ATR Impact CandlesATR Impact Candles: Simplify Your Trading with Pure Price Action

You don’t need dozens of cluttered indicators to catch what really matters. With ATR Impact Candles, you get a powerful, single-tool solution that cuts through the noise by focusing on what truly drives the market: price action and volatility. This indicator highlights only those candlesticks that pack a punch—showing you when the market’s range is exceptionally strong relative to its recent behavior. Whether you’re a scalper or a swing trader, ATR Impact Candles empowers you to time your entries and exits with confidence, letting you trade based on real market momentum.

⸻

Indicator Overview

The indicator is designed for TradingView and is implemented in Pine Script (version 5). Its primary purpose is to highlight specific candles that meet a defined volatility condition based on the Average True Range (ATR). Instead of modifying every candle’s appearance, the indicator only changes the color of those “signal” candles that exceed a user-defined multiple of the ATR. The rest of the candles remain in their traditional black and white appearance—preserving the classic candlestick chart look.

⸻

Key Features

1. ATR-Based Signal Identification:

• ATR Calculation:

The indicator calculates the ATR using a configurable lookback period (default is 14 periods). The ATR is a common volatility measure that reflects the average range of price movement.

• Threshold Condition:

A candle is flagged as a signal if its range (high minus low) meets or exceeds a specified multiple (the “ATR Factor”) of the ATR. By default, this factor is set to 2, meaning any candle whose range is at least twice the ATR is considered significant.

2. Dynamic Candle Coloring:

• Signal Candles:

• When a candle meets the ATR threshold condition:

• Up Candles: are colored green.

• Down Candles: are colored red.

• Non-Signal Candles:

• Candles that do not meet the threshold condition retain their classic appearance:

• Up candles are white.

• Down candles are black.

3. User Configurability:

• ATR Period:

Traders can adjust the ATR period to tailor the volatility measure to different markets or timeframes.

• ATR Factor:

The multiple of the ATR that defines a signal candle is also configurable, giving flexibility to experiment with different thresholds for what constitutes “significant” price movement.

• Overlay Display:

The indicator runs in overlay mode on the chart, meaning it directly affects the appearance of the candlestick bars without interfering with other chart elements.

4. Additional Visual Aid:

• Threshold Line Plot:

The script optionally plots a line representing the ATR multiplied by the chosen factor. This line serves as a visual benchmark on the chart, allowing traders to see at what level the ATR threshold lies relative to the price action.

⸻

How It Works

1. ATR Calculation:

The indicator first calculates the Average True Range (ATR) for the defined period. This value is updated for each new candle.

2. Range Comparison:

For each candle, the indicator calculates the range (high - low) and compares it to the threshold, which is the ATR multiplied by the user-defined factor.

3. Conditional Coloring:

• If the Candle’s Range ≥ (ATR * Factor):

• The candle is marked as a “signal candle.”

• Its color is set to green if it is an up candle (close is greater than or equal to open) or red if it is a down candle.

• Otherwise:

• The candle retains its classic look, with up candles in white and down candles in black.

4. Chart Display:

By applying these rules to every candle, the indicator visually emphasizes those moments when the market shows unusually large price movements relative to its recent average volatility. This helps traders quickly spot potential breakouts or reversals.

⸻

Practical Applications

• Volatility Breakouts:

Identify candles that may signal the start of a breakout or strong reversal.

• Risk Management:

Adjust stop-loss levels or position sizes when unusually volatile candles are detected.

• Signal Confirmation:

Combine with other technical indicators or chart patterns to reinforce entry or exit decisions.

⸻

ATR Impact Candles is your essential, no-nonsense tool for filtering out market noise and focusing solely on significant price action. Simplify your trading decisions and harness the power of volatility with one clear, effective indicator.

Cari dalam skrip untuk "ATR"

EDUVEST UTBOT ADJ - Adaptive ATR Trailing StopEDUVEST UTBOT ADJ - Adaptive ATR Trailing Stop with Session-Based Sensitivity

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ ORIGINALITY

This indicator is an enhanced version of the classic UT Bot concept, featuring automatic session-based ATR sensitivity adjustment. Unlike the original UT Bot which uses a fixed sensitivity value, this version dynamically adapts to different trading sessions (Tokyo, London, New York) and automatically detects asset characteristics to optimize signal generation.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ WHAT IT DOES

- Generates BUY and SELL signals based on ATR trailing stop crossovers with a moving average

- Automatically adjusts sensitivity based on current trading session (Tokyo/London/NY)

- Auto-detects asset type and applies optimized parameters for each instrument

- Displays real-time session information and volatility status

- Provides alert functionality with customizable cooldown periods

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ HOW IT WORKS

【Core Logic: ATR Trailing Stop】

The indicator calculates an ATR-based trailing stop using the formula:

Trailing Stop = Price ± (Sensitivity × ATR)

When price is above the trailing stop and rising, the stop trails below price.

When price is below the trailing stop and falling, the stop trails above price.

【Signal Generation】

- BUY Signal: Price crosses above the trailing stop AND Moving Average crosses above the trailing stop

- SELL Signal: Price crosses below the trailing stop AND Moving Average crosses below the trailing stop

【Session-Based Sensitivity Adjustment】

The indicator adjusts ATR sensitivity based on trading session (JST timezone):

- Tokyo (08:00-15:00): Lower sensitivity (reduced by adjustment value) - typically quieter markets

- London (15:00-23:00): Base sensitivity - moderate volatility

- New York (23:00-08:00): Higher sensitivity (increased by adjustment value) - higher volatility

【Dynamic ATR Adjustment】

When enabled, the indicator compares current ATR to its smoothed average:

- ATR Ratio = Current ATR / SMA(ATR, smoothing period)

- Volatility Multiplier = 1.0 + (Sensitivity × (2.0 - ATR Ratio))

This reduces sensitivity during high volatility (fewer false signals) and increases sensitivity during low volatility (faster response).

【Auto Asset Detection】

The indicator automatically detects the traded instrument and applies optimized parameters:

- Stable pairs (USDJPY, EURUSD, USDCHF): Base sensitivity 1.5-1.8

- Moderate pairs (AUDUSD, USDCAD, EURJPY): Base sensitivity 2.0-2.3

- Volatile pairs (GBPUSD): Base sensitivity 2.8

- Commodities (GOLD/XAUUSD): Base sensitivity 3.5

- Indices (NASDAQ/NAS100): Base sensitivity 4.0

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ HOW TO USE

【Recommended Settings】

- Timeframe: 15 minutes or higher (15M, 1H, 4H recommended)

- Best performance on: Forex majors, Gold, NASDAQ

- Enable "Auto Asset Detection" for optimized parameters

【Entry Rules】

- BUY: Enter long when green BUY label appears

- SELL: Enter short when pink SELL label appears

【Session Panel】

The top-right panel displays:

- Current trading session (Tokyo/London/NY)

- Volatility status (High Chance/Medium Chance/Caution)

- Mode (AUTO/MANUAL)

【Alert Setup】

1. Enable "Viewer Alert Display" in settings

2. Set cooldown period (default: 15 minutes) to avoid signal spam

3. Create alert with "Any alert() function call" condition

【Important Notes】

- This indicator does not repaint - signals are confirmed at bar close

- Lower timeframes (1M, 5M) may generate excessive signals

- Always use proper risk management and confirm with other analysis

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ SETTINGS OVERVIEW

🎯 Alert Settings

- Viewer Alert Display: Enable/disable alert labels

- Cooldown Function: Prevent rapid consecutive signals

- Cooldown Time: Minutes between alerts (5-60)

🔧 Dynamic ATR Settings

- Enable Dynamic ATR: Auto-adjust based on volatility

- ATR Period: Calculation period (default: 14)

- ATR Smoothing: Smoothing period for ratio calculation

- Volatility Sensitivity: How much to adjust (0.1-1.0)

🕐 Session ATR Adjustment

- Enable Time Adjustment: Session-based sensitivity

- Show Session Info: Display session panel

📊 Asset Settings

- Auto Asset Detection: Automatically optimize for instrument

- Manual settings available when auto-detection is disabled

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

█ CREDITS

Based on the original UT Bot concept by QuantNomad.

Enhanced with session-based adaptation and auto-asset detection by EduVest.

