Cari dalam skrip untuk "ATR"

ATR+This is an indicator which uses the ATR (average true range) to calculate take profit levels, stop loss levels, and position sizing.

It acts an ATR indicator, based on concepts found in the No Nonsense Forex (NNFX) trading system.

ATR works by looking at the past N periods (14 by default) to see on average, how many pips or dollars an asset has moved. It is widely used by itself or as part of another indicator.

This script also implements money/risk management to determine:

Take Profit : 1.00x ATR (default)

Stop Loss : 1.50x ATR (default)

Risk : 2% of account size (default)

Position Sizing : How many lots/shares/units you need to achieve the indicated risk

Trade Value : The total cost of the lots/shares/units

This indicator only displays information in the status line. It does not guarantee a successful trade, and is only intended to be used to calculate take profit and stop loss levels, or as a point of reference when entering trades. Always do your own research.

ATR %Displays ATR percentage with 2SD. When value is greater than 12% I consider the stock as highly volatile

ATR DeltaThe ATR Delta indicator is based on the concept of Average True Range (ATR), which reflects the average price range over a specified period. By calculating the difference between current and previous ATR values, the ATR Delta provides valuable insights into volatility shifts in the market. This information can help traders identify periods of heightened or diminished price movement, enabling them to adjust their strategies accordingly.

The ATR Delta indicator consists of two main calculations:

-- ATR Calculation : The Average True Range (ATR) is calculated using the specified length parameter. It measures the average price range (including gaps) during that period. A larger ATR value indicates higher volatility, while a smaller value indicates lower volatility.

-- ATR Delta Calculation : The ATR Delta is calculated by subtracting the ATR value of the previous bar from the current ATR value. This calculation captures the change in volatility between the two periods, providing a measure of how volatility has evolved.

Positive ATR Delta values indicate an increase in volatility compared to the previous period. It suggests that price movements have expanded, potentially indicating a more active market. On the other hand, negative ATR Delta values indicate a decrease in volatility compared to the previous period. It suggests that price movements have contracted, potentially signaling a calmer or range-bound market.

The ATR Delta indicator uses coloration to visually represent the relationship between the ATR Delta, zero, and a signal line:

-- Green color is assigned when the ATR Delta is positive, above the signal line, and increasing. This coloration suggests a scenario of higher volatility, as the market is experiencing upward momentum in price swings.

-- Red color is assigned when the ATR Delta is negative, below the signal line, and decreasing. This coloration suggests a scenario of lower volatility, as the market is experiencing downward momentum in price swings.

-- Gray color is assigned for other cases when the ATR Delta and signal line relationship does not meet the above conditions.

These colors are reflected in the columns of the ATR Delta as well as the bar coloration.

The ATR Delta indicator includes a signal line, which acts as a reference for interpreting the ATR Delta values. The signal line is calculated as a moving average (EMA) of the ATR Delta over a specified length. It helps smooth out the ATR Delta fluctuations, providing a clearer indication of the underlying trend in volatility changes. When the ATR Delta crosses above the signal line, it may suggest a potential increase in volatility, indicating a market that is becoming more active. Conversely, when the ATR Delta crosses below the signal line, it may suggest a potential decrease in volatility, indicating a market that is becoming less active.

The coloration of the signal line in the ATR Delta indicator helps to differentiate between positive and negative values and provides further insight into market sentiment. When the signal line is positive, indicating increasing volatility, it is colored lime. This color choice reinforces the bullish sentiment and signifies potential opportunities for trend continuation or breakouts. On the other hand, when the signal line is negative, indicating decreasing volatility, it is colored fuchsia. This color choice highlights the bearish sentiment and suggests potential range-bound or consolidation periods. These colors are reflected in the background of the indicator.

The ATR Delta indicator offers several potential applications for traders:

-- Volatility Analysis : The ATR Delta is invaluable for understanding and analyzing volatility dynamics in the market. Traders can observe the changes in ATR Delta values and use them to assess the current level of price movement. This information can help determine the appropriate strategies and risk management approaches.

-- Breakout Strategies : Traders often use the ATR Delta to identify periods of increased volatility, which frequently accompany breakouts. By monitoring the ATR Delta, traders can anticipate potential price breakouts and adjust their entry and exit levels accordingly.

-- Trend Confirmation : Combining the ATR Delta with trend-following indicators allows traders to validate the strength of a trend. Higher ATR Delta values during an uptrend may indicate stronger momentum and a higher likelihood of continuation. Conversely, lower ATR Delta values during a downtrend may suggest a potential consolidation phase or trend reversal.

Limitations :

-- Lagging Indicator : The ATR Delta indicator is based on historical data and calculates the difference between current and previous ATR values. As a result, it may lag behind real-time market conditions. Traders should be aware of this delay and consider it when making trading decisions. It is advisable to combine the ATR Delta with other indicators or price action analysis for a more comprehensive assessment of market conditions.

-- Parameter Sensitivity : The ATR Delta indicator's effectiveness can be influenced by the selection of its parameters, such as the length of the ATR and signal line. Different market conditions may require adjustments to these parameters to better capture volatility changes. Traders should carefully test and optimize the indicator's parameters to align with the characteristics of the specific market or asset they are trading.

-- Market Regime Changes : The ATR Delta indicator assumes that volatility changes occur gradually. However, in rapidly changing market regimes or during news events, volatility can spike or drop abruptly, potentially rendering the indicator less effective. Traders should exercise caution and consider using additional tools or techniques to identify and adapt to such market conditions.

The ATR Delta indicator is a valuable tool for traders seeking to analyze and monitor volatility dynamics in the market. By calculating the difference between current and previous ATR values, it provides insights into changes in price movement and helps identify periods of increased or decreased volatility. Traders can leverage the ATR Delta to fine-tune their strategies, validate trend strength, and identify potential breakout opportunities. However, it is essential to recognize the limitations of the indicator, including its lagging nature and sensitivity to parameter selection. By combining the ATR Delta with other technical analysis tools and applying sound risk management practices, traders can enhance their decision-making process and potentially improve their trading outcomes.

ATR Gerchik LightAverage True Range ( ATR ) is a technical analysis indicator that measures volatility in the market. ATR is a moving average of the true range over a period of time.

ATR calculation procedure:

1. Determine the true maximum - this is the highest of the current maximum and yesterday's closing price of the day.

2. Determine the true minimum - this is the smallest of the current minimum and yesterday's closing price.

3. Determine the true range - this is the distance between the true maximum and minimum.

4. We exclude extremely large candles (> x2 ATR) and extremely small ones (< 0.5 ATR) from the obtained true ranges.

5. We calculate the average for the selected period based on the remaining range.

6. We calculate the percentage of the current True Range relative to the average ATR value for the previous period.

Description:

If you analyze it yourself, you will see that 75-80% of the time, the instrument moves only 1 ATR per day. You must understand that if an instrument has, for example, moved 80% of its daily range, it is not advisable to purchase it. This is comparable to a car's fuel tank: if the tank is almost empty, the car won't go far. Most indicators that calculate ATR include anomalous candles, which give unreliable results and lead to incorrect decisions. Because of this, many traders prefer to calculate ATR on their own.

However, the Gerchik ATR indicator accounts for anomalous candles and filters out extremely large candles (> 2x ATR) and extremely small ones (< 0.5x ATR). Additionally, this indicator immediately shows the consumed “fuel” of the instrument as a percentage, so you don't have to calculate the distance traveled yourself. This allows you to make quick, informed decisions. If we see that the tank is almost empty, it is logical not to get into that car today. When building any strategy, you must rely on the average movement.

Key Features:

Anomalous Candle Filtering: Excludes extremely large and small candles to provide more reliable ATR values.

Consumed Fuel Indicator: Shows the percentage of the ATR consumed, helping traders quickly assess the remaining potential movement.

Daily Timeframe Focus: Designed specifically for use on daily charts for accurate long-term analysis.

Practical Applications:

Entry and Exit Points: Use the ATR to determine optimal entry and exit points by assessing market volatility and potential price movement.

Stop-Loss Placement: Calculate stop-loss levels based on ATR to ensure they are placed at appropriate distances, accounting for current market volatility.

Trend Confirmation: Use the percentage of ATR consumed to confirm the strength of a trend and decide whether to enter or exit trades.

Examples of Use:

Trend Following: During strong trends, ATR helps identify periods of increased volatility, signaling potential breakouts or reversals.

Range Trading: In ranging markets, ATR can highlight periods of low volatility, indicating consolidation and potential breakout zones.

Note: The indicator is displayed and works only on the daily timeframe!

The indicator was created according to the instructions, description of the functionality, and strategy of Mr. Gerchik. Thank you so much, Chief!

