CNN Fear and Greed StrategyAdaptation of the CNN Fear and Greed Index Indicator (Original by EdgeTools)

The following changes have been implemented:

Put/Call Ratio Data Source: The data source for the Put/Call Ratio has been updated.

Bond Data Source: The data sources for the bond components (Safe Haven Demand and Junk Bond Demand) have been updated.

Normalization Adjustment: The normalization method has been adjusted to allow the CNN Fear and Greed Index to display over a longer historical period, optimizing it for backtesting purposes.

Style Modification: The display style has been modified for a simpler and cleaner appearance.

Strategy Logic Addition: Added a new strategy entry condition: index >= 25 AND index crosses over its 5-period Simple Moving Average (SMA), and a corresponding exit condition of holding the position for 252 bars (days).

CNN Fear & Greed Backtest Strategy (Adapted)

This script is an adaptation of the popular CNN Fear & Greed Index, originally created by EdgeTools, with significant modifications to optimize it for long-term backtesting on the TradingView platform.

The core function of the Fear & Greed Index is to measure the current emotional state of the stock market, ranging from 0 (Extreme Fear) to 100 (Extreme Greed). It operates on the principle that excessive fear drives prices too low (a potential buying opportunity), and excessive greed drives them too high (a potential selling opportunity).

Key Components of the Index (7 Factors)

The composite index is calculated as a weighted average of seven market indicators, each normalized to a score between 0 and 100:

Market Momentum: S&P 500's current level vs. its 125-day Moving Average.

Stock Price Strength: Stocks hitting 52-week highs vs. those hitting 52-week lows.

Stock Price Breadth: Measured by the McClellan Volume Summation Index (or similar volume/breadth metric).

Put/Call Ratio: The relationship between volume of put options (bearish bets) and call options (bullish bets).

Market Volatility: The CBOE VIX Index relative to its 50-day Moving Average.

Safe Haven Demand: The relative performance of stocks (S&P 500) vs. bonds.

Junk Bond Demand: The spread between high-yield (junk) bonds and U.S. Treasury yields.

Critical Adaptations for Backtesting

To improve the index's utility for quantitative analysis, the following changes were made:

Long-Term Normalization: The original normalization method (ta.stdev over a short LENGTH) has been replaced or adjusted to use longer historical data. This change ensures the index generates consistent and comparable sentiment scores across decades of market history, which is crucial for reliable backtesting results.

Updated Data Sources: Specific ticker requests for the Put/Call Ratio and Bond components (Safe Haven and Junk Bond Demand) have been updated to use the most reliable and long-running data available on TradingView, reducing data gaps and improving chart continuity.

Simplified Visuals: The chart display is streamlined, focusing only on the final Fear & Greed Index line and key threshold levels (25, 50, 75) for quick visual assessment.

Integrated Trading Strategy

This script also includes a simple, rules-based strategy designed to test the counter-trend philosophy of the index:

Entry Logic (Long Position): A long position is initiated when the market shows increasing fear, specifically when the index score is less than or equal to the configurable FEAR_LEVEL (default 25) and the index crosses above its own short-term 5-period Simple Moving Average (SMA). This crossover acts as a confirmation that sentiment may be starting to turn around from peak fear.

Exit Logic (Time-Based): All positions are subject to a time-based exit after holding for 252 trading days (approximately one year). This fixed holding period aims to capture the typical duration of a cyclical market recovery following a major panic event.

Cari dalam skrip untuk "ha溢价率"

Higher Timeframe Candle LevelsThis is an indicator that shows higher time frame candle levels from various preset timeframes. These higher time frame candles act as support and resistance levels, so look for reversals and continuations off of these levels. When price exceeds the high or low of these levels, you should look for breakouts in the same direction and trade with the trend.

It includes candle levels for the following timeframes: 1 hour, 4 hour, 1 day, 1 week, 1 month, 1 quarter and 1 year. The indicator also includes a trend candle coloring feature, trend strength scoring table, stop loss feature, line identification labels, alerts for trend changes, alerts for level touches and full customization of all options.

How To Trade With This Indicator

These higher timeframe candle levels will act as support and resistance levels, so look for price to react at any of the levels you have turned on and then look for potential bounce or reversal signs at those levels so you can trade those direction changes. Price outside of the higher timeframe candle highs and low typically signals a breakout as well, so look for price to continue after passing the highs or lows.

