VD Zig Zag with SMAIntroduction

The VD Zig Zag with SMA indicator is a powerful tool designed to streamline technical analysis by combining Zig Zag swing lines with a Simple Moving Average (SMA). It offers traders a clear and intuitive way to analyze price trends, market structure, and potential reversals, all within a customizable framework.

Definition

The Zig Zag indicator is a trend-following tool that highlights significant price movements by filtering out smaller fluctuations. It visually connects swing highs and lows to reveal the underlying market structure. When paired with an SMA, it provides an additional layer of trend confirmation, helping traders align their strategies with market momentum.

Calculations

Zig Zag Logic:

Swing highs and lows are determined using a user-defined length parameter.

The highest and lowest points within the specified range are identified using the ta.highest() and ta.lowest() functions.

Zig Zag lines dynamically connect these swing points to visually map price movements.

SMA Logic:

The SMA is calculated using the closing prices over a user-defined period.

It smooths out price action to provide a clearer view of the prevailing trend.

The indicator allows traders to adjust the Zig Zag length and SMA period to suit their preferred trading timeframe and strategy.

Takeaways

Enhanced Trend Analysis: The Zig Zag lines clearly define the market's structural highs and lows, helping traders identify trends and reversals.

Customizable Parameters: Both the swing length and SMA period can be tailored for short-term or long-term trading strategies.

Visual Clarity: By filtering out noise, the indicator simplifies chart analysis and enables better decision-making.

Multi-Timeframe Support: Adapts seamlessly to the chart's timeframe, ensuring usability across all trading horizons.

Limitations

Lagging Nature: As with any indicator, the Zig Zag and SMA components are reactive and may lag during sudden price movements.

Sensitivity to Parameters: Improper parameter settings can lead to overfitting, where the indicator reacts too sensitively or misses significant trends.

Does Not Predict: This indicator identifies trends and structure but does not provide forward-looking predictions.

Summary

The VD Zig Zag with SMA indicator is a versatile and easy-to-use tool that combines the strengths of Zig Zag swing analysis and moving average trends. It helps traders filter market noise, visualize structural patterns, and confirm trends with greater confidence. While it comes with limitations inherent to all technical tools, its customizable features and multi-timeframe adaptability make it an excellent addition to any trader’s toolkit.

Additional Features

Have an idea or a feature you'd like to see added?

Feel free to reach out or share your suggestions here—I’m always open to updates!

Cari dalam skrip untuk "TAKE"

Custom V2 KillZone US / FVG / EMAThis indicator is designed for traders looking to analyze liquidity levels, opportunity zones, and the underlying trend across different trading sessions. Inspired by the ICT methodology, this tool combines analysis of Exponential Moving Averages (EMA), session management, and Fair Value Gap (FVG) detection to provide a structured and disciplined approach to trading effectively.

Indicator Features

Identifying the Underlying Trend with Two EMAs

The indicator uses two EMAs on different, customizable timeframes to define the underlying trend:

EMA1 (default set to a daily timeframe): Represents the primary underlying trend.

EMA2 (default set to a 4-hour timeframe): Helps identify secondary corrections or impulses within the main trend.

These two EMAs allow traders to stay aligned with the market trend by prioritizing trades in the direction of the moving averages. For example, if prices are above both EMAs, the trend is bullish, and long trades are favored.

Analysis of Market Sessions

The indicator divides the day into key trading sessions:

Asian Session

London Session

US Pre-Open Session

Liquidity Kill Session

US Kill Zone Session

Each session is represented by high and low zones as well as mid-lines, allowing traders to visualize liquidity levels reached during these periods. Tracking the price levels in different sessions helps determine whether liquidity levels have been "swept" (taken) or not, which is essential for ICT methodology.

Liquidity Signal ("OK" or "STOP")

A specific signal appears at the end of the "Liquidity Kill" session (just before the "US Kill Zone" session):

"OK" Signal: Indicates that liquidity conditions are favorable for trading the "US Kill Zone" session. This means that liquidity levels have been swept in previous sessions (Asian, London, US Pre-Open), and the market is ready for an opportunity.

"STOP" Signal: Indicates that it is not favorable to trade the "US Kill Zone" session, as certain liquidity conditions have not been met.

The "OK" or "STOP" signal is based on an analysis of the high and low levels from previous sessions, allowing traders to ensure that significant liquidity zones have been reached before considering positions in the "Kill Zone".

Detection of Fair Value Gaps (FVG) in the US Kill Zone Session

When an "OK" signal is displayed, the indicator identifies Fair Value Gaps (FVG) during the "US Kill Zone" session. These FVGs are areas where price may return to fill an "imbalance" in the market, making them potential entry points.

Bullish FVG: Detected when there is a bullish imbalance, providing a buying opportunity if conditions align with the underlying trend.

Bearish FVG: Detected when there is a bearish imbalance, providing a selling opportunity in the trend direction.

FVG detection aligns with the ICT Silver Bullet methodology, where these imbalance zones serve as probable entry points during the "US Kill Zone".

How to Use This Indicator

Check the Underlying Trend

Before trading, observe the two EMAs (daily and 4-hour) to understand the general market trend. Trades will be prioritized in the direction indicated by these EMAs.

Monitor Liquidity Signals After the Asian, London, and US Pre-Open Sessions

The high and low levels of each session help determine if liquidity has already been swept in these areas. At the end of the "Liquidity Kill" session, an "OK" or "STOP" label will appear:

"OK" means you can look for trading opportunities in the "US Kill Zone" session.

"STOP" means it is preferable not to take trades in the "US Kill Zone" session.

Look for Opportunities in the US Kill Zone if the Signal is "OK"

When the "OK" label is present, focus on the "US Kill Zone" session. Use the Fair Value Gaps (FVG) as potential entry points for trades based on the ICT methodology. The identified FVGs will appear as colored boxes (bullish or bearish) during this session.

Use ICT Methodology to Manage Your Trades

Follow the FVGs as potential reversal zones in the direction of the trend, and manage your positions according to your personal strategy and the rules of the ICT Silver Bullet method.

Customizable Settings

The indicator includes several customization options to suit the trader's preferences:

EMA: Length, source (close, open, etc.), and timeframe.

Market Sessions: Ability to enable or disable each session, with color and line width settings.

Liquidity Signals: Customization of colors for the "OK" and "STOP" labels.

FVG: Option to display FVGs or not, with customizable colors for bullish and bearish FVGs, and the number of bars for FVG extension.

-------------------------------------------------------------------------------------------------------------

Cet indicateur est conçu pour les traders souhaitant analyser les niveaux de liquidité, les zones d’opportunité, et la tendance de fond à travers différentes sessions de trading. Inspiré de la méthodologie ICT, cet outil combine l'analyse des moyennes mobiles exponentielles (EMA), la gestion des sessions de marché, et la détection des Fair Value Gaps (FVG), afin de fournir une approche structurée et disciplinée pour trader efficacement.

MERCURY by DrAbhiramSivprasad"MERCURY by DrAbhiramSivprasad"

Developed from over 10 years of personal trading experience, the Mercury Indicator is a strategic tool designed to enhance accuracy in trading decisions. Think of it as a guiding light—a supportive tool that helps traders refine and build more robust strategies by integrating multiple powerful elements into a single indicator. I’ll be sharing some examples to illustrate how I use this indicator in my own trading journey, highlighting its potential to improve strategy accuracy.

Reason behind the combination of emas , cpr and vwap is it provides very good support and resistance in my trading carrier so now i brought them together in one plate

How It Works:

Mercury combines three essential elements—EMA, VWAP, and CPR—each of which plays a vital role in detecting support and resistance:

Exponential Moving Averages (EMAs): Known for their strength in providing dynamic support and resistance levels, EMAs help in identifying trends and shifts in momentum. This indicator includes a dashboard with up to nine customizable EMAs, showing whether each is acting as support or resistance based on real-time price movement.

Volume Weighted Average Price (VWAP): VWAP also provides valuable support and resistance, often regarded as a fair price level by institutional traders. Paired with EMAs, it forms a dual-layered support/resistance system, adding an additional level of confirmation.

Central Pivot Range (CPR): By combining CPR with EMAs and VWAP, Mercury highlights “traffic blocks” in your target journey. This means it identifies zones where price is likely to stall or reverse, providing additional guidance for navigating entries and exits.