________________________

Average True Range ( ATR , средний истинный диапазон) – это индикатор технического анализа, который измеряет волатильность на рынке. ATR представляет собой скользящее среднее истинного диапазона за определенный период времени.

Порядок расчета ATR:

1. Определяем истинный максимум – это наивысшее из текущего максимума и вчерашней цены закрытия дня.

2. Определяем истинный минимум – это наименьшее из текущего минимума и вчерашней цены закрытия.

3. Определяем истинный диапазон – это расстояние между истинным максимумом и минимумом.

4. Исключаем из полученных истинных диапазонов экстремально большие свечи (> x2 ATR) и экстремально маленькие (< 0.5 ATR).

5. Рассчитываем среднее за выбранный период исходя из оставшегося диапазона.

6 . Рассчитываем процент текущего истинного диапазона (True Range) относительно среднего значения ATR за предыдущий период.

Описание:

Если вы сами проанализируете, то увидите, что 75-80% времени инструмент ходит только 1 ATR. И вы должны понимать, что если инструмент внутри дня прошел, к примеру, 80% своего движения, то этот инструмент больше нельзя покупать. Это можно сравнить с баком машины: если бак почти пустой, машина далеко не уедет. Большинство индикаторов, которые рассчитывают ATR, производят расчет с паранормальными свечами. Это дает недостоверный результат и приводит к неверным решениям. Многие трейдеры из-за этого не используют готовые индикаторы и предпочитают считать ATR самостоятельно. Но индикатор ATR Gerchik учитывает паранормальные свечи и фильтрует экстремально большие свечи (> x2 ATR) и экстремально маленькие (< 0.5 ATR). Также этот индикатор сразу показывает израсходованный "бензин" инструмента в процентах. И вам не надо самостоятельно высчитывать пройденный путь. Вы можете быстро принимать правильные решения. Если мы видим, что бак почти пустой, логично не садиться в эту машину сегодня. Когда вы строите какую-то стратегию, вы должны обязательно полагаться на среднестатистическое движение.

Существует много стратегий, завязанных на ATR, которые учитывают волатильность инструмента, запас хода, точки разворота, места выставления стоп-лоссов (SL) и тейк-профитов (TP) и другие факторы. Я не буду останавливаться на них, так как каждый может найти описание этих стратегий и использовать их на свой выбор.

Индикатор отображается и работает только на дневном таймфрейме!

Индикатор создан по наставлениям, описанию функционала и стратегии господина Герчика. Огромное спасибо, Шеф!

ATR (Average True Range) mit relative/absolute Zahlen GERMAN:

Schnelle Zusammenfassung:

Dieses Skript basiert auf dem ATR-Indikator und wurde so angepasst, dass sowohl relative (%) als auch absolute Zahlen angezeigt werden. Es bietet eine Darstellung des ATR in absoluten und prozentualen Werten sowie multipliziert mit den Faktoren x2, x2.5 und x3. Diese Darstellung erleichtert die Festlegung von Stop-Kursen, insbesondere für Trailing Stops und Trailing Abstände.

Periode:

Die Periode ist einstellbar und definiert die Länge der Berechnung des ATR (Standardwert: 14).

Glättung: Es stehen verschiedene Methoden zur Auswahl, um die Daten zu glätten (RMA, SMA, EMA, WMA).

Berechnungen:

ATR (Absolute Zahl): Berechnung der durchschnittlichen wahren Reichweite (ATR) unter Verwendung der ausgewählten Glättungsmethode und Periode.

ATR (Prozentualer Wert): Berechnung des ATR als Prozentsatz des aktuellen Schlusskurses.

Multiplikation des ATR: Berechnung des ATR multipliziert mit den Faktoren 2, 2.5 und 3 zur Einschätzung verschiedener Handelsszenarien.

Darstellung:

Absoluter ATR-Wert: Darstellung der absoluten ATR-Werte in Blau.

Relative ATR-Werte (%): Darstellung der prozentualen ATR-Werte, ohne Linie in der Grafik (transparent).

Multiplizierte ATR-Werte (x2, x2.5, x3): Darstellung der multiplizierten ATR-Werte in den Farben Grün (x2), Orange (x2.5) und Lila (x3).

Textbeschriftungen: Für jeden absoluten ATR-Wert und seine Multiplikationen werden Textbeschriftungen links im Chart angezeigt.

Verwendung des Indikators:

Dieser Indikator unterstützt Trader und Analysten dabei, die durchschnittliche wahre Reichweite (ATR) eines Finanzinstruments zu verstehen und zu visualisieren. Die verschiedenen Multiplikationen des ATR ermöglichen es, potenzielle Preisbewegungen zu analysieren und Handelsstrategien zu entwickeln, die auf der Volatilität basieren.

Hinweis:

Dies ist meine persönliche Meinung und Einstellung. Dieses Skript stellt keine Bankberatung oder Anlageempfehlung dar. Die Nutzung erfolgt auf eigenes Risiko und Verantwortung des Nutzers.

----------------------------------------------------------------------

ENGLISH:

Quick Summary:

This script is based on the ATR (Average True Range) indicator and has been modified to display both relative (%) and absolute values. It provides a representation of ATR in absolute and percentage terms, as well as multiplied by factors x2, x2.5, and x3. This visualization aids in setting stop-loss levels, especially for trailing stops and trailing distances.

Period:

The period is adjustable and defines the length of the ATR calculation (default: 14).

Smoothing: Various methods are available to smooth the data (RMA, SMA, EMA, WMA).

Calculations:

ATR (Absolute Value): Computes the Average True Range using the selected smoothing method and period.

ATR (Percentage Value): Calculates the ATR as a percentage of the current closing price.

Multiplication of ATR: Computes the ATR multiplied by factors 2, 2.5, and 3 to assess different trading scenarios.

Visualization:

Absolute ATR Value: Displays the absolute ATR values in blue.

Relative ATR Values (%): Shows the ATR values as percentages, without lines in the chart (transparent).

Multiplied ATR Values (x2, x2.5, x3): Presents the multiplied ATR values in green (x2), orange (x2.5), and purple (x3).

Text Labels: Text labels are shown on the left side of the chart for each absolute ATR value and its multiples.

Use of the Indicator:

This indicator helps traders and analysts understand and visualize the Average True Range (ATR) of a financial instrument. The different multipliers of ATR allow for the analysis of potential price movements and the development of trading strategies based on volatility.

Disclaimer:

This represents my personal opinion and viewpoint. This script does not constitute bank advice or investment recommendations. Use it at your own risk and responsibility.

ATR Bands with ATR Cross + InfoTableOverview

This Pine Script™ indicator is designed to enhance traders' ability to analyze market volatility, trend direction, and position sizing directly on their TradingView charts. By plotting Average True Range (ATR) bands anchored at the OHLC4 price, displaying crossover labels, and providing a comprehensive information table, this tool offers a multifaceted approach to technical analysis.

Key Features:

ATR Bands Anchored at OHLC4: Visual representation of short-term and long-term volatility bands centered around the average price.

OHLC4 Dotted Line: A dotted line representing the average of Open, High, Low, and Close prices.

ATR Cross Labels: Visual cues indicating when short-term volatility exceeds long-term volatility and vice versa.

Information Table: Displays real-time data on market volatility, calculated position size based on risk parameters, and trend direction relative to the 20-period Smoothed Moving Average (SMMA).

Purpose

The primary purpose of this indicator is to:

Assess Market Volatility: By comparing short-term and long-term ATR values, traders can gauge the current volatility environment.

Determine Optimal Position Sizing: A calculated position size based on user-defined risk parameters helps in effective risk management.

Identify Trend Direction: Comparing the current price to the 20-period SMMA assists in determining the prevailing market trend.

Enhance Decision-Making: Visual cues and real-time data enable traders to make informed trading decisions with greater confidence.

How It Works

1. ATR Bands Anchored at OHLC4

Average True Range (ATR) Calculations

Short-Term ATR (SA): Calculated over a 9-period using ta.atr(9).

Long-Term ATR (LA): Calculated over a 21-period using ta.atr(21).

Plotting the Bands

OHLC4 Dotted Line: Plotted using small circles to simulate a dotted line due to Pine Script limitations.

ATR(9) Bands: Plotted in blue with semi-transparent shading.

ATR(21) Bands: Plotted in orange with semi-transparent shading.

Overlap: Bands can overlap, providing visual insights into changes in volatility.

2. ATR Cross Labels

Crossover Detection:

SA > LA: Indicates increasing short-term volatility.

Detected using ta.crossover(SA, LA).

A green upward label "SA>LA" is plotted below the bar.

SA < LA: Indicates decreasing short-term volatility.

Detected using ta.crossunder(SA, LA).

A red downward label "SA LA, then the market is considered volatile.

Display: Shows "Yes" or "No" based on the comparison.

b. Position Size Calculation

Risk Total Amount: User-defined input representing the total capital at risk.

