Cari dalam skrip untuk "GOLD"

Gold Pullback Strategy [Backtest + Alerts]XAU USD M5 M15 TP1-1

BUY Pull black EMA 21

Storsi oversold

GOLD Volume-Based Entry StrategyShort Description:

This script identifies potential long entries by detecting two consecutive bars with above-average volume and bullish price action. When these conditions are met, a trade is entered, and an optional profit target is set based on user input. This strategy can help highlight momentum-driven breakouts or trend continuations triggered by a surge in buying volume.

How It Works

Volume Moving Average

A simple moving average of volume (vol_ma) is calculated over a user-defined period (default: 20 bars). This helps us distinguish when volume is above or below recent averages.

Consecutive Green Volume Bars

First bar: Must be bullish (close > open) and have volume above the volume MA.

Second bar: Must also be bullish, with volume above the volume MA and higher than the first bar’s volume.

When these two bars appear in sequence, we interpret it as strong buying pressure that could drive price higher.

Entry & Profit Target

Upon detecting these two consecutive bullish bars, the script places a long entry.

A profit target is set at current price plus a user-defined fixed amount (default: 5 USD).

You can adjust this target, or you can add a stop-loss in the script to manage risk further.

Visual Cues

Buy Signal Marker appears on the chart when the second bar confirms the signal.

Green Volume Columns highlight the bars that fulfill the criteria, providing a quick visual confirmation of high-volume bullish bars.

Works fine on 1M-2M-5M-15M-30M. Do not use it on higher TF. Due the lack of historical data on lower TF, the backtest result is limited.

Gold & EUR/USD LTF liquidity Sweep + Market structure shift on a lower time frame for sniper entries

Gold Option Signals with EMA and RSIIndicators:

Exponential Moving Averages (EMAs): Faster to respond to recent price changes compared to simple moving averages.

RSI: Measures the magnitude of recent price changes to evaluate overbought or oversold conditions.

Signal Generation:

Buy Call Signal: Generated when the short EMA crosses above the long EMA and the RSI is not overbought (below 70).

Buy Put Signal: Generated when the short EMA crosses below the long EMA and the RSI is not oversold (above 30).

Plotting:

EMAs: Plotted on the chart to visualize trend directions.

Signals: Plotted as shapes on the chart where conditions are met.

RSI Background Color: Changes to red for overbought and green for oversold conditions.

Steps to Use:

Add the Script to TradingView:

Open TradingView, go to the Pine Script editor, paste the script, save it, and add it to your chart.

Interpret the Signals:

Buy Call Signal: Look for green labels below the price bars.

Buy Put Signal: Look for red labels above the price bars.

Customize Parameters:

Adjust the input parameters (e.g., lengths of EMAs, RSI levels) to better fit your trading strategy and market conditions.

Testing and Validation

To ensure that the script works as expected, you can test it on historical data and validate the signals against known price movements. Adjust the parameters if necessary to improve the accuracy of the signals.

Golden Cross VWMA & EMA 4h PinescriptlabsThis strategy combines the 50-period Volume-Weighted Moving Average (VWMA) on the current timeframe with a 200-period Simple Moving Average (SMA) on the 4-hour timeframe. This combination of indicators with different characteristics and time horizons aims to identify strong and sustained trends across multiple timeframes.

The VWMA is a variant of the moving average that assigns greater weight to periods of higher volatility, helping to avoid misleading signals. On the other hand, the 4-hour SMA is used as an additional trend filter in a shorter-term horizon. By combining these two indicators, the strategy can leverage the strength of the VWMA to capture the main trend, but only when confirmed by the SMA in the lower timeframe.

Buy signals are generated when the VWMA crosses above the 4-hour SMA, indicating a potential bullish trend aligned in both timeframes. Sell signals occur on a bearish cross, suggesting a possible reversal of the main trend.

The default parameters are a 50-period VWMA and a 200-period 4-hour SMA. It is recommended to adjust these lengths according to the traded instrument and the desired timeframe. It is also crucial to use stop losses and profit targets to properly manage risk.

By combining indicators of different types and timeframes, this strategy aims to provide a more comprehensive view of trend strength.

Español:

Esta estrategia combina la Volume-Weighted Moving Average (VWMA) de 50 períodos en el timeframe actual con una Simple Moving Average (SMA) de 200 períodos en el timeframe de 4 horas. Esta combinación de indicadores de distinta naturaleza y horizontes temporales busca identificar tendencias fuertes y sostenidas en múltiples timeframes.

