Cowabunga System from babypips.comPlease do read the information below as well, especially if you are new to Forex.

The Cowabunga System is a type of Mechanical Trading System that filters trades based on the trend of the 4 hour chart with EMAs and some other familiar indicators (RSI, Stochastics and MACD) while entering trades base on 15 minute chart.

I have coded (quite amateurishly) the basic system onto a 15 minute chart (the 4 hour settings are coded as well). The author says the system is to be traded off the 15 minute chart with the 4 hour chart only as a reference for trend direction.

4 Hour Chart Settings

5 EMA

10 EMA

Stochastics (10,3,3)

RSI (9)

Then we move onto the 15 minute chart, where he gives us the trade entry rules.

15 Minute Chart Settings

5 EMA

10 EMA

Stochastics (10,3,3)

RSI (9)

MACD (12,26,9)

Entry Rules - long entry rules used, obviously reverse these for shorting.

1. EMA must cross above the 10 EMA.

2. RSI must be greater than 50 and not overbought.

3. Stochastic must be headed up and not be in overbought territory.

4. MACD histogram must go from negative to positive OR be negative and start to increase in value.

What I did.

1. Set the RSI and Stochastic levels to avoid entries when they indicate overbought conditions for long and oversold conditions for short (80 and 20 levels).

2. Users can input specific times they want to backtest.

3. User's can configure profit targets, trailing stops and stops. Default is set it to was 100 pips profit target with a 40 pip trailing stop. (Note, when you are changing these values, please note that each pip is worth 10, so 100 pips is entered as 1000.)

The Cowabunga System from babypips.com is another popular and active system. The author, Pip Surfer, continues to post wins and losses with this system. It shows there is a lot of honesty and integrity with this system if the author keeps up to date even 10 years later and is not afraid of sharing the times the system causes losses.

As an example of this, here is post he shared just last week . It's almost like a journal, he gives specific times and reasons why he entered, lets the readers know when he was stopped out, etc. I think that what he does is equally important as his system.

To read more about this system, visit the thread on babypips.com, click here.

Cari dalam skrip untuk "A股+股票筛选器+10元以下"

ICT Quant-Core: Liquidity Intelligence [Dual-Engine]🔥 THE ULTIMATE LIQUIDITY FILTERING ENGINE

Most SMC traders lose money because they "catch falling knives" on every local wick. This algorithm solves this problem by using DUAL-CORE logic and a signal quality scoring system.

This is no ordinary pivot indicator.

⚙️ HOW DOES IT WORK? (DUAL-CORE LOGIC)

The algorithm analyzes the market on two levels simultaneously:

1️⃣ MACRO CORE (Lookback 50 - "WHALE 🐋")

Tracks key levels from recent weeks/months.

This is where institutions build their positions.

Signals from this core have the highest priority (Score 10/10).

2️⃣ LOCAL CORE (Lookback 20 - "ROACH 🐟")

Tracks internal market structure and noise.

Signals are filtered by the Main Trend. If the trend is down, Local Longs are marked as "TRAP."

🧠 SMART FILTERS (QUANT LAYERS)

Instead of entering on every line touch, the script requires confirmation:

✅ RECLAIM LOGIC: Price must close back above/below the liquidity level (Swing Failure Pattern).

✅ RVOL FILTER: Requires relative volume > 1.2x the average (institutional track).

✅ SCORING SYSTEM (0-10): Each signal receives a score.

- 10/10: Macro Grab in line with the trend + high volume.

- 3/10: Local Grab against the trend (risky).

📊 ANALYTICAL DASHBOARD

In the lower right corner, you'll find the "Command Center":

- Trend Status (Distribution/Accumulation)

- Whale's Last Move (Price and Direction)

- Current Tactics (e.g., "Ignore Longs, Search for Shorts")

- Filter Status (RSI, Volume, Reclaim)

🚀 HOW TO USE IT?

1. Set the H4 timeframe.

2. Wait for a signal with a rating > 7/10.

3. Ignore "Fish/Local" signals (small icons) if they contradict the Dashboard color.

4. Entry occurs only after the candle closes (Reclaim).

Smart RSI MTF Matrix [DotGain]Summary

Are you tired of trading trend signals, only to miss the bigger picture because you are focused on a single timeframe?

The Smart RSI MTF Matrix is the ultimate "Cockpit View" for momentum traders. Unlike chart overlays that can sometimes clutter your price action, this indicator organizes RSI conditions across 10 different timeframes simultaneously into a clean, separate Heatmap pane.

It monitors everything from the 5-minute chart all the way up to the 12-Month view , giving you a complete X-ray vision of the market's momentum structure instantly.

⚙️ Core Components and Logic

The Smart RSI MTF Matrix relies on a sophisticated hierarchy to deliver clear, actionable context:

Multi-Timeframe Engine: The script runs 10 independent RSI calculations in the background, organized in rows from bottom (Short Term) to top (Long Term).

Classic RSI Thresholds:

Overbought (> 70): Indicates price may be extended to the upside.

Oversold (< 30): Indicates price may be extended to the downside.

Smart Visibility System (The "Secret Sauce"): Not all signals are equal. A 5-minute signal is "noise" compared to a Yearly signal. This indicator automatically applies Transparency to differentiate importance. The visibility increases by 10% for each higher timeframe slot (Row).

🚦 How to Read the Matrix

The indicator plots dots in 10 stacked rows. The position and opacity tell you the direction and significance:

🟥 RED DOTS (Overbought Condition)

Trigger: RSI is above 70 on that specific timeframe.

Meaning: Potential bearish reversal or pullback.

🟩 GREEN DOTS (Oversold Condition)

Trigger: RSI is below 30 on that specific timeframe.

Meaning: Potential bullish reversal or bounce.

⚪ GRAY DOTS (Neutral)

Trigger: RSI is between 30 and 70.

Meaning: No extreme momentum present.

👻 TRANSPARENCY (Signal Strength)

The visibility of the dot tells you exactly which Timeframe (Row) is triggered. The higher the row, the more solid the color:

Faint (10-30% Visibility): Rows 1-3 (5m, 15m, 1h). Used for scalping entries.

Medium (40-60% Visibility): Rows 4-6 (4h, 1D, 1W). Used for swing trading context.

Solid (70-100% Visibility): Rows 7-10 (1M, 3M, 6M, 12M). Used for identifying major macro cycles.

Visual Elements

Structure: Row 1 (Bottom) represents the 5-minute timeframe. Row 10 (Top) represents the 12-Month timeframe.

Vertical Alignment: If you see a vertical column of Red or Green dots, it indicates Multi-Timeframe Confluence —a highly probable reversal point.

Key Benefit

The goal of the Smart RSI MTF Matrix is to keep your main chart clean while providing maximum information. You can instantly see if a short-term pullback (Faint Green Dot) is happening within a long-term uptrend (Solid Gray/Red Dot), allowing for precision entries.

Have fun :)

Disclaimer

This "Smart RSI MTF Matrix" indicator is provided for informational and educational purposes only. It does not, and should not be construed as, financial, investment, or trading advice.

The signals generated by this tool (both "Buy" and "Sell" indications) are the result of a specific set of algorithmic conditions. They are not a direct recommendation to buy or sell any asset. All trading and investing in financial markets involves substantial risk of loss. You can lose all of your invested capital.

Past performance is not indicative of future results. The signals generated may produce false or losing trades. The creator (© DotGain) assumes no liability for any financial losses or damages you may incur as a result of using this indicator.

You are solely responsible for your own trading and investment decisions. Always conduct your own research (DYOR) and consider your personal risk tolerance before making any trades.

Stochastic Hash Strat [Hash Capital Research]# Stochastic Hash Strategy by Hash Capital Research

## 🎯 What Is This Strategy?

The **Stochastic Slow Strategy** is a momentum-based trading system that identifies oversold and overbought market conditions to capture mean-reversion opportunities. Think of it as a "buy low, sell high" approach with smart mathematical filters that remove emotion from your trading decisions.

Unlike fast-moving indicators that generate excessive noise, this strategy uses **smoothed stochastic oscillators** to identify only the highest-probability setups when momentum truly shifts.

---

## 💡 Why This Strategy Works

Most traders fail because they:

- **Chase prices** after big moves (buying high, selling low)

- **Overtrade** in choppy, directionless markets

- **Exit too early** or hold losses too long

This strategy solves all three problems:

1. **Entry Discipline**: Only trades when the stochastic oscillator crosses in extreme zones (oversold for longs, overbought for shorts)

2. **Cooldown Filter**: Prevents revenge trading by forcing a waiting period after each trade

3. **Fixed Risk/Reward**: Pre-defined stop-loss and take-profit levels ensure consistent risk management

**The Math Behind It**: The stochastic oscillator measures where the current price sits relative to its recent high-low range. When it's below 25, the market is oversold (time to buy). When above 70, it's overbought (time to sell). The crossover with its moving average confirms momentum is shifting.