License: Mozilla Public License 2.0

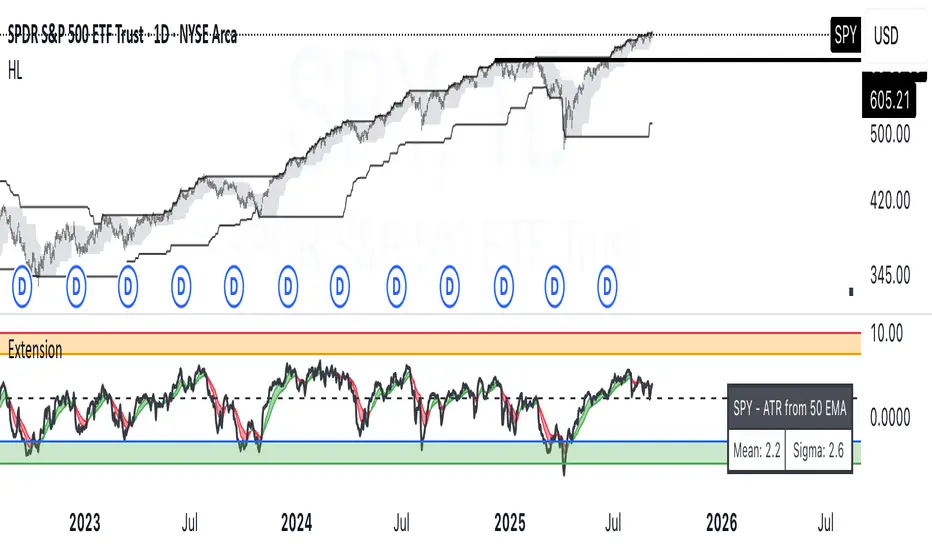

ATR Extension from Moving Average, with Robust Sigma Bands

# ATR Extension from Moving Average, with Robust Sigma Bands

**What it does**

This indicator measures how far price is from a selected moving average, expressed in **ATR multiples**, then overlays **robust sigma bands** around the long run central tendency of that extension. Positive values mean price is extended above the MA, negative values mean price is extended below the MA. The signal adapts to volatility through ATR, which makes comparisons consistent across symbols and regimes.

**Why it can help**

* Normalizes distance to an MA by ATR, which controls for changing volatility

* Uses the **bar’s extreme** against the MA, not just the close, so it captures true stretch

* Computes a **median** and **standard deviation** of the extension over a multi-year window, which yields simple, intuitive bands for trend and mean-reversion decisions

---

## Inputs

* **MA length**: default 50, options 200, 64, 50, 20, 9, 4, 3

* **MA timeframe**: Daily or Weekly. The MA is computed on the chosen higher timeframe through `request.security`.

* **MA type**: EMA or SMA

* **Years lookback**: 1 to 10 years, default 5. This sets the sample for the median and sigma calculation, `years * 365` bars.

* **Line width**: visual width of the plotted extension series

* **Table**: optional on-chart table that displays the current long run **median** and **sigma** of the extension, with selectable text size

**Fixed parameters in this release**

* **ATR length**: 20 on the daily timeframe

* **ATR type**: classic ATR. ADR percent is not enabled in this version.

---

## Plots and colors

* **Main plot**: “Extension from 50d EMA” by default. Value is in **ATR multiples**.

* **Reference lines**:

* `median` line, black dashed

* +2σ orange, +3σ red

* −2σ blue, −3σ green

---

## How it is calculated

1. **Moving average** on the selected higher timeframe: EMA or SMA of `close`.

2. **Extreme-based distance** from MA, as a percent of price:

* If `close > MA`, use `(high − MA) / close * 100`

* Else, use `(low − MA) / close * 100`

3. **ATR percent** on the daily timeframe: `ATR(20) / close * 100`

4. **ATR multiples**: extension percent divided by ATR percent

5. **Robust center and spread** over the chosen lookback window:

* Center: **median** of the ATR-multiple series

* Spread: **standard deviation** of that series

* Bands: center ± 1σ, 2σ, 3σ, with 2σ and 3σ drawn

This design yields an intuitive unit scale. A value of **+2.0** means price is about 2 ATR above the selected MA by the most stretched side of the current bar. A value of **−3.0** means roughly 3 ATR below.

---

## Practical use

* **Trend continuation**

* Sustained readings near or above **+1σ** together with a rising MA often signal healthy momentum.

* **Mean reversion**

* Spikes into **±2σ** or **±3σ** can identify stretched conditions for fade setups in range or late-trend environments.

* **Regime awareness**

* The **median** moves slowly. When median drifts positive for many months, the market spends more time extended above the MA, which often marks bullish regimes. The opposite applies in bearish regimes.

**Notes**

* The MA can be set to Weekly while ATR remains Daily. This is deliberate, it keeps the normalization stable for most symbols.

* On very short intraday charts, the extension remains meaningful since it references the session’s extreme against a higher-timeframe MA and a daily ATR.

* Symbols with short histories may not fill the lookback window. Bands will adapt as data accrues.

---

## Table overlay

Enable **Table → Show** to see:

* “ATR from \”

* Current **median** and **sigma** of the extension series for your lookback

---

## Recommended settings

* **Swing equities**: 50 EMA on Daily, 5 to 7 years

* **Index trend work**: 200 EMA on Daily, 10 years

* **Position trading**: 20 or 50 EMA on Weekly MA, 5 to 10 years

---

## Interpretation examples

* Reading **+2.7** with price above a rising 50 EMA, near prior highs

* Strong trend extension, consider pyramiding in trend systems or waiting for a pullback if you are a mean-reverter.

* Reading **−2.2** into multi-month support with flattening MA

* Stretch to the downside that often mean-reverts, size entries based on your system rules.

---

## Credits

The concept of measuring stretch from a moving average in ATR units has a rich community history. This implementation and its presentation draw on ideas popularized by **Jeff Sun**, **SugarTrader**, and **Steve D Jacobs**. Thanks to each for their contributions to ATR-based extension thinking.

---

## License

This script and description are distributed under **MPL-2.0**, consistent with the header in the source code.

---

## Changelog

* **v1.0**: Initial public release. Daily ATR normalization, EMA or SMA on D or W timeframe, robust median and sigma bands, optional table.

---

## Disclaimer

This tool is for educational use only. It is not financial advice. Always test on your own data and strategies, then manage risk accordingly.

Multiple ATR Lines with Current Price PercentageThis indicator plots multiple lines based on the Average True Range (ATR) on the chart, helping traders identify potential support and resistance levels. Specifically, it draws three lines above the price and three lines below the price at different multiples of the ATR. Additionally, it plots a dynamic line at the current price level, which shows how much percentage of the ATR the current price has traveled from a specific point.

How it works:

ATR-Based Lines: The indicator calculates three upper and three lower levels based on the ATR of the selected period. These levels represent 1x, 2x, and 3x ATR above and below the current price.

Current Price Line: A dotted line follows the current price, displaying the percentage of the ATR that the price has moved.

Labels: Each line is labeled with its respective ATR multiple (1x ATR, 2x ATR, 3x ATR), and the current price line shows the percentage of the ATR traveled.

Use Cases:

Identifying Market Volatility: Traders can use this indicator to see how far the price has moved relative to its average volatility.

Support and Resistance Levels: The ATR lines can be treated as potential support and resistance zones, providing insight into price targets or stop-loss placement.

Dynamic Tracking: The percentage of ATR traveled helps traders understand the market momentum relative to its historical volatility.

Settings:

ATR Length: The user can adjust the length of the ATR calculation period.

ATR Multiplier: A multiplier to adjust the distance of the lines relative to the ATR.

Advantages:

Clear visualization of market volatility through ATR-based levels.

Real-time tracking of the price’s movement relative to ATR, giving traders a better understanding of price action.

Customizable settings for different trading styles.

Adaptive EMA with ATR and Standard Deviation [QuantAlgo]Adaptive EMA with ATR and Standard Deviation by QuantAlgo 📈✨

Introducing the Adaptive EMA with ATR and Standard Deviation , a comprehensive trend-following indicator designed to combine the smoothness of an Exponential Moving Average (EMA) with the volatility adjustments of Average True Range (ATR) and Standard Deviation. This synergy allows traders and investors to better identify market trends while accounting for volatility, delivering clearer signals in both trending and volatile market conditions. This indicator is suitable for traders and investors seeking to balance trend detection and volatility management, offering a robust and adaptable approach across various asset classes and timeframes.

💫 Core Concept and Innovation

The Adaptive EMA with ATR and Standard Deviation brings together the trend-smoothing properties of the EMA and the volatility sensitivity of ATR and Standard Deviation. By using the EMA to track price movements over time, the indicator smooths out minor fluctuations while still providing valuable insights into overall market direction. However, market volatility can sometimes distort simple moving averages, so the ATR and Standard Deviation components dynamically adjust the trend signals, offering more nuanced insights into trend strength and reversals. This combination equips traders with a powerful tool to navigate unpredictable markets while minimizing false signals.

