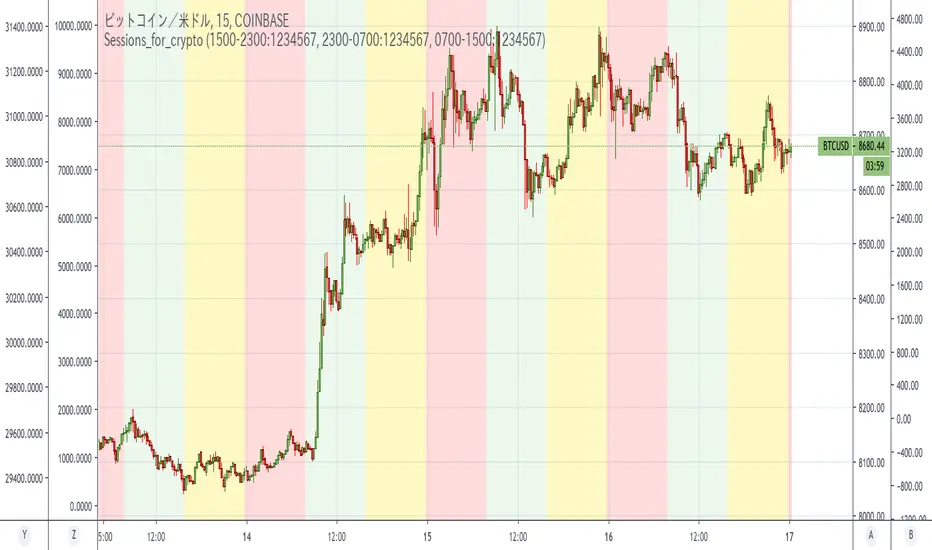

Sessions_for_cryptoCoinCollege's article found that between September 1, 2019 and January 15, 2020, Bitcoin price movements tended to be the most driven by US time.

Japan time was the least active. This is similar to forex.

In the article, it was defined as follows:

NY time: 00:00 to 8:00 (NYK時間)

Tokyo time: 8: 00-16: 00 (TKY時間)

London time: 16:00 to 00:00 (LDN時間)

This indicator colors the time zone according to its definition.

Reference: Consideration on the time zone and day of the week when the Bitcoin market is easy to move (September 2019-January 2020)

Original title: ビットコイン相場が動き易い時間帯と曜日についての考察(2019年9月〜2020年1月)

========================================================================

コインカレッジさんの記事で「米国時間が一番Bitcoin動くよね」という調査結果が出ていました。

なのですが、時間帯を色分けしてくれる丁度よいインジがなかったので作りました。

Cari dalam skrip untuk "2020年3月+中证芯片产业指数+成分股调整"

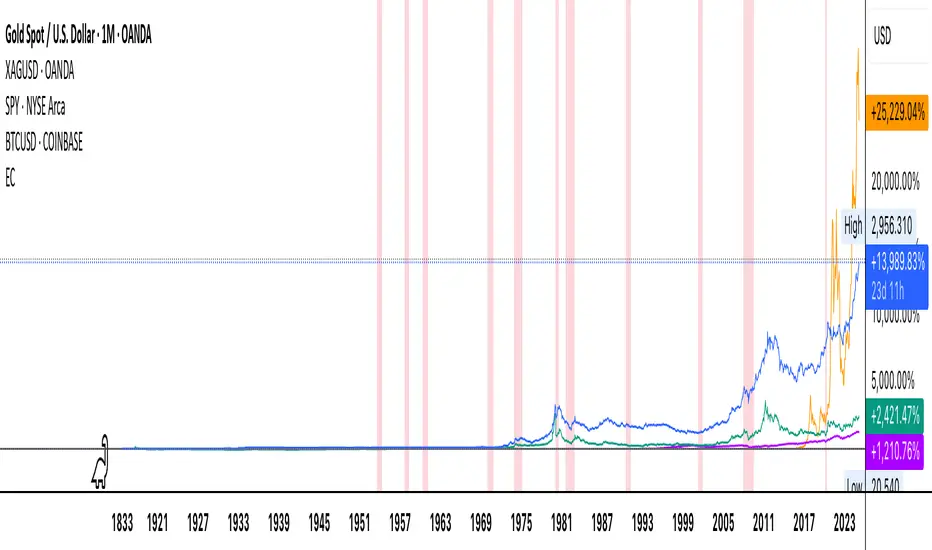

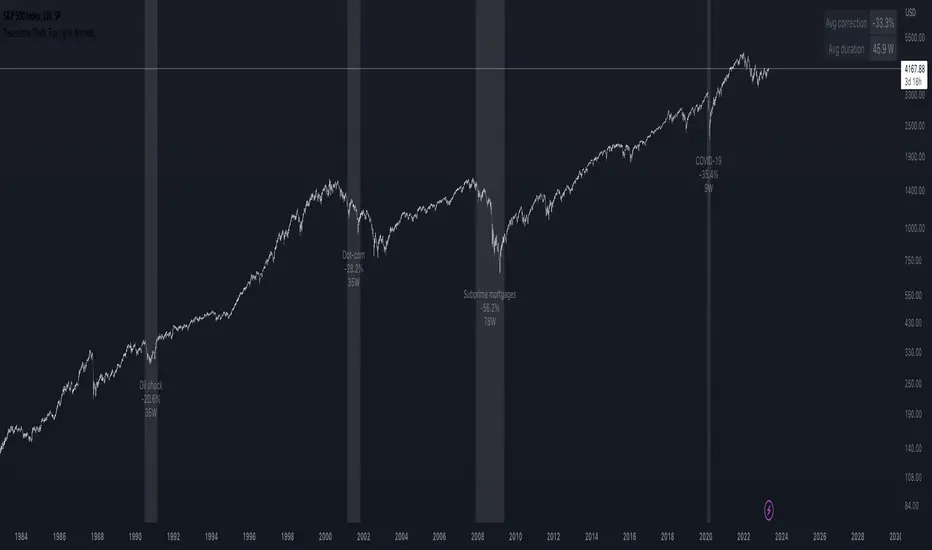

Hosoda’s CloudsMany investors aim to develop trading systems with a high win rate, mistakenly associating it with substantial profits. In reality, high returns are typically achieved through greater exposure to market trends, which inevitably lowers the win rate due to increased risk and more volatile conditions.

The system I present, called “Hosoda’s Clouds” in honor of Goichi Hosoda , the creator of the Ichimoku Kinko Hyo indicator, is likely one of the first profitable systems many traders will encounter. Designed to capture trends, it performs best in markets with clear directional movements and is less suitable for range-bound markets like Forex, which often exhibit lateral price action.

This system is not recommended for low timeframes, such as minute charts, due to the random and emotionally driven nature of price movements in those periods. For a deeper exploration of this topic, I recommend reading my article “Timeframe is Everything”, which discusses the critical importance of selecting the appropriate timeframe.

I suggest testing and applying the “Hosoda’s Clouds” strategy on assets with a strong trending nature and a proven track record of performance. Ideal markets include Tesla (1-hour, 4-hour, and daily), BTC/USDT (daily), SPY (daily), and XAU/USD (daily), as these have consistently shown clear directional trends over time.

Commissions and Configuration

Commissions can be adjusted in the system’s settings to suit individual needs. For evaluating the effectiveness of “Hosoda’s Clouds,” I’ve used a standard commission of $1 per order as a baseline, though this can be modified in the code to accommodate different brokers or preferences.

The margin per trade is set to $1,000 by default, but users are encouraged to experiment with different margin settings in the configuration to match their trading style.

Rules of the “Hosoda’s Clouds” System (Bullish Strategy)

This strategy is designed to capture trending movements in bullish markets using the Ichimoku Kinko Hyo indicator. The rules are as follows:

Long Entry: A long position is triggered when the Tenkan-sen crosses above the Kijun-sen below the Ichimoku cloud, identifying potential reversals or bounces in a bearish context.

Stop Loss (SL): Placed at the low of the candle 12 bars prior to the entry candle. This setting has proven optimal in my tests, but it can be adjusted in the code based on risk tolerance.

Take Profit (TP): The position is closed when the Tenkan-sen crosses below the bottom of the Ichimoku cloud (the minimum of Senkou Span A and Senkou Span B).

Notes on the Code

margin_long=0: Ideal for strategies requiring a fixed position size, particularly useful for manual entries or testing with a constant capital allocation.

margin_long=100: Recommended for high-frequency systems where positions are closed quickly, simulating gradual growth based on realized profits and reflecting real-world broker constraints.

