Indicator - Multiple Moving Averages 1.0Features:

- Each moving average has customizable length, type and source

- The ability to change the source of all moving averages with one input (changing an individual MA source will override the general for that MA)

- At a glance comparison of 20 SMA and 20 VWMA to gauge volume trend

Defaults: Four SMAs (20, 50, 100, 200) and a 20 VWMA.

Usage:

- Use Fibonacci levels, pivots .etc for confluence

- Personally, I like to set overall source to low in uptrends, to high in downtrends and then set alerts for when the price crosses any of the averages. Then pay particular attention to the candlesticks and other indicators.

TODO:

- Add alerts option so that it send alert on crossing up or down any alert lines.

Cari dalam skrip untuk "20蒙古币兑换人民币"

XPloRR MA-Trailing-Stop StrategyXPloRR MA-Trailing-Stop Strategy

Long term MA-Trailing-Stop strategy with Adjustable Signal Strength to beat Buy&Hold strategy

None of the strategies that I tested can beat the long term Buy&Hold strategy. That's the reason why I wrote this strategy.

Purpose: beat Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

My buy strategy is triggered by the fast buy EMA (blue) crossing over the slow buy SMA curve (orange) and the fast buy EMA has a certain up strength.

My sell strategy is triggered by either one of these conditions:

the EMA(6) of the close value is crossing under the trailing stop value (green) or

the fast sell EMA (navy) is crossing under the slow sell SMA curve (red) and the fast sell EMA has a certain down strength.

The trailing stop value (green) is set to a multiple of the ATR(15) value.

ATR(15) is the SMA(15) value of the difference between the high and low values.

The scripts shows a lot of graphical information:

The close value is shown in light-green. When the close value is lower then the buy value, the close value is shown in light-red. This way it is possible to evaluate the virtual losses during the trade.

the trailing stop value is shown in dark-green. When the sell value is lower then the buy value, the last color of the trade will be red (best viewed when zoomed)(in the example, there are 2 trades that end in gain and 2 in loss (red line at end))

the EMA and SMA values for both buy and sell signals are shown as a line

the buy and sell(close) signals are labeled in blue

How to use this strategy?

Every stock has it's own "DNA", so first thing to do is tune the right parameters to get the best strategy values voor EMA , SMA, Strength for both buy and sell and the Trailing Stop (#ATR).

Look in the strategy tester overview to optimize the values Percent Profitable and Net Profit (using the strategy settings icon, you can increase/decrease the parameters)

Then keep using these parameters for future buy/sell signals only for that particular stock.

Do the same for other stocks.

Important : optimizing these parameters is no guarantee for future winning trades!

Here are the parameters:

Fast EMA Buy: buy trigger when Fast EMA Buy crosses over the Slow SMA Buy value (use values between 10-20)

Slow SMA Buy: buy trigger when Fast EMA Buy crosses over the Slow SMA Buy value (use values between 30-100)

Minimum Buy Strength: minimum upward trend value of the Fast SMA Buy value (directional coefficient)(use values between 0-120)

Fast EMA Sell: sell trigger when Fast EMA Sell crosses under the Slow SMA Sell value (use values between 10-20)

Slow SMA Sell: sell trigger when Fast EMA Sell crosses under the Slow SMA Sell value (use values between 30-100)

Minimum Sell Strength: minimum downward trend value of the Fast SMA Sell value (directional coefficient)(use values between 0-120)

Trailing Stop (#ATR): the trailing stop value as a multiple of the ATR(15) value (use values between 2-20)

Example parameters for different stocks (Start capital: 1000, Order=100% of equity, Period 1/1/2005 to now) compared to the Buy&Hold Strategy(=do nothing):

BEKB(Bekaert): EMA-Buy=12, SMA-Buy=44, Strength-Buy=65, EMA-Sell=12, SMA-Sell=55, Strength-Sell=120, Stop#ATR=20

NetProfit: 996%, #Trades: 6, %Profitable: 83%, Buy&HoldProfit: 78%

BAR(Barco): EMA-Buy=16, SMA-Buy=80, Strength-Buy=44, EMA-Sell=12, SMA-Sell=45, Strength-Sell=82, Stop#ATR=9

NetProfit: 385%, #Trades: 7, %Profitable: 71%, Buy&HoldProfit: 55%

AAPL(Apple): EMA-Buy=12, SMA-Buy=45, Strength-Buy=40, EMA-Sell=19, SMA-Sell=45, Strength-Sell=106, Stop#ATR=8

NetProfit: 6900%, #Trades: 7, %Profitable: 71%, Buy&HoldProfit: 2938%

TNET(Telenet): EMA-Buy=12, SMA-Buy=45, Strength-Buy=27, EMA-Sell=19, SMA-Sell=45, Strength-Sell=70, Stop#ATR=14

NetProfit: 129%, #Trade

EMA Indicators with BUY sell SignalCombine 3 EMA indicators into 1. Buy and Sell signal is based on

- Buy signal based on 20 Days Highest High resistance

- Sell signal based on 10 Days Lowest Low support

Input :-

1 - Short EMA (20), Mid EMA (50) and Long EMA (200)

2 - Resistance (20) = 20 Days Highest High line

3 - Support (10) = 10 Days Lowest Low line

Breakout/Buy/Sell v6.5

Break Buy Sell Indicator v6.5 — Publish Description

What it is

A Heikin Ashi breakout event marker that runs a simple, sequential playbook:

BRK (intrabar) → BUY (bar close) → SELL (first Red Top-Test close).

Not a swing-high/low tool and not a full strategy—this is a breakout event detector.

How it works

A BRK prints intrabar only when core breakout confluence is present on the current bar:

Squeeze: Bollinger Band width below its lookback average × factor.

Break: High/close pushes beyond the lookback high (Early/Strict modes).

Volume: Volume > SMA(volume) × multiplier (mode-dependent).

Candle quality: Close in the top of the bar’s range (mode-dependent).

Adaptive override (optional): Close > prior high + k·ATR and body ≥ k·ATR.

After a BRK:

BUY prints on bar close (confirmation of that breakout bar).

A Top-Test Ladder (tiny triangles above bars) tracks “pressure” via spacing:

green → yellow → red (defaults: Yellow=2, Red=4).

SELL prints on the first red top-test bar close.

Notes:

Built and tuned on Heikin Ashi; use HA for matching placements.

Replay shows BRK & BUY on the same bar (no intrabar simulation). Live: they are staggered.

Inputs

Core Conditions:

BB Length • BB Mult • Squeeze Lookback • Squeeze Factor • Breakout Lookback

Volume SMA Length • Volume Mult (Early/Strict) • Candle Close-in-Range %

Mode: Early (high may break) / Strict (close must break)

Adaptive Override (ATR): Enable • ATR Length • k (break) • k (body)

Top-Test Ladder: Bars gap for Yellow • Bars gap for Red (≥)

Trade Signals: Enable Buy/Sell • Suppress extra BRK while in trade • Plot labels

Visuals: Debug paints (squeeze bg, Pmp diamonds, volume dots, ladder marks)

Signals & Alerts

BRK (intrabar): triangle below bar

BUY (on close): label below bar

SELL (Red Top-Test, on close): label above bar

Create these alerts (exactly three):

Breakout — Once Per Bar

BUY — Once Per Bar Close

SELL (Red Top-Test) — Once Per Bar Close

How to use

Wait for BRK intrabar (attention).

BUY at the close of that bar.

Ride through green/yellow ladder; SELL on the first red top-test close.

Optional: keep “Suppress extra BRK” ON to avoid spam during the trade.

Suggested settings

Chart: Heikin Ashi

Defaults to match screenshots:

Mode Early • BB 20/2.0 • Squeeze 0.60 • Breakout Lookback 20

Volume SMA 20 • Early mult 1.5

Adaptive ON (ATR 14, break/body 0.5)

Ladder Yellow=2, Red=4

Enable Buy/Sell ON • Suppress extra BRK ON • Debug paints ON

Timeframes: 15–45m, 2–4h, 1D (1–5m = advanced/noisier)

What it does NOT do

Not a full strategy, risk model, or trade manager.

Not a swing high/low system.

No multi-timeframe logic; it runs on the chart timeframe.

Tips & Notes

If yellow rarely appears, that’s normal—Pmp thrusts reset the ladder to green.

Keep alerts exactly as listed to avoid duplicates (don’t also use “Any alert() function call”).

Switching off HA will shift BUY/SELL timing (different OHLC basis).

Changelog

v6.5 — BRK intrabar retained; BUY on bar close; SELL on first Red Top-Test close; cleaner 3-alert workflow; ladder defaults tuned (Yellow=2, Red=4).

Disclaimer

Educational only. Not financial advice. Backtest and size risk before live use.