You can use the direction of the higher timeframe candles as your trend as well. Try to only trade in the direction of the trend of the higher timeframes to increase the likelihood of your trade going in your favor.

The highs and lows of daily and up levels are excellent levels to find quick reversal off of. Watch for price action to struggle to break through these levels and then trade the reversal. If price breaks through these levels easily, watch for price to retest the level and then continue beyond that level. Trade the retest in the direction of the trend.

The open, close and midline levels are excellent for trading bounces. Watch for price to form wicks beyond these levels and close on the other side and use that as a sign that price may bounce there. Use that with price action to confirm your trade and then take trades off of those level bounces.

Use the alerts for daily and up timeframe level touches across all of your favorite markets so that way you are always notified in real time when price is at a level that could provide a potential trading opportunity.

Higher Time Frame Candle Levels

The indicator shows the current candle open, previous open, previous high, previous low, previous close and previous candle body midline levels of each candle for each time frame. This helps you easily see what is going on with the higher time frame candles and read the price action from your lower time frame charts.

Each candle level will paint red if it was a down candle or green if it was an up candle, except the midlines and current candle open lines, those are a different color for easy differentiation. The line colors can be customized to your preferences in the settings and you can also toggle the candle body coloring on or off, as well as change the color of the candle body background.

Each timeframe can be adjusted to your preferences, allowing you to turn all of the levels on or off. You can also adjust how many previous candles show up on your chart so you can backtest it and see for yourself how accurate these levels are.

When adjusting the number of candles, you will get a notification if you have more than 500 lines turned on, so just turn down the number of levels for whatever timeframe you can’t see on your chart to lower that number below 500. The notification will go away once you are under 500 lines again. Each candle has 6 lines if all levels are turned on for that timeframe: open, current candle open, close, high, low and midline. The default settings keep you under 500 lines total, so just be aware of that limitation when adjusting those numbers and adjust the number of levels down on the timeframes that are not useful on the current chart bar.

You can also extend the levels right on any time frame from the daily levels and above. This is useful when price is breaking above or below all levels and you need to know if there are any other previous candle levels in the way as price moves away from the most recent higher time frame candles.

To understand the intraday trend of each higher time frame, look to see where price is at according to each higher time frame candle. If the price is above the midline of the candle, it is bullish. If the price is above the candle body it is more bullish. If the price is above the high, it is very bullish. If the price is below the midline of the candle, it is bearish. If the price is below the candle body it is more bearish. If the price is below the low, it is very bearish. Make sure you backtest this yourself and go through lots of historical data to get a feel for how price reacts to these levels and establishes the trend. Then use that trend information to your advantage and trade in the direction of the trend.

Since users are limited to a certain amount of historical bars based on which Tradingview plan you have, some longer timeframe levels won’t show up because the start of that candle is too far back in history. You will get a notification at the top of that chart if that happens. It will tell you to lower the display timeframe for that timeframe until that notification goes away, which means it was able to plot the most recent candle for that timeframe on your chart.

Trend Candle Coloring

The indicator includes a feature that paints the candles based on whether the current time frame candles are above or below the most recent midline, candle body or high & low of a higher time frame candle of your choice. This helps you see the overall trend of the higher timeframe so you can trade with the trend.

The candle coloring will have an up color, down color and neutral color which can all be customized to suit your preferences. If the current time frame candle close is above the setting you choose, it will show the up color. If the current time frame candle close is below the setting you choose, it will show the down color. If the current time frame candle close is equal to or in the middle of the setting you chose, it will show the neutral color.

So, for example if you set it to candle body, then it will show the up color if the current candle is above the top of the candle body, down color if it is below the bottom of the candle body and neutral color if it is inside the candle body. This helps you wait for price action to move beyond the inside of the previous higher time frame candle before taking a position when price is breaking out of that previous candle so you can trade the momentum of that move. The candle coloring is fully customizable, but make sure to turn off your candle coloring on other indicators and your chart settings for it to show up properly.

Trend Strength Scoring Table

The trend strength scoring table displays a table at the bottom of the screen(table position is customizable), showing a score for the trend strength of each higher time frame. If the current candle close is above the midline, its strength is 1. If the current candle close is above the midline, but below the top of the candle body, its strength is 2. If the current candle close is above the high, its strength is 3. The same goes for below the midline, bottom of the candle body and below the low, but the scores would be negative 1, 2 or 3 instead.

