ATT Model with Buy/Sell SignalsIndicator Summary

This indicator is based on the ATT (Arithmetic Time Theory) model, using specific turning points derived from the ATT sequence (3, 11, 17, 29, 41, 47, 53, 59) to identify potential market reversals. It also integrates the RSI (Relative Strength Index) to confirm overbought and oversold conditions, triggering buy and sell signals when conditions align with the ATT sequence and RSI level.

Turning Points: Detected based on the ATT sequence applied to bar count. This suggests high-probability areas where the market could turn.

RSI Filter: Adds strength to the signals by ensuring buy signals occur when RSI is oversold (<30) and sell signals when RSI is overbought (>70).

Max Signals Per Session: Limits signals to two per session to reduce over-trading.

Entry Criteria

Buy Signal: Enter a buy trade if:

The indicator displays a green "BUY" marker.

RSI is below the oversold level (default <30), suggesting a potential upward reversal.

Sell Signal: Enter a sell trade if:

The indicator displays a red "SELL" marker.

RSI is above the overbought level (default >70), indicating a potential downward reversal.

Exit Criteria

Take Profit (TP):

Define TP as a fixed percentage or point value based on the asset's volatility. For example, set TP at 1.5-2x the risk, or a predefined point target (like 50-100 points).

Alternatively, exit the position when price approaches a key support/resistance level or the next significant swing high/low.

Stop Loss (SL):

Place the SL below the recent low (for buys) or above the recent high (for sells).

Set a fixed SL in points or percentage based on the asset’s average movement range, like an ATR-based stop, or limit it to a specific risk amount per trade (1-2% of account).

Trailing into Profit

Use a trailing strategy to lock in profits and let winning trades run further. Two main options:

ATR Trailing Stop:

Set the trailing stop based on the ATR (Average True Range), adjusting every time a new candle closes. This can help in volatile markets by keeping the stop at a consistent distance based on recent price movement.

Break-Even and Partial Profits:

When the price moves in your favor by a set amount (e.g., 1:1 risk/reward), move SL to the entry (break-even).

Take partial profit at intermediate levels (e.g., 50% at 1:1 RR) and trail the remainder.

Risk Management for Prop Firm Evaluation

Prop firms often have strict rules on daily loss limits, max drawdowns, and minimum profit targets. Here’s how to align your strategy with these:

Limit Risk per Trade:

Keep risk per trade to a conservative level (e.g., 1% or lower of your account balance). This allows for more room in case of a drawdown and aligns with most prop firm requirements.

Daily Loss Limits:

Set a daily stop-loss that ensures you don’t exceed the firm’s rules. For example, if the daily limit is 5%, stop trading once you reach a 3-4% drawdown.

Avoid Over-Trading:

Stick to the max signals per session rule (one or two trades). Taking only high-probability setups reduces emotional and reactive trades, preserving capital.

Stick to a Profit Target:

Aim to meet the evaluation’s profit goal efficiently but avoid risky or oversized trades to reach it faster.

Avoid Major Economic Events:

News events can disrupt technical setups. Avoid trading around significant releases (like FOMC or NFP) to reduce the chance of sudden losses due to high volatility.

Summary

Using this strategy with discipline, a structured entry/exit approach, and tight risk management can maximize your chances of passing a prop firm evaluation. The ATT model’s turning points, combined with the RSI, provide an edge by highlighting reversal zones, while limiting trades to 1-2 per session helps maintain controlled risk.

Cari dalam skrip untuk "17个交易日涨幅第一的股票(非新股)有哪些"

Pulse DPO: Major Cycle Tops and Bottoms█ OVERVIEW

Pulse DPO is an oscillator designed to highlight Major Cycle Tops and Bottoms .

It works on any market driven by cycles. It operates by removing the short-term noise from the price action and focuses on the market's cyclical nature.

This indicator uses a Normalized version of the Detrended Price Oscillator (DPO) on a 0-100 scale, making it easier to identify major tops and bottoms.

Credit: The DPO was first developed by William Blau in 1991.

█ HOW TO READ IT

Pulse DPO oscillates in the range between 0 and 100. A value in the upper section signals an OverBought (OB) condition, while a value in the lower section signals an OverSold (OS) condition.

Generally, the triggering of OB and OS conditions don't necessarily translate into swing tops and bottoms, but rather suggest caution on approaching a market that might be overextended.

Nevertheless, this indicator has been customized to trigger the signal only during remarkable top and bottom events.

I suggest using it on the Daily Time Frame , but you're free to experiment with this indicator on other time frames.

The indicator has Built-in Alerts to signal the crossing of the Thresholds. Please don't act on an isolated signal, but rather integrate it to work in conjunction with the indicators present in your Trading Plan.

█ OB SIGNAL ON: ENTERING OVERBOUGHT CONDITION

When Pulse DPO crosses Above the Top Threshold it Triggers ON the OB signal. At this point the oscillator line shifts to OB color.

When Pulse DPO enters the OB Zone, please beware! In this Area the Major Players usually become Active Sellers to the Public. While the OB signal is On, it might be wise to Consider Selling a portion or the whole Long Position.

Please note that even though this indicator aims to focus on major tops and bottoms, a strong trending market might trigger the OB signal and stay with it for a long time. That's especially true on young markets and on bubble-mode markets.

█ OB SIGNAL OFF: EXITING OVERBOUGHT CONDITION

When Pulse DPO crosses Below the Top Threshold it Triggers OFF the OB signal. At this point the oscillator line shifts to its normal color.

When Pulse DPO exits the OB Zone, please beware because a Major Top might just have occurred. In this Area the Major Players usually become Aggressive Sellers. They might wind up any remaining Long Positions and Open new Short Positions.

This might be a good area to Open Shorts or to Close/Reverse any remaining Long Position. Whatever you choose to do, it's usually best to act quickly because the market is prone to enter into panic mode.

█ OS SIGNAL ON: ENTERING OVERSOLD CONDITION

When Pulse DPO crosses Below the Bottom Threshold it Triggers ON the OS signal. At this point the oscillator line shifts to OS color.

When Pulse DPO enters the OS Zone, please beware because in this Area the Major Players usually become Active Buyers accumulating Long Positions from the desperate Public.

While the OS signal is On, it might be wise to Consider becoming a Buyer or to implement a Dollar-Cost Averaging (DCA) Strategy to build a Long Position towards the next Cycle. In contrast to the tops, the OS state usually takes longer to resolve a major bottom.

█ OS SIGNAL OFF: EXITING OVERSOLD CONDITION

When Pulse DPO crosses Above the Bottom Threshold it Triggers OFF the OS signal. At this point the oscillator line shifts to its normal color.

When Pulse DPO exits the OS Zone, please beware because a Major Bottom might already be in place. In this Area the Major Players become Aggresive Buyers. They might wind up any remaining Short Positions and Open new Long Positions.

This might be a good area to Open Longs or to Close/Reverse any remaining Short Positions.

█ WHY WOULD YOU BE INTERESTED IN THIS INDICATOR?

This indicator is built over a solid foundation capable of signaling Major Cycle Tops and Bottoms across many markets. Let's see some examples:

Early Bitcoin Years: From 0 to 1242

This chart is in logarithmic mode in order to properly display various exponential cycles. Pulse DPO is properly signaling the major early highs from 9-Jun-2011 at 31.50, to the next one on 9-Apr-2013 at 240 and the epic top from 29-Nov-2013 at 1242.

Due to the massive price movements, the OB condition stays pinned during most of the exponential price action. But as you can see, the OB condition quickly vanishes once the Cycle Top has been reached. As the market matures, the OB condition becomes more exceptional and triggers much closer from the Cycle Top.

With regards to Cycle Bottoms, the early bottom of 2 after having peaked at 31.50 doesn’t get captured by the indicator. That is the only cycle bottom that escapes the Pulse DPO when the bottom threshold is set at a value of 5. In that event, the oscillator low reached 6.95.

Bitcoin Adoption Spreading: From 257 to 73k

This chart is in logarithmic mode in order to properly display various exponential cycles. Pulse DPO is properly signaling all the major highs from 17-Dec-2017 at 19k, to the next one on 14-Apr-2021 at 64k and the most recent top from 9-Nov-2021 at 68k.

During the massive run of 2017, the OB condition still stayed triggered for a few weeks on each swing top. But on the next cycles it started to signal only for a few days before each swing top actually happened. The OB condition during the last cycle top triggered only for 3 days. Therefore the signal grows in focus as the market matures.

At the time of publishing this indicator, Bitcoin printed a new All Time High (ATH) on 13-Mar-2024 at 73k. That run didn’t trigger the OB condition. Therefore, if the indicator is correct the Bitcoin market still has some way to grow during the next months.

