Trading Sessions with Holidays & Timer🌍 Trading Sessions Matter

Markets breathe in cycles. When Tokyo, London, or New York steps in, liquidity shifts and price often reacts fast.

Example: New York closed BTC at $110K, and when traders woke up, the price was already $113K. That gap says everything about overnight pressure and the next move.

⚡ Indicator Features

✅ Session boxes (Tokyo, London, NY) with custom colors & time zones

✅ Open/close lines → spot gaps & momentum

✅ Average price per session → see where pressure builds

✅ Tick range → quick volatility check

✅ 🏖 Holiday markers → avoid false quiet markets

✅ Live status table → session OPEN / CLOSED + countdown timer

🚀 How to Use

Works on intraday timeframes (1m–4h)

Watch session opens/closes → liquidity shift points

Compare ranges & averages between Tokyo, London, NY

Use the timer to prep before the next wave

This tool helps you visualize the heartbeat of global markets session by session.

🔖 #BTCUSDT #Forex #TradingSessions #Crypto #DayTrading

Cari dalam skrip untuk "Cycle"

True Open CalculationsIndicator Description: True Open Calculations

This custom Pine Script indicator calculates and plots key "True Open" levels based on specific time intervals and trading sessions. The True Open levels represent significant price points on the chart, helping traders identify key reference points tied to various market opening times. These levels are important for understanding price action in relation to market sessions and trading cycles. The indicator is designed to plot lines corresponding to different "True Opens" on the chart and display labels with the associated information.

Key Features:

True Year Open:

This represents the opening price on the first Monday of April each year. It serves as a reference point for the yearly price level.

Plot Color: Green.

True Month Open:

This represents the opening price on the second Monday of each month. It helps in identifying monthly trends and provides a key reference for monthly price movements.

Plot Color: Blue.

True Week Open:

This represents the opening price every Monday at 6:00 PM. It gives traders a level to track weekly opening movements and can be useful for weekly trend analysis.

Plot Color: Orange.

True Day Open:

This represents the opening price at 12:00 AM (midnight) each day. It serves as a daily benchmark for price action at the start of the trading day.

Plot Color: Red.

True New York Session Open:

This represents the opening price at 7:30 AM (New York session start time). This level is crucial for traders focused on the New York trading session.

Plot Color: Purple.

Additional Features:

Labels: The indicator displays labels to the right of each plotted line to describe which "True Open" it represents (e.g., "True Year Open," "True Month Open," etc.).

Dynamic Plotting: The lines are only plotted on the current candle, and the lines are dynamically updated for each time period based on the corresponding "True Open."

Visual Cues: The colors of the plotted lines (green, blue, orange, red, purple) help quickly distinguish between different "True Open" levels, making it easy for traders to track price action and make informed decisions.

Use Cases:

Yearly, Monthly, Weekly, Daily, and Session Benchmarking: This indicator provides traders with important price levels to use as benchmarks for the current year, month, week, and day, helping to identify trends and potential reversals.

Session Awareness: It is particularly useful for traders who want to track key market sessions, such as the New York session, and their impact on price movement.

Long-term Analysis: By including the yearly open, this indicator helps traders gain a broader perspective on market trends and provides context for analyzing shorter-term price movements.

Benefits:

Helps identify important reference points for longer-term trends (yearly, monthly) as well as shorter-term moves (daily, weekly, and session).

Visually intuitive with color-coded lines and labels, allowing quick and easy identification of key market open levels.

Dynamic and real-time: The indicator plots and updates the True Open levels dynamically as the market progresses.

Trading Sessions Highs/Lows | InvrsROBINHOODTrading Sessions Highs/Lows | InvrsROBINHOOD

🚀 A powerful indicator for tracking key trading sessions and the highs and lows of each session!

📌 Description

The Trading Sessions Highs/Lows indicator visually marks the most critical trading sessions—Asia, London, and New York—using small colored dots at the bottom of the candle. It also tracks and plots the highs and lows of each session, along with the Daily Open and Weekly Open levels.

This tool is designed to help traders identify session-based liquidity zones, price reactions, and potential trade setups with minimal chart clutter.

