AK_ TREND ID AS A STRATEGY : FOR EDUCATIONAL PURPOSES ONLYJust converted the AK_ TREND ID into a strategy , to show the efficiency of this simple indicator. I used SPX in this example, to display that the indicator has been accurate for a long time.

Cari dalam skrip untuk "algo"

Guided144Algorithm conditions suggested by a friend, works best on daily tf for bitcoin.

simple cycle trading of buy and sell..

A great guide for trading those complicated moves.

ALGO 3h, 1h, 2hThis script tracks the crossing of the 10EMA on the 3h timeframe and the 200EMA on the 1h timeframe to open LONGS and SHORTS. Whether those LONGS or SHORTS actually trigger is based on the first 2 EMA's position in relation to a 3rd "controller" EMA.

11// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © gilanns

//@version=5

//

VERSION = 'v13'// 2024.3.20

strategy(

'ALGOX',

shorttitle = 'ALGOX ' + VERSION,

overlay = true,

explicit_plot_zorder = true,

pyramiding = 0,

default_qty_type = strategy.percent_of_equity,

default_qty_value = 50,

calc_on_every_tick = false,

process_orders_on_close = true,

max_bars_back = 500,

initial_capital = 5000,

commission_type = strategy.commission.percent,

commission_value = 0.02

)

//Truncate Function

truncate(number, decimals) =>

factor = math.pow(10, decimals)

int(number * factor) / factor

//

// === INPUTS ===

TPSType = input.string('Trailing', 'What TPS should be taken : ', options = )

setupType = input.string('Open/Close', title='What Trading Setup should be taken : ', options= )

scolor = input(true, title='Show coloured Bars to indicate Trend?')

almaRibbon = input(false, title='Enable Ribbon?')

//tradeType = input.string('BOTH', title='What trades should be taken : ', options= )

// === /INPUTS ===

// Display the probabilities in a table

//text01_ = str.tostring(timeframe.multiplier * intRes, '####')

//t = timenow + math.round(ta.change(time) * 25)

//var label lab01 = na

//label.delete(lab01)

//lab01 := label.new(t, close, text=text01_, style=label.style_label_left, yloc=yloc.price, xloc=xloc.bar_time, textalign=text.align_left, textcolor=color.white)

// Constants colours that include fully non-transparent option.

green100 = #008000FF

lime100 = #00FF00FF

red100 = #FF0000FF

blue100 = #0000FFFF

aqua100 = #00FFFFFF

darkred100 = #8B0000FF

gray100 = #808080FF

/////////////////////////////////////////////

// Create non-repainting security function

rp_security(_symbol, _res, _src) =>

request.security(_symbol, _res, _src )

//

f_tfInMinutes() =>

_tfInMinutes = timeframe.period == '1' ? '3' : timeframe.period == '3' ? '5' : timeframe.period == '5' ? '15' : timeframe.period == '15' ? '30' : timeframe.period == '30' ? '60' : timeframe.period == '60' ? '240' : 'D'

_tfInMinutes

my_time1 = f_tfInMinutes()

tfmult = 18 //input.int(18, "Input Timeframe Multiplier")

f_resInMinutes() =>

_resInMinutes = timeframe.multiplier * (

timeframe.isseconds ? 1. / 60. :

timeframe.isminutes ? 1. :

timeframe.isdaily ? 1440. :

timeframe.isweekly ? 10080. :

timeframe.ismonthly ? 43800. : na)

my_time = str.tostring(f_resInMinutes()*tfmult)

useSource = close //input.string('Close', 'What Source to be used?', options = )

enableFilter = input(true, "Enable Backtesting Range Filtering")

fromDate = input.time(timestamp("01 Jan 2023 00:00 +0300"), "Start Date")

toDate = input.time(timestamp("31 Dec 2099 00:00 +0300"), "End Date")

tradeDateIsAllowed = not enableFilter or (time >= fromDate and time <= toDate)

filter1 = 'Filter with Atr'

filter2 = 'Filter with RSI'

filter3 = 'Atr or RSI'

filter4 = 'Atr and RSI'

filter5 = 'No Filtering'

filter6 = 'Entry Only in sideways market(By ATR or RSI)'

filter7 = 'Entry Only in sideways market(By ATR and RSI)'

typefilter = input.string(filter5, title='Sideways Filtering Input', options= , group='Strategy Options')

RSI = truncate(ta.rsi(close, input.int(7, group='RSI Filterring')), 2)

toplimitrsi = input.int(45, title='TOP Limit', group='RSI Filterring')

botlimitrsi = input.int(10, title='BOT Limit', group='RSI Filterring')

//ST = input.bool(true, title='Show Supertrend?', group='Supertrend Indicator')

//period = input.int(1440, group='Supertrend Indicator')

//mult = input.float(2.612, group='Supertrend Indicator')

atrfiltLen = 5 //input.int(5, minval=1, title='atr Length', group='Sideways Filtering Input')

atrMaType = 'EMA' //input.string('EMA', options= , group='Sideways Filtering Input', title='atr Moving Average Type')

atrMaLen = 5 //input.int(5, minval=1, title='atr MA Length', group='Sideways Filtering Input')

//filtering

atra = request.security(syminfo.tickerid, '', ta.atr(atrfiltLen))

atrMa = atrMaType == 'EM' ? ta.ema(atra, atrMaLen) : ta.sma(atra, atrMaLen)

updm = ta.change(high)

downdm = -ta.change(low)

plusdm = na(updm) ? na : updm > downdm and updm > 0 ? updm : 0

minusdm = na(downdm) ? na : downdm > updm and downdm > 0 ? downdm : 0

cndSidwayss1 = atra >= atrMa

cndSidwayss2 = RSI > toplimitrsi or RSI < botlimitrsi

cndSidways = cndSidwayss1 or cndSidwayss2

cndSidways1 = cndSidwayss1 and cndSidwayss2

Sidwayss1 = atra <= atrMa

Sidwayss2 = RSI < toplimitrsi and RSI > botlimitrsi

Sidways = Sidwayss1 or Sidwayss2

Sidways1 = Sidwayss1 and Sidwayss2

trendType = typefilter == filter1 ? cndSidwayss1 : typefilter == filter2 ? cndSidwayss2 : typefilter == filter3 ? cndSidways : typefilter == filter4 ? cndSidways1 : typefilter == filter5 ? RSI > 0 : typefilter == filter6 ? Sidways : typefilter == filter7 ? Sidways1 : na

// === /INPUTS ===

tf = my_time //input('15')

r = ticker.heikinashi(syminfo.tickerid)

openSeriesAlt = request.security(r, tf, open, lookahead=barmerge.lookahead_on)

closeSeriesAlt = request.security(r, tf, close, lookahead=barmerge.lookahead_on)

//openP = plot(almaRibbon ? openSeriesAlt : na, color=color.new(color.lime, 0), linewidth=3)

//closeP = plot(almaRibbon ? closeSeriesAlt : na, color=color.new(color.red, 0), linewidth=3)

BUYOC = ta.crossover(closeSeriesAlt, openSeriesAlt) and setupType == "Open/Close" and trendType

SELLOC = ta.crossunder(closeSeriesAlt, openSeriesAlt) and setupType == "Open/Close" and trendType

//strategy.entry('sell', direction=strategy.short, qty=trade_size, comment='sell', when=sel_entry)

//strategy.entry('buy', direction=strategy.long, qty=trade_size, comment='buy', when=buy_entry)

//trendColour = closeSeriesAlt > openSeriesAlt ? color.green : color.red

//bcolour = closeSeriesAlt > openSeriesAlt ? lime100 : red100

//barcolor(scolor ? bcolour : na, title='Bar Colours')

//closeP = plot(almaRibbon ? closeSeriesAlt : na, title='Close Series', color=color.new(trendColour, 20), linewidth=2, style=plot.style_line)

//openP = plot(almaRibbon ? openSeriesAlt : na, title='Open Series', color=color.new(trendColour, 20), linewidth=2, style=plot.style_line)

//fill(closeP, openP, color=color.new(trendColour, 80))

//

//rt = input(true, title="ATR Based REnko is the Default, UnCheck to use Traditional ATR?")

atrLen = 3 //input.int(3, title="RENKO_ATR", group = "Renko Settings")

isATR = true //input.bool(true, title="RENKO_USE_RENKO_ATR", group = "Renko Settings")

tradLen1 = 1000 //input.int(1000, title="RENKO_TRADITIONAL", group = "Renko Settings")

//Code to be implemented in V2

//mul = input(1, "Number Of minticks")

//value = mul * syminfo.mintick

tradLen = tradLen1 * 1

param = isATR ? ticker.renko(syminfo.tickerid, "ATR", atrLen) : ticker.renko(syminfo.tickerid, "Traditional", tradLen)

renko_close = request.security(param, my_time, close, lookahead=barmerge.lookahead_on)

renko_open = request.security(param, my_time, open, lookahead=barmerge.lookahead_on)

//============================================

//Sniper------------------------------------------------------------------------------------------------------------------------------------- // Signal 2

//============================================

//============================================

//EMA_CROSS-------------------------------------------------------------------------------------------------------------------------------- // Signal 4

//============================================

EMA1_length=input.int(2, "EMA1_length", group = "Renko Settings")

EMA2_length=input.int(10, "EMA2_length", group = "Renko Settings")

a = ta.ema(renko_close, EMA1_length)

b = ta.ema(renko_close, EMA2_length)

//BUY = ta.cross(a, b) and a > b and renko_open < renko_close

//SELL = ta.cross(a, b) and a < b and renko_close < renko_open

///////////////////////////////

// Determine long and short conditions

BUYR = ta.crossover(a, b) and setupType == "Renko" and trendType

SELLR = ta.crossunder(a, b) and setupType == "Renko" and trendType

sel_color = setupType == "Open/Close" ? closeSeriesAlt < openSeriesAlt : setupType == "Renko" ? renko_close < renko_open : na

buy_color = setupType == "Open/Close" ? closeSeriesAlt > openSeriesAlt : setupType == "Renko" ? renko_close > renko_open : na

sel_entry = setupType == "Open/Close" ? SELLOC : setupType == "Renko" ? SELLR : na

buy_entry = setupType == "Open/Close" ? BUYOC : setupType == "Renko" ? BUYR : na

trendColour = buy_color ? color.green : color.red

bcolour = buy_color ? lime100 : red100

barcolor(scolor ? bcolour : na, title='Bar Colours')

p11=plot(almaRibbon and setupType == "Open/Close" ? closeSeriesAlt : almaRibbon and setupType == "Renko" ? renko_close : na, style=plot.style_circles, linewidth=1, color=color.new(trendColour, 80), title="RENKO_1")

p22=plot(almaRibbon and setupType == "Open/Close" ? openSeriesAlt : almaRibbon and setupType == "Renko" ? renko_open : na, style=plot.style_circles, linewidth=1, color=color.new(trendColour, 80), title="RENKO_2")

fill(p11, p22, color=color.new(trendColour, 50), title="RENKO_fill")

