Simple 17 Indicator BFThis is an indicator version of my Simple 17 script.

The rules are simple, when the price closes after crossing above the MA, we have a long signal. When the price closes after crossing below the MA we have a short signal.

I have set up alerts that fire upon these crosses, one for long, one for short.

Cari dalam skrip untuk "17个交易日涨幅第一的股票(非新股)有哪些"

Simple 17 BF 🚀A Simple Moving Average of period 17 based on ohlc4 values. We go long when price closes above it. We go short when price closes below it. No stop loss. No take profit.

This strategy is really to showcase how effective a basic system can be, and that with discipline and patience, trading does not need to be complex to yield good results over time.

You can change the Moving Average type, source and period in the settings as well as the backtesting range. I found 17 period SMA with ohlc4 to be a good fit for XBT/USD on Daily timeframe but for other pairs, the type, source and period will likely differ.

INSTRUCTIONS

Red turns to Green = Long Entry/Short Exit

Green turns to Red = Short Entry/Long Exit

The entries are based on when price crosses the MA and this is what the backtest is based on. We exit the current trade when we get an opposing signal and enter the new trade.

Chicago 17:00-19:00 Overnight RangeThis indicator will map out range high and range low of previous 17:00 - 19:00 of the chart. It can also display mid range if needed

Ultimate Moving Average Package (17 MA's)Included is the:

VWAP

Current time frame 10 EMA

Current time frame 20 EMA

Current time frame 50 EMA

Current time frame 10 SMA

Current time frame 20 SMA

Current time frame 50 SMA

Daily 10 EMA

Daily 20 EMA

Daily 50 EMA

Daily 50 SMA

Daily 100 SMA

Daily 200 SMA

Weekly 100 SMA

Weekly 200 SMA

Monthly 100 SMA

Monthly 200 SMA

All Daily/Weekly/Monthly MA's can be seen on intraday charts. Current time frame MA's change depending on your time frame. Obviously you dont need all 17 on your chart but you can pick the ones you like and disable the rest.

EMA72 com Difusor - Cor Dinâmica e Espessuras Ajustadas17 EMA

72 EMA (with diffuser included, green signals buy, red signals sell)

72 EMA on the weekly chart

Ichimoku Wave Oscillator with Custom MAIchimoku Wave Oscillator with Custom MA - Pine Script Description

This script uses various types of moving averages (MA) to implement the concept of Ichimoku wave theory for wave analysis. The user can select from SMA, EMA, WMA, TEMA, SMMA to visualize the difference between short-term, medium-term, and long-term waves, while identifying potential buy and sell signals at crossover points.

Key Features:

MA Type Selection:

The user can select from SMA (Simple Moving Average), EMA (Exponential Moving Average), WMA (Weighted Moving Average), TEMA (Triple Exponential Moving Average), and SMMA (Smoothed Moving Average) to calculate the waves. This script is unique in that it combines TEMA and SMMA, distinguishing it from other simple moving average-based indicators.

TEMA (Triple Exponential Moving Average): Best suited for capturing short-term trends with quick responsiveness.

SMMA (Smoothed Moving Average): Useful for identifying long-term trends with minimal noise, providing more stable signals.

Wave Calculations:

The script calculates three waves: Wave 9-17, Wave 17-26, and Wave 9-26, each of which analyzes different time horizons.

Wave 9-17 (blue): Primarily used for analyzing short-term trends, ideal for detecting quick changes.

Wave 17-26 (red): Used to analyze medium-term trends, providing a more stable market direction.

Wave 9-26 (green): Represents long-term trends, suitable for understanding broader trend shifts.

Baseline (0 Line):

Each wave is visualized around the 0 line, where waves above the line indicate an uptrend and waves below the line indicate a downtrend. This allows for easy identification of trend reversals.

Crossover Signals:

CrossUp: When Wave 9-17 (short-term wave) crosses Wave 17-26 (medium-term wave) upward, it is considered a buy signal, indicating a potential upward trend shift.

CrossDown: When Wave 9-17 (short-term wave) crosses Wave 17-26 downward, it is considered a sell signal, indicating a potential downward trend shift.

Background Color for Signal:

The script visually highlights the signals with background colors. When a buy signal occurs, the background turns green, and when a sell signal occurs, the background turns red. This makes it easier to spot reversal points.

Calculation Method:

The script calculates the difference between moving averages to display the wave oscillation. Wave 9-17, Wave 17-26, and Wave 9-26 represent the difference between the moving averages for different time periods, allowing for analysis of short-term, medium-term, and long-term trends.

Wave 9-17 = MA(9) - MA(17): Represents the difference between the short-term moving averages.

Wave 17-26 = MA(17) - MA(26): Represents the difference between medium-term moving averages.

Wave 9-26 = MA(9) - MA(26): Provides insight into the long-term trend.

This calculation method effectively visualizes the oscillation of waves and helps identify trend reversals at crossover points.

Uniqueness of the Script:

Unlike other moving average-based indicators, this script combines TEMA (Triple Exponential Moving Average) and SMMA (Smoothed Moving Average) to capture both short-term sensitivity and long-term stability in trends. This duality makes the script more versatile for different market conditions.

TEMA is ideal for short-term traders who need quick signals, while SMMA is useful for long-term investors seeking stability and noise reduction. By combining these two, this script provides a more refined analysis of trend changes across various timeframes.

How to Use:

This script is effective for trend analysis and reversal detection. By visualizing the crossover points between the waves, users can spot potential buy and sell signals to make more informed trading decisions.

Scalping strategies can rely on Wave 9-17 to detect quick trend changes, while those looking for medium-term trends can analyze signals from Wave 17-26.

For a broader market overview, Wave 9-26 helps users understand the long-term market trend.

This script is built on the concept of wave theory to anticipate trend changes, making it suitable for various timeframes and strategies. The user can tailor the characteristics of the waves by selecting different MA types, allowing for flexible application across different trading strategies.

Ichimoku Wave Oscillator with Custom MA - Pine Script 설명

이 스크립트는 다양한 이동 평균(MA) 유형을 활용하여 일목 파동론의 개념을 기반으로 파동 분석을 시도하는 지표입니다. 사용자는 SMA, EMA, WMA, TEMA, SMMA 중 원하는 이동 평균을 선택할 수 있으며, 이를 통해 단기, 중기, 장기 파동 간의 차이를 시각화하고, 교차점에서 상승 및 하락 신호를 포착할 수 있습니다.

주요 기능:

이동 평균(MA) 유형 선택:

사용자는 SMA(단순 이동 평균), EMA(지수 이동 평균), WMA(가중 이동 평균), TEMA(삼중 지수 이동 평균), SMMA(평활 이동 평균) 중 하나를 선택하여 파동을 계산할 수 있습니다. 이 스크립트는 TEMA와 SMMA의 독창적인 조합을 통해 기존의 단순한 이동 평균 지표와 차별화됩니다.

TEMA(삼중 지수 이동 평균): 빠른 반응으로 단기 트렌드를 포착하는 데 적합합니다.

SMMA(평활 이동 평균): 장기적인 추세를 파악하는 데 유용하며, 노이즈를 최소화하여 안정적인 신호를 제공합니다.

파동(Wave) 계산:

이 스크립트는 Wave 9-17, Wave 17-26, Wave 9-26의 세 가지 파동을 계산하여 각각 단기, 중기, 장기 추세를 분석합니다.

Wave 9-17 (파란색): 주로 단기 추세를 분석하는 데 사용되며, 빠른 추세 변화를 포착하는 데 유용합니다.

Wave 17-26 (빨간색): 중기 추세를 분석하는 데 사용되며, 좀 더 안정적인 시장 흐름을 보여줍니다.

Wave 9-26 (녹색): 장기 추세를 나타내며, 큰 흐름의 방향성을 파악하는 데 적합합니다.

