Volume Weighted LR Z ScoreThis indicator calculates the Volume Weighted Linear Regression

Z-Score (VWLRZS). Unlike a standard Z-Score which measures

deviation from a static mean, this oscillator measures the

statistical distance of price from a dynamic Volume-Weighted

Linear Regression Line (Analysis of Residuals).

Key Features:

1. **Volatility Decomposition:** The indicator separates volatility

based on the 'Estimate Bar Statistics' option.

- **Standard Mode (`Estimate Bar Statistics` = OFF):** Calculates

standard Regression Residuals using the selected `Source`

for both the regression line (baseline) and the signal.

- **Decomposition Mode (`Estimate Bar Statistics` = ON):**

Uses a hybrid statistical approach:

a) **The Model (Baseline):** Uses an estimator to calculate

the 'within-bar' mean and fits the Linear Regression

through these statistical centers. This creates a

stable, trend-following expectation model.

b) **The Signal (Observation):** Compares the actual `Source`

(e.g., Close) against this regression line.

(Result: A Z-Score that measures deviations from the current

trend slope rather than a flat average).

2. **Visual Decomposition Logic:** Total Standard Deviation (of

Residuals) is the primary metric displayed. Since Standard

Deviations are not linearly additive (sqrt(a+b) != sqrt(a)+sqrt(b)),

this indicator calculates the *exact* Total Z-Score and partitions

the area underneath based on the Variance Ratio. This ensures the

displayed total volatility remains mathematically accurate while

showing relative composition.

3. **Normalization (Exponential Regression):** Includes an optional

'Normalize' mode. When enabled, the indicator calculates the

Linear Regression on logarithmic data. Mathematically, this

transforms the baseline into an **Exponential Regression Curve**,

making it ideal for analyzing assets with compounding growth

characteristics (constant percentage trend).

4. **Full Divergence Suite (Class A, B, C):** The indicator's

primary feature is its integrated divergence engine. It

automatically detects and plots all three major divergence

classes between price and the Z-Score:

- Regular (A): Signals potential trend exhaustion and reversals.

- Hidden (B): Signals potential trend continuations during pullbacks.

- Exaggerated (C): Signals weakness at double tops/bottoms.

5. **Divergence Filtering and Visualization:**

- **Price Tolerance Filter:** Divergence detection is enhanced

with a percentage-based price tolerance (`pivPrcTol`) to

filter out insignificant market noise, leading to more

robust signals.

- **Persistent Visualization:** Divergence markers are plotted

for the entire duration of the signal and are visually

anchored to the oscillator level of the confirming pivot.

- **Flexible Pivot Algorithms:** Supports various underlying

mathematical models for pivot detection provided by the

core library

6. **Note on Confirmation (Lag):** Divergence signals rely on a

pivot confirmation method to ensure they do not repaint.

- The **Start** of a divergence is only detected *after* the

confirming pivot is fully formed (a delay based on

`Pivot Right Bars`).

- The **End** of a divergence is detected either instantly

(if the signal is invalidated by price action) or with

a delay (when a new, non-divergent pivot is confirmed).

7. **Multi-Timeframe (MTF) Capability:**

- **MTF Calculation:** The Z-Score line *itself* can be calculated on a

higher timeframe, with standard options to handle gaps

(`Fill Gaps`) and prevent repainting (`Wait for...`).

- **Limitation:** The Divergence detection engine (`pivDiv`)

is designed for the active timeframe. Using it in MTF mode

is not recommended as step-data can lead to inaccurate

pivot detection.

8. **Integrated Alerts:** Includes a comprehensive set of built-in

alerts for the Z-Score crossing the neutral line, the configured

Threshold levels, and the start/end of all divergence types.

---

**DISCLAIMER**

1. **For Informational/Educational Use Only:** This indicator is

provided for informational and educational purposes only. It does

not constitute financial, investment, or trading advice, nor is

it a recommendation to buy or sell any asset.

2. **Use at Your Own Risk:** All trading decisions you make based on

the information or signals generated by this indicator are made

solely at your own risk.

3. **No Guarantee of Performance:** Past performance is not an

indicator of future results. The author makes no guarantee

regarding the accuracy of the signals or future profitability.

4. **No Liability:** The author shall not be held liable for any

financial losses or damages incurred directly or indirectly from

the use of this indicator.

5. **Signals Are Not Recommendations:** The alerts and visual signals

(e.g., crossovers) generated by this tool are not direct

recommendations to buy or sell. They are technical observations

for your own analysis and consideration.

Cari dalam skrip untuk "Exponential"

ED by bigmmED by bigmm identifies significant price divergences from the 200-period Exponential Moving Average (EMA) by analyzing closing and opening price extremes. This tool marks the three most recent candles with the largest percentage deviations.

Key Features

EMA200 Analysis: Uses the 200-period Exponential Moving Average as the primary reference level for measuring price deviations

Deviation Calculation: Computes percentage-based deviations for both closing (below EMA) and opening (above EMA) prices

Top 3 Extremes: Identifies and marks only the three most recent maximum deviations for each direction

Visual Simplicity: Uses minimalistic green and red dots for clear visual identification without chart clutter

Historical Analysis: Evaluates the last 1440 bars (approximately 3 years on daily timeframe) to find significant deviation patterns

Recommended Usage

Best used on higher timeframes (H4, D1, W1) for the following reasons:

Reduced Noise: Higher timeframes filter out market noise and provide cleaner deviation signals

Trend Context: EMA200 carries more significance on daily and weekly charts as a major trend indicator

Strategic Signals: Extreme deviations on higher timeframes often correspond to important support/resistance levels and potential reversal zones

Reduced False Signals: Longer timeframes minimize whipsaws and provide more reliable extreme readings

Position Trading: Ideal for swing traders and position traders who base decisions on daily or weekly price action

4 Fibonacci EMAsAdd 4 Fibonacci EMAs to your charts with one indicator.

Configureable by value, so they don't necessarily have to use Fibonacci numbers, and by colors.

ONE RING 8 MA Bands with RaysCycle analysis tool ...

MAs: Eight moving averages (MA1–MA8) with customizable lengths, types (RMA, WMA, EMA, SMA), and offsets

Bands: Upper/lower bands for each MA, calculated based on final_pctX (Percentage mode) or final_ptsX (Points mode), scaled by multiplier

Rays: Forward-projected lines for bands, with customizable start points, styles (Solid, Dashed, Dotted), and lengths (up to 500 bars)

Band Choices

Manual: Uses individual inputs for band offsets

Uniform: Sets all offsets to base_pct (e.g., 0.1%) or base_pts (e.g., 0.1 points)

Linear: Scales linearly (e.g., base_pct * 1, base_pct * 2, base_pct * 3 ..., base_pct * 8)

Exponential: Scales exponentially (e.g., base_pct * 1, base_pct * 2, base_pct * 4, base_pct * 8 ..., base_pct * 128)

ATR-Based: Offsets are derived from the Average True Range (ATR), scaled by a linear factor. Dynamic bands that adapt to market conditions, useful for breakout or mean-reversion strategies. (final_pct1 = base_pct * atr, final_pct2 = base_pct * atr * 2, ..., final_pct8 = base_pct * atr * 8)

Geometric: Offsets follow a geometric progression (e.g., base_pct * r^0, base_pct * r^1, base_pct * r^2, ..., where r is a ratio like 1.5) This is less aggressive than Exponential (which uses powers of 2) and provides a smoother progression.

Example: If base_pct = 0.1, r = 1.5, then final_pct1 = 0.1%, final_pct2 = 0.15%, final_pct3 = 0.225%, ..., final_pct8 ≈ 1.71%

Harmonic: Offsets are based on harmonic flavored ratios. final_pctX = base_pct * X / (9 - X), final_ptsX = base_pts * X / (9 - X) for X = 1 to 8 This creates a harmonic-like progression where offsets increase non-linearly, ensuring MA8 bands are wider than MA1 bands, and avoids duplicating the Linear choice above.

