Bitcoin Events HistoryWith this tool, you can travel back to Bitcoin’s very first price quote and retrace its entire history directly on your chart. Major events are plotted as labels or markers, providing context for how significant moments shaped Bitcoin’s journey.

Key Features

Comprehensive Event Coverage: From Bitcoin’s inception to the most recent updates.

Custom View: Change label colors, styles, sizes, and fonts using the script’s settings.

Regular Updates: New events are added regularly to keep the history current.

Replay History

Use Bar Replay Mode to step through Bitcoin’s price history and see events unfold in sequence.

Follow the on-screen instructions for a more immersive experience.

Community Contributions

If you notice a significant event missing or misplaced on a particular date, feel free to leave a comment! Your suggestions will be considered for the next update.

To all Bitcoin enthusiasts, traders, and anyone eager to explore the history of cryptocurrency from its inception, I hope you enjoy this indicator :)

Cari dalam skrip untuk "bitcoin"

Bitcoin Logarithmic Growth Curve 2024The Bitcoin logarithmic growth curve is a concept used to analyze Bitcoin's price movements over time. The idea is based on the observation that Bitcoin's price tends to grow exponentially, particularly during bull markets. It attempts to give a long-term perspective on the Bitcoin price movements.

The curve includes an upper and lower band. These bands often represent zones where Bitcoin's price is overextended (upper band) or undervalued (lower band) relative to its historical growth trajectory. When the price touches or exceeds the upper band, it may indicate a speculative bubble, while prices near the lower band may suggest a buying opportunity.

Unlike most Bitcoin growth curve indicators, this one includes a logarithmic growth curve optimized using the latest 2024 price data, making it, in our view, superior to previous models. Additionally, it features statistical confidence intervals derived from linear regression, compatible across all timeframes, and extrapolates the data far into the future. Finally, this model allows users the flexibility to manually adjust the function parameters to suit their preferences.

The Bitcoin logarithmic growth curve has the following function:

y = 10^(a * log10(x) - b)

In the context of this formula, the y value represents the Bitcoin price, while the x value corresponds to the time, specifically indicated by the weekly bar number on the chart.

How is it made (You can skip this section if you’re not a fan of math):

To optimize the fit of this function and determine the optimal values of a and b, the previous weekly cycle peak values were analyzed. The corresponding x and y values were recorded as follows:

113, 18.55

240, 1004.42

451, 19128.27

655, 65502.47

The same process was applied to the bear market low values:

103, 2.48

267, 211.03

471, 3192.87

676, 16255.15

Next, these values were converted to their linear form by applying the base-10 logarithm. This transformation allows the function to be expressed in a linear state: y = a * x − b. This step is essential for enabling linear regression on these values.

For the cycle peak (x,y) values:

2.053, 1.268

2.380, 3.002

2.654, 4.282

2.816, 4.816

And for the bear market low (x,y) values:

2.013, 0.394

2.427, 2.324

2.673, 3.504

2.830, 4.211

Next, linear regression was performed on both these datasets. (Numerous tools are available online for linear regression calculations, making manual computations unnecessary).

Linear regression is a method used to find a straight line that best represents the relationship between two variables. It looks at how changes in one variable affect another and tries to predict values based on that relationship.

The goal is to minimize the differences between the actual data points and the points predicted by the line. Essentially, it aims to optimize for the highest R-Square value.

Below are the results:

It is important to note that both the slope (a-value) and the y-intercept (b-value) have associated standard errors. These standard errors can be used to calculate confidence intervals by multiplying them by the t-values (two degrees of freedom) from the linear regression.

These t-values can be found in a t-distribution table. For the top cycle confidence intervals, we used t10% (0.133), t25% (0.323), and t33% (0.414). For the bottom cycle confidence intervals, the t-values used were t10% (0.133), t25% (0.323), t33% (0.414), t50% (0.765), and t67% (1.063).

