Black-76 Options on Futures [Loxx]Black-76 Options on Futures is an adaptation of the Black-Scholes-Merton Option Pricing Model including Analytical Greeks and implied volatility calculations. The following information is an excerpt from Espen Gaarder Haug's book "Option Pricing Formulas". This version is to price Options on Futures. The options sensitivities (Greeks) are the partial derivatives of the Black-Scholes-Merton ( BSM ) formula. Analytical Greeks for our purposes here are broken down into various categories:

Delta Greeks: Delta, DDeltaDvol, Elasticity

Gamma Greeks: Gamma, GammaP, DGammaDvol, Speed

Vega Greeks: Vega , DVegaDvol/Vomma, VegaP

Theta Greeks: Theta

Rate/Carry Greeks: Rho futures option

Probability Greeks: StrikeDelta, Risk Neutral Density

(See the code for more details)

Black-Scholes-Merton Option Pricing

The Black-Scholes-Merton model can be "generalized" by incorporating a cost-of-carry rate b. This model can be used to price European options on stocks, stocks paying a continuous dividend yield, options on futures , and currency options:

c = S * e^((b - r) * T) * N(d1) - X * e^(-r * T) * N(d2)

p = X * e^(-r * T) * N(-d2) - S * e^((b - r) * T) * N(-d1)

where

d1 = (log(S / X) + (b + v^2 / 2) * T) / (v * T^0.5)

d2 = d1 - v * T^0.5

b = r ... gives the Black and Scholes (1973) stock option model.

b = r — q ... gives the Merton (1973) stock option model with continuous dividend yield q.

b = 0 ... gives the Black (1976) futures option model. <== this is the one used for this indicator!

b = 0 and r = 0 ... gives the Asay (1982) margined futures option model.

b = r — rf ... gives the Garman and Kohlhagen (1983) currency option model.

Inputs

S = Stock price.

X = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

d = dividend yield

v = Volatility of the underlying asset price

cnd (x) = The cumulative normal distribution function

nd(x) = The standard normal density function

convertingToCCRate(r, cmp ) = Rate compounder

gImpliedVolatilityNR(string CallPutFlag, float S, float x, float T, float r, float b, float cm , float epsilon) = Implied volatility via Newton Raphson

gBlackScholesImpVolBisection(string CallPutFlag, float S, float x, float T, float r, float b, float cm ) = implied volatility via bisection

Implied Volatility: The Bisection Method

The Newton-Raphson method requires knowledge of the partial derivative of the option pricing formula with respect to volatility ( vega ) when searching for the implied volatility . For some options (exotic and American options in particular), vega is not known analytically. The bisection method is an even simpler method to estimate implied volatility when vega is unknown. The bisection method requires two initial volatility estimates (seed values):

1. A "low" estimate of the implied volatility , al, corresponding to an option value, CL

2. A "high" volatility estimate, aH, corresponding to an option value, CH

The option market price, Cm , lies between CL and cH . The bisection estimate is given as the linear interpolation between the two estimates:

v(i + 1) = v(L) + (c(m) - c(L)) * (v(H) - v(L)) / (c(H) - c(L))

Replace v(L) with v(i + 1) if c(v(i + 1)) < c(m), or else replace v(H) with v(i + 1) if c(v(i + 1)) > c(m) until |c(m) - c(v(i + 1))| <= E, at which point v(i + 1) is the implied volatility and E is the desired degree of accuracy.

Implied Volatility: Newton-Raphson Method

The Newton-Raphson method is an efficient way to find the implied volatility of an option contract. It is nothing more than a simple iteration technique for solving one-dimensional nonlinear equations (any introductory textbook in calculus will offer an intuitive explanation). The method seldom uses more than two to three iterations before it converges to the implied volatility . Let

v(i + 1) = v(i) + (c(v(i)) - c(m)) / (dc / dv (i))

until |c(m) - c(v(i + 1))| <= E at which point v(i + 1) is the implied volatility , E is the desired degree of accuracy, c(m) is the market price of the option, and dc/ dv (i) is the vega of the option evaluaated at v(i) (the sensitivity of the option value for a small change in volatility ).

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Cari dalam skrip untuk "市值76亿的股票"

Open Source Ichimoku Kinkō hyō Keizen 改善Open Source Ichimoku Kinkō hyō Keizen 改善

First of all, thank you for using my work, making changes and continuing to share it for free.

I chose as indicator name Ichimoku Kinkō hyō Keizen logically simply by

what the word Keizen reflects a Japanese method which means continuous improvement and quality.

The goal here is to correct already any offset faults that should not be present and to try

to bring the indicator of new things that can serve and advance

and provide additional support for the decision.

A continuation will surely be planned which will bring its batch of new elements which will come

naturally be grafted to this tool.

Possibility of adding or not adding new lines Jun (76), Kan (226), Junkan A, B (676).

- Junakan To be calculated on the average of Jun / Kan 151 periods.

- Junkan B calculate over the 676 periods.

- Possibility of adding or not adding a new kinkohoyo calculate on Jun (76) and Kan (226).

- Possibility of adding or not adding a new Kumo calculate over 676 periods.

- Possibility of coloring or not the kumos or the kinkohyos.

- Possibility of adding or not Chikō 9,26,52,76,226,676.

- Ability to display or not passive lines in the future, 5 shots ahead of the movement of lines, provided that the extremes are not broken.

Thank you:

Thanks to TomQSD to have tested all the different versions of this project and to have contributed his criticism that helped me a lot to develop the tool.

Thanks to Herveo for having agreed to share his code

on the passive lines.

Remarks:

Not all options are activated at the same time.

Please do not uncheck the boxes in style, only change the colors.

To enable or disable lines, go to input parameters.

//////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////

Open Source Ichimoku Kinkō hyō Keizen 改善

Tous d'abord, merci d'utiliser mon travail, d'apporter des modification et de continuer à le partager gratuitement.

J'ai choisi comme nom d’indicateur Ichimoku Kinkō hyō Keizen en toute logique tout simplement par

ce que le mot Keizen reflète une méthode Japonaise qui veut dire amélioration en continue et qualité.

Le but ici est de corriger déjà tout les défauts de décalage qui ne devraient pas être présents et d’essayer

d’apporter sans trop charger l’indicateur des choses nouvelles qui peuvent servir et faire progresser

et apporter une aide supplémentaire à la décision.

Une suite sera sûrement prévue qui apportera son lot d'éléments nouveaux qui viendront

naturellement se greffer à cet outil.

- Possibilité d’ajout ou non de nouvelles lignes Jun (76) , Kan (226) , Junkan A,B (676).

- Junakan A calculer sur la moyenne de Jun/Kan 151 périodes.

- Junkan B calculer sur les 676 périodes.

- Possibilité d’ajout ou non d’un nouveau kinkohoyo calculer sur le Jun (76) et le Kan (226).

- Possibilité d’ajout ou non d’un nouveau Kumo calculer sur 676 périodes.

- Possibilité de colorier ou non le ou les kumos et le ou les kinkohyos.

- Possibilité d’ajout ou non de Chikō 9,26,52,76,226,676.

- Possibilité d’afficher ou non de lignes passives dans le future, 5 coups d’avance sur les déplacement des lignes, a condition que les extrêmes ne soient pas rompu.

Remerciement :

Merci à TomQSD d'avoir tester toutes les différentes versions de ce projet et d’avoir apporter sa critique qui m'a beaucoup aidé à développer l’outil.

Merci à Herveo pour sont accord d’avoir bien voulu partager son code

sur les lignes passives.

Remarques:

Toutes les options ne sont pas toutes à activer en même temps.

Merci de ne pas décocher les cases dans style, modifiez seulement les couleurs.

Pour activer ou désactiver des lignes, allez dans paramètres en entrée.