Ex. offsets for base_pct = 0.1: MA1: ±0.0125% (0.1 * 1/8), MA2: ±0.0286% (0.1 * 2/7), MA3: ±0.05% (0.1 * 3/6), MA4: ±0.08% (0.1 * 4/5), MA5: ±0.125% (0.1 * 5/4), MA6: ±0.2% (0.1 * 6/3), MA7: ±0.35% (0.1 * 7/2), MA8: ±0.8% (0.1 * 8/1)

Square Root: Offsets grow with the square root of the band index (e.g., base_pct * sqrt(1), base_pct * sqrt(2), ..., base_pct * sqrt(8)). This creates a gradual widening, less aggressive than Linear or Exponential. Set final_pct1 = base_pct * sqrt(1), final_pct2 = base_pct * sqrt(2), ..., final_pct8 = base_pct * sqrt(8).

Example: If base_pct = 0.1, then final_pct1 = 0.1%, final_pct2 ≈ 0.141%, final_pct3 ≈ 0.173%, ..., final_pct8 ≈ 0.283%.

Fibonacci: Uses Fibonacci ratios (e.g., base_pct * 1, base_pct * 1.618, base_pct * 2.618

Percentage vs. Points Toggle:

In Percentage mode, bands are calculated as ma * (1 ± (final_pct / 100) * multiplier)

In Points mode, bands are calculated as ma ± final_pts * multiplier, where final_pts is in price units.

Threshold Setting for Slope:

Threshold setting for determining when the slope would be significant enough to call it a change in direction. Can check efficiency by setting MA1 to color on slope temporarily

Arrow table: Shows slope direction of 8 MAs using an Up or Down triangle, or shows Flat condition if no triangle.

Universal Adaptive Tracking🙏🏻 Behold, this is UAT (Universal Adaptive Tracker) , with less words imma proceed how it compares with alternatives:

^^ comparison with non-adaptive quadratic regression (purple line), that has higher overshoots, less precision

^^ comparison with JMA and its adaptive gain. JMA’s gain is heavily limited, while UAT’s negative and positive gains are soft-saturated with p-order Möbius transform

This drop is inspired by, dedicated to, and made will all love towards Jurik Research , who retired in October 2k21. When some1 steps out, some1 has to step in, and that time it’s me (again xd). But there’s some history u gotta know:

Some history u gotta know:

In ~2008 dudes from forexfactory reverse engineered Jurik Moving Average

In late 1990s dudes from Jurik Research approximated the best possible adaptive tracking filter for evolution of prices via engineering miracles

Today in 2k26, me I'm gonna present to you the real mathematical objects/entities behind JMA top-edge engineered approximates. You will prolly be even more happy now then all the dem together back then.

Why all this?

When we talk about object tracking stuff, e.g. air defense, drones, missiles, projectiles, prices, etc, it all comes down to adaptive control and (Position & Velocity & Acceleration) aka PVA state space models (the real stuff many of you count as DSP ).

Why? Cuz while position (P) : (mean), or position & velocity (PV) : (linear regression) are stable enough in dem own ways, Position & Velocity & Acceleration (PVA) : (quadratic regression+) require adaptivity do be stable. And real world stuff needs PVA, due to non-linearity for starters.

So that’s why. If your goal is Really smoothing and no lag, u gotta go there. I see a lot of folks are crazy with it and want it, so here is it, for y’all. And good news, this is perfect for your favorite Moving Windows.

How to use it

The upper study:

The final filter (main state): just as you use other fast smoothers, MAs, etc, you know better than me here

You can also turn in volatility bands in script’s style settings, these do not require any adjustments

Finally, you can turn on, in the same place, separate trackers each based on negative and positive volatility exclusively. When both are almost equal, that indicates stability & persistence in markets. May sound like it’s nothing important, but I've never seen anything like it before. Also, if you'd allow your our inner mental gym hero gloriously arise, you can argue that these 2 separate trackers represent 2 fair prices (one for sellers, one for buyers). All better then 1 imaginary fair price for both (forget about it)

The lower study:

The lower study: you can analyze streams of upward of downward volatilities separately. This is incredibly powerful

You can also turn these off and turn on neg & pos intensities, and use them as trend detector, when each or both cross 1.5 (naturally neutral) threshold.

^^ Upper study with expected typical and maximum volatility bands turned On

...

The method explained

What you got in the end is non-linear, adaptive, lighting fast when needed and slow when required price tracking. All built upon real math entities/objects, not a brilliantly engineered approximation of them. No parameters to optimize, data tells it all.

... It all starts from a process model, in our cause this is...

MFPM (Mechanical Feedback Price Model)

Doesn’t make gaussian assumptions like most quant mainstream tech, accepts that innovations are Laplace “at best”, relies in L inf and L0 spaces.

I created this model neither trynna fit non-fitting ARMA / variants, nor trynna be silly assuming that price state evolution and markets are random.

Theory behind it: if no new volume comes, then price evolution would be simply guided by the feedback based on previous trading activity, pushing prices towards the midrange between 2 latest datapoints, being the main force behind so called “pullbacks” and reason why most pullbacks end just a bit past 50% of a move.

This is the Real mechanical feedback based mean reversion, that is always there in the markets no matter what, think of it as a background process that is always there, and fresh new volume deviates prices away from it. Btw, this can also be expressed as AR2 with both phis = 0.5 .

Then I separate positive and negative innovations from this model and process them separately, reflecting the asymmetry between buy and sell forces, smth that most forget. Both of these follow exponential distribution . Each stream has its own memory so here we use recursive operators . We track maximum innovations (differences between real and expected datapoints) with exponentially decaying damping factor, and keep tracking typical innovation, with the same factor.

Then we calculate what’s called in lovely audio engineering as “ crest factor ”, the difference is we don’t do RMS and stuff. But hey again we work with laplace innovations, so we keep things in L0 and L inf spirit. Then we go a couple of steps further, making this crest factor truly relative (resolution agnostic), and then, most importantly, we apply a natural saturation on it based on p-order Möbius transform, but not with arbitrary p and L, but guided by informational limits of the data. These final "intensity" parameters are what we need next to make our object tracking adaptive.

Extended Beta(2, 2) Window

This is imo the main part of this. Looking at tapering windows in DSP and how wavelets are made from derivatives of PDF functions of probability distributions, I figured that why use just one derivative? That made me come up with Universal Moving Average , that combines PDF and CDF of Beta(2, 2) distribution . And that is fine for P (position) tracking model.

Here we need PVA (position & velocity & acceleration). We can realize that everything starts from PDF, and by adding derivatives and anti-derivatives of it as factors of final window weights, we can create smth truly unique, a weightset that is non-arbitrary and naturally provides response alike quadratic regression does, But, naturally smoothed.

Why do I consider this a discovery, a primordial math object? Because x^2 itself and Beta(2, 2) based on it are the only primitives, esp out of all these dozens of DSP tapering windows, that provide you a finite amount of derivatives. You can keep differentiating Hann window until the kingdom f come, while Welch window aka Beta(2, 2) has a natural stopping point, because the 3rd derivative is 0, so we can’t use it. Symmetrically, we do 2 steps up from PDF, getting 1st and second anti-derivatives. What’s lovely, symmetrically, 3rd antiderivative even tho exist, it stops making any sense. 2nd one still makes sense, it’s smth like “potential” of probability distribution, not really discussed in mainstream open access sources.

Finally, the last part is to introduce adaptivity using these intensity exponents we’ve calculated with MFPM. We do 2 separate trackers, one using the negative intensity exponent, another one uses positive intensity exponent.

And at the end, even tho using both together is cool, the final state estimate is calculated simply as the state which intensity has higher.