The final bull cycle function is:

y = 10^(4.058 ± 0.133 * log10(x) – 6.44 ± 0.324)

The final bear cycle function is:

y = 10^(4.684 ± 0.025 * log10(x) – -9.034 ± 0.063)

The main Criticisms of growth curve models:

The Bitcoin logarithmic growth curve model faces several general criticisms that we’d like to highlight briefly. The most significant, in our view, is its heavy reliance on past price data, which may not accurately forecast future trends. For instance, previous growth curve models from 2020 on TradingView were overly optimistic in predicting the last cycle’s peak.

This is why we aimed to present our process for deriving the final functions in a transparent, step-by-step scientific manner, including statistical confidence intervals. It's important to note that the bull cycle function is less reliable than the bear cycle function, as the top band is significantly wider than the bottom band.

Even so, we still believe that the Bitcoin logarithmic growth curve presented in this script is overly optimistic since it goes parly against the concept of diminishing returns which we discussed in this post:

This is why we also propose alternative parameter settings that align more closely with the theory of diminishing returns.

Our recommendations:

Drawing on the concept of diminishing returns, we propose alternative settings for this model that we believe provide a more realistic forecast aligned with this theory. The adjusted parameters apply only to the top band: a-value: 3.637 ± 0.2343 and b-parameter: -5.369 ± 0.6264. However, please note that these values are highly subjective, and you should be aware of the model's limitations.

Conservative bull cycle model:

y = 10^(3.637 ± 0.2343 * log10(x) - 5.369 ± 0.6264)

Bitcoin Regression Price BoundariesTLDR

DCA into BTC at or below the blue line. DCA out of BTC when price approaches the red line. There's a setting to toggle the future extrapolation off/on.

INTRODUCTION

Regression analysis is a fundamental and powerful data science tool, when applied CORRECTLY . All Bitcoin regressions I've seen (Rainbow Log, Stock-to-flow, and non-linear models), have glaring flaws ... Namely, that they have huge drift from one cycle to the next.

Presented here, is a canonical application of this statistical tool. "Canonical" meaning that any trained analyst applying the established methodology, would arrive at the same result. We model 3 lines:

Upper price boundary (red) - Predicted the April 2021 top to within 1%

Lower price boundary (green)- Predicted the Dec 2022 bottom within 10%

Non-bubble best fit line (blue) - Last update was performed on Feb 28 2024.

NOTE: The red/green lines were calculated using solely data from BEFORE 2021.

"I'M INTRUIGED, BUT WHAT EXACTLY IS REGRESSION ANALYSIS?"

Quite simply, it attempts to draw a best-fit line over some set of data. As you can imagine, there are endless forms of equations that we might try. So we need objective means of determining which equations are better than others. This is where statistical rigor is crucial.

We check p-values to ensure that a proposed model is better than chance. When comparing two different equations, we check R-squared and Residual Standard Error, to determine which equation is modeling the data better. We check residuals to ensure the equation is sufficiently complex to model all the available signal. We check adjusted R-squared to ensure the equation is not *overly* complex and merely modeling random noise.

While most people probably won't entirely understand the above paragraph, there's enough key terminology in for the intellectually curious to research.

DIVING DEEPER INTO THE 3 REGRESSION LINES ABOVE

WARNING! THIS IS TECHNICAL, AND VERY ABBREVIATED

We prefer a linear regression, as the statistical checks it allows are convenient and powerful. However, the BTCUSD dataset is decidedly non-linear. Thus, we must log transform both the x-axis and y-axis. At the end of this process, we'll use e^ to transform back to natural scale.

Plotting the log transformed data reveals a crucial visual insight. The best fit line for the blowoff tops is different than for the lower price boundary. This is why other models have failed. They attempt to model ALL the data with just one equation. This causes drift in both the upper and lower boundaries. Here we calculate these boundaries as separate equations.

