Breadth-Driven Swing StrategyWhat it does

This script trades the S&P 500 purely on market breadth extremes:

• Data source : INDEX:S5TH = % of S&P 500 stocks above their own 200-day SMA (range 0–100).

• Buy when breadth is washed-out.

• Sell when breadth is overheated.

It is long-only by design; shorting and ATR trailing stops have been removed to keep the logic minimal and transparent.

⸻

Signals in plain English

1. Long entry

A. A 200-EMA trough in breadth is printed and the trough value is ≤ 40 %.

or

B. A 5-EMA trough appears, its prominence passes the user threshold, and the lowest breadth reading in the last 20 bars is ≤ 20 %.

(Toggle this secondary trigger on/off with “ Enter also on 5-EMA trough ”.)

2. Exit (close long)

First 200-EMA peak whose breadth value is ≥ 70 %.

3. Risk control

A fixed stop-loss (% of entry price, default 8 %) is attached to every long trade.

⸻

Key parameters (defaults shown)

• Long EMA length 200 • Short EMA length 5

• Peak prominence 0.5 pct-pts • Trough prominence 3 pct-pts

• Peak level 70 % • Trough level 40 % • 5-EMA trough level 20 %

• Fixed stop-loss 8 %

• “Enter also on 5-EMA trough” = true (allows additional entries on extreme momentum reversals)

Feel free to tighten or relax any of these thresholds to match your risk profile or account for different market regimes.

⸻

How to use it

1. Load the script on a daily SPX / SPY chart.

(The price chart drives order execution; the breadth series is pulled internally and does not need to be on the chart.)

2. Verify the breadth feed.

INDEX:S5TH is updated after each session; your broker must provide it.

3. Back-test across several cycles.

Two decades of daily data is recommended to see how the rules behave in bear markets, range markets, and bull trends.

4. Adjust position sizing in the Properties tab.

The default is “100 % of equity”; change it if you prefer smaller allocations or pyramiding caps.

⸻

Why it can help

• Breadth signals often lead price, allowing entries before index-level momentum turns.

• Simple, rule-based exits prevent “waiting for confirmation” paralysis.

• Only one input series—easy to audit, no black-box math.

Trade-offs

• Relies on a single breadth metric; other internals (advance/decline, equal-weight returns, etc.) are ignored.

• May sit in cash during shallow pullbacks that never push breadth ≤ 40 %.

• Signals arrive at the end of the session (breadth is EoD data).

⸻

Disclaimer

This script is provided for educational purposes only and is not financial advice. Markets are risky; test thoroughly and use your own judgment before trading real money.

ストラテジー概要

本スクリプトは S&P500 のマーケットブレッド(内部需給) だけを手がかりに、指数をスイングトレードします。

• ブレッドデータ : INDEX:S5TH

(S&P500 採用銘柄のうち、それぞれの 200 日移動平均線を上回っている銘柄比率。0–100 %)

• 買い : ブレッドが極端に売られたタイミング。

• 売り : ブレッドが過熱状態に達したタイミング。

余計な機能を削り、ロングオンリー & 固定ストップ のシンプル設計にしています。

⸻

シグナルの流れ

1. ロングエントリー

• 条件 A : 200-EMA がトラフを付け、その値が 40 % 以下

• 条件 B : 5-EMA がトラフを付け、

・プロミネンス条件を満たし

・直近 20 本のブレッドス最小値が 20 % 以下

• B 条件は「5-EMA トラフでもエントリー」を ON にすると有効

2. ロング決済

最初に出現した 200-EMA ピーク で、かつ値が 70 % 以上 のバーで手仕舞い。

3. リスク管理

各トレードに 固定ストップ(初期価格から 8 %)を設定。

⸻

主なパラメータ(デフォルト値)

• 長期 EMA 長さ : 200 • 短期 EMA 長さ : 5

• ピーク判定プロミネンス : 0.5 %pt • トラフ判定プロミネンス : 3 %pt

• ピーク水準 : 70 % • トラフ水準 : 40 % • 5-EMA トラフ水準 : 20 %

• 固定ストップ : 8 %

• 「5-EMA トラフでもエントリー」 : ON

相場環境やリスク許容度に合わせて閾値を調整してください。

⸻

使い方

1. 日足の SPX / SPY チャート にスクリプトを適用。

2. ブレッドデータの供給 (INDEX:S5TH) がブローカーで利用可能か確認。

3. 20 年以上の期間でバックテスト し、強気相場・弱気相場・レンジ局面での挙動を確認。

4. 資金配分 は プロパティ → 戦略実行 で調整可能(初期値は「資金の 100 %」)。

⸻

強み

• ブレッドは 価格より先行 することが多く、天底を早期に捉えやすい。

• ルールベースの出口で「もう少し待とう」と迷わずに済む。

• 入力 series は 1 本のみ、ブラックボックス要素なし。

注意点・弱み

• 単一指標に依存。他の内部需給(A/D ライン等)は考慮しない。

• 40 % を割らない浅い押し目では機会損失が起こる。

• ブレッドは終値ベースの更新。ザラ場中の変化は捉えられない。

⸻

免責事項

本スクリプトは 学習目的 で提供しています。投資助言ではありません。

実取引の前に必ず自己責任で十分な検証とリスク管理を行ってください。

Cari dalam skrip untuk "港股央企红利etf"

Anchored Bollinger Band Range [SS]This is the anchored Bollinger band indicator.

What it does?

The anchored BB indicator:

Takes a user defined range and calculates the Standard Deviation of the entire selected range for the high and low values.

Computes a moving average of the high and low during the selected period (which later becomes the breakout range average)

Anchors to the last high and last low of the period range to add up to 4 standard deviations to the upside and downside, giving you 4 high and low targets.

How can you use it?

The anchored BB indicator has many applicable uses, including

Identifying daily ranges based on premarket trading activity ( see below ):

Finding breakout ranges for intraday pattern setups ( see below ):

Identified pattern of interest:

Applying Anchored BB:

Identifying daily or pattern biases based on the position to the opening breakout range average (blue line). See the examples with explanations:

ex#1:

ex#2:

The Opening Breakout Average

As you saw in the examples above, the blue line represents the opening breakout range average.

This is the average high of the period of interest and the average low of the period of interest.

Price action above this line would be considered Bullish, and Bearish if below.

This also acts as a retracement zone in non-trending markets. For example:

Best Use Cases

Identify breakout ranges for patterns on larger timeframes. For example

This pattern on SPY, if we overlay the Anchored BB:

You want to see it actually breakout from this range and hold to confirm a breakout. Failure to exceed the BB range, means that it is just ranging with no real breakout momentum.

Identify conservative ranges for a specific period in time, for example QQQ:

Worst Use Cases

Using it as a hard and fast support and resistance indicator. This is not what it is for and ranges can be exceeded with momentum. The key is looking for whether ranges are exceeded (i.e. high momentum, thus breakout play) or they are not (thus low volume, rangy).

Using it for longer term outlooks. This is not ideal for long term ranges, as with any Bollinger/standard deviation based approach, it is only responsive to CURRENT PA and cannot forecast FUTURE PA.

User Inputs

The indicator is really straight forward. There are 2 optional inputs and 1 required input.

Period Selection: Required. Selects the period for the indicator to perform the analysis on. You just select it with your mouse on the chart.

Visible MA: Optional. You can choose to have the breakout range moving average visible or not.