Why This Combination Matters:

Using these three tools together gives you a more complete view of the market. VWAP and EMAs offer dynamic trend direction and support/resistance, while CPR pinpoints critical price zones. This combination helps you find high-probability trades, adding clarity to complex market situations and enabling stronger confirmation on trend or reversal decisions.

How to Use:

Trend Confirmation: Check if all EMAs are aligned (green for uptrend, red for downtrend), which is visible in the EMA dashboard. An alignment across VWAP, CPR, and EMAs signifies high confidence in trend direction.

Breakouts & Breakdowns: Mercury has an alert system to signal when a price breakout or breakdown occurs across VWAP, EMA1, and EMA2. This can help in spotting strong directional moves.

Example Application: In my trading, I use Mercury to identify support/resistance zones, confirming trends with EMA/VWAP alignment and using CPR as a checkpoint. I find this especially useful for day trading and swing setups.

Recommended Timeframes:

Day Trading: 5 to 15-minute charts for swift, actionable insights.

Swing Trading: 1-hour or 4-hour charts for broader trend analysis.

Note:

The Mercury Indicator should be used as a supportive tool rather than a standalone strategy, guiding you toward informed decisions in line with your trading style and goals.

EXAMPLE OF TRADE

you can see the cart of XAUUSD on 11th nov 2024

1.SHORT POSITION - TIME FRAME 15 MIN

So here for a short position you need to wait for a breakdown candle which will print in orange post the candle you need to check ema dashboard is completly red that indicates no traffic blocks in your journey to destiny target from ema's and you can take the target from nearest cpr support line

TAKEN IN XAUUSD you can see in chart of XAUUSD on 7th nov

2.LONG POSITION - TIME FRAME 15 MIN -

So here for long position you need to wait for a breakout candle from indicator thats here is blue and check all ema boxes are green and candle body should close above all the 3 lines here it is the both ema 1 and 2 and the vwap line then you can take and entry and your target will be the nearest resistance from the daily cpr

3. STOP LOSS CRITERIA

After the entry any candle close below any of the last line from entry for example we have 3 lines vwap and ema 1 and 2 lines and u have made an entry and the last line before the entry is vwap then if any candle closes below vwap can be considered as stoploss like wise in any lines

The MERCURY indicator is a comprehensive trading tool designed to enhance traders' ability to identify trends, breakouts, and reversals effectively. Created by Dr. Abhiram Sivprasad, this indicator integrates several technical elements, including Central Pivot Range (CPR), EMA crossovers, VWAP levels, and a table-based EMA dashboard, to offer a holistic trading view.

Core Components and Functionality:

Central Pivot Range (CPR):

The CPR in MERCURY provides a central pivot level along with Below Central (BC) and Top Central (TC) pivots. These levels act as potential support and resistance, useful for identifying reversal points and zones where price may consolidate.

Exponential Moving Averages (EMAs):

MERCURY includes up to nine EMAs, with a customizable EMA crossover alert system. This feature enables traders to see shifts in trend direction, especially when shorter EMAs cross longer ones.

VWAP (Volume-Weighted Average Price):

VWAP is incorporated as a dynamic support/resistance level and, combined with EMA crossovers, helps refine entry and exit points for higher probability trades.

Breakout and Breakdown Alerts:

MERCURY monitors conditions for upside and downside breakouts. For an upside breakout, all EMAs turn green and a candle closes above VWAP, EMA1, and EMA2. Similarly, all EMAs turning red, combined with a close below VWAP and EMA1/EMA2, signals a downside breakdown. Continuous alerts are available until the trend shifts.

Real-Time EMA Dashboard:

A table displays each EMA’s relative position (Above or Below), helping traders quickly gauge trend direction. Colors in the table adjust to long/short conditions based on EMA alignment.

Usage Recommendations:

Trend Confirmation:

Use the CPR, EMA alignments, and VWAP to confirm uptrends and downtrends. The table highlights trends, making it easy to spot long or short setups at a glance.

Breakout and Breakdown Alerts:

The alert system is customizable for continuous notifications on critical price levels. When all EMAs align in one direction (green for long, red for short) and the close is above or below VWAP and key EMAs, the indicator confirms a breakout/breakdown.

Adaptable for Different Styles:

Day Trading: Traders can set shorter EMAs for quick insights.

Swing Trading: Longer EMAs combined with CPR offer insights into sustained trends.

Recommended Settings:

Timeframes: MERCURY is suitable for timeframes as low as 5 minutes for intraday traders, up to daily charts for trend analysis.

Symbols: Works across forex, stocks, and crypto. Adjust EMA lengths for asset volatility.

Example Strategy:

Long Entry: When the price crosses above CPR and closes above both EMA1 and EMA2.

Short Entry: When the price falls below CPR with a close below both EMA1 and EMA2.

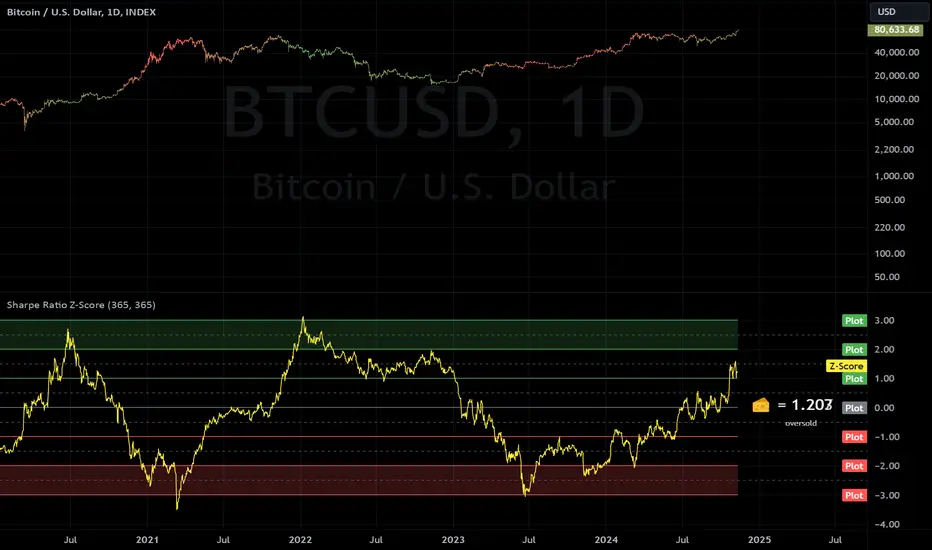

Sharpe Ratio Z-ScoreThis indicator calculates the Sharpe Ratio and its Z-Score , which are used to evaluate the risk-adjusted return of an asset over a given period. The Sharpe Ratio is computed using the average return and the standard deviation of returns, while the Z-Score standardizes this ratio to assess how far the current Sharpe Ratio deviates from its historical average.

The Sharpe Ratio is a measure of how much return an investment has generated relative to the risk it has taken. In the context of this script, the risk-free rate is assumed to be 0, but in real applications, it would typically be the return on a safe investment, like a Treasury bond. A higher Sharpe Ratio indicates that the investment's returns are higher compared to its risk, making it a more favorable investment. Conversely, a lower Sharpe Ratio suggests that the investment may not be worth the risk.

Calculation:

Daily Returns Calculation: The script calculates the daily return of the asset. This measures the percentage change in the asset’s closing price from one period to the next.

Sharpe Ratio Calculation: The Sharpe Ratio is calculated by taking the average daily return and dividing it by the standard deviation of the returns, then multiplying by the square root of the period length.

Usage:

Traders and Investors can use the Sharpe Ratio to evaluate how well the asset is compensating for risk. A high Sharpe Ratio indicates a high return per unit of risk, whereas a low or negative Sharpe Ratio suggests poor risk-adjusted returns. In overbought times, an asset would have high/positive returns per unit of risk. In oversold times, an asset would have low/negative returns per unit of risk.

The Z-Score provides a way to compare the current Sharpe Ratio to its historical distribution, offering a more standardized view of how extreme or typical the current ratio is.

Positive Z-score: Indicates that the asset's return is significantly lower than its risk, suggesting potential oversold conditions.

Negative Z-score: Indicates that the asset's return is significantly higher than its risk, suggesting potential overbought conditions.

Red Zone (-3 to -2): Strong overbought conditions.

Green Zone (2 to 3): Strong oversold conditions.

Sharpe Ratio Limitations:

While the Sharpe Ratio is widely used to evaluate risk-adjusted returns, it has its limitations.

