Time-Decaying Percentile Oscillator [BackQuant]Time-Decaying Percentile Oscillator

1. Big-picture idea

Traditional percentile or stochastic oscillators treat every bar in the look-back window as equally important. That is fine when markets are slow, but if volatility regime changes quickly yesterday’s print should matter more than last month’s. The Time-Decaying Percentile Oscillator attempts to fix that blind spot by assigning an adjustable weight to every past price before it is ranked. The result is a percentile score that “breathes” with market tempo much faster to flag new extremes yet still smooth enough to ignore random noise.

2. What the script actually does

Build a weight curve

• You pick a look-back length (default 28 bars).

• You decide whether weights fall Linearly , Exponentially , by Power-law or Logarithmically .

• A decay factor (lower = faster fade) shapes how quickly the oldest price loses influence.

• The array is normalised so all weights still sum to 1.

Rank prices by weighted mass

• Every close in the window is paired with its weight.

• The pairs are sorted from low to high.

• The cumulative weight is walked until it equals your chosen percentile level (default 50 = median).

• That price becomes the Time-Decayed Percentile .

Find dispersion with robust statistics

• Instead of a fragile standard deviation the script measures weighted Median-Absolute-Deviation about the new percentile.

• You multiply that deviation by the Deviation Multiplier slider (default 1.0) to get a non-parametric volatility band.

Build an adaptive channel

• Upper band = percentile + (multiplier × deviation)

• Lower band = percentile – (multiplier × deviation)

Normalise into a 0-100 oscillator

• The current close is mapped inside that band:

0 = lower band, 50 = centre, 100 = upper band.

• If the channel squeezes, tiny moves still travel the full scale; if volatility explodes, it automatically widens.

Optional smoothing

• A second-stage moving average (EMA, SMA, DEMA, TEMA, etc.) tames the jitter.

• Length 22 EMA by default—change it to tune reaction speed.

Threshold logic

• Upper Threshold 70 and Lower Threshold 30 separate standard overbought/oversold states.

• Extreme bands 85 and 15 paint background heat when aggressive fade or breakout trades might trigger.

Divergence engine

• Looks back twenty bars.

• Flags Bullish divergence when price makes a lower low but oscillator refuses to confirm (value < 40).

• Flags Bearish divergence when price prints a higher high but oscillator stalls (value > 60).

3. Component walk-through

• Source – Any price series. Close by default, switch to typical price or custom OHLC4 for futures spreads.

• Look-back Period – How many bars to rank. Short = faster, long = slower.

• Base Percentile Level – 50 shows relative position around the median; set to 25 / 75 for quartile tracking or 90 / 10 for extreme tails.

• Deviation Multiplier – Higher values widen the dynamic channel, lowering whipsaw but delaying signals.

• Decay Settings

– Type decides the curve shape. Exponential (default 1.16) mimics EMA logic.

– Factor < 1 shrinks influence faster; > 1 spreads influence flatter.

– Toggle Enable Time Decay off to compare with classic equal-weight stochastic.

• Smoothing Block – Choose one of seven MA flavours plus length.

• Thresholds – Overbought / Oversold / Extreme levels. Push them out when working on very mean-reverting assets like FX; pull them in for trend monsters like crypto.

• Display toggles – Show or hide threshold lines, extreme filler zones, bar colouring, divergence labels.

• Colours – Bullish green, bearish red, neutral grey. Every gradient step is automatically blended to generate a heat map across the 0-100 range.

4. How to read the chart

• Oscillator creeping above 70 = market auctioning near the top of its adaptive range.

• Fast poke above 85 with no follow-through = exhaustion fade candidate.

• Slow grind that lives above 70 for many bars = valid bullish trend, not a fade.

• Cross back through 50 shows balance has shifted; treat it like a micro trend change.

• Divergence arrows add extra confidence when you already see two-bar reversal candles at range extremes.

• Background shading (semi-transparent red / green) warns of extreme states and throttles your position size.

5. Practical trading playbook

Mean-reversion scalps

1. Wait for oscillator to reach your desired OB/ OS levels

2. Check the slope of the smoothing MA—if it is flattening the squeeze is mature.

3. Look for a one- or two-bar reversal pattern.

4. Enter against the move; first target = midline 50, second target = opposite threshold.

5. Stop loss just beyond the extreme band.

Trend continuation pullbacks

1. Identify a clean directional trend on the price chart.

2. During the trend, TDP will oscillate between midline and extreme of that side.

3. Buy dips when oscillator hits OS levels, and the same for OB levels & shorting

4. Exit when oscillator re-tags the same-side extreme or prints divergence.

Volatility regime filter

• Use the Enable Time Decay switch as a regime test.

• If equal-weight oscillator and decayed oscillator diverge widely, market is entering a new volatility regime—tighten stops and trade smaller.

Divergence confirmation for other indicators

• Pair TDP divergence arrows with MACD histogram or RSI to filter false positives.

• The weighted nature means TDP often spots divergence a bar or two earlier than standard RSI.

Swing breakout strategy

1. During consolidation, band width compresses and oscillator oscillates around 50.

2. Watch for sudden expansion where oscillator blasts through extreme bands and stays pinned.

3. Enter with momentum in breakout direction; trail stop behind upper or lower band as it re-expands.

6. Customising decay mathematics

Linear – Each older bar loses the same fixed amount of influence. Intuitive and stable; good for slow swing charts.

Exponential – Influence halves every “decay factor” steps. Mirrors EMA thinking and is fastest to react.

Power-law – Mid-history bars keep more authority than exponential but oldest data still fades. Handy for commodities where seasonality matters.

Logarithmic – The gentlest curve; weight drops sharply at first then levels off. Mimics how traders remember dramatic moves for weeks but forget ordinary noise quickly.

Turn decay off to verify the tool’s added value; most users never switch back.

7. Alert catalogue

• TD Overbought / TD Oversold – Cross of regular thresholds.

• TD Extreme OB / OS – Breach of danger zones.

• TD Bullish / Bearish Divergence – High-probability reversal watch.

• TD Midline Cross – Momentum shift that often precedes a window where trend-following systems perform.

8. Visual hygiene tips

• If you already plot price on a dark background pick Bullish Color and Bearish Color default; change to pastel tones for light themes.

• Hide threshold lines after you memorise the zones to declutter scalping layouts.

• Overlay mode set to false so the oscillator lives in its own panel; keep height about 30 % of screen for best resolution.

9. Final notes

Time-Decaying Percentile Oscillator marries robust statistical ranking, adaptive dispersion and decay-aware weighting into a simple oscillator. It respects both recent order-flow shocks and historical context, offers granular control over responsiveness and ships with divergence and alert plumbing out of the box. Bolt it onto your price action framework, trend-following system or volatility mean-reversion playbook and see how much sooner it recognises genuine extremes compared to legacy oscillators.

Backtest thoroughly, experiment with decay curves on each asset class and remember: in trading, timing beats timidity but patience beats impulse. May this tool help you find that edge.

Cari dalam skrip untuk "25年黄金价格走势预测"

Tradeable Candle Detection By Raja SaienTradeable Candle Detection By Raja Saien

Overview:

This advanced candle detection tool is designed to help traders identify high-quality trade setups and avoid fake moves, based on candle structure, volume, and RSI conditions. Unlike many indicators that are limited to specific sessions, this script works across all market sessions, giving you full flexibility to trade 24/7.

🔍 Key Features:

All Session Support (24/7 Trading)

Detects tradeable setups during any time of the day, including Asian, London, New York, and overlapping hours.

No restriction to any specific session — trade when the opportunity is there!

Fake Move Detection 🚫

Identifies candles with long wicks, small bodies, and low volume — typical signs of manipulation or indecision.

Displays a “No Trade Zone – Fake Move” label to help you avoid poor entries.

Real Move Detection ✅

Highlights candles with strong bodies, short wicks, and high volume — ideal conditions for trade entries.

Helps you focus only on high-probability, momentum-driven moves.

RSI-Based Confirmation

Uses RSI to ensure trade entries align with momentum:

Bullish Entry Allowed: Candle is bullish + RSI between 50–75.

Bearish Entry Allowed: Candle is bearish + RSI between 25–50.

Avoid Trades: RSI is overbought/oversold or showing divergence.

Divergence Detection

Detects bearish divergence in bullish setups and bullish divergence in bearish setups — warns against risky entries.

Visual Zones & Candle Highlights

Plots horizontal lines at candle highs/lows and extended zones based on candle range.

Dominant candles are highlighted in black for quick visual spotting.