📊 Technical Breakdown and Calculations

The Adaptive EMA with ATR and Standard Deviation relies on three key technical components:

1. Exponential Moving Average (EMA): The EMA forms the base of the trend detection. Unlike a Simple Moving Average (SMA), the EMA gives more weight to recent price changes, allowing it to react more quickly to new data. Users can adjust the length of the EMA to make it more or less responsive to price movements.

2. Standard Deviation Bands: These bands are calculated from the standard deviation of the EMA and represent dynamic volatility thresholds. The upper and lower bands expand or contract based on recent price volatility, providing more accurate signals in both calm and volatile markets.

3. ATR-Based Volatility Filter: The Average True Range (ATR) is used to measure market volatility over a user-defined period. It helps refine the trend signals by filtering out false positives caused by minor price swings. The ATR filter ensures that the indicator only signals significant market movements.

⚙️ Step-by-Step Calculation:

1. EMA Calculation: First, the indicator calculates the EMA over a specified period based on the chosen price source (e.g., close, high, low).

2. Standard Deviation Bands: Then, it computes the standard deviation of the EMA and applies a multiplier to create upper and lower bands around the EMA. These bands adjust dynamically with the level of market volatility.

3. ATR Filtering: In addition to the standard deviation bands, the ATR is applied as a secondary filter to help refine the trend signals. This step helps eliminate signals generated by short-term price spikes or corrections, ensuring that the signals are more reliable.

4. Trend Detection: When the price crosses above the upper band, a bullish trend is identified, while a move below the lower band signals a bearish trend. The system accounts for both the standard deviation and ATR bands to generate these signals.

✅ Customizable Inputs and Features

The Adaptive EMA with ATR and Standard Deviation provides a range of customizable options to fit various trading/investing styles:

📈 Trend Settings:

1. Price Source: Choose the price type (e.g., close, high, low) to base the EMA calculation on, influencing how the trend is tracked.

2. EMA Length: Adjust the length to control how quickly the EMA reacts to price changes. A shorter length provides a more responsive EMA, while a longer period smooths out short-term fluctuations.

🌊 Volatility Controls:

1. Standard Deviation Multiplier: This parameter controls the sensitivity of the trend detection by adjusting the distance between the upper and lower bands from the EMA.

2. TR Length and Multiplier: Fine-tune the ATR settings to control how volatility is filtered, adjusting the indicator’s responsiveness during high or low volatility phases.

🎨 Visualization and Alerts:

1. Bar Coloring: Select different colors for uptrends and downtrends, providing a clear visual cue when trends change.

2. Alerts: Set up alerts to notify you when the price crosses the upper or lower bands, signaling a potential long or short trend shift. Alerts can help you stay informed without constant chart monitoring.

📈 Practical Applications

The Adaptive EMA with ATR and Standard Deviation is ideal for traders and investors looking to balance trend-following strategies with volatility management. Key uses include:

Detecting Trend Reversals: The dynamic bands help identify when the market shifts direction, providing clear signals when a trend reversal is likely.

Filtering Market Noise: By applying both Standard Deviation and ATR filtering, the indicator helps reduce false signals during periods of heightened volatility.

Volatility-Based Risk Management: The adaptability of the bands ensures that traders can manage risk more effectively by responding to shifts in volatility while keeping focus on long-term trends.

⭐️ Comprehensive Summary

The Adaptive EMA with ATR and Standard Deviation is a highly customizable indicator that provides traders with clearer signals for trend detection and volatility management. By dynamically adjusting its calculations based on market conditions, it offers a powerful tool for navigating both trending and volatile markets. Whether you're looking to detect early trend reversals or avoid false signals during periods of high volatility, this indicator gives you the flexibility and accuracy to improve your trading and investing strategies.

Note: The Adaptive EMA with ATR and Standard Deviation is designed to enhance your market analysis but should not be relied upon as the sole basis for trading or investing decisions. Always combine it with other analytical tools and practices. No statements or signals from this indicator constitute financial advice. Past performance is not indicative of future results.

VIX, ATR, and Volatility Indicatorhere what the indictor do !

The "VIX, ATR, and Volatility Indicator" combines the Volatility Index (VIX), Average True Range (ATR), and moving averages to provide insights into market volatility.

VIX (Volatility Index):

The VIX measures the expected volatility in the market over the next 30 days. A higher VIX value indicates increased market volatility, while a lower value suggests lower volatility.

ATR (Average True Range):

The ATR is a technical indicator that measures the average range between high and low prices over a specified period. It provides a sense of the market's volatility by considering price movements. Higher ATR values indicate greater volatility, while lower values indicate lower volatility.

Moving Averages:

The indicator calculates both an Exponential Moving Average (EMA) and Simple Moving Average (SMA) with a specific period (e.g., 50).

Moving averages smooth out price data to identify trends and potential areas of support or resistance.

Volatility Detection:

By comparing the current closing price to the EMA and SMA, the indicator determines if there is high volatility.

If the current closing price is higher than either the EMA or SMA, it indicates potential high volatility.

Visualization:

The VIX and ATR are typically plotted on the chart, providing a visual representation of market volatility and price range.

Additionally, markers or labels may be used to highlight periods of high volatility when the current price exceeds the moving averages.

what are the VIX and ATR

Volatility Index (VIX):

Monitor the VIX value from financial platforms or market data providers. A higher VIX value indicates increased market volatility, suggesting potential trading opportunities. Conversely, a lower VIX value indicates lower volatility, which may influence your trading strategy.

Average True Range (ATR):

Calculate the ATR manually or use charting platforms that provide ATR as an indicator.

Plot the ATR on your trading chart to visualize the range of price movements.

Determine suitable entry and exit points based on ATR values. For example, higher ATR values may indicate larger potential price swings, while lower ATR values may suggest a more stable market.

how it work

Fetching VIX Data:

The request.security function is used to fetch the daily VIX data from the "CBOE:VIX" symbol. It retrieves the closing price of the VIX for each day.

Calculating ATR:

The ta.atr function calculates the Average True Range (ATR) with a period of 14. ATR measures the average range between the high and low prices over the specified period, providing an indication of market volatility.

Calculating Moving Averages:

Two types of moving averages are calculated: Exponential Moving Average (EMA) and Simple Moving Average (SMA). Both moving averages are calculated using a period of 50, but you can adjust the period as needed.

The ta.ema function calculates the Exponential Moving Average, which places greater weight on recent prices.

The ta.sma function calculates the Simple Moving Average, which gives equal weight to all prices in the period.

Identifying High Volatility:

The indicator determines if there is high volatility by comparing the current closing price to both the EMA and SMA.

If the current closing price is higher than either the EMA or SMA, the isHighVolatility variable is set to true, indicating potential high volatility.

Plotting the Indicators:

The VIX and ATR are plotted using the plot function, assigning colors and line widths for visual differentiation.

The plotshape function is used to plot markers below the bars to indicate highly volatile periods. The isHighVolatility variable determines when the markers appear.

% / ATR Buy, Target, Stop + Overlay & P/L% / ATR Buy, Target, Stop + Overlay & P/L

This tool combines volatility‑based and fixed‑percentage trade planning into a single, on‑chart overlay—with built‑in profit‑and‑loss estimates. Toggle between ATR or percentage modes, plot your Buy, Target and Stop levels, and see the dollar gain or loss for a specified position size—all in one interactive table and chart display.

NOTE: To activate plotted lines, price labels, P/L rows and table values, enter a Buy Price greater than zero.

What It Does

Mode Toggle: Choose between “ATR” (volatility‑based) or “%” (fixed‑percentage) calculations.

Buy Price Input: Manually enter your entry price.

ATR Mode:

Target = Buy + (ATR × Target Multiplier)

Stop = Buy − (ATR × Stop Multiplier)

Percentage Mode:

Target = Buy × (1 + Target % / 100)

Stop = Buy × (1 – Stop % / 100)

P/L Estimates: Specify a dollar amount to “invest” at your Buy price, and the script calculates:

Gain ($): Profit if Target is hit

Loss ($): Cost if Stop is hit

Visual Overlay: Draws horizontal lines for Buy, Target and Stop, with optional price labels on the chart scale.

Interactive Table: Displays Buy, Target, Stop, ATR/timeframe info (in ATR mode), percentages (in % mode), and P/L rows.

Customization Options

Line Settings:

Choose color, style (solid/dashed/dotted), and width for Buy, Target, Stop lines.