Key Features:

✅ Session markers (Asia, London, NY AM, NY Lunch, NY PM) plotted as small dots

✅ Plots session highs and lows for market structure insights

✅ Daily Open line for intraday reference

✅ Weekly Open line for higher timeframe bias

✅ Alerts for session high/low breaks to capture momentum shifts

✅ User-defined UTC offset for global traders

✅ Customizable session colors for personal preference

📖 How to Use the Indicator

1️⃣ Understanding the Sessions

Asia Session (Yellow Dot) → Marks liquidity buildup & pre-London moves

London Session (Blue Dot) → Strong volatility, breakout opportunities

New York AM Session (Green Dot) → Major trends & institutional participation

New York Lunch (Red Dot) → Low volume, ranging market

New York PM Session (Dark Green Dot) → End-of-day movements & reversals

2️⃣ Session Highs & Lows for Market Structure

Session Highs can act as resistance or breakout points.

Session Lows can act as support or stop-hunt zones.

Break of a session high/low with volume may indicate continuation or reversal.

3️⃣ Using the Daily & Weekly Open

The Daily Open (Black Line) helps gauge the intraday trend.

Above Daily Open → Bearish Bias

Below Daily Open → Bullish Bias

The Weekly Open (Red Line) sets the higher timeframe directional bias.

4️⃣ Alerts for Breakouts

The indicator will trigger alerts when price breaks session highs or lows.

Useful for setting stop-losses, breakout trades, and risk management.

💡 Why This Indicator is Important for Beginners

1️⃣ Avoids Overtrading:

Many beginners trade in low-volume periods (NY Lunch, Asia session) and get stuck in choppy price action.

This indicator highlights when volatility is high so traders focus on better opportunities.

2️⃣ Session-Based Liquidity Traps:

Market makers often run stops at session highs/lows before reversing.

Watching session breaks prevents traders from falling into liquidity grabs.

3️⃣ Reduces Emotional Trading:

If price is above the Daily Open, a beginner shouldn’t look for shorts.

If price is below a key session low, it may signal a fake breakout.

4️⃣ Aligns with Institutional Trading:

Smart money traders use session highs/lows to set stop hunts & reversals.

Beginners can use this indicator to spot these zones before entering trades.

🛡️ How to Mitigate Risk with This Indicator

✅ Wait for Confirmations – Don’t trade blindly at session highs/lows. Look for wicks, rejections, or break/retests.

✅ Use Stop-Loss Above/Below Session Levels – If you’re going long, set SL below a session low. If short, set SL above a session high.

✅ Watch Volume & News Events – Breakouts without strong volume or news may be fake moves.

✅ Combine with Other Strategies – Use price action, trendlines, or EMAs with this indicator for higher probability trades.

✅ Use the Weekly Open for Trend Bias – If price stays below the Weekly Open, avoid bullish setups unless key support holds.

🎯 Who is This Indicator For?

📌 Beginners who need clear session-based trading levels.

📌 Day traders & scalpers looking to refine their intraday setups.

📌 Smart money traders using liquidity concepts.

📌 Swing traders tracking higher timeframe momentum shifts.

🚀 Final Thoughts

This indicator is an essential tool for traders who want to understand market structure, liquidity, and volatility cycles. Whether you’re trading forex, stocks, or crypto, it helps you stay on the right side of the market and avoid unnecessary risks.

🔹 Set it up, customize your colors, define your UTC offset, and start trading smarter today! 🏆📈

Yearly Profit BackgroundDescription:

The Yearly Profit Background indicator is a powerful tool designed to help traders quickly visualize the profitability of each calendar year on their charts. By analyzing the annual performance of an asset, this indicator colors the background of each completed year green if the year was profitable (close > open) or red if it resulted in a loss (close < open). This visual representation allows traders to identify long-term trends and historical performance at a glance.

Key Features:

Annual Profit Calculation: Automatically calculates the yearly performance based on the opening price of January 1st and the closing price of December 31st.

Visual Background Coloring: Highlights each completed year with a green (profit) or red (loss) background, making it easy to spot trends.

Customizable Transparency: The background colors are set at 90% transparency, ensuring they don’t obstruct your chart analysis.

Optional Price Plots: Displays the annual opening (blue line) and closing (orange line) prices for additional context.

How to Use:

Add the indicator to your chart.

Observe the background colors for each completed year:

Green: The year was profitable.

Red: The year resulted in a loss.

Use the optional price plots to analyze annual opening and closing levels.

Ideal For:

Long-term investors analyzing historical performance.

Traders looking to identify multi-year trends.

Anyone interested in visualizing annual market cycles.

