INFLECTION NEXUS - SPAINFLECTION NEXUS - SPA (Shadow Portfolio Adaptive)

Foreword: The Living Algorithm

For decades, technical analysis has been a conversation between a trader and a static chart. We apply our indicators with their fixed-length inputs, and we hope that our rigid tools can somehow capture the essence of a market that is fluid, chaotic, and perpetually evolving. When our tools fail, we are told to "adapt." But what if the tools themselves could learn that lesson? What if our indicators could adapt not just for us, but with us?

This script, INFLECTION NEXUS - SPA, is the realization of that vision. It is an advanced analytical framework built around a revolutionary core: the Shadow Portfolio Adaptive (SPA) Engine . The buy and sell signals you see on the chart are an evolution of the logic from my previous work, "Turning Point." However, this is not a simple combination of two scripts. The SPA engine so fundamentally transforms the nature of the analysis that it creates an entirely new class of indicator. This publication is a showcase of that groundbreaking, self-learning engine.

This system is undeniably complex. When you first load it, the sheer volume of information may feel overwhelming. That is a testament to the depth of its analysis. This guide is designed to be your comprehensive manual, to break down every single component, every color, every number, into simple, understandable concepts. By the end of this document, you will not only master its functions but will also possess a deeper understanding of the market dynamics it is designed to reveal.

Chapter 1: The Paradigm Shift - Why the SPA Engine is a Leap Forward

To grasp the innovation here, we must first deconstruct the severe limitations of traditional "adaptive" indicators.

Part A: The Traditional Model - Driving by the Rear-View Mirror

Conventional "adaptive" systems are fundamentally reactive. They operate on a slow, inefficient loop: they wait for their own specific, biased signal to fire, wait for that trade to close, and only after a long and statistically significant "warm-up" period of 50-100 trades do they finally make a small, retrospective adjustment. They are always adapting to a market that no longer exists.

Part B: The SPA Model - The Proactive Co-Pilot

The Shadow Portfolio Adaptive (SPA) engine is a complete re-imagining of this process. It is not reactive; it is proactive, data-saturated, and instantly aware.

Continuous, Unbiased Learning: The SPA engine does not wait for a signal to learn. Its Shadow Portfolio is constantly running 5-bar long and short trades in the background. It learns from every single 5-bar slice of market action , giving it a continuous, unbiased stream of performance data. It is the difference between reading a textbook chapter and having a live sparring partner in the ring 24/7.

Instantaneous Market Awareness - The End of the "Warm-Up": This is the critical innovation. The SPA engine does not require a 100-trade warm-up period. The learning does not start after 50 trades; it begins on the 6th bar of the chart when the first shadow trade closes. From that moment on, the system is market-aware, analyzing data, and capable of making intelligent adjustments. The SPA engine is not adapting to old wins and losses. It is adapting, in near real-time, to the market's ever-shifting character, volatility, and personality.

Chapter 2: The Anatomy of the SPA Engine - A Granular Deep Dive

The engine is composed of three primary systems that work in a sophisticated, interconnected symphony.

Section 1: The Shadow Portfolio (The Information Harvester)

What it is, Simply: Think of this as the script's eyes and ears. It's a team of 10 virtual traders (5 long, 5 short) who are constantly taking small, quick trades to feel out the market.

How it Works, Simply: On every new bar, a new "long" trader and a new "short" trader enter the market. Exactly 5 bars later, they close their positions. This cycle is perpetual and relentless.

The Critical 'Why': Because these virtual traders enter and exit based on a fixed time (5 bars), not on a "good" or "bad" signal, their results are completely unbiased . They are simply measuring: "What happened to price over the last 5 bars?" This provides the raw, untainted truth about the market's behavior that the rest of the system needs to learn effectively.

The Golden Metric (ATR Normalization): The engine doesn't just look at dollar P&L. It's smarter than that. It asks a more intelligent question: "How much did this trade make relative to the current volatility?"

Analogy: Imagine a flea and an elephant. If they both jump 1 inch, who is more impressive? The flea. The SPA engine understands this. A $10 profit when the market is dead quiet is far more significant than a $10 profit during a wild, volatile swing.

The Formula: realized_atr = (close - trade.entry) / trade.atr_entry. It takes the raw profit and divides it by the Average True Range (a measure of volatility) at the moment of entry. This gives a pure, "apples-to-apples" score for every single trade, which is the foundational data point for all learning.

Section 2: The Cognitive Map (The Long-Term Brain)

What it is, Simply: This is the engine's deep memory, its library of experiences. Imagine a giant, 64-square chessboard (8x8 grid). Each square on the board represents a very specific type of market environment.

The Two Dimensions of Thought (The 'How'): How does it know which square we are on? It looks at two things:

The Market's Personality (X-Axis): Is the market behaving like a disciplined soldier, marching in a clear trend? Or is it like a chaotic, unpredictable child, running all over the place? The engine calculates a "Regime" score to figure this out.

The Market's Energy Level (Y-Axis): Is the market sleepy and quiet, or is it wide-awake and hyperactive? The engine measures "Normalized Volatility" to determine this.

The Power of Generalization (The 'Why'): When a Shadow Portfolio trade closes, its result is recorded in the corresponding square on the chessboard. But here's the clever part: it also shares a little bit of that lesson with the squares immediately next to it (using a Gaussian Kernel).

Analogy: If you touch a hot stove and learn "don't touch," your brain is smart enough to know you probably shouldn't touch the hot oven door next to it either, even if you haven't touched it directly. The Cognitive Map does the same thing, allowing it to make intelligent inferences even in market conditions it has seen less frequently. Each square remembers what indicator settings worked best in that specific environment.

Section 3: The Adaptive Engine (The Central Nervous System)

What it is, Simply: This is the conductor of the orchestra. It takes information from all other parts of the system and decides exactly what to do.

The Symphony of Inputs: It listens to three distinct sources of information before making a decision:

The Short-Term Memory (Rolling Stats): It looks at the performance of the last rollN shadow trades. This is its immediate, recent experience.

The Long-Term Wisdom (Cognitive Map): It consults the grand library of the Cognitive Map to see what has worked best in the current market type over the long haul.

The Gut Instinct (Bin Learning): It keeps a small "mini-batch" of the most recent trades. If this batch shows a very strong, sudden pattern, it can trigger a rapid, reflexive adjustment, like pulling your hand away from a flame.

The Fusion Process: It then blends these three opinions together in a sophisticated way. It gives more weight to the opinions it's more confident in (e.g., a Cognitive Map square with hundreds of trades of experience) and uses your Adaptation Intensity (dialK) input to decide how much to listen to its "gut instinct." The final decision is then smoothed to ensure the indicator's parameters change in a stable, intelligent way.

Chapter 3: The Control Panel - A Novice's Guide to Every Input

This is the most important chapter. Let's break down what these confusing settings actually do in the simplest terms possible.

--- SECTION 1: THE DRIVER'S SEAT (SIGNAL ENGINE & BASE SETTINGS) ---

🧾 Signal Engine (Turning Point):

What it is: These are the rules for the final BUY and SELL signs.

Think of it like this: The SPA engine is the smart robot that tunes your race car. These settings are you, the driver, telling the robot what kind of race you're in.

Enable Reversal Mode: You tell the robot, "I want to race on a curvy track with lots of turns." The robot will tune the car to be agile for catching tops and bottoms.

Enable Breakout Mode: You tell the robot, "I want to race on a long, straight track." The robot will tune the car for pure speed to follow the trend.

Require New Extreme: This is a quality filter. It tells the driver, "Don't look for a turn unless we've just hit a new top speed on the straightaway." It makes sure the reversal is from a real extreme.

Min Bars Between Signals: This is the "pit stop" rule. You're telling the robot, "After you show me a sign, wait at least 10 bars before showing another one, so I don't get confused."

⚡ ATR Bands (Base Inputs):

What they are: These are the starting settings for your car before the robot starts tuning it. These are your factory defaults.

Sensitivity: This is the "Bump Detector." A low number means the car feels every tiny pebble on the road. A high number means it only notices the big speed bumps. You want to set it so it notices the important bumps (real market structure) but ignores the pebbles (noise).

ATR Period & Multiplier: These set the starting size of the "safety lane" (the green and blue bands) around your car. The robot's main job is to constantly adjust the size of this safety lane to perfectly fit the current road conditions.

📊 & 📈 Filter Settings (RSI & Volume):

What they are: These are your co-pilot's confirmation checks.

Enable RSI Filter: Your co-pilot will check the "Engine Temperature" (RSI). He won't let you hit the gas (BUY) if the engine is already overheating (overbought).