Fills: Optional. You can choose to have the fills plotted or not.

And that is the indicator! Very easy to use and hope you enjoy and find it helpful!

As always, safe trades everyone! 🚀

Cointegration Buy and Sell Signals [EdgeTerminal]The Cointegration Buy And Sell Signals is a sophisticated technical analysis tool to spot high-probability market turning points — before they fully develop on price charts.

Most reversal indicators rely on raw price action, visual patterns, or basic and common indicator logic — which often suffer in noisy or trending markets. In most cases, they lag behind the actual change in trend and provide useless and late signals.

This indicator is rooted in advanced concepts from statistical arbitrage, mean reversion theory, and quantitative finance, and it packages these ideas in a user-friendly visual format that works on any timeframe and asset class.

It does this by analyzing how the short-term and long-term EMAs behave relative to each other — and uses statistical filters like Z-score, correlation, volatility normalization, and stationarity tests to issue highly selective Buy and Sell signals.

This tool provides statistical confirmation of trend exhaustion, allowing you to trade mean-reverting setups. It fades overextended moves and uses signal stacking to reduce false entries. The entire indicator is based on a very interesting mathematically grounded model which I will get into down below.

Here’s how the indicator works at a high level:

EMAs as Anchors: It starts with two Exponential Moving Averages (EMAs) — one short-term and one long-term — to track market direction.

Statistical Spread (Regression Residuals): It performs a rolling linear regression between the short and long EMA. Instead of using the raw difference (short - long), it calculates the regression residual, which better models their natural relationship.

Normalize the Spread: The spread is divided by historical price volatility (ATR) to make it scale-invariant. This ensures the indicator works on low-priced stocks, high-priced indices, and crypto alike.

Z-Score: It computes a Z-score of the normalized spread to measure how “extreme” the current deviation is from its historical average.

Dynamic Thresholds: Unlike most tools that use fixed thresholds (like Z = ±2), this one calculates dynamic thresholds using historical percentiles (e.g., top 10% and bottom 10%) so that it adapts to the asset's current behavior to reduce false signals based on market’s extreme volatility at a certain time.

Z-Score Momentum: It tracks the direction of the Z-score — if Z is extreme but still moving away from zero, it's too early. It waits for reversion to start (Z momentum flips).

Correlation Check: Uses a rolling Pearson correlation to confirm the two EMAs are still statistically related. If they diverge (low correlation), no signal is shown.

Stationarity Filter (ADF-like): Uses the volatility of the regression residual to determine if the spread is stationary (mean-reverting) — a key concept in cointegration and statistical arbitrage. It’s not possible to build an exact ADF filter in Pine Script so we used the next best thing.

Signal Control: Prevents noisy charts and overtrading by ensuring no back-to-back buy or sell signals. Each signal must alternate and respect a cooldown period so you won’t be overwhelmed and won’t get a messy chart.

Important Notes to Remember:

The whole idea behind this indicator is to try to use some stat arb models to detect shifting patterns faster than they appear on common indicators, so in some cases, some assumptions are made based on historic values.

This means that in some cases, the indicator can “jump” into the conclusion too quickly. Although we try to eliminate this by using stationary filters, correlation checks, and Z-score momentum detection, there is still a chance some signals that are generated can be too early, in the stock market, that's the same as being incorrect. So make sure to use this with other indicators to confirm the movement.

How To Use The Indicator:

You can use the indicator as a standalone reversal system, as a filter for overbought and oversold setups, in combination with other trend indicators and as a part of a signal stack with other common indicators for divergence spotting and fade trades.

The indicator produces simple buy and sell signals when all criteria is met. Based on our own testing, we recommend treating these signals as standalone and independent from each other . Meaning that if you take position after a buy signal, don’t wait for a sell signal to appear to exit the trade and vice versa.

This is why we recommend using this indicator with other advanced or even simple indicators as an early confirmation tool.

The Display Table:

The floating diagnostic table in the top-right corner of the chart is a key part of this indicator. It's a live statistical dashboard that helps you understand why a signal is (or isn’t) being triggered, and whether the market conditions are lining up for a potential reversal.

1. Z-Score

What it shows: The current Z-score value of the volatility-normalized spread between the short EMA and the regression line of the long EMA.

Why it matters: Z-score tells you how statistically extreme the current relationship is. A Z-score of:

0 = perfectly average

> +2 = very overbought

< -2 = very oversold

How to use it: Look for Z-score reaching extreme highs or lows (beyond dynamic thresholds). Watch for it to start reversing direction, especially when paired with green table rows (see below)

2. Z-Score Momentum

What it shows: The rate of change (ROC) of the Z-score:

Zmomentum=Zt − Zt − 1

Why it matters: This tells you if the Z-score is still stretching out (e.g., getting more overbought/oversold), or reverting back toward the mean.

How to use it: A positive Z-momentum after a very low Z-score = potential bullish reversal A negative Z-momentum after a very high Z-score = potential bearish reversal. Avoid signals when momentum is still pushing deeper into extremes

3. Correlation

What it shows: The rolling Pearson correlation coefficient between the short EMA and long EMA.

Why it matters: High correlation (closer to +1) means the EMAs are still statistically connected — a key requirement for cointegration or mean reversion to be valid.

How to use it: Look for correlation > 0.7 for reliable signals. If correlation drops below 0.5, ignore the Z-score — the EMAs aren’t moving together anymore

4. Stationary

What it shows: A simplified "Yes" or "No" answer to the question:

“Is the spread statistically stable (stationary) and mean-reverting right now?”

Why it matters: Mean reversion strategies only work when the spread is stationary — that is, when the distance between EMAs behaves like a rubber band, not a drifting cloud.

How to use it: A "Yes" means the indicator sees a consistent, stable spread — good for trading. "No" means the market is too volatile, disjointed, or chaotic for reliable mean reversion. Wait for this to flip to "Yes" before trusting signals

5. Last Signal

What it shows: The last signal issued by the system — either "Buy", "Sell", or "None"

Why it matters: Helps avoid confusion and repeated entries. Signals only alternate — you won’t get another Buy until a Sell happens, and vice versa.

How to use it: If the last signal was a "Buy", and you’re watching for a Sell, don’t act on more bullish signals. Great for systems where you only want one position open at a time

6. Bars Since Signal

What it shows: How many bars (candles) have passed since the last Buy or Sell signal.

Why it matters: Gives you context for how long the current condition has persisted

How to use it: If it says 1 or 2, a signal just happened — avoid jumping in late. If it’s been 10+ bars, a new opportunity might be brewing soon. You can use this to time exits if you want to fade a recent signal manually

Indicator Settings:

Short EMA: Sets the short-term EMA period. The smaller the number, the more reactive and more signals you get.

Long EMA: Sets the slow EMA period. The larger this number is, the smoother baseline, and more reliable trend bases are generated.

Z-Score Lookback: The period or bars used for mean & std deviation of spread between short and long EMAs. Larger values result in smoother signals with fewer false positives.

Volatility Window: This value normalizes the spread by historical volatility. This allows you to prevent scale distortion, showing you a cleaner and better chart.

Correlation Lookback: How many periods or how far back to test correlation between slow and long EMAs. This filters out false positives when EMAs lose alignment.

Hurst Lookback: The multiplier to approximate stationarity. Lower leads to more sensitivity to regime change, higher produces a more stricter filtering.