Extend lines rightward only or in both directions.

Table Settings:

Position the table (top/bottom × left/right).

Toggle individual rows: Buy Price; Target (multiplier or %); Stop (multiplier or %); Target ATR %; Stop ATR %; ATR Time Frame; ATR Value; Gain ($); Loss ($).

Customize text colors for each row and background transparency.

General Inputs:

ATR length and optional ATR timeframe override (e.g. use daily ATR on an intraday chart).

Target/Stop multipliers or percentages.

Dollar Amount for P/L calculations.

How to Use It for Trading

Plan Your Entry: Enter your intended Buy Price and position size (dollar amount).

Select Mode: Toggle between ATR or % mode depending on whether you prefer volatility‑based or fixed offsets.

Assess R:R and P/L: Instantly see your Target, Stop levels, and potential profit or loss in dollars.

Visual Reference: Lines and price labels update in real time as you tweak inputs—ideal for live trading, backtesting or trade journaling.

Ideal For

Traders who want both volatility‑based and percentage‑based exit options in one tool

Those who need on‑chart P/L estimates based on position size

Swing and intraday traders focused on objective, rule‑based trade management

Anyone who uses ATR for adaptive stops/targets or fixed percentages for simpler exits

Multi-Timeframe ATR Levels by Hitesh2603Description:

"Multi-Timeframe ATR Levels by Hitesh2603" is a versatile and adaptive indicator designed to help traders identify key price levels based on the Average True Range (ATR) from a higher timeframe. The script automatically adapts to the current chart’s timeframe and allows you to customize the higher timeframe for ATR calculations, making it ideal for intraday and swing trading strategies.

The indicator plots upper and lower price levels based on the ATR multiplier, providing clear visual cues for potential profit-taking or exit points. It also includes features like editable timeframe presets , historical level plotting , labels , and alerts , making it a powerful tool for traders of all experience levels.

---

Key Features:

1. Automatic Timeframe Adaptation : - The script automatically detects the current chart’s timeframe and selects the appropriate higher timeframe for ATR calculations.

2. Editable Preset Timeframe Pairs : - Customize the higher timeframe for each chart timeframe directly in the indicator settings.

3. Dynamic ATR-Based Levels :- Plots upper and lower price levels using the formula:

- Upper Level = Current Candle Open + (Previous Candle ATR * Multiplier)

- Lower Level = Current Candle Open - (Previous Candle ATR * Multiplier)

4. Customizable Inputs :

- Adjust ATR length, multiplier, line length, colors, and more.

5. Labels :

- Displays the exact values of the upper and lower levels for easy reference.

6. Historical Levels :

- Optionally plots historical levels for all candles.

7. Alerts :

- Get notified when the price crosses the upper or lower levels.

---

Use Cases:

1. Intraday Trading :

- Use the script on a 5-minute or 15-minute chart with a 1-hour higher timeframe to identify intraday profit-taking or exit points.

2. Swing Trading :

- Use the script on a 1-hour or 4-hour chart with a daily higher timeframe to identify swing trading opportunities.

3. Position Trading :

- Use the script on a daily chart with a weekly higher timeframe to identify key levels for position trading.

4. Breakout Confirmation :

- Use the upper and lower levels as confirmation points for breakouts or reversals.

5. Risk Management :

- Use the levels to set stop-loss or take-profit targets based on market volatility.

---

How to Use:

1. Add the Script to Your Chart :

- Search for "Multi-Timeframe ATR Levels by Hitesh2603" in the TradingView indicator library and add it to your chart.

2. Customize the Settings :

- Adjust the inputs (e.g., ATR length, multiplier, line length, colors, etc.) to suit your trading strategy.

3. Set the Higher Timeframe :

- The script will automatically display an input for the higher timeframe based on the current chart’s timeframe. Customize it as needed.

4. Interpret the Levels :

- The script will plot two horizontal lines (upper and lower levels) on the chart. Use these levels for profit-taking, exits, or breakout confirmation.

5. Enable Alerts :

- Set up alerts to get notified when the price crosses the upper or lower levels.

---

Input Parameters:

1. ATR Length :

- The period used to calculate the ATR (default: 14).

2. ATR Multiplier :

- The multiplier applied to the ATR to calculate the levels (default: 0.65).

3. Line Length :

- The number of candles to extend the lines (default: 10).

4. Show Labels :

- Toggle to display the exact values of the levels (default: true).

5. Show Historical Levels :

- Toggle to plot historical levels for all candles (default: false).

6. Line Colors :

- Customize the colors of the upper and lower levels.

7. Line Width :

- Adjust the thickness of the lines (default: 2).

---

Example:

- Current Chart : 5-minute

- Higher Timeframe : 1-hour

- Previous Hour’s ATR : 4.6

- Current Hour’s Open : 102

- Multiplier : 0.65

Levels :

- Upper Level = 102 + (4.6 * 0.65) = 105.0

- Lower Level = 102 - (4.6 * 0.65) = 99.0

The script will plot horizontal lines at 105.0 and 99.0 on the 5-minute chart.

---

Alerts:

- Price Crosses Upper Level :

- Triggered when the price crosses above the upper level.

- Price Crosses Lower Level :

- Triggered when the price crosses below the lower level.

---

Notes:

- The script is designed to be flexible and adaptable to various trading styles and timeframes.

- Always backtest and validate the indicator with your trading strategy before using it in live trading.

---

Credits:

- Developed by Hitesh2603 .

- Special thanks to the TradingView community for inspiration and support.

[SHORT ONLY] ATR Sell the Rip Mean Reversion Strategy█ STRATEGY DESCRIPTION

The "ATR Sell the Rip Mean Reversion Strategy" is a contrarian system that targets overextended price moves on stocks and ETFs. It calculates an ATR‐based trigger level to identify shorting opportunities. When the current close exceeds this smoothed ATR trigger, and if the close is below a 200-period EMA (if enabled), the strategy initiates a short entry, aiming to profit from an anticipated corrective pullback.

█ HOW IS THE ATR SIGNAL BAND CALCULATED?

This strategy computes an ATR-based signal trigger as follows:

Calculate the ATR

The strategy computes the Average True Range (ATR) using a configurable period provided by the user:

atrValue = ta.atr(atrPeriod)

Determine the Threshold

Multiply the ATR by a predefined multiplier and add it to the current close:

atrThreshold = close + atrValue * atrMultInput

Smooth the Threshold

Apply a Simple Moving Average over a specified period to smooth out the threshold, reducing noise:

signalTrigger = ta.sma(atrThreshold, smoothPeriodInput)

█ SIGNAL GENERATION

1. SHORT ENTRY

A Short Signal is triggered when:

The current close is above the smoothed ATR signal trigger.

The trade occurs within the specified trading window (between Start Time and End Time).

If the EMA filter is enabled, the close must also be below the 200-period EMA.

2. EXIT CONDITION

An exit Signal is generated when the current close falls below the previous bar’s low (close < low ), indicating a potential bearish reversal and prompting the strategy to close its short position.

█ ADDITIONAL SETTINGS

ATR Period: The period used to calculate the ATR, allowing for adaptability to different volatility conditions (default is 20).

ATR Multiplier: The multiplier applied to the ATR to determine the raw threshold (default is 1.0).

Smoothing Period: The period over which the raw ATR threshold is smoothed using an SMA (default is 10).

Start Time and End Time: Defines the time window during which trades are allowed.

EMA Filter (Optional): When enabled, short entries are only executed if the current close is below the 200-period EMA, confirming a bearish trend.

█ PERFORMANCE OVERVIEW

This strategy is designed for use on the Daily timeframe, targeting stocks and ETFs by capitalizing on overextended price moves.

It utilizes a dynamic, ATR-based trigger to identify when prices have potentially peaked, setting the stage for a mean reversion short entry.

The optional EMA filter helps align trades with broader market trends, potentially reducing false signals.

Backtesting is recommended to fine-tune the ATR multiplier, smoothing period, and EMA settings to match the volatility and behavior of specific markets.

CCI+EMA Strategy with Percentage or ATR TP/SL [Alifer]This is a momentum strategy based on the Commodity Channel Index (CCI), with the aim of entering long trades in oversold conditions and short trades in overbought conditions.

Optionally, you can enable an Exponential Moving Average (EMA) to only allow trading in the direction of the larger trend. Please note that the strategy will not plot the EMA. If you want, for visual confirmation, you can add to the chart an Exponential Moving Average as a second indicator, with the same settings used in the strategy’s built-in EMA.

The strategy also allows you to set internal Stop Loss and Take Profit levels, with the option to choose between Percentage-based TP/SL or ATR-based TP/SL.