La VWMA es una variante de la media móvil que asigna mayor ponderación a los períodos de mayor volatilidad, lo que ayuda a evitar señales engañosas. Por otro lado, la SMA de 4 horas se utiliza como un filtro adicional de tendencia en un horizonte de corto plazo. Al combinar estos dos indicadores, la estrategia puede aprovechar la fortaleza de la VWMA para capturar la tendencia principal, pero sólo cuando es confirmada por la SMA en el timeframe menor.

Las señales de compra se generan cuando la VWMA cruza al alza la SMA de 4 horas, indicando una potencial tendencia alcista alineada en ambos horizontes temporales. Las señales de venta ocurren en el cruce bajista, sugiriendo una posible reversión de la tendencia principal.

Los parámetros predeterminados son: VWMA de 50 períodos y SMA de 4 horas de 200 períodos. Se recomienda ajustar estas longitudes según el instrumento operado y el horizonte temporal deseado. También es crucial utilizar stops y objetivos de ganancias para controlar adecuadamente el riesgo.

Al combinar indicadores de diferentes tipos y timeframes, esta estrategia busca brindar una visión más completa de la fuerza de la tendencia.

Golden Swing Strategy - Souradeep DeyThis strategy is developed by Mr. Souradeep Dey. Strategy is based on RSI, Stoch, BB & Supertrend.

Coding by Rajkumar

Golden Swing StrategyBuying Conditions

RSI should be 50 or above

Stochastic %K should be above %D

Day Low Should be below SuperTrend

SuperTrend should remain green before & EOD

SuperTrend should be below Mid Bollinger

Buy next day at open or within 0.5xATR(previous day) of SuperTrend with 1.1ATR SL & 2.2 ATR target

Selling Conditions

RSI should be 50 or below.

Stochastic %K should be below %D

Day high Should be above SuperTrend

SuperTrend should remain Red before & EOD

SuperTrend should be above Mid Bollinger

Sell next day at open or within 0.5xATR (previous day) of SuperTrend with 1.1xATR SL & 2.2x ATR target

Golden Cross Optimised For Reversal (by Coinrule)A moving average crossing is a common and widely adopted trading strategy. A short-term MA crossing above a long-term one provides the buy-signal. The opposite generates a sell-signal for the strategy.

Although very popular, this strategy has some limitations that lead to frequent "false signals" and only a few very profitable trades. If the strategy provides two many trades, that generates

the risk for more potential losses

more transaction fees paid

capital allocated to the strategy, thus the impossibility of catching other potential opportunities.

Applying an additional filter to the strategy, consisting of the crossing happening below a longer-term moving average, allows increasing the chances of catching the first crossing signaling a reversal.

The indicator is set to work with three moving averages.

Buy signal: The MA(9) to cross above the MA(50), which must be below the MA(100)

Sell Signal: The MA(9) to cross below the MA(50)

This indicator works significantly better on lower time frames, where it can reduce the noise of getting too many non-profitable signals from a conventional crossing strategy.

The indicator has been backtested mostly on cryptocurrencies.

Golden Ratio MultiplierThe moving averages 350 and 111 by themselves do a great job of identifying market tops/bottoms. The fraction 350/111 is very close to Pi as well (3.15) so that's is suspicious in its own right.

Nonetheless, fibonacci retracements/multiplies of the 350 SMA does a remarkable job of finding reversal points. I commented out a couple of multiplies for simplicity's sake (the lines became rather crowded). However, the script is open source so you all can copy it into Pine Editor and delete the "//" and add it back to the script.

Cheers.

Golden Ratio Multiplier: Multiplied Moving AveragesThe script for plotting DMAs from the study made by @PositiveCrypto (twitter)

Golden Ratio Multiplier: Multiplied Moving AveragesMultiplied moving averages script visualizing the study made by @PositiveCrypto (twitter).

GoldFinger .007Goldfinger.

He's the man, the man with the midas touch.

A spider's touch.

Such a cold finger.

Beckons you to enter his web of sin

But don't go in.

MTF EMA Traffic Light System Trend Alignment for ScalpersMTF EMA Traffic Light – Trend Bias System

This indicator is designed to help traders quickly identify high-probability trend alignment using multiple timeframes and EMAs.

It analyzes price relative to the 13 EMA and 55 EMA on:

1 Minute

5 Minute

15 Minute

1 Hour

4 Hour

Then it converts that data into a simple Traffic Light system to guide trade decisions.