Upper Boundary (in red) = e^(3.24*ln(x)-15.8)

Lower Boundary (green) = e^(0.602*ln^2(x) - 4.78*ln(x) + 7.17)

Non-Bubble best fit (blue) = e^(0.633*ln^2(x) - 5.09*ln(x) +8.12)

* (x) = The number of days since July 18 2010

Anyone familiar with Bitcoin, knows it goes in cycles where price goes stratospheric, typically measured in months; and then a lengthy cool-off period measured in years. The non-bubble best fit line methodically removes the extreme upward deviations until the residuals have the closest statistical semblance to normal data (bell curve shaped data).

Whereas the upper/lower boundary only gets re-calculated in hindsight (well after a blowoff or capitulation occur), the Non-Bubble line changes ever so slightly with each new datapoint. The last update to this line was made on Feb 28, 2024.

ENOUGH NERD TALK! HOW CAN I APPLY THIS?

In the simplest terms, anything below the blue line is a statistical buying opportunity. The closer you approach the green line (the lower boundary) the more statistically strong that opportunity is. As price approaches the red line, is a growing statistical likelyhood/danger of an imminent blowoff top.

So a wise trader would DCA (dollar cost average) into Bitcoin below the blue line; and would DCA out of Bitcoin as it approaches the red line. Historically, you may or may not have a large time-window during points of maximum opportunity. So be vigilant! Anything within 10-20% of the boundary should be regarded as extreme opportunity.

Note: You can toggle the future extrapolation of these lines in the settings (default on).

CLOSING REMARKS

Keep in mind this is a pure statistical analysis. It's likely that this model is probing a complex, real economic process underlying the Bitcoin price. Statistical models like this are most accurate during steady state conditions, where the prevailing fundamentals are stable. (The astute observer will note, that the regression boundaries held despite the economic disruption of 2020).

Thus, it cannot be understated: Should some drastic fundamental change occur in the underlying economic landscape of cryptocurrency, Bitcoin itself, or the broader economy, this model could drastically deviate, and become significantly less accurate.

Furthermore, the upper/lower boundaries cross in the year 2037. THIS MODEL WILL EVENTUALLY BREAK DOWN. But for now, given that Bitcoin price moves on the order of 2000% from bottom to top, it's truly remarkable that, using SOLELY pre-2021 data, this model was able to nail the top/bottom within 10%.

Bitcoin Pi Cycle Top Indicator - Daily Timeframe Only1 Day Timeframe Only

The Bitcoin Pi Cycle Top Indicator has garnered attention for its historical effectiveness in identifying the timing of Bitcoin's market cycle peaks with remarkable precision, typically within a margin of 3 days.

It utilizes a specific combination of moving averages—the 111-day moving average and a 2x multiple of the 350-day moving average—to signal potential tops in the Bitcoin market.

The 111-day moving average (MA): This shorter-term MA is chosen to reflect more recent price action and trends within the Bitcoin market.

The 350-day moving average (MA) multiplied by 2: This longer-term MA is adjusted to capture broader market trends and cycles over an extended period.

The key premise behind the Bitcoin Pi Cycle Top Indicator is that a potential market top for Bitcoin can be signaled when the 111-day MA crosses above the 350-day MA (which has been doubled). Historically, this crossover event has shown a remarkable correlation with the peaks of Bitcoin's price cycles, making it a tool of interest for traders and investors aiming to anticipate significant market shifts.

#Bitcoin

Bitcoin Price to Volume per $1 FeeTransaction value to transaction fee:

The Bitcoin network's efficiency, usability and volume scalability has been improving over time and this can be measured by dividing the average transaction volume by the transaction fee.

The indicator give us:

Price to volume per $1 fee = BTC price / (avg tx value / avg tx fee)

A low ratio of "Price to volume per $1 fee" indicates that the Bitcoin network is being used for high volumes in comparison to the Bitcoin price, which means that the network is cost-effective compared to the price. On the other hand, a high "Price to volume per $1 fee" suggests that the average transaction size is smaller than the price of Bitcoin, which means that the network is less cost-effective compared to the Bitcoin price.