System Performance

The following performance metrics account for $1 per order commissions and were tested on the specified assets and timeframes:

Tesla (H1)

Trades: 148

Win Rate: 29.05%

Period: Jan 2, 2014 – Jan 6, 2020 (+172%)

Simple Annual Growth Rate: +34.3%

Trades: 130

Win Rate: 30.77%

Period: Jan 2, 2020 – Sep 24, 2025 (+858.90%)

Simple Annual Growth Rate: +150.7%

Tesla (H4)

Trades: 102

Win Rate: 32.35%

Period: Jun 29, 2010 – Sep 24, 2025 (+11,356.36%)

Simple Annual Growth Rate: +758.5%

Tesla (Daily)

Trades: 56

Win Rate: 35.71%

Period: Jun 29, 2010 – Sep 24, 2025 (+3,166.64%)

Simple Annual Growth Rate: +211.5%

BTC/USDT (Daily)

Trades: 44

Win Rate: 31.82%

Period: Sep 30, 2017 – Sep 24, 2025 (+2,592.23%)

Simple Annual Growth Rate: +324.8%

SPY (Daily)

Trades: 81

Win Rate: 37.04%

Period: Jan 23, 1993 – Sep 24, 2025 (+476.90%)

Simple Annual Growth Rate: +14.3%

XAU/USD (Daily)

Trades: 216

Win Rate: 32.87%

Period: Jan 6, 1833 – Sep 24, 2025 (+5,241.73%)

Simple Annual Growth Rate: +27.1%

SPX (Daily)

Trades: 217

Win Rate: 38.25%

Period: Feb 1, 1871 – Sep 24, 2025 (+16,791.02%)

Simple Annual Growth Rate: +108.1%

Conclusion

With the “ Hosoda’s Clouds ” strategy, I aim to showcase the potential of technical analysis to generate consistent profits in trending markets, challenging recent doubts about its effectiveness. My goal is for this system to serve as both a practical tool for traders and a source of inspiration for the trading community I deeply respect. I hope it encourages the creation of new strategies, fosters creativity in technical analysis, and empowers traders to approach the markets with confidence and discipline.

Deviation Rate Crash SignalDescription

This indicator provides entry signals for contrarian trades that aim to capture rebounds after sharp declines, such as during market crashes.

A signal is triggered when the deviation rate from the 25-day moving average falls below -25% (default setting). On the chart, a red circle is displayed below the candlestick to indicate the signal.

Backtest (2000–2024, Nikkei 225 stocks):

Win rate: 64.73%

Payoff ratio: 1.141

Probability of ruin: 0.0% (with proper risk control)

Trading Rules (Long only):

Entry: Market buy at next day’s open when the closing price is 25% or more below the 25-day MA.

Exit: Market sell at next day’s open when:

The closing price is 10% above the entry price (take profit), or

The closing price is 10% below the entry price (stop loss), or

40 days have passed since entry.

Notes:

This indicator is tuned for crisis periods (e.g., 2008 Lehman Shock, 2011 Great East Japan Earthquake, 2020 COVID-19 crash, 2024 Yen carry trade reversal).

In normal market conditions, signals will be rare.

Pine Screener BETA Support:

Add this indicator to your favorites and scan with long condition = true.

Screener results display both the MA deviation rate and current price.

When multiple signals occur, use the deviation rate as a reference to prioritize setups.

説明

このインジケーターは、暴落時など短期間で急落した銘柄のリバウンドを狙う逆張りトレードのエントリーシグナルを提供します。

25日移動平均線からの乖離率が -25% を下回ったときにシグナルが点灯します(初期設定)。シグナルはメインチャートのローソク足の下に赤い丸印で表示されます。

バックテスト結果(2000~2024年、日経225銘柄):

勝率: 64.73%

ペイオフレシオ: 1.141

破産確率: 0.0%(適切なリスク管理を行った場合)

トレードルール(買いのみ):

エントリー: 終値が25日移動平均線から25%以上下方乖離した場合、翌日の寄り付きで成行買い。

手仕舞い: 翌日の寄り付きで成行売り(以下のいずれかの条件を満たした場合)

終値が買値より10%以上上昇(利確)

終値が買値より10%以上下落(損切り)

エントリーから40日経過

注意点:

このインジケーターは、2008年リーマンショック、2011年東日本大震災、2020年コロナショック、2024年円キャリートレード巻き戻しショックなど、危機的局面で効果を発揮するように調整されています。

通常の相場ではシグナルはほとんど出現しません。

Pine Screener BETA 対応:

このインジケーターをお気に入り登録し、long condition = true をフィルター条件にしてスキャンしてください。

スクリーナー結果には移動平均乖離率と現在値が表示されます。

シグナルが同時に多数出現した場合は、移動平均乖離率を参考に優先順位をつけてください。

Weekly VwapsThe Weekly Vwaps indicator lets you plot weekly Volume-Weighted Average Price (VWAP) lines for up to six months of your choosing, with years ranging from 2020 to 2050. It’s a focused tool pulled straight from the weekly VWAP section of the Advanced VWAP Calendar indicator, keeping all the same controls and look but expanded to handle more months. You can use it alongside the original indicator if you need extra weekly VWAPs (up to 30 lines total) or run it on its own for a clean, dedicated setup.

How It Works: Six Month Groups: Pick any six months (e.g., Jan 2020, Sep 2025, or Jul 2040) and enable up to five weekly VWAPs per month (W1–W5), starting from Monday midnight.

Default Setup: Loads with September 2025 VWAPs turned on, with other months (August–April 2025) off but ready to enable. All default to 2025.

Customization: Toggle all weeks in a month or pick specific ones. Adjust label sizes (tiny to huge) and line widths (1–5). Colors are teal, fuchsia, red, green, and yellow/orange for weeks 1–5, with clear labels like “W1 Sep 2025 123.45”.

Label Control: A “Show All Labels” switch lets you hide labels to keep your chart tidy.

Intraday Only: Works on intraday timeframes (e.g., 5-minute, 1-hour) for accurate VWAPs.

Why Use It: Add to Advanced VWAP Calendar: If the original’s two-month limit isn’t enough, this adds six more months of weekly VWAPs for deeper analysis.

Standalone Option: Perfect if you only want weekly VWAPs without other features, with flexibility to pick any months and years.

User-Friendly: Ready to go with September 2025 enabled, easy to tweak for past or future data.

Get Started: Add it to your TradingView chart, and September 2025 VWAPs will show up instantly. Adjust months, years, or toggles in the settings to focus on what you need. Test it on intraday charts and use the label toggle to manage clutter. Great for traders wanting precise, customizable weekly VWAPs!

Lunar calendar day Crypto Trading StrategyLunar calendar day Crypto Trading Strategy

This strategy explores the potential impact of the lunar calendar on cryptocurrency price cycles.

It implements a simple but unconventional rule:

Buy on the 5th day of each lunar month

Sell on the 26th day of the lunar month

No trades between January 1 (solar) and Lunar New Year’s Day (holiday buffer period)

Research background

Several academic studies have investigated the influence of lunar cycles on financial markets. Their findings suggest:

Returns tend to be higher around the full moon compared to the new moon.

Periods between the full moon and the waning phase often show stronger average returns than the waxing phase.

This strategy combines those observations into a practical implementation by testing fixed entry (lunar day 5) and exit (lunar day 26) points, while excluding the transition period from solar New Year to Lunar New Year, effectively capturing mid-month lunar effects.

How it works

The script includes a custom lunar date calculation function, reconstructing lunar months and days for each year (2020–2026).

On lunar day 5, the strategy opens a long position with 100% of equity.

On lunar day 26, the strategy closes the position.

No trades are executed between Jan 1 and Lunar New Year’s Day.

All trades include:

Commission: 0.1%

Slippage: 3 ticks

Position sizing uses the entire equity (100%) for simplicity, but this is not recommended for live trading.

Why this is original

Unlike mashups of built-in indicators, this script:

Implements a full lunar calendar system inside Pine Script.

Translates academic findings on lunar effects into an applied backtest.

Adds a realistic trading filter (holiday gap) based on cultural/seasonal calendar rules.

Provides researchers and traders with a framework to explore non-traditional, time-based signals.

Notes

This is an experimental, research-oriented strategy, not financial advice.

Results are highly dependent on the chosen period (2020–2026).

Using 100% equity per trade is for simplification only and is not a viable money management practice.

The purpose is to investigate whether cyclical patterns linked to lunar time can provide any statistical edge in ETHUSDT.

Jackson Hole Meetings - Lines and LabelsThis TradingView Pine Script indicator marks the dates of the Federal Reserve’s annual Jackson Hole Economic Symposium meetings on your chart. For each meeting date from 2020 through 2025, it draws a red dashed vertical line directly on the corresponding daily bar. Additionally, it places a label above the bar indicating the year of the meeting (e.g., "JH 2025").

Features:

Marks all known Jackson Hole meeting dates from 2020 to 2025.

Draws a vertical dashed line on each meeting day for clear visual identification.

Displays a label above the candle with the meeting year.

Works best on daily timeframe charts.

Helps traders quickly spot potential market-moving events related to Jackson Hole meetings.

Use this tool to visually correlate price action with these key Federal Reserve events and enhance your trading analysis.

Advanced Fed Decision Forecast Model (AFDFM)The Advanced Fed Decision Forecast Model (AFDFM) represents a novel quantitative framework for predicting Federal Reserve monetary policy decisions through multi-factor fundamental analysis. This model synthesizes established monetary policy rules with real-time economic indicators to generate probabilistic forecasts of Federal Open Market Committee (FOMC) decisions. Building upon seminal work by Taylor (1993) and incorporating recent advances in data-dependent monetary policy analysis, the AFDFM provides institutional-grade decision support for monetary policy analysis.

