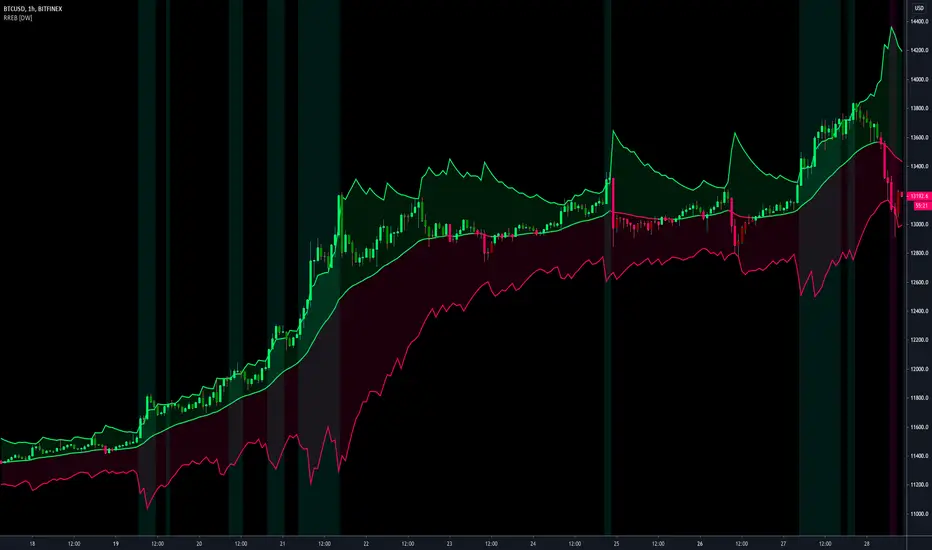

Robust Channel [tbiktag]Introducing the Robust Channel indicator.

This indicator is based on a remarkable property of robust statistics , namely, the resistance to the presence of data points that deviate significantly from the established trend (generally speaking, outliers ). Being outlier-resistant, the Robust Channel indicator “remembers” a pre-existing trend and thus exhibits a very peculiar "lag" in case of a sharp price change. This allows high-confidence identification of such price actions as a trend reversal, range break, pullback, etc.

In the case of trending and range-bound market conditions, the price remains within the channel most of the time, fluctuating around the central line.

Technical details

The central line is calculated using the repeated median slope algorithm. For each data point in a lookback window of a user-specified Length , this method calculates the median slope of the lines that connect that point to all other points inside the window. The overall median of these median slopes is then calculated and used as an estimate of the trend slope. The algorithm is very efficient as it uses an on-the-fly procedure to update the array containing the slopes (new data pushed - old data removed).

The outer line is then calculated as the central line plus the Length -period standard deviation of the price data multiplied by a user-defined Channel Width Factor . The inner line is defined analogously below the central line.

Usage

As a stand-alone indicator, the Robust Channel can be applied similarly to the Bollinger Bands and the Keltner Channel:

A close above the outer line can be interpreted as a bullish signal and a close below the inner line as a bearish signal.

Likewise, a return to the channel from below after a break may serve as a bullish signal, while a return from above may indicate bearish sentiment.

Robust Channel can be also used to confirm chart patterns such as double tops and double bottoms.

If you like this indicator, feel free to leave your feedback in the comments below!

Penunjuk Pine Script®