Trend + RSI + Volume//@version=5

strategy("SPY Trend RSI Volume Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// === Inputs ===

emaFastLen = input.int(20, title="Fast EMA")

emaSlowLen = input.int(50, title="Slow EMA")

rsiLen = input.int(14, title="RSI Period")

rsiLongThresh = input.int(55, title="RSI Threshold for Long")

rsiShortThresh = input.int(45, title="RSI Threshold for Short")

volumeMultiplier = input.float(1.5, title="Volume Multiplier")

atrLen = input.int(14, title="ATR Length")

riskReward = input.float(2.0, title="Risk-Reward Ratio")

atrMult = input.float(1.5, title="ATR Multiplier")

// === Indicators ===

emaFast = ta.ema(close, emaFastLen)

emaSlow = ta.ema(close, emaSlowLen)

rsi = ta.rsi(close, rsiLen)

avgVolume = ta.sma(volume, 20)

atr = ta.atr(atrLen)

// === Conditions ===

// Trend

isBullish = emaFast > emaSlow

isBearish = emaFast < emaSlow

// Volume

volSpike = volume > avgVolume * volumeMultiplier

// Entry conditions

longCondition = isBullish and rsi > rsiLongThresh and volSpike and close > emaFast

shortCondition = isBearish and rsi < rsiShortThresh and volSpike and close < emaFast

// === Entries ===

if (longCondition)

stopLoss = close - atr * atrMult

takeProfit = close + (close - stopLoss) * riskReward

strategy.entry("Long", strategy.long)

strategy.exit("TP/SL Long", from_entry="Long", stop=stopLoss, limit=takeProfit)

if (shortCondition)

stopLoss = close + atr * atrMult

takeProfit = close - (stopLoss - close) * riskReward

strategy.entry("Short", strategy.short)

strategy.exit("TP/SL Short", from_entry="Short", stop=stopLoss, limit=takeProfit)

// === Plotting ===

plot(emaFast, title="EMA 20", color=color.orange)

plot(emaSlow, title="EMA 50", color=color.blue)

EMA Range OscillatorEMA Range Oscillator (ERO) - User Guide

Overview

The EMA Range Oscillator (ERO) is a technical indicator that measures the distance between two Exponential Moving Averages (EMAs) and the distance between price and EMA. It normalizes these distances into a 0-100 range, helping traders identify trend strength, market momentum, and potential reversal points.

Components

Main Line

Green Line: EMA20 > EMA50 (Uptrend)

Red Line: EMA20 < EMA50 (Downtrend)

Histogram

White Histogram: Price distance from EMA20

Key Levels

Upper Level (80): High divergence zone

Middle Level (50): Neutral zone

Lower Level (20): Low divergence zone

Parameters

ParameterDefaultDescriptionFast EMA20Short-term EMA periodSlow EMA50Long-term EMA periodNormalization Period100Lookback period for scalingUpper80Upper threshold levelLower20Lower threshold level

How to Read the Indicator

High Values (Above 80)

Strong trend in progress

EMAs are widely separated

High momentum

Potential overbought/oversold conditions

Watch for possible trend exhaustion

Low Values (Below 20)

Consolidation phase

EMAs are close together

Low volatility

Potential breakout setup

Range-bound market conditions

Middle Zone (20-80)

Normal market conditions

Moderate trend strength

Balanced momentum

Look for directional clues from color changes

Trend Display Table (with Change Alerts)📌 Indicator: Trend Display Table (with Change Alerts)

This indicator helps identify trend direction based on a 15-minute 20 SMA compared against a 10 EMA applied to that SMA.

Trend Logic:

Bullish → 20 SMA crosses above 10 EMA (on SMA values)

Bearish → 20 SMA crosses below 10 EMA (on SMA values)

Neutral → No crossover (trend continues from previous state)

Display:

A compact trend table appears on the chart (top-right), showing the current trend with customizable colors, font size, and background.

Alerts:

Alerts are triggered only when the trend changes (from Bullish → Bearish or Bearish → Bullish).

This prevents repeated alerts on every bar.

✅ Useful for:

Confirming higher timeframe trend bias

Filtering trades in choppy markets

Getting notified instantly when the trend flips

DYNAMIC TRADING DASHBOARDStudy Material for the "Dynamic Trading Dashboard"

This Dynamic Trading Dashboard is designed as an educational tool within the TradingView environment. It compiles commonly used market indicators and analytical methods into one visual interface so that traders and learners can see relationships between indicators and price action. Understanding these indicators, step by step, can help traders develop discipline, improve technical analysis skills, and build strategies. Below is a detailed explanation of each module.

________________________________________

1. Price and Daily Reference Points

The dashboard displays the current price, along with percentage change compared to the day’s opening price. It also highlights whether the price is moving upward or downward using directional symbols. Alongside, it tracks daily high, low, open, and daily range.

For traders, daily levels provide valuable reference points. The daily high and low are considered intraday support and resistance, while the median price of the day often acts as a pivot level for mean reversion traders. Monitoring these helps learners see how price oscillates within daily ranges.

________________________________________

2. VWAP (Volume Weighted Average Price)

VWAP is calculated as a cumulative average price weighted by volume. The dashboard compares the current price with VWAP, showing whether the market is trading above or below it.

For traders, VWAP is often a guide for institutional order flow. Price trading above VWAP suggests bullish sentiment, while trading below VWAP indicates bearish sentiment. Learners can use VWAP as a training tool to recognize trend-following vs. mean reversion setups.

________________________________________

3. Volume Analysis

The system distinguishes between buy volume (when the closing price is higher than the open) and sell volume (when the closing price is lower than the open). A progress bar highlights the ratio of buying vs. selling activity in percentage.

This is useful because volume confirms price action. For instance, if prices rise but sell volume dominates, it can signal weakness. New traders learning with this tool should focus on how volume often precedes price reversals and trends.

________________________________________

4. RSI (Relative Strength Index)

RSI is a momentum oscillator that measures price strength on a scale from 0 to 100. The dashboard classifies RSI readings into overbought (>70), oversold (<30), or neutral zones and adds visual progress bars.

RSI helps learners understand momentum shifts. During training, one should notice how trending markets can keep RSI extended for longer periods (not immediate reversal signals), while range-bound markets react more sharply to RSI extremes. It is an excellent tool for practicing trend vs. range identification.

________________________________________

5. MACD (Moving Average Convergence Divergence)

The MACD indicator involves a fast EMA, slow EMA, and signal line, with focus on crossovers. The dashboard shows whether a “bullish cross” (MACD above signal line) or “bearish cross” (MACD below signal line) has occurred.

MACD teaches traders to identify trend momentum shifts and divergence. During practice, traders can explore how MACD signals align with VWAP trends or RSI levels, which helps in building a structured multi-indicator analysis.

________________________________________

6. Stochastic Oscillator

This indicator compares the current close relative to a range of highs and lows over a period. Displayed values oscillate between 0 and 100, marking zones of overbought (>80) and oversold (<20).

Stochastics are useful for students of trading to recognize short-term momentum changes. Unlike RSI, it reacts faster to price volatility, so false signals are common. Part of the training exercise can be to observe how stochastic “flips” can align with volume surges or daily range endpoints.

________________________________________

7. Trend & Momentum Classification

The dashboard adds simple labels for trend (uptrend, downtrend, neutral) based on RSI thresholds. Additionally, it provides quick momentum classification (“bullish hold”, “bearish hold”, or neutral).

This is beneficial for beginners as it introduces structured thinking: differentiating long-term market bias (trend) from short-term directional momentum. By combining both, traders can practice filtering signals instead of trading randomly.

________________________________________

8. Accumulation / Distribution Bias

Based on RSI levels, the script generates simplified tags such as “Accumulate Long”, “Accumulate Short”, or “Wait”.

This is purely an interpretive guide, helping learners think in terms of accumulation phases (when markets are low) and distribution phases (when markets are high). It reinforces the concept that trading is not only directional but also involves timing.

________________________________________

9. Overall Market Status and Score

Finally, the dashboard compiles multiple indicators (VWAP position, RSI, MACD, Stochastics, and price vs. median levels) into a Market Score expressed as a percentage. It also labels the market as Overbought, Oversold, or Normal.

This scoring system isn’t a recommendation but a learning framework. Students can analyze how combining different indicators improves decision-making. The key training focus here is confluence: not depending on one indicator but observing when several conditions align.

Extended Study Material with Formulas

________________________________________

1. Daily Reference Levels (High, Low, Open, Median, Range)

• Day High (H): Maximum price of the session.

DayHigh=max(Hightoday)DayHigh=max(Hightoday)

• Day Low (L): Minimum price of the session.

DayLow=min(Lowtoday)DayLow=min(Lowtoday)

• Day Open (O): Opening price of the session.

DayOpen=OpentodayDayOpen=Opentoday

• Day Range:

Range=DayHigh−DayLowRange=DayHigh−DayLow

• Median: Mid-point between high and low.

Median=DayHigh+DayLow2Median=2DayHigh+DayLow

These act as intraday guideposts for seeing how far the price has stretched from its key reference levels.

________________________________________

2. VWAP (Volume Weighted Average Price)

VWAP considers both price and volume for a weighted average:

VWAPt=∑i=1t(Pricei×Volumei)∑i=1tVolumeiVWAPt=∑i=1tVolumei∑i=1t(Pricei×Volumei)

Here, Price_i can be the average price (High + Low + Close) ÷ 3, also known as hlc3.

• Interpretation: Price above VWAP = bullish bias; Price below = bearish bias.

________________________________________

3. Volume Buy/Sell Analysis

The dashboard splits total volume into buy volume and sell volume based on candle type.