//

lxTrigger = false

sxTrigger = false

leTrigger = buy_entry

seTrigger = sel_entry

// === /ALERT conditions.

buy = leTrigger //ta.crossover(closeSeriesAlt, openSeriesAlt)

sell = seTrigger //ta.crossunder(closeSeriesAlt, openSeriesAlt)

varip wasLong = false

varip wasShort = false

if barstate.isconfirmed

wasLong := false

else

if buy

wasLong := true

if barstate.isconfirmed

wasShort := false

else

if sell

wasShort := true

plotshape(wasLong, color = color.yellow)

plotshape(wasShort, color = color.yellow)

//plotshape(almaRibbon ? buy : na, title = "Buy", text = 'Buy', style = shape.labelup, location = location.belowbar, color= #39ff14, textcolor = #FFFFFF, size = size.tiny)

//plotshape(almaRibbon ? sell : na, title = "Exit", text = 'Exit', style = shape.labeldown, location = location.abovebar, color= #ff1100, textcolor = #FFFFFF, size = size.tiny)

// === STRATEGY ===

i_alert_txt_entry_long = "Short Exit" //input.text_area(defval = "Short Exit", title = "Long Entry Message", group = "Alerts")

i_alert_txt_exit_long = "Long Exit" //input.text_area(defval = "Long Exit", title = "Long Exit Message", group = "Alerts")

i_alert_txt_entry_short = "Go Short" //input.text_area(defval = "Go Short", title = "Short Entry Message", group = "Alerts")

i_alert_txt_exit_short = "Go Long" //input.text_area(defval = "Go Long", title = "Short Exit Message", group = "Alerts")

// Entries and Exits with TP/SL

//tradeType

if buy and TPSType == "Trailing" and tradeDateIsAllowed

strategy.close("Short" , alert_message = i_alert_txt_exit_short)

strategy.entry("Long" , strategy.long , alert_message = i_alert_txt_entry_long)

if sell and TPSType == "Trailing" and tradeDateIsAllowed

strategy.close("Long" , alert_message = i_alert_txt_exit_long)

strategy.entry("Short" , strategy.short, alert_message = i_alert_txt_entry_short)

//tradeType

if buy and TPSType == "Options" and tradeDateIsAllowed

// strategy.close("Short" , alert_message = i_alert_txt_exit_short)

strategy.entry("Long" , strategy.long , alert_message = i_alert_txt_entry_long)

if sell and TPSType == "Options" and tradeDateIsAllowed

strategy.close("Long" , alert_message = i_alert_txt_exit_long)

// strategy.entry("Short" , strategy.short, alert_message = i_alert_txt_entry_short)

G_RISK = '■ ' + 'Risk Management'

//#region ———— <↓↓↓ G_RISK ↓↓↓> {

//ATR SL Settings

atrLength = 20 //input.int(20, minval=1, title='ATR Length')

profitFactor = 2.5 //input(2.5, title='Take Profit Factor')

stopFactor = 1 //input(1.0, title='Stop Loss Factor')

// Calculate ATR

tpatrValue = ta.atr(atrLength)

// Calculate take profit and stop loss levels for buy signals

takeProfit1_buy = 1 * profitFactor * tpatrValue //close + profitFactor * atrValue

takeProfit2_buy = 2 * profitFactor * tpatrValue //close + 2 * profitFactor * atrValue

takeProfit3_buy = 3 * profitFactor * tpatrValue //close + 3 * profitFactor * atrValue

stopLoss_buy = close - takeProfit1_buy //stopFactor * tpatrValue

// Calculate take profit and stop loss levels for sell signals

takeProfit1_sell = 1 * profitFactor * tpatrValue //close - profitFactor * atrValue

takeProfit2_sell = 2 * profitFactor * tpatrValue //close - 2 * profitFactor * atrValue

takeProfit3_sell = 3 * profitFactor * tpatrValue //close - 3 * profitFactor * atrValue

stopLoss_sell = close + takeProfit1_sell //stopFactor * tpatrValue

// ———————————

//Tooltip

T_LVL = '(%) Exit Level'

T_QTY = '(%) Adjust trade exit volume'

T_MSG = 'Paste JSON message for your bot'

//Webhook Message

O_LEMSG = 'Long Entry'

O_LXMSGSL = 'Long SL'

O_LXMSGTP1 = 'Long TP1'

O_LXMSGTP2 = 'Long TP2'

O_LXMSGTP3 = 'Long TP3'

O_LXMSG = 'Long Exit'

O_SEMSG = 'Short Entry'

O_SXMSGSL = 'Short SL'

O_SXMSGA = 'Short TP1'

O_SXMSGB = 'Short TP2'

O_SXMSGC = 'Short TP3'

O_SXMSGX = 'Short Exit'

// on whole pips) for forex currency pairs.

pip_size = syminfo.mintick * (syminfo.type == "forex" ? 10 : 1)

// On the last historical bar, show the instrument's pip size

//if barstate.islastconfirmedhistory

// label.new(x=bar_index + 2, y=close, style=label.style_label_left,

// color=color.navy, textcolor=color.white, size=size.large,

// text=syminfo.ticker + "'s pip size is:\n" +

// str.tostring(pip_size))

// ——————————— | | | Line length guide |

i_lxLvlTP1 = leTrigger ? takeProfit1_buy : seTrigger ? takeProfit1_sell : na //input.float (1, 'Level TP1' , group = G_RISK, tooltip = T_LVL)

i_lxQtyTP1 = input.float (50, 'Qty TP1' , group = G_RISK, tooltip = T_QTY)

i_lxLvlTP2 = leTrigger ? takeProfit2_buy : seTrigger ? takeProfit2_sell : na //input.float (1.5, 'Level TP2' , group = G_RISK, tooltip = T_LVL)

i_lxQtyTP2 = input.float (30, 'Qty TP2' , group = G_RISK, tooltip = T_QTY)

i_lxLvlTP3 = leTrigger ? takeProfit3_buy : seTrigger ? takeProfit3_sell : na //input.float (2, 'Level TP3' , group = G_RISK, tooltip = T_LVL)

i_lxQtyTP3 = input.float (20, 'Qty TP3' , group = G_RISK, tooltip = T_QTY)

i_lxLvlSL = leTrigger ? takeProfit1_buy : seTrigger ? takeProfit1_sell : na //input.float (0.5, 'Stop Loss' , group = G_RISK, tooltip = T_LVL)

i_sxLvlTP1 = i_lxLvlTP1

i_sxQtyTP1 = i_lxQtyTP1

i_sxLvlTP2 = i_lxLvlTP2

i_sxQtyTP2 = i_lxQtyTP2

i_sxLvlTP3 = i_lxLvlTP3

i_sxQtyTP3 = i_lxQtyTP3

i_sxLvlSL = i_lxLvlSL

G_MSG = '■ ' + 'Webhook Message'

i_leMsg = O_LEMSG //input.string (O_LEMSG ,'Long Entry' , group = G_MSG, tooltip = T_MSG)

i_lxMsgSL = O_LXMSGSL //input.string (O_LXMSGSL ,'Long SL' , group = G_MSG, tooltip = T_MSG)

i_lxMsgTP1 = O_LXMSGTP1 //input.string (O_LXMSGTP1,'Long TP1' , group = G_MSG, tooltip = T_MSG)

i_lxMsgTP2 = O_LXMSGTP2 //input.string (O_LXMSGTP2,'Long TP2' , group = G_MSG, tooltip = T_MSG)

i_lxMsgTP3 = O_LXMSGTP3 //input.string (O_LXMSGTP3,'Long TP3' , group = G_MSG, tooltip = T_MSG)

i_lxMsg = O_LXMSG //input.string (O_LXMSG ,'Long Exit' , group = G_MSG, tooltip = T_MSG)

i_seMsg = O_SEMSG //input.string (O_SEMSG ,'Short Entry' , group = G_MSG, tooltip = T_MSG)

i_sxMsgSL = O_SXMSGSL //input.string (O_SXMSGSL ,'Short SL' , group = G_MSG, tooltip = T_MSG)

i_sxMsgTP1 = O_SXMSGA //input.string (O_SXMSGA ,'Short TP1' , group = G_MSG, tooltip = T_MSG)

i_sxMsgTP2 = O_SXMSGB //input.string (O_SXMSGB ,'Short TP2' , group = G_MSG, tooltip = T_MSG)

i_sxMsgTP3 = O_SXMSGC //input.string (O_SXMSGC ,'Short TP3' , group = G_MSG, tooltip = T_MSG)

i_sxMsg = O_SXMSGX //input.string (O_SXMSGX ,'Short Exit' , group = G_MSG, tooltip = T_MSG)

i_src = close

G_DISPLAY = 'Display'

//

i_alertOn = true //input.bool (true, 'Alert Labels On/Off' , group = G_DISPLAY)

i_barColOn = true //input.bool (true, 'Bar Color On/Off' , group = G_DISPLAY)

// ———————————

// @function Calculate the Take Profit line, and the crossover or crossunder

f_tp(_condition, _conditionValue, _leTrigger, _seTrigger, _src, _lxLvlTP, _sxLvlTP)=>

var float _tpLine = 0.0

_topLvl = _src + _lxLvlTP //TPSType == "Fixed %" ? _src + (_src * (_lxLvlTP / 100)) : _src + _lxLvlTP

_botLvl = _src - _lxLvlTP //TPSType == "Fixed %" ? _src - (_src * (_sxLvlTP / 100)) : _src - _sxLvlTP

_tpLine := _condition != _conditionValue and _leTrigger ? _topLvl :

_condition != -_conditionValue and _seTrigger ? _botLvl :

nz(_tpLine )

