MACD At Scales with AlertsI use the horizontal scale lines on the MACD indicator as part of my scalping strategy along with other indicators like RSI/EMA and Market Cipher B when trading BTC

I am looking for a cross above or below the 12.5 and 25 horizontal scale lines, along with lining up other indicators

I set my alerts on the 5 min TF and look to the 15 and 30 min TF's for further confirmation.

I have find the scale lines to be very useful for visual reference of the crosses, above/below 25 lines is mostly a safer trade, crosses above/below 12.5 lines can have more risk, crosses between 0 baseline and 12.5 can have a higher return but have much more risk.

Don't ever use just this indicator by itself, you must always have at least 2 indicators running

This is an example of the TF's not lining up, so a entry here would be high risk

This is an example of the TF's lining up, so a entry here would be less risk

Cari dalam skrip untuk "25年黄金价格走势预测"

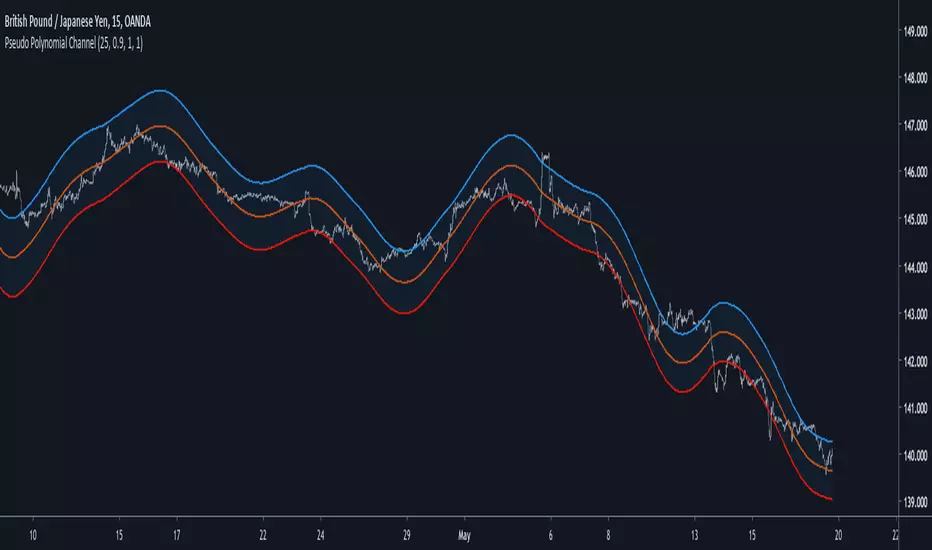

Pseudo Polynomial ChannelIntroduction

Back when i started using pine i made a script called periodic channel who aimed to rescale an average correlated sine wave to the price...don't worked very well. So i tried to fix problems induced by the indicator without much success, i had to redo it from scratch while abandoning the idea of rescaling correlated smooth functions to the price, at that time i also received requests regarding polynomial channel, some plateformes included this indicator, this led me to the idea to estimate it in order to both respond to the periodic channel problems and the requests i received, i have tried many many things and recently i tweaked a linear extrapolation to have an approximation.

Linear Extrapolation To Pseudo Polynomial Regression

I could be wrong but a polynomial regression must use constant parameters in order to provide a really smooth output, at least constant for a set of time. The moving averages forms (Savitzky-Golay moving average) who smooth polynomials across a window to the data don't have such smoothness, so how to estimate a polynomial regression while having a parameter providing control over the smoothness, a response to this is by using a recursive linear extrapolation. I posted a linear extrapolation indicator long ago, i used the same formula while adding a function to morph the output and the input in the form of :

morph * output + (1-morph) * input

How can this provide an estimate of a polynomial regression ? Well i'm not even sure myself but if you use the output as input (morph = 1) for the linear extrapolation function you should get a rough estimate of a line, this is what i thought at first and it proved to be right

Based on this observation i thought that it would be possible to get polynomial results by lowering morph, and as expected it worked well but showed a periodic pattern, this is why i smooth k in line 10.

0.9 for morph work well, higher values create sometimes smoother results but damage heavily the estimation.

Parameters

Morph have been introduced earlier, it control the amount of output and input the linear extrapolation should process, lower values create rougher but more stables results, if you see that the estimation is going nuts lower morph or change length, also lower length if you increase morph .

High overshoot, morph to 0.8 can help have a better estimation at the cost of less smoothness.

Length control the indicator smoothing, this parameter differ heavily from other filters, therefore low values can create mid/long term smoothing, it can also depend on which market instrument you are applying it, so there are no fixed optimal length.

Mult control how spread the bands are, to do so mult multiply the cumulative mean error, you can change this error measurement by anything you want like standard deviation/atr/range but take into account that you may create a separate parameter to control the error instead of length . Mult can be a float and like length can have different optimal values depending on the market the indicator is applied to.

Flatten do exactly what is name imply, it flatten the overall output to have a better estimation, can be a float. The result is less smooth.

Flatten = 2

More Exemples

BTCUSD length = 25 and mult = 4

XPDUSD length = 25 and mult = 1

ALPHABET length = 6 and morph = 0.99

Conclusion

I tried to estimate a polynomial channel by using recursion in the linear extrapolation function. This build is way more stable than the periodic channel but its still a bit inaccurate in my opinion. I hope this code can still help someone build something really nice, if so share your results :)

I apologize for those expecting a legit polynomial channel build but i really don't know how to do that, as i said parameters for the regression must be constants, i hope it still fine :)

Thanks for reading !

Modified Gann HiLo ActivatorIntroduction

The gann hilo activator is a trend indicator developed by Robert Krausz published into W. D. Gann Treasure Discovered: Simple Trading Plans for Stocks & Commodities . This indicator crate a trailing stop aiming to show the direction of the trend.

This indicator is fairly easy to compute and dont require lot of skills to understand. First we calculate the simple moving average of both price high and price low, when the close price is higher than the moving average of the price high the indicator return the moving average of the price low, else the indicator return the moving average of the price high if the close price is lower than the moving average of the price low.

My indicator add a different calculation method in order to avoid whipsaw trades as well as adding significance to the moving average length. A Median method has been added to provide more robustness.

The Indicator

The indicator is a simple trailing stop aiming to show the direction of the trend. The indicator use a different source instead of the price high/low for its calculation. The first method is the "SMA" method which like the classic hilo indicator use a simple moving average for the calculation of the indicator.

Sma Method with length = 25

The "Median" use a moving median instead of a simple moving average, this provide more robustness.

Median Method with length = 25

The shape is less curved and the indicator can sometimes avoid whipsaw with high's length periods.

Mult Parameter

The mult parameter is a parameter set to be lower or equal to 1 and greater or equal to 0. High values allow the indicator to be far from the price thus avoiding whipsaw trades, lower ones lower the distance from the price. A mult parameter of 0.1 approximate the original hilo indicator.

In blue the indicator with mult = 0.1 and in radical red the original hilo activator.

Conclusion

The modifications allow more control over the indicator as well as adding more robustness while the original one is destined to fail when market price is more complex.

Thanks for reading :)

For any questions/suggestions feel free to pm me

Average Candle LengthThis script is designed to show you the average candle size in pips (wick to wick) for however many bars you choose (20 is default).