Risk per 1 Stock: User-defined input representing the risk associated with one unit of the asset.

Purpose: Helps traders determine the appropriate position size based on their risk tolerance and current market volatility.

c. Is Price > 20 SMMA?

SMMA Calculation:

Calculated using a 20-period Smoothed Moving Average with ta.rma(close, 20).

Logic: If the current close price is above the SMMA, the trend is considered upward.

Display: Shows "Yes" or "No" based on the comparison.

How to Use

Step 1: Add the Indicator to Your Chart

Copy the Script: Copy the entire Pine Script code into the TradingView Pine Editor.

Save and Apply: Save the script and click "Add to Chart."

Step 2: Configure Inputs

Risk Parameters: Adjust the "Risk Total Amount" and "Risk per 1 Stock" in the indicator settings to match your personal risk management strategy.

Step 3: Interpret the Visuals

ATR Bands

Width of Bands: Wider bands indicate higher volatility; narrower bands indicate lower volatility.

Band Overlap: Pay attention to areas where the blue and orange bands diverge or converge.

OHLC4 Dotted Line

Serves as a central reference point for the ATR bands.

Helps visualize the average price around which volatility is measured.

ATR Cross Labels

"SA>LA" Label:

Indicates short-term volatility is increasing relative to long-term volatility.

May signal potential breakout or trend acceleration.

"SA 20 SMMA?

Use this to confirm trend direction before entering or exiting trades.

Practical Example

Imagine you are analyzing a stock and notice the following:

ATR(9) Crosses Above ATR(21):

A green "SA>LA" label appears.

The info table shows "Yes" for "Is ATR-based price volatile."

Position Size:

Based on your risk parameters, the position size is calculated.

Price Above 20 SMMA:

The info table shows "Yes" for "Is price > 20 SMMA."

Interpretation:

The market is experiencing increasing short-term volatility.

The trend is upward, as the price is above the 20 SMMA.

You may consider entering a long position, using the calculated position size to manage risk.

Customization

Colors and Transparency:

Adjust the colors of the bands and labels to suit your preferences.

Risk Parameters:

Modify the default values for risk amounts in the inputs.

Moving Average Period:

Change the SMMA period if desired.

Limitations and Considerations

Lagging Indicators: ATR and SMMA are lagging indicators and may not predict future price movements.

Market Conditions: The effectiveness of this indicator may vary across different assets and market conditions.

Risk of Overfitting: Relying solely on this indicator without considering other factors may lead to suboptimal trading decisions.

Conclusion

This indicator combines essential elements of technical analysis to provide a comprehensive tool for traders. By visualizing ATR bands anchored at the OHLC4, indicating volatility crossovers, and providing real-time data on position sizing and trend direction, it aids in making informed trading decisions.

Whether you're a novice trader looking to understand market volatility or an experienced trader seeking to refine your strategy, this indicator offers valuable insights directly on your TradingView charts.

Code Summary

The script is written in Pine Script™ version 5 and includes:

Calculations for OHLC4, ATRs, Bands, SMMA:

Uses built-in functions like ta.atr() and ta.rma() for calculations.

Plotting Functions:

plotshape() for the OHLC4 dotted line.

plot() and fill() for the ATR bands.

Crossover Detection:

ta.crossover() and ta.crossunder() for detecting ATR crosses.

Labeling Crossovers:

label.new() to place informative labels on the chart.

Information Table Creation:

table.new() to create the table.

table.cell() to populate it with data.

Acknowledgments

ATR and SMMA Concepts: Built upon standard technical analysis concepts widely used in trading.

Pine Script™: Leveraged the capabilities of Pine Script™ version 5 for advanced charting and analysis.

Note: Always test any indicator thoroughly and consider combining it with other forms of analysis before making trading decisions. Trading involves risk, and past performance is not indicative of future results.

Happy Trading!

ATR Plots + OverlayATR Plots + Overlay

This tool calculates and displays Average True Range (ATR)-based levels on your chart for any selected timeframe, giving traders a quick visual reference for expected price movement relative to the most recent bar’s open price. It plots guide levels above and below that open and shows how much of the typical ATR-based range has already been covered—all in one interactive table and on-chart overlay.

What It Does

ATR Calculation:

Uses true range data over a user-defined period (default 14), smoothed via RMA, SMA, EMA, or WMA, on the selected timeframe (e.g., 1h, 4h, daily) to calculate the ATR value.

Projected Levels:

Plots four reference levels relative to the open price of the most recent bar on the chosen timeframe:

+100% ATR: Open + ATR

+50% ATR: Open + 50% of ATR

−50% ATR: Open − 50% of ATR

−100% ATR: Open − ATR

Coverage %:

Tracks high and low prices for the current session on the selected timeframe and calculates what percentage of the ATR has already been covered:

Coverage % = (High − Low) ÷ ATR × 100

Interactive Table:

Shows the ATR value and current coverage percentage in a customizable table overlay. Position, color scheme, borders, transparency, and an optional empty top row are all adjustable via settings.

Customization Options

Table Settings:

Position the table (top/bottom × left/right).

Customize background color, text color, border color, and thickness.

Optionally add an empty top row for spacing.

Line Settings:

Choose color, line style (solid/dotted/dashed), and width.

Lines automatically update with each new bar on the selected timeframe, anchored to that bar’s open price.

General Inputs:

ATR length (number of bars).

Smoothing method (RMA, SMA, EMA, WMA).

Timeframe selection for ATR calculations (e.g., 15m, 1h, Daily).

How to Use It for Trading

Measure Volatility: Quickly gauge the expected price movement based on ATR for any timeframe.

Identify Overextension: Use the coverage % to see how much of the expected ATR range is already consumed.

Plan Entries & Exits: Align trade targets and stops with ATR levels for more objective planning.

Visual Reference: Horizontal guide lines and table update automatically as new bars form, keeping information clear and actionable.

Ideal For

Intraday traders using ATR levels to frame trades.

Swing traders wanting ATR-based reference points for larger timeframes.

Anyone seeking a volatility-based framework for planning stops, targets, or identifying overextended conditions.

ATR+ Advanced Sessions ATR for DaterangeATR+ Advanced Sessions ATR for Daterange

The ATR+ adds the following additional filters to the stock ATR indicator by Tradingview:

- Calculates the overall average ATR for a user defined daterange, optionally filtered by trading session and selected weekdays, presented as a secondary line over the standard ATR line.

- Basic ATR line, with colour highlight to indicate the selected sessions, days and timeframe being calculated by the average ATR+ line.

- Average ATR+ line indicating the average of all ATRs within the defined timeframe, optionally filtered by instances of a selected trading session and selected weekdays.

- Customisable appearance.

- The ATR+ also includes the basic ATR configuration options typically found in the standard ATR by Tradingview, including period length and smoothing type. Defaults are set to the factory standards: 14 length, RMA smoothing type.

What Is the Average True Range (ATR)?

The ATR is a technical analysis tool that measures market volatility by decomposing the entire range asset price for that period. Investopedia describes the ATR as follows:

"The average true range (ATR) is a technical analysis indicator, introduced by market technician J. Welles Wilder Jr. in his book New Concepts in Technical Trading Systems, that measures market volatility by decomposing the entire range of an asset price for that period.

The true range indicator is taken as the greatest of the following: current high less the current low; the absolute value of the current high less the previous close; and the absolute value of the current low less the previous close. The ATR is then a moving average, generally using 14 days, of the true ranges."

For more information on the ATR and its calculations and use cases, see here:

Investopedia link here.

Tradingview link here.

Note

The indicator may time out if the number of bars being calculated is too long. If this happens, you will need to reduce the datetime range, or increase the chart timeframe in order to reduce the number of bars being calculated and the indicator will attempt to recalculate.

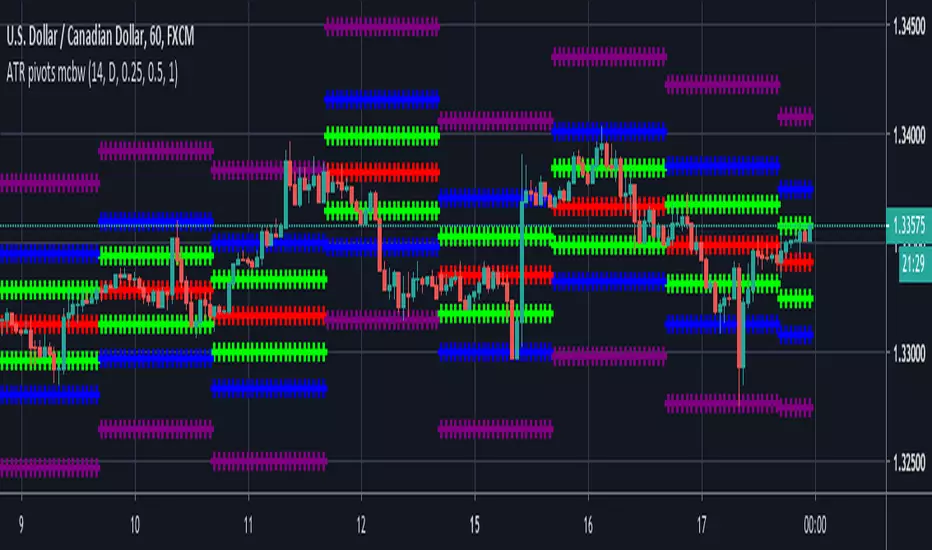

ATR based Pivots mcbwHey everyone this is an exciting new script I have prepared for you.