// @function Similar to "ta.crossover" or "ta.crossunder"

f_cross(_scr1, _scr2, _over)=>

_cross = _over ? _scr1 > _scr2 and _scr1 < _scr2 :

_scr1 < _scr2 and _scr1 > _scr2

// ———————————

//

var float condition = 0.0

var float slLine = 0.0

var float entryLine = 0.0

//

entryLine := leTrigger and condition <= 0.0 ? close :

seTrigger and condition >= 0.0 ? close : nz(entryLine )

//

slTopLvl = TPSType == "Fixed %" ? i_src + (i_src * (i_lxLvlSL / 100)) : i_src + i_lxLvlSL

slBotLvl = TPSType == "Fixed %" ? i_src - (i_src * (i_sxLvlSL / 100)) : i_src - i_lxLvlSL

slLine := condition <= 0.0 and leTrigger ? slBotLvl :

condition >= 0.0 and seTrigger ? slTopLvl : nz(slLine )

slLong = f_cross(low, slLine, false)

slShort = f_cross(high, slLine, true )

//

= f_tp(condition, 1.2,leTrigger, seTrigger, i_src, i_lxLvlTP3, i_sxLvlTP3)

= f_tp(condition, 1.1,leTrigger, seTrigger, i_src, i_lxLvlTP2, i_sxLvlTP2)

= f_tp(condition, 1.0,leTrigger, seTrigger, i_src, i_lxLvlTP1, i_sxLvlTP1)

tp3Long = f_cross(high, tp3Line, true )

tp3Short = f_cross(low, tp3Line, false)

tp2Long = f_cross(high, tp2Line, true )

tp2Short = f_cross(low, tp2Line, false)

tp1Long = f_cross(high, tp1Line, true )

tp1Short = f_cross(low, tp1Line, false)

switch

leTrigger and condition <= 0.0 => condition := 1.0

seTrigger and condition >= 0.0 => condition := -1.0

tp3Long and condition == 1.2 => condition := 1.3

tp3Short and condition == -1.2 => condition := -1.3

tp2Long and condition == 1.1 => condition := 1.2

tp2Short and condition == -1.1 => condition := -1.2

tp1Long and condition == 1.0 => condition := 1.1

tp1Short and condition == -1.0 => condition := -1.1

slLong and condition >= 1.0 => condition := 0.0

slShort and condition <= -1.0 => condition := 0.0

lxTrigger and condition >= 1.0 => condition := 0.0

sxTrigger and condition <= -1.0 => condition := 0.0

longE = leTrigger and condition <= 0.0 and condition == 1.0

shortE = seTrigger and condition >= 0.0 and condition == -1.0

longX = lxTrigger and condition >= 1.0 and condition == 0.0

shortX = sxTrigger and condition <= -1.0 and condition == 0.0

longSL = slLong and condition >= 1.0 and condition == 0.0

shortSL = slShort and condition <= -1.0 and condition == 0.0

longTP3 = tp3Long and condition == 1.2 and condition == 1.3

shortTP3 = tp3Short and condition == -1.2 and condition == -1.3

longTP2 = tp2Long and condition == 1.1 and condition == 1.2

shortTP2 = tp2Short and condition == -1.1 and condition == -1.2

longTP1 = tp1Long and condition == 1.0 and condition == 1.1

shortTP1 = tp1Short and condition == -1.0 and condition == -1.1

// ——————————— {

//

if strategy.position_size <= 0 and longE and TPSType == "ATR" and tradeDateIsAllowed

strategy.entry( 'Long', strategy.long, alert_message = i_leMsg, comment = 'LE')

if strategy.position_size > 0 and condition == 1.0 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'LXTP1', from_entry = 'Long', qty_percent = i_lxQtyTP1, limit = tp1Line, stop = slLine, comment_profit = 'LXTP1', comment_loss = 'SL', alert_profit = i_lxMsgTP1, alert_loss = i_lxMsgSL)

if strategy.position_size > 0 and condition == 1.1 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'LXTP2', from_entry = 'Long', qty_percent = i_lxQtyTP2, limit = tp2Line, stop = slLine, comment_profit = 'LXTP2', comment_loss = 'SL', alert_profit = i_lxMsgTP2, alert_loss = i_lxMsgSL)

if strategy.position_size > 0 and condition == 1.2 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'LXTP3', from_entry = 'Long', qty_percent = i_lxQtyTP3, limit = tp3Line, stop = slLine, comment_profit = 'LXTP3', comment_loss = 'SL', alert_profit = i_lxMsgTP3, alert_loss = i_lxMsgSL)

if longX and tradeDateIsAllowed

strategy.close( 'Long', alert_message = i_lxMsg, comment = 'LX')

//

if strategy.position_size >= 0 and shortE and TPSType == "ATR" and tradeDateIsAllowed

strategy.entry( 'Short', strategy.short, alert_message = i_leMsg, comment = 'SE')

if strategy.position_size < 0 and condition == -1.0 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'SXTP1', from_entry = 'Short', qty_percent = i_sxQtyTP1, limit = tp1Line, stop = slLine, comment_profit = 'SXTP1', comment_loss = 'SL', alert_profit = i_sxMsgTP1, alert_loss = i_sxMsgSL)

if strategy.position_size < 0 and condition == -1.1 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'SXTP2', from_entry = 'Short', qty_percent = i_sxQtyTP2, limit = tp2Line, stop = slLine, comment_profit = 'SXTP2', comment_loss = 'SL', alert_profit = i_sxMsgTP2, alert_loss = i_sxMsgSL)

if strategy.position_size < 0 and condition == -1.2 and TPSType == "ATR" and tradeDateIsAllowed

strategy.exit( id = 'SXTP3', from_entry = 'Short', qty_percent = i_sxQtyTP3, limit = tp3Line, stop = slLine, comment_profit = 'SXTP3', comment_loss = 'SL', alert_profit = i_sxMsgTP3, alert_loss = i_sxMsgSL)

if shortX and tradeDateIsAllowed

strategy.close( 'Short', alert_message = i_sxMsg, comment = 'SX')

// ———————————

c_tp = leTrigger or seTrigger ? na :

condition == 0.0 ? na : color.green

c_entry = leTrigger or seTrigger ? na :

condition == 0.0 ? na : color.blue

c_sl = leTrigger or seTrigger ? na :

condition == 0.0 ? na : color.red

p_tp1Line = plot ( condition == 1.0 or condition == -1.0 ? tp1Line : na, title = "TP Line 1", color = c_tp, linewidth = 1, style = plot.style_linebr)

p_tp2Line = plot ( condition == 1.0 or condition == -1.0 or condition == 1.1 or condition == -1.1 ? tp2Line : na, title = "TP Line 2", color = c_tp, linewidth = 1, style = plot.style_linebr)

p_tp3Line = plot ( condition == 1.0 or condition == -1.0 or condition == 1.1 or condition == -1.1 or condition == 1.2 or condition == -1.2 ? tp3Line : na, title = "TP Line 3", color = c_tp, linewidth = 1, style = plot.style_linebr)

p_entryLine = plot ( condition >= 1.0 or condition <= -1.0 ? entryLine : na, title = "Entry Line", color = c_entry, linewidth = 1, style = plot.style_linebr)

p_slLine = plot ( condition == 1.0 or condition == -1.0 or condition == 1.1 or condition == -1.1 or condition == 1.2 or condition == -1.2 ? slLine : na, title = "SL Line", color = c_sl, linewidth = 1, style = plot.style_linebr)

//fill( p_tp3Line, p_entryLine, color = leTrigger or seTrigger ? na :color.new(color.green, 90))

fill( p_entryLine, p_slLine, color = leTrigger or seTrigger ? na :color.new(color.red, 90))

//

plotshape( i_alertOn and longE, title = 'Long', text = 'Long', textcolor = color.white, color = color.green, style = shape.labelup, size = size.tiny, location = location.belowbar)

plotshape( i_alertOn and shortE, title = 'Short', text = 'Short', textcolor = color.white, color = color.red, style = shape.labeldown, size = size.tiny, location = location.abovebar)

plotshape( i_alertOn and (longX or shortX) ? close : na, title = 'Close', text = 'Close', textcolor = color.white, color = color.gray, style = shape.labelup, size = size.tiny, location = location.absolute)

l_tp = i_alertOn and (longTP1 or shortTP1) ? close : na

plotshape( l_tp, title = "TP1 Cross", text = "TP1", textcolor = color.white, color = color.olive, style = shape.labelup, size = size.tiny, location = location.absolute)

plotshape( i_alertOn and (longTP2 or shortTP2) ? close : na, title = "TP2 Cross", text = "TP2", textcolor = color.white, color = color.olive, style = shape.labelup, size = size.tiny, location = location.absolute)

plotshape( i_alertOn and (longTP3 or shortTP3) ? close : na, title = "TP3 Cross", text = "TP3", textcolor = color.white, color = color.olive, style = shape.labelup, size = size.tiny, location = location.absolute)

plotshape( i_alertOn and (longSL or shortSL) ? close : na, title = "SL Cross", text = "SL", textcolor = color.white, color = color.maroon, style = shape.labelup, size = size.tiny, location = location.absolute)

//

plot( na, title = "─── ───", editable = false, display = display.data_window)

plot( condition, title = "condition", editable = false, display = display.data_window)

plot( strategy.position_size * 100, title = ".position_size", editable = false, display = display.data_window)

//#endregion }

// ——————————— <↑↑↑ G_RISK ↑↑↑>

//#region ———— <↓↓↓ G_SCRIPT02 ↓↓↓> {

// @function Queues a new element in an array and de-queues its first element.

f_qDq(_array, _val) =>

array.push(_array, _val)

_return = array.shift(_array)