🚦 How It Works

Each timeframe is classified as:

🟢 BULL – Price above both EMAs

🔴 BEAR – Price below both EMAs

🟡 MIXED – No clear direction

The system focuses on lower-timeframe alignment:

When 1m + 5m + 15m are aligned → Strong setup

When mixed → Caution

When misaligned → Stand aside

🟢 GREEN State (Full Trade Mode)

Triggered when:

✔ 1m, 5m, and 15m are all BULL → Long Bias

✔ 1m, 5m, and 15m are all BEAR → Short Bias

Rules:

Full position size

Trade with trend

Look for EMA pullbacks

Let winners run

🟡 YELLOW State (Caution Mode)

Triggered when:

✔ Lower timeframes are mixed

Rules:

Reduce size

Take quick profits

No holding

Defensive trading

🔴 RED State (No Trade)

Triggered when:

✔ No clear alignment

Rules:

Stay out

Mark key levels

Protect capital

📋 Dashboard Panel

The indicator displays a real-time table showing:

Each timeframe’s bias

Overall market state

Trade rules

This allows you to read market structure in seconds without switching charts.

🎯 Best Use

This tool works best for:

✔ Scalping

✔ Intraday trading

✔ Trend continuation setups

✔ EMA pullback strategies

Recommended for:

Forex

Indices

Gold

Crypto

⚠️ Risk Disclaimer

This indicator is a decision-support tool, not a guarantee of profits.

Always use:

Proper risk management

Stop losses

Personal trade rules

Never risk more than you can afford to lose.

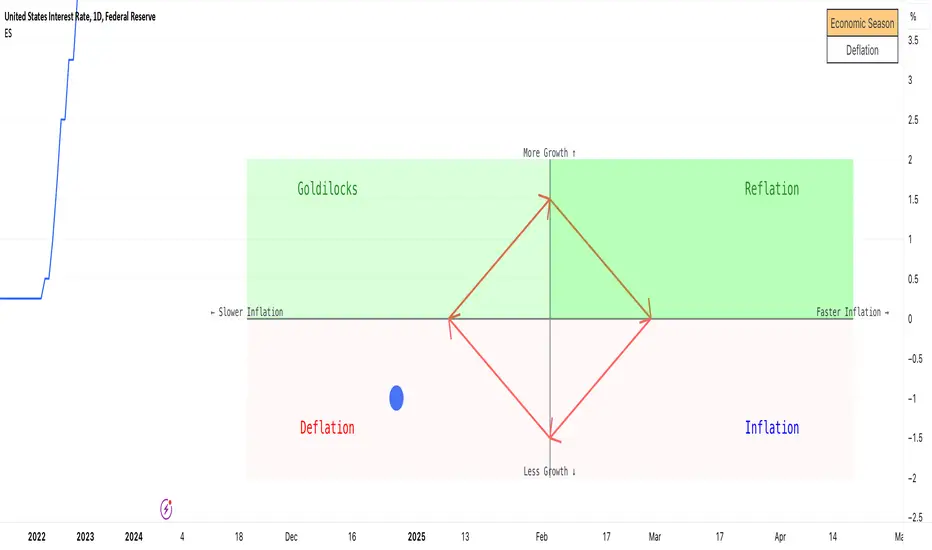

Economic Seasons [Daveatt]Ever wondered what season your economy is in?

Just like Mother Nature has her four seasons, the economy cycles through its own seasons! This indicator helps you visualize where we are in the economic cycle by tracking two key metrics:

📊 What We're Tracking:

1. Interest Rates (USIRYY) - The yearly change in interest rates

2. Inflation Rate (USINTR) - The rate at which prices are rising

The magic happens when we normalize these values (fancy math that makes the numbers play nice together) and compare them to their recent averages. We use a lookback period to calculate the standard deviation and determine if we're seeing higher or lower than normal readings.

🔄 The Four Economic Seasons & Investment Strategy:

1. 🌸 Goldilocks (↑Growth, ↓Inflation)

"Not too hot, not too cold" - The economy is growing steadily without overheating.

BEST TIME TO: Buy growth stocks, technology, consumer discretionary

WHY: Companies can grow earnings in this ideal environment of low rates and stable prices

2. 🌞 Reflation (↑Growth, ↑Inflation)

"Party time... but watch your wallet!" - The economy is heating up.

BEST TIME TO: Buy commodities, banking stocks, real estate

WHY: These sectors thrive when inflation rises alongside growth

3. 🌡️ Inflation (↓Growth, ↑Inflation)

"Ouch, my purchasing power!" - Growth slows while prices keep rising.

BEST TIME TO: Rotate into value stocks, consumer staples, healthcare

WHY: These defensive sectors maintain pricing power during inflationary periods

4. ❄️ Deflation (↓Growth, ↓Inflation)

"Winter is here" - Both growth and inflation are falling.

