Bollinger Aurora Velocity [Pineify]Pineify - Bollinger Aurora Velocity

The Bollinger Aurora Velocity is an enhanced volatility and trend analysis indicator that transforms the classic Bollinger Bands into a visually stunning, multi-dimensional trading tool. By combining standard deviation bands with historical extreme tracking and dynamic momentum coloring, this indicator provides traders with deeper insights into volatility cycles, squeeze conditions, and trend strength all in one overlay.

Key Features

Classic Bollinger Bands with customizable period and standard deviation multiplier

Nebula Memory Cloud tracking historical band extremes for volatility context

Volatility Squeeze Detection with visual dot indicators on the basis line

Gradient-based candle coloring reflecting normalized price position

Multi-layer aurora gradient fills for intuitive visual analysis

How It Works

The indicator begins with a standard Bollinger Bands calculation using a simple moving average as the basis line, with upper and lower bands placed at a user-defined multiple of standard deviation. This core structure measures price volatility and identifies overbought/oversold conditions.

The Nebula Memory Cloud extends beyond traditional bands by tracking the highest point of the upper band and lowest point of the lower band over a configurable lookback period. This creates an outer envelope showing the maximum volatility expansion in recent history.

Trading Ideas and Insights

The Volatility Squeeze is a powerful concept where contracting Bollinger Bands often precede significant price breakouts. This indicator detects squeezes by comparing the current band width to its 100-period simple moving average. When the current range falls below this average, yellow dots appear on the basis line, alerting traders to potential explosive moves ahead.

When squeeze dots appear and the outer nebula cloud shows significant distance from the current bands, it suggests volatility is at a historical low relative to recent extremes—a setup often followed by strong directional moves.

How Multiple Indicators Work Together

Bollinger Bands establish the primary volatility envelope and mean-reversion zones

The Nebula Cloud provides historical context, showing how current volatility compares to recent extremes

Squeeze Detection identifies compression phases using relative bandwidth analysis

Normalized Scoring translates price position into a 0-100 scale for gradient coloring

Unique Aspects

Unlike standard Bollinger Bands indicators, the Aurora Velocity creates a heat-map effect on price bars. The normalized score calculates where price sits within the bands as a percentage, then applies a smooth gradient from bearish to bullish colors. This allows traders to instantly perceive momentum strength—saturated bullish colors near the upper band indicate strong upward pressure, while saturated bearish colors near the lower band signal selling dominance.

The aurora-style gradient fills between band layers create visual depth, making it easy to distinguish the core volatility zone from the historical extreme boundaries.

How to Use

Monitor candle colors for momentum direction—bright green indicates bullish positioning, bright red signals bearish pressure

Watch for yellow squeeze dots on the basis line as early warning for potential breakouts

Use the outer nebula cloud to assess if current volatility is testing historical extremes

Set alerts for price breakouts above the upper band or below the lower band

Combine squeeze conditions with the nebula cloud width to gauge breakout potential

Customization

Base Period - Controls Bollinger Bands calculation length (default: 20)

Standard Deviation Multiplier - Adjusts band width from the basis (default: 2.0)

Price Source - Select the price input for calculations (default: close)

Nebula Memory Length - Lookback period for tracking historical extremes (default: 50)

Color Settings - Customize bullish and bearish gradient colors

Conclusion

The Bollinger Aurora Velocity elevates traditional Bollinger Bands analysis by adding historical volatility context through the Nebula Cloud, precise squeeze detection for breakout anticipation, and intuitive momentum visualization through gradient candle coloring. This combination helps traders identify not just where price is relative to volatility bands, but how that volatility compares to recent history and when compression may lead to expansion.

Cari dalam skrip untuk "breakout"

Prism Band Dynamics [JOAT]Prism Band Dynamics - Bollinger-Style Bands with Force Detection

Introduction and Purpose

Prism Band Dynamics is an open-source overlay indicator that creates dynamic Bollinger-style bands with an innovative "force detection" system. The core problem this indicator solves is that standard Bollinger Bands show volatility but don't indicate directional momentum. When all three band components (upper, lower, basis) move in the same direction, it indicates strong directional force that standard bands don't highlight.

This indicator addresses that by detecting when all band components align directionally, providing a clear signal of market force.

Why Force Detection Matters

Standard Bollinger Bands expand and contract based on volatility, but they don't tell you about directional momentum. Force detection adds this dimension:

1. Bullish Force - Upper band, lower band, AND basis all moving up together. This indicates strong upward momentum where even the lower support level is rising.

2. Bearish Force - Upper band, lower band, AND basis all moving down together. This indicates strong downward momentum where even the upper resistance level is falling.

3. Neutral - Mixed movement indicates consolidation or uncertainty.

How Force Detection Works

bool upperUp = upper > upper

bool lowerUp = lower > lower

bool basisUp = basis > basis

int forceFull = if upperUp and lowerUp and basisUp

1 // Bullish force

else if upperDn and lowerDn and basisDn

-1 // Bearish force

else

0 // Neutral

Additional Features

Squeeze Detection - Identifies when band width contracts below threshold, often preceding large moves

Gradient Fills - Color intensity reflects force strength

Direction Change Arrows - Visual markers when force direction shifts

Dashboard Information

Force - Current force status (BULLISH/BEARISH/NEUTRAL)

Position - Price location within bands (Upper/Mid/Lower Zone)

Band Width - Current width percentage with expansion/contraction label

Volatility - Squeeze status (SQUEEZE/NORMAL)

Force Count - Bars since last force change

How to Use This Indicator

For Trend Following:

1. Enter long when force turns BULLISH

2. Enter short when force turns BEARISH

3. Exit or reduce when force turns NEUTRAL

For Squeeze Breakouts:

1. Watch for SQUEEZE status in dashboard

2. Prepare for breakout in either direction

3. Enter when force confirms direction after squeeze

For Mean Reversion:

1. Only trade mean-reversion when force is NEUTRAL

2. Avoid fading moves when force is active

3. Use band touches as entry points during neutral force

Input Parameters

Length (20) - Period for basis and standard deviation

Multiplier (2.0) - Standard deviation multiplier for bands

MA Type (SMA) - Basis calculation method

Squeeze Threshold (0.5) - Band width percentage for squeeze detection

Timeframe Recommendations

4H-Daily: Cleanest force signals

1H: Good balance of signals and reliability

15m: More signals but more noise

Limitations

Force detection can lag during rapid reversals

Squeeze breakouts can fail (false breakouts)

Works best in markets with clear trending/ranging phases

Open-Source and Disclaimer

This script is published as open-source under the Mozilla Public License 2.0 for educational purposes.

This indicator does not constitute financial advice. Force detection does not guarantee trend continuation. Always use proper risk management.

- Made with passion by officialjackofalltrades

4H Candle Curves4H Candle Curves - Detailed User Guide

OVERVIEW

This indicator reveals curve vs continuation behavior in NQ Futures by analyzing how price responds after breaking the first-hour range. Based on 10+ years of statistical analysis (2013-2025, 3,136+ trading days), it identifies which 4-hour sessions exhibit mean reversion (curve) behavior versus trend continuation when Q2 (second hour) breaks Q1 (first hour) extremes.

⚠️ IMPORTANT: This indicator is specifically designed for NQ FUTURES ONLY. All curve probabilities and statistics were derived from a decade-long dataset of NQ 1-minute bars. Using this on other instruments will produce inaccurate results.

CORE CONCEPT: THE CURVE

What is a "Curve"?

A curve occurs when price breaks out of the first hour's range in Q2 (hour 2), but then reverses direction in the second half (Q3+Q4) to make a new extreme on the opposite side.

Curve Example (Upside Break → Downside Reversal):

Q1 (Hour 1): Price establishes range 25,000 - 25,050

Q2 (Hour 2): Price breaks ABOVE Q1 high, reaches 25,100

Q3+Q4 (Hours 3-4): Price curves back down, makes new LOW below 25,000

Result: Q2 broke high, but second half curved back to make new low below Q1 = CURVE

What is "Continuation"?

Continuation occurs when Q2 breaks Q1 range and the second half extends further in the same direction.

Continuation Example (Upside Break → Further Upside):

Q1 (Hour 1): Price establishes range 25,000 - 25,050

Q2 (Hour 2): Price breaks ABOVE Q1 high, reaches 25,100

Q3+Q4 (Hours 3-4): Price continues higher, makes new HIGH above 25,100

Result: Q2 broke high, second half made new high above Q2 = CONTINUATION

THE CRITICAL DISCOVERY: 6AM IS THE CURVE SESSION

Curve Probabilities by Session:

When Q2 Breaks Q1 HIGH:

6AM: 60.6% curve (new low below Q1) | 38.5% continuation

2AM: 38.4% curve | 46.7% continuation (balanced)

10AM: 17.2% curve | 60.4% continuation ← STRONG continuation bias

6PM: 29.6% curve | 59.0% continuation

10PM: 27.5% curve | 55.1% continuation

When Q2 Breaks Q1 LOW:

6AM: 64.4% curve (new high above Q1) | 35.0% continuation ← HIGHEST curve

2AM: 42.8% curve | 43.3% continuation (balanced)

10AM: 16.7% curve | 51.6% continuation ← STRONG continuation bias

6PM: 33.7% curve | 51.1% continuation

10PM: 33.1% curve | 48.6% continuation

Key Insight:

6AM is THE ONLY SESSION with >60% curve probability in both directions. This makes it a uniquely exploitable mean reversion session. When Q2 breaks Q1 range during 6AM, expect the second half to curve back 60-64% of the time.