With regards to Cycle Bottoms, the bottom of 3k after having peaked at19k got captured within the wide OS zone. The bottom of 15k after having peaked at 68k got captured too within the OS accumulation area.

Gold

Pulse DPO behaves surprisingly well on a long standing market such as Gold. Moving back to the 197x years it’s been signaling most Cycle Tops and Bottoms with precision. During the last cycle, it shows topping at 2k and bottoming at 1.6k.

The current price action is signaling OB condition in the range of 2.5k to 2.7k. Looking at past cycles, it tends to trigger on and off at multiple swing tops until reaching the final cycle top. Therefore this might indicate the first wave within a potential gold run.

Oil

On the Oil market, we can see that most of the cycle tops and bottoms since the 80s got signaled. The only exception being the low from 2020 which didn’t trigger.

EURUSD

On Forex markets the Pulse DPO also behaves as expected. Looking back at EURUSD we can see the marketing triggering OB and OS conditions during major cycle tops and bottoms from recent times until the 80s.

S&P 500

On the S&P 500 the Pulse DPO catched the lows from 2016 and 2020. Looking at present price action, the recent ATH didn’t trigger the OB condition. Therefore, the indicator is allowing room for another leg up during the next months.

Amazon

On the Amazon chart the Pulse DPO is mirroring pretty accurately the major swings. Scrolling back to the early 2000s, this chart resembles early exponential swings in the crypto space.

Tesla

Moving onto a younger tech stock, Pulse DPO captures pretty accurately the major tops and bottoms. The chart is shown in logarithmic scale to better display the magnitude of the moves.

█ SETTINGS

This indicator is ideal for identifying major market turning points while filtering out short-term noise. You are free to adjust the parameters to align with your preferred trading style.

Parameters : This section allows you to customize any of the Parameters that shape the Oscillator.

Oscillator Length: Defines the period for calculating the Oscillator.

Offset: Shifts the oscillator calculation by a certain number of periods, which is typically half the Oscillator Length.

Lookback Period: Specifies how many bars to look back to find tops and bottoms for normalization.

Smoothing Length: Determines the length of the moving average used to smooth the oscillator.

Thresholds : This section allows you to customize the Thresholds that trigger the OB and OS conditions.

Top: Defines the value of the Top Threshold.

Bottom: Defines the value of the Bottom Threshold.

Flashtrader´s Statistical BandwidthsThe vast majority of traders exclusively concern

themselves with trend-following in all its facets. Scoring

points with trends on a regular basis is a difficult task

since prices do not constantly move in one direction

or another. In the case of the DAX future, for example,

only about 30 per cent of all trading days in a year are

trend days. And of these, there are x percent long ones

and x per cent short ones. Catching the very days when

prices rise or fall from the opening to the close is a major

challenge for a trader who also needs to have previously

recognised the corresponding direction.

However, there are also other ways of profit-taking

every day – for example, by using the mean reversion

strategy. The idea behind this is the fact that prices reach

a high and a low every day – but very rarely close at the

high or the low. This means that prices always move

away from these extreme points and the closing price is

somewhere in between. A profitable trading strategy can

be developed out of this.

But how can you know where the high and the low

will be tomorrow? Is it possible for you to know this in

advance? No – because no one can predict the future. Or

can they? At least it can be statistically determined how

high or low prices could go tomorrow. There is a high

degree of probability that one of the two possibilities

will materialise. It will then be necessary to act.

Calculation

Classic pivot points for the following day are calculated

from the high, low and closing price. But does it really

make sense to use such a mix? I don’t think so and

use a different calculation for this strategy. In a first step,

only the differences between the start and the high or low

are calculated on a daily basis. To avoid being dependent

on individual days and outliers, it is advisable to calculate,

in a second step, the average of these differences over

the past five days. Finally, this average will then be added

at the opening price of the current trading day for the

upper statistical bandwidth and subtracted for the lower

bandwidth.

upper bandwidth = oSTB (violet dashed line in the chart)

lower bandwidth = uSTB (violet dashedline in the chart)

The second interesting question is, if the previous day's high has been exceeded, how much further can the price rise from a mathematical/statistical point of view?

These calculated previous day highs expansions are shown as red dashed lines

Previous day's high expansion = VTHA

Previous day's low expansion = VTTA

For further orientation, the previous day's high (VTH) and the previous day's low (VTT) are shown in light blue dashed lines

And as a supplement, the previous day's close in the DAX Future at 10:00 p.m. VTSA in violet solid lines and the previous day's close in the cash register at 5:30 p.m. VTSN in yellow solid lines

Reaching the calculated extreme values does not mean that the trend has to change immediately, but there is at least temporary exhaustion potential with which you can earn a few points every day in the area of scalping.

Example for cheap entry long:

Example for cheap entry short:

Deutsch:

Die Masse der Trader beschäftigt sich ausschließlich mit Trendfolge in all ihren Facetten. Mit Trends regelmäßig zu punkten ist ein schwieriges Unterfangen, da die Kurse nicht ständig in die eine oder andere Richtung laufen. Beim DAX-Future zum Beispiel sind von allen Börsentagen im Jahr lediglich zirka 30 Prozent Trendtage. Davon sind dann auch noch x Prozent Long und x Prozent Short. Hier genau die Tage abzupassen, an denen die Kurse von Börsenbeginn bis zum Schluss steigen beziehungsweise fallen, ist eine große Herausforderung – wobei der Trader zuvor noch die entsprechende Richtung erkannt haben muss. Es gibt jedoch auch noch andere Methoden täglich Gewinne mitzunehmen, zum Beispiel mit der Mean-Reversion-Strategie (Mittelwertumkehr).

Hintergrund ist die Tatsache, dass die Kurse jeden Tag ein Hoch und ein Tief erreichen – aber sehr selten am Hoch oder am Tief schließen. Das bedeutet, dass die Preise sich immer wie der von diesen Extrempunkten wegbewegen und der Schlusskurs irgendwo dazwischen liegt. Hieraus lässt sich eine profitable Handelsstrategie entwickeln. Aber woher kannst Du wissen, wo morgen das Hoch und das Tief sein wird? Kannst Du das vorher schon wissen? Nein – denn niemand kann die Zukunft vorhersagen. Oder doch? Statistisch lässt sich zumindest bestimmen, wie hoch und wie tief die Kurse morgen steigen oder fallen könnten. Eine Seite wird mit sehr hoher Wahrscheinlichkeit ein treffen. Dann gilt es zu handeln.

Berechnung Klassischer Pivot-Punkte für den folgenden Tag werden aus Hoch, Tief und Schlusskurs berechnet. Aber ist es wirklich sinnvoll, einen solchen Mix zu verwenden? Ich finde das nicht und verwenden für diese Strategie eine andere Berechnung. Im ersten Schritt werden täglich die Differenzen nur vom Start bis zum Hoch beziehungsweise Tief errechnet. Um nicht von einzelnen Tagen und Ausreißern abhängig zu sein, empfiehlt es sich, in einem zweiten Schritt den Durchschnitt dieser Differenzen über die letzten fünf Tage zu errechnen. Zuletzt wird dann dieser Durchschnitt zum Eröffnungskurs des aktuellen Handelstages für die obere statistische Bandbreite addiert und für die untere Bandbreite subtrahiert.

Obere statistische Bandbreite = oSTB (violette gestrichelte Linie im Chart)

Untere statistische Bandbreite = uSTB (violette gestrichelte Linie im Chart)

Die zweite interessante Frage ist, wenn das Vortageshoch überschritten wurde, wie weit kann der Kurs dann noch steigen aus mathematisch/statistischer Sicht?

Diese berechneten Vortagesextremausdehnungen sind als rote gestrichelte Linien dargestellt

Vortageshochausdehnung = VTHA

Vortagestiefausdehnung = VTTA

Für die weitere Orientierung sind die Vortageshochs (VTH) und die Vortagestiefs (VTT) als hellblaue gestrichelte Linien abgebildet.

Als Ergänzung wird noch der Vortages Schluss im Dax Future um 22:00 Uhr VTSA mit einer violetten durchgezogenen Linie und der Kassamarktschluss um 17:30 Uhr mit einer gelben durchgezogenen Linie gezeigt.

Das Erreichen der berechneten Extremwerte bedeutet nicht, das der Trend sofort drehen muss, aber es sind zumindest temporäre Erschöpfungspotentiale mit denen sich im Bereich scalping täglich einige Punkte verdienen lassen.

Beispiel für günstigen Einstieg Long:

Beispiel für günstigen Einstieg Short:

Night Low Liquidity Congestions with 4 Trading SessionsThis indicator is designed to help traders visualize and analyze key market periods of low liquidity during the night and identify high-activity zones in the morning. It also includes customizable time sessions for major global markets, including the European and American sessions, as well as the London Close session.