Fat Tails: It assumes that returns are normally distributed and does not account for extreme events or "fat tails" in the return distribution. This can be problematic for assets like cryptocurrencies, which may experience large, sudden price swings that skew the return distribution.

Single Risk Factor: The Sharpe Ratio only considers standard deviation (total volatility) as a measure of risk, ignoring other types of risks like skewness or kurtosis, which may also impact an asset’s performance.

Time Frame Sensitivity: The accuracy of the Sharpe Ratio and its Z-Score is heavily influenced by the time frame chosen for the calculation. A longer period may smooth out short-term fluctuations, while a shorter period might be more sensitive to recent volatility.

Overbought and Oversold Zones: The script marks overbought and oversold conditions based on the Z-Score, but this is not a guarantee of market reversal. It’s important to combine this tool with other technical indicators and fundamental analysis for a more comprehensive market evaluation.

Volatility: The Sharpe Ratio and Z-Score depend on the volatility (standard deviation) of the asset’s returns. For highly volatile assets, such as cryptocurrencies, the Sharpe Ratio may not fully capture the true risk or may be misleading if the volatility is transient.

Doesn't Account for Downside Risk: The Sharpe Ratio treats upside and downside volatility equally, which may not reflect how investors perceive risk. Some investors may be more concerned with downside risk, which the Sharpe Ratio does not distinguish from upside fluctuations.

Important Considerations:

The Sharpe Ratio should not be used in isolation. While it provides valuable insights into risk-adjusted returns, it is important to combine it with other performance and risk indicators to form a more comprehensive market evaluation. Relying solely on the Sharpe Ratio may lead to misleading conclusions, particularly in volatile or non-normally distributed markets.

When integrated into a broader investment strategy, the Sharpe Ratio can help traders and investors better assess the risk-return profile of an asset, identifying periods of potential overperformance or underperformance. However, it should be used alongside other tools to ensure more informed decision-making, especially in highly fluctuating markets.

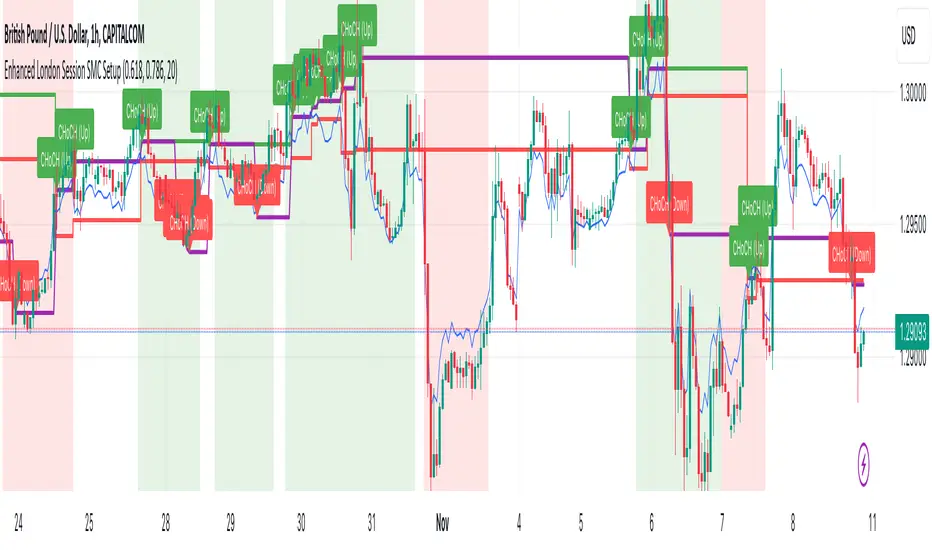

Enhanced London Session SMC SetupEnhanced London Session SMC Setup Indicator

This Pine Script-based indicator is designed for traders focusing on the London trading session, leveraging smart money concepts (SMC) to identify potential trading opportunities in the GBP/USD currency pair. The script uses multiple techniques such as Order Block Detection, Imbalance (Fair Value Gap) Analysis, Change of Character (CHoCH) detection, and Fibonacci retracement levels to aid in market structure analysis, providing a well-rounded approach to trade setups.

Features:

London Session Highlight:

The indicator visually marks the London trading session (from 08:00 AM to 04:00 PM UTC) on the chart using a blue background, signaling when the high-volume, high-impulse moves tend to occur, helping traders focus their analysis on this key session.

Order Block Detection:

Identifies significant impulse moves that may form order blocks (supply and demand zones). Order blocks are areas where institutions have executed large orders, often leading to price reversals or continuation. The indicator plots the high and low of these order blocks, providing key levels to monitor for potential entries.

Imbalance (Fair Value Gap) Detection:

Detects and highlights price imbalances or fair value gaps (FVG) where the market has moved too quickly, creating a gap in price action. These areas are often revisited by price, offering potential trade opportunities. The upper and lower bounds of the imbalance are visually marked for easy reference.

Change of Character (CHoCH) Detection:

This feature identifies potential trend reversals by detecting significant changes in market character. When the price action shifts from bullish to bearish or vice versa, a CHoCH signal is triggered, and the corresponding level is marked on the chart. This can help traders catch trend reversals at key levels.

Fibonacci Retracement Levels:

The script calculates and plots the key Fibonacci retracement levels (0.618 and 0.786 by default) based on the highest and lowest points over a user-defined swing lookback period. These levels are commonly used by traders to identify potential pullback zones where price may reverse or find support/resistance.

Directional Bias Based on Market Structure:

The indicator provides a market structure analysis by comparing the current highs and lows to the previous periods' highs and lows. This helps in identifying whether the market is in a bullish or bearish state, providing a clear directional bias for trade setups.

Alerts:

The indicator comes with built-in alert conditions to notify the trader when an order block, imbalance, CHoCH, or other significant price action event is detected, ensuring timely action can be taken.

Ideal Usage:

Timeframe: Suitable for intraday trading, particularly focusing on the London session (08:00 AM to 04:00 PM UTC).

Currency Pair: Specifically designed for GBP/USD but can be adapted to other pairs with similar market behavior.

Trading Strategy: Best used in conjunction with a price action strategy, focusing on the key levels identified (order blocks, FVG, CHoCH) and using Fibonacci retracement levels for precision entries.

Target Audience: Ideal for traders who follow smart money concepts (SMC) and are looking for a structured approach to identify high-probability setups during the London session.

Original Keltner with Support And ResistanceThis indicator is based on the original Keltner Channels using typical price and calculating the 10 period average of high - low

Typical price = (high + low + close)/3

In this case, I've taken Typical price as (open + high + low + close)/4 on the advice of John Bollinger from his book Bollinger on Bollinger Bands.

Buy Line = 10 Period Typical Price Average + 10 Period Average of (High - Low)

Sell Line = 10 Period Typical Price Average - 10 Period Average of (High - Low)

This is the basis for the indicator. I've added the highest of the Buy Line and lowest of the Sell Line for the same period which acts as Support and Resistance.

If price is trending below the Lowest of Sell Line, take only sell trades and the Lowest Line acts as resistance.

If price is trending above the Highest of Buy Line, take only buy trades and the Highest Line acts as support.

Target Trend [BigBeluga]The Target Trend indicator is a trend-following tool designed to assist traders in capturing directional moves while managing entry, stop loss, and profit targets visually on the chart. Using adaptive SMA bands as the core trend detection method, this indicator dynamically identifies shifts in trend direction and provides structured exit points through customizable target levels.

SP500:

🔵 IDEA

The Target Trend indicator’s concept is to simplify trade management by providing automated visual cues for entries, stops, and targets directly on the chart. When a trend change is detected, the indicator prints an up or down triangle to signal entry direction, plots three customizable target levels for potential exits, and calculates a stop-loss level below or above the entry point. The indicator continuously adapts as price moves, making it easier for traders to follow and manage trades in real time.

When price crosses a target level, the label changes to a check mark, confirming that the target has been achieved. Similarly, if the stop-loss level is hit, the label changes to an "X," and the line becomes dashed, indicating that the stop loss has been activated. This feature provides traders with a clear visual trail of whether their targets or stop loss have been hit, allowing for easier trade tracking and exit strategy management.

🔵 KEY FEATURES & USAGE

SMA Bands for Trend Detection: The indicator uses adaptive SMA bands to identify the trend direction. When price crosses above or below these bands, a new trend is detected, triggering entry signals. The entry point is marked on the chart with a triangle symbol, which updates with each new trend change.