⚙️ Custom Inputs:

Minimum Body Size Threshold

Wick-to-Body Ratio for Fake Move

Volume Strength Multiplier

Candle Dominance Precision (% of range)

RSI Period and Source

Optional session filter (can be turned off to enable all-session detection)

🛎️ Alerts Included:

✅ Long Entry Confirmed – Strong bullish candle with supporting RSI

✅ Short Entry Confirmed – Strong bearish candle with supporting RSI

🚫 Fake Move Detected – Weak structure + low volume, no trade

🧠 How to Use:

Wait for a dominant black candle to appear.

Read the label to understand:

✅ Green = Trade Allowed

⚠️ Orange = Avoid (due to RSI or divergence)

🚫 Red = Fake Move (stay out)

Combine with support/resistance, SMC, or price action strategy for confluence.

🟢 "Trade any session, any time – with confidence, precision, and control. Powered by Raja Saien."

Built for traders who value smart entries and reliable signals across all time zones.

ATR % Line from LoD/HoDATR % Line Trading Indicator - Entry Filter Tool

This Pine Script creates a sophisticated ATR (Average True Range) percentage-based entry filter indicator for TradingView that helps traders avoid buying overextended stocks and identify optimal entry zones based on volatility.

Core Functionality - Entry Discipline

The script calculates a maximum entry threshold by taking a percentage of the Average True Range (ATR) and projecting it from the current day's low. This creates a dynamic "no-buy zone" that adapts to market volatility, helping traders avoid purchasing stocks that have already moved too far from their daily base.

Key Calculation:

Measures the ATR over a specified period (default: 14 bars)

Takes a user-defined percentage of that ATR (default: 25%)

Projects this distance from the day's low to establish a maximum entry threshold

Entry Rule: Avoid buying when price exceeds this ATR% level from the daily low or high.

Visual Features

Entry Threshold Line:

Draws a horizontal line at the calculated maximum entry level

Line extends forward for clear visualization of the "no-buy zone"

Red zones above this line indicate overextended conditions

Fully customizable appearance with color, width, and style options

Smart Entry Alerts:

Optional labels show the ATR percentage threshold and exact price level

Visual confirmation when stocks are trading in acceptable entry zones vs. extended areas

Real-Time Monitoring Table:

Displays current distance from daily low as ATR percentage

Shows whether current price is in "safe entry zone" or "extended territory"

Customizable display options for clean chart analysis

Practical Applications for Entry Management

Avoiding Extended Entries:

Primary Use: Don't initiate long positions when price is more than X% ATR from the daily low

Prevents buying stocks that have already made their daily move

Reduces risk of buying at temporary tops within the trading session

Entry Zone Identification:

Price trading below the ATR% line = potential entry opportunity

Price trading above the ATR% line = wait for pullback or skip the trade

Combines volatility analysis with momentum discipline

Risk Management Benefits:

Improved Entry Timing: Enter closer to daily support levels

Better Risk/Reward: Shorter distance to stop loss (daily low)

Reduced Chasing: Systematic approach prevents FOMO-driven entries

Volatility Awareness: Higher volatility stocks get wider acceptable entry ranges

Configuration for Entry Filtering

Key Settings for Entry Management:

ATR Percentage: Set your maximum acceptable extension (15-30% common for day trading)

Reference Point: Use "Low" to measure extension from daily base

Line Style: Make highly visible to clearly see entry threshold

Alert Integration: Visual confirmation of entry-friendly zones

Typical Usage Scenarios:

Conservative Entries: 15-20% ATR from daily low

Moderate Extensions: 25-35% ATR for stronger momentum plays

Aggressive Setups: 40%+ ATR for breakout situations (use with caution)

Entry Strategy Integration

Pre-Market Planning:

Set ATR% threshold based on stock's typical volatility

Identify key levels where entries become unfavorable

Plan alternative entry strategies for extended stocks

Intraday Execution:

Monitor real-time ATR% extension from daily low

Avoid new long positions when threshold is exceeded

Wait for pullbacks to re-enter acceptable entry zones

This tool transforms volatility analysis into practical entry discipline, helping traders maintain consistent entry standards and avoid the costly mistake of chasing overextended stocks. By respecting ATR-based extension limits, traders can improve their entry timing and overall trade profitability.

Dynamic S/R System - Pivot + ChannelDynamic S/R System - Pivot + Channel

A comprehensive Support & Resistance indicator combining dual methodologies for institutional-grade price level analysis

📊 CORE FEATURES

Dual Detection System

• Pivot-Based Levels - Historical turning points with intelligent touch counting

• Dynamic Channel S/R - Trend-aware linear regression boundaries

• Smart Level Management - Auto-merges similar levels, removes weak/outdated ones

Volume Integration

• Multi-timeframe volume analysis using EMA oscillator and spike detection

• Volume confirmation for all breakout signals to filter false moves

• Real-time volume status (Normal/High/Spike) in live information panel

Intelligent Touch Counting

• Automatic level validation through touch frequency analysis

• Strength classification with visual differentiation (colors/thickness)

• Level labels showing exact touch count (S3, R5, etc.)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎨 VISUAL ELEMENTS

Line System

Solid Lines: Pivot-based S/R levels

Dashed Lines: Dynamic channel boundaries

Color Coding:

• 🔵 Blue/🔴 Red: Standard support/resistance

• 🟠 Orange: Strong levels (multiple touches)

• 🟣 Purple: Channel S/R levels

Signal Labels

• "B" - Pivot S/R breakout with volume confirmation

• "CB" - Channel boundary breakout

• "Bull/Bear Wick" - False breakout detection (wick rejections)

Information Panel

Real-time analysis displays:

• Total resistance/support levels detected

• Closest S/R levels to current price

• Volume status and position relative to levels

• Current market position assessment

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

✅ KEY ADVANTAGES

Multi-Method Validation

Combines historical pivot analysis with dynamic trend channels for comprehensive market view

False Breakout Protection

• Volume confirmation requirements

• Wick analysis to identify failed attempts

• Multiple validation criteria before signal generation

Adaptive Level Management

• Automatically updates as new pivots form

• Removes outdated/weak levels

• Maintains clean, relevant level display

Institutional-Grade Analysis

• Touch counting reveals institutional respect levels

• Volume integration shows smart money activity

• Strength classification identifies high-probability zones

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⏰ OPTIMAL USE CASES

Best Timeframes

• Daily - Primary recommendation for swing trading

• 4-Hour - Intraday analysis and entries

• Weekly - Long-term position planning

Ideal Markets

• Crypto pairs (especially ETH/BTC, BTC/USD)

• Forex majors with good volume data

• Large-cap stocks with institutional participation

Trading Applications

• Entry/exit planning around key S/R levels

• Breakout confirmation with volume validation

• Risk management using nearest S/R for stops

• Trend analysis through channel dynamics

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

⚙️ CONFIGURATION GUIDELINES

Conservative Setup (Higher Confidence)

Min Pivot Strength: 3-4

Volume Threshold: 25-30%

Max Levels: 6-8

Aggressive Setup (More Signals)

Min Pivot Strength: 2

Volume Threshold: 15-20%

Max Levels: 10-12

🔔 ALERT SYSTEM

Breakout Alerts

• Resistance/Support breaks with volume confirmation

• Channel boundary violations

• Approaching strong S/R levels

Advanced Notifications

• Strong level approaches (within 0.5% of price)

• False breakout detection

• Volume spike confirmations

📈 TRADING STRATEGY GUIDE

Entry Strategy

1. Wait for price to approach identified S/R level

2. Confirm with volume analysis (spike/high volume preferred)

3. Watch for wick formations indicating rejection

4. Enter on confirmed breakout with volume or bounce with rejection

Risk Management

• Use nearest S/R level for stop placement

• Scale position size based on level strength (touch count)

• Monitor volume confirmation for exit signals

Market Context

• Combine with higher timeframe trend analysis

• Consider overall market sentiment and volatility

• Use channel direction for bias confirmation

Transform complex S/R analysis into actionable trading intelligence with institutional-level insights for professional trading decisions.

Momentum DivergenceOverview

The Momentum Divergence Oscillator is a valuable tool designed for traders who are familiar with basic charting but want to deepen their market insights. This indicator combines a momentum calculation with divergence detection, presenting the data in an intuitive way with a blue momentum line and colored divergence signals ("Bull" and "Bear"). It’s perfect for refining entry and exit points across various timeframes, especially for scalping or swing trading strategies.

Understanding the Concepts

What is Momentum?

Momentum measures the speed and strength of a price movement by comparing the current closing price to a previous close over a set period. In this indicator, it’s calculated as the difference between the current close and the close from a user-defined number of bars ago (default: 10). A rising momentum line indicates accelerating upward momentum, while a falling line suggests slowing momentum or a potential reversal. This helps you gauge whether a trend is gaining power or losing steam, making it a key indicator for spotting overbought or oversold conditions.