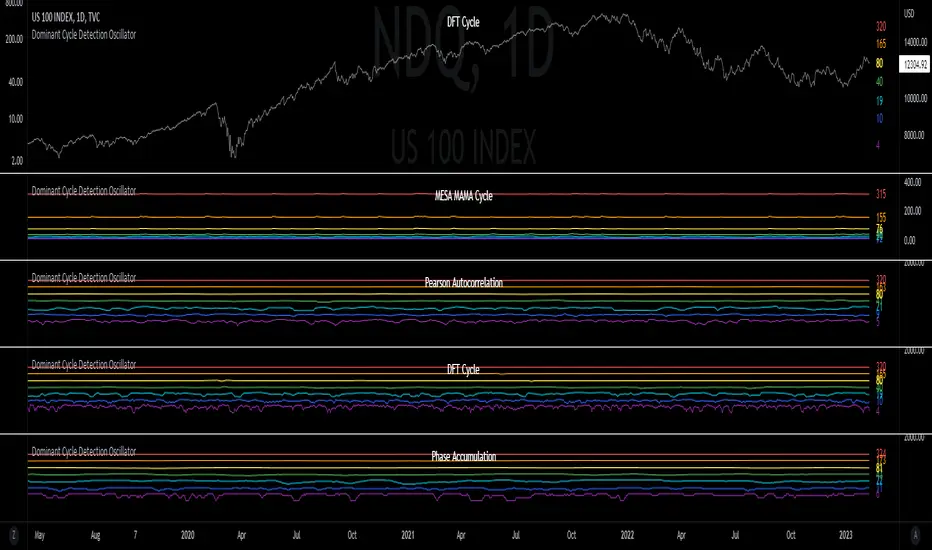

Dominant Cycle Detection OscillatorThis is a Dominant Cycle Detection Oscillator that searches multiple ranges of wavelengths within a spectrum. Choose one of 4 different dominant cycle detection methods (MESA MAMA cycle, Pearson Autocorrelation, Discreet Fourier Transform, and Phase Accumulation) to determine the most dominant cycles and see the historical results. Straight lines can indicate a steady dominant cycle; while Wavy lines might indicate a varying dominant cycle length. The steadier the cycle, the easier it may be to predict future events in that cycle (keep the log scale in mind when considering steadiness). The presence of evenly divisible (or harmonic) cycle lengths may also indicate stronger cycles; for example, 19, 38, and 76 dominant lengths for the 2x, 4x, and 8x cycles. Practically, a trader can use these cycle outputs as the default settings for other Hurst/cycle indicators. For example, if you see dominant cycle oscillator outputs of 38 & 76 for the 4x and 8x cycle respectively, you might want to test/use defaults of 38 & 76 for the 4x & 8x lengths in the bandpass, diamond/semi-circle notation, moving average & envelope, and FLD instead of the defaults 40 & 80 for a more fine-tuned analysis.

Muting the oscillator's historical lines and overlaying the indicator on the chart can visually cue a trader to the cycle lengths without taking up extra panes. The DFT Cycle lengths with muted historical lines have been overlayed on the chart in the photo.

The y-axis scale for this indicator's pane (just the oscillator pane, not the chart) most likely needs to be changed to logarithmic to look normal, but it depends on the search ranges in your settings. There are instructions in the settings. In the photo, the MESA MAMA scale is set to regular (not logarithmic) which demonstrates how difficult it can be to read if not changed.

In the Spectral Analysis chapter of Hurst's book Profit Magic, he recommended doing a Fourier analysis across a spectrum of frequencies. Hurst acknowledged there were many ways to do this analysis but recommended the method described by Lanczos. Currently in this indicator, the closest thing to the method described by Lanczos is the DFT Discreet Fourier Transform method.

Shoutout to @lastguru for the dominant cycle library referenced in this code. He mentioned that he may add more methods in the future.

Hurst Diamond Notation PivotsThis is a fairly simple indicator for diamond notation of past hi/lo pivot points, a common method in Hurst analysis. The diamonds mark the troughs/peaks of each cycle. They are offset by their lookback and thus will not 'paint' until after they happen so anticipate accordingly. Practically, traders can use the average length of past pivot periods to forecast future pivot periods in time🔮. For example, if the average/dominant number of bars in an 80-bar pivot point period/cycle is 76, then a trader might forecast that the next pivot could occur 76-ish bars after the last confirmed pivot. The numbers/labels on the y-axis display the cycle length used for pivot detection. This indicator doesn't repaint, but it has a lot of lag; Please use it for forecasting instead of entry signals. This indicator scans for new pivots in the form of a rainbow line and circle; once the hi/lo has happened and the lookback has passed then the pivot will be plotted. The rainbow color per wavelength theme seems to be authentic to Hurst (or modern Hurst software) and has been included as a default.

AB=CD Pattern Educational (Source Code)This indicator was intended as educational purpose only for AB=CD Patterns.

AB=CD Patterns were explained and modernized starting from The Harmonic Trader and Harmonic Trading: Volume One until Volume Three written by Scott M Carney.

Indikator ini bertujuan sebagai pendidikan sahaja untuk AB=CD Pattern.

AB=CD Patterns telah diterangkan dan dimodenkan bermula dari The Harmonic Trader dan Harmonic Trading: Volume One hingga Volume Three ditulis oleh Scott M Carney.

Indicator features :

1. List AB=CD patterns including ratio and reference page.

2. For desktop display only, not for mobile.

Kemampuan indikator :

1. Senarai AB=CD pattern termasuk ratio and rujukan muka surat.

2. Untuk paparan desktop sahaja, bukan untuk mobile.

FAQ

1. Credits / Kredit

Scott M Carney

Scott M Carney, Harmonic Trading: Volume One until Volume Three

2. Pattern and Chapter involved / Pattern dan Bab terlibat

Ideal AB=CD - The Harmonic Trader - Page 118 & 129

Standard AB=CD - The Harmonic Trader - Page 116, 117, 127 & 128, Harmonic Trading: Volume One - Page 42, 51, Harmonic Trading: Volume Three - Page 76 & 78

Alternate AB=CD - The Harmonic Trader - Page 142 & 145, Harmonic Trading: Volume One - Page 62, 63

Perfect AB=CD - Harmonic Trading: Volume One - Page 64 & 66

Reciprocal AB=CD - Harmonic Trading: Volume Two - Page 74 & 76

AB=CD with ab=cd - The Harmonic Trader - Page 149 & 153

AB=CD with BC Layering Technique - Harmonic Trading: Volume Three - Page 81 & 84

3. Code Usage / Penggunaan Kod

Free to use for personal usage but credits are most welcomed especially for credits to Scott M Carney.

Bebas untuk kegunaan peribadi tetapi kredit adalah amat dialu-alukan terutamanya kredit kepada Scott M Carney.

Bullish / Bearish Ideal AB=CD

Bullish / Bearish Standard AB=CD

Bullish / Bearish Alternate AB=CD

Bullish / Bearish Perfect AB=CD

Bullish / Bearish Reciprocal AB=CD (Additional value for reciprocal retracement 3.140 and 3.618)

Bullish / Bearish AB=CD with ab=cd

Bullish / Bearish AB=CD with BC Layering Technique

[fikira] Fibonacci MA / EMA's (Fibma / Fibema)I've made SMA/EMA's NOT based on the principle of the 2(1+1), 3(2+1),

5(3+2), 8(5+3), 13(8+5), 21(13+8), 34(21+13), 55(34+21), ... numbers,

but based on these following Fibonacci numbers:

0,236

0,382

0,500

0,618

0,764

1

Ending up with 2 series of Fibma / Fibema:

"Tiny Fibma / Fibema":

24, 38, 50, 62, 76, 100

"Big Fibma / Fibema":

236, 382, 500, 618, 764, 1000

IMHO it is striking how these lines often act as Resistance/Support,

although (except the 50, 100 & 500) they are not typical MA/EMA's.

They perform very well on every Timeframe as well!

Week:

3 Days:

1 Day:

4h:

1h:

Even on the 15 minutes:

Or 5':

Things to watch for:

Price compared to the Tiny or Big Fibma / Fibema (below or above)

Price compared to important Fibma / Fibema (for example below or

above MA 236, MA 764, MA 1000, ...)

Crossing of Fibma / Fibema 24/76, 236/764 and 38/62, 382/618

(bullish crossover = Lime coloured "cloud", bearish crossunder = Red coloured "cloud"),

...

I've made a change in barcolor if the close crosses the "Big Fibma / Fibema 500"

If price closes above MA/EMA 500, the first bar is yellow coloured,

if price stays above this level, candles are coloured lime/orange (= very bullish)

If price closes under MA/EMA 500, the first bar is purple,

if price stays under this level, candles are standard coloured (= very bearish)

Strategy will follow,

Thanks!

Covengers Ichimoku Cloud ver 0.2Ichimoku Cloud by SigmaJ in TEAM Coin Avenegers

ver 0.1 -> ver 0.2 Release !

Ver 0.2 updated.... like below...

+ Yumdung Momentum

Yumdung Momentum is based on Ichimoku Base Number Line

42 , 65 , 76, 129, 172 , 226

These Lines mean Resist / Support.

If There are many lines at one price, there could be STRONG Resist or Supprot Line.

-

코치모쿠 0.1 -> 0.2 버전 공개!

버전 0.2에는 다음과 같은 내용이 추가되었씁니다.

+ 윰멘텀 (윰둥이 모맨텀)

윰멘텀은 일목균형표에서 말하는 기본 수치에 대한 내용을 담고 있습니다.

