Bollinger Bounce Reversal Strategy – Visual EditionOverview:

The Bollinger Bounce Reversal Strategy – Visual Edition is designed to capture potential reversal moves at price extremes—often termed “bounce points”—by using a combination of technical indicators. The strategy integrates Bollinger Bands, MACD, and volume analysis, and it provides rich on‑chart visual cues to help traders understand its signals and conditions. Additionally, the strategy enforces a maximum of 5 trades per day and uses fixed risk management parameters. This publication is intended for educational purposes and offers a systematic, transparent approach that you can further adjust to fit your market or risk profile.

How It Works:

Bollinger Bands:

A 20‑period simple moving average (SMA) and a user‑defined standard deviation multiplier (default 2.0) are used to calculate the Bollinger Bands.

When the price reaches or crosses these bands (i.e. falls below the lower band or rises above the upper band), it suggests that the price is in an extreme, potentially oversold or overbought, state.

MACD Filter:

The MACD (calculated with standard lengths, e.g. 12, 26, 9) provides momentum information.

For a bullish (long) signal, the MACD line should be above its signal line; for a bearish (short) signal, the MACD line should be below.

Volume Confirmation:

The strategy uses a 20‑period volume moving average to determine if current volume is strong enough to validate a signal.

A signal is confirmed only if the current volume is at or above a specified multiple (by default, 1.0×) of this moving average, ensuring that the move is supported by increased market participation.

Visual Cues:

Bollinger Bands and Fill: The basis (SMA), upper, and lower Bollinger Bands are plotted, and the area between the upper and lower bands is filled with a semi‑transparent color.

Signal Markers: When a long or short signal is generated, corresponding markers (labels) appear on the chart.

Background Coloring: The chart’s background changes color (green for long signals and red for short signals) on the bars where signals occur.

Information Table: An on‑chart table displays key indicator values (MACD, signal line, volume, average volume) and the number of trades executed that day.

Entry Conditions:

Long Entry:

A long trade is triggered when the previous bar’s close is below the lower Bollinger Band and the current bar’s close crosses above it, combined with a bullish MACD condition and strong volume.

Short Entry:

A short trade is triggered when the previous bar’s close is above the upper Bollinger Band and the current bar’s close crosses below it, with a bearish MACD condition and high volume.

Risk Management:

Daily Trade Limit: The strategy restricts trading to no more than 5 trades per day.

Stop-Loss and Take-Profit:

For each position, a stop loss is set at a fixed percentage away from the entry price (typically 2%), and a take profit is set to target a 1:2 risk-reward ratio (typically 4% from the entry price).

Backtesting Setup:

Initial Capital: $10,000

Commission: 0.1% per trade

Slippage: 1 tick per bar

These realistic parameters help ensure that backtesting results reflect the conditions of an average trader.

Disclaimer:

Past performance is not indicative of future results. This strategy is experimental and provided solely for educational purposes. It is essential to backtest extensively and paper trade before any live deployment. All risk management practices are advisory, and you should adjust parameters to suit your own trading style and risk tolerance.

Conclusion:

By combining Bollinger Bands, MACD, and volume analysis, the Bollinger Bounce Reversal Strategy – Visual Edition provides a clear, systematic method to identify potential reversal opportunities at price extremes. The added visual cues help traders quickly interpret signals and assess market conditions, while strict risk management and a daily trade cap help keep trading disciplined. Adjust and refine the settings as needed to better suit your specific market and risk profile.

Cari dalam skrip untuk "entry"

EMA Crossover Backtest [BarScripts]This indicator lets you backtest an EMA crossover strategy with built-in risk management and trade tracking. It simulates long and short trades based on EMA crossovers, allowing you to fine-tune entry conditions, stop-loss placement, and reward/risk settings.

🔹 How It Works:

Long Entry: Fast EMA crosses above Slow EMA, and price closes above Fast EMA.

Short Entry: Fast EMA crosses below Slow EMA, and price closes below Fast EMA.

Stop Loss: Set based on previous bars or a fixed amount.

Take Profit: Adjustable reward/risk ratio.

Higher Timeframe Confluence: Confirms trades based on a larger timeframe.

Trade Hours Filter: Limits trades to specific time windows.

🔹 Key Features:

✅ Shows Entry & Exit Points with visual trade lines.

✅ Customizable EMA Lengths to fit any strategy.

✅ P&L Tracking & Statistics to measure performance.

✅ Position Sizing Options: Fixed position, fixed risk, or percentage of balance.

✅ Commissions Tracking (based on total trades, not contracts).

Use this tool to fine-tune your EMA crossover strategy and see how it performs over time! 🚀

💬 Let me know your feedback—suggest improvements, report issues, or request new features!

Volatility Momentum Breakout StrategyDescription:

Overview:

The Volatility Momentum Breakout Strategy is designed to capture significant price moves by combining a volatility breakout approach with trend and momentum filters. This strategy dynamically calculates breakout levels based on market volatility and uses these levels along with trend and momentum conditions to identify trade opportunities.

How It Works:

1. Volatility Breakout:

• Methodology:

The strategy computes the highest high and lowest low over a defined lookback period (excluding the current bar to avoid look-ahead bias). A multiple of the Average True Range (ATR) is then added to (or subtracted from) these levels to form dynamic breakout thresholds.

• Purpose:

This method helps capture significant price movements (breakouts) while ensuring that only past data is used, thereby maintaining realistic signal generation.

2. Trend Filtering:

• Methodology:

A short-term Exponential Moving Average (EMA) is applied to determine the prevailing trend.

• Purpose:

Long trades are considered only when the current price is above the EMA, indicating an uptrend, while short trades are taken only when the price is below the EMA, indicating a downtrend.

3. Momentum Confirmation:

• Methodology:

The Relative Strength Index (RSI) is used to gauge market momentum.

• Purpose:

For long entries, the RSI must be above a mid-level (e.g., above 50) to confirm upward momentum, and for short entries, it must be below a similar threshold. This helps filter out signals during overextended conditions.

Entry Conditions:

• Long Entry:

A long position is triggered when the current closing price exceeds the calculated long breakout level, the price is above the short-term EMA, and the RSI confirms momentum (e.g., above 50).

• Short Entry:

A short position is triggered when the closing price falls below the calculated short breakout level, the price is below the EMA, and the RSI confirms momentum (e.g., below 50).

Risk Management:

• Position Sizing:

Trades are sized to risk a fixed percentage of account equity (set here to 5% per trade in the code, with each trade’s stop loss defined so that risk is limited to approximately 2% of the entry price).

• Stop Loss & Take Profit:

A stop loss is placed a fixed ATR multiple away from the entry price, and a take profit target is set to achieve a 1:2 risk-reward ratio.

• Realistic Backtesting:

The strategy is backtested using an initial capital of $10,000, with a commission of 0.1% per trade and slippage of 1 tick per bar—parameters chosen to reflect conditions faced by the average trader.

Important Disclaimers:

• No Look-Ahead Bias:

All breakout levels are calculated using only past data (excluding the current bar) to ensure that the strategy does not “peek” into future data.

• Educational Purpose:

This strategy is experimental and provided solely for educational purposes. Past performance is not indicative of future results.

• User Responsibility:

Traders should thoroughly backtest and paper trade the strategy under various market conditions and adjust parameters to fit their own risk tolerance and trading style before live deployment.

Conclusion:

By integrating volatility-based breakout signals with trend and momentum filters, the Volatility Momentum Breakout Strategy offers a unique method to capture significant price moves in a disciplined manner. This publication provides a transparent explanation of the strategy’s components and realistic backtesting parameters, making it a useful tool for educational purposes and further customization by the TradingView community.

Advanced Multi-Timeframe Trading System (Risk Managed)Description:

This strategy is an original approach that combines two main analytical components to identify potential trade opportunities while simulating realistic trading conditions:

1. Market Trend Analysis via an Approximate Hurst Exponent

• What It Does:

The strategy computes a rough measure of market trending using an approximate Hurst exponent. A value above 0.5 suggests persistent, trending behavior, while a value below 0.5 indicates a tendency toward mean-reversion.

• How It’s Used:

The Hurst exponent is calculated on both the chart’s current timeframe and a higher timeframe (default: Daily) to capture both local and broader market dynamics.

2. Fibonacci Retracement Levels

• What It Does:

Using daily high and low data from a selected timeframe (default: Daily), the script computes key Fibonacci retracement levels.