Automated Targets and Stop Loss Management: Upon a new trend signal, the indicator automatically plots three price targets and a stop loss level. These levels provide traders with structured exit points for potential gains and a clear risk limit. The stop loss is placed below or above the entry point, depending on the trend direction, to manage downside risk effectively.

Visual Target and Stop Loss Validation: As price hits each target, the label beside the level updates to a check mark, indicating that the target has been reached. Similarly, if the stop loss is activated, the stop loss label changes to an "X," and the line becomes dashed. This feature visually confirms whether targets or stop losses are hit, simplifying trade management.

The indicator also marks the entry price at each trend change with a label on the chart, allowing traders to quickly see their initial entry point relative to current price and target levels.

🔵 CUSTOMIZATION

Trend Length: Set the lookback period for the trend-detection SMA bands to adjust the sensitivity to trend changes.

Targets Setting: Customize the number and spacing of the targets to fit your trading style and market conditions.

Visual Styles: Adjust the appearance of labels, lines, and symbols on the chart for a clearer view and personalized layout.

🔵 CONCLUSION

The Target Trend indicator offers a streamlined approach to trend trading by integrating entry, target, and stop loss management into a single visual tool. With automatic tracking of target levels and stop loss hits, it helps traders stay focused on the current trend while keeping track of risk and reward with minimal effort.

Range Detect SystemTechnical analysis indicator designed to identify potential significant price ranges and the distribution of volume within those ranges. The system helps traders calculate POC and show volume history. Also detecting breakouts or potential reversals. System identifies ranges with a high probability of price consolidation and helps screen out extreme price moves or ranges that do not meet certain volatility thresholds.

⭕️ Key Features

Range Detection — identifies price ranges where consolidation is occurring.

Volume Profile Calculation — indicator calculates the Point of Control (POC) based on volume distribution within the identified range, enhancing the analysis of market structure.

Volume History — shows where the largest volume was traded from the center of the range. If the volume is greater in the upper part of the range, the color will be green. If the volume is greater in the lower part, the color will be red.

Range Filtering — Includes multi-level filtering options to avoid ranges that are too volatile or outside normal ranges.

Visual Customization — Shows graphical indicators for potential bullish or bearish crossovers at the upper and lower range boundaries. Users can choose the style and color of the lines, making it easier to visualize ranges and important levels on the chart.

Alerts — system will notify you when a range has been created and also when the price leaves the range.

⭕️ How it works

Extremes (Pivot Points) are taken as a basis, after confirming the relevance of the extremes we take the upper and lower extremes and form a range. We check if it does not violate a number of rules and filters, perform volume calculations, and only then is the range displayed.

Pivot points is a built-in feature that shows an extremum if it has not been updated N bars to the left and N bars to the right. Therefore, there is a delay depending on the bars specified to check, which allows for a more accurate range. This approach allows not to make unnecessary recalculations, which completely eliminates the possibility of redrawing or range changes.

⭕️ Settings

Left Bars and Right Bars — Allows you to define the point that is the highest among the specified number of bars to the left and right of this point.

Range Logic — Select from which point to draw the range. Maximums only, Minimums only or both.

Use Wick — Option to consider the wick of the candles when identifying Range.

Breakout Confirmation — The number of bars required to confirm a breakout, after which the range will close.

Minimum Range Length — Sets the minimum number of candles needed for a range to be considered valid.

Row Size — Number of levels to calculate POC. *Larger values increase the script load.

% Range Filter — Dont Show Range is than more N% of Average Range.

Multi Filter — Allows use of Bollinger Bands, ATR, SMA, or Highest-Lowest range channels for filtering ranges based on volatility.

Range Hit — Shows graphical labels when price hits the upper or lower boundaries of the range, signaling potential reversal or breakout points.

Range Start — Show points where Range was created.

STANDARD DEVIATION INDICATOR BY WISE TRADERWISE TRADER STANDARD DEVIATION SETUP: The Ultimate Volatility and Trend Analysis Tool

Unlock the power of STANDARD DEVIATIONS like never before with the this indicator, a versatile and comprehensive tool designed for traders who seek deeper insights into market volatility, trend strength, and price action. This advanced indicator simultaneously plots three sets of customizable Deviations, each with unique settings for moving average types, standard deviations, and periods. Whether you’re a swing trader, day trader, or long-term investor, the STANDARD DEVIATION indicator provides a dynamic way to spot potential reversals, breakouts, and trend-following opportunities.

Key Features:

STANDARD DEVIATIONS Configuration : Monitor three different Bollinger Bands at the same time, allowing for multi-timeframe analysis within a single chart.

Customizable Moving Average Types: Choose from SMA, EMA, SMMA (RMA), WMA, and VWMA to calculate the basis of each band according to your preferred method.

Dynamic Standard Deviations: Set different standard deviation multipliers for each band to fine-tune sensitivity for various market conditions.

Visual Clarity: Color-coded bands with adjustable thicknesses provide a clear view of upper and lower boundaries, along with fill backgrounds to highlight price ranges effectively.

Enhanced Trend Detection: Identify potential trend continuation, consolidation, or reversal zones based on the position and interaction of price with the three bands.

Offset Adjustment: Shift the bands forward or backward to analyze future or past price movements more effectively.

Why Use Triple STANDARD DEVIATIONS ?

STANDARD DEVIATIONS are a popular choice among traders for measuring volatility and anticipating potential price movements. This indicator takes STANDARD DEVIATIONS to the next level by allowing you to customize and analyze three distinct bands simultaneously, providing an unparalleled view of market dynamics. Use it to:

Spot Volatility Expansion and Contraction: Track periods of high and low volatility as prices move toward or away from the bands.

Identify Overbought or Oversold Conditions: Monitor when prices reach extreme levels compared to historical volatility to gauge potential reversal points.

Validate Breakouts: Confirm the strength of a breakout when prices move beyond the outer bands.

Optimize Risk Management: Enhance your strategy's risk-reward ratio by dynamically adjusting stop-loss and take-profit levels based on band positions.

Ideal For:

Forex, Stocks, Cryptocurrencies, and Commodities Traders looking to enhance their technical analysis.

Scalpers and Day Traders who need rapid insights into market conditions.

Swing Traders and Long-Term Investors seeking to confirm entry and exit points.

Trend Followers and Mean Reversion Traders interested in combining both strategies for maximum profitability.

Harness the full potential of STANDARD DEVIATIONS with this multi-dimensional approach. The "STANDARD DEVIATIONS " indicator by WISE TRADER will become an essential part of your trading arsenal, helping you make more informed decisions, reduce risks, and seize profitable opportunities.

Who is WISE TRADER ?

Wise Trader is a highly skilled trader who launched his channel in 2020 during the COVID-19 pandemic, quickly building a loyal following. With thousands of paid subscribed members and over 70,000 YouTube subscribers, Wise Trader has become a trusted authority in the trading world. He is known for his ability to navigate significant events, such as the Indian elections and stock market crashes, providing his audience with valuable insights into market movements and volatility. With a deep understanding of macroeconomics and its correlation to global stock markets, Wise Trader shares informed strategies that help traders make better decisions. His content covers technical analysis, trading setups, economic indicators, and market trends, offering a comprehensive approach to understanding financial markets. The channel serves as a go-to resource for traders who want to enhance their skills and stay informed about key market developments.

Liquidity VisualizerThe "Liquidity Visualizer" indicator is designed to help traders visualize potential areas of liquidity on a price chart. In trading, liquidity often accumulates around key levels where market participants have placed their stop orders or pending orders. These levels are commonly found at significant highs and lows, where traders tend to set their stop-losses or take-profit orders. The indicator aims to highlight these areas by drawing unbroken lines that extend indefinitely until breached by the price action.

Specifically, this indicator identifies and marks pivot highs and pivot lows, which are price levels where a trend changes direction. When a pivot high or pivot low is formed, it is represented on the chart with a horizontal line that continues to extend until the price touches or surpasses that level. The line remains in place as long as the level remains unbroken, which means there is potential liquidity still resting at that level.

The concept behind this indicator is that liquidity is likely to be resting at unbroken pivot points. These levels are areas where stop-loss orders or pending buy/sell orders may have accumulated, making them attractive zones for large market participants, such as institutions, to target. By visualizing these unbroken levels, traders can gain insight into where liquidity might be concentrated and where potential price reversals or significant movements could occur as liquidity is taken out.