기본 수치는 42, 65, 76, 129, 172, 226 입니다.

이 라인이 뭉쳐진 곳은 지지/저항의 역할을 할 가능성이 큽니다.

한 가격에 이 라인들이 뭉쳐있다면, 그곳은 강력한 지지 혹은 저항이 됩니다.

ST-Stochastic DashboardST-Stochastic Dashboard: User Manual & Functionality

1. Introduction

The ST-Stochastic Dashboard is a comprehensive tool designed for traders who utilize the Stochastic Oscillator. It combines two key features into a single indicator:

A standard, fully customizable Stochastic Oscillator plotted directly on your chart.

A powerful Multi-Timeframe (MTF) Dashboard that shows the status of the Stochastic %K value across three different timeframes of your choice.

This allows you to analyze momentum on your current timeframe while simultaneously monitoring for confluence or divergence on higher or lower timeframes, all without leaving your chart.

Disclaimer: In accordance with TradingView's House Rules, this document describes the technical functionality of the indicator. It is not financial advice. The indicator provides data based on user-defined parameters; all trading decisions are the sole responsibility of the user. Past performance is not indicative of future results.

2. How It Works (Functionality)

The indicator is divided into two main components:

A. The Main Stochastic Indicator (Chart Pane)

This is the visual representation of the Stochastic Oscillator for the chart's current timeframe.

%K Line (Blue): This is the main line of the oscillator. It shows the current closing price in relation to the high-low range over a user-defined period. A high value means the price is closing near the top of its recent range; a low value means it's closing near the bottom.

%D Line (Black): This is the signal line, which is a moving average of the %K line. It is used to smooth out the %K line and generate trading signals.

Overbought Zone (Red Area): By default, this zone is above the 75 level. When the Stochastic lines are in this area, it indicates that the asset may be "overbought," meaning the price is trading near the peak of its recent price range.

Oversold Zone (Blue Area): By default, this zone is below the 25 level. When the Stochastic lines are in this area, it indicates that the asset may be "oversold," meaning the price is trading near the bottom of its recent price range.

Crossover Signals:

Buy Signal (Blue Up Triangle): A blue triangle appears below the candles when the %K line crosses above the Oversold line (e.g., from 24 to 26). This suggests a potential shift from bearish to bullish momentum.

Sell Signal (Red Down Triangle): A red triangle appears above the candles when the %K line crosses below the Overbought line (e.g., from 76 to 74). This suggests a potential shift from bullish to bearish momentum.

B. The Multi-Timeframe Dashboard (Table on Chart)

This is the informational table that appears on your chart. Its purpose is to give you a quick, at-a-glance summary of the Stochastic's condition on other timeframes.

Function: The script uses TradingView's request.security() function to pull the %K value from three other timeframes that you specify in the settings.

Efficiency: The table is designed to update only on the last (most recent) bar (barstate.islast) to ensure the script runs efficiently and does not slow down your chart.

Columns:

Timeframe: Displays the timeframe you have selected (e.g., '5', '15', '60').

Stoch %K: Shows the current numerical value of the %K line for that specific timeframe, rounded to two decimal places.

Status: Interprets the %K value and displays a clear status:

OVERBOUGHT (Red Background): The %K value is above the "Upper Line" setting.

OVERSOLD (Blue Background): The %K value is below the "Lower Line" setting.

NEUTRAL (Black/Dark Background): The %K value is between the Overbought and Oversold levels.

3. Settings / Parameters in Detail

You can access these settings by clicking the "Settings" (cogwheel) icon on the indicator name.

Stochastic Settings

This group controls the behavior and appearance of the main Stochastic indicator plotted in the pane.

Stochastic Period (length)

Description: This is the lookback period used to calculate the Stochastic Oscillator. It defines the number of past bars to consider for the high-low range.

Default: 9

%K Smoothing (smoothK)

Description: This is the moving average period used to smooth the raw Stochastic value, creating the %K line. A higher value results in a smoother, less sensitive line.

Default: 3

%D Smoothing (smoothD)

Description: This is the moving average period applied to the %K line to create the %D (signal) line. A higher value creates a smoother signal line that lags further behind the %K line.

Default: 6

Lower Line (Oversold) (ul)

Description: This sets the threshold for the oversold condition. When the %K line is below this value, the dashboard will show "OVERSOLD". It is also the level the %K line must cross above to trigger a Buy Signal triangle.

Default: 25

Upper Line (Overbought) (ll)

Description: This sets the threshold for the overbought condition. When the %K line is above this value, the dashboard will show "OVERBOUGHT". It is also the level the %K line must cross below to trigger a Sell Signal triangle.

Default: 75

Dashboard Settings

This group controls the data and appearance of the multi-timeframe table.

Timeframe 1 (tf1)

Description: The first timeframe to be displayed in the dashboard.

Default: 5 (5 minutes)

Timeframe 2 (tf2)

Description: The second timeframe to be displayed in the dashboard.

Default: 15 (15 minutes)

Timeframe 3 (tf3)

Description: The third timeframe to be displayed in the dashboard.

Default: 60 (1 hour)

Dashboard Position (table_pos)

Description: Allows you to select where the dashboard table will appear on your chart.

Options: top_right, top_left, bottom_right, bottom_left

Default: bottom_right

4. How to Use & Interpret

Configuration: Adjust the Stochastic Settings to match your trading strategy. The default values (9, 3, 6) are common, but feel free to experiment. Set the Dashboard Settings to the timeframes that are most relevant to your analysis (e.g., your entry timeframe, a medium-term timeframe, and a long-term trend timeframe).

Analysis with the Dashboard: The primary strength of this tool is confluence. Look for situations where multiple timeframes align. For example:

If the dashboard shows OVERSOLD on the 15-minute, 60-minute, and your current 5-minute chart, a subsequent Buy Signal on your 5-minute chart may carry more weight.

Conversely, if your 5-minute chart shows OVERSOLD but the 60-minute chart is strongly OVERBOUGHT, it could indicate that you are looking at a minor pullback in a larger downtrend.

Interpreting States:

Overbought is not an automatic "sell" signal. It simply means momentum has been strong to the upside, and the price is near its recent peak. It could signal a potential reversal, but the price can also remain overbought for extended periods in a strong uptrend.

Oversold is not an automatic "buy" signal. It means momentum has been strong to the downside. While it can signal a potential bounce, prices can remain oversold for a long time in a strong downtrend.

Use the signals and dashboard states as a source of information to complement your overall trading strategy, which should include other forms of analysis such as price action, support/resistance levels, or other indicators.

Briese CoT Movement IndexThis Briese CoT (Commitments of Traders) Movement Index histogram indicator was built based on the formula by Stephen Briese in his book "The Commitments of Traders Bible":

"...difference between the COT Index and its reading of one or several weeks prior. I use six." —Chapter 7, page 75.

The code is a bit of a remix of the "ICT Commitment of Traders°" indicator by toodegrees and is meant for use in a new pane below a Weekly Chart .

The upper and lower thresholds are +40/-40. Some context: "A ± 40 point surge in the COT Index within a six-week period frequently marks the end of a counter-trend price reaction"

40 Point CoT Surge Rules (Commercials) from page 76

"During a correction from a prevailing uptrend, a +40 point movement in the CoT Index within a six-week period often marks the end of a corrective pullback, and the resumption of the major uptrend."

"During a reaction in a prevailing downtrend, a -40 point movement in the CoT Index within a six-week period frequently marks the end of a price reaction, and the resumption of the established downtrend."

"The failure of a ± point CoT Movement Index signal to restart the prevailing trend is a tip-off to a major trend change"

I'd recommend reading Briese's book for examples on how to properly interpret this indictor.

This indicator can be used in conjunction with another one I've published called the "Williams x Briese Hybrid CoT Index" which can be found on my scripts page.

Bullish Reversal Bar Strategy [Skyrexio]Overview

Bullish Reversal Bar Strategy leverages the combination of candlestick pattern Bullish Reversal Bar (description in Methodology and Justification of Methodology), Williams Alligator indicator and Williams Fractals to create the high probability setups. Candlestick pattern is used for the entering into trade, while the combination of Williams Alligator and Fractals is used for the trend approximation as close condition. Strategy uses only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator or the candlestick pattern invalidation to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Trend Trade Filter: strategy uses Alligator and Fractal combination as high probability trend filter.