This trend strength table allows you to quickly identify the trend on each higher time frame so you can wait until the trend is the same across all time frames before placing a trade in the direction of the trend. It also shows a total score on the far right side that adds all of the current trend scores together to give you a total strength score. Try to only trade when that number is very high compared to how many time frames you have turned on. Each time frame can have up to a maximum score of 3 if bullish and -3 if bearish. Each time frame in the table can be turned on or off to suit your preferences.

Stop Loss Feature

There is also a stop loss feature that you can set to whatever time frame you choose and whatever direction you chose, such as long or short. It will follow the most recent higher time frame candle’s trend using one of the following settings: candle body, high & low or midline. Once a new higher time frame candle is created, the stop loss will update to the most recent candle’s levels so you can use these levels as a trailing stop loss to maximize your wins.

If you have it set to use the candle body and it is set to long mode, then the stop loss will use the previous higher time frame candle’s lowest candle body level. So if it was an up candle previously, it will use the open. If it was a down candle previously, it will use the close. The opposite is true for short positions.

The stop loss will start working once you turn it on in the settings and will update automatically as new higher time frame candles are formed. It also shows a line of where the stop loss was previously since it was turned on.

I recommend using the high & low setting, especially when the market starts trending.

Candle Level Identification Labels

There are labels for each level starting with the 4 hour time frame and above so you can easily tell what level of each candle you are looking at, even if the rest of the candle is not showing within the chart pane. You can customize the label coloring for up candles and down candles and midlines as well as adjust the number of bars that the labels are offset from the current bar so they are visible on your chart without overlapping the current price action or other indicator labels. Labels for each time frame can be turned on or off as needed. The 1 hour labels were not included because it clogs up the chart, but it has labels for all time frames from the 4 hour candles and up.

Alerts

The indicator includes alerts for when the trend has changed to the opposite direction. The trend change alert is based on your settings for the Trend Candle Coloring. Whatever settings you have the trend candle coloring set to, will be used to set up your alerts. The Trend Candle Coloring setting must be turned on as well when creating your alerts for it to work properly. Make sure to backtest your settings and then create your alerts.

It also has alerts for when price is touching an open or close, high or low, midline or any of those levels for each timeframe. This allows you to be notified when price touches one of these levels so you can check the chart and look for potential trade opportunities if price wants to bounce off of that level. To make it easy for you to get alerts on many different tickers, just use the alert for any level touch on whatever timeframes you want.

Other Indicators To Pair This With

Use this in combination with our Trend Strength Indicator so you can visually see the historic and current trend for all of these levels. You should also use our Breakout Scanner to find other markets with strong trends so you always know which market is trending the strongest and can trade those. Trend Strength Indicator, Higher Timeframe Candle Levels and the Breakout Scanner all use the same levels and calculate the trend scores the same way so they are designed to work together to help you quickly be able to read a chart and find what direction to trade in.

Sector Analysis [SS]Introducing the most powerful sector analysis tool/indicator available, to date, in Pine!

This is a whopper indicator, so be sure to read carefully to ensure you understand its applications and uses!

First of all, because this is a whopper, let's go over the key functional points of the indicator.

The indicator compares the 11 main sector ETFs against whichever ticker you are looking at.

The functions include the following:

Ability to pull technicals from the sectors, such as RSI, Stochastic and Z-Score;

Ability to look at the correlation of the sector ETF to the current ticker you are looking at.

Ability to calculate the R2 value between the ticker you are looking at and each sector.

The ability to run a Two Tailed T-Test against the log returns of the Ticker of interest and the Sector (to analyze statistically significant returns between sectors/tickers).

The ability to analyze the distribution of returns across all sector ETFs.

The ability to pull buying and selling volume across all sector ETFs.

The ability to create an integrated moving average using a sector ETF to predict the expected close range of a ticker of interest.

These are the highlight functions. Below, I will go more into them, what they mean and how to use them.

Pulling Technicals

This is pretty straight forward. You can pull technicals, such as RSI, Stochastic and Z-Score from all the sector ETFs and view them in a table.

See below for the example:

Pulling Correlation

In order to see which sector your ticker of interest follows more closely, we need to look first at correlation and then at R2.