• Buy Volume:

BuyVol=Volumeif Close > Open, else 0BuyVol=Volumeif Close > Open, else 0

• Sell Volume:

SellVol=Volumeif Close < Open, else 0SellVol=Volumeif Close < Open, else 0

• Buy Ratio (%):

VolumeRatio=BuyVolBuyVol+SellVol×100VolumeRatio=BuyVol+SellVolBuyVol×100

This helps traders gauge who is in control during a session—buyers or sellers.

________________________________________

4. RSI (Relative Strength Index)

RSI measures strength of momentum by comparing gains vs. losses.

Step 1: Compute average gains (AG) and losses (AL).

AG=Average of Upward Closes over N periodsAG=Average of Upward Closes over N periodsAL=Average of Downward Closes over N periodsAL=Average of Downward Closes over N periods

Step 2: Calculate relative strength (RS).

RS=AGALRS=ALAG

Step 3: RSI formula.

RSI=100−1001+RSRSI=100−1+RS100

• Used to detect overbought (>70), oversold (<30), or neutral momentum zones.

________________________________________

5. MACD (Moving Average Convergence Divergence)

• Fast EMA:

EMAfast=EMA(Close,length=fast)EMAfast=EMA(Close,length=fast)

• Slow EMA:

EMAslow=EMA(Close,length=slow)EMAslow=EMA(Close,length=slow)

• MACD Line:

MACD=EMAfast−EMAslowMACD=EMAfast−EMAslow

• Signal Line:

Signal=EMA(MACD,length=signal)Signal=EMA(MACD,length=signal)

• Histogram:

Histogram=MACD−SignalHistogram=MACD−Signal

Crossovers between MACD and Signal are used in studying bullish/bearish phases.

________________________________________

6. Stochastic Oscillator

Stochastic compares the current close against a range of highs and lows.

%K=Close−LowestLowHighestHigh−LowestLow×100%K=HighestHigh−LowestLowClose−LowestLow×100

Where LowestLow and HighestHigh are the lowest and highest values over N periods.

The %D line is a smooth version of %K (using a moving average).

%D=SMA(%K,smooth)%D=SMA(%K,smooth)

• Values above 80 = overbought; below 20 = oversold.

________________________________________

7. Trend and Momentum Classification

This dashboard generates simplified trend/momentum logic using RSI.

• Trend:

• RSI < 40 → Downtrend

• RSI > 60 → Uptrend

• In Between → Neutral

• Momentum Bias:

• RSI > 70 → Bullish Hold

• RSI < 30 → Bearish Hold

• Otherwise Neutral

This is not predictive, only a classification framework for educational use.

________________________________________

8. Accumulation/Distribution Bias

Based on extreme RSI values:

• RSI < 25 → Accumulate Long Bias

• RSI > 80 → Accumulate Short Bias

• Else → Wait/No Action

This helps learners understand the idea of accumulation at lows (strength building) and distribution at highs (profit booking).

________________________________________

9. Overall Market Status and Score

The tool adds up 5 bullish conditions:

1. Price above VWAP

2. RSI > 50

3. MACD > Signal

4. Stochastic > 50

5. Price above Daily Median

BullishScore=ConditionsMet5×100BullishScore=5ConditionsMet×100

Then it categorizes the market:

• RSI > 70 or Stoch > 80 → Overbought

• RSI < 30 or Stoch < 20 → Oversold

• Else → Normal

This encourages learners to think in terms of probabilistic conditions instead of single-indicator signals.

________________________________________

⚠️ Warning:

• Trading financial markets involves substantial risk.

• You can lose more money than you invest.

• Past performance of indicators does not guarantee future results.

• This script must not be copied, resold, or republished without authorization from aiTrendview.

By using this material or the code, you agree to take full responsibility for your trading decisions and acknowledge that this is not financial advice.

________________________________________

⚠️ Disclaimer and Warning (From aiTrendview)

This Dynamic Trading Dashboard is created strictly for educational and research purposes on the TradingView platform. It does not provide financial advice, buy/sell recommendations, or guaranteed returns. Any use of this tool in live trading is completely at the user’s own risk. Markets are inherently risky; losses can exceed initial investment.

The intellectual property of this script and its methodology belongs to aiTrendview. Unauthorized reproduction, modification, or redistribution of this code is strictly prohibited. By using this study material or the script, you acknowledge personal responsibility for any trading outcomes. Always consult professional financial advisors before making investment decisions.

Multi Stoch + VWAP Heatmap + Histogram + ScalpingThis indicator was developed by referencing various indicators from many contributors. I apologize that I cannot identify all the original authors due to the numerous sources referenced. Thank you to everyone who contributed to the trading community.

Important Notice: Please use this indicator with sufficient caution and proper risk management. I do not assume any responsibility for any losses incurred from using this indicator. Trade at your own risk.

Alternative version:

Acknowledgment & Disclaimer:

This indicator incorporates ideas and concepts from numerous community indicators. I sincerely apologize for not being able to properly credit all the original creators due to the extensive references used. My heartfelt gratitude goes out to all the talented developers in the trading community.

Risk Warning: Please exercise extreme caution when using this indicator. All trading involves substantial risk of loss, and I accept no liability for any financial losses that may result from the use of this indicator. Always implement proper risk management and trade responsibly.

Multi Stoch + VWAP Heatmap + Histogram + Scalping Usage Guide

🔧 Basic Settings

Parameter Settings (Recommended for XAU/USD)

Fast Stoch Length: 5 # Ultra-short term trend

Medium Stoch Length: 14 # Short term trend

Slow Stoch Length: 21 # Medium term trend

%K Smoothing: 2 # High sensitivity setting

%D Smoothing: 2 # High sensitivity setting

Overbought Level: 75 # Sell zone

Oversold Level: 25 # Buy zone

📈 Reading the Chart

1. Histogram (Background Bar Chart)

Green tones: Strong uptrend

Red tones: Strong downtrend

Gray: Trendless/neutral

2. Line Display

Blue lines: Ultra-short term Stochastic (K1/D1)

Orange lines: Short term Stochastic (K2/D2)

Purple lines: Medium term Stochastic (K3/D3)

Yellow line: VWAP (normalized)

3. Horizontal Lines

Upper line (75): Sell zone

Center line (50): Neutral line

Lower line (25): Buy zone

🎯 Signal Types and Meanings

Scalping Signals (● marks)

Green ● (bottom): 📈 Scalp buy entry

RSI(7) < 25 + K1 < 30 combination

VWAP bounce targeting

Red ● (top): 📉 Scalp sell entry

RSI(7) > 75 + K1 > 70 combination

VWAP rejection targeting

Main Trend Signals

▲ (large, green): 💪 Strong buy signal - Multiple conditions aligned

▼ (large, red): 💪 Strong sell signal - Multiple conditions aligned

△ (medium, green): 📈 Normal buy signal

▽ (medium, orange): 📉 Normal sell signal

Warning/Reversal Signals

▼ (pink): ⚠️ Sell warning - Trend reversal caution

△ (teal): ⚠️ Buy warning - Trend reversal caution

Cross Signals (● marks, positioned up/down)

Green ● (bottom): Histogram crosses above VWAP

Red ● (top): Histogram crosses below VWAP

🚀 Practical Usage

Scalping Strategy (1-5 minute charts recommended)

Entry: Enter on green ● or red ● signals

Take Profit: At opposite zone or next ● signal

Stop Loss: Around 10-15 pips (for gold)

Time Session: London-NY overlap optimal

Swing Trading Strategy (15min-1hour charts)

Entry: Strong ▲▼ signals

Take Profit: Opposite warning signals (▼△)

Stop Loss: VWAP reverse break or 30-50 pips

Day Trading Strategy (5-15 minute charts)

Trend Confirmation: Histogram color

Entry: △▽ signals

Take Profit: Opposite zone reached

Stop Loss: 20-30 pips

⚡ XAU/USD Specific Usage

Session-Based Strategy

Tokyo Session (9-15 JST): Wait and see, small scalps

London Session (16-24 JST): Main trading

NY Session (22-6 JST): Most active, all signals valid

Major News Events

Pre-announcement: Reduce positions

Post-announcement: Trend following with ● signals

🔍 Filter Functions

ATR Filter

Small price movements filtered as noise

Signals only on significant price moves

Time Filter

Strong signals only during high volatility sessions

Weaker signals during low volatility periods

Consecutive Signal Prevention

Duplicate signals within 2 bars filtered out

Prevents noise trading

⚙️ Settings Customization

For Aggressive Trading

Signal Cooldown: 1 # More frequent signals

ATR Length: 5 # More sensitive filter

For Conservative Trading

Signal Cooldown: 5 # Relaxed signals

ATR Length: 20 # Stricter filter

Overbought: 80 # More extreme levels

Oversold: 20

📱 Recommended Alert Settings

Strong Buy/Sell Signal: Priority ★★★

Scalping Buy/Sell Signal: Priority ★★☆

Reverse Warning: Priority ★★★ (for position management)

⚠️ Important Notes

Scalping requires quick decision-making

Multiple timeframe confirmation recommended

Exercise caution during major news events

Risk management is top priority

This indicator is a versatile multi-functional tool suitable for short to medium-term trading strategies!