I was reading an old forex bulletin article some time ago when I came across this: solar.murty.net (or you can download the full bulletin with lots of other good articles here: www.forexfactory.com).

You can already buy this for metatrader (www.mql5.com) so I figured to make it for free for tradingview.

This bulletin suggested that you can reasonably predict daily volatility by adding or subtracting multiples of the daily ATR to the daily opening. Using this you can choose multiples to use as price targets and alternatively as stop losses. For example, if you already have a sense of market direction you can buy at market open place a stop loss at - 1 daily ATR and a profit target at + 3 ATRs for a risk to reward ratio of 3. If you are looking for smaller/quicker moves with a ratio of 3 you can have a stop loss at -0.25 ATR and a take profit at +0.75 ATR.

Alternatively this article also suggests to use this method to catch volatility breakouts. If price is higher than the + 1 ATR area then you can safely assume it will be going to the +2 ATR area so you can put a buy stop at + 1 ATR with a profit target at + 2 ATR with a stop loss at +0.5 ATR to catch a volatility breakout with a risk to reward ratio of 2!

Even further there are methods that you can use with ATRs of multiple window sizes, for example by opening two copies of this indicator and measuring recent volatility with a 1 week window and long term volatility within a 1 month window. If the short term volatility is crossing the long term volatility then there is a high probability chance that even more price movement will occur.

However I have found that this method is good for more than daily volatility , it can also be used to measure weekly volatility , and monthly volatility and use these multiples as good long term price targets.

To select if you want daily, weekly, or monthly values of the ATR of volatility you're using go to the settings and click on the options in the "Opening period". The default window of the ATR here is 14 periods, but you can change this if you want to in "ATR period". Most importantly you are able to select which multiples of the ATR you would like to use in the settings in "ATR multiple 1" which is the green line, "ATR multiple 2" which is the blue line, and "ATR multiple 3" which is the purple line. You can select any values you want to put in these, the choice of 0.25, 0.5, and 1 is not special, some people use fibonacci numbers here or simply 0.33, 0.66, and 0.99.

Repainting issue: This script uses the daily value of the Average True Range (ATR), which measures the volatility that is happening today. If price becomes more volatile then the value of the ATR can increase throughout the day, but it can never decrease. What this means is that the ATR based pivots are able to expand away from the opening price, which should not affect the trades that you take based on these areas. If you base your take profit on one of these ATR multiples and the daily volatility increase this means that your take profit area will be closer to your entry than the ATR multiple. Meaning that your trades will be more conservative.

While this all may sound very technical it is super intuitive, throw this on your chart and play around with it :)

Happy trading!

ATR Trailing Stop with ATR Targets [v6]What the Indicator Does

This custom TradingView indicator is designed for active traders who want to automate and visualize their trailing stop management and target setting, using true market volatility. It combines the Average True Range (ATR) with dynamic market structure logic to:

Trail a stop-loss behind major swings in real time, using 2×ATR (adjustable) from the highest high in uptrends or the lowest low in downtrends.

Flip trading bias between bullish and bearish when the stop is breached.

Identify and plot three profit targets (at 1, 2, and 3 ATR from the breakout/flip point) after every stop-flip, helping traders scale out or set take-profits objectively.

Maintain a visible presence on your chart every bar to avoid indicator errors, with color and labeling for clear distinction between long/short phases.

How the Indicator Works

1. ATR Calculation

ATR Period and Multiplier: You select your preferred ATR length (default is 14 bars) and a multiplier (default is 2.0).

Volatility Adjustment: ATR measures the average "true" bar range, so the trailing stop and targets adapt to current volatility.

2. Trailing Stop Logic

Uptrend (bullish bias): The indicator tracks the highest high made since the last bearish-to-bullish flip and sets the stop at - .

The stop only raises (never lowers) during an uptrend, protecting gains in strong moves.

Downtrend (bearish bias): Tracks the lowest low made since the last bullish-to-bearish flip, with stop at + .

The stop only lowers (never raises) in a downtrend.

Flip Point: If price closes through the trailing stop, the current bias “flips,” and the logic reverses (bullish to bearish or vice versa). At the new close, flip price and bar index are stored for target calculation.

3. ATR Targets after Flip

After each stop flip:

Three targets—based on the new close price—are calculated and plotted:

Long flip (new bull bias): Target1 = close + 1×ATR, Target2 = close + 2×ATR, Target3 = close + 3×ATR.

Short flip (new bear bias): Target1 = close - 1×ATR, Target2 = close - 2×ATR, Target3 = close - 3×ATR.

These targets help with scaling out, partial profit-taking, or setting automated orders.

4. Visual Feedback

Trailing stop line: Green for long bias, red for short bias.

Targets: Distinct color-coded circles at 1, 2, 3 ATR levels from the most recent flip.

Flip Labels: Mark the bar and price where bias flipped (“Long Flip” or “Short Flip”) for quick pattern recognition.

Subtle background shading: Ensures TradingView's requirement for “indicator output every bar.”

How to Use This Indicator

Parameter Setup

ATR Period and Multiplier: Adjust to match the timeframe and volatility of your instrument.

Lower periods/multipliers for short-term/volatile trading.

Higher values for smoother signals or higher timeframes.

Starting Trend: Set to match the expected initial bias if the instrument has strong trend characteristics.

Trading Application

1. Daily Bias Approach

Establish your bias in line with your trading plan (e.g., only trade long if price is above the previous day's high, short below the previous day's low).

Only look for trades in the indicator's current bias direction, as expressed by the stop and background color.

2. Entry

Use the indicator as a real-time confirmation or trailing stop for your entries.

Breakout: Enter when price establishes the current bias, using the trailing stop as your risk level.

Reversal: Wait for a bias flip after an extended move; enter in the direction of the new bias.

VWAP Rebound: Combine with a VWAP bounce—enter only if the indicator bias supports your direction.

3. Exits/Targets

Trailing stop management: Move your stop according to the plotted line; exit if your stop is hit.

Profit-taking: Scale out or take profits as price approaches each ATR-based target.

Use the dynamic labeling to identify reversal flips and reset your plan if stopped or the bias changes.

4. Market Context

Filter and frame setups by watching correlated indicators (DXY, VIX, AUDJPY, put/call ratio) and upcoming news; trade only in the daily bias direction for best consistency.

5. Practical Tips

Combine this indicator with your custom watchlist and alert settings to get notified on flips or targets.

Review the last label ("Long Flip"/"Short Flip") and targets to plan partial exits.

Remember: ATR adapts to volatility, so the stop and targets stay proportionate even when price action shifts.

ATR Buy, Target, Stop + OverlayATR Buy, Target, Stop + Overlay

This tool is to assist traders with precise trade planning using the Average True Range (ATR) as a volatility-based reference.

This script plots buy, target, and stop-loss levels on the chart based on a user-defined buy price and ATR-based multipliers, allowing for objective and adaptive trade management.

*NOTE* In order for the indicator to initiate plotted lines and table values a non-zero number must be entered into the settings.

What It Does:

Buy Price Input: Users enter a manual buy price (e.g., an executed or planned trade entry).

ATR-Based Target and Stop: The script calculates:

Target Price = Buy + (ATR × Target Multiplier)

Stop Price = Buy − (ATR × Stop Multiplier)

Customizable Timeframe: Optionally override the ATR timeframe (e.g., use daily ATR on a 1-hour chart).

Visual Overlay: Lines are drawn directly on the price chart for the Buy, Target, and Stop levels.

Interactive Table: A table is displayed with relevant levels and ATR info.

Customization Options:

Line Settings:

Adjust color, style (solid/dashed/dotted), and width for Buy, Target, and Stop lines.

Choose whether to extend lines rightward only or in both directions.

Table Settings:

Choose position (top/bottom, left/right).

Toggle individual rows for Buy, Target, Stop, ATR Timeframe, and ATR Value.

Customize text color and background transparency.

How to Use It for Trading:

Plan Your Trade: Enter your intended buy price when planning a trade.