Why Use This Indicator?

Understanding the annual performance of an asset is crucial for making informed trading decisions. The Yearly Profit Background indicator simplifies this process by providing a clear, visual representation of yearly profitability, helping you spot patterns and trends that might otherwise go unnoticed.

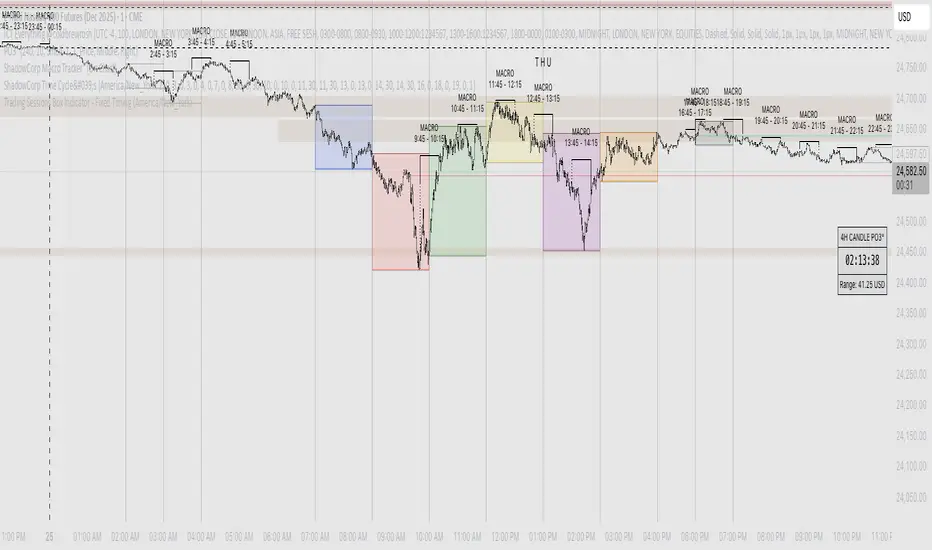

Macro Timing Window Signal ⏱️ Macro Timing Window Signal – Check/X Indicator

This indicator displays a green check mark ✔️ or red X ✖️ in the top-right corner of the chart based on a repeating macro time cycle that divides every hour into active and inactive windows.

How it works:

• ✔️ Green Check (Active Macro Window):

Appears from xx:45 → xx:15 of the next hour (30-minute macro window).

• ✖️ Red X (Inactive Macro Window):

Appears from xx:16 → xx:44 (mid-hour cooldown window).

• Optional flash signal at the exact macro flip points (xx:45, xx:00, xx:15) to highlight transitions.

• Supports sound alerts so you never miss the start or end of a macro window.

This tool is designed for traders who incorporate macro-driven time cycles, liquidity sessions, or algorithmic delivery windows into their strategy.

The display is fixed on-screen, clean, and unobtrusive, ensuring instant recognition of the current macro state without cluttering the chart.

Maancyclus Volatiliteitsindicator (2025)This Moon Cycle Volatility Indicator for TradingView is designed to help traders track and analyze market volatility around specific lunar phases, namely the Full Moon and New Moon. The indicator marks the dates of these moon phases on the chart and measures volatility using the Average True Range (ATR) indicator, which gauges market price fluctuations.

Key Features:

Moon Phase Markers: The indicator marks the Full Moon and New Moon on the chart using labels. Blue labels are placed below bars for Full Moons, while red labels are placed above bars for New Moons. These markers are based on a manually curated list of moon phase dates for the year 2025.

Volatility Calculation: The indicator calculates market volatility using the ATR (14), which provides a sense of market movement and potential risk. Volatility is plotted as histograms, with blue histograms representing volatility around Full Moons and red histograms around New Moons.

Comparative Analysis: By comparing the volatility around these moon phases to the average volatility, traders can spot potential patterns or heightened market movements. This can inform trading strategies, such as anticipating increased market activity around specific lunar events.

In essence, this tool helps traders identify potential high-volatility periods tied to lunar cycles, which could impact market sentiment and price action.

Smoothed ROC Z-Score with TableSmoothed ROC Z-Score with Table

This indicator calculates the Rate of Change (ROC) of a chosen price source and transforms it into a smoothed Z-Score oscillator, allowing you to identify market cycle tops and bottoms with reduced noise.

How it works:

The ROC is calculated over a user-defined length.