10AM shows the opposite: Strong continuation bias (60% when Q2 breaks high, 52% when Q2 breaks low). 10AM breakouts tend to follow through.

HOW IT WORKS: THE QUARTER SYSTEM

The Six 4-Hour Candles (EST):

Each trading day (6pm-5pm) is divided into six 4-hour periods:

6PM (18:00-22:00) - Evening/Globex open | Blue box

10PM (22:00-02:00) - Asia session | Purple box

2AM (02:00-06:00) - Early London | Orange box

6AM (06:00-10:00) - Late London + NY Open | Green box ← THE CURVE SESSION

10AM (10:00-14:00) - NY Morning | Red box ← THE CONTINUATION SESSION

2PM (14:00-17:00) - NY Afternoon | Yellow box (3 hours only)

The Four Quarters:

Each 4-hour candle (except 2PM) is divided into four 1-hour quarters:

Q1 (Hour 1, minutes 0-60): Establishes initial range

Q2 (Hour 2, minutes 60-120): Tests Q1 range - breaks or holds?

Q3 (Hour 3, minutes 120-180): Second half begins

Q4 (Hour 4, minutes 180-240): Second half completes

2PM candle only has 3 hours (14:00-17:00), so quarters are adjusted accordingly.

The Three-Step Analysis:

STEP 1: Q1 Establishes Range

The first hour sets the high and low for the session. This becomes the reference range.

STEP 2: Q2 Break Detection

The indicator monitors whether Q2 (hour 2) breaks above Q1 high or below Q1 low.

STEP 3: Second Half Response

Once Q2 breaks Q1 range, the indicator tracks what happens in Q3+Q4:

Does price CURVE back to make new extreme on opposite side?

Does price CONTINUE to make new extreme in same direction?

Or does price stay within the established range?

VISUAL ELEMENTS EXPLAINED

1. 4-Hour Candle Boxes

Colored boxes display the high-to-low range of each 4H candle:

Blue = 6PM (evening session start)

Purple = 10PM (Asia session)

Orange = 2AM (early London)

Green = 6AM ← THE CURVE SESSION (watch for mean reversion)

Red = 10AM ← THE CONTINUATION SESSION (trend follow-through)

Yellow = 2PM (afternoon close, 3 hours only)

2. Quarter Separator Lines

Vertical dotted lines mark the boundaries between quarters (1H, 2H, 3H marks). This helps you see:

When Q1 ends (after 1 hour)

When Q2 ends / second half begins (after 2 hours)

When Q3 ends (after 3 hours)

3. Candle Name Labels

At the 2-hour mark (Q2/Q3 boundary), a label shows:

Candle name (e.g., "6am")

Directional indicator:

🔼 = Q2 broke Q1 HIGH

🔽 = Q2 broke Q1 LOW

⚠️ = Q2 broke BOTH Q1 high and low (extended range)

No symbol = Q2 stayed within Q1 range

THE LIVE STATUS TABLE

Located in your chosen corner (default: bottom-right), this table shows real-time analysis of the current 4H candle.

Header Row:

"LIVE: CANDLE" - Shows which 4H session you're currently in

Quarter Row:

"Quarter: Q1/Q2/Q3/Q4 (Hour X)" - Shows which quarter you're currently forming

STATUS Section:

The status updates dynamically based on what has happened:

During Q1-Q2 (First Half):

"⏳ Q1 Building..." - First hour forming, range being established

"⏳ Q2 Building..." - Second hour in progress, Q2 within Q1 range so far

"🔼 Q2 Broke Q1 HIGH" - Q2 has broken above Q1 high

"🔽 Q2 Broke Q1 LOW" - Q2 has broken below Q1 low

"⚠️ Q2 Broke BOTH Q1 Extremes" - Q2 extended range in both directions

During Q3-Q4 (Second Half):

"✓ CURVE CONFIRMED" - Q2 broke one direction, second half reversed to opposite side

"✓ CONTINUATION CONFIRMED" - Q2 broke one direction, second half extended further same direction

"⏳ 2nd Half In Progress" - Q2 broke Q1, waiting to see if curve or continuation

"📊 No Q2 Break Occurred" - Q2 stayed within Q1 range (no curve/continuation setup)

EXPECTATION Section:

Shows the probabilities based on the current state:

When Q2 breaks Q1 high in 6AM:

EXPECT 2nd half:

CURVE (low < Q1): 60.6%

CONT (high > Q2): 38.5%

This tells you there's a 60.6% chance the second half will curve back to make a new low below Q1, versus 38.5% chance it continues higher above Q2.

When curve/continuation is confirmed:

Q2 broke high → 2nd half made new LOW below Q1

Curve: 60.6%

Shows what actually happened and the historical probability.

Color Coding:

Purple background = Curve confirmed (mean reversion occurred)

Green background = Continuation confirmed (upside extension)

Red background = Continuation confirmed (downside extension)

Blue background = Second half in progress, watching

Yellow background = No Q2 break (no setup)

Gray background = Still in first half, building

THE CURVE REFERENCE TABLE

Located in your chosen corner (default: bottom-left), this table provides a quick reference for all sessions.

Table Structure:

TOP SECTION: "When Q2 BREAKS Q1 HIGH"

BOTTOM SECTION: "When Q2 BREAKS Q1 LOW"

How to Read:

"Curve" column = % of time second half makes new extreme on OPPOSITE side

"Cont" column = % of time second half makes new extreme in SAME direction

"Winner" column = Which behavior is more likely

Purple highlight = Curve is the winner (higher %)

Blue highlight = Continuation is the winner

🔥 symbol = Strong edge (>60%)

Quick Reference Usage:

You're in 10AM session, Q2 just broke Q1 high. Look at top section, 10AM row:

Curve: 17.2%

Cont: 60.4%

Winner: CONT

Interpretation: 10AM breakouts tend to follow through. Only 17% chance of curving back. Trade with the break, not against it.

PRACTICAL TRADING EXAMPLES

Example 1: Perfect 6AM Curve Setup

Scenario:

6AM candle in progress

7:00 AM: Q1 ends, range is 18,000 - 18,050

7:30 AM: Price breaks above 18,050, reaches 18,075 (Q2 broke Q1 high)

Live table shows: "🔼 Q2 Broke Q1 HIGH"

Expectation: "CURVE (low < Q1): 60.6%"

Trading Decision:

Even though price broke to new highs, the 60.6% curve probability suggests looking for short opportunities expecting price to curve back below 18,000 in Q3-Q4.

Typical Outcome:

8:15 AM (Q3): Price starts declining

9:15 AM (Q4): Price makes new low at 17,990

Result: ✓ CURVE CONFIRMED

Example 2: 10AM Continuation Signal

Scenario:

10AM candle in progress

11:00 AM: Q1 ends, range is 18,100 - 18,150

11:45 AM: Price breaks above 18,150, reaches 18,180 (Q2 broke Q1 high)

Live table shows: "🔼 Q2 Broke Q1 HIGH"

Expectation: "CONT (high > Q2): 60.4%"

Trading Decision:

With 60.4% continuation probability, breakout likely to follow through. Look for long opportunities expecting extension above 18,180 in Q3-Q4.

Typical Outcome:

12:30 PM (Q3): Price continues higher to 18,200

1:15 PM (Q4): Price makes new high at 18,225

Result: ✓ CONTINUATION CONFIRMED

Example 3: Using Reference Table During Live Trading

You see Q2 breaking Q1 low during 2AM session:

Quick reference check:

2AM row, "When Q2 BREAKS Q1 LOW" section

Curve: 42.8% | Cont: 43.3% | Winner: Balanced

Interpretation: This is a coin flip - 2AM session is balanced when Q2 breaks low. Don't force a directional bias. Wait for second half price action confirmation or skip the setup.

Example 4: No Setup Scenario

Scenario:

6AM candle, Q2 ends at 8:00 AM

Q2 stayed within Q1 range (no break above or below)

Live table shows: "📊 No Q2 Break Occurred"

Trading Decision:

No curve/continuation setup exists. This analysis only applies when Q2 breaks Q1 range. Monitor for different strategies or wait for next 4H candle.

UNDERSTANDING THE UNDERLYING METHODOLOGY

Data Foundation:

Instrument: NQ Futures (E-mini NASDAQ-100)

Timeframe: 1-minute bars for precise quarter tracking

Period: January 2013 - December 2025

Sample: 3,136+ complete trading days

Total 4H Candles Analyzed: ~18,800+ individual sessions

Analysis Process:

For each 4H candle in the dataset:

Calculate Q1 high and low (first hour range)

Track whether Q2 breaks Q1 high, Q1 low, both, or neither

When Q2 breaks Q1 range, measure second half response:

Did Q3+Q4 make new low below Q1? (curve when Q2 broke high)

Did Q3+Q4 make new high above Q1? (curve when Q2 broke low)

Did Q3+Q4 make new high above Q2? (continuation when Q2 broke high)

Did Q3+Q4 make new low below Q2? (continuation when Q2 broke low)

Calculate percentages for each session

Why NQ-Specific?