What is a Divergence?

A divergence occurs when the price action and the momentum indicator move in opposite directions, often signaling a potential trend reversal. The Momentum Divergence Oscillator highlights two types:

Bullish Divergence: When the price forms a lower low (indicating weakness), but the momentum shows a higher low (suggesting underlying strength). This can foreshadow an upward reversal.

Bearish Divergence: When the price reaches a higher high (showing strength), but the momentum records a lower high (indicating fading momentum). This may hint at an impending downward turn.

How the Indicator Works

The indicator plots a momentum line in a separate pane below your chart, giving you a clear view of price momentum over time. It also scans for divergences using adjustable lookback periods (default: 5 bars left and right) and a range window (default: 5-60 bars) to ensure relevance. When a divergence is detected, it’s visually highlighted, and you can customize the sensitivity through input settings like the momentum length and pivot lookback. Alerts are included to notify you of new divergence signals in real-time, saving you from constant monitoring.

How to Apply It

Identifying Opportunities: Use bullish divergences ("Bull") as a cue to consider long positions, especially when confirmed by support levels or a moving average crossover. Bearish divergences ("Bear") can signal short opportunities, particularly near resistance zones.

Combining with Other Tools: Pair this oscillator with indicators like the Relative Strength Index (RSI) or volume analysis to filter out false signals and increase confidence in your trades. For example, a bullish divergence with rising volume can be a stronger buy signal.

Timeframe Flexibility: Test it on shorter timeframes (e.g., 5-minute charts) for quick scalping trades or longer ones (e.g., 1-hour or 4-hour charts) for swing trading, adjusting the momentum length to suit the market’s pace.

Alert Setup: Enable the built-in alerts to get notified when a divergence forms, allowing you to react promptly without staring at the screen all day.

Strategy Example

Spot a bullish divergence on a 15-minute chart where the price hits a lower low, but the momentum rises.

Confirm with a break above a 20-period EMA and increasing volume.

Enter a long position with a stop-loss below the recent low and a take-profit near the next resistance level.

Customization Tips

Adjust the "Momentum Length" (default: 10) to make the oscillator more or less sensitive—shorter lengths react faster, while longer ones smooth out noise.

Tweak the "Pivot Lookback" settings to widen or narrow the divergence detection range based on your trading style.

Use the "Range Upper/Lower" inputs to focus on divergences within a specific timeframe that matches your strategy.

Important Considerations

b]This indicator is a technical analysis tool, not a guaranteed trading system. Always pair it with a solid strategy and strict risk management, such as setting stop-losses.

In strong trending markets, divergences can sometimes produce false signals. Consider adding a trend filter (e.g., ADX below 25) to avoid whipsaws.

Experiment with the settings on a demo account or backtest to find what works best for your preferred markets and timeframes.

JHW Volume Based Buy and Sell MomentumThe JHW Volume-Based Buy and Sell Momentum indicator is a custom momentum oscillator designed to capture market sentiment based on volume dynamics and price rate of change (ROC). It aims to identify bullish or bearish momentum by analyzing how price reacts to increasing or decreasing trading volume.

Core Logic:

The indicator calculates the Rate of Change (ROC) of the closing price.

It then accumulates this ROC separately based on whether the current volume is lower or higher than the previous bar:

If volume decreases, the ROC is added to a "negative volume index" accumulator.

If volume increases, the ROC is added to a "positive volume index" accumulator.

These two accumulators are combined to form a net momentum line.

Smoothing:

A Simple Moving Average (SMA) is applied to both accumulators over a user-defined period (default: 25 bars).

The sum of these smoothed values forms the signal line.

Visualization:

The indicator plots:

The net momentum line (yellow).

The smoothed signal line (blue).

The area between the two lines is filled with color:

Yellow when momentum is above the signal (bullish).

Blue when momentum is below the signal (bearish).

Bar colors are also adjusted to reflect the current momentum state.

Use Case:

This indicator helps traders:

Detect volume-driven momentum shifts.

Identify potential buy or sell zones based on volume behavior.

Confirm trends or spot early reversals.

Supertrend with ADX & MTF MA Filter# **Supertrend with ADX & MTF MA Filter - Comprehensive Explanation**

---

## **1. Purpose of This Indicator**

This indicator combines three powerful technical analysis tools to create a robust trading system:

✅ **Supertrend** (Trend-following)

✅ **ADX Filter** (Trend strength confirmation)

✅ **MTF MA Filter** (Multi-timeframe trend direction confirmation)

**Primary Goals:**

✔ **Identify high-probability trend reversals** with confirmation from multiple indicators

✔ **Filter out weak trends** using ADX (Average Directional Index)

✔ **Add higher timeframe context** with MTF (Multi-TimeFrame) Moving Average

✔ **Reduce false signals** by requiring confluence between all three components

---

## **2. Core Logic & Components**

### **A. Supertrend (Base Indicator)**

- **Calculation:**

```pine

up = hl2 - (Multiplier * ATR(Periods))

dn = hl2 + (Multiplier * ATR(Periods))

```

- **Bullish trend** when price > `up` (green line)

- **Bearish trend** when price < `dn` (red line)

- **Why Supertrend?**

- Simple yet effective trend-following system

- Adapts to volatility via ATR (Average True Range)

---

### **B. ADX Filter (Trend Strength Confirmation)**

- **ADX Calculation:**

```pine

= calcADX(adxLength, adxSmoothing)

strongTrend = adxVal >= adxThreshold

```

- **ADX > Threshold (Default: 20)** = Strong trend

- **DI+ > DI-** = Bullish momentum

- **DI- > DI+** = Bearish momentum

- **Why ADX?**

- Avoids trading in choppy markets (low ADX = weak trend)

- Confirms if Supertrend signals occur in a strong trend

---

### **C. MTF MA Filter (Higher Timeframe Trend Alignment)**

- **Moving Average Calculation:**

```pine

= getMA(maSource, maLength, maType, maTF)

```

- **MA Type:** SMA, EMA, WMA, or DEMA

- **Timeframe:** Any (1m, 5m, 1H, 4H, D, W, M)

- **Trend Direction:**

- **Buy Signal:** MA must be **rising**

- **Sell Signal:** MA must be **falling**

- **Why MTF MA?**

- Aligns trades with the **higher timeframe trend**

- Reduces counter-trend entries

---

## **3. How to Use This Indicator**

### **A. Buy Conditions (All Must Be True)**

1. **Supertrend turns bullish** (price crosses above `up` line)

2. **ADX ≥ Threshold** (trend is strong)

3. **Higher timeframe MA is rising** (confirms bullish bias)

### **B. Sell Conditions (All Must Be True)**

1. **Supertrend turns bearish** (price crosses below `dn` line)

2. **ADX ≥ Threshold** (trend is strong)

3. **Higher timeframe MA is falling** (confirms bearish bias)

### **C. Recommended Settings**

| Parameter | Recommended Value | Description |

|-----------|------------------|-------------|

| **ATR Period** | 14 | Sensitivity of Supertrend |

| **Multiplier** | 1.5-3.0 | Adjust for volatility |

| **ADX Threshold** | 20-25 | Higher = stricter trend filter |

| **MA Length** | 20-50 | Smoothness of trend filter |

| **MA Timeframe** | 1H/D | Align with trading style |

---

## **4. Trading Strategies**

### **A. Trend-Following Strategy**

- **Enter:** When all 3 conditions align (Supertrend + ADX + MA)

- **Exit:** When Supertrend flips or ADX drops below threshold

### **B. Pullback Strategy**

- **Wait for:**

- Supertrend in trend direction

- ADX remains strong

- MA still aligned

- **Enter:** On pullback to Supertrend line

### **C. Multi-Timeframe Confirmation**

- **Intraday traders:** Use 4H/D MA for trend bias

- **Swing traders:** Use D/W MA for trend bias

---

## **5. Advantages Over Standard Supertrend**

✔ **Fewer false signals** (ADX filters weak trends)

✔ **Higher timeframe alignment** (avoids trading against larger trends)

✔ **Customizable MA types** (SMA, EMA, WMA, DEMA)

✔ **Works on all markets** (stocks, forex, crypto)

---

### **Final Thoughts**

This indicator is designed for traders who want **high-confidence trend signals** by combining:

🔹 **Supertrend** (entry trigger)

🔹 **ADX** (trend strength filter)

🔹 **MTF MA** (higher timeframe trend alignment)

By requiring all three components to align, it significantly improves signal quality compared to standalone Supertrend systems.