RSI Length & Lookbacks: These tune how your co-pilot's temperature gauge works. The defaults are standard.

Require Volume Spike: Your co-pilot will check the "Crowd Noise" (Volume). He won't give you a signal unless he hears the crowd roar, confirming that a lot of people are interested in this move.

🎯 Signal Quality Control:

Enable Major Levels Only: This tells your co-pilot to be extra picky. He will only confirm signals that happen after a huge, powerful move, ignoring all the small stuff.

--- SECTION 2: THE ROBOT'S BRAIN (ENGINE & LEARNING CONTROLS) ---

🎛️ Master Control:

Adaptation Intensity (dialK): THIS IS THE ROBOT'S PERSONALITY DIAL.

Turn it DOWN (1-5): The robot becomes a "Wise Old Professor." It thinks very slowly and carefully, gathers lots of data, and only makes a change when it is 100% sure. Its advice is very reliable but might come a little late.

Turn it UP (15-20): The robot becomes a "Hyper-Reactive Teenager." It has a short attention span, reacts instantly to everything it sees, and changes its mind constantly. It's super-fast to new information but might get faked out a lot.

The Default (10): A "Skilled Professional." The perfect balance of thoughtful and responsive. Start here.

🧠 Adaptive Engine:

Enable Adaptive System: This is the main power button for your robot. Turn it off, and you're driving a normal, non-smart car. Turn it on, and the robot takes over the tuning.

Use Shadow Cycle: This turns on the robot's "practice laps." The robot can't learn without practicing. This must be on for the robot to work.

Lock ATR Bands: This is a visual choice. "Locked" means the safety lanes on your screen stay where your factory defaults put them (the robot still makes changes to the signals in the background). "Unlocked" means you see the safety lanes moving and changing shape in real-time as the robot tunes them.

🎯 Learning (Global + Risk):

What they are: These are the deep-level settings for how your robot's brain processes information.

Rolling Window Size: This is the robot's "Short-Term Memory." How many of the last few practice laps should it remember? A small number means it only cares about what just happened. A big number means it remembers the last hour of practice.

Learn Rate & Smooth Alpha: This is "How big of a change should the robot make?" and "How smoothly should it make the change?" Think of it as turning the steering wheel. A high learn rate is like yanking the wheel; a low one is like a gentle turn. The smoothing makes sure the turn is graceful.

WinRate Thresholds & PnL Cap: These are rules for the robot's learning. They tell it what a "good" or "bad" outcome looks like and tell it to ignore crazy, once-in-a-lifetime events so its memory doesn't get corrupted.

--- SECTION 3: THE GARAGE (RISK, MEMORY & VISUALS) ---

⚠️ Risk Management:

What they are: These are safety rules you can give to your co-pilot for your own awareness. They appear on the dashboard.

The settings: You can set a max number of trades, a max loss for the day, and a "time out" period after a few losses.

Apply Risk to Shadow: This is an important switch. If you turn this ON, your safety rules also apply to the robot's practice laps. If you hit your max loss, the robot stops practicing and learning. It's recommended to leave this OFF so the robot can learn 24/7, even if you have stopped trading.

🗺️ Cognitive Map, STM & Checkpoints:

What it is: The robot's "Long-Term Memory" or its entire library of racing experience.

Use Cognitive Map & STM: These switches turn on the long-term and short-term memory banks. You want these on for the smartest robot.

Map Settings (Grid, Sigma, Half-Life): These are very advanced settings for neuroscientists. They control how the robot's brain is structured and how it forgets old information. The defaults are expertly tuned.

The Checkpoint System: This is the "Save Your Game" button for the robot.

To Save: Check Emit Checkpoint Now. Go to your alert log, and you will see a very long password. Copy this password.

To Load: Paste that password into the Memory Checkpoint box. Then, check Apply Checkpoint On Next Bar. The robot will instantly download all of its saved memories and experience.

🎨 Visuals & 🧩 Display Params:

What they are: These are all about how your screen looks.

You can control everything: The size and shape of the little diamonds (Entry Orbs), whether you see the purple Adapt Pulse, and where the Dashboards appear on your screen. You can change the Theme to Dark, Light, or Neon. These settings don't change how the robot thinks, only how it presents its information to you.

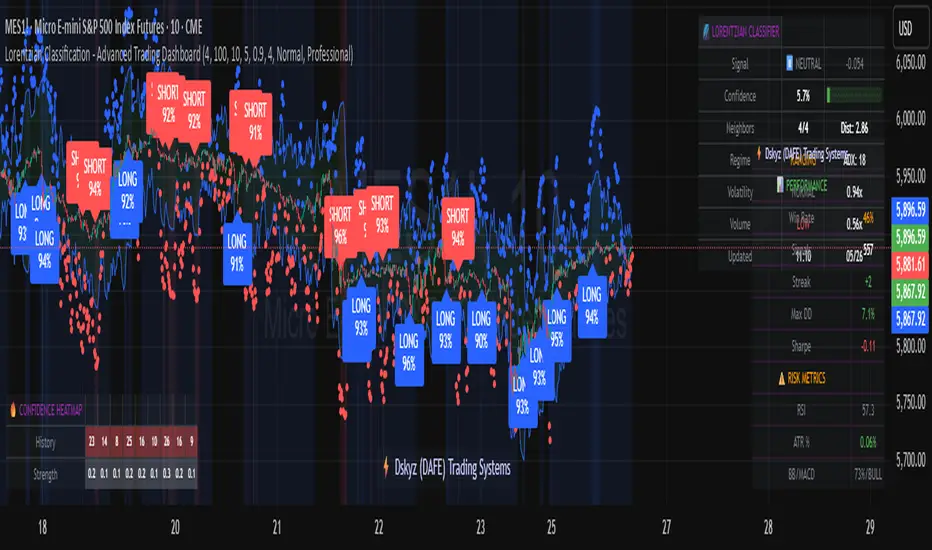

Chapter 4: The Command Center - Decoding the Dashboard

PANEL A (INFLECTION NEXUS): Your high-level mission control, showing the engine's classification of the current Market Context and the performance summary of the Shadow Portfolio.

PANEL B (SHADOW PORTFOLIO ADAPTIVE): Your deep diagnostic screen.

Performance Metrics: View advanced risk-adjusted stats like the Sharpe Ratio to understand the quality of the market movements the engine is learning from.

Adaptive Parameters (Live vs Base): THIS IS THE MOST CRITICAL SECTION. It shows the engine's Live parameters right next to your (Base) inputs. When the Live values deviate, the engine is communicating its learned wisdom to you. For example, a Live ATR Multiplier of 2.5 versus your Base of 1.4 is the engine telling you: "Caution. The market is currently experiencing high fake-outs and requires giving positions more room to breathe." This section is a direct translation of the engine's learning into actionable insight.

Chapter 5: Reading the Canvas - On-Chart Visuals

The Bands (Green/Blue Lines): These are not static Supertrend lines. They are the physical manifestation of the engine's current thinking. As the engine learns and adapts its ATR Period and Multiplier, you will see these bands widen, tighten, and adjust their distance from price. They are alive.

The Labels (BUY/SELL): These are the final output of the "Turning Point" logic, now supercharged and informed by the fully adaptive SPA engine.

The Purple Pulse (Dot and Background Glow): This is your visual cue that the engine is "thinking." Every time you see this pulse, it means the SPA has just completed a learning cycle and updated its parameters. It is actively recalibrating itself to the market.

Chapter 6: A Manifesto on Innovation and Community

I want to conclude with a personal note on why I dedicate countless hours to building systems like this and sharing them openly.

My purpose is to drive innovation, period. I am not in this space to follow the crowd or to re-package old ideas. The world does not need a 100th version of a slightly modified MACD. Real progress, real breakthroughs, come from venturing into the wilderness, from asking "what if?" and from pursuing concepts that lie at the very edge of possibility.

I am not afraid of being wrong. I am not afraid of being bested by my peers. In fact, I welcome it. If another developer takes an idea from this engine, improves it, and builds something even more magnificent, that is a profound win for our entire community. The only failure I recognize is the failure to try. The only trap I fear is the creative complacency of producing sterile, recycled work just to appease the status quo.

I love this community, and I believe with every fiber of my being that we have barely scratched the surface of what can be discovered and created. This script is my contribution to that shared journey. It is a tool, an idea, and a challenge to all of us: let's keep pushing.

DISCLAIMER: This script is an advanced analytical tool provided for educational and research purposes ONLY. It does not constitute financial advice. All trading involves substantial risk of loss. Past performance is not indicative of future results. Please use this tool responsibly and as part of a comprehensive trading plan.