Assess Risk/Reward: The script immediately visualizes the potential stop-loss and target level, helping assess R:R ratios.

Adapt to Volatility: Use ATR-based levels to scale stop and target dynamically depending on current market volatility.

Higher Timeframe ATR: Select a different timeframe for the ATR calculation to smooth noise on lower timeframe charts.

On-the-Chart Reference: Visually track trade zones directly on the price chart—ideal for live trading or strategy backtesting.

Ideal For:

Swing traders and intraday traders

Risk management and trade planning

Traders using ATR-based exits or scaling

Visualizing asymmetric risk/reward setups

How I Use This:

After entering a trade, adding an entry price will plot desired ATR target and stop level for visualization.

Adjusting ATR multiplier values assists in evaluating and planning trades.

Visualization assists in comparing ATR multiples to recent support and resistance levels.

ATR-based TP/SL with Dynamic RREnglish

This indicator combines the power of the Average True Range (ATR) with dynamic calculations for Take Profit (TP) and Stop Loss (SL) levels, offering a clear visualization of trading opportunities and their respective Risk-Reward Ratios (RRR).

Features:

Dynamic TP/SL Calculation:

TP and SL levels are derived using user-defined ATR multipliers for precise positioning.

Multipliers are flexible, allowing traders to adjust according to their strategies.

Risk-Reward Ratio (RRR):

Automatically calculates and displays the RRR for each trade signal.

Helps traders quickly assess if a trade aligns with their risk management plan.

Entry Conditions:

Buy signals occur when the closing price crosses above the 20-period Simple Moving Average (SMA).

Sell signals occur when the closing price crosses below the 20-period SMA.

Visual Aids:

Red and green lines indicate Stop Loss and Take Profit levels.

Blue and orange labels show the RRR for long and short trades, respectively.

How It Works:

The indicator uses the ATR to calculate TP and SL levels:

TP: Adjusted based on the desired Risk-Reward Ratio (RR).

SL: Proportional to the ATR multiplier.

Entry signals are plotted with "BUY" or "SELL" markers, while the respective TP/SL levels are drawn as horizontal lines.

Why Use This Indicator?

Perfect for traders who value precise risk management.

Helps identify trades with favorable RRR (e.g., greater than 1.5 or 2.0).

Ideal for swing traders, day traders, and scalpers looking to automate their decision-making process.

Customization:

ATR Length: Control the sensitivity of ATR-based calculations.

ATR Multipliers: Set the TP and SL distances relative to the ATR.

Desired RRR: Define the risk/reward ratio you aim to achieve.

Important Notes:

The indicator does not place trades automatically; it is for visual and analytical purposes.

Always backtest and combine it with additional analysis for best results.

French

Cet indicateur combine la puissance de l’Average True Range (ATR) avec des calculs dynamiques pour les niveaux de Take Profit (TP) et de Stop Loss (SL), tout en offrant une visualisation claire des opportunités de trading et de leurs Ratios Risque/Rendement (RRR).

Fonctionnalités :

Calcul Dynamique des TP/SL :

Les niveaux de TP et SL sont calculés à l'aide de multiplicateurs ATR définis par l’utilisateur pour une position précise.

Les multiplicateurs sont personnalisables pour s'adapter à votre stratégie de trading.

Ratio Risque/Rendement (RRR) :

Calcule et affiche automatiquement le ratio RRR pour chaque signal de trade.

Permet aux traders d’évaluer rapidement si un trade correspond à leur plan de gestion des risques.

Conditions d'Entrée :

Les signaux d'achat apparaissent lorsque le prix de clôture traverse au-dessus de la moyenne mobile simple (SMA) à 20 périodes.

Les signaux de vente apparaissent lorsque le prix de clôture traverse en dessous de la SMA à 20 périodes.

Aides Visuelles :

Lignes rouges et vertes pour indiquer les niveaux de Stop Loss et de Take Profit.

Étiquettes bleues et orange pour afficher le RRR des trades longs et courts, respectivement.

Comment Cela Fonctionne :

L'indicateur utilise l’ATR pour calculer les niveaux TP et SL :

TP : Calculé dynamiquement en fonction du ratio risque/rendement souhaité (RRR).

SL : Proportionnel au multiplicateur ATR défini par l’utilisateur.

Les signaux d’entrée sont représentés par des étiquettes "BUY" ou "SELL", tandis que les niveaux de TP/SL sont tracés sous forme de lignes horizontales.

Pourquoi Utiliser Cet Indicateur ?

Idéal pour les traders soucieux d’une gestion rigoureuse des risques.

Identifie les opportunités de trades avec des RRR favorables (par exemple, supérieurs à 1.5 ou 2.0).

Convient aux swing traders, day traders et scalpeurs souhaitant automatiser leur processus de décision.

Personnalisation :

Longueur de l’ATR : Contrôlez la sensibilité des calculs basés sur l’ATR.

Multiplicateurs ATR : Ajustez les distances TP et SL par rapport à l’ATR.

Ratio RRR souhaité : Définissez le ratio risque/rendement que vous visez.

Remarques Importantes :

Cet indicateur n’exécute pas de trades automatiquement ; il est destiné à un usage visuel et analytique uniquement.

Toujours backtester et combiner avec une analyse supplémentaire pour de meilleurs résultats.

parametre par type de trading:

1. Pour les Scalpers :

Style de trading : Trades rapides sur de petites variations de prix, souvent sur des unités de temps courtes (1 min, 5 min).

Recommandations de paramètres :

ATR Length : 7 (plus court pour réagir rapidement à la volatilité).

Multiplicateur SL : 1.0 (Stop Loss proche pour limiter les pertes).

RR souhaité : 1.5 à 2.0 (bon équilibre entre risque et récompense).

Résultat attendu : Des trades fréquents, avec une probabilité raisonnable de toucher le TP tout en limitant les pertes.

2. Pour les Day Traders :

Style de trading : Trades qui durent plusieurs heures dans la journée, souvent sur des unités de temps moyennes (15 min, 1h).

Recommandations de paramètres :

ATR Length : 14 (standard pour capturer une volatilité modérée).

Multiplicateur SL : 1.5 (Stop Loss à distance raisonnable pour supporter les fluctuations intrajournalières).

RR souhaité : 2.0 à 3.0 (ciblez une bonne récompense par rapport au risque).

Résultat attendu : Moins de trades, mais un RR élevé pour compenser les pertes potentielles.

3. Pour les Swing Traders :

Style de trading : Trades qui durent plusieurs jours, souvent sur des unités de temps longues (4h, 1 jour).

Recommandations de paramètres :

ATR Length : 20 (pour capturer des mouvements de volatilité plus larges).

Multiplicateur SL : 2.0 (Stop Loss large pour supporter des fluctuations importantes).

RR souhaité : 3.0 ou plus (ciblez de gros mouvements de prix).

Résultat attendu : Des trades moins fréquents mais potentiellement très lucratifs.

4. Pour les Actifs Volatils (Crypto, Commodités) :

Problème spécifique : Les actifs volatils ont souvent des mouvements brusques.

Recommandations de paramètres :

ATR Length : 7 ou 10 (plus court pour suivre rapidement les variations).

Multiplicateur SL : 1.5 à 2.0 (assez large pour ne pas être déclenché prématurément).

RR souhaité : 1.5 à 2.0 (favorisez des récompenses réalistes sur des mouvements volatils).

Résultat attendu : Trades qui s’adaptent à la volatilité sans sortir trop tôt.

5. Pour les Marchés Stables (Indices, Actions Blue Chip) :

Problème spécifique : Les mouvements sont souvent lents et prévisibles.

Recommandations de paramètres :

ATR Length : 14 ou 20 (capture une volatilité modérée).

Multiplicateur SL : 1.0 à 1.5 (Stop Loss serré pour maximiser l’efficacité).

RR souhaité : 2.0 à 3.0 (ciblez des ratios plus élevés sur des mouvements moins fréquents).

Résultat attendu : Maximisation des profits sur des tendances claires.

Recommandation Générale :

Si vous ne savez pas par où commencer, utilisez ces paramètres par défaut :

ATR Length : 14

Multiplicateur SL : 1.5

RR souhaité : 2.0

ATR Bands (Keltner Channel), Wick and SRSI Signals [MW]Introduction

This indicator uses a novel combination of ATR Bands, candle wicks crossing the ATR upper and lower bands, and baseline, and combines them with the Stochastic SRSI oscillator to provide early BUY and SELL signals in uptrends, downtrends, and in ranging price conditions.

How it’s unique

People generally understand Bollinger Bands and Keltner Channels. Buy at the bottom band, sell at the top band. However, because the bands themselves are not static, impulsive moves can render them useless. People also generally understand wicks. Candles with large wicks can represent a change in pattern, or volatile price movement. Combining those two to determine if price is reaching a pivot point is relatively novel. When Stochastic RSI (SRSI) filtering is also added, it becomes a genuinely unique combination that can be used to determine trade entries and exits.