**→ Best for:** Swing trading, trend-following, and avoiding choppy markets.

Reversal Point Dynamics⇋ Reversal Point Dynamics (RPD)

This is not an indicator; it is a complete system for deconstructing the mechanics of a market reversal. Reversal Point Dynamics (RPD) moves far beyond simplistic pattern recognition, venturing into a deep analysis of the underlying forces that cause trends to exhaust, pause, and turn. It is engineered from the ground up to identify high-probability reversal points by quantifying the confluence of market dynamics in real-time.

Where other tools provide a static signal, RPD delivers a dynamic probability. It understands that a true market turning point is not a single event, but a cascade of failing momentum, structural breakdown, and a shift in market order. RPD's core engine meticulously analyzes each of these dynamic components—the market's underlying state, its velocity and acceleration, its degree of chaos (entropy), and its structural framework. These forces are synthesized into a single, unified Probability Score, offering you an unprecedented, transparent view into the conviction behind every potential reversal.

This is not a "black box" system. It is an open-architecture engine designed to empower the discerning trader. Featuring real-time signal projection, an integrated Fibonacci R2R Target Engine, and a comprehensive dashboard that acts as your Dynamics Control Center , RPD gives you a complete, holistic view of the market's state.

The Theoretical Core: Deconstructing Market Dynamics

RPD's analytical power is born from the intelligent synthesis of multiple, distinct theoretical models. Each pillar of the engine analyzes a different facet of market behavior. The convergence of these analyses—the "Singularity" event referenced in the dashboard—is what generates the final, high-conviction probability score.

1. Pillar One: Quantum State Analysis (QSA)

This is the foundational analysis of the market's current state within its recent context. Instead of treating price as a random walk, QSA quantizes it into a finite number of discrete "states."

Formulaic Concept: The engine establishes a price range using the highest high and lowest low over the Adaptive Analysis Period. This range is then divided into a user-defined number of Analysis Levels. The current price is mapped to one of these states (e.g., in a 9-level system, State 0 is the absolute low, and State 8 is the absolute high).

Analytical Edge: This acts as a powerful foundational filter. The engine will only begin searching for reversal signals when the market has reached a statistically stretched, extreme state (e.g., State 0 or 8). The Edge Sensitivity input allows you to control exactly how close to this extreme edge the price must be, ensuring you are trading from points of maximum potential exhaustion.

2. Pillar Two: Price State Roc (PSR) - The Dynamics of Momentum

This pillar analyzes the kinetic forces of the market: its velocity and acceleration. It understands that it’s not just where the price is, but how it got there that matters.

Formulaic Concept: The psr function calculates two derivatives of price.

Velocity: (price - price ). This measures the speed and direction of the current move.

Acceleration: (velocity - velocity ). This measures the rate of change in that speed. A negative acceleration (deceleration) during a strong rally is a critical pre-reversal warning, indicating momentum is fading even as price may be pushing higher.

Analytical Edge: The engine specifically hunts for exhaustion patterns where momentum is clearly decelerating as price reaches an extreme state. This is the mechanical signature of a weakening trend.

3. Pillar Three: Market Entropy Analysis - The Dynamics of Order & Chaos

This is RPD's chaos filter, a concept borrowed from information theory. Entropy measures the degree of randomness or disorder in the market's price action.

Formulaic Concept: The calculateEntropy function analyzes recent price changes. A market moving directionally and smoothly has low entropy (high order). A market chopping back and forth without direction has high entropy (high chaos). The value is normalized between 0 and 1.

Analytical Edge: The most reliable trades occur in low-entropy, ordered environments. RPD uses the Entropy Threshold to disqualify signals that attempt to form in chaotic, unpredictable conditions, providing a powerful shield against whipsaw markets.

4. Pillar Four: The Synthesis Engine & Probability Calculation

This is where all the dynamic forces converge. The final probability score is a weighted calculation that heavily rewards confluence.

Formulaic Concept: The calculateProbability function intelligently assembles the final score:

A Base Score is established from trend strength and entropy.

An Entropy Score adds points for low entropy (order) and subtracts for high entropy (chaos).

A significant Divergence Bonus is awarded for a classic momentum divergence.

RSI & Volume Bonuses are added if momentum oscillators are in extreme territory or a volume spike confirms institutional interest.

MTF & Adaptive Bonuses add further weight for alignment with higher timeframe structure.

Analytical Edge: A signal backed by multiple dynamic forces (e.g., extreme state + decelerating momentum + low entropy + volume spike) will receive an exponentially higher probability score. This is the very essence of analyzing reversal point dynamics.

The Command Center: Mastering the Inputs

Every input is a precise lever of control, allowing you to fine-tune the RPD engine to your exact trading style, market, and timeframe.

🧠 Core Algorithm

Predictive Mode (Early Detection):

What It Is: Enables the engine to search for potential reversals on the current, unclosed bar.

How It Works: Analyzes intra-bar acceleration and state to identify developing exhaustion. These signals are marked with a ' ? ' and are tentative.

How To Use It: Enable for scalping or very aggressive day trading to get the earliest possible indication. Disable for swing trading or a more conservative approach that waits for full bar confirmation.

Live Signal Mode (Current Bar):

What It Is: A highly aggressive mode that plots tentative signals with a ' ! ' on the live bar based on projected price and momentum. These signals repaint intra-bar.

How It Works: Uses a linear regression projection of the close to anticipate a reversal.

How To Use It: For advanced users who use intra-bar dynamics for execution and understand the nature of repainting signals.

Adaptive Analysis Period:

What It Is: The main lookback period for the QSA, PSR, and Entropy calculations. This is the engine's "memory."

How It Works: A shorter period makes the engine highly sensitive to local price swings. A longer period makes it focus only on major, significant market structure.

How To Use It: Scalping (1-5m): 15-25. Day Trading (15m-1H): 25-40. Swing Trading (4H+): 40-60.

Fractal Strength (Bars):

What It Is: Defines the strength of the pivot detection used for confirming reversal events.

How It Works: A value of '2' requires a candle's high/low to be more extreme than the two bars to its left and right.

How To Use It: '2' is a robust standard. Increase to '3' for an even stricter definition of a structural pivot, which will result in fewer signals.

MTF Multiplier:

What It Is: Integrates pivot data from a higher timeframe for confluence.

How It Works: A multiplier of '4' on a 15-minute chart will pull pivot data from the 1-hour chart (15 * 4 = 60m).

How To Use It: Set to a multiple that corresponds to your preferred higher timeframe for contextual analysis.

🎯 Signal Settings

Min Probability %:

What It Is: Your master quality filter. A signal is only plotted if its score exceeds this threshold.

How It Works: Directly filters the output of the final probability calculation.

How To Use It: High-Quality (80-95): For A+ setups only. Balanced (65-75): For day trading. Aggressive (50-60): For scalping.

Min Signal Distance (Bars):

What It Is: A noise filter that prevents signals from clustering in choppy conditions.

How It Works: Enforces a "cooldown" period of N bars after a signal.

How To Use It: Increase in ranging markets to focus on major swings. Decrease on lower timeframes.

Entropy Threshold:

What It Is: Your "chaos shield." Sets the maximum allowable market randomness for a signal.

How It Works: If calculated entropy is above this value, the signal is invalidated.

How To Use It: Lower values (0.1-0.5): Extremely strict. Higher values (0.7-1.0): More lenient. 0.85 is a good balance.

Adaptive Entropy & Aggressive Mode:

What It Is: Toggles for dynamically adjusting the engine's core parameters.

How It Works: Adaptive Entropy can slightly lower the required probability in strong trends. Aggressive Mode uses more lenient settings across the board.

How To Use It: Keep Adaptive on. Use Aggressive Mode sparingly, primarily for scalping highly volatile assets.

📊 State Analysis

Analysis Levels:

What It Is: The number of discrete "states" for the QSA.

How It Works: More levels create a finer-grained analysis of price location.

How To Use It: 6-7 levels are ideal. Increasing to 9 can provide more precision on very volatile assets.

Edge Sensitivity:

What It Is: Defines how close to the absolute top/bottom of the range price must be.

How It Works: '0' means price must be in the absolute highest/lowest state. '3' allows a signal within the top/bottom 3 states.

How To Use It: '3' provides a good balance. Lower it to '1' or '0' if you only want to trade extreme exhaustion.

The Dashboard: Your Dynamics Control Center

The dashboard provides a transparent, real-time view into the engine's brain. Use it to understand the context behind every signal and to gauge the current market environment at a glance.

🎯 UNIFIED PROB SCORE

TOTAL SCORE: The highest probability score (either Peak or Valley) the engine is currently calculating. This is your main at-a-glance conviction metric. The "Singularity" header refers to the event where market dynamics align—the event RPD is built to detect.

Quality: A human-readable interpretation of the Total Score. "EXCEPTIONAL" (🌟) is a rare, A+ confluence event. "STRONG" (💪) is a high-quality, tradable setup.