• How It’s Used:

• The 61.8% level (Golden Ratio) serves as a key threshold:

• A long entry is signaled when the price crosses above this level if the daily Hurst exponent confirms a trending market.

• The 38.2% level is used to identify short-entry opportunities when the price crosses below it and the daily Hurst indicates non-trending conditions.

Signal Logic:

• Long Entry:

When the price crosses above the 61.8% Fibonacci level (Golden Ratio) and the daily Hurst exponent is greater than 0.5, suggesting a trending market.

• Short Entry:

When the price crosses below the 38.2% Fibonacci level and the daily Hurst exponent is less than 0.5, indicating a less trending or potentially reversing market.

Risk Management & Trade Execution:

• Stop-Loss:

Each trade is risk-managed with a stop-loss set at 2% below (for longs) or above (for shorts) the entry price. This ensures that no single trade risks more than a small, sustainable portion of the account.

• Take Profit:

A take profit order targets a risk-reward ratio of 1:2 (i.e., the target profit is twice the amount risked).

• Position Sizing:

Trades are executed with a fixed position size equal to 10% of account equity.

• Trade Frequency Limits:

• Daily Limit: A maximum of 5 trades per day

• Overall Limit: No more than 510 trades during the backtesting period (e.g., since 2019)

These limits are imposed to simulate realistic trading frequency and to avoid overtrading in backtest results.

Backtesting Parameters:

• Initial Capital: $10,000

• Commission: 0.1% per trade

• Slippage: 1 tick per bar

These settings aim to reflect the conditions faced by the average trader and help ensure that the backtesting results are realistic and not misleading.

Chart Overlays & Visual Aids:

• Fibonacci Levels:

The key Fibonacci retracement levels are plotted on the chart, and the zone between the 61.8% and 38.2% levels is highlighted to show a key retracement area.

• Market Trend Background:

The chart background is tinted green when the daily Hurst exponent indicates a trending market (value > 0.5) and red otherwise.

• Information Table:

An on-chart table displays key parameters such as the current Hurst exponent, daily Hurst value, the number of trades executed today, and the global trade count.

Disclaimer:

Past performance is not indicative of future results. This strategy is experimental and provided solely for educational purposes. It is essential that you backtest and paper trade using your own settings before considering any live deployment. The Hurst exponent calculation is an approximation and should be interpreted as a rough gauge of market behavior. Adjust the parameters and risk management settings according to your personal risk tolerance and market conditions.

Additional Notes:

• Originality & Usefulness:

This script is an original mashup that combines trend analysis with Fibonacci retracement methods. The description above explains how these components work together to provide trading signals.

• Realistic Results:

The strategy uses realistic account sizes, commission rates, slippage, and risk management rules to generate backtesting results that are representative of real-world trading.

• Educational Purpose:

This script is intended to support the TradingView community by offering insights into combining multiple analysis techniques in one strategy. It is not a “get-rich-quick” system but rather an educational tool to help traders understand risk management and trade signal logic.

By using this script, you acknowledge that trading involves risk and that you are responsible for testing and adjusting the strategy to fit your own trading environment. This publication is fully open source, and any modifications should include proper attribution if significant portions of the code are reused.

Prev Day High EMA Crossover with 7-Day SMA Trailing StopPrev Day High EMA Crossover with 7-Day SMA Trailing Stop

Overview

This indicator is designed for traders who seek high-probability breakout trades using a combination of Exponential Moving Averages (EMAs), the previous day's high, and a 7-day Simple Moving Average (SMA) trailing stop. It helps identify bullish and bearish crossover signals while ensuring confirmation with price action above or below key levels.

How It Works

1. Entry Signals:

✅ Bullish Entry:

The 9 EMA crosses above the 15 EMA (bullish momentum).

The price is above the previous day’s high (confirming a breakout).

The candle closes above the open (bullish confirmation).

✅ Bearish Entry:

The 9 EMA crosses below the 15 EMA (bearish momentum).

The price is below the previous day’s high (confirming a failure to break higher).

The candle closes below the open (bearish confirmation).

2. Exit Strategy (Trailing Stop):

📌 Long Exit: If in a long trade, exit when the price closes below the 7-day SMA.

📌 Short Exit: If in a short trade, exit when the price closes above the 7-day SMA.

High-Probability IndicatorExplanation of the Code

Trend Filter (EMA):

A 50-period Exponential Moving Average (EMA) is used to determine the overall trend.

trendUp is true when the price is above the EMA.

trendDown is true when the price is below the EMA.

Momentum Filter (RSI):

A 14-period RSI is used to identify overbought and oversold conditions.

oversold is true when RSI ≤ 30.

overbought is true when RSI ≥ 70.

Volatility Filter (ATR):

A 14-period Average True Range (ATR) is used to measure volatility.

ATR is multiplied by a user-defined multiplier (default: 2.0) to set a volatility threshold.

Ensures trades are only taken during periods of sufficient volatility.

Entry Conditions:

Long Entry: Price is above the EMA (uptrend), RSI is oversold, and the candle range exceeds the ATR threshold.

Short Entry: Price is below the EMA (downtrend), RSI is overbought, and the candle range exceeds the ATR threshold.

Exit Conditions:

Take Profit: A fixed percentage above/below the entry price.

Stop Loss: A fixed percentage below/above the entry price.

Visualization:

The EMA is plotted on the chart.

Background colors highlight uptrends and downtrends.

Buy and sell signals are displayed as labels on the chart.

Alerts:

Alerts are triggered for buy and sell signals.

How to Use the Indicator

Trend Filter:

Only take trades in the direction of the trend (e.g., long in an uptrend, short in a downtrend).

Momentum Filter:

Look for oversold conditions in an uptrend for long entries.

Look for overbought conditions in a downtrend for short entries.

Volatility Filter:

Ensure the candle range exceeds the ATR threshold to avoid low-volatility trades.

Risk Management:

Use the built-in take profit and stop loss levels to manage risk.

Optimization Tips

Backtesting:

Test the indicator on multiple timeframes and assets to evaluate its performance.

Adjust the input parameters (e.g., EMA length, RSI length, ATR multiplier) to optimize for specific markets.

Combination with Other Strategies:

Add additional filters, such as volume analysis or support/resistance levels, to improve accuracy.

Risk Management:

Use proper position sizing and risk-reward ratios to maximize profitability.

Disclaimer

No indicator can guarantee an 85% win ratio due to the inherent unpredictability of financial markets. This script is provided for educational purposes only. Always conduct thorough backtesting and paper trading before using any strategy in live trading.

Let me know if you need further assistance or enhancements!

Candle Emotion Index (CEI) StrategyThe Candle Emotion Index (CEI) Strategy is an innovative sentiment-based trading approach designed to help traders identify and capitalize on market psychology. By analyzing candlestick patterns and combining them into a unified metric, the CEI Strategy provides clear entry and exit signals while dynamically managing risk. This strategy is ideal for traders looking to leverage market sentiment to identify high-probability trading opportunities.

How It Works

The CEI Strategy is built around three core oscillators that reflect key emotional states in the market:

Indecision Oscillator . Measures market uncertainty using patterns like Doji and Spinning Tops. High values indicate hesitation, signaling potential turning points.

Fear Oscillator . Tracks bearish sentiment through patterns like Shooting Star, Hanging Man, and Bearish Engulfing. Helps identify moments of intense selling pressure.

Greed Oscillator . Detects bullish sentiment using patterns like Marubozu, Hammer, Bullish Engulfing, and Three White Soldiers. Highlights periods of strong buying interest.

These oscillators are averaged into the Candle Emotion Index (CEI):

CEI = (Indecision + Fear + Greed) / 3

This single value quantifies overall market sentiment and drives the strategy’s trading decisions.

Key Features

Sentiment-Based Trading Signals . Long Entry: Triggered when the CEI crosses above a lower threshold (e.g., 0.1), indicating increasing bullish sentiment. Short Entry: Triggered when the CEI crosses above a higher threshold (e.g., 0.2), signaling rising bearish sentiment.

Volume Confirmation . Trades are validated only if volume exceeds a user-defined multiplier of the average volume over the lookback period. This ensures entries are backed by significant market activity.

Break-Even Recovery Mechanism . If a trade moves into a loss, the strategy attempts to recover to break-even instead of immediately exiting at a loss. This feature provides flexibility, allowing the market to recover while maintaining disciplined risk management.