---

## 📊 Best Markets & Timeframes

### ⭐ OPTIMAL PERFORMANCE:

**Crude Oil (WTI) - 12H Timeframe**

- **Why it works**: Oil markets have predictable volatility patterns and respect technical levels

**AAVE/USD - 4H to 12H Timeframe**

- **Why it works**: DeFi tokens exhibit strong momentum cycles with clear extremes

### ✅ Also Works Well On:

- **BTC/USD** (12H, Daily) - Lower frequency but high win rate

- **ETH/USD** (8H, 12H) - Balanced volatility and liquidity

- **Gold (XAU/USD)** (Daily) - Classic mean-reversion asset

- **EUR/USD** (4H, 8H) - Lower volatility, requires patience

### ❌ Avoid Using On:

- Timeframes below 4H (too much noise)

- Low-liquidity altcoins (wide spreads kill performance)

- Strongly trending markets without pullbacks (Bitcoin in 2021)

- News-driven instruments during major events

---

## 🎛️ Understanding The Settings

### Core Stochastic Parameters

**Stochastic Length (Default: 16)**

- Controls the lookback period for price comparison

- Lower = faster reactions, more signals (10-14 for volatile markets)

- Higher = smoother signals, fewer trades (16-21 for stable markets)

- **Pro tip**: Use 10 for crypto 4H, 16 for commodities 12H

**Overbought Level (Default: 70)**

- Threshold for short entries

- Lower values (65-70) = more trades, earlier entries

- Higher values (75-80) = fewer but higher-conviction trades

- **Sweet spot**: 70 works for most assets

**Oversold Level (Default: 25)**

- Threshold for long entries

- Higher values (25-30) = more trades, earlier entries

- Lower values (15-20) = fewer but stronger bounce setups

- **Sweet spot**: 20-25 depending on market conditions

**Smooth K & Smooth D (Default: 7 & 3)**

- Additional smoothing to filter out whipsaws

- K=7 makes the indicator slower and more reliable

- D=3 is the signal line that confirms the trend

- **Don't change these unless you know what you're doing**

---

### Risk Management

**Stop Loss % (Default: 2.2%)**

- Automatically exits losing trades

- Should be 1.5x to 2x your average market volatility

- Too tight = death by a thousand cuts

- Too wide = uncontrolled losses

- **Calibration**: Check ATR indicator and set SL slightly above it

**Take Profit % (Default: 7%)**

- Automatically exits winning trades

- Should be 2.5x to 3x your stop loss (reward-to-risk ratio)

- This default gives 7% / 2.2% = 3.18:1 R:R

- **The golden rule**: Never have R:R below 2:1

---

### Trade Filters

**Bar Cooldown Filter (Default: ON, 3 bars)**

- **What it does**: Forces you to wait X bars after closing a trade before entering a new one

- **Why it matters**: Prevents emotional revenge trading and overtrading in choppy markets

- **Settings guide**:

- 3 bars = Standard (good for most cases)

- 5-7 bars = Conservative (oil, slow-moving assets)

- 1-2 bars = Aggressive (only for experienced traders)

**Exit on Opposite Extreme (Default: ON)**

- Closes your long when stochastic hits overbought (and vice versa)

- Acts as an early profit-taking mechanism

- **Leave this ON** unless you're testing other exit strategies

**Divergence Filter (Default: OFF)**

- Looks for price/momentum divergences for additional confirmation

- **When to enable**: Trending markets where you want fewer but higher-quality trades

- **Keep OFF for**: Mean-reverting markets (oil, forex, most of the time)

---

## 🚀 Quick Start Guide

### Step 1: Set Up in TradingView

1. Open TradingView and navigate to your chart

2. Click "Pine Editor" at the bottom

3. Copy and paste the strategy code

4. Click "Add to Chart"

5. The strategy will appear in a separate pane below your price chart

### Step 2: Choose Your Market

**If you're trading Crude Oil:**

- Timeframe: 12H

- Keep all default settings

- Watch for signals during London/NY overlap (8am-11am EST)

**If you're trading AAVE or crypto:**

- Timeframe: 4H or 12H

- Consider these adjustments:

- Stochastic Length: 10-14 (faster)

- Oversold: 20 (more aggressive)

- Take Profit: 8-10% (higher targets)

### Step 3: Wait for Your First Signal

**LONG Entry** (Green circle appears):

- Stochastic crosses up below oversold level (25)

- Price likely near recent lows

- System places limit order at take profit and stop loss

**SHORT Entry** (Red circle appears):

- Stochastic crosses down above overbought level (70)

- Price likely near recent highs

- System places limit order at take profit and stop loss

**EXIT** (Orange circle):

- Position closes either at stop, target, or opposite extreme

- Cooldown period begins

### Step 4: Let It Run

The biggest mistake? **Interfering with the system.**

- Don't close trades early because you're scared

- Don't skip signals because you "have a feeling"

- Don't increase position size after a big win

- Don't revenge trade after a loss

**Follow the system or don't use it at all.**

---

### Important Risks:

1. **Drawdown Pain**: You WILL experience losing streaks of 5-7 trades. This is mathematically normal.

2. **Whipsaw Markets**: Choppy, range-bound conditions can trigger multiple small losses.

3. **Gap Risk**: Overnight gaps can cause your actual fill to be worse than the stop loss.

4. **Slippage**: Real execution prices differ from backtested prices (factor in 0.1-0.2% slippage).

---

## 🔧 Optimization Guide

### When to Adjust Settings:

**Market Volatility Increased?**

- Widen stop loss by 0.5-1%

- Increase take profit proportionally

- Consider increasing cooldown to 5-7 bars

**Getting Too Few Signals?**

- Decrease stochastic length to 10-12

- Increase oversold to 30, decrease overbought to 65

- Reduce cooldown to 2 bars

**Getting Too Many Losses?**

- Increase stochastic length to 18-21 (slower, smoother)

- Enable divergence filter

- Increase cooldown to 5+ bars

- Verify you're on the right timeframe

### A/B Testing Method:

1. **Run default settings for 50 trades** on your chosen market

2. Document: Win rate, profit factor, max drawdown, emotional tolerance

3. **Change ONE variable** (e.g., oversold from 25 to 20)

4. Run another 50 trades

5. Compare results

6. Keep the better version

**Never change multiple settings at once** or you won't know what worked.

---

## 📚 Educational Resources

### Key Concepts to Learn:

**Stochastic Oscillator**

- Developed by George Lane in the 1950s

- Measures momentum by comparing closing price to price range

- Formula: %K = (Close - Low) / (High - Low) × 100

- Similar to RSI but more sensitive to price movements

**Mean Reversion vs. Trend Following**

- This is a **mean reversion** strategy (price returns to average)

- Works best in ranging markets with defined support/resistance

- Fails in strong trending markets (2017 Bitcoin, 2020 Tech stocks)

- Complement with trend filters for better results

**Risk:Reward Ratio**

- The cornerstone of profitable trading

- Winning 40% of trades with 3:1 R:R = profitable

- Winning 60% of trades with 1:1 R:R = breakeven (after fees)

- **This strategy aims for 45% win rate with 2.5-3:1 R:R**

### Recommended Reading:

- *"Trading Systems and Methods"* by Perry Kaufman (Chapter on Oscillators)

- *"Mean Reversion Trading Systems"* by Howard Bandy

- *"The New Trading for a Living"* by Dr. Alexander Elder

---

## 🛠️ Troubleshooting

### "I'm not seeing any signals!"

**Check:**

- Is your timeframe 4H or higher?

- Is the stochastic actually reaching extreme levels (check if your asset is stuck in middle range)?

- Is cooldown still active from a previous trade?

- Are you on a low-liquidity pair?

**Solution**: Switch to a more volatile asset or lower the overbought/oversold thresholds.

---

### "The strategy keeps losing money!"

**Check:**

- What's your win rate? (Below 35% is concerning)

- What's your profit factor? (Below 0.8 means serious issues)

- Are you trading during major news events?

- Is the market in a strong trend?

**Solution**:

1. Verify you're using recommended markets/timeframes

2. Increase cooldown period to avoid choppy markets

3. Reduce position size to 5% while you diagnose

4. Consider switching to daily timeframe for less noise

---

### "My stop losses keep getting hit!"

**Check:**

- Is your stop loss tighter than the average ATR?

- Are you trading during high-volatility sessions?

- Is slippage eating into your buffer?

**Solution**:

1. Calculate the 14-period ATR

2. Set stop loss to 1.5x the ATR value

3. Avoid trading right after market open or major news

4. Factor in 0.2% slippage for crypto, 0.1% for oil

---

## 💪 Pro Tips from the Trenches

### Psychological Discipline

**The Three Deadly Sins:**

1. **Skipping signals** - "This one doesn't feel right"

2. **Early exits** - "I'll just take profit here to be safe"

3. **Revenge trading** - "I need to make back that loss NOW"

**The Solution:** Treat your strategy like a business system. Would McDonald's skip making fries because the cashier "doesn't feel like it today"? No. Systems work because of consistency.