🎓 Trading Examples

Scalping Example

Wait for green ● at oversold level (below 30)

Enter long position immediately

Target: 50 level or red ● signal

Stop: Below recent swing low

Day Trading Example

Histogram turns green (bullish trend)

Wait for △ buy signal near support

Target: Overbought level (75)

Exit: Warning signal ▼ appears

Risk Management Rules

Never risk more than 2% per trade

Use proper position sizing

Set stops before entry

Take partial profits at key levels

This comprehensive guide will help you maximize the potential of this advanced multi-timeframe indicator!

Advanced Volume Profile Pro Delta + POC + VAH/VAL# Advanced Volume Profile Pro - Delta + POC + VAH/VAL Analysis System

## WHAT THIS SCRIPT DOES

This script creates a comprehensive volume profile analysis system that combines traditional volume-at-price distribution with delta volume calculations, Point of Control (POC) identification, and Value Area (VAH/VAL) analysis. Unlike standard volume indicators that show only total volume over time, this script analyzes volume distribution across price levels and estimates buying vs selling pressure using multiple calculation methods to provide deeper market structure insights.

## WHY THIS COMBINATION IS ORIGINAL AND USEFUL

**The Problem Solved:** Traditional volume indicators show when volume occurs but not where price finds acceptance or rejection. Standalone volume profiles lack directional bias information, while basic delta calculations don't provide structural context. Traders need to understand both volume distribution AND directional sentiment at key price levels.

**The Solution:** This script implements an integrated approach that:

- Maps volume distribution across price levels using configurable row density

- Estimates delta (buying vs selling pressure) using three different methodologies

- Identifies Point of Control (highest volume price level) for key support/resistance

- Calculates Value Area boundaries where 70% of volume traded

- Provides real-time alerts for key level interactions and volume imbalances

**Unique Features:**

1. **Developing POC Visualization**: Real-time tracking of Point of Control migration throughout the session via blue dotted trail, revealing institutional accumulation/distribution patterns before they complete

2. **Multi-Method Delta Calculation**: Price Action-based, Bid/Ask estimation, and Cumulative methods for different market conditions

3. **Adaptive Timeframe System**: Auto-adjusts calculation parameters based on chart timeframe for optimal performance

4. **Flexible Profile Types**: N Bars Back (precise control), Days Back (calendar-based), and Session-based analysis modes

5. **Advanced Imbalance Detection**: Identifies and highlights significant buying/selling imbalances with configurable thresholds

6. **Comprehensive Alert System**: Monitors POC touches, Value Area entry/exit, and major volume imbalances

## HOW THE SCRIPT WORKS TECHNICALLY

### Core Volume Profile Methodology:

**1. Price Level Distribution:**

- Divides price range into user-defined rows (10-50 configurable)

- Calculates row height: `(Highest Price - Lowest Price) / Number of Rows`

- Distributes each bar's volume across price levels it touched proportionally

**2. Delta Volume Calculation Methods:**

**Price Action Method:**

```

Price Range = High - Low

Buy Pressure = (Close - Low) / Price Range

Sell Pressure = (High - Close) / Price Range

Buy Volume = Total Volume × Buy Pressure

Sell Volume = Total Volume × Sell Pressure

Delta = Buy Volume - Sell Volume

```

**Bid/Ask Estimation Method:**

```

Average Price = (High + Low + Close) / 3

Buy Volume = Close > Average ? Volume × 0.6 : Volume × 0.4

Sell Volume = Total Volume - Buy Volume

```

**Cumulative Method:**

```

Buy Volume = Close > Open ? Volume : Volume × 0.3

Sell Volume = Close ≤ Open ? Volume : Volume × 0.3

```

**3. Point of Control (POC) Identification:**

- Scans all price levels to find maximum volume concentration

- POC represents the price level with highest trading activity

- Acts as significant support/resistance level

- **Developing POC Feature**: Tracks POC evolution in real-time via blue dotted trail, showing how institutional interest migrates throughout the session. Upward POC migration indicates accumulation patterns, downward migration suggests distribution, providing early trend signals before price confirmation.

**4. Value Area Calculation:**

- Starts from POC and expands up/down to encompass 70% of total volume

- VAH (Value Area High): Upper boundary of value area

- VAL (Value Area Low): Lower boundary of value area

- Expansion algorithm prioritizes direction with higher volume

**5. Adaptive Range Selection:**

Based on profile type and timeframe optimization:

- **N Bars Back**: Fixed lookback period with performance optimization (20-500 bars)

- **Days Back**: Calendar-based analysis with automatic timeframe adjustment (1-365 days)

- **Session**: Current trading session or custom session times

### Performance Optimization Features:

- **Sampling Algorithm**: Reduces calculation load on large datasets while maintaining accuracy

- **Memory Management**: Clears previous drawings to prevent performance degradation

- **Safety Constraints**: Prevents excessive memory usage with configurable limits

## HOW TO USE THIS SCRIPT

### Initial Setup:

1. **Profile Configuration**: Select profile type based on trading style:

- N Bars Back: Precise control over data range

- Days Back: Intuitive calendar-based analysis

- Session: Real-time session development

2. **Row Density**: Set number of rows (30 default) - more rows = higher resolution, slower performance

3. **Delta Method**: Choose calculation method based on market type:

- Price Action: Best for trending markets

- Bid/Ask Estimate: Good for ranging markets

- Cumulative: Smoothed approach for volatile markets

4. **Visual Settings**: Configure colors, position (left/right), and display options

### Reading the Profile:

**Volume Bars:**

- **Length**: Represents relative volume at that price level

- **Color**: Green = net buying pressure, Red = net selling pressure

- **Intensity**: Darker colors indicate volume imbalances above threshold

**Key Levels:**

- **POC (Blue Line)**: Highest volume price - major support/resistance

- **VAH (Purple Dashed)**: Value Area High - upper boundary of fair value

- **VAL (Orange Dashed)**: Value Area Low - lower boundary of fair value

- **Value Area Fill**: Shaded region showing main trading range

**Developing POC Trail:**

- **Blue Dotted Lines**: Show real-time POC evolution throughout the session

- **Migration Patterns**: Upward trail indicates bullish accumulation, downward trail suggests bearish distribution

- **Early Signals**: POC movement often precedes price movement, providing advance warning of institutional activity

- **Institutional Footprints**: Reveals where smart money concentrated volume before final POC establishment

### Trading Applications:

**Support/Resistance Analysis:**

- POC acts as magnetic price level - expect reactions

- VAH/VAL provide intermediate support/resistance levels

- Profile edges show areas of low volume acceptance

**Developing POC Analysis:**

- **Upward Migration**: POC moving higher = institutional accumulation, bullish bias

- **Downward Migration**: POC moving lower = institutional distribution, bearish bias

- **Stable POC**: Tight clustering = balanced market, range-bound conditions

- **Early Trend Detection**: POC direction change often precedes price breakouts

**Entry Strategies:**

- Buy at VAL with POC as target (in uptrends)

- Sell at VAH with POC as target (in downtrends)

- Breakout plays above/below profile extremes

**Volume Imbalance Trading:**

- Strong buying imbalance (>60% threshold) suggests continued upward pressure

- Strong selling imbalance suggests continued downward pressure

- Imbalances near key levels provide high-probability setups

**Multi-Timeframe Context:**

- Use higher timeframe profiles for major levels

- Lower timeframe profiles for precise entries

- Session profiles for intraday trading structure

## SCRIPT SETTINGS EXPLANATION

### Volume Profile Settings:

- **Profile Type**: Determines data range for calculation

- N Bars Back: Exact number of bars (20-500 range)

- Days Back: Calendar days with timeframe adaptation (1-365 days)

- Session: Trading session-based (intraday focus)

- **Number of Rows**: Profile resolution (10-50 range)

- **Profile Width**: Visual width as chart percentage (10-50%)

- **Value Area %**: Volume percentage for VA calculation (50-90%, 70% standard)

- **Auto-Adjust**: Automatically optimizes for different timeframes

### Delta Volume Settings:

- **Show Delta Volume**: Enable/disable delta calculations

- **Delta Calculation Method**: Choose methodology based on market conditions

- **Highlight Imbalances**: Visual emphasis for significant volume imbalances

- **Imbalance Threshold**: Percentage for imbalance detection (50-90%)

### Session Settings:

- **Session Type**: Daily, Weekly, Monthly, or Custom periods

- **Custom Session Time**: Define specific trading hours

- **Previous Sessions**: Number of historical sessions to display

### Days Back Settings:

- **Lookback Days**: Number of calendar days to analyze (1-365)

- **Automatic Calculation**: Script automatically converts days to bars based on timeframe:

- Intraday: Accounts for 6.5 trading hours per day

- Daily: 1 bar per day

- Weekly/Monthly: Proportional adjustment

### N Bars Back Settings:

- **Lookback Bars**: Exact number of bars to analyze (20-500)