Different futures contracts exhibit different intraday personality:

NQ (NASDAQ):

Tech-heavy, volatility-prone

6AM shows extreme curve behavior (60-64%) due to NY Open reversal tendency

10AM shows strong continuation (60%) as trends establish

ES (S&P 500) would show different probabilities because:

Lower volatility than NQ

Different institutional participation patterns

Different response to macro events

The indicator's probabilities are calibrated specifically to NQ behavior patterns. Using it on ES, RTY, or other instruments will produce misleading signals.

ORIGINALITY & INNOVATION

What Makes This Indicator Unique:

Quarter-Based Curve Analysis: Unlike traditional indicators that only identify breakouts, this tracks what happens after the breakout. The curve vs continuation framework is novel and provides directional edge.

Session-Specific Behavior: Recognizes that 6AM behaves fundamentally differently than 10AM. Most indicators apply the same logic across all sessions. This indicator provides session-specific probabilities.

Statistical Validation: Every probability shown is backed by 10+ years of data (2,900+ candles per session). Not based on theory or discretionary observation.

Real-Time Quarter Tracking: Precisely identifies which quarter you're in and what stage of the pattern is forming. Provides forward-looking probabilities based on current state.

The 6AM Discovery: The 60-64% curve probability in 6AM is a quantified, repeatable edge that contradicts traditional "breakout = continuation" assumptions. This session exhibits mean reversion characteristics that most traders miss.

Dual-Direction Analysis: Tracks both upside breaks (Q2 > Q1 high) and downside breaks (Q2 < Q1 low) separately, as they can have different probabilities.

Visual Quarter System: The combination of colored boxes, quarter separators, and real-time labels provides instant visual understanding of pattern stage and expected behavior.

HOW TO USE THIS INDICATOR

Step 1: Identify Current 4H Candle

Check which colored box you're in and what session it represents.

Step 2: Wait for Q2 to Complete

The setup doesn't exist until Q2 (hour 2) breaks Q1 range. Monitor the live table.

Step 3: Check Q2 Break Status

Did Q2 break Q1 high? Q1 low? Both? Or neither?

Step 4: Consult Reference Table

Look up current session in curve reference table. What's the probability?

Step 5: Apply Session-Specific Strategy

For 6AM (60-64% curve):

Q2 breaks high → Expect curve back for new low

Q2 breaks low → Expect curve back for new high

Strategy: FADE the Q2 break, look for reversal entries in Q3-Q4

For 10AM (52-60% continuation):

Q2 breaks high → Expect continuation higher

Q2 breaks low → Expect continuation lower

Strategy: TRADE WITH the Q2 break, look for continuation entries in Q3-Q4

For 2AM (38-43% curve, 43-47% continuation):

Balanced probabilities

Strategy: Wait for Q3 price action to confirm direction, or skip

For 6PM/10PM (50-59% continuation):

Moderate continuation bias

Strategy: Lean with the break but use tight stops

Step 6: Monitor Live Status

Watch the live table for confirmation:

"✓ CURVE CONFIRMED" = Mean reversion occurred

"✓ CONTINUATION CONFIRMED" = Follow-through occurred

"⏳ 2nd Half In Progress" = Still developing

BEST PRACTICES

Focus on 6AM for curve trades - This is THE high-probability mean reversion session

Focus on 10AM for continuation trades - This is THE high-probability breakout session

Be cautious with 2AM - Balanced probabilities mean lower edge

Use quarter separators - Enter trades early in Q3 after Q2 break, don't wait for Q4

Combine with price action - Don't blindly fade 6AM or follow 10AM; wait for confirming price structure

Respect the 60% rule - 6AM curve happens 60% of time, which means 40% it doesn't. Manage risk accordingly

Watch for "No Q2 Break" - If Q2 doesn't break Q1, this analysis doesn't apply

Consider overnight context - If 6AM opens with huge gap, curve probability may be affected

SETTINGS & CUSTOMIZATION

Display Settings:

Show 4H Candle Boxes - Toggle colored range boxes

Box Colors - Customize color for each session

Show Quarter Separators - Show/hide 1H, 2H, 3H lines

Show Candle Name Labels - Show/hide session labels at 2H mark

Separator Line Style - Solid/Dashed/Dotted

Max Historical Candles - How many past 4H candles to display (1-50)

Table Settings:

Show Live Status Table - Toggle real-time analysis table

Show Curve Reference Table - Toggle probability reference table

Table Positions - Place tables in any corner

Table Text Size - Tiny/Small/Normal

LIMITATIONS & DISCLAIMERS

NQ FUTURES ONLY - All probabilities are NQ-specific, do not use on other instruments

Requires Q2 break - No curve/continuation setup exists if Q2 stays within Q1 range

Probabilities, not certainties - 60% means it happens 6 out of 10 times, not every time

Lower timeframe noise - 1-minute tracking can be choppy, consider using 5min+ for entries

Gap days - Large overnight gaps may affect curve/continuation probabilities

Not standalone - Use as confluence with your strategy, not as sole decision factor

Historical performance - Past statistics don't guarantee future results

WHY THE CURVE CONCEPT MATTERS

Traditional trading wisdom says: "Breakout = Continuation"

This indicator proves that's not always true. Specifically, during the 6AM session (late London + NY Open), when Q2 breaks the Q1 range, price curves back to the opposite extreme 60-64% of the time.

This creates a unique exploitable edge:

Most breakout traders go LONG when Q2 breaks Q1 high

But in 6AM, 60.6% of the time, price curves back down for new low

Shorting the breakout (counter-intuitive) is the higher-probability trade

The 10AM session shows the opposite:

Breakouts in 10AM tend to follow through (52-60%)

Traditional "trade the breakout" strategy works better here

By knowing which session you're in, you can adapt your strategy to match the session's personality.

FINAL NOTES

This indicator distills 10+ years of NQ intraday behavior into actionable, session-specific probabilities. The discovery that 6AM exhibits 60-64% curve behavior while 10AM exhibits 52-60% continuation behavior provides a statistical edge for mean reversion and trend-following traders respectively.

The highest-probability setups:

6AM Q2 break → FADE (60-64% edge for curve)

10AM Q2 break → FOLLOW (52-60% edge for continuation)

2AM = SKIP (balanced probabilities, no clear edge)

Master the 6AM curve and 10AM continuation first. These two sessions provide the clearest statistical edges.

Remember: Trade with proper risk management. This tool provides probabilities based on historical behavior, not predictions of future performance.

Clean Volume (SUV)The Problem with Raw Volume

Traditional volume bars tell you how much traded, but not whether that amount is unusual. This creates noise that misleads traders:

Stock A averages 1M shares with wild daily swings (500K-2M is normal). Today's 2M volume looks like a spike—but it's just a routine high day.

Stock B averages 1M shares with rock-steady volume (950K-1.05M typical). Today's 2M volume is genuinely extraordinary—institutions are clearly active.

Both show identical 200% relative volume. But Stock B's reading is far more significant. Raw volume and simple relative volume (RVol) can't distinguish between these situations, leading to:

- False signals on naturally volatile stocks

- Missed signals on stable stocks where smaller deviations matter

- Inconsistent comparisons across different securities

---

A Solution: Standardized Unexpected Volume (SUV)

SUV applies statistical normalization to volume, measuring how many standard deviations today's volume is from the mean. This z-score approach accounts for each stock's individual volume stability, not just its average.

SUV = (Today's Volume - Average Volume) / Standard Deviation of Volume

Using the examples above:

- Stock A (high volatility): SUV = 2.0 — elevated but not unusual for this stock

- Stock B (low volatility): SUV = 10.0 — extremely unusual, demands attention

SUV automatically calibrates to each security's behaviour, making volume readings comparable across any stock, ETF, or timeframe.

---

What SUV Is Good For

✅ Identifying genuine volume anomalies — separates signal from noise

✅ Comparing volume across different securities — apples-to-apples z-scores

✅ Spotting institutional activity — large players create statistically significant footprints

✅ Confirming breakouts — high SUV validates price moves

✅ Detecting exhaustion — extreme SUV after extended moves may signal climax

✅ Finding "dry" setups — negative SUV reveals quiet accumulation periods

---

Where SUV Has Limitations

⚠️ Earnings/news events — SUV will spike dramatically (by design), but the statistical reading may be less meaningful when fundamentals change

⚠️ Low-float stocks — extreme volume volatility can produce erratic SUV readings

⚠️ First 20 bars — needs lookback period to establish baseline; early readings are less reliable

⚠️ Doesn't predict direction — SUV measures volume intensity, not whether price will rise or fall

---

How to Read This Indicator

Bar Height

Displays actual volume (like a traditional volume chart) so you can still see absolute levels.