---

### Position Management

**Scaling In/Out** (Advanced)

- Enter 50% position at signal

- Add 50% if stochastic reaches 10 (oversold) or 90 (overbought)

- Exit 50% at 1.5x take profit, let the rest run

**This is NOT for beginners.** Master the basic system first.

---

### Market Awareness

**Oil Traders:**

- OPEC meetings = volatility spikes (avoid or widen stops)

- US inventory reports (Wed 10:30am EST) = avoid trading 2 hours before/after

- Summer driving season = different patterns than winter

**Crypto Traders:**

- Monday-Tuesday = typically lower volatility (fewer signals)

- Thursday-Sunday = higher volatility (more signals)

- Avoid trading during exchange maintenance windows

---

## ⚖️ Legal Disclaimer

This trading strategy is provided for **educational purposes only**.

- Past performance does not guarantee future results

- Trading involves substantial risk of loss

- Only trade with capital you can afford to lose

- No one associated with this strategy is a licensed financial advisor

- You are solely responsible for your trading decisions

**By using this strategy, you acknowledge that you understand and accept these risks.**

---

## 🙏 Acknowledgments

Strategy development inspired by:

- George Lane's original Stochastic Oscillator work

- Modern quantitative trading research

- Community feedback from hundreds of backtests

Built with ❤️ for retail traders who want systematic, disciplined approaches to the markets.

---

**Good luck, stay disciplined, and trade the system, not your emotions.**

Static K-means Clustering | InvestorUnknownStatic K-Means Clustering is a machine-learning-driven market regime classifier designed for traders who want a data-driven structure instead of subjective indicators or manually drawn zones.

This script performs offline (static) K-means training on your chosen historical window. Using four engineered features:

RSI (Momentum)

CCI (Price deviation / Mean reversion)

CMF (Money flow / Strength)

MACD Histogram (Trend acceleration)

It groups past market conditions into K distinct clusters (regimes). After training, every new bar is assigned to the nearest cluster via Euclidean distance in 4-dimensional standardized feature space.

This allows you to create models like:

Regime-based long/short filters

Volatility phase detectors

Trend vs. chop separation

Mean-reversion vs. breakout classification

Volume-enhanced money-flow regime shifts

Full machine-learning trading systems based solely on regimes

Note:

This script is not a universal ML strategy out of the box.

The user must engineer the feature set to match their trading style and target market.

K-means is a tool, not a ready made system, this script provides the framework.

Core Idea

K-means clustering takes raw, unlabeled market observations and attempts to discover structure by grouping similar bars together.

// STEP 1 — DATA POINTS ON A COORDINATE PLANE

// We start with raw, unlabeled data scattered in 2D space (x/y).

// At this point, nothing is grouped—these are just observations.

// K-means will try to discover structure by grouping nearby points.

//

// y ↑

// |

// 12 | •

// | •

// 10 | •

// | •

// 8 | • •

// |

// 6 | •

// |

// 4 | •

// |

// 2 |______________________________________________→ x

// 2 4 6 8 10 12 14

//

//

//

// STEP 2 — RANDOMLY PLACE INITIAL CENTROIDS

// The algorithm begins by placing K centroids at random positions.

// These centroids act as the temporary “representatives” of clusters.

// Their starting positions heavily influence the first assignment step.

//

// y ↑

// |

// 12 | •

// | •

// 10 | • C2 ×

// | •

// 8 | • •

// |

// 6 | C1 × •

// |

// 4 | •

// |

// 2 |______________________________________________→ x

// 2 4 6 8 10 12 14

//

//

//

// STEP 3 — ASSIGN POINTS TO NEAREST CENTROID

// Each point is compared to all centroids.

// Using simple Euclidean distance, each point joins the cluster

// of the centroid it is closest to.

// This creates a temporary grouping of the data.

//

// (Coloring concept shown using labels)

//

// - Points closer to C1 → Cluster 1

// - Points closer to C2 → Cluster 2

//

// y ↑

// |

// 12 | 2

// | 1

// 10 | 1 C2 ×

// | 2

// 8 | 1 2

// |

// 6 | C1 × 2

// |

// 4 | 1

// |

// 2 |______________________________________________→ x

// 2 4 6 8 10 12 14

//

// (1 = assigned to Cluster 1, 2 = assigned to Cluster 2)

// At this stage, clusters are formed purely by distance.

Your chosen historical window becomes the static training dataset , and after fitting, the centroids never change again.

This makes the model:

Predictable

Repeatable

Consistent across backtests

Fast for live use (no recalculation of centroids every bar)

Static Training Window

You select a period with:

Training Start

Training End

Only bars inside this range are used to fit the K-means model. This window defines:

the market regime examples

the statistical distributions (means/std) for each feature

how the centroids will be positioned post-trainin

Bars before training = fully transparent

Training bars = gray

Post-training bars = full colored regimes

Feature Engineering (4D Input Vector)

Every bar during training becomes a 4-dimensional point:

This combination balances: momentum, volatility, mean-reversion, trend acceleration giving the algorithm a richer "market fingerprint" per bar.

Standardization

To prevent any feature from dominating due to scale differences (e.g., CMF near zero vs CCI ±200), all features are standardized:

standardize(value, mean, std) =>

(value - mean) / std

Centroid Initialization

Centroids start at diverse coordinates using various curves:

linear

sinusoidal

sign-preserving quadratic

tanh compression

init_centroids() =>

// Spread centroids across using different shapes per feature

for c = 0 to k_clusters - 1

frac = k_clusters == 1 ? 0.0 : c / (k_clusters - 1.0) // 0 → 1

v = frac * 2 - 1 // -1 → +1

array.set(cent_rsi, c, v) // linear

array.set(cent_cci, c, math.sin(v)) // sinusoidal

array.set(cent_cmf, c, v * v * (v < 0 ? -1 : 1)) // quadratic sign-preserving

array.set(cent_mac, c, tanh(v)) // compressed

This makes initial cluster spread “random” even though true randomness is hardly achieved in pinescript.

K-Means Iterative Refinement

The algorithm repeats these steps:

(A) Assignment Step, Each bar is assigned to the nearest centroid via Euclidean distance in 4D:

distance = sqrt(dx² + dy² + dz² + dw²)

(B) Update Step, Centroids update to the mean of points assigned to them. This repeats iterations times (configurable).

LIVE REGIME CLASSIFICATION

After training, each new bar is:

Standardized using the training mean/std

Compared to all centroids

Assigned to the nearest cluster

Bar color updates based on cluster

No re-training occurs. This ensures:

No lookahead bias

Clean historical testing

Stable regimes over time

CLUSTER BEHAVIOR & TRADING LOGIC

Clusters (0, 1, 2, 3…) hold no inherent meaning. The user defines what each cluster does.

Example of custom actions:

Cluster 0 → Cash

Cluster 1 → Long

Cluster 2 → Short

Cluster 3+ → Cash (noise regime)

This flexibility means:

One trader might have cluster 0 as consolidation.

Another might repurpose it as a breakout-loading zone.

A third might ignore 3 clusters entirely.

Example on ETHUSD

Important Note:

Any change of parameters or chart timeframe or ticker can cause the “order” of clusters to change

The script does NOT assume any cluster equals any actionable bias, user decides.

PERFORMANCE METRICS & ROC TABLE

The indicator computes average 1-bar ROC for each cluster in:

Training set

Test (live) set

This helps measure:

Cluster profitability consistency

Regime forward predictability

Whether a regime is noise, trend, or reversion-biased

EQUITY SIMULATION & FEES

Designed for close-to-close realistic backtesting.

Position = cluster of previous bar

Fees applied only on regime switches. Meaning:

Staying long → no fee

Switching long→short → fee applied

Switching any→cash → fee applied

Fee input is percentage, but script already converts internally.

Disclaimers

⚠️ This indicator uses machine-learning but does not predict the future. It classifies similarity to past regimes, nothing more.

⚠️ Backtest results are not indicative of future performance.

⚠️ Clusters have no inherent “bullish” or “bearish” meaning. You must interpret them based on your testing and your own feature engineering.