- **Precise Control**: Best for systematic analysis and backtesting

### Visual Customization:

- **Colors**: Bullish (green), Bearish (red), and level colors

- **Profile Position**: Left or Right side of chart

- **Profile Offset**: Distance from current price action

- **Labels**: Show/hide level labels and values

- **Smooth Profile Bars**: Enhanced visual appearance

### Alert Configuration:

- **POC Touch**: Alerts when price interacts with Point of Control

- **VA Entry/Exit**: Alerts for Value Area boundary interactions

- **Major Imbalance**: Alerts for significant volume imbalances

## VISUAL FEATURES

### Profile Display:

- **Horizontal Bars**: Volume distribution across price levels

- **Color Coding**: Delta-based coloring for directional bias

- **Smooth Rendering**: Optional smoothing for cleaner appearance

- **Transparency**: Configurable opacity for chart readability

### Level Lines:

- **POC**: Solid blue line with optional label

- **VAH/VAL**: Dashed colored lines with value displays

- **Extension**: Lines extend across relevant time periods

- **Value Area Fill**: Optional shaded region between VAH/VAL

### Information Table:

- **Current Values**: Real-time POC, VAH, VAL prices

- **VA Range**: Value Area width calculation

- **Positioning**: Multiple table positions available

- **Text Sizing**: Adjustable for different screen sizes

## IMPORTANT USAGE NOTES

**Realistic Expectations:**

- Volume profile analysis provides structural context, not trading signals

- Delta calculations are estimations based on price action, not actual order flow

- Past volume distribution does not guarantee future price behavior

- Combine with other analysis methods for comprehensive market view

**Best Practices:**

- Use appropriate profile types for your trading style:

- Day Trading: Session or Days Back (1-5 days)

- Swing Trading: Days Back (10-30 days) or N Bars Back

- Position Trading: Days Back (60-180 days)

- Consider market context (trending vs ranging conditions)

- Verify key levels with additional technical analysis

- Monitor profile development for changing market structure

**Performance Considerations:**

- Higher row counts increase calculation complexity

- Large lookback periods may affect chart performance

- Auto-adjust feature optimizes for most use cases

- Consider using session profiles for intraday efficiency

**Limitations:**

- Delta calculations are estimations, not actual transaction data

- Profile accuracy depends on available price/volume history

- Effectiveness varies across different instruments and market conditions

- Requires understanding of volume profile concepts for optimal use

**Data Requirements:**

- Requires volume data for accurate calculations

- Works best on liquid instruments with consistent volume

- May be less effective on very low volume or exotic instruments

This script serves as a comprehensive volume analysis tool for traders who need detailed market structure information with integrated directional bias analysis and real-time POC development tracking for informed trading decisions.

Bottom Reversal Radar — Berk v1.4Bottom Reversal Radar — Berk v1.4

What it does:

Combines RSI recovery after oversold, MACD bull cross, close above EMA8, near-EMA200 proximity, volume expansion, and simple bullish divergence (pivot lows) into a single score.

Signal: Trigger when Score ≥ Threshold (default 3). Set alert via Create Alert → “Dipten Dönüş — Ana Sinyal” → Once per bar close.

How it works

RSI recovery: After touching oversold (30), RSI crosses up 35 within last X bars.

MACD bull cross: MACD Line crosses above Signal.

Close above EMA8 and BOS (close above recent swing high) confirm momentum.

Near EMA200: Price within −5%…+2% band adds a point.

Volume spike: Volume ≥ 1.5× SMA(20) adds a point.

Bullish divergence: Lower price low + higher RSI low (pivot 3/3) adds a point.

Inputs

RSI(14), rsiOS=30, rsiRecover=35, Volume SMA(20) with 1.5× multiplier, EMA200 proximity band −5%…+2%, lookbackBars=5, Score threshold default 3.

Usage tips

Best on Daily / 4H. If too many false positives: raise threshold to 4 and volume to 1.8–2.0×.

Pair with Screener filters: RSI≥35, MACD Line>Signal, Price above EMA8, Volume/Avg(20)≥1.5, and near EMA200 (%).

Disclaimer

For educational purposes only. Not financial advice.

Release notes (v1.4)

Fixed bullDiv typo; simplified visuals; Pine v5.

Tags: rsi, macd, ema, volume, divergence, reversal, trend, screener, bist, stocks, crypto

Seasonality Monte Carlo Forecaster [BackQuant]Seasonality Monte Carlo Forecaster

Plain-English overview

This tool projects a cone of plausible future prices by combining two ideas that traders already use intuitively: seasonality and uncertainty. It watches how your market typically behaves around this calendar date, turns that seasonal tendency into a small daily “drift,” then runs many randomized price paths forward to estimate where price could land tomorrow, next week, or a month from now. The result is a probability cone with a clear expected path, plus optional overlays that show how past years tended to move from this point on the calendar. It is a planning tool, not a crystal ball: the goal is to quantify ranges and odds so you can size, place stops, set targets, and time entries with more realism.

What Monte Carlo is and why quants rely on it

• Definition . Monte Carlo simulation is a way to answer “what might happen next?” when there is randomness in the system. Instead of producing a single forecast, it generates thousands of alternate futures by repeatedly sampling random shocks and adding them to a model of how prices evolve.

• Why it is used . Markets are noisy. A single point forecast hides risk. Monte Carlo gives a distribution of outcomes so you can reason in probabilities: the median path, the 68% band, the 95% band, tail risks, and the chance of hitting a specific level within a horizon.

• Core strengths in quant finance .

– Path-dependent questions : “What is the probability we touch a stop before a target?” “What is the expected drawdown on the way to my objective?”

– Pricing and risk : Useful for path-dependent options, Value-at-Risk (VaR), expected shortfall (CVaR), stress paths, and scenario analysis when closed-form formulas are unrealistic.

– Planning under uncertainty : Portfolio construction and rebalancing rules can be tested against a cloud of plausible futures rather than a single guess.

• Why it fits trading workflows . It turns gut feel like “seasonality is supportive here” into quantitative ranges: “median path suggests +X% with a 68% band of ±Y%; stop at Z has only ~16% odds of being tagged in N days.”

How this indicator builds its probability cone

1) Seasonal pattern discovery

The script builds two day-of-year maps as new data arrives:

• A return map where each calendar day stores an exponentially smoothed average of that day’s log return (yesterday→today). The smoothing (90% old, 10% new) behaves like an EWMA, letting older seasons matter while adapting to new information.

• A volatility map that tracks the typical absolute return for the same calendar day.

It calculates the day-of-year carefully (with leap-year adjustment) and indexes into a 365-slot seasonal array so “March 18” is compared with past March 18ths. This becomes the seasonal bias that gently nudges simulations up or down on each forecast day.

2) Choice of randomness engine

You can pick how the future shocks are generated:

• Daily mode uses a Gaussian draw with the seasonal bias as the mean and a volatility that comes from realized returns, scaled down to avoid over-fitting. It relies on the Box–Muller transform internally to turn two uniform random numbers into one normal shock.

• Weekly mode uses bootstrap sampling from the seasonal return history (resampling actual historical daily drifts and then blending in a fraction of the seasonal bias). Bootstrapping is robust when the empirical distribution has asymmetry or fatter tails than a normal distribution.

Both modes seed their random draws deterministically per path and day, which makes plots reproducible bar-to-bar and avoids flickering bands.

3) Volatility scaling to current conditions

Markets do not always live in average volatility. The engine computes a simple volatility factor from ATR(20)/price and scales the simulated shocks up or down within sensible bounds (clamped between 0.5× and 2.0×). When the current regime is quiet, the cone narrows; when ranges expand, the cone widens. This prevents the classic mistake of projecting calm markets into a storm or vice versa.

4) Many futures, summarized by percentiles

The model generates a matrix of price paths (capped at 100 runs for performance inside TradingView), each path stepping forward for your selected horizon. For each forecast day it sorts the simulated prices and pulls key percentiles:

• 5th and 95th → approximate 95% band (outer cone).

• 16th and 84th → approximate 68% band (inner cone).

• 50th → the median or “expected path.”

These are drawn as polylines so you can immediately see central tendency and dispersion.

5) A historical overlay (optional)

Turn on the overlay to sketch a dotted path of what a purely seasonal projection would look like for the next ~30 days using only the return map, no randomness. This is not a forecast; it is a visual reminder of the seasonal drift you are biasing toward.

Inputs you control and how to think about them

Monte Carlo Simulation

• Price Series for Calculation . The source series, typically close.

• Enable Probability Forecasts . Master switch for simulation and drawing.

• Simulation Iterations . Requested number of paths to run. Internally capped at 100 to protect performance, which is generally enough to estimate the percentiles for a trading chart. If you need ultra-smooth bands, shorten the horizon.

• Forecast Days Ahead . The length of the cone. Longer horizons dilute seasonal signal and widen uncertainty.

• Probability Bands . Draw all bands, just 95%, just 68%, or a custom level (display logic remains 68/95 internally; the custom number is for labeling and color choice).

• Pattern Resolution . Daily leans on day-of-year effects like “turn-of-month” or holiday patterns. Weekly biases toward day-of-week tendencies and bootstraps from history.

• Volatility Scaling . On by default so the cone respects today’s range context.

Plotting & UI

• Probability Cone . Plots the outer and inner percentile envelopes.

• Expected Path . Plots the median line through the cone.