Dynamic Risk Management . Maximum Holding Period: Trades are closed after a user-defined number of candles to avoid overexposure to prolonged uncertainty. Profit-Taking Conditions: Positions are exited when favorable price moves are confirmed by increased volume, locking in gains. Loss Threshold: Trades are exited early if the price moves unfavorably beyond a set percentage of the entry price, limiting potential losses.

Cooldown Period . After a trade is closed, a cooldown period prevents immediate re-entry, reducing overtrading and improving signal quality.

Why Use This Strategy?

The CEI Strategy combines advanced sentiment analysis with robust trade management, making it a powerful tool for traders seeking to understand market psychology and identify high-probability setups. Its unique features, such as the break-even recovery mechanism and volume confirmation, add an extra layer of discipline and reliability to trading decisions.

Best Practices

Combine with Other Indicators . Use trend-following tools (e.g., moving averages, ADX) and momentum oscillators (e.g., RSI, MACD) to confirm signals.

Align with Key Levels . Incorporate support and resistance levels for refined entries and exits.

Multi-Market Compatibility . Apply this strategy to forex, crypto, stocks, or any asset class with strong volume and price action.

Sunil 2 Bar Breakout StrategyDetailed Explanation of the Sunil 2 Bar Breakout Strategy

Introduction

The Sunil 2 Bar Breakout Strategy is a simple yet effective price-action-based approach designed to identify breakout opportunities in financial markets. This strategy analyzes the movement of the last three candles to detect momentum and initiates trades in the direction of the breakout. It is equipped with a built-in stop-loss mechanism to protect capital, making it suitable for traders looking for a structured and disciplined trading system.

The strategy works well across different timeframes and asset classes, including indices, stocks, forex, and cryptocurrencies. Its versatility makes it ideal for both intraday and swing trading.

Core Concept

The strategy revolves around two primary conditions: breakout identification and risk management.

Breakout Identification:

Long Trade Setup: The strategy identifies bullish breakouts when:

The current candle's closing price is higher than the previous candle's closing price.

The high of the previous candle is greater than the highs of the two candles before it.

Short Trade Setup: The strategy identifies bearish breakouts when:

The current candle's closing price is lower than the previous candle's closing price.

The low of the previous candle is lower than the lows of the two candles before it.

Risk Management:

Stop-Loss: For each trade, a stop-loss is automatically set:

For long trades, the stop-loss is set to the low of the previous candle.

For short trades, the stop-loss is set to the high of the previous candle.

This ensures that losses are minimized if the breakout fails.

Exit Logic:

The trade is closed automatically when the stop-loss is hit.

This approach maintains discipline and prevents emotional trading.

Strategy Workflow

Entry Criteria:

Long Entry: A long trade is triggered when:

The current close is greater than the previous close.

The high of the previous candle exceeds the highs of the two candles before it.

Short Entry: A short trade is triggered when:

The current close is less than the previous close.

The low of the previous candle is below the lows of the two candles before it.

Stop-Loss Placement:

For long trades, the stop-loss is set at the low of the previous candle.

For short trades, the stop-loss is set at the high of the previous candle.

Trade Management:

Trades are exited automatically if the stop-loss level is hit.

The strategy avoids re-entering trades until new breakout conditions are met.

Default Settings

Position Sizing:

The default position size is set to 1% of the account equity. This ensures proper risk management and prevents overexposure to the market.

Stop-Loss:

Stop-loss levels are automatically calculated based on the previous candle’s high or low.

Timeframes:

The strategy is versatile and works across multiple timeframes. However, it is recommended to test it on 15-minute, 1-hour, and daily charts for optimal performance.

Key Features

Automated Trade Execution:

The strategy handles both trade entry and exit automatically based on pre-defined conditions.

Built-In Risk Management:

The automatic stop-loss placement ensures losses are minimized on failed breakouts.

Works Across Markets:

The strategy is compatible with a wide range of instruments, including indices, stocks, forex, and cryptocurrencies.

Clear Signals:

Entry and exit points are straightforward and based on objective conditions, reducing ambiguity.

Versatility:

Can be used for both day trading and swing trading, depending on the chosen timeframe.

Best Practices for Using This Strategy

Backtesting:

Test the strategy on your chosen instrument and timeframe using TradingView's Strategy Tester to evaluate its performance.

Market Conditions:

The strategy performs best in trending markets or during periods of high volatility. Avoid using it in range-bound or choppy markets.

Position Sizing:

Use the default position size (1% of equity) or adjust based on your risk tolerance and account size.

Instrument Selection:

Focus on instruments with good liquidity and volatility, such as indices (e.g., NIFTY, BANKNIFTY), forex pairs, or major cryptocurrencies (e.g., Bitcoin, Ethereum).

Potential Enhancements

To make the strategy even more robust, consider adding the following optional features:

Stop-Loss Multiplier:

Allow users to customize the stop-loss distance as a multiple of the default level (e.g., 1.5x the low or high of the previous candle).

Take-Profit Levels:

Add user-defined take-profit levels, such as a fixed risk-reward ratio (e.g., 1:2).

Time Filter:

Include an option to restrict trading to specific market hours (e.g., avoid low-liquidity times).

Conclusion

The Sunil 2 Bar Breakout Strategy is an excellent tool for traders looking to capitalize on breakout opportunities while maintaining disciplined risk management. Its simplicity, combined with its effectiveness, makes it suitable for traders of all experience levels. By adhering to the clearly defined rules, traders can achieve consistent results while avoiding emotional trading decisions.

This strategy is a reliable addition to any trader’s toolbox and is designed to work seamlessly across different market conditions and instruments.

BullBear with Volume-Percentile TP - Strategy [presentTrading] Happy New Year, everyone! I hope we have a fantastic year ahead.

It's been a while since I published an open script, but it's time to return.

This strategy introduces an indicator called Bull Bear Power, combined with an advanced take-profit system, which is the main innovative and educational aspect of this script. I hope all of you find some useful insights here. Welcome to engage in meaningful exchanges. This is a versatile tool suitable for both novice and experienced traders.

█ Introduction and How it is Different

Unlike traditional strategies that rely solely on price or volume indicators, this approach combines Bull Bear Power (BBP) with volume percentile analysis to identify optimal entry and exit points. It features a dynamic take-profit mechanism based on ATR (Average True Range) multipliers adjusted by volume and percentile factors, ensuring adaptability to diverse market conditions. This multifaceted strategy not only improves signal accuracy but also optimizes risk management, distinguishing it from conventional trading methods.

BTCUSD 6hr performance

Disable the visualization of Bull Bear Power (BBP) to clearly view the Z-Score.

█ Strategy, How it Works: Detailed Explanation

The BBP Strategy with Volume-Percentile TP utilizes several interconnected components to analyze market data and generate trading signals. Here's an overview with essential equations:

🔶 Core Indicators and Calculations

1. Exponential Moving Average (EMA):

- **Purpose:** Smoothens price data to identify trends.

- **Formula:**

EMA_t = (Close_t * (2 / (lengthInput + 1))) + (EMA_(t-1) * (1 - (2 / (lengthInput + 1))))

- Usage: Baseline for Bull and Bear Power.

2. Bull and Bear Power:

- Bull Power: `BullPower = High_t - EMA_t`

- Bear Power: `BearPower = Low_t - EMA_t`

- BBP:** `BBP = BullPower + BearPower`

- Interpretation: Positive BBP indicates bullish strength, negative indicates bearish.

3. Z-Score Calculation:

- Purpose: Normalizes BBP to assess deviation from the mean.

- Formula:

Z-Score = (BBP_t - bbp_mean) / bbp_std

- Components:

- `bbp_mean` = SMA of BBP over `zLength` periods.

- `bbp_std` = Standard deviation of BBP over `zLength` periods.

- Usage: Identifies overbought or oversold conditions based on thresholds.