📊 ORDER FLOW & COMPONENT ANALYSIS

Volume Spike: Shows if the current volume is significantly higher than average (YES/NO). A 'YES' adds major confirmation.

Peak/Valley Conf: This breaks down the probability score into its directional components, showing you the separate confidence levels for a potential top (Peak) versus a bottom (Valley).

🌌 MARKET STRUCTURE

HTF Trend: Shows the direction of the underlying trend based on a Supertrend calculation.

Entropy: The current market chaos reading. "🔥 LOW" is an ideal, ordered state for trading. "😴 HIGH" is a warning of choppy, unpredictable conditions.

🔮 FIB & R2R ZONE (Large Dashboard)

This section gives you the status of the Fibonacci Target Engine. It shows if an Active Channel (entry zone) or Stop Zone (invalidation zone) is active and displays the precise price levels for the static entry, target, and stop calculated at the time of the signal.

🛡️ FILTERS & PREDICTIVES (Large Dashboard)

This panel provides a status check on all the bonus filters. It shows the current RSI Status, whether a Divergence is present, and if a Live Pending signal is forming.

The Visual Interface: A Symphony of Data

Every visual element is designed for instant, intuitive interpretation of market dynamics.

Signal Markers: These are the primary outputs of the engine.

▼/▲ b: A fully confirmed signal that has passed all filters.

? b: A tentative signal generated in Predictive Mode, indicating developing dynamics.

◈ b: This diamond icon replaces the standard triangle when the signal is confirmed by a strong momentum divergence, highlighting it as a superior setup where dynamics are misaligned with price.

Harmonic Wave: The flowing, colored wave around the price.

What It Represents: The market's "flow dynamic" and volatility.

How to Interpret It: Expanding waves show increasing volatility. The color is tied to the "Quantum Color" in your theme, representing the underlying energy field of the market.

Entropy Particles: The small dots appearing above/below price.

What They Represent: A direct visualization of the "order dynamic."

How to Interpret Them: Their presence signifies a low-entropy, ordered state ideal for trading. Their color indicates the direction of momentum (PSR velocity). Their absence means the market is too chaotic (high entropy).

The Fibonacci Target Engine: The dynamic R2R system appearing post-signal.

Static Fib Levels: Colored horizontal lines representing the market's "structural dynamic."

The Green "Active Channel" Box: Your zone of consideration. An area to manage a potential entry.

Development Philosophy

Reversal Point Dynamics was engineered to answer a fundamental question: can we objectively measure the forces behind a market turn? It is a synthesis of concepts from market microstructure, statistics, and information theory. The objective was never to create a "perfect" system, but to build a robust decision-support tool that provides a measurable, statistical edge by focusing on the principle of confluence.

By demanding that multiple, independent market dynamics align simultaneously, RPD filters out the vast majority of market noise. It is designed for the trader who thinks in terms of probability and risk management, not in terms of certainties. It is a tool to help you discount the obvious and bet on the unexpected alignment of market forces.

"Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected."

— George Soros

Trade with insight. Trade with anticipation.

— Dskyz, for DAFE Trading Systems

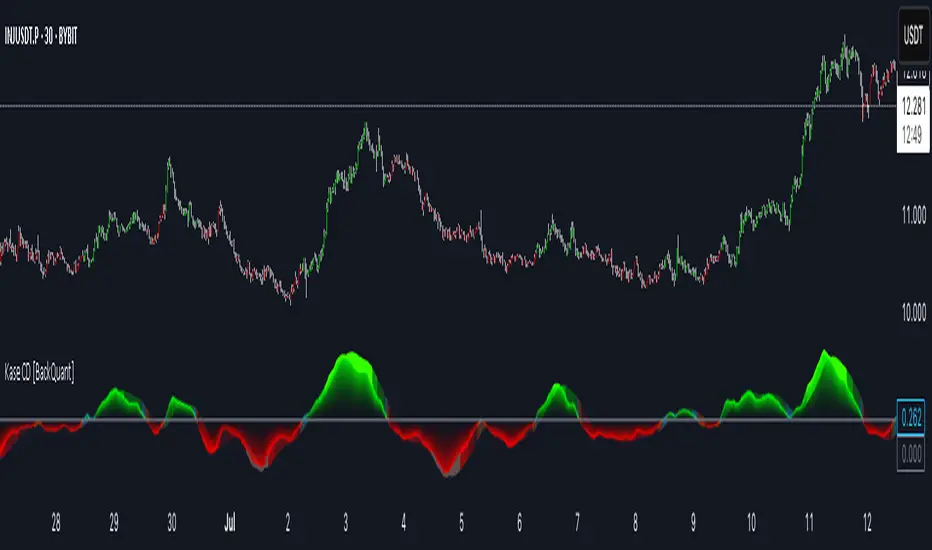

Kase Convergence Divergence [BackQuant]Kase Convergence Divergence

The Kase Convergence Divergence is a sophisticated oscillator designed to measure directional market strength through the lens of volatility-adjusted log return structures. Inspired by Cynthia Kase’s work on statistical momentum and price projection ranges, this unique indicator offers a hybrid framework that merges signal processing, multi-length sweep logic, and adaptive smoothing techniques.

Unlike traditional momentum oscillators like MACD or RSI, which rely on static moving average differences, KCD introduces a dual-process system combining:

Kase-style statistical range projection (via log returns and volatility),

A sweeping loop of lookback lengths for robustness,

First and second derivative modes to capture both velocity and acceleration of price movement.

Core Logic & Computation

The KCD calculation is centered on two volatility-normalized transforms:

KSDI Up: Measures how far the current high has moved relative to a past low, normalized by return volatility.

KSDI Down: Measures how far the current low has moved relative to a past high, also normalized.

For every length in a user-defined sweep range (e.g., 25–35), both KSDI_up and KSDI_dn are computed, and their maximum values across the loop are retained. The difference between these two max values produces the raw signal:

KPO (Kase Projection Oscillator): Measures directional skew.

KCD (Kase Convergence Divergence): Defined as KPO – MA(KPO) — similar in spirit to MACD but structurally different.

Users can choose to visualize either the first derivative (KPO) , or the second derivative (KCD) , depending on market conditions or strategy style.

Key Features

✅ Multi-Length Sweep Logic: Improves signal reliability by aggregating statistical range projections across a set of lookbacks.

✅ Advanced Smoothing Modes: Supports DEMA, HMA, TEMA, LINREG, WMA and more for dynamic adaptation.

✅ Dual Derivative Modes: Choose between speed (first derivative) or smoothness (second derivative) to fit your trading regime.

✅ Color-Encoded Signal Bands: Heatmap-style oscillator coloring enhances visual feedback on trend strength.

✅ Candlestick Painting: Optional bar coloring makes it easy to spot trend shifts on the main chart.

✅ Adaptive Fill Zones: Green and red fills between the oscillator and zero line help distinguish bullish and bearish regimes at a glance.

Practical Applications

📈 Trend Confirmation: Use KCD as a secondary confirmation layer after breakout or pullback entries.

📉 Momentum Shifts: Crossover and crossunder of the zero line highlight potential regime changes.

📊 Strategy Filters: Incorporate into algos to avoid trendless or mean-reverting environments.

🧪 Derivative Switching: Flip between KPO and KCD modes depending on whether you want to measure acceleration or deceleration of price flow.

Alerts & Signals

Two built-in alerts help you catch regime shifts in real time:

Long Signal: Triggered when the selected oscillator crosses above zero.

Short Signal: Triggered when it crosses below zero.

These events can be used to generate entries, exits, or trend validation cues in multi-layer systems.

Conclusion

The Kase Convergence Divergence goes beyond traditional oscillators by offering a volatility-normalized, derivative-aware signal engine with enhanced visual dynamics. Its sweeping architecture and dynamic fill logic make it especially powerful for identifying trending environments, filtering chop, and adding statistical rigor to your trading toolkit.

Whether you’re a discretionary trader seeking precision, or a quant looking to model more robust return structures, KCD offers a creative yet analytically grounded solution.

Pattern Detector [theUltimator5]🎯 Overview

The Pattern Detector is a comprehensive technical analysis indicator that automatically identifies and visualizes multiple pattern types on your charts. Built with advanced ZigZag technology and sophisticated pattern recognition algorithms, this tool helps traders spot high-probability trading opportunities across all timeframes and markets.