Bar Color (SUV Intensity)

Color intensity reflects the SUV z-score. Brighter = more unusual.

Up Days (Green Gradient):

| Color | SUV Range | Meaning |

|--------------|-----------|------------------------------------------|

| Bright Green | ≥ 3.0 | EXTREME — Highly unusual buying activity |

| Green | ≥ 2.0 | VERY HIGH — Significant accumulation |

| Light Green | ≥ 1.5 | HIGH — Above-average interest |

| Pale Green | ≥ 1.0 | ELEVATED — Moderately active |

| Muted Green | 0 to 1.0 | NORMAL — Typical volume |

| Dark Grey | < 0 | DRY — Below-average, quiet |

Down Days (Red Gradient):

| Color | SUV Range | Meaning |

|------------|-----------|-----------------------------------------|

| Bright Red | ≥ 3.0 | EXTREME — Panic selling or capitulation |

| Red | ≥ 2.0 | VERY HIGH — Heavy distribution |

| Light Red | ≥ 1.5 | HIGH — Active selling |

| Pale Red | ≥ 1.0 | ELEVATED — Moderate selling |

| Muted Red | 0 to 1.0 | NORMAL — Routine down day |

| Dark Grey | < 0 | DRY — Light profit-taking |

Coiled State (Tan/Beige):

When detected, bars turn muted tan regardless of direction. This indicates:

- Volume compression (SUV below threshold for consecutive days)

- Volatility contraction (ATR below average)

- Price tightness (small recent moves)

Coiled states may precede significant breakouts.

Special Markers

"P" Label (Blue) — Pocket Pivot detected. Morales & Kacher's signal fires when:

- Price closes higher than previous close

- Price closes above the open (green candle)

- Volume exceeds the highest down-day volume of the last 10 bars

Pocket Pivots may indicate institutional buying before a traditional breakout.

"C" Label (Orange) — Coiled state confirmed. The stock is consolidating with compressed volume and tight price action. Watch for expansion.

Dashboard

The configurable dashboard displays real-time metrics. Default items:

- Vol — Current bar volume

- SUV — Z-score value

- Class — Classification (EXTREME/VERY HIGH/HIGH/ELEVATED/NORMAL/DRY/COILED)

- Proj RVol — Projected end-of-day relative volume (intraday only)

Additional optional items: Direction, Coil Status, Relative ATR, Pocket Pivot, Average Volume.

---

Practical Usage Tips

1. SUV ≥ 2 on breakouts — Validates the move has institutional participation

2. Watch for SUV < 0 bases — Quiet accumulation zones where smart money builds positions

3. Coil → Expansion — After consecutive coiled days, the first SUV ≥ 1.5 bar often signals direction

4. Pocket Pivots in bases — Early accumulation signals before price breaks out

5. Extreme SUV (≥3) after extended moves — May indicate climax/exhaustion rather than continuation

---

Settings Overview

| Group | Key Settings |

|-----------------|-----------------------------------------------------|

| SUV Settings | Lookback period (default 20) |

| Coil Detection | Enable/disable, sensitivity thresholds |

| Pocket Pivot | Enable/disable, lookback period |

| Display | Dashboard style (Ribbon/Table), position, text size |

| Dashboard Items | Toggle which metrics appear |

| Colors | Fully customizable gradient colors |

---

Credits

SUV concept adapted from academic literature on standardized unexpected volume in market microstructure research. Pocket Pivot methodology based on Gil Morales and Chris Kacher's work. Coil detection inspired by volatility contraction patterns.

---

This indicator does not provide financial advice. Always combine volume analysis with price action, market context, and proper risk management. No animals were harmed during the coding and testing of this indicator.

Volume Profile VisionVolume Profile Vision - Complete Description

Overview

Volume Profile Vision (VPV) is an advanced volume profile indicator that visualizes where trading activity has occurred at different price levels over a specified time period. Unlike traditional volume indicators that show volume over time, this indicator displays volume distribution across price levels, helping traders identify key support/resistance zones, fair value areas, and potential reversal points.

What Makes This Indicator Original

Volume Profile Vision introduces several unique features not found in standard volume profile tools:

Dual-Direction Histogram Display:

Unlike conventional volume profiles that only show bars extending in one direction, VPV displays volume bars extending both left (into historical candles) and right (as a traditional histogram). This bi-directional approach allows traders to see exactly where historical price action intersected with high-volume nodes.

Real-Time Candle Highlighting: The indicator dynamically highlights volume bars that intersect with the current candle's price range, making it immediately obvious which volume levels are currently in play.

Four Professional Color Schemes: Each color scheme uses distinct gradient algorithms and visual encoding systems:

Traffic Light: Uses red (POC), green (VA boundaries), yellow (HVN), with grayscale gradients outside the value area

Aurora Glass: Modern cyan-to-magenta gradient with hot magenta POC highlighting

Obsidian Precision: Professional dark theme with white POC and electric cyan accents

Black Ice: Monochromatic cyan family with graduated intensity

Adaptive Transparency System: Automatically adjusts bar transparency based on position relative to value area, with special handling for each color scheme to maintain visual clarity.

Core Concepts & Calculations

Volume Distribution Analysis

The indicator divides the visible price range into user-defined price levels (default: 80 levels) and calculates the total volume traded at each level by:

Scanning back through the specified lookback period (customizable or visible range)

For each historical bar, determining which price levels the bar's high/low range intersects

Accumulating volume for each intersected price level

Optionally filtering by bullish/bearish volume only

Point of Control (POC)

The POC is the price level with the highest traded volume during the analyzed period. This represents the "fairest" price where most traders agreed on value. The indicator marks this with distinct coloring (red in Traffic Light, magenta in Aurora Glass, white in Obsidian Precision, cyan in Black Ice).

Trading Significance: POC acts as a strong magnet for price - markets tend to return to fair value. When price is away from POC, traders watch for:

Mean reversion opportunities when price is far from POC

Rejection signals when price tests POC from above/below

Breakout confirmation when price breaks through and holds beyond POC

Value Area (VA)

The Value Area encompasses the price range where a specified percentage (default: 68%) of all volume traded. This represents the range of "accepted value" by market participants.

Calculation Method:

Start at the POC (highest volume level)

Expand upward and downward, adding adjacent price levels

Always add the level with higher volume next

Continue until accumulated volume reaches the VA percentage threshold

Value Area High (VAH): Upper boundary of accepted value - acts as resistance

Value Area Low (VAL): Lower boundary of accepted value - acts as support

Trading Significance:

Price spending time inside VA indicates market equilibrium

Breakouts above VAH suggest bullish momentum shift

Breakdowns below VAL suggest bearish momentum shift

Returns to VA boundaries often provide high-probability entry zones

High Volume Nodes (HVN)

Price levels with volume exceeding a threshold percentage (default: 80%) of POC volume. These represent areas of strong agreement and consolidation.

Trading Significance:

HVNs act as strong support/resistance zones

Price tends to consolidate at HVNs before making directional moves

Breaking through an HVN often signals strong momentum

Low Volume Nodes (LVN)

Price levels within the Value Area with volume ≤30% of POC volume. These are zones price moved through quickly with minimal consolidation.

Trading Significance:

LVNs represent areas of rejection - price finds little acceptance

Price tends to move rapidly through LVN zones

Useful for setting stop-losses (below LVN for longs, above for shorts)

Can identify potential gaps or "air pockets" in the market structure

Grayscale POC Detection

A secondary POC detection system identifies the highest volume level outside the Value Area (with a 2-level buffer to avoid confusion). This helps identify significant volume accumulation zones that exist beyond the main value area.

How to Use This Indicator

Setup

Choose Lookback Period:

Enable "Use Visible Range" to analyze only what's on your chart

Or set "Fixed Range Lookback Depth" (default: 200 bars) for consistent analysis

Adjust Profile Resolution:

"Number of Price Levels" (default: 80) - higher = more granular analysis, lower = broader zones

Select Color Scheme:

Traffic Light: Best for clear POC/VA/HVN identification

Aurora Glass: Modern aesthetic for dark charts

Obsidian Precision: Professional trader preference

Black Ice: Minimalist single-color family

Visual Customization

Left Extension: How far back the left-side histogram extends into historical candles (default: 490 bars)

Right Extension: Width of the traditional histogram bars on the right (default: 50 bars)

Right Margin: Space between current price bar and histogram (default: 0 for flush alignment)

Left Profile Gap: Space between left-side histogram and candles (default: 0)

Trading Strategies

Strategy 1: Value Area Mean Reversion

Wait for price to move outside the Value Area (above VAH or below VAL)

Look for rejection signals (wicks, bearish/bullish candles)

Enter trades toward the POC

Take profits as price returns to POC or opposite VA boundary

Strategy 2: Breakout Confirmation

Identify when price is consolidating within the Value Area

Wait for a strong close above VAH (bullish) or below VAL (bearish)

Enter on the breakout or on first pullback to the VA boundary

Target previous HVNs or swing highs/lows outside the VA

Strategy 3: POC Support/Resistance

Watch for price approaching the POC level

If approaching from below, look for bullish reversal patterns at POC (support)