The idea is that if the average candle size for the last 20 bars is, let's say 25, you would probably not want to set your stop loss less than 25 because it is more likely to get hit.

if you find this script helpful, tips and donations are always appreciated (venmo @rick-munoz) :)

Future Least Squares Moving Average//+------------------------------------------------------------------+

// | Future Least Squares Moving Average |

// | 未来予測LSMA |

// | Ver.1.0 |

// | Copyright Sakura |

//+------------------------------------------------------------------+

//LSMAは一時回帰直線の現在地の点の集合であるということは、未来の点を使えば未来を描けるはずというアホなことを無理やり考えました。

//結論はうまくいかなかったですので、パラメーターをいじって誤魔化しという結果に。

//それでも、先に書いてますので急激な価格変動に対処できる訳もなくといった感じになっています。

//displacementは一目に合わせたいので26固定の方向でとしたいところですが厳しいですね。

//

//設定例

//SMA(25)≒FLSMA(25,7,13)

//SMA(50)≒FLSMA(50,13,26)

//SMA(75)≒FLSMA(75,20,26)

How to automate this strategy for free using a chrome extension.Hey everyone,

Recently we developed a chrome extension for automating TradingView strategies using the alerts they provide. Initially we were charging a monthly fee for the extension, but we have now decided to make it FREE for everyone. So to display the power of automating strategies via TradingView, we figured we would also provide a profitable strategy along with the custom alert script and commands for the alerts so you can easily cut and paste to begin trading for profit while you sleep.

Step 1:

You are going to need to download the Chrome Extension called AutoView. You can get the extension for free by following this link: bit.ly ( I had to shorten the link as it contains Google and TV automatically converts it to a symbol)

Step 2: Go to your chrome extension page, and under the new extension you'll see a "settings" button. In the setting you will have to connect and give permission to the exchange 1broker allowing the extension to place your orders automatically when triggered by an alert.

Step 3: Setup the strategy and custom script for the alerts in TradingView. The attached script is the strategy, you can play with the settings yourself to try and get better numbers/performance if you please.

This following script is for the custom alerts:

//@version=2

study("4All-Alert", shorttitle="Alerts")

src = close

len = input(4, minval=1, title="Length")

up = rma(max(change(src), 0), len)

down = rma(-min(change(src), 0), len)

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

rsin = input(5)

sn = 100 - rsin

ln = 0 + rsin

short = crossover(rsi, sn) ? 1 : 0

long = crossunder(rsi, ln) ? 1 : 0

plot(long, "Long", color=green)

plot(short, "Short", color=red)

Now that you have the extension installed, the custom strategy and alert scripts in place, you simply need to create the alerts.

To get the alerts to communicate with the extension properly, there is a specific syntax that you will need to put in the message of the alert. You can find more details about the syntax here : gist.github.com

For this specific strategy, I use the Alerts script, long/short greater than 0.9 on close.

In the message for a long place this as your message:

Long

c=order b=short

c=position b=short l=200 t=market

b=long q=0.01 l=200 t=market tp=13 sl=25

and for the short...

Short

c=order b=long

c=position b=long l=200 t=market

b=short q=0.01 l=200 t=market tp=13 sl=25

If you'll notice in my above messages, compared to the strategy my tp and sl (take profit and stop loss) vary by a few pips. This is to cover the market opens and spread on 1broker. You can change the tp and sl in the strategy to the above and see that the overall profit will not vary much at all.

I hope this all makes sense and it is enough to not only make some people money, but to show the power of coming up with your own strategy and automating it using TradingView alerts and the free Chrome Extension AutoView.

ps. I highly recommend upgrading your TradingView account so you have access to back testing and multiple alerts.

There is really no reason you won't cover the cost and then some on a monthly basis using the tools provided.

Best of luck and happy trading.

Note: The extension currently allows for automation on 2 exchanges; 1broker and Okcoin. If you do not have accounts there, we'd appreciate you signing up using our referral links.

www.okcoin.com

1broker.com

BOCS Channel Scalper Indicator - Mean Reversion Alert System# BOCS Channel Scalper Indicator - Mean Reversion Alert System

## WHAT THIS INDICATOR DOES:

This is a mean reversion trading indicator that identifies consolidation channels through volatility analysis and generates alert signals when price enters entry zones near channel boundaries. **This indicator version is designed for manual trading with comprehensive alert functionality.** Unlike automated strategies, this tool sends notifications (via popup, email, SMS, or webhook) when trading opportunities occur, allowing you to manually review and execute trades. The system assumes price will revert to the channel mean, identifying scalp opportunities as price reaches extremes and preparing to bounce back toward center.

## INDICATOR VS STRATEGY - KEY DISTINCTION:

**This is an INDICATOR with alerts, not an automated strategy.** It does not execute trades automatically. Instead, it:

- Displays visual signals on your chart when entry conditions are met

- Sends customizable alerts to your device/email when opportunities arise

- Shows TP/SL levels for reference but does not place orders

- Requires you to manually enter and exit positions based on signals

- Works with all TradingView subscription levels (alerts included on all plans)

**For automated trading with backtesting**, use the strategy version. For manual control with notifications, use this indicator version.

## ALERT CAPABILITIES:

This indicator includes four distinct alert conditions that can be configured independently:

**1. New Channel Formation Alert**

- Triggers when a fresh BOCS channel is identified

- Message: "New BOCS channel formed - potential scalp setup ready"

- Use this to prepare for upcoming trading opportunities

**2. Long Scalp Entry Alert**

- Fires when price touches the long entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "LONG scalp signal at 24731.75 | TP: 24743.2 | SL: 24716.5"

**3. Short Scalp Entry Alert**

- Fires when price touches the short entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "SHORT scalp signal at 24747.50 | TP: 24735.0 | SL: 24762.75"

**4. Any Entry Signal Alert**

- Combined alert for both long and short entries

- Use this if you want a single alert stream for all opportunities

- Message: "BOCS Scalp Entry: at "

**Setting Up Alerts:**

1. Add indicator to chart and configure settings

2. Click the Alert (⏰) button in TradingView toolbar

3. Select "BOCS Channel Scalper" from condition dropdown

4. Choose desired alert type (Long, Short, Any, or Channel Formation)

5. Set "Once Per Bar Close" to avoid false signals during bar formation

6. Configure delivery method (popup, email, webhook for automation platforms)

7. Save alert - it will fire automatically when conditions are met

**Alert Message Placeholders:**

Alerts use TradingView's dynamic placeholder system:

- {{ticker}} = Symbol name (e.g., NQ1!)

- {{close}} = Current price at signal

- {{plot_1}} = Calculated take profit level

- {{plot_2}} = Calculated stop loss level

These placeholders populate automatically, creating detailed notification messages without manual configuration.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This indicator is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Indicator**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the indicator ideal for active day traders who want continuous alert opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased signal frequency also means higher potential commission costs and requires disciplined trade selection when acting on alerts.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The indicator normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The indicator uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The indicator tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The indicator uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. Visual markers (arrows and labels) appear on chart, and configured alerts fire immediately.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents alert spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long alert will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The indicator includes a multi-timeframe ATR filter to avoid alerts during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while viewing 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Alerts enabled

- If ATR < threshold: No alerts fire

This prevents notifications during dead zones where mean reversion is unreliable due to insufficient price movement. The ATR status is displayed in the info table with visual confirmation (✓ or ✗).