BEST TIME TO: Focus on quality bonds, cash positions, and dividend aristocrats

WHY: Capital preservation becomes key; high-quality fixed income provides safety

🎯 Strategic Trading Points:

- BUY AGGRESSIVELY: During late Deflation/early Goldilocks (the spring thaw)

- HOLD & ACCUMULATE: Throughout Goldilocks and early Reflation

- START TAKING PROFITS: During late Reflation/early Inflation

- DEFENSIVE POSITIONING: Throughout Inflation and Deflation

⚠️ Warning Signs to Watch:

- Goldilocks → Reflation: Time to reduce growth stock exposure

- Reflation → Inflation: Begin rotating into defensive sectors

- Inflation → Deflation: Quality becomes crucial

- Deflation → Goldilocks: Start building new positions

The blue dot shows you where we are right now in this cycle.

The red arrows in the middle remind us that this is a continuous cycle - one season flows into the next, just like in nature!

💡 Pro Tip: The transitions between seasons often provide the best opportunities - but also the highest risks. Use additional indicators and fundamental analysis to confirm these shifts.

Remember: Just like you wouldn't wear a winter coat in summer, you shouldn't use a Goldilocks strategy during Inflation! Time your trades with the seasons. 🎯

Happy Trading! 📈

RSI Fibonacci Flow [JOAT]RSI Fibonacci Flow - Advanced Fibonacci Retracement with RSI Confluence

Introduction

RSI Fibonacci Flow is an open-source overlay indicator that combines automatic Fibonacci retracement levels with RSI momentum analysis to identify high-probability trading zones. The indicator automatically detects swing highs and lows, draws Fibonacci levels, and generates confluence signals when RSI conditions align with key Fibonacci zones.

This indicator is designed for traders who use Fibonacci retracements but want additional confirmation from momentum analysis before entering trades.

Originality and Purpose

This indicator is NOT a simple mashup of RSI and Fibonacci tools. It is an original implementation that creates a synergistic relationship between two complementary analysis methods:

Why Combine RSI with Fibonacci? Fibonacci retracements identify WHERE price might reverse, but they don't tell you WHEN. RSI provides the timing component by showing momentum exhaustion. When price reaches the Golden Zone (50%-61.8%) AND RSI shows oversold conditions, the probability of a successful bounce increases significantly.

Original Confluence Scoring System: The indicator calculates a 0-5 confluence score that weights multiple factors: Golden Zone presence (+2), entry zone presence (+1), RSI extreme alignment (+1), RSI divergence (+1), and strong RSI momentum (+1). This scoring system is original to this indicator.

Automatic Pivot Detection: Unlike manual Fibonacci tools, this indicator automatically detects swing highs and lows using a configurable pivot algorithm, then draws Fibonacci levels accordingly. The pivot detection uses a center-bar comparison method that checks if a bar's high/low is the highest/lowest within the specified depth on both sides.

Dynamic Trend Awareness: The indicator determines trend direction based on pivot sequence (last pivot was high or low) and adjusts Fibonacci orientation accordingly. In uptrends, 0% is at swing low; in downtrends, 0% is at swing high.

Each component serves a specific purpose:

Fibonacci levels identify potential reversal zones based on natural price ratios

RSI provides momentum context to filter out low-probability setups

Confluence scoring quantifies setup quality for position sizing decisions

Automatic pivot detection removes subjectivity from level placement

Core Concept: RSI-Fibonacci Confluence

The most powerful trading setups occur when multiple factors align. RSI Fibonacci Flow identifies these moments by:

Automatically detecting price pivots and drawing Fibonacci levels

Tracking which Fibonacci zone the current price occupies

Monitoring RSI for overbought/oversold conditions

Generating signals when RSI extremes coincide with key Fibonacci levels

Scoring confluence strength on a 0-5 scale

When price reaches the Golden Zone (50%-61.8%) while RSI shows oversold conditions in an uptrend, the probability of a bounce increases significantly.

Fibonacci Levels Explained

The indicator draws nine Fibonacci levels based on the most recent swing:

0% (Swing Low/High): The starting point of the move

23.6%: Shallow retracement - often seen in strong trends

38.2%: First significant support/resistance level

50%: Psychological midpoint of the move

61.8% (Golden Ratio): The most important Fibonacci level

78.6%: Deep retracement - last defense before trend failure

100% (Swing High/Low): The end point of the move

127.2% (TP1): First extension target for take profit

161.8% (TP2): Second extension target for take profit

The Golden Zone

The area between 50% and 61.8% is highlighted as the "Golden Zone" because:

It represents the optimal retracement depth for trend continuation

Institutional traders often place orders in this zone

It offers favorable risk-to-reward ratios

Price frequently bounces from this area in healthy trends

When price enters the Golden Zone, the indicator highlights it with a semi-transparent box and optional background coloring.