The correlation will look at the immediate relationship over a specified time. A highly positive value, indicates a strong, symbiotic relationship, which the sector and the ticker follow each other. This would be represented by a correlation of 0.8 or higher.

A strong negative correlation, such as -0.8 or lower, indicates that the sector and the ticker are completely opposite. When one goes up, the other goes down and vice versa.

You can adjust your correlation assessment length directly in the settings menu:

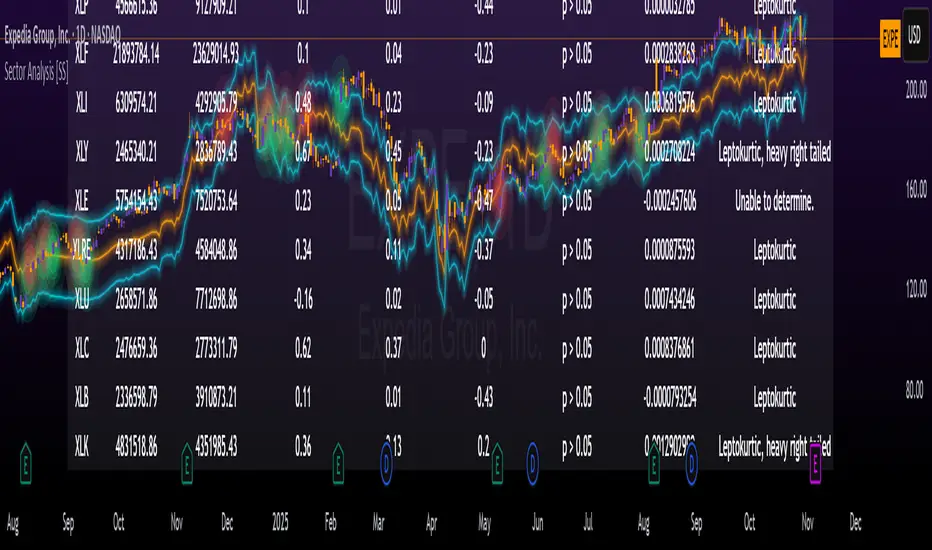

If you want to use a sector ETF to find the expected range for a ticker of interest, it is important to locate the highest, POSITIVE, correlation value. Here are the results for MSFT at a correlation lookback of 200:

In this example, we can see the best relationship is with the ETF XLK.

Analysis of R2

R2 is an important metric. It essentially measures how much of the variance between 2 tickers are explained by a simple, linear relationship.

A high R2 means that a huge degree of variance can be explained between the 2 tickers. A low R2 means that it cannot and that the 2 tickers are likely not integrated or closely related.

In general, if you want to use the sector ETF to find the mean and trading range and identify over-valuation/over-extension and under-extension statistically, you need to see both a high correlation and a high R-Squared. These 2 metrics should be analyzed together.

Let's take a look at MSFT:

Here, despite the correlation implying that XLK was the ticker we should use to analyze, when we look at the R Squared, we see actually, we should be using XLI.

XLI has a strong positive relationship with MSFT, albeit a bit less than XLK, but the R2 is solid, > 0.9, indicating the XLI explains much of MSFT's variance.

Two Tailed T-Test

A two tailed T-test analyzes whether there is a statistically significant difference between 2 different groups, or in our case, tickers.

The T-Test is conducted on the log returns of the ticker of interest and the sector. You then can see the P value results, whether it is significant or not. Let's look at MSFT again:

Looking at this, we can see there is no statistically significant difference in returns between MSFT and any of the sectors.

We can also see the SMA of the log returns for more detailed comparison.

If we were to observe a significant finding on the T-Test metrics, this would indicate that one sector either outperforms or underperforms your ticker to a statistically significant degree! If you stumble upon this, you would check the average log returns to compare against the average returns of your ticker of interest, to see whether there is better performance or worse performance from the sector ETF vs. your ticker of interest.

Analyzing the Distribution

The indicator will also analyze the distribution of returns.

This is an interesting option as it can help you ascertain risk. Normally distributed returns imply mean reverting behavviour. Deviations from that imply trending behaviour with higher risk expectancy. If we look at the distribution statistics currently over the last 200 trading days, here are the results:

Here, we can see all show signs of trending, as none of the returns are normally distributed. The highest risk sectors are XLK and XLY.

Why are they the highest risk?