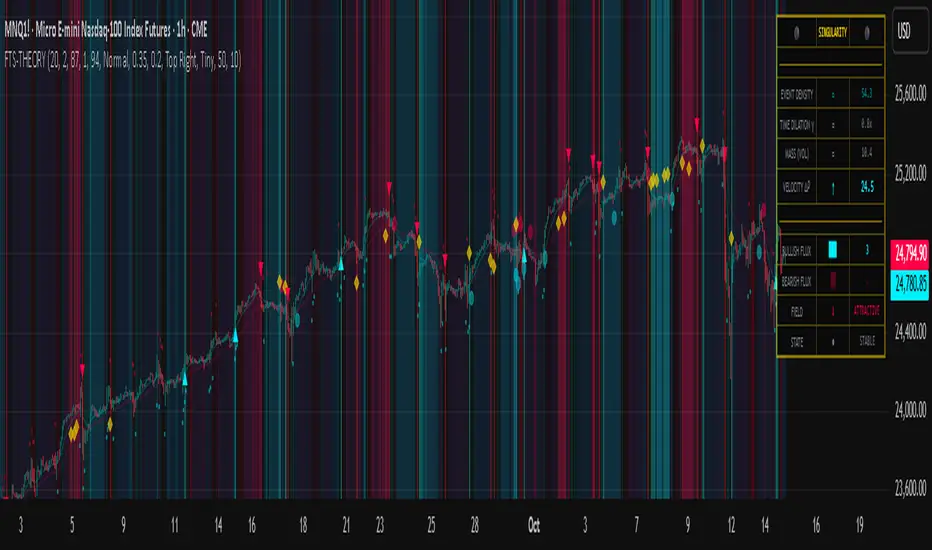

Flux-Tensor Singularity [FTS]Flux-Tensor Singularity - Multi-Factor Market Pressure Indicator

The Flux-Tensor Singularity (FTS) is an advanced multi-factor oscillator that combines volume analysis, momentum tracking, and volatility-weighted normalization to identify critical market inflection points. Unlike traditional single-factor indicators, FTS synthesizes price velocity, volume mass, and volatility context into a unified framework that adapts to changing market regimes.

This indicator identifies extreme market conditions (termed "singularities") where multiple confirming factors converge, then uses a sophisticated scoring system to determine directional bias. It is designed for traders seeking high-probability setups with built-in confluence requirements.

THEORETICAL FOUNDATION

The indicator is built on the premise that market time is not constant - different market conditions contain varying levels of information density. A 1-minute bar during a major news event contains far more actionable information than a 1-minute bar during overnight low-volume trading. Traditional indicators treat all bars equally; FTS does not.

The theoretical framework draws conceptual parallels to physics (purely as a mental model, not literal physics):

Volume as Mass: Large volume represents significant market participation and "weight" behind price moves. Just as massive objects have stronger gravitational effects, high-volume moves carry more significance.

Price Change as Velocity: The rate of price movement through price space represents momentum and directional force.

Volatility as Time Dilation: When volatility is high relative to its historical norm, the "information density" of each bar increases. The indicator weights these periods more heavily, similar to how time dilates near massive objects in physics.

This is a pedagogical metaphor to create a coherent mental model - the underlying mathematics are standard financial calculations combined in a novel way.

MATHEMATICAL FRAMEWORK

The indicator calculates a composite singularity value through four distinct steps:

Step 1: Raw Singularity Calculation

S_raw = (ΔP × V) × γ²

Where:

ΔP = Price Velocity = close - close

V = Volume Mass = log(volume + 1)

γ² = Time Dilation Factor = (ATR_local / ATR_global)²

Volume Transformation: Volume is log-transformed because raw volume can have extreme outliers (10x-100x normal). The logarithm compresses these spikes while preserving their significance. This is standard practice in volume analysis.

Volatility Weighting: The ratio of short-term ATR (5 periods) to long-term ATR (user-defined lookback) is squared to create a volatility amplification factor. When local volatility exceeds global volatility, this ratio increases, amplifying the raw singularity value. This makes the indicator regime-aware.

Step 2: Normalization

The raw singularity values are normalized to a 0-100 scale using a stochastic-style calculation:

S_normalized = ((S_raw - S_min) / (S_max - S_min)) × 100

Where S_min and S_max are the lowest and highest raw singularity values over the lookback period.

Step 3: Epsilon Compression

S_compressed = 50 + ((S_normalized - 50) / ε)

This is the critical innovation that makes the sensitivity control functional. By applying compression AFTER normalization, the epsilon parameter actually affects the final output:

ε < 1.0: Expands range (more signals)

ε = 1.0: No change (default)

ε > 1.0: Compresses toward 50 (fewer, higher-quality signals)

For example, with ε = 2.0, a normalized value of 90 becomes 70, making threshold breaches rarer and more significant.

Step 4: Smoothing

S_final = EMA(S_compressed, smoothing_period)

An exponential moving average removes high-frequency noise while preserving trend.

SIGNAL GENERATION LOGIC

When the tensor crosses above the upper threshold (default 90) or below the lower threshold (default 10), an extreme event is detected. However, the indicator does NOT immediately generate a buy or sell signal. Instead, it analyzes market context through a multi-factor scoring system:

Scoring Components:

Price Structure (+1 point): Current bar bullish/bearish

Momentum (+1 point): Price higher/lower than N bars ago

Trend Context (+2 points): Fast EMA above/below slow EMA (weighted heavier)

Acceleration (+1 point): Rate of change increasing/decreasing

Volume Multiplier (×1.5): If volume > average, multiply score

The highest score (bullish vs bearish) determines signal direction. This prevents the common indicator failure mode of "overbought can stay overbought" by requiring directional confirmation.

Signal Conditions:

A BUY signal requires:

Extreme event detection (tensor crosses threshold)

Bullish score > Bearish score

Price confirmation: Bullish candle (optional, user-controlled)

Volume confirmation: Volume > average (optional, user-controlled)

Momentum confirmation: Positive momentum (optional, user-controlled)

A SELL signal requires the inverse conditions.

INPUTS EXPLAINED - Core Parameters:

Global Horizon (Context): Default 20. Lookback period for normalization and volatility comparison. Higher values = smoother but less responsive. Lower values = more signals but potentially more noise.

Tensor Smoothing: Default 3. EMA period applied to final output. Removes "quantum foam" (high-frequency noise). Range 1-20.

Singularity Threshold: Default 90. Values above this (or below 100-threshold) trigger extreme event detection. Higher = rarer, stronger signals.

Signal Sensitivity (Epsilon): Default 1.0. Post-normalization compression factor. This is the key innovation - it actually works because it's applied AFTER normalization. Range 0.1-5.0.

Signal Interpreter Toggles:

Require Price Confirmation: Default ON. Only generates buy signals on bullish candles, sell signals on bearish candles. Reduces false signals but may delay entry.

Require Volume Confirmation: Default ON. Only signals when volume > average. Critical for stocks/crypto, less important for forex (unreliable volume data).

Use Momentum Filter: Default ON. Requires momentum agreement with signal direction. Prevents counter-trend signals.

Momentum Lookback: Default 5. Number of bars for momentum calculation. Shorter = more responsive, longer = trend-following bias.

Visual Controls:

Colors: Customizable colors for bullish flux, bearish flux, background, and event horizon.

Visual Transparency: Default 85. Master control for all visual elements (accretion disk, field lines, particles, etc.). Range 50-99. Signals and dashboard have separate controls.

Visibility Toggles: Individual on/off switches for:

Gravitational field lines (trend EMAs)

Field reversals (trend crossovers)

Accretion disk (background gradient)

Singularity diamonds (neutral extreme events)

Energy particles (volume bursts)

Event horizon flash (extreme event background)

Signal background flash

Signal Size: Tiny/Small/Normal triangle size

Signal Offsets: Separate controls for buy and sell signal vertical positioning (percentage of price)

Dashboard Settings:

Show Dashboard: Toggle on/off

Position: 9 placement options (all corners, centers, middles)

Text Size: Tiny/Small/Normal/Large

Background Transparency: 0-50, separate from visual transparency

VISUAL ELEMENTS EXPLAINED

1. Accretion Disk (Background Gradient):

A three-layer gradient background that intensifies as the tensor approaches extremes. The outer disk appears at any non-neutral reading, the inner disk activates above 70 or below 30, and the core layer appears above 85 or below 15. Color indicates direction (cyan = bullish, red = bearish). This provides instant visual feedback on market pressure intensity.

2. Gravitational Field Lines (EMAs):

Two trend-following EMAs (10 and 30 period) visualized as colored lines. These represent the "curvature" of market trend - when they diverge, trend is strong; when they converge, trend is weakening. Crossovers mark potential trend reversals.

3. Field Reversals (Circles):

Small circles appear when the fast EMA crosses the slow EMA, indicating a potential trend change. These are distinct from extreme events and appear at normal market structure shifts.

4. Singularity Diamonds:

Small diamond shapes appear when the tensor reaches extreme levels (>90 or <10) but doesn't meet the full signal criteria. These are "watch" events - extreme pressure exists but directional confirmation is lacking.

5. Energy Particles (Dots):

Tiny dots appear when volume exceeds 2× average, indicating significant participation. Color matches bar direction. These highlight genuine high-conviction moves versus low-volume drifts.

6. Event Horizon Flash:

A golden background flash appears the instant any extreme threshold is breached, before directional analysis. This alerts you to pay attention.

7. Signal Background Flash:

When a full buy/sell signal is confirmed, the background flashes cyan (buy) or red (sell). This is your primary alert that all conditions are met.