🔶 Volume Analysis

1. Volume Moving Average (`vol_sma`):

vol_sma = (Volume_1 + Volume_2 + ... + Volume_vol_period) / vol_period

2. Volume Multiplier (`vol_mult`):

vol_mult = Current Volume / vol_sma

- Thresholds:

- High Volume: `vol_mult > 2.0`

- Medium Volume: `1.5 < vol_mult ≤ 2.0`

- Low Volume: `1.0 < vol_mult ≤ 1.5`

🔶 Percentile Analysis

1. Percentile Calculation (`calcPercentile`):

Percentile = (Number of values ≤ Current Value / perc_period) * 100

2. Thresholds:

- High Percentile: >90%

- Medium Percentile: >80%

- Low Percentile: >70%

🔶 Dynamic Take-Profit Mechanism

1. ATR-Based Targets:

TP1 Price = Entry Price ± (ATR * atrMult1 * TP_Factor)

TP2 Price = Entry Price ± (ATR * atrMult2 * TP_Factor)

TP3 Price = Entry Price ± (ATR * atrMult3 * TP_Factor)

- ATR Calculation:

ATR_t = (True Range_1 + True Range_2 + ... + True Range_baseAtrLength) / baseAtrLength

2. Adjustment Factors:

TP_Factor = (vol_score + price_score) / 2

- **vol_score** and **price_score** are based on current volume and price percentiles.

Local performance

🔶 Entry and Exit Logic

1. Long Entry: If Z-Score crosses above 1.618, then Enter Long.

2. Short Entry: If Z-Score crosses below -1.618, then Enter Short.

3. Exiting Positions:

If Long and Z-Score crosses below 0:

Exit Long

If Short and Z-Score crosses above 0:

Exit Short

4. Take-Profit Execution:

- Set multiple exit orders at dynamically calculated TP levels based on ATR and adjusted by `TP_Factor`.

█ Trade Direction

The strategy determines trade direction using the Z-Score from the BBP indicator:

- Long Positions:

- Condition: Z-Score crosses above 1.618.

- Short Positions:

- Condition: Z-Score crosses below -1.618.

- Exiting Trades:

- Long Exit: Z-Score drops below 0.

- Short Exit: Z-Score rises above 0.

This approach aligns trades with prevailing market trends, increasing the likelihood of successful outcomes.

█ Usage

Implementing the BBP Strategy with Volume-Percentile TP in TradingView involves:

1. Adding the Strategy:

- Copy the Pine Script code.

- Paste it into TradingView's Pine Editor.

- Save and apply the strategy to your chart.

2. Configuring Settings:

- Adjust parameters like EMA length, Z-Score thresholds, ATR multipliers, volume periods, and percentile settings to match your trading preferences and asset behavior.

3. Backtesting:

- Use TradingView’s backtesting tools to evaluate historical performance.

- Analyze metrics such as profit factor, drawdown, and win rate.

4. Optimization:

- Fine-tune parameters based on backtesting results.

- Test across different assets and timeframes to enhance adaptability.

5. Deployment:

- Apply the strategy in a live trading environment.

- Continuously monitor and adjust settings as market conditions change.

█ Default Settings

The BBP Strategy with Volume-Percentile TP includes default parameters designed for balanced performance across various markets. Understanding these settings and their impact is essential for optimizing strategy performance:

Bull Bear Power Settings:

- EMA Length (`lengthInput`): 21

- **Effect:** Balances sensitivity and trend identification; shorter lengths respond quicker but may generate false signals.

- Z-Score Length (`zLength`): 252

- **Effect:** Long period for stable mean and standard deviation, reducing false signals but less responsive to recent changes.

- Z-Score Threshold (`zThreshold`): 1.618

- **Effect:** Higher threshold filters out weaker signals, focusing on significant market moves.

Take Profit Settings:

- Use Take Profit (`useTP`): Enabled (`true`)

- **Effect:** Activates dynamic profit-taking, enhancing profitability and risk management.

- ATR Period (`baseAtrLength`): 20

- **Effect:** Shorter period for sensitive volatility measurement, allowing tighter profit targets.

- ATR Multipliers:

- **Effect:** Define conservative to aggressive profit targets based on volatility.

- Position Sizes:

- **Effect:** Diversifies profit-taking across multiple levels, balancing risk and reward.

Volume Analysis Settings:

- Volume MA Period (`vol_period`): 100

- **Effect:** Longer period for stable volume average, reducing the impact of short-term spikes.

- Volume Multipliers:

- **Effect:** Determines volume conditions affecting take-profit adjustments.

- Volume Factors:

- **Effect:** Adjusts ATR multipliers based on volume strength.

Percentile Analysis Settings:

- Percentile Period (`perc_period`): 100

- **Effect:** Balances historical context with responsiveness to recent data.

- Percentile Thresholds:

- **Effect:** Defines price and volume percentile levels influencing take-profit adjustments.

- Percentile Factors:

- **Effect:** Modulates ATR multipliers based on price percentile strength.

Impact on Performance:

- EMA Length: Shorter EMAs increase sensitivity but may cause more false signals; longer EMAs provide stability but react slower to market changes.

- Z-Score Parameters:*Longer Z-Score periods create more stable signals, while higher thresholds reduce trade frequency but increase signal reliability.

- ATR Multipliers and Position Sizes: Higher multipliers allow for larger profit targets with increased risk, while diversified position sizes help in securing profits at multiple levels.

- Volume and Percentile Settings: These adjustments ensure that take-profit targets adapt to current market conditions, enhancing flexibility and performance across different volatility environments.

- Commission and Slippage: Accurate settings prevent overestimation of profitability and ensure the strategy remains viable after accounting for trading costs.

Conclusion

The BBP Strategy with Volume-Percentile TP offers a robust framework by combining BBP indicators with volume and percentile analyses. Its dynamic take-profit mechanism, tailored through ATR adjustments, ensures that traders can effectively capture profits while managing risks in varying market conditions.

Fibonacci Retracement Strategy for CryptoThe Enhanced Fibonacci Retracement Strategy is designed to help traders capitalize on key Fibonacci levels for both long and short trades. This script automatically identifies significant swing highs and lows within a customizable lookback period and dynamically plots Fibonacci retracement levels (0%, 23.6%, 38.2%, 50%, 61.8%, 78.6%, and 100%) as support and resistance levels.

Key Features:

Automatic Fibonacci Levels:

The script identifies the highest high and lowest low over a user-defined lookback period to calculate Fibonacci retracement levels.

Dual-Directional Trading:

Long Trades: Triggered when the price crosses above the 61.8% retracement level, anticipating a reversal.

Short Trades: Triggered when the price crosses below the 38.2% retracement level, capturing potential downward movement.

Compact Line Option:

Users can toggle "Compact Fibonacci Lines" to reduce visual clutter on the chart, making the lines shorter and easier to interpret.

Dynamic Alerts:

Alerts are embedded directly into the strategy logic for entry and exit points.

Long Entry: Triggered when the price bounces above the 61.8% level.

Long Exit: Triggered when the price reaches the 23.6% level.

Short Entry: Triggered when the price crosses below the 38.2% level.

Short Exit: Triggered when the price reaches the 78.6% level.

Clear Visualization:

Fibonacci levels are plotted with distinct colors and dashed lines (optional compact view),

providing traders with clear and actionable levels to make decisions.

Inputs:

Lookback Period: Number of candles to calculate swing highs and lows.

Plot Fibonacci Levels: Toggle to enable/disable plotting levels.

Compact Fibonacci Lines: Reduce the length of Fibonacci lines for a cleaner chart.

How It Works:

The strategy identifies a high-low range within the lookback period.

Fibonacci levels are calculated based on the range and plotted on the chart.

Long Trade Example:

Enter when the price crosses above the 61.8% level.

Exit when the price reaches the 23.6% level.

Short Trade Example:

Enter when the price crosses below the 38.2% level.

Exit when the price reaches the 78.6% level.

Best Use Cases:

Trending Markets: Use retracements to time entries in the direction of the trend.

Range-Bound Markets: Identify and trade reversals near key Fibonacci levels.

Important Notes:

This strategy is not financial advice and should be backtested thoroughly before live trading.

Risk management is crucial! Consider using stop-loss orders for protection.

Customize inputs to suit your preferred timeframe and trading style.

Smart Wick Concept (SWC)Smart Wick Concept (SWC)

The Smart Wick Concept (SWC) is a unique trend-following strategy designed to capture precise entry points in trending markets. This indicator identifies trade opportunities based on higher timeframe trends and wick behavior on lower timeframes, making it an effective tool for intraday and swing traders.

Key Features:

Trend Identification:

SWC uses the H1 timeframe to define the primary market trend (bullish or bearish), ensuring alignment with the overall market direction.

Precise Entry Signals:

Entry opportunities are generated on the M15 timeframe when a candle's wick interacts with the prior candle's range. This approach minimizes false signals and enhances accuracy.

Stop Loss and Take Profit Levels:

The indicator automatically calculates suggested stop loss and take profit levels based on market dynamics, providing traders with a clear risk-reward framework.