T he main functionalities include:

- Night Low Liquidity Phase: This highlights periods with typically low market activity during the night (default: 20:01–5:59). It also displays the total range (in pips) during this phase, allowing traders to identify potential price consolidations.

- Morning Hot Zone: This focuses on high-activity periods in the early morning (default: 6:00–7:59), providing visual cues without altering bar colors.

- European Trading Session: Displays the European market’s open hours (default: 8:00–12:00), shaded in blue, to mark increased volatility typically seen during this period.

- American Trading Session: Marks the active hours of the U.S. market (default: 12:01–16:59), where market activity tends to peak.

- London Close Area: Highlights the closing hours of the London market (default: 17:00–20:00), allowing traders to track potential liquidity shifts.

Key Features:

1. Customizable Time Sessions:

- The indicator allows for full customization of the start and end times for each market session, making it adaptable to different instruments and trading style.

- Traders can choose their preferred color and opacity for each time zone to suit their charting preferences.

2. Night Low Liquidity Pip Range Calculation:

- Automatically calculates and displays the pip range for the Night Low Liquidity phase.

- The range is colored red if it exceeds the specified threshold and green if it remains below it.

3. Alarm System:

- Customizable alerts for H1, M15, and M5 timeframes.

- Traders can set alerts to trigger just before a bar closes during specific sessions (European, American, or London Close) and on selected days of the week (Monday–Friday).

- The alarm system allows for full customization of active hours and days, giving traders full control over their notifications.

4. Clear Visual Cues:

- The indicator uses transparent shading to differentiate market sessions, making it easy to spot different phases of the trading day.

- Each session is visually distinct and can be toggled on or off based on trader preferences.

Ideal For:

- Traders who focus on intraday strategies and want to understand how market sessions affect liquidity and volatility.

- Those looking to trade during specific time windows like the Night Low Liquidity or Morning Hot Zones.

- Traders who need to automate their alerts based on specific market hours and close events for major timeframes.

Chande Momentum Oscillator StrategyThe Chande Momentum Oscillator (CMO) Trading Strategy is based on the momentum oscillator developed by Tushar Chande in 1994. The CMO measures the momentum of a security by calculating the difference between the sum of recent gains and losses over a defined period. The indicator offers a means to identify overbought and oversold conditions, making it suitable for developing mean-reversion trading strategies (Chande, 1997).

Strategy Overview:

Calculation of the Chande Momentum Oscillator (CMO):

The CMO formula considers both positive and negative price changes over a defined period (commonly set to 9 days) and computes the net momentum as a percentage.

The formula is as follows:

CMO=100×(Sum of Gains−Sum of Losses)(Sum of Gains+Sum of Losses)

CMO=100×(Sum of Gains+Sum of Losses)(Sum of Gains−Sum of Losses)

This approach distinguishes the CMO from other oscillators like the RSI by using both price gains and losses in the numerator, providing a more symmetrical measurement of momentum (Chande, 1997).

Entry Condition:

The strategy opens a long position when the CMO value falls below -50, signaling an oversold condition where the price may revert to the mean. Research in mean-reversion, such as by Poterba and Summers (1988), supports this approach, highlighting that prices often revert after sharp movements due to overreaction in the markets.

Exit Conditions:

The strategy closes the long position when:

The CMO rises above 50, indicating that the price may have become overbought and may not provide further upside potential.

Alternatively, the position is closed 5 days after the buy signal is triggered, regardless of the CMO value, to ensure a timely exit even if the momentum signal does not reach the predefined level.

This exit strategy aligns with the concept of time-based exits, reducing the risk of prolonged exposure to adverse price movements (Fama, 1970).

Scientific Basis and Rationale:

Momentum and Mean-Reversion:

The strategy leverages the well-known phenomenon of mean-reversion in financial markets. According to research by Jegadeesh and Titman (1993), prices tend to revert to their mean over short periods following strong movements, creating opportunities for traders to profit from temporary deviations.

The CMO captures this mean-reversion behavior by monitoring extreme price conditions. When the CMO reaches oversold levels (below -50), it signals potential buying opportunities, whereas crossing overbought levels (above 50) indicates conditions for selling.

Market Efficiency and Overreaction:

The strategy takes advantage of behavioral inefficiencies and overreactions, which are often the drivers behind sharp price movements (Shiller, 2003). By identifying these extreme conditions with the CMO, the strategy aims to capitalize on the market’s tendency to correct itself when price deviations become too large.

Optimization and Parameter Selection:

The 9-day period used for the CMO calculation is a widely accepted timeframe that balances responsiveness and noise reduction, making it suitable for capturing short-term price fluctuations. Studies in technical analysis suggest that oscillators optimized over such periods are effective in detecting reversals (Murphy, 1999).

Performance and Backtesting:

The strategy's effectiveness is confirmed through backtesting, which shows that using the CMO as a mean-reversion tool yields profitable opportunities. The use of time-based exits alongside momentum-based signals enhances the reliability of the strategy by ensuring that trades are closed even when the momentum signal alone does not materialize.

Conclusion:

The Chande Momentum Oscillator Trading Strategy combines the principles of momentum measurement and mean-reversion to identify and capitalize on short-term price fluctuations. By using a widely tested oscillator like the CMO and integrating a systematic exit approach, the strategy effectively addresses both entry and exit conditions, providing a robust method for trading in diverse market environments.

References:

Chande, T. S. (1997). The New Technical Trader: Boost Your Profit by Plugging into the Latest Indicators. John Wiley & Sons.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Ultimate Oscillator Trading StrategyThe Ultimate Oscillator Trading Strategy implemented in Pine Script™ is based on the Ultimate Oscillator (UO), a momentum indicator developed by Larry Williams in 1976. The UO is designed to measure price momentum over multiple timeframes, providing a more comprehensive view of market conditions by considering short-term, medium-term, and long-term trends simultaneously. This strategy applies the UO as a mean-reversion tool, seeking to capitalize on temporary deviations from the mean price level in the asset’s movement (Williams, 1976).

Strategy Overview:

Calculation of the Ultimate Oscillator (UO):

The UO combines price action over three different periods (short-term, medium-term, and long-term) to generate a weighted momentum measure. The default settings used in this strategy are:

Short-term: 6 periods (adjustable between 2 and 10).

Medium-term: 14 periods (adjustable between 6 and 14).

Long-term: 20 periods (adjustable between 10 and 20).

The UO is calculated as a weighted average of buying pressure and true range across these periods. The weights are designed to give more emphasis to short-term momentum, reflecting the short-term mean-reversion behavior observed in financial markets (Murphy, 1999).

Entry Conditions:

A long position is opened when the UO value falls below 30, indicating that the asset is potentially oversold. The value of 30 is a common threshold that suggests the price may have deviated significantly from its mean and could be due for a reversal, consistent with mean-reversion theory (Jegadeesh & Titman, 1993).

Exit Conditions:

The long position is closed when the current close price exceeds the previous day’s high. This rule captures the reversal and price recovery, providing a defined point to take profits.

The use of previous highs as exit points aligns with breakout and momentum strategies, as it indicates sufficient strength for a price recovery (Fama, 1970).

Scientific Basis and Rationale:

Momentum and Mean-Reversion:

The strategy leverages two well-established phenomena in financial markets: momentum and mean-reversion. Momentum, identified in earlier studies like those by Jegadeesh and Titman (1993), describes the tendency of assets to continue in their direction of movement over short periods. Mean-reversion, as discussed by Poterba and Summers (1988), indicates that asset prices tend to revert to their mean over time after short-term deviations. This dual approach aims to buy assets when they are temporarily oversold and capitalize on their return to the mean.

Multi-timeframe Analysis:

The UO’s incorporation of multiple timeframes (short, medium, and long) provides a holistic view of momentum, unlike single-period oscillators such as the RSI. By combining data across different timeframes, the UO offers a more robust signal and reduces the risk of false entries often associated with single-period momentum indicators (Murphy, 1999).

Trading and Market Efficiency:

Studies in behavioral finance, such as those by Shiller (2003), show that short-term inefficiencies and behavioral biases can lead to overreactions in the market, resulting in price deviations. This strategy seeks to exploit these temporary inefficiencies, using the UO as a signal to identify potential entry points when the market sentiment may have overly pushed the price away from its average.

Strategy Performance:

Backtests of this strategy show promising results, with profit factors exceeding 2.5 when the default settings are optimized. These results are consistent with other studies on short-term trading strategies that capitalize on mean-reversion patterns (Jegadeesh & Titman, 1993). The use of a dynamic, multi-period indicator like the UO enhances the strategy’s adaptability, making it effective across different market conditions and timeframes.