A moving average and standard deviation over a separate window are used to standardize the ROC into a Z-Score.

This Z-Score is further smoothed using an exponential moving average (EMA) to filter noise and highlight clearer cycle signals.

The smoothed Z-Score oscillates around zero, with upper and lower bands defined by user inputs (default ±2 standard deviations).

When the Z-Score reaches or exceeds ±3 (customizable), the value shown in the table is clamped at ±2 for clearer interpretation.

The indicator plots the smoothed Z-Score line with zero and band lines, and displays a colored Z-Score table on the right for quick reference.

How to read it:

Values near zero indicate neutral momentum.

Rising Z-Scores towards the upper band suggest increasing positive momentum, possible market tops or strength.

Falling Z-Scores towards the lower band indicate negative momentum, potential bottoms or weakness.

The color-coded table gives an easy visual cue: red/orange for strong positive signals, green/teal for strong negative signals, and gray for neutral zones.

Use cases:

Identify turning points in trending markets.

Filter noisy ROC data for cleaner signals.

Combine with other indicators to time entries and exits more effectively.

US Construction Spending & Manufacturing Employment YoY % ChangeUsage Notes: Timeframe: Use a monthly chart, as TTLCONS and MANEMP are monthly data. Other timeframes result in interpolation.

Data Availability: As of October 2025, TTLCONS is available until July 2025 and MANEMP until August 2025 (automatically via TradingView).

The Unsung Heroes: Why C&M Are the True Indicators

Imagine the economy is a highly sensitive vehicle. Quarterly reported GDP is like a quarterly glance at the odometer—it's slow, often delayed, and clearly refers to the past. Anyone who wants to predict future developments needs something much faster.

This is where construction and manufacturing come into play. These two sectors are the machine builders of the economy and provide us with real-time feedback. They form the backbone of economic forecasting for several important reasons:

1. Monetary policy indicators: Both sectors are highly sensitive to monetary policy developments, such as interest rate changes. If developers are unable to finance large residential or commercial projects and manufacturers postpone capital-intensive factory expansions, for example, declines in construction demand would quickly affect other sectors.

2. The backbone of the secondary sector: These industries constitute the secondary sector of the economy, meaning they are concerned with the actual transformation and production of goods, not just the extraction of raw materials or the provision of intangible services. One could argue that while they only account for about 15% of GDP in the US, their impact is massive and cyclical.

3. The timeliness advantage: Forget quarterly lags. Both construction output and manufacturing employment data are released monthly. This timely, frequent data allows analysts to assess economic momentum much more quickly than if they had to wait for delayed GDP reports.

In the US, some analysts have even titled their articles with the bold claim: "Housing construction is the business cycle." Fluctuations in housing construction are frequent and large, and a decline in activity is almost always accompanied by a subsequent decline in GDP.

enigmaMarkets move, but price remembers.

Long before indicators flash signals or momentum shifts, price reacts to levels that were already there — quiet, patient, and unmoving.

This tool reveals those levels.

Fixed price intervals — the kind institutions respect, algorithms acknowledge, and charts quietly obey — are drawn automatically above and below current price. No predictions. No signals. Just structure.

The levels don’t chase price.

They wait for it.

On their own, they are simple.

Paired with time, context, and comparison, they become something else entirely.

When price reaches a level in alignment with a larger cycle, reactions tend to be cleaner and more decisive.

When related markets arrive at similar prices but disagree in direction, the divergence often tells a deeper story.

And when those moments occur within broader macro conditions, the response is rarely random.

Use these levels to observe reactions, pauses, rejections, and expansions.

Use them to frame risk across sessions, instruments, and regimes.

Use them to see how short-term movement fits inside a much larger narrative.

Nothing here tells you when to trade.

It only reveals where price matters — and when the market is paying attention.

If you know, you know.

Ultimate Trend System — FINAL MASTER EDITIONUltimate Trend System — FINAL MASTER EDITION

A complete, multi‑layered trend‑detection engine designed for precision execution and clarity.

This final edition fuses trend, momentum, volatility, and filtering into one symmetrical logic system — enabling traders to instantly visualize directional strength and avoid false signals during choppy markets.

🔹 System Overview

The Ultimate Trend System consolidates several classic trading frameworks into a unified model.

It dynamically generates BUY, SELL, and STOP tags directly on the chart — each derived from clean, interlinked conditions that measure both momentum and structure.