If approaching from above, look for bearish reversal patterns at POC (resistance)

Trade in the direction of the bounce with stops beyond the POC

Strategy 4: LVN Fast Movement Zones

Identify LVN zones within the Value Area (marked with "LVN" label)

When price enters an LVN, expect rapid movement through the zone

Avoid entering trades within LVNs

Use LVNs as confirmation of directional momentum

Alert System

The indicator includes 7 customizable alert conditions:

POC Touch: Alerts when price comes within 0.5 ATR of POC

VAH/VAL Touch: Alerts at Value Area boundaries

VA Breakout: Alerts on breakouts above VAH or below VAL

HVN Touch: Alerts when price contacts High Volume Nodes

LVN Entry: Alerts when entering Low Volume zones

POC Shift: Alerts when POC moves to a new price level

Reading the Profile

Price Labels (shown on the right side):

POC: Point of Control - highest volume price level

VAH: Value Area High - upper boundary of accepted value

VAL: Value Area Low - lower boundary of accepted value

LVN: Low Volume Node - expect fast movement through this zone

Color Intensity Interpretation:

Brighter colors = higher volume concentration

Dimmer colors = lower volume

Abrupt color changes = transition between volume zones

Gaps in the histogram = price levels with no trading activity

Technical Details

Volume Accumulation Logic:

For each bar in lookback period:

For each price level:

If bar's high/low range intersects price level:

Add bar's volume to that price level's total

Gradient Algorithm:

Traffic Light: Dual-range piecewise gradient (0-50% and 50-100% volume intensity)

Aurora Glass: Linear cyan-to-magenta interpolation

Obsidian Precision: Dark blue gradient with cyan highlights

Black Ice: Three-stage cyan intensity progression

Real-Time Updates:

The profile recalculates on every bar, including real-time tick data, ensuring the volume distribution always reflects current market structure.

Best Practices

Timeframe Selection: Use higher timeframes (4H, Daily) for swing trading, lower timeframes (5min, 15min) for day trading

Combine with Price Action: Volume profile shows WHERE, price action shows WHEN

Multiple Timeframe Analysis: Check daily VP for major levels, then drill down to intraday for entries

Volume Type Selection: Use "Bullish" volume in uptrends, "Bearish" in downtrends, or "Both" for complete picture

Adjust VA Percentage: 68% (default) captures one standard deviation; try 70% for tighter or 60% for broader value areas

Performance Notes

Maximum bars back: 5000 (handles deep historical analysis)

Maximum boxes: 500 (handles complex profiles)

Optimized calculation: Only recalculates on last bar for efficiency

Real-time capable: Updates as new ticks arrive

RSI Strategy [PrimeAutomation]⯁ OVERVIEW

The RSI Strategy is a momentum-driven trading system built around the behavior of the Relative Strength Index (RSI).

Instead of using traditional overbought/oversold zones, this strategy focuses on RSI breakouts with volatility-based trailing stops, adaptive profit-targets, and optional early-exit logic.

It is designed to capture strong continuation moves after momentum shifts while protecting trades using ATR-based dynamic risk management.

⯁ CONCEPTS

RSI Breakout Momentum: Entries happen when RSI breaks above/below custom thresholds, signaling a shift in momentum rather than mean reversion.

Volatility-Adjusted Risk: ATR defines both stop-loss and profit-target distances, scaling positions based on market volatility.

Dynamic Trailing Stop: The strategy maintains an adaptive trailing level that tightens as price moves in the trade’s favor.

Single-Position System: Only one trade at a time (no pyramiding), maximizing clarity and simplifying execution.

⯁ KEY FEATURES

RSI Signal Engine

• Long when RSI crosses above Upper threshold

• Short when RSI crosses below Lower threshold

These levels are configurable and optimized for trend-momentum detection.

ATR-Based Stop-Loss

A custom ATR multiplier defines the initial stop.

• Long stop = price – ATR × multiplier

• Short stop = price + ATR × multiplier

Stops adjust continuously using a trailing model.

ATR-Based Take Profit (Optional)

Profit targets scale with volatility.

• Long TP = entry + ATR × TP-multiplier

• Short TP = entry – ATR × TP-multiplier

Users can disable TP and rely solely on trailing stops.

Real-Time Trailing Logic

The stop updates bar-by-bar:

• In a long trade → stop moves upward only

• In a short trade → stop moves downward only

This keeps the stop tight as trends develop.

Early Exit Module (Optional)

After X bars in a trade, opposite RSI signals trigger exit.

This reduces holding time during weak follow-through phases.

Full Visual Layer

• RSI plotted with threshold fills

• Entry/TP/Stop visual lines

• Color-coded zones for clarity

⯁ HOW TO USE

Look for RSI Breakouts:

Focus on RSI crossing above the upper boundary (long) or below the lower boundary (short). These moments identify fresh momentum surges.

Use ATR Levels to Manage Risk:

Because stops and targets scale with volatility, the strategy adapts well to both quiet and explosive market phases.

Monitor Trailing Stops for Trend Continuation:

The trailing stop is the primary driver of exits—often outperforming fixed targets by catching larger runs.

Use on Liquid Markets & Mid-Higher Timeframes:

The system performs best where RSI and ATR signals are clean—crypto majors, FX, and indices.

⯁ CONCLUSION

The RSI Strategy is a modern RSI breakout system enhanced with volatility-adaptive risk management and flexible exit logic. It is designed for traders who prefer momentum confirmation over mean reversion, offering a disciplined framework with robust protections and dynamic trend-following capability.

Its blend of ATR-based stops, optional profit targets, and RSI-driven entries makes it a reliable strategy across a wide range of market conditions.

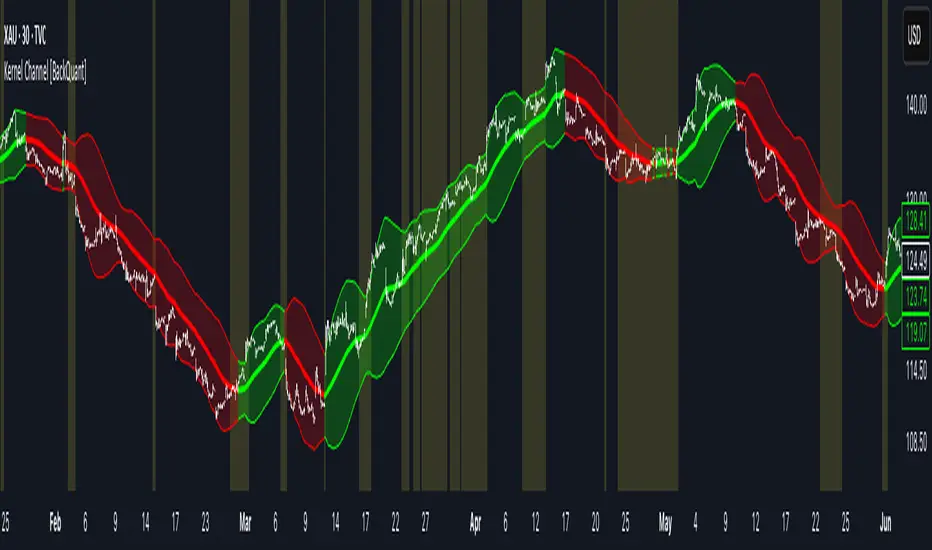

Kernel Channel [BackQuant]Kernel Channel

A non-parametric, kernel-weighted trend channel that adapts to local structure, smooths noise without lagging like moving averages, and highlights volatility compressions, expansions, and directional bias through a flexible choice of kernels, band types, and squeeze logic.

What this is

This indicator builds a full trend channel using kernel regression rather than classical averaging. Instead of a simple moving average or exponential weighting, the midline is computed as a kernel-weighted expectation of past values. This allows it to adapt to local shape, give more weight to nearby bars, and reduce distortion from outliers.

You can think of it as a sliding local smoother where you define both the “window” of influence (Window Length) and the “locality strength” (Bandwidth). The result is a flexible midline with optional upper and lower bands derived from kernel-weighted ATR or kernel-weighted standard deviation, letting you visualize volatility in a structurally consistent way.

Three plotting modes help demonstrate this difference:

When the midline is shown alone, you get a smooth, adaptive baseline that behaves almost like a regression moving average, as shown in this view:

When full channels are enabled, you see how standard deviation reacts to local structure with dynamically widening and tightening bands, a mode illustrated here:

When ATR mode is chosen instead of StdDev, band width reflects breadth of movement rather than variance, creating a volatility-aware envelope like the example here:

Why kernels

Classical moving averages allocate fixed weights. Kernels let the user define weighting shape:

Epanechnikov — emphasizes bars near the current bar, fades fast, stable and smooth.

Triangular — linear decay, simple and responsive.

Laplacian — exponential decay from the current point, sharper reactivity.

Cosine — gentle periodic decay, balanced smoothness for trend filters.

Using these in combination with a bandwidth parameter gives fine control over smoothness vs responsiveness. Smaller bandwidths give sharper local sensitivity, larger bandwidths give smoother curvature.