Note that the dynamics of transaction fees may change over time as new use cases emerge in the Bitcoin chain. These use cases include L2s such as Stacks, where DeFi applications can run, and Bitcoin Ordinals.

It's worth mentioning that Bitcoin is not only a cost-effective way of transferring value, but also highly energy efficient. Despite receiving criticism for its energy consumption, when we compare its energy usage to other industries (such as banking and gold) and correlate it with the transaction volumes, we can easily conclude that Bitcoin's energy efficiency is remarkable when compared to other methods of transferring value.

Bitcoin Google Trends OverlayThis indicator overlays Bitcoin Google trends data starting from 16/12/2018 until 10/12/2023. To have more recent data, you will need to update the data points manually.

If it is not showing properly, you need to plot the indicator to a new scale. Try also to use a logarithmic scale to better correlate the Bitcoin Google Trends data.

Interpretation:

Google Trends data and the Bitcoin price are very correlated. Google Trends data is a good indicator of market sentiment, but it usually lags.

Bitcoin Correlation MapHello everyone,

This indicator shows the correlation coefficients of altcoins with bitcoin in a table.

What is the correlation coefficient?

The correlation coefficient is a value that takes a value between 0 and 1 when a parity makes similar movements with the reference parity, and takes a value between 0 and -1 when it makes opposite movements.

In order to obtain more meaningful and real-time results in this indicator, the weighted average of the correlation values of the last 200bar was used. You can change the bar length as you wish. With the correlation value, you can see the parities that have similar movements with bitcoin and integrate them into your strategy.

You can change the coin list as you wish, and you can also calculate their correlation with etherium instead of bitcoin .

The indicator shows the correlation value of 36 altcoins at the moment.

The indicator indicates the color of the correlated parities as green and the color of the inversely correlated parities as red.

Cheers

Bitcoin Miner Extreme SellingThis script is for identifying extreme selling. Judging by the chart, Bitcoin miners often (not always) sell hard for two reasons: to take profit into parabolic price rises, or to stay solvent when the price is very low.

Extreme selling thus often coincides with long-term tops and bottoms in Bitcoin price. This can be a useful EXTRA data point when trying to time long-term Bitcoin spot or crypto equity investment (NOT advice, you remain responsible, etc). The difference between selling measured in BTC and in USD gives a reasonable idea of whether miners are selling to make a profit or to stay solvent.

CREDITS

The idea for using the ratio of miner outflows to reserves comes from the "Bitcoin Miner Sell Pressure" script by the pioneering capriole_charles.

The two request.security calls are identical. Another similarity is that you have to sum the outflows to make it make sense. But it doesn't make much difference, it turns out from testing, to use an average of the reserves, so I didn't. All other code is different.

The script from capriole_charles uses Bollinger bands to highlight periods when sell pressure is high, uses a rolling 30-day sum, and only uses the BTC metrics.

My script uses a configurable 2-6 week rolling sum (there's nothing magical about one month), uses different calculations, and uses BTC, USD, and composite metrics.

INPUTS

Rolling Time Basis : Determines how much data is rolled up. At the lowest level, daily data is too volatile. If you choose, e.g., 1 week, then the indicator displays the relative selling on a weekly basis. Longer time periods, obviously, are smoother but delayed, while shorter time periods are more reactive. There is no "real" time period, only an explicit interpretation.

Show Data > Outflows : Displays the relative selling data, along with a long-term moving average. You might use this option if you want to compare the "real" heights of peaks across history.

Show Data > Delta (the default): Only the difference between the relative selling and the long-term moving average is displayed, along with an average of *that*. This is more signal and less noise.

Base Currency : Configure whether the calculations use BTC or USD as the metric. This setting doesn't use the BTC price at all; it switches the data requested from INTOTHEBLOCK.