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. These levels are displayed as visual lines with labels and included in alert messages for reference when manually placing orders.

### Stop Loss Placement:

Stop losses are calculated just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. SL levels are displayed on chart and included in alert notifications as suggested stop placement.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

## INPUT PARAMETERS:

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long alert generation on/off

- **Enable Short Scalps**: Toggle short alert generation on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between alerts (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for alert enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time indicator status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Long Color**: Customize long signal color (default: darker green for readability)

- **Short Color**: Customize short signal color (default: red)

- **TP/SL Colors**: Customize take profit and stop loss line colors

- **Line Length**: Visual length of TP/SL reference lines (5-200 bars)

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short alerts

- **TP/SL reference lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing channel status, last signal, entry/TP/SL prices, risk/reward ratio, and ATR filter status

- **Visual confirmation** when alerts fire via on-chart markers synchronized with notifications

## HOW TO USE:

### For 1-3 Minute Scalping with Alerts (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars to reduce alert spam

- **Alert Setup**: Configure "Any Entry Signal" for combined long/short notifications

- **Execution**: When alert fires, verify chart visuals, then manually place limit order at entry zone with provided TP/SL levels

### For 5-15 Minute Day Trading with Alerts:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- **Alert Setup**: Configure separate "Long Scalp Entry" and "Short Scalp Entry" alerts if you trade directionally based on bias

- **Execution**: Review channel structure on alert, confirm ATR filter shows ✓, then enter manually

### For 30-60 Minute Swing Scalping with Alerts:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- **Alert Setup**: Use "New Channel Formation" to prepare for setups, then "Any Entry Signal" for execution alerts

- **Execution**: Larger timeframes allow more analysis time between alert and entry

### Webhook Integration for Semi-Automation:

- Configure alert webhook URL to connect with platforms like TradersPost, TradingView Paper Trading, or custom automation

- Alert message includes all necessary order parameters (direction, entry, TP, SL)

- Webhook receives structured data when signal fires

- External platform can auto-execute based on alert payload

- Still maintains manual oversight vs full strategy automation

## USAGE CONSIDERATIONS:

- **Manual Discipline Required**: Alerts provide opportunities but execution requires judgment. Not all alerts should be taken - consider market context, trend, and channel quality

- **Alert Timing**: Alerts fire on bar close by default. Ensure "Once Per Bar Close" is selected to avoid false signals during bar formation

- **Notification Delivery**: Mobile/email alerts may have 1-3 second delay. For immediate execution, use desktop popups or webhook automation

- **Cooldown Necessity**: Without cooldown, rapidly touching price action can generate excessive alerts. Start with 3-bar cooldown and adjust based on alert volume

- **ATR Filter Impact**: Enabling ATR filter dramatically reduces alert count but improves quality. Track filter status in info table to understand when you're receiving fewer alerts

- **Commission Awareness**: High alert frequency means high potential trade count. Calculate if your commission structure supports frequent scalping before acting on all alerts

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features are not included in this indicator version. Multi-timeframe ATR requires higher-tier TradingView subscription for request.security() functionality on timeframes below chart timeframe.

## KNOWN LIMITATIONS:

- **Indicator does not execute trades** - alerts are informational only; you must manually place all orders

- **Alert delivery depends on TradingView infrastructure** - delays or failures possible during platform issues

- **No position tracking** - indicator doesn't know if you're in a trade; you must manage open positions independently

- **TP/SL levels are reference only** - you must manually set these on your broker platform; they are not live orders

- **Immediate touch entry can generate many alerts** in choppy zones without adequate cooldown

- **Channel deletion at 10-tick breaks** may be too aggressive or lenient depending on instrument tick size

- **ATR filter from lower timeframes** requires TradingView Premium/Pro+ for request.security()

- **Mean reversion logic fails** in strong breakout scenarios - alerts will fire but trades may hit stops

- **No partial closing capability** - full position management is manual; you determine scaling out

- **Alerts do not account for gaps** or overnight price changes; morning alerts may be stale

## RISK DISCLOSURE:

Trading involves substantial risk of loss. This indicator provides signals for educational and informational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Mean reversion strategies can experience extended drawdowns during trending markets. Alerts are not guaranteed to be profitable and should be combined with your own analysis. Stop losses may not fill at intended levels during extreme volatility or gaps. Never trade with capital you cannot afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Always verify alerts against current market conditions before executing trades manually.

## ACKNOWLEDGMENT & CREDITS:

This indicator is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based alert generation, comprehensive alert condition system with customizable notifications, multi-timeframe ATR volatility filtering, cooldown period for alert management, dual TP methods (fixed points vs channel percentage), visual TP/SL reference lines, and real-time status monitoring table. This indicator version is specifically designed for manual traders who prefer alert-based decision making over automated execution.

MTL One-Stop PRO Here’s the English version you can paste into the script description or a Telegram post.

---

# MTL One-Stop PRO v6

**EMAs • PDH/PDL • PWH/PWL • PMH/PML • RSI/ADX/OBV/ATR • Readiness**

## What it draws on the chart

* **EMA bands (21/50/200)** on price + a **21–50 ribbon** — quick read of impulse/pullback and location vs. the moving averages.

* **Prior period levels:**

* **PDH/PDL** (previous day high/low) — *blue*.

* **PWH/PWL** (previous week high/low) — *orange dashed*.

* **PMH/PML** (previous month high/low) — *purple dashed*.

Labels are printed on the right margin to keep the chart clean.

* **“Readiness” panel** (bottom-right): summary metrics and quick long/short readiness scores.

## Readiness panel — fields & meaning

* **TF / Trend**

* `Trend 1 (21>50>200)` — bullish EMA stack.

* `Trend −1 (21<50<200)` — bearish EMA stack.

* `Trend = mix` — mixed/sideways structure.

* **RSI** (calculated on the selected TF) — momentum gauge. Rule of thumb: >50 bullish, <50 bearish.

* **ADX** — trend strength. Practical zone **20–25+**.

* **ATR %** — volatility as % of price (= ATR(14)/Close·100). Helps classify regime: low/normal/high.

* **OBV ↑/↓** — accumulation/distribution direction (arrow from the OBV slope/smoothing).

* **Near PDH? / Near PDL?** — proximity flags to key extremes (within a user-set threshold; handy for breakout/fakeout/retest scenarios).

* **LongScore / ShortScore (0–5)** — quick “readiness” rating:

* +1 for trend aligned with the scenario (EMA stack).

* +1 for RSI in favor.

* +1 for ADX in the working zone.

* +1 for OBV in favor.

* +1 for price positioning (for longs — closer to **PDL/PWL** pullback or **PDH/PWH** breakout; for shorts — the opposite).

Sum → priority: **4–5/5** aggressive, **2–3/5** only with a pattern, **0–1/5** skip.