Z Threshold Percentile: This value sets how extreme Z-score must be to trigger a signal. For example, 90 equals only top/bottom 10% of extremes, 80 = more frequent.

Min Bars Between Signals: This hard stop prevents back-to-back signals. The idea is to avoid over-trading or whipsaws in volatile markets even when Hurst lookback and volatility window values are not enough to filter signals.

Some More Recommendations:

We recommend trying different EMA pairs (10/50, 21/100, 5/20) for different asset behaviors. You can set percentile to 85 or 80 if you want more frequent but looser signals. You can also use the Z-score reversion monitor for powerful confirmation.

Tango Rocket velas 1.3Tango Rocket Indicator:

Daily Volatility Range Projection

This indicator identifies the 3 largest-bodied candles from the last N daily bars and calculates a projected price range centered on the current day’s opening price. The projected channel is displayed for the current day and past days, helping visualize potential daily movement and historical volatility patterns.

SuperZweig thrust (<= 30 dias)SuperZweig Thrust (≤ 30-day breadth trigger)

This study tracks the classic Zweig Breadth Thrust pattern, but restricts valid signals to a 30-bar (≈ 30-trading-day) window.

---

What it plots

| Plot | Meaning |

|------|---------|

| **Blue line** – `EMA10` | 10-bar exponential moving average of the _breadth ratio_:`advancing issues / (advancing + declining)` |

| **Red h-line 0.35** | Oversold threshold ( < 0.35 ) |

| **Green h-line 0.64** | Overbought threshold ( > 0.64 ) |

| **Red “×”** | The moment EMA10 crosses **down** through 0.35 |

| **Green “●”** | The moment EMA10 crosses **up** through 0.64 |

| **Green “BUY” label** | Complete Super-Zweig thrust: red × followed by green ● **within 30 daily bars** |

Signal logic

1. **Trigger phase** – when EMA10 drops below 0.35

*Script starts a 30-bar countdown.*

2. **Confirmation phase** – if, while the countdown is active, EMA10 rises above 0.64:

*A single “BUY” label is plotted beneath that bar.*

3. **Expiry** – if 30 bars elapse without the 0.64 cross, the cycle resets; no signal is produced.

4. After any valid “BUY” the cycle also resets, so a new signal requires a fresh cross < 0.35.

Inputs

* **EMA length** – default 10.

* **Advancing / Declining symbols** – default `ADVS` / `DECS` (NYSE issues); can be pointed to any Exchange-specific or custom breadth tickers.

Typical use

Apply on a **daily chart** of a broad index (e.g., S&P; 500).

A printed “BUY” indicates a historically rare surge in market breadth often associated with durable rallies. Combine with other risk-management and trend filters before trading.

Stochastics + CM Williams VixFix (Simple Buy Signal)📈 Stochastics + CM Williams VixFix (Simple Buy Signal)

This indicator combines two powerful tools to detect potential bottoming opportunities:

✅ Stochastics: Looks for momentum reversals. A signal is triggered when both %K and %D are below the oversold threshold (default: 20), suggesting the asset is deeply oversold.

✅ CM Williams Vix Fix: A volatility-based fear detector. When it spikes above its dynamic threshold, it indicates potential panic selling — often preceding a market bounce.

💡 Buy Signal is generated when:

%K and %D are both below 20

VixFix shows a volatility spike (green condition)

Use this script to identify high-probability reversal setups, especially during market corrections or panic phases.

SPY 0DTE Scalper - Auto AlertsTimeframes:

Main chart: 1-minute (for precision entries)

Confirmations: 3-minute or 5-minute (to avoid fakeouts)

Indicators I Use:

VWAP – Orange line → Institutional fair value

EMA 9 – Green line → Short-term momentum

EMA 21 – Red line → Trend filter

Custom Pullback Signal Script – Marks buy/sell/pullback signals with labels (triangles)

Above VWAP = Bullish Bias

Below VWAP = Bearish Bias

Institutions treat this as the "fair price" — so I do too.

EMA 9 (Green):

If price hugs or bounces off EMA 9 = 🔥 strong continuation move.

I use this as my guide for momentum.

EMA 21 (Red):

Great for trend confirmation.

Above EMA 21 = Trend building to the upside.

Below EMA 21 = Weakness or possible reversal.

💸 Step 3: How I Read the Signals

✅ BUY Signal:

Price breaks above VWAP with volume 1.5x+ average

Candle must close strong (not a wickfest)

EMA 9 becomes my trailing stop for the move

🚨 SELL Signal:

Price breaks below VWAP with strong volume

Clean body close below → momentum shift to the downside

EMA 9 again = trailing resistance guide

🔵 Pullback Long (Blue Triangle Under Candle):

Bullish continuation entry

Price pulls back to EMA 9 or 21, but stays above VWAP

Low-risk re-entry after a breakout

🟣 Pullback Short (Purple Triangle Above Candle):

Bearish continuation entry

Price retraces into EMA 9, but stays below VWAP & EMA 21

Ideal for catching second legs after breakdowns

Easy MA SignalsEasy MA Signals

Overview

Easy MA Signals is a versatile Pine Script indicator designed to help traders visualize moving average (MA) trends, generate buy/sell signals based on crossovers or custom price levels, and enhance chart analysis with volume-based candlestick coloring. Built with flexibility in mind, it supports multiple MA types, crossover options, and customizable signal appearances, making it suitable for traders of all levels. Whether you're a day trader, swing trader, or long-term investor, this indicator provides actionable insights while keeping your charts clean and intuitive.

Configure the Settings

The indicator is divided into three input groups for ease of use:

General Settings:

Candlestick Color Scheme: Choose from 10 volume-based color schemes (e.g., Sapphire Pulse, Emerald Spark) to highlight high/low volume candles. Select “None” for TradingView’s default colors.

Moving Average Length: Set the MA period (default: 20). Adjust for faster (lower values) or slower (higher values) signals.

Moving Average Type: Choose between SMA, EMA, or WMA (default: EMA).

Show Buy/Sell Signals: Enable/disable signal plotting (default: enabled).

Moving Average Crossover: Select a crossover type (e.g., MA vs VWAP, MA vs SMA50) for signals or “None” to disable.

Volume Influence: Adjust how volume impacts candlestick colors (default: 1.2). Higher values make thresholds stricter.

Signal Appearance Settings:

Buy/Sell Signal Shape: Choose shapes like triangles, arrows, or labels for signals.

Buy/Sell Signal Position: Place signals above or below bars.

Buy/Sell Signal Color: Customize colors for better visibility (default: green for buy, red for sell).

Custom Price Alerts:

Custom Buy/Sell Alert Price: Set specific price levels for alerts (default: 0, disabled). Enter a non-zero value to enable.

Set Up Alerts

To receive notifications (e.g., sound, popup, email) when signals or custom price levels are hit:

Click the Alert button (alarm clock icon) in TradingView.

Select Easy MA Signals as the condition and choose one of the four alert types:

MA Crossover Buy Alert: Triggers on MA crossover buy signals.

MA Crossover Sell Alert: Triggers on MA crossover sell signals.

Custom Buy Alert: Triggers when price crosses above the custom buy price.

Custom Sell Alert: Triggers when price crosses below the custom sell price.

Enable Play Sound and select a sound (e.g., “Bell”).

Set the frequency (e.g., Once Per Bar Close for confirmed signals) and create the alert.