^^ impulse response of our final kernel with fixed (non adaptive) intensity exponents: 1 (blue) and 2 (red). You see it's all about phase

…

And that’s all folks.

…

Actually no …

Last, not least, is the ability to add additional innovation weight to the kernel:

^^ Weighting by innovations “On”. Provides incredible tracking precision, paid with smoothness. I think this screenshot, showing what happened after the gap, and how the tracker managed to react, explains it all.

...

Live Long and Prosper, all good TradingView

∞

taLibrary "ta"

█ OVERVIEW

This library holds technical analysis functions calculating values for which no Pine built-in exists.

Look first. Then leap.

█ FUNCTIONS

cagr(entryTime, entryPrice, exitTime, exitPrice)

It calculates the "Compound Annual Growth Rate" between two points in time. The CAGR is a notional, annualized growth rate that assumes all profits are reinvested. It only takes into account the prices of the two end points — not drawdowns, so it does not calculate risk. It can be used as a yardstick to compare the performance of two instruments. Because it annualizes values, the function requires a minimum of one day between the two end points (annualizing returns over smaller periods of times doesn't produce very meaningful figures).

Parameters:

entryTime : The starting timestamp.

entryPrice : The starting point's price.

exitTime : The ending timestamp.

exitPrice : The ending point's price.

Returns: CAGR in % (50 is 50%). Returns `na` if there is not >=1D between `entryTime` and `exitTime`, or until the two time points have not been reached by the script.

█ v2, Mar. 8, 2022

Added functions `allTimeHigh()` and `allTimeLow()` to find the highest or lowest value of a source from the first historical bar to the current bar. These functions will not look ahead; they will only return new highs/lows on the bar where they occur.

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `high`.

Returns: (float) The highest value tracked.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `low`.

Returns: (float) The lowest value tracked.

█ v3, Sept. 27, 2022

This version includes the following new functions:

aroon(length)

Calculates the values of the Aroon indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the Aroon-Up and Aroon-Down values.

coppock(source, longLength, shortLength, smoothLength)

Calculates the value of the Coppock Curve indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

longLength (simple int) : (simple int) Number of bars for the fast ROC value (length).

shortLength (simple int) : (simple int) Number of bars for the slow ROC value (length).

smoothLength (simple int) : (simple int) Number of bars for the weigted moving average value (length).

Returns: (float) The oscillator value.

dema(source, length)

Calculates the value of the Double Exponential Moving Average (DEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `source`.

dema2(src, length)

An alternate Double Exponential Moving Average (Dema) function to `dema()`, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `src`.

dm(length)

Calculates the value of the "Demarker" indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

ema2(src, length)

An alternate ema function to the `ta.ema()` built-in, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Number of bars (length).

Returns: (float) The exponentially weighted moving average of the `src`.

eom(length, div)

Calculates the value of the Ease of Movement indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

div (simple int) : (simple int) Divisor used for normalzing values. Optional. The default is 10000.

Returns: (float) The oscillator value.

frama(source, length)

The Fractal Adaptive Moving Average (FRAMA), developed by John Ehlers, is an adaptive moving average that dynamically adjusts its lookback period based on fractal geometry.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The fractal adaptive moving average of the `source`.

ft(source, length)

Calculates the value of the Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

ht(source)

Calculates the value of the Hilbert Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

ichimoku(conLength, baseLength, senkouLength)

Calculates values of the Ichimoku Cloud indicator, including tenkan, kijun, senkouSpan1, senkouSpan2, and chikou. NOTE: offsets forward or backward can be done using the `offset` argument in `plot()`.

Parameters:

conLength (int) : (series int) Length for the Conversion Line (Tenkan). The default is 9 periods, which returns the mid-point of the 9 period Donchian Channel.

baseLength (int) : (series int) Length for the Base Line (Kijun-sen). The default is 26 periods, which returns the mid-point of the 26 period Donchian Channel.

senkouLength (int) : (series int) Length for the Senkou Span 2 (Leading Span B). The default is 52 periods, which returns the mid-point of the 52 period Donchian Channel.

Returns: ( [float, float, float, float, float ]) A tuple of the Tenkan, Kijun, Senkou Span 1, Senkou Span 2, and Chikou Span values. NOTE: by default, the senkouSpan1 and senkouSpan2 should be plotted 26 periods in the future, and the Chikou Span plotted 26 days in the past.

ift(source)

Calculates the value of the Inverse Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

kvo(fastLen, slowLen, trigLen)

Calculates the values of the Klinger Volume Oscillator.

Parameters:

fastLen (simple int) : (simple int) Length for the fast moving average smoothing parameter calculation.

slowLen (simple int) : (simple int) Length for the slow moving average smoothing parameter calculation.

trigLen (simple int) : (simple int) Length for the trigger moving average smoothing parameter calculation.

Returns: ( [float, float ]) A tuple of the KVO value, and the trigger value.

pzo(length)

Calculates the value of the Price Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

rms(source, length)

Calculates the Root Mean Square of the `source` over the `length`.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The RMS value.

rwi(length)

Calculates the values of the Random Walk Index.

Parameters:

length (simple int) : (simple int) Lookback and ATR smoothing parameter length.

Returns: ( [float, float ]) A tuple of the `rwiHigh` and `rwiLow` values.

stc(source, fast, slow, cycle, d1, d2)

Calculates the value of the Schaff Trend Cycle indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

fast (simple int) : (simple int) Length for the MACD fast smoothing parameter calculation.

slow (simple int) : (simple int) Length for the MACD slow smoothing parameter calculation.

cycle (simple int) : (simple int) Number of bars for the Stochastic values (length).

d1 (simple int) : (simple int) Length for the initial %D smoothing parameter calculation.

d2 (simple int) : (simple int) Length for the final %D smoothing parameter calculation.

Returns: (float) The oscillator value.

stochFull(periodK, smoothK, periodD)

Calculates the %K and %D values of the Full Stochastic indicator.

Parameters:

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

stochRsi(lengthRsi, periodK, smoothK, periodD, source)

Calculates the %K and %D values of the Stochastic RSI indicator.

Parameters:

lengthRsi (simple int) : (simple int) Length for the RSI smoothing parameter calculation.

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

source (float) : (series int/float) Series of values to process. Optional. The default is `close`.

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

supertrend(factor, atrLength, wicks)

Calculates the values of the SuperTrend indicator with the ability to take candle wicks into account, rather than only the closing price.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (simple int) : (simple int) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when reversing trend, or to use the close price. Optional. Default is false.

Returns: ( [float, int ]) A tuple of the superTrend value and trend direction.

szo(source, length)

Calculates the value of the Sentiment Zone Oscillator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

t3(source, length, vf)

Calculates the value of the Tilson Moving Average (T3).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

vf (simple float) : (simple float) Volume factor. Affects the responsiveness.

Returns: (float) The Tilson moving average of the `source`.

t3Alt(source, length, vf)

An alternate Tilson Moving Average (T3) function to `t3()`, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

vf (simple float) : (simple float) Volume factor. Affects the responsiveness.

Returns: (float) The Tilson moving average of the `source`.

tema(source, length)

Calculates the value of the Triple Exponential Moving Average (TEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The triple exponentially weighted moving average of the `source`.

tema2(source, length)

An alternate Triple Exponential Moving Average (TEMA) function to `tema()`, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The triple exponentially weighted moving average of the `source`.

trima(source, length)

Calculates the value of the Triangular Moving Average (TRIMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The triangular moving average of the `source`.

trima2(src, length)

An alternate Triangular Moving Average (TRIMA) function to `trima()`, which allows a "series int" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int) Number of bars (length).

Returns: (float) The triangular moving average of the `src`.

trix(source, length, signalLength, exponential)

Calculates the values of the TRIX indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

signalLength (simple int) : (simple int) Length for smoothing the signal line.

exponential (simple bool) : (simple bool) Condition to determine whether exponential or simple smoothing is used. Optional. The default is `true` (exponential smoothing).