Methodology

The strategy opens long trade when the following price met the conditions:

1.Current candle's high shall be below the Williams Alligator's lines (Jaw, Lips, Teeth)(all details in "Justification of Methodology" paragraph)

2.Price shall create the candlestick pattern "Bullish Reversal Bar". Optionally if MFI and AO filters are enabled current candle shall have the decreasing AO and at least one of three recent bars shall have the squat state on the MFI (all details in "Justification of Methodology" paragraph)

3.If price breaks through the high of the candle marked as the "Bullish Reversal Bar" the long trade is open at the price one tick above the candle's high

4.Initial stop loss is placed at the Bullish Reversal Bar's candle's low

5.If price hit the Bullish Reversal Bar's low before hitting the entry price potential trade is cancelled

6.If trade is active and initial stop loss has not been hit, trade is closed when the combination of Alligator and Williams Fractals shall consider current trend change from upward to downward.

Strategy settings

In the inputs window user can setup strategy setting:

Enable MFI (if true trades are filtered using Market Facilitation Index (MFI) condition all details in "Justification of Methodology" paragraph), by default = false)

Enable AO (if true trades are filtered using Awesome Oscillator (AO) condition all details in "Justification of Methodology" paragraph), by default = false)

Justification of Methodology

Let's explore the key concepts of this strategy and understand how they work together. The first and key concept is the Bullish Reversal Bar candlestick pattern. This is just the single bar pattern. The rules are simple:

Candle shall be closed in it's upper half

High of this candle shall be below all three Alligator's lines (Jaw, Lips, Teeth)

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

Fractals, another tool by Bill Williams, help identify potential reversal points on a price chart. A fractal forms over at least five consecutive bars, with the middle bar showing either:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often use fractals alongside other indicators to confirm trends or reversals, enhancing decision-making accuracy.

How do these tools work together in this strategy? Let’s consider an example of an uptrend.

When the price breaks above an up fractal, it signals a potential bullish trend. This occurs because the up fractal represents a shift in market behavior, where a temporary high was formed due to selling pressure. If the price revisits this level and breaks through, it suggests the market sentiment has turned bullish.

The breakout must occur above the Alligator’s teeth line to confirm the trend. A breakout below the teeth is considered invalid, and the downtrend might still persist. Conversely, in a downtrend, the same logic applies with down fractals.

How we can use all these indicators in this strategy? This strategy is a counter trend one. Candle's high shall be below all Alligator's lines. During this market stage the bullish reversal bar candlestick pattern shall be printed. This bar during the downtrend is a high probability setup for the potential reversal to the upside: bulls were able to close the price in the upper half of a candle. The breaking of its high is a high probability signal that trend change is confirmed and script opens long trade. If market continues going down and break down the bullish reversal bar's low potential trend change has been invalidated and strategy close long trade.

If market really reversed and started moving to the upside strategy waits for the trend change form the downtrend to the uptrend according to approximation of Alligator and Fractals combination. If this change happens strategy close the trade. This approach helps to stay in the long trade while the uptrend continuation is likely and close it if there is a high probability of the uptrend finish.

Optionally users can enable MFI and AO filters. First of all, let's briefly explain what are these two indicators. The Awesome Oscillator (AO), created by Bill Williams, is a momentum-based indicator that evaluates market momentum by comparing recent price activity to a broader historical context. It assists traders in identifying potential trend reversals and gauging trend strength.

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

This indicator is filtering signals in the following way: if current AO bar is decreasing this candle can be interpreted as a bullish reversal bar. This logic is applicable because initially this strategy is a trend reversal, it is searching for the high probability setup against the current trend. Decreasing AO is the additional high probability filter of a downtrend.

Let's briefly look what is MFI. The Market Facilitation Index (MFI) is a technical indicator that measures the price movement per unit of volume, helping traders gauge the efficiency of price movement in relation to trading volume. Here's how you can calculate it:

MFI = (High−Low)/Volume

MFI can be used in combination with volume, so we can divide 4 states. Bill Williams introduced these to help traders interpret the interaction between volume and price movement. Here’s a quick summary:

Green Window (Increased MFI & Increased Volume): Indicates strong momentum with both price and volume increasing. Often a sign of trend continuation, as both buying and selling interest are rising.

Fake Window (Increased MFI & Decreased Volume): Shows that price is moving but with lower volume, suggesting weak support for the trend. This can signal a potential end of the current trend.

Squat Window (Decreased MFI & Increased Volume): Shows high volume but little price movement, indicating a tug-of-war between buyers and sellers. This often precedes a breakout as the pressure builds.

Fade Window (Decreased MFI & Decreased Volume): Indicates a lack of interest from both buyers and sellers, leading to lower momentum. This typically happens in range-bound markets and may signal consolidation before a new move.

For our purposes we are interested in squat bars. This is the sign that volume cannot move the price easily. This type of bar increases the probability of trend reversal. In this indicator we added to enable the MFI filter of reversal bars. If potential reversal bar or two preceding bars have squat state this bar can be interpret as a reversal one.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.12.31. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -5.29%

Maximum Single Profit: +29.99%

Net Profit: +5472.66 USDT (+54.73%)

Total Trades: 103 (33.98% win rate)

Profit Factor: 1.634

Maximum Accumulated Loss: 1231.15 USDT (-8.32%)

Average Profit per Trade: 53.13 USDT (+0.94%)

Average Trade Duration: 76 hours

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h ETH/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

Bollinger Bands Enhanced StrategyOverview

The common practice of using Bollinger bands is to use it for building mean reversion or squeeze momentum strategies. In the current script Bollinger Bands Enhanced Strategy we are trying to combine the strengths of both strategies types. It utilizes Bollinger Bands indicator to buy the local dip and activates trailing profit system after reaching the user given number of Average True Ranges (ATR). Also it uses 200 period EMA to filter trades only in the direction of a trend. Strategy can execute only long trades.

Unique Features

Trailing Profit System: Strategy uses user given number of ATR to activate trailing take profit. If price has already reached the trailing profit activation level, scrip will close long trade if price closes below Bollinger Bands middle line.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Major Trend Filter: Strategy utilizes 100 period EMA to take trades only in the direction of a trend.

Flexible Risk Management: Users can choose number of ATR as a stop loss (by default = 1.75) for trades. This is flexible approach because ATR is recalculated on every candle, therefore stop-loss readjusted to the current volatility.

Methodology

First of all, script checks if currently price is above the 200-period exponential moving average EMA. EMA is used to establish the current trend. Script will take long trades on if this filtering system showing us the uptrend. Then the strategy executes the long trade if candle’s low below the lower Bollinger band. To calculate the middle Bollinger line, we use the standard 20-period simple moving average (SMA), lower band is calculated by the substruction from middle line the standard deviation multiplied by user given value (by default = 2).

When long trade executed, script places stop-loss at the price level below the entry price by user defined number of ATR (by default = 1.75). This stop-loss level recalculates at every candle while trade is open according to the current candle ATR value. Also strategy set the trailing profit activation level at the price above the position average price by user given number of ATR (by default = 2.25). It is also recalculated every candle according to ATR value. When price hit this level script plotted the triangle with the label “Strong Uptrend” and start trail the price at the middle Bollinger line. It also started to be plotted as a green line.

When price close below this trailing level script closes the long trade and search for the next trade opportunity.

Risk Management

The strategy employs a combined and flexible approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined ATR stop loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 1.75*ATR drop from the entry point, but it can be adjusted according to the trader's preferences.

There is no fixed take profit, but strategy allows user to define user the ATR trailing profit activation parameter. By default, this stop-loss is set to a 2.25*ATR growth from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Bollinger bangs indicator to open long trades in the local dips. If price reached the lower band there is a high probability of bounce. Here is an issue: during the strong downtrend price can constantly goes down without any significant correction. That’s why we decided to use 200-period EMA as a trend filter to increase the probability of opening long trades during major uptrend only.

Usually, Bollinger Bands indicator is using for mean reversion or breakout strategies. Both of them have the disadvantages. The mean reversion buys the dip, but closes on the return to some mean value. Therefore, it usually misses the major trend moves. The breakout strategies usually have the issue with too high buy price because to have the breakout confirmation price shall break some price level. Therefore, in such strategies traders need to set the large stop-loss, which decreases potential reward to risk ratio.

In this strategy we are trying to combine the best features of both types of strategies. Script utilizes ate ATR to setup the stop-loss and trailing profit activation levels. ATR takes into account the current volatility. Therefore, when we setup stop-loss with the user-given number of ATR we increase the probability to decrease the number of false stop outs. The trailing profit concept is trying to add the beat feature from breakout strategies and increase probability to stay in trade while uptrend is developing. When price hit the trailing profit activation level, script started to trail the price with middle line if Bollinger bands indicator. Only when candle closes below the middle line script closes the long trade.