기준선(0 라인):

각 파동은 0 라인을 기준으로 변동성을 시각화합니다. 0 위에 있는 파동은 상승세, 0 아래에 있는 파동은 하락세를 나타내며, 이를 통해 추세의 전환을 쉽게 확인할 수 있습니다.

파동 교차 신호:

CrossUp: Wave 9-17(단기 파동)이 Wave 17-26(중기 파동)을 상향 교차할 때, 상승 신호로 간주됩니다. 이는 단기적인 추세 변화가 발생할 수 있음을 의미합니다.

CrossDown: Wave 9-17(단기 파동)이 Wave 17-26(중기 파동)을 하향 교차할 때, 하락 신호로 해석됩니다. 이는 시장이 약세로 돌아설 가능성을 나타냅니다.

배경 색상 표시:

교차 신호가 발생할 때, 상승 신호는 녹색 배경, 하락 신호는 빨간색 배경으로 시각적으로 강조되어 사용자가 신호를 쉽게 인식할 수 있습니다.

계산 방식:

이 스크립트는 이동 평균 간의 차이를 계산하여 각 파동의 변동성을 나타냅니다. Wave 9-17, Wave 17-26, Wave 9-26은 각각 설정된 주기의 이동 평균(MA)의 차이를 통해, 시장의 단기, 중기, 장기 추세 변화를 시각적으로 표현합니다.

Wave 9-17 = MA(9) - MA(17): 단기 추세의 차이를 나타냅니다.

Wave 17-26 = MA(17) - MA(26): 중기 추세의 차이를 나타냅니다.

Wave 9-26 = MA(9) - MA(26): 장기적인 추세 방향을 파악할 수 있습니다.

이러한 계산 방식은 파동의 변동성을 파악하는 데 유용하며, 추세의 교차점을 통해 상승/하락 신호를 잡아냅니다.

스크립트의 독창성:

이 스크립트는 기존의 이동 평균 기반 지표들과 달리, TEMA(삼중 지수 이동 평균)와 SMMA(평활 이동 평균)을 함께 사용하여 짧은 주기와 긴 주기의 트렌드를 동시에 파악할 수 있도록 설계되었습니다. 이를 통해 단기 트렌드의 민감한 변화와 장기 트렌드의 안정성을 모두 반영합니다.

TEMA는 단기 트레이더에게 빠르고 민첩한 신호를 제공하며, SMMA는 장기 투자자에게 보다 안정적이고 긴 호흡의 트렌드를 파악하는 데 유리합니다. 두 지표의 결합으로, 다양한 시장 환경에서 추세의 변화를 더 정교하게 분석할 수 있습니다.

사용 방법:

이 스크립트는 추세 분석과 변곡점 포착에 효과적입니다. 각 파동 간의 교차점을 시각적으로 확인하고, 상승 또는 하락 신호를 포착하여 매매 시점 결정을 도울 수 있습니다.

스캘핑 전략에서는 Wave 9-17을 주로 참고하여 빠르게 추세 변화를 잡아내고, 중기 추세를 참고하고 싶은 경우 Wave 17-26을 사용해 신호를 분석할 수 있습니다.

장기적인 시장 흐름을 파악하고자 할 때는 Wave 9-26을 통해 큰 트렌드를 확인할 수 있습니다.

이 스크립트는 파동 이론의 개념을 기반으로 시장의 추세 변화를 예측하는 데 유용하며, 다양한 시간대와 전략에 맞추어 사용할 수 있습니다. 특히, 사용자가 선택한 MA 유형에 따라 파동의 특성을 변화시킬 수 있어, 여러 매매 전략에 유연하게 대응할 수 있습니다.

RSI Full Forecast [Titans_Invest]RSI Full Forecast

Get ready to experience the ultimate evolution of RSI-based indicators – the RSI Full Forecast, a boosted and even smarter version of the already powerful: RSI Forecast

Now featuring over 40 additional entry conditions (forecasts), this indicator redefines the way you view the market.

AI-Powered RSI Forecasting:

Using advanced linear regression with the least squares method – a solid foundation for machine learning - the RSI Full Forecast enables you to predict future RSI behavior with impressive accuracy.

But that’s not all: this new version also lets you monitor future crossovers between the RSI and the MA RSI, delivering early and strategic signals that go far beyond traditional analysis.

You’ll be able to monitor future crossovers up to 20 bars ahead, giving you an even broader and more precise view of market movements.

See the Future, Now:

• Track upcoming RSI & RSI MA crossovers in advance.

• Identify potential reversal zones before price reacts.

• Uncover statistical behavior patterns that would normally go unnoticed.

40+ Intelligent Conditions:

The new layer of conditions is designed to detect multiple high-probability scenarios based on historical patterns and predictive modeling. Each additional forecast is a window into the price's future, powered by robust mathematics and advanced algorithmic logic.

Full Customization:

All parameters can be tailored to fit your strategy – from smoothing periods to prediction sensitivity. You have complete control to turn raw data into smart decisions.

Innovative, Accurate, Unique:

This isn’t just an upgrade. It’s a quantum leap in technical analysis.

RSI Full Forecast is the first of its kind: an indicator that blends statistical analysis, machine learning, and visual design to create a true real-time predictive system.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the RSI, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an RSI time series like this:

Time →

RSI →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted RSI, which can be crossed with the actual RSI to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public RSI with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining RSI with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

RSI Full Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

• Overbought: When the RSI is above 70, indicating that the asset may be overbought.

• Oversold: When the RSI is below 30, indicating that the asset may be oversold.

• Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

📈 RSI Forecast:

🔹 RSI (Crossover) MA Forecast

🔹 RSI (Crossunder) MA Forecast

🔹 RSI Forecast 1 > MA Forecast 1

🔹 RSI Forecast 1 < MA Forecast 1

🔹 RSI Forecast 2 > MA Forecast 2

🔹 RSI Forecast 2 < MA Forecast 2

🔹 RSI Forecast 3 > MA Forecast 3

🔹 RSI Forecast 3 < MA Forecast 3

🔹 RSI Forecast 4 > MA Forecast 4

🔹 RSI Forecast 4 < MA Forecast 4

🔹 RSI Forecast 5 > MA Forecast 5

🔹 RSI Forecast 5 < MA Forecast 5

🔹 RSI Forecast 6 > MA Forecast 6

🔹 RSI Forecast 6 < MA Forecast 6

🔹 RSI Forecast 7 > MA Forecast 7

🔹 RSI Forecast 7 < MA Forecast 7

🔹 RSI Forecast 8 > MA Forecast 8

🔹 RSI Forecast 8 < MA Forecast 8

🔹 RSI Forecast 9 > MA Forecast 9

🔹 RSI Forecast 9 < MA Forecast 9

🔹 RSI Forecast 10 > MA Forecast 10

🔹 RSI Forecast 10 < MA Forecast 10

🔹 RSI Forecast 11 > MA Forecast 11

🔹 RSI Forecast 11 < MA Forecast 11

🔹 RSI Forecast 12 > MA Forecast 12

🔹 RSI Forecast 12 < MA Forecast 12

🔹 RSI Forecast 13 > MA Forecast 13

🔹 RSI Forecast 13 < MA Forecast 13

🔹 RSI Forecast 14 > MA Forecast 14

🔹 RSI Forecast 14 < MA Forecast 14

🔹 RSI Forecast 15 > MA Forecast 15

🔹 RSI Forecast 15 < MA Forecast 15

🔹 RSI Forecast 16 > MA Forecast 16

🔹 RSI Forecast 16 < MA Forecast 16

🔹 RSI Forecast 17 > MA Forecast 17

🔹 RSI Forecast 17 < MA Forecast 17

🔹 RSI Forecast 18 > MA Forecast 18

🔹 RSI Forecast 18 < MA Forecast 18

🔹 RSI Forecast 19 > MA Forecast 19

🔹 RSI Forecast 19 < MA Forecast 19

🔹 RSI Forecast 20 > MA Forecast 20

🔹 RSI Forecast 20 < MA Forecast 20

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

📉 RSI Forecast:

🔸 RSI (Crossover) MA Forecast

🔸 RSI (Crossunder) MA Forecast

🔸 RSI Forecast 1 > MA Forecast 1

🔸 RSI Forecast 1 < MA Forecast 1

🔸 RSI Forecast 2 > MA Forecast 2

🔸 RSI Forecast 2 < MA Forecast 2

🔸 RSI Forecast 3 > MA Forecast 3

🔸 RSI Forecast 3 < MA Forecast 3

🔸 RSI Forecast 4 > MA Forecast 4

🔸 RSI Forecast 4 < MA Forecast 4

🔸 RSI Forecast 5 > MA Forecast 5

🔸 RSI Forecast 5 < MA Forecast 5

🔸 RSI Forecast 6 > MA Forecast 6

🔸 RSI Forecast 6 < MA Forecast 6

🔸 RSI Forecast 7 > MA Forecast 7

🔸 RSI Forecast 7 < MA Forecast 7

🔸 RSI Forecast 8 > MA Forecast 8

🔸 RSI Forecast 8 < MA Forecast 8

🔸 RSI Forecast 9 > MA Forecast 9

🔸 RSI Forecast 9 < MA Forecast 9

🔸 RSI Forecast 10 > MA Forecast 10

🔸 RSI Forecast 10 < MA Forecast 10

🔸 RSI Forecast 11 > MA Forecast 11

🔸 RSI Forecast 11 < MA Forecast 11

🔸 RSI Forecast 12 > MA Forecast 12

🔸 RSI Forecast 12 < MA Forecast 12

🔸 RSI Forecast 13 > MA Forecast 13

🔸 RSI Forecast 13 < MA Forecast 13

🔸 RSI Forecast 14 > MA Forecast 14

🔸 RSI Forecast 14 < MA Forecast 14

🔸 RSI Forecast 15 > MA Forecast 15

🔸 RSI Forecast 15 < MA Forecast 15

🔸 RSI Forecast 16 > MA Forecast 16

🔸 RSI Forecast 16 < MA Forecast 16

🔸 RSI Forecast 17 > MA Forecast 17

🔸 RSI Forecast 17 < MA Forecast 17

🔸 RSI Forecast 18 > MA Forecast 18

🔸 RSI Forecast 18 < MA Forecast 18

🔸 RSI Forecast 19 > MA Forecast 19

🔸 RSI Forecast 19 < MA Forecast 19

🔸 RSI Forecast 20 > MA Forecast 20

🔸 RSI Forecast 20 < MA Forecast 20

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Full Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

PubLibCandleTrendLibrary "PubLibCandleTrend"

candle trend, multi-part candle trend, multi-part green/red candle trend, double candle trend and multi-part double candle trend conditions for indicator and strategy development

chh()

candle higher high condition

Returns: bool

chl()

candle higher low condition

Returns: bool

clh()

candle lower high condition

Returns: bool

cll()

candle lower low condition

Returns: bool

cdt()

candle double top condition

Returns: bool

cdb()

candle double bottom condition

Returns: bool

gc()

green candle condition

Returns: bool

gchh()

green candle higher high condition

Returns: bool

gchl()

green candle higher low condition

Returns: bool

gclh()

green candle lower high condition

Returns: bool

gcll()

green candle lower low condition

Returns: bool

gcdt()

green candle double top condition

Returns: bool

gcdb()

green candle double bottom condition

Returns: bool

rc()

red candle condition

Returns: bool

rchh()

red candle higher high condition

Returns: bool

rchl()

red candle higher low condition

Returns: bool

rclh()

red candle lower high condition

Returns: bool

rcll()

red candle lower low condition

Returns: bool

rcdt()

red candle double top condition

Returns: bool

rcdb()

red candle double bottom condition

Returns: bool

chh_1p()

1-part candle higher high condition

Returns: bool

chh_2p()

2-part candle higher high condition

Returns: bool

chh_3p()

3-part candle higher high condition

Returns: bool

chh_4p()

4-part candle higher high condition

Returns: bool

chh_5p()

5-part candle higher high condition

Returns: bool

chh_6p()

6-part candle higher high condition

Returns: bool

chh_7p()

7-part candle higher high condition

Returns: bool

chh_8p()

8-part candle higher high condition

Returns: bool

chh_9p()

9-part candle higher high condition

Returns: bool

chh_10p()

10-part candle higher high condition

Returns: bool

chh_11p()

11-part candle higher high condition

Returns: bool

chh_12p()

12-part candle higher high condition

Returns: bool

chh_13p()

13-part candle higher high condition

Returns: bool

chh_14p()

14-part candle higher high condition

Returns: bool

chh_15p()

15-part candle higher high condition

Returns: bool

chh_16p()

16-part candle higher high condition

Returns: bool

chh_17p()

17-part candle higher high condition

Returns: bool

chh_18p()

18-part candle higher high condition

Returns: bool

chh_19p()

19-part candle higher high condition

Returns: bool

chh_20p()

20-part candle higher high condition

Returns: bool

chh_21p()

21-part candle higher high condition

Returns: bool

chh_22p()

22-part candle higher high condition

Returns: bool

chh_23p()

23-part candle higher high condition

Returns: bool

chh_24p()

24-part candle higher high condition

Returns: bool

chh_25p()

25-part candle higher high condition

Returns: bool

chh_26p()

26-part candle higher high condition

Returns: bool

chh_27p()

27-part candle higher high condition

Returns: bool

chh_28p()

28-part candle higher high condition

Returns: bool

chh_29p()

29-part candle higher high condition

Returns: bool

chh_30p()

30-part candle higher high condition

Returns: bool

chl_1p()

1-part candle higher low condition

Returns: bool

chl_2p()

2-part candle higher low condition

Returns: bool

chl_3p()

3-part candle higher low condition

Returns: bool

chl_4p()

4-part candle higher low condition

Returns: bool

chl_5p()

5-part candle higher low condition

Returns: bool

chl_6p()

6-part candle higher low condition

Returns: bool

chl_7p()

7-part candle higher low condition

Returns: bool

chl_8p()

8-part candle higher low condition

Returns: bool

chl_9p()

9-part candle higher low condition

Returns: bool

chl_10p()

10-part candle higher low condition

Returns: bool

chl_11p()

11-part candle higher low condition

Returns: bool

chl_12p()

12-part candle higher low condition

Returns: bool

chl_13p()

13-part candle higher low condition

Returns: bool

chl_14p()

14-part candle higher low condition

Returns: bool

chl_15p()

15-part candle higher low condition

Returns: bool

chl_16p()

16-part candle higher low condition

Returns: bool

chl_17p()

17-part candle higher low condition

Returns: bool

chl_18p()

18-part candle higher low condition

Returns: bool

chl_19p()

19-part candle higher low condition

Returns: bool

chl_20p()

20-part candle higher low condition

Returns: bool

chl_21p()

21-part candle higher low condition

Returns: bool

chl_22p()

22-part candle higher low condition

Returns: bool

chl_23p()

23-part candle higher low condition

Returns: bool

chl_24p()

24-part candle higher low condition

Returns: bool

chl_25p()

25-part candle higher low condition

Returns: bool

chl_26p()

26-part candle higher low condition

Returns: bool

chl_27p()

27-part candle higher low condition

Returns: bool

chl_28p()

28-part candle higher low condition

Returns: bool

chl_29p()

29-part candle higher low condition

Returns: bool

chl_30p()

30-part candle higher low condition

Returns: bool

clh_1p()

1-part candle lower high condition

Returns: bool

clh_2p()

2-part candle lower high condition

Returns: bool

clh_3p()

3-part candle lower high condition

Returns: bool

clh_4p()

4-part candle lower high condition

Returns: bool

clh_5p()

5-part candle lower high condition

Returns: bool

clh_6p()

6-part candle lower high condition

Returns: bool

clh_7p()