The indicator helps traders make more informed decisions by showing them key price levels that may attract significant market activity. For instance, if a trader sees multiple unbroken pivot high lines above the current price, they might infer that there is a cluster of liquidity in that area, which could lead to a price spike as those levels are breached. Similarly, unbroken pivot lows may indicate areas where downside liquidity is concentrated.

In summary, this indicator acts as a "liquidity visualizer," providing traders with a clear, visual representation of potential liquidity resting at significant pivot points. This information can be valuable for understanding where price might be drawn to, and where large movements might occur as liquidity is targeted and removed by market participants.

Larry Williams Valuation Index [tradeviZion]Larry Williams Valuation Index

Welcome to the Larry Williams Valuation Index by tradeviZion! This script is an interpretation of Larry Williams' famous WillVal (Valuation) Index, originally developed in 1990 to help traders determine whether a market or asset is overvalued or undervalued. We've extended it to support multiple securities and offer alerts for different valuation levels, helping you make more informed trading decisions.

What is the Valuation Index?

The Valuation Index measures how a security's current price compares to its historical price action. It helps identify whether the security is overvalued (priced too high), undervalued (priced too low), or in a normal range.

This version supports multiple securities and uses valuation parameters to help you assess the relative valuation of three securities simultaneously. It can help you determine the best times to enter (buy) or exit (sell) the market.

Key Features

Multi-Security Analysis: Analyze up to three securities simultaneously to get a broader view of market conditions.

Valuation Levels: Automatically calculate overvaluation and undervaluation levels or set manual levels for consistent analysis.

Custom Alerts: Create custom alerts when securities move between overvalued, undervalued, or normal ranges.

Customizable Table Display: Display a table with valuation values and their status on the chart.

Getting Started

Step 1: Adding the Script to Your Chart

First, add the Larry Williams Valuation Index script to your chart on TradingView. The script is designed to work with any timeframe, but for best results, use weekly or daily timeframes for a longer-term perspective.

Step 2: Configuring Securities

The script allows you to analyze up to three different securities :

Security 1 (Default: DXY)

Security 2 (Default: GC1!)

Security 3 (Default: ZB1!)

You can enable or disable each security individually.

Custom Timeframe Option: You have the option to select a custom timeframe for analysis. This allows you to see whether the security is overvalued or undervalued in lower or higher timeframes. Note that this feature is experimental and has not been extensively tested. Larry Williams originally used the weekly timeframe to determine if a stock was overvalued or undervalued. By default, the indicator compares the current price with the security based on the selected timeframe, except if you choose to use a custom timeframe.

Pro Tip : New users can start with the default securities to understand the concept before using other assets.

Step 3: Valuation Index Settings

Short EMA Length : This is the short-term average used for calculations. A lower value makes it more responsive to recent price changes.

Long EMA Length : This is the long-term average, used to smooth the valuation over time.

Valuation Length (Default: 156) : Represents approximately three years of daily bars (as recommended by Larry Williams).

How is the Valuation Index Calculated?

The valuation calculation is done using a method called WVI (WillVal Index), which compares the current price of a security to the price of another correlated security. Here’s a step-by-step explanation:

1. Data Collection: The script takes the closing price of the security you are analyzing and the closing price of the correlated security.

2. Ratio Calculation : The ratio of the two prices is calculated:

Price Ratio = (Price of your security) / (Price of correlated security) * 100.

This ratio helps determine how expensive or cheap your security is compared to the correlated one.

3. Exponential Moving Averages (EMAs) : The price ratio is used to calculate short-term and long-term EMAs (Exponential Moving Averages). EMAs are used to create smooth lines that represent the average price of a security over a specific period of time, with more weight given to recent data. By calculating both short-term and long-term EMAs, we can identify the trend direction and how the security is performing compared to its historical averages.

4. Valuation Index Calculation:

The Valuation Index is calculated as the difference between the short-term EMA and the long-term EMA. This difference helps to determine if the security is currently overvalued or undervalued:

A positive value indicates that the price is above its longer-term trend, suggesting potential overvaluation.

A negative value indicates that the price is below its longer-term trend, suggesting potential undervaluation.

5. Normalization:

To make the valuation easier to interpret, the calculated valuation index is then normalized using the highest and lowest values over the selected valuation length (e.g., 156 bars).

This normalization process converts the index into a percentage between 0 and 100, where higher values indicate overvaluation and lower values indicate undervaluation.

Step 4: Understanding Valuation Levels

The valuation levels indicate whether a security is currently undervalued, overvalued, or in a normal range.

Manual Levels : You can manually set the overvaluation and undervaluation thresholds (default is 85 for overvalued and 15 for undervalued).

Auto Levels : The script can automatically calculate these levels based on recent price action, allowing you to adapt to changing market conditions.

Auto Levels Calculation Explained:

The Auto Levels are calculated by taking the average of the valuation indices for all three securities (e.g., index1, index2, and index3).

The script then looks at the highest and lowest values of this average over a selected number of recent bars (e.g., 50 bars).

The overvaluation level is determined by taking the highest value and multiplying it by a multiplier (e.g., 5). Similarly, the undervaluation level is calculated using the lowest value and the multiplier.

These dynamic levels adjust according to recent price action, providing an adaptive approach to identifying overvalued and undervalued conditions.

Step 5: How to Use the Script to Make Trading Decisions

For new users, here's a step-by-step trading strategy you can use with the Valuation Index:

1. Identify Undervalued Opportunities

When two or more securities are in the undervalued range (below 15 for manual or below automatically calculated undervalue levels), wait for at least two of these securities to turn from undervalued to normal .

This transition indicates a potential buy opportunity .

2. Buying Signal

When at least two securities transition from undervalued to normal, you can consider buying the asset.

This indicates that the market may be recovering from undervalued conditions and could be moving into a growth phase.

3. Selling Signal

Exit when the price high closes below the EMA 21 (21-day exponential moving average).

Alternatively, if the valuation index reaches overvalued levels (above 85 manually or auto-calculated), wait for it to drop back to normal . This can be another point to exit the trade .

You can also use any other sell condition based on your r isk management strategy .

Alerts for Valuation Levels

The script includes alerts to notify you of changing market conditions:

To activate these alerts, follow these steps, referring to the provided screenshot with detailed steps:

1. Enable Alerts : Click on the settings gear icon on the script title in your chart. In the settings menu, scroll to the section labeled Alerts Settings .

Enable Alerts by checking the Enable Alerts box.

Set the Required Securities for Alert (default is 2 securities).

Choose the Alert Frequency : Selecting Once Per Bar Close will trigger alerts only at the close of each bar, ensuring you receive confirmed signals rather than potentially noisy intermediate signals.

2. Select Alert Type : Choose the type of alert you want to activate, such as Alert on Overvalued, Alert on Undervalued, Alert on Over to Normal , or Alert on Under to Normal .

3. Save Settings : Click OK to save your alert settings.

4. Add Alert on Indicator : Click the "..." (More button) next to the indicator name on the chart and select " Add alert on tradeviZion - WillVal ".

5. Create Alert : In the Create Alert window:

Set Condition to tradeviZion - WillVal .

Ensure Any alert() function call is selected.

Set the Alert Name and select your Expiration preferences.

6. Set Notification Preferences : Go to the Notifications tab and select how you want to receive notifications, such as via app notification, toast notification, email , or sound alert . Adjust these preferences to best suit your needs.

7. Click Create : Finally, click Create to activate the alert.

These alerts will help you stay informed about key market conditions and take action accordingly, ensuring you do not miss critical trading opportunities.

Understanding the Table Display

The script includes an interactive table on the chart to show the valuation status of each security:

Security : The name of the security being analyzed.

Value : The current valuation index value.

Status : Indicates whether the security is overvalued, undervalued , or in a normal range.

Color: Displays a color code for easy identification of status:

Red for overvalued.

Green for undervalued.

Other colors represent normal valuation levels.

Empowering Messages : Motivational messages are displayed to encourage disciplined trading. These messages will change periodically, helping keep a positive trading mindset.

Acknowledgment

This tool builds upon the foundational work of Larry Williams, who developed the WillVal (Valuation) Index concept. It also incorporates enhancements to extend multi-security analysis, valuation normalization, and advanced alerting features, providing a more versatile and powerful indicator. The Larry Williams Valuation Index [ tradeviZion ] helps traders make informed decisions by assessing overvalued and undervalued conditions for multiple securities simultaneously.