Backtest Results

Operating window: Date range of backtests is 2020.10.01 - 2024.07.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -9.78%

Maximum Single Profit: +25.62%

Net Profit: +6778.11 USDT (+67.78%)

Total Trades: 111 (48.65% win rate)

Profit Factor: 2.065

Maximum Accumulated Loss: 853.56 USDT (-6.60%)

Average Profit per Trade: 61.06 USDT (+1.62%)

Average Trade Duration: 76 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

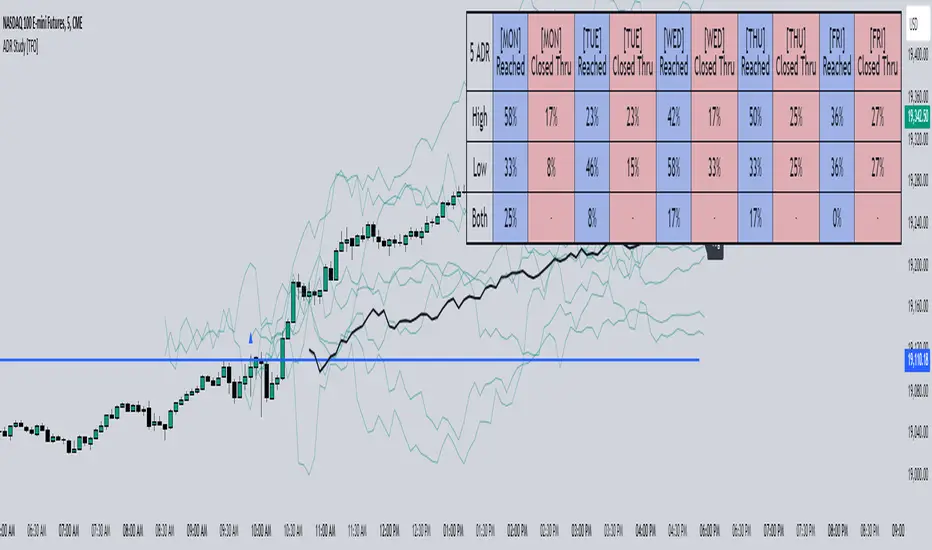

ADR Study [TFO]This indicator is focused on the Average Daily Range (ADR), with the goal of collecting data to show how often price reaches/closes through these levels, as well as a look at historical moves that reached ADR and at similar times of day to study how price moved for the remainder of the session.

The ADR here (blue line) is calculated using the difference between a day's highest and lowest points. If our ADR length is 5, then we are taking this difference from the last 5 days and averaging them together. At the following day's open, we take half of this average and plot it above and below the daily opening price to place theoretical limits on how far price may move according to the lookback period. The triangles indicate when price has reached ADR (either +ADR or -ADR), and alerts can be created for these events.

The Scale Factor is an optional parameter to scale the ADR by a certain amount. If set to 2 for example, then the ADR would be 2x the average daily range. This value will be reflected in the statistics options so that users can see how different values affect the outcomes.

Show Table will display data collected on how often price reaches these levels, and how often price closes through them, for each day of the week. By default, these are colored as blue and red, respectively. From the following chart of NQ1!, we can see for example that on Mondays, price reached +ADR 38% of the time and closed through it 23% of the time. Note that the statistics for closing through the ADR levels are derived from all instances, not just those that reached ADR.

Show Sample Sizes will display how many instances were collected for all given sets of data. Referring to the same example of NQ1!, we can see that this particular chart has collected data from 109 Mondays. From those Mondays, 41 reached +ADR (38%, verifying our initial claim) and 25 closed through it (23%). This is important to understand the scope of the data that we're working with, as percentages can be misleading for smaller sample sizes.

Show Histogram will plot the same exact data as the table, just in a histogram form to visually emphasize the differences on a day-by-day basis. On this chart of RTY1!, we can see for example from the top histogram that on Wednesdays, 40% reached +ADR and only 22% closed through it. Similarly if we look at the bottom histogram, we can see that Wednesdays reached -ADR 46% of the time and closed through it only 28% of the time.

We can also use Show Sample Sizes to display the same information that would be in the table, showing how many instances were collected for each event. In this case we can see that we observed 175 Fridays, where 76 reached +ADR (43%) and 44 closed above it (25%).

Show Historical Moves is an interesting feature of this script. When enabled, if price has reached +/- ADR in the current session, the indicator will plot the evolution of the close prices from all past sessions that reached +/- ADR to see how they traded for the remainder of the session. These calculations are made with respect to the ADR range at the time that price traded through these levels.

Historical Proximity (Bars) allows the user to observe historical moves where price reached ADR within this many bars of the current session (assuming price has reached an ADR level in the current session). In the above chart, this is set to 1000 so that we can observe each and every instance where price reached an ADR level. However, we can refine this a bit more.

By limiting the Historical Proximity to something like 20, we are only considering historical moves that reached ADR within 20 bars of todays +ADR reach (9:50 am EST, noted by the blue triangle up). We can enable Show Average Move to display the average move by the filtered dataset, and Match +/-ADR to only observe moves inline with the current day's price action (in this case, only moves that reached +ADR, since price has not reached -ADR).

We can add one more filter to this data with the setting Only Show Days That: closed through ADR; closed within ADR; or either. The option either is what you see above, as we are considering both days that closed through ADR and days that closed within it (note that in this case, closing within ADR simply means that price reached +ADR and closed the day below it, and vice versa for -ADR; this does not mean that price must have closed in between +ADR and -ADR). If we set this to only show instances that closed within ADR, we see the following data.

Alternatively, we can choose to Only Show Days That closed through ADR, where we would see the following data. In this case, the average move very much resembles the price action that occurred on this particular day. This is in no way guaranteed, but it makes an interesting case for how we could use this data in our analysis by observing similar, historical price action.

Please note that this data will change over time on a rolling basis due to TradingView's bar lookback, and that for this same reason, lower timeframes will yield less data than larger timeframes.

Ichimoku Theories [LuxAlgo]The Ichimoku Theories indicator is the most complete Ichimoku tool you will ever need. Four tools combined into one to harness all the power of Ichimoku Kinkō Hyō.

This tool features the following concepts based on the work of Goichi Hosoda:

Ichimoku Kinkō Hyō: Original Ichimoku indicator with its five main lines and kumo.

Time Theory: automatic time cycle identification and forecasting to understand market timing.

Wave Theory: automatic wave identification to understand market structure.

Price Theory: automatic identification of developing N waves and possible price targets to understand future price behavior.

🔶 ICHIMOKU KINKŌ HYŌ

Ichimoku with lines only, Kumo only and both together

Let us start with the basics: the Ichimoku original indicator is a tool to understand the market, not to predict it, it is a trend-following tool, so it is best used in trending markets.

Ichimoku tells us what is happening in the market and what may happen next, the aim of the tool is to provide market understanding, not trading signals.

The tool is based on calculating the mid-point between the high and low of three pre-defined ranges as the equilibrium price for short (9 periods), medium (26 periods), and long (52 periods) time horizons:

Tenkan sen: middle point of the range of the last 9 candles

Kinjun sen: middle point of the range of the last 26 candles

Senkou span A: middle point between Tankan Sen and Kijun Sen, plotted 26 candles into the future

Senkou span B: midpoint of the range of the last 52 candles, plotted 26 candles into the future

Chikou span: closing price plotted 26 candles into the past

Kumo: area between Senkou pans A and B (kumo means cloud in Japanese)

The most basic use of the tool is to use the Kumo as an area of possible support or resistance.

🔶 TIME THEORY

Current cycles and forecast

Time theory is a critical concept used to identify historical and current market cycles, and use these to forecast the next ones. This concept is based on the Kihon Suchi (translating to "Basic Numbers" in Japanese), these are 9 and 26, and from their combinations we obtain the following sequence:

9, 17, 26, 33, 42, 51, 65, 76, 129, 172, 200, 257

The main idea is that the market moves in cycles with periods set by the Kihon Suchi sequence.

When the cycle has the same exact periods, we obtain the Taito Suchi (translating to "Same Number" in Japanese).

This tool allows traders to identify historical and current market cycles and forecast the next one.

🔹 Time Cycle Identification

Presentation of 4 different modes: SWINGS, HIGHS, KINJUN, and WAVES .

The tool draws a horizontal line at the bottom of the chart showing the cycles detected and their size.

The following settings are used:

Time Cycle Mode: up to 7 different modes

Wave Cycle: Which wave to use when WAVE mode is selected, only active waves in the Wave Theory settings will be used.