Customizable Parameters:

SWC allows traders to adjust key settings, such as the higher timeframe and minimum trend range, to align with their trading preferences and market conditions.

How It Works:

Bullish Entry:

Higher timeframe trend must be bullish.

A M15 candle must dip below the previous candle’s low and close back above it, signaling a potential buy opportunity.

Bearish Entry:

Higher timeframe trend must be bearish.

A M15 candle must exceed the previous candle’s high and close back below it, signaling a potential sell opportunity.

Risk Management:

Stop loss is placed at the low (for buys) or high (for sells) of the current M15 candle.

Take profit targets are calculated at twice the risk, ensuring a favorable risk-reward ratio.

Benefits:

Aligns trades with market momentum.

Reduces noise by filtering out weak or sideways trends.

Provides a structured approach to trading XAUUSD and other volatile instruments.

Use Cases:

The Smart Wick Concept is ideal for traders looking for a disciplined and data-driven approach to trading. While it is optimized for XAUUSD, it can also be applied to other trending markets such as major currency pairs or indices with some parameter adjustments.

Disclaimer:

This indicator is a trading tool and should not be used as a standalone strategy. Always backtest the indicator thoroughly and use proper risk management to protect your capital. Past performance does not guarantee future results.

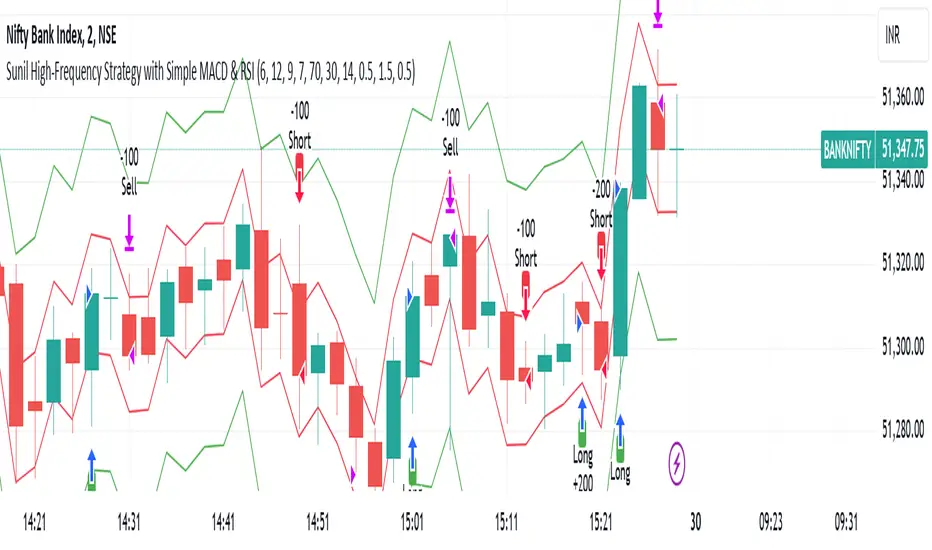

Sunil High-Frequency Strategy with Simple MACD & RSISunil High-Frequency Strategy with Simple MACD & RSI

This high-frequency trading strategy uses a combination of MACD and RSI to identify quick market opportunities. By leveraging these indicators, combined with dynamic risk management using ATR, it aims to capture small but frequent price movements while ensuring tight control over risk.

Key Features:

Indicators Used:

MACD (Moving Average Convergence Divergence): The strategy uses a shorter MACD configuration (Fast Length of 6 and Slow Length of 12) to capture quick price momentum shifts. A MACD crossover above the signal line triggers a buy signal, while a crossover below the signal line triggers a sell signal.

RSI (Relative Strength Index): A shorter RSI length of 7 is used to gauge overbought and oversold market conditions. The strategy looks for RSI confirmation, with a long trade initiated when RSI is below the overbought level (70) and a short trade initiated when RSI is above the oversold level (30).

Risk Management:

Dynamic Stop Loss and Take Profit: The strategy uses ATR (Average True Range) to calculate dynamic stop loss and take profit levels based on market volatility.

Stop Loss is set at 0.5x ATR to limit risk.

Take Profit is set at 1.5x ATR to capture reasonable price moves.

Trailing Stop: As the market moves in the strategy’s favor, the position is protected by a trailing stop set at 0.5x ATR, allowing the strategy to lock in profits as the price moves further.

Entry & Exit Signals:

Long Entry: Triggered when the MACD crosses above the signal line (bullish crossover) and RSI is below the overbought level (70).

Short Entry: Triggered when the MACD crosses below the signal line (bearish crossover) and RSI is above the oversold level (30).

Exit Conditions: The strategy exits long or short positions based on the stop loss, take profit, or trailing stop activation.

Frequent Trades:

This strategy is designed for high-frequency trading, with trade signals occurring frequently as the MACD and RSI indicators react quickly to price movements. It works best on lower timeframes such as 1-minute, 5-minute, or 15-minute charts, but can be adjusted for different timeframes based on the asset’s volatility.

Customizable Parameters:

MACD Settings: Adjust the Fast Length, Slow Length, and Signal Length to tune the MACD’s sensitivity.

RSI Settings: Customize the RSI Length, Overbought, and Oversold levels to better match your trading style.

ATR Settings: Modify the ATR Length and multipliers for Stop Loss, Take Profit, and Trailing Stop to optimize risk management according to market volatility.

Important Notes:

Market Conditions: This strategy is designed to capture smaller, quicker moves in trending markets. It may not perform well during choppy or sideways markets.

Optimizing for Asset Volatility: Adjust the ATR multipliers based on the asset’s volatility to suit the risk-reward profile that fits your trading goals.

Backtesting: It's recommended to backtest the strategy on different assets and timeframes to ensure optimal performance.

Summary:

The Sunil High-Frequency Strategy leverages a simple combination of MACD and RSI with dynamic risk management (using ATR) to trade small but frequent price movements. The strategy ensures tight stop losses and reasonable take profits, with trailing stops to lock in profits as the price moves in favor of the trade. It is ideal for scalping or intraday trading on lower timeframes, aiming for quick entries and exits with controlled risk.

EMA Crossover with RSI and DistanceEMA Crossover with RSI and Distance Strategy

This strategy combines Exponential Moving Averages (EMA) with Relative Strength Index (RSI) and distance-based conditions to generate buy, sell, and neutral signals. It is designed to help traders identify entry and exit points based on multiple technical indicators.

Key Components:

Exponential Moving Averages (EMA):

The strategy uses four EMAs: EMA 5, EMA 13, EMA 40, and EMA 55.

A buy signal (long) is triggered when EMA 5 crosses above EMA 13 and EMA 40 crosses above EMA 55.

A sell signal (short) is generated when EMA 55 crosses above EMA 40.

The distance between EMAs (5 and 13) is also important. If the current distance between EMA 5 and EMA 13 is smaller than the average distance over the last 5 candles, a neutral condition is triggered, preventing a signal even if all other conditions are met.

Relative Strength Index (RSI):

The 14-period RSI is used to determine market strength and direction.

The strategy requires RSI to be above 50 and greater than the average RSI (over the past 14 periods) for a buy signal.

If the RSI is above 60, a green signal is given, indicating a strong bullish condition, even if the EMA conditions are not fully met.

If the RSI is below 40, a red signal is given, indicating a strong bearish condition, regardless of the EMA crossover.

Distance Conditions:

The strategy calculates the distance between EMA 5 and EMA 13 on each candle and compares it to the average distance of the last 5 candles.

If the current distance between EMA 5 and EMA 13 is lower than the average of the last 5 candles, a neutral signal is triggered. This helps avoid entering a trade when the market is losing momentum.

Additionally, if the distance between EMA 40 and EMA 13 is greater than the previous distance, the previous signal is kept intact, ensuring that the trend is still strong enough for the signal to remain valid.

Signal Persistence:

Once a buy (green) or sell (red) signal is triggered, it remains intact as long as the price is closing above EMA 5 for long trades or below EMA 55 for short trades.

If the price moves below EMA 5 for long trades or above EMA 55 for short trades, the signal is recalculated based on the most recent conditions.

Signal Display:

Green Signals: Represent a strong buy signal and are shown below the candle when the RSI is above 60.

Red Signals: Represent a strong sell signal and are shown above the candle when the RSI is below 40.