Note : Always practice proper risk management and thoroughly test the indicator to ensure it aligns with your trading strategy. Past performance is not indicative of future results.

Trade smarter with TradeVizion—unlock your trading potential today!

(Early Test) Weekly Seasonality with Dynamic Kelly Criterion# Enhancing Trading Strategies with the Weekly Seasonality Dynamic Kelly Criterion Indicator

Amidst this pursuit to chase price, a common pitfall emerges: an overemphasis on price movements without adequate attention to risk management, probabilistic analysis, and strategic position sizing. To address these challenges, I developed the **Weekly Seasonality with Dynamic Kelly Criterion Indicator**. It is designed to refocus traders on essential aspects of trading, such as risk management and probabilistic returns, thereby catering to both short-term swing traders and long-term investors aiming for tax-efficient positions.

## The Motivation Behind the Indicator

### Overemphasis on Price: A Common Trading Pitfall

Many traders concentrate heavily on price charts and technical indicators, often neglecting the underlying principles of risk management and probabilistic analysis. This overemphasis on price can lead to:

- **Overtrading:** Making frequent trades based solely on price movements without considering the associated risks.

- **Poor Risk Management:** Failing to set appropriate stop-loss levels or position sizes, increasing the potential for significant losses.

- **Emotional Trading:** Letting emotions drive trading decisions rather than objective analysis, which can result in impulsive and irrational trades.

### The Need for Balanced Focus

To achieve sustained trading success, it is crucial to balance price analysis with robust risk management and probabilistic strategies. Key areas of focus include:

1. **Risk Management:** Implementing strategies to protect capital, such as setting stop-loss orders and determining appropriate position sizes based on risk tolerance.

2. **Probabilistic Analysis:** Assessing the likelihood of various market outcomes to make informed trading decisions.

3. **Swing Trading Percent Returns:** Capitalizing on short- to medium-term price movements by buying assets below their average return and selling them above.

## Introducing the Weekly Seasonality with Dynamic Kelly Criterion Indicator

The **Weekly Seasonality with Dynamic Kelly Criterion Indicator** is designed to integrate these essential elements into a comprehensive tool that aids traders in making informed, risk-aware decisions. Below, we explore the key components and functionalities of this indicator.

### Key Components of the Indicator

1. **Average Return (%)**

- **Definition:** The mean percentage return for each week across multiple years.

- **Purpose:** Serves as a benchmark to identify weeks with above or below-average performance, guiding buy and sell decisions.

2. **Positive Percentage (%)**

- **Definition:** The proportion of weeks that yielded positive returns.

- **Purpose:** Indicates the consistency of positive returns, helping traders gauge the reliability of certain weeks for trading.

3. **Volatility (%)**

- **Definition:** The standard deviation of weekly returns.

- **Purpose:** Measures the variability of returns, providing insights into the risk associated with trading during specific weeks.

4. **Kelly Ratio**

- **Definition:** A mathematical formula used to determine the optimal size of a series of bets to maximize the logarithmic growth of capital.

- **Purpose:** Balances potential returns against risks, guiding traders on the appropriate position size to take.

5. **Adjusted Kelly Fraction**

- **Definition:** The Kelly Ratio adjusted based on user-defined risk tolerance and external factors like Federal Reserve (Fed) stance.

- **Purpose:** Personalizes the Kelly Criterion to align with individual risk preferences and market conditions, enhancing risk management.

6. **Position Size ($)**

- **Definition:** The calculated amount to invest based on the Adjusted Kelly Fraction.

- **Purpose:** Ensures that position sizes are aligned with risk management strategies, preventing overexposure to any single trade.

7. **Max Drawdown (%)**

- **Definition:** The maximum observed loss from a peak to a trough of a portfolio, before a new peak is attained.

- **Purpose:** Assesses the worst-case scenario for losses, crucial for understanding potential capital erosion.

### Functionality and Benefits

- **Weekly Data Aggregation:** Aggregates weekly returns across multiple years to provide a robust statistical foundation for decision-making.

- **Quarterly Filtering:** Allows users to filter weeks based on quarters, enabling seasonality analysis and tailored strategies aligned with specific timeframes.

- **Dynamic Risk Adjustment:** Incorporates the Dynamic Kelly Criterion to adjust position sizes in real-time based on changing risk profiles and market conditions.

- **User-Friendly Visualization:** Presents all essential metrics in an organized Summary Table, facilitating quick and informed decision-making.

## The Origin of the Kelly Criterion and Addressing Its Limitations

### Understanding the Kelly Criterion

The Kelly Criterion, developed by John L. Kelly Jr. in 1956, is a formula used to determine the optimal size of a series of bets to maximize the long-term growth of capital. The formula considers both the probability of winning and the payout ratio, balancing potential returns against the risk of loss.

**Kelly Formula:**

\

Where:

- \( b \) = the net odds received on the wager ("b to 1")

- \( p \) = probability of winning

- \( q \) = probability of losing ( \( q = 1 - p \) )

### The Risk of Ruin

While the Kelly Criterion is effective in optimizing growth, it carries inherent risks:

- **Overbetting:** If the input probabilities or payout ratios are misestimated, the Kelly Criterion can suggest overly aggressive position sizes, leading to significant losses.

- **Assumption of Constant Probabilities:** The criterion assumes that probabilities remain constant, which is rarely the case in dynamic markets.

- **Ignoring External Factors:** Traditional Kelly implementations do not account for external factors such as Federal Reserve rates, margin requirements, or market volatility, which can impact risk and returns.

### Addressing Traditional Limitations

Recognizing these limitations, the **Weekly Seasonality with Dynamic Kelly Criterion Indicator** introduces enhancements to the traditional Kelly approach:

- **Incorporation of Fed Stance:** Adjusts the Kelly Fraction based on the current stance of the Federal Reserve (neutral, dovish, or hawkish), reflecting broader economic conditions that influence market behavior.

- **Margin and Leverage Considerations:** Accounts for margin rates and leverage, ensuring that position sizes remain within manageable risk parameters.

- **Dynamic Adjustments:** Continuously updates position sizes based on real-time risk assessments and probabilistic analyses, mitigating the risk of ruin associated with static Kelly implementations.

## How the Indicator Aids Traders

### For Short-Term Swing Traders

Short-term swing traders thrive on capitalizing over weekly price movements. The indicator aids them by:

- **Identifying Favorable Weeks:** Highlights weeks with above-average returns and favorable volatility, guiding entry and exit points.

- **Optimal Position Sizing:** Utilizes the Adjusted Kelly Fraction to determine the optimal amount to invest, balancing potential returns with risk exposure.

- **Probabilistic Insights:** Provides metrics like Positive Percentage (%) and Kelly Ratio to assess the likelihood of favorable outcomes, enhancing decision-making.

### For Long-Term Tax-Free Investors

This is effectively a drop-in replacement for DCA which uses fixed position size that doesn't change based on market conditions, as a result, it's like catching multiple falling knifes by the blade and smiling with blood on your hand... I don't know about you, but I'd rather juggle by the hilt and look like an actual professional...

Long-term investors, especially those seeking tax-free positions (e.g., through retirement accounts), benefit from:

- **Consistent Risk Management:** Ensures that position sizes are aligned with long-term capital preservation strategies.

- **Seasonality Analysis:** Allows for strategic positioning based on historical performance trends across different weeks and quarters.

- **Dynamic Adjustments:** Adapts to changing market conditions, maintaining optimal risk profiles over extended investment horizons.

### Developers

Please double check the logic and functionality because I think there are a few issue and I need to crowd source solutions and be responsible about the code I publish. If you have corrections, please DM me or leave a respectful comment.

I want to publish this by the end of the year and include other things like highlighting triple witching weeks, adding columns for volume % stats, VaR and CVaR, alpha, beta (to see the seasonal alpha and beta based off a benchmark ticker and risk free rate ticker and other little goodies.

$TUBR: Stop Loss IndicatorATR-Based Stop Loss Indicator for TradingView by The Ultimate Bull Run Community: TUBR

**Overview**

The ATR-Based Stop Loss Indicator is a custom tool designed for traders using TradingView. It helps you determine optimal stop loss levels by leveraging the Average True Range (ATR), a popular measure of market volatility. By adapting to current market conditions, this indicator aims to minimize premature stop-outs and enhance your risk management strategy.