Because the indicator has found a heavy right tailed distribution, indicated sudden and erratic mean reversion/losses are possible.

Creating an MA

Now for the big bonus of the indicator!

The indicator can actually create a regression based range from closely correlated sectors, so you can see, in sectors that are strongly correlated to your ticker, whether your ticker is over-bought, oversold or has mean reverted.

Let's look at MSFT using XLI, our previously identified sector with a high correlation and high R2 value:

The results are pretty impressive.

You can see that MSFT has rode the mean of the sector on the daily timeframe for quite some time. Each time it over extended itself above the sector implied range, it mean reverted.

Currently, if you were to trade based on Pairs or statistics, MSFT is no trade as it is currently trading at its sector mean.

If you are a visual person, you can have the indicator plot the mean reversion points directly:

Green represents a bullish mean reversion and red a bearish mean reversion.

Concluding Remarks

If you like pair trading, following the link between sectors and tickers or want a more objective way to determine whether a ticker is over-bought or oversold, this indicator can help you.

In addition to doing this, the indicator can provide risk insights into different sectors by looking at the distribution, as well as identify under-performing sectors or tickers.

It can also shed light on sectors that may be technically over-bought or oversold by looking at Z-Score, stochastics and RSI.

Its a whopper and I really hope you find it helpful and useful!

Thanks everyone for reading and checking this out!

Safe trades!

GTI BGTI: RSI Suite (Standard • Stochastic • Smoothed)

A three-layer momentum and trend toolkit that combines Standard RSI, Stochastic RSI, and a Smoothed/“Macro” RSI to help you read intraday swings, trend transitions, and high-probability reversal/continuation spots.

All in one pane with intuitive coloring and optional divergence markers and alerts.

Why this works

* Stochastic RSI (K/D) visualizes fast momentum swings and timing.

* Standard RSI moves more gradually, helping confirm trend transitions that may span several Stochastic cycles.

* Smoothed RSI (Average → Macro) adds a second-pass filter and slope persistence to reveal the macro direction while suppressing noise.

Used together, Stochastic guides entries/exits around local highs/lows, while the RSI layers improve confidence when a small swing is likely part of a larger turn.

What you’ll see

* Standard RSI (yellow; pink above Bull line, aqua below Bear line).

* Stochastic RSI (K/D) with contextual colors:

* Greens when RSI is weak/oversold (bearish conditions → watch for bullish reversals/continuations).

* Reds when RSI is strong/overbought (bullish conditions → watch for bearish reversals/continuations).

* Smoothed (Macro) RSI with trend color:

* Red when macro is ascending (bullish),

* Aqua when macro is descending (bearish).

* Divergences (optional markers):

* Bearish: RSI Lower High + Price Higher High (red ⬇).

* Bullish: RSI Higher Low + Price Lower Low (green ⬆).

* No repaint: pivots confirm after the chosen right-bars window.

How to use it

* Bullish Reversal

* Macro RSI is reversing at a higher low after price has been in a overall downtrend

* Stochastic RSI is switching from green to red in an overall downtrend

* Bullish Oversold

* Macro RSI is reversing from a significantly low level after price has a short but strong dip during an overall uptrend

* Stochastic RSI is switching from green to red in an overall uptrend

* Bullish Continuation

* Macro RSI is ascending with a strong slope or forming a higher low above the 50 line

* Stochastic RSI is reaching a bottom but still painted red

* Bearish Reversal

* Macro RSI is reversing at a lower high after price has been in a overall uptrend

* Stochastic RSI is switching from red to green in an overall uptrend

* Bearish Overbought

* Macro RSI is reversing from a significantly high level after price has a short but strong jump during an overall downtrend

* Stochastic RSI is switching from red to green in an overall downtrend

* Bearish Continuation

* Macro RSI is descending with a strong slope or forming a lower high below the 50 line

* Stochastic RSI is reaching a top but still painted green

* Divergences: Use as signals of exhaustion—best when aligned with Macro RSI color/slope and key levels (e.g., Bull/Bear lines, 50 midline).