• Historical Overlay . Dotted seasonal-only projection for context.

• Band Transparency/Colors . Customize primary (outer) and secondary (inner) band colors and the mean path color. Use higher transparency for cleaner charts.

What appears on your chart

• A cone starting at the most recent bar, fanning outward. The outer lines are the ~95% band; the inner lines are the ~68% band.

• A median path (default blue) running through the center of the cone.

• An info panel on the final historical bar that summarizes simulation count, forecast days, number of seasonal patterns learned, the current day-of-year, expected percentage return to the median, and the approximate 95% half-range in percent.

• Optional historical seasonal path drawn as dotted segments for the next 30 bars.

How to use it in trading

1) Position sizing and stop logic

The cone translates “volatility plus seasonality” into distances.

• Put stops outside the inner band if you want only ~16% odds of a stop-out due to noise before your thesis can play.

• Size positions so that a test of the inner band is survivable and a test of the outer band is rare but acceptable.

• If your target sits inside the 68% band at your horizon, the payoff is likely modest; outside the 68% but inside the 95% can justify “one-good-push” trades; beyond the 95% band is a low-probability flyer—consider scaling plans or optionality.

2) Entry timing with seasonal bias

When the median path slopes up from this calendar date and the cone is relatively narrow, a pullback toward the lower inner band can be a high-quality entry with a tight invalidation. If the median slopes down, fade rallies toward the upper band or step aside if it clashes with your system.

3) Target selection

Project your time horizon to N bars ahead, then pick targets around the median or the opposite inner band depending on your style. You can also anchor dynamic take-profits to the moving median as new bars arrive.

4) Scenario planning & “what-ifs”

Before events, glance at the cone: if the 95% band already spans a huge range, trade smaller, expect whips, and avoid placing stops at obvious band edges. If the cone is unusually tight, consider breakout tactics and be ready to add if volatility expands beyond the inner band with follow-through.

5) Options and vol tactics

• When the cone is tight : Prefer long gamma structures (debit spreads) only if you expect a regime shift; otherwise premium selling may dominate.

• When the cone is wide : Debit structures benefit from range; credit spreads need wider wings or smaller size. Align with your separate IV metrics.

Reading the probability cone like a pro

• Cone slope = seasonal drift. Upward slope means the calendar has historically favored positive drift from this date, downward slope the opposite.

• Cone width = regime volatility. A widening fan tells you that uncertainty grows fast; a narrow cone says the market typically stays contained.

• Mean vs. price gap . If spot trades well above the median path and the upper band, mean-reversion risk is high. If spot presses the lower inner band in an up-sloping cone, you are in the “buy fear” zone.

• Touches and pierces . Touching the inner band is common noise; piercing it with momentum signals potential regime change; the outer band should be rare and often brings snap-backs unless there is a structural catalyst.

Methodological notes (what the code actually does)

• Log returns are used for additivity and better statistical behavior: sim_ret is applied via exp(sim_ret) to evolve price.

• Seasonal arrays are updated online with EWMA (90/10) so the model keeps learning as each bar arrives.

• Leap years are handled; indexing still normalizes into a 365-slot map so the seasonal pattern remains stable.

• Gaussian engine (Daily mode) centers shocks on the seasonal bias with a conservative standard deviation.

• Bootstrap engine (Weekly mode) resamples from observed seasonal returns and adds a fraction of the bias, which captures skew and fat tails better.

• Volatility adjustment multiplies each daily shock by a factor derived from ATR(20)/price, clamped between 0.5 and 2.0 to avoid extreme cones.

• Performance guardrails : simulations are capped at 100 paths; the probability cone uses polylines (no heavy fills) and only draws on the last confirmed bar to keep charts responsive.

• Prerequisite data : at least ~30 seasonal entries are required before the model will draw a cone; otherwise it waits for more history.

Strengths and limitations

• Strengths :

– Probabilistic thinking replaces single-point guessing.

– Seasonality adds a small but meaningful directional bias that many markets exhibit.

– Volatility scaling adapts to the current regime so the cone stays realistic.

• Limitations :

– Seasonality can break around structural changes, policy shifts, or one-off events.

– The number of paths is performance-limited; percentile estimates are good for trading, not for academic precision.

– The model assumes tomorrow’s randomness resembles recent randomness; if regime shifts violently, the cone will lag until the EWMA adapts.

– Holidays and missing sessions can thin the seasonal sample for some assets; be cautious with very short histories.

Tuning guide

• Horizon : 10–20 bars for tactical trades; 30+ for swing planning when you care more about broad ranges than precise targets.

• Iterations : The default 100 is enough for stable 5/16/50/84/95 percentiles. If you crave smoother lines, shorten the horizon or run on higher timeframes.

• Daily vs. Weekly : Daily for equities and crypto where month-end and turn-of-month effects matter; Weekly for futures and FX where day-of-week behavior is strong.

• Volatility scaling : Keep it on. Turn off only when you intentionally want a “pure seasonality” cone unaffected by current turbulence.

Workflow examples

• Swing continuation : Cone slopes up, price pulls into the lower inner band, your system fires. Enter near the band, stop just outside the outer line for the next 3–5 bars, target near the median or the opposite inner band.

• Fade extremes : Cone is flat or down, price gaps to the upper outer band on news, then stalls. Favor mean-reversion toward the median, size small if volatility scaling is elevated.

• Event play : Before CPI or earnings on a proxy index, check cone width. If the inner band is already wide, cut size or prefer options structures that benefit from range.

Good habits

• Pair the cone with your entry engine (breakout, pullback, order flow). Let Monte Carlo do range math; let your system do signal quality.

• Do not anchor blindly to the median; recalc after each bar. When the cone’s slope flips or width jumps, the plan should adapt.

• Validate seasonality for your symbol and timeframe; not every market has strong calendar effects.

Summary

The Seasonality Monte Carlo Forecaster wraps institutional risk planning into a single overlay: a data-driven seasonal drift, realistic volatility scaling, and a probabilistic cone that answers “where could we be, with what odds?” within your trading horizon. Use it to place stops where randomness is less likely to take you out, to set targets aligned with realistic travel, and to size positions with confidence born from distributions rather than hunches. It will not predict the future, but it will keep your decisions anchored to probabilities—the language markets actually speak.

Correlation HeatMap Matrix Data [TradingFinder]🔵 Introduction

Correlation is a statistical measure that shows the degree and direction of a linear relationship between two assets.

Its value ranges from -1 to +1 : +1 means perfect positive correlation, 0 means no linear relationship, and -1 means perfect negative correlation.

In financial markets, correlation is used for portfolio diversification, risk management, pairs trading, intermarket analysis, and identifying divergences.

Correlation HeatMap Matrix Data TradingFinder is a Pine Script v6 library that calculates and returns raw correlation matrix data between up to 20 symbols. It only provides the data – it does not draw or render the heatmap – making it ideal for use in other scripts that handle visualization or further analysis. The library uses ta.correlation for fast and accurate calculations.

It also includes two helper functions for visual styling :

CorrelationColor(corr) : takes the correlation value as input and generates a smooth gradient color, ranging from strong negative to strong positive correlation.

CorrelationTextColor(corr) : takes the correlation value as input and returns a text color that ensures optimal contrast over the background color.

Library

"Correlation_HeatMap_Matrix_Data_TradingFinder"

CorrelationColor(corr)

Parameters:

corr (float)

CorrelationTextColor(corr)

Parameters:

corr (float)

Data_Matrix(Corr_Period, Sym_1, Sym_2, Sym_3, Sym_4, Sym_5, Sym_6, Sym_7, Sym_8, Sym_9, Sym_10, Sym_11, Sym_12, Sym_13, Sym_14, Sym_15, Sym_16, Sym_17, Sym_18, Sym_19, Sym_20)

Parameters:

Corr_Period (int)

Sym_1 (string)

Sym_2 (string)

Sym_3 (string)

Sym_4 (string)

Sym_5 (string)

Sym_6 (string)

Sym_7 (string)

Sym_8 (string)

Sym_9 (string)

Sym_10 (string)

Sym_11 (string)

Sym_12 (string)

Sym_13 (string)

Sym_14 (string)

Sym_15 (string)

Sym_16 (string)

Sym_17 (string)

Sym_18 (string)

Sym_19 (string)

Sym_20 (string)

🔵 How to use

Import the library into your Pine Script using the import keyword and its full namespace.

Decide how many symbols you want to include in your correlation matrix (up to 20). Each symbol must be provided as a string, for example FX:EURUSD .

Choose the correlation period (Corr\_Period) in bars. This is the lookback window used for the calculation, such as 20, 50, or 100 bars.

Call Data_Matrix(Corr_Period, Sym_1, ..., Sym_20) with your selected parameters. The function will return an array containing the correlation values for every symbol pair (upper triangle of the matrix plus diagonal).