How it works (core logic)

The indicator computes three building blocks:

1) Kernel-weighted midline

For every bar, a sliding window looks back Window Length bars. Each bar in this window receives a kernel weight depending on:

its index distance from the present

the chosen kernel shape

the bandwidth parameter (locality)

Weights form the denominator, weighted values form the numerator, and the resulting ratio is the kernel regression mean. This midline is the central trend.

2) Kernel-based width

You choose one of two band types:

Kernel ATR — ATR values are kernel-averaged, producing a smooth, volatility-based width that is not dependent on variance. Ideal for directional trend channels and regime separation.

Kernel StdDev — local variance around the midline is computed through kernel weighting. This produces a true statistical envelope that narrows in quiet periods and widens in noisy areas.

Width is scaled using Band Multiplier , controlling how far the envelope extends.

3) Upper and lower channels

Provided midline and width exist, the channel edges are:

Upper = midline + bandMult × width

Lower = midline − bandMult × width

These create smooth structures around price that adapt continuously.

Plotting modes

The indicator supports multiple visual styles depending on what you want to emphasize.

When only the midline is displayed, you get a pure kernel trend: a smooth regression-like curve that reacts to local structure while filtering noise, demonstrated here: This provides a clean read on direction and slope.

With full channels enabled, the behavior of the bands becomes visible. Standard deviation mode creates elastic boundaries that tighten during compressions and widen during turbulence, which you can see in the band-focused demonstration: This helps identify expansion events, volatility clusters, and breakouts.

ATR mode shifts interpretation from statistical variance to raw movement amplitude. This makes channels less sensitive to outliers and more consistent across trend phases, as shown in this ATR variation example: This mode is particularly useful for breakout systems and bar-range regimes.

Regime detection and bar coloring

The slope of the midline defines directional bias:

Up-slope → green

Down-slope → red

Flat → gray

A secondary regime filter compares close to the channel:

Trend Up Strong — close above upper band and midline rising.

Trend Down Strong — close below lower band and midline falling.

Trend Up Weak — close between midline and upper band with rising slope.

Trend Down Weak — close between lower band and midline with falling slope.

Compression mode — squeeze conditions.

Bar coloring is optional and can be toggled for cleaner charts.

Squeeze logic

The indicator includes non-standard squeeze detection based on relative width , defined as:

width / |midline|

This gives a dimensionless measure of how “tight” or “loose” the channel is, normalized for trend level.

A rolling window evaluates the percentile rank of current width relative to past behavior. If the width is in the lowest X% of its last N observations, the script flags a squeeze environment. This highlights compression regions that may precede breakouts or regime shifts.

Deviation highlighting

When using Kernel StdDev mode, you may enable deviation flags that highlight bars where price moves outside the channel:

Above upper band → bullish momentum overextension

Below lower band → bearish momentum overextension

This is turned off in ATR mode because ATR widths do not represent distributional variance.

Alerts included

Kernel Channel Long — midline turns up.

Kernel Channel Short — midline turns down.

Price Crossed Midline — crossover or crossunder of the midline.

Price Above Upper — early momentum expansion.

Price Below Lower — downward volatility expansion.

These help automate regime changes and breakout detection.

How to use it

Trend identification

The midline acts as a bias filter. Rising midline means trend strength upward, falling midline means downward behavior. The channel width contextualizes confidence.

Breakout anticipation

Kernel StdDev compressions highlight areas where price is coiling. Breakouts often follow narrow relative width. ATR mode provides structural expansion cues that are smooth and robust.

Mean reversion

StdDev mode is suitable for fade setups. Moves to outer bands during low volatility often revert to the midline.

Continuation logic

If price breaks above the upper band while midline is rising, the indicator flags strong directional expansion. Same logic for breakdowns on the lower band.

Volatility characterization

Kernel ATR maps raw bar movements and is excellent for identifying regime shifts in markets where variance is unstable.

Tuning guidance

For smoother long-term trend tracking

Larger window (150–300).

Moderate bandwidth (1.0–2.0).

Epanechnikov or Cosine kernel.

ATR mode for stable envelopes.

For swing trading / short-term structure

Window length around 50–100.

Bandwidth 0.6–1.2.

Triangular for speed, Laplacian for sharper reactions.

StdDev bands for precise volatility compression.

For breakout systems

Smaller bandwidth for sharp local detection.

ATR mode for stable envelopes.

Enable squeeze highlighting for identifying setups early.

For mean-reversion systems

Use StdDev bands.

Moderate window length.

Highlight deviations to locate overextended bars.

Settings overview

Kernel Settings

Source

Window Length

Bandwidth

Kernel Type (Epanechnikov, Triangular, Laplacian, Cosine)

Channel Width

Band Type (Kernel ATR or Kernel StdDev)

Band Multiplier

Visuals

Show Bands

Color Bars By Regime

Highlight Squeeze Periods

Highlight Deviation

Lookback and Percentile settings

Colors for uptrend, downtrend, squeeze, flat

Trading applications

Trend filtering — trade only in direction of the midline slope.

Breakout confirmation — expansion outside the bands while slope agrees.

Squeeze timing — compression periods often precede the next directional leg.

Volatility-aware stops — ATR mode makes channel edges suitable for adaptive stop placement.

Structural swing mapping — StdDev bands help locate midline pullbacks vs distributional extremes.

Bias rotation — bar coloring highlights when regime shifts occur.

Notes

The Kernel Channel is not a signal generator by itself, but a structural map. It helps classify trend direction, volatility environment, distribution shape, and compression cycles. Combine it with your entry and exit framework, risk parameters, and higher-timeframe confirmation.

It is designed to behave consistently across markets, to avoid the bluntness of classical averages, and to reveal subtle curvature in price that traditional channels miss. Adjust kernel type, bandwidth, and band source to match the noise profile of your instrument, then use squeeze logic and deviation highlighting to guide timing.

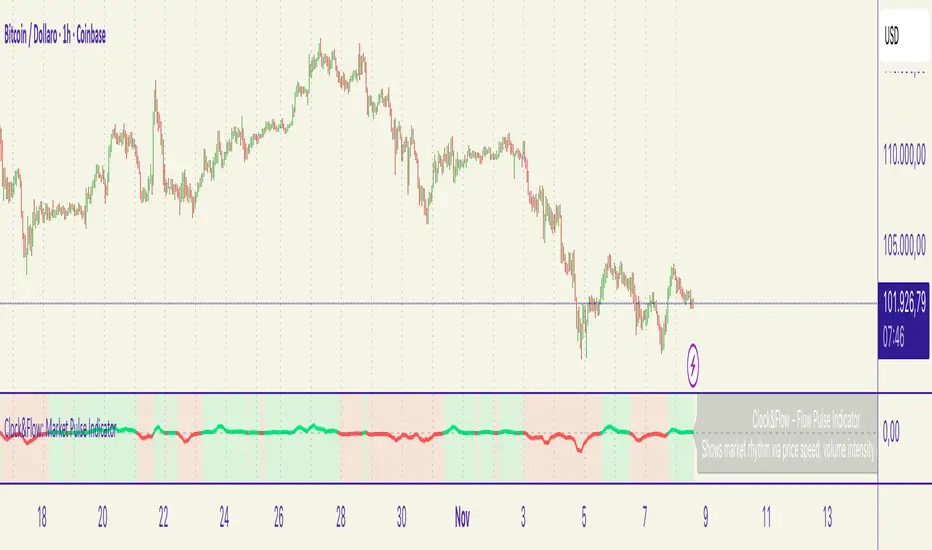

Clock&Flow – Market Pulse IndicatorClock&Flow – Market Pulse Indicator

1) General Purpose

The Market Pulse Indicator is designed to visualize the strength and direction of market flow in a clear, intuitive way.

Unlike common volume or momentum indicators, it blends three essential dimensions — price velocity, normalized volume, and volatility (ATR) — to highlight when market pressure is truly meaningful.

It helps identify genuine liquidity inflows/outflows, potential exhaustion zones, and moments of compression or expansion within the price structure.

2) Data Sources

All data is directly taken from the current chart’s feed on TradingView:

Price (close): to measure relative price change.

Volume: to detect the intensity of market participation (normalized to average).

ATR (Average True Range): to evaluate volatility relative to price levels.

No external data or off-platform sources are used.

3) Logic and Calculation Steps

Price Velocity: calculates the percentage change between the current close and the close N bars ago.

priceChange = (close - close ) / close

Normalized Volume: compares current volume to its moving average over the same period.

volNorm = volume / sma(volume, length)

Normalized Volatility: ATR divided by price to adjust for instrument scale.

atrNorm = atr(length) / close

Combination : multiplies the three components into one raw value that represents market pulse intensity.

rawPulse = priceChange * volNorm * (1 + atrNorm)

Smoothing: a moving average (smoothLen) is applied to create a cleaner and more readable oscillator line.

flowPulse = sma(rawPulse * multiplier, smoothLen)

4) Parameters (Default Settings)

length (20): analysis period for price change, volume, and ATR.

smoothLen (5): smoothing factor; higher values reduce noise.

multiplier (100): scales the output for readability; adjust to fit chart scale.