✨ Key Features

🔍 Multi-Pattern Detection System

Harmonic Patterns: Butterfly, Gartley, Bat, and Crab patterns with precise Fibonacci ratios

Classic Reversal Patterns: Head & Shoulders and Inverse Head & Shoulders

Double Patterns: Double Tops and Double Bottoms with extreme validation

Wedge Patterns: Rising and Falling Wedges with volume confirmation

📊 Advanced ZigZag Engine

Customizable sensitivity (5-50 levels)

Depth multiplier for multi-timeframe analysis

Real-time pivot detection with noise filtering

Option to display ZigZag lines only for pure price action analysis

🎨 Visualization

Clean pattern lines with distinct color coding

Point labeling system (X, A, B, C, D for harmonics / LS, H, RS for H&S)

Pattern name displays with bullish/bearish direction

Price target projections with arrow indicators

Subtle pattern fills for enhanced visibility

🛠️ Settings & Configuration

Core ZigZag Settings

ZigZag Sensitivity (5-50): Controls pattern detection sensitivity. Lower values detect more patterns but may include noise. Higher values focus on major swings only.

ZigZag Depth Multiplier (1-5): Multiplies sensitivity for deeper analysis. Level 1 = most responsive, Level 5 = major swings only.

Pattern Detection Toggles

Show ZigZag Lines Only: Displays pure ZigZag without pattern detection for price structure analysis

Detect Harmonic Patterns: Enable/disable Fibonacci-based harmonic pattern detection

Detect Head & Shoulders: Toggle classic reversal pattern identification

Detect Double Tops/Bottoms: Enable double pattern detection with extreme validation

Detect Wedge Patterns: Toggle wedge pattern detection with volume confirmation

Display Options

Show Pattern Names: Display pattern names directly on chart (e.g., "Butterfly (Bullish)")

Show Point Labels: Add lettered labels at key pattern points for structure identification

Project Harmonic Targets: Show projected completion points for incomplete harmonic patterns

📈 Pattern Types Explained

Harmonic Patterns 🦋

Advanced Fibonacci-based patterns that provide high-probability reversal signals:

Butterfly: AB=0.786 XA, BC=0.382-0.886 AB, CD=1.618-2.24 BC

Gartley: AB=0.618 XA, BC=0.382-0.886 AB, CD=1.272-1.618 BC

Bat: AB=0.382-0.50 XA, BC=0.382-0.886 AB, CD=1.618-2.24 BC

Crab: AB=0.382-0.618 XA, BC=0.382-0.886 AB, CD=2.24-3.618 BC

Head & Shoulders 👤

Classic three-peak reversal pattern indicating trend exhaustion:

Standard H&S: Bearish reversal at tops

Inverse H&S: Bullish reversal at bottoms

Automatic neckline validation and price target calculation

Double Patterns 📊

Powerful reversal patterns with extreme validation:

Double Top: Two similar highs with valley between (bearish)

Double Bottom: Two similar lows with peak between (bullish)

Includes lookback period validation to ensure patterns are significant extremes

Wedge Patterns 📐

Continuation/reversal patterns with converging trend lines:

Rising Wedge: Converging upward slopes (typically bearish)

Falling Wedge: Converging downward slopes (typically bullish)

Volume confirmation required for increased accuracy

🎯 Trading Applications

Entry Signals

Harmonic Patterns: Enter at point D completion with targets at point A

H&S Patterns: Enter on neckline break with calculated targets

Double Patterns: Enter on support/resistance break with measured moves

Wedge Patterns: Enter on breakout direction with volume confirmation

Risk Management

Use pattern structure for logical stop placement

Pattern invalidation levels provide clear exit rules

Multiple pattern confirmation increases probability

Multi-Timeframe Analysis

Higher ZigZag depth for longer-term patterns

Lower sensitivity for short-term trading patterns

Combine with other timeframes for confluence

⚙️ Optimal Settings

For Day Trading (1m-15m charts)

ZigZag Sensitivity: 5-9

Depth Multiplier: 1-2

Enable all pattern types for maximum opportunities

For Swing Trading (1H-4H charts)

ZigZag Sensitivity: 9-15

Depth Multiplier: 2-3

Focus on harmonic and H&S patterns

For Position Trading (Daily+ charts)

ZigZag Sensitivity: 15-25

Depth Multiplier: 3-5

Emphasize major harmonic and double patterns

🔧 Technical Specifications

Maximum Lookback: 5000 bars for comprehensive analysis

Pattern Overlap Prevention: Intelligent filtering prevents duplicate patterns

Performance Optimized: Efficient algorithms for real-time detection

Volume Integration: Advanced volume analysis for wedge confirmation

Fibonacci Precision: 10% tolerance for harmonic ratio validation

📚 How to Use

Add to Chart: Apply indicator to any timeframe/market

Configure Settings: Adjust sensitivity based on trading style

Enable Patterns: Toggle desired pattern types

Analyze Results: Look for completed patterns with clear structure

Plan Trades: Use price targets and pattern invalidation for trade management

Perfect for both novice and experienced traders seeking systematic pattern recognition with visualization and entry/exit signals.

Risk Distribution HistogramStatistical risk visualization and analysis tool for any ticker 📊

The Risk Distribution Histogram visualizes the statistical distribution of different risk metrics for any financial instrument. It converts risk data into histograms with quartile-based color coding, so that traders can understand their risk, tail-risks, exposure patterns and make data-driven decisions based on empirical evidence rather than assumptions.

The indicator supports multiple risk calculation methods, each designed for different aspects of market analysis, from general volatility assessment to tail risk analysis.

Risk Measurement Methods

Standard Deviation

Captures raw daily price volatility by measuring the dispersion of price movements. Ideal for understanding overall market conditions and timing volatility-based strategies.

Use case: Options trading and volatility analysis.

Average True Range (ATR)

Measures true range as a percentage of price, accounting for gaps and limit moves. Valuable for position sizing across different price levels.

Use case: Position sizing and stop-loss placement.

The chart above illustrates how ATR statistical distribution can be used by looking at the ATR % of price distribution. For example, 90% of the movements are below 5%.

Downside Deviation

Only considers negative price movements, making it ideal for checking downside risk and capital protection rather than capturing upside volatility.

Use case: Downside protection strategies and stop losses.

Drawdown Analysis

Tracks peak-to-trough declines, providing insight into maximum loss potential during different market conditions.

Use case: Risk management and capital preservation.

The chart above illustrates tale risk for the asset (TQQQ), showing that it is possible to have drawdowns higher than 20%.

Entropy-Based Risk (EVaR)

Uses information theory to quantify market uncertainty. Higher entropy values indicate more unpredictable price action, valuable for detecting regime changes.

Use case: Advanced risk modeling and tail-risk.

VIX Histogram

Incorporates the market's fear index directly into analysis, showing how current volatility expectations compare to historical patterns. The CAPITALCOM:VIX histogram is independent from the ticker on the chart.

Use case: Volatility trading and market timing.

Visual Features

The histogram uses quartile-based color coding that immediately shows where current risk levels stand relative to historical patterns:

Green (Q1): Low Risk (0-25th percentile)

Yellow (Q2): Medium-Low Risk (25-50th percentile)

Orange (Q3): Medium-High Risk (50-75th percentile)

Red (Q4): High Risk (75-100th percentile)

The data table provides detailed statistics, including:

Count Distribution: Historical observations in each bin

PMF: Percentage probability for each risk level

CDF: Cumulative probability up to each level

Current Risk Marker: Shows your current position in the distribution

Trading Applications

When current risk falls into upper quartiles (Q3 or Q4), it signals conditions are riskier than 50-75% of historical observations. This guides position sizing and portfolio adjustments.

Key applications:

Position sizing based on empirical risk distributions

Monitoring risk regime changes over time

Comparing risk patterns across timeframes

Risk distribution analysis improves trade timing by identifying when market conditions favor specific strategies.

Enter positions during low-risk periods (Q1)

Reduce exposure in high-risk periods (Q4)

Use percentile rankings for dynamic stop-loss placement

Time volatility strategies using distribution patterns

Detect regime shifts through distribution changes

Compare current conditions to historical benchmarks

Identify outlier events in tail regions

Validate quantitative models with empirical data

Configuration Options

Data Collection

Lookback Period: Control amount of historical data analyzed

Date Range Filtering: Focus on specific market periods

Sample Size Validation: Automatic reliability warnings

Histogram Customization

Bin Count: 10-50 bins for different detail levels

Auto/Manual Bin Width: Optimize for your data range

Visual Preferences: Custom colors and font sizes

Implementation Guide

Start with Standard Deviation on daily charts for the most intuitive introduction to distribution-based risk analysis.

Method Selection: Begin with Standard Deviation

Setup: Use daily charts with 20-30 bins

Interpretation: Focus on quartile transitions as signals

Monitoring: Track distribution changes for regime detection

The tool provides comprehensive statistics including mean, standard deviation, quartiles, and current position metrics like Z-score and percentile ranking.