## How to read & use (fits the “Top-setup 1D/3D/1W” flow)

## Settings (main groups)

* **EMAs (on price):** lengths/visibility 21/50/200, enable the 21–50 “ribbon”.

* **Levels:** toggles for **PDH/PDL**, **PWH/PWL**, **PMH/PML**.

* **Oscillators (calc TF):** choose the timeframe used to compute **RSI/ADX/OBV/ATR** (e.g., compute on **D** while analyzing 1H/3H).

* **Readiness:** proximity threshold to levels (in ATR fractions), working-zone bounds for ADX/RSI.

## Pro tips

* **Colors map to period:** purple = month, orange = week, blue = day.

* Watch **level clusters** (e.g., PWH≈PMH): frequent reversal/fakeout zones.

* **ATR %** guides tactics: in low vol, breakouts underperform; in higher vol, retests and fakeouts improve.

## Important

The indicator **does not generate auto-signals** or replace risk management. It structures levels/context and speeds up the workflow of your checklist (SMC/liquidity/EMA/ATR/RSI/ADX/OBV) in the 1D/3D/1W pipeline.

---

Want a mini “recommended thresholds” card (RSI/ADX/ATR%) per TF and a 60-second “how to build a trade” tutorial for the description?

BOCS Channel Scalper Strategy - Automated Mean Reversion System# BOCS Channel Scalper Strategy - Automated Mean Reversion System

## WHAT THIS STRATEGY DOES:

This is an automated mean reversion trading strategy that identifies consolidation channels through volatility analysis and executes scalp trades when price enters entry zones near channel boundaries. Unlike breakout strategies, this system assumes price will revert to the channel mean, taking profits as price bounces back from extremes. Position sizing is fully customizable with three methods: fixed contracts, percentage of equity, or fixed dollar amount. Stop losses are placed just outside channel boundaries with take profits calculated either as fixed points or as a percentage of channel range.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This strategy is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Version**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the scalper ideal for active day traders who want continuous opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased trade frequency also means higher commission costs and requires tighter risk management.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The strategy normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The strategy uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The strategy tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The strategy uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. This captures mean reversion opportunities as price reaches channel extremes.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents signal spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long signal will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The strategy includes a multi-timeframe ATR filter to avoid trading during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while trading on 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Trading enabled

- If ATR < threshold: No signals fire

This prevents entries during dead zones where mean reversion is unreliable due to insufficient price movement.

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. Larger percentages aim for opposite channel edge.

### Stop Loss Placement:

Stop losses are placed just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. If price breaks through, the range is no longer valid and position exits.

### Trade Execution Logic:

When entry conditions are met (price in zone, cooldown satisfied, ATR filter passed, no existing position):

1. Calculate entry price at zone boundary

2. Calculate TP and SL based on selected method

3. Execute strategy.entry() with calculated position size

4. Place strategy.exit() with TP limit and SL stop orders

5. Update info table with active trade details

The strategy enforces one position at a time by checking strategy.position_size == 0 before entry.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

### Position Sizing System:

Three methods calculate position size:

**Fixed Contracts**:

- Uses exact contract quantity specified in settings

- Best for futures traders (e.g., "trade 2 NQ contracts")

**Percentage of Equity**:

- position_size = (strategy.equity × equity_pct / 100) / close

- Dynamically scales with account growth

**Cash Amount**:

- position_size = cash_amount / close

- Maintains consistent dollar exposure regardless of price

## INPUT PARAMETERS:

### Position Sizing:

- **Position Size Type**: Choose Fixed Contracts, % of Equity, or Cash Amount

- **Number of Contracts**: Fixed quantity per trade (1-1000)

- **% of Equity**: Percentage of account to allocate (1-100%)

- **Cash Amount**: Dollar value per position ($100+)

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long entries on/off

- **Enable Short Scalps**: Toggle short entries on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between signals (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for trade enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time strategy status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Color Settings**: Customize long/short/TP/SL colors

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short entries

- **Active TP/SL lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing position status, channel state, last signal, entry/TP/SL prices, and ATR status

## HOW TO USE:

### For 1-3 Minute Scalping (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars

- Position Size: 1-2 contracts

### For 5-15 Minute Day Trading:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- Position Size: Fixed contracts or 5-10% equity

### For 30-60 Minute Swing Scalping:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- Position Size: % of equity recommended

## BACKTEST CONSIDERATIONS:

- Strategy performs best in ranging, mean-reverting markets

- Strong trending markets produce more stop losses as price breaks channels

- ATR filter significantly reduces trade count but improves quality during low volatility

- Cooldown period trades signal quantity for signal quality

- Commission and slippage materially impact sub-5-minute timeframe performance

- Shorter timeframes require tighter entry zones (15-20%) to catch quick reversions

- % of Channel TP adapts better to varying channel sizes than fixed points

- Fixed contract sizing recommended for consistent risk per trade in futures

**Backtesting Parameters Used**: This strategy was developed and tested using realistic commission and slippage values to provide accurate performance expectations. Recommended settings: Commission of $1.40 per side (typical for NQ futures through discount brokers), slippage of 2 ticks to account for execution delays on fast-moving scalp entries. These values reflect real-world trading costs that active scalpers will encounter. Backtest results without proper cost simulation will significantly overstate profitability.

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features require data feed with volume information but are optional for core functionality.

## KNOWN LIMITATIONS:

- Immediate touch entry can fire multiple times in choppy zones without adequate cooldown

- Channel deletion at 10-tick breaks may be too aggressive or lenient depending on instrument tick size

- ATR filter from lower timeframes requires higher-tier TradingView subscription (request.security limitation)

- Mean reversion logic fails in strong breakout scenarios leading to stop loss hits

- Position sizing via % of equity or cash amount calculates based on close price, may differ from actual fill price

- No partial closing capability - full position exits at TP or SL only

- Strategy does not account for gap openings or overnight holds

## RISK DISCLOSURE:

Trading involves substantial risk of loss. Past performance does not guarantee future results. This strategy is for educational purposes and backtesting only. Mean reversion strategies can experience extended drawdowns during trending markets. Stop losses may not fill at intended levels during extreme volatility or gaps. Thoroughly test on historical data and paper trade before risking real capital. Use appropriate position sizing and never risk more than you can afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Automated trading systems can malfunction - monitor all live positions actively.

## ACKNOWLEDGMENT & CREDITS:

This strategy is built upon the channel detection methodology created by **AlgoAlpha** in the "Smart Money Breakout Channels" indicator. Full credit and appreciation to AlgoAlpha for pioneering the normalized volatility approach to identifying consolidation patterns. The core channel formation logic using normalized price standard deviation is AlgoAlpha's original contribution to the TradingView community.

Enhancements to the original concept include: mean reversion entry logic (vs breakout), immediate touch-based signals, multi-timeframe ATR volatility filtering, flexible position sizing (fixed/percentage/cash), cooldown period filtering, dual TP methods (fixed points vs channel percentage), automated strategy execution with exit management, and real-time position monitoring table.