The strategy can be adapted to multiple assets and timeframes:

Pick an asset and a timeframe

Zoom back as far as possible to identify meaningful positive and negative peaks of the CCI

Set Overbought and Oversold at a rough average of the peaks you identified

Adjust TP/SL according to your risk management strategy

Like the strategy? Give it a boost!

Have any questions? Leave a comment or drop me a message.

CAUTIONARY WARNING

Please note that this is a complex trading strategy that involves several inputs and conditions. Before using it in live trading, it is highly recommended to thoroughly test it on historical data and use risk management techniques to safeguard your capital. After backtesting, it's also highly recommended to perform a first live test with a small amount. Additionally, it's essential to have a good understanding of the strategy's behavior and potential risks. Only risk what you can afford to lose .

USED INDICATORS

1 — COMMODITY CHANNEL INDEX (CCI)

The Commodity Channel Index (CCI) is a technical analysis indicator used to measure the momentum of an asset. It was developed by Donald Lambert and first published in Commodities magazine (now Futures) in 1980. Despite its name, the CCI can be used in any market and is not just for commodities. The CCI compares current price to average price over a specific time period. The indicator fluctuates above or below zero, moving into positive or negative territory. While most values, approximately 75%, fall between -100 and +100, about 25% of the values fall outside this range, indicating a lot of weakness or strength in the price movement.

The CCI was originally developed to spot long-term trend changes but has been adapted by traders for use on all markets or timeframes. Trading with multiple timeframes provides more buy or sell signals for active traders. Traders often use the CCI on the longer-term chart to establish the dominant trend and on the shorter-term chart to isolate pullbacks and generate trade signals.

CCI is calculated with the following formula:

(Typical Price - Simple Moving Average) / (0.015 x Mean Deviation)

Some trading strategies based on CCI can produce multiple false signals or losing trades when conditions turn choppy. Implementing a stop-loss strategy can help cap risk, and testing the CCI strategy for profitability on your market and timeframe is a worthy first step before initiating trades.

2 — AVERAGE TRUE RANGE (ATR)

The Average True Range (ATR) is a technical analysis indicator that measures market volatility by calculating the average range of price movements in a financial asset over a specific period of time. The ATR was developed by J. Welles Wilder Jr. and introduced in his book “New Concepts in Technical Trading Systems” in 1978.

The ATR is calculated by taking the average of the true range over a specified period. The true range is the greatest of the following:

The difference between the current high and the current low.

The difference between the previous close and the current high.

The difference between the previous close and the current low.

The ATR can be used to set stop-loss orders. One way to use ATR for stop-loss orders is to multiply the ATR by a factor (such as 2 or 3) and subtract it from the entry price for long positions or add it to the entry price for short positions. This can help traders set stop-loss orders that are more adaptive to market volatility.

3 — EXPONENTIAL MOVING AVERAGE (EMA)

The Exponential Moving Average (EMA) is a type of moving average (MA) that places a greater weight and significance on the most recent data points.

The EMA is calculated by taking the average of the true range over a specified period. The true range is the greatest of the following:

The difference between the current high and the current low.

The difference between the previous close and the current high.

The difference between the previous close and the current low.

The EMA can be used by traders to produce buy and sell signals based on crossovers and divergences from the historical average. Traders often use several different EMA lengths, such as 10-day, 50-day, and 200-day moving averages.

The formula for calculating EMA is as follows:

Compute the Simple Moving Average (SMA).

Calculate the multiplier for weighting the EMA.

Calculate the current EMA using the following formula:

EMA = Closing price x multiplier + EMA (previous day) x (1-multiplier)

STRATEGY EXPLANATION

1 — INPUTS AND PARAMETERS

The strategy uses the Commodity Channel Index (CCI) with additional options for an Exponential Moving Average (EMA), Take Profit (TP) and Stop Loss (SL).

length : The period length for the CCI calculation.

overbought : The overbought level for the CCI. When CCI crosses above this level, it may signal a potential short entry.

oversold : The oversold level for the CCI. When CCI crosses below this level, it may signal a potential long entry.

useEMA : A boolean input to enable or disable the use of Exponential Moving Average (EMA) as a filter for long and short entries.

emaLength : The period length for the EMA if it is used.

2 — CCI CALCULATION

The CCI indicator is calculated using the following formula:

(src - ma) / (0.015 * ta.dev(src, length))

src is the typical price (average of high, low, and close) and ma is the Simple Moving Average (SMA) of src over the specified length.

3 — EMA CALCULATION

If the useEMA option is enabled, an EMA is calculated with the given emaLength .

4 — TAKE PROFIT AND STOP LOSS METHODS

The strategy offers two methods for TP and SL calculations: percentage-based and ATR-based.

tpSlMethod_percentage : A boolean input to choose the percentage-based method.

tpSlMethod_atr : A boolean input to choose the ATR-based method.

5 — PERCENTAGE-BASED TP AND SL

If tpSlMethod_percentage is chosen, the strategy calculates the TP and SL levels based on a percentage of the average entry price.

tp_percentage : The percentage value for Take Profit.

sl_percentage : The percentage value for Stop Loss.

6 — ATR-BASED TP AND SL

If tpSlMethod_atr is chosen, the strategy calculates the TP and SL levels based on Average True Range (ATR).

atrLength : The period length for the ATR calculation.

atrMultiplier : A multiplier applied to the ATR to set the SL level.

riskRewardRatio : The risk-reward ratio used to calculate the TP level.

7 — ENTRY CONDITIONS

The strategy defines two conditions for entering long and short positions based on CCI and, optionally, EMA.

Long Entry: CCI crosses below the oversold level, and if useEMA is enabled, the closing price should be above the EMA.

Short Entry: CCI crosses above the overbought level, and if useEMA is enabled, the closing price should be below the EMA.

8 — TP AND SL LEVELS

The strategy calculates the TP and SL levels based on the chosen method and updates them dynamically.

For the percentage-based method, the TP and SL levels are calculated as a percentage of the average entry price.

For the ATR-based method, the TP and SL levels are calculated using the ATR value and the specified multipliers.

9 — EXIT CONDITIONS

The strategy defines exit conditions for both long and short positions.

If there is a long position, it will be closed either at TP or SL levels based on the chosen method.

If there is a short position, it will be closed either at TP or SL levels based on the chosen method.

Additionally, positions will be closed if CCI crosses back above oversold in long positions or below overbought in short positions.

10 — PLOTTING

The script plots the CCI line along with overbought and oversold levels as horizontal lines.

The CCI line is colored red when above the overbought level, green when below the oversold level, and white otherwise.

The shaded region between the overbought and oversold levels is plotted as well.

Scalper's toolkit - ATR WidgetWidget specifically designed for scalping. Many settings to fit the instrument and view preferences to make it fit into your chart window how you like, even on mobile.

** I have 5 other features to add into this in the very near future, as I use this as my primary tool for Risk reward. This script will be updated in the near future as more features are coded into it. See bottom for notes on plans

Features:

Displays a quick view of the ATR value on the chart, in decimal PIPs or directly in Points - a key value for scalping using the DOM for point value settings and one click trading on fast time frames.

Automatic calculation of stop and target distance for a predetermined Risk Reward Ratio (Set with the settings panel), and then also displayed in PIPs or Points for easy use in quick trading.

Works on most all instruments/pairs/cryptos with multiple precision levels for correct values to be shown in the widget.

Fully customizable -

ATR period Base setting, just like a normal ATR indicator

Display in : PIPs or Points

ATR based stop distance, using a multiplier. 2 is the most common multiplier used, and the default setting.

Risk Reward Calculation using the Stop Loss value.

-Quickly helps with proper target and stop sizing for the volatility in the price on the current trade entry point.

-Set to any ratio you wish, from 1:0.1 all the way to 1:100 or more, unlimited R ratio settings to fit your strategy and risk tolerances.

Position anywhere on the chart window with 9 preset locations available (Pine script limitation)

Show as a column layout or a row layout

Customize the Size, with 5 preset widget sizes, from tiny to huge (Pine script limitation)

-Mobile Friendly - Tiny or Small may be too small on PC, but can be used for Mobile so the widget does not become too large over the chart.

Custom text, background, and boarder colors

Custom Boarder Size - 0 size is no boarder

Set up:

-Open the settings panel.

First section is the basic settings for the ATR - the length (Default is 14) and to use a PIP value display, or Point value display.