Enjoy, and please let me know your feedback! 😊🥂

Pullback Pro Dow Strategy v7 (ADX Filter)

### **Strategy Description (For TradingView)**

#### **Title:** Pullback Pro: Dow Theory & ADX Strategy

---

#### **1. Summary**

This strategy is designed to identify and trade pullbacks within an established trend, based on the core principles of Dow Theory. It uses market structure (pivot highs and lows) to determine the trend direction and an Exponential Moving Average (EMA) to pinpoint pullback entry opportunities.

To enhance trade quality and avoid ranging markets, an ADX (Average Directional Index) filter is integrated to ensure that entries are only taken when the trend has sufficient momentum.

---

#### **2. Core Logic: How It Works**

The strategy's logic is broken down into three main steps:

**Step 1: Trend Determination (Dow Theory)**

* The primary trend is identified by analyzing recent pivot points.

* An **Uptrend** is confirmed when the script detects a pattern of higher highs and higher lows (HH/HL).

* A **Downtrend** is confirmed by a pattern of lower highs and lower lows (LH/LL).

* If neither pattern is present, the strategy considers the market to be in a range and will not seek trades.

**Step 2: Entry Signal (Pullback to EMA)**

* Once a clear trend is established, the strategy waits for a price correction.

* **Long Entry:** In a confirmed uptrend, a long position is initiated when the price pulls back and crosses *under* the specified EMA.

* **Short Entry:** In a confirmed downtrend, a short position is initiated when the price rallies and crosses *over* the EMA.

**Step 3: Confirmation & Risk Management**

* **ADX Filter:** To ensure the trend is strong enough to trade, an entry signal is only validated if the ADX value is above a user-defined threshold (e.g., 25). This helps filter out weak signals during choppy or consolidating markets.

* **Stop Loss:** The initial Stop Loss is automatically and logically placed at the last market structure point:

* For long trades, it's placed at the `lastPivotLow`.

* For short trades, it's placed at the `lastPivotHigh`.

* **Take Profit:** Two Take Profit levels are calculated based on user-defined Risk-to-Reward (R:R) ratios. The strategy allows for partial profit-taking at the first target (TP1), moving the remainder of the position to the second target (TP2).

---

#### **3. Input Settings Explained**

**① Dow Theory Settings**

* **Pivot Lookback Period:** Determines the sensitivity for detecting pivot highs and lows. A smaller number makes it more sensitive to recent price swings; a larger number focuses on more significant, longer-term pivots.

**② Entry Logic (Pullback)**

* **Pullback EMA Length:** Sets the period for the Exponential Moving Average used to identify pullback entries.

**③ Risk & Exit Management**

* **Take Profit 1 R:R:** Sets the Risk-to-Reward ratio for the first take-profit target.

* **Take Profit 1 (%):** The percentage of the position to be closed when TP1 is hit.

* **Take Profit 2 R:R:** Sets the Risk-to-Reward ratio for the final take-profit target.

**④ Filters**

* **Use ADX Trend Filter:** A master switch to enable or disable the ADX filter.

* **ADX Length:** The lookback period for the ADX calculation.

* **ADX Threshold:** The minimum ADX value required to confirm a trade signal. Trades will only be placed if the ADX is above this level.

---

#### **4. Best Practices & Recommendations**

* This is a trend-following system. It is designed to perform best in markets that exhibit clear, sustained trending behavior.

* It may underperform in choppy, sideways, or strongly ranging markets. The ADX filter is designed to help mitigate this, but no filter is perfect.

* **Crucially, you must backtest this strategy thoroughly** on your preferred financial instrument and timeframe before considering any live application.

* Experiment with the `Pivot Lookback Period`, `Pullback EMA Length`, and `ADX Threshold` to optimize performance for a specific market's characteristics.

---

#### **DISCLAIMER**

This script is provided for educational and informational purposes only. It does not constitute financial advice. All trading involves a high level of risk, and past performance is not indicative of future results. You are solely responsible for your own trading decisions. The author assumes no liability for any financial losses you may incur from using this strategy. Always conduct your own research and due diligence.

NY Open Breakout [ATR-5000]# **New York Open Breakout Indicator **

## **📌 Overview**

This **Pine Script** indicator identifies high-probability breakout opportunities at the **New York market open (13:30 UTC)** based on **volatility filters** using **customizable ATR periods and thresholds**.

### **🔹 Key Features**

✅ **Fully Customizable ATR Periods** (2 to **5000** bars)

✅ **Adjustable Thresholds** (0.01% to 5.00%)

✅ **Opening Range (OR) Filter** (0.01% to 5.00%)

✅ **Clean Visuals** – Only highlights the **13:30 UTC candle** when conditions are met

✅ **Real-Time Info Panel** – Displays current ATR & threshold settings

✅ **Automatic Daily Reset** – Fresh signals every trading day

---

## **📊 How It Works**

### **1️⃣ Volatility Check (13:25 UTC)**

- Calculates **two ATR values** (user-defined periods)

- Compares them against **custom % thresholds**

- Only proceeds if **both ATRs exceed** their required volatility levels

### **2️⃣ Opening Range Confirmation (13:30 UTC)**

- Measures the **high-low range** of the 13:30 candle

- Validates if the range meets the **minimum % threshold**

- If all conditions pass → **Highlights the candle** in your chosen color

### **3️⃣ Visual Feedback**

- **🟣 Colored Candle** → Valid breakout signal

- **📊 Info Table** → Shows current ATR settings & thresholds

---

## **⚙️ Customization Options**

| **Setting** | **Default** | **Adjustable Range** |

|---------------------------|------------|----------------------|

| **First ATR Period** | 14 | **2–5000** bars |

| **Second ATR Period** | 161 | **2–5000** bars |

| **First ATR Threshold** | 0.42% | **0.01%–5.00%** |

| **Second ATR Threshold** | 0.40% | **0.01%–5.00%** |

| **OR Range Threshold** | 0.42% | **0.01%–5.00%** |

| **Candle Color** | Purple | **Any color** |

---

## **📈 Best Use Cases**

✔ **Forex (EURUSD, GBPUSD)** – Captures NY session momentum

✔ **Indices (SPX, NASDAQ)** – Works well with opening volatility

✔ **Commodities (Gold, Oil)** – Filters out low-energy days

---

## **🔧 How to Adjust Settings**

1. **Click the gear icon (⚙️)** on your TradingView chart

2. **Modify ATR periods & thresholds** as needed

3. **Change the candle color** for better visibility

---

## **🚀 Why This Indicator?**

- **No repainting** – Signals lock in after candle close

- **No clutter** – Only marks valid 13:30 candles

- **Adaptable** – Works on **any market & timeframe**

- **Fully automated** – No manual adjustments needed

---

### **📥 Apply & Start Trading!**

Simply **load the script** on TradingView and customize it to fit your strategy! 🚀

Asset Premium/Discount Monitor📊 Overview

The Asset Premium/Discount Monitor is a tool for analyzing the relative value between two correlated assets. It measures when one asset is trading at a premium or discount compared to its historical relationship with another asset, helping traders identify potential mean reversion opportunities, or pairs trading opportunities.

🎯 Use Cases

Perfect for analyzing:

NASDAQ:MSTR vs CRYPTO:BTCUSD - MicroStrategy's premium/discount to Bitcoin

NASDAQ:COIN vs BITSTAMP:BTCUSD - Coinbase's relative value to Bitcoin

NASDAQ:TSLA vs NASDAQ:QQQ - Tesla's premium to tech sector

Regional banks AMEX:KRE vs AMEX:XLF - Individual bank stocks vs financial sector

Any two correlated assets where relative value matters

Example of a trade: MSTR vs BTC - When indicator shows MSTR at 95% percentile (extreme premium): Short MSTR, Buy BTC. Then exit when the spread reverts to the mean, say 40-60% percentile.

🔧 How It Works

Core Calculation

Ratio Analysis: Calculates the price ratio between your asset and the correlated asset

Historical Baseline: Establishes the "normal" relationship using a 252-day moving average. You can change this.