Analyze the Chart

Moving Average Line: Displays the selected MA with color changes (green for bullish, red for bearish, gray for neutral) based on price position relative to the MA.

Buy/Sell Signals: Appear as shapes or labels when crossovers or custom price levels are hit.

Candlestick Colors: If a color scheme is selected, candles change color based on volume strength (high, low, or neutral), aiding in trend confirmation.

Why Use Easy MA Signals?

Easy MA Signals is designed to simplify technical analysis while offering advanced customization. It’s ideal for traders who want:

A clear visualization of MA trends and crossovers.

Flexible signal generation based on MA crossovers or custom price levels.

Volume-enhanced candlestick coloring to identify market strength.

Easy-to-use settings with tooltips for beginners and pros alike.

This script is particularly valuable because it combines multiple features into one indicator, reducing chart clutter and providing actionable insights without overwhelming the user.

Benefits of Easy MA Signals

Highly Customizable: Supports SMA, EMA, and WMA with adjustable lengths.

Offers multiple crossover options (VWAP, SMA10, SMA20, etc.) for tailored strategies.

Custom price alerts allow precise targeting of key levels.

Volume-Based Candlestick Coloring: 10 unique color schemes highlight volume strength, helping traders confirm trends.

Adjustable volume influence ensures adaptability to different markets.

Flexible Signal Visualization: Choose from various signal shapes (triangles, arrows, labels) and positions (above/below bars).

Customizable colors improve visibility on any chart background.

Alert Integration: Built-in alert conditions for crossovers and custom prices support sound, email, and app notifications.

Easy setup for real-time trading decisions.

User-Friendly Design: Organized input groups with clear tooltips make configuration intuitive.

Suitable for beginners and advanced traders alike.

Example Use Cases

Swing Trading with MA Crossovers:

Scenario: A trader wants to trade Bitcoin (BTC/USD) on a 4-hour chart using an EMA crossover strategy.

Setup:

Set Moving Average Type to EMA, Length to 20.

Set Moving Average Crossover to “MA vs SMA50”.

Enable Show Buy/Sell Signals and choose “arrowup” for buy, “arrowdown” for sell.

Select “Emerald Spark” for candlestick colors to highlight volume surges.

Usage: Buy when the EMA20 crosses above the SMA50 (green arrow appears) and volume is high (dark green candles). Sell when the EMA20 crosses below the SMA50 (red arrow). Set alerts for real-time notifications.

Scalping with Custom Price Alerts:

Scenario: A day trader monitors Tesla (TSLA) on a 5-minute chart and wants alerts at specific support/resistance levels.

Setup:

Set Custom Buy Alert Price to 150.00 (support) and Custom Sell Alert Price to 160.00 (resistance).

Use “labelup” for buy signals and “labeldown” for sell signals.

Keep Moving Average Crossover as “None” to focus on price alerts.

Usage: Receive a sound alert and label when TSLA crosses 150.00 (buy) or 160.00 (sell). Use volume-colored candles to confirm momentum before entering trades.

When NOT to Use Easy MA Signals

High-Frequency Trading: Reason: The indicator relies on moving averages and volume, which may lag in ultra-fast markets (e.g., sub-second trades). High-frequency traders may need specialized tools with real-time tick data.

Alternative: Use order book or market depth indicators for faster execution.

Low-Volatility or Sideways Markets:

Reason: MA crossovers and custom price alerts can generate false signals in choppy, range-bound markets, leading to whipsaws.

Alternative: Use oscillators like RSI or Bollinger Bands to trade within ranges.

This indicator is tailored more towards less experienced traders. And as always, paper trade until you are comfortable with how this works if you're unfamiliar with trading! We hope you enjoy this and have great success. Thanks for your interested in Easy MA Signals!

Polygot Moving AveragesDescription

This is essentially a source merger of Bollinger Bands by Trading View and Simple Moving Averages by stoxxinbox. My additions and subtractions are minimal. There is the BB MA, which I default at 5d, and the other 4 averages are the standard 21, 50, 100, 200, day moving averages. I default the averaging method to WMA (Weighted Moving Average). The method of averaging can be changed as also can the lengths of the inputs to match user preferences. This is what I wanted for an indicator and didn't find.

Usage

The same as you would use any other BB or MA indicator. The benefit of this one is that it has 4 MAs, one MA with the Bollinger Bands attached, and the colours adjusted to be easy on the eyes when using high contrast themes, to be discernible yet sit quietly in the background with lines and candle sticks everywhere shouting for attention. I use it as a base first indicator which I can hide easily (imagine hiding five MA indicators individually constantly) when the more serious indicators come into play.

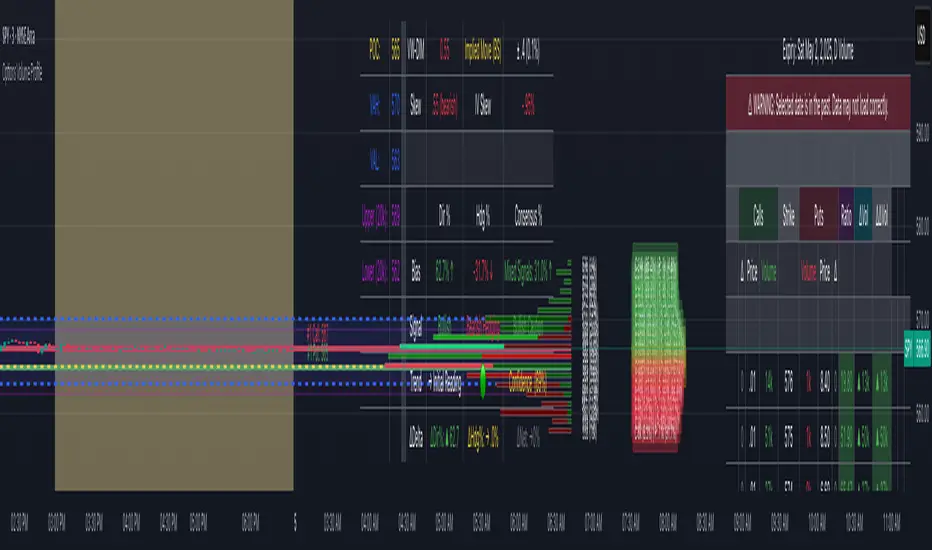

Options Volume ProfileOptions Volume Profile

Introduction

Unlock institutional-level options analysis directly on your charts with Options Volume Profile - a powerful tool designed to visualize and analyze options market activity with precision and clarity. This indicator bridges the gap between technical price action and options flow, giving you a comprehensive view of market sentiment through the lens of options activity.

What Is Options Volume Profile?

Options Volume Profile is an advanced indicator that analyzes call and put option volumes across multiple strikes for any symbol and expiration date available on TradingView. It provides a real-time visual representation of where money is flowing in the options market, helping identify potential support/resistance levels, market sentiment, and possible price targets.

Key Features

Comprehensive Options Data Visualization

Dynamic strike-by-strike volume profile displayed directly on your chart

Real-time tracking of call and put volumes with custom visual styling

Clear display of important value areas including POC (Point of Control)

Value Area High/Low visualization with customizable line styles and colors

BK Daily Range Identification

Secondary lines marking significant volume thresholds

Visual identification of key strike prices with substantial options activity

Value Area Cloud Visualization

Configurable cloud overlays for value areas

Enhanced visual identification of high-volume price zones

Detailed Summary Table

Complete breakdown of call and put volumes per strike

Percentage analysis of call vs put activity for sentiment analysis

Color-coded volume data for instant pattern recognition

Price data for both calls and puts at each strike

Custom Strike Selection

Configure strikes above and below ATM (At The Money)

Flexible strike spacing and rounding options

Custom base symbol support for various options markets

Use Cases

1. Identifying Key Support & Resistance

Visualize where major options activity is concentrated to spot potential support and resistance zones. The POC and Value Area lines often act as magnets for price.