Multi Indicator Screener# 📊 Multi-Indicator Screener | BB + KC Squeeze + RSI + MACD + ADX

### 🔹 Institutional-Grade Multi-Symbol Scanner with Breakout Alerts

---

## 📌 Overview

The **Multi-Indicator Screener** is an advanced dashboard that monitors **10 symbols simultaneously** with **multi-indicator confluence**:

- 🔹 **Bollinger Bands + Keltner Channel (Squeeze Logic)**

- 🔹 **RSI + MACD Confirmation**

- 🔹 **ADX Trend Strength**

- 🔹 **ATR-based Trailing Stops**

- 🔹 **Volume-Confirmed Breakouts**

Designed for **professional traders**, this screener highlights **high-probability setups** across multiple assets in real time.

---

## ✨ Key Features

### 🔹 Bollinger Band Suite

- ✅ Detects **directional bias** (Bullish / Bearish / Neutral).

- ✅ Marks **Breakouts (Up/Down)** with optional **volume confirmation**.

- ✅ LazyBear-style **Squeeze Detection**:

- 🔒 Squeeze ON → Low volatility, contraction phase.

- 🚀 Squeeze OFF → Breakout potential.

- Neutral → No clear squeeze.

### 🔹 RSI + MACD Confluence

- ✅ RSI confirmation above user-defined threshold (default 55).

- ✅ MACD crossover confirmation.

- ✅ RSI value color-coded in table:

- 🔴 Oversold (<30)

- 🟢 Strong bullish (>60)

- 🟢 Lime (>75 = very strong)

- 🟠 Neutral zone

### 🔹 ADX Trend Strength

- ✅ Displays **ADX value**, plus **+DI / -DI**.

- ✅ ADX > 25 → Highlighted as strong trend.

### 🔹 ATR Trailing Stop Loss

- ✅ Auto-calculated **buy-side trailing stop** & **sell-side trailing stop**.

- ✅ Adjustable via multiplier input.

### 🔹 Multi-Symbol Screener Table

- ✅ Preloaded with **Top 10 Nifty 50 symbols** (customizable).

- ✅ Dashboard columns include:

- Symbol

- BB Direction

- Breakout

- Squeeze Status

- Higher-TF BB Confirmation

- RSI + MACD Signals

- RSI Value

- ADX, +DI, -DI

- Trailing SL (Buy/Sell)

- Volume Confirmation

---

## 🔔 Alerts

Each symbol has **independent breakout alerts**:

- 📢 `Volume-Confirmed BB Breakout Detected`

Alerts fire when a **breakout above/below Bollinger Bands** is confirmed with **above-average volume**.

---

## 📖 How to Use

1. **Select Symbols**

- By default, loads top Nifty 50 stocks.

- Replace with your preferred tickers (`NSE:RELIANCE`, `NASDAQ:AAPL`, `BINANCE:BTCUSDT`, etc.).

2. **Enable Presets**

- **Scalping Mode** → BB Length = 10, Multiplier = 1.5 (more sensitive).

- **Swing Mode** → BB Length = 30, Multiplier = 2.5 (smoother).

3. **Monitor Table**

- Look for **✔️ confirmations** across BB, RSI, MACD, ADX, and Volume.

- Strong setups = multiple confirmations aligning.

4. **Set Alerts**

- Add alerts for your desired symbols to never miss a breakout.

---

## 🎯 Best For

- ✅ Scalpers & Swing Traders

- ✅ Multi-asset monitoring (stocks, forex, crypto)

- ✅ Traders using **volatility breakout + momentum confirmation**

- ✅ Institutional-style dashboard users

---

## ⚠️ Disclaimer

This script is for **educational purposes only**.

It is **not financial advice**. Please backtest before trading.

---

BNF 25/50 MA Pullback Screener (Uptrend-Below / Downtrend-Above)Buy candidates: stocks in an uptrend (25MA > 50MA, optional rising slopes) that are currently pulled back below the MAs.

• Sell/short candidates: stocks in a downtrend (25MA < 50MA, optional falling slopes) that are currently pushed above the MAs.

It plots the MAs, paints the background for trend context, drops signals on the chart, shows a status panel, and exposes alert conditions so you can screen your watchlist via alerts.

Kalman Ema Crosses - [JTCAPITAL]Kalman EMA Crosses - is a modified way to use Kalman Filters applied on Exponential Moving Averages (EMA Crosses) for Trend-Following.

The Kalman filter is a recursive smoothing algorithm that reduces noise from raw price or indicator data, and in this script it is applied both directly to price and on top of EMA calculations. The goal is to create cleaner, more reliable crossover signals between two EMAs that are less prone to false triggers caused by volatility or market noise.

The indicator works by calculating in the following steps:

Source Selection

The script starts by selecting the price input (default is Close, but can be adjusted). This chosen source is the foundation for all further smoothing and EMA calculations.

Kalman Filtering on Price

Depending on user settings, the selected source is passed through one of two independent Kalman filters. The filter takes into account process noise (representing expected market randomness) and measurement noise (representing uncertainty in the price data). The Kalman filter outputs a smoothed version of price that minimizes noise and preserves underlying trend structure.

EMA Calculation

Two exponential moving averages (EMA 1 and EMA 2) are then computed on the Kalman-smoothed price. The lengths of these EMAs are fully customizable (default 15 and 25).

Kalman Filtering on EMA Values

Instead of directly using raw EMA curves, the script applies a second layer of Kalman filtering to the EMA values themselves. This step significantly reduces whipsaw behavior, creating smoother crossovers that emphasize real momentum shifts rather than temporary volatility spikes.

Trend Detection via EMA Crossovers

-A bullish trend is detected when EMA 1 (fast) crosses above EMA 2 (slow).

-A bearish trend is detected when EMA 1 crosses below EMA 2.

The detected trend state is stored and used to dynamically color the plots.

Visual Representation

Both EMAs are plotted on the chart. Their colors shift to blue during bullish phases and purple during bearish phases. The area between the two EMAs is filled with a shaded region to clearly highlight trending conditions.

Buy and Sell Conditions :

- Buy Condition : When the Kalman-smoothed EMA 1 crosses above the Kalman-smoothed EMA 2, a bullish crossover is confirmed.

- Sell Condition : When EMA 1 crosses below EMA 2, a bearish crossover is confirmed.

Users may enhance the robustness of these signals by adjusting process noise, measurement noise, or EMA lengths. Lower measurement noise values make the filter react faster (but potentially noisier), while higher values make it smoother (but slower).

Features and Parameters :

- Source : Selectable price input (Close, Open, High, Low, etc.).

- EMA 1 Length : Defines the fast EMA period.

- EMA 2 Length : Defines the slow EMA period.

- Process Noise : Controls how much randomness the Kalman filter assumes in price dynamics.

- Measurement Noise : Controls how much uncertainty is assumed in raw input data.

- Kalman Usage : Option to apply Kalman filtering either before EMA calculation (on price) or after (on EMA values).

Specifications :

Kalman Filter

The Kalman filter is an optimal recursive algorithm that estimates the state of a system from noisy measurements. In trading, it is used to smooth prices or indicator values. By balancing process noise (expected volatility) with measurement noise (data uncertainty), it generates a smoothed signal that reacts adaptively to market conditions.

Exponential Moving Average (EMA)

An EMA is a weighted moving average that emphasizes recent data more heavily than older data. This makes it more responsive than a simple moving average (SMA). EMAs are widely used to identify trends and momentum shifts.