Premium Measurement: Measures current deviation from historical average as a percentage

Statistical Context: Provides percentile rankings and standard deviation bands

The Math

Premium % = (Current Ratio / Historical Average Ratio - 1) × 100

🎨 Customization Options

Correlated Asset: Choose any symbol for comparison

Lookback Period: Adjust historical baseline (50-1000 days)

Smoothing: Reduce noise with moving average (1-50 days)

Visual Toggles: Show/hide bands and percentile lines

Color Themes: Customize premium/discount colors

📊 Interpretation Guide

Premium/Discount Reading

Positive %: Asset trading above historical relationship (premium)

Negative %: Asset trading below historical relationship (discount)

Near 0%: Asset at fair value relative to correlation

Percentile Ranking

90%+: Near recent highs - potential selling opportunity

10% and below: Near recent lows - potential buying opportunity

25-75%: Normal trading range

Signal Classifications

🔴 SELL PREMIUM: Asset expensive relative to recent range

🟡 Premium Rich: Moderately expensive, monitor for reversal

⚪ NEUTRAL: Fair value territory

🟡 Discount Opportunity: Moderately cheap, potential accumulation zone

🟢 BUY DISCOUNT: Asset cheap relative to recent range

🚨 Built-in Alerts

Extreme Premium Alert: Triggers when percentile > 95%

Extreme Discount Alert: Triggers when percentile < 5%

⚠️ Important Notes

Works best with highly correlated assets

Historical relationships can change - monitor correlation strength

Not investment advice - use as one factor in your analysis

Backtest thoroughly before implementing any strategy

🔄 Updates & Future Features

This indicator will be continuously improved based on user feedback. So... please give me your feedback!

VoVix DEVMA🌌 VoVix DEVMA: A Deep Dive into Second-Order Volatility Dynamics

Welcome to VoVix+, a sophisticated trading framework that transcends traditional price analysis. This is not merely another indicator; it is a complete system designed to dissect and interpret the very fabric of market volatility. VoVix+ operates on the principle that the most powerful signals are not found in price alone, but in the behavior of volatility itself. It analyzes the rate of change, the momentum, and the structure of market volatility to identify periods of expansion and contraction, providing a unique edge in anticipating major market moves.

This document will serve as your comprehensive guide, breaking down every mathematical component, every user input, and every visual element to empower you with a profound understanding of how to harness its capabilities.

🔬 THEORETICAL FOUNDATION: THE MATHEMATICS OF MARKET DYNAMICS

VoVix+ is built upon a multi-layered mathematical engine designed to measure what we call "second-order volatility." While standard indicators analyze price, and first-order volatility indicators (like ATR) analyze the range of price, VoVix+ analyzes the dynamics of the volatility itself. This provides insight into the market's underlying state of stability or chaos.

1. The VoVix Score: Measuring Volatility Thrust

The core of the system begins with the VoVix Score. This is a normalized measure of volatility acceleration or deceleration.

Mathematical Formula:

VoVix Score = (ATR(fast) - ATR(slow)) / (StDev(ATR(fast)) + ε)

Where:

ATR(fast) is the Average True Range over a short period, representing current, immediate volatility.

ATR(slow) is the Average True Range over a longer period, representing the baseline or established volatility.

StDev(ATR(fast)) is the Standard Deviation of the fast ATR, which measures the "noisiness" or consistency of recent volatility.

ε (epsilon) is a very small number to prevent division by zero.

Market Implementation:

Positive Score (Expansion): When the fast ATR is significantly higher than the slow ATR, it indicates a rapid increase in volatility. The market is "stretching" or expanding.

Negative Score (Contraction): When the fast ATR falls below the slow ATR, it indicates a decrease in volatility. The market is "coiling" or contracting.

Normalization: By dividing by the standard deviation, we normalize the score. This turns it into a standardized measure, allowing us to compare volatility thrust across different market conditions and timeframes. A score of 2.0 in a quiet market means the same, relatively, as a score of 2.0 in a volatile market.

2. Deviation Analysis (DEV): Gauging Volatility's Own Volatility

The script then takes the analysis a step further. It calculates the standard deviation of the VoVix Score itself.

Mathematical Formula:

DEV = StDev(VoVix Score, lookback_period)

Market Implementation:

This DEV value represents the magnitude of chaos or stability in the market's volatility dynamics. A high DEV value means the volatility thrust is erratic and unpredictable. A low DEV value suggests the change in volatility is smooth and directional.

3. The DEVMA Crossover: Identifying Regime Shifts

This is the primary signal generator. We take two moving averages of the DEV value.

Mathematical Formula:

fastDEVMA = SMA(DEV, fast_period)

slowDEVMA = SMA(DEV, slow_period)

The Core Signal:

The strategy triggers on the crossover and crossunder of these two DEVMA lines. This is a profound concept: we are not looking at a moving average of price or even of volatility, but a moving average of the standard deviation of the normalized rate of change of volatility.

Bullish Crossover (fastDEVMA > slowDEVMA): This signals that the short-term measure of volatility's chaos is increasing relative to the long-term measure. This often precedes a significant market expansion and is interpreted as a bullish volatility regime.

Bearish Crossunder (fastDEVMA < slowDEVMA): This signals that the short-term measure of volatility's chaos is decreasing. The market is settling down or contracting, often leading to trending moves or range consolidation.

⚙️ INPUTS MENU: CONFIGURING YOUR ANALYSIS ENGINE

Every input has been meticulously designed to give you full control over the strategy's behavior. Understanding these settings is key to adapting VoVix+ to your specific instrument, timeframe, and trading style.

🌀 VoVix DEVMA Configuration

🧬 Deviation Lookback: This sets the lookback period for calculating the DEV value. It defines the window for measuring the stability of the VoVix Score. A shorter value makes the system highly reactive to recent changes in volatility's character, ideal for scalping. A longer value provides a smoother, more stable reading, better for identifying major, long-term regime shifts.

⚡ Fast VoVix Length: This is the lookback period for the fastDEVMA. It represents the short-term trend of volatility's chaos. A smaller number will result in a faster, more sensitive signal line that reacts quickly to market shifts.

🐌 Slow VoVix Length: This is the lookback period for the slowDEVMA. It represents the long-term, baseline trend of volatility's chaos. A larger number creates a more stable, slower-moving anchor against which the fast line is compared.

How to Optimize: The relationship between the Fast and Slow lengths is crucial. A wider gap (e.g., 20 and 60) will result in fewer, but potentially more significant, signals. A narrower gap (e.g., 25 and 40) will generate more frequent signals, suitable for more active trading styles.

🧠 Adaptive Intelligence

🧠 Enable Adaptive Features: When enabled, this activates the strategy's performance tracking module. The script will analyze the outcome of its last 50 trades to calculate a dynamic win rate.

⏰ Adaptive Time-Based Exit: If Enable Adaptive Features is on, this allows the strategy to adjust its Maximum Bars in Trade setting based on performance. It learns from the average duration of winning trades. If winning trades tend to be short, it may shorten the time exit to lock in profits. If winners tend to run, it will extend the time exit, allowing trades more room to develop. This helps prevent the strategy from cutting winning trades short or holding losing trades for too long.

⚡ Intelligent Execution

📊 Trade Quantity: A straightforward input that defines the number of contracts or shares for each trade. This is a fixed value for consistent position sizing.

🛡️ Smart Stop Loss: Enables the dynamic stop-loss mechanism.

🎯 Stop Loss ATR Multiplier: Determines the distance of the stop loss from the entry price, calculated as a multiple of the current 14-period ATR. A higher multiplier gives the trade more room to breathe but increases risk per trade. A lower multiplier creates a tighter stop, reducing risk but increasing the chance of being stopped out by normal market noise.

💰 Take Profit ATR Multiplier: Sets the take profit target, also as a multiple of the ATR. A common practice is to set this higher than the Stop Loss multiplier (e.g., a 2:1 or 3:1 reward-to-risk ratio).

🏃 Use Trailing Stop: This is a powerful feature for trend-following. When enabled, instead of a fixed stop loss, the stop will trail behind the price as the trade moves into profit, helping to lock in gains while letting winners run.

🎯 Trail Points & 📏 Trail Offset ATR Multipliers: These control the trailing stop's behavior. Trail Points defines how much profit is needed before the trail activates. Trail Offset defines how far the stop will trail behind the current price. Both are based on ATR, making them fully adaptive to market volatility.

⏰ Maximum Bars in Trade: This is a time-based stop. It forces an exit if a trade has been open for a specified number of bars, preventing positions from being held indefinitely in stagnant markets.

⏰ Session Management

These inputs allow you to confine the strategy's trading activity to specific market hours, which is crucial for day trading instruments that have defined high-volume sessions (e.g., stock market open).

🎨 Visual Effects & Dashboard

These toggles give you complete control over the on-chart visuals and the dashboard. You can disable any element to declutter your chart or focus only on the information that matters most to you.

📊 THE DASHBOARD: YOUR AT-A-GLANCE COMMAND CENTER

The dashboard centralizes all critical information into one compact, easy-to-read panel. It provides a real-time summary of the market state and strategy performance.

🎯 VOVIX ANALYSIS

Fast & Slow: Displays the current numerical values of the fastDEVMA and slowDEVMA. The color indicates their direction: green for rising, red for falling. This lets you see the underlying momentum of each line.