As the great computer scientist Herbert A. Simon, a pioneer of artificial intelligence, famously said:

"Learning is any process by which a system improves performance from experience."

*Tooltips were updated with a comprehensive guide

May this engine enhance your experience.

— Dskyz, for DAFE Trading Systems

Cari dalam skrip untuk "deep股票代码"

Sector Rotation & Money Flow Dashboard📊 Overview

The Sector Rotation & Money Flow Dashboard is a comprehensive market analysis tool that tracks 39 major sector ETFs in real-time, providing institutional-grade insights into sector rotation, momentum shifts, and money flow patterns. This indicator helps traders identify which sectors are attracting capital, which are losing favor, and where the next opportunities might emerge.

Perfect for swing traders, position traders, and investors who want to stay ahead of sector rotation and ride the strongest trends while avoiding weak sectors.

🎯 What This Indicator Does

Tracks 39 Major Sectors: From technology to utilities, cryptocurrencies to commodities

Calculates Multiple Timeframes: 1-week, 1-month, 3-month, and 6-month performance

Advanced Momentum Metrics: Proprietary momentum score and acceleration calculations

Relative Strength Analysis: Compare sector performance against any benchmark index

Money Flow Signals: Visual indicators showing where institutional money is moving

Smart Filtering: Pre-built strategy filters for different trading styles

Trend Detection: Emoji-based visual system for quick trend identification

💡 Key Features

1. Performance Metrics

Multiple timeframe analysis (1W, 1M, 3M, 6M)

Month-over-month change tracking

Relative strength vs benchmark index

2. Advanced Analytics

Momentum Score: Weighted composite of recent performance

Acceleration: Rate of change in momentum (second derivative)

Money Flow Signals: IN/OUT/TURN/WATCH indicators

3. Strategy Preset Filters

🎯 Swing Trade: High momentum opportunities

📈 Trend Follow: Established uptrends

🔄 Mean Reversion: Oversold bounce candidates

💎 Value Hunt: Deep value opportunities

🚀 Breakout: Emerging strength

⚠️ Risk Off: Sectors to avoid

4. Customization

All 39 sector ETFs can be customized

Adjustable benchmark index

Flexible display options

Multiple sorting methods

📋 Settings Documentation

Display Settings

Show Table (Default: On)

Toggles the entire dashboard display

Table Position (Default: Middle Center)

Choose from 9 positions on your chart

Options: Top/Middle/Bottom × Left/Center/Right

Rows to Show (Default: 15)

Number of sectors displayed (5-40)

Useful for focusing on top/bottom performers

Sort By (Default: Momentum)

1M/3M/6M: Sort by specific timeframe performance

Momentum: Weighted recent performance score

Acceleration: Rate of momentum change

1M Change: Month-over-month improvement

RS: Relative strength vs benchmark

Flow: IN First: Prioritize sectors with inflows

Flow: TURN First: Focus on reversal candidates

Recovery Plays: Oversold sectors recovering

Oversold Bounce: Deepest declines with positive signs

Top Gainers/Losers 3M: Best/worst quarterly performers

Best Acc + Mom: Combined strength score

Worst Acc (Topping): Sectors losing momentum

Filter Settings

Strategy Preset Filter (Default: All)

All: No filtering

🎯 Swing Trade: Mom >5, Acc >2, Money flowing in

📈 Trend Follow: Positive 1M & 3M, RS >0

🔄 Mean Reversion: Oversold but improving

💎 Value Hunt: Down >10% with recovery signs

🚀 Breakout: Rapid momentum surge

⚠️ Risk Off: Declining or topping sectors

Custom Flow Filter: Use manual flow filter

Custom Flow Signal Filter (Default: All)

Only active when Strategy Preset = "Custom Flow Filter"

IN Only: Strong inflows

TURN Only: Reversal signals

WATCH Only: Recovery candidates

OUT Only: Outflow sectors

Active Flows Only: Any non-neutral signal

Hide Low Volume ETFs (Default: Off)

Filters out illiquid sectors (future enhancement)

Visual Settings

Show Trend Emojis (Default: On)

🚀 Breakout (Strong 1M + High Acceleration)

🔥 Hot Recovery (From -10% to positive)

💪 Steady Uptrend (All timeframes positive)

➡️ Sideways/Ranging

⚠️ Warning/Topping (Up >15%, now slowing)

📉 Falling (Negative + declining)

🔄 Bottoming (Improving from lows)

Compact Mode (Default: Off)

Removes decimals for cleaner display

Useful when showing many rows

Min Data Points Required (Default: 3)

Minimum data points needed to display a sector

Prevents showing sectors with insufficient data

Relative Strength Settings

RS Benchmark Index (Default: AMEX:SPY)

Index to compare all sectors against

Can use SPY, QQQ, IWM, or any other index

RS Period (Days) (Default: 21)

Lookback period for RS calculation

21 days = 1 month, 63 days = 3 months, etc.

Sector ETF Settings (Groups 1-39)

Each sector has two inputs:

Symbol: The ticker (e.g., "AMEX:XLF")

Name: Display name (e.g., "Financials")

All 39 sectors can be customized to track different ETFs or markets.

📈 Column Explanations

Sector: ETF name/description

1M%: 1-month (21-day) performance

3M%: 3-month (63-day) performance

6M%: 6-month (126-day) performance

Mom: Momentum score (weighted average, recent-biased)

Acc: Acceleration (momentum rate of change)

Δ1M: Month-over-month change

RS: Relative strength vs benchmark

Flow: Money flow signal

↗️ IN: Strong inflows

🔄 TURN: Potential reversal

👀 WATCH: Recovery candidate

↘️ OUT: Outflows

—: Neutral

🎮 Usage Tips

For Swing Traders (3-14 days)

Use "🎯 Swing Trade" filter

Sort by "Acceleration" or "Momentum"

Look for Flow = "IN" and Mom >10

Confirm with positive RS

For Position Traders (2-8 weeks)

Use "📈 Trend Follow" filter

Sort by "RS" or "Best Acc + Mom"

Focus on consistent green across timeframes

Ensure RS >3 for market leaders

For Value Investors

Use "💎 Value Hunt" filter

Sort by "Recovery Plays" or "Top Losers 3M"

Look for improving Δ1M

Check for "WATCH" or "TURN" signals

For Risk Management

Regularly check "⚠️ Risk Off" filter

Sort by "Worst Acc (Topping)"

Review holdings for ⚠️ warning emojis

Exit sectors showing "OUT" flow

Market Regime Recognition

Bull Market: Many sectors showing "IN" flow, positive RS

Bear Market: Widespread "OUT" flows, negative RS

Rotation: Mixed flows, some "IN" while others "OUT"

Recovery: Multiple "TURN" and "WATCH" signals

🔧 Pro Tips

Combine Filters + Sorting: Filter first to narrow candidates, then sort to prioritize

Multi-Timeframe Confirmation: Best setups show alignment across 1M, 3M, and momentum

RS is Key: Sectors outperforming SPY (RS >0) tend to continue outperforming

Acceleration Matters: Positive acceleration often precedes price breakouts

Flow Transitions: "WATCH" → "TURN" → "IN" progression identifies new trends early

Regular Scans:

Daily: Check "Acceleration" sort

Weekly: Review "1M Change"

Monthly: Analyze "RS" shifts

Divergence Signals:

Price up but Acceleration down = Potential top

Price down but Acceleration up = Potential bottom

Sector Pairs Trading: Long sectors with "IN" flow, short sectors with "OUT" flow

⚠️ Important Notes

This indicator makes 40 security requests (maximum allowed)

Best used on Daily timeframe

Data updates in real-time during market hours

Some ETFs may show "—" if data is unavailable

🎯 Common Strategies

"Follow the Flow"

Only trade sectors showing "IN" flow with positive RS

"Rotation Catcher"

Focus on "TURN" signals in sectors down >15% from highs

"Momentum Rider"

Trade top 3 sectors by Momentum score, exit when Acceleration turns negative

"Mean Reversion"

Buy sectors in bottom 20% by 3M performance when Δ1M improves

"Relative Strength Leader"

Maintain positions only in sectors with RS >5

Not financial advice - always do additional research

Inflection PointInflection Point - The Adaptive Confluence Reversal Engine

This is not just another peak and valley indicator; it is a complete and total reimagining of how market turning points are detected, qualified, and acted upon. Born from the foundational concepts explored in systems like my earlier creation, DAFE - Turning Point, Inflection Point is a ground-up engineering feat designed for the modern trader. It moves beyond static rules and simple pattern recognition into the realm of dynamic, multi-factor confluence analysis and adaptive machine learning.