What’s the benefit

The benefit of the indicator is that it can help potentially identify pivots WHEN THEY HAPPEN, and with potentially minimal retracement, depending on the trader’s time window. Many indicators wait for a trend to be established, or wait for a breakout to occur, or have to wait for some form of confirmation. In the interpretation used by this indicator, bands, wicks, and SRSI cycles provide both the signal and confirmation.

It takes into account 3 elements:

Price approaching the upper or lower band or the baseline - MEANING: Price is becoming extended based on calculations that use the candle trading range.

A candle wick of a defined proportion (e.g. wick is 1/2 the size of a full candle OR candle body) crosses a band or baseline, but the body does not cross the band or baseline - MEANING: Buyers and sellers are both very active.

The Stochastic RSI reading is above 80 for SELL signals and below 20 for BUY signals - MEANING: Additional confirmation that price is becoming extended based on the current cyclic price pattern.

How to Use

SIGNALS

Buy Signals - Green(ish):

B Signal - Potential pivot up from the lower band when using the preferred multiplier

B1 Signal - Potential pivot up from the lower band when using phi * multiplier

B2 Signal - Potential pivot up from the lower band when using 1/2 * multiplier

B3 Signal - Potential pivot up from baseline

Sell Signals - Red(ish):

S Signal - Potential pivot down from the upper band when using the preferred multiplier

S1 Signal - Potential pivot down from the upper band when using

S2 Signal - Potential pivot down from the upper band when using 1/2 * multiplier

S3 Signal - Potential pivot down from the baseline

DISCUSSION

During an uptrend or downtrend, signals from the baseline can help traders identify areas where they may enter the trending move with the least amount of drawdown. In both cases, entry points can occur with baseline signals in the direction of the trend.

For example, in an uptrend (when the price is forming higher highs and higher lows, or when the baseline is rising), price tends to oscillate between the upper band and baseline. In this case, the baseline BUY signal (B3) can show an entry point.

In a downtrend (when the price is forming lower highs and lower lows, or when the baseline is falling), price tends to oscillate between the baseline and the lower band. In this case, the baseline SELL signal (S3) can show an entry point.

During consolidation, when price is ranging, price tends to oscillate between the upper and lower bands, while crossing through the baseline unperturbed. Here, entry points can occur at the upper and lower bands.

When all conditions are met at the lower band during consolidation, a BUY signal (B), can occur. This signal may also occur prior to a break out of consolidation to the upside.

When all conditions are met at the upper band during consolidation, a SELL signal (S), can occur. This signal may also occur prior to a break out of consolidation to the downside.

Additional B1, B2, and S1, and S2 signals can be displayed that use the bands based on a multiplier that is half that of the primary one, and phi (0.618) times the primary multiplier as a way to quickly check for signals occurring along different, but related, bands.

Calculations

ATR Bands, or Keltner Channels, are a technical analysis tool that are used to measure market volatility and identify overbought or oversold conditions in the trading of financial instruments, such as stocks, bonds, commodities, and currencies. ATR Bands consist of three lines plotted on a price chart:

Middle Band, Basis, or Baseline: This is typically a simple moving average (SMA) of the closing prices over a certain period. It represents the intermediate-term trend of the asset's price.

Upper Band: This is calculated by adding a certain number of ATRs to the middle band (SMA). The upper band adjusts itself with the increase in volatility.

Lower Band: This is calculated by subtracting the same number of ATRs from the middle band (SMA). Like the upper band, the lower band adjusts to changes in volatility.

The candle wick signals occur if the wick is at the specified ratio compared to either the entire candle or the candle body. The upper band, lower band, and baseline signals happen if the wick is the specified ratio of the total candle size. For the major signals for upper and lower bands, these occur when the wick extends outside of the bands while closing a candle inside of the bands. For the baseline signals, they occur if a wick crosses a baseline but closes on the other side.

Settings

CHANNEL SETTINGS

Baseline EMA Period (Default: 21): Period length of the moving average basis line.

ATR Period (Default: 21): The number of periods over which the Average True Range (ATR) is calculated.

Basis MA Type (Default: SMA): The moving average type for the basis line.

Multiplier (Default: 2.5: The deviation multiplier used to calculate the band distance from the basis line.

ADDITIONAL CHANNELS

Half of Multiplier Offset (Default: True): Toggles the display of the ATR bands that are set a distance of half of the ATR multiplier.

Quarter of Multiplier Offset (Default: false): Toggles the display of the ATR bands that are set a distance of one quarter of the ATR multiplier.

Phi (Φ) Offset (Default: false): Toggles the display of the ATR bands that are set a distance of phi (Φ) times the ATR multiplier.

WICK SETTINGS FOR CANDLE FILTERS

Wick Ratio for Bands (Default: 0.4): The ratio of wick size to total candle size for use at upper and lower bands.

Wick Ratio for Baseline (Default: 0.4): The ratio of wick size to total candle size for use at baseline.

Use Candle Body (rather than full candle size) (Default: false): Determines whether wick calculations use the candle body or the entire candle size.

VISUAL PREFERENCES - SIGNALS

Show Signals (Default: true): Allows signal labels to be shown.

Show Signals from 1/2 Band Offset (Default: false): Toggle signals originating from 1/2 offset upper and lower bands.

Show Signals from Phi (Φ) Band Offset (Default: false): Toggle signals originating from phi (Φ) offset upper and lower bands.

Show Baseline Signals (Default: false): Toggle Baseline signals.

VISUAL PREFERENCES - BANDS

Show ATR (Keltner) Bands (Default: true): Use a background color inside the Bollinger Bands.

Fill Bands (Default: true): Use a background color inside the Bollinger Bands.

STOCHASTIC SETTINGS

Use Stochastic RSI Filtering (Default: False): This will only trigger some SELL signals when the stochastic RSI is above 80, and BUY signals when below 20.

K (Default: 3): The smoothing level for the Stochastic RSI.

RSI Length (Default: 14): The period length for the RSI calculation.

Stochastic Length (Default: 8): The period length over which the stochastic calculation is performed.

Other Usage Notes and Limitations

To understand future price movement, this indicator assumes that 3 things must be known:

Evidence of a change of market structure. This can be demonstrated by increased volatility, consolidation, volume spikes (which can be tracked with the MW Volume Impulse Indicator) or, in the case of this indicator, candle wicks.

The potential cause of the change. It could be a VWAP line (which can be tracked with the Multi VWAP , and Multi VWAP from Gaps indicators), an event, an important support or resistance level, a key moving average, or many other things. This indicator assumes the ATR bands can be a cause.

The current position in the price cycle. Oscillators like the RSI, and MACD, are typical measures of price oscillation (other oscillators like the Price and Volume Stochastic Divergence indicator can also be useful). This indicator uses the Stochastic RSI oscillator to determine overbought and oversold conditions.

When evidence of the change appears, and the potential cause of the change is identified, and the price oscillation is at a favorable position for the desired trading direction, this indicator will generate a signal.

ATR Bands (or Keltner Channels) are used to determine when price might “revert to the mean”. Crossing, or being near the upper or lower band, can indicate an overbought or oversold condition, which could lead to a price reversal. By tracking the behavior of candle wicks during these events, we can see how active the battle is between buyers and sellers.

If the top of a wick is large, it may indicate that sellers are aggressively attempting to bring the price down. Conversely, if the bottom wick is large, it can indicate that buyers are actively trying to counter the price action caused by selling pressure.

When this wicking action occurs at times when price is not near the upper band, lower band, or baseline, it could indicate the presence of an important level. That could mean a nearby VWAP line, a supply or demand zone, a round price number, or a number of other factors. In any case, this wick may be the first indication of a price reversal.

Shorter baseline periods may be better for short period trading like scalping or day trading, while longer period baselines can show signals that are better suited to swing trading, or longer term investing.

It's important for traders to be aware of the limitations of any indicator and to use them as part of a broader, well-rounded trading strategy that includes risk management, fundamental analysis, and other tools that can help with reducing false signals, determining trend direction, and providing additional confirmation for a trade decision. Diversifying strategies and not relying solely on one type of indicator or analysis can help mitigate some of these risks.

The TradingView platform allows a maximum of 500 labels per chart. This means that if your settings allow for a lot of signals, labels for earlier ones may not appear if the total number of labels exceeds 500 for the chart.

ATR Based Support and Resistance Zones [UAlgo]🔶 ATR Based Support and Resistance Indicator 🔶

The ATR Based Support and Resistance Indicator is a technical tool designed for TradingView users to analyze and visualize support and resistance levels based on the Average True Range (ATR) indicator. ATR is a widely used volatility indicator that measures the average trading range of an asset over a specified period. This indicator utilizes ATR values to dynamically calculate and display support and resistance zones on the price chart.