2. Analyzing Market Sentiment

Compare call versus put volume distribution to gauge directional bias. Heavy call volume suggests bullish sentiment, while heavy put volume indicates bearish positioning.

3. Planning Around Institutional Activity

Volume profile analysis reveals where professional traders are positioning themselves, allowing you to align with or trade against smart money.

4. Setting Precise Targets

Use the POC and Value Area High/Low lines as potential profit targets when planning your trades.

5. Spotting Unusual Options Activity

The color-coded volume table instantly highlights anomalies in options flow that may signal upcoming price movements.

Customization Options

The indicator offers extensive customization capabilities:

Symbol & Data Settings : Configure base symbol and data aggregation

Strike Selection : Define number of strikes above/below ATM

Expiration Date Settings : Set specific expiry dates for analysis

Strike Configuration : Customize strike spacing and rounding

Profile Visualization : Adjust offset, width, opacity, and height

Labels & Line Styles : Fully configurable text and visual elements

Value Area Settings : Customize POC and Value Area visualization

Secondary Line Settings : Configure the BK Daily Range appearance

Cloud Visualization : Add colored overlays for enhanced visibility

How to Use

Apply the indicator to your chart

Configure the expiration date to match your trading timeframe

Adjust strike selection and spacing to match your instrument

Use the volume profile and summary table to identify key levels

Trade with confidence knowing where the real money is positioned

Perfect for options traders, futures traders, and anyone who wants to incorporate institutional-level options analysis into their trading strategy.

Take your trading to the next level with Options Volume Profile - where price meets institutional positioning.

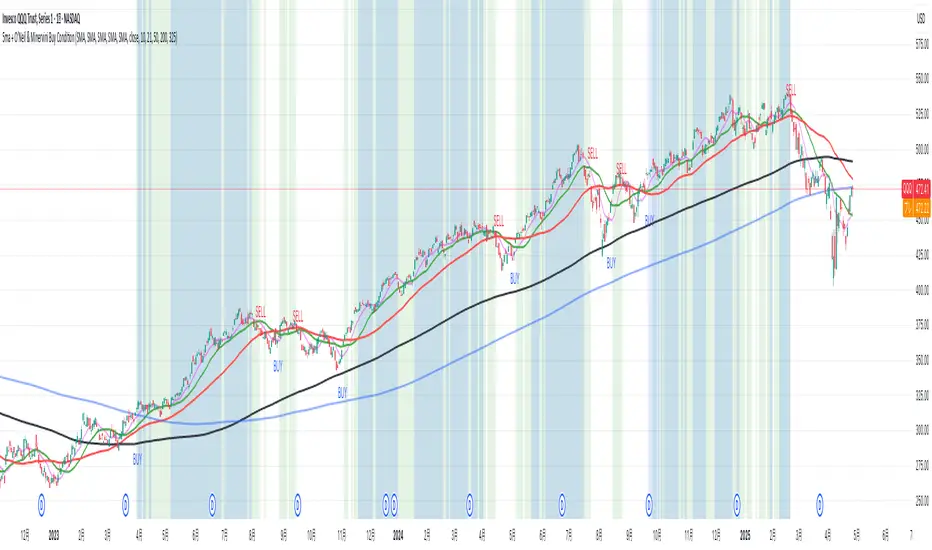

5ma + O’Neil & Minervini Buy ConditionIndicator Overview

5ma + O’Neil & Minervini Buy Condition is an original TradingView indicator that extends beyond a simple collection of standard moving averages by offering:

- Five Fully Independent Lines : Each of MA1–MA5 can be configured as SMA, EMA, WMA, or VWMA with its own period and data source. This level of customization unlocks unique combinations no existing script provides.

- Synergy of Multiple Timeframes : Default settings (10, 21, 50, 200, 325) reflect ultra‑short, short, medium, long, and volume‑weighted long‑term perspectives. The layered structure functions as a multi‑filter, sharpening entry signals and trend confirmation beyond any single MA.

- Integrated Buy Conditions : Built‑in O’Neil and Minervini buy filters use fixed SMA‑based rules (50 & 200 SMA rising within 15% of 52‑week high; 10 > 21 > 50 SMA rising within high/low thresholds), plus a combined condition highlighting when both methods align.

- Clean Visualization & Style Controls : Background coloring for each buy condition appears only in the Style tab under clearly named parameters (O’Neil Buy Condition, Minervini Buy Condition, Both Conditions). MA lines support transparent default colors and customizable line width for optimal readability without clutter.

Calculation & Logic

SMA: (P₁ + P₂ + … + Pₙ) ÷ N

EMA: α = 2 ÷ (N + 1)

EMA_today = (Price_today – EMA_yesterday) × α + EMA_yesterday

WMA: (P₁×N + P₂×(N–1) + … + Pₙ×1) ÷

VWMA: Σ(Pᵢ×Vᵢ) ÷ Σ(Vᵢ) for i = 1…N

```

Buy Condition Logic

- O’Neil: Price > 50 SMA & 200 SMA (both rising) **and** within 15% of the 52‑week high.

- Minervini : 10 SMA > 21 SMA > 50 SMA (both short‑term SMAs rising) **and** within 25% of the 52‑week high **and** at least 25% above the 52‑week low.

- Combined : Both O’Neil and Minervini conditions true.

Usage Examples

1. Short‑Mid Cross : Observe MA1/MA2 crossover while MA3/MA4 confirm trend strength.

2. Volume‑Weighted Long‑Term : Use VWMA as MA5 to filter institutional‑strength pullbacks.

3. Multi‑Filter Entry : Look for purple background (Both Conditions) on daily chart as high‑confidence entry.

Why It’s Unique

- Not a Mash‑Up : Though built on standard MA formulas, the customizable layering and built‑in buy filters create a novel multi‑dimensional analysis tool.

- Trader‑Friendly : Detailed comments in the code explain parameter choices, calculation methods, and practical entry scenarios so that even Pine novices can understand the underlying mechanics.

- Publication‑Ready : Description and code demonstrate originality, add clear value, and comply with house‑rule requirements by explaining why and how components interact, not just listing features.

- Combined Custom MA & Buy Conditions : By integrating customizable moving averages with built-in buy filters, users can easily recognize O’Neil and Minervini recommended setups.

Midnight (Daily) OpenMidnight (Daily) Open v1.0

Overview

Plots a real‑time horizontal line at the U.S. session “midnight” open (i.e. the daily candle’s open price) on any intraday chart. Optionally displays a label with the exact price, making it easy to see how price reacts to the session open.

Key Benefits

Immediate Context: See at a glance where today’s session began, helping identify support/resistance.

Consistent Reference: Works on any symbol or intraday timeframe.

Customizable Styling: Tweak colors, line thickness, and label appearance to match your chart theme.

Features

Retrieves the daily open via request.security() (Pine v6).

Draws or updates a single horizontal line that extends into the future.

Optional price label on the last bar, with user‑defined text and background colors.

Zero repainting—always shows the true daily open.

Moving Average Trend ToolsI. How M.A.T.T. Adds Value to the TradingView Community:

The "Moving Average Trend Tools" (M.A.T.T.) is a versatile Pine Script v6 indicator that empowers traders with clear trend analysis, reliable trade signals, and real-time insights. Its intuitive design and robust features make it a valuable addition to the TradingView Community Scripts by catering to traders of all levels. Here’s why it stands out:

Clear Trend Visualization: M.A.T.T. plots a moving average (MA) with dynamic coloring—green for rising, red for falling, and gray for flat—based on a user-defined lookback period. This simplifies trend interpretation, helping traders quickly assess market momentum.

Reliable Trade Signals : The script identifies price crossovers above or below the MA, plotting green circles for bullish crosses and red for bearish, confirmed on closed bars to prevent repainting. These signals guide entry and exit points for trend-following or reversal strategies.

Real-Time Extension Detection : M.A.T.T. calculates percentage price deviations from the MA, displaying real-time labels when thresholds (e.g., 6%) are exceeded. This highlights overextended moves, ideal for spotting reversals or pullbacks, with alerts to keep traders informed.

Extensive Customization : Traders can tailor the MA type (SMA, EMA, WMA, HMA), length, colors, line width, and label sizes. This flexibility supports diverse strategies across markets like stocks, forex, and crypto, from scalping to swing trading.

Automated Alerts : Alert conditions for crossovers and extensions integrate seamlessly with TradingView’s system, enabling traders to stay updated without constant chart monitoring.

M.A.T.T. combines trend analysis, signal generation, and overextension detection into a single, user-friendly tool. Its accessibility, reliability, and educational value for Pine Script learners make it a compelling contribution to the community.

II. What M.A.T.T. Does, How It Works, and Its Originality:

What It Does :

M.A.T.T. enhances trend analysis and trade decision-making through three core features:

Dynamic MA Visualization: Plots a customizable MA (SMA, EMA, WMA, or HMA) with trend-based coloring to reflect rising, falling, or flat market conditions.

Price Crossover Signals : Marks bullish (green circles) and bearish (red circles) crossovers, confirmed on closed bars, with alerts for trade opportunities.

Price Extension Labels : Displays real-time percentage deviations of price from the MA, with alerts when user-defined thresholds are breached, signaling potential reversals.

How It Works :

M.A.T.T. leverages Pine Script v6 for precise calculations and user-friendly outputs:

Inputs: Users select MA type, length, lookback period, colors, and thresholds for extensions, plus label styles and sizes for customization.

MA Calculation : A switch function computes the chosen MA (e.g., ta.ema(close, 21) for EMA). Trend direction is determined using ta.rising or ta.falling over the lookback period, coloring the MA accordingly.

Crossover Logic : Bullish crossovers (close > ma and close < ma ) and bearish crossovers (close < ma and close > ma ) are plotted as circles on confirmed bars (barstate.isconfirmed) to ensure reliability. Alerts trigger only on the first bar of a crossover.

Extension Logic : Percentage deviations are calculated as ((price - ma) / ma) * 100, using the high for above-MA extensions and low for below. Labels appear in real-time when thresholds are exceeded, with alerts on transitions to avoid noise.

Why It’s Original

M.A.T.T. distinguishes itself through a unique blend of features and thoughtful design:

All-in-One Design : It integrates dynamic MA coloring, non-repainting crossover signals, and real-time extension detection, addressing trend identification, trade signals, and overextension warnings in one tool—unlike most MA indicators that focus on a single aspect.

Real-Time Extension Labels : Displaying percentage deviations with customizable thresholds is a rare feature, ideal for volatile markets and not commonly found in standard scripts.

Non-Repainting Signals : Confirmed crossover signals enhance reliability for live trading, setting M.A.T.T. apart from less rigorous indicators.

Optimized Alert Condtions : Alerts trigger only on transitions (e.g., first bar of a crossover or extension), reducing noise and improving usability.

Visual and Functional Flexibility : Support for four MA types, extensive customization, and a clean interface (dynamic colors, tiny circles, clear labels) make it adaptable and user-friendly.

While MA plotting or crossovers exist elsewhere, M.A.T.T.’s seamless integration, real-time extension detection, alert conditions, and focus on reliability and customization create a distinctive, practical tool. Its balance of simplicity and sophistication makes it a unique asset for the TradingView community.

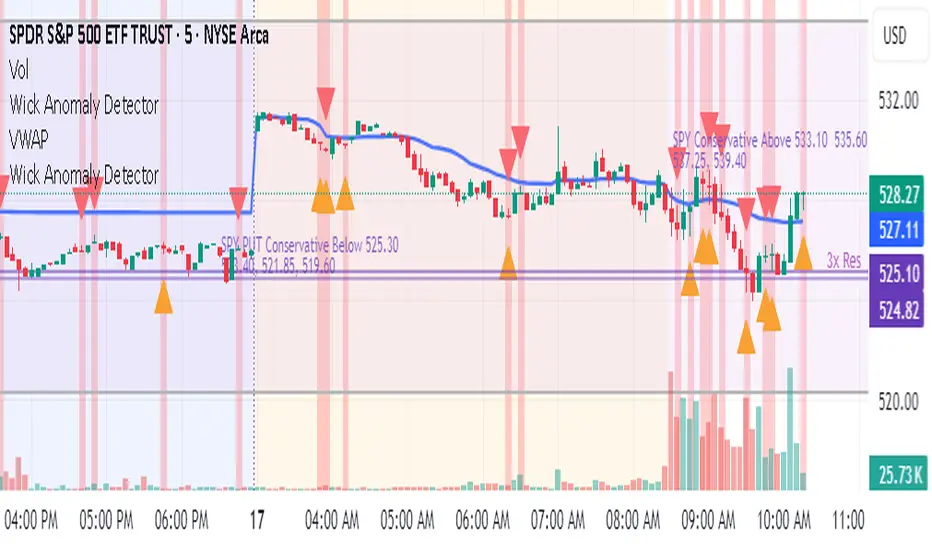

Wick Anomaly DetectorWick Anomaly Detector

This script helps identify candles with unusually large wicks compared to their body size — a common sign of price anomalies, false prints, or low-liquidity moves.

🔍 What it does:

Flags candles with upper or lower wicks that exceed a user-defined ratio (default: 3x the body size)

Helps traders spot suspicious spikes or “bad ticks,” especially in pre-market or illiquid stocks

📈 Use it to:

Avoid fake breakouts

Confirm real price action

Clean up your technical analysis

Customize the wick-to-body threshold as needed. Add volume filters or time filters for more precision.

Created for educational purposes — use with proper risk management!

TASC 2025.05 Trading The Channel█ OVERVIEW

This script implements channel-based trading strategies based on the concepts explained by Perry J. Kaufman in the article "A Test Of Three Approaches: Trading The Channel" from the May 2025 edition of TASC's Traders' Tips . The script explores three distinct trading methods for equities and futures using information from a linear regression channel. Each rule set corresponds to different market behaviors, offering flexibility for trend-following, breakout, and mean-reversion trading styles.

█ CONCEPTS

Linear regression

Linear regression is a model that estimates the relationship between a dependent variable and one or more independent variables by fitting a straight line to the observed data. In the context of financial time series, traders often use linear regression to estimate trends in price movements over time.

The slope of the linear regression line indicates the strength and direction of the price trend. For example, a larger positive slope indicates a stronger upward trend, and a larger negative slope indicates the opposite. Traders can look for shifts in the direction of a linear regression slope to identify potential trend trading signals, and they can analyze the magnitude of the slope to support trading decisions.

One caveat to linear regression is that most financial time series data does not follow a straight line, meaning a regression line cannot perfectly describe the relationships between values. Prices typically fluctuate around a regression line to some degree. As such, analysts often project ranges above and below regression lines, creating channels to model the expected extent of the data's variability. This strategy constructs a channel based on the method used in Kaufman's article. It measures the maximum distances from points on the linear regression line to historical price values, then adds those distances and the current slope to the regression points.

Depending on the trading style, traders might look for prices to move outside an established channel for breakout signals, or they might look for price action to reach extremes within the channel for potential mean reversion opportunities.

█ STRATEGY CALCULATIONS

Primary trade rules

This strategy implements three distinct sets of rules for trend, breakout, and mean-reversion trades based on the methods Kaufman describes in his article:

Trade the trend (Rule 1) : Open new positions when the sign of the slope changes, indicating a potential trend reversal. Close short trades and enter a long trade when the slope changes from negative to positive, and do the opposite when the slope changes from positive to negative.

Trade channel breakouts (Rule 2) : Open new positions when prices cross outside the linear regression channel for the current sample. Close short trades and enter a long trade when the price moves above the channel, and do the opposite when the price moves below the channel.

Trade within the channel (Rule 3) : Open new positions based on price values within the channel's range. Close short trades and enter a long trade when the price is near the channel's low, within a specified percentage of the channel's range, and do the opposite when the price is near the channel's high. With this rule, users can also filter the trades based on the channel's slope. When the filter is active, long positions are allowed only when the slope is positive, and short positions are allowed only when it is negative.

Position sizing

Kaufman's strategy uses specific trade sizes for equities and futures markets:

For an equities symbol, the number of shares traded is $10,000 divided by the current price.

For a futures symbol, the number of contracts traded is based on a volatility-adjusted formula that divides $25,000 by the product of the 20-bar average true range and the instrument's point value.

By default, this script automatically uses these sizes for its trade simulation on equities and futures symbols and does not simulate trading on other symbols. However, users can control position sizes from the "Settings/Properties" tab and enable trade simulation on other symbol types by selecting the "Manual" option in the script's "Position sizing" input.

Stop-loss

This strategy includes the option to place an accompanying stop-loss order for each trade, which users can enable from the "SL %" input in the "Settings/Inputs" tab. When enabled, the strategy places a stop-loss order at a specified percentage distance from the closing price where the entry order occurs, allowing users to compare how the strategy performs with added loss protection.

█ USAGE

This strategy adapts its display logic for the three trading approaches based on the rule selected in the "Trade rule" input:

For all rules, the script plots the linear regression slope in a separate pane. The plot is color-coded to indicate whether the current slope is positive or negative.

When the selected rule is "Trade the trend", the script plots triangles in the separate pane to indicate when the slope's direction changes from positive to negative or vice versa. Additionally, it plots a color-coded SMA on the main chart pane, allowing visual comparison of the slope to directional changes in a moving average.

When the rule is "Trade channel breakouts" or "Trade within the channel", the script draws the current period's linear regression channel on the main chart pane, and it plots bands representing the history of the channel values from the specified start time onward.

When the rule is "Trade within the channel", the script plots overbought and oversold zones between the bands based on a user-specified percentage of the channel range to indicate the value ranges where new trades are allowed.

Users can customize the strategy's calculations with the following additional inputs in the "Settings/Inputs" tab:

Start date : Sets the date and time when the strategy begins simulating trades. The script marks the specified point on the chart with a gray vertical line. The plots for rules 2 and 3 display the bands and trading zones from this point onward.

Period : Specifies the number of bars in the linear regression channel calculation. The default is 40.

Linreg source : Specifies the source series from which to calculate the linear regression values. The default is "close".

Range source : Specifies whether the script uses the distances from the linear regression line to closing prices or high and low prices to determine the channel's upper and lower ranges for rules 2 and 3. The default is "close".

Zone % : The percentage of the channel's overall range to use for trading zones with rule 3. The default is 20, meaning the width of the upper and lower zones is 20% of the range.

SL% : If the checkbox is selected, the strategy adds a stop-loss to each trade at the specified percentage distance away from the closing price where the entry order occurs. The checkbox is deselected by default, and the default percentage value is 5.

Position sizing : Determines whether the strategy uses Kaufman's predefined trade sizes ("Auto") or allows user-defined sizes from the "Settings/Properties" tab ("Manual"). The default is "Auto".

Long trades only : If selected, the strategy does not allow short positions. It is deselected by default.

Trend filter : If selected, the strategy filters positions for rule 3 based on the linear regression slope, allowing long positions only when the slope is positive and short positions only when the slope is negative. It is deselected by default.

NOTE: Because of this strategy's trading rules, the simulated results for a specific symbol or channel configuration might have significantly fewer than 100 trades. For meaningful results, we recommend adjusting the start date and other parameters to achieve a reasonable number of closed trades for analysis.

Additionally, this strategy does not specify commission and slippage amounts by default, because these values can vary across market types. Therefore, we recommend setting realistic values for these properties in the "Cost simulation" section of the "Settings/Properties" tab.

Fractal Wave MarkerFractal Wave Marker is an indicator that processes relative extremes of fluctuating prices within 2 periodical aspects. The special labeling system detects and visually marks multi-scale turning points, letting you visualize fractal echoes within unfolding cycles dynamically.

What This Indicator Does

Identifies major and minor swing highs/lows based on adjustable period.

Uses Phi in power exponent to compute a higher-degree swing filter.

Labels of higher degree appear only after confirmed base swings — no phantom levels, no hindsight bias. What you see is what the market has validated.

Swing points unfold in a structured, alternating rhythm . No two consecutive pivots share the same hierarchical degree!

Inspired by the Fractal Market Hypothesis, this script visualizes the principle that market behavior repeats across time scales, revealing structured narrative of "random walk". This inherent sequencing ensures fractal consistency across timeframes. "Fractal echoes" demonstrate how smaller price swings can proportionally mirror larger ones in both structure and timing, allowing traders to anticipate movements by recursive patterns. Cycle Transitions highlight critical inflection points where minor pivots flip polarity such as a series of lower highs progress into higher highs—signaling the birth of a new macro trend. A dense dense clusters of swing points can indicate Liquidity Zones, acting as footprints of institutional accumulation or distribution where price action validates supply and demand imbalances.

Visualization of nested cycles within macro trend anchors - a main feature specifically designed for the chartists who prioritize working with complex wave oscillations their analysis.

FeraTrading Relative Volume IndicatorThis FeraTrading Relative Volume Indicator measures relative volume pressure by comparing buying and selling activity, smoothed using a configurable average. It helps traders identify volume-driven momentum shifts, offering dynamic buy and sell signals based on weighted pressure values.

Key Features:

📈 Relative Volume (RV) Line: Measures net buying/selling pressure using volume-weighted price action.

🟢 Buy Signals: Triggered when RV crosses above a smoothed moving average (SMA 1).

🔴 Sell Signals (optional): Triggered when RV crosses below a separate SMA (SMA 2).

🔍 Customizable Inputs: Adjust smoothing length, weight, and signal sensitivity.

🕯️ Weighted Candles (optional): Visualizes custom OHLC based on volume-weighted volatility.

📊 Two SMAs: Use separate or combined moving averages to analyze trends in pressure.

🎨 Flexible Styling: Customize line and signal colors to match your chart setup.

Use Cases:

Spotting accumulation/distribution phases

Timing entries during volume surges

Confirming breakout momentum with underlying volume pressure

This indicator was developed by FeraTrading to visualize relative volume pressure.

Buffett Indicator (Wilshire 5000 / GDP)The Buffett Indicator (Wilshire 5000 / GDP) is a macroeconomic metric used to assess whether the U.S. stock market is overvalued or undervalued. It is calculated by dividing the total market capitalization (represented by the Wilshire 5000 Index) by the U.S. Gross Domestic Product (GDP). A value above 1 (or 100%) may indicate an overvalued market, while a value below 1 suggests potential undervaluation. This indicator is best suited for long-term investment analysis.

RSI in pane and 3 EMAs on chartCustom RSI in Pane + 3 EMAs on Chart — with Optional RSI Divergence Detection

Combines RSI in a separate pane with 3 EMAs on the chart and optional RSI-based divergence detection. Useful for analyzing both momentum and trend structure.

Features

RSI Pane

Custom RSI calculation (not built-in ta.rsi) with adjustable source and length

Overlay optional moving average (SMA, EMA, SMMA/RMA, WMA, VWMA, or Bollinger Bands) Overbought/oversold gradient fill for visual clarity (70 / 30 zones)

Midline (50) for neutral RSI territory

RSI Divergence Detection

Optional: toggle on/off with one input

Regular Bullish Divergence : Price makes a lower low, RSI makes a higher low

Regular Bearish Divergence : Price makes a higher high, RSI makes a lower high

Customizable lookback for pivot detection

Visual markers and labels plotted on RSI

Built-in alert conditions for both divergence types

3 EMA Trend Indicators on Price Chart

Three customizable EMAs (default: 20, 50, 200)

Color-coded and clearly plotted on main chart

Use to determine short/mid/long-term trend bias

No repainting or smoothing artifacts

Why use this script?

Gives a full view of trend + momentum without cluttering the main price chart, and it helps confirm entries and exits by observing RSI behavior alongside EMAs. The optional divergence detection can act as a signal for potential exhaustion or reversal (not entry signals on their own). It is a Good fit for traders who use RSI zones, divergences, and EMA structure in their decision-making, both for intra-day and swing trades (where it performs best).

How to use

Add this script to your chart. EMAs will appear on the main price chart; RSI and divergence will appear in a separate pane.

Adjust RSI and MA settings to fit your trading style (e.g., fast RSI for scalping, slower for swing)

Enable "Show Divergence" if you want visual alerts and markers

Use alerts to get notified when a divergence occurs without watching the chart

Always check the divergences on different time frames to validate the setup, and do not consider them valid on small time frames (<15 minutes).

Built for traders who want both momentum and trend context in a single tool — without clutter, repainting, or noise. I created this script to streamline my own analysis and avoid switching between multiple indicators. It's not meant to be a "signal generator" but a visual assistant for making better decisions. If you find it useful or have feedback, feel free to reach out.

Scalper's Fractal Cloud with RSI + VWAP + MACD (Fixed)Scalper’s Fractal Confluence Dashboard

1. Purpose of the Indicator

This TradingView indicator script provides a high-confluence setup for scalping and day trading. It blends momentum indicators (RSI, MACD), trend bias tools (EMA Cloud, VWAP), and structure (fractal swings, gap zones) to help confirm precise entries and exits.

2. Components of the Indicator

- EMA Cloud (50 & 200 EMA): Trend bias – green means bullish, red means bearish. Avoid longs under red cloud.

- VWAP: Institutional volume anchor. Ideal entries are pullbacks to VWAP in direction of trend.

- Gap Zones: Shows open-air zones (white space) where price can move fast. Used to anticipate momentum moves.

- ZigZag Swings: Marks structural pivots (highs/lows) – useful for stop placement and range anticipation.

- MACD Histogram: Shows bullish or bearish momentum via background color.

- RSI: Overbought (>70) or oversold (<30) warnings. Good for exits or countertrend reversion plays.

- EMA Spread Label: Quick view of momentum strength. Wide spread = strong trend.

3. Scalping Entry Checklist

Before entering a trade, confirm these conditions:

• • Bias: EMA cloud color supports trade direction

• • Price is above/below VWAP (confirming institutional flow)

• • MACD histogram matches direction (green for long, red for short)

• • RSI not at extreme (unless you’re fading trend)

• • If entering gap zone, expect fast move

• • Recent swing high/low nearby for target or stop

4. Risk & Sizing Guidelines

Risk 1–2% of account per trade. Place stop below recent swing low (for longs) or high (for shorts). Use fractional sizing near VWAP or white space zones for scalping reversals.

5. Daily Trade Journal Template

- Date:

- Ticker:

- Setup Type (VWAP pullback, Gap Break, EMA reversion):

- Entry Time:

- Bias (Green/Red Cloud):

- RSI Level / MACD Reading:

- Stop Loss:

- Target:

- Result (P/L):

- What I Did Well:

- What Needs Work:

Webby's Market OrderThis is visual representation of Webby's Market Order.

When three consecutive lows are above 21 EMA, Uptrend expectation is natural.

When three highs are below 21 EMA, Downtrend expectation is natural.

Alert Conditions can be set when uptrend and down trend are expected.

Use this indicator with IXIC or SPY or major indices.

This is set at three lows/Highs above 21 EMA as looked by Mike Webster.

FT-RSISummary of the Custom RSI Indicator Script (For Futu Niuniu Platform):

This Pine Script code implements a triple-period RSI indicator with horizontal reference lines (70, 50, 30) for technical analysis on the Futu Niuniu trading platform.

Key Features:

Multi-period RSI Calculation:

Computes three RSI values using 9, 14, and 22-period lengths to capture short-term, standard, and smoothed momentum signals.

Utilizes the Relative Moving Average (RMA) method for RSI calculation (ta.rma function).

Horizontal Reference Bands:

Upper Band (70): Red dotted line (semi-transparent) to identify overbought conditions.

Middle Band (50): Green dotted line as the neutral equilibrium level.

Lower Band (30): Blue dotted line (semi-transparent) to highlight oversold zones.

Visual Customization:

Distinct colors for each RSI line:

RSI (9): Orange (#F79A00)

RSI (14): Green (#49B50D)

RSI (22): Blue (#5188FF)

All lines have a thickness of 2 pixels for clear visibility.

Platform Compatibility:

This script is designed for Futu Niuniu’s charting system, leveraging Pine Script syntax adaptations supported by the platform. The horizontal bands and multi-period RSI logic help traders analyze trend strength and potential reversal points efficiently.

Note: Ensure Futu Niuniu’s scripting environment supports ta.rma and hline functions for proper execution.

StonkGame Major Market Open/ClosePlots vertical lines for Tokyo, London, and New York session opens and closes — auto-adjusted to your chart's timezone.

Open lines = lighter, dashed style.

Close lines = solid, full-color style.

Helps identify key liquidity windows, session-driven volatility, and clean market structure — without chart clutter.

Fully customizable colors and line styles for a professional, minimal look.