If you choose Composite (the default), the script combines BTC and USD together in a relative way (you can't simply add them, as USD is a much bigger absolute value).

In Composite mode, the peaks are coloured red if BTC selling is higher than USD, which usually indicates forced selling, and green if USD is higher, which usually indicates profit-taking. This categorisation is not perfectly accurate but it is interesting insomuch as it is derived from block data and not Bitcoin price.

In BTC or USD mode, a gradient is used to give a rough visual idea of how far from the average the current value is, and to make it look pretty.

USAGE NOTES

Because of the long-term moving averages, the length of the chart does make a difference. I recommend running the script on the longest Bitcoin chart, ticker BLX.

To use it to compare selling with pivots in crypto equities, use a split chart: one BLX with the indicator applied, and one with the equity of your choice. Sync Interval, Crosshair, Time, and Date Range, but not Symbol.

Bitcoin Golden Pi CyclesTops are signaled by the fast top MA crossing above the slow top MA, and bottoms are signaled by the slow bottom MA crossing above the fast bottom MA. Alerts can be set on top and bottom prints. Does not repaint.

Similar to the work of Philip Swift regarding the Bitcoin Pi Cycle Top, I’ve recently come across a similar mathematically curious ratio that corresponds to Bitcoin cycle bottoms. This ratio was extracted from skirmantas’ Bitcoin Super Cycle indicator . Cycle bottoms are signaled when the 700D SMA crosses above the 137D SMA (because this indicator is closed source, these moving averages were reverse-engineered). Such crossings have historically coincided with the January 2015 and December 2018 bottoms. Also, although yet to be confirmed as a bottom, a cross occurred June 19, 2022 (two days prior to this article)

The original pi cycle uses the doubled 350D SMA and the 111D SMA . As pointed out this gives the original pi cycle top ratio:

350/111 = 3.1532 ≈ π

Also, as noted by Swift, 111 is the best integer for dividing 350 to approximate π. What is mathematically interesting about skirmanta’s ratio?

700/138 = 5.1095

After playing around with this for a while I realized that 5.11 is very close to the product of the two most numerologically significant geometrical constants, π and the golden ratio, ϕ:

πϕ = 5.0832

However, 138 turns out to be the best integer denominator to approximate πϕ:

700/138 = 5.0725 ≈ πϕ

This is what I’ve dubbed the Bitcoin Golden Pi Bottom Ratio.

In the spirit of numerology I must mention that 137 does have some things going for it: it’s a prime number and is very famously almost exactly the reciprocal of the fine structure constant (α is within 0.03% of 1/137).

Now why 350 and 700 and not say 360 and 720? After all, 360 is obviously much more numerologically significant than 350, which is proven by the fact that 360 has its own wikipedia page, and 350 does not! Using 360/115 and 720/142, which are also approximations of π and πϕ respectively, this also calls cycle tops and bottoms.

There are infinitely many such ratios that could work to approximate π and πϕ (although there are a finite number whose daily moving averages are defined). Further analysis is needed to find the range(s) of numerators (the numerator determines the denominator when maintaining the ratio) that correctly produce bottom and top signals.

Bitcoin Risk RangeThis is an extension of the original 'Bitcoin Bubble' indicator I previously made, but shows the necessary price required to reach a range of bitcoin's bubble level in the short term. I recommend using this metric with a daily timeframe to have an adequate amount of data.

Bitcoin Movement vs. Coin's Movement MTFThis script tracks the percent change of Bitcoin vs. the percent change of the coin on the chart. Crypto markets are usually affected greatly by Bitcoin swings so being able to see if the given coin is trending above or below Bitcoin is useful market data. All choices made with this script are your own! Thanks.

Bitcoin - CME Futures Friday Close

This indicator displays the weekly Friday closing price according to the CME trading hours (Friday 4pm CT).