8. Signal Triangles:

The actual buy (▲) and sell (▼) markers. These only appear when ALL selected confirmation criteria are satisfied. Position is offset from bars to avoid overlap with other indicators.

DASHBOARD METRICS EXPLAINED

The dashboard displays real-time calculated values:

Event Density: Current tensor value (0-100). Above 90 or below 10 = critical. Icon changes: 🔥 (extreme high), ❄️ (extreme low), ○ (neutral).

Time Dilation (γ): Current volatility ratio squared. Values >2.0 indicate extreme volatility environments. >1.5 = elevated, >1.0 = above average. Icon: ⚡ (extreme), ⚠ (elevated), ○ (normal).

Mass (Vol): Log-transformed volume value. Compared to volume ratio (current/average). Icon: ● (>2× avg), ◐ (>1× avg), ○ (below avg).

Velocity (ΔP): Raw price change. Direction arrow indicates momentum direction. Shows the actual price delta value.

Bullish Flux: Current bullish context score. Displayed as both a bar chart (visual) and numeric value. Brighter when bullish score dominates.

Bearish Flux: Current bearish context score. Same visualization as bullish flux. These scores compete - the winner determines signal direction.

Field: Trend direction based on EMA relationship. "Repulsive" (uptrend), "Attractive" (downtrend), "Neutral" (ranging). Icon: ⬆⬇↔

State: Current market condition:

🚀 EJECTION: Buy signal active

💥 COLLAPSE: Sell signal active

⚠ CRITICAL: Extreme event, no directional confirmation

● STABLE: Normal market conditions

HOW TO USE THE INDICATOR

1. Wait for Extreme Events:

The indicator is designed to be selective. Don't trade every fluctuation - wait for tensor to reach >90 or <10. This alone is not a signal.

2. Check Context Scores:

Look at the Bullish Flux vs Bearish Flux in the dashboard. If scores are close (within 1-2 points), the market is indecisive - skip the trade.

3. Confirm with Signals:

Only act when a full triangle signal appears (▲ or ▼). This means ALL your selected confirmation criteria have been met.

4. Use with Price Structure:

Combine with support/resistance levels. A buy signal AT support is higher probability than a buy signal in the middle of nowhere.

5. Respect the Dashboard State:

When State shows "CRITICAL" (⚠), it means extreme pressure exists but direction is unclear. These are the most dangerous moments - wait for resolution.

6. Volume Matters:

Energy particles (dots) and the Mass metric tell you if institutions are participating. Signals without volume confirmation are lower probability.

MARKET AND TIMEFRAME RECOMMENDATIONS

Scalping (1m-5m):

Lookback: 10-14

Smoothing: 5-7

Threshold: 85

Epsilon: 0.5-0.7

Note: Expect more noise. Confirm with Level 2 data. Best on highly liquid instruments.

Intraday (15m-1h):

Lookback: 20-30 (default settings work well)

Smoothing: 3-5

Threshold: 90

Epsilon: 1.0

Note: Sweet spot for the indicator. High win rate on liquid stocks, forex majors, and crypto.

Swing Trading (4h-1D):

Lookback: 30-50

Smoothing: 3

Threshold: 90-95

Epsilon: 1.5-2.0

Note: Signals are rare but high conviction. Combine with higher timeframe trend analysis.

Position Trading (1D-1W):

Lookback: 50-100

Smoothing: 5-7

Threshold: 95

Epsilon: 2.0-3.0

Note: Extremely rare signals. Only trade the most extreme events. Expect massive moves.

Market-Specific Settings:

Forex (EUR/USD, GBP/USD, etc.):

Volume data is unreliable (spot forex has no centralized volume)

Disable "Require Volume Confirmation"

Focus on momentum and trend filters

News events create extreme singularities

Best on 15m-1h timeframes

Stocks (High-Volume Equities):

Volume confirmation is CRITICAL - keep it ON

Works excellently on AAPL, TSLA, SPY, etc.

Morning session (9:30-11:00 ET) shows highest event density

Earnings announcements create guaranteed extreme events

Best on 5m-1h for day trading, 1D for swing trading

Crypto (BTC, ETH, major alts):

Reduce threshold to 85 (crypto has constant high volatility)

Volume spikes are THE primary signal - keep volume confirmation ON

Works exceptionally well due to 24/7 trading and high volatility

Epsilon can be reduced to 0.7-0.8 for more signals

Best on 15m-4h timeframes

Commodities (Gold, Oil, etc.):

Gold responds to macro events (Fed announcements, geopolitical events)

Oil responds to supply shocks

Use daily timeframe minimum

Increase lookback to 50+

These are slow-moving markets - be patient

Indices (SPX, NDX, etc.):

Institutional volume matters - keep volume confirmation ON

Opening hour (9:30-10:30 ET) = highest singularity probability

Strong correlation with VIX - high VIX = more extreme events

Best on 15m-1h for day trading

WHAT MAKES THIS INDICATOR UNIQUE

1. Post-Normalization Sensitivity Control:

Unlike most oscillators where sensitivity controls don't actually work (they're applied before normalization, which then rescales everything), FTS applies epsilon compression AFTER normalization. This means the sensitivity parameter genuinely affects signal frequency. This is a novel implementation not found in standard oscillators.

2. Multi-Factor Confluence Requirement:

The indicator doesn't just detect "overbought" or "oversold" - it detects extreme conditions AND THEN analyzes context through five separate factors (price structure, momentum, trend, acceleration, volume). Most indicators are single-factor; FTS requires confluence.

3. Volatility-Weighted Normalization:

By squaring the ATR ratio (local/global), the indicator adapts to changing market regimes. A 1% move in a low-volatility environment is treated differently than a 1% move in a high-volatility environment. Traditional indicators treat all moves equally regardless of context.

4. Volume Integration at the Core:

Volume isn't an afterthought or optional filter - it's baked into the fundamental equation as "mass." The log transformation handles outliers elegantly while preserving significance. Most price-based indicators completely ignore volume.

5. Adaptive Scoring System:

Rather than fixed buy/sell rules ("RSI >70 = sell"), FTS uses competitive scoring where bullish and bearish evidence compete. The winner determines direction. This solves the classic problem of "overbought markets can stay overbought during strong uptrends."

6. Comprehensive Visual Feedback:

The multi-layer visualization system (accretion disk, field lines, particles, flashes) provides instant intuitive feedback on market state without requiring dashboard reading. You can see pressure building before extreme thresholds are hit.

7. Separate Extreme Detection and Signal Generation:

"Singularity diamonds" show extreme events that don't meet full criteria, while "signal triangles" only appear when ALL conditions are met. This distinction helps traders understand when pressure exists versus when it's actionable.

COMPARISON TO EXISTING INDICATORS

vs. RSI/Stochastic:

These normalize price relative to recent range. FTS normalizes (price change × log volume × volatility ratio) - a composite metric, not just price position.

vs. Chaikin Money Flow:

CMF combines price and volume but lacks volatility context and doesn't use adaptive normalization or post-normalization compression.

vs. Bollinger Bands + Volume:

Bollinger Bands show volatility but don't integrate volume or create a unified oscillator. They're separate components, not synthesized.

vs. MACD:

MACD is pure momentum. FTS combines momentum with volume weighting and volatility context, plus provides a normalized 0-100 scale.

The specific combination of log-volume weighting, squared volatility amplification, post-normalization epsilon compression, and multi-factor directional scoring is unique to this indicator.

LIMITATIONS AND PROPER DISCLOSURE

Not a Holy Grail:

No indicator is perfect. This tool identifies high-probability setups but cannot predict the future. Losses will occur. Use proper risk management.

Requires Confirmation:

Best used in conjunction with price action analysis, support/resistance levels, and higher timeframe trend. Don't trade signals blindly.

Volume Data Dependency:

On forex (spot) and some low-volume instruments, volume data is unreliable or tick-volume only. Disable volume confirmation in these cases.

Lagging Components:

The EMA smoothing and trend filters are inherently lagging. In extremely fast moves, signals may appear after the initial thrust.

Extreme Event Rarity:

With conservative settings (high threshold, high epsilon), signals can be rare. This is by design - quality over quantity. If you need more frequent signals, reduce threshold to 85 and epsilon to 0.7.

Not Financial Advice:

This indicator is an analytical tool. All trading decisions and their consequences are solely your responsibility. Past performance does not guarantee future results.

BEST PRACTICES

Don't trade every singularity - wait for context confirmation

Higher timeframes = higher reliability

Combine with support/resistance for entry refinement

Volume confirmation is CRITICAL for stocks/crypto (toggle off only for forex)

During major news events, singularities are inevitable but direction may be uncertain - use wider stops

When bullish and bearish flux scores are close, skip the trade

Test settings on your specific instrument/timeframe before live trading

Use the dashboard actively - it contains critical diagnostic information

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

Quantum Market Analyzer X7Quantum Market Analyzer X7 - Complete Study Guide

Table of Contents

1. Overview

2. Indicator Components

3. Signal Interpretation

4. Live Market Analysis Guide

5. Best Practices

6. Limitations and Considerations

7. Risk Disclaimer

________________________________________

Overview

The Quantum Market Analyzer X7 is a comprehensive multi-timeframe technical analysis indicator that combines traditional and modern analytical methods. It aggregates signals from multiple technical indicators across seven key analysis categories to provide traders with a consolidated view of market sentiment and potential trading opportunities.