Neutral Signals: Displayed when the conditions for entry are not met, specifically when the EMA distance condition is violated.

Long and Short Signals: Additional signals are shown based on the EMA crossovers and RSI conditions. These signals are plotted below the candle for long positions and above the candle for short positions.

Trade Logic:

Long Entry: Enter a long trade when EMA 5 crosses above EMA 13, EMA 40 crosses above EMA 55, and the RSI is above 50 and greater than the average RSI. Additionally, the current distance between EMA 5 and EMA 13 should be larger than the average distance of the last 5 candles.

Short Entry: Enter a short trade when EMA 55 crosses above EMA 40 and the RSI is below 40.

Neutral Condition: If the distance between EMA 5 and EMA 13 is smaller than the average distance over the last 5 candles, the strategy will not trigger a signal, even if other conditions are met.

HOD/LOD/PMH/PML/PDH/PDL Strategy by @tradingbauhaus This script is a trading strategy @tradingbauhaus designed to trade based on key price levels, such as the High of Day (HOD), Low of Day (LOD), Premarket High (PMH), Premarket Low (PML), Previous Day High (PDH), and Previous Day Low (PDL). Below, I’ll explain in detail what the script does:

Core Functionality of the Script:

Calculates Key Price Levels:

HOD (High of Day): The highest price of the current day.

LOD (Low of Day): The lowest price of the current day.

PMH (Premarket High): The highest price during the premarket session (before the market opens).

PML (Premarket Low): The lowest price during the premarket session.

PDH (Previous Day High): The highest price of the previous day.

PDL (Previous Day Low): The lowest price of the previous day.

Draws Horizontal Lines on the Chart:

Plots horizontal lines on the chart for each key level (HOD, LOD, PMH, PML, PDH, PDL) with specific colors for easy visual identification.

Defines Entry and Exit Rules:

Long Entry (Buy): If the price crosses above the PMH (Premarket High) or the PDH (Previous Day High).

Short Entry (Sell): If the price crosses below the PML (Premarket Low) or the PDL (Previous Day Low).

Long Exit: If the price reaches the HOD (High of Day) during a long position.

Short Exit: If the price reaches the LOD (Low of Day) during a short position.

How the Script Works Step by Step:

Calculates Key Levels:

Uses the request.security function to fetch the HOD and LOD of the current day, as well as the highs and lows of the previous day (PDH and PDL).

Calculates the PMH and PML during the premarket session (before 9:30 AM).

Plots Levels on the Chart:

Uses the plot function to draw horizontal lines on the chart representing the key levels (HOD, LOD, PMH, PML, PDH, PDL).

Each level has a specific color for easy identification:

HOD: White.

LOD: Purple.

PDH: Orange.

PDL: Blue.

PMH: Green.

PML: Red.

Defines Trading Rules:

Uses conditions with ta.crossover and ta.crossunder to detect when the price crosses key levels.

Long Entry: If the price crosses above the PMH or PDH, a long position (buy) is opened.

Short Entry: If the price crosses below the PML or PDL, a short position (sell) is opened.

Long Exit: If the price reaches the HOD during a long position, the position is closed.

Short Exit: If the price reaches the LOD during a short position, the position is closed.

Executes Orders Automatically:

Uses the strategy.entry and strategy.close functions to open and close positions automatically based on the defined rules.

Advantages of This Strategy:

Based on Key Levels: Uses important price levels that often act as support and resistance.

Easy to Visualize: Horizontal lines on the chart make it easy to identify levels.

Automated: Entries and exits are executed automatically based on the defined rules.

Limitations of This Strategy:

Dependent on Volatility: Works best in markets with significant price movements.

False Crosses: There may be false crosses that generate incorrect signals.

No Advanced Risk Management: Does not include dynamic stop-loss or take-profit mechanisms.

How to Improve the Strategy:

Add Stop-Loss and Take-Profit: To limit losses and lock in profits.

Filter Signals with Indicators: Use RSI, MACD, or other indicators to confirm signals.

Optimize Levels: Adjust key levels based on the asset’s behavior.

In summary, this script is a trading strategy that operates based on key price levels, such as HOD, LOD, PMH, PML, PDH, and PDL. It is useful for traders who want to trade based on significant support and resistance levels.

Trend Trader-Remastered StrategyOfficial Strategy for Trend Trader - Remastered

Indicator: Trend Trader-Remastered (TTR)

Overview:

The Trend Trader-Remastered is a refined and highly sophisticated implementation of the Parabolic SAR designed to create strategic buy and sell entry signals, alongside precision take profit and re-entry signals based on marked Bill Williams (BW) fractals. Built with a deep emphasis on clarity and accuracy, this indicator ensures that only relevant and meaningful signals are generated, eliminating any unnecessary entries or exits.

Please check the indicator details and updates via the link above.

Important Disclosure:

My primary objective is to provide realistic strategies and a code base for the TradingView Community. Therefore, the default settings of the strategy version of the indicator have been set to reflect realistic world trading scenarios and best practices.

Key Features:

Strategy execution date&time range.

Take Profit Reduction Rate: The percentage of progressive reduction on active position size for take profit signals.

Example:

TP Reduce: 10%

Entry Position Size: 100

TP1: 100 - 10 = 90

TP2: 90 - 9 = 81

Re-Entry When Rate: The percentage of position size on initial entry of the signal to determine re-entry.

Example:

RE When: 50%

Entry Position Size: 100

Re-Entry Condition: Active Position Size < 50

Re-Entry Fill Rate: The percentage of position size on initial entry of the signal to be completed.

Example:

RE Fill: 75%

Entry Position Size: 100

Active Position Size: 50

Re-Entry Order Size: 25

Final Active Position Size:75

Important: Even RE When condition is met, the active position size required to drop below RE Fill rate to trigger re-entry order.

Key Points:

'Process Orders on Close' is enabled as Take Profit and Re-Entry signals must be executed on candle close.

'Calculate on Every Tick' is enabled as entry signals are required to be executed within candle time.

'Initial Capital' has been set to 10,000 USD.

'Default Quantity Type' has been set to 'Percent of Equity'.

'Default Quantity' has been set to 10% as the best practice of investing 10% of the assets.

'Currency' has been set to USD.

'Commission Type' has been set to 'Commission Percent'

'Commission Value' has been set to 0.05% to reflect the most realistic results with a common taker fee value.

IU open equal to high/low strategyIU open equal to high/low strategy:

The "IU Open Equal to High/Low Strategy" is designed to identify and trade specific market conditions where the day's first price action shows a strong directional bias. This strategy automatically enters trades based on the relationship between the market's open price and its first high or low of the day.

Entry Conditions:

1. Long Entry: A long position is initiated when the first open price of the session equals the day's first low. This signals a potential upward move.

2. Short Entry: A short position is initiated when the first open price of the session equals the day's first high. This signals a potential downward move.

Exit Conditions:

1. Stop Loss (SL): For both long and short trades, the stop loss is calculated based on the low or high of the candle where the position was entered.

2. Take Profit (TP): The take profit is set using a Risk-to-Reward (RTR) ratio, which is customizable by the user. The TP is calculated relative to the entry price and the distance between the entry and the stop loss.

Additional Features:

- Plots are used to visualize the entry price, stop loss, and take profit levels directly on the chart, providing clear and actionable insights.

- Labels are displayed to indicate the occurrence of the "Open == Low" or "Open == High" conditions for easier identification of potential trade setups.

- A dynamic fill highlights the areas between the entry price and the stop loss or take profit, offering a clear visual representation of the trade's risk and reward zones.

This strategy is designed for traders looking to capitalize on directional momentum at the start of the trading session. It is customizable, allowing users to set their desired Risk-to-Reward ratio and tailor the strategy to fit their trading style.

IU EMA Channel StrategyIU EMA Channel Strategy

Overview:

The IU EMA Channel Strategy is a simple yet effective trend-following strategy that uses two Exponential Moving Averages (EMAs) based on the high and low prices. It provides clear entry and exit signals by identifying price crossovers relative to the EMAs while incorporating a built-in Risk-to-Reward Ratio (RTR) for effective risk management.

Inputs ( Settings ):

- RTR (Risk-to-Reward Ratio): Define the ratio for risk-to-reward (default = 2).

- EMA Length: Adjust the length of the EMA channels (default = 100).

How the Strategy Works

1. EMA Channels:

- High-based EMA: EMA calculated on the high price.

- Low-based EMA: EMA calculated on the low price.