Here you also see a "Precision" Setting. **Because each instrument returns different precision ATR values, it is difficult to determine with code what those values will be ahead of time to do the math in the background. Even some 2 decimal instruments return 5 decimal ATR values, so this setting filters that** Just use the dropdown and choose how many decimal places the instrument has from 2 - 5 decimals

The second section is for risk and reward calculations, and can be disabled if you do not want to see these values.

The first value is the "ATR Multiplier" Typically, a 2x multiplier is used on the ATR to determine how far away to place your stop loss from the entry, placing it out of harm's way from normal market activity.

The second value is the Reward target distance, based from the stop loss size. This quickly calculates your target to match your intended reward ratio, saving some manual work to calculate this by hand every trade.

** Note: because of the math used in the code, you may see odd values on some instruments, like indexes. If you have the precision correct, try changing the "Show in Pips" to "Show in Points", as this may solve the issue.

The last two sections are purely for how the widget looks and how/where it shows on the screen. These can be set however you like. To have no boarder, just set the "Frame size" value to 0.

Additional Updates planned:

Pip value calculation (2 feature uses)

-This will serve 2 purposes. The widget will calculate the value of the trade based on the lot size. It will also have a risk limit, so if the ATR get's too high for the current risk settings, It will show red to warn you of a high risk situation before you trade.

Example, you have a set limit of 3 dollars per trade using .02 lot sizing. If the ATR get's too high, The Stop value will be more risk than you would like to use at that trade sizing. Reduce the trade size, or wait for ATR to come lower.

Purpose 2: lot size calculation, so if you wanted to maximize the use of risk available. If you wanted to risk 600 for example, it would use the ATR you have set for the risk, and determine the proper lot size for the amount of volatility in the market. This way, you Risk Exactly, or as close as possible to 600 for the the current trade conditions.

Extra use for this value: Show the Current trade amounts at risk and for gain in money values on the side of the pip/point value. Know what you're risking and also trading for in monetary value.

ATR candle Comparison- Early momentum Detection (2 feature uses)

Will show an additional section on the bottom of the widget to show how each candle compares to the one before, up to the last 5, and show if ATR went down, up, or stayed the same over the last 5 candles.

Show an additional symbol to indicate the current candle status in comparison to the close of the last candle. Real time of if the ATR is getting larger, smaller, or staying the same.

Dynamic ATR BandsDescription:

The Dynamic ATR Bands indicator visualizes ATR-based stop-loss, take-profit, and trailing levels. Bands can be drawn relative to a fixed entry price or dynamically relative to the current price. It is ideal for trend-following, swing trading, and hybrid strategies, especially on volatile or noisy instruments.

Key Features:

Base ATR Bands:

Plots ATR-based bands above and below a reference price.

Acts as initial stop-loss or target guidance.

Adjustable multiplier (default 1× ATR).

Extra ATR Band:

Add an additional ATR band at a custom multiplier.

Position it above or below the reference price.

Useful for trailing stops or extended profit targets.

Hybrid Entry Mode:

Use Fixed Entry Price: bands are drawn relative to your entry and remain fixed.

Dynamic Mode: bands behave like standard ATR bands, moving with the current price.

Allows visualization of hybrid ATR stop-loss and trailing strategies.

Clean Visuals:

Color-coded bands differentiate base (solid) from extra (semi-transparent).

How to Use:

Set ATR length and multipliers according to your strategy.

Toggle hybrid entry mode and input your entry price, or leave off for dynamic bands.

Set the extra band multiplier and choose its position (upper/lower).

Use the bands as visual guides for stop-loss, take-profit, and trailing levels.

Inputs:

ATR Length: number of periods for ATR calculation

Base ATR Multiplier: distance of base bands from reference price

Extra ATR Multiplier: distance for the additional band

Extra Band Position: choose Upper or Lower

Use Fixed Entry Price: toggle hybrid entry mode

Entry Price: specify entry price if hybrid mode is enabled

Note:

This script is visual only; it does not place trades. It is designed to help plan ATR-based stop-loss, take-profit, and hybrid trade management visually on the chart.

1m Scalping ATR (with SL & Zones)A universal ATR indicator that anchors volatility to your stop-loss.

Read any market (FX, JPY pairs, Gold/Silver, indices, crypto) consistently—regardless of pip/point conventions and timeframe.

Why this indicator?

Classic ATR is absolute (pips/points) and feels different across markets/TFs. ATR Takeoff normalizes ATR to your stop-loss in pips and highlights clear zones for “quiet / ideal / too volatile,” so you instantly know if a 10-pip SL fits current conditions.

Key features

Auto pip detection (FX, JPY, XAU/XAG, indices, BTC/ETH).

Selectable ATR source: chart timeframe or fixed ATR TF (e.g., “15”, “30”, “60”).

Display modes:

Percent of SL – ATR relative to SL in %, great for M1 (typical 10–30%).

Multiple of SL – ATR as a multiple of SL (e.g., 0.6× / 1.0× / 1.2×).

Panel zones:

Green = “Ready for takeoff” (≤ Low), Yellow = reference (Mid), Red = too volatile (≥ High).

Status badge (top-right): Quiet / ATR ok / Wild, current ATR/SL value, ATR TF used.

Direction-agnostic: Works the same for longs and shorts.

Inputs (at a glance)

Length / Smoothing (RMA/SMA/EMA/WMA): ATR base settings.

Your Stop-Loss (Pips): Reference SL (e.g., 10).

ATR Timeframe (empty = chart): Use chart TF or a fixed TF.

Display Mode: “Percent of SL” or “Multiple of SL.”

Low/Mid/High (Percent Mode): Zone thresholds in % of SL.

Low/Mid/High (Multiple Mode): Zone thresholds in ×SL.

Recommended defaults

Length 14, Smoothing RMA, SL 10 pips

Display Mode: Percent of SL

Low/Mid/High (%): 15 / 20 / 25

ATR Timeframe: empty (= chart) for reactive, or “30” for smoother M30 context with M1 entries.

How to use

Set SL (pips). 2) Choose display mode. 3) Optionally pick ATR TF.

Interpretation:

≤ Low (green): setups allowed.

≈ Mid (yellow): neutral reference.

≥ High (red): too volatile → adjust SL/size or wait.

Note: Auto-pip relies on common ticker naming; verify on exotic symbols.

Disclaimer: For research/education. Not financial advice.

DEMA ATR Strategy [PrimeAutomation]⯁ OVERVIEW

The DEMA ATR Strategy combines trend-following logic with adaptive volatility filters to identify strong momentum phases and manage trades dynamically.

It uses a Double Exponential Moving Average (DEMA) anchored to ATR volatility bands, creating a self-adjusting trend baseline.

When the adjusted DEMA shifts direction, the strategy enters positions and scales out profit in phases based on ATR-driven targets.

This system adapts to volatility, filters noise, and seeks sustained directional moves.

⯁ KEY FEATURES

DEMA-Volatility Hybrid Filter

Uses Double EMA with ATR expansion/compression logic to form a dynamic trend baseline.

Directional Shift Entries

Entries occur when the adjusted DEMA flips trend (bullish crossover or bearish crossunder vs its past value).

Noise Reduction Mechanism

ATR range caps extreme moves and prevents false flips during choppy volatility spikes.

Multi-Level Take Profits

Targets scale out positions at 1×, 2×, and 3× ATR multiples in the trade direction.

Volatility-Adaptive Targets

ATR multiplier ensures profit targets expand/contract based on market conditions.

Single-Direction Exposure

No pyramiding; the strategy flips position only when trend shifts.

Automated Trade Finalization

When all profit targets trigger, the position is fully closed.

⯁ STRATEGY LOGIC

Trend Direction:

DEMA baseline is modified using ATR upper/lower envelopes.

• If the adjusted DEMA rises above previous value → Bullish

• If it falls below previous value → Bearish

Entry Rules:

• Enter Long when bullish shift occurs and no long position exists

• Enter Short when bearish shift occurs and no short position exists

Take Profit Logic:

3 partial exits for each trade based on ATR:

• TP1 = ±1× ATR

• TP2 = ±2× ATR

• TP3 = ±3× ATR

Profit distribution: 30% / 30% / 40%

Exit Conditions:

• Exit when all TPs hit (full scale-out if sum of all TPs 100%)

• Opposite trend signal closes current trade and opens new one

⯁ WHEN TO USE

Trending environments

Medium–high volatility phases

Swing trading and intraday trend plays

Markets that respect momentum continuation (crypto, indices, FX majors)

⯁ CONCLUSION

This strategy blends DEMA trend recognition with ATR-based volatility adaptation to generate cleaner directional entries and structured take-profit exits. It is designed to capture momentum phases while avoiding noise-driven false signals, delivering a disciplined and scalable trend-following approach.