Returns: ( [float, float, float ]) A tuple of the TRIX value, the signal value, and the histogram.

uo(fastLen, midLen, slowLen)

Calculates the value of the Ultimate Oscillator.

Parameters:

fastLen (simple int) : (series int) Number of bars for the fast smoothing average (length).

midLen (simple int) : (series int) Number of bars for the middle smoothing average (length).

slowLen (simple int) : (series int) Number of bars for the slow smoothing average (length).

Returns: (float) The oscillator value.

vhf(source, length)

Calculates the value of the Vertical Horizontal Filter.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

vi(length)

Calculates the values of the Vortex Indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the viPlus and viMinus values.

vzo(length)

Calculates the value of the Volume Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

williamsFractal(period)

Detects Williams Fractals.

Parameters:

period (int) : (series int) Number of bars (length).

Returns: ( [bool, bool ]) A tuple of an up fractal and down fractal. Variables are true when detected.

wpo(length)

Calculates the value of the Wave Period Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

█ v7, Nov. 2, 2023

This version includes the following new and updated functions:

atr2(length)

An alternate ATR function to the `ta.atr()` built-in, which allows a "series float" `length` argument.

Parameters:

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The ATR value.

changePercent(newValue, oldValue)

Calculates the percentage difference between two distinct values.

Parameters:

newValue (float) : (series int/float) The current value.

oldValue (float) : (series int/float) The previous value.

Returns: (float) The percentage change from the `oldValue` to the `newValue`.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

highestSince(cond, source)

Tracks the highest value of a series since the last occurrence of a condition.

Parameters:

cond (bool) : (series bool) A condition which, when `true`, resets the tracking of the highest `source`.

source (float) : (series int/float) Series of values to process. Optional. The default is `high`.

Returns: (float) The highest `source` value since the last time the `cond` was `true`.

lowestSince(cond, source)

Tracks the lowest value of a series since the last occurrence of a condition.

Parameters:

cond (bool) : (series bool) A condition which, when `true`, resets the tracking of the lowest `source`.

source (float) : (series int/float) Series of values to process. Optional. The default is `low`.

Returns: (float) The lowest `source` value since the last time the `cond` was `true`.

relativeVolume(length, anchorTimeframe, isCumulative, adjustRealtime)

Calculates the volume since the last change in the time value from the `anchorTimeframe`, the historical average volume using bars from past periods that have the same relative time offset as the current bar from the start of its period, and the ratio of these volumes. The volume values are cumulative by default, but can be adjusted to non-accumulated with the `isCumulative` parameter.

Parameters:

length (simple int) : (simple int) The number of periods to use for the historical average calculation.

anchorTimeframe (simple string) : (simple string) The anchor timeframe used in the calculation. Optional. Default is "D".

isCumulative (simple bool) : (simple bool) If `true`, the volume values will be accumulated since the start of the last `anchorTimeframe`. If `false`, values will be used without accumulation. Optional. The default is `true`.

adjustRealtime (simple bool) : (simple bool) If `true`, estimates the cumulative value on unclosed bars based on the data since the last `anchor` condition. Optional. The default is `false`.

Returns: ( [float, float, float ]) A tuple of three float values. The first element is the current volume. The second is the average of volumes at equivalent time offsets from past anchors over the specified number of periods. The third is the ratio of the current volume to the historical average volume.

rma2(source, length)

An alternate RMA function to the `ta.rma()` built-in, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The rolling moving average of the `source`.

supertrend2(factor, atrLength, wicks)

An alternate SuperTrend function to `supertrend()`, which allows a "series float" `atrLength` argument.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (float) : (series int/float) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when reversing trend, or to use the close price. Optional. Default is `false`.

Returns: ( [float, int ]) A tuple of the superTrend value and trend direction.

vStop(source, atrLength, atrFactor)

Calculates an ATR-based stop value that trails behind the `source`. Can serve as a possible stop-loss guide and trend identifier.

Parameters:

source (float) : (series int/float) Series of values that the stop trails behind.

atrLength (simple int) : (simple int) Length for the ATR smoothing parameter calculation.

atrFactor (float) : (series int/float) The multiplier of the ATR value. Affects the maximum distance between the stop and the `source` value. A value of 1 means the maximum distance is 100% of the ATR value. Optional. The default is 1.

Returns: ( [float, bool ]) A tuple of the volatility stop value and the trend direction as a "bool".

vStop2(source, atrLength, atrFactor)

An alternate Volatility Stop function to `vStop()`, which allows a "series float" `atrLength` argument.

Parameters:

source (float) : (series int/float) Series of values that the stop trails behind.

atrLength (float) : (series int/float) Length for the ATR smoothing parameter calculation.

atrFactor (float) : (series int/float) The multiplier of the ATR value. Affects the maximum distance between the stop and the `source` value. A value of 1 means the maximum distance is 100% of the ATR value. Optional. The default is 1.

Returns: ( [float, bool ]) A tuple of the volatility stop value and the trend direction as a "bool".

Removed Functions:

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

trima2(src, length)

An alternate Triangular Moving Average (TRIMA) function to `trima()`, which allows a

"series int" length argument.

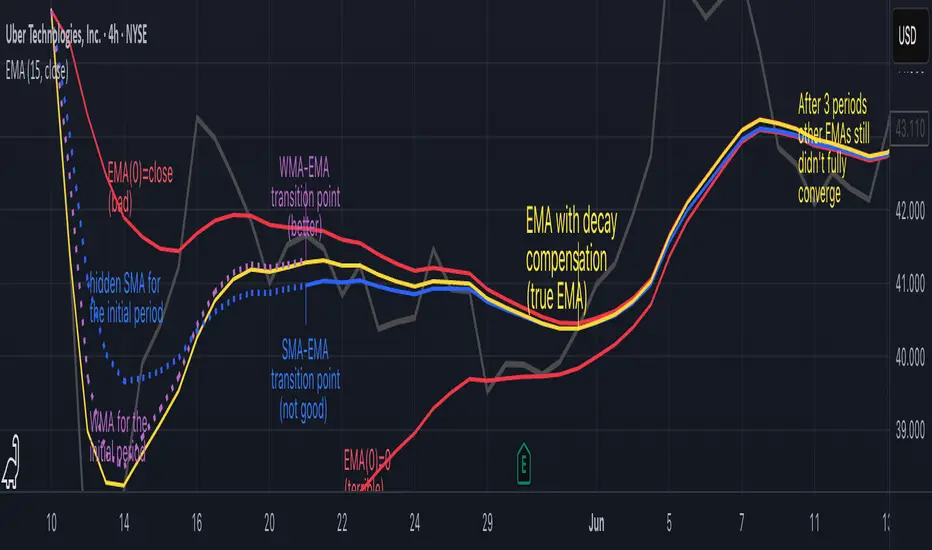

Why EMA Isn't What You Think It IsMany new traders adopt the Exponential Moving Average (EMA) believing it's simply a "better Simple Moving Average (SMA)". This common misconception leads to fundamental misunderstandings about how EMA works and when to use it.

EMA and SMA differ at their core. SMA use a window of finite number of data points, giving equal weight to each data point in the calculation period. This makes SMA a Finite Impulse Response (FIR) filter in signal processing terms. Remember that FIR means that "all that we need is the 'period' number of data points" to calculate the filter value. Anything beyond the given period is not relevant to FIR filters – much like how a security camera with 14-day storage automatically overwrites older footage, making last month's activity completely invisible regardless of how important it might have been.

EMA, however, is an Infinite Impulse Response (IIR) filter. It uses ALL historical data, with each past price having a diminishing - but never zero - influence on the calculated value. This creates an EMA response that extends infinitely into the past—not just for the last N periods. IIR filters cannot be precise if we give them only a 'period' number of data to work on - they will be off-target significantly due to lack of context, like trying to understand Game of Thrones by watching only the final season and wondering why everyone's so upset about that dragon lady going full pyromaniac.