EMA Crossovers

The crossing of a fast EMA above a slow EMA suggests bullish momentum, while the opposite suggests bearish momentum. This is a cornerstone technique in trend-following systems.

Dual Kalman Filtering

Applying Kalman both to raw price and to the EMAs themselves reduces whipsaws further. It creates crossover signals that are not only smoothed but also validated across two levels of noise reduction. This significantly enhances signal reliability compared to traditional EMA crossovers.

Process Noise

Represents the filter’s assumption about how much the underlying market can randomly change between steps. Higher values make the filter adapt faster to sudden changes, while lower values make it more stable.

Measurement Noise

Represents uncertainty in price data. A higher measurement noise value means the filter trusts the model more than the observed data, leading to smoother results. A lower value makes the filter more reactive to observed price fluctuations.

Trend Coloring & Fill

The use of dynamic colors and filled regions provides immediate visual recognition of trend states, helping traders act faster and with greater clarity.

Enjoy!

Stochastic [Paifc0de]Stochastic — clean stochastic oscillator with visual masking, neutral markers, and basic filters

What it does

This indicator plots a standard stochastic oscillator (%K with smoothing and %D) and adds practical quality-of-life features for lower timeframes: optional visual masking when %K hugs overbought/oversold, neutral K–D cross markers, session-gated edge triangles (K crossing 20/80), and simple filters (minimum %K slope, minimum |K–D| gap, optional %D slope agreement, mid-zone mute, and a cooldown between markers). Display values are clamped to 0–100 to keep the panel scale stable. The tool is for research/education and does not generate entries/exits or financial advice.

Default preset: 20 / 10 / 10

K Length = 20

Classic lookback used in many textbooks. On intraday charts it balances responsiveness and stability: short enough to react to momentum shifts, long enough to avoid constant whipsaws. In practice it captures ~the last 20 bars’ position of close within the high–low range.

K Smoothing = 10

A 10-period SMA applied to the raw %K moderates the “saw-tooth” effect that raw stochastic can exhibit in choppy phases. The smoothing reduces over-reaction to micro spikes while preserving the main rhythm of swings; visually, %K becomes a continuous path that is easier to read.

D Length = 10

%D is the moving average of smoothed %K. With 10, %D becomes a clearly slower guide line. The larger separation between %K(10-SMA) and %D(10-SMA of %K) produces cleaner crosses and fewer spurious toggles than micro settings (e.g., 3/3/3). On M5–M15 this pair often yields readable cross cycles without flooding the chart.

How the 20/10/10 trio behaves

In persistent trends, %K will spend more time near 20 or 80; the 10-period smoothing delays flips slightly and emphasizes only meaningful turn attempts.

In ranges, %K oscillates around mid-zone (40–60). With 10/10 smoothing, cross signals cluster less densely; combining with the |K–D| gap filter helps keep only decisive crosses.

If your symbol is unusually volatile or illiquid, reduce K Length (e.g., 14) or reduce K Smoothing (e.g., 7) to keep responsiveness. If crosses feel late, decrease D Length (e.g., 7). If noise is excessive, increase K Smoothing first, then consider raising D Length.

Visuals

OB/OS lines: default 80/20 reference levels and a midline at 50.

Masking near edges: %K can be temporarily hidden when it is pressing an edge, approaching it with low slope, or going nearly flat near the boundary. This keeps the panel readable during “stuck at the edge” phases.

Soft glow (optional): highlights %K’s active path; can be turned off.

Light/Dark palette: quick toggle to match your chart theme.

Scale safety: all plotted values (lines, fills, markers) are clamped to 0–100 to prevent the axis from expanding beyond the stochastic range.

Markers and filters

Neutral K–D cross markers: circles in the mid-zone when %K crosses %D.

Edge triangles: show when %K crosses 20 or 80; can be restricted to a session window (02:00–12:00 ET).

Filters (optional):

Min %K slope: require a minimum absolute slope so very flat crosses are ignored.

Min |K–D| gap: demand separation between lines at the cross moment.

%D slope agreement: keep crosses that align with %D’s direction.

Mid-zone mute: suppress crosses inside a user-defined 40–60 band (defaults).

Cooldown: minimum bars between successive markers.

Parameters (quick guide)

K Length / K Smoothing / D Length: core stochastic settings. Start with 20/10/10; tune K Smoothing first if you see too much jitter.

Overbought / Oversold (80/20): adjust for assets that tend to trend (raise to 85/15) or mean-revert (lower to 75/25).

Slope & gap filters: increase on very noisy symbols; reduce if you miss too many crosses.

Session window (triangles only): use if you want edge markers only during active hours.

Marker size and offset: cosmetic; they do not affect calculations.

Alerts

K–D Cross Up (filtered) and K–D Cross Down (filtered): fire when a cross passes your filters/cooldown.

Edge Up / Edge Down: fire when %K crosses the 20/80 levels.

All alerts confirm on bar close.

Notes & attribution

Original implementation and integration by Paifc0de; no third-party code is copied.

This indicator is for research/education and does not provide entries/exits or financial advice.

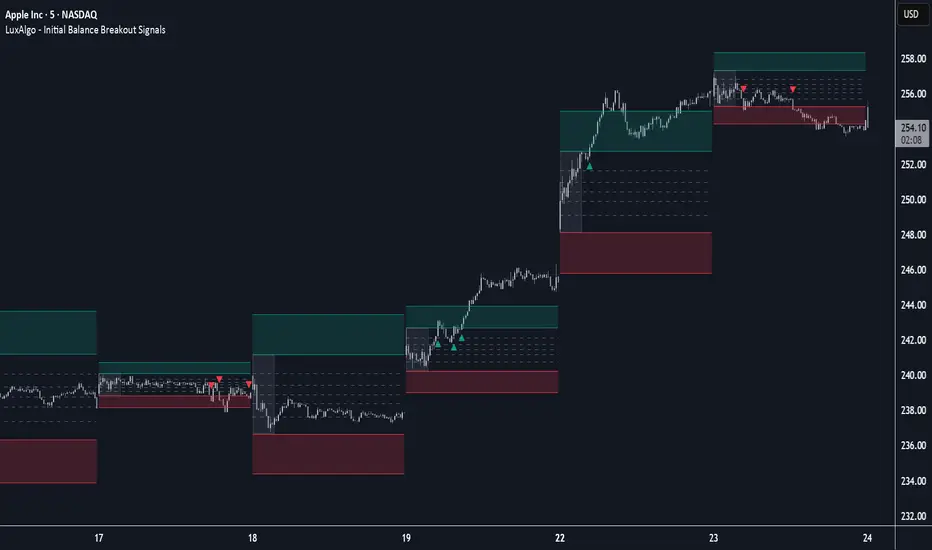

Initial Balance Breakout Signals [LuxAlgo]The Initial Balance Breakout Signals help traders identify breakouts of the Initial Balance (IB) range.

The indicator includes automatic detection of IB or can use custom sessions, highlights top and bottom IB extensions, custom Fibonacci levels, and goes further with an IB forecast with two different modes.