7-part candle lower high condition

Returns: bool

clh_8p()

8-part candle lower high condition

Returns: bool

clh_9p()

9-part candle lower high condition

Returns: bool

clh_10p()

10-part candle lower high condition

Returns: bool

clh_11p()

11-part candle lower high condition

Returns: bool

clh_12p()

12-part candle lower high condition

Returns: bool

clh_13p()

13-part candle lower high condition

Returns: bool

clh_14p()

14-part candle lower high condition

Returns: bool

clh_15p()

15-part candle lower high condition

Returns: bool

clh_16p()

16-part candle lower high condition

Returns: bool

clh_17p()

17-part candle lower high condition

Returns: bool

clh_18p()

18-part candle lower high condition

Returns: bool

clh_19p()

19-part candle lower high condition

Returns: bool

clh_20p()

20-part candle lower high condition

Returns: bool

clh_21p()

21-part candle lower high condition

Returns: bool

clh_22p()

22-part candle lower high condition

Returns: bool

clh_23p()

23-part candle lower high condition

Returns: bool

clh_24p()

24-part candle lower high condition

Returns: bool

clh_25p()

25-part candle lower high condition

Returns: bool

clh_26p()

26-part candle lower high condition

Returns: bool

clh_27p()

27-part candle lower high condition

Returns: bool

clh_28p()

28-part candle lower high condition

Returns: bool

clh_29p()

29-part candle lower high condition

Returns: bool

clh_30p()

30-part candle lower high condition

Returns: bool

cll_1p()

1-part candle lower low condition

Returns: bool

cll_2p()

2-part candle lower low condition

Returns: bool

cll_3p()

3-part candle lower low condition

Returns: bool

cll_4p()

4-part candle lower low condition

Returns: bool

cll_5p()

5-part candle lower low condition

Returns: bool

cll_6p()

6-part candle lower low condition

Returns: bool

cll_7p()

7-part candle lower low condition

Returns: bool

cll_8p()

8-part candle lower low condition

Returns: bool

cll_9p()

9-part candle lower low condition

Returns: bool

cll_10p()

10-part candle lower low condition

Returns: bool

cll_11p()

11-part candle lower low condition

Returns: bool

cll_12p()

12-part candle lower low condition

Returns: bool

cll_13p()

13-part candle lower low condition

Returns: bool

cll_14p()

14-part candle lower low condition

Returns: bool

cll_15p()

15-part candle lower low condition

Returns: bool

cll_16p()

16-part candle lower low condition

Returns: bool

cll_17p()

17-part candle lower low condition

Returns: bool

cll_18p()

18-part candle lower low condition

Returns: bool

cll_19p()

19-part candle lower low condition

Returns: bool

cll_20p()

20-part candle lower low condition

Returns: bool

cll_21p()

21-part candle lower low condition

Returns: bool

cll_22p()

22-part candle lower low condition

Returns: bool

cll_23p()

23-part candle lower low condition

Returns: bool

cll_24p()

24-part candle lower low condition

Returns: bool

cll_25p()

25-part candle lower low condition

Returns: bool

cll_26p()

26-part candle lower low condition

Returns: bool

cll_27p()

27-part candle lower low condition

Returns: bool

cll_28p()

28-part candle lower low condition

Returns: bool

cll_29p()

29-part candle lower low condition

Returns: bool

cll_30p()

30-part candle lower low condition

Returns: bool

gc_1p()

1-part green candle condition

Returns: bool

gc_2p()

2-part green candle condition

Returns: bool

gc_3p()

3-part green candle condition

Returns: bool

gc_4p()

4-part green candle condition

Returns: bool

gc_5p()

5-part green candle condition

Returns: bool

gc_6p()

6-part green candle condition

Returns: bool

gc_7p()

7-part green candle condition

Returns: bool

gc_8p()

8-part green candle condition

Returns: bool

gc_9p()

9-part green candle condition

Returns: bool

gc_10p()

10-part green candle condition

Returns: bool

gc_11p()

11-part green candle condition

Returns: bool

gc_12p()

12-part green candle condition

Returns: bool

gc_13p()

13-part green candle condition

Returns: bool

gc_14p()

14-part green candle condition

Returns: bool

gc_15p()

15-part green candle condition

Returns: bool

gc_16p()

16-part green candle condition

Returns: bool

gc_17p()

17-part green candle condition

Returns: bool

gc_18p()

18-part green candle condition

Returns: bool

gc_19p()

19-part green candle condition

Returns: bool

gc_20p()

20-part green candle condition

Returns: bool

gc_21p()

21-part green candle condition

Returns: bool

gc_22p()

22-part green candle condition

Returns: bool

gc_23p()

23-part green candle condition

Returns: bool

gc_24p()

24-part green candle condition

Returns: bool

gc_25p()

25-part green candle condition

Returns: bool

gc_26p()

26-part green candle condition

Returns: bool

gc_27p()

27-part green candle condition

Returns: bool

gc_28p()

28-part green candle condition

Returns: bool

gc_29p()

29-part green candle condition

Returns: bool

gc_30p()

30-part green candle condition

Returns: bool

rc_1p()

1-part red candle condition

Returns: bool

rc_2p()

2-part red candle condition

Returns: bool

rc_3p()

3-part red candle condition

Returns: bool

rc_4p()

4-part red candle condition

Returns: bool

rc_5p()

5-part red candle condition

Returns: bool

rc_6p()

6-part red candle condition

Returns: bool

rc_7p()

7-part red candle condition

Returns: bool

rc_8p()

8-part red candle condition

Returns: bool

rc_9p()

9-part red candle condition

Returns: bool

rc_10p()

10-part red candle condition

Returns: bool

rc_11p()

11-part red candle condition

Returns: bool

rc_12p()

12-part red candle condition

Returns: bool

rc_13p()

13-part red candle condition

Returns: bool

rc_14p()

14-part red candle condition

Returns: bool

rc_15p()

15-part red candle condition

Returns: bool

rc_16p()

16-part red candle condition

Returns: bool

rc_17p()

17-part red candle condition

Returns: bool

rc_18p()

18-part red candle condition

Returns: bool

rc_19p()

19-part red candle condition

Returns: bool

rc_20p()

20-part red candle condition

Returns: bool

rc_21p()

21-part red candle condition

Returns: bool

rc_22p()

22-part red candle condition

Returns: bool

rc_23p()

23-part red candle condition

Returns: bool

rc_24p()

24-part red candle condition

Returns: bool

rc_25p()

25-part red candle condition

Returns: bool

rc_26p()

26-part red candle condition

Returns: bool

rc_27p()

27-part red candle condition

Returns: bool

rc_28p()

28-part red candle condition

Returns: bool

rc_29p()

29-part red candle condition

Returns: bool

rc_30p()

30-part red candle condition

Returns: bool

cdut()

candle double uptrend condition

Returns: bool

cddt()

candle double downtrend condition

Returns: bool

cdut_1p()

1-part candle double uptrend condition

Returns: bool

cdut_2p()

2-part candle double uptrend condition

Returns: bool

cdut_3p()

3-part candle double uptrend condition

Returns: bool

cdut_4p()

4-part candle double uptrend condition

Returns: bool

cdut_5p()

5-part candle double uptrend condition

Returns: bool

cdut_6p()

6-part candle double uptrend condition

Returns: bool

cdut_7p()

7-part candle double uptrend condition

Returns: bool

cdut_8p()

8-part candle double uptrend condition

Returns: bool

cdut_9p()

9-part candle double uptrend condition

Returns: bool

cdut_10p()

10-part candle double uptrend condition

Returns: bool

cdut_11p()

11-part candle double uptrend condition

Returns: bool

cdut_12p()

12-part candle double uptrend condition

Returns: bool

cdut_13p()

13-part candle double uptrend condition

Returns: bool

cdut_14p()

14-part candle double uptrend condition

Returns: bool

cdut_15p()

15-part candle double uptrend condition

Returns: bool

cdut_16p()