The area between these two EMAs creates a "channel" that visually highlights potential support and resistance zones.

2. Entry Rules:

- Long Entry: When the price closes above the high-based EMA (crossover).

- Short Entry: When the price closes below the low-based EMA (crossunder).

These entries ensure trades are taken in the direction of momentum.

3. Stop Loss (SL) and Take Profit (TP):

- Stop Loss:

- For long positions, the SL is set at the previous bar's low.

- For short positions, the SL is set at the previous bar's high.

- Take Profit:

- TP is automatically calculated using the Risk-to-Reward Ratio (RTR) you define.

- Example: If RTR = 2, the TP will be 2x the risk distance.

4. Exit Rules:

- Positions are closed at either the stop loss or the take profit level.

- The strategy manages exits automatically to enforce disciplined risk management.

Visual Features

1. EMA Channels:

- The high and low EMAs are dynamically color-coded:

- Green: Price is above the EMA (bullish condition).

- Red: Price is below the EMA (bearish condition).

- The area between the EMAs is shaded for better visual clarity.

2. Stop Loss and Take Profit Zones:

- SL and TP levels are plotted for both long and short positions.

- Zones are filled with:

- Red: Stop Loss area.

- Green: Take Profit area.

Be sure to manage your risk and position size properly.

InspireHER Dynamic EMA RR Positioning IndicatorDynamic EMA and RR Positioning Indicator

This indicator is designed to provide traders with highly customizable buy and sell signals based on EMA (Exponential Moving Average) crossovers and Risk-to-Reward (RR) ratios. It works on any timeframe and allows users to toggle price data and additional position boxes for visualizing trade setups. Additionally, traders can choose between displaying dots or labeled signals for buy/sell indicators, making this tool versatile and user-friendly for different preferences and strategies.

What Makes This Indicator Unique

Customizable Parameters: The script offers extensive options for tailoring the indicator to your preferred trading style and strategy:

EMA: Configurable through settings (default is a 21-period EMA).

Risk-to-Reward Ratio (RR): Adjustable to meet your desired RR levels (default is 1:2.5).

Lookback Period: Visualizes buy/sell signals over the last six months.

Position Boxes for Trade Visualization: The indicator can "draw" position boxes on the chart, showing potential entry points, stop-loss (SL), and take-profit (TP) levels based on the selected RR. These visual aids simplify decision-making and help evaluate trade opportunities directly on the chart.

Price Data Toggle: Traders can choose to view or hide price data related to trade signals, including TP, SL, and RR values. By default, this is turned off to maintain a clean chart but can be activated when needed.

Flexible Signal Display Options:

Dots Mode: Displays buy signals as green dots and sell signals as red dots on the chart.

Label Mode: Displays buy signals as labels with the word "Buy" in green and sell signals as labels with the word "Sell" in red.

This toggle allows traders to customize how signals are displayed for a more personalized trading experience.

Simple Signal View: A toggle option provides a cleaner chart by enabling or disabling additional visual elements like circles or labels.

How It Works

Buy Signal: Triggered when the price crosses the EMA and closes above it.

Entry: Top of the candle.

Stop-Loss: Bottom of the candle.

Take-Profit: Calculated based on the selected RR.

Sell Signal: Triggered when the price crosses the EMA and closes below it.

Entry: Bottom of the candle.

Stop-Loss: Top of the candle.

Take-Profit: Calculated based on the selected RR.

Default Settings

EMA: 21-period.

Risk-to-Reward Ratio: 1:2.5.

Price Data: Off (can be toggled on in settings).

Position Boxes: Off (can be toggled on in settings).

Signal Display: Labels mode with "Buy" (green) and "Sell" (red) enabled by default; can be toggled to Dots mode.

Timeframe: Any timeframe supported.

How to Use

Add the Indicator to Your Chart: Once applied, the EMA line and buy/sell signals will appear by default.

Customize Settings: Navigate to the indicator's settings to adjust EMA, RR, or enable/disable Price Data, Position Boxes, or switch between Dots and Label modes.

Trade with Confidence: Use the visual aids and signals to assess trade opportunities based on your strategy and timeframe.

This indicator combines the reliability of EMA-based signals with the flexibility of configurable RR, visual trade setups, and multiple signal display options, making it a powerful tool for all types of traders. Happy Trading!!

Supertrend and MACD strategyThe Supertrend and MACD Strategy is a comprehensive trading approach designed to capitalize on market trends by using a combination of the Supertrend indicator, the Exponential Moving Average (EMA), and the Moving Average Convergence Divergence (MACD). This strategy aims to identify optimal entry and exit points for both long and short trades, while incorporating strict risk management rules.

Indicators Used:

Supertrend: This indicator is used to identify the overall trend direction. It provides clear signals for trend reversals, helping traders to enter trades in the direction of the prevailing trend.

200-period EMA: This long-term moving average is used to determine the primary trend direction. The strategy only takes long trades when the price is above the 200 EMA and short trades when the price is below it.

MACD: The MACD is used to gauge the momentum and confirm the signals provided by the Supertrend and EMA. It consists of the MACD line, the signal line, and the histogram.

Entry Conditions:

Long Entry:

The Supertrend indicator shows an uptrend (direction > 0).

The MACD line is above the signal line (macd > signal).

The price is above the 200-period EMA (close > ema200).

Short Entry:

The Supertrend indicator shows a downtrend (direction < 0).

The MACD line is below the signal line (macd < signal).

The price is below the 200-period EMA (close < ema200).

Exit Conditions:

Long Exit:

Exit the long position when the MACD line crosses below the signal line (ta.crossunder(macd, signal)).

Set a stop loss (SL) below the lowest low of the last 10 periods (lowestLow - 1).

Short Exit:

Exit the short position when the MACD line crosses above the signal line (ta.crossover(macd, signal)).

Set a stop loss (SL) above the highest high of the last 10 periods (highestHigh + 1).

Risk Management:

The strategy ensures that no new positions are opened if there is already an open trade, preventing overexposure in the market.

Alerts:

Alerts are set to notify traders when the MACD crosses the signal line, providing timely updates for potential exit points.

Composite Oscillation Indicator Based on MACD and OthersThis indicator combines various technical analysis tools to create a composite oscillator that aims to capture multiple aspects of market behavior. Here's a breakdown of its components:

* Individual RSIs (xxoo1-xxoo15): The code calculates the RSI (Relative Strength Index) of numerous indicators, including volume-based indicators (NVI, PVI, OBV, etc.), price-based indicators (CCI, CMO, etc.), and moving averages (WMA, ALMA, etc.). It also includes the RSI of the MACD histogram (xxoo14).

* Composite RSI (xxoojht): The individual RSIs are then averaged to create a composite RSI, aiming to provide a more comprehensive view of market momentum and potential turning points.

* MACD Line RSI (xxoo14): The RSI of the MACD histogram incorporates the momentum aspect of the MACD indicator into the composite measure.

* Double EMA (co, coo): The code employs two Exponential Moving Averages (EMAs) of the composite RSI, with different lengths (9 and 18 periods).

* Difference (jo): The difference between the two EMAs (co and coo) is calculated, aiming to capture the rate of change in the composite RSI.

* Smoothed Difference (xxp): The difference (jo) is further smoothed using another EMA (9 periods) to reduce noise and enhance the signal.

* RSI of Smoothed Difference (cco): Finally, the RSI is applied to the smoothed difference (xxp) to create the core output of the indicator.

Market Applications and Trading Strategies:

* Overbought/Oversold: The indicator's central line (plotted at 50) acts as a reference for overbought/oversold conditions. Values above 50 suggest potential overbought zones, while values below 50 indicate oversold zones.

* Crossovers and Divergences: Crossovers of the cco line above or below its previous bar's value can signal potential trend changes. Divergences between the cco line and price action can also provide insights into potential trend reversals.

* Emoji Markers: The code adds emoji markers ("" for bullish and "" for bearish) based on the crossover direction of the cco line. These can provide a quick visual indication of potential trend shifts.

* Colored Fill: The area between the composite RSI line (xxoojht) and the central line (50) is filled with color to visually represent the prevailing market sentiment (green for above 50, red for below 50).

Trading Strategies (Examples):

* Long Entry: Consider a long entry (buying) signal when the cco line crosses above its previous bar's value and the composite RSI (xxoojht) is below 50, suggesting a potential reversal from oversold conditions.