If we only consider a number of data points equal to the EMA's period, we are capturing no more than 86.5% of the total weight of the EMA calculation. Relying on he period window alone (the warm-up period) will provide only 1 - (1 / e^2) weights, which is approximately 1−0.1353 = 0.8647 = 86.5%. That's like claiming you've read a book when you've skipped the first few chapters – technically, you got most of it, but you probably miss some crucial early context.

▶️ What is period in EMA used for?

What does a period parameter really mean for EMA? When we select a 15-period EMA, we're not selecting a window of 15 data points as with an SMA. Instead, we are using that number to calculate a decay factor (α) that determines how quickly older data loses influence in EMA result. Every trader knows EMA calculation: α = 1 / (1+period) – or at least every trader claims to know this while secretly checking the formula when they need it.

Thinking in terms of "period" seriously restricts EMA. The α parameter can be - should be! - any value between 0.0 and 1.0, offering infinite tuning possibilities of the indicator. When we limit ourselves to whole-number periods that we use in FIR indicators, we can only access a small subset of possible IIR calculations – it's like having access to the entire RGB color spectrum with 16.7 million possible colors but stubbornly sticking to the 8 basic crayons in a child's first art set because the coloring book only mentioned those by name.

For example:

Period 10 → alpha = 0.1818

Period 11 → alpha = 0.1667

What about wanting an alpha of 0.17, which might yield superior returns in your strategy that uses EMA? No whole-number period can provide this! Direct α parameterization offers more precision, much like how an analog tuner lets you find the perfect radio frequency while digital presets force you to choose only from predetermined stations, potentially missing the clearest signal sitting right between channels.

Sidenote: the choice of α = 1 / (1+period) is just a convention from 1970s, probably started by J. Welles Wilder, who popularized the use of the 14-day EMA. It was designed to create an approximate equivalence between EMA and SMA over the same number of periods, even thought SMA needs a period window (as it is FIR filter) and EMA doesn't. In reality, the decay factor α in EMA should be allowed any valye between 0.0 and 1.0, not just some discrete values derived from an integer-based period! Algorithmic systems should find the best α decay for EMA directly, allowing the system to fine-tune at will and not through conversion of integer period to float α decay – though this might put a few traditionalist traders into early retirement. Well, to prevent that, most traditionalist implementations of EMA only use period and no alpha at all. Heaven forbid we disturb people who print their charts on paper, draw trendlines with rulers, and insist the market "feels different" since computers do algotrading!

▶️ Calculating EMAs Efficiently

The standard textbook formula for EMA is:

EMA = CurrentPrice × alpha + PreviousEMA × (1 - alpha)

But did you know that a more efficient version exists, once you apply a tiny bit of high school algebra:

EMA = alpha × (CurrentPrice - PreviousEMA) + PreviousEMA

The first one requires three operations: 2 multiplications + 1 addition. The second one also requires three ops: 1 multiplication + 1 addition + 1 subtraction.

That's pathetic, you say? Not worth implementing? In most computational models, multiplications cost much more than additions/subtractions – much like how ordering dessert costs more than asking for a water refill at restaurants.

Relative CPU cost of float operations :

Addition/Subtraction: ~1 cycle

Multiplication: ~5 cycles (depending on precision and architecture)

Now you see the difference? 2 * 5 + 1 = 11 against 5 + 1 + 1 = 7. That is ≈ 36.36% efficiency gain just by swapping formulas around! And making your high school math teacher proud enough to finally put your test on the refrigerator.

▶️ The Warmup Problem: how to start the EMA sequence right

How do we calculate the first EMA value when there's no previous EMA available? Let's see some possible options used throughout the history:

Start with zero : EMA(0) = 0. This creates stupidly large distortion until enough bars pass for the horrible effect to diminish – like starting a trading account with zero balance but backdating a year of missed trades, then watching your balance struggle to climb out of a phantom debt for months.

Start with first price : EMA(0) = first price. This is better than starting with zero, but still causes initial distortion that will be extra-bad if the first price is an outlier – like forming your entire opinion of a stock based solely on its IPO day price, then wondering why your model is tanking for weeks afterward.

Use SMA for warmup : This is the tradition from the pencil-and-paper era of technical analysis – when calculators were luxury items and "algorithmic trading" meant your broker had neat handwriting. We first calculate an SMA over the initial period, then kickstart the EMA with this average value. It's widely used due to tradition, not merit, creating a mathematical Frankenstein that uses an FIR filter (SMA) during the initial period before abruptly switching to an IIR filter (EMA). This methodology is so aesthetically offensive (abrupt kink on the transition from SMA to EMA) that charting platforms hide these early values entirely, pretending EMA simply doesn't exist until the warmup period passes – the technical analysis equivalent of sweeping dust under the rug.

Use WMA for warmup : This one was never popular because it is harder to calculate with a pencil - compared to using simple SMA for warmup. Weighted Moving Average provides a much better approximation of a starting value as its linear descending profile is much closer to the EMA's decay profile.

These methods all share one problem: they produce inaccurate initial values that traders often hide or discard, much like how hedge funds conveniently report awesome performance "since strategy inception" only after their disastrous first quarter has been surgically removed from the track record.

▶️ A Better Way to start EMA: Decaying compensation

Think of it this way: An ideal EMA uses an infinite history of prices, but we only have data starting from a specific point. This creates a problem - our EMA starts with an incorrect assumption that all previous prices were all zero, all close, or all average – like trying to write someone's biography but only having information about their life since last Tuesday.

But there is a better way. It requires more than high school math comprehension and is more computationally intensive, but is mathematically correct and numerically stable. This approach involves compensating calculated EMA values for the "phantom data" that would have existed before our first price point.

Here's how phantom data compensation works:

We start our normal EMA calculation:

EMA_today = EMA_yesterday + α × (Price_today - EMA_yesterday)

But we add a correction factor that adjusts for the missing history:

Correction = 1 at the start

Correction = Correction × (1-α) after each calculation

We then apply this correction:

True_EMA = Raw_EMA / (1-Correction)

This correction factor starts at 1 (full compensation effect) and gets exponentially smaller with each new price bar. After enough data points, the correction becomes so small (i.e., below 0.0000000001) that we can stop applying it as it is no longer relevant.

Let's see how this works in practice:

For the first price bar:

Raw_EMA = 0

Correction = 1

True_EMA = Price (since 0 ÷ (1-1) is undefined, we use the first price)

For the second price bar:

Raw_EMA = α × (Price_2 - 0) + 0 = α × Price_2

Correction = 1 × (1-α) = (1-α)

True_EMA = α × Price_2 ÷ (1-(1-α)) = Price_2

For the third price bar:

Raw_EMA updates using the standard formula

Correction = (1-α) × (1-α) = (1-α)²

True_EMA = Raw_EMA ÷ (1-(1-α)²)

With each new price, the correction factor shrinks exponentially. After about -log₁₀(1e-10)/log₁₀(1-α) bars, the correction becomes negligible, and our EMA calculation matches what we would get if we had infinite historical data.

This approach provides accurate EMA values from the very first calculation. There's no need to use SMA for warmup or discard early values before output converges - EMA is mathematically correct from first value, ready to party without the awkward warmup phase.

Here is Pine Script 6 implementation of EMA that can take alpha parameter directly (or period if desired), returns valid values from the start, is resilient to dirty input values, uses decaying compensator instead of SMA, and uses the least amount of computational cycles possible.