Conclusion:

The Ultimate Oscillator Trading Strategy effectively combines momentum and mean-reversion principles to trade on temporary market inefficiencies. By utilizing multiple periods in its calculation, the UO provides a more reliable and comprehensive measure of momentum, reducing the likelihood of false signals and increasing the profitability of trades. This aligns with modern financial research, showing that strategies based on mean-reversion and multi-timeframe analysis can be effective in capturing short-term price movements.

References:

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Williams, L. (1976). Ultimate Oscillator. Market research and technical trading analysis.

Williams %R StrategyThe Williams %R Strategy implemented in Pine Script™ is a trading system based on the Williams %R momentum oscillator. The Williams %R indicator, developed by Larry Williams in 1973, is designed to identify overbought and oversold conditions in a market, helping traders time their entries and exits effectively (Williams, 1979). This particular strategy aims to capitalize on short-term price reversals in the S&P 500 (SPY) by identifying extreme values in the Williams %R indicator and using them as trading signals.

Strategy Rules:

Entry Signal:

A long position is entered when the Williams %R value falls below -90, indicating an oversold condition. This threshold suggests that the market may be near a short-term bottom, and prices are likely to reverse or rebound in the short term (Murphy, 1999).

Exit Signal:

The long position is exited when:

The current close price is higher than the previous day’s high, or

The Williams %R indicator rises above -30, indicating that the market is no longer oversold and may be approaching an overbought condition (Wilder, 1978).

Technical Analysis and Rationale:

The Williams %R is a momentum oscillator that measures the level of the close relative to the high-low range over a specific period, providing insight into whether an asset is trading near its highs or lows. The indicator values range from -100 (most oversold) to 0 (most overbought). When the value falls below -90, it indicates an oversold condition where a reversal is likely (Achelis, 2000). This strategy uses this oversold threshold as a signal to initiate long positions, betting on mean reversion—an established principle in financial markets where prices tend to revert to their historical averages (Jegadeesh & Titman, 1993).

Optimization and Performance:

The strategy allows for an adjustable lookback period (between 2 and 25 days) to determine the range used in the Williams %R calculation. Empirical tests show that shorter lookback periods (e.g., 2 days) yield the most favorable outcomes, with profit factors exceeding 2. This finding aligns with studies suggesting that shorter timeframes can effectively capture short-term momentum reversals (Fama, 1970; Jegadeesh & Titman, 1993).

Scientific Context:

Mean Reversion Theory: The strategy’s core relies on mean reversion, which suggests that prices fluctuate around a mean or average value. Research shows that such strategies, particularly those using oscillators like Williams %R, can exploit these temporary deviations (Poterba & Summers, 1988).

Behavioral Finance: The overbought and oversold conditions identified by Williams %R align with psychological factors influencing trading behavior, such as herding and panic selling, which often create opportunities for price reversals (Shiller, 2003).

Conclusion:

This Williams %R-based strategy utilizes a well-established momentum oscillator to time entries and exits in the S&P 500. By targeting extreme oversold conditions and exiting when these conditions revert or exceed historical ranges, the strategy aims to capture short-term gains. Scientific evidence supports the effectiveness of short-term mean reversion strategies, particularly when using indicators sensitive to momentum shifts.

References:

Achelis, S. B. (2000). Technical Analysis from A to Z. McGraw Hill.

Fama, E. F. (1970). Efficient Capital Markets: A Review of Theory and Empirical Work. The Journal of Finance, 25(2), 383-417.

Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

Murphy, J. J. (1999). Technical Analysis of the Financial Markets: A Comprehensive Guide to Trading Methods and Applications. New York Institute of Finance.

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.

Shiller, R. J. (2003). From Efficient Markets Theory to Behavioral Finance. Journal of Economic Perspectives, 17(1), 83-104.

Williams, L. (1979). How I Made One Million Dollars… Last Year… Trading Commodities. Windsor Books.

Wilder, J. W. (1978). New Concepts in Technical Trading Systems. Trend Research.

This explanation provides a scientific and evidence-based perspective on the Williams %R trading strategy, aligning it with fundamental principles in technical analysis and behavioral finance.

VATICAN BANK CARTELVATICAN BANK CARTEL - Precision Signal Detection for Buyers.

The VATICAN BANK CARTEL indicator is a highly sophisticated tool designed specifically for buyers, helping them identify key market trends and generate actionable buy signals. Utilizing advanced algorithms, this indicator employs a multi-variable detection mechanism that dynamically adapts to price movements, offering real-time insights to assist in executing profitable buy trades. This indicator is optimized solely for identifying buying opportunities, ensuring that traders are equipped to make well-timed entries and exits, without signals for shorting or selling.

The recommended settings for VATICAN BANK CARTEL indicator is as follows:-

Depth Engine = 20,30,40,50,100.

Deviation Engine = 3,5,7,15,20.

Backstep Engine = 15,17,20,25.

NOTE:- But you can also use this indicator as per your setting, whichever setting gives you best results use that setting.

Key Features:

1.Adaptive Depth, Deviation, and Backstep Inputs:

The core of this indicator is its customizable Depth Engine, Deviation Engine, and Backstep Engine parameters. These inputs allow traders to adjust the sensitivity of the trend detection algorithm based on specific market conditions:

Depth: Defines how deep the indicator scans historical price data for potential trend reversals.

Deviation: Determines the minimum required price fluctuation to confirm a market movement.

Backstep: Sets the retracement level to filter false signals and maintain the accuracy of trend detection.

2. Visual Signal Representation:

The VATICAN BANK CARTEL plots highly visible labels on the chart to mark trend reversals. These labels are customizable in terms of size and transparency, ensuring clarity in various chart environments. Traders can quickly spot buying opportunities with green labels and potential square-off points with red labels, focusing exclusively on buy-side signals.

3.Real-Time Alerts:

The indicator is equipped with real-time alert conditions to notify traders of significant buy or square-off buy signals. These alerts, which are triggered based on the indicator’s internal signal logic, ensure that traders never miss a critical market movement on the buy side.

4.Custom Label Size and Transparency:

To enhance visual flexibility, the indicator allows the user to adjust label size (from small to large) and transparency levels. This feature provides a clean, adaptable view suited for different charting styles and timeframes.

How It Works:

The VATICAN BANK CARTEL analyzes the price action using a sophisticated algorithm that considers historical low and high points, dynamically detecting directional changes. When a change in market direction is detected, the indicator plots a label at the key reversal points, helping traders confirm potential entry points:

- Buy Signal (Green): Indicates potential buying opportunities based on a trend reversal.

- Square-Off Buy Signal (Red): Marks the exit point for open buy positions, allowing traders to take profits or protect capital from potential market reversals.

Note: This indicator is exclusively designed to provide signals for buyers. It does not generate sell or short signals, making it ideal for traders focused solely on identifying optimal buying opportunities in the market.

Customizable Parameters:

- Depth Engine: Fine-tunes the historical data analysis for signal generation.

- Deviation Engine: Adjusts the minimum price change required for detecting trends.

- Backstep Engine: Controls the indicator's sensitivity to retracements, minimizing false signals.

- Labels Transparency: Adjusts the opacity of the labels, ensuring they integrate seamlessly into any chart layout.

- Buy and Sell Colors: Customizable color options for buy and square-off buy labels to match your preferred color scheme.

- Label Size: Select between five different label sizes for optimal chart visibility.

Ideal For:

This indicator is ideal for both beginner and experienced traders looking to enhance their buying strategy with a highly reliable, visual, and alert-driven tool. The VATICAN BANK CARTEL adapts to various timeframes, making it suitable for day traders, swing traders, and long-term investors alike—focused exclusively on buying opportunities.

Benefits and Applications:

1.Intraday Trading: The VATICAN BANK CARTEL indicator is particularly well-suited for intraday trading, as it provides accurate and timely "buy" and "square-off buy" signals based on the current market dynamics.

2.Trend-following Strategies: Traders who employ trend-following strategies can leverage the indicator's ability to identify the overall market direction, allowing them to align their trades with the dominant trend.

3.Swing Trading: The dynamic price tracking and signal generation capabilities of the indicator can be beneficial for swing traders, who aim to capture medium-term price movements.

Security Measures:

1. The code includes a security notice at the beginning, indicating that it is subject to the Mozilla Public License 2.0, which is a reputable open-source license.

2. The code does not appear to contain any obvious security vulnerabilities or malicious content that could compromise user data or accounts.

NOTE:- This indicator is provided under the Mozilla Public License 2.0 and is subject to its terms and conditions.

Disclaimer: The usage of VATICAN BANK CARTEL indicator might or might not contribute to your trading capital(money) profits and losses and the author is not responsible for the same.

IMPORTANT NOTICE:

While the indicator aims to provide reliable "buy" and "square-off buy" signals, it is crucial to understand that the market can be influenced by unpredictable events, such as natural disasters, political unrest, changes in monetary policies, or economic crises. These unforeseen situations may occasionally lead to false signals generated by the VATICAN BANK CARTEL indicator.