* Short Entry: Conversely, consider a short entry (selling) signal when the cco line crosses below its previous bar's value and the composite RSI (xxoojht) is above 50, suggesting a potential reversal from overbought conditions.

* Confirmation: Always combine the indicator's signals with other technical analysis tools and price action confirmation for better trade validation.

Additional Notes:

* The indicator offers a complex combination of multiple indicators. Consider testing and optimizing the parameters (EMAs, RSI periods) to suit your trading style and market conditions.

* Backtesting with historical data can help assess the indicator's effectiveness and identify potential strengths and weaknesses in different market environments.

* Remember that no single indicator is perfect, and the cco indicator should be used in conjunction with other forms of analysis to make informed trading decisions.

By understanding the logic behind this composite oscillator and its potential applications, you can incorporate it into your trading strategy to potentially identify trends, gauge market sentiment, and generate trading signals.

TrendWave VWAP Indicator with ATR-based SignalsThe TrendWave VWAP Indicator with ATR-Based Signals is a robust TradingView tool for traders who prioritize precision and adaptability. This indicator combines the Volume-Weighted Average Price (VWAP) with the Average True Range (ATR) to provide actionable entry and exit signals while dynamically filtering out sideways market conditions. Designed with flexibility in mind, the indicator offers extensive customization options to tailor signals and filtering to individual trading styles.

Key Features and Customizable Settings

VWAP Integration

VWAP offers a volume-weighted benchmark, ideal for tracking price trends in relation to average trading levels. Customization: Traders can enable or disable VWAP functionality via a toggle, allowing easy adjustments based on market conditions or strategy preferences.

ATR-Based Signal Levels

ATR provides volatility-based levels for precise entry and exit points by measuring average price range. Customization: Traders can set the ATR length (default: 14) and the multiplier (default: 1.5) for adjusting sensitivity. A sideways threshold can be set to control the ATR value at which the indicator pauses signals, helping to avoid low-volatility markets.

Signal Cooldown

To reduce noise in choppy conditions, a signal cooldown enforces a minimum number of bars between signals. Customization: The cooldown period (default: 10 bars) can be adjusted to match preferred trading frequency and discipline requirements.

Signal Logic

Long Entry: Activated when price crosses above the VWAP in a trending market. Cooldown applies to avoid consecutive signals.

Long Exit: Triggered when price crosses below the VWAP.

Short Entry: Initiated when price crosses below the VWAP, in non-sideways conditions.

Short Exit: Occurs when price crosses back above the VWAP following a short position.

Visual Indicators

The VWAP is displayed as a line on the chart for easy trend reference. Entry and exit signals are clearly marked with color-coded shapes, enhancing readability without clutter.

Practical Application

The TrendWave VWAP Indicator with ATR-Based Signals provides tailored entries and exits for trending markets. Its customization options make it suitable for traders who require flexibility and precision in varying market conditions. By adjusting VWAP, ATR, and cooldown parameters, users can fine-tune the indicator to suit different trading styles, making it an essential tool for disciplined trading in dynamic markets.

HBK Price Action Strategy HBKPrice Action Strategy for XAUUSD with a Favorable Risk-Reward Ratio

Understanding the Strategy:

This strategy leverages price action principles to identify potential entry and exit points for XAUUSD on a 5-minute timeframe. The core idea is to identify price action patterns that suggest a high probability of a particular direction, and then to set stop-loss and take-profit levels to manage risk and reward.

Key Price Action Patterns to Watch:

Pin Bar: A pin bar is a candlestick with a long wick in one direction and a small body in the opposite direction. It often signals a reversal in the current trend.

Inside Bar: An inside bar forms when the current candle's high is lower than the previous candle's high, and the current candle's low is higher than the previous candle's low. It often indicates indecision or a potential breakout.

Engulfing Pattern: An engulfing pattern occurs when the current candle completely engulfs the previous candle. A bullish engulfing pattern signals a potential uptrend, while a bearish engulfing pattern signals a potential downtrend.

Risk-Reward Ratio:

A favorable risk-reward ratio is crucial for long-term trading success. Aim for a minimum risk-reward ratio of 1:2, meaning you risk $1 to potentially gain $2.

Entry and Exit Signals:

Long Entry:

Identify a bullish pin bar or engulfing pattern.

Wait for a confirmation candle to close above the pin bar's high or the engulfing pattern's high.

Place a stop-loss below the recent swing low.

Set a take-profit target at a key resistance level or a multiple of the stop-loss distance.

Short Entry:

Identify a bearish pin bar or engulfing pattern.

Wait for a confirmation candle to close below the pin bar's low or the engulfing pattern's low.

Place a stop-loss above the recent swing high.

Set a take-profit target at a key support level or a multiple of the stop-loss distance.

Additional Tips:

Use Support and Resistance Levels: Identify key support and resistance levels to set your stop-loss and take-profit targets.

Consider Market Sentiment: Pay attention to market sentiment and news events that may impact gold prices.

Manage Risk: Always use stop-loss orders to limit potential losses.

Be Patient: Don't force trades. Wait for high-probability setups.

Practice Discipline: Stick to your trading plan and avoid impulsive decisions.

Remember:

Price action trading requires practice and patience.

Backtest your strategy on historical data to refine your approach.

Always adapt to changing market conditions.

By following these guidelines and practicing disciplined risk management, you can increase your chances of success in trading XAUUSD on a 5-minute timeframe.

XAUUSD 10-Minute StrategyThis XAUUSD 10-Minute Strategy is designed for trading Gold vs. USD on a 10-minute timeframe. By combining multiple technical indicators (MACD, RSI, Bollinger Bands, and ATR), the strategy effectively captures both trend-following and reversal opportunities, with adaptive risk management for varying market volatility. This approach balances high-probability entries with robust volatility management, making it suitable for traders seeking to optimise entries during significant price movements and reversals.

Key Components and Logic:

MACD (12, 26, 9):

Generates buy signals on MACD Line crossovers above the Signal Line and sell signals on crossovers below the Signal Line, helping to capture momentum shifts.

RSI (14):

Utilizes oversold (below 35) and overbought (above 65) levels as a secondary filter to validate entries and avoid overextended price zones.

Bollinger Bands (20, 2):

Uses upper and lower Bollinger Bands to identify potential overbought and oversold conditions, aiming to enter long trades near the lower band and short trades near the upper band.

ATR-Based Stop Loss and Take Profit:

Stop Loss and Take Profit levels are dynamically set as multiples of ATR (3x for stop loss, 5x for take profit), ensuring flexibility with market volatility to optimise exit points.

Entry & Exit Conditions:

Buy Entry: T riggered when any of the following conditions are met:

MACD Line crosses above the Signal Line

RSI is oversold

Price drops below the lower Bollinger Band

Sell Entry: Triggered when any of the following conditions are met:

MACD Line crosses below the Signal Line

RSI is overbought

Price moves above the upper Bollinger Band

Exit Strategy: Trades are closed based on opposing entry signals, with adaptive spread adjustments for realistic exit points.

Backtesting Configuration & Results:

Backtesting Period: July 21, 2024, to October 30, 2024

Symbol Info: XAUUSD, 10-minute timeframe, OANDA data source

Backtesting Capital: Initial capital of $700, with each trade set to 10 contracts (equivalent to approximately 0.1 lots based on the broker’s contract size for gold).

Users should confirm their broker's contract size for gold, as this may differ. This script uses 10 contracts for backtesting purposes, aligned with 0.1 lots on brokers offering a 100-contract specification.

Key Backtesting Performance Metrics:

Net Profit: $4,733.90 USD (676.27% increase)

Total Closed Trades: 526

Win Rate: 53.99%

Profit Factor: 1.44 (1.96 for Long trades, 1.14 for Short trades)

Max Drawdown: $819.75 USD (56.33% of equity)

Sharpe Ratio: 1.726

Average Trade: $9.00 USD (0.04% of equity per trade)

This backtest reflects realistic conditions, with a spread adjustment of 38 points and no slippage or commission applied. The settings aim to simulate typical retail trading conditions. However, please adjust the initial capital, contract size, and other settings based on your account specifics for best results.

Usage:

This strategy is tuned specifically for XAUUSD on a 10-minute timeframe, ideal for both trend-following and reversal trades. The ATR-based stop loss and take profit levels adapt dynamically to market volatility, optimising entries and exits in varied conditions. To backtest this script accurately, ensure your broker’s contract specifications for gold align with the parameters used in this strategy.