Show Time Cycles: keep a cleaner chart by disabling cycles visualisation

Show last X time cycles: how many cycles to display

🔹 Time Cycle Forecast

Showcasing the two forecasting patterns: Kihon Suchi and Taito Suchi

The tool plots horizontal lines, a solid anchor line, and several dotted forecast lines.

The following settings are used:

Show time cycle forecast: to keep things clean

Forecast Pattern: comes in two flavors

Kihon Suchi plots a line from the anchor at each number in the Kihon Suchi sequence.

Taito Suchi plot lines from the anchor with the same size detected in the anchored cycle

Anchor forecast on last X time cycle: traders can place the anchor in any detected cycle

🔶 WAVE THEORY

All waves activated with overlapping

The main idea behind this theory is that markets move like waves in the sea, back and forth (making swing lows and highs). Understanding the current market structure is key to having realistic expectations of what the market may do next. The waves are divided into Simple and Complex.

The following settings are used:

Basic Waves: allows traders to activate waves I, V and N

Complex Waves: allows traders to activate waves P, Y and W

Overlapping waves: to avoid missing out on any of the waves activated

Show last X waves: how many waves will be displayed

🔹 Basic Waves

The three basic waves

The basic waves from which all waves are made are I, V, and N

I wave: one leg moves

V wave: two legs move, one against the other

N wave: Three legs move, push, pull back, and another push

🔹 Complex Waves

Three complex waves

There are other waves like

P wave: contracting market

Y wave: expanding market

W wave: double top or double bottom

🔶 PRICE THEORY

All targets for the current N wave with their calculations

This theory is based on identifying developing N waves and predicting potential price targets based on that developing wave.

The tool displays 4 basic targets (V, E, N, and NT) and 3 extended targets (2E and 3E) according to the calculations shown in the chart above. Traders can enable or disable each target in the settings panel.

🔶 USING EVERYTHING TOGETHER

Please DON'T do this. This is not how you use it

Now the real example:

Daily chart of Nasdaq 100 futures (NQ1!) with our Ichimoku analysis

Time, waves, and price theories go together as one:

First, we identify the current time cycles and wave structure.

Then we forecast the next cycle and possible key price levels.

We identify a Taito Suchi with both legs of exactly 41 candles on each I wave, both together forming a V wave, the last two I waves are part of a developing N wave, and the time cycle of the first one is 191 candles. We forecast this cycle into the future and get 22nd April as a key date, so in 6 trading days (as of this writing) the market would have completed another Taito Suchi pattern if a new wave and time cycle starts. As we have a developing N wave we can see the potential price targets, the price is actually between the NT and V targets. We have a bullish Kumo and the price is touching it, if this Kumo provides enough support for the price to go further, the market could reach N or E targets.

So we have identified the cycle and wave, our expectations are that the current cycle is another Taito Suchi and the current wave is an N wave, the first I wave went for 191 candles, and we expect the second and third I waves together to amount to 191 candles, so in theory the N wave would complete in the next 6 trading days making a swing high. If this is indeed the case, the price could reach the V target (it is almost there) or even the N target if the bulls have the necessary strength.

We do not predict the future, we can only aim to understand the current market conditions and have future expectations of when (time), how (wave), and where (price) the market will make the next turning point where one side of the market overcomes the other (bulls vs bears).

To generate this chart, we change the following settings from the default ones:

Swing length: 64

Show lines: disabled

Forecast pattern: TAITO SUCHI

Anchor forecast: 2

Show last time cycles: 5

I WAVE: enabled

N WAVE: disabled

Show last waves: 5

🔶 SETTINGS

Show Swing Highs & Lows: Enable/Disable points on swing highs and swing lows.

Swing Length: Number of candles to confirm a swing high or swing low. A higher number detects larger swings.

🔹 Ichimoku Kinkō Hyō

Show Lines: Enable/Disable the 5 Ichimoku lines: Kijun sen, Tenkan sen, Senkou span A & B and Chikou Span.

Show Kumo: Enable/Disable the Kumo (cloud). The Kumo is formed by 2 lines: Senkou Span A and Senkou Span B.

Tenkan Sen Length: Number of candles for Tenkan Sen calculation.

Kinjun Sen Length: Number of candles for the Kijun Sen calculation.

Senkou Span B Length: Number of candles for Senkou Span B calculation.

Chikou & Senkou Offset: Number of candles for Chikou and Senkou Span calculation. Chikou Span is plotted in the past, and Senkou Span A & B in the future.

🔹 Time Theory

Show Time Cycle Forecast: Enable/Disable time cycle forecast vertical lines. Disable for better performance.

Forecast Pattern: Choose between two patterns: Kihon Suchi (basic numbers) or Taito Suchi (equal numbers).

Anchor forecast on last X time cycle: Number of time cycles in the past to anchor the time cycle forecast. The larger the number, the deeper in the past the anchor will be.

Time Cycle Mode: Choose from 7 time cycle detection modes: Tenkan Sen cross, Kijun Sen cross, Kumo change between bullish & bearish, swing highs only, swing lows only, both swing highs & lows and wave detection.

Wave Cycle: Choose which type of wave to detect from 6 different wave types when the time cycle mode is set to WAVES.

Show Time Cycles: Enable/Disable time cycle horizontal lines. Disable for better performance.

how last X time cycles: Maximum number of time cycles to display.

🔹 Wave Theory

Basic Waves: Enable/Disable the display of basic waves, all at once or one at a time. Disable for better performance.

Complex Waves: Enable/Disable complex wave display, all at once or one by one. Disable for better performance.

Overlapping Waves: Enable/Disable the display of waves ending on the same swing point.

Show last X waves: 'Maximum number of waves to display.

🔹 Price Theory

Basic Targets: Enable/Disable horizontal price target lines. Disable for better performance.

Extended Targets: Enable/Disable extended price target horizontal lines. Disable for better performance.

Order Block Refiner [TradingFinder]🔵 Introduction

The "Refinement" feature allows you to adjust the width of the order block according to your strategy. There are two modes, "Aggressive" and "Defensive," in the "Order Block Refine". The difference between "Aggressive" and "Defensive" lies in the width of the order block.

For risk-averse traders, the "Defensive" mode is suitable as it provides a lower loss limit and a greater reward-to-risk ratio. For risk-taking traders, the "Aggressive" mode is more appropriate. These traders prefer to enter trades at higher prices, and this mode, which has a wider order block width, is more suitable for this group of individuals.

Important :

One of the advantages of using this library is increased code accuracy. Not only does it have the capability to create order blocks, but you can also simply define the condition for order block creation (true/false) and "bar_index," and you'll find the primary range without applying any filters.

🟣 Order Block Refinement Algorithm

The order block ranges are filtered in two stages. In the first stage, the "Open," "High," "Low," and "Close" of the current order block candle, its two or three previous candles, and one subsequent candle (if available) are examined. In this stage, minimum and maximum distances are calculated, and logical range filters are applied.

In the second stage, two modes, "Aggressive" and "Defensive," are calculated.

For the "Defensive" mode, the width of these ranges is compared with the "ATR" (Average True Range) of period 55, and if they are smaller than "ATR" or 1 to more than 4 times "ATR," the width of the range is reduced from 0 to 80 percent.

For the "Aggressive" mode, you get the same output as the first filter, which usually has a wider width than the "Defensive" mode.

• Order Block Refiner : Off

• Order Block Refiner : On / "Aggressive Mode"

• Order Block Refiner : On / "Defensive Mode"

🔵 How to Use

OBRefiner(string OBType, string OBRefine, string RefineMethod, bool TriggerCondition, int Index) =>

Parameters:

• OBType (string)

• OBRefine (string)

• RefineMethod (string)

• TriggerCondition (bool)

• Index (int)

To add "Order Block Refiner Library", you must first add the following code to your script.

import TFlab/OrderBlockRefiner_TradingFinder/1

OBType : This parameter receives 2 inputs. If the order block you want to "Refine" is of type demand, you should enter "Demand," and if it's of type supply, you should enter "Supply."

OBRefine : Set to "On" if you want the "Refine" operation to be performed. Otherwise, set to "Off."

RefineMethod : This input receives 2 modes, "Aggressive" and "Defensive." You can switch between these modes according to your needs.

TriggerCondition : Enter the condition with which the order block is formed in this parameter.

Index : Enter the "bar_index" of the candle where the order block is formed in this parameter.

🟣 Function Outputs

This function has 6 outputs: "bar_index" at the beginning of the "Distal" line, "bar_index+1" at the end of the "Distal" line, "Price" at the "Distal" line, "bar_index" at the beginning of the "Proximal" line, "bar_index+1" at the end of the "Proximal" line, and "Price" at the "Proximal" line, which can be used to draw order blocks.