Where other indicators provide a guess, Inflection Point provides a probability. It meticulously analyzes the market's deepest currents—momentum, exhaustion, and reversal velocity—and fuses them into a single, unified "Confluence Score." This is not a simple combination of indicators; it is an intelligent, weighted system where each component works in concert, creating an analytical engine that is orders of magnitude more sophisticated and reliable than any standard reversal tool.

Furthermore, Inflection Point learns. Through its advanced Adaptive Learning Engine, it constantly monitors its own performance, adjusting its confidence and selectivity in real-time based on its recent success rate. This allows it to adapt its behavior to any security, on any timeframe, with remarkable success.

Theoretical Foundation - Confluence Core

Inflection Point's predictive power does not come from a single, magical formula. It comes from the intelligent synthesis of three critical market phenomena, weighted and scored in real-time to generate a single, high-conviction probability rating.

1. Factor One: Pre-Reversal Momentum State (RSI Analysis)

Instead of reacting to a simple RSI cross, Inflection Point proactively scans for the build-up of momentum that precedes a reversal.

• Formulaic Concept: It measures the highest RSI value over a lookback period for peaks and the lowest RSI for valleys. A signal is only considered valid if significant momentum has been established before the turn, indicating a stretched market condition ripe for reversal.

• Asymmetric Sophistication: The engine uses different, optimized thresholds for bull and bear momentum, recognizing that markets often fall faster than they rise.

2. Factor Two: Volatility Exhaustion (Bollinger Band Analysis)

A true reversal often occurs when price makes a final, exhaustive push into unsustainable territory.

• Formulaic Concept: The engine detects when price has significantly pierced the outer Bollinger Bands. This is not just a touch, but a statistical deviation from the mean that signals volatility exhaustion, where the energy for the current move is likely depleted.

3. Factor Three: Reversal Strength (Rate of Change Analysis)

The character of a reversal matters. A sharp, decisive turn is more significant than a slow, meandering one.

• Formulaic Concept: Using a short-term Rate of Change (ROC), the engine measures the velocity of the reversal itself. A higher ROC score adds significant weight to the final probability, confirming that the new direction has conviction.

4. The Final Calculation: The Adaptive Learning Engine

This is the system's "brain." It maintains a history of its past signals and calculates its real-time win rate. This hitRate is then used to generate an adaptiveMultiplier.

• Self-Correction: In "Quality Control" mode, a high win rate makes the indicator more selective, demanding a higher probability score to issue a signal, thereby protecting streaks. A lower win rate makes it slightly less selective to ensure it continues learning from new market conditions.

• The result is a system that is not static, but a living, breathing tool that adapts its personality to the unique rhythm of any chart.

Why Inflection Point is a Paradigm Shift

Inflection Point is fundamentally different from other reversal indicators for three key reasons:

Confluence Over Isolation: Standard indicators look at one thing (e.g., RSI > 70). Inflection Point simultaneously analyzes momentum, volatility, and velocity, understanding that true reversals are a product of multiple converging factors. It answers not just "if," but "why" a reversal is likely.

Probabilistic Over Binary: Other tools give you a simple "yes" or "no." Inflection Point provides a probability score from 0-100, allowing you to gauge the conviction of every potential signal. This empowers you to differentiate between a weak setup and an A+ opportunity.

Adaptive Over Static: Every other indicator uses the same rules forever. Inflection Point's Adaptive Engine means it is constantly refining its own logic based on what is actually working in the current market, on the specific asset you are trading. It is tailored to the now.

The Inputs Menu - Your Command Center

Every setting is a lever of control, allowing you to tune the engine to your precise trading style and market focus.

🧠 Neural Core Engine

Analysis Depth: This is the primary lookback for the Bollinger Band and other core calculations. A shorter depth makes the indicator faster and more sensitive, ideal for scalping. A longer depth makes it slower and more stable, ideal for swing trading.

Minimum Probability %: This is your master signal filter. It sets the minimum Confluence Score required to plot a signal. Higher values (85-95) will give you only the highest-conviction A+ setups. Lower values (70-80) will show more potential opportunities.

🤖 Adaptive Neural Learning

Enable Adaptive Learning Engine: Toggles the entire learning system. Disabling it will make the indicator's logic static.

Peak/Valley Success Threshold (ATR): This defines what constitutes a "successful" trade for the learning engine. A value of 1.5 means price must move 1.5x the ATR in your favor for the signal to be marked as a win. Adjust this to match your personal take-profit strategy.

Adaptive Mode: This dictates how the engine uses its hitRate. "Quality Control" is recommended for its intelligent filtering. "Aggressive" will always boost signal scores, useful for finding more setups in a known, trending environment.

Asymmetric Balance: Allows you to apply a "boost" to either peak (short) or valley (long) signals. If you find the market you're trading has stronger long reversals, you can increase the "Valley Signal Boost" to catch them more effectively.

🛡️ Elite Filters

Market Noise Filter: An exceptional tool for avoiding choppy markets. It counts the number of directional changes in the last 5 bars. If the market is whipping back and forth too much, it will block the signal. Lower the "Max Direction Changes" to be extremely selective.

Volume Filter: Requires signal confirmation from a significant volume spike. The "Volume Multiplier" dictates how large this spike must be (e.g., 1.2 = 20% above average volume). This is invaluable for filtering out low-conviction moves in stocks and crypto.

The Dashboard - Your Analytical Co-Pilot

The dashboard is not just a set of numbers; it is a holistic overview of the market's health and the engine's current state.

Unified AI Score: This section provides the most critical, at-a-glance information. "Total Score" is the current probability reading, while "Quality" gives you a human-readable interpretation. "Win Rate" shows the real-time performance of the Adaptive Engine.

Order Flow (OFPI): This measures the "weight" of money behind recent price moves by analyzing price change relative to volume. A high positive OFPI suggests strong buying pressure, while a high negative value suggests strong selling pressure. It gives you a peek into the market's underlying flow.

Component Analysis: This allows you to see the individual "Peak" and "Valley" confidence scores before they are filtered, giving you insight into building momentum before a signal forms.

Market Structure: This panel assesses the broader environment. "HTF Trend" tells you the direction of the larger trend (based on EMAs), while "Vol Regime" tells you if the market is in a high, medium, or low volatility state. Use this to align your signals with the broader market context.

Filter & Engine Statistics: Available on the "Large" dashboard, this provides deep insight into how many signals are being blocked by your filters and the current status of the Adaptive Engine's multiplier.

The Visual Interface - A Symphony of Data

Every visual element on the chart is designed for instant interpretation and insight.

Signal Markers: Simple, clean triangles mark the exact bar of a valid signal. A box is drawn around the high/low of the signal bar to highlight the precise point of inflection.

Dynamic Support/Resistance Zones: These are the glowing lines on your chart. They are not static lines; they are dynamic levels that represent the current battlefield between buyers and sellers.

Cyber Cyan (Valley Blue): This is the current Support Zone. This is the price level the market is currently trying to defend.

Neural Pink (Peak Red): This is the current Resistance Zone. This is the price level the market is currently trying to break through.

Grey (Next Level): This line is a projection, based on the current momentum and the size of the S/R range, of where the next major level of conflict will likely be. It acts as a potential price target.

Development & Philosophy

Inflection Point was not assembled; it was engineered. It represents hundreds of hours of research into market dynamics, statistical analysis, and machine learning principles. The goal was to create a tool that moves beyond the limitations of traditional technical analysis, which often fails in modern, algorithm-driven markets. By building a system based on multi-factor confluence and self-adaptive logic, Inflection Point provides a quantifiable, statistical edge that is simply unattainable with simpler tools. This is the result of a relentless pursuit of a better, more intelligent way to trade.

Universal Applicability

The principles of momentum, exhaustion, and velocity are universal to all freely traded markets. Because of its adaptive core and robust filtering options, Inflection Point has proven to be exceptionally effective on any security (stocks, crypto, forex, indices, futures) and on any timeframe (from 1-minute scalping charts to daily swing trading charts).

" Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected. "

— George Soros

Trade with insight. Trade with anticipation.

— Dskyz, for DAFE Trading Systems

Hosoda’s CloudsMany investors aim to develop trading systems with a high win rate, mistakenly associating it with substantial profits. In reality, high returns are typically achieved through greater exposure to market trends, which inevitably lowers the win rate due to increased risk and more volatile conditions.

The system I present, called “Hosoda’s Clouds” in honor of Goichi Hosoda , the creator of the Ichimoku Kinko Hyo indicator, is likely one of the first profitable systems many traders will encounter. Designed to capture trends, it performs best in markets with clear directional movements and is less suitable for range-bound markets like Forex, which often exhibit lateral price action.