In addition, a built‑in information panel summarizes live indicator states for quick decision‑making without checking multiple indicators.

⚙️ Core Logic Components

SMA (20‑period): Identifies trend slope; rising → bullish bias, falling → bearish bias.

VWAP: Defines fair‑value position — Above, Below, or Inside volume‑weighted average price.

QQE‑Lite (RSI): Tracks internal momentum shifts by comparing RSI to its EMA smoothing.

ATR Strength: Classifies current volatility regime as Turbo, Strong, or Weak.

SuperTrend: Confirms structural trend direction using an ATR‑based trailing model.

Choppiness Filter: Suppresses signals when short‑term volatility contracts or range noise dominates.

Fakeout Detection: Prevents false triggers after deceptive breakouts or reversals.

🧩 Execution Logic

BUY Signal: All major trend engines align bullishly, with clean structure and momentum.

SELL Signal: All major engines align bearishly, with clean structure and momentum.

STOP Phase: Appears once per cycle to mark neutral or transition zones; automatically locks further stops until a new entry signal is confirmed.

🟩🟥 Visual Elements

Green Labels: Confirmed bullish entry (BUY).

Red Labels: Confirmed bearish entry (SELL).

Yellow Labels: STOP state (trend exhaustion or consolidation).

Panel: Displays live readings for VWAP, SMA, QQE, ATR regime, and SuperTrend direction.

🧠 Design Philosophy

Built for simplicity, speed, and precision — the Final Master Edition strips away noise without losing analytical depth.

It can serve as a standalone trend system or foundation layer for more advanced frameworks like auto‑execution or multi‑engine HUDs.

VIX Counter-Trend StrategyVIX Panic Index VOO Bottom-Fishing Strategy

📊 Strategy Overview

This strategy utilizes the VIX (Volatility Index) as a market sentiment indicator to help investors rationally enter positions during periods of extreme market panic, using objective technical signals to avoid emotional decision-making. It is designed to capture rebound opportunities in VOO (or other US equity ETFs) following panic-driven selloffs.

🎯 Entry and Exit Conditions

Entry Conditions (both must be met):

VIX reaches or exceeds the set threshold (default 25, adjustable)

VIX death crosses below its moving average (default 5-day MA), confirming panic sentiment is beginning to recede

Exit Conditions (three modes available):

Holding Period Mode: Exit after holding for the set number of days (default 100 days)

VIX Decline Mode: Exit when VIX falls below the set threshold (default 20)

Either Condition Mode: Exit when either condition is met

⚠️ Important Warnings

Not Suitable for Leveraged ETF Bottom-Fishing: VIX reflects market volatility. Using leveraged ETFs (such as TQQQ, SOXL) increases risk due to decay effects and greater volatility, potentially causing larger losses during panic periods.

Bear Market Inaccuracy Risk: This strategy assumes markets will rebound from panic. However, during prolonged bear markets or systemic risks (such as the 2008 financial crisis or 2022 rate hike cycle), VIX may remain elevated for extended periods, triggering multiple buy signals while prices continue declining, rendering the strategy ineffective.

Recommended to Combine with Market Trend Analysis: Works better in bull market conditions. In bear markets, consider raising VIX thresholds or suspending use.

For Reference Only, Not Investment Advice: Historical performance does not guarantee future results. Please use cautiously according to your personal risk tolerance.

VIX 恐慌指數 VOO 抄底策略

📊 策略目的

本策略利用 VIX 恐慌指數作為市場情緒指標,幫助投資人在市場極度恐慌時理性進場抄底,並透過客觀的技術訊號避免情緒化操作。適合用於捕捉 VOO(或其他美股 ETF)在恐慌性下跌後的反彈機會。

🎯 進出場條件

進場條件(同時滿足):

VIX 指數達到設定門檻以上(預設 25,可調整)

VIX 死亡交叉其均線(預設 5 日均線),確認恐慌情緒開始回落

出場條件(三種模式可選):

持有天數模式:持有達到設定天數後出場(預設 100 天)

VIX 回落模式:VIX 降至設定門檻以下時出場(預設 20)

兩者皆可模式:任一條件滿足即出場

⚠️ 重要警語

不適合槓桿型 ETF 抄底:VIX 反映的是市場波動度,使用槓桿 ETF(如 TQQQ、SOXL)會因為衰減效應和更大波動而增加風險,可能在恐慌期間造成更大虧損。