🔶 USAGE

The initial balance is the price range made within the first hour of the trading session. It is an intraday concept based on the idea that high volume and volatility enter the market through institutional trading at the start of the session, setting the tone for the rest of the day.

The initial balance is useful for gauging market sentiment, or, in other words, the relationship between buyers and sellers.

Bullish sentiment: Price trades above the IB range.

Mixed sentiment: Price trades within the IB range.

Bearish sentiment: Price trades below the IB range.

The initial balance high and low are important levels that many traders use to gauge sentiment. There are two main ideas behind trading around the IB range.

IB Extreme Breakout: When the price breaks and holds the IB high or low, there is a high probability that the price will continue in that direction.

IB Extreme Rejection: When the price tries to break those levels but fails, there is a high probability that it will reach the opposite IB extreme.

This indicator is a complete Initial Balance toolset with custom sessions, breakout signals, IB extensions, Fibonacci retracements, and an IB forecast. All of these features will be explained in the following sections.

🔹 Custom Sessions and Signals

By default, sessions for Initial Balance and breakout signals are in Auto mode. This means that Initial Balance takes the first hour of the trading session and shows breakout signals for the rest of the session.

With this option, traders can use the tool for open range trading, making it highly versatile. The concept behind open range (OR) is the same as that of initial balance (IB), but in OR, the range is determined by the first minute, three or five minutes, or up to the first 30 minutes of the trading session.

As shown in the image above, the top chart uses the Auto feature for the IB and Breakouts sessions. The bottom chart has the Auto feature disabled to use custom sessions for both parameters. In this case, the first three minutes of the trading session are used, turning the tool into an Open Range trading indicator.

This chart shows another example of using custom sessions to display overnight NASDAQ futures sessions.

The left chart shows a custom session from the Tokyo open to the London open, and the right chart shows a custom session from the London open to the New York open.

The chart shows both the Asian and European sessions, their top and bottom extremes, and the breakout signals from those extremes.

🔹 Initial Balance Extensions

Traders can easily extend both extremes of the Initial Balance to display their preferred targets for breakouts. Enable or disable any of them and set the IB percentage to use for the extension.

As the chart shows, the percentage selected on the settings panel directly affects the displayed levels.

Setting 25 means the tool will use a quarter of the detected initial balance range for extensions beyond the IB extremes. Setting 100 means the full IB range will be used.

Traders can use these extensions as targets for breakout signals.

🔹 Fibonacci Levels

Traders can display default or custom Fibonacci levels on the IB range to trade retracements and assess the strength of market movements. Each level can be enabled or disabled and customized by level, color, and line style.

As we can see on the chart, after the IB was completed, prices were unable to fall below the 0.236 Fibonacci level. This indicates significant bullish pressure, so it is expected that prices will rise.

Traders can use these levels as guidelines to assess the strength of the side trying to penetrate the IB. In this case, the sellers were unable to move the market beyond the first level.

🔹 Initial Balance Forecast

The tool features two different forecasting methods for the current IB. By default, it takes the average of the last ten values and applies a multiplier of one.

IB Against Previous Open: averages the difference between IB extremes and the open of the previous session.

Filter by current day of the week: averages the difference between IB extremes and the open of the current session for the same day of the week.

This feature allows traders to see the difference between the current IB and the average of the last IBs. It makes it very easy to interpret: if the current IB is higher than the average, buyers are in control; if it is lower than the average, sellers are in control.

For example, on the left side of the chart, we can see that the last day was very bullish because the IB was completely above the forecasted value. This is the IB mean of the last ten trading days.

On the right, we can see that on Monday, September 15, the IB traded slightly higher but within the forecasted value of the IB mean of the last ten Mondays. In this case, it is within expectations.

🔶 SETTINGS

Display Last X IBs: Select how many IBs to display.

Initial Balance: Choose a custom session or enable the Auto feature.

Breakouts: Enable or disable breakouts. Choose custom session or enable the Auto feature.

🔹 Extensions

Top Extension: Enable or disable the top extension and choose the percentage of IB to use.

Bottom extension: Enable or disable the bottom extension and choose the percentage of IB to use.

🔹 Fibonacci Levels

Display Fibonacci: Enable or disable Fibonacci levels.

Reverse: Reverse Fibonacci levels.

Levels, Colors & Style

Display Labels: Enable or disable labels and choose text size.

🔹 Forecast

Display Forecast: Select the forecast method.

- IB Against Previous Open: Calculates the average difference between the IB high and low and the previous day's IB open price.

- Filter by Current Day of Week: Calculates the average difference between the IB high and low and the IB open price for the same day of the week.

Forecast Memory: The number of data points used to calculate the average.

Forecast Multiplier: This multiplier will be applied to the average. Bigger numbers will result in wider predicted ranges.

Forecast Colors: Choose from a variety of colors.

Forecast Style: Choose a line style.

🔹 Style

Initial Balance Colors

Extension Transparency: Choose the extension's transparency. 0 is solid, and 100 is fully transparent.

Options Max Pain Calculator [BackQuant]Options Max Pain Calculator

A visualization tool that models option expiry dynamics by calculating "max pain" levels, displaying synthetic open interest curves, gamma exposure profiles, and pin-risk zones to help identify where market makers have the least payout exposure.

What is Max Pain?

Max Pain is the theoretical expiration price where the total dollar value of outstanding options would be minimized. At this price level, option holders collectively experience maximum losses while option writers (typically market makers) have minimal payout obligations. This creates a natural gravitational pull as expiration approaches.

Core Features

Visual Analysis Components:

Max Pain Line: Horizontal line showing the calculated minimum pain level

Strike Level Grid: Major support and resistance levels at key option strikes

Pin Zone: Highlighted area around max pain where price may gravitate

Pain Heatmap: Color-coded visualization showing pain distribution across prices

Gamma Exposure Profile: Bar chart displaying net gamma at each strike level

Real-time Dashboard: Summary statistics and risk metrics

Synthetic Market Modeling**

Since Pine Script cannot access live options data, the indicator creates realistic synthetic open interest distributions based on configurable market parameters including volume patterns, put/call ratios, and market maker positioning.

How It Works

Strike Generation:

The tool creates a grid of option strikes centered around the current price. You can control the range, density, and whether strikes snap to realistic market increments.

Open Interest Modeling:

Using your inputs for average volume, put/call ratios, and market maker behavior, the indicator generates synthetic open interest that mirrors real market dynamics:

Higher volume at-the-money with decay as strikes move further out

Adjustable put/call bias to reflect current market sentiment

Market maker inventory effects and typical short-gamma positioning

Weekly options boost for near-term expirations

Pain Calculation:

For each potential expiry price, the tool calculates total option payouts:

Call options contribute pain when finishing in-the-money

Put options contribute pain when finishing in-the-money

The strike with minimum total pain becomes the Max Pain level

Gamma Analysis:

Net gamma exposure is calculated at each strike using standard option pricing models, showing where hedging flows may be most intense. Positive gamma creates price support while negative gamma can amplify moves.