This system is not recommended for low timeframes, such as minute charts, due to the random and emotionally driven nature of price movements in those periods. For a deeper exploration of this topic, I recommend reading my article “Timeframe is Everything”, which discusses the critical importance of selecting the appropriate timeframe.

I suggest testing and applying the “Hosoda’s Clouds” strategy on assets with a strong trending nature and a proven track record of performance. Ideal markets include Tesla (1-hour, 4-hour, and daily), BTC/USDT (daily), SPY (daily), and XAU/USD (daily), as these have consistently shown clear directional trends over time.

Commissions and Configuration

Commissions can be adjusted in the system’s settings to suit individual needs. For evaluating the effectiveness of “Hosoda’s Clouds,” I’ve used a standard commission of $1 per order as a baseline, though this can be modified in the code to accommodate different brokers or preferences.

The margin per trade is set to $1,000 by default, but users are encouraged to experiment with different margin settings in the configuration to match their trading style.

Rules of the “Hosoda’s Clouds” System (Bullish Strategy)

This strategy is designed to capture trending movements in bullish markets using the Ichimoku Kinko Hyo indicator. The rules are as follows:

Long Entry: A long position is triggered when the Tenkan-sen crosses above the Kijun-sen below the Ichimoku cloud, identifying potential reversals or bounces in a bearish context.

Stop Loss (SL): Placed at the low of the candle 12 bars prior to the entry candle. This setting has proven optimal in my tests, but it can be adjusted in the code based on risk tolerance.

Take Profit (TP): The position is closed when the Tenkan-sen crosses below the bottom of the Ichimoku cloud (the minimum of Senkou Span A and Senkou Span B).

Notes on the Code

margin_long=0: Ideal for strategies requiring a fixed position size, particularly useful for manual entries or testing with a constant capital allocation.

margin_long=100: Recommended for high-frequency systems where positions are closed quickly, simulating gradual growth based on realized profits and reflecting real-world broker constraints.

System Performance

The following performance metrics account for $1 per order commissions and were tested on the specified assets and timeframes:

Tesla (H1)

Trades: 148

Win Rate: 29.05%

Period: Jan 2, 2014 – Jan 6, 2020 (+172%)

Simple Annual Growth Rate: +34.3%

Trades: 130

Win Rate: 30.77%

Period: Jan 2, 2020 – Sep 24, 2025 (+858.90%)

Simple Annual Growth Rate: +150.7%

Tesla (H4)

Trades: 102

Win Rate: 32.35%

Period: Jun 29, 2010 – Sep 24, 2025 (+11,356.36%)

Simple Annual Growth Rate: +758.5%

Tesla (Daily)

Trades: 56

Win Rate: 35.71%

Period: Jun 29, 2010 – Sep 24, 2025 (+3,166.64%)

Simple Annual Growth Rate: +211.5%

BTC/USDT (Daily)

Trades: 44

Win Rate: 31.82%

Period: Sep 30, 2017 – Sep 24, 2025 (+2,592.23%)

Simple Annual Growth Rate: +324.8%

SPY (Daily)

Trades: 81

Win Rate: 37.04%

Period: Jan 23, 1993 – Sep 24, 2025 (+476.90%)

Simple Annual Growth Rate: +14.3%

XAU/USD (Daily)

Trades: 216

Win Rate: 32.87%

Period: Jan 6, 1833 – Sep 24, 2025 (+5,241.73%)

Simple Annual Growth Rate: +27.1%

SPX (Daily)

Trades: 217

Win Rate: 38.25%

Period: Feb 1, 1871 – Sep 24, 2025 (+16,791.02%)

Simple Annual Growth Rate: +108.1%

Conclusion

With the “ Hosoda’s Clouds ” strategy, I aim to showcase the potential of technical analysis to generate consistent profits in trending markets, challenging recent doubts about its effectiveness. My goal is for this system to serve as both a practical tool for traders and a source of inspiration for the trading community I deeply respect. I hope it encourages the creation of new strategies, fosters creativity in technical analysis, and empowers traders to approach the markets with confidence and discipline.

Real 10Y Yield (DGS10 - T10YIE)The Real 10Y Yield (DGS10 – T10YIE) indicator computes the inflation-adjusted U.S. 10-year Treasury yield by subtracting the 10-year breakeven inflation rate (T10YIE) from the nominal 10-year Treasury yield (DGS10), both sourced directly from FRED. By filtering out inflation expectations, this script reveals the true, real borrowing cost over a 10-year horizon—one of the most reliable gauges of overall risk sentiment and capital–market health.

How It Works

Data Inputs

• DGS10 (Nominal 10-Year Treasury Yield)

• T10YIE (10-Year Breakeven Inflation Rate)

Both series are fetched on a daily timeframe via request.security from FRED.

Real Yield Calculation

pine

Copy

Edit

real10y = DGS10 – T10YIE

A positive value indicates that nominal yields exceed inflation expectations (real yields are positive), while a negative value signals deep-negative real rates.

Thresholds & Coloring

• Bullish Zone: Real yield < –0.1 %

• Bearish Zone: Real yield > +0.1 %

The background turns green when real yields drop below –0.1 %, reflecting an ultra-accommodative environment that historically aligns with risk-on rallies. It turns red when real yields exceed +0.1 %, indicating expensive real borrowing costs and a potential shift toward risk-off.

Alerts

• Deep-Negative Real Yields (Bullish): Triggers when real yield < –0.1 %

• High Real Yields (Bearish): Triggers when real yield > +0.1 %

Why It’s Powerful

Forward-Looking Sentiment Gauge

Real yields incorporate both market-implied inflation and nominal rates, making them a leading indicator for risk appetite, equity flows, and crypto demand.

Clear, Actionable Zones

The –0.1 % / +0.1 % thresholds cleanly delineate structurally bullish vs. bearish regimes, removing noise and false signals common in nominal-only yield studies.

Macro & Cross-Asset Confluence

Combine with equity indices, dollar strength (DXY), or credit spreads for a fully contextual macro view. When real yields break deeper negative alongside weakening dollar, it often precedes stretch in risk assets.

Automatic Alerts

Never miss regime shifts—alerts notify you the moment real yields breach key zones, so you can align your strategy with prevailing macro momentum.

How to Use

Add to a separate pane for unobstructed visibility.

Monitor breaks beneath –0.1 % for early “risk-on” signals in stocks, commodities, and crypto.

Watch for climbs above +0.1 % to hedge or rotate into defensive assets.

Combine with your existing trend-following or mean-reversion strategies to improve timing around major market turning points.

–––

Feel free to adjust the threshold lines to your preferred sensitivity (e.g., tighten to ±0.05 %), or overlay with moving averages to smooth out whipsaws. This script is ideal for macro traders, portfolio managers, and quantitative quants who demand a distilled, inflation-adjusted view of real rates.

True Breakout Pattern [TradingFinder] Breakout Signal Indicator🔵 Introduction

In many market conditions, what initially appears to be a decisive breakout often turns out to be nothing more than a false breakout or fake breakout. Price breaks through a key swing level or an important support and resistance zone, only to quickly return to its previous range.

These failed breakouts, which are often the result of liquidity traps or market manipulation, serve more as a warning sign of structural weakness than confirmation of a new trend.

This indicator is designed around the concept of the fake breakout.

The logic is simple but precise : when price breaks a swing level and returns to that level within a maximum of five candles, the move is considered a false breakout. At this point, a Fibonacci retracement is applied to the recent price swing to evaluate the pullback area.

If price, within ten candles after the return to the breakout level, enters the Fibonacci zone between 0.618 and 1.0, the setup becomes valid for a potential entry. This area is identified as a long entry zone, with the stop loss placed just beyond the 1.0 level and the take profit defined based on the desired risk-to-reward ratio.

By combining accurate detection of false breakouts, analysis of price reaction to swing levels, and alignment with Fibonacci retracement logic, this framework allows traders to identify opportunities often missed by others. In a market where failed breakouts are a common and recurring phenomenon, this indicator aims to transform these traps into measurable trading opportunities.

Long Setup :

Short Setup :

🔵 How to Use

This indicator operates based on the recognition of false breakouts from structural levels in the market, specifically swing levels, and combines that with Fibonacci retracement analysis.

In this strategy, trades are only considered when price returns to the broken level within a defined time window and reacts appropriately inside a predefined Fibonacci range. Depending on the direction of the initial breakout, the system outlines two scenarios for long and short setups.

🟣 Long Setup

In the long setup, price initially breaks below a support level or swing low. If the price returns to the broken level within a maximum of five candles, the move is identified as a fake breakout.