Sample :

= Refiner.OBRefiner('Demand', 'Off', 'Aggressive',BuMChMain_Trigger, BuMChMain_Index)

if BuMChMain_Trigger

BuMChHlineMain := line.new(BuMChMain_Xp1 , BuMChMain_Yp12 , bar_index , BuMChMain_Yp12, color = color.black , style = line.style_dotted)

BuMChLlineMain := line.new(BuMChMain_Xd1 , BuMChMain_Yd12 , bar_index , BuMChMain_Yd12, color = color.black , style = line.style_dotted)

BuMChFilineMain := linefill.new(BuMChHlineMain ,BuMChLlineMain , color = color.rgb(76, 175, 80 , 75 ) )

Long EMA Strategy with Advanced Exit OptionsThis strategy is designed for traders seeking a trend-following system with a focus on precision and adaptability.

**Core Strategy Concept**

The essence of this strategy lies in use of Exponential Moving Averages (EMAs) to identify potential long (buy) positions based on the relative positions of short-term, medium-term, and long-term EMAs. The use of EMAs is a classic yet powerful approach to trend detection, as these indicators smooth out price data over time, emphasizing the direction of recent price movements and potentially signaling the beginning of new trends.

**Customizable Parameters**

- **EMA Periods**: Users can define the periods for three EMAs - long-term, medium-term, and short-term - allowing for a tailored approach to capture trends based on individual trading styles and market conditions.

- **Volatility Filter**: An optional Average True Range (ATR)-based volatility filter can be toggled on or off. When activated, it ensures that trades are only entered when market volatility exceeds a user-defined threshold, aiming to filter out entries during low-volatility periods which are often characterized by indecisive market movements.

- **Trailing Stop Loss**: A trailing stop loss mechanism, expressed as a percentage of the highest price achieved since entry, provides a dynamic way to manage risk by allowing profits to run while cutting losses.

- **EMA Exit Condition**: This advanced exit option enables closing positions when the short-term EMA crosses below the medium-term EMA, serving as a signal that the immediate trend may be reversing.

- **Close Below EMA Exit**: An additional exit condition, which is disabled by default, allows positions to be closed if the price closes below a user-selected EMA. This provides an extra layer of flexibility and risk management, catering to traders who prefer to exit positions based on specific EMA thresholds.

**Operational Mechanics**

Upon activation, the strategy evaluates the current price in relation to the set EMAs. A long position is considered when the current price is above the long-term EMA, and the short-term EMA is above the medium-term EMA. This setup aims to identify moments where the price momentum is strong and likely to continue.

The strategy's versatility is further enhanced by its optional settings:

- The **Volatility Filter** adjusts the sensitivity of the strategy to market movements, potentially improving the quality of the entries during volatile market conditions.

The Average True Range (ATR) is a key component of this filter, providing a measure of market volatility by calculating the average range between the high and low prices over a specified number of periods. Here's how you can adjust the volatility filter settings for various market conditions, focusing on filtering out low-volatility markets:

Setting Examples for Volatility Filter

1. High Volatility Markets (e.g., Cryptocurrencies, Certain Forex Pairs):

ATR Periods: 14 (default)

ATR Multiplier: Setting the multiplier to a lower value, such as 1.0 or 1.2, can be beneficial in high-volatility markets. This sensitivity allows the strategy to react to volatility changes more quickly, ensuring that you're entering trades during periods of significant movement.

2. Medium Volatility Markets (e.g., Major Equity Indices, Medium-Volatility Forex Pairs):

ATR Periods: 14 (default)

ATR Multiplier: A multiplier of 1.5 (default) is often suitable for medium volatility markets. It provides a balanced approach, ensuring that the strategy filters out low-volatility conditions without being overly restrictive.

3. Low Volatility Markets (e.g., Some Commodities, Low-Volatility Forex Pairs):

ATR Periods: Increasing the ATR period to 20 or 25 can smooth out the volatility measure, making it less sensitive to short-term fluctuations. This adjustment helps in focusing on more significant trends in inherently stable markets.

ATR Multiplier: Raising the multiplier to 2.0 or even 2.5 increases the threshold for volatility, effectively filtering out low-volatility conditions. This setting ensures that the strategy only triggers trades during periods of relatively higher volatility, which are more likely to result in significant price movements.

How to Use the Volatility Filter for Low-Volatility Markets

For traders specifically interested in filtering out low-volatility markets, the key is to adjust the ATR Multiplier to a higher level. This adjustment increases the threshold required for the market to be considered sufficiently volatile for trade entries. Here's a step-by-step guide:

Adjust the ATR Multiplier: Increase the ATR Multiplier to create a higher volatility threshold. A multiplier of 2.0 to 2.5 is a good starting point for very low-volatility markets.

Fine-Tune the ATR Periods: Consider lengthening the ATR calculation period if you find that the strategy is still entering trades in undesirable low-volatility conditions. A longer period provides a more averaged-out measure of volatility, which might better suit your needs.

Monitor and Adjust: Volatility is not static, and market conditions can change. Regularly review the performance of your strategy in the context of current market volatility and adjust the settings as necessary.

Backtest in Different Conditions: Before applying the strategy live, backtest it across different market conditions with your adjusted settings. This process helps ensure that your approach to filtering low-volatility conditions aligns with your trading objectives and risk tolerance.

By fine-tuning the volatility filter settings according to the specific characteristics of the market you're trading in, you can enhance the performance of this strategy

- The **Trailing Stop Loss** and **EMA Exit Conditions** provide two layers of exit strategies, focusing on capital preservation and profit maximization.

**Visualizations**

For clarity and ease of use, the strategy plots the three EMAs and, if enabled, the ATR threshold on the chart. These visual cues not only aid in decision-making but also help in understanding the market's current trend and volatility state.

**How to Use**

Traders can customize the EMA periods to fit their trading horizon, be it short, medium, or long-term trading. The volatility filter and exit options allow for further customization, making the strategy adaptable to different market conditions and personal risk tolerance levels.

By offering a blend of trend-following principles with advanced risk management features, this strategy aims to cater to a wide range of trading styles, from cautious to aggressive. Its strength lies in its flexibility, allowing traders to fine-tune settings to their specific needs, making it a potentially valuable tool in the arsenal of any trader looking for a disciplined approach to navigating the markets.

Hosoda Waves ABCThe Hosoda Waves indicator was devised by Goichi Hosoda, the creator of the Ichimoku system, with the idea that previous highs and lows could determine future price ranges to which the market would react. Hosoda's projections include the NT, N, V, and E waves, derived from calculations based on both upward and downward ABC swings. The calculations for Hosoda's waves are as follows:

NT Wave = C + (C - A)

N Wave = B + (B - A)

V Wave = B + (B - C)

E Wave = C + (B - A)

This indicator visually represents the calculations by Hosoda. Additionally, Hosoda indicated time cycles: 9, 17, 26, 33, 42, 51, 65, 76, etc., which are not integrated into this indicator as they are not considered effective in contemporary times.

Once applied to the chart, the interactive Pine Script tool version 5 will prompt you to identify 3 points of "low-high-low" or "high-low-high," both for upward and downward movements. Once clicked, these price points can be moved. If you change the time frame or market instrument, the indicator must be removed because it remains tied to the prices where it was initially drawn.

RSI Bands + Levels (Miu)This indicator was designed to plot lines from prices of overbought (OB) and oversold (OS) RSI levels in chart. It will also create a visible band between these levels.

It's main utility is to show in chart current and past prices for OB/OS RSI levels. Traditionally the RSI is considered overbought when above 70 and oversold when below 30 but you can customize these values in settings. The RSI oscillates between zero and 100.

Users can easily identify overbought and oversold prices using this indicator and then it is expected to help users to make better strategic decisions with their trades.

There are some extra options available in settings:

- Customizable RSI levels

- Customizable RSI length

- RSI Levels: if activated, it will draw lines above OB line and below OS line according to the multiplier, so it will plot sequential lines that goes in different RSI levels (e.g: RSI 72, 74, 76, 78 and 80).

- Backgroud only: it will remove these lines and keep only a backgroung color instead

- RSI 50: it will draw a line as RSI 50

- Customizable multiplier

Enjoy!

Implied and Historical Volatility v4There is a famous option strategy📊 played on volatility📈. Where people go short on volatility, generally, this strategy is used before any significant event or earnings release. The basic phenomenon is that the Implied Volatility shoots up before the event and drops after the event, while the volatility of the security does not increase in most of the scenarios. 💹

I have tried to create an Indicator using which you

can analyse the historical change in Implied Volatility Vs Historic Volatility.