16-part candle double uptrend condition

Returns: bool

cdut_17p()

17-part candle double uptrend condition

Returns: bool

cdut_18p()

18-part candle double uptrend condition

Returns: bool

cdut_19p()

19-part candle double uptrend condition

Returns: bool

cdut_20p()

20-part candle double uptrend condition

Returns: bool

cdut_21p()

21-part candle double uptrend condition

Returns: bool

cdut_22p()

22-part candle double uptrend condition

Returns: bool

cdut_23p()

23-part candle double uptrend condition

Returns: bool

cdut_24p()

24-part candle double uptrend condition

Returns: bool

cdut_25p()

25-part candle double uptrend condition

Returns: bool

cdut_26p()

26-part candle double uptrend condition

Returns: bool

cdut_27p()

27-part candle double uptrend condition

Returns: bool

cdut_28p()

28-part candle double uptrend condition

Returns: bool

cdut_29p()

29-part candle double uptrend condition

Returns: bool

cdut_30p()

30-part candle double uptrend condition

Returns: bool

cddt_1p()

1-part candle double downtrend condition

Returns: bool

cddt_2p()

2-part candle double downtrend condition

Returns: bool

cddt_3p()

3-part candle double downtrend condition

Returns: bool

cddt_4p()

4-part candle double downtrend condition

Returns: bool

cddt_5p()

5-part candle double downtrend condition

Returns: bool

cddt_6p()

6-part candle double downtrend condition

Returns: bool

cddt_7p()

7-part candle double downtrend condition

Returns: bool

cddt_8p()

8-part candle double downtrend condition

Returns: bool

cddt_9p()

9-part candle double downtrend condition

Returns: bool

cddt_10p()

10-part candle double downtrend condition

Returns: bool

cddt_11p()

11-part candle double downtrend condition

Returns: bool

cddt_12p()

12-part candle double downtrend condition

Returns: bool

cddt_13p()

13-part candle double downtrend condition

Returns: bool

cddt_14p()

14-part candle double downtrend condition

Returns: bool

cddt_15p()

15-part candle double downtrend condition

Returns: bool

cddt_16p()

16-part candle double downtrend condition

Returns: bool

cddt_17p()

17-part candle double downtrend condition

Returns: bool

cddt_18p()

18-part candle double downtrend condition

Returns: bool

cddt_19p()

19-part candle double downtrend condition

Returns: bool

cddt_20p()

20-part candle double downtrend condition

Returns: bool

cddt_21p()

21-part candle double downtrend condition

Returns: bool

cddt_22p()

22-part candle double downtrend condition

Returns: bool

cddt_23p()

23-part candle double downtrend condition

Returns: bool

cddt_24p()

24-part candle double downtrend condition

Returns: bool

cddt_25p()

25-part candle double downtrend condition

Returns: bool

cddt_26p()

26-part candle double downtrend condition

Returns: bool

cddt_27p()

27-part candle double downtrend condition

Returns: bool

cddt_28p()

28-part candle double downtrend condition

Returns: bool

cddt_29p()

29-part candle double downtrend condition

Returns: bool

cddt_30p()

30-part candle double downtrend condition

Returns: bool

PubLibTrendLibrary "PubLibTrend"

trend, multi-part trend, double trend and multi-part double trend conditions for indicator and strategy development

rlut()

return line uptrend condition

Returns: bool

dt()

downtrend condition

Returns: bool

ut()

uptrend condition

Returns: bool

rldt()

return line downtrend condition

Returns: bool

dtop()

double top condition

Returns: bool

dbot()

double bottom condition

Returns: bool

rlut_1p()

1-part return line uptrend condition

Returns: bool

rlut_2p()

2-part return line uptrend condition

Returns: bool

rlut_3p()

3-part return line uptrend condition

Returns: bool

rlut_4p()

4-part return line uptrend condition

Returns: bool

rlut_5p()

5-part return line uptrend condition

Returns: bool

rlut_6p()

6-part return line uptrend condition

Returns: bool

rlut_7p()

7-part return line uptrend condition

Returns: bool

rlut_8p()

8-part return line uptrend condition

Returns: bool

rlut_9p()

9-part return line uptrend condition

Returns: bool

rlut_10p()

10-part return line uptrend condition

Returns: bool

rlut_11p()

11-part return line uptrend condition

Returns: bool

rlut_12p()

12-part return line uptrend condition

Returns: bool

rlut_13p()

13-part return line uptrend condition

Returns: bool

rlut_14p()

14-part return line uptrend condition

Returns: bool

rlut_15p()

15-part return line uptrend condition

Returns: bool

rlut_16p()

16-part return line uptrend condition

Returns: bool

rlut_17p()

17-part return line uptrend condition

Returns: bool

rlut_18p()

18-part return line uptrend condition

Returns: bool

rlut_19p()

19-part return line uptrend condition

Returns: bool

rlut_20p()

20-part return line uptrend condition

Returns: bool

rlut_21p()

21-part return line uptrend condition

Returns: bool

rlut_22p()

22-part return line uptrend condition

Returns: bool

rlut_23p()

23-part return line uptrend condition

Returns: bool

rlut_24p()

24-part return line uptrend condition

Returns: bool

rlut_25p()

25-part return line uptrend condition

Returns: bool

rlut_26p()

26-part return line uptrend condition

Returns: bool

rlut_27p()

27-part return line uptrend condition

Returns: bool

rlut_28p()

28-part return line uptrend condition

Returns: bool

rlut_29p()

29-part return line uptrend condition

Returns: bool

rlut_30p()

30-part return line uptrend condition

Returns: bool

dt_1p()

1-part downtrend condition

Returns: bool

dt_2p()

2-part downtrend condition

Returns: bool

dt_3p()

3-part downtrend condition

Returns: bool

dt_4p()

4-part downtrend condition

Returns: bool

dt_5p()

5-part downtrend condition

Returns: bool

dt_6p()

6-part downtrend condition

Returns: bool

dt_7p()

7-part downtrend condition

Returns: bool

dt_8p()

8-part downtrend condition

Returns: bool

dt_9p()

9-part downtrend condition

Returns: bool

dt_10p()

10-part downtrend condition

Returns: bool

dt_11p()

11-part downtrend condition

Returns: bool

dt_12p()

12-part downtrend condition

Returns: bool

dt_13p()

13-part downtrend condition

Returns: bool

dt_14p()

14-part downtrend condition

Returns: bool

dt_15p()

15-part downtrend condition

Returns: bool

dt_16p()

16-part downtrend condition

Returns: bool

dt_17p()

17-part downtrend condition

Returns: bool

dt_18p()

18-part downtrend condition

Returns: bool

dt_19p()

19-part downtrend condition

Returns: bool

dt_20p()

20-part downtrend condition

Returns: bool

dt_21p()

21-part downtrend condition

Returns: bool

dt_22p()

22-part downtrend condition

Returns: bool

dt_23p()

23-part downtrend condition

Returns: bool

dt_24p()

24-part downtrend condition

Returns: bool

dt_25p()

25-part downtrend condition

Returns: bool

dt_26p()

26-part downtrend condition

Returns: bool

dt_27p()

27-part downtrend condition

Returns: bool

dt_28p()

28-part downtrend condition

Returns: bool

dt_29p()

29-part downtrend condition

Returns: bool

dt_30p()

30-part downtrend condition

Returns: bool

ut_1p()

1-part uptrend condition

Returns: bool

ut_2p()

2-part uptrend condition

Returns: bool

ut_3p()

3-part uptrend condition

Returns: bool

ut_4p()

4-part uptrend condition

Returns: bool

ut_5p()

5-part uptrend condition

Returns: bool

ut_6p()

6-part uptrend condition

Returns: bool

ut_7p()

7-part uptrend condition

Returns: bool

ut_8p()

8-part uptrend condition

Returns: bool

ut_9p()

9-part uptrend condition

Returns: bool

ut_10p()