Key Settings

Basic Configuration:

Number of Strikes: Controls grid density (recommended: 15-25)

Days to Expiration: Time until option expiry

Strike Range: Price range around current level (recommended: 8-15%)

Strike Increment: Spacing between strikes

Market Parameters:

Average Daily Volume: Baseline for synthetic open interest

Put/Call Volume Ratio: Market sentiment bias (>1.0 = bearish, <1.0 = bullish) It does not work if set to 1.0

Implied Volatility: Current option volatility estimate

Market Maker Factors: Dealer positioning and hedging intensity

Display Options:

Model Complexity: Simple (line only), Standard (+ zones), Advanced (+ heatmap/gamma)

Visual Elements: Toggle individual components on/off

Theme: Dark/Light mode

Update Frequency: Real-time or daily calculation

Reading the Display

Dashboard Table (Top Right):

Current Price vs Max Pain Level

Distance to Pain: Percentage gap (smaller = higher pin risk)

Pin Risk Assessment: HIGH/MEDIUM/LOW based on proximity and time

Days to Expiry and Strike Count

Model complexity level

Visual Elements:

Red Line: Max Pain level where payout is minimized

Colored Zone: Pin risk area around max pain

Dotted Lines: Major strike levels (green = support, orange = resistance)

Color Bar: Pain heatmap (blue = high pain, red = low pain/max pain zones)

Horizontal Bars: Gamma exposure (green = positive, red = negative)

Yellow Dotted Line: Gamma flip level where hedging behavior changes

Trading Applications

Expiration Pinning:

When price is near max pain with limited time remaining, there's increased probability of gravitating toward that level as market makers hedge their positions.

Support and Resistance:

High open interest strikes often act as magnets, with max pain representing the strongest gravitational pull.

Volatility Expectations:

Above gamma flip: Expect dampened volatility (long gamma environment)

Below gamma flip: Expect amplified moves (short gamma environment)

Risk Assessment:

The pin risk indicator helps gauge likelihood of price manipulation near expiry, with HIGH risk suggesting potential range-bound action.

Best Practices

Setup Recommendations

Start with Model Complexity set to "Standard"

Use realistic strike ranges (8-12% for most assets)

Set put/call ratio based on current market sentiment

Adjust implied volatility to match current levels

Interpretation Guidelines:

Small distance to pain + short time = high pin probability

Large gamma bars indicate key hedging levels to monitor

Heatmap intensity shows strength of pain concentration

Multiple nearby strikes can create wider pin zones

Update Strategy:

Use "Daily" updates for cleaner visuals during trading hours

Switch to "Every Bar" for real-time analysis near expiration

Monitor changes in max pain level as new options activity emerges

Important Disclaimers

This is a modeling tool using synthetic data, not live market information. While the calculations are mathematically sound and the modeling realistic, actual market dynamics involve numerous factors not captured in any single indicator.

Max pain represents theoretical minimum payout levels and suggests where natural market forces may create gravitational pull, but it does not guarantee price movement or predict exact expiration levels. Market gaps, news events, and changing volatility can override these dynamics.

Use this tool as additional context for your analysis, not as a standalone trading signal. The synthetic nature of the data makes it most valuable for understanding market structure and potential zones of interest rather than precise price prediction.

Technical Notes

The indicator uses established option pricing principles with simplified implementations optimized for Pine Script performance. Gamma calculations use standard financial models while pain calculations follow the industry-standard definition of minimized option payouts.

All visual elements use fixed positioning to prevent movement when scrolling charts, and the tool includes performance optimizations to handle real-time calculation without timeout errors.

Small Business Economic Conditions - Statistical Analysis ModelThe Small Business Economic Conditions Statistical Analysis Model (SBO-SAM) represents an econometric approach to measuring and analyzing the economic health of small business enterprises through multi-dimensional factor analysis and statistical methodologies. This indicator synthesizes eight fundamental economic components into a composite index that provides real-time assessment of small business operating conditions with statistical rigor. The model employs Z-score standardization, variance-weighted aggregation, higher-order moment analysis, and regime-switching detection to deliver comprehensive insights into small business economic conditions with statistical confidence intervals and multi-language accessibility.

1. Introduction and Theoretical Foundation

The development of quantitative models for assessing small business economic conditions has gained significant importance in contemporary financial analysis, particularly given the critical role small enterprises play in economic development and employment generation. Small businesses, typically defined as enterprises with fewer than 500 employees according to the U.S. Small Business Administration, constitute approximately 99.9% of all businesses in the United States and employ nearly half of the private workforce (U.S. Small Business Administration, 2024).

The theoretical framework underlying the SBO-SAM model draws extensively from established academic research in small business economics and quantitative finance. The foundational understanding of key drivers affecting small business performance builds upon the seminal work of Dunkelberg and Wade (2023) in their analysis of small business economic trends through the National Federation of Independent Business (NFIB) Small Business Economic Trends survey. Their research established the critical importance of optimism, hiring plans, capital expenditure intentions, and credit availability as primary determinants of small business performance.

The model incorporates insights from Federal Reserve Board research, particularly the Senior Loan Officer Opinion Survey (Federal Reserve Board, 2024), which demonstrates the critical importance of credit market conditions in small business operations. This research consistently shows that small businesses face disproportionate challenges during periods of credit tightening, as they typically lack access to capital markets and rely heavily on bank financing.

The statistical methodology employed in this model follows the econometric principles established by Hamilton (1989) in his work on regime-switching models and time series analysis. Hamilton's framework provides the theoretical foundation for identifying different economic regimes and understanding how economic relationships may vary across different market conditions. The variance-weighted aggregation technique draws from modern portfolio theory as developed by Markowitz (1952) and later refined by Sharpe (1964), applying these concepts to economic indicator construction rather than traditional asset allocation.

Additional theoretical support comes from the work of Engle and Granger (1987) on cointegration analysis, which provides the statistical framework for combining multiple time series while maintaining long-term equilibrium relationships. The model also incorporates insights from behavioral economics research by Kahneman and Tversky (1979) on prospect theory, recognizing that small business decision-making may exhibit systematic biases that affect economic outcomes.

2. Model Architecture and Component Structure

The SBO-SAM model employs eight orthogonalized economic factors that collectively capture the multifaceted nature of small business operating conditions. Each component is normalized using Z-score standardization with a rolling 252-day window, representing approximately one business year of trading data. This approach ensures statistical consistency across different market regimes and economic cycles, following the methodology established by Tsay (2010) in his treatment of financial time series analysis.

2.1 Small Cap Relative Performance Component

The first component measures the performance of the Russell 2000 index relative to the S&P 500, capturing the market-based assessment of small business equity valuations. This component reflects investor sentiment toward smaller enterprises and provides a forward-looking perspective on small business prospects. The theoretical justification for this component stems from the efficient market hypothesis as formulated by Fama (1970), which suggests that stock prices incorporate all available information about future prospects.

The calculation employs a 20-day rate of change with exponential smoothing to reduce noise while preserving signal integrity. The mathematical formulation is:

Small_Cap_Performance = (Russell_2000_t / S&P_500_t) / (Russell_2000_{t-20} / S&P_500_{t-20}) - 1

This relative performance measure eliminates market-wide effects and isolates the specific performance differential between small and large capitalization stocks, providing a pure measure of small business market sentiment.

2.2 Credit Market Conditions Component