Yesterday's ATR DrawerWith this ATR Drawer, you can easily see what yesterday's ATR was compared to today's High/Low , you don't have to draw it yourself, and if you want, it will also show you yesterday's ATR number in the corner.

When a new High/Low is created during the day, the lines automatically adapt . So if a new high is created, the lower ATR line will move up, and vice versa. Every day, it recalculates and redraws the lines to yesterday's ATR level.

You can add 1 line above and 1 line below yesterday's ATR, which will be at the percentage distance from yesterday's original ATR line. So basically this allows you to set the average range that is usually reached after the ATR is broken .

You can set:

- ATR length

- ATR line width

- Line color

- Show/hide yesterday's ATR

- Upper Avr. Range After ATR Exceeded (%)

- Lower Avr. Range After ATR Exceeded (%)

ATR Regime Filter (median & P70)ATR Regime Filter (Median & P70)

Purpose

Filter your signals by the volatility regime. The indicator compares the current ATR to two rolling statistical thresholds—the median (P50) and the 70th percentile (P70)—to avoid trading during quiet phases and prioritize setups when the market “breathes.”

How it works

Computes ATR(14) on a user-defined source timeframe (srcTF) via request.security.

Converts a target window in days (days) into bars of the source TF.

Due to Pine limits, the effective window is capped at 5000 bars (shown in an optional label).

Calculates Median (P50) and P70 of ATR over the effective window.

Exposes two booleans:

ATR > Median (normal-to-elevated volatility)

ATR > P70 (elevated volatility)

Display

Plots: ATR, Median, P70.

Panel background (bgcolor):

light green when ATR > P70

teal when ATR > Median

neutral otherwise

Optional label: shows source TF, effective window size (bars & days), and the boolean states.

Inputs

ATR length (default 14)

TF source ATR (srcTF, e.g., “1”, “5”, “15”)

Target window (days) (days, default 20)

Show label (bool)

Suggested use

Breakout/Momentum: require ATR > P70 in addition to your breakout conditions (close beyond level, volume, retest).

Range/Mean reversion: at minimum require ATR > Median.

In strategies, use ATR > Median/P70 as a filter alongside price structure, volume, and EMAs.

Limitations

On very short source TFs (e.g., 1-min), the window may be clipped to 5000 bars (~3.5 days). Increase srcTF (5m/15m) if you want a true 15–30 day history.

ATR measures magnitude, not direction—combine with trend/structure signals.

Rolling ATR Bands | Flux Charts💎 GENERAL OVERVIEW

Introducing the Rolling ATR Bands indicator! This indicator overlays adaptive bands around the price, using the Average True Range (ATR) to define dynamic support and resistance levels. The Rolling ATR Bands are color-coded to visually indicate potential trend strength, shifting between bearish, neutral, and bullish colors. This tool can help traders interpret price volatility, as well as identify probable trend changes, continuations, or reversals. For more information about the process, check the "HOW DOES IT WORK ?" section.

Features of the new Rolling ATR Bands:

ATR Bands With Customizable ATR Length & Multiplier

Smooth Trend Strength With Adjustable Smoothing Options

Color-coded bands Representing Bearish, Neutral, or Bullish Trends

Alerts for Retests & Breaks

Customizable Visuals

📌 HOW DOES IT WORK?

The Rolling ATR Bands indicator calculates the ATR based on the specified length and multiplier to form upper and lower bands around the price. These bands adapt with market volatility, widening during high volatility and contracting during lower volatility periods.

In addition, the indicator calculates a "trend strength" score by combining an interpolated RSI, Supertrend, and EMA crossover. This score is smoothed with a customizable length, and a color gradient is applied to visually denote the strength of bearish, neutral, or bullish conditions.

Here's how to interpret the bands:

Upper Band: Acts as dynamic resistance; when price approaches or touches it, this often suggests potential overbought conditions.

Lower Band: Acts as dynamic support; touching or nearing this band might indicate potential oversold conditions.

Color Shifts: Color changes indicate shifts in trend direction. For example, a green color suggests a bullish trend, while red hints at bearish tendencies.

🚩 UNIQUENESS

What sets the Rolling ATR Bands apart is the combined use of interpolated RSI, Supertrend, and EMA cross values, creating a weighted trend strength score. This integration allows for nuanced, color-coded visual cues that respond quickly to trend changes without excessive noise, offering traders an intuitive view of both trend direction and potential momentum. You can also set up alerts for retest & alerts for upper and lower bands to get informed of potential movements.

⚙️ SETTINGS

1. General Configuration

ATR Length : Controls the ATR calculation length for the bands.

Smoothing: Adjusts the trend strength smoothing to control sensitivity to trend changes.

ATR Multiplier : Sets the width of the bands by multiplying the ATR value.

Trend Smoothing : Higher settings will result in longer periods of time required for trend to change direction from bullish to bearish and vice versa.

Anrazzi - EMAs/ATR - 1.0.2The Anrazzi – EMAs/ATR indicator is a multi-purpose overlay designed to help traders track trend direction and market volatility in a single clean tool.

It plots up to six customizable moving averages (MAs) and an Average True Range (ATR) value directly on your chart, allowing you to quickly identify market bias, dynamic support/resistance, and volatility levels without switching indicators.

This script is ideal for traders who want a simple, configurable, and efficient way to combine trend-following signals with volatility-based position sizing.

📌 Key Features

Six Moving Averages (MA1 → MA6)

Toggle each MA on/off individually

Choose between EMA or SMA for each

Customize length and color

Perfect for spotting trend direction and pullback zones

ATR Display

Uses Wilder’s ATR formula (ta.rma(ta.tr(true), 14))

Can be calculated on current or higher timeframe

Adjustable multiplier for position sizing (e.g., 1.5× ATR stops)

Displays cleanly in the bottom-right corner

Custom Watermark

Displays symbol + timeframe in top-right

Adjustable color and size for streamers, screenshots, or clear charting

Compact UI

Organized with group and inline inputs for quick configuration

Lightweight and optimized for real-time performance

⚙️ How It Works

MAs: The script uses either ta.ema() or ta.sma() to compute each moving average based on the user-selected type and length.

ATR: The ATR is calculated using ta.rma(ta.tr(true), 14) (Wilder’s smoothing), and optionally scaled by a multiplier for easier use in risk management.

Tables: ATR value and watermark are displayed using table.new() so they stay anchored to the screen regardless of zoom level.

📈 How to Use

Enable the MAs you want to track and adjust their lengths, type, and colors.

Enable ATR if you want to see volatility — optionally select a higher timeframe for broader context.

Use MAs to:

Identify overall trend direction (e.g. price above MA20 = bullish)

Spot pullback zones for entries

See when multiple MAs cluster together as support/resistance zones

Use ATR value to:

Size your stop-loss dynamically (e.g. stop = entry − 1.5×ATR)

Detect volatility breakouts (ATR spikes = market expansion)

🎯 Recommended For

Day traders & swing traders

Trend-following & momentum strategies

Volatility-based risk management

Traders who want a clean, all-in-one dashboard

Realtime ATR-Based Stop Loss Numerical OverlayRealtime ATR-Based Stop Loss Numerical Overlay

A simple, effective tool for dynamic risk management based on ATR (Average True Range) without adding cluttered and distracting lines all over your chart.

📌 Description

This script plots a real-time stop loss level using the Average True Range (ATR) on your chart, helping you set consistent, volatility-based stops. It supports both:

✅ Current chart timeframe

✅ Custom fixed timeframe inputs (1m, 5m, 15m, 1h, etc.)

The stop level is calculated as:

Stop = ATR × Multiplier

and updates in real-time. An overlay table displays on the bottom-right of your chart with the calculated stop value in a clean, simple way.

⚙️ Settings

ATR Timeframe Source:

Choose between using the current chart's timeframe or a fixed one (e.g. 5, 15, 60, D, etc).

ATR Length:

Period used to calculate the ATR (default is 14).

Stop Loss Multiplier:

Multiplies the ATR value to define your stop (e.g., 1.5 × ATR).

Wait for Timeframe Closes:

If enabled, the ATR value waits for the selected timeframe’s candle to close before updating. If unselected, it will update in real time.

🛠️ How to Use

Add this script to your chart from your indicators list.

Configure your desired timeframe, ATR length, and multiplier in the settings panel.

Use the value shown in the table overlay as your suggested stop loss distance from entry.

Adjust your position sizing accordingly to fit your risk tolerance.