Key Features:

• Multi-Indicator Analysis: Combines 20+ technical indicators

• Real-Time Dashboard: Professional interface with customizable display

• Signal Aggregation: Weighted scoring system for overall market sentiment

• Advanced Analytics: Includes Order Block detection, Supertrend, and Volume analysis

• Visual Progress Indicators: Easy-to-read progress bars for signal strength

________________________________________

Indicator Components

1. Oscillators Section

Purpose: Identifies overbought/oversold conditions and momentum changes

Included Indicators:

• RSI (14): Relative Strength Index - momentum oscillator

• Stochastic (14): Compares closing price to price range

• CCI (20): Commodity Channel Index - cycle identification

• Williams %R (14): Momentum indicator similar to Stochastic

• MACD (12,26,9): Moving Average Convergence Divergence

• Momentum (10): Rate of price change

• ROC (9): Rate of Change

• Bollinger Bands (20,2): Volatility-based indicator

Signal Interpretation:

• Strong Buy (6+ points): Multiple oscillators indicate oversold conditions

• Buy (2-5 points): Moderate bullish momentum

• Neutral (-1 to 1 points): Balanced conditions

• Sell (-2 to -5 points): Moderate bearish momentum

• Strong Sell (-6+ points): Multiple oscillators indicate overbought conditions

2. Moving Averages Section

Purpose: Determines trend direction and strength

Included Indicators:

• SMA: 10, 20, 50, 100, 200 periods

• EMA: 10, 20, 50 periods

Signal Logic:

• Price >2% above MA = Strong Buy (+2)

• Price above MA = Buy (+1)

• Price below MA = Sell (-1)

• Price >2% below MA = Strong Sell (-2)

Signal Interpretation:

• Strong Buy (6+ points): Price well above multiple MAs, strong uptrend

• Buy (2-5 points): Price above most MAs, bullish trend

• Neutral (-1 to 1 points): Mixed MA signals, consolidation

• Sell (-2 to -5 points): Price below most MAs, bearish trend

• Strong Sell (-6+ points): Price well below multiple MAs, strong downtrend

3. Order Block Analysis

Purpose: Identifies institutional support/resistance levels and breakouts

How It Works:

• Detects historical levels where large orders were placed

• Monitors price behavior around these levels

• Identifies breakouts from established order blocks

Signal Types:

• BULLISH BRK (+2): Breakout above resistance order block

• BEARISH BRK (-2): Breakdown below support order block

• ABOVE SUP (+1): Price holding above support

• BELOW RES (-1): Price rejected at resistance

• NEUTRAL (0): No significant order block interaction

4. Supertrend Analysis

Purpose: Trend following indicator based on Average True Range

Parameters:

• ATR Period: 10 (default)

• ATR Multiplier: 6.0 (default)

Signal Types:

• BULLISH (+2): Price above Supertrend line

• BEARISH (-2): Price below Supertrend line

• NEUTRAL (0): Transition period

5. Trendline/Channel Analysis

Purpose: Identifies trend channels and breakout patterns

Components:

• Dynamic trendline calculation using pivot points

• Channel width based on historical volatility

• Breakout detection algorithm

Signal Types:

• UPPER BRK (+2): Breakout above upper channel

• LOWER BRK (-2): Breakdown below lower channel

• ABOVE MID (+1): Price above channel midline

• BELOW MID (-1): Price below channel midline

6. Volume Analysis

Purpose: Confirms price movements with volume data

Components:

• Volume spikes detection

• On Balance Volume (OBV)

• Volume Price Trend (VPT)

• Money Flow Index (MFI)

• Accumulation/Distribution Line

Signal Calculation: Multiple volume indicators are combined to determine institutional activity and confirm price movements.

________________________________________

Signal Interpretation

Overall Summary Signals

The indicator aggregates all component signals into an overall market sentiment:

Signal Score Range Interpretation Action

STRONG BUY 10+ Overwhelming bullish consensus Consider long positions

BUY 4-9 Moderate to strong bullish bias Look for long opportunities

NEUTRAL -3 to 3 Mixed signals, consolidation Wait for clearer direction

SELL -4 to -9 Moderate to strong bearish bias Look for short opportunities

STRONG SELL -10+ Overwhelming bearish consensus Consider short positions

Progress Bar Interpretation

• Filled bars indicate signal strength

• Green bars: Bullish signals

• Red bars: Bearish signals

• More filled bars = stronger conviction

________________________________________

Live Market Analysis Guide

Step 1: Initial Assessment

1. Check Overall Summary: Start with the main signal

2. Verify with Component Analysis: Ensure signals align

3. Look for Divergences: Identify conflicting signals

Step 2: Timeframe Analysis

1. Set Appropriate Timeframe: Use 1H for intraday, 4H/1D for swing trading

2. Multi-Timeframe Confirmation: Check higher timeframes for trend context

3. Entry Timing: Use lower timeframes for precise entry points

Step 3: Signal Confirmation Process.

For Buy Signals:

1. Oscillators: Look for oversold conditions (RSI <30, Stoch <20)

2. Moving Averages: Price should be above key MAs

3. Order Blocks: Confirm bounce from support levels

4. Volume: Check for accumulation patterns

5. Supertrend: Ensure bullish trend alignment.

For Sell Signals:

1. Oscillators: Look for overbought conditions (RSI >70, Stoch >80)

2. Moving Averages: Price should be below key MAs

3. Order Blocks: Confirm rejection at resistance levels

4. Volume: Check for distribution patterns

5. Supertrend: Ensure bearish trend alignment.

Step 4: Risk Management Integration

1. Signal Strength Assessment: Stronger signals = larger position size

2. Stop Loss Placement: Use Order Block levels for stops

3. Take Profit Targets: Based on channel analysis and resistance levels

4. Position Sizing: Adjust based on signal confidence

________________________________________

Best Practices

Entry Strategies

1. High Conviction Entries: Wait for STRONG BUY/SELL signals

2. Confluence Trading: Look for multiple components aligning

3. Breakout Trading: Use Order Block and Trendline breakouts

4. Trend Following: Align with Supertrend direction.

Risk Management

1. Never Risk More Than 2% Per Trade: Regardless of signal strength

2. Use Stop Losses: Place at invalidation levels

3. Scale Positions: Stronger signals warrant larger (but still controlled) positions

4. Diversification: Don't rely solely on one indicator.

Market Conditions

1. Trending Markets: Focus on Supertrend and MA signals

2. Range-Bound Markets: Emphasize Oscillator and Order Block signals

3. High Volatility: Reduce position sizes, widen stops

4. Low Volume: Be cautious of breakout signals.

Common Mistakes to Avoid

1. Signal Chasing: Don't enter after signals have already moved significantly

2. Ignoring Context: Consider overall market conditions

3. Overtrading: Wait for high-quality setups

4. Poor Risk Management: Always use appropriate position sizing

________________________________________

Limitations and Considerations

Technical Limitations

1. Lagging Nature: All technical indicators are based on historical data

2. False Signals: No indicator is 100% accurate

3. Market Regime Changes: Indicators may perform differently in various market conditions

4. Whipsaws: Possible in choppy, sideways markets.

Optimal Use Cases

1. Trending Markets: Performs best in clear trending environments

2. Medium to High Volatility: Requires sufficient price movement for signals

3. Liquid Markets: Works best with adequate volume and tight spreads

4. Multiple Timeframe Analysis: Most effective when used across different timeframes.

When to Use Caution

1. Major News Events: Fundamental analysis may override technical signals

2. Market Opens/Closes: Higher volatility can create false signals

3. Low Volume Periods: Signals may be less reliable

4. Holiday Trading: Reduced participation affects signal quality

________________________________________

Risk Disclaimer

IMPORTANT LEGAL DISCLAIMER FROM aiTrendview

WARNING: TRADING INVOLVES SUBSTANTIAL RISK OF LOSS

This Quantum Market Analyzer X7 indicator ("the Indicator") is provided for educational and informational purposes only. By using this indicator, you acknowledge and agree to the following terms:

No Investment Advice

• The Indicator does NOT constitute investment advice, financial advice, or trading recommendations

• All signals generated are based on historical price data and mathematical calculations

• Past performance does not guarantee future results

• No representation is made that any account will achieve profits or losses similar to those shown.