_return

var line a_slLine = array.new_line(1)

var line a_entryLine = array.new_line(1)

var line a_tp3Line = array.new_line(1)

var line a_tp2Line = array.new_line(1)

var line a_tp1Line = array.new_line(1)

var label a_slLabel = array.new_label(1)

var label a_tp3label = array.new_label(1)

var label a_tp2label = array.new_label(1)

var label a_tp1label = array.new_label(1)

var label a_entryLabel = array.new_label(1)

newEntry = longE or shortE

entryIndex = 1

entryIndex := newEntry ? bar_index : nz(entryIndex )

lasTrade = bar_index >= entryIndex

l_right = 10

if TPSType == "ATR"

line.delete( f_qDq(a_slLine, line.new( entryIndex, slLine, last_bar_index + l_right, slLine, style = line.style_solid, color = c_sl)))

if TPSType == "ATR"

line.delete( f_qDq(a_entryLine, line.new( entryIndex, entryLine, last_bar_index + l_right, entryLine, style = line.style_solid, color = color.blue)))

if TPSType == "ATR"

line.delete( f_qDq(a_tp3Line, line.new( entryIndex, tp3Line, last_bar_index + l_right, tp3Line, style = line.style_solid, color = c_tp)))

if TPSType == "ATR"

line.delete( f_qDq(a_tp2Line, line.new( entryIndex, tp2Line, last_bar_index + l_right, tp2Line, style = line.style_solid, color = c_tp)))

if TPSType == "ATR"

line.delete( f_qDq(a_tp1Line, line.new( entryIndex, tp1Line, last_bar_index + l_right, tp1Line, style = line.style_solid, color = c_tp)))

if TPSType == "ATR"

label.delete( f_qDq(a_slLabel, label.new( last_bar_index + l_right, slLine, 'SL: ' + str.tostring(slLine, '##.###'), style = label.style_label_left, textcolor = color.white, color = c_sl)))

if TPSType == "ATR"

label.delete( f_qDq(a_entryLabel, label.new( last_bar_index + l_right, entryLine, 'Entry: ' + str.tostring(entryLine, '##.###'), style = label.style_label_left, textcolor = color.white, color = color.blue)))

if TPSType == "ATR"

label.delete( f_qDq(a_tp3label, label.new( last_bar_index + l_right, tp3Line, 'TP3: ' + str.tostring(tp3Line, '##.###') + " - Target Pips : - " + str.tostring(longE ? tp3Line - entryLine : entryLine - tp3Line, "#.##"), style = label.style_label_left, textcolor = color.white, color = c_tp)))

if TPSType == "ATR"

label.delete( f_qDq(a_tp2label, label.new( last_bar_index + l_right, tp2Line, 'TP2: ' + str.tostring(tp2Line, '##.###'), style = label.style_label_left, textcolor = color.white, color = c_tp)))

if TPSType == "ATR"

label.delete( f_qDq(a_tp1label, label.new( last_bar_index + l_right, tp1Line, 'TP1: ' + str.tostring(tp1Line, '##.###'), style = label.style_label_left, textcolor = color.white, color = c_tp)))

//#endregion }

// ——————————— <↑↑↑ G_SCRIPT02 ↑↑↑>

c_barCol = close > open ? color.rgb(120, 9, 139) : color.rgb(69, 155, 225)

barcolor(

i_barColOn ? c_barCol : na)

// ———————————

//

if longE or shortE or longX or shortX

alert(message = 'Any Alert', freq = alert.freq_once_per_bar_close)

if longE

alert(message = 'Long Entry', freq = alert.freq_once_per_bar_close)

if shortE

alert(message = 'Short Entry', freq = alert.freq_once_per_bar_close)

if longX

alert(message = 'Long Exit', freq = alert.freq_once_per_bar_close)

if shortX

alert(message = 'Short Exit', freq = alert.freq_once_per_bar_close)

//#endregion }

// ——————————— <↑↑↑ G_SCRIPT03 ↑↑↑>

// This source code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © TraderHalai

// This script was born out of my quest to be able to display strategy back test statistics on charts to allow for easier backtesting on devices that do not natively support backtest engine (such as mobile phones, when I am backtesting from away from my computer). There are already a few good ones on TradingView, but most / many are too complicated for my needs.

//

//Found an excellent display backtest engine by 'The Art of Trading'. This script is a snippet of his hard work, with some very minor tweaks and changes. Much respect to the original author.

//

//Full credit to the original author of this script. It can be found here: www.tradingview.com

//

// This script can be copied and airlifted onto existing strategy scripts of your own, and integrates out of the box without implementation of additional functions. I've also added Max Runup, Average Win and Average Loss per trade to the orignal script.

//

//Will look to add in more performance metrics in future, as I further develop this script.

//

//Feel free to use this display panel in your scripts and strategies.

//Thanks and enjoy! :)

//@version=5

//strategy("Strategy BackTest Display Statistics - TraderHalai", overlay=true, default_qty_value= 5, default_qty_type = strategy.percent_of_equity, initial_capital=10000, commission_type=strategy.commission.percent, commission_value=0.1)

//DEMO basic strategy - Use your own strategy here - Jaws Mean Reversion from my profile used here

//source = input(title = "Source", defval = close)

///////////////////////////// --- BEGIN TESTER CODE --- ////////////////////////

// COPY below into your strategy to enable display

////////////////////////////////////////////////////////////////////////////////

// Declare performance tracking variables

drawTester = input.bool(true, "Strategy Performance", group='Dashboards', inline="Show Dashboards")

var balance = strategy.initial_capital

var drawdown = 0.0

var maxDrawdown = 0.0

var maxBalance = 0.0

var totalWins = 0

var totalLoss = 0

// Prepare stats table

var table testTable = table.new(position.top_right, 5, 2, border_width=1)

f_fillCell(_table, _column, _row, _title, _value, _bgcolor, _txtcolor) =>

_cellText = _title + "\n" + _value

table.cell(_table, _column, _row, _cellText, bgcolor=_bgcolor, text_color=_txtcolor)

// Custom function to truncate (cut) excess decimal places

//truncate(_number, _decimalPlaces) =>

// _factor = math.pow(10, _decimalPlaces)

// int(_number * _factor) / _factor

// Draw stats table

var bgcolor = color.new(color.black,0)

if drawTester and tradeDateIsAllowed

if barstate.islastconfirmedhistory

// Update table

dollarReturn = strategy.netprofit

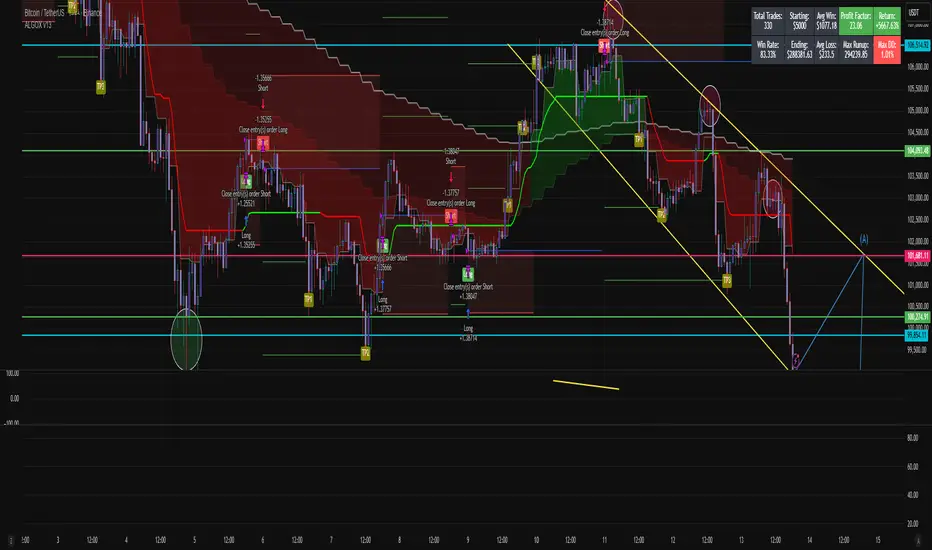

f_fillCell(testTable, 0, 0, "Total Trades:", str.tostring(strategy.closedtrades), bgcolor, color.white)

f_fillCell(testTable, 0, 1, "Win Rate:", str.tostring(truncate((strategy.wintrades/strategy.closedtrades)*100,2)) + "%", bgcolor, color.white)

f_fillCell(testTable, 1, 0, "Starting:", "$" + str.tostring(strategy.initial_capital), bgcolor, color.white)

f_fillCell(testTable, 1, 1, "Ending:", "$" + str.tostring(truncate(strategy.initial_capital + strategy.netprofit,2)), bgcolor, color.white)

f_fillCell(testTable, 2, 0, "Avg Win:", "$"+ str.tostring(truncate(strategy.grossprofit / strategy.wintrades, 2)), bgcolor, color.white)

f_fillCell(testTable, 2, 1, "Avg Loss:", "$"+ str.tostring(truncate(strategy.grossloss / strategy.losstrades, 2)), bgcolor, color.white)

f_fillCell(testTable, 3, 0, "Profit Factor:", str.tostring(truncate(strategy.grossprofit / strategy.grossloss,2)), strategy.grossprofit > strategy.grossloss ? color.green : color.red, color.white)

f_fillCell(testTable, 3, 1, "Max Runup:", str.tostring(truncate(strategy.max_runup, 2 )), bgcolor, color.white)

f_fillCell(testTable, 4, 0, "Return:", (dollarReturn > 0 ? "+" : "") + str.tostring(truncate((dollarReturn / strategy.initial_capital)*100,2)) + "%", dollarReturn > 0 ? color.green : color.red, color.white)

f_fillCell(testTable, 4, 1, "Max DD:", str.tostring(truncate((strategy.max_drawdown / strategy.equity) * 100 ,2)) + "%", color.red, color.white)

// --- END TESTER CODE --- ///////////////

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © niceGear68734

//@version=5

//strategy("Table to filter trades per day", overlay=true, use_bar_magnifier = true, initial_capital = 5000, calc_on_every_tick = true, calc_on_order_fills = true, commission_type = strategy.commission.cash_per_contract)

//~ ___________________________________________________________________________

//~ !!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

//~ !!!!!!!!!!!!!!!_________________ START _________________!!!!!!!!!!!!!!!!!

i_showweeklyPerformance = input.bool(false, 'Weekly Performance', group='Dashboards', inline="Show Dashboards")

//__________________________ User Inputs ___________________________________

var const string g_table = "Table Settings"

i_table_pos = "Top Left" //input.string(defval = "Top Left", title = "Position", options = , group = g_table, inline = "1", tooltip = "It sets the location of the table")

i_text_size = "Normal" //input.string(defval = "Normal", title = "Set the size of text", options = , tooltip = "This option is used to change the size of the text in the table")

var const string g_general = "General Settings"

i_check_open_close = "Opened" //input.string("Opened", "Check when the trade :", , group = g_general, tooltip = "This parameter defines what to check for. If opened is selected, the results will show the trades that opened on that day. If closed is selected, the results will show the trades that closed on that day")

i_timezone = "Exchange" //input.string("Exchange", title = "Set the Timezone", options = , group = g_general, tooltip = "You can use this setting whenever you want to change the time that the trade has closed/opened")