A horizontal line is displayed until the CME opens again on Sunday 5pm CT.

This indicator is based on the thesis, that during the weekend the Bitcoin price tends to mean reverse to the CME closing price of the prior Friday. The level can also act as support/resistance. This indicator gives a visualization of this key level for the relevant time window.

Furthermore the indicator helps to easily identify, if there is an up or down gap in the CME Bitcoin contract.

Bitcoin Daily Support/ResistanceA new indicator for tradingview.

Indicator Overview

The 2-Year MA Multiplier is intended to be used as a long term investment tool.

It highlights periods where buying or selling Bitcoin during those times would have produced outsized returns.

To do this, it uses a moving average (MA) line, the 2yr MA, and also a multiplication of that moving average line, 2yr MA x5.

Note: the x5 multiplication is of the price values of the 2yr moving average, not of its time period.

Buying Bitcoin when price drops below the 2yr MA (green line) has historically generated outsized returns. Selling Bitcoin when price goes above the 2yr MA x 5 (red line) has been historically effective for taking profit.

Why This Happens

As Bitcoin is adopted, it moves through market cycles. These are created by periods where market participants are over-excited causing the price to over-extend, and periods where they are overly pessimistic where the price over-contracts. Identifying and understanding these periods can be beneficial to the long term investor.

This tool is a simple and effective way to highlight those periods

MA 50/100/150 was historically good support and resistance. When we cross them we have a new trend that is established.

Bitcoin Funds PremiumDisplay the % premium of 4 different Bitcoin Funds relative to the price of Bitcoin in your current chart.

BTCC ETF

QBTC Fund

GBTC Trust

VBTC ETN

This indicator uses the metrics from the fund management websites to calculate the "Net Asset Value per Unit (NAVPU)" to calculate the true underlying value of the fund.

The difference is then compared to the price of Bitcoin in the chart you have open.

Note that the metrics change and therefore the graph is not accurate for long past timeframes.

If TradingView would expand their script language in a way to ingest CSV data from the funds website then this could be improved.

You can update the metrics for each fund in the settings dialogue.

The script will autodetect the currency pairs of your current graph and only display compatible funds:

BTC / USD will show BTCC.U, QBTC.U and GBTC

BTC / CAD will show BTCC and QBTC

BTC / EUR will show VBTC

The script should not show in other currency pairs so it will not mess up other charts you might switch to.

If you find bugs with this logic, please comment below so I can fix them.

Due to TradingViews "no-links in description" policy, you need to google each funds website yourself to find the current metrics. These search terms should help:

BTCC search "Purpose Bitcoin ETF"

QBTC search "3iq The Bitcoin Fund (QBTC)"

GBTC search "Grayscale® Bitcoin Trust"

VBTC search "VanEck Vectors Bitcoin ETN"

Bitcoin Funds OverlayOverlay the Net Asset Value per Unit (NAVPU) of 4 different Bitcoin Funds on your Bitcoin chart.

BTCC ETF

QBTC Fund

GBTC Trust

VBTC ETN

This indicator uses the metrics from the fund management websites to calculate the "Net Asset Value per Unit (NAVPU)" to display the true underlying value of the fund.

Note that the metrics can change and therefore the graph is not accurate for long past timeframes.

You can update the metrics for each fund in the settings dialogue.

The script will autodetect the currency pairs of your current graph and only display compatible funds:

BTC / USD will show BTCC.U, QBTC.U and GBTC

BTC / CAD will show BTCC and QBTC

BTC / EUR will show VBTC

The script should not show in other currency pairs so it will not mess up other charts you might switch to.

If you find bugs with this logic, please comment below so I can fix them.