10-part uptrend condition

Returns: bool

ut_11p()

11-part uptrend condition

Returns: bool

ut_12p()

12-part uptrend condition

Returns: bool

ut_13p()

13-part uptrend condition

Returns: bool

ut_14p()

14-part uptrend condition

Returns: bool

ut_15p()

15-part uptrend condition

Returns: bool

ut_16p()

16-part uptrend condition

Returns: bool

ut_17p()

17-part uptrend condition

Returns: bool

ut_18p()

18-part uptrend condition

Returns: bool

ut_19p()

19-part uptrend condition

Returns: bool

ut_20p()

20-part uptrend condition

Returns: bool

ut_21p()

21-part uptrend condition

Returns: bool

ut_22p()

22-part uptrend condition

Returns: bool

ut_23p()

23-part uptrend condition

Returns: bool

ut_24p()

24-part uptrend condition

Returns: bool

ut_25p()

25-part uptrend condition

Returns: bool

ut_26p()

26-part uptrend condition

Returns: bool

ut_27p()

27-part uptrend condition

Returns: bool

ut_28p()

28-part uptrend condition

Returns: bool

ut_29p()

29-part uptrend condition

Returns: bool

ut_30p()

30-part uptrend condition

Returns: bool

rldt_1p()

1-part return line downtrend condition

Returns: bool

rldt_2p()

2-part return line downtrend condition

Returns: bool

rldt_3p()

3-part return line downtrend condition

Returns: bool

rldt_4p()

4-part return line downtrend condition

Returns: bool

rldt_5p()

5-part return line downtrend condition

Returns: bool

rldt_6p()

6-part return line downtrend condition

Returns: bool

rldt_7p()

7-part return line downtrend condition

Returns: bool

rldt_8p()

8-part return line downtrend condition

Returns: bool

rldt_9p()

9-part return line downtrend condition

Returns: bool

rldt_10p()

10-part return line downtrend condition

Returns: bool

rldt_11p()

11-part return line downtrend condition

Returns: bool

rldt_12p()

12-part return line downtrend condition

Returns: bool

rldt_13p()

13-part return line downtrend condition

Returns: bool

rldt_14p()

14-part return line downtrend condition

Returns: bool

rldt_15p()

15-part return line downtrend condition

Returns: bool

rldt_16p()

16-part return line downtrend condition

Returns: bool

rldt_17p()

17-part return line downtrend condition

Returns: bool

rldt_18p()

18-part return line downtrend condition

Returns: bool

rldt_19p()

19-part return line downtrend condition

Returns: bool

rldt_20p()

20-part return line downtrend condition

Returns: bool

rldt_21p()

21-part return line downtrend condition

Returns: bool

rldt_22p()

22-part return line downtrend condition

Returns: bool

rldt_23p()

23-part return line downtrend condition

Returns: bool

rldt_24p()

24-part return line downtrend condition

Returns: bool

rldt_25p()

25-part return line downtrend condition

Returns: bool

rldt_26p()

26-part return line downtrend condition

Returns: bool

rldt_27p()

27-part return line downtrend condition

Returns: bool

rldt_28p()

28-part return line downtrend condition

Returns: bool

rldt_29p()

29-part return line downtrend condition

Returns: bool

rldt_30p()

30-part return line downtrend condition

Returns: bool

dut()

double uptrend condition

Returns: bool

ddt()

double downtrend condition

Returns: bool

dut_1p()

1-part double uptrend condition

Returns: bool

dut_2p()

2-part double uptrend condition

Returns: bool

dut_3p()

3-part double uptrend condition

Returns: bool

dut_4p()

4-part double uptrend condition

Returns: bool

dut_5p()

5-part double uptrend condition

Returns: bool

dut_6p()

6-part double uptrend condition

Returns: bool

dut_7p()

7-part double uptrend condition

Returns: bool

dut_8p()

8-part double uptrend condition

Returns: bool

dut_9p()

9-part double uptrend condition

Returns: bool

dut_10p()

10-part double uptrend condition

Returns: bool

dut_11p()

11-part double uptrend condition

Returns: bool

dut_12p()

12-part double uptrend condition

Returns: bool

dut_13p()

13-part double uptrend condition

Returns: bool

dut_14p()

14-part double uptrend condition

Returns: bool

dut_15p()

15-part double uptrend condition

Returns: bool

dut_16p()

16-part double uptrend condition

Returns: bool

dut_17p()

17-part double uptrend condition

Returns: bool

dut_18p()

18-part double uptrend condition

Returns: bool

dut_19p()

19-part double uptrend condition

Returns: bool

dut_20p()

20-part double uptrend condition

Returns: bool

dut_21p()

21-part double uptrend condition

Returns: bool

dut_22p()

22-part double uptrend condition

Returns: bool

dut_23p()

23-part double uptrend condition

Returns: bool

dut_24p()

24-part double uptrend condition

Returns: bool

dut_25p()

25-part double uptrend condition

Returns: bool

dut_26p()

26-part double uptrend condition

Returns: bool

dut_27p()

27-part double uptrend condition

Returns: bool

dut_28p()

28-part double uptrend condition

Returns: bool

dut_29p()

29-part double uptrend condition

Returns: bool

dut_30p()

30-part double uptrend condition

Returns: bool

ddt_1p()

1-part double downtrend condition

Returns: bool

ddt_2p()

2-part double downtrend condition

Returns: bool

ddt_3p()

3-part double downtrend condition

Returns: bool

ddt_4p()

4-part double downtrend condition

Returns: bool

ddt_5p()

5-part double downtrend condition

Returns: bool

ddt_6p()

6-part double downtrend condition

Returns: bool

ddt_7p()

7-part double downtrend condition

Returns: bool

ddt_8p()

8-part double downtrend condition

Returns: bool

ddt_9p()

9-part double downtrend condition

Returns: bool

ddt_10p()

10-part double downtrend condition

Returns: bool

ddt_11p()

11-part double downtrend condition

Returns: bool

ddt_12p()

12-part double downtrend condition

Returns: bool

ddt_13p()

13-part double downtrend condition

Returns: bool

ddt_14p()

14-part double downtrend condition

Returns: bool

ddt_15p()

15-part double downtrend condition

Returns: bool

ddt_16p()

16-part double downtrend condition

Returns: bool

ddt_17p()

17-part double downtrend condition

Returns: bool

ddt_18p()

18-part double downtrend condition

Returns: bool

ddt_19p()

19-part double downtrend condition

Returns: bool

ddt_20p()

20-part double downtrend condition

Returns: bool

ddt_21p()

21-part double downtrend condition

Returns: bool

ddt_22p()

22-part double downtrend condition

Returns: bool

ddt_23p()

23-part double downtrend condition

Returns: bool

ddt_24p()

24-part double downtrend condition

Returns: bool

ddt_25p()

25-part double downtrend condition

Returns: bool

ddt_26p()

26-part double downtrend condition

Returns: bool

ddt_27p()

27-part double downtrend condition

Returns: bool

ddt_28p()

28-part double downtrend condition

Returns: bool

ddt_29p()

29-part double downtrend condition

Returns: bool

ddt_30p()