//~_____________________________ Switches ___________________________________

table_pos = switch i_table_pos

"Bottom Right" => position.bottom_right

"Bottom Left" => position.bottom_left

"Top Right" => position.top_right

"Top Left" => position.top_left

timezone_setting = i_timezone == "Exchange" ? syminfo.timezone : i_timezone

text_size = switch i_text_size

"Small" => size.small

"Normal" => size.normal

"Large" => size.large

//__________________________ Array Declaration _____________________________

var string t_column_names = array.from( "", "Sun", "Mon", "Tue", "Wed", "Thur", "Fri", "Sat") // Columns header names

var string t_row_names = array.from("", "Total Trades", "Loss", "Win", "Win Rate" ) // Rows header names

var t_column_size = array.size(t_column_names)

var t_row_size = array.size(t_row_names)

var string a_closed_trades = array.new_string() // Save the total number of trades

var string a_loss_trades = array.new_string() // Save the number of losing trades

var string a_win_trades = array.new_string() // Save the number of winning trades

var _a_day_week = array.new_int() // Save the day of the week to split data

// __________________________ Custom Functions ________________________________

//~ create a counter so that it gives a number to strategy.closed_trades.entry_time(counter)

var trade_number = -1

if strategy.closedtrades > strategy.closedtrades

trade_number += 1

f_strategy_closedtrades_hour() =>

switch

i_check_open_close =="Closed" => dayofweek(strategy.closedtrades.exit_time(trade_number), timezone_setting)

i_check_open_close =="Opened" => dayofweek(strategy.closedtrades.entry_time(trade_number), timezone_setting)

f_data(_i) =>

var _closed_trades = 0

var _loss_trades = 0

var _win_trades = 0

var _txt_closed_trades = ""

var _txt_loss_trades = ""

var _txt_win_trades = ""

if strategy.closedtrades > strategy.closedtrades and f_strategy_closedtrades_hour() == _i

_closed_trades += 1

_txt_closed_trades := str.tostring(_closed_trades)

if strategy.losstrades > strategy.losstrades and f_strategy_closedtrades_hour() == _i

_loss_trades += 1

_txt_loss_trades := str.tostring(_loss_trades)

if strategy.wintrades > strategy.wintrades and f_strategy_closedtrades_hour() == _i

_win_trades += 1

_txt_win_trades := str.tostring(_win_trades)

//__________________________

var string array1 = array.new_string(5)

var string array2 = array.new_string(5)

var string array3 = array.new_string(5)

var string array4 = array.new_string(5)

var string array5 = array.new_string(5)

var string array6 = array.new_string(5)

var string array7 = array.new_string(5)

f_pass_data_to_array(_i, _array) =>

= f_data(_i)

array.set(_array,1 , cl)

array.set(_array,2,loss)

array.set(_array,3,win)

if cl != ""

array.set(_array,4,str.tostring(str.tonumber(win) / str.tonumber(cl) * 100 , "##") + " %")

if cl != "" and win == ""

array.set(_array,4,"0 %")

for i = 1 to 7

switch

i == 1 => f_pass_data_to_array(i,array1)

i == 2 => f_pass_data_to_array(i,array2)

i == 3 => f_pass_data_to_array(i,array3)

i == 4 => f_pass_data_to_array(i,array4)

i == 5 => f_pass_data_to_array(i,array5)

i == 6 => f_pass_data_to_array(i,array6)

i == 7 => f_pass_data_to_array(i,array7)

f_retrieve_data_to_table(_i, _j) =>

switch

_i == 1 => array.get(array1, _j)

_i == 2 => array.get(array2, _j)

_i == 3 => array.get(array3, _j)

_i == 4 => array.get(array4, _j)

_i == 5 => array.get(array5, _j)

_i == 6 => array.get(array6, _j)

_i == 7 => array.get(array7, _j)

//~ ___________________________ Create Table ________________________________

create_table(_col, _row, _txt) =>

var table _tbl = table.new(position = table_pos, columns = t_column_size , rows = t_row_size, border_width=1)

color _color = _row == 0 or _col == 0 ? color.rgb(3, 62, 106) : color.rgb(2, 81, 155)

table.cell(_tbl, _col, _row, _txt, bgcolor = _color, text_color = color.white, text_size = text_size)

//~___________________________ Fill With Data _______________________________

if barstate.islastconfirmedhistory and i_showweeklyPerformance and tradeDateIsAllowed

for i = 0 to t_column_size - 1 by 1

for j = 0 to t_row_size - 1 by 1

_txt = ""

if i >= 0 and j == 0

_txt := array.get(t_column_names, i)

if j >= 0 and i == 0

_txt := array.get(t_row_names, j)

if i >= 1 and j >= 1 and j <= 5

_txt := f_retrieve_data_to_table( i , j)

create_table(i ,j , _txt)

//~ ___________________________ Notice ______________________________________

if timeframe.in_seconds() > timeframe.in_seconds("D")

x = table.new(position.middle_center,1,1,color.aqua)

table.cell_set_text(x,0,0,"Please select lower timeframes (Daily or lower)")

//~ !!!!!!!!!!!!!!!_________________ STOP _________________!!!!!!!!!!!!!!!!!!

//~ !!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

//~ ___________________________________________________________________________

// Global Dashboard Variables

// ░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░

// Dashboard Table Text Size

i_tableTextSize = "Normal" //input.string(title="Dashboard Size", defval="Normal", options= , group="Dashboards")

table_text_size(s) =>

switch s

"Auto" => size.auto

"Huge" => size.huge

"Large" => size.large

"Normal" => size.normal

"Small" => size.small

=> size.tiny

tableTextSize = table_text_size(i_tableTextSize)

// Monthly Table Performance Dashboard By @QuantNomad

// ░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░░

i_showMonthlyPerformance = input.bool(false, 'Monthly Performance', group='Dashboards', inline="Show Dashboards")

i_monthlyReturnPercision = 2

if i_showMonthlyPerformance and tradeDateIsAllowed

new_month = month(time) != month(time )

new_year = year(time) != year(time )

eq = strategy.equity

bar_pnl = eq / eq - 1

cur_month_pnl = 0.0

cur_year_pnl = 0.0

// Current Monthly P&L;

cur_month_pnl := new_month ? 0.0 :

(1 + cur_month_pnl ) * (1 + bar_pnl) - 1

// Current Yearly P&L;

cur_year_pnl := new_year ? 0.0 :

(1 + cur_year_pnl ) * (1 + bar_pnl) - 1

// Arrays to store Yearly and Monthly P&Ls;

var month_pnl = array.new_float(0)

var month_time = array.new_int(0)

var year_pnl = array.new_float(0)

var year_time = array.new_int(0)

last_computed = false

if (not na(cur_month_pnl ) and (new_month or barstate.islastconfirmedhistory))

if (last_computed )

array.pop(month_pnl)

array.pop(month_time)

array.push(month_pnl , cur_month_pnl )

array.push(month_time, time )

if (not na(cur_year_pnl ) and (new_year or barstate.islastconfirmedhistory))

if (last_computed )

array.pop(year_pnl)

array.pop(year_time)

array.push(year_pnl , cur_year_pnl )

array.push(year_time, time )

last_computed := barstate.islastconfirmedhistory ? true : nz(last_computed )

// Monthly P&L; Table

var monthly_table = table(na)

if (barstate.islastconfirmedhistory)

monthly_table := table.new(position.bottom_right, columns = 14, rows = array.size(year_pnl) + 1, border_width = 1)

table.cell(monthly_table, 0, 0, "", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 1, 0, "Jan", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 2, 0, "Feb", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 3, 0, "Mar", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 4, 0, "Apr", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 5, 0, "May", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 6, 0, "Jun", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 7, 0, "Jul", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 8, 0, "Aug", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 9, 0, "Sep", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 10, 0, "Oct", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 11, 0, "Nov", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 12, 0, "Dec", bgcolor = #cccccc, text_size=tableTextSize)

table.cell(monthly_table, 13, 0, "Year", bgcolor = #999999, text_size=tableTextSize)

for yi = 0 to array.size(year_pnl) - 1

table.cell(monthly_table, 0, yi + 1, str.tostring(year(array.get(year_time, yi))), bgcolor = #cccccc, text_size=tableTextSize)

y_color = array.get(year_pnl, yi) > 0 ? color.new(color.teal, transp = 40) : color.new(color.gray, transp = 40)

table.cell(monthly_table, 13, yi + 1, str.tostring(math.round(array.get(year_pnl, yi) * 100, i_monthlyReturnPercision)), bgcolor = y_color, text_color=color.new(color.white, 0),text_size=tableTextSize)

for mi = 0 to array.size(month_time) - 1

m_row = year(array.get(month_time, mi)) - year(array.get(year_time, 0)) + 1

m_col = month(array.get(month_time, mi))

m_color = array.get(month_pnl, mi) > 0 ? color.new(color.teal, transp = 40) : color.new(color.maroon, transp = 40)

table.cell(monthly_table, m_col, m_row, str.tostring(math.round(array.get(month_pnl, mi) * 100, i_monthlyReturnPercision)), bgcolor = m_color, text_color=color.new(color.white, 0), text_size=tableTextSize)

hide = timeframe.isintraday

// Input for EMA period

emaPeriod = 48 //input.int(48, title="EMA Period")

emaPeriod2 = 2 //input.int(2, title="EME Period 2")

emaPeriod3 = 21 //input.int(21, title="EMA Period")

// Input to toggle EMA Cloud

showcloud = input.bool(true, title="Plot EMA?", group='EMA & ATR', inline="Show EMA's & ATR")

useHTF = input.bool(true, title = "Use Higher Time Frame?")

matimeframe = useHTF ? my_time1 : ''

// EMA calculations

ema = request.security(syminfo.tickerid, matimeframe, ta.ema(close, emaPeriod))

ema2 = request.security(syminfo.tickerid, matimeframe, ta.ema(close,emaPeriod2))

ema3 = request.security(syminfo.tickerid, matimeframe,ta.ema(close, emaPeriod3))

emaColor = close > ema3 ? color.new(color.rgb(56, 142, 60, 63), 50) : color.new(color.rgb(147, 40, 51, 38), 50)