// Enhanced EMA function with proper initialization and efficient calculation

ema(series float source, simple int period=0, simple float alpha=0)=>

// Input validation - one of alpha or period must be provided

if alpha<=0 and period<=0

runtime.error("Alpha or period must be provided")

// Calculate alpha from period if alpha not directly specified

float a = alpha > 0 ? alpha : 2.0 / math.max(period, 1)

// Initialize variables for EMA calculation

var float ema = na // Stores raw EMA value

var float result = na // Stores final corrected EMA

var float e = 1.0 // Decay compensation factor

var bool warmup = true // Flag for warmup phase

if not na(source)

if na(ema)

// First value case - initialize EMA to zero

// (we'll correct this immediately with the compensation)

ema := 0

result := source

else

// Standard EMA calculation (optimized formula)

ema := a * (source - ema) + ema

if warmup

// During warmup phase, apply decay compensation

e *= (1-a) // Update decay factor

float c = 1.0 / (1.0 - e) // Calculate correction multiplier

result := c * ema // Apply correction

// Stop warmup phase when correction becomes negligible

if e <= 1e-10

warmup := false

else

// After warmup, EMA operates without correction

result := ema

result // Return the properly compensated EMA value

▶️ CONCLUSION

EMA isn't just a "better SMA"—it is a fundamentally different tool, like how a submarine differs from a sailboat – both float, but the similarities end there. EMA responds to inputs differently, weighs historical data differently, and requires different initialization techniques.

By understanding these differences, traders can make more informed decisions about when and how to use EMA in trading strategies. And as EMA is embedded in so many other complex and compound indicators and strategies, if system uses tainted and inferior EMA calculatiomn, it is doing a disservice to all derivative indicators too – like building a skyscraper on a foundation of Jell-O.

The next time you add an EMA to your chart, remember: you're not just looking at a "faster moving average." You're using an INFINITE IMPULSE RESPONSE filter that carries the echo of all previous price actions, properly weighted to help make better trading decisions.

EMA done right might significantly improve the quality of all signals, strategies, and trades that rely on EMA somewhere deep in its algorithmic bowels – proving once again that math skills are indeed useful after high school, no matter what your guidance counselor told you.

Smart Money Flow Signals [QuantAlgo]🟢 Overview

The Smart Money Flow Signals indicator synthesizes significant volume-price dynamics through multi-component analysis to identify potential accumulation and distribution phases driven by substantial market participants. It combines Money Flow Index momentum, Chaikin Money Flow accumulation patterns, volume-weighted price momentum, and buying/selling pressure metrics into a unified composite oscillator that quantifies periods of concentrated capital movement, helping traders and investors identify conditions where significant volume participants may be actively positioning across multiple market conditions and timeframes.

🟢 How It Works

The indicator's core methodology lies in its weighted composite approach, where multiple volume-price components are calculated sequentially and then integrated to create a comprehensive significant flow activity signal.

First, the Money Flow Index (MFI) is calculated to measure buying and selling pressure by incorporating volume into price momentum analysis:

raw_money_flow = source * volume

positive_flow = source >= source ? raw_money_flow : 0

negative_flow = source < source ? raw_money_flow : 0

positive_money_flow = math.sum(positive_flow, mfi_period)

negative_money_flow = math.sum(negative_flow, mfi_period)

money_flow_index = 100 - 100 / (1 + positive_money_flow / negative_money_flow)

This creates an RSI-style momentum indicator that tracks whether money (price × volume) is flowing into or out of the asset, with values ranging from 0 to 100 where readings above 50 suggest buying pressure dominance.

Then, Chaikin Money Flow (CMF) is computed to evaluate accumulation and distribution by analyzing where prices close within each bar's range, weighted by volume:

money_flow_multiplier = high != low ? (close - low - (high - close)) / (high - low) : 0

money_flow_volume = money_flow_multiplier * volume

volume_sma = ta.sma(volume, trend_period)

chaikin_money_flow = volume_sma != 0 ? ta.sma(money_flow_volume, trend_period) / volume_sma : 0

Positive CMF values indicate accumulation (closes near the high of the range), while negative values indicate distribution (closes near the low of the range), with volume weighting emphasizing periods of significant participation.

Next, Volume Analysis is performed to quantify current volume intensity relative to historical averages:

volume_average = ta.sma(volume, trend_period)

volume_strength = volume_average != 0 ? volume / volume_average : 1

volume_weight = math.log(volume_strength + 1)

The logarithmic transformation creates a volume weight that amplifies signals during high-volume periods while preventing extreme volume spikes from overwhelming the composite calculation.

Following this, Buy/Sell Pressure is quantified by comparing cumulative volume during bullish versus bearish candles:

buying_pressure = math.sum(volume * (close >= open ? 1 : 0), trend_period)

selling_pressure = math.sum(volume * (close < open ? 1 : 0), trend_period)

pressure_ratio = (buying_pressure - selling_pressure) / (buying_pressure + selling_pressure) * 100

This creates a directional pressure ratio that reveals whether significant participants are predominantly buying or selling, expressed as a percentage between -100 (all selling) and +100 (all buying).

Then, Volume-Weighted Momentum is calculated through an exponential smoothing channel that adjusts price deviation based on volume intensity:

exponential_smooth_average = ta.ema(source, momentum_channel_period)

deviation = ta.ema(math.abs(source - exponential_smooth_average), momentum_channel_period)

channel_index = deviation != 0 ? (source - exponential_smooth_average) / (0.015 * deviation) * (1 + volume_weight * 0.5) : 0

This channel index measures how far price has deviated from its exponential average relative to typical deviation, with the volume weight multiplier (1 + volume_weight * 0.5) amplifying the signal when significant volume accompanies the price movement.

Finally, the Composite Wave is constructed by combining all components with specific weighting to create the final oscillator:

momentum_wave = ta.ema(channel_index, trend_period)

money_flow_wave = (money_flow_index - 50) * 1.2

chaikin_flow_wave = chaikin_money_flow * 100

composite_wave = momentum_wave * 0.5 + chaikin_flow_wave * 0.3 + money_flow_wave * 0.2

smoothed_wave = ta.sma(composite_wave, signal_smoothing)

This creates a multi-dimensional volume flow oscillator that combines price-volume momentum, accumulation-distribution patterns, and buying-selling pressure into a single signal, providing traders with probabilistic insights into periods of concentrated market activity and directional bias based on weighted component convergence.

🟢 Signal Interpretation

▶ Positive Values (Above Zero, Green): Composite money flow above equilibrium indicating net accumulation pressure, positive buying volume dominance, and bullish volume-price alignment = Favorable conditions for long positions, significant capital flowing into the asset = Buy/hold opportunities

▶ Negative Values (Below Zero, Red): Composite money flow below equilibrium indicating net distribution pressure, negative selling volume dominance, and bearish volume-price alignment = Unfavorable conditions for long positions, significant capital flowing out of the asset = Sell/short opportunities

▶ Extreme Overbought Zone: Excessive bullish money flow indicating potential accumulation exhaustion, where buying pressure may have reached unsustainable levels with elevated reversal risk = Caution on new longs, potential distribution phase beginning, profit-taking zone for existing positions

▶ Extreme Oversold Zone: Excessive bearish money flow indicating potential distribution exhaustion, where selling pressure may have reached unsustainable levels with elevated reversal risk = Caution on new shorts, potential accumulation phase beginning, buying opportunity zone for contrarian entries

▶ Smoothed Trend Line (White) Alignment: When the smoothed trend line confirms the composite wave direction, it validates the underlying volume-price trend and filters false signals caused by short-term noise

▶ Volume Intensity Correlation: Gradient intensity (color saturation) reflects combined wave strength, volume participation, and directional alignment, where darker/more saturated colors indicate stronger concentrated activity and higher-probability directional moves

🟢 Features

▶ Preconfigured Presets: Three optimized parameter configurations accommodate different trading styles, timeframes, and market analysis approaches.

1. "Default" provides balanced volume flow measurement suitable for swing trading on 4-hour and daily charts, offering moderate responsiveness to money flow shifts with standard RSI-equivalent MFI period and moderate smoothing for most market conditions.