空頭市場失準風險:本策略假設市場會從恐慌中反彈,但在長期空頭或系統性風險(如 2008 金融危機、2022 升息循環)中,VIX 可能長期處於高檔,多次觸發買入訊號卻持續下跌,導致策略失效。

建議搭配大盤趨勢判斷:在多頭格局中使用效果較佳,空頭格局建議提高 VIX 門檻或暫停使用。

僅供參考,非投資建議:歷史績效不代表未來表現,請依個人風險承受度謹慎使用。

DCA Position vs Cash HoldingThis indicator visualizes the performance of a simulated dollar-cost averaging (DCA) strategy compared to simply holding cash. It models the cumulative position size and value of buying a fixed dollar amount of the asset per candle over a configurable lookback period.

🔍 What It Shows:

Simulates buying $1 (or any amount) of the asset per candle

Tracks the total units accumulated and their current market value

Plots the difference between the DCA position value and total cash spent

Highlights when DCA buyers are underwater — a potential contrarian buy zone

📈 How to Use:

Values above zero indicate DCA outperformance vs cash

Values below zero signal structural drawdown — often a high-conviction bulk-buy opportunity

Use as a sentiment overlay to time discretionary adds or confirm regime shifts

⚙️ Inputs:

Lookback Window: Number of candles used to simulate DCA accumulation

DCA Amount: Dollar value purchased per candle

This tool is ideal for traders seeking to quantify accumulation efficiency, identify cycle inflection points, and visualize sentiment-weighted cost basis dynamics.

Shadow Corp 90min Boxes90-min cycle boxes, marks 90min session highs and lows with color coded boxes.

Intraday Time Cycle Levels (Labels + Alerts + Colors)Jag japp detta spelet fram och tbx.

Tack för ert förtoende.

SCPEM - Socionomic Crypto Peak Model (0-85 Scale)SCPEM Indicator Overview

The SCPEM (Socionomic Crypto Peak Evaluation Model) indicator is a TradingView tool designed to approximate cycle peaks in cryptocurrency markets using socionomic theory, which links market behavior to collective social mood. It generates a score from 0-85 (where 85 signals extreme euphoria and high reversal risk) and plots it as a blue line on the chart for visual backtesting and real-time analysis.

#### How It Works

The indicator uses technical proxies to estimate social mood factors, as Pine Script cannot fetch external data like sentiment indices or social media directly. It calculates a weighted composite score on each bar:

- Proxies derive from price, volume, and volatility data.

- The raw sum of factor scores (max ~28) is normalized to 0-85.

- The score updates historically for backtesting, showing mood progression over time.

- Alerts trigger if the score exceeds 60, indicating high peak probability.

Users can adjust inputs (e.g., lengths for RSI or pivots) to fine-tune for different assets or timeframes.

Metrics Used (Technical Proxies)

Crypto-Specific Sentiment

Approximated by RSI (overbought levels indicate greed).

Social Media Euphoria

Based on volume relative to its SMA (spikes suggest herding/FOMO).

Broader Social Mood Proxies

Derived from ATR volatility (high values signal uncertain/mixed mood).

Search and Cultural Interest Proxied by OBV trend (rising accumulation implies growing interest).

Socionomic Wildcard

Uses Bollinger Band width (expansion for positive mood, contraction for negative).

Elliott Wave Position

Counts recent price pivots (more swings indicate later wave stages and exhaustion).

Simplified STH-MVRV + Z-ScoreSimplified Short Term Holder MVRV (STH-MVRV) + Z-Score Indicator

Description:

This indicator visualizes the Short Term Holder Market Value to Realized Value ratio (STH-MVRV) and its normalized Z-Score, providing insight into Bitcoin’s market cycle phases and potential overbought or oversold conditions.

How it works:

The STH-MVRV ratio compares the market value of coins held by short-term holders to their realized value, helping to identify periods of profit-taking or accumulation by these holders.

The indicator calculates three versions:

STH-MVRV (MVRV): Ratio of current MVRV to its 155-day SMA.

STH-MVRV (Price): Ratio of BTC price to its 155-day SMA.

STH-MVRV (AVG): Average of the above two ratios.

You can select which ratio to display via the input dropdown.

Threshold Lines:

Adjustable upper and lower threshold lines mark significant levels where market sentiment might shift.