🔶 Indicator Settings

ATR Length: This setting allows users to specify the length of the period over which the ATR indicator is calculated. A longer period results in a smoother ATR value, providing a broader view of market volatility.

ATR Multiplier: The ATR multiplier enables users to adjust the sensitivity of the support and resistance zones. Increasing the multiplier widens the zones, while decreasing it narrows them, allowing traders to customize the indicator according to their trading preferences and market conditions.

🔶 Key Features

Trend Identification: The indicator identifies potential support and resistance zones based on the relationship between the ATR values and the price action. When the current ATR value exceeds a certain threshold determined by the ATR multiplier, it indicates a significant price movement, potentially signaling a trend reversal or continuation.

Impulse Detection: The indicator detects impulses in price movement by comparing the current ATR value with the previous value. An impulse is identified when the current ATR value is greater than or equal to the previous value, indicating a sudden surge in market volatility.

Bearish Impulse Example :

Bullish Impulse Example:

Color-Coded Impulses: Impulse candles are color-coded for easy visualization of bullish (green) and bearish (red) impulses. This feature helps traders quickly identify potential trading opportunities and market trends.

Wick Percentage Calculation: The indicator calculates the percentage of the wick length relative to the true range of each candle. Users can specify a threshold percentage, and when the wick percentage exceeds this threshold, it indicates a potential support or resistance zone.

Support and Resistance Zones: The indicator plots support and resistance zones based on the calculated wick percentage. These zones are visualized as rectangular boxes on the price chart, highlighting areas where price reversals or significant price movements are likely to occur.

Customizable Styling: Users can customize the styling of support and resistance zones, including line style, width, border color, and background color. This flexibility allows traders to adapt the indicator's visual appearance to their personal preferences and trading strategies.

🔶 Usage

Traders can utilize the ATR Based Support and Resistance Indicator in various ways :

Trend Direction Analysis: By observing the color-coded impulse candles, traders can identify the prevailing trend direction (bullish or bearish) based on the frequency and magnitude of impulses.

Entry and Exit Signals: Traders can use the detected support and resistance zones as potential entry and exit points for their trades. When price approaches these zones, it may indicate a trading opportunity or signal the need to adjust stop-loss or take-profit levels.

Confirmation Tool: The indicator serves as a confirmation tool for identifying potential reversal or continuation signals in conjunction with other technical indicators or trading strategies.

ATR Volatility and Trend AnalysisATR Volatility and Trend Analysis

Unlock the power of the Average True Range (ATR) with the ATR Volatility and Trend Analysis indicator. This comprehensive tool is designed to provide traders with a multi-faceted view of market dynamics, combining volatility analysis, dynamic support and resistance levels, and trend detection into a single, easy-to-use indicator.

How It Works

The ATR Volatility and Trend Analysis indicator is built upon the core concept of the ATR, a classic measure of market volatility. It expands on this by providing several key features:

Dynamic ATR Bands: The indicator plots three sets of upper and lower bands around the price. These bands are calculated by multiplying the current ATR value by user-defined multipliers. They act as dynamic support and resistance levels, widening during volatile periods and contracting during calm markets.

Volatility Breakout Signals: Identify potential breakouts with precision. The indicator generates a signal when the current ATR value surges above its own moving average by a specified threshold, indicating a significant increase in volatility that could lead to a strong price move.

Trend Detection: The indicator determines the market trend by analyzing both price action and ATR behavior. A bullish trend is signaled when the price is above its moving average and volatility is increasing. Conversely, a bearish trend is signaled when the price is below its moving average and volatility is increasing.

How to Use the ATR Multi-Band Indicator

Identify Support and Resistance: Use the ATR bands as key levels. Price approaching the outer bands may indicate overbought or oversold conditions, while a break of the bands can signal a strong continuation.

Confirm Breakouts: Look for a volatility breakout signal to confirm the strength behind a price move. A breakout from a consolidation range accompanied by a volatility signal is a strong indicator of a new trend.

Trade with the Trend: Use the background coloring and trend signals to align your trades with the dominant market direction. Enter long positions during confirmed bullish trends and short positions during bearish trends.

Set Up Alerts: The indicator includes alerts for band crosses, trend changes, and volatility breakouts, ensuring you never miss a potential trading opportunity.

What makes it different?

While many indicators use ATR, the ATR Volatility and Trend Analysis tool is unique in its integration of multiple ATR-based concepts into a single, cohesive system. It doesn't just show volatility; it interprets it in the context of price action to deliver actionable trend and breakout signals, making it a complete solution for ATR-based analysis.

Disclaimer

This indicator is designed as a technical analysis tool and should be used in conjunction with other forms of analysis and proper risk management.

Past performance does not guarantee future results, and traders should thoroughly test any strategy before implementing it with real capital.

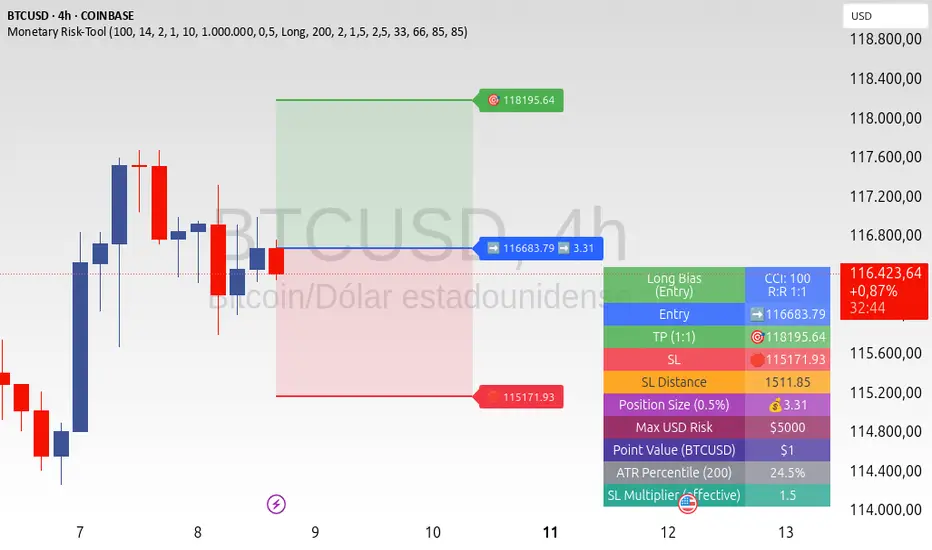

ATR+CCI Monetary Risk Tool - TP/SL⚙️ ATR+CCI Monetary Risk Tool — Volatility-aware TP/SL & Position Sizing

Exact prices (no rounding), ATR-percentile dynamic stops, and risk-budget sizing for consistent execution.

🧠 What this indicator is

A risk-first planning tool. It doesn’t generate orders; it gives you clean, objective levels (Entry, SL, TP) and position size derived from your risk budget. It shows only the latest setup to keep charts readable, and a compact on-chart table summarizing the numbers you actually act on.

✨ What makes it different

Dynamic SL by regime (ATR percentile): Instead of a fixed multiple, the SL multiplier adapts to the current volatility percentile (low / medium / high). That helps avoid tight stops in noisy markets and over-wide stops in quiet markets.

Risk budgeting, not guesswork: Size is computed from Account Balance × Max Risk % divided by SL distance × point value. You risk the same dollars across assets/timeframes.

Precision that matches your instrument: Entry, TP, SL, and SL Distance are displayed as exact prices (no rounding), truncated to syminfo.mintick so they align with broker/exchange precision.

Symbol-aware point value: Uses syminfo.pointvalue so you don’t maintain tick tables.

Non-repaint option: Work from closed bars to keep the plan stable.

🔧 How to use (quick start)

Add to chart and pick your timeframe and symbol.

In settings:

Set Account Balance (USD) and Max Risk per Trade (%).

Choose R:R (1:1 … 1:5).

Pick ATR Period and CCI Period (defaults are sensible).

Keep Dynamic ATR ON to adapt SL by regime.

Keep Use closed-bar values ON to avoid repaint when planning.

Read the labels (Entry/TP/SL) and the table (SL Distance, Position Size, Max USD Risk, ATR Percentile, effective SL Mult).

Combine with your entry trigger (price action, levels, momentum, etc.). This indicator handles risk & targets.

📐 How levels are computed

Bias: CCI ≥ 0 ⇒ long, otherwise short.

ATR Percentile: Percent rank of ATR(atrPeriod) over a lookback window.

Effective SL Mult:

If percentile < Low threshold ⇒ use Low SL Mult (tighter).

If between thresholds ⇒ use Base SL Mult.

If percentile > High threshold ⇒ use High SL Mult (wider).