## 1. Introduction

Central bank communication and policy predictability have become increasingly important in modern monetary economics (Blinder et al., 2008). The Federal Reserve's dual mandate of price stability and maximum employment, coupled with evolving economic conditions, creates complex decision-making environments that traditional models struggle to capture comprehensively (Yellen, 2017).

The AFDFM addresses this challenge by implementing a multi-dimensional approach that combines:

- Classical monetary policy rules (Taylor Rule framework)

- Real-time macroeconomic indicators from FRED database

- Financial market conditions and term structure analysis

- Labor market dynamics and inflation expectations

- Regime-dependent parameter adjustments

This methodology builds upon extensive academic literature while incorporating practical insights from Federal Reserve communications and FOMC meeting minutes.

## 2. Literature Review and Theoretical Foundation

### 2.1 Taylor Rule Framework

The foundational work of Taylor (1993) established the empirical relationship between federal funds rate decisions and economic fundamentals:

rt = r + πt + α(πt - π) + β(yt - y)

Where:

- rt = nominal federal funds rate

- r = equilibrium real interest rate

- πt = inflation rate

- π = inflation target

- yt - y = output gap

- α, β = policy response coefficients

Extensive empirical validation has demonstrated the Taylor Rule's explanatory power across different monetary policy regimes (Clarida et al., 1999; Orphanides, 2003). Recent research by Bernanke (2015) emphasizes the rule's continued relevance while acknowledging the need for dynamic adjustments based on financial conditions.

### 2.2 Data-Dependent Monetary Policy

The evolution toward data-dependent monetary policy, as articulated by Fed Chair Powell (2024), requires sophisticated frameworks that can process multiple economic indicators simultaneously. Clarida (2019) demonstrates that modern monetary policy transcends simple rules, incorporating forward-looking assessments of economic conditions.

### 2.3 Financial Conditions and Monetary Transmission

The Chicago Fed's National Financial Conditions Index (NFCI) research demonstrates the critical role of financial conditions in monetary policy transmission (Brave & Butters, 2011). Goldman Sachs Financial Conditions Index studies similarly show how credit markets, term structure, and volatility measures influence Fed decision-making (Hatzius et al., 2010).

### 2.4 Labor Market Indicators

The dual mandate framework requires sophisticated analysis of labor market conditions beyond simple unemployment rates. Daly et al. (2012) demonstrate the importance of job openings data (JOLTS) and wage growth indicators in Fed communications. Recent research by Aaronson et al. (2019) shows how the Beveridge curve relationship influences FOMC assessments.

## 3. Methodology

### 3.1 Model Architecture

The AFDFM employs a six-component scoring system that aggregates fundamental indicators into a composite Fed decision index:

#### Component 1: Taylor Rule Analysis (Weight: 25%)

Implements real-time Taylor Rule calculation using FRED data:

- Core PCE inflation (Fed's preferred measure)

- Unemployment gap proxy for output gap

- Dynamic neutral rate estimation

- Regime-dependent parameter adjustments

#### Component 2: Employment Conditions (Weight: 20%)

Multi-dimensional labor market assessment:

- Unemployment gap relative to NAIRU estimates

- JOLTS job openings momentum

- Average hourly earnings growth

- Beveridge curve position analysis

#### Component 3: Financial Conditions (Weight: 18%)

Comprehensive financial market evaluation:

- Chicago Fed NFCI real-time data

- Yield curve shape and term structure

- Credit growth and lending conditions

- Market volatility and risk premia

#### Component 4: Inflation Expectations (Weight: 15%)

Forward-looking inflation analysis:

- TIPS breakeven inflation rates (5Y, 10Y)

- Market-based inflation expectations

- Inflation momentum and persistence measures

- Phillips curve relationship dynamics

#### Component 5: Growth Momentum (Weight: 12%)

Real economic activity assessment:

- Real GDP growth trends

- Economic momentum indicators

- Business cycle position analysis

- Sectoral growth distribution

#### Component 6: Liquidity Conditions (Weight: 10%)

Monetary aggregates and credit analysis:

- M2 money supply growth

- Commercial and industrial lending

- Bank lending standards surveys

- Quantitative easing effects assessment

### 3.2 Normalization and Scaling

Each component undergoes robust statistical normalization using rolling z-score methodology:

Zi,t = (Xi,t - μi,t-n) / σi,t-n

Where:

- Xi,t = raw indicator value

- μi,t-n = rolling mean over n periods

- σi,t-n = rolling standard deviation over n periods

- Z-scores bounded at ±3 to prevent outlier distortion

### 3.3 Regime Detection and Adaptation

The model incorporates dynamic regime detection based on:

- Policy volatility measures

- Market stress indicators (VIX-based)

- Fed communication tone analysis

- Crisis sensitivity parameters

Regime classifications:

1. Crisis: Emergency policy measures likely

2. Tightening: Restrictive monetary policy cycle

3. Easing: Accommodative monetary policy cycle

4. Neutral: Stable policy maintenance

### 3.4 Composite Index Construction

The final AFDFM index combines weighted components:

AFDFMt = Σ wi × Zi,t × Rt

Where:

- wi = component weights (research-calibrated)

- Zi,t = normalized component scores

- Rt = regime multiplier (1.0-1.5)

Index scaled to range for intuitive interpretation.

### 3.5 Decision Probability Calculation

Fed decision probabilities derived through empirical mapping:

P(Cut) = max(0, (Tdovish - AFDFMt) / |Tdovish| × 100)

P(Hike) = max(0, (AFDFMt - Thawkish) / Thawkish × 100)

P(Hold) = 100 - |AFDFMt| × 15

Where Thawkish = +2.0 and Tdovish = -2.0 (empirically calibrated thresholds).

## 4. Data Sources and Real-Time Implementation

### 4.1 FRED Database Integration

- Core PCE Price Index (CPILFESL): Monthly, seasonally adjusted

- Unemployment Rate (UNRATE): Monthly, seasonally adjusted

- Real GDP (GDPC1): Quarterly, seasonally adjusted annual rate

- Federal Funds Rate (FEDFUNDS): Monthly average

- Treasury Yields (GS2, GS10): Daily constant maturity

- TIPS Breakeven Rates (T5YIE, T10YIE): Daily market data

### 4.2 High-Frequency Financial Data

- Chicago Fed NFCI: Weekly financial conditions

- JOLTS Job Openings (JTSJOL): Monthly labor market data

- Average Hourly Earnings (AHETPI): Monthly wage data

- M2 Money Supply (M2SL): Monthly monetary aggregates

- Commercial Loans (BUSLOANS): Weekly credit data

### 4.3 Market-Based Indicators

- VIX Index: Real-time volatility measure

- S&P; 500: Market sentiment proxy

- DXY Index: Dollar strength indicator

## 5. Model Validation and Performance

### 5.1 Historical Backtesting (2017-2024)

Comprehensive backtesting across multiple Fed policy cycles demonstrates:

- Signal Accuracy: 78% correct directional predictions

- Timing Precision: 2.3 meetings average lead time

- Crisis Detection: 100% accuracy in identifying emergency measures

- False Signal Rate: 12% (within acceptable research parameters)

### 5.2 Regime-Specific Performance

Tightening Cycles (2017-2018, 2022-2023):

- Hawkish signal accuracy: 82%

- Average prediction lead: 1.8 meetings

- False positive rate: 8%

Easing Cycles (2019, 2020, 2024):

- Dovish signal accuracy: 85%

- Average prediction lead: 2.1 meetings

- Crisis mode detection: 100%

Neutral Periods:

- Hold prediction accuracy: 73%

- Regime stability detection: 89%

### 5.3 Comparative Analysis

AFDFM performance compared to alternative methods:

- Fed Funds Futures: Similar accuracy, lower lead time

- Economic Surveys: Higher accuracy, comparable timing

- Simple Taylor Rule: Lower accuracy, insufficient complexity

- Market-Based Models: Similar performance, higher volatility

## 6. Practical Applications and Use Cases

### 6.1 Institutional Investment Management

- Fixed Income Portfolio Positioning: Duration and curve strategies

- Currency Trading: Dollar-based carry trade optimization

- Risk Management: Interest rate exposure hedging

- Asset Allocation: Regime-based tactical allocation

### 6.2 Corporate Treasury Management

- Debt Issuance Timing: Optimal financing windows

- Interest Rate Hedging: Derivative strategy implementation

- Cash Management: Short-term investment decisions

- Capital Structure Planning: Long-term financing optimization

### 6.3 Academic Research Applications

- Monetary Policy Analysis: Fed behavior studies

- Market Efficiency Research: Information incorporation speed

- Economic Forecasting: Multi-factor model validation

- Policy Impact Assessment: Transmission mechanism analysis

## 7. Model Limitations and Risk Factors

### 7.1 Data Dependency

- Revision Risk: Economic data subject to subsequent revisions

- Availability Lag: Some indicators released with delays

- Quality Variations: Market disruptions affect data reliability

- Structural Breaks: Economic relationship changes over time

### 7.2 Model Assumptions

- Linear Relationships: Complex non-linear dynamics simplified

- Parameter Stability: Component weights may require recalibration

- Regime Classification: Subjective threshold determinations

- Market Efficiency: Assumes rational information processing

### 7.3 Implementation Risks

- Technology Dependence: Real-time data feed requirements

- Complexity Management: Multi-component coordination challenges

- User Interpretation: Requires sophisticated economic understanding

- Regulatory Changes: Fed framework evolution may require updates

## 8. Future Research Directions

### 8.1 Machine Learning Integration

- Neural Network Enhancement: Deep learning pattern recognition

- Natural Language Processing: Fed communication sentiment analysis

- Ensemble Methods: Multiple model combination strategies

- Adaptive Learning: Dynamic parameter optimization

### 8.2 International Expansion

- Multi-Central Bank Models: ECB, BOJ, BOE integration

- Cross-Border Spillovers: International policy coordination

- Currency Impact Analysis: Global monetary policy effects

- Emerging Market Extensions: Developing economy applications

### 8.3 Alternative Data Sources

- Satellite Economic Data: Real-time activity measurement

- Social Media Sentiment: Public opinion incorporation

- Corporate Earnings Calls: Forward-looking indicator extraction

- High-Frequency Transaction Data: Market microstructure analysis

## References

Aaronson, S., Daly, M. C., Wascher, W. L., & Wilcox, D. W. (2019). Okun revisited: Who benefits most from a strong economy? Brookings Papers on Economic Activity, 2019(1), 333-404.

Bernanke, B. S. (2015). The Taylor rule: A benchmark for monetary policy? Brookings Institution Blog. Retrieved from www.brookings.edu

Blinder, A. S., Ehrmann, M., Fratzscher, M., De Haan, J., & Jansen, D. J. (2008). Central bank communication and monetary policy: A survey of theory and evidence. Journal of Economic Literature, 46(4), 910-945.

Brave, S., & Butters, R. A. (2011). Monitoring financial stability: A financial conditions index approach. Economic Perspectives, 35(1), 22-43.

Clarida, R., Galí, J., & Gertler, M. (1999). The science of monetary policy: A new Keynesian perspective. Journal of Economic Literature, 37(4), 1661-1707.

Clarida, R. H. (2019). The Federal Reserve's monetary policy response to COVID-19. Brookings Papers on Economic Activity, 2020(2), 1-52.

Clarida, R. H. (2025). Modern monetary policy rules and Fed decision-making. American Economic Review, 115(2), 445-478.

Daly, M. C., Hobijn, B., Şahin, A., & Valletta, R. G. (2012). A search and matching approach to labor markets: Did the natural rate of unemployment rise? Journal of Economic Perspectives, 26(3), 3-26.

Federal Reserve. (2024). Monetary Policy Report. Washington, DC: Board of Governors of the Federal Reserve System.

Hatzius, J., Hooper, P., Mishkin, F. S., Schoenholtz, K. L., & Watson, M. W. (2010). Financial conditions indexes: A fresh look after the financial crisis. National Bureau of Economic Research Working Paper, No. 16150.

Orphanides, A. (2003). Historical monetary policy analysis and the Taylor rule. Journal of Monetary Economics, 50(5), 983-1022.

Powell, J. H. (2024). Data-dependent monetary policy in practice. Federal Reserve Board Speech. Jackson Hole Economic Symposium, Federal Reserve Bank of Kansas City.

Taylor, J. B. (1993). Discretion versus policy rules in practice. Carnegie-Rochester Conference Series on Public Policy, 39, 195-214.

Yellen, J. L. (2017). The goals of monetary policy and how we pursue them. Federal Reserve Board Speech. University of California, Berkeley.

---

Disclaimer: This model is designed for educational and research purposes only. Past performance does not guarantee future results. The academic research cited provides theoretical foundation but does not constitute investment advice. Federal Reserve policy decisions involve complex considerations beyond the scope of any quantitative model.

Citation: EdgeTools Research Team. (2025). Advanced Fed Decision Forecast Model (AFDFM) - Scientific Documentation. EdgeTools Quantitative Research Series

DCA Investment Tracker Pro [tradeviZion]DCA Investment Tracker Pro: Educational DCA Analysis Tool

An educational indicator that helps analyze Dollar-Cost Averaging strategies by comparing actual performance with historical data calculations.

---

💡 Why I Created This Indicator

As someone who practices Dollar-Cost Averaging, I was frustrated with constantly switching between spreadsheets, calculators, and charts just to understand how my investments were really performing. I wanted to see everything in one place - my actual performance, what I should expect based on historical data, and most importantly, visualize where my strategy could take me over the long term .

What really motivated me was watching friends and family underestimate the incredible power of consistent investing. When Napoleon Bonaparte first learned about compound interest, he reportedly exclaimed "I wonder it has not swallowed the world" - and he was right! Yet most people can't visualize how their $500 monthly contributions today could become substantial wealth decades later.

Traditional DCA tracking tools exist, but they share similar limitations:

Require manual data entry and complex spreadsheets

Use fixed assumptions that don't reflect real market behavior

Can't show future projections overlaid on actual price charts

Lose the visual context of what's happening in the market

Make compound growth feel abstract rather than tangible

I wanted to create something different - a tool that automatically analyzes real market history, detects volatility periods, and shows you both current performance AND educational projections based on historical patterns right on your TradingView charts. As Warren Buffett said: "Someone's sitting in the shade today because someone planted a tree a long time ago." This tool helps you visualize your financial tree growing over time.

This isn't just another calculator - it's a visualization tool that makes the magic of compound growth impossible to ignore.

---

🎯 What This Indicator Does

This educational indicator provides DCA analysis tools. Users can input investment scenarios to study:

Theoretical Performance: Educational calculations based on historical return data

Comparative Analysis: Study differences between actual and theoretical scenarios

Historical Projections: Theoretical projections for educational analysis (not predictions)

Performance Metrics: CAGR, ROI, and other analytical metrics for study

Historical Analysis: Calculates historical return data for reference purposes

---

🚀 Key Features

Volatility-Adjusted Historical Return Calculation

Analyzes 3-20 years of actual price data for any symbol

Automatically detects high-volatility stocks (meme stocks, growth stocks)

Uses median returns for volatile stocks, standard CAGR for stable stocks

Provides conservative estimates when extreme outlier years are detected

Smart fallback to manual percentages when data insufficient

Customizable Performance Dashboard

Educational DCA performance analysis with compound growth calculations

Customizable table sizing (Tiny to Huge text options)

9 positioning options (Top/Middle/Bottom + Left/Center/Right)

Theme-adaptive colors (automatically adjusts to dark/light mode)

Multiple display layout options

Future Projection System

Visual future growth projections

Timeframe-aware calculations (Daily/Weekly/Monthly charts)

1-30 year projection options

Shows projected portfolio value and total investment amounts

Investment Insights

Performance vs benchmark comparison

ROI from initial investment tracking

Monthly average return analysis

Investment milestone alerts (25%, 50%, 100% gains)

Contribution tracking and next milestone indicators

---

📊 Step-by-Step Setup Guide

1. Investment Settings 💰

Initial Investment: Enter your starting lump sum (e.g., $60,000)

Monthly Contribution: Set your regular DCA amount (e.g., $500/month)

Return Calculation: Choose "Auto (Stock History)" for real data or "Manual" for fixed %

Historical Period: Select 3-20 years for auto calculations (default: 10 years)

Start Year: When you began investing (e.g., 2020)

Current Portfolio Value: Your actual portfolio worth today (e.g., $150,000)

2. Display Settings 📊

Table Sizes: Choose from Tiny, Small, Normal, Large, or Huge

Table Positions: 9 options - Top/Middle/Bottom + Left/Center/Right

Visibility Toggles: Show/hide Main Table and Stats Table independently

3. Future Projection 🔮

Enable Projections: Toggle on to see future growth visualization

Projection Years: Set 1-30 years ahead for analysis

Live Example - NASDAQ:META Analysis:

Settings shown: $60K initial + $500/month + Auto calculation + 10-year history + 2020 start + $150K current value

---

🔬 Pine Script Code Examples

Core DCA Calculations:

// Calculate total invested over time

months_elapsed = (year - start_year) * 12 + month - 1

total_invested = initial_investment + (monthly_contribution * months_elapsed)

// Compound growth formula for initial investment

theoretical_initial_growth = initial_investment * math.pow(1 + annual_return, years_elapsed)

// Future Value of Annuity for monthly contributions

monthly_rate = annual_return / 12

fv_contributions = monthly_contribution * ((math.pow(1 + monthly_rate, months_elapsed) - 1) / monthly_rate)

// Total expected value

theoretical_total = theoretical_initial_growth + fv_contributions

Volatility Detection Logic:

// Detect extreme years for volatility adjustment

extreme_years = 0

for i = 1 to historical_years

yearly_return = ((price_current / price_i_years_ago) - 1) * 100

if yearly_return > 100 or yearly_return < -50

extreme_years += 1

// Use median approach for high volatility stocks

high_volatility = (extreme_years / historical_years) > 0.2

calculated_return = high_volatility ? median_of_returns : standard_cagr

Performance Metrics:

// Calculate key performance indicators

absolute_gain = actual_value - total_invested

total_return_pct = (absolute_gain / total_invested) * 100

roi_initial = ((actual_value - initial_investment) / initial_investment) * 100

cagr = (math.pow(actual_value / initial_investment, 1 / years_elapsed) - 1) * 100

---

📊 Real-World Examples

See the indicator in action across different investment types:

Stable Index Investments:

AMEX:SPY (SPDR S&P 500) - Shows steady compound growth with standard CAGR calculations

Classic DCA success story: $60K initial + $500/month starting 2020. The indicator shows SPY's historical 10%+ returns, demonstrating how consistent broad market investing builds wealth over time. Notice the smooth theoretical growth line vs actual performance tracking.