---

**Key Features**

- **Dynamic Stop Loss Levels**: Calculates stop loss prices based on the ATR, providing both long and short stop loss suggestions.

- **Customizable Parameters**: Adjust the ATR period, multiplier, and smoothing method to suit your trading style and the specific instrument you're trading.

- **Visual Aids**: Plots stop loss lines directly on your chart for easy visualization.

- **Alerts and Notifications** (Optional): Set up alerts to notify you when the price approaches or hits your stop loss levels.

---

**Understanding the Indicator**

1. **Average True Range (ATR)**:

- **What It Is**: ATR measures market volatility by calculating the average range between high and low prices over a specified period.

- **Why It's Useful**: A higher ATR indicates higher volatility, which can help you set stop losses that accommodate market fluctuations.

2. **ATR Multiplier**:

- **Purpose**: Determines how far your stop loss is placed from the current price based on the ATR.

- **Example**: An ATR multiplier of 1.5 means the stop loss is set at 1.5 times the ATR away from the current price.

3. **Smoothing Methods**:

- **Options**: Choose from RMA (default), SMA, EMA, WMA, or Hull MA.

- **Effect**: Different smoothing methods can make the ATR more responsive or smoother, affecting where the stop loss is placed.

---

**How the Indicator Works**

- **Long Stop Loss Calculation**:

- **Formula**: `Long Stop Loss = Close Price - (ATR * ATR Multiplier)`

- **Purpose**: For long positions, the stop loss is set below the current price to protect against downside risk.

- **Short Stop Loss Calculation**:

- **Formula**: `Short Stop Loss = Close Price + (ATR * ATR Multiplier)`

- **Purpose**: For short positions, the stop loss is set above the current price to protect against upside risk.

- **Plotting on the Chart**:

- **Green Line**: Represents the suggested stop loss level for long positions.

- **Red Line**: Represents the suggested stop loss level for short positions.

---

**How to Use the Indicator**

1. **Adding the Indicator to Your Chart**:

- **Step 1**: Copy the PineScript code of the indicator.

- **Step 2**: In TradingView, click on **Pine Editor** at the bottom of the platform.

- **Step 3**: Paste the code into the editor and click **Add to Chart**.

- **Step 4**: The indicator will appear on your chart with the default settings.

2. **Adjusting the Settings**:

- **ATR Period**:

- **Definition**: Number of periods over which the ATR is calculated.

- **Adjustment**: Increase for a smoother ATR; decrease for a more responsive ATR.

- **ATR Multiplier**:

- **Definition**: Factor by which the ATR is multiplied to set the stop loss distance.

- **Adjustment**: Increase to widen the stop loss (less likely to be hit); decrease to tighten the stop loss.

- **Smoothing Method**:

- **Options**: RMA, SMA, EMA, WMA, Hull MA.

- **Adjustment**: Experiment to see which method aligns best with your trading strategy.

- **Display Options**:

- **Show Long Stop Loss**: Toggle to display or hide the long stop loss line.

- **Show Short Stop Loss**: Toggle to display or hide the short stop loss line.

3. **Interpreting the Indicator**:

- **Long Positions**:

- **Action**: Set your stop loss at the value indicated by the green line when entering a long trade.

- **Short Positions**:

- **Action**: Set your stop loss at the value indicated by the red line when entering a short trade.

- **Adjusting Stop Losses**:

- **Trailing Stops**: You may choose to adjust your stop loss over time, moving it in the direction of your trade as the ATR-based stop loss levels change.

4. **Implementing in Your Trading Strategy**:

- **Risk Management**:

- **Position Sizing**: Use the stop loss distance to calculate your position size based on your risk tolerance.

- **Consistency**: Apply the same settings consistently to maintain discipline.

- **Combining with Other Indicators**:

- **Enhance Decision-Making**: Use in conjunction with trend indicators, support and resistance levels, or other technical analysis tools.

- **Alerts Setup** (If included in the code):

- **Purpose**: Receive notifications when the price approaches or hits your stop loss level.

- **Configuration**: Set up alerts in TradingView based on the alert conditions defined in the indicator.

---

**Benefits of Using This Indicator**

- **Adaptive Risk Management**: By accounting for current market volatility, the indicator helps prevent setting stop losses that are too tight or too wide.

- **Minimize Premature Stop-Outs**: Reduces the likelihood of being stopped out due to normal price fluctuations.

- **Flexibility**: Customizable settings allow you to tailor the indicator to different trading instruments and timeframes.

- **Visualization**: Clear visual representation of stop loss levels aids in quick decision-making.

---

**Things to Consider**

- **Market Conditions**:

- **High Volatility**: Be cautious as ATR values—and thus stop loss distances—can widen, increasing potential losses.

- **Low Volatility**: Tighter stop losses may increase the chance of being stopped out by minor price movements.

- **Backtesting and Optimization**:

- **Historical Analysis**: Test the indicator on past data to evaluate its effectiveness and adjust settings accordingly.

- **Continuous Improvement**: Regularly reassess and fine-tune the parameters to adapt to changing market conditions.

- **Risk Per Trade**:

- **Alignment with Risk Tolerance**: Ensure the stop loss level keeps potential losses within your acceptable risk per trade (e.g., 1-2% of your trading capital).

- **Emotional Discipline**:

- **Stick to Your Plan**: Avoid making impulsive changes to your stop loss levels based on emotions rather than analysis.

---

**Example Usage Scenario**

1. **Setting Up a Long Trade**:

- **Entry Price**: $100

- **ATR Value**: $2

- **ATR Multiplier**: 1.5

- **Calculated Stop Loss**: $100 - ($2 * 1.5) = $97

- **Action**: Place a stop loss order at $97.

2. **During the Trade**:

- **Price Increases to $105**

- **ATR Remains at $2**

- **New Stop Loss Level**: $105 - ($2 * 1.5) = $102

- **Action**: Move your stop loss up to $102 to lock in profits.

---

**Final Tips**

- **Documentation**: Keep a trading journal to record your trades, stop loss levels, and observations for future reference.

- **Education**: Continuously educate yourself on risk management and technical analysis to enhance your trading skills.

- **Support**: Engage with trading communities or seek professional advice if you're unsure about implementing the indicator effectively.

---

**Conclusion**

The ATR-Based Stop Loss Indicator is a valuable tool for traders looking to enhance their risk management by setting stop losses that adapt to market volatility. By integrating this indicator into your trading routine, you can improve your ability to protect capital and potentially increase profitability. Remember to use it as part of a comprehensive trading strategy, and always adhere to sound risk management principles.

---

**How to Access the Indicator**

To start using the ATR-Based Stop Loss Indicator, follow these steps:

1. **Obtain the Code**: Copy the PineScript code provided for the indicator.

2. **Create a New Indicator in TradingView**:

- Open TradingView and navigate to the **Pine Editor**.

- Paste the code into the editor.

- Click **Save** and give your indicator a name.

3. **Add to Chart**: Click **Add to Chart** to apply the indicator to your current chart.

4. **Customize Settings**: Adjust the input parameters to suit your preferences and start integrating the indicator into your trading strategy.

---

**Disclaimer**

Trading involves significant risk, and it's possible to lose all your capital. The ATR-Based Stop Loss Indicator is a tool to aid in decision-making but does not guarantee profits or prevent losses. Always conduct your own analysis and consider seeking advice from a financial professional before making trading decisions.

Dynamic ConfluenceThe Dynamic MA Confluence Indicator is a powerful tool designed to simplify your trading experience by automatically identifying the most influential moving average (MA) lengths on your chart. Whether you're using Simple Moving Averages (SMA) or Exponential Moving Averages (EMA), this indicator helps you pinpoint the MA length that holds the greatest confluence, allowing you to make informed trading decisions with ease.

How It Works:

This indicator analyzes a wide range of moving averages, from short-term to long-term, to determine which ones are closest to each other. By setting a "Proximity Percentage," you can control how close these MAs need to be to be considered as having confluence. The indicator then calculates the average of these close MAs to establish a dynamic support or resistance level on your chart.

Why Use This Indicator?

Automatic Optimization: Unsure of which MA length to apply? The indicator automatically highlights the MA length with the most confluence, giving you a clear edge in identifying significant market levels.

Adaptability: Choose between SMA and EMA to suit your trading strategy and market conditions.