Due to TradingViews "no-links in description" policy, you need to google each funds website yourself to find the current metrics. These search terms should help:

BTCC search "Purpose Bitcoin ETF"

QBTC search "3iq The Bitcoin Fund (QBTC)"

GBTC search "Grayscale® Bitcoin Trust"

VBTC search "VanEck Vectors Bitcoin ETN"

Bitcoin Bulls and Bears by @dbtrBitcoin 🔥 Bulls & Bears 🔥

v1.0

This free-of-charge BTC market analysis indicator helps you better understand what's going with Bitcoin from a high-level perspective. At a glance, it will give you an immediate understanding of Bitcoin’s historic price channel dating back to 2011, past and current market cycles, as well as current key support levels.

Usage

Use this indicator with any BTCUSD pairs , ideally with a long price history (such as BNC:BLX )

We recommend to use this indicator in log mode, combined with Weekly or Monthly timeframe.

Features

🕵🏻♂️ Historic price channel curve since 2011

🚨 Bull & bear market cycles (dynamic)

🔥 All-time highs (dynamic)

🌟 Weekly support (dynamic, based on 20 SMA )

💪 Long-term support (channel bottom)

🔝 Potential future price targets (dynamic)

❎ Overbought RSI coloring

📏 Log/non-log support

🌚 Dark mode support

Remarks

With exception of the price channel curve, anything in this indicator is calculated dynamically , including bull/bear market cycles (based on a tweaked 20SMA), ATHs, and so on. As a result, historic market cycles may not be 100% accurately reflected and may also differ slightly in between various time-frames (closest result: Monthly). The indicator may even consider periods of heavy ups/downs as their own market cycles, even though they weren’t. Due to its dynamic nature, this indicator can however adapt to the future and helps you quickly identify potential changes in market structure, even if the indicator is no longer updated.

On top of that bullmarket cycles (colored in green) feature an ingrained RSI: the darker the green color, the more the RSI is overbought and close to a correction (darkest color in the chart = 90 Weekly RSI). In comparison with past bull cycles, it helps you easily spot potential reversal zones.

Thanks

Thanks to @quantadelic and @mabonyi which both have worked on the BTC "growth zones" indicator including the price channel, of which I have used parts of the code as well as the actual price channel data.

Follow me

Follow me here on TradingView to be notified as soon as new free and premium indicators and trading strategies are published. Inquire me for any other requests.

Enjoy & happy trading!

Bitcoin Estimated Transaction FeeThis is the estimated fee you can expect to pay to have your bitcoin transaction confirm in 1 block. The estimation is derived from the daily total revenue miners received divided by the daily total number of transactions.

An option to change to a different currency is provided.

Notes on transaction fees:

Most exchanges do not provide an option to change the fee amount, and charge a static fee. A notable exception is Deribit.

The newer Bech32 wallet format, also known as native or SegWit, use a lower fee for the same transaction as legacy addresses. The addresses start with "bc1".

Mania was $60 USD to move bitcoin to an exchange you've only just heard of to buy a different coin with funny name :)

Bitcoin DAA OscillatorAn oscillator of Bitcoin's Daily Active Addresses (DAA) and fundamental metric of the utilization of the Bitcoin network.

Helps to identify:

Potential buy zones (green) - when the network utilization is low & increasing

Potential sell zones (red) - when the network utilization is high & decreasing

Bitcoin Logarithmic Curves OscillatorThis a companion indicator for the Bitcoin Logarithmic Growth Curves indicator.

This is an oscillator version of the above. When the indicator is at / near 1 then Bitcoin price is at / near the upper range of its long-term logarithmic growth trend. When at / near 0 then price is at / near the lower range of that trend.

This indicator only works with the BLX Brave New Coin Index (ticker:BLX) and only on 1 day, 3 day, or 1 week timeframes.

Bitcoin Fibonacci Log RegressionThe "Zero Line" is the calculated logarithmic regression of Bitcoin over the last decade.

The rainbow above the Zero Line are the Fibonacci multiples from 0 --> 1 of the log regression (0.236, 0.382, etc.)

The rainbow below the Zero Line is identical, except that the multiples are negative (-0.236, -0.382, etc.)