2. "Fast Response" delivers heightened sensitivity optimized for active intraday trading and scalping on 1-minute to 1-hour charts, using compressed calculation periods across all components and minimal smoothing to capture rapid volume flow changes and quick trend shifts as they develop, ideal for early entry/exit opportunities with acceptance of increased signal frequency during consolidation.

3. "Smooth Trend" offers conservative extreme identification ideal for position trading and long-term analysis on daily to weekly charts, employing extended periods across all money flow components with substantial smoothing to filter short-term noise and isolate only strong, sustained accumulation and distribution phases driven by significant volume participants.

▶ Built-in Alerts: Seven alert conditions enable comprehensive automated monitoring of significant money flow transitions and extreme market states.

1. "Bullish Flow" triggers when the composite wave crosses above zero, signaling the shift from distribution to accumulation and concentrated buying activity beginning.

2. "Bearish Flow" activates when the composite wave crosses below zero, signaling the shift from accumulation to distribution and concentrated selling activity starting.

3. "Any Flow Direction Change" provides a combined notification for either bullish or bearish crossover regardless of direction, useful for general money flow momentum shifts.

4. "Extreme Overbought" alerts when the composite wave reaches or exceeds the overbought threshold (default +60), indicating excessive buying pressure and potential exhaustion.

5. "Extreme Oversold" notifies when the composite wave reaches or falls below the oversold threshold (default -60), indicating excessive selling pressure and potential capitulation.

6. "Overbought Reversal" triggers specifically when the wave crosses back down through the overbought level after being extended, signaling the beginning of distribution from extreme levels.

7. "Oversold Reversal" activates when the wave crosses back up through the oversold level after being extended, signaling the beginning of accumulation from extreme levels.

▶ Color Customization: Six visual themes (Classic, Aqua, Cosmic, Ember, Neon, plus Custom) accommodate different chart backgrounds and visual preferences, ensuring optimal contrast and immediate identification of bullish versus bearish volume flow conditions across various devices and screen sizes. Optional bar coloring provides instant visual context of current significant volume activity intensity and direction without switching between the price pane and indicator pane, enabling traders and investors to immediately assess volume-price positioning dynamics while analyzing price action.

Moving_AveragesLibrary "Moving_Averages"

This library contains majority important moving average functions with int series support. Which means that they can be used with variable length input. For conventional use, please use tradingview built-in ta functions for moving averages as they are more precise. I'll use functions in this library for my other scripts with dynamic length inputs.

ema(src, len)

Exponential Moving Average (EMA)

Parameters:

src : Source

len : Period

Returns: Exponential Moving Average with Series Int Support (EMA)

alma(src, len, a_offset, a_sigma)

Arnaud Legoux Moving Average (ALMA)

Parameters:

src : Source

len : Period

a_offset : Arnaud Legoux offset

a_sigma : Arnaud Legoux sigma

Returns: Arnaud Legoux Moving Average (ALMA)

covwema(src, len)

Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

covwma(src, len)

Coefficient of Variation Weighted Moving Average (COVWMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Moving Average (COVWMA)

dema(src, len)

DEMA - Double Exponential Moving Average

Parameters:

src : Source

len : Period

Returns: DEMA - Double Exponential Moving Average

edsma(src, len, ssfLength, ssfPoles)

EDSMA - Ehlers Deviation Scaled Moving Average

Parameters:

src : Source

len : Period

ssfLength : EDSMA - Super Smoother Filter Length

ssfPoles : EDSMA - Super Smoother Filter Poles

Returns: Ehlers Deviation Scaled Moving Average (EDSMA)

eframa(src, len, FC, SC)

Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

Parameters:

src : Source

len : Period

FC : Lower Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

SC : Upper Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

Returns: Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

ehma(src, len)

EHMA - Exponential Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Exponential Hull Moving Average (EHMA)

etma(src, len)

Exponential Triangular Moving Average (ETMA)

Parameters:

src : Source

len : Period

Returns: Exponential Triangular Moving Average (ETMA)

frama(src, len)

Fractal Adaptive Moving Average (FRAMA)

Parameters:

src : Source

len : Period

Returns: Fractal Adaptive Moving Average (FRAMA)

hma(src, len)

HMA - Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Hull Moving Average (HMA)

jma(src, len, jurik_phase, jurik_power)

Jurik Moving Average - JMA

Parameters:

src : Source

len : Period

jurik_phase : Jurik (JMA) Only - Phase

jurik_power : Jurik (JMA) Only - Power

Returns: Jurik Moving Average (JMA)

kama(src, len, k_fastLength, k_slowLength)

Kaufman's Adaptive Moving Average (KAMA)

Parameters:

src : Source

len : Period

k_fastLength : Number of periods for the fastest exponential moving average

k_slowLength : Number of periods for the slowest exponential moving average

Returns: Kaufman's Adaptive Moving Average (KAMA)

kijun(_high, _low, len, kidiv)

Kijun v2

Parameters:

_high : High value of bar

_low : Low value of bar

len : Period

kidiv : Kijun MOD Divider

Returns: Kijun v2

lsma(src, len, offset)

LSMA/LRC - Least Squares Moving Average / Linear Regression Curve

Parameters:

src : Source

len : Period

offset : Offset

Returns: Least Squares Moving Average (LSMA)/ Linear Regression Curve (LRC)

mf(src, len, beta, feedback, z)

MF - Modular Filter

Parameters:

src : Source

len : Period

beta : Modular Filter, General Filter Only - Beta

feedback : Modular Filter Only - Feedback

z : Modular Filter Only - Feedback Weighting

Returns: Modular Filter (MF)

rma(src, len)

RMA - RSI Moving average

Parameters:

src : Source

len : Period

Returns: RSI Moving average (RMA)

sma(src, len)

SMA - Simple Moving Average

Parameters:

src : Source

len : Period

Returns: Simple Moving Average (SMA)

smma(src, len)

Smoothed Moving Average (SMMA)

Parameters:

src : Source

len : Period

Returns: Smoothed Moving Average (SMMA)

stma(src, len)

Simple Triangular Moving Average (STMA)

Parameters:

src : Source

len : Period

Returns: Simple Triangular Moving Average (STMA)

tema(src, len)

TEMA - Triple Exponential Moving Average

Parameters:

src : Source

len : Period

Returns: Triple Exponential Moving Average (TEMA)

thma(src, len)

THMA - Triple Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Triple Hull Moving Average (THMA)

vama(src, len, volatility_lookback)

VAMA - Volatility Adjusted Moving Average

Parameters:

src : Source

len : Period

volatility_lookback : Volatility lookback length

Returns: Volatility Adjusted Moving Average (VAMA)

vidya(src, len)

Variable Index Dynamic Average (VIDYA)

Parameters:

src : Source

len : Period

Returns: Variable Index Dynamic Average (VIDYA)

vwma(src, len)

Volume-Weighted Moving Average (VWMA)

Parameters:

src : Source

len : Period

Returns: Volume-Weighted Moving Average (VWMA)

wma(src, len)

WMA - Weighted Moving Average

Parameters:

src : Source

len : Period

Returns: Weighted Moving Average (WMA)

zema(src, len)

Zero-Lag Exponential Moving Average (ZEMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Exponential Moving Average (ZEMA)

zsma(src, len)

Zero-Lag Simple Moving Average (ZSMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Simple Moving Average (ZSMA)

evwma(src, len)

EVWMA - Elastic Volume Weighted Moving Average

Parameters:

src : Source

len : Period

Returns: Elastic Volume Weighted Moving Average (EVWMA)

tt3(src, len, a1_t3)

Tillson T3

Parameters:

src : Source

len : Period

a1_t3 : Tillson T3 Volume Factor

Returns: Tillson T3

gma(src, len)

GMA - Geometric Moving Average

Parameters:

src : Source

len : Period

Returns: Geometric Moving Average (GMA)

wwma(src, len)