Users should exercise caution and diligence when relying on the indicator's signals, as the market's behavior can be unpredictable, and external factors may impact the accuracy of the signals. It is recommended to thoroughly backtest the indicator's performance in various market conditions and to use it as one of the many tools in a comprehensive trading strategy, rather than solely relying on its output.

Ultimately, the success of the VATICAN BANK CARTEL indicator will depend on the user's ability to adapt it to their specific trading style, market conditions, and risk management approach. Continuous monitoring, analysis, and adjustment of the indicator's settings may be necessary to maintain its effectiveness in the ever-evolving financial markets.

DEVELOPER:- yashgode9

PineScript:- version:- 5

This indicator aims to enhance trading decision-making by combining DEPTH, DEVIATION, BACKSTEP with custom signal generation, offering a comprehensive tool for traders seeking clear "buy" and "square-off buy" signals on the TradingView platform.

Essa's Indicator 2.0Essa's Indicator V2: Beginner's Guide

This custom TradingView indicator has been designed to help you identify key trading opportunities based on session highs/lows, volatility, and moving averages. Below is a breakdown of the main features:

1. Exponential Moving Averages (EMAs)

Fast EMA (Blue Line): Tracks the short-term market trend (default: 9-period EMA).

Slow EMA (Red Line): Tracks the longer-term market trend (default: 21-period EMA).

You can turn on/off the EMAs using the "Show EMAs" option in the settings.

EMAs help smooth out price action and give a clearer picture of trends. A crossover of the fast EMA above the slow EMA can signal an upward trend, while the reverse may indicate a downward trend.

2. Session Highs and Lows

The indicator tracks price highs and lows for three major trading sessions:

London Session (Red): Highlighted in red. Active between 08:00 and 17:00 (LDN timezone) or 03:00 and 12:00 (NY timezone).

New York Session (Blue): Highlighted in blue. Active between 12:00 and 21:00 (LDN timezone) or 07:00 and 16:00 (NY timezone).

Asia Session (Yellow): Highlighted in yellow. Active between 22:00 and 08:00 (LDN timezone) or 18:00 and 03:00 (NY timezone).

Highs and lows for each session are plotted on the chart as lines. Breakouts from these levels can signal important trading opportunities:

London High/Low: Red lines.

New York High/Low: Blue lines.

Asia High/Low: Yellow lines.

The background color also changes depending on the active session:

London: Light red background.

New York: Light blue background.

Asia: Light yellow background.

3. Breakout Alerts

You can set alerts when the price breaks above or below session highs/lows:

Break Above London High: Alert triggered when the price crosses the London session high.

Break Below London Low: Alert triggered when the price falls below the London session low.

Similar alerts exist for the New York and Asia sessions as well.

4. Volatility-Adjusted EMA

The EMAs in this indicator are adjusted based on volatility (ATR - Average True Range). This allows the EMAs to respond to market conditions more dynamically, giving you more accurate trend readings in volatile markets.

5. ZigZag Feature (Optional)

You can enable the ZigZag feature to help visualize the price action's highs and lows:

ZigZag Lines: Highlight major peaks and troughs in price movements, helping you spot trends more easily.

This is helpful for identifying reversals or trend continuations.

6. Fractal Markers

This indicator uses fractals to mark potential turning points in the market:

Green Triangles (Above the Price): Indicate up fractals (potential reversal points where the price could move upwards).

Red Triangles (Below the Price): Indicate down fractals (potential reversal points where the price could move downwards).

Fractals can be a helpful confirmation tool when identifying entry and exit points.

7. Custom Timezone Options

You can choose between London (LDN) and New York (NY) timezones in the settings to adapt the session times to your trading location. This ensures the session high/low markers are displayed correctly for your trading region.

By default, the New York (NY) timezone is enabled for FXCM charts in the UK.

For BTC charts, you will need to switch to the appropriate time zone manually.

Thanks

Essa

Winning and Losing StreaksThe Pine Script indicator "Winning and Losing Streaks" tracks and visualizes the length of consecutive winning and losing streaks in a financial series, such as stock prices. Here’s a detailed description of the indicator, including the relevance of statistical analysis and streak tracking.

Indicator Description

The "Winning and Losing Streaks" indicator in Pine Script is designed to analyze and display streaks of consecutive winning and losing days in trading data. It helps traders and analysts understand the persistence of trends in price movements.

Here’s how it functions:

Streak Calculation:

Winning Streak: A series of consecutive days where the closing price is higher than the previous day's closing price.

Losing Streak: A series of consecutive days where the closing price is lower than the previous day's closing price.

Doji Candles: The indicator also considers Doji candles, where the difference between the opening and closing prices is minimal relative to the high-low range, and excludes these from being counted as winning or losing days.

Statistical Analysis:

The indicator computes the maximum and average lengths of winning and losing streaks.

It also tracks the current streak lengths and maintains arrays to store the historical streak data.

Visualization:

Histograms: Winning and losing streaks are visualized using histograms, which provide a clear graphical representation of streak lengths over time.

Relevance of Statistical Analysis and Streak Tracking

1. Statistical Significance of Streaks

Tracking winning and losing streaks has significant statistical implications for trading strategies and risk management:

Autocorrelation: Streaks in financial time series can reveal autocorrelation, where past returns influence future returns. Studies have shown that financial time series often exhibit autocorrelation, which can be used to forecast future price movements (Lo, 1991; Jegadeesh & Titman, 1993). Understanding streaks helps in identifying and leveraging these patterns.

Behavioral Finance: Streak analysis aligns with concepts from behavioral finance, such as the "hot-hand fallacy," where investors may perceive trends as more persistent than they are (Gilovich, Vallone, & Tversky, 1985). Statistical streak analysis provides a more objective view of trend persistence, helping to avoid biases.

2. Risk Management and Strategy Development

Risk Assessment: Identifying the length and frequency of losing streaks is crucial for managing risk and adjusting trading strategies. Long losing streaks can indicate potential strategy weaknesses or market regime changes, prompting a reassessment of trading rules and risk management practices (Brock, Lakonishok, & LeBaron, 1992).

Strategy Optimization: Statistical analysis of streaks can aid in optimizing trading strategies. For example, understanding the average length of winning and losing streaks can help in setting more effective stop-loss and take-profit levels, as well as in determining the optimal position sizing (Fama & French, 1993).

Scientific References:

Lo, A. W. (1991). "Long-Term Memory in Stock Market Prices." Econometrica, 59(5), 1279-1313. This paper discusses the presence of long-term memory in stock prices, which is relevant for understanding the persistence of streaks.

Jegadeesh, N., & Titman, S. (1993). "Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency." Journal of Finance, 48(1), 65-91. This study explores momentum and reversal strategies, which are related to the concept of streaks.

Gilovich, T., Vallone, R., & Tversky, A. (1985). "The Hot Hand in Basketball: On the Misperception of Random Sequences." Cognitive Psychology, 17(3), 295-314. This paper provides insight into the psychological aspects of streaks and persistence.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). "Simple Technical Trading Rules and the Stochastic Properties of Stock Returns." Journal of Finance, 47(5), 1731-1764. This research examines the effectiveness of technical trading rules, relevant for streak-based strategies.

Fama, E. F., & French, K. R. (1993). "Common Risk Factors in the Returns on Stocks and Bonds." Journal of Financial Economics, 33(1), 3-56. This paper provides a foundation for understanding risk factors and strategy performance.

By analyzing streaks, traders can gain valuable insights into market dynamics and refine their trading strategies based on empirical evidence.

Fibonacci Levels for Recent CandlesThis Pine Script indicator calculates and plots 17 predefined Fibonacci retracement levels based on the high and low of a user-defined number of previous candles. The levels are drawn on the chart for the most recent candles, as specified by the user, allowing traders to see how these historical Fibonacci levels align with the current price action.

Weighted US Liquidity ROC Indicator with FED RatesThe Weighted US Liquidity ROC Indicator is a technical indicator that measures the Rate of Change (ROC) of a weighted liquidity index. This index aggregates multiple monetary and liquidity measures to provide a comprehensive view of liquidity in the economy. The ROC of the liquidity index indicates the relative change in this index over a specified period, helping to identify trend changes and market movements.

1. Liquidity Components:

The indicator incorporates various monetary and liquidity measures, including M1, M2, the monetary base, total reserves of depository institutions, money market funds, commercial paper, and repurchase agreements (repos). Each of these components is assigned a weight that reflects its relative importance to overall liquidity.

2. ROC Calculation:

The Rate of Change (ROC) of the weighted liquidity index is calculated by finding the difference between the current value of the index and its value from a previous period (ROC period), then dividing this difference by the value from the previous period. This gives the percentage increase or decrease in the index.