To get a basic idea of how the security moved during different events.

Notes:

a) Implied Volatility is calculated using the bisection method and Black 76 model option pricing model.

b) For the risk-free rate I have fetched the price of the “10-Year Indian Government Bond” price and calculated its yield to be used as our Risk-Free rate.

Relative Strength Screener V2 - Top 100 volume leadersNew and improved strength heatmap for the top 100 volume leaders in the S&P. Coded in a workaround to the 40 request.security limitation that currently exists in Pine. Added the ability to input the number of columns (time frames) you wish to display.

For 3 time frame analysis, add the indicator to your chart 3 times. Change the number of columns to 3 for each of these indicators. Specify the column and time frame for each one (example, 5 minute for column 1, 1 hour for column 2 and Daily chart for column 3). It will automatically resize the columns/tables to properly display the output. This provides a sort of "Strength Heatmap" for the top 100 stocks in the S&P. To achieve this, make a copy of the indicator and substitute lines 68-105 with the following premade watchlists :

Make a copy 1 - FIrst 38 volume leaders in the S&P

s01 = input.symbol('AAPL', group = 'Symbols', inline = 's01')

s02 = input.symbol('ABBV', group = 'Symbols', inline = 's02')

s03 = input.symbol('ABT', group = 'Symbols', inline = 's03')

s04 = input.symbol('ACN', group = 'Symbols', inline = 's04')

s05 = input.symbol('AEP', group = 'Symbols', inline = 's05')

s06 = input.symbol('AIG', group = 'Symbols', inline = 's06')

s07 = input.symbol('AMAT', group = 'Symbols', inline = 's07')

s08 = input.symbol('AMD', group = 'Symbols', inline = 's08')

s09 = input.symbol('APA', group = 'Symbols', inline = 's09')

s10 = input.symbol('ATVI', group = 'Symbols', inline = 's10')

s11 = input.symbol('AXP', group = 'Symbols', inline = 's11')

s12 = input.symbol('BA', group = 'Symbols', inline = 's12')

s13 = input.symbol('BBWI', group = 'Symbols', inline = 's13')

s14 = input.symbol('BBY', group = 'Symbols', inline = 's14')

s15 = input.symbol('BK', group = 'Symbols', inline = 's15')

s16 = input.symbol('BMY', group = 'Symbols', inline = 's16')

s17 = input.symbol('BRK.B', group = 'Symbols', inline = 's17')

s18 = input.symbol('C', group = 'Symbols', inline = 's18')

s19 = input.symbol('CAT', group = 'Symbols', inline = 's19')

s20 = input.symbol('CCL', group = 'Symbols', inline = 's20')

s21 = input.symbol('CFG', group = 'Symbols', inline = 's21')

s22 = input.symbol('CL', group = 'Symbols', inline = 's22')

s23 = input.symbol('CNC', group = 'Symbols', inline = 's23')

s24 = input.symbol('COF', group = 'Symbols', inline = 's24')

s25 = input.symbol('COP', group = 'Symbols', inline = 's25')

s26 = input.symbol('COST', group = 'Symbols', inline = 's26')

s27 = input.symbol('CRM', group = 'Symbols', inline = 's27')

s28 = input.symbol('CVS', group = 'Symbols', inline = 's28')

s29 = input.symbol('CVX', group = 'Symbols', inline = 's29')

s30 = input.symbol('DAL', group = 'Symbols', inline = 's30')

s31 = input.symbol('DIS', group = 'Symbols', inline = 's31')

s32 = input.symbol('DISCA', group = 'Symbols', inline = 's32')

s33 = input.symbol('DISCK', group = 'Symbols', inline = 's33')

s34 = input.symbol('DISH', group = 'Symbols', inline = 's34')

s35 = input.symbol('DLTR', group = 'Symbols', inline = 's35')

s36 = input.symbol('DOW', group = 'Symbols', inline = 's36')

s37 = input.symbol('DVN', group = 'Symbols', inline = 's37')

s38 = input.symbol('EBAY', group = 'Symbols', inline = 's38')

Make a copy 2 - Tickers 39 to 76

s01 = input.symbol('EOG', group = 'Symbols', inline = 's01')

s02 = input.symbol('F', group = 'Symbols', inline = 's02')

s03 = input.symbol('FB', group = 'Symbols', inline = 's03')

s04 = input.symbol('FCX', group = 'Symbols', inline = 's04')

s05 = input.symbol('FIS', group = 'Symbols', inline = 's05')

s06 = input.symbol('GE', group = 'Symbols', inline = 's06')

s07 = input.symbol('GIS', group = 'Symbols', inline = 's07')

s08 = input.symbol('GM', group = 'Symbols', inline = 's08')

s09 = input.symbol('GS', group = 'Symbols', inline = 's09')

s10 = input.symbol('HD', group = 'Symbols', inline = 's10')

s11 = input.symbol('IBM', group = 'Symbols', inline = 's11')

s12 = input.symbol('INTC', group = 'Symbols', inline = 's12')

s13 = input.symbol('JNJ', group = 'Symbols', inline = 's13')

s14 = input.symbol('JPM', group = 'Symbols', inline = 's14')

s15 = input.symbol('KR', group = 'Symbols', inline = 's15')

s16 = input.symbol('LUV', group = 'Symbols', inline = 's16')

s17 = input.symbol('LVS', group = 'Symbols', inline = 's17')

s18 = input.symbol('MA', group = 'Symbols', inline = 's18')

s19 = input.symbol('MCD', group = 'Symbols', inline = 's19')

s20 = input.symbol('MCHP', group = 'Symbols', inline = 's20')

s21 = input.symbol('MDT', group = 'Symbols', inline = 's21')

s22 = input.symbol('MET', group = 'Symbols', inline = 's22')

s23 = input.symbol('MGM', group = 'Symbols', inline = 's23')

s24 = input.symbol('MOS', group = 'Symbols', inline = 's24')

s25 = input.symbol('MPC', group = 'Symbols', inline = 's25')

s26 = input.symbol('MRK', group = 'Symbols', inline = 's26')

s27 = input.symbol('MRNA', group = 'Symbols', inline = 's27')

s28 = input.symbol('MS', group = 'Symbols', inline = 's28')

s29 = input.symbol('MSFT', group = 'Symbols', inline = 's29')

s30 = input.symbol('MU', group = 'Symbols', inline = 's30')

s31 = input.symbol('NCLH', group = 'Symbols', inline = 's31')

s32 = input.symbol('NEE', group = 'Symbols', inline = 's32')

s33 = input.symbol('NEM', group = 'Symbols', inline = 's33')

s34 = input.symbol('NFLX', group = 'Symbols', inline = 's34')

s35 = input.symbol('NKE', group = 'Symbols', inline = 's35')

s36 = input.symbol('NVDA', group = 'Symbols', inline = 's36')

s37 = input.symbol('ORCL', group = 'Symbols', inline = 's37')

s38 = input.symbol('OXY', group = 'Symbols', inline = 's38')

Make a copy 3 - tickers 77 to 114

s01 = input.symbol('PENN', group = 'Symbols', inline = 's01')

s02 = input.symbol('PEP', group = 'Symbols', inline = 's02')

s03 = input.symbol('PFE', group = 'Symbols', inline = 's03')

s04 = input.symbol('PG', group = 'Symbols', inline = 's04')

s05 = input.symbol('PM', group = 'Symbols', inline = 's05')

s06 = input.symbol('PYPL', group = 'Symbols', inline = 's06')

s07 = input.symbol('QCOM', group = 'Symbols', inline = 's07')

s08 = input.symbol('RTX', group = 'Symbols', inline = 's08')

s09 = input.symbol('SBUX', group = 'Symbols', inline = 's09')

s10 = input.symbol('SCHW', group = 'Symbols', inline = 's10')

s11 = input.symbol('SLB', group = 'Symbols', inline = 's11')

s12 = input.symbol('SYF', group = 'Symbols', inline = 's12')

s13 = input.symbol('T', group = 'Symbols', inline = 's13')

s14 = input.symbol('TFC', group = 'Symbols', inline = 's14')

s15 = input.symbol('TGT', group = 'Symbols', inline = 's15')

s16 = input.symbol('TJX', group = 'Symbols', inline = 's16')

s17 = input.symbol('TMUS', group = 'Symbols', inline = 's17')

s18 = input.symbol('TSLA', group = 'Symbols', inline = 's18')

s19 = input.symbol('TWTR', group = 'Symbols', inline = 's19')

s20 = input.symbol('TXN', group = 'Symbols', inline = 's20')

s21 = input.symbol('UAL', group = 'Symbols', inline = 's21')