// Plotting EMA's

plot_ema1 = plot(hide ? ema : na, style=plot.style_line, color=color.new(color.rgb(255, 255, 255, 100), 50), title="EMA", linewidth=2)

plot_ema2 = plot(hide ? ema2 : na, style=plot.style_line, color=color.new(color.rgb(255, 255, 255, 100), 50), title="EMA", linewidth=1)

plot_ema3 = plot(ema3, style=plot.style_line, color=emaColor, title="EMA", linewidth=1)

// EMA Cloud

cloudColor = ema2 > ema ? color.new(#0f8513, 80) : color.new(#a81414, 80)

cloudColor2 = ema2 > ema3 ? color.new(#0f8513, 50) : color.new(#a81414, 50)

cloudColor := showcloud ? cloudColor : na

fill(plot_ema1, plot_ema2, color=cloudColor, title="EMA Cloud")

fill(plot_ema3, plot_ema2, color=cloudColor, title="EMA Cloud")

/////////////////////////////////////////////////////////////// © BackQuant ///////////////////////////////////////////////////////////////

// This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © BackQuant

import TradingView/ta/4 as ta

//@version=5

//indicator(

// title="DEMA Adjusted Average True Range ",

// shorttitle = "DEMA ATR ",

// overlay=true,

// timeframe="",

// timeframe_gaps=true

// )

// Define User Inputs

simple bool showAtr = input.bool(true, "Plot Dema?", group='EMA & ATR', inline="Show EMA's & ATR")

simple bool haCandles = true //input.bool(true, "Use HA Candles?")

simple int periodDema = 7 //input.int(7, "Dema Period", group = "Dema Atr")

series float sourceDema = close //input.source(close, "Calculation Source", group = "Dema Atr")

simple int periodAtr = 14 //input.int(14, "Period", group = "Dema Atr")

simple float factorAtr = 1.7 //input.float(1.7, "Factor", step = 0.01, group = "Dema Atr")

simple color longColour = #00ff00

simple color shortColour = #ff0000

/////////////////////////////////////////////////////////////// © BackQuant ///////////////////////////////////////////////////////////////

// Use HA Candles?

heikinashi_close = request.security(

symbol = ticker.heikinashi(syminfo.tickerid),

timeframe = timeframe.period,

expression = close,

gaps = barmerge.gaps_off,

lookahead = barmerge.lookahead_on

)

var series float source = close

if haCandles == true

source := heikinashi_close

if haCandles == false

source := sourceDema

/////////////////////////////////////////////////////////////// © BackQuant ///////////////////////////////////////////////////////////////

// Function

DemaAtrWithBands(periodDema, source, lookback, atrFactor)=>

ema1 = ta.ema(source, periodDema)

ema2 = ta.ema(ema1, periodDema)

demaOut = 2 * ema1 - ema2

atr = ta.atr(lookback)

trueRange = atr * atrFactor

DemaAtr = demaOut

DemaAtr := nz(DemaAtr , DemaAtr)

trueRangeUpper = demaOut + trueRange

trueRangeLower = demaOut - trueRange

if trueRangeLower > DemaAtr

DemaAtr := trueRangeLower

if trueRangeUpper < DemaAtr

DemaAtr := trueRangeUpper

DemaAtr

// Function Out

DemaAtr = DemaAtrWithBands(periodDema, source, periodAtr, factorAtr)

/////////////////////////////////////////////////////////////// © BackQuant ///////////////////////////////////////////////////////////////

// Conditions

DemaAtrLong = DemaAtr > DemaAtr

DemaAtrShort = DemaAtr < DemaAtr

// Colour Condtions

var color Trendcolor = #ffffff

if DemaAtrLong

Trendcolor := longColour

if DemaAtrShort

Trendcolor := shortColour

// Plotting

plot( showAtr ? DemaAtr : na, "ATR", color=Trendcolor, linewidth = 2 )

// ==========================================================================================

[STRATEGY] Moving Average CrossoverHello friends,

This is a comprehensive backtesting engine for Moving Average crossover strategies, supporting over 63 types of moving averages and filters. It allows you to test, compare, and optimize crossover behaviors between any two moving averages with flexible profit and risk management tools.

Built upon the Moving Average Crossover foundation, this advanced version lets you manually backtest more than 4096 combinations of moving average types. When combined with customizable periods, take-profits, and stop-loss levels, the total number of possible configurations becomes virtually unlimited.

🛠 How It Works

The system tests crossovers between two selected moving averages, with full control over their types, lengths, and trading direction. Integrated bracket settings enable dynamic take-profit, stop-loss, and trailing-stop management using units such as % , ATR , points , pips , or ticks .

You can restrict backtesting to a custom date range for focused performance evaluation or run it across the instrument’s full history.

🔥 Key Features

Supports 63+ moving average and filter types — including algorithms by Ehlers , Jurik , Kaufman , Apirine , Tillson , and Dürschner

Customizable MA types, periods, and strategy direction

Full-featured bracket control: TP, SL, and TSL in ATR, %, points, pips, or ticks

Backtest window customization (start, end, or range)

Direction filter: Longs only, Shorts only, or Both

Dynamic trade labeling and color-coded visualization

Option to exit only at TP, SL, or TSL

If you'd like access or have any questions, feel free to reach out to me directly via DM.

👋 Good luck and happy trading!

Paid script

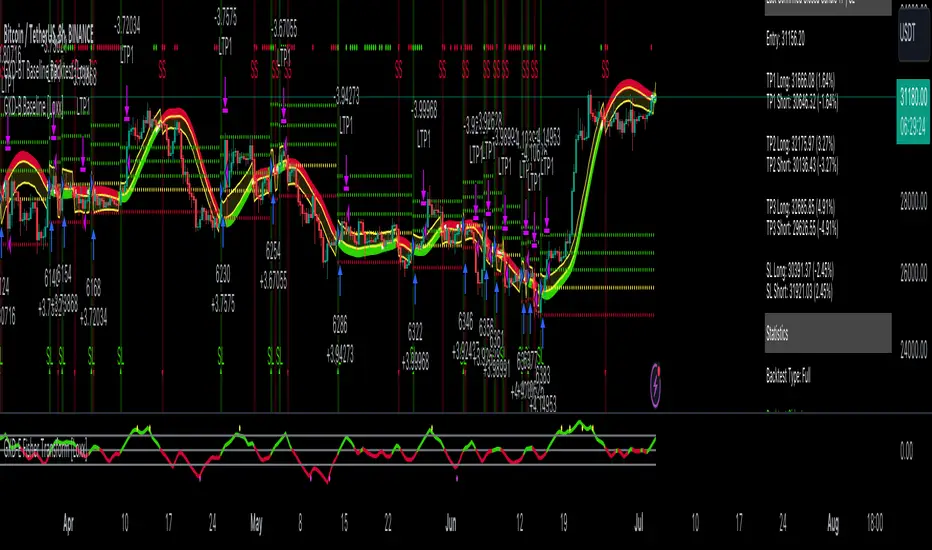

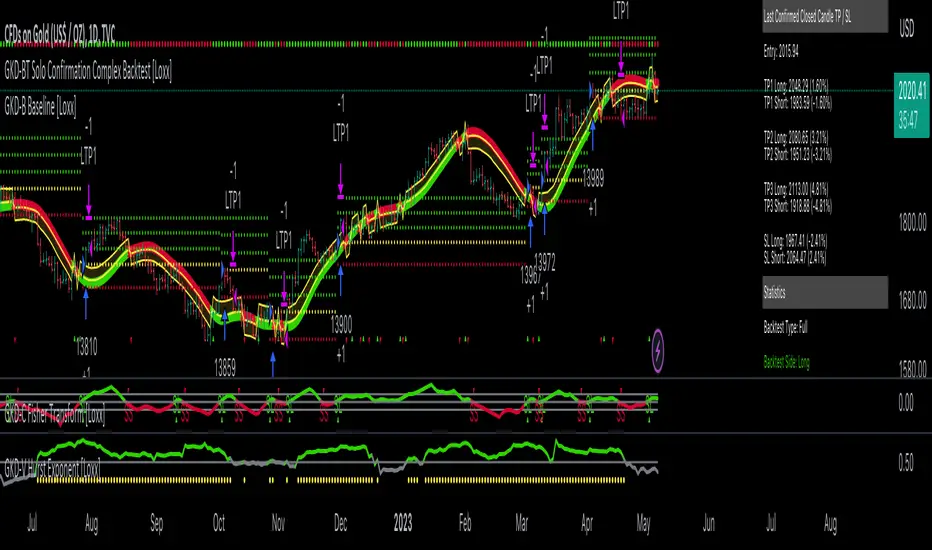

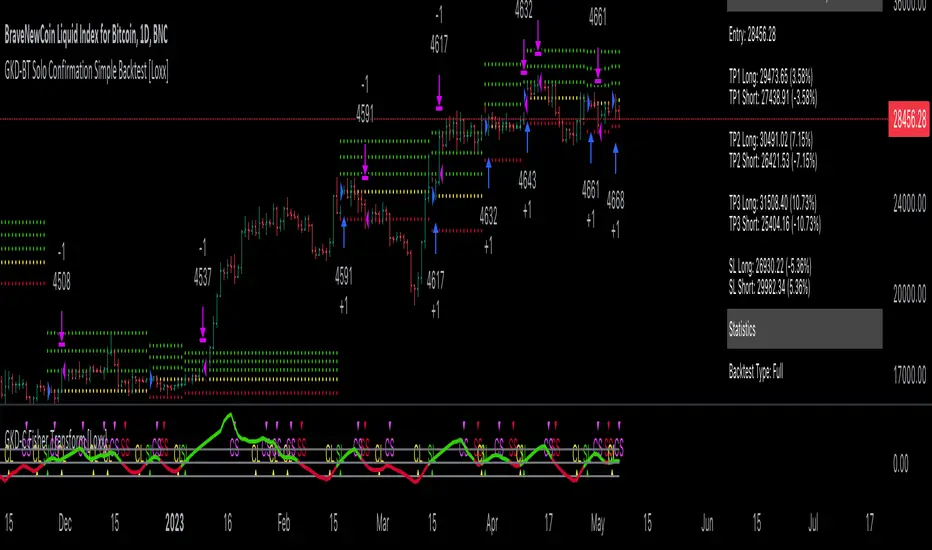

GKD-BT Baseline Backtest [Loxx]The Giga Kaleidoscope GKD-BT Baseline Backtest is a backtesting module included in Loxx's "Giga Kaleidoscope Modularized Trading System."