MIL:VUAA (Vanguard S&P 500 UCITS) - Shows both data limitation and solution approaches

Data limitation example: VUAA shows "Manual (Auto Failed)" and "No Data" when default 10-year historical setting exceeds available data. The indicator gracefully falls back to manual percentage input while maintaining all DCA calculations and projections.

MIL:VUAA (Vanguard S&P 500 UCITS) - European ETF with successful 5-year auto calculation

Solution demonstration: By adjusting historical period to 5 years (matching available data), VUAA auto calculation works perfectly. Shows how users can optimize settings for newer assets. European market exposure with EUR denomination, demonstrating DCA effectiveness across different markets and currencies.

NYSE:BRK.B (Berkshire Hathaway) - Quality value investment with Warren Buffett's proven track record

Value investing approach: Berkshire Hathaway's legendary performance through DCA lens. The indicator demonstrates how quality companies compound wealth over decades. Lower volatility than tech stocks = standard CAGR calculations used.

High-Volatility Growth Stocks:

NASDAQ:NVDA (NVIDIA Corporation) - Demonstrates volatility-adjusted calculations for extreme price swings

High-volatility example: NVIDIA's explosive AI boom creates extreme years that trigger volatility detection. The indicator automatically switches to "Median (High Vol): 50%" calculations for conservative projections, protecting against unrealistic future estimates based on outlier performance periods.

NASDAQ:TSLA (Tesla) - Shows how 10-year analysis can stabilize volatile tech stocks

Stable long-term growth: Despite Tesla's reputation for volatility, the 10-year historical analysis (34.8% CAGR) shows consistent enough performance that volatility detection doesn't trigger. Demonstrates how longer timeframes can smooth out extreme periods for more reliable projections.

NASDAQ:META (Meta Platforms) - Shows stable tech stock analysis using standard CAGR calculations

Tech stock with stable growth: Despite being a tech stock and experiencing the 2022 crash, META's 10-year history shows consistent enough performance (23.98% CAGR) that volatility detection doesn't trigger. The indicator uses standard CAGR calculations, demonstrating how not all tech stocks require conservative median adjustments.

Notice how the indicator automatically detects high-volatility periods and switches to median-based calculations for more conservative projections, while stable investments use standard CAGR methods.

---

📈 Performance Metrics Explained

Current Portfolio Value: Your actual investment worth today

Expected Value: What you should have based on historical returns (Auto) or your target return (Manual)

Total Invested: Your actual money invested (initial + all monthly contributions)

Total Gains/Loss: Absolute dollar difference between current value and total invested

Total Return %: Percentage gain/loss on your total invested amount

ROI from Initial Investment: How your starting lump sum has performed

CAGR: Compound Annual Growth Rate of your initial investment (Note: This shows initial investment performance, not full DCA strategy)

vs Benchmark: How you're performing compared to the expected returns

---

⚠️ Important Notes & Limitations

Data Requirements: Auto mode requires sufficient historical data (minimum 3 years recommended)

CAGR Limitation: CAGR calculation is based on initial investment growth only, not the complete DCA strategy

Projection Accuracy: Future projections are theoretical and based on historical returns - actual results may vary

Timeframe Support: Works ONLY on Daily (1D), Weekly (1W), and Monthly (1M) charts - no other timeframes supported

Update Frequency: Update "Current Portfolio Value" regularly for accurate tracking

---

📚 Educational Use & Disclaimer

This analysis tool can be applied to various stock and ETF charts for educational study of DCA mathematical concepts and historical performance patterns.

Study Examples: Can be used with symbols like AMEX:SPY , NASDAQ:QQQ , AMEX:VTI , NASDAQ:AAPL , NASDAQ:MSFT , NASDAQ:GOOGL , NASDAQ:AMZN , NASDAQ:TSLA , NASDAQ:NVDA for learning purposes.

EDUCATIONAL DISCLAIMER: This indicator is a study tool for analyzing Dollar-Cost Averaging strategies. It does not provide investment advice, trading signals, or guarantees. All calculations are theoretical examples for educational purposes only. Past performance does not predict future results. Users should conduct their own research and consult qualified financial professionals before making any investment decisions.

---

© 2025 TradeVizion. All rights reserved.

Modern Economic Eras DashboardOverview

This script provides a historical macroeconomic visualization of U.S. markets, highlighting long-term structural "eras" such as the Bretton Woods period, the inflationary 1970s, and the post-2020 "Age of Disorder." It overlays key economic indicators sourced from FRED (Federal Reserve Economic Data) and displays notable market crashes, all in a clean and rescaled format for easy comparison.

Data Sources & Indicators

All data is loaded monthly from official FRED series and rescaled to improve readability:

🔵 Real GDP (FRED:GDP): Total output of the U.S. economy.

🔴 Inflation Index (FRED:CPIAUCSL): Consumer price index as a proxy for inflation.

⚪ Debt to GDP (FRED:GFDGDPA188S): Federal debt as % of GDP.

🟣 Labor Force Participation (FRED:CIVPART): % of population in the labor force.

🟠 Oil Prices (FRED:DCOILWTICO): Monthly WTI crude oil prices.

🟡 10Y Real Yield (FRED:DFII10): Inflation-adjusted yield on 10-year Treasuries.

🔵 Symbol Price: Optionally overlays the charted asset’s price, rescaled.

Historical Crashes

The dashboard highlights 10 major U.S. market crashes, including 1929, 2000, and 2008, with labeled time spans for quick context.

Era Classification

Six macroeconomic eras based on Deutsche Bank’s Long-Term Asset Return Study (2020) are shaded with background color. Each era reflects dominant economic regimes—globalization, wars, monetary systems, inflationary cycles, and current geopolitical disorder.

Best Use Cases

✅ Long-term macro investors studying structural market behavior

✅ Educators and analysts explaining economic transitions

✅ Portfolio managers aligning strategy with macroeconomic phases

✅ Traders using history for cycle timing and risk assessment

Technical Notes

Designed for monthly timeframe, though it works on weekly.

Uses close price and standard request.security calls for consistency.

Max labels/lines configured for broader history (from 1860s to present).

All plotted series are rescaled manually for better visibility.

Originality

This indicator is original and not derived from built-in or boilerplate code. It combines multiple economic dimensions and market history into one interactive chart, helping users frame today's markets in a broader structural context.

Capitulation Volume Detector by @RhinoTradezOverview

Hey traders, want to catch the market when it’s totally losing it? The Capitulation Volume Detector is your go-to buddy for spotting those wild moments when panic selling takes over. Picture this: prices plummet, volume explodes, and everyone’s bailing out—that’s capitulation, and it might just signal a turning point. This script throws a bright marker on your chart whenever the chaos hits, so you can decide if it’s time to jump in or sit tight. Built fresh in Pine Script v6, it’s sleek, customizable, and packs an alert to keep you posted—perfect for stocks, indices like SPY, or even crypto chaos.

Inspired by epic sell-offs like March 2020’s COVID crash, this tool’s here to help you navigate the storm with a smile (and maybe a profit).

What It Does

Capitulation volume is that “everyone’s out!” moment: a steep price drop meets a massive volume surge, hinting that sellers are tapped out. It’s not a guaranteed reversal—sometimes the bleeding continues—but it’s a loud clue that fear’s peaked. Here’s the magic:

Volume Check : Measures current volume against a customizable average (default: 20 bars).

Price Plunge : Tracks the percentage drop from the last close.

Capitulation Cal l: When volume rockets past your threshold (e.g., 2x average) and price tanks (e.g., -5%), you get a red triangle above the bar.

Stay Alert : Fires off a detailed message (e.g., “Volume 300M > 200M, Drop -10%”) so you’re never caught off guard.

Think of it as your market meltdown radar—simple, effective, and ready to roll.

Functionality Breakdown

Volume Surge Spotter :

Uses a 20-bar Simple Moving Average (SMA) of volume as your baseline.

Flags any bar where volume exceeds this average by your chosen multiplier (default: 2x).

Price Drop Detector :

Calculates the percentage change from the prior close.

Triggers when the drop’s bigger than your set limit (default: -5%).

Capitulation Marker:

Combines both signals: high volume + sharp drop = capitulation.

Slaps a red triangle above the bar for instant “whoa, there it is!” vibes.

Real-Time Alerts :

Sends a custom alert with volume and drop details, keeping you in the loop without babysitting the chart.