The indicator also plots a baseline at 1.0 as a reference.

Z-Score Explanation:

The Z-Score is a normalized value scaled between -3 and +3, calculated relative to the chosen threshold levels.

When the ratio hits the upper threshold, the Z-Score approaches +2, indicating potential overbought conditions.

Conversely, reaching the lower threshold corresponds to a Z-Score near -2, signaling potential oversold conditions.

This Z-Score is shown in a clear table in the top right corner of the chart for easy monitoring.

Data Sources:

MVRV data is fetched from the BTC_MVRV dataset.

Price data is sourced from the BTC/USD index.

Usage:

Use this indicator to assess short-term holder market behavior and to help identify buying or selling opportunities based on extremes indicated by the Z-Score.

Combining this tool with other analysis can improve timing decisions in Bitcoin trading.

Katik Cycle 56 DaysThis script plots vertical dotted lines on the chart every 56 trading days, starting from the first bar. It calculates intervals based on the bar_index and draws the lines for both historical and future dates by projecting the lines forward.

The lines are extended across the entire chart height using extend=extend.both, ensuring visibility regardless of chart zoom level. You can customize the interval length using the input box.

Note: Use this only for 1D (Day) candle so that you can find the changes in the trend...

It Screams When Crypto BottomsGet ready to ride the crypto rollercoaster with your new favourite tool for catching Bitcoin at its juiciest, most oversold moments.

This isn’t just another boring indicator — it screams when it’s time to load your bags and get ready for the ride back up!

Expect it to scream just once or twice per cycle at the very bottom, so you know exactly when the party starts!

Why You'll Love It:

Crypto-Exclusive Magic: It does not really matter what chart you are on; this indicator only bothers about the original and realised market cap of BTC. We all know the rest will follow.

Big Picture Focus: Designed for daily. No noisy intraday drama — just pure, clear signals.

Screaming Alerts: When the signal hits, it’s like a neon sign screaming, “Crypto Bottomed!"

Think of this indicator as your backstage pass to the crypto world’s most dramatic moments. It’s not subtle — it’s bold, loud, and ready to help you time the market like a pro.

P.S.: Use it only on a daily chart. Don’t even try it on shorter timeframes — it won’t scream, and you’ll miss the show! 🙀

AMDX Time ZoneThis script is base on the theory of @traderdaye, on the TimeZone AMDX

Accumulation

Manipulation

Distribution

X reversal / continuation

OR

AMDX

It show you the box on intraday Timeframe:

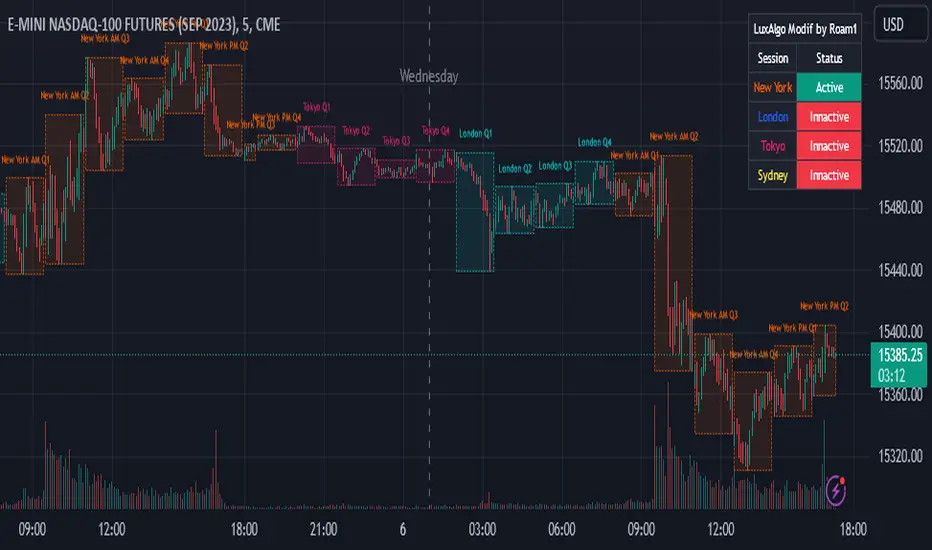

Q1: 18.00 - 19.30 | Q2: 19.30 - 21.00 | Q3: 21.00 - 22.30 | Q4: 22.30 - 00.00 (90min Cycles of the Asian Session)