*** IMPORTANT ***

* Stack confluence, don’t single-signal trade. Look for:

* 1) Macro RSI color & slope (red = ascending/bullish, aqua = descending/bearish)

* 2) Standard RSI location (above/below Bull/Bear lines or 50)

* 3) Stoch flip + direction

* 4) Price structure (HH/HL vs LH/LL)

* 5) Divergence type (regular vs hidden) at meaningful levels

* Trade with the macro

* Prioritize longs when Macro RSI is red or just flipped up

* Prioritize shorts when Macro RSI is aqua or just flipped down

* Counter-trend setups = smaller size and faster management.

* Location > signal

* The same crossover/divergence is higher quality near Bull (~60)/Bear(~40) or extremes than in the mid-range chop around 50.

* Early vs confirmed

* Use the early pivot heads-up for anticipation, but scale in only after the confirmed pivot (right-bars complete). If early signal fails to confirm, stand down.

* Define invalidation upfront

* For divergence entries, place stops beyond the pivot extreme (LL/HH). If Macro RSI flips against your trade or RSI breaks back through 50 with slope, exit or tighten.

* Multi-timeframe alignment

* Best results come when entry timeframe (e.g., 1H) aligns with higher-TF macro (e.g., 4H/D). If they disagree, treat it as mean-reversion only.

* Avoid common traps

* Skip: isolated Stochastic flips without RSI support, divergences without price HH/LL confirmation, and serial divergences when Macro RSI slope is strong against the idea.

* Parameter guidance

* Start with defaults; then tune: confirmBars 3–7, minSlope 0.05–0.15 RSI pts/bar, pivot left/right tighter for faster but noisier signals, wider for cleaner but fewer.

* Alerts = workflow, not auto-trades

* Use Macro Flip + Divergence alerts as a checklist trigger; enter only when your confluence rules are met and risk is defined.

Key inputs (tweak to your market/timeframe)

* RSI / Stochastic lengths and K/D smoothing.

* Bull / Bear Lines (default 61.1 / 43.6).

* Average RSI Method/Length (SMA/EMA/RMA/WMA) + Macro Smooth Length.

* Trend confirmation: bars of persistence and minimum slope to reduce flip noise.

* Pivot look-back (left/right) for divergence confirmation strictness.

Alerts included

* Macro Flip Up / Down (Smoothed RSI regime change).

* RSI Bullish/Bearish Divergence (confirmed at pivot).

* Stochastic RSI continuation/divergence (optional).

Tips

* Level + Slope matter. High/low RSI level flags conditions; slope confirms impulse/continuation.

* Let Stochastic time the swing; let Macro RSI filter the trend.

* Tighten or loosen pivot windows to trade fewer/cleaner vs. more/faster signals.

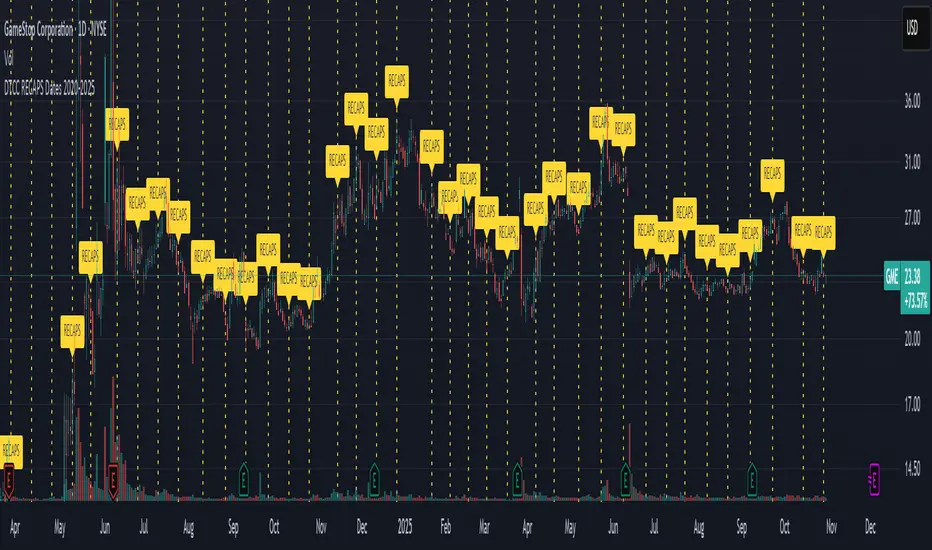

DTCC RECAPS Dates 2020-2025This is a simple indicator which marks the RECAPS dates of the DTCC, during the periods of 2020 to 2025.