For example :

var string Sym_1 = '' , var string Sym_2 = '' , var string Sym_3 = '' , var string Sym_4 = '' , var string Sym_5 = '' , var string Sym_6 = '' , var string Sym_7 = '' , var string Sym_8 = '' , var string Sym_9 = '' , var string Sym_10 = ''

var string Sym_11 = '', var string Sym_12 = '', var string Sym_13 = '', var string Sym_14 = '', var string Sym_15 = '', var string Sym_16 = '', var string Sym_17 = '', var string Sym_18 = '', var string Sym_19 = '', var string Sym_20 = ''

switch Market

'Forex' => Sym_1 := 'EURUSD' , Sym_2 := 'GBPUSD' , Sym_3 := 'USDJPY' , Sym_4 := 'USDCHF' , Sym_5 := 'USDCAD' , Sym_6 := 'AUDUSD' , Sym_7 := 'NZDUSD' , Sym_8 := 'EURJPY' , Sym_9 := 'EURGBP' , Sym_10 := 'GBPJPY'

,Sym_11 := 'AUDJPY', Sym_12 := 'EURCHF', Sym_13 := 'EURCAD', Sym_14 := 'GBPCAD', Sym_15 := 'CADJPY', Sym_16 := 'CHFJPY', Sym_17 := 'NZDJPY', Sym_18 := 'AUDNZD', Sym_19 := 'USDSEK' , Sym_20 := 'USDNOK'

'Stock' => Sym_1 := 'NVDA' , Sym_2 := 'AAPL' , Sym_3 := 'GOOGL' , Sym_4 := 'GOOG' , Sym_5 := 'META' , Sym_6 := 'MSFT' , Sym_7 := 'AMZN' , Sym_8 := 'AVGO' , Sym_9 := 'TSLA' , Sym_10 := 'BRK.B'

,Sym_11 := 'UNH' , Sym_12 := 'V' , Sym_13 := 'JPM' , Sym_14 := 'WMT' , Sym_15 := 'LLY' , Sym_16 := 'ORCL', Sym_17 := 'HD' , Sym_18 := 'JNJ' , Sym_19 := 'MA' , Sym_20 := 'COST'

'Crypto' => Sym_1 := 'BTCUSD' , Sym_2 := 'ETHUSD' , Sym_3 := 'BNBUSD' , Sym_4 := 'XRPUSD' , Sym_5 := 'SOLUSD' , Sym_6 := 'ADAUSD' , Sym_7 := 'DOGEUSD' , Sym_8 := 'AVAXUSD' , Sym_9 := 'DOTUSD' , Sym_10 := 'TRXUSD'

,Sym_11 := 'LTCUSD' , Sym_12 := 'LINKUSD', Sym_13 := 'UNIUSD', Sym_14 := 'ATOMUSD', Sym_15 := 'ICPUSD', Sym_16 := 'ARBUSD', Sym_17 := 'APTUSD', Sym_18 := 'FILUSD', Sym_19 := 'OPUSD' , Sym_20 := 'USDT.D'

'Custom' => Sym_1 := Sym_1_C , Sym_2 := Sym_2_C , Sym_3 := Sym_3_C , Sym_4 := Sym_4_C , Sym_5 := Sym_5_C , Sym_6 := Sym_6_C , Sym_7 := Sym_7_C , Sym_8 := Sym_8_C , Sym_9 := Sym_9_C , Sym_10 := Sym_10_C

,Sym_11 := Sym_11_C, Sym_12 := Sym_12_C, Sym_13 := Sym_13_C, Sym_14 := Sym_14_C, Sym_15 := Sym_15_C, Sym_16 := Sym_16_C, Sym_17 := Sym_17_C, Sym_18 := Sym_18_C, Sym_19 := Sym_19_C , Sym_20 := Sym_20_C

= Corr.Data_Matrix(Corr_period, Sym_1 ,Sym_2 ,Sym_3 ,Sym_4 ,Sym_5 ,Sym_6 ,Sym_7 ,Sym_8 ,Sym_9 ,Sym_10,Sym_11,Sym_12,Sym_13,Sym_14,Sym_15,Sym_16,Sym_17,Sym_18,Sym_19,Sym_20)

Loop through or index into this array to retrieve each correlation value for your custom layout or logic.

Pass each correlation value to CorrelationColor() to get the corresponding gradient background color, which reflects the correlation’s strength and direction (negative to positive).

For example :

Corr.CorrelationColor(SYM_3_10)

Pass the same correlation value to CorrelationTextColor() to get the correct text color for readability against that background.

For example :

Corr.CorrelationTextColor(SYM_1_1)

Use these colors in a table or label to render your own heatmap or any other visualization you need.

Scanner ADX & VolumenThis indicator is a market scanner specifically designed for scalping traders. Its function is to simultaneously monitor 30 cryptocurrency pairs from the BingX exchange to identify entry opportunities based on the start of a new, strengthening trend.

Strategy and Logic:

The scanner is based on the combination of two key conditions on a 15-minute timeframe:

Trend Strength (ADX): The primary signal is generated when the ADX (Average Directional Index) crosses above the 20 level. An ADX moving above this threshold suggests that the market is breaking out of a consolidation phase and that a new trend (either bullish or bearish) is beginning to gain strength.

Volume Confirmation: To validate the ADX signal, the indicator checks if the current candle's volume is higher than its simple moving average (defaulting to 20 periods). An increase in volume confirms market interest and participation, adding greater reliability to the emerging move.

How to Use It:

The indicator displays a table in the top-right corner of your chart with the following information:

Par: The name of the cryptocurrency pair.

ADX: The current ADX value. It turns green when it exceeds the 20 level.

Volume: Shows "OK" if the current volume is higher than its average.

Signal: This is the most important column. When both conditions (ADX crossover and high volume) are met, it will display the message "¡ENTRADA!" ("ENTRY!") with a highlighted background, alerting you to a potential trading opportunity.

In summary, this scanner saves you the effort of manually analyzing 30 charts, allowing you to focus solely on the assets that present the best conditions for a scalping trade.

Scanner ADX & Volumen This indicator is a market scanner specifically designed for scalping traders. Its function is to simultaneously monitor 30 cryptocurrency pairs from the BingX exchange to identify entry opportunities based on the start of a new, strengthening trend.

Strategy and Logic:

The scanner is based on the combination of two key conditions on a 15-minute timeframe:

Trend Strength (ADX): The primary signal is generated when the ADX (Average Directional Index) crosses above the 20 level. An ADX moving above this threshold suggests that the market is breaking out of a consolidation phase and that a new trend (either bullish or bearish) is beginning to gain strength.

Volume Confirmation: To validate the ADX signal, the indicator checks if the current candle's volume is higher than its simple moving average (defaulting to 20 periods). An increase in volume confirms market interest and participation, adding greater reliability to the emerging move.

How to Use It:

The indicator displays a table in the top-right corner of your chart with the following information:

Par: The name of the cryptocurrency pair.

ADX: The current ADX value. It turns green when it exceeds the 20 level.

Volume: Shows "OK" if the current volume is higher than its average.

Signal: This is the most important column. When both conditions (ADX crossover and high volume) are met, it will display the message "¡ENTRADA!" ("ENTRY!") with a highlighted background, alerting you to a potential trading opportunity.

In summary, this scanner saves you the effort of manually analyzing 30 charts, allowing you to focus solely on the assets that present the best conditions for a scalping trade.

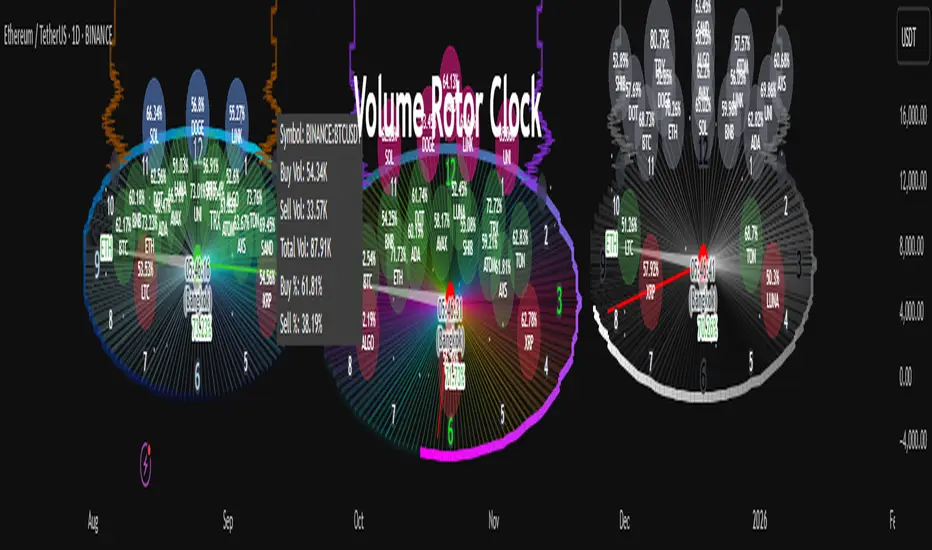

Volume Rotor Clock [hapharmonic]🕰️ Volume Rotor Clock

The Volume Rotor Clock is an indicator that separates buy and sell volume, compiling these volumes over a recent number of bars or a specified past period, as defined by the user. This helps to reveal accumulation (buying) or distribution (selling) behavior, showing which side has superior volume. With its unique and beautiful display, the Volume Rotor Clock is more than just a timepiece; it's a dynamic dashboard that visualizes the buying and selling pressure of your favorite symbols, all wrapped in an elegant and fully customizable interface.