█ GKD-BT Baseline Backtest

The GKD-BT Baseline Backtest allows traders to backtest the Regular and Stepped baselines used in the GKD trading system. This module includes 65+ moving averages and 15+ types of volatility to choose from.

Additionally, this backtest module provides the option to test the GKD-B indicator with 1 to 3 take profits and 1 stop loss. The Trading backtest allows for the use of 1 to 3 take profits, while the Full backtest is limited to 1 take profit. The Trading backtest also offers the capability to apply a trailing take profit.

In terms of the percentage of trade removed at each take profit, this backtest module has the following hardcoded values:

Take profit 1: 50% of the trade is removed

Take profit 2: 25% of the trade is removed

Take profit 3: 25% of the trade is removed

Stop loss: 100% of the trade is removed

After each take profit is achieved, the stop loss level is adjusted. When take profit 1 is reached, the stop loss is moved to the entry point. Similarly, when take profit 2 is reached, the stop loss is shifted to take profit 1. The trailing take profit feature comes into play after take profit 2 or take profit 3, depending on the number of take profits selected in the settings. The trailing take profit is always activated on the final take profit when 2 or more take profits are chosen.

The backtest also offers the capability to restrict by a specific date range, allowing for simulated forward testing based on past data. Additionally, users have the option to display or hide a trading panel that provides relevant information about the backtest, statistics, and the current trade. It is also possible to activate alerts and toggle sections of the trading panel on or off. On the chart, historical take profit and stop loss levels are represented by horizontal lines overlaid for reference.

This backtest also includes an optional GKD-E Exit indicator that can be used to test early exits.

The GKD system utilizes volatility-based take profits and stop losses. Each take profit and stop loss is calculated as a multiple of volatility. You can change the values of the multipliers in the settings as well.

To utilize this strategy, follow these steps:

1. (Required) Import the value "Input into NEW GKD-BT Backtest" from the GKD-B Baseline indicator into the GKD-BT Baseline Backtest field "Import GKD-B Baseline"

2. (Optional) Import the value "Input into NEW GKD-BT Backtest" from the GKD-E Exit indicator into the GKD-BT Baseline Backtest field "Import GKD-E Exit". You can toggle the Exit on or off using the "Activate GKD-E Exit" option.

Baselines that are compatible with this backtest module:

GKD-B Baseline

GKD-B Stepped Baseline

Volatility Types Included

17 types of volatility are included in this indicator

Close-to-Close

Parkinson

Garman-Klass

Rogers-Satchell

Yang-Zhang

Garman-Klass-Yang-Zhang

Exponential Weighted Moving Average

Standard Deviation of Log Returns

Pseudo GARCH(2,2)

Average True Range

True Range Double

Standard Deviation

Adaptive Deviation

Median Absolute Deviation

Efficiency-Ratio Adaptive ATR

Mean Absolute Deviation

Static Percent

█ Giga Kaleidoscope Modularized Trading System

Core components of an NNFX algorithmic trading strategy

The NNFX algorithm is built on the principles of trend, momentum, and volatility. There are six core components in the NNFX trading algorithm:

1. Volatility - price volatility; e.g., Average True Range, True Range Double, Close-to-Close, etc.

2. Baseline - a moving average to identify price trend

3. Confirmation 1 - a technical indicator used to identify trends

4. Confirmation 2 - a technical indicator used to identify trends

5. Continuation - a technical indicator used to identify trends

6. Volatility/Volume - a technical indicator used to identify volatility/volume breakouts/breakdown

7. Exit - a technical indicator used to determine when a trend is exhausted

8. Metamorphosis - a technical indicator that produces a compound signal from the combination of other GKD indicators*

*(not part of the NNFX algorithm)

What is Volatility in the NNFX trading system?

In the NNFX (No Nonsense Forex) trading system, ATR (Average True Range) is typically used to measure the volatility of an asset. It is used as a part of the system to help determine the appropriate stop loss and take profit levels for a trade. ATR is calculated by taking the average of the true range values over a specified period.

True range is calculated as the maximum of the following values:

-Current high minus the current low

-Absolute value of the current high minus the previous close

-Absolute value of the current low minus the previous close

ATR is a dynamic indicator that changes with changes in volatility. As volatility increases, the value of ATR increases, and as volatility decreases, the value of ATR decreases. By using ATR in NNFX system, traders can adjust their stop loss and take profit levels according to the volatility of the asset being traded. This helps to ensure that the trade is given enough room to move, while also minimizing potential losses.

Other types of volatility include True Range Double (TRD), Close-to-Close, and Garman-Klass

What is a Baseline indicator?

The baseline is essentially a moving average, and is used to determine the overall direction of the market.

The baseline in the NNFX system is used to filter out trades that are not in line with the long-term trend of the market. The baseline is plotted on the chart along with other indicators, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR).

Trades are only taken when the price is in the same direction as the baseline. For example, if the baseline is sloping upwards, only long trades are taken, and if the baseline is sloping downwards, only short trades are taken. This approach helps to ensure that trades are in line with the overall trend of the market, and reduces the risk of entering trades that are likely to fail.

By using a baseline in the NNFX system, traders can have a clear reference point for determining the overall trend of the market, and can make more informed trading decisions. The baseline helps to filter out noise and false signals, and ensures that trades are taken in the direction of the long-term trend.

What is a Confirmation indicator?

Confirmation indicators are technical indicators that are used to confirm the signals generated by primary indicators. Primary indicators are the core indicators used in the NNFX system, such as the Average True Range (ATR), the Moving Average (MA), and the Relative Strength Index (RSI).

The purpose of the confirmation indicators is to reduce false signals and improve the accuracy of the trading system. They are designed to confirm the signals generated by the primary indicators by providing additional information about the strength and direction of the trend.

Some examples of confirmation indicators that may be used in the NNFX system include the Bollinger Bands, the MACD (Moving Average Convergence Divergence), and the MACD Oscillator. These indicators can provide information about the volatility, momentum, and trend strength of the market, and can be used to confirm the signals generated by the primary indicators.

In the NNFX system, confirmation indicators are used in combination with primary indicators and other filters to create a trading system that is robust and reliable. By using multiple indicators to confirm trading signals, the system aims to reduce the risk of false signals and improve the overall profitability of the trades.

What is a Continuation indicator?

In the NNFX (No Nonsense Forex) trading system, a continuation indicator is a technical indicator that is used to confirm a current trend and predict that the trend is likely to continue in the same direction. A continuation indicator is typically used in conjunction with other indicators in the system, such as a baseline indicator, to provide a comprehensive trading strategy.

What is a Volatility/Volume indicator?

Volume indicators, such as the On Balance Volume (OBV), the Chaikin Money Flow (CMF), or the Volume Price Trend (VPT), are used to measure the amount of buying and selling activity in a market. They are based on the trading volume of the market, and can provide information about the strength of the trend. In the NNFX system, volume indicators are used to confirm trading signals generated by the Moving Average and the Relative Strength Index. Volatility indicators include Average Direction Index, Waddah Attar, and Volatility Ratio. In the NNFX trading system, volatility is a proxy for volume and vice versa.

By using volume indicators as confirmation tools, the NNFX trading system aims to reduce the risk of false signals and improve the overall profitability of trades. These indicators can provide additional information about the market that is not captured by the primary indicators, and can help traders to make more informed trading decisions. In addition, volume indicators can be used to identify potential changes in market trends and to confirm the strength of price movements.

What is an Exit indicator?

The exit indicator is used in conjunction with other indicators in the system, such as the Moving Average (MA), the Relative Strength Index (RSI), and the Average True Range (ATR), to provide a comprehensive trading strategy.

The exit indicator in the NNFX system can be any technical indicator that is deemed effective at identifying optimal exit points. Examples of exit indicators that are commonly used include the Parabolic SAR, the Average Directional Index (ADX), and the Chandelier Exit.

The purpose of the exit indicator is to identify when a trend is likely to reverse or when the market conditions have changed, signaling the need to exit a trade. By using an exit indicator, traders can manage their risk and prevent significant losses.

In the NNFX system, the exit indicator is used in conjunction with a stop loss and a take profit order to maximize profits and minimize losses. The stop loss order is used to limit the amount of loss that can be incurred if the trade goes against the trader, while the take profit order is used to lock in profits when the trade is moving in the trader's favor.

Overall, the use of an exit indicator in the NNFX trading system is an important component of a comprehensive trading strategy. It allows traders to manage their risk effectively and improve the profitability of their trades by exiting at the right time.

What is an Metamorphosis indicator?

The concept of a metamorphosis indicator involves the integration of two or more GKD indicators to generate a compound signal. This is achieved by evaluating the accuracy of each indicator and selecting the signal from the indicator with the highest accuracy. As an illustration, let's consider a scenario where we calculate the accuracy of 10 indicators and choose the signal from the indicator that demonstrates the highest accuracy.

The resulting output from the metamorphosis indicator can then be utilized in a GKD-BT backtest by occupying a slot that aligns with the purpose of the metamorphosis indicator. The slot can be a GKD-B, GKD-C, or GKD-E slot, depending on the specific requirements and objectives of the indicator. This allows for seamless integration and utilization of the compound signal within the GKD-BT framework.

How does Loxx's GKD (Giga Kaleidoscope Modularized Trading System) implement the NNFX algorithm outlined above?

Loxx's GKD v2.0 system has five types of modules (indicators/strategies). These modules are:

1. GKD-BT - Backtesting module (Volatility, Number 1 in the NNFX algorithm)

2. GKD-B - Baseline module (Baseline and Volatility/Volume, Numbers 1 and 2 in the NNFX algorithm)

3. GKD-C - Confirmation 1/2 and Continuation module (Confirmation 1/2 and Continuation, Numbers 3, 4, and 5 in the NNFX algorithm)

4. GKD-V - Volatility/Volume module (Confirmation 1/2, Number 6 in the NNFX algorithm)

5. GKD-E - Exit module (Exit, Number 7 in the NNFX algorithm)

6. GKD-M - Metamorphosis module (Metamorphosis, Number 8 in the NNFX algorithm, but not part of the NNFX algorithm)

(additional module types will added in future releases)

Each module interacts with every module by passing data to A backtest module wherein the various components of the GKD system are combined to create a trading signal.

That is, the Baseline indicator passes its data to Volatility/Volume. The Volatility/Volume indicator passes its values to the Confirmation 1 indicator. The Confirmation 1 indicator passes its values to the Confirmation 2 indicator. The Confirmation 2 indicator passes its values to the Continuation indicator. The Continuation indicator passes its values to the Exit indicator, and finally, the Exit indicator passes its values to the Backtest strategy.

This chaining of indicators requires that each module conform to Loxx's GKD protocol, therefore allowing for the testing of every possible combination of technical indicators that make up the six components of the NNFX algorithm.

What does the application of the GKD trading system look like?

Example trading system:

Backtest: GKD-BT Baseline Backtest as shown on the chart above

Baseline: Hull Moving Average as shown on the chart above

Volatility/Volume: Hurst Exponent

Confirmation 1: Sherif's HiLo

Confirmation 2: uf2018

Continuation: Coppock Curve

Exit: Fisher Transform as shown on the chart above

Metamorphosis: Baseline Optimizer

Each GKD indicator is denoted with a module identifier of either: GKD-BT, GKD-B, GKD-C, GKD-V, GKD-M, or GKD-E. This allows traders to understand to which module each indicator belongs and where each indicator fits into the GKD system.

█ Giga Kaleidoscope Modularized Trading System Signals

Standard Entry

1. GKD-C Confirmation gives signal

2. Baseline agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

1-Candle Standard Entry

1a. GKD-C Confirmation gives signal

2a. Baseline agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Baseline Entry

1. GKD-B Baseline gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Volatility/Volume agrees

7. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

1-Candle Baseline Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSBC Bars Back' prior

Next Candle

1b. Price retraced

2b. Baseline agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Volatility/Volume Entry

1. GKD-V Volatility/Volume gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Confirmation 2 agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Volatility/Volume Entry

1a. GKD-V Volatility/Volume gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSVVC Bars Back' prior

Next Candle

1b. Price retraced

2b. Volatility/Volume agrees

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Baseline agrees

Confirmation 2 Entry

1. GKD-C Confirmation 2 gives signal

2. Confirmation 1 agrees

3. Price inside Goldie Locks Zone Minimum

4. Price inside Goldie Locks Zone Maximum

5. Volatility/Volume agrees

6. Baseline agrees

7. Confirmation 1 signal was less than 7 candles prior

1-Candle Confirmation 2 Entry

1a. GKD-C Confirmation 2 gives signal

2a. Confirmation 1 agrees

3a. Price inside Goldie Locks Zone Minimum

4a. Price inside Goldie Locks Zone Maximum

5a. Confirmation 1 signal was less than 'Maximum Allowable PSC2C Bars Back' prior

Next Candle

1b. Price retraced

2b. Confirmation 2 agrees

3b. Confirmation 1 agrees

4b. Volatility/Volume agrees

5b. Baseline agrees

PullBack Entry

1a. GKD-B Baseline gives signal

2a. Confirmation 1 agrees

3a. Price is beyond 1.0x Volatility of Baseline

Next Candle

1b. Price inside Goldie Locks Zone Minimum

2b. Price inside Goldie Locks Zone Maximum

3b. Confirmation 1 agrees

4b. Confirmation 2 agrees

5b. Volatility/Volume agrees

Continuation Entry

1. Standard Entry, 1-Candle Standard Entry, Baseline Entry, 1-Candle Baseline Entry, Volatility/Volume Entry, 1-Candle Volatility/Volume Entry, Confirmation 2 Entry, 1-Candle Confirmation 2 Entry, or Pullback entry triggered previously

2. Baseline hasn't crossed since entry signal trigger

4. Confirmation 1 agrees

5. Baseline agrees

6. Confirmation 2 agrees

GKD-BT Giga Confirmation Stack Backtest [Loxx]Giga Kaleidoscope GKD-BT Giga Confirmation Stack Backtest is a Backtesting module included in Loxx's "Giga Kaleidoscope Modularized Trading System".

█ GKD-BT Giga Confirmation Stack Backtest

The Giga Confirmation Stack Backtest module allows users to perform backtesting on Long and Short signals from the confluence between GKD-C Confirmation 1 and GKD-C Confirmation 2 indicators. This module encompasses two types of backtests: Trading and Full. The Trading backtest permits users to evaluate individual trades, whether Long or Short, one at a time. Conversely, the Full backtest allows users to analyze either Longs or Shorts separately by toggling between them in the settings, enabling the examination of results for each signal type. The Trading backtest emulates actual trading conditions, while the Full backtest assesses all signals, regardless of being Long or Short.

Additionally, this backtest module provides the option to test using indicators with 1 to 3 take profits and 1 stop loss. The Trading backtest allows for the use of 1 to 3 take profits, while the Full backtest is limited to 1 take profit. The Trading backtest also offers the capability to apply a trailing take profit.

In terms of the percentage of trade removed at each take profit, this backtest module has the following hardcoded values:

Take profit 1: 50% of the trade is removed.

Take profit 2: 25% of the trade is removed.

Take profit 3: 25% of the trade is removed.

Stop loss: 100% of the trade is removed.

After each take profit is achieved, the stop loss level is adjusted. When take profit 1 is reached, the stop loss is moved to the entry point. Similarly, when take profit 2 is reached, the stop loss is shifted to take profit 1. The trailing take profit feature comes into play after take profit 2 or take profit 3, depending on the number of take profits selected in the settings. The trailing take profit is always activated on the final take profit when 2 or more take profits are chosen.

The backtest module also offers the capability to restrict by a specific date range, allowing for simulated forward testing based on past data. Additionally, users have the option to display or hide a trading panel that provides relevant information about the backtest, statistics, and the current trade. It is also possible to activate alerts and toggle sections of the trading panel on or off. On the chart, historical take profit and stop loss levels are represented by horizontal lines overlaid for reference.

To utilize this strategy, follow these steps:

1. Adjust the "Confirmation Type" in the GKD-C Confirmation 1 Indicator to "GKD New."

2. GKD-C Confirmation 1 Import: Import the value "Input into NEW GKD-BT Backtest" from the GKD-C Confirmation 1 module into the GKD-BT Giga Confirmation Stack Backtest module setting named "Import GKD-C Confirmation 1."

3. Adjust the "Confirmation Type" in the GKD-C Confirmation 2 Indicator to "GKD New."

4. GKD-C Confirmation 2 Import: Import the value "Input into NEW GKD-BT Backtest" from the GKD-C Confirmation 2 module into the GKD-BT Giga Confirmation Stack Backtest module setting named "Import GKD-C Confirmation 2."

█ Giga Confirmation Stack Backtest Entries

Entries are generated from the confluence of a GKD-C Confirmation 1 and GKD-C Confirmation 2 indicators. The Confirmation 1 gives the signal and the Confirmation 2 indicator filters or "approves" the the Confirmation 1 signal. If Confirmation 1 gives a long signal and Confirmation 2 shows a downtrend, then the long signal is rejected. If Confirmation 1 gives a long signal and Confirmation 2 shows an uptrend, then the long signal is approved and sent to the backtest execution engine.

█ Volatility Types Included

The GKD system utilizes volatility-based take profits and stop losses. Each take profit and stop loss is calculated as a multiple of volatility. Users can also adjust the multiplier values in the settings.

This module includes 17 types of volatility:

Close-to-Close

Parkinson

Garman-Klass

Rogers-Satchell

Yang-Zhang

Garman-Klass-Yang-Zhang

Exponential Weighted Moving Average

Standard Deviation of Log Returns

Pseudo GARCH(2,2)

Average True Range

True Range Double

Standard Deviation

Adaptive Deviation

Median Absolute Deviation

Efficiency-Ratio Adaptive ATR

Mean Absolute Deviation

Static Percent

Close-to-Close

Close-to-Close volatility is a classic and widely used volatility measure, sometimes referred to as historical volatility.

Volatility is an indicator of the speed of a stock price change. A stock with high volatility is one where the price changes rapidly and with a larger amplitude. The more volatile a stock is, the riskier it is.

Close-to-close historical volatility is calculated using only a stock's closing prices. It is the simplest volatility estimator. However, in many cases, it is not precise enough. Stock prices could jump significantly during a trading session and return to the opening value at the end. That means that a considerable amount of price information is not taken into account by close-to-close volatility.

Despite its drawbacks, Close-to-Close volatility is still useful in cases where the instrument doesn't have intraday prices. For example, mutual funds calculate their net asset values daily or weekly, and thus their prices are not suitable for more sophisticated volatility estimators.

Parkinson

Parkinson volatility is a volatility measure that uses the stock’s high and low price of the day.

The main difference between regular volatility and Parkinson volatility is that the latter uses high and low prices for a day, rather than only the closing price. This is useful as close-to-close prices could show little difference while large price movements could have occurred during the day. Thus, Parkinson's volatility is considered more precise and requires less data for calculation than close-to-close volatility.

One drawback of this estimator is that it doesn't take into account price movements after the market closes. Hence, it systematically undervalues volatility. This drawback is addressed in the Garman-Klass volatility estimator.

Garman-Klass

Garman-Klass is a volatility estimator that incorporates open, low, high, and close prices of a security.

Garman-Klass volatility extends Parkinson's volatility by taking into account the opening and closing prices. As markets are most active during the opening and closing of a trading session, it makes volatility estimation more accurate.

Garman and Klass also assumed that the process of price change follows a continuous diffusion process (Geometric Brownian motion). However, this assumption has several drawbacks. The method is not robust for opening jumps in price and trend movements.

Despite its drawbacks, the Garman-Klass estimator is still more effective than the basic formula since it takes into account not only the price at the beginning and end of the time interval but also intraday price extremes.

Researchers Rogers and Satchell have proposed a more efficient method for assessing historical volatility that takes into account price trends. See Rogers-Satchell Volatility for more detail.

Rogers-Satchell

Rogers-Satchell is an estimator for measuring the volatility of securities with an average return not equal to zero.