Customization Options

Tune it to your trading style with these easy settings:

Volume Multiplier (x Avg): Starts at 2.0 (2x average volume). Bump it to 3.0 for only the wildest spikes or dial it to 1.5 for more frequent catches. Range: 1.0-10.0, step 0.1.

Price Drop Threshold (%): Default 5.0 (a -5% drop). Go big with 10.0 for crash-level falls or ease to 3.0 for lighter dips. Range: 1.0-20.0, step 0.1.

Average Volume Period: Default 20 bars. Stretch it to 50 for a broader view or shrink to 10 for quick reactions. Range: 1-100.

Capitulation Marker Color: Red by default—because panic’s loud! Switch it to blue, green, or pink to match your chart’s personality.

How to Use It

Drop It On : Add it to any chart with volume data—SPY daily for market moves, /ES 15-minute for intraday action, or your go-to stock.

Play with Settings : Hit the indicator’s config gear and tweak the multiplier, drop threshold, period, or marker color to fit your vibe.

Set an Alert : Right-click the indicator, add an alert with “Any alert() function call,” and get pinged when capitulation strikes.

Watch the Action : Look for those red triangles on big drop days—pair with your favorite reversal signals for extra oomph.

Pro Tips

Daily Charts : Catch market-wide capitulations like March 23, 2020 (SPY: -10%, 3x volume).

Intraday : Spot flash crashes or sector sell-offs on 15-minute or 5-minute bars.

Context Matters : High volume alone isn’t enough—check the VIX or candlestick patterns (e.g., hammers) to confirm a bottom.

Economic Crises by @zeusbottradingEconomic Crises Indicator by @zeusbottrading

Description and Use Case

Overview

The Economic Crises Highlight Indicator is designed to visually mark major economic crises on a TradingView chart by shading these periods in red. It provides a historical context for financial analysis by indicating when major recessions occurred, helping traders and analysts assess the performance of assets before, during, and after these crises.

What This Indicator Shows

This indicator highlights the following major economic crises (from 1953 to 2020), which significantly impacted global markets:

• 1953 Korean War Recession

• 1957 Monetary Tightening Recession

• 1960 Investment Decline Recession

• 1969 Employment Crisis

• 1973 Oil Crisis

• 1980 Inflation Crisis

• 1981 Fed Monetary Policy Recession

• 1990 Oil Crisis and Gulf War Recession

• 2001 Dot-Com Bubble Crash

• 2008 Global Financial Crisis (Great Recession)

• 2020 COVID-19 Recession

Each of these periods is shaded in red with 80% transparency, allowing you to clearly see the impact of economic downturns on various financial assets.

How This Indicator is Useful

This indicator is particularly valuable for:

✅ Comparative Performance Analysis – It allows traders and investors to compare how different assets (e.g., Gold, Silver, S&P 500, Bitcoin) performed before, during, and after major economic crises.

✅ Identifying Market Trends – Helps recognize recurring patterns in asset price movements during times of financial distress.

✅ Risk Management & Strategy Development – Understanding how markets reacted in the past can assist in making better-informed investment decisions for future downturns.

✅ Gold, Silver & Bitcoin as Safe Havens – Comparing precious metals and cryptocurrencies against traditional stocks (e.g., SPY) to analyze their performance as hedges during economic turmoil.

How to Use It in Your Analysis

By overlaying this indicator on your Gold, Silver, SPY, and Bitcoin chart (for example), you can quickly spot historical market reactions and use that insight to predict possible behaviors in future downturns.

⸻

How to Apply This in TradingView?

1. Click on Use on chart under the image.

2. Overlay it with Gold ( OANDA:XAUUSD ), Silver ( OANDA:XAGUSD ), SPY ( AMEX:SPY ), and Bitcoin ( COINBASE:BTCUSD ) for comparative analysis.

⸻

Conclusion

This indicator serves as a powerful historical reference for traders analyzing asset performance during economic downturns. By studying past crises, you can develop a data-driven investment strategy and improve your market insights. 🚀📈

Let me know if you need any modifications or enhancements!

Classic Nacked Z-Score ArbitrageThe “Classic Naked Z-Score Arbitrage” strategy employs a statistical arbitrage model based on the Z-score of the price spread between two assets. This strategy follows the premise of pair trading, where two correlated assets, typically from the same market sector, are traded against each other to profit from relative price movements (Gatev, Goetzmann, & Rouwenhorst, 2006). The approach involves calculating the Z-score of the price spread between two assets to determine market inefficiencies and capitalize on short-term mispricing.

Methodology

Price Spread Calculation:

The strategy calculates the spread between the two selected assets (Asset A and Asset B), typically from different sectors or asset classes, on a daily timeframe.

Statistical Basis – Z-Score:

The Z-score is used as a measure of how far the current price spread deviates from its historical mean, using the standard deviation for normalization.

Trading Logic:

• Long Position:

A long position is initiated when the Z-score exceeds the predefined threshold (e.g., 2.0), indicating that Asset A is undervalued relative to Asset B. This signals an arbitrage opportunity where the trader buys Asset B and sells Asset A.

• Short Position:

A short position is entered when the Z-score falls below the negative threshold, indicating that Asset A is overvalued relative to Asset B. The strategy involves selling Asset B and buying Asset A.

Theoretical Foundation

This strategy is rooted in mean reversion theory, which posits that asset prices tend to return to their long-term average after temporary deviations. This form of arbitrage is widely used in statistical arbitrage and pair trading techniques, where investors seek to exploit short-term price inefficiencies between two assets that historically maintain a stable price relationship (Avery & Sibley, 2020).

Further, the Z-score is an effective tool for identifying significant deviations from the mean, which can be seen as a signal for the potential reversion of the price spread (Braucher, 2015). By capturing these inefficiencies, traders aim to profit from convergence or divergence between correlated assets.

Practical Application

The strategy aligns with the Financial Algorithmic Trading and Market Liquidity analysis, emphasizing the importance of statistical models and efficient execution (Harris, 2024). By utilizing a simple yet effective risk-reward mechanism based on the Z-score, the strategy contributes to the growing body of research on market liquidity, asset correlation, and algorithmic trading.

The integration of transaction costs and slippage ensures that the strategy accounts for practical trading limitations, helping to refine execution in real market conditions. These factors are vital in modern quantitative finance, where liquidity and execution risk can erode profits (Harris, 2024).

References

• Gatev, E., Goetzmann, W. N., & Rouwenhorst, K. G. (2006). Pairs Trading: Performance of a Relative-Value Arbitrage Rule. The Review of Financial Studies, 19(3), 1317-1343.

• Avery, C., & Sibley, D. (2020). Statistical Arbitrage: The Evolution and Practices of Quantitative Trading. Journal of Quantitative Finance, 18(5), 501-523.

• Braucher, J. (2015). Understanding the Z-Score in Trading. Journal of Financial Markets, 12(4), 225-239.

• Harris, L. (2024). Financial Algorithmic Trading and Market Liquidity: A Comprehensive Analysis. Journal of Financial Engineering, 7(1), 18-34.

10-Year Yields Table for Major CurrenciesThe "10-Year Yields Table for Major Currencies" indicator provides a visual representation of the 10-year government bond yields for several major global economies, alongside their corresponding Rate of Change (ROC) values. This indicator is designed to help traders and analysts monitor the yields of key currencies—such as the US Dollar (USD), British Pound (GBP), Japanese Yen (JPY), and others—on a daily timeframe. The 10-year yield is a crucial economic indicator, often used to gauge investor sentiment, inflation expectations, and the overall health of a country's economy (Higgins, 2021).

Key Components:

10-Year Government Bond Yields: The indicator displays the daily closing values of 10-year government bond yields for major economies. These yields represent the return on investment for holding government bonds with a 10-year maturity and are often considered a benchmark for long-term interest rates. A rise in bond yields generally indicates that investors expect higher inflation and/or interest rates, while falling yields may signal deflationary pressures or lower expectations for future economic growth (Aizenman & Marion, 2020).

Rate of Change (ROC): The ROC for each bond yield is calculated using the formula:

ROC=Current Yield−Previous YieldPrevious Yield×100

ROC=Previous YieldCurrent Yield−Previous Yield×100

This percentage change over a one-day period helps to identify the momentum or trend of the bond yields. A positive ROC indicates an increase in yields, often linked to expectations of stronger economic performance or rising inflation, while a negative ROC suggests a decrease in yields, which could signal concerns about economic slowdown or deflation (Valls et al., 2019).

Table Format: The indicator presents the 10-year yields and their corresponding ROC values in a table format for easy comparison. The table is color-coded to differentiate between countries, enhancing readability. This structure is designed to provide a quick snapshot of global yield trends, aiding decision-making in currency and bond market strategies.

Plotting Yield Trends: In addition to the table, the indicator plots the 10-year yields as lines on the chart, allowing for immediate visual reference of yield movements across different currencies. The plotted lines provide a dynamic view of the yield curve, which is a vital tool for economic analysis and forecasting (Campbell et al., 2017).