This tool is especially useful for traders looking for adaptive risk management that evolves with market volatility — whether scalping intraday or swing trading.

💡 Pro Tip

The ATR stop can also be used to dynamically trail your stop behind price movement.

ADR, ATR & VOL OverlayThis is a combined version of 2 of my other indicators:

ADR / ATR Overlay

VOL / AVG Overlay

This indicator will display the following as an overlay on your chart:

ADR

% of ADR

ADR % of Price

ATR

% of ATR

ATR % of Price

Custom Session Volume

Average For Selected Session

Volume Percentage Comparison

Description:

ADR : Average Day Range

% of ADR : Percentage that the current price move has covered its average.

ADR % of Price : The percentage move implied by the average range.

ATR : Average True Range

% of ATR : Percentage that the current price move has covered its average.

ATR % of Price : The percentage move implied by the average true range.

Custom Session Volume : User chosen time frame to monitor volume

Average For Selected Session : Average for the custom session volume

Volume Percentage Comparison : Current session compared to the average (calculated at session close)

Options:

ADR/ATR:

Time Frame

Length

Smoothing

Volume:

Set Custom Time Frame For Calculations

Set Custom Time Frame For Average Comparison

Set Custom Time Zone

Table:

Enable / Disable Each Value

Change Text Color

Change Background Color

Change Table location

Add/Remove extra row for placement

ADR / ATR Example:

The ADR and ATR can be used to provide information about average price moves to help set targets, stop losses, entries and exits based on the potential average moves.

Example: If the "% of ADR" is reading 100%, then 100% of the asset's average price range has been covered, suggesting that an additional move beyond the range has a lower probability.

Example: "ADR % of Price" provides potential price movement in percentage which can be used to asses R/R for asset.

Example: ADR (D) reading is 100% at market close but ATR (D) is at 70% at close. This suggests that there is a potential (coverage) move of 30% in Pre/Post market as suggested by averages.

Custom Volume Session Example:

Set indicator to 30 period average. Set custom time frame to 9:30am to 10:30am Eastern/New York.

When the time frame for the calculation is closed, the indicator will provide a comparison of the current days volume compared to the average of 30 previous days for that same time frame and display it as a percentage in the table.

In this example you could compare how the first hour of the trading day compares to the previous 30 day's average, aiding in evaluating the potential volume for the remainder of the day.

Notes:

Times must be entered in 24 hour format. (1pm = 13:00 etc.)

Volume indicator is for Intra-day time frames, not > Day.

How I use these values:

I use these calculations to determine if a ticker symbol has the necessary range to achieve target gains, to determine if the price oscillation is within "normal" ranges to determine if the trading day will be choppy, and to determine placement of stops and targets within average ranges in combination with support, resistance and retracement levels.

ATR X-PowerATR X-Power is a simple graphical representation of Average True Range.

The ATR is calculated on a daily basis and averaged over the "Length" specified in settings (default is 14 days).

At the start of the day, the starting price is recorded and five horizontal lines are drawn which illustrate possible ranges for the day:

Starting price

Starting price + ATR (+100%)

Starting price - ATR (-100%)

Starting price + ATR/2 (+50%)

Starting price - ATR/2 (-50%)

The final two lines are drawn using the ATR half values in such a way that a X is formed. The X represents possible motion of the price back to starting price (also known as reversion to mean). The two lines are drawn as follows:

Beginning at (Starting Price + ATR/2) and ending at (Starting Price - ATR/2)

Beginning at (Starting Price - ATR/2) and ending at (Starting Price + ATR/2)

Use cases:

ATR presents us with the average amount of price fluctuation we can expect to see in a single day on a specific instrument

If price is near the extremes (+/-100% ATR) for the day, then probability of it moving outside that range is low, which increases odds of a reversal

Bugs?

Kindly report any issues you run into and I'll try to fix them promptly.

Thank you!

Average True Range (ATR %) Stop Loss CalculatorThis indicator takes the average of a series of ATR to calculate what I would consider an optimum stop loss placement represented in percentage (read below for full overview).

While the data is plotted what is most helpful are the actual numbers presented and for my charts I remove most of the plotting.

This indicator is most helpful on the daily timeframe but can be used for all timeframes such as the 4HR, 1HR or even 15M.

This indicator should not be used alone. It should be used in conjunction with proper price action analysis. It’s also a great indicator if you chart using Value Channels. Ideally you want your stop placement to be below at least one core Value Channel boundary range. In addition to standard support and resistance and some key moving averages the market respects. This also works best when trading with the prevailing BIAS of the instrument (bull or bear).

Cryptos: Generally, that means you’re buying on retracements that fit the end of a structured move. The other option is using this in a clear up trending market where the pull backs are clearly being supported with buying.

FOREX: I built another indicator for FOREX search: ATRPIPS with SL

WTI: Helpful but I have different rules for when I trade WTI. I rely upon VCs and diagnal VCs much more when trading this.

Equities: Helpful but with the increase of volatility as well as uncertainty of Bias of the market-- this should be used as more of a guide than

What is most important is the actual percentage numbers but I've found graphing 1-3 of the actual ATRs is helpful. The rest just uncheck the checkbox in the options.

Indicator Overview:

Value 1 - 3 Period ATR (maroon)

Value 2 - 7 Period ATR (green)

Value 3 - 30 Period ATR (blue)

Value 4 - 90 Period ATR (blue, bold)

Value 5 - 1 Period ATR (green)

Value 6 - 1 Period ATR (red)

Value 6 – Prime Stop Loss Placement (maroon). This is the average of all above ATRs multiplied by 1.5

Value 7 - Move Left (red). Experimental value. This is the difference between (prime stop loss) and 1 day period move. Two ways to use this value. Use as a tighter stop loss placement. The other option is to use as a retrace target for purchase and using the Prime Stop Placement value as you’re stop loss.

All ATRs use the LOW price of the period. After testing both the low and close I’ve settled on the low to capture the most volatility you will typically experience.

Once again, this indicator should be used in conjunction with your proven trade system.

Also, by knowing what the values are within the indicator you could just eye ball what would be the best stop placement depending on the ATR or 1 or 2 ATRs you find most represent the volatility of what you are trading.

I will be expanding on this indicator by bringing in average measured moves as well as volume analysis and most likely with color changes and modifications.

Background:

While using and refining my trade system I've noticed that most moves happen in 3 periods. So we start there. The 7 period is good for a 24 hour market such as crypto (although weekend trading can be a hit or miss) and to some extent FOREX. The longer periods of 30 & 90 are to smooth out the data set. The final value of the 1 period is to bring a little more recency to the calculation.

Why multiply the average by 1.5? I've found in my own trading and system I built to be the best placement (in conjunction with VCs) to ensure you're stop isn't to close and is within the instrument you are trading volatility .

I'm looking at making this more intelligent as well as take into account volume and structured moves.

Dynamic ATR-based Renko Overlay - Non repaintingDaily ATR-Based Renko Overlay

Overview

This Pine Script v5 indicator creates a dynamic Renko overlay on your time-based charts (optimized for 1-minute timeframes), using the previous period's ATR from a user-specified higher timeframe (default: 1-hour) to determine brick sizes. Unlike traditional Renko charts, this is an overlay that draws Renko bricks directly on top of your existing candles, allowing you to combine the noise-filtering power of Renko with the full features of time-based charts.

It's designed for traders who want Renko's trend-clarity benefits without switching chart types, especially useful for intraday trading in volatile markets like forex, stocks, or crypto.

Key Features

- Adaptive Brick Sizing: Brick size is calculated as a percentage (default 40%) of the previous period's ATR (Average True Range, default length 14) from the selected higher timeframe (default: 1-hour). This makes bricks volatility-adjusted—larger in high-vol periods to reduce noise, smaller in low-vol for more detail.

- Periodic Recalculation: Resets brick size at the start of each new period based on the user-specified reset timeframe (default: daily), using the prior period's ATR from the chosen timeframe. This ensures relevance without unwanted disruptions.

- Traditional Renko Logic: Uses 1-box reversal (a full brick against the trend to reverse). Bricks form based on closing prices, ignoring time and minor fluctuations.

- Visual Style: Stepped lines with green (up) and red (down) fills for a box-like appearance. Semi-transparent for easy overlay on candles.

- Customizable Inputs:

- ATR Length: Adjust the ATR period (default: 14).

- Percentage of ATR: Fine-tune brick sensitivity (default: 0.4 or 40%; range 0-1).

- ATR Timeframe: Specify the timeframe for ATR calculation (default: "60" for 1-hour; enter as a string like "240" for 4-hour, "D" for daily, etc.).