At this stage, a Fibonacci retracement is drawn from the recent high to the low. If price, within ten candles of returning to the level, moves into the 0.618 to 1.0 Fibonacci zone, the conditions for a long entry are met.

The stop loss is placed slightly below the 1.0 level, while the take profit is set based on the trader’s preferred risk-reward ratio. This setup aims to capture deeply discounted entries at low risk, aligned with smart money reversals.

🟣 Short Setup

In the short setup, the price breaks above a resistance level or swing high. If the price returns to that level within five candles, the move is again treated as a false breakout. Fibonacci is then drawn from the recent low to the high to observe the retracement area.

Should price enter the 0.618 to 1.0 Fibonacci range within ten candles of returning, a short entry is considered valid. In this case, the stop loss is placed just above the 1.0 level, and the take profit is adjusted based on the intended risk-reward target. This method allows traders to identify high-probability short setups by focusing on failed breakouts and deep pullbacks.

🔵 Settings

🟣 Logical settings

Swing period : You can set the swing detection period.

Valid After Trigger Bars : Limits how many candles after a fake breakout the entry zone remains valid.

Max Swing Back Method : It is in two modes "All" and "Custom". If it is in "All" mode, it will check all swings, and if it is in "Custom" mode, it will check the swings to the extent you determine.

Max Swing Back : You can set the number of swings that will go back for checking.

🟣 Display settings

Displaying or not displaying swings and setting the color of labels and lines.

🟣 Alert Settings

Alert False Breakout : Enables alerts for Breakout.

Message Frequency : Determines the frequency of alerts. Options include 'All' (every function call), 'Once Per Bar' (first call within the bar), and 'Once Per Bar Close' (final script execution of the real-time bar). Default is 'Once per Bar'.

Show Alert Time by Time Zone : Configures the time zone for alert messages. Default is 'UTC'.

🔵 Conclusion

A sound understanding of the false breakout phenomenon and its relationship to structural price behavior is essential for technical traders aiming to improve precision and consistency. Many poor trading decisions stem from misinterpreting failed breakouts and entering too early into weak signals.

A structured approach, grounded in the analysis of swing levels and validated through specific price action and timing rules, can turn these misleading moves into valuable trade opportunities.

This indicator, by combining fake breakout detection with time filters and Fibonacci-based retracement zones, helps traders only engage with the market when multiple confirming factors are in alignment. The result is a strategy that emphasizes probability, risk control, and clarity in decision-making, offering a solid edge in navigating today’s volatile markets.

Lyapunov Market Instability (LMI)Lyapunov Market Instability (LMI)

What is Lyapunov Market Instability?

Lyapunov Market Instability (LMI) is a revolutionary indicator that brings chaos theory from theoretical physics into practical trading. By calculating Lyapunov exponents—a measure of how rapidly nearby trajectories diverge in phase space—LMI quantifies market sensitivity to initial conditions. This isn't another oscillator or trend indicator; it's a mathematical lens that reveals whether markets are in chaotic (trending) or stable (ranging) regimes.

Inspired by the meditative color field paintings of Mark Rothko, this indicator transforms complex chaos mathematics into an intuitive visual experience. The elegant simplicity of the visualization belies the sophisticated theory underneath—just as Rothko's seemingly simple color blocks contain profound depth.

Theoretical Foundation (Chaos Theory & Lyapunov Exponents)

In dynamical systems, the Lyapunov exponent (λ) measures the rate of separation of infinitesimally close trajectories:

λ > 0: System is chaotic—small changes lead to dramatically different outcomes (butterfly effect)

λ < 0: System is stable—trajectories converge, perturbations die out

λ ≈ 0: Edge of chaos—transition between regimes

Phase Space Reconstruction

Using Takens' embedding theorem , we reconstruct market dynamics in higher dimensions:

Time-delay embedding: Create vectors from price at different lags

Nearest neighbor search: Find historically similar market states

Trajectory evolution: Track how these similar states diverged over time

Divergence rate: Calculate average exponential separation

Market Application

Chaotic markets (λ > threshold): Strong trends emerge, momentum dominates, use breakout strategies

Stable markets (λ < threshold): Mean reversion dominates, fade extremes, range-bound strategies work

Transition zones: Market regime about to change, reduce position size, wait for confirmation

How LMI Works

1. Phase Space Construction

Each point in time is embedded as a vector using historical prices at specific delays (τ). This reveals the market's hidden attractor structure.

2. Lyapunov Calculation

For each current state, we:

- Find similar historical states within epsilon (ε) distance

- Track how these initially similar states evolved

- Measure exponential divergence rate

- Average across multiple trajectories for robustness

3. Signal Generation

Chaos signals: When λ crosses above threshold, market enters trending regime

Stability signals: When λ crosses below threshold, market enters ranging regime

Divergence detection: Price/Lyapunov divergences signal potential reversals

4. Rothko Visualization

Color fields: Background zones represent market states with Rothko-inspired palettes

Glowing line: Lyapunov exponent with intensity reflecting market state

Minimalist design: Focus on essential information without clutter

Inputs:

📐 Lyapunov Parameters

Embedding Dimension (default: 3)

Dimensions for phase space reconstruction

2-3: Simple dynamics (crypto/forex) - captures basic momentum patterns

4-5: Complex dynamics (stocks/indices) - captures intricate market structures

Higher dimensions need exponentially more data but reveal deeper patterns

Time Delay τ (default: 1)

Lag between phase space coordinates

1: High-frequency (1m-15m charts) - captures rapid market shifts

2-3: Medium frequency (1H-4H) - balances noise and signal

4-5: Low frequency (Daily+) - focuses on major regime changes

Match to your timeframe's natural cycle

Initial Separation ε (default: 0.001)

Neighborhood size for finding similar states

0.0001-0.0005: Highly liquid markets (major forex pairs)

0.0005-0.002: Normal markets (large-cap stocks)

0.002-0.01: Volatile markets (crypto, small-caps)

Smaller = more sensitive to chaos onset

Evolution Steps (default: 10)

How far to track trajectory divergence

5-10: Fast signals for scalping - quick regime detection

10-20: Balanced for day trading - reliable signals

20-30: Slow signals for swing trading - major regime shifts only

Nearest Neighbors (default: 5)

Phase space points for averaging

3-4: Noisy/fast markets - adapts quickly

5-6: Balanced (recommended) - smooth yet responsive

7-10: Smooth/slow markets - very stable signals

📊 Signal Parameters

Chaos Threshold (default: 0.05)

Lyapunov value above which market is chaotic

0.01-0.03: Sensitive - more chaos signals, earlier detection

0.05: Balanced - optimal for most markets

0.1-0.2: Conservative - only strong trends trigger

Stability Threshold (default: -0.05)

Lyapunov value below which market is stable

-0.01 to -0.03: Sensitive - quick stability detection

-0.05: Balanced - reliable ranging signals

-0.1 to -0.2: Conservative - only deep stability

Signal Smoothing (default: 3)

EMA period for noise reduction

1-2: Raw signals for experienced traders

3-5: Balanced - recommended for most

6-10: Very smooth for position traders

🎨 Rothko Visualization

Rothko Classic: Deep reds for chaos, midnight blues for stability

Orange/Red: Warm sunset tones throughout

Blue/Black: Cool, meditative ocean depths

Purple/Grey: Subtle, sophisticated palette

Visual Options:

Market Zones : Background fields showing regime areas

Transitions: Arrows marking regime changes

Divergences: Labels for price/Lyapunov divergences

Dashboard: Real-time state and trading signals

Guide: Educational panel explaining the theory

Visual Logic & Interpretation

Main Elements

Lyapunov Line: The heart of the indicator

Above chaos threshold: Market is trending, follow momentum

Below stability threshold: Market is ranging, fade extremes

Between thresholds: Transition zone, reduce risk

Background Zones: Rothko-inspired color fields

Red zone: Chaotic regime (trending)

Gray zone: Transition (uncertain)

Blue zone: Stable regime (ranging)

Transition Markers:

Up triangle: Entering chaos - start trend following

Down triangle: Entering stability - start mean reversion

Divergence Signals:

Bullish: Price makes low but Lyapunov rising (stability breaking down)

Bearish: Price makes high but Lyapunov falling (chaos dissipating)

Dashboard Information

Market State: Current regime (Chaotic/Stable/Transitioning)

Trading Bias: Specific strategy recommendation

Lyapunov λ: Raw value for precision

Signal Strength: Confidence in current regime

Last Change: Bars since last regime shift

Action: Clear trading directive

Trading Strategies

In Chaotic Regime (λ > threshold)