Risk Acknowledgment

• TRADING CARRIES SUBSTANTIAL RISK: You may lose some or all of your invested capital

• LEVERAGE AMPLIFIES RISK: Margin trading can result in losses exceeding your initial investment

• MARKET VOLATILITY: Financial markets are inherently unpredictable and volatile

• TECHNICAL ANALYSIS LIMITATIONS: No technical indicator is infallible or guarantees profitable trades.

User Responsibility

• YOU ARE SOLELY RESPONSIBLE for all trading decisions and their consequences

• CONDUCT YOUR OWN RESEARCH: Always perform independent analysis before making trading decisions

• CONSULT PROFESSIONALS: Seek advice from qualified financial advisors

• RISK MANAGEMENT: Implement appropriate risk management strategies

No Warranties

• The Indicator is provided "AS IS" without warranties of any kind

• aiTrendview makes no representations about the accuracy, reliability, or suitability of the Indicator

• Technical glitches, data feed issues, or calculation errors may occur

• The Indicator may not work as expected in all market conditions.

Limitation of Liability

• aiTrendview SHALL NOT BE LIABLE for any direct, indirect, incidental, or consequential damages

• This includes but is not limited to: trading losses, missed opportunities, data inaccuracies, or system failures

• MAXIMUM LIABILITY is limited to the amount paid for the indicator (if any)

Code Usage and Distribution

• This indicator is published on TradingView in accordance with TradingView's house rules

• UNAUTHORIZED MODIFICATION or redistribution of this code is prohibited

• Users may not claim ownership of this intellectual property

• Commercial use requires explicit written permission from aiTrendview.

Compliance and Regulations

• VERIFY LOCAL REGULATIONS: Ensure compliance with your jurisdiction's trading laws

• Some trading strategies may not be suitable for all investors

• Tax implications of trading are your responsibility

• Report trading activities as required by law

Specific Risk Factors

1. False Signals: The Indicator may generate incorrect buy/sell signals

2. Market Gaps: Overnight gaps can invalidate technical analysis

3. Fundamental Events: News and economic data can override technical signals

4. Liquidity Risk: Some markets may have insufficient liquidity

5. Technology Risk: Platform failures or connectivity issues may prevent order execution.

Professional Trading Warning

• THIS IS NOT PROFESSIONAL TRADING SOFTWARE: Not intended for institutional or professional trading

• NO REGULATORY APPROVAL: This indicator has not been approved by any financial regulatory authority

• EDUCATIONAL PURPOSE: Designed primarily for learning technical analysis concepts

FINAL WARNING

NEVER INVEST MONEY YOU CANNOT AFFORD TO LOSE

Trading financial instruments involves significant risk. The majority of retail traders lose money. Before using this indicator in live trading:

1. Practice on paper/demo accounts extensively

2. Start with small position sizes

3. Develop a comprehensive trading plan

4. Implement strict risk management rules

5. Continuously educate yourself about market dynamics

By using the Quantum Market Analyzer X7, you acknowledge that you have read, understood, and agree to this disclaimer. You assume full responsibility for all trading decisions and their outcomes.

Contact: For questions about this disclaimer or the indicator, contact aiTrendview through official TradingView channels only.

________________________________________

This study guide and indicator are published on TradingView in compliance with TradingView's community guidelines and house rules. All users must adhere to TradingView's terms of service when using this indicator.

Document Version: 1.0

Publisher: aiTrendview

________________________________________

Disclaimer

The content provided in this blog post is for educational and training purposes only. It is not intended to be, and should not be construed as, financial, investment, or trading advice. All charting and technical analysis examples are for illustrative purposes. Trading and investing in financial markets involve substantial risk of loss and are not suitable for every individual. Before making any financial decisions, you should consult with a qualified financial professional to assess your personal financial situation.

Aquantprice: Institutional Structure MatrixSETUP GUIDE

Open TradingView

Go to Indicators

Search: Aquantprice: Institutional Structure Matrix

Click Add to Chart

Customize:

Min Buy = 10, Min Sell = 7

Show only PP, R1, S1, TC, BC

Set Decimals = 5 (Forex) or 8 (Crypto)

USE CASES & TRADING STRATEGIES

1. CPR Confluence Trading (Most Popular)

Rule: Enter when ≥3 timeframes show Buy ≥10/15 or Sell ≥7/13

text Example:

Daily: 12/15 Buy

Weekly: 11/15 Buy

Monthly: 10/15 Buy

→ **STRONG LONG BIAS**

Enter on pullback to nearest **S1 or L3**

2. Hot Zone Scalping (Forex & Indices)

Rule: Trade only when price is in Hot Zone (closest 2 levels)

text Hot: S1-PP → Expect bounce or breakout

Action:

- Buy at S1 if Buy Count ↑

- Sell at PP if Sell Count ↑

3. Institutional Reversal Setup

Rule: Price at H3/L3 + Reversal Condition

text Scenario:

Price touches **Monthly L3**

L3 in **Hot Zone**

Buy Count = 13/15

→ **High-Probability Reversal Long**

4. CPR Width Filter (Avoid Choppy Markets)

Rule: Trade only if CPR Label = "Strong Trend"

text CPR Size < 0.25 → Trending

CPR Size > 0.75 → Sideways (Avoid)

5. Multi-Timeframe Bias Dashboard

Use "Buy" and "Sell" columns as a sentiment meter

TimeframeBuySellBiasDaily123BullishWeekly89BearishMonthly112Bullish

→ Wait for alignment before entering

HOW TO READ THE TABLE

Column Meaning Time frame D, W, M, 3M, 6M, 12MOpen Price Current session open PP, TC, BC, etc. Pivot levels (color-coded if in Hot Zone) Buy X/15 conditions met (≥10 = Strong Buy)Sell X/13 conditions met (≥7 = Strong Sell)CPR Size Histogram + Label (Trend vs Range)Zone Hot: PP-S1, Med: S2-L3, etc. + PP Distance

PRO TIPS

Best on 5M–1H charts for entries

Use with volume or order flow for confirmation

Set alerts on Buy ≥12/15 or Sell ≥10/13

Hide unused levels to reduce clutter

Combine with AQuantPrice Dashboard (Small TF) for full system

IDEAL MARKETS

Forex (EURUSD, GBPUSD, USDJPY)

Indices (NAS100, SPX500, DAX)

Crypto (BTC, ETH – use 6–8 decimals)

Commodities (Gold, Oil)

🚀 **NEW INDICATOR ALERT**

**Aquantprice: Institutional Structure Matrix**

The **ALL-IN-ONE CPR Dashboard** used by smart money traders.

✅ **6 Timeframes in 1 Table** (Daily → Yearly)

✅ **15 Buy + 13 Sell Conditions** (Institutional Logic)

✅ **Hot Zones, CPR Width, PP Distance**

✅ **Fully Customizable – Show/Hide Any Level**

✅ **Real-Time Zone Detection** (Hot, Med, Low)

✅ **Precision up to 8 Decimals**

**No more switching charts. No more confusion.**

See **where institutions are positioned** — instantly.

👉 **Add to Chart Now**: Search **"Aquantprice: Institutional Structure Matrix"**

🔥 **Free Access | Pro-Level Insights**

*By AQuant – Trusted by 10,000+ Traders*

#CPR #PivotTrading #SmartMoney #TradingView

FINAL TAGLINE

"See What Institutions See — Before They Move."

Aquantprice: Institutional Structure Matrix

Your Edge. One Dashboard.

VIX Regime AnalyzerVIX Regime Analyzer

The VIX Regime Analyzer is an analytical tool that examines historical VIX patterns to provide insights into how your asset typically performs under similar volatility conditions.

Key Features:

Historical Pattern Matching: Automatically scans up to 1,000 bars of history to find all periods when VIX was at levels similar to today, using customizable tolerance ranges (absolute or percentage-based).

Forward-Looking Statistics: For each VIX regime match, calculates what actually happened to your asset over the next 1, 5, 10, and 20 trading days, providing both average returns and probability of positive outcomes.

Regime Classification System: Intelligently categorizes the current market environment as bullish or bearish: Visual Historical Context:

Background shading throughout your chart highlights every historical period when VIX matched current levels, color-coded by subsequent performance (green for gains, red for losses).