Enhanced Decision-Making: By focusing on the MA length with the greatest influence, you can better anticipate market movements and adjust your strategies accordingly.

Customizable Sensitivity: Adjust the Proximity Percentage to fine-tune the indicator's sensitivity, ensuring it aligns with your trading preferences.

Key Feature:

Current Key Confluence MA Length: Displayed in an optional table, this feature shows the MA length that currently has the most impact on the confluence level, providing you with actionable insights at a glance.

Whether you're a seasoned trader or just starting, the Dynamic MA Confluence Indicator offers a streamlined approach to understanding market dynamics, helping you trade smarter and with more confidence. This presentation text is designed to clearly communicate the purpose, functionality, and benefits of the indicator, making it easy for users to understand its value and how it can enhance their trading strategies.

The Dynamic MA Confluence Indicator is a tool designed to assist traders in analyzing market trends. It should not be considered as financial advice or a guarantee of future performance. Trading involves significant risk, and it is possible to lose more than your initial investment. Users should conduct their own research and consider their financial situation before making trading decisions. Always consult with a financial advisor if you are unsure about any trading strategies or decisions. This disclaimer is intended to remind users of the inherent risks in trading and the importance of conducting their own due diligence.

Season ChartThis overlay is built on the idea of seasonal charts.

It is constructed by taking the percentage change from each close and recording that change for every trading day of any year that is within the sample. We then take the average for each day of all the years.

These averages are then cumulated to create the chart as per traditional seasonal chart construction.

I have also taken a trimmed mean of the averages to try and dampen the impact one off moves that may have a dramatic effect on the daily averages (for example the crash to $0 in oil in April 2020) however, even removing 10% may not guarantee one off moves won’t affect the average.

The construction of the chart is completely dependent on the data provided by TradingView and so it is recommended that if longer sample sizes are used, the user go back to check that the years contained within the sample have a full history. Some data may have large gaps in their history and this can distort the seasonality readings.

I have attempted to align the chart with the first trading day of the year, but the start of some months may be out by a day or two as it becomes difficult to track all weeks with differing market holidays closures each year and this in turn varies the total amount of actual trading days in each year as well as leap years.

This overlay is designed for the Daily time frame only and will not work on Crypto or any other instrument that trades outside of usual business weekdays. Future updates may include the ability to adapt to Crypto instruments.

All feedback and comments welcome!

RSI Trend Following StrategyOverview

The RSI Trend Following Strategy utilizes Relative Strength Index (RSI) to enter the trade for the potential trend continuation. It uses Stochastic indicator to check is the price is not in overbought territory and the MACD to measure the current price momentum. Moreover, it uses the 200-period EMA to filter the counter trend trades with the higher probability. The strategy opens only long trades.

Unique Features

Dynamic stop-loss system: Instead of fixed stop-loss level strategy utilizes average true range (ATR) multiplied by user given number subtracted from the position entry price as a dynamic stop loss level.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Two layers trade filtering system: Strategy utilizes MACD and Stochastic indicators measure the current momentum and overbought condition and use 200-period EMA to filter trades against major trend.

Trailing take profit level: After reaching the trailing profit activation level script activates the trailing of long trade using EMA. More information in methodology.

Wide opportunities for strategy optimization: Flexible strategy settings allows users to optimize the strategy entries and exits for chosen trading pair and time frame.

Methodology

The strategy opens long trade when the following price met the conditions:

RSI is above 50 level.

MACD line shall be above the signal line

Both lines of Stochastic shall be not higher than 80 (overbought territory)

Candle’s low shall be above the 200 period EMA

When long trade is executed, strategy set the stop-loss level at the price ATR multiplied by user-given value below the entry price. This level is recalculated on every next candle close, adjusting to the current market volatility.

At the same time strategy set up the trailing stop validation level. When the price crosses the level equals entry price plus ATR multiplied by user-given value script starts to trail the price with trailing EMA(by default = 20 period). If price closes below EMA long trade is closed. When the trailing starts, script prints the label “Trailing Activated”.

Strategy settings

In the inputs window user can setup the following strategy settings:

ATR Stop Loss (by default = 1.75)

ATR Trailing Profit Activation Level (by default = 2.25)

MACD Fast Length (by default = 12, period of averaging fast MACD line)

MACD Fast Length (by default = 26, period of averaging slow MACD line)

MACD Signal Smoothing (by default = 9, period of smoothing MACD signal line)

Oscillator MA Type (by default = EMA, available options: SMA, EMA)

Signal Line MA Type (by default = EMA, available options: SMA, EMA)

RSI Length (by default = 14, period for RSI calculation)

Trailing EMA Length (by default = 20, period for EMA, which shall be broken close the trade after trailing profit activation)

Justification of Methodology

This trading strategy is designed to leverage a combination of technical indicators—Relative Strength Index (RSI), Moving Average Convergence Divergence (MACD), Stochastic Oscillator, and the 200-period Exponential Moving Average (EMA)—to determine optimal entry points for long trades. Additionally, the strategy uses the Average True Range (ATR) for dynamic risk management to adapt to varying market conditions. Let's look in details for which purpose each indicator is used for and why it is used in this combination.

Relative Strength Index (RSI) is a momentum indicator used in technical analysis to measure the speed and change of price movements in a financial market. It helps traders identify whether an asset is potentially overbought (overvalued) or oversold (undervalued), which can indicate a potential reversal or continuation of the current trend.

How RSI Works? RSI tracks the strength of recent price changes. It compares the average gains and losses over a specific period (usually 14 periods) to assess the momentum of an asset. Average gain is the average of all positive price changes over the chosen period. It reflects how much the price has typically increased during upward movements. Average loss is the average of all negative price changes over the same period. It reflects how much the price has typically decreased during downward movements.

RSI calculates these average gains and losses and compares them to create a value between 0 and 100. If the RSI value is above 70, the asset is generally considered overbought, meaning it might be due for a price correction or reversal downward. Conversely, if the RSI value is below 30, the asset is considered oversold, suggesting it could be poised for an upward reversal or recovery. RSI is a useful tool for traders to determine market conditions and make informed decisions about entering or exiting trades based on the perceived strength or weakness of an asset's price movements.

This strategy uses RSI as a short-term trend approximation. If RSI crosses over 50 it means that there is a high probability of short-term trend change from downtrend to uptrend. Therefore RSI above 50 is our first trend filter to look for a long position.

The MACD (Moving Average Convergence Divergence) is a popular momentum and trend-following indicator used in technical analysis. It helps traders identify changes in the strength, direction, momentum, and duration of a trend in an asset's price.

The MACD consists of three components:

MACD Line: This is the difference between a short-term Exponential Moving Average (EMA) and a long-term EMA, typically calculated as: MACD Line = 12 period EMA − 26 period EMA

Signal Line: This is a 9-period EMA of the MACD Line, which helps to identify buy or sell signals. When the MACD Line crosses above the Signal Line, it can be a bullish signal (suggesting a buy); when it crosses below, it can be a bearish signal (suggesting a sell).

Histogram: The histogram shows the difference between the MACD Line and the Signal Line, visually representing the momentum of the trend. Positive histogram values indicate increasing bullish momentum, while negative values indicate increasing bearish momentum.

This strategy uses MACD as a second short-term trend filter. When MACD line crossed over the signal line there is a high probability that uptrend has been started. Therefore MACD line above signal line is our additional short-term trend filter. In conjunction with RSI it decreases probability of following false trend change signals.

The Stochastic Indicator is a momentum oscillator that compares a security's closing price to its price range over a specific period. It's used to identify overbought and oversold conditions. The indicator ranges from 0 to 100, with readings above 80 indicating overbought conditions and readings below 20 indicating oversold conditions.

It consists of two lines:

%K: The main line, calculated using the formula (CurrentClose−LowestLow)/(HighestHigh−LowestLow)×100 . Highest and lowest price taken for 14 periods.

%D: A smoothed moving average of %K, often used as a signal line.

This strategy uses stochastic to define the overbought conditions. The logic here is the following: we want to avoid long trades in the overbought territory, because when indicator reaches it there is a high probability that the potential move is gonna be restricted.

The 200-period EMA is a widely recognized indicator for identifying the long-term trend direction. The strategy only trades in the direction of this primary trend to increase the probability of successful trades. For instance, when the price is above the 200 EMA, only long trades are considered, aligning with the overarching trend direction.