Cyatophilum Scalping Bot V2 [BACKTEST]Improved version of Cyatophilum Scalping Bot

Default settings for BITMEX:XBTUSD

2% stop loss

2% trailing take profit

Cari dalam skrip untuk "backtest"

Combo Backtest 123 Reversal & Breakout Range Short This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Breakout Range Short Strategy

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Bill Williams. AO with Signal Line This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator plots the oscillator as a histogram where blue denotes

periods suited for buying and red . for selling. If the current value

of AO (Awesome Oscillator) is above previous, the period is considered

suited for buying and the period is marked blue. If the AO value is not

above previous, the period is considered suited for selling and the

indicator marks it as red.

You can make changes in the property for set calculating strategy MA, EMA, WMA

WARNING:

- For purpose educate only

- This script to change bars colors.

Cyatophilum PSAR Bot Trader V2 [BACKTEST]A strategy built upon Parabolic Stop And Reverse.

This new version includes my whole Trend Detector / Stop Loss / Takeprofit / Trailing System.

RePaNoCHa [Backtest]This is a very long script and adjusting the settings can be a bit slow so I share some settings. (these may be even better)

It has no security() and no Heikin Ashi so no repaint and Backtest is real.

It's important to adjust correctly the tics/pips correction.

All timeframes but good results at 2H

Default settings for ETHUSD (BITMEX) 2H

Alerts version coming soon...

Enjoy!!!

"Este script es la repanocha"

XBTUSD (BITMEX)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 8

T3 Volume Factor = 0.9

Range Filter+ADX == true

Sampling Period = 16

Range Multiplier = 1.3

Flat Market Trades == true

ADX lenght = 10

ADX Threshold = 20

Parabolic SAR == true

SAR start = 0.03

SAR inc = 0.02

SAR max = 0.3

Pyramiding = 15

Trailing Stop Activation % = 0.5

Trailing Stop Offset % (when profit=0.5 %) = 0.2

Trailing Stop Offset % (when profit=10 %) = 1.2

Stop Loss = 3.2

Tics/Pips Correction = 10

Initial Capital = 1000

Quantity = 100 %

Commission value = 0.075 %

ETHUSD (BITMEX)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 6

T3 Volume Factor = 0.7

Range Filter+ADX == true

Sampling Period = 10

Range Multiplier = 0.9

Flat Market Trades == true

ADX lenght = 11

ADX Threshold = 19

Parabolic SAR == true

SAR start = 0.06

SAR inc = 0.07

SAR max = 0.15

Pyramiding = 15

Trailing Stop Activation % = 0.5

Trailing Stop Offset % (when profit=0.5 %) = 0.25

Trailing Stop Offset % (when profit=10 %) = 1.5

Stop Loss = 3.2

Tics/Pips Correction = 100

Initial Capital = 1000

Quantity = 100 %

Commission value = 0.075 %

BNBUSDT (BINANCE)

Timeframe = 2H

Position Side = LONG

Source = hlc3

T3 == true

T3 Length = 6

T3 Volume Factor = 0.7

Range Filter+ADX == true

Sampling Period = 17

Range Multiplier = 1.3

Flat Market Trades == true

ADX lenght = 5

ADX Threshold = 18

Parabolic SAR == true

SAR start = 0.04

SAR inc = 0.03

SAR max = 0.25

Pyramiding = 15

Trailing Stop Activation % = 0.5

Trailing Stop Offset % (when profit=0.5 %) = 0.25

Trailing Stop Offset % (when profit=10 %) = 1.5

Stop Loss == false

Tics/Pips Correction = 10000

Initial Capital = 1000

Quantity = 100 %

Commission value = 0.075 %

LTCUSDT (BINANCE)

Timeframe = 2H

Position Side = LONG

Source = hlc3

T3 == true

T3 Length = 3

T3 Volume Factor = 1

Range Filter+ADX == true

Sampling Period = 11

Range Multiplier = 1.1

Flat Market Trades == true

ADX lenght = 6

ADX Threshold = 22

Parabolic SAR == true

SAR start = 0.07

SAR inc = 0.04

SAR max = 0.15

Pyramiding = 15

Trailing Stop Activation % = 0.5

Trailing Stop Offset % (when profit=0.5 %) = 0.25

Trailing Stop Offset % (when profit=10 %) = 1.5

Stop Loss == false

Tics/Pips Correction = 100

Initial Capital = 1000

Quantity = 100 %

Commission value = 0.075 %

TRXUSDT (BINANCE)

Timeframe = 2H

Position Side = LONG

Source = hlc3

T3 == true

T3 Length = 7

T3 Volume Factor = 1

Range Filter+ADX == true

Sampling Period = 8

Range Multiplier = 1.1

Flat Market Trades == true

ADX lenght = 4

ADX Threshold = 22

Parabolic SAR == true

SAR start = 0.07

SAR inc = 0.04

SAR max = 0.15

Pyramiding = 15

Trailing Stop Activation % = 0.5

Trailing Stop Offset % (when profit=0.5 %) = 0.25

Trailing Stop Offset % (when profit=10 %) = 1.5

Stop Loss == false

Tics/Pips Correction = 100000

Initial Capital = 1000

Quantity = 100 %

Commission value = 0.075 %

NAS100 (OANDA)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 3

T3 Volume Factor = 1

Range Filter+ADX == true

Sampling Period = 12

Range Multiplier = 1.3

Flat Market Trades == true

ADX lenght = 18

ADX Threshold = 21

Parabolic SAR == true

SAR start = 0.08

SAR inc = 0.06

SAR max = 0.25

Pyramiding = 15

Trailing Stop Activation % = 0.2

Trailing Stop Offset % (when profit=0.5 %) = 0.15

Trailing Stop Offset % (when profit=10 %) = 1

Stop Loss == false

Tics/Pips Correction = 10

Initial Capital = 1000

Quantity = 3 contracts

Commission value = 0.2 USD per contract

NATGAS(OANDA)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 3

T3 Volume Factor = 1

Range Filter+ADX == true

Sampling Period = 15

Range Multiplier = 1.3

Flat Market Trades == true

ADX lenght = 12

ADX Threshold = 21

Parabolic SAR == true

SAR start = 0.08

SAR inc = 0.06

SAR max = 0.4

Pyramiding = 15

Trailing Stop Activation % = 0.2

Trailing Stop Offset % (when profit=0.5 %) = 0.15

Trailing Stop Offset % (when profit=10 %) = 1

Stop Loss == false

Tics/Pips Correction = 1000

Initial Capital = 1000

Quantity = 4500 contracts

Commission value = 0.002 USD per contract

SPX500 (OANDA)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 4

T3 Volume Factor = 0.8

Range Filter+ADX == true

Sampling Period = 14

Range Multiplier = 1.3

Flat Market Trades == true

ADX lenght = 12

ADX Threshold = 17

Parabolic SAR == true

SAR start = 0.09

SAR inc = 0.04

SAR max = 0.2

Pyramiding = 15

Trailing Stop Activation % = 0.15

Trailing Stop Offset % (when profit=0.5 %) = 0.1

Trailing Stop Offset % (when profit=10 %) = 0.5

Stop Loss = 1.5

Tics/Pips Correction = 10

Initial Capital = 1000

Quantity = 8 contracts

Commission value = 0.2 USD per contract

US30 (OANDA)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 4

T3 Volume Factor = 0.9

Range Filter+ADX == true

Sampling Period = 11

Range Multiplier = 1.1

Flat Market Trades == true

ADX lenght = 16

ADX Threshold = 24

Parabolic SAR == true

SAR start = 0.08

SAR inc = 0.03

SAR max = 0.05

Pyramiding = 15

Trailing Stop Activation % = 0.15

Trailing Stop Offset % (when profit=0.5 %) = 0.075

Trailing Stop Offset % (when profit=10 %) = 0.5

Stop Loss = 1.5

Tics/Pips Correction = 10

Initial Capital = 1000

Quantity = 1 contracts

Commission value = 1.5 USD per contract

WHEAT (OANDA)

Timeframe = 2H

Position Side = BOTH

Source = hlc3

T3 == true

T3 Length = 3

T3 Volume Factor = 1.1

Range Filter+ADX == true

Sampling Period = 12

Range Multiplier = 0.9

Flat Market Trades == true

ADX lenght = 13

ADX Threshold = 21

Parabolic SAR == true

SAR start = 0.1

SAR inc = 0.05

SAR max = 0.15

Pyramiding = 15

Trailing Stop Activation % = 0.2

Trailing Stop Offset % (when profit=0.5 %) = 0.1

Trailing Stop Offset % (when profit=10 %) = 1

Stop Loss = 2.5

Tics/Pips Correction = 1000

Initial Capital = 1000

Quantity = 2500 contracts

Commission value = 0.003 USD per contract

Bitcoin FREE BACKTEST Version BTCUSD 5m BITFINEXA strategy for trading BTC/USD in 5m timeframe.

The strategy includes long and short trades.

You can find the Alert Setup version below.

Commodity Selection Index Backtest The Commodity Selection Index ("CSI") is a momentum indicator. It was

developed by Welles Wilder and is presented in his book New Concepts in

Technical Trading Systems. The name of the index reflects its primary purpose.

That is, to help select commodities suitable for short-term trading.

A high CSI rating indicates that the commodity has strong trending and volatility

characteristics. The trending characteristics are brought out by the Directional

Movement factor in the calculation--the volatility characteristic by the Average

True Range factor.

Wilder's approach is to trade commodities with high CSI values (relative to other

commodities). Because these commodities are highly volatile, they have the potential

to make the "most money in the shortest period of time." High CSI values imply

trending characteristics which make it easier to trade the security.

The Commodity Selection Index is designed for short-term traders who can handle

the risks associated with highly volatile markets.

WARNING:

- For purpose educate only

- This script to change bars colors.

Three Outside Down Backtest This is a three candlestick bearish reversal pattern consisting of a bearish

engulfing pattern formed by the first two candlesticks then followed by a down

candlestick with a lower close than the prior candlestick.

WARNING:

- For purpose educate only

- This script to change bars colors.

Adaptive Zero Lag EMA v2 (Strategy w/ Backtest Date Range)This is a modified strategy including Date Range Selection for dasanc's incredible "Adaptive Zero Lag EMA v2":

The Original:

ALMA TEMA Base with Backtest Range & EWO Filter (With Inputs)ALMA TEMA Base with Backtest Range & EWO Filter (With Inputs)

ICOM ALMA TEMA Base with Backtest Range & EWO FilterICOM ALMA TEMA Base with Backtest Range & EWO Filter

Cyatophilum Ichimoku Small TimeFrames [BACKTEST]A script for daytraders trading small timeframes.

Currently in developpement.

If you want to try it send me a PM, and give a like to receive updates.

Donchian BacktestExecutes backtest using donchian channels breakout strategy (buy on upper breakout / sell on lower breakout)

Donchian period can be customized differenly for upper and lower channels

Bearish Harami Backtest This is a bearish reversal pattern formed by two candlesticks in which a short

real body is contained within the prior session's long real body. Usually the

second real body is the opposite color of the first real body. The Harami pattern

is the reverse of the Engulfing pattern.

WARNING:

- For purpose educate only

- This script to change bars colors.

HATbot v1 Automation Script and Indicator [Backtest]This is the debut release of HATbot.

HATbot is a terrible name for a new trend following indicator and strategy script.

Backtest window: 2018-01-01 to 2019-01-01.

Initial capital: $1000

Shorting: enabled

HMA EABy default, the strategy works best on 1h timeframe. In theory, it should run well on any timeframe, but you will absolutely need to adjust the Hull Resolution. I recommend starting with 4x the current view (aka, if you are using 5m candles, set the resolution to 20min, which is 4 * 5m).

The settings are pretty self explanatory:

Start Month - Month of the year to begin backtest (automatically beings at 1st of month)

Risk Per Trade (%) - How much of your equity to risk on each trade.

Leverage - Amount of buying power/Margin you have available

Loss (pips) - Distance in pips from the entry to place Stop Loss

Profit (pips) - Distance in pips from entry to place target Take Profit

Trigger Trail (%) - Distance in percentage from entry to begin a trailing Stop Loss

Trail Dist. (pips) - Offset distance of trailing Stop Loss

Hull Res. (min) - Length of candle in minutes to use when calculating the HMA

Hull Period (bars) - Smoothing period for HMA

Bullish Engulfing Backtest This is a bullish reversal pattern formed by two candlesticks. Following a downtrend,

the first candlestick is a down candlestick which is followed by an up candlestick

which has a long real body that engulfs or contains the real body of the prior bar.

The Engulfing pattern is the reverse of the Harami pattern.

WARNING:

- For purpose educate only

- This script to change bars colors.

Bearish Engulfing Backtest This is a bearish candlestick reversal pattern formed by two candlesticks.

Following an uptrend, the first candlestick is a up candlestick which is

followed by a down candlestick which has a long real body that engulfs or

contains the real body of the prior bar. The Engulfing pattern is the reverse

of the Harami pattern.

WARNING:

- For purpose educate only

- This script to change bars colors.

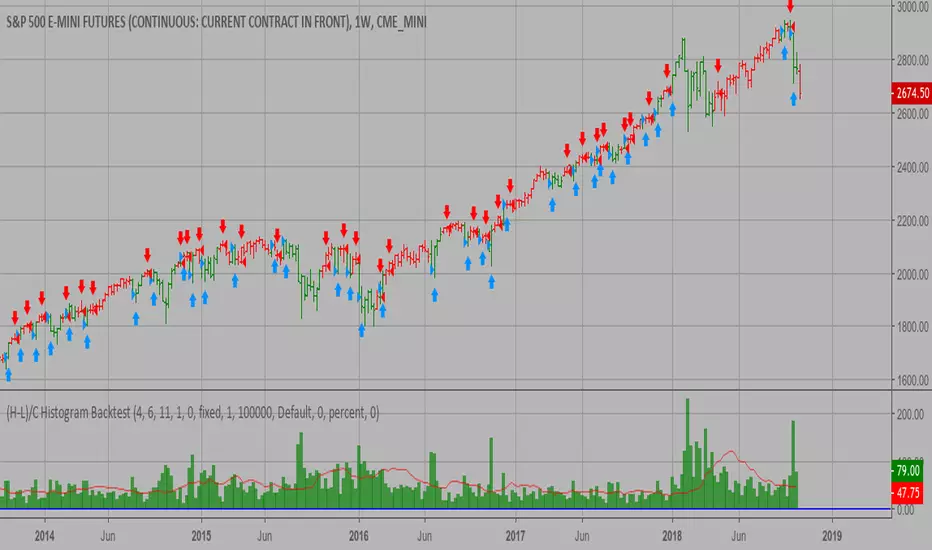

(H-L)/C Histogram Backtest This histogram displays (high-low)/close

Can be applied to any time frame.

WARNING:

- For purpose educate only

- This script to change bars colors.

CMO & WMA Backtest ver 2.0 This indicator plots Chandre Momentum Oscillator and its WMA on the

same chart. This indicator plots the absolute value of CMO.

The CMO is closely related to, yet unique from, other momentum oriented

indicators such as Relative Strength Index, Stochastic, Rate-of-Change,

etc. It is most closely related to Welles Wilder?s RSI, yet it differs

in several ways:

- It uses data for both up days and down days in the numerator, thereby

directly measuring momentum;

- The calculations are applied on unsmoothed data. Therefore, short-term

extreme movements in price are not hidden. Once calculated, smoothing

can be applied to the CMO, if desired;

- The scale is bounded between +100 and -100, thereby allowing you to clearly

see changes in net momentum using the 0 level. The bounded scale also allows

you to conveniently compare values across different securities.