Applications:

This indicator is particularly useful for currency traders, bond investors, and economic analysts who need to monitor the relationship between bond yields and currency strength. The 10-year yield can be a leading indicator of economic health and interest rate expectations, which often impact currency valuations. For instance, higher yields in the US tend to attract foreign investment, strengthening the USD, while declining yields in the Eurozone might signal economic weakness, leading to a depreciating Euro.

Conclusion:

The "10-Year Yields Table for Major Currencies" indicator combines essential economic data—10-year government bond yields and their rate of change—into a single, accessible tool. By tracking these yields, traders can better understand global economic trends, anticipate currency movements, and refine their trading strategies.

References:

Aizenman, J., & Marion, N. (2020). The High-Frequency Data of Global Bond Markets: An Analysis of Bond Yields. Journal of International Economics, 115, 26-45.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (2017). The Econometrics of Financial Markets. Princeton University Press.

Higgins, M. (2021). Macroeconomic Analysis: Bond Markets and Inflation. Harvard Business Review, 99(5), 45-60.

Valls, A., Ferreira, M., & Lopes, M. (2019). Understanding Yield Curves and Economic Indicators. Financial Markets Review, 32(4), 72-91.

Quadruple WitchingThis Pine Script code defines an indicator named "Display Quadruple Witching" that highlights the chart background in green on specific days known as "Quadruple Witching." Quadruple Witching refers to the third Friday of March, June, September, and December when four types of financial contracts—stock index futures, stock index options, stock options, and single stock futures—expire simultaneously. This phenomenon often leads to increased market volatility and trading volume.

The indicator calculates the date of the third Friday of each quarter and highlights the chart background on these dates. This feature helps traders anticipate potential market impacts associated with Quadruple Witching.

Importance of Quadruple Witching

Quadruple Witching is significant in financial markets for several reasons:

Increased Market Activity: On these dates, the market often experiences a surge in trading volume as traders and institutions adjust their positions in response to the expiration of multiple derivative contracts (CFA Institute, 2020).

Price Movements: The simultaneous expiration of various contracts can lead to substantial price fluctuations and increased market volatility. These movements can be unpredictable and present both risks and opportunities for traders (Bodnaruk, 2019).

Market Impact: The adjustments made by institutional investors and traders due to the expirations can have a pronounced impact on stock prices and market indices. This effect is particularly noticeable in the days surrounding Quadruple Witching (Campbell, 2021).

References

CFA Institute. (2020). The Impact of Quadruple Witching on Financial Markets. CFA Institute Research Foundation. Retrieved from CFA Institute.

Bodnaruk, A. (2019). The Effect of Option Expiration on Stock Prices. Journal of Financial Economics, 131(1), 45-64. doi:10.1016/j.jfineco.2018.08.004

Campbell, J. Y. (2021). The Behaviour of Stock Prices Around Expiration Dates. Journal of Financial Economics, 141(2), 577-600. doi:10.1016/j.jfineco.2021.01.001

These references provide a deeper understanding of how Quadruple Witching influences market dynamics and why being aware of these dates can be crucial for trading strategies.

Pre-COVID High and COVID LowOverview

The "Pre-COVID High and COVID Low" indicator is designed to identify and mark significant price levels on your chart, specifically targeting the pre-COVID-19 high and the low during the initial COVID-19 market impact. This script is particularly useful for traders who are interested in analyzing how stocks or other financial instruments reacted during the onset of the COVID-19 pandemic, providing a historical perspective that may help in making informed trading decisions.

How It Works

Date Ranges : The script uses predefined date ranges to calculate the highest and lowest price levels before and during the early stages of the COVID-19 pandemic. These ranges are:

Pre-COVID High: Between January 1, 2020, and March 31, 2020.

COVID Low: Between March 1, 2020, and March 31, 2020.

Calculation Method :

The highest price during the pre-COVID period is tracked and recorded as the "Pre-COVID High".

The lowest price during the specified COVID period is tracked and recorded as the "COVID Low".

Visibility Conditions : The script includes logic to ensure that these historical levels are only displayed if they fall within a range close to the current visible price range on the chart. This prevents the indicator from compressing the price scale unduly.

How to Use It

Adding to Your Char t: To use this indicator, add it to any chart on TradingView. It works best with daily time frames to clearly visualize the impact over these specific months.

Interpretation :

The "Pre-COVID High" is marked with a red line and is labeled the first day it becomes applicable.

The "COVID Low" is marked with a green line and is similarly labeled on its applicable day.

Trading Strategy Consideration : Traders can use these historical levels as potential support or resistance zones for their trading strategies. These levels can indicate significant price points where the market previously showed strong reactions.

Correlation Coefficient - DXY & XAUPublishing my first indicator on TradingView. Essentially a modification of the Correlation Coefficient indicator, that displays a 2 ticker symbols' correlation coefficient vs, the chart presently loaded.. You can modify the symbols, but the default uses DXY and XAU, which have been displaying strong negative correlation.

As with the built-in CC (Correlation Coefficient) indicator, readings are taken the same way:

Positive Correlation = anything above 0 | stronger as it moves up towards 1 | weaker as it moves back down towards 0

Negative Correlation = anything below 0 | stronger moving down towards -1 | weaker moving back up towards 0

This is primarily created to work with the Bitcoin weekly chart, for comparing DXY and Gold (XAU) price correlations (in advance, when possible). If you change the chart timeframe to something other than weekly, consider playing with the Length input, which is set to 35 by default where I think it best represents correlations with Bitcoin's weekly timeframe for DXY and Gold.

The intention is that you might be able to determine future direction of Bitcoin based on positive or negative correlations of Gold and/or the US Dollar Index. DXY has been making peaks and valleys prior to Bitcoin since after March 2020 black swan event, where it peaked just after instead. In the future, it may flip over again and Bitcoin may hit major highs or lows prior to DXY, again. So, keep an eye on the charts for all 3, as well as the indicator correlations.

Currently, we've moved back into negative correlation between Bitcoin and DXY, and positive correlation with Bitcoin and Gold:

Negative Correlation b/w Bitcoin and DXY - if DXY moves up, Bitcoin likely moves down, or if DXY moves down, Bitcoin likely moves up (or if Bitcoin were to move first before DXY, as it did on March 2020, instead)

Positive Correlation b/w Bitcoin and Gold - Bitcoin and Gold will likely move up or down with each other.

DXY is represented by the green histogram and label, Gold is represented by the yellow histogram and label. Again, you can modify the tickers you want to check against, and you can modify the colors for their histograms / labels.

The inspiration from came from noticing areas of same date or delayed negative correlation between Bitcoin and DXY, here is one of my most recent posts about that:

Please let me know if you have any questions, or would like to see updates to the indicator to make it easier to use or add more useful features to it.

I hope this becomes useful to you in some way. Thank you for your support!

Cheers,

dudebruhwhoa :)

Recessions & crises shading (custom dates & stats)Shades your chart background to flag events such as crises or recessions, in similar fashion to what you see on FRED charts. The advantage of this indicator over others is that you can quickly input custom event dates as text in the menu to analyse their impact for your specific symbol. The script automatically labels, calculates and displays the peak to through percentage corrections on your current chart.

By default the indicator is configured to show the last 6 US recessions. If you have custom events which will benefit others, just paste the input string in the comments below so one can simply copy/paste in their indicator.

Example event input (No spaces allowed except for the label name. Enter dates as YYYY-MM-DD.)

2020-02-01,2020-03-31,COVID-19

2007-12-01,2009-05-31,Subprime mortgages

2001-03-01,2001-10-30,Dot-com bubble

1990-07-01,1991-03-01,Oil shock

1981-07-01,1982-11-01,US unemployment

1980-01-01,1980-07-01,Volker

1973-11-01,1975-03-01,OPEC

Days in rangeThis script is a little widget that I made to do some homework on the VIX.

As you can see in the chart I was analyzing the 2008 market crash and the stats that followed it after until the market started to recover.

You can see that theory in my "Ideas" tab.

This is an interactive set of lines that you can use to count the the bars inside and outside of your chosen range, and the percentage outside that range.

You should initially enter the price range of your product in the menu and set some arbitrary dates that you can easily see on your chart.

Drag and drop the lines around to suit what price and the dates you are analyzing.

The table will display the bar count inside and outside of the range, the total bars, and the percentage outside that range.

I personally used this as a tool to study the overall average of the product, compared with the behavior during major market events.

It is currently my opinion that post 2020 analysis needs to take into account the behavior of any given product prior to 2020 when the

VIX was in its comfort zone. Not to say that a price valuation hasn't been set, but that the movement to that price was outside of "Normal Market Conditions,"

and the time factor to return to that value might be skewed. Other factors would need to be considered at that point pertaining to your specific product or corelating indicator.

I could see this tool being useful to Forex and commodities traders. But that isn't my field so that that for what it is. I do think it would perform best on something that is more

pegged to a price range. I personally would use it on product's, like the VIX, that I use as an indicator product. That is what it was designed for.

But I suppose it could be used for Mean price and time related analysis, maybe with a Vwap, SMA or other breakout style indicators.

Volume analysis might be pretty sporty. Possibly time patterns... the possibilities could be endless. Or... limited.

I am publishing this for my trade group so that it can be tinkered with to find other helpful ways to use it.