Q1: 00.00 - 01.30 | Q2: 01.30 - 03.00 | Q3: 03.00 - 04.30 | Q4: 04.30 - 06.00 (90min Cycles of the London Session)

Q1: 06.00 - 07.30 | Q2: 07.30 - 09.00 | Q3: 09.00 - 10.30 | Q4: 10.30 - 12.00 (90min Cycles of the NY Session)

Q1: 12.00 - 13.30 | Q2: 13.30 - 15.00 | Q3: 15.00 - 16.30 | Q4: 16.30 - 18.00 (90min Cycles of the PM Session)

You can extend this theory to the day => to the week => to the month

Thanks LuxAlgo for the base,

Hope you enjoy it

OPEX & VIX Expiry Markers (Past, Present, Future)Expiry Date Indicator for Options & Index Traders

Track Key Expiration Dates Automatically

For traders focused on options, indices, and expiration-based strategies, staying aware of key expiration dates is essential. This TradingView indicator automatically plots OPEX, VIX Expiry, and Quarterly Expirations on your charts—helping you plan trades more effectively without manual tracking.

Features:

✔ OPEX Expiration Markers – Highlights the third Friday of each month, when equity and index options expire.

✔ VIX Expiration Tracking – Marks Wednesday VIX expirations, useful for volatility-based trades.

✔ Quarterly Expiration Highlights – Identifies major market expiration cycles for better trade management.

✔ Live Countdown to Next OPEX – Displays how many days remain until the next expiration.

✔ Works on Any Timeframe – Past, present, and future expiration dates update dynamically.

✔ Customizable Settings – Enable or disable specific features based on your trading style.

Ideal for Traders Who Use:

📈 SPX / SPY / NDX / VIX Options Strategies

📅 Iron Condors, Credit Spreads, and Expiration-Based Trades

This tool helps traders stay ahead of expiration cycles, ensuring they never miss an important date. Simple, effective, and built for seamless integration into your trading workflow.

This keeps it professional and to the point without overhyping it. Let me know if you'd like any further refinements! 🚀

ICT IPDA LookbackThis description is tailored for the TradingView community, using the specific terminology associated with Michael Huddleston's (ICT) Interbank Price Delivery Algorithm (IPDA).

📜 TradingView Indicator Description

ICT IPDA Lookback Engine (20-40-60 Day Cycles)

Overview This indicator automates the IPDA Data Range lookback periods as taught by Michael J. Huddleston (ICT). In the Interbank Price Delivery Algorithm, time is the primary filter. The algorithm references specific lookback windows—20, 40, and 60 trading days—to seek liquidity and rebalance inefficiencies.

Instead of manually counting bars every morning, this tool plots precise vertical anchors to help you identify the Institutional Order Flow and the "Draw on Liquidity" (DOL) within the current dealing range.

🛠️ Key Features

Rolling Lookback Anchors: Automatically plots red vertical lines at the 20, 40, and 60-day intervals.

Time-Based Accuracy: Calculated using calendar-adjusted trading days to ensure the lines land on the correct institutional data points, regardless of weekends or holidays.

Multi-Asset Support: Works seamlessly across Forex, Futures, Indices, and Commodities.

Real-Time Movement: The lines shift dynamically with the current candle, maintaining the exact IPDA window as the algorithm processes new data.

💡 How to Use (ICT IPDA Logic)

Define the Context: Look back at the 20-day range (Short-term), 40-day range (Intermediate-term), and 60-day range (Long-term).

Identify PD Arrays: Use these vertical lines to anchor your search for Old Highs/Lows, Fair Value Gaps (FVG), and Order Blocks (OB) within those specific windows.

Determine Premium vs. Discount: Check where the current price sits relative to the Highs and Lows of these three ranges to establish your Daily Bias.

Quarterly Shifts: Monitor how price reacts as it reaches the extremity of the 60-day lookback, often signaling a potential "Quarterly Shift" in institutional direction.

📖 Technical Details

Indicator Type: Overlay

Calculations: Uses timenow and millisecond conversion for precise "Calendar Day" placement.

Best Timeframes: Designed for the Daily (1D) chart but can be used on lower timeframes (H4, H1, M15) to visualize the higher-timeframe data ranges while scalping.

Bitcoin Cycles Halvins/Tops/Bottoms By CrBeThis Script shows you the actual Bitcoin tops and bottoms dates.