30-part double downtrend condition

Returns: bool

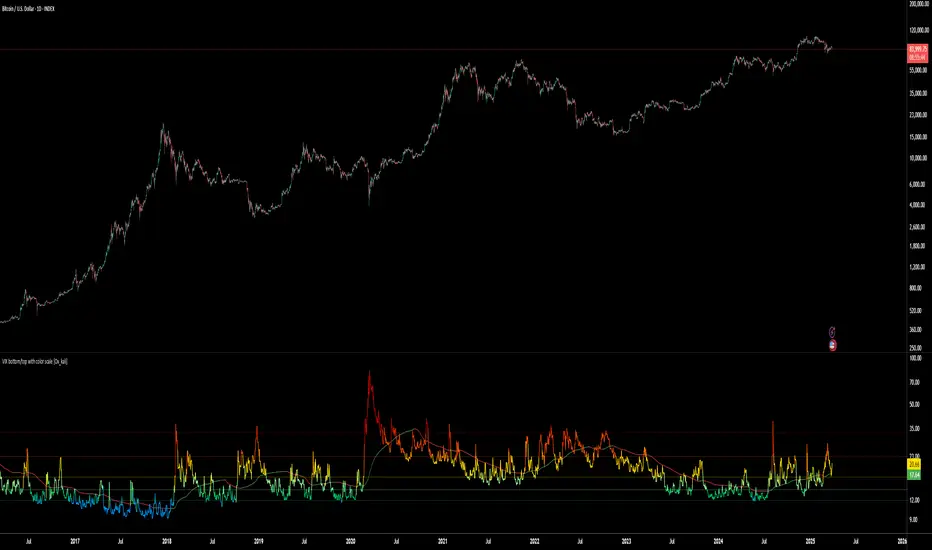

VIX bottom/top with color scale [Ox_kali]📊 Introduction

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The “VIX Bottom/Top with Color Scale” script is designed to provide an intuitive, color-coded visualization of the VIX (Volatility Index), helping traders interpret market sentiment and volatility extremes in real time.

It segments the VIX into clear threshold zones, each associated with a specific market condition—ranging from fear to calm—using a dynamic color-coded system.

This script offers significant value for the following reasons:

Intuitive Risk Interpretation: Color-coded zones make it easy to interpret market sentiment at a glance.

Dynamic Trend Detection: A 200-period SMA of the VIX is plotted and dynamically colored based on trend direction.

Customization and Flexibility: All colors are editable in the parameters panel, grouped under “## Color parameters ##”.

Visual Clarity: Key thresholds are marked with horizontal lines for quick reference.

Practical Trading Tool: Helps identify high-risk and low-risk environments based on volatility levels.

🔍 Key Indicators

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

VIX (CBOE Volatility Index) : Measures market volatility and investor fear.

SMA 200 : Long-term trendline of the VIX, with color-coded direction (green = uptrend, red = downtrend).

Color-coded VIX Levels:

🔴 33+ → Something bad just happened

🟠 23–33 → Something bad is happening

🟡 17–23 → Something bad might happen

🟢 14–17 → Nothing bad is happening

✅ 12–14 → Nothing bad will ever happen

🔵 <12 → Something bad is going to happen

🧠 Originality and Purpose

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Unlike traditional VIX indicators that only plot a line, this script enhances interpretation through visual segmentation and dynamic trend tracking.

It serves as a risk-awareness tool that transforms the VIX into a simple, emotional market map.

This is the first version of the script, and future updates may include alerts, background fills, and more advanced features.

⚙️ How It Works

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The script maps the current VIX value to a range and applies the corresponding color.

It calculates a SMA 200 and colors it green or red depending on its slope.

It displays horizontal dotted lines at key thresholds (12, 14, 17, 23, 33).

All colors are configurable via input parameters under the group: "## Color parameters ##".

🧭 Indicator Visualization and Interpretation

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The VIX line changes color based on market condition zones.

The SMA line shows long-term direction with dynamic color.

Horizontal threshold lines visually mark the transitions between volatility zones.

Ideal for quickly identifying periods of fear, caution, or stability.

🛠️ Script Parameters

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Grouped under “## Color parameters ##”, the following elements are customizable:

🎨 VIX Zone Colors:

33+ → Red

23–33 → Orange

17–23 → Yellow

14–17 → Light Green

12–14 → Dark Green

<12 → Blue

📈 SMA Colors:

Uptrend → Green

Downtrend → Red

These settings allow users to match the script’s visuals to their preferred chart style or theme.

✅ Conclusion

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

The “VIX Bottom/Top with Color Scale” is a clean, powerful script designed to simplify how traders view volatility.

By combining long-term trend data with real-time color-coded sentiment analysis, this script becomes a go-to reference for managing risk, timing trades, or simply staying in tune with market mood.

🧪 Notes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This is version 1 of the script. More features such as alert conditions, background fill, and dashboard elements may be added soon. Feedback is welcome!

💡 Color code concept inspired by the original VIX interpretation chart by @nsquaredvalue on Twitter. Big thanks for the visual clarity! 💡

⚠️ Disclaimer

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This script is a visual tool designed to assist in market analysis. It does not guarantee future performance and should be used in conjunction with proper risk management. Past performance is not indicative of future results.

Super EMA PrismThis script implements the Binary Trade Logic (BTL) algorithm to calculate two distinct scores that range from 0 to 7. One score is calculated assigning a power of 2 weight to the positive sign of 3 Phi^3 distant Moving Average (MA) slopes. The other score is calculated assigning a power of 2 weight to the sign of the difference between the price and the value of 3 Phi^3 distant Moving Average (MA).

For the first score, hereafter called as the angle score (AS), the largest MA slope positive sign receives weight 4, the middle length MA slope positive sign receives weight 2 and the shortest MA slope positive sign receives weight 1. The positive sign of an MA is defined as 1 if the slope of the MA is positive and 0, otherwise. Therefore, for MAs 305, 72 and 17, if slope(MA305) > 0, slope(MA72) < 0 and slope(MA17) > 0, then score will be 4*1 + 2*0 + 1*1 = 5. Up to my knowledge, this score was first proposed by Bo Williams and named by him as Prisma.

For the second score, hereafter called as the value score (VS), if the price > largest MA, it receives weight 4. If the price > the middle length MA, it receives weight 2 and if the price > the the shortest MA, it receives weight 1. Therefore, for MAs 305, 72 and 17, if price < MA305, price > MA72 and price > MA17, then score will be 4*0 + 2*1 + 1*1 = 3. Up to my knowledge, this score was first proposed by Bo Williams and named by him as Prisma.

Both AS and VS are calculated for Phi^3 lengths (610, 144, 34) and for Phi^3/2 lengths (305, 72, 17). The scores of the same kind calculated for each set of length are combined multiplying the Phi^3 length score by 10 and adding with with the Phi^3/2 score, therefore providing a 2 digit score ranging from 0 to 77. For instance, if we have AS(610, 144, 34) = 7 and AS(305, 72, 17) = 5, we have AS=75. At the same time, if we have VS(610, 144, 34) = 6 and VS(305, 72, 17) = 4, we have VS=64.

VS score is plotted by default in black, but it can be on white for dark themes. AS is plotted with the color of the longest MA used.

Chart background is colored according to the range of values for AS and VS, checked in the following order:

if AS >= 13 and VS <= 13 then back color = red

if AS >= 13 or VS <= 13 then back color = orange

if AS >= 64 and VS >= 64 then back color = green

if AS >= 64 or VS >= 64 then back color = blue

otherwise back color = none (white o black)

Optimized Future Time Cycles V2Time Cycle-Based Indicator Overview

This script utilizes Time Cycles to visually display the periodic fluctuations of the past and future, helping to predict key market turning points and trend shifts.

The indicator is fully customizable and marks periodic vertical lines and labels on the chart based on a specified reference date.

1. Key Features

Time Cycle Settings

Displays various user-defined time cycles (e.g., 9 days, 17 days, 26 days) visually on the chart.

Each cycle is distinguished by unique colors and labels for clear identification.

Allows users to set a reference date, from which past and future cycles are calculated.

Past and Future Cycle Visualization

Future Cycles:

Predicts potential points of market fluctuations or trend changes in the future.

Vertical lines represent future turning points based on the defined time cycles.

Past Cycles:

Displays how cyclical patterns manifested in historical market data.

Helps identify recurring patterns and similar historical market conditions.

Customizable Visuals

Adjust line styles (solid, dashed, etc.) and label spacing for a cleaner chart, even with multiple cycles displayed.

Separately toggle the visibility of past and future cycles for a more tailored analysis experience.

2. How to Use and Interpret the Indicator

Setting the Reference Date

The reference date is crucial for this indicator and works best when set to significant market events or turning points.