WWMA - Welles Wilder Moving Average

Parameters:

src : Source

len : Period

Returns: Welles Wilder Moving Average (WWMA)

ama(src, _high, _low, len, ama_f_length, ama_s_length)

AMA - Adjusted Moving Average

Parameters:

src : Source

_high : High value of bar

_low : Low value of bar

len : Period

ama_f_length : Fast EMA Length

ama_s_length : Slow EMA Length

Returns: Adjusted Moving Average (AMA)

cma(src, len)

Corrective Moving average (CMA)

Parameters:

src : Source

len : Period

Returns: Corrective Moving average (CMA)

gmma(src, len)

Geometric Mean Moving Average (GMMA)

Parameters:

src : Source

len : Period

Returns: Geometric Mean Moving Average (GMMA)

ealf(src, len, LAPercLen_, FPerc_)

Ehler's Adaptive Laguerre filter (EALF)

Parameters:

src : Source

len : Period

LAPercLen_ : Median Length

FPerc_ : Median Percentage

Returns: Ehler's Adaptive Laguerre filter (EALF)

elf(src, len, LAPercLen_, FPerc_)

ELF - Ehler's Laguerre filter

Parameters:

src : Source

len : Period

LAPercLen_ : Median Length

FPerc_ : Median Percentage

Returns: Ehler's Laguerre Filter (ELF)

edma(src, len)

Exponentially Deviating Moving Average (MZ EDMA)

Parameters:

src : Source

len : Period

Returns: Exponentially Deviating Moving Average (MZ EDMA)

pnr(src, len, rank_inter_Perc_)

PNR - percentile nearest rank

Parameters:

src : Source

len : Period

rank_inter_Perc_ : Rank and Interpolation Percentage

Returns: Percentile Nearest Rank (PNR)

pli(src, len, rank_inter_Perc_)

PLI - Percentile Linear Interpolation

Parameters:

src : Source

len : Period

rank_inter_Perc_ : Rank and Interpolation Percentage

Returns: Percentile Linear Interpolation (PLI)

rema(src, len)

Range EMA (REMA)

Parameters:

src : Source

len : Period

Returns: Range EMA (REMA)

sw_ma(src, len)

Sine-Weighted Moving Average (SW-MA)

Parameters:

src : Source

len : Period

Returns: Sine-Weighted Moving Average (SW-MA)

vwap(src, len)

Volume Weighted Average Price (VWAP)

Parameters:

src : Source

len : Period

Returns: Volume Weighted Average Price (VWAP)

mama(src, len)

MAMA - MESA Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: MESA Adaptive Moving Average (MAMA)

fama(src, len)

FAMA - Following Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Following Adaptive Moving Average (FAMA)

hkama(src, len)

HKAMA - Hilbert based Kaufman's Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Hilbert based Kaufman's Adaptive Moving Average (HKAMA)

Demonstration of how history length affects all EMA valuesI saw some discussion of this so I whipped up an example to prove the that effect of history length on EMA values is pronounced, even for bars much further than the EMA length from the first candle of the chart.

This chart has two 89-bar EMAs of the close: a green one and a red one. However, for the red one, the first 89 bars of the graph are considered to have a close of "0", which is exactly whatTradingView's EMA calculation uses for bars before the start of the graph.

This is because unlike other moving averages, which reference the price of previous bars, the EMA references the EMA of previous bars. Therefore, bars closer to the beginning of the chart, where TradingView can't calculate an EMA because there is no previous EMA and therefore uses 0, will return substantially different values for the EMA() function that the same cart would with more history.

The further a bar is back in history, the less influence it has. However, every single historical bar has some influence on the EMA of every later bar.

To allow you to see this for yourself, this script contains the following inputs which you can change to see the effect:

-EMA period (default 89)

-Number of bars to ignore for EMA2 (default 89)

-decimal precision to show differences in. By making this a large number you can see that, although the effects diminish, history length affects all EMA values for the char.

-label spacing (increase this if you have a long history and run into TV's 50-label limit)

Multiple EMAMultiple EMA. Color switch of slowest EMA (def=200) when price close below or above. Trend marker when fastest EMA (def=9) cross slowest EMA (def=200).

Multiple EMAMultiple EMA lines. Color switch of slowest EMA (def=200) when price close above or below. Trend marker when fastest EMA (def=9) cross slowest one.

Mean Reversion Cloud (Ornstein-Uhlenbeck) // AlgoFyreThe Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator detects mean-reversion opportunities by applying the Ornstein-Uhlenbeck process. It calculates a dynamic mean using an Exponential Weighted Moving Average, surrounded by volatility bands, signaling potential buy/sell points when prices deviate.

TABLE OF CONTENTS

🔶 ORIGINALITY

🔸Adaptive Mean Calculation

🔸Volatility-Based Cloud

🔸Speed of Reversion (θ)

🔶 FUNCTIONALITY

🔸Dynamic Mean and Volatility Bands

🞘 How it works

🞘 How to calculate

🞘 Code extract

🔸Visualization via Table and Plotshapes

🞘 Table Overview

🞘 Plotshapes Explanation

🞘 Code extract

🔶 INSTRUCTIONS

🔸Step-by-Step Guidelines

🞘 Setting Up the Indicator

🞘 Understanding What to Look For on the Chart

🞘 Possible Entry Signals

🞘 Possible Take Profit Strategies

🞘 Possible Stop-Loss Levels

🞘 Additional Tips

🔸Customize settings

🔶 CONCLUSION

▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅

🔶 ORIGINALITY The Mean Reversion Cloud (Ornstein-Uhlenbeck) is a unique indicator that applies the Ornstein-Uhlenbeck stochastic process to identify mean-reverting behavior in asset prices. Unlike traditional moving average-based indicators, this model uses an Exponentially Weighted Moving Average (EWMA) to calculate the long-term mean, dynamically adjusting to recent price movements while still considering all historical data. It also incorporates volatility bands, providing a "cloud" that visually highlights overbought or oversold conditions. By calculating the speed of mean reversion (θ) through the autocorrelation of log returns, this indicator offers traders a more nuanced and mathematically robust tool for identifying mean-reversion opportunities. These innovations make it especially useful for markets that exhibit range-bound characteristics, offering timely buy and sell signals based on statistical deviations from the mean.

🔸Adaptive Mean Calculation Traditional MA indicators use fixed lengths, which can lead to lagging signals or over-sensitivity in volatile markets. The Mean Reversion Cloud uses an Exponentially Weighted Moving Average (EWMA), which adapts to price movements by dynamically adjusting its calculation, offering a more responsive mean.

🔸Volatility-Based Cloud Unlike simple moving averages that only plot a single line, the Mean Reversion Cloud surrounds the dynamic mean with volatility bands. These bands, based on standard deviations, provide traders with a visual cue of when prices are statistically likely to revert, highlighting potential reversal zones.

🔸Speed of Reversion (θ) The indicator goes beyond price averages by calculating the speed at which the price reverts to the mean (θ), using the autocorrelation of log returns. This gives traders an additional tool for estimating the likelihood and timing of mean reversion, making the signals more reliable in practice.

🔶 FUNCTIONALITY The Mean Reversion Cloud (Ornstein-Uhlenbeck) indicator is designed to detect potential mean-reversion opportunities in asset prices by applying the Ornstein-Uhlenbeck stochastic process. It calculates a dynamic mean through the Exponentially Weighted Moving Average (EWMA) and plots volatility bands based on the standard deviation of the asset's price over a specified period. These bands create a "cloud" that represents expected price fluctuations, helping traders to identify overbought or oversold conditions. By calculating the speed of reversion (θ) from the autocorrelation of log returns, the indicator offers a more refined way of assessing how quickly prices may revert to the mean. Additionally, the inclusion of volatility provides a comprehensive view of market conditions, allowing for more accurate buy and sell signals.

Let's dive into the details: