracker with VWAP and Economic Event Integration

Description

This indicator provides visual tracking of major trading sessions (Asian, London, New York) combined with VWAP calculations and macroeconomic event zones. It's designed for intraday traders who need to monitor session overlaps, liquidity periods, and high-impact news events.

The basic script of trading sessions was taken as a basis and refined for greater convenience.

Key Features:

Customizable Session Tracking: Visualize up to 3 trading sessions with adjustable time zones (supports IANA & GMT formats)

Dynamic VWAP Integration: Built-in Volume-Weighted Average Price calculation

Macro Event Zones: Highlights key economic announcement windows (adjustable for summer/winter time)

Price Action Visualization: Displays open/close prices, session ranges, and average price levels

Automatic DST Adjustment: Uses IANA timezone database for daylight savings awareness

How It Works

1. Trading Session Detection

Three fully configurable sessions (e.g., Asia, London, New York)

Each session displays:

Colored background zone

Opening price (dashed line)

Closing price (dashed line)

Average price (dotted line)

Optional label with session name

2. VWAP Calculation

Standard Volume-Weighted Average Price plotted as circled line

Helps identify fair value within each session

3. Macro Event Zones

Special highlighted period for economic news releases

Automatically adjusts for summer/winter time

Default set to 1000-1200 (summer) or 0900-1100 (winter) GMT-5 (US session open)

Why This Indicator is Unique

Multi-Session Awareness

Unlike simple session indicators, this tool:

Tracks price development within each session

Shows session overlaps (critical for volatility periods)

Maintains separate VWAP calculations across sessions

Professional-Grade Features

IANA timezone support (automatic DST handling)

Customizable visual elements (toggle labels, ranges, averages)

Object-based architecture (clean, efficient rendering)

News event integration (helps avoid trading during high-impact releases)

Usage Recommendations

Best Timeframes

1-minute to 1-hour charts (intraday focus)

Not recommended for daily+ timeframes

Trading Applications

1. Session Breakout Strategy: Trade breakouts when London/New York sessions open

2. VWAP Reversion: Fade moves that deviate too far from VWAP

3. News Avoidance: Reduce position sizing during macro event windows

Visual Example

Asian session (red)

London session (blue)

New York session (purple)

Macro event zone (white)

VWAP line (gold circles)

The basic script of trading sessions was taken as a basis and refined for greater convenience.

Dskyz (DAFE) MAtrix with ATR-Powered Precision Dskyz (DAFE) MAtrix with ATR-Powered Precision

This cutting‐edge futures trading strategy built to thrive in rapidly changing market conditions. Developed for high-frequency futures trading on instruments such as the CME Mini MNQ, this strategy leverages a matrix of sophisticated moving averages combined with ATR-based filters to pinpoint high-probability entries and exits. Its unique combination of adaptable technical indicators and multi-timeframe trend filtering sets it apart from standard strategies, providing enhanced precision and dynamic responsiveness.

imgur.com

Core Functional Components

1. Advanced Moving Averages

A distinguishing feature of the DAFE strategy is its robust, multi-choice moving averages (MAs). Clients can choose from a wide array of MAs—each with specific strengths—in order to fine-tune their trading signals. The code includes user-defined functions for the following MAs:

imgur.com

Hull Moving Average (HMA):

The hma(src, len) function calculates the HMA by using weighted moving averages (WMAs) to reduce lag considerably while smoothing price data. This function computes an intermediate WMA of half the specified length, then a full-length WMA, and finally applies a further WMA over the square root of the length. This design allows for rapid adaptation to price changes without the typical delays of traditional moving averages.

Triple Exponential Moving Average (TEMA):

Implemented via tema(src, len), TEMA uses three consecutive exponential moving averages (EMAs) to effectively cancel out lag and capture price momentum. The final formula—3 * (ema1 - ema2) + ema3—produces a highly responsive indicator that filters out short-term noise.

Double Exponential Moving Average (DEMA):

Through the dema(src, len) function, DEMA calculates an EMA and then a second EMA on top of it. Its simplified formula of 2 * ema1 - ema2 provides a smoother curve than a single EMA while maintaining enhanced responsiveness.

Volume Weighted Moving Average (VWMA):

With vwma(src, len), this MA accounts for trading volume by weighting the price, thereby offering a more contextual picture of market activity. This is crucial when volume spikes indicate significant moves.

Zero Lag EMA (ZLEMA):

The zlema(src, len) function applies a correction to reduce the inherent lag found in EMAs. By subtracting a calculated lag (based on half the moving average window), ZLEMA is exceptionally attuned to recent price movements.

Arnaud Legoux Moving Average (ALMA):

The alma(src, len, offset, sigma) function introduces ALMA—a type of moving average designed to be less affected by outliers. With parameters for offset and sigma, it allows customization of the degree to which the MA reacts to market noise.

Kaufman Adaptive Moving Average (KAMA):

The custom kama(src, len) function is noteworthy for its adaptive nature. It computes an efficiency ratio by comparing price change against volatility, then dynamically adjusts its smoothing constant. This results in an MA that quickly responds during trending periods while remaining smoothed during consolidation.

Each of these functions—integrated into the strategy—is selectable by the trader (via the fastMAType and slowMAType inputs). This flexibility permits the tailored application of the MA most suited to current market dynamics and individual risk management preferences.

2. ATR-Based Filters and Risk Controls

ATR Calculation and Volatility Filter:

The strategy computes the Average True Range (ATR) over a user-defined period (atrPeriod). ATR is then used to derive both:

Volatility Assessment: Expressed as a ratio of ATR to closing price, ensuring that trades are taken only when volatility remains within a safe, predefined threshold (volatilityThreshold).

ATR-Based Entry Filters: Implemented as atrFilterLong and atrFilterShort, these conditions ensure that for long entries the price is sufficiently above the slow MA and vice versa for shorts. This acts as an additional confirmation filter.

Dynamic Exit Management:

The exit logic employs a dual approach:

Fixed Stop and Profit Target: Stops and targets are set at multiples of ATR (fixedStopMultiplier and profitTargetATRMult), helping manage risk in volatile markets.

Trailing Stop Adjustments: A trailing stop is calculated using the ATR multiplied by a user-defined offset (trailOffset), which captures additional profits as the trade moves favorably while protecting against reversals.

3. Multi-Timeframe Trend Filtering

The strategy enhances its signal reliability by leveraging a secondary, higher timeframe analysis:

15-Minute Trend Analysis:

By retrieving 15-minute moving averages (fastMA15m and slowMA15m) via request.security, the strategy determines the broader market trend. This secondary filter (enabled or disabled through useTrendFilter) ensures that entries are aligned with the prevailing market direction, thereby reducing the incidence of false signals.

4. Signal and Execution Logic

Combined MA Alignment:

The entry conditions are based primarily on the alignment of the fast and slow MAs. A long condition is triggered when the current price is above both MAs and the fast MA is above the slow MA—complemented by the ATR filter and volume conditions. The reverse applies for a short condition.

Volume and Time Window Validation:

Trades are permitted only if the current volume exceeds a minimum (minVolume) and the current hour falls within the predefined trading window (tradingStartHour to tradingEndHour). An additional volume spike check (comparing current volume to a moving average of past volumes) further filters for optimal market conditions.

Comprehensive Order Execution:

The strategy utilizes flexible order execution functions that allow pyramiding (up to 10 positions), ensuring that it can scale into positions as favorable conditions persist. The use of both market entries and automated exits (with profit targets, stop-losses, and trailing stops) ensures that risk is managed at every step.

5. Integrated Dashboard and Metrics

For transparency and real-time analysis, the strategy includes:

On-Chart Visualizations:

Both fast and slow MAs are plotted on the chart, making it easy to see the market’s technical foundation.

Dynamic Metrics Dashboard:

A built-in table displays crucial performance statistics—including current profit/loss, equity, ATR (both raw and as a percentage), and the percentage gap between the moving averages. These metrics offer immediate insight into the health and performance of the strategy.

Input Parameters: Detailed Breakdown

Every input is meticulously designed to offer granular control:

Fast & Slow Lengths:

Determine the window size for the fast and slow moving averages. Smaller values yield more sensitivity, while larger values provide a smoother, delayed response.

Fast/Slow MA Types:

Choose the type of moving average for fast and slow signals. The versatility—from basic SMA and EMA to more complex ones like HMA, TEMA, ZLEMA, ALMA, and KAMA—allows customization to fit different market scenarios.

ATR Parameters:

atrPeriod and atrMultiplier shape the volatility assessment, directly affecting entry filters and risk management through stop-loss and profit target levels.

Trend and Volume Filters:

Inputs such as useTrendFilter, minVolume, and the volume spike condition help confirm that a trade occurs in active, trending markets rather than during periods of low liquidity or market noise.

Trading Hours:

Restricting trade execution to specific hours (tradingStartHour and tradingEndHour) helps avoid illiquid or choppy markets outside of prime trading sessions.

Exit Strategies:

Parameters like trailOffset, profitTargetATRMult, and fixedStopMultiplier provide multiple layers of risk management and profit protection by tailoring how exits are generated relative to current market conditions.

Pyramiding and Fixed Trade Quantity:

The strategy supports multiple entries within a trend (up to 10 positions) and sets a predefined trade quantity (fixedQuantity) to maintain consistent exposure and risk per trade.

Dashboard Controls:

The resetDashboard input allows for on-the-fly resetting of performance metrics, keeping the strategy’s performance dashboard accurate and up-to-date.

Why This Strategy is Truly Exceptional

Multi-Faceted Adaptability:

The ability to switch seamlessly between various moving average types—each suited to particular market conditions—enables the strategy to adapt dynamically. This is a testament to the high level of coding sophistication and market insight infused within the system.

Robust Risk Management:

The integration of ATR-based stops, profit targets, and trailing stops ensures that every trade is executed with well-defined risk parameters. The system is designed to mitigate unexpected market swings while optimizing profit capture.

Comprehensive Market Filtering:

By combining moving average crossovers with volume analysis, volatility thresholds, and multi-timeframe trend filters, the strategy only enters trades under the most favorable conditions. This multi-layered filtering reduces noise and enhances signal quality.

-Final Thoughts-

The Dskyz Adaptive Futures Elite (DAFE) MAtrix with ATR-Powered Precision strategy is not just another trading algorithm—it is a multi-dimensional, fully customizable system built on advanced technical principles and sophisticated risk management techniques. Every function and input parameter has been carefully engineered to provide traders with a system that is both powerful and transparent.

For clients seeking a state-of-the-art trading solution that adapts dynamically to market conditions while maintaining strict discipline in risk management, this strategy truly stands in a class of its own.

****Please show support if you enjoyed this strategy. I'll have more coming out in the near future!!

-Dskyz

Caution

DAFE is experimental, not a profit guarantee. Futures trading risks significant losses due to leverage. Backtest, simulate, and monitor actively before live use. All trading decisions are your responsibility.

RSI3M3+ v.1.8RSI3M3+ v.1.8 Indicator

This script is an advanced trading indicator based on Walter J. Bressert's cycle analysis methodology, combined with an RSI (Relative Strength Index) variation. Let me break it down and explain how it works.

Core Concepts

The RSI3M3+ indicator combines:

A short-term RSI (3-period)

A 3-period moving average to smooth the RSI

Bressert's cycle analysis principles to identify optimal trading points