3. Visualization:

The ROC value is plotted as a histogram, with positive and negative changes indicated by different colors. The Federal Funds Rate is also plotted separately to show the impact of central bank policy on liquidity.

Discussion of the Relationship Between Liquidity and Stock Market Returns

The relationship between liquidity and stock market returns has been extensively studied in financial economics. Here are some key insights supported by scientific research:

Liquidity and Stock Returns:

Liquidity Premium Theory: One of the primary theories is the liquidity premium theory, which suggests that assets with higher liquidity typically offer lower returns because investors are willing to accept lower yields for more liquid assets. Conversely, assets with lower liquidity may offer higher returns to compensate for the increased risk associated with their illiquidity (Amihud & Mendelson, 1986).

Empirical Evidence: Research by Fama and French (1992) has shown that liquidity is an important factor in explaining stock returns. Their studies suggest that stocks with lower liquidity tend to have higher expected returns, aligning with the liquidity premium theory.

Market Impact of Liquidity Changes:

Liquidity Shocks: Changes in liquidity can impact stock returns significantly. For example, an increase in liquidity is often associated with higher stock prices, as it reduces the cost of trading and enhances market efficiency (Chordia, Roll, & Subrahmanyam, 2000). Conversely, a liquidity shock, such as a sudden decrease in market liquidity, can lead to higher volatility and lower stock prices.

Financial Crises: During financial crises, liquidity tends to dry up, leading to sharp declines in stock market returns. For instance, studies on the 2008 financial crisis illustrate how a reduction in market liquidity exacerbated the decline in stock prices (Brunnermeier & Pedersen, 2009).

Central Bank Policies and Liquidity:

Monetary Policy Impact: Central bank policies, such as changes in the Federal Funds Rate, directly influence market liquidity. Lower interest rates generally increase liquidity by making borrowing cheaper, which can lead to higher stock market returns. On the other hand, higher rates can reduce liquidity and negatively impact stock prices (Bernanke & Gertler, 1999).

Policy Expectations: The anticipation of changes in monetary policy can also affect stock market returns. For example, expectations of rate cuts can lead to a rise in stock prices even before the actual policy change occurs (Kuttner, 2001).

Key References:

Amihud, Y., & Mendelson, H. (1986). "Asset Pricing and the Bid-Ask Spread." Journal of Financial Economics, 17(2), 223-249.

Fama, E. F., & French, K. R. (1992). "The Cross-Section of Expected Stock Returns." Journal of Finance, 47(2), 427-465.

Chordia, T., Roll, R., & Subrahmanyam, A. (2000). "Market Liquidity and Trading Activity." Journal of Finance, 55(2), 265-289.

Brunnermeier, M. K., & Pedersen, L. H. (2009). "Market Liquidity and Funding Liquidity." Review of Financial Studies, 22(6), 2201-2238.

Bernanke, B. S., & Gertler, M. (1999). "Monetary Policy and Asset Prices." NBER Working Paper No. 7559.

Kuttner, K. N. (2001). "Monetary Policy Surprises and Interest Rates: Evidence from the Fed Funds Futures Market." Journal of Monetary Economics, 47(3), 523-544.

These studies collectively highlight how liquidity influences stock market returns and how changes in liquidity conditions, influenced by monetary policy and other factors, can significantly impact stock prices and market stability.

FXN - Week and Day Separator midnight open. A simple modification of the regular FXN day separator indicator. It starts the days at 12:00 of the time-zone you select as opposed to the regular 17:00 server time.

Chandelier Exit Strategy with 200 EMA FilterStrategy Name and Purpose

Chandelier Exit Strategy with 200EMA Filter

This strategy uses the Chandelier Exit indicator in combination with a 200-period Exponential Moving Average (EMA) to generate trend-based trading signals. The main purpose of this strategy is to help traders identify high-probability entry points by leveraging the Chandelier Exit for stop loss levels and the EMA for trend confirmation. This strategy aims to provide clear rules for entries and exits, improving overall trading discipline and performance.

Originality and Usefulness

This script integrates two powerful indicators to create a cohesive and effective trading strategy:

Chandelier Exit : This indicator is based on the Average True Range (ATR) and identifies potential stop loss levels. The Chandelier Exit helps manage risk by setting stop loss levels at a distance from the highest high or lowest low over a specified period, multiplied by the ATR. This ensures that the stop loss adapts to market volatility.

200-period Exponential Moving Average (EMA) : The EMA acts as a trend filter. By ensuring trades are only taken in the direction of the overall trend, the strategy improves the probability of success. For long entries, the close price must be above the 200 EMA, indicating a bullish trend. For short entries, the close price must be below the 200 EMA, indicating a bearish trend.

Combining these indicators adds layers of confirmation and risk management, enhancing the strategy's effectiveness. The Chandelier Exit provides dynamic stop loss levels based on market volatility, while the EMA ensures trades align with the prevailing trend.

Entry Conditions

Long Entry

A buy signal is generated by the Chandelier Exit.

The close price is above the 200 EMA, indicating a strong bullish trend.

Short Entry

A sell signal is generated by the Chandelier Exit.

The close price is below the 200 EMA, indicating a strong bearish trend.

Exit Conditions

For long positions: The position is closed when a sell signal is generated by the Chandelier Exit.

For short positions: The position is closed when a buy signal is generated by the Chandelier Exit.

Risk Management

Account Size: 1,000,00 yen

Commission and Slippage: 17 pips commission and 1 pip slippage per trade

Risk per Trade: 10% of account equity

Stop Loss: For long trades, the stop loss is placed slightly below the candle that generated the buy signal. For short trades, the stop loss is placed slightly above the candle that generated the sell signal. The stop loss levels are dynamically adjusted based on the ATR.

Settings Options

ATR Period: Set the period for calculating the ATR to determine the Chandelier Exit levels.

ATR Multiplier: Set the multiplier for ATR to define the distance of stop loss levels from the highest high or lowest low.

Use Close Price for Extremums: Choose whether to use the close price for calculating the extremums.

EMA Period: Set the period for the EMA to adjust the trend filter sensitivity.

Show Buy/Sell Labels: Choose whether to display buy and sell labels on the chart for visual confirmation.

Highlight State: Choose whether to highlight the bullish or bearish state on the chart.

Sufficient Sample Size

The strategy has been backtested with a sufficient sample size to evaluate its performance accurately. This ensures that the strategy's results are statistically significant and reliable.

Notes

This strategy is based on historical data and does not guarantee future results.

Thoroughly backtest and validate results before using in live trading.

Market volatility and other external factors can affect performance and may not yield expected results.

Acknowledgment

This strategy uses the Chandelier Exit indicator. Special thanks to the original contributors for their work on the Chandelier Exit concept.

Clean Chart Explanation

The script is published with a clean chart to ensure that its output is readily identifiable and easy to understand. No other scripts are included on the chart, and any drawings or images used are specifically to illustrate how the script works.

CME Trading Hours HighlightDisplay the times when the CME is or isn't trading, on a non-CME symbol.

The Chicago Mercantile Exchange hours are usually from 17:00 one day to 16:00 the next, with an hour's break. Trading halts from Friday evening to Sunday evening. The exchange is in Chicago.

You might want to display these hours if you trade the same asset on a different exchange. For example, you might want to overlay the CME BTC1! hours on a Coinbase BTC chart to see how trading in these futures contracts affects the market.

Inputs:

Shade Outside Trading Hours - If selected (the default), then the chart background is shaded when the CME is closed. If unselected, the background is shaded when it's open.

Highlight Color - The colour to use for the background shade.

Just for fun, I wanted to publish a useful script that only took up one line 😁

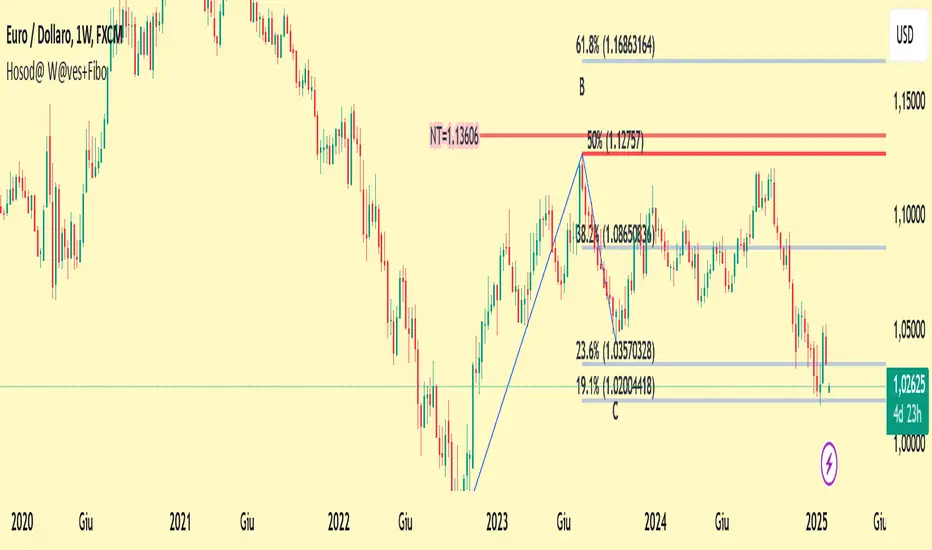

Ichimoku Theories [LuxAlgo]The Ichimoku Theories indicator is the most complete Ichimoku tool you will ever need. Four tools combined into one to harness all the power of Ichimoku Kinkō Hyō.