Pivot Detection System

The indicator uses a configurable pivot detection algorithm:

pivotDetect(float src, int len, bool isHigh) =>

int halfLen = len / 2

float centerVal = nz(src , src)

bool isPivot = true

for i = 0 to len - 1

if isHigh

if nz(src , src) > centerVal

isPivot := false

break

else

if nz(src , src) < centerVal

isPivot := false

break

isPivot ? centerVal : float(na)

This identifies swing highs and lows by checking if a bar's high/low is the highest/lowest within the specified depth on both sides.

Visual Components

1. Fibonacci Lines

Horizontal lines at each Fibonacci level:

Solid lines for major levels (0%, 50%, 61.8%, 100%)

Dashed lines for secondary levels (23.6%, 38.2%, 78.6%)

Dotted lines for extension levels (127.2%, 161.8%)

Color-coded for easy identification

Configurable line width

2. Fibonacci Labels

Price labels at each level showing:

Fibonacci percentage

Actual price at that level

Golden Zone label highlighted

TP1 and TP2 labels for targets

3. Golden Zone Box

A semi-transparent box highlighting the 50%-61.8% zone:

Gold colored border and fill

Extends from swing start to current bar (or beyond if extended)

Provides clear visual of the optimal entry zone

4. ZigZag Lines

Connecting lines between detected pivots:

Cyan for moves from low to high

Orange for moves from high to low

Helps visualize market structure

Configurable line width

5. Pivot Markers

Small labels at detected swing points:

"HH" (Higher High) at swing highs

"LL" (Lower Low) at swing lows

Helps track market structure

6. Entry Signals

BUY and SELL labels when confluence conditions are met:

BUY: RSI oversold + price in entry zone + uptrend + positive momentum

SELL: RSI overbought + price in entry zone + downtrend + negative momentum

Labels include "RSI+FIB" to indicate confluence

Confluence Scoring System

The indicator calculates a confluence score from 0 to 5:

+2 points: Price is in the Golden Zone (50%-61.8%)

+1 point: Price is in the entry zone (38.2%-61.8%)

+1 point: RSI is oversold in uptrend OR overbought in downtrend

+1 point: RSI divergence detected (bullish or bearish)

+1 point: Strong RSI momentum (change > 2 points)

Confluence ratings:

STRONG (4-5): Multiple factors align - high probability setup

MODERATE (2-3): Some factors align - proceed with caution

WEAK (0-1): Few factors align - wait for better setup

Dashboard Panel

The 10-row dashboard provides comprehensive analysis:

RSI Value: Current RSI reading (large text)

RSI State: OVERBOUGHT, OVERSOLD, BULLISH, BEARISH, or NEUTRAL

Fib Trend: UPTREND or DOWNTREND based on last pivot sequence

Price Zone: Current Fibonacci zone (e.g., "GOLDEN ZONE", "38.2% - 50%")

Price: Current close price (large text)

Confluence: Score rating with numeric value (e.g., "STRONG (4/5)")

Nearest Fib: Closest key Fibonacci level with price

TP1 (127.2%): First take profit target price

TP2 (161.8%): Second take profit target price

Input Parameters

Pivot Detection:

Pivot Depth: Bars to look back for swing detection (default: 10)

Min Deviation %: Minimum price move to confirm pivot (default: 1.0)

RSI Settings:

RSI Length: Period for RSI calculation (default: 14)

Source: Price source (default: close)

Overbought: Upper threshold (default: 70)

Oversold: Lower threshold (default: 30)

Fibonacci Display:

Show Fib Lines: Toggle Fibonacci lines (default: enabled)

Show Fib Labels: Toggle price labels (default: enabled)

Show Golden Zone Box: Toggle zone highlight (default: enabled)

Line Width: Thickness of Fibonacci lines (default: 2)

Extend Fib Lines: Extend lines into future (default: enabled)

ZigZag:

Show ZigZag: Toggle connecting lines (default: enabled)

ZigZag Width: Line thickness (default: 2)

Signals:

Show Entry Signals: Toggle BUY/SELL labels (default: enabled)

Show TP Levels: Toggle take profit in dashboard (default: enabled)

Show RSI-Fib Confluence: Toggle confluence analysis (default: enabled)

Dashboard:

Show Dashboard: Toggle information panel (default: enabled)

Position: Choose corner placement

Colors:

Bullish: Color for bullish elements (default: cyan)