Follow trends aggressively: Breakouts have high success rate

Use momentum strategies: Moving average crossovers work well

Wider stops: Expect larger swings

Pyramid into winners: Trends tend to persist

In Stable Regime (λ < threshold)

Fade extremes: Mean reversion dominates

Use oscillators: RSI, Stochastic work well

Tighter stops: Smaller expected moves

Scale out at targets: Trends don't persist

In Transition Zone

Reduce position size: Uncertainty is high

Wait for confirmation: Let regime establish

Use options: Volatility strategies may work

Monitor closely: Quick changes possible

Advanced Techniques

- Multi-Timeframe Analysis

- Higher timeframe LMI for regime context

- Lower timeframe for entry timing

- Alignment = highest probability trades

- Divergence Trading

- Most powerful at regime boundaries

- Combine with support/resistance

- Use for early reversal detection

- Volatility Correlation

- Chaos often precedes volatility expansion

- Stability often precedes volatility contraction

- Use for options strategies

Originality & Innovation

LMI represents a genuine breakthrough in applying chaos theory to markets:

True Lyapunov Calculation: Not a simplified proxy but actual phase space reconstruction and divergence measurement

Rothko Aesthetic: Transforms complex math into meditative visual experience

Regime Detection: Identifies market state changes before price makes them obvious

Practical Application: Clear, actionable signals from theoretical physics

This is not a combination of existing indicators or a visual makeover of standard tools. It's a fundamental rethinking of how we measure and visualize market dynamics.

Best Practices

Start with defaults: Parameters are optimized for broad market conditions

Match to your timeframe: Adjust tau and evolution steps

Confirm with price action: LMI shows regime, not direction

Use appropriate strategies: Chaos = trend, Stability = reversion

Respect transitions: Reduce risk during regime changes

Alerts Available

Chaos Entry: Market entering chaotic regime - prepare for trends

Stability Entry: Market entering stable regime - prepare for ranges

Bullish Divergence: Potential bottom forming

Bearish Divergence: Potential top forming

Chart Information

Script Name: Lyapunov Market Instability (LMI) Recommended Use: All markets, all timeframes Best Performance: Liquid markets with clear regimes

Academic References

Takens, F. (1981). "Detecting strange attractors in turbulence"

Wolf, A. et al. (1985). "Determining Lyapunov exponents from a time series"

Rosenstein, M. et al. (1993). "A practical method for calculating largest Lyapunov exponents"

Note: After completing this indicator, I discovered @loxx's 2022 "Lyapunov Hodrick-Prescott Oscillator w/ DSL". While both explore Lyapunov exponents, they represent independent implementations with different methodologies and applications. This indicator uses phase space reconstruction for regime detection, while his combines Lyapunov concepts with HP filtering.

Disclaimer

This indicator is for research and educational purposes only. It does not constitute financial advice or provide direct buy/sell signals. Chaos theory reveals market character, not future prices. Always use proper risk management and combine with your own analysis. Past performance does not guarantee future results.

See markets through the lens of chaos. Trade the regime, not the noise.

Bringing theoretical physics to practical trading through the meditative aesthetics of Mark Rothko

Trade with insight. Trade with anticipation.

— Dskyz , for DAFE Trading Systems

Divergence Macro Sentiment Indicator (DMSI)The Divergence Macro Sentiment Indicator (DMSI)

Think of DMSI as your daily “mood ring” for the markets. It boils down the tug-of-war between growth assets (S&P 500, copper, oil) and safe havens (gold, VIX) into one clear histogram—so you instantly know if the bulls have broad backing or are charging ahead with one foot tied behind.

🔍 What You’re Seeing

Green bars (above zero): Risk-on conviction.

Equities and commodities are rallying while gold and volatility retreat.

Red bars (below zero): Risk-off caution.

Gold or VIX are climbing even as stocks rise—or stocks aren’t fully joined by oil/copper.

Zero line: The line in the sand between “full-steam ahead” and “proceed with care.”

📈 How to Read It

Cross-Zero Signals

Bullish trigger: DMSI flips up through zero after a red stretch → fresh long entries.

Bearish trigger: DMSI tumbles below zero from green territory → tighten stops or go defensive.

Divergence Warnings

If SPX makes new highs but DMSI is rolling over (lower green bars or red), that’s your early red flag—rallies may fizzle.

Strength Confirmation

On pullbacks, only buy dips when DMSI ≥ 0. When DMSI is deeply positive, you can be more aggressive on position size or add leverage.

💡 Trade Guidance & Use Cases

Trend Filter: Only take your S&P or sector-ETF long setups when DMSI is non-negative—avoids hollow rallies.

Macro Pair Trades:

Deep red DMSI: go long gold or gold miners (GLD, GDX).

Strong green DMSI: lean into cyclicals, industrials, even energy names.

Risk Management:

Scale out as DMSI fades into negative territory mid-trade.

Scale in or add to winners when it stays bullish.

Swing Confirmation: Overlay on any oscillator or price-pattern system—accept signals only when the macro tide is flowing in your favour.

🚀 Why It Works

Markets don’t move in a vacuum. When stocks rally but the “real-economy” metals and volatility aren’t cooperating, something’s off under the hood. DMSI catches those cross-asset cracks before price alone can—and gives you an early warning system for smarter entries, tighter risk, and bigger gains when the macro trend really kicks in.

Price Action Dynamics Oscillator (PADO)1 minute ago

Price Action Dynamics Oscillator (PADO)

Indicator Overview and Technical Deep Dive

Concept and Philosophy

The Price Action Dynamics Oscillator (PADO) is a sophisticated technical analysis tool designed to provide multi-dimensional insights into market behavior by decomposing price action into manipulation and distribution metrics. The indicator goes beyond traditional momentum or trend indicators by introducing a nuanced approach to understanding market microstructure.

Key Architectural Components

1. Timeframe and Depth Selection

Pivot Depth Options:

Short Term (Length: 12 periods)

Intermediate Term (Length: 20 periods)

Long Term (Length: 100 periods)

This flexible configuration allows traders to adapt the indicator's sensitivity to different market conditions and trading styles.

2. Core Calculation Methodology

Manipulation Metrics

Calculates manipulation differently for green (bullish) and red (bearish) candles

Normalized against Average True Range (ATR) for consistent comparison across different volatility environments

Green Candle Manipulation: (Open - Low) / ATR

Red Candle Manipulation: (High - Open) / ATR

Distribution Metrics

Measures the directional strength and potential momentum shift

Green Candle Distribution: (Close - Open)

Red Candle Distribution: (Open - Close)

3. Normalization and Smoothing

Uses Simple Moving Average (SMA) for smoothing

Dynamic length calculation based on price range distance

Ensures minimum SMA length of 2 to prevent calculation errors

Unique Features

Visualization Toggles

Traders can selectively display:

Manipulation data

Distribution data

Long-term reference lines

Valuation metrics

Strategy signals

Valuation Comparative Analysis

Compares current manipulation and distribution metrics to 1000-bar long-term averages

Color-coded visualization for quick interpretation

Blue: Manipulation above average

Purple: Manipulation below average

Orange: Distribution above average

Yellow: Distribution below average

Strategy Deployment

Generates a composite strategy signal by comparing manipulation and distribution valuations

Uses Exponential Moving Average (EMA) for smoother signal generation

Incorporates volatility bands for context-aware signal interpretation

Quadrant Analysis

Classifies market state into four quadrants based on manipulation and distribution valuations:

Q1: Low Manipulation, High Distribution

Q2: High Manipulation, High Distribution

Q3: Low Manipulation, Low Distribution

Q4: High Manipulation, Low Distribution

Each quadrant is color-coded to provide visual market state representation.

Warning Signals

Manipulation Warning: When strategy crosses below low volatility band

Distribution Warning: When strategy crosses above high volatility band

Visual Indicators

Bar coloration based on strategy momentum

Multiple color states representing different market dynamics

Recommended Use Cases

Intraday and swing trading

Multi-timeframe market analysis

Volatility and momentum assessment

Trend reversal and continuation identification

Potential Limitations

Complexity might require significant trader education

Performance can vary across different market conditions

Requires careful parameter optimization

Recommended Settings

Best used on liquid markets with clear price action

Ideal for:

Forex

Futures

Large-cap stocks

Cryptocurrency pairs

Customization and Optimization

Traders should:

Backtest across multiple assets

Adjust timeframe settings

Calibrate visualization toggles

Use in conjunction with other technical indicators

Licensing

Mozilla Public License 2.0

Open-source and modification-friendly

Conclusion

The PADO represents an advanced approach to market analysis, blending traditional technical analysis with innovative metrics for deeper market understanding.