5) How to Read the Indicator

Market Pulse > 0 (green): net inflow of liquidity; buying pressure dominates.

Market Pulse < 0 (red): net outflow of liquidity; selling pressure dominates.

Near 0: neutral phase; market balance or consolidation.

Sudden peaks: strong bursts of flow — often coincide with news releases or session overlaps.

Confirmations: use as a second-level filter before entering trades or to confirm momentum behind a breakout.

6) Divergences

Divergences between price and Market Pulse are key signals of weakening flow strength:

Bullish divergence: price forms lower lows while Market Pulse forms higher lows → selling pressure is fading; potential reversal or bounce.

Bearish divergence: price forms higher highs while Market Pulse fails to confirm → buying momentum is losing strength; potential correction ahead.

For reliability, look for divergences on higher timeframes (H4, Daily).

On lower timeframes, treat them as early warnings.

7) Typical Use Cases

Breakout confirmation: price breaks resistance with a rising Market Pulse → confirms genuine participation.

False signal filter: price breaks a level but Market Pulse remains flat/negative → likely fake breakout.

Pullback entry: after a breakout, wait for a short retracement and a new positive pulse → safer entry point.

Exit signal: if you’re long and Market Pulse suddenly turns negative with strong volume → consider partial exit or tighter stops.

8) Recommended Timeframes

Intraday / Scalping: 5–30 min charts with length 10–14, smoothLen 3–5.

Swing trading: 1h–4h charts with length 20–50.

Position trading: Daily charts with larger length (50–100) for smoother data.

Always optimize parameters to the specific asset — there are no universal settings.

9) Limitations

This indicator is not a trading system — it’s a decision-support tool.

Results depend on the quality of the volume data available for the symbol.

Performance and sensitivity are influenced by length, smoothing, and multiplier values — always test before live trading.

Use alongside sound risk and money management.

10) Disclaimer

This script is provided for educational purposes only and does not constitute financial advice.

Trading and investing involve significant risk, including the potential loss of capital.

Always test indicators in simulation environments and make independent decisions based on your own analysis and risk tolerance.

Italiano

1) Scopo generale

Flow Pulse è un oscillatore pensato per visualizzare la forza e la direzione del flusso di mercato in modo immediato. Non è un semplice indicatore di volume né una copia di RSI/MACD: combina tre dimensioni fondamentali — variazione di prezzo, volume normalizzato e volatilità — per mettere in evidenza i momenti in cui la pressione dei partecipanti è realmente significativa.

È ideale per identificare: entrate guidate da flussi reali, potenziali esaurimenti, momenti di compressione/espansione del movimento e segnali di conferma per breakout o rimbalzi.

2) Dati utilizzati

L’indicatore usa esclusivamente dati disponibili sulla piattaforma TradingView del grafico corrente:

price (close) — per calcolare la variazione percentuale del prezzo;

volume per misurare l’intensità degli scambi (normalizzato su media);

ATR (Average True Range) — per normalizzare la volatilità rispetto al prezzo;

Tutti i feed (prezzo e volume) sono quelli forniti dall’exchange/fornitore dati collegato al simbolo sul grafico.

3) Logica e passaggi di calcolo

Velocità del prezzo: calcolo della variazione percentuale tra la chiusura corrente e la chiusura N barre fa:

priceChange = (close - close ) / close

— misura la direzione e magnitudine del movimento in termine relativo.

Volume normalizzato: rapporto tra il volume corrente e la media mobile semplice del volume su length barre:

volNorm = volume / sma(volume, length)

— evidenzia volumi anomali rispetto alla media.

Volatilità normalizzata (ATR): rapporto ATR/close per rendere la volatilità comparabile across price levels:

atrNorm = atr(length) / close

Combinazione: il prodotto di questi fattori (con un piccolo offset su ATR) genera un valore grezzo:

rawPulse = priceChange * volNorm * (1 + atrNorm)

— se priceChange e volNorm sono positivi e l’ATR è presente, il rawPulse sarà significativamente positivo.

Smoothing: media mobile semplice (SMA) applicata al rawPulse e moltiplicazione per un fattore scalare (multiplier) per portare il range su livelli leggibili:

flowPulse = sma(rawPulse * multiplier, smoothLen)

4) Parametri esposti (default consigliati)

length (periodo analisi) — default 20: influenza calcolo Δ% e media volumi; allunga la finestra storica.

smoothLen (smussamento) — default 5: smoothing del segnale per ridurre rumore.

multiplier — default 100: fattore di scala per rendere l’oscillatore più leggibile.

5) Interpretazione pratica dei valori

FlowPulse > 0 (verde): predominanza di flusso d’ingresso — pressione d’acquisto. Maggiore il valore, più forte la convinzione (volume + movimento + volatilità).

FlowPulse < 0 (rosso): predominanza di flusso in uscita — pressione di vendita.

Vicino a 0: assenza di flussi netti chiari; mercato piatto o bilanciato.

Picchi repentini: indicano accelerate di flusso — spesso coincidono con rotture, open/close session, news.

Sostegno al trade: usa FlowPulse come conferma prima di entrare su breakout o come avviso di attenzione su esaurimenti.

6) Divergenze (come leggerle)

Le divergenze tra prezzo e FlowPulse sono segnali importanti:

Divergenza rialzista (bullish divergence): prezzo fa nuovi minimi mentre FlowPulse non fa nuovi minimi (o forma minimo relativo più alto) → indica che la spinta di vendita non è supportata da volume/volatilità, possibile inversione/rimbalzo.

Divergenza ribassista (bearish divergence): prezzo fa nuovi massimi mentre FlowPulse non li conferma (o forma massimo relativo più basso) → la spinta d’acquisto è “debole”, possibile esaurimento e inversione.

Note pratiche: cercare divergenze su timeframe maggiori (H4, D) per maggiore attendibilità; sui timeframe minori prendere solo come early warning.

7) Esempi d’uso operativo

Conferma breakout: prezzo rompe resistenza + FlowPulse positivo e crescente → breakout più probabile e con volumi reali.

Filtro per falsi segnali: prezzo rompe ma FlowPulse è piatto/negativo → alto rischio di false breakout.

Entrata per pullback: dopo breakout, attendere un pullback con FlowPulse che torna positivo → ingresso più prudente.

Gestione delle uscite: se sei long e FlowPulse improvvisamente si inverte in negativo su volumi elevati → considerare riduzione posizione o stop.

8) Timeframe consigliati

Intraday / Scalping: M5–M30 con length ridotto (es. 10–14) e smoothLen piccolo.

Swing trading: H1–H4 con length 20–50.

Position trading: D1 con length maggiore per filtrare rumore.

Testa i parametri sul tuo asset e timeframe; nessun parametro è universale.

9) Limitazioni e avvertenze

L’indicatore non è un sistema di trading completo: è un tool di informazione e timing.

Dipende dalla qualità dei dati di volume del simbolo: su alcuni titoli/mercati (es. alcuni ETF, Forex su certi broker) il volume può essere parziale o non rappresentativo.

I valori di margine/multiplier e smoothing influenzano sensibilmente sensibilità e falsi segnali: backtest e ottimizzazione sono raccomandati.

Non usare il solo FlowPulse per entrare su leva elevata senza gestione del rischio12) Disclaimer da inserire

Disclaimer: Questo indicatore è fornito solo a scopo didattico e non costituisce consulenza finanziaria. L’uso comporta rischi: valuta sempre la gestione del rischio e testa su conto demo prima dell’applicazione in reale.

saodisengxiaoyu-lianghua-2.1- This indicator is a modular, signal-building framework designed to generate long and short signals by combining a chosen leading indicator with selectable confirmation filters. It runs on Pine Script version 5, overlays directly on price, and is built to be highly configurable so traders can tailor the signal logic to their market, timeframe, and trading style. It includes a dashboard to visualize which conditions are active and whether they validate a signal, and it outputs clear buy/sell labels and alert conditions so you can automate or monitor trades with confidence.

Core Design

- Leading Indicator: You choose one primary signal generator from a broad list (for example, Range Filter, Supertrend, MACD, RSI, Ichimoku, and many others). This serves as the anchor of the system and determines when a preliminary long or short setup exists.

- Confirmation Filters: You can enable additional filters that validate the leading signal before it becomes actionable. Each “respect…” input toggles a filter on or off. These filters include popular tools like EMA, 2/3 EMA crosses, RQK (Nadaraya Watson), ADX/DMI, Bollinger-based oscillators, MACD variations, QQE, Hull, VWAP, Choppiness Index, Damiani Volatility, and more.

- Signal Expiry: To avoid waiting indefinitely for confirmations, the indicator counts how many consecutive bars the leading condition holds. If confirmations do not align within a defined number of bars, the setup expires. This controls latency and helps reduce late or stale entries.

- Alternating Signals: An optional mode enforces alternation (long must follow short and vice versa), helping avoid repeated entries in the same direction without a meaningful reset.

- Aggregation Logic: The final long/short conditions are formed by combining the leading condition with all selected confirmation filters through logical conjunction. Only if all enabled filters validate the signal (within expiry constraints) does the indicator consider it a confirmed long or short.