Bearish: Color for bearish elements (default: orange)

Neutral: Color for neutral elements (default: gray)

Golden Zone: Color for Golden Zone highlight (default: gold)

How to Use RSI Fibonacci Flow

Identifying Entry Zones:

Wait for price to retrace to the 38.2%-61.8% zone

Check if RSI is approaching oversold (for longs) or overbought (for shorts)

Look for STRONG confluence rating in the dashboard

Enter when BUY or SELL signal appears

Setting Take Profit Targets:

TP1 at 127.2% extension for conservative target

TP2 at 161.8% extension for aggressive target

Consider scaling out at each level

Using the Price Zone:

"BELOW 23.6%" - Price hasn't retraced much; wait for deeper pullback

"23.6% - 38.2%" - Shallow retracement; strong trend continuation possible

"38.2% - 50%" - Good entry zone for trend trades

"GOLDEN ZONE" - Optimal entry zone; highest probability

"61.8% - 78.6%" - Deep retracement; trend may be weakening

"78.6% - 100%" - Very deep; trend reversal possible

"ABOVE/BELOW 100%" - Trend has likely reversed

Confluence Trading Strategy:

Only take trades with confluence score of 3 or higher

STRONG confluence (4-5) warrants larger position size

MODERATE confluence (2-3) warrants smaller position size

WEAK confluence (0-1) - wait for better setup

Alert Conditions

Ten alert conditions are available:

RSI-Fib BUY Signal: Strong bullish confluence detected

RSI-Fib SELL Signal: Strong bearish confluence detected

Price in Golden Zone: Price enters 50%-61.8% zone

New Pivot High: Swing high detected

New Pivot Low: Swing low detected

RSI Overbought: RSI crosses above overbought threshold

RSI Oversold: RSI crosses below oversold threshold

Bullish Divergence: Potential bullish RSI divergence

Bearish Divergence: Potential bearish RSI divergence

Strong Confluence: Confluence score reaches 4 or higher

Understanding Trend Direction

The indicator determines trend based on pivot sequence:

UPTREND: Last pivot was a low after a high (expecting move up)

DOWNTREND: Last pivot was a high after a low (expecting move down)

Fibonacci levels are drawn accordingly:

In uptrend: 0% at swing low, 100% at swing high

In downtrend: 0% at swing high, 100% at swing low

Bar Coloring

When confluence features are enabled:

Cyan bars on strong bullish signals

Orange bars on strong bearish signals

Gold-tinted bars when price is in Golden Zone

Best Practices

Use on 1H timeframe or higher for more reliable pivots

Adjust Pivot Depth based on timeframe (higher for longer timeframes)

Wait for price to enter Golden Zone before considering entries

Confirm RSI is in favorable territory before trading

Use extension levels (127.2%, 161.8%) for realistic profit targets

Combine with support/resistance and candlestick patterns

Higher confluence scores indicate higher probability setups

Limitations

Pivot detection has inherent lag (must wait for confirmation)

Fibonacci levels are subjective - different swings produce different levels

Works best in trending markets with clear swings

RSI can remain overbought/oversold in strong trends

Not all Golden Zone entries will be successful

The source code is open and available for review and modification.

Disclaimer

This indicator is provided for educational and informational purposes only. It is not financial advice. Trading involves substantial risk of loss. Past performance does not guarantee future results. Fibonacci levels are not guaranteed support/resistance - they are probability zones based on historical price behavior. Always conduct your own analysis and use proper risk management.

- Made with passion by officialjackofalltrades :D

Liquidity Sweep Guardian (Universal % or point based)

Liquidity Sweep Guardian - Complete User Guide

## Overview

The **Liquidity Sweep Guardian** is a visual warning system designed to prevent premature counter-trend trades (fades) near Previous Day High (PDH) and Previous Day Low (PDL) levels. This indicator helps you avoid one of the most common trading mistakes: fading too early before liquidity sweeps complete.

---

## 🎯 Core Trading Principle

### **THE GOLDEN RULE: Don't Fade Until It's Unlocked**

Price often **accelerates into key levels** to sweep liquidity before reversing. Trading against this momentum is extremely dangerous.

**The Process:**

1. **Danger Zone** (Red/White Box) = ⚠️ **DO NOT FADE** - Sweep likely incoming

2. **Sweep Occurs** (Triangle marker appears) = Price penetrates the level

3. **Reclaim Happens** (Price returns above/below level) = Level is tested

4. **🔓 UNLOCKED** (Gold border, green label) = **NOW you may CONSIDER a fade**

> **Important:** "UNLOCKED" means you may now *consider* a fade setup. It is NOT a trade signal itself. You still need your entry confirmation, risk management, and trade plan.