For the first time ever, Bitcoin broke through the Zero Line (the natural regression) when it dumped on March 12-13. It looked at though the regression was invalidated when, in fact, it simply made an unprecedented move to a lower Fibonacci multiple.

Enjoy.

Bitcoin Stock to FlowModeling Bitcoin's Value With Scarcity

The Stock to Flow model for Bitcoin suggests that Bitcoin price is driven by scarcity over time.

Bitcoin is the first scarce digital object the world has ever seen. It is scarce like silver & gold, and can be sent over the internet, radio, satellite etc. Bitcoin includes a mathematical mechanism to restrict its supply over time making it more rare as time goes on. Digital Scarcity.

In 2017 BTC exceeded the market capitalization of Silver. After the next halving in 2024, Bitcoin will become the hardest asset the world has ever seen, rarer than Gold.

There is only enough Bitcoin in the world for each person to own .0023 BTC. Because of this, Bitcoin's value should continue to rise over time.

Bitcoin Circulating Supply Overlay [BigBitsIO]This script shows the estimated circulating supply of Bitcoin on any given day.

Features:

- Estimated Bitcoin circulating supply calculated daily

- Uses the Bitcoin reward schedule, past halving dates, and the next upcoming halving estimated date to calculate the current estimated supply.

- Optionally includes an option to use "Log Reduction" on the chart

*** DISCLAIMER: For educational and entertainment purposes only. Nothing in this content should be interpreted as financial advice or a recommendation to buy or sell any sort of security or investment including all types of crypto. DYOR, TYOB. ***

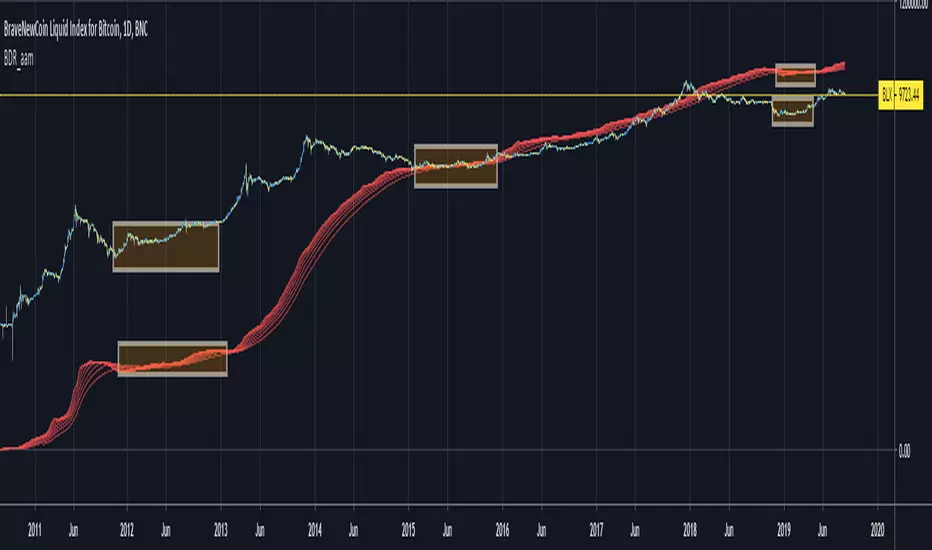

Bitcoin Difficulty Ribbon [aamonkey]This is another tool to find big cycle bottoms that is very unknown yet effective.

The Difficulty Ribbon speaks to the impact of miner selling pressure on Bitcoin`s price action.

When network difficulty reduces its rate of climb, miners are going out of business, leaving only the strong miners who proportionally need to sell less of their coins to remain operational, this leads to less sell pressure and more room for bullish price action.

The best times to buy Bitcoin are zones where the ribbon compresses.

The ribbon consists of simple moving averages of Bitcoin network difficulty so the rate of change of difficulty can be easily seen.