- Visualization and Alerts: The script plots buy/sell labels at signal points, provides alert conditions for automation, and displays a compact dashboard summarizing the leading indicator’s status and each confirmation’s pass/fail result using checkmarks.

Leading Indicator Options

- The indicator includes a very large menu of leading tools, each with its own logic to determine uptrend or downtrend impulses. Highlights include:

- Range Filter: Uses a dynamic centerline and bands computed via conditional EMA/SMA and range sizing to define directional movement. It can operate in a default mode or an alternative “DW” mode.

- Rational Quadratic Kernel (RQK): Applies a kernel smoothing model (Nadaraya Watson) to detect uptrends and downtrends with a focus on noise reduction.

- Supertrend, Half Trend, SSL Channel: Classic trend-following tools that derive direction from ATR-based bands or moving average channels.

- Ichimoku Cloud and SuperIchi: Multi-component systems validating trend via cloud position, conversion/base line relationships, projected cloud, and lagging span.

- TSI (True Strength Index), DPO (Detrended Price Oscillator), AO (Awesome Oscillator), MACD, STC (Schaff Trend Cycle), QQE Mod: Momentum and cycle tools that parse direction from crossovers, zero-line behavior, and momentum shifts.

- Donchian Trend Ribbon, Chandelier Exit: Trend and exit tools that can validate breakouts or sustained trend strength.

- ADX/DMI: Measures trend strength and directional movement via +DI/-DI relationships and minimum ADX thresholds.

- RSI and Stochastic: Use crossovers, level exits, or threshold filters to gate entries based on overbought/oversold dynamics or relative strength trends.

- Vortex, Chaikin Money Flow, VWAP, Bull Bear Power, ROC, Wolfpack Id, Hull Suite: A diverse set of directional, momentum, and volume-based indicators to suit different markets and styles.

- Trendline Breakout and Range Detector: Price-behavior filters that confirm signals during breakouts or within defined ranges.

Confirmation Filters

- Each filter is optional. When enabled, it must validate the leading condition for a signal to pass. Examples:

- EMA Filter: Requires price to be above a specified EMA for longs and below for shorts, filtering signals that contradict broader trend or baseline levels.

- 2 EMA Cross and 3 EMA Cross: Enforce moving average cross conditions (fast above slow for long, the reverse for short) or a three-line stacking logic for more stringent trend alignment.

- RQK, Supertrend, Half Trend, Donchian, QQE, Hull, MACD (crossover vs. zero-line), AO (zero line or AC momentum variants), SSL: Each adds its characteristic validation pattern.

- RSI family (MA cross, exits OB/OS zones, threshold levels) plus RSI MA direction and RSI/RSI MA limits: Multiple ways to constrain signals via relative strength behavior and trajectories.

- Choppiness Index and Damiani Volatility: Prevent entries during ranging conditions or insufficient volatility; choppiness thresholds and volatility states gate the trade.

- VWAP, Volume modes (above MA, simple up/down, delta), Chaikin Money Flow: Volume and flow conditions that ensure signals happen in supportive liquidity or accumulation/distribution contexts.

- ADX/DMI thresholds: Demand a minimum trend strength and directional DI alignment to reduce whipsaw trades.

- Trendline Breakout and Range Detector: Confirm that the price is breaking structure or remains within active range consistent with the leading setup.

- By combining several filters you can create strict, conservative entries or looser setups depending on your goals.

Range Filter Engine

- A core building block, the Range Filter uses conditional EMA and SMA functions to compute adaptive bands around a dynamic centerline. It supports two types:

- Type 1: The centerline updates when price exceeds the band thresholds; bands define acceptable drift ranges.

- Type 2: Uses quantized steps (via floor operations) relative to the previous centerline to handle larger moves in discrete increments.

- The engine offers smoothing for range values using a secondary EMA and can switch between raw and averaged outputs. Its hi/lo bands and centerline compose a corridor that defines directional movement and potential breakout confirmation.

Signal Construction

- The script computes:

- leadinglongcond and leadingshortcond : The primary directional signals from the chosen leading indicator.

- longCond and shortCond : Final signals formed by combining the leading conditions with all enabled confirmations. Each confirmation contributes a boolean gate. If a filter is disabled, it contributes a neutral pass-through, keeping the logic intact without enforcing that condition.

- Expiry Logic: The code counts consecutive bars where the leading condition remains true. If confirmations do not line up within the user-defined “Signal Expiry Candle Count,” the setup is abandoned and the signal does not trigger.

- Alternation: An optional state ensures that long and short signals alternate. This can reduce repeated entries in the same direction without a clear reset.

- Finally, longCondition and shortCondition represent the actionable signals after expiry and alternation logic. These drive the label plotting and alert conditions.

Visualization

- Buy and Sell Labels: When longCondition or shortCondition confirm, the script plots annotated labels directly on the chart, making entries easy to see at a glance. The labels use color coding and clear text tags (“long” vs. “short”).

- Dashboard: A table summarizes the status of the leading indicator and all confirmations. Each row shows the indicator label and whether it passed (✔️) or failed (❌) on the current bar. This intensely practical UI helps you diagnose why a signal did or did not trigger, empowering faster strategy iteration and parameter tuning.

- Failed Confirmation Markers: If a setup expires (count exceeds the limit) and confirmations failed to align, the script can mark the chart with a small label and provide a tooltip listing which confirmations did not pass. It’s a helpful audit trail to understand missed trades or prevent “chasing” invalid signals.

- Data Window Values: The script outputs signal states to the data window, which can be useful for debugging or building composite conditions in multi-indicator templates.

Inputs and Parameters

- You control the indicator from a comprehensive input panel:

- Setup: Signal expiry count, whether to enforce alternating signals, and whether to display labels and the dashboard (including position and size).

- Leading Indicator: Choose the primary signal generator from the large list.

- Per-Filter Toggles: For each confirmation, a respect... toggle enables or disables it. Many include sub-options (like MACD type, Stochastic mode, RSI mode, ADX variants, thresholds for choppiness/volatility, etc.) to fine-tune behavior.

- Range Filter Settings: Choose type and behavior; select default vs. DW mode and smoothing. The underlying functions adjust band sizes using ATR, average change, standard deviation, or user-defined scales.

- Because everything is customizable, you can adapt the indicator to different assets, volatility regimes, and timeframes.

Alerts and Automation

- The script defines alert conditions tied to longCondition and shortCondition . You can set these alerts in your chart to trigger notifications or webhook calls for automated execution in external bots. The alert text is simple, and you can configure your own message template when creating alerts in the chart, including JSON payloads for algorithmic integration.

Typical Workflow

- Select a Leading Indicator aligned with your style. For trend following, Supertrend or SSL may be appropriate; for momentum, MACD or TSI; for range/trend-change detection, Range Filter, RQK, or Donchian.

- Add a few key Confirmation Filters that complement the leading signal. For example:

- Pair Supertrend with EMA Filter and RSI MA Direction to ensure trend alignment and positive momentum.

- Combine MACD Crossover with ADX/DMI and Volume Above MA to avoid signals in low-trend or low-liquidity conditions.

- Use RQK with Choppiness Index and Damiani Volatility to only act when the market is trending and volatile enough.

- Set a sensible Signal Expiry Candle Count. Shorter expiry keeps entries timely and reduces lag; longer expiry captures setups that mature slowly.

- Observe the Dashboard during live markets to see which filters pass or fail, then iterate. Tighten or loosen thresholds and filter combinations as needed.

- For automation, turn on alerts for the final conditions and use webhook payloads to notify your trading robot.

Strengths and Practical Notes

- Flexibility: The indicator is a toolkit rather than a single rigid model. It lets you test different combinations rapidly and visualize outcomes immediately.

- Clarity: Labels, dashboard, and failed-confirmation markers make it easy to audit behavior and refine settings without digging into code.

- Robustness: The expiry and alternation options add discipline, avoiding the temptation to enter late or repeatedly in one direction without a reset.

- Modular Design: The logical gates (“respect…”) make the behavior transparent: if a filter is on, it must pass; if it’s off, the signal ignores it. This keeps reasoning clean.

- Avoiding Overfitting: Because you can stack many filters, it’s tempting to over-constrain signals. Start simple (one leading indicator and one or two confirmations). Add complexity only if it demonstrably improves your edge across varied market regimes.

Limitations and Recommendations

- No single configuration is universally optimal. Markets change; tune filters for the instrument and timeframe you trade and revisit settings periodically.

- Trend filters can underperform in choppy markets; likewise, momentum filters can false-trigger in quiet periods. Consider using Choppiness Index or Damiani to gate signals by regime.

- Use expiry wisely. Too short may miss good setups that need a few bars to confirm; too long may cause late entries. Balance responsiveness and accuracy.

- Always consider risk management externally (position sizing, stops, profit targets). The indicator focuses on signal quality; combining it with robust trade management methods will improve results.

Example Configurations

- Trend-Following Setup:

- Leading: Supertrend uptrend for longs and downtrend for shorts.