---

## 📊 Visual Elements Explained

### 1. **Danger Zone Boxes (Red Border by Default)**

**Two types of zones around PDH/PDL:**

- **Outer Danger Zone** (White fill): ±75pts (or 0.30%) around the level

- Indicates proximity to a key level where sweeps commonly occur

- Yellow/cautious trading zone

- **Inner Critical Zone** (Black fill): ±25pts (or 0.10%) around the level

- Highest probability area for liquidity sweep traps

- Avoid fading here at all costs

**What to do:**

- When price enters these zones, **wait and watch**

- Do not initiate counter-trend positions

- Allow the sweep to play out

### 2. **Unlocked Zones (Gold Border #ffeb3b)**

When a zone turns **gold/yellow** with green fill:

- The level has been swept AND reclaimed

- The liquidity grab is complete

- You may now look for fade opportunities with proper confirmation

### 3. **PDH/PDL Lines**

- **PDH Line** (Red): Previous Day High with price label

- **PDL Line** (Green): Previous Day Low with price label

- These are your key reference levels for the session

### 4. **Sweep Labels**

**Triangle Markers (SWEEP):**

- **Green Triangle** = Clean sweep (10-25pts penetration)

- **Orange Triangle** = Extended sweep (25-50pts penetration)

- **Red Triangle** = Deep penetration (50+ pts) - likely continuation, not reversal

**Warning Labels:**

- **⚠️ DEEP CONTINUATION?** = Penetration too deep, probably NOT a reversal setup

**Unlock Labels:**

- **🔓 LONG UNLOCKED** = PDL swept and reclaimed, may consider long fades

- **🔓 SHORT UNLOCKED** = PDH swept and reclaimed, may consider short fades

---

## ⚙️ Settings Guide

### **Calculation Mode**

**Use Percentage Mode (Default: ON)**

- ✅ **Enabled**: Universal mode - works on NQ, ES, RTY, stocks, crypto, forex

- ❌ **Disabled**: Fixed points mode - for specific instruments only

**When to use each:**

- **Percentage Mode**: Trading multiple instruments, or instruments with varying price levels

- **Fixed Points Mode**: Single instrument focus (e.g., only trading NQ at current levels)

### **Danger Zone Settings**

**Percentage Mode (Default for Universal Use):**

- **Danger Zone**: 0.30% each side (≈75pts on NQ@25,000)

- **Critical Zone**: 0.10% each side (≈25pts on NQ@25,000)

**Fixed Points Mode (For NQ Specifically):**

- **Danger Zone**: 75 points each side

- **Critical Zone**: 25 points each side

**Adjustment Tips:**

- For more volatile instruments: Increase percentages/points

- For less volatile instruments: Decrease percentages/points

- For higher timeframes: Use wider zones

- For lower timeframes: Use tighter zones

### **Sweep Classification**

**What defines a "real" sweep:**

- **Minimum**: 10pts / 0.04% - Shallow penetration may not grab enough liquidity

- **Optimal**: 10-25pts / 0.04-0.10% - "Goldilocks zone" for reversal setups

- **Extended**: 25-50pts / 0.10-0.20% - Deeper sweep, less reliable

- **Continuation**: 50+pts / 0.20%+ - Too deep, likely NOT reversing

**Max Bars for Reclaim**: 5 bars (default)

- Price should reclaim the level relatively quickly

- If it takes too long, the sweep may have failed

### **Visual Customization**

**Box Settings:**

- **Left Extension**: 60 bars (how far back the box extends)

- **Right Extension**: 50 bars (how far forward the box extends)

**Toggle Options:**

- Show/Hide Danger Zone Boxes

- Show/Hide PDH/PDL Lines

- Show/Hide Price Labels on lines

- Show/Hide Sweep Labels

- Show/Hide Unlock Labels

### **Color Customization**

All colors are fully customizable:

- Danger Zone Fill & Border

- Critical Zone Fill & Border

- Unlocked Zone Fill & Border

- PDH/PDL Line Colors

- PDH/PDL Label Colors

- Border Widths (1-5 pixels)

- Line Widths (1-5 pixels)

---

## 🎓 Trading Strategy Examples

### **Example 1: Long Setup at PDL**

1. **Morning**: Price approaches PDL (danger zone appears)

2. **Don't Fade Yet**: Price enters critical zone - resist urge to buy

3. **Sweep**: Price drops 15pts below PDL (green triangle appears)

4. **Reclaim**: Price closes back above PDL within 3 bars

5. **🔓 UNLOCKED**: Gold border + "LONG UNLOCKED" label appears

6. **Trade Setup**: Now look for bullish confirmation (order flow, structure, etc.)