PADO Quadrant Color Analysis: Deep Dive

Quadrant Color Scheme Breakdown

Quadrant 1: Lime Green Background (RGB: 0, 255, 21, 90)

Condition: val_manip < 1 AND val_distr > 1

Market Interpretation:

Low Manipulation Pressure

High Distribution Activity

Potential Scenario:

Smart money might be gradually distributing positions

Trading Implications:

Caution for current trend followers

Potential preparation for trend change

Increased probability of consolidation or reversal

Quadrant 2: Bright Blue Background (RGB: 0, 191, 255, 90)

Condition: val_manip > 1 AND val_distr > 1

Market Interpretation:

High Manipulation Pressure

High Distribution Activity

Potential Scenario:

Strong institutional involvement

Potential market transition phase

Significant volume and momentum

Trading Implications:

High volatility expected

Increased market uncertainty

Potential for sharp price movements

Requires careful risk management

Quadrant 3: Light Gray Background (RGB: 252, 252, 252, 90)

Condition: val_manip < 1 AND val_distr < 1

Market Interpretation:

Low Manipulation Pressure

Low Distribution Activity

Potential Scenario:

Market consolidation

Reduced institutional activity

Potential low-volatility period

Trading Implications:

Range-bound market

Reduced trading opportunities

Potential setup for future breakout

Ideal for mean reversion strategies

Quadrant 4: Light Yellow Background (Hex: #f6ff0019)

Condition: val_manip > 1 AND val_distr < 1

Market Interpretation:

High Manipulation Pressure

Low Distribution Activity

Potential Scenario:

Accumulation of positions

Trading Implications:

Increased probability of directional move soon

Color Psychology and Technical Significance

Color Selection Rationale

Lime Green (Q1): Represents potential growth and transition

Bright Blue (Q2): Signifies high energy and institutional activity

Light Gray (Q3): Indicates neutrality and consolidation

Transparent Green (Q4): Suggests emerging trend potential

Advanced Interpretation Guidelines

Color Transition Analysis

Observe how the quadrant colors change

Rapid color shifts might indicate:

Market regime changes

Shifts in institutional sentiment

Potential trend acceleration or reversal

Technical Implementation Notes

Calculation Snippet

pinescriptCopyq1 = (val_manip < 1) and (val_distr > 1)

q2 = (val_manip > 1) and (val_distr > 1)

q3 = (val_manip < 1) and (val_distr < 1)

q4 = (val_manip > 1) and (val_distr < 1)

bgcolor(q1 ? color.rgb(0, 255, 21, 90):

q2 ? color.rgb(0, 191, 255, 90):

q3 ? color.rgb(252, 252, 252, 90):

q4 ? #f6ff0019:na)

Alpha Channel (Transparency)

90 and 0x19 values ensure background color doesn't overwhelm chart

Allows underlying price action to remain visible

Subtle visual cue without significant chart obstruction

Practical Trading Recommendations

Never Trade Solely on Quadrant Colors

Use as a complementary analysis tool

Combine with other technical and fundamental indicators

Timeframe Considerations

Validate quadrant signals across multiple timeframes

Longer timeframes provide more reliable signals

Risk Management

Set appropriate stop-loss levels

Use position sizing strategies

Be prepared for false signals

Recommended Workflow

Identify current quadrant

Assess overall market context

Confirm with other indicators

Execute with proper risk management

Goertzel Cycle Composite Wave [Loxx]As the financial markets become increasingly complex and data-driven, traders and analysts must leverage powerful tools to gain insights and make informed decisions. One such tool is the Goertzel Cycle Composite Wave indicator, a sophisticated technical analysis indicator that helps identify cyclical patterns in financial data. This powerful tool is capable of detecting cyclical patterns in financial data, helping traders to make better predictions and optimize their trading strategies. With its unique combination of mathematical algorithms and advanced charting capabilities, this indicator has the potential to revolutionize the way we approach financial modeling and trading.

*** To decrease the load time of this indicator, only XX many bars back will render to the chart. You can control this value with the setting "Number of Bars to Render". This doesn't have anything to do with repainting or the indicator being endpointed***

█ Brief Overview of the Goertzel Cycle Composite Wave

The Goertzel Cycle Composite Wave is a sophisticated technical analysis tool that utilizes the Goertzel algorithm to analyze and visualize cyclical components within a financial time series. By identifying these cycles and their characteristics, the indicator aims to provide valuable insights into the market's underlying price movements, which could potentially be used for making informed trading decisions.

The Goertzel Cycle Composite Wave is considered a non-repainting and endpointed indicator. This means that once a value has been calculated for a specific bar, that value will not change in subsequent bars, and the indicator is designed to have a clear start and end point. This is an important characteristic for indicators used in technical analysis, as it allows traders to make informed decisions based on historical data without the risk of hindsight bias or future changes in the indicator's values. This means traders can use this indicator trading purposes.

The repainting version of this indicator with forecasting, cycle selection/elimination options, and data output table can be found here:

Goertzel Browser

The primary purpose of this indicator is to:

1. Detect and analyze the dominant cycles present in the price data.

2. Reconstruct and visualize the composite wave based on the detected cycles.

To achieve this, the indicator performs several tasks:

1. Detrending the price data: The indicator preprocesses the price data using various detrending techniques, such as Hodrick-Prescott filters, zero-lag moving averages, and linear regression, to remove the underlying trend and focus on the cyclical components.

2. Applying the Goertzel algorithm: The indicator applies the Goertzel algorithm to the detrended price data, identifying the dominant cycles and their characteristics, such as amplitude, phase, and cycle strength.

3. Constructing the composite wave: The indicator reconstructs the composite wave by combining the detected cycles, either by using a user-defined list of cycles or by selecting the top N cycles based on their amplitude or cycle strength.

4. Visualizing the composite wave: The indicator plots the composite wave, using solid lines for the cycles. The color of the lines indicates whether the wave is increasing or decreasing.

This indicator is a powerful tool that employs the Goertzel algorithm to analyze and visualize the cyclical components within a financial time series. By providing insights into the underlying price movements, the indicator aims to assist traders in making more informed decisions.

█ What is the Goertzel Algorithm?

The Goertzel algorithm, named after Gerald Goertzel, is a digital signal processing technique that is used to efficiently compute individual terms of the Discrete Fourier Transform (DFT). It was first introduced in 1958, and since then, it has found various applications in the fields of engineering, mathematics, and physics.

The Goertzel algorithm is primarily used to detect specific frequency components within a digital signal, making it particularly useful in applications where only a few frequency components are of interest. The algorithm is computationally efficient, as it requires fewer calculations than the Fast Fourier Transform (FFT) when detecting a small number of frequency components. This efficiency makes the Goertzel algorithm a popular choice in applications such as:

1. Telecommunications: The Goertzel algorithm is used for decoding Dual-Tone Multi-Frequency (DTMF) signals, which are the tones generated when pressing buttons on a telephone keypad. By identifying specific frequency components, the algorithm can accurately determine which button has been pressed.

2. Audio processing: The algorithm can be used to detect specific pitches or harmonics in an audio signal, making it useful in applications like pitch detection and tuning musical instruments.

3. Vibration analysis: In the field of mechanical engineering, the Goertzel algorithm can be applied to analyze vibrations in rotating machinery, helping to identify faulty components or signs of wear.

4. Power system analysis: The algorithm can be used to measure harmonic content in power systems, allowing engineers to assess power quality and detect potential issues.

The Goertzel algorithm is used in these applications because it offers several advantages over other methods, such as the FFT:

1. Computational efficiency: The Goertzel algorithm requires fewer calculations when detecting a small number of frequency components, making it more computationally efficient than the FFT in these cases.

2. Real-time analysis: The algorithm can be implemented in a streaming fashion, allowing for real-time analysis of signals, which is crucial in applications like telecommunications and audio processing.

3. Memory efficiency: The Goertzel algorithm requires less memory than the FFT, as it only computes the frequency components of interest.

4. Precision: The algorithm is less susceptible to numerical errors compared to the FFT, ensuring more accurate results in applications where precision is essential.

The Goertzel algorithm is an efficient digital signal processing technique that is primarily used to detect specific frequency components within a signal. Its computational efficiency, real-time capabilities, and precision make it an attractive choice for various applications, including telecommunications, audio processing, vibration analysis, and power system analysis. The algorithm has been widely adopted since its introduction in 1958 and continues to be an essential tool in the fields of engineering, mathematics, and physics.

█ Goertzel Algorithm in Quantitative Finance: In-Depth Analysis and Applications