User Inputs:

VIX Level Tolerance (+/-): How closely VIX must match (default: ±5 points)

Use Relative Tolerance (%): Switch to percentage-based matching for consistency across different VIX levels

Lookback Period: How many bars to analyze

Highlight Historical VIX Matches: Toggle background highlighting of past matching periods

The Data Table

The statistics box appears in the right handside of your chart and contains three main sections:

Section 1: VIX REGIME

Current VIX: The live VIX closing price

Range: The tolerance band being searched (e.g., if VIX is 18 with ±5 tolerance, range is 13-23)

Historical Samples: Number of matching periods found in the lookback window (minimum 10 required for statistical validity)

Section 2: FORWARD RETURN

Shows the average percentage change in your asset over different timeframes following similar VIX levels:

Avg Next Day: What typically happened by the next trading session

Avg Next 5 Days: Average 5-day forward performance

Avg Next 10 Days: Average 10-day forward performance

Avg Next 20 Days: Average 20-day forward performance (approximately 1 month)

Section 3: PROBABILITY UP

Shows the win rate - the percentage of times your asset closed higher after VIX matched current levels:

Next Day: Probability of being up the next session

Next 5 Days: Probability of being up after 5 days

Next 10 Days: Probability of being up after 10 days

Next 20 Days: Probability of being up after 20 days

Colors:

🟢 Green: Bullish regimes (various strengths)

🔴 Red: Bearish regimes (various strengths)

🟡 Yellow: Choppy/uncertain regime

When "Highlight Historical VIX Matches" is enabled:

Scroll back through your chart and you'll see colored backgrounds highlighting every period when VIX matched today's level. The color tells you whether that match led to gains (green) or losses (red). This provides instant visual pattern recognition - you can quickly see if similar VIX levels historically led to bullish or bearish outcomes.

Practical Example:

If you see that most historical periods with similar VIX levels are highlighted in green, it suggests the current VIX level has historically been a bullish signal for your asset.

How The Indicator Makes Decisions

The regime classification uses both magnitude AND probability to avoid false signals:

Example of Strong Classification:

Average 5-day return: +1.5%

Win rate: 65%

Result: STRONG BULLISH (both high return and high probability)

Example of Weak Signal:

Average 5-day return: +2.0%

Win rate: 35%

Result: CHOPPY (high average but low consistency = unreliable)

This dual-factor approach ensures the indicator doesn't mislead you with regimes that had a few huge winners but mostly losers, or vice versa.

Best Practices

Combine with your existing strategy: Use this as a regime filter rather than standalone signals

Check sample size: More historical matches = more reliable statistics

Consider multiple timeframes: If 5-day and 20-day metrics disagree, proceed with caution

Asset-specific tuning: Different assets may require different tolerance settings

VIX spikes: The indicator is particularly useful during VIX spikes to understand if panic is justified

What Makes This Different

Unlike simple VIX indicators that just plot the fear index, this tool:

Quantifies the actual impact of VIX levels on YOUR specific asset

Provides probability-based forecasts rather than subjective interpretation

Shows historical context visually so you can see patterns at a glance

Uses rigorous statistical criteria to avoid false regime classifications

Advanced Psychological Levels with Dynamic Spacing═══════════════════════════════════════

ADVANCED PSYCHOLOGICAL LEVELS WITH DYNAMIC SPACING

═══════════════════════════════════════

A comprehensive psychological price level indicator that automatically identifies and displays round number levels across multiple timeframes. Features dynamic ATR-based spacing, smart crypto detection, distance tracking, and customizable alert system.

───────────────────────────────────────

WHAT THIS INDICATOR DOES

───────────────────────────────────────

This indicator automatically draws psychological price levels (round numbers) that often act as support and resistance:

- Dynamic ATR-Based Spacing - Adapts level spacing to market volatility

- Multiple Level Types - Major (250 pip), Standard (100 pip), Mid, and Intraday levels

- Smart Asset Detection - Automatically adjusts for Forex, Crypto, Indices, and CFDs

- Crypto Price Adaptation - Intelligent level spacing based on cryptocurrency price magnitude

- Distance Information Table - Real-time percentage distance to nearest levels

- Combined Level Labels - Clear identification when multiple level types coincide

- Performance Optimized - Configurable visible range and label limits

- Comprehensive Alerts - Notifications when price crosses any level type

───────────────────────────────────────

HOW IT WORKS

───────────────────────────────────────

PSYCHOLOGICAL LEVELS CONCEPT:

Psychological levels are round numbers where traders tend to place orders, creating natural support and resistance zones. These include:

- Forex: 1.0000, 1.0100, 1.0050 (pips)

- Crypto: $100, $1,000, $10,000 (whole numbers)

- Indices: 10,000, 10,500, 11,000 (points)

Why They Matter:

- Traders naturally gravitate to round numbers

- Stop losses cluster at these levels

- Take profit orders concentrate here

- Institutional algorithmic trading often targets these levels

DYNAMIC ATR-BASED SPACING:

Traditional Method:

- Fixed spacing regardless of volatility

- May be too tight in volatile markets

- May be too wide in quiet markets

Dynamic Method (Recommended):

- Uses ATR (Average True Range) to measure volatility

- Automatically adjusts level spacing

- Tighter levels in low volatility

- Wider levels in high volatility

Calculation:

1. Calculate ATR over specified period (default: 14)

2. Multiply by ATR multiplier (default: 2.0)

3. Round to nearest psychological level

4. Generate levels at dynamic intervals

Benefits:

- Adapts to market conditions

- More relevant levels in all volatility regimes

- Reduces clutter in trending markets

- Provides more detail in ranging markets

LEVEL TYPES:

Major Levels (250 pip/point):

- Highest significance

- Primary support/resistance zones

- Color: Red (default)

- Style: Solid lines

- Spacing: 2.5x standard step

Standard Levels (100 pip/point):

- Secondary importance

- Common psychological barriers

- Color: Blue (default)

- Style: Dashed lines

- Spacing: Standard step

Mid Levels (50% between major):

- Optional intermediate levels

- Halfway between major levels

- Color: Gray (default)

- Style: Dotted lines

- Usage: Additional confluence points

Intraday Levels (sub-100 pip):

- For intraday traders

- Fine-grained precision

- Color: Yellow (default)

- Style: Dotted lines

- Only shown on intraday timeframes

SMART ASSET DETECTION:

Forex Pairs:

- Detects major currency pairs automatically

- Uses pip-based calculations

- Standard: 100 pips (0.0100)

- Major: 250 pips (0.0250)

- Intraday: 20, 50, 80 pip subdivisions

Cryptocurrencies:

- Automatic price magnitude detection

- Adaptive spacing based on price:

* Under $0.10: Levels at $0.01, $0.05

* $0.10-$1: Levels at $0.10, $0.50

* $1-$10: Levels at $1, $5

* $10-$100: Levels at $10, $50

* $100-$1,000: Levels at $100, $500

* $1,000-$10,000: Levels at $1,000, $5,000

* Over $10,000: Levels at $5,000, $10,000

Indices & CFDs:

- Fixed point-based system

- Major: 500 point intervals (with 250 sub-levels)

- Standard: 100 point intervals

- Suitable for stock indices like SPX, NASDAQ

COMBINED LEVEL LABELS:

When multiple level types coincide at the same price:

- Single line drawn (highest priority color)

- Combined label shows all types

- Priority: Major > Standard > Mid > Intraday

Example Label Formats:

- "1.1000 Major" - Major level only

- "1.1000 Std + Major" - Both standard and major

- "50000 Intra + Mid + Std" - Three levels coincide

Benefits:

- Cleaner chart appearance

- Clear identification of confluence

- Reduced visual clutter

- Easy to spot high-importance levels

DISTANCE INFORMATION TABLE:

Real-time tracking of nearest levels:

Table Contents:

- Nearest major level above (price and % distance)

- Nearest standard level above (price and % distance)

- Nearest standard level below (price and % distance)

Display:

- Top right corner (configurable)

- Color-coded by level type

- Real-time percentage calculations

- Helpful for position management

Usage:

- Identify proximity to key levels

- Set realistic profit targets

- Gauge potential move magnitude

- Monitor approaching resistance/support

ALERT SYSTEM:

Comprehensive crossing alerts:

Alert Types:

- Major Level Crosses

- Standard Level Crosses

- Intraday Level Crosses

Alert Modes:

- First Cross Only: Alert once when level is crossed

- All Crosses: Alert every time level is crossed

Alert Information:

- Level type crossed

- Specific price level

- Direction (above/below)

- One alert per bar to prevent spam

Configuration:

- Enable/disable by level type

- Choose alert frequency

- Customize for your trading style

───────────────────────────────────────

HOW TO USE

───────────────────────────────────────

INITIAL SETUP:

General Settings:

1. Enable "Use Dynamic ATR-Based Spacing" (recommended)

2. Set ATR Period (14 is standard)

3. Adjust ATR Multiplier (2.0 is balanced)

Visibility Settings:

1. Set Visible Range % (10% recommended for clarity)

2. Adjust Label Offset for readability

3. Configure performance limits if needed

Level Selection:

1. Enable/disable level types based on trading style

2. Adjust line counts for each type

3. Choose line styles and colors for visibility

TRADING STRATEGIES:

Breakout Trading:

1. Wait for price to approach major or standard level

2. Monitor for consolidation near level

3. Enter on confirmed break above/beyond level

4. Stop loss just beyond the broken level

5. Target: Next major or standard level

Rejection Trading:

1. Identify major psychological level

2. Wait for price to test the level

3. Look for rejection signals (wicks, bearish/bullish candles)

4. Enter in direction of rejection

5. Stop beyond the level

6. Target: Previous level or mid-level

Range Trading:

1. Identify range between two major levels

2. Buy at lower psychological level