### **Example 2: Avoiding a Trap at PDH**

1. **Afternoon**: Price rallies into PDH danger zone

2. **Temptation**: You want to short here (it "looks toppy")

3. **Sweep**: Price breaks 50pts above PDH (red triangle + ⚠️ warning)

4. **Continuation**: Deep penetration suggests continuation, not reversal

5. **Result**: No unlock occurs, price keeps running higher - trap avoided!

### **Example 3: Failed Unlock (No Trade)**

1. Price sweeps PDL by 12pts (green triangle)

2. Price struggles to reclaim PDL, stays below for 10+ bars

3. No "UNLOCKED" label appears

4. **Correct Action**: Do not fade - sweep failed to reclaim

---

## 📱 Alerts

The indicator includes built-in alerts for:

- **Entering Danger Zones**: Get warned when price approaches PDH/PDL

- **Sweep Detection**: Know immediately when a level is swept

- **Unlock Signals**: Get notified when fade setups become available

- **Continuation Warnings**: Alert when penetration suggests continuation

**To Set Alerts:**

1. Right-click indicator → "Add Alert"

2. Select desired alert condition

3. Configure notification preferences

---

## ⚠️ Important Disclaimers

### **What This Indicator IS:**

✅ A visual warning system to prevent premature fades

✅ A tool to identify when liquidity sweeps have completed

✅ A framework for counter-trend trade timing

### **What This Indicator IS NOT:**

❌ A complete trading system

❌ An entry signal generator

❌ A guarantee of trade success

❌ A substitute for proper risk management

### **Always Remember:**

- "UNLOCKED" = You may CONSIDER a fade (not a signal to trade)

- You still need your own entry confirmation

- You still need proper stop placement

- You still need position sizing and risk management

- Not every unlock leads to a successful trade

- Market context and order flow still matter

---

## 🔧 Recommended Settings by Instrument

### **NQ (Nasdaq-100 E-mini Futures)**

- Mode: Percentage or Fixed Points

- Percentage: 0.30% / 0.10% (default)

- Fixed Points: 75pts / 25pts (default)

### **ES (S&P 500 E-mini Futures)**

- Mode: Percentage

- Danger: 0.25% / Critical: 0.08%

- Or Fixed Points: 15pts / 5pts

### **RTY (Russell 2000 E-mini Futures)**

- Mode: Percentage

- Danger: 0.35% / Critical: 0.12%

- Or Fixed Points: 8pts / 3pts

### **Stocks (High Volume Large Caps)**

- Mode: Percentage (recommended)

- Danger: 0.20-0.40% / Critical: 0.08-0.15%

- Adjust based on ATR and volatility

### **Crypto (BTC, ETH)**

- Mode: Percentage (essential)

- Danger: 0.40-0.60% / Critical: 0.15-0.20%

- Higher volatility requires wider zones

---

## 💡 Pro Tips

1. **Use on Higher Timeframes**: Works best on 5min, 15min, 1hr charts

2. **Combine with Order Flow**: Use with footprint/delta for confirmation

3. **Watch Volume**: Strong volume on sweep = better reversal potential

4. **Consider Time of Day**: Sweeps during RTH often more reliable

5. **Multiple Timeframes**: Check if higher TF also shows unlock

6. **Don't Force Trades**: Not every session produces clean setups

7. **Journal Results**: Track which unlock types work best for you

8. **Respect Continuation Signals**: When indicator says "too deep," listen

---

## 🆘 Troubleshooting

**Q: Box isn't showing up**

A: Check that "Show Danger Zone Boxes" is enabled in Visual Settings

**Q: No price on labels**

A: Enable "Show Price Labels on Lines" in Visual Settings

**Q: Zones seem too tight/wide**

A: Adjust Danger Zone % or points based on current volatility

**Q: Getting too many/too few unlocks**

A: Adjust sweep classification thresholds (min/max penetration)

**Q: Want thicker/thinner lines**

A: Adjust line widths in "PDH/PDL Line Colors" section

**Q: Colors not matching my chart theme**

A: Fully customize all colors in the color settings groups

---

## 📚 Additional Resources

- Study price action around PDH/PDL on your instruments

- Learn about liquidity sweeps and stop hunts

- Understand market structure and order flow

- Practice identifying setups on replay/historical data

- Keep a trading journal of unlock scenarios

---

*Remember: The best trade is often the one you don't take. This indicator helps you avoid the trades you shouldn't take, so you can focus on the ones you should.*