This tool features the following concepts based on the work of Goichi Hosoda:

Ichimoku Kinkō Hyō: Original Ichimoku indicator with its five main lines and kumo.

Time Theory: automatic time cycle identification and forecasting to understand market timing.

Wave Theory: automatic wave identification to understand market structure.

Price Theory: automatic identification of developing N waves and possible price targets to understand future price behavior.

🔶 ICHIMOKU KINKŌ HYŌ

Ichimoku with lines only, Kumo only and both together

Let us start with the basics: the Ichimoku original indicator is a tool to understand the market, not to predict it, it is a trend-following tool, so it is best used in trending markets.

Ichimoku tells us what is happening in the market and what may happen next, the aim of the tool is to provide market understanding, not trading signals.

The tool is based on calculating the mid-point between the high and low of three pre-defined ranges as the equilibrium price for short (9 periods), medium (26 periods), and long (52 periods) time horizons:

Tenkan sen: middle point of the range of the last 9 candles

Kinjun sen: middle point of the range of the last 26 candles

Senkou span A: middle point between Tankan Sen and Kijun Sen, plotted 26 candles into the future

Senkou span B: midpoint of the range of the last 52 candles, plotted 26 candles into the future

Chikou span: closing price plotted 26 candles into the past

Kumo: area between Senkou pans A and B (kumo means cloud in Japanese)

The most basic use of the tool is to use the Kumo as an area of possible support or resistance.

🔶 TIME THEORY

Current cycles and forecast

Time theory is a critical concept used to identify historical and current market cycles, and use these to forecast the next ones. This concept is based on the Kihon Suchi (translating to "Basic Numbers" in Japanese), these are 9 and 26, and from their combinations we obtain the following sequence:

9, 17, 26, 33, 42, 51, 65, 76, 129, 172, 200, 257

The main idea is that the market moves in cycles with periods set by the Kihon Suchi sequence.

When the cycle has the same exact periods, we obtain the Taito Suchi (translating to "Same Number" in Japanese).

This tool allows traders to identify historical and current market cycles and forecast the next one.

🔹 Time Cycle Identification

Presentation of 4 different modes: SWINGS, HIGHS, KINJUN, and WAVES .

The tool draws a horizontal line at the bottom of the chart showing the cycles detected and their size.

The following settings are used:

Time Cycle Mode: up to 7 different modes

Wave Cycle: Which wave to use when WAVE mode is selected, only active waves in the Wave Theory settings will be used.

Show Time Cycles: keep a cleaner chart by disabling cycles visualisation

Show last X time cycles: how many cycles to display

🔹 Time Cycle Forecast

Showcasing the two forecasting patterns: Kihon Suchi and Taito Suchi

The tool plots horizontal lines, a solid anchor line, and several dotted forecast lines.

The following settings are used:

Show time cycle forecast: to keep things clean

Forecast Pattern: comes in two flavors

Kihon Suchi plots a line from the anchor at each number in the Kihon Suchi sequence.

Taito Suchi plot lines from the anchor with the same size detected in the anchored cycle

Anchor forecast on last X time cycle: traders can place the anchor in any detected cycle

🔶 WAVE THEORY

All waves activated with overlapping

The main idea behind this theory is that markets move like waves in the sea, back and forth (making swing lows and highs). Understanding the current market structure is key to having realistic expectations of what the market may do next. The waves are divided into Simple and Complex.

The following settings are used:

Basic Waves: allows traders to activate waves I, V and N

Complex Waves: allows traders to activate waves P, Y and W

Overlapping waves: to avoid missing out on any of the waves activated

Show last X waves: how many waves will be displayed

🔹 Basic Waves

The three basic waves

The basic waves from which all waves are made are I, V, and N

I wave: one leg moves

V wave: two legs move, one against the other

N wave: Three legs move, push, pull back, and another push

🔹 Complex Waves

Three complex waves

There are other waves like

P wave: contracting market

Y wave: expanding market

W wave: double top or double bottom

🔶 PRICE THEORY

All targets for the current N wave with their calculations

This theory is based on identifying developing N waves and predicting potential price targets based on that developing wave.

The tool displays 4 basic targets (V, E, N, and NT) and 3 extended targets (2E and 3E) according to the calculations shown in the chart above. Traders can enable or disable each target in the settings panel.

🔶 USING EVERYTHING TOGETHER

Please DON'T do this. This is not how you use it

Now the real example:

Daily chart of Nasdaq 100 futures (NQ1!) with our Ichimoku analysis

Time, waves, and price theories go together as one:

First, we identify the current time cycles and wave structure.

Then we forecast the next cycle and possible key price levels.

We identify a Taito Suchi with both legs of exactly 41 candles on each I wave, both together forming a V wave, the last two I waves are part of a developing N wave, and the time cycle of the first one is 191 candles. We forecast this cycle into the future and get 22nd April as a key date, so in 6 trading days (as of this writing) the market would have completed another Taito Suchi pattern if a new wave and time cycle starts. As we have a developing N wave we can see the potential price targets, the price is actually between the NT and V targets. We have a bullish Kumo and the price is touching it, if this Kumo provides enough support for the price to go further, the market could reach N or E targets.

So we have identified the cycle and wave, our expectations are that the current cycle is another Taito Suchi and the current wave is an N wave, the first I wave went for 191 candles, and we expect the second and third I waves together to amount to 191 candles, so in theory the N wave would complete in the next 6 trading days making a swing high. If this is indeed the case, the price could reach the V target (it is almost there) or even the N target if the bulls have the necessary strength.

We do not predict the future, we can only aim to understand the current market conditions and have future expectations of when (time), how (wave), and where (price) the market will make the next turning point where one side of the market overcomes the other (bulls vs bears).

To generate this chart, we change the following settings from the default ones:

Swing length: 64

Show lines: disabled

Forecast pattern: TAITO SUCHI

Anchor forecast: 2

Show last time cycles: 5

I WAVE: enabled

N WAVE: disabled

Show last waves: 5

🔶 SETTINGS

Show Swing Highs & Lows: Enable/Disable points on swing highs and swing lows.

Swing Length: Number of candles to confirm a swing high or swing low. A higher number detects larger swings.

🔹 Ichimoku Kinkō Hyō

Show Lines: Enable/Disable the 5 Ichimoku lines: Kijun sen, Tenkan sen, Senkou span A & B and Chikou Span.

Show Kumo: Enable/Disable the Kumo (cloud). The Kumo is formed by 2 lines: Senkou Span A and Senkou Span B.

Tenkan Sen Length: Number of candles for Tenkan Sen calculation.

Kinjun Sen Length: Number of candles for the Kijun Sen calculation.

Senkou Span B Length: Number of candles for Senkou Span B calculation.

Chikou & Senkou Offset: Number of candles for Chikou and Senkou Span calculation. Chikou Span is plotted in the past, and Senkou Span A & B in the future.

🔹 Time Theory

Show Time Cycle Forecast: Enable/Disable time cycle forecast vertical lines. Disable for better performance.

Forecast Pattern: Choose between two patterns: Kihon Suchi (basic numbers) or Taito Suchi (equal numbers).

Anchor forecast on last X time cycle: Number of time cycles in the past to anchor the time cycle forecast. The larger the number, the deeper in the past the anchor will be.

Time Cycle Mode: Choose from 7 time cycle detection modes: Tenkan Sen cross, Kijun Sen cross, Kumo change between bullish & bearish, swing highs only, swing lows only, both swing highs & lows and wave detection.

Wave Cycle: Choose which type of wave to detect from 6 different wave types when the time cycle mode is set to WAVES.

Show Time Cycles: Enable/Disable time cycle horizontal lines. Disable for better performance.

how last X time cycles: Maximum number of time cycles to display.

🔹 Wave Theory

Basic Waves: Enable/Disable the display of basic waves, all at once or one at a time. Disable for better performance.

Complex Waves: Enable/Disable complex wave display, all at once or one by one. Disable for better performance.

Overlapping Waves: Enable/Disable the display of waves ending on the same swing point.

Show last X waves: 'Maximum number of waves to display.

🔹 Price Theory

Basic Targets: Enable/Disable horizontal price target lines. Disable for better performance.

Extended Targets: Enable/Disable extended price target horizontal lines. Disable for better performance.

Aroon and ASH strategy - ETHERIUM [IkkeOmar]Intro:

This post introduces a Pine Script strategy, as an example if anyone needs a push to get started. This example is a strategy on ETH, obviously it isn't a good strategy, and I wouldn't share my own good strategies because of alpha decay. This strategy combines two technical indicators: Aroon and Absolute Strength Histogram (ASH).

Overview:

The strategy employs the Aroon indicator alongside the Absolute Strength Histogram (ASH) to determine market trends and potential trade setups. Aroon helps identify the strength and direction of a trend, while ASH provides insights into the strength of momentum. By combining these indicators, the strategy aims to capture profitable trading opportunities in Ethereum markets. Normally when developing strats using indicators, you want to find some good indicators, but you NEED to understand their strengths and weaknesses, other indicators can be incorporated to minimize the downs of another indicator. Try to look for synergy in your indicators!

Indicator settings:

Aroon Indicator:

- Two sets of parameters are used for the Aroon indicator:

- For Long Positions: Aroon periods are set to 56 (upper) and 20 (lower).

- For Short Positions: Aroon periods are set to 17 (upper) and 55 (lower).

Absolute Strength Histogram (ASH):

ASH is calculated with a length of 9 bars using the closing price as the data source.

Trading Conditions:

The strategy incorporates specific conditions to initiate and exit trades:

Start Date:

Traders can specify the start date for backtesting purposes.

Trade Direction:

Traders can select the desired trade direction: Long, Short, or Both.

Entry and Exit Conditions:

1. Long Position Entry: A long position is initiated when the Aroon indicator crosses over (crossover) the lower Aroon threshold, indicating a potential uptrend.

2. Long Position Exit: A long position is closed when the Aroon indicator crosses under (crossunder) the lower Aroon threshold.

3. Short Position Entry: A short position is initiated when the Aroon indicator crosses under (crossunder) the upper Aroon threshold, signaling a potential downtrend.

4. Short Position Exit: A short position is closed when the Aroon indicator crosses over (crossover) the upper Aroon threshold.

Disclaimer:

THIS ISN'T AN OPTIMAL STRATEGY AT ALL! It was just an old project from when I started learning pine script!

The backtest doesn't promise the same results in the future, always do both in-sample and out-of-sample testing when backtesting a strategy. And make sure you forward test it as well before implementing it!

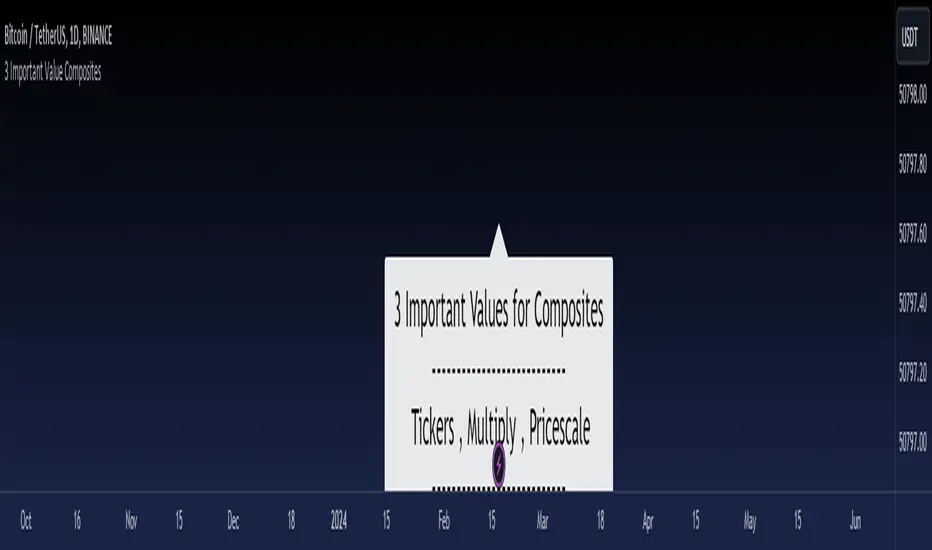

3 Important Value CompositesCalculated on February 17, 2024. USDT 378 items, BTC 282 items, BINANCE

This is a watchlist, along with the most accurate computed values that I could achieve. It may be beneficial for those who want to change values from the "120x ticker screener (composite tickers)" indicator, which is one of the excellent indicators to bypass the limitation of the request. security() function that limits to only 40 requests. I've thought about this before but couldn't succeed, but someone finally did it. :)

--> 120x ticker screener (composite tickers)

Thank you once again for this idea.

You must look for this and change it.

t1 = 'symbol', n1 = Multiply , r1 = Pricescale(decimal)

Example of grouping: Group 1

BINANCE:ETHUSDT , BINANCE:FDUSDUSDT , BINANCE:BTCUSDT

2, 4, 2

13, 10

█ Note

• Tickers: For your watchlist, arrange them from left to right, pairing them in groups of 3.

• Pricescale: This represents the decimal length, arrange them from left to right, pairing them in groups of 3.

• Multiply: This involves multiplying the first 2 items in each pair of watchlists. Arrange them from left to right, pairing them in groups of 2.

* If you group items incorrectly, it may lead to inaccurate results.

* Please be advised that if one of the values in the "Pricescale"(decimal) trio changes, there may be a need to adjust those values accordingly to ensure correct digit separation. Otherwise, within the group, the numbers might appear peculiar.

Bitcoin's Logarithmic ChannelLogarithmic growth is a reasonable way to describe the long term growth of bitcoin's market value: for a network that is experiencing growing adoption and is powered by an asset with a finite and disinflationary supply, it’s natural to expect a more explosive growth of its market capitalization early on, followed by diminishing returns as the network and the asset mature.

I used publicly available data to model the market capitalization of bitcoin, deriving thereform a set of three curves forming a logarithmic growth channel for the market capitalization of bitcoin. Using the time series for the circulating supply, we derive a logarithmic growth channel for the bitcoin price.

Model uses publicly available data from July 17, 2010 to December 31, 2022. Everything since the beginning of 2023 is a prediction.

Past performance is not a guarantee of future results.

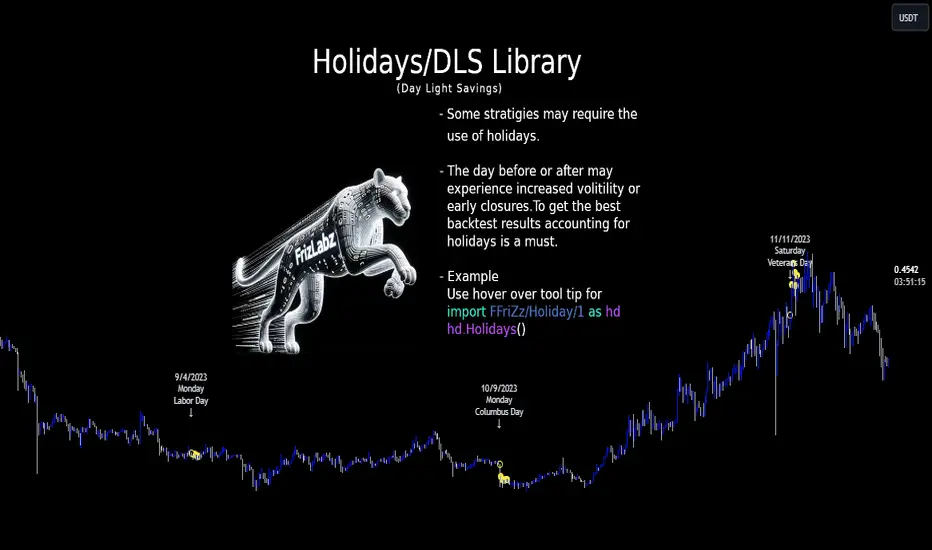

HolidayLibrary "Holiday"

- Full Control over Holidays and Daylight Savings Time (DLS)

The Holiday Library is an essential tool for traders and analysts who engage in backtesting and live trading . This comprehensive library enables the incorporation of crucial calendar elements - specifically Daylight Savings Time (DLS) adjustments and public holidays - into trading strategies and backtesting environments.

Key Features:

- DLS Adjustments: The library takes into account the shifts in time due to Daylight Savings. This feature is particularly vital for backtesting strategies, as DLS can impact trading hours, which in turn affects the volatility and liquidity in the market. Accurate DLS adjustments ensure that backtesting scenarios are as close to real-life conditions as possible.