If anyone finds something interesting with other indicators, please drop a comment below and I could consider creating a script to integrate with this tool.

Adaptive Candlestick Pattern Recognition System█ INTRODUCTION

Nearly three years in the making, intermittently worked on in the few spare hours of weekends and time off, this is a passion project I undertook to flesh out my skills as a computer programmer. This script currently recognizes 85 different candlestick patterns ranging from one to five candles in length. It also performs statistical analysis on those patterns to determine prior performance and changes the coloration of those patterns based on that performance. In searching TradingView's script library for scripts similar to this one, I had found a handful. However, when I reviewed the ones which were open source, I did not see many that truly captured the power of PineScrypt or leveraged the way it works to create efficient and reliable code; one of the main driving factors for releasing this 5,000+ line behemoth open sourced.

Please take the time to review this description and source code to utilize this script to its fullest potential.

█ CONCEPTS

This script covers the following topics: Candlestick Theory, Trend Direction, Higher Timeframes, Price Analysis, Statistic Analysis, and Code Design.

Candlestick Theory - This script focuses solely on the concept of Candlestick Theory: arrangements of candlesticks may form certain patterns that can potentially influence the future price action of assets which experience those patterns. A full list of patterns (grouped by pattern length) will be in its own section of this description. This script contains two modes of operation for identifying candlestick patterns, 'CLASSIC' and 'BREAKOUT'.

CLASSIC: In this mode, candlestick patterns will be identified whenever they appear. The user has a wide variety of inputs to manipulate that can change how certain patterns are identified and even enable alerts to notify themselves when these patterns appear. Each pattern selected to appear will have their Profit or Loss (P/L) calculated starting from the first candle open succeeding the pattern to a candle close specified some number of candles ahead. These P/L calculations are then collected for each pattern, and split among partitions of prior price action of the asset the script is currently applied to (more on that in Higher Timeframes ).

BREAKOUT: In this mode, P/L calculations are held off until a breakout direction has been confirmed. The user may specify the number of candles ahead of a pattern's appearance (from one to five) that a pattern has to confirm a breakout in either an upward or downward direction. A breakout is constituted when there is a candle following the appearance of the pattern that closes above/at the highest high of the pattern, or below/at its lowest low. Only then will percent return calculations be performed for the pattern that's been identified, and these percent returns are broken up not only by the partition they had appeared in but also by the breakout direction itself. Patterns which do not breakout in either direction will be ignored, along with having their labels deleted.

In both of these modes, patterns may be overridden. Overrides occur when a smaller pattern has been detected and ends up becoming one (or more) of the candles of a larger pattern. A key example of this would be the Bearish Engulfing and the Three Outside Down patterns. A Three Outside Down necessitates a Bearish Engulfing as the first two candles in it, while the third candle closes lower. When a pattern is overridden, the return for that pattern will no longer be tracked. Overrides will not occur if the tail end of a larger pattern occurs at the beginning of a smaller pattern (Ex: a Bullish Engulfing occurs on the third candle of a Three Outside Down and the candle immediately following that pattern, the Three Outside Down pattern will not be overridden).

Important Functionality Note: These patterns are only searched for at the most recently closed candle, not on the currently closing candle, which creates an offset of one for this script's execution. (SEE LIMITATIONS)

Trend Direction - Many of the patterns require a trend direction prior to their appearance. Noting TradingView's own publication of candlestick patterns, I utilize a similar method for determining trend direction. Moving Averages are used to determine which trend is currently taking place for candlestick patterns to be sought out. The user has access to two Moving Averages which they may individually modify the following for each: Moving Average type (list of 9), their length, width, source values, and all variables associated with two special Moving Averages (Least Squares and Arnaud Legoux).

There are 3 settings for these Moving Averages, the first two switch between the two Moving Averages, and the third uses both. When using individual Moving Averages, the user may select a 'price point' to compare against the Moving Average (default is close). This price point is compared to the Moving Average at the candles prior to the appearance of candle patterns. Meaning: The close compared to the Moving Average two candles behind determines the trend direction used for Candlestick Analysis of one candle patterns; three candles behind for two candle patterns and so on. If the selected price point is above the Moving Average, then the current trend is an 'uptrend', 'downtrend' otherwise.

The third setting using both Moving Averages will compare the lengths of each, and trend direction is determined by the shorter Moving Average compared to the longer one. If the shorter Moving Average is above the longer, then the current trend is an 'uptrend', 'downtrend' otherwise. If the lengths of the Moving Averages are the same, or both Moving Averages are Symmetrical, then MA1 will be used by default. (SEE LIMITATIONS)

Higher Timeframes - This script employs the use of Higher Timeframes with a few request.security calls. The purpose of these calls is strictly for the partitioning of an asset's chart, splitting the returns of patterns into three separate groups. The four inputs in control of this partitioning split the chart based on: A given resolution to grab values from, the length of time in that resolution, and 'Upper' and 'Lower Limits' which split the trading range provided by that length of time in that resolution that forms three separate groups. The default values for these four inputs will partition the current chart by the yearly high-low range where: the 'Upper' partition is the top 20% of that trading range, the 'Middle' partition is 80% to 33% of the trading range, and the 'Lower' partition covers the trading range within 33% of the yearly low.

Patterns which are identified by this script will have their returns grouped together based on which partition they had appeared in. For example, a Bullish Engulfing which occurs within a third of the yearly low will have its return placed separately from a Bullish Engulfing that occurred within 20% of the yearly high. The idea is that certain patterns may perform better or worse depending on when they had occurred during an asset's trading range.

Price Analysis - Price Analysis is a major part of this script's functionality as it can fundamentally change how patterns are shown to the user. The settings related to Price Analysis include setting the number of candles ahead of a pattern's appearance to determine the return of that pattern. In 'BREAKOUT' mode, an additional setting allows the user to specify where the P/L calculation will begin for a pattern that had appeared and confirmed. (SEE LIMITATIONS)

The calculation for percent returns of patterns is illustrated with the following pseudo-code (CLASSIC mode, this is a simplified version of the actual code):

type patternObj

int ID

int partition

type returnsArray

float returns

// No pattern found = na returned

patternObj TEST_VAL = f_FindPattern()

priorTestVal = TEST_VAL

if not na( priorTestVal )

pnlMatrixRow = priorTestVal.ID

pnlMatrixCol = priorTestVal.partition

matrixReturn = matrix.get(PERCENT_RETURNS, pnlMatrixRow, pnlMatrixCol)

percentReturn = ( (close - open ) / open ) * 100%

array.push(matrixReturn.returns, percentReturn)

Statistic Analysis - This script uses Pine's built-in array functions to conduct the Statistic Analysis for patterns. When a pattern is found and its P/L calculation is complete, its return is added to a 'Return Array' User-Defined-Type that contains numerous fields which retain information on a pattern's prior performance. The actual UDT is as follows:

type returnArray

float returns = na

int size = 0

float avg = 0

float median = 0

float stdDev = 0

int polarities = na

All values within this UDT will be updated when a return is added to it (some based on user input). The array.avg , array.median and array.stdev will be ran and saved into their respective fields after a return is placed in the 'returns' array. The 'polarities' integer array is what will be changed based on user input. The user specifies two different percentages that declare 'Positive' and 'Negative' returns for patterns. When a pattern returns above, below, or in between these two values, different indices of this array will be incremented to reflect the kind of return that pattern had just experienced.

These values (plus the full name, partition the pattern occurred in, and a 95% confidence interval of expected returns) will be displayed to the user on the tooltip of the labels that identify patterns. Simply scroll over the pattern label to view each of these values.

Code Design - Overall this script is as much of an art piece as it is functional. Its design features numerous depictions of ASCII Art that illustrate what is being attempted by the functions that identify patterns, and an incalculable amount of time was spent rewriting portions of code to improve its efficiency. Admittedly, this final version is nearly 1,000 lines shorter than a previous version (one which took nearly 30 seconds after compilation to run, and didn't do nearly half of what this version does). The use of UDTs, especially the 'patternObj' one crafted and redesigned from the Hikkake Hunter 2.0 I published last month, played a significant role in making this script run efficiently. There is a slight rigidity in some of this code mainly around pattern IDs which are responsible for displaying the abbreviation for patterns (as well as the full names under the tooltips, and the matrix row position for holding returns), as each is hard-coded to correspond to that pattern.

However, one thing I would like to mention is the extensive use of global variables for pattern detection. Many scripts I had looked over for ideas on how to identify candlestick patterns had the same idea; break the pattern into a set of logical 'true/false' statements derived from historically referencing candle OHLC values. Some scripts which identified upwards of 20 to 30 patterns would reference Pine's built-in OHLC values for each pattern individually, potentially requesting information from TradingView's servers numerous times that could easily be saved into a variable for re-use and only requested once per candle (what this script does).

█ FEATURES

This script features a massive amount of switches, options, floating point values, detection settings, and methods for identifying/tailoring pattern appearances. All modifiable inputs for patterns are grouped together based on the number of candles they contain. Other inputs (like those for statistics settings and coloration) are grouped separately and presented in a way I believe makes the most sense.