Instead of just tracking price, this indicator focuses on the engine behind the movement: volume. It helps you instantly identify which assets are under accumulation (buying) and which are under distribution (selling).

---

🎨 20 Pre-configured Templates

---

🧐 Interpreting the Clock Display

The interface is designed to give you multiple layers of information at a glance. Let's break down what each part represents.

1. The Main Clock Hands (Current Chart Symbol)

The clock hands—hour, minute, and second—are dedicated to the symbol on your current active chart .

Minute Hand: Displays the base currency of the current symbol (e.g., USDT, USD) at its tip.

Hour Hand: Displays the percentage of the winning volume side (buy vs. sell) at its tip.

Color Gauge: The color of the text characters at the tip of both the hour and minute hands acts as your primary volume gauge for the current symbol.

If buy volume is dominant , the text will be green .

If sell volume is dominant , the text will be red .

Tooltip: Hovering your mouse over the text at the tip of the hour or minute or other spherical elements hand will reveal a detailed tooltip with the precise Buy Volume, Sell Volume, Total Volume, Buy %, and Sell % for the current chart's symbol.

2. The Volume Scanner: Bulls & Bears (Symbols Inside the Clock) 🐂🐻

The circular symbols scattered inside the clock face are your multi-symbol volume scanner. They represent the assets you've selected in the indicator's settings.

Green Circles (Bulls - Upper Half): These represent symbols from your list where the total buy volume is greater than the total sell volume over the defined "Lookback" period. They are considered to be under bullish accumulation. The size of the circle and its text grows larger as the buy percentage becomes more dominant. The percentage shown within the circle represents the buy volume's share of the total volume, calculated over the 'Lookback (Bars)' you've set.

Red Circles (Bears - Lower Half): These represent symbols where the total sell volume is greater than the total buy volume. They are considered to be under bearish distribution or selling pressure. The size of the circle indicates the dominance of the sell-side volume. The percentage shown within the circle represents the sell volume's share of the total volume, calculated over the 'Lookback (Bars)' you've set.

3. The Bullish Watchlist (Symbols Above the Clock) ⭐

The symbols arranged neatly along the top edge of the clock are the "best of the bulls." They are symbols that are not only bullish but have also passed an additional, powerful strength filter.

What it Means: A symbol appears here when it shows signs of sustained, high-volume buying interest . It's a way to filter out noise and focus on assets with potentially significant accumulation phases.

The Filter Logic: For a bullish symbol (where total buy volume > total sell volume) to be promoted to the watchlist, its trading volume must meet specific criteria based on this formula:

ta.barssince(not(volume > ta.sma(volume, X))) >= Y

In plain English, this means: The indicator checks how many consecutive bars the `volume` has been greater than its `X`-bar Simple Moving Average (`ta.sma(volume, X)`). If this count is greater than or equal to `Y` bars, the condition is met.

(You can configure `X` (Volume MA Length) and `Y` (Consecutive Days Above MA) in the settings.)

Why it's Useful: This filter is powerful because it looks for consistency . A single spike in volume can be an anomaly. However, when an asset's volume remains consistently above its recent average for several consecutive days, it strongly suggests that larger players or a significant portion of the market are actively accumulating the asset. This sustained interest can often precede a significant upward price trend.

---

⚙️ Indicator Settings Explained

The Volume Rotor Clock is highly customizable. Here’s a detailed walkthrough of every setting available in the "Inputs" tab.

🎨 Color Scheme

This group allows you to control the entire aesthetic of the clock.

Template: Choose from a wide variety of professionally designed color themes.

Use Template: A simple checkbox to switch between using a pre-designed theme and creating your own.

`Checked`: You can select a theme from the dropdown menu, which offers 20 unique templates like "Cyberpunk Neon" or "Forest Green". All custom color settings below will be disabled (grayed out and unclickable).

`Unchecked`: The template dropdown is disabled, and you gain full control over every color element in the sections below.

🖌️ Custom Appearance & Colors

These settings are only active when "Use Template" is unchecked.

Flame Head / Tail: Sets the start and end colors for the dynamic flame effect that traces the clock's border, representing the second hand.

Numbers / Main Numbers: Customize the color of the regular hour numbers (1, 2, 4, 5...) and the main cardinal numbers (3, 6, 9, 12).

Sunburst Colors (1-6): Controls the six colors used in the gradient background for the "sunburst" effect inside the clock face.

Hands & Digital: Fine-tune the colors for the Hour/Minute Hand, Second Hand, central Pivot point, and the digital time display.

Chain Color / Width: Customize the appearance of the two chains holding the clock.

📡 Volume Scanner

Control the behavior of the multi-symbol scanner.

Show Scanner Labels: A master switch to show or hide all the bull/bear symbol circles inside the clock.

Lookback (Bars): A crucial setting that defines the calculation period for buy/sell volume for all scanned symbols. The calculation is a sum over the specified number of recent bars.

`0`: Calculates using the current bar only .

`7`: Calculates the sum of volume over the last 8 bars (the current bar + 7 historical bars).

Symbols List: Here you can enable/disable up to 20 slots and input the ticker for each symbol you want to scan (e.g., BINANCE:BTCUSDT , NASDAQ:AAPL ).

⭐ Bullish Watchlist Filter

Configure the criteria for the elite watchlist symbols displayed above the clock.

Enable Watchlist: A master switch to turn the entire watchlist feature on or off.

Volume MA Length: Sets the lookback period `(X)` for the Simple Moving Average of volume used in the filter.

Consecutive Days Above MA: Sets the minimum number of consecutive days `(Y)` that volume must close above its MA to qualify.

Symbols Per Row: Determines the maximum number of watchlist symbols that can fit in a single row before a new row is created above it.

Background / Text Color: When not using a template, you can set custom colors for the watchlist symbols' background and text.

📏 Position & Size

Adjust the clock's placement and dimensions on your chart.

Clock Timezone: Sets the timezone for the digital and analog time display. You can use standard formats like "America/New_York" or enter "Exchange" to sync with the chart's timezone.

Radius (Bars): Controls the overall size of the clock. The radius is measured in terms of the number of bars on the x-axis.

X Offset (Bars): Moves the entire clock horizontally. Positive values shift it to the right; negative values shift it to the left.

Y Offset (Price %): Moves the entire clock vertically as a percentage of your screen's price pane. Positive values move it up; negative values move it down.

Egg vs Tennis Ball — Drop/Rebound StrengthEgg vs Tennis Ball — Drop/Rebound Meter

What it does

Classifies selloffs as either:

Eggs — dead‑cat, no bounce

Tennis Balls — fast, decisive rebound

Core features

Detects swing drops from a Pivot High (PH) to a Pivot Low (PL)

Requires drops to be meaningful (volatility‑aware, ATR‑scaled)

Draws a bounce threshold line and a deadline

Decides outcome based on speed and extent of rebound

Tracks scores and win rates across multiple lookback windows

Includes a color‑coded meter and current streak display

Visuals at a glance

Gray diagonal — drop from PH to PL

Teal dotted horizontal — bounce threshold, from PH to the deadline

Solid green — Tennis Ball (bounce line broken before the deadline)

Solid red — Egg (deadline expired before the bounce)

Optional PH / PL labels for clarity

How the decision is made

1) Find pivots — symmetric pivots using Pivot Left / Right; PL confirms after Right bars.

2) Qualify the drop — Drop Size = PH − PL; must be ≥ (Drop Threshold × ATR at PL).

3) Define the bounce line — PL + (Bounce Multiple × Drop Size). 1.00× = full retrace to PH; up to 2.00× for overshoot.

4) Set the deadline — Drop Bars = PL index − PH index; Deadline = Drop Bars × Recovery Factor; timer starts from PH or PL.

5) Resolve — Tennis Ball if price hits the bounce line before the deadline; Egg if the deadline passes first.

Scoring system (−100 to +100)

+100 = perfect Tennis Ball (fastest possible + full overshoot)

−100 = perfect Egg (no recovery)

In between: scored by rebound speed and extent, shaped by your weight settings

Meter Table

Columns (toggle on/off)

All (off by default)

Last N1 (default 5)

Last N2 (default 10)

Last N3 (default 20)

Rows

Tennis / Eggs — counts

% Tennis — win rate

Avg Score — normalized quality from −100 to +100

Streak — overall (not windowed), e.g., +3 = 3 Tennis Balls in a row, −4 = 4 Eggs in a row

Alerts

Tennis Ball – Fast Rebound — triggers when the bounce line is broken in time

Egg – Window Expired — triggers when the deadline passes without a bounce

Inputs

① Drop Detection

Pivot Left / Right

ATR Length

Drop Threshold × ATR

② Bounce Requirement

Bounce Multiple × Drop Size (0.10–2.00×)

③ Timing

Timer Start — PH or PL

Recovery Factor × Drop Bars

Break Trigger — Close or High

④ Display

Show Pivot/Outcome Labels

Line Width

Table Position (corner)

⑤ Meter Columns

Show All (off by default)

Show N1 / N2 / N3 (5, 10, 20 by default)

⑥ Scoring Weights