Stop-Loss: SL = Entry ± ATR × SL_Mult (minus for long, plus for short).

Take-Profit: TP = Entry ± (Entry − SL) × R (R from the R:R dropdown).

Position Size:

USD Risk = Balance × Risk%

Contracts = USD Risk ÷ (|Entry − SL| × PointValue)

For futures, quantity is floored to whole contracts.

Exact prices: Entry/TP/SL and SL Distance are not rounded; they’re truncated to mintick so what you see matches valid price increments.

📊 What you’ll see on chart

Latest Entry (blue), TP (green), SL (red) with labels (optional emojis: ➡️ 🎯 🛑).

Info Table with:

Bias, Entry, TP, SL (exact, truncated to mintick)

SL Distance (exact, truncated)

Position Size (contracts/units)

Max USD Risk

Point Value

ATR Percentile and effective SL Mult

🧪 Practical examples

High-volatility session (e.g., XAUUSD, 1H): ATR percentile is high ⇒ wider SL, smaller size. Reduces churn from normal noise during macro events.

Range-bound market (e.g., EURUSD, 4H): ATR percentile low ⇒ tighter SL, better R:R. Helps you avoid carrying unnecessary risk.

Index swing planning (e.g., ES1!, Daily): Non-repaint levels + risk budgeting = consistent sizing across days/weeks, easier to review and journal.

🧭 Why traders should use it

Consistency: Same dollar risk regardless of instrument or volatility regime.

Clarity: One-trade view forces focus; you see the numbers that matter.

Adaptivity: Stops calibrated to the market’s current behavior, not last month’s.

Discipline: A visible checklist (SL distance, size, USD risk) before you hit buy/sell.

🔧 Input guide (practical defaults)

CCI Period: 100 by default; use as a bias filter, not an entry signal.

ATR Period: 14 by default; raise for smoother, lower for more reactive.

ATR Percentile Lookback: 200 by default (stable regime detection).

Percentile thresholds: 33/66 by default; widen the gap to change how often regimes switch.

SL Mults: Start ~1.5 / 2.0 / 2.5 (low/base/high). Tune by asset.

Risk % per trade: Common pro ranges are 0.25–1.0%; adjust to your risk tolerance.

R:R: Start with 1:2 or 1:3 for balanced skew; adapt to strategy edge.

Closed-bar values: Keep ON for planning/live; turn OFF only for exploration.

💡 Best practices

Combine with your entry logic (structure, momentum, liquidity levels).

Review ATR percentile and effective SL Mult across sessions so you understand regime shifts.

For futures, remember size is floored to whole contracts—safer by design.

Journal trades with the table snapshot to improve risk discipline over time.

⚠️ Notes & limitations

This is not a strategy; it does not place orders or alerts.

No slippage/commissions modeled here; build a strategy() version for backtests that mirror your broker/exchange.

Displayed non-price metrics use two decimals; prices and SL Distance are exact (truncated to mintick).

📎 Disclaimer

For educational purposes only. Not financial advice. Markets involve risk. Test thoroughly before trading live.

ATR Bands with Optional Risk/Reward Colors█ OVERVIEW

This indicator projects ATR bands and, optionally, colors them based on a risk/reward advantage for those who trade breakouts/breakdowns using moving averages as partial or full exit points.

█ DEFINITIONS

► True Range

The True Range is a measure of the volatility of a financial asset and is defined as the maximum difference among one of the following values:

- The high of the current period minus the low of the current period.

- The absolute value of the high of the current period minus the closing price of the previous period.

- The absolute value of the low of the current period minus the closing price of the previous period.

► Average True Range

The Average True Range was developed by J. Welles Wilder Jr. and was introduced in his 1978 book titled "New Concepts in Technical Trading Systems". It is calculated as an average of the true range values over a certain number of periods (usually 14) and is commonly used to measure volatility and set stop-loss and profit targets (1).

For example, if you are looking at a daily chart and you want to calculate the 14-day ATR, you would take the True Range of the previous 14 days, calculate their average, and this would be the ATR for that day. The process is then repeated every day to obtain a series of ATR values over time.

The ATR can be smoothed using different methods, such as the Simple Moving Average (SMA), the Exponential Moving Average (EMA), or others, depending on the user's preferences or analysis needs.

► ATR Bands

The ATR bands are created by adding or subtracting the ATR from a reference point (usually the closing price). This process generates bands around the central point that expand and contract based on market volatility, allowing traders to assess dynamic support and resistance levels and to adapt their trading strategies to current market conditions.

█ INDICATOR

► ATR Bands

The indicator provides all the essential parameters for calculating the ATR: period length, time frame, smoothing method, and multiplier.

It is then possible to choose the reference point from which to create the bands. The most commonly used reference points are Open, High, Low, and Close, but you can also choose the commonly used candle averages: HL2, HLC3, HLCC4, OHLC4. Among these, there is also a less common "OC2", which represents the average of the candle body. Additionally, two parameters have been specifically created for this indicator: Open/Close and High/Low.

With the "Open/Close" parameter, the upper band is calculated from the higher value between Open and Close, while the lower one is calculated from the lower value between Open and Close. In the case of bullish candles, therefore, the Close value is taken as the starting point for the upper band and the Open value for the lower one; conversely, in bearish candles, the Open value is used for the upper band and the Close value for the lower band. This setting can be useful for precautionally generating broader bands when trading with candlesticks like hammers or inverted hammers.

The "High/Low" parameter calculates the upper band starting from the High and the lower band starting from the Low. Among all the available options, this one allows drawing the widest bands.

Other possible options to improve the drawing of ATR bands, aligning them with the price action, are:

• Doji Smoothing: When the current candle is a doji (having the same Open and Close price), the bands assume the values they had on the previous candle. This can be useful to avoid steep fluctuations of the bands themselves.

• Extend to High/Low: Extends the bands to the High or Low values when they exceed the value of the band.

• Round Last Cent: Expands the upper band by one cent if the price ends with x.x9, and the lower band if the price ends with x.x1. This function only works when the asset's tick is 0.01.

► Risk/Reward Advantage

The indicator optionally colors the ATR bands after setting a breakpoint, one or two risk/reward ratios, and a series of moving averages. This function allows you to know in advance whether entering a trade can provide an advantage over the risk. The band is colored when the ratio between the distance from the break point to the band and the distance from the break point to the first available moving average reaches at least the set ratio value. It is possible to set two colorings, one for a minimum risk/reward ratio and one for an optimal risk/reward ratio.

The break point can be chosen between High/Low (High in case of breakout, Low in case of breakdown) or Open/Close (on breakouts, Close with bullish candles or Open with bearish candles; on breakdowns, Close with bearish candles or Open with bullish candles).

It is possible to choose up to 10 moving averages of various types, including the VWAP with the Anchor Period (2).

Depending on the "Price to MA" setting, the bands can be individually or simultaneously colored.

By selecting "Single Direction," the risk/reward calculation is performed only when all moving averages are above or below the break point, resulting in only one band being colored at a time. For this reason, when the break point is in between the moving averages, the calculation is not executed. This setting can be useful for strategies involving price movement from a level towards a series of specific moving averages (for example, in reversals starting from a certain level towards the VWAP with possible partial take profits on some previous moving averages, or simply in trend following towards one or more moving averages).

Choosing "Both Directions" the risk/reward ratio is calculated based on the first available moving averages both above and below the price. This setting is useful for those who operate in range bound markets or simply take advantage of movements between moving averages.

█ NOTE

This script may not be suitable for scalping strategies that require immediate entries due to the inability to know the ATR of a candle in advance until its closure. Once the candle is closed, you should have time to place a stop or stop-limit order, so your strategy should not anticipate an immediate start with the next candle. Even more conveniently, if your strategy involves an entry on a pullback, you can place a limit order at the breakout level.

(1) www.tradingview.com

(2) For convenience, the code for the Anchor Period has been entirely copied from the VWAP code provided by TradingView.

ATR Grid Levels [By MUQWISHI]▋ INTRODUCTION :

The “ATR Levels” produces a sequence of horizontal line levels above and below the Center Line (reference level). They are sized based on the instrument's volatility, representing the average historical price movement on a selected higher timeframe using the average true range (ATR) indicator.

_______________________

▋ OVERVIEW:

_______________________

▋ IMPLEMENTATION:

The indicator starts by drawing a Center Line that is selected by the user from a variety of common levels. Then, it draws a sequence of horizontal lines above and below the Center Line, which are sized based on the most confirmed average true range (ATR) at the selected higher timeframe.

In the top right corner of the chart, there is a table displaying both the selected ATR (in the right cell) and the ATR of the current bar (in the left cell). This feature enables users to compare these two values. It's important to note that the ATR of the current bar may not be confirmed yet, as the market is still active.