Both past and future cycles are calculated based on the reference date, and overlapping cycles may indicate periods of high volatility or strong trend shifts.

Cycle Analysis

Interpretation by Cycle Duration:

Short-term Cycles (9, 17 days): Useful for predicting quick market fluctuations.

Mid- to Long-term Cycles (26, 52, 200 days): Ideal for identifying major trend changes.

Overlapping Cycles:

When multiple cycles converge, significant turning points or strong market movements are likely.

Importance of Past Cycles

Past cycles are invaluable for identifying repetitive patterns in the market.

For example, analyzing strong turning points from past cycles can help anticipate similar scenarios in the future.

3. Tips for Using the Indicator

Optimize Line Styles:

When displaying both past and future cycles, charts may become cluttered. Adjusting line styles or colors can help maintain visual clarity.

Short-term vs. Long-term Cycles:

Short-term Cycles: Best suited for strategies like scalping or day trading.

Long-term Cycles: Useful for capturing major trend shifts or identifying macroeconomic changes.

Recommended Combination with Other Indicators:

Combine the Time Cycle indicator with moving averages, wave indicators, RSI, or Bollinger Bands for better results.

The time cycle identifies the timing of turning points, while tools like moving averages or RSI provide insights into trend direction during these critical moments.

4. Conclusion

This Time Cycle indicator visualizes past and future periodic fluctuations, enabling effective predictions of market trends and turning points.

The reference date and overlapping cycles are essential for pinpointing critical turning points.

The newly added past cycle visualization feature enhances the ability to recognize recurring patterns and leverage historical data for more accurate predictions.

시간 주기(Time Cycle) 기반 지표 소개

이 스크립트는 **시간 주기(Time Cycle)**를 활용해 과거와 미래의 주기적 변동을 시각적으로 보여주어, 시장의 추세 변화 시점과 변곡점을 예측하는 데 도움을 줍니다.

지표는 사용자 정의가 가능하며, 설정된 기준 날짜를 기반으로 주기적인 수직선과 레이블을 차트에 표시합니다.

1. 주요 기능

시간 주기 설정

사용자가 설정한 다양한 시간 주기(예: 9일, 17일, 26일 등)를 시각적으로 표시.

각 주기는 고유한 색상과 레이블로 구분되어 명확하게 차트에 나타납니다.

**기준 날짜(reference date)**를 설정하여, 해당 날짜를 기준으로 과거와 미래의 주기를 계산합니다.

미래와 과거 주기 표시

미래 주기:

미래의 시장 변동 시점이나 추세 변화 가능성이 높은 지점을 예측할 수 있습니다.

설정된 시간 주기에 따라 미래 변곡점을 차트에 수직선으로 나타냅니다.

과거 주기:

과거 시장에서 주기적 변동이 어떻게 나타났는지 확인 가능합니다.

이를 통해 반복되는 패턴이나 과거와 유사한 시장 상황을 파악할 수 있습니다.

시각적 사용자 설정

수직선 스타일(실선, 점선 등)과 레이블 간격을 조정하여, 복잡한 차트에서도 깔끔하게 정보를 확인할 수 있습니다.

과거와 미래의 주기 표시를 개별적으로 조정 가능하여 사용자 맞춤형 분석이 가능합니다.

2. 지표 사용 및 해석 방법

기준 날짜 설정

**기준 날짜(reference date)**는 시장에서 중요한 변동이 있었던 날을 기준으로 설정하는 것이 가장 효과적입니다.

기준 날짜를 기반으로 과거와 미래 주기가 계산되며, 주기가 겹치는 시점에서 강한 변동성이 나타날 가능성이 높습니다.

주기 분석

주기별 해석:

단기 주기 (9일, 17일): 빠른 변동성을 예측.

중·장기 주기 (26일, 52일, 200일): 큰 추세 변화를 예측.

주기가 겹치는 시점은 중요한 변곡점이 될 가능성이 크며, 추세 전환의 신호로 볼 수 있습니다.

과거 주기의 중요성

과거 주기는 시장의 반복 패턴을 찾는 데 유용합니다.

예를 들어, 과거 주기에서 강한 변곡점이 나타났던 시점을 분석하면, 미래에도 유사한 상황이 발생할 가능성을 예측할 수 있습니다.

3. 지표 활용 팁

수직선 스타일 최적화:

과거와 미래 주기를 모두 표시하면 차트가 복잡해질 수 있으므로, 선 스타일이나 색상을 조정하여 시각적으로 덜 혼란스럽게 설정하세요.

단기 vs. 장기 주기:

단기 주기는 스캘핑과 같은 빠른 매매 전략에 유용하며,

장기 주기는 대세 추세 변화를 포착하는 데 유리합니다.

결합 사용 추천:

시간 주기(Time Cycle) 지표는 이평선 파동 지표 또는 RSI, 볼린저 밴드와 함께 사용하면 더욱 효과적입니다.

시간 주기는 변곡점의 시점을 알려주고, 이평선 파동이나 RSI는 그 시점에서의 추세 방향성을 보완해 줍니다.

4. 결론

이 시간 주기(Time Cycle) 지표는 과거와 미래의 주기적 변동을 시각화하여, 시장의 추세 변화와 변곡점을 효과적으로 예측할 수 있습니다.

특히, 기준 날짜 설정과 주기적 겹침은 중요한 변곡점을 파악하는 핵심입니다.

새롭게 추가된 과거 주기 표시 기능은 반복 패턴을 확인하고 과거 데이터를 바탕으로 더 정교한 예측을 가능하게 합니다.

Cycles 90mThe cycles are separated by vertical lines. The first cycle (Q1) is marked with a red line because it is a manipulative cycle where you should not open positions. Other cycles are green (Q2, Q3, Q4).

You can add the time of the current candle, its size and position on the chart in the settings

The time is highlighted in red in the timeframes 9:30-9:40, 10:00-10:10, 11:00-11:30, 15:30-15:40, 16:00-16:10, 17:00-17:10, 17:30-17:40, as price movements are most often expected during these timeframes.

The cycle lines automatically disappear if you open a timeframe above M15

Custom EMA PrismThis script implements the Binary Logic Trading (BLT) algorithm to calculate a score from 0 to 7. This score is calculated assigning a power of 2 weight to the positive sign of 3 Phi^3 distant EMAs' slopes. The largest EMA slope positive sign receives weight 4, the middle length EMA slope positive sign receives weight 2 and the shortest EMA slope positive sign receives weight 1. The positive sign of an EMA is defined as 1 if the slope of the EMA is positive and 0, otherwise. Therefore, for EMAs 305, 72 and 17, if slope(EMA305) > 0, slope(EMA72) < 0 and slope(EMA17) > 0, then score will be 4*1 + 2*0 + 1*1 = 5. Up to my knowledge, this score was first proposed by Bo Williams and named by him as Prisma.

Due too sampling issues, this script ONLY WORKS with graphic time of 1d. I would like to thanks to MrBitmanBob for showing me how to get quotations from a graphic time distinct from the current one.

This script also gets sampling data from graphic times 2h and 30m to calculate their score. As, even for smaller graphic times, price data is sampled at the current time frequency, the EMA lengths for those smaller graphic times needed to be proportionally decreased, meaning that when calculating the score for 1d with lengths 305, 72 and 17, the score for 2h must be calculated with lengths 72, 17 and 4, and the score for 30m must be calculated with lengths 17, 4 an 1. I understand that some precision may be lost but it is the best that is possible.

There is an optional setting for Crypto Currencies that instead of calculating the score for 1d, 2h and 30m, it calculates the score for 1d, 4h and 60m. This is due to the fact that Crypto Currencies are traded 24x7. Despite of this setting, the labels at the Style tab of the settings window remains 2h and 30m, because they must be constants.

This script with the corresponding EMAs chart and the EMAs Angle chart provides a broader view of the trading scenario.

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.