These dates have marked clear settlement squeezes in the past, such as GME's squeeze of January 2021.

------------------------------------------------------------------------------------------------------------------

The Depository Trust & Clearing Corporation (DTCC) has published the 2025 schedule for its Reconfirmation and Re-pricing Service (RECAPS) through the National Securities Clearing Corporation (NSCC). RECAPS is a monthly process for comparing and re-pricing eligible equities, municipals, corporate bonds, and Unit Investment Trusts (UITs) that have aged two business days or more .

At its core, the Reconfirmation and Re-pricing Service (RECAPS) is a risk management tool used by the National Securities Clearing Corporation (NSCC), a subsidiary of the DTCC. Its primary purpose is to reduce the risks associated with aged, unsettled trades in the U.S. securities market .

When a trade is executed, it is sent to the NSCC for clearing and settlement. However, for various reasons, some trades may not settle on their scheduled date and become "aged." These unsettled trades create risk for both the trading parties and the clearinghouse (NSCC) because the value of the underlying securities can change over time. If a trade fails to settle and one of the parties defaults, the NSCC may have to step in to complete the transaction at the current market price, which could result in a loss.

RECAPS mitigates this risk by systematically re-pricing these aged, open trading obligations to the current market value. This process ensures that the financial obligations of the clearing members accurately reflect the present value of the securities, preventing the accumulation of significant, unmanaged market risk .

Detailed Mechanics: How Does it Work?

The RECAPS process revolves around two key dates you asked about: the RECAPS Date and the Settlement Date .

The RECAPS Date: On this day, the NSCC runs a process to identify all eligible trades that have remained unsettled for two business days or more. These "aged" trades are then re-priced to the current market value. This re-pricing is not just a simple recalculation; it generates new settlement instructions. The original, unsettled trade is effectively cancelled and replaced with a new one at the current market price. This is done through the NSCC's Obligation Warehouse.

The Settlement Date: This is typically the business day following the RECAPS date. On this date, the financial settlement of the re-priced trades occurs. The difference in value between the original trade price and the new, re-priced value is settled between the two trading parties. This "mark-to-market" adjustment is processed through the members' settlement accounts at the DTCC.

Essentially, the process ensures that any gains or losses due to price changes in the underlying security are realized and settled periodically, rather than being deferred until the trade is ultimately settled or cancelled.

Are These Dates Used to Check Margin Requirements?

Yes, indirectly, this process is closely tied to managing margin and collateral requirements for NSCC members. Here’s how:

The NSCC requires its members to post collateral to a clearing fund, which acts as a mutualized guarantee against defaults. The amount of collateral each member must provide is calculated based on their potential risk exposure to the clearinghouse.

By re-pricing aged trades to current market values through RECAPS, the NSCC gets a more accurate picture of each member's outstanding obligations and, therefore, their current risk profile. If a member has a large number of unsettled trades that have moved against them in value, the re-pricing will crystallize that loss, which will be settled the next day.

This regular re-pricing and settlement of aged trades prevent the build-up of large, unrealized losses that could increase a member's risk profile beyond what their posted collateral can cover. While RECAPS is not the only mechanism for calculating margin (the NSCC has a complex system for daily margin calls based on overall portfolio risk), it is a crucial component for managing the specific risk posed by aged, unsettled transactions. It ensures that the value of these obligations is kept current, which in turn helps ensure that collateral levels remain adequate.

--------------------------------------------------------------------------------------------------------------

Future dates of 2025:

- November 12, 2025 (Wed)

- November 25, 2025 (Tue)

- December 11, 2025 (Thu)

- December 29, 2025 (Mon)

The dates for 2026 haven't been published yet at this time.

The RECAPS process is essentially the industry's way of retrying the settlement of all unresolved FTDs, netting outstanding obligations, and gradually forcing resolution (either delivery or buy-in). Monitoring RECAPS cycles is one way to track the lifecycle, accumulation, and eventual resolution (or persistence) of failures to deliver in the U.S. market.

The US Stock market has become a game of settlement dates and FTDs, therefore this can be useful to track.

[AS] MACD-v & Hist [Alex Spiroglou | S.M.A.R.T. TRADER SYSTEMS] MACD-v & MACD-v Histogram

=======================================

Volatility Normalised Momentum 📈

Twice Awarded Indicator 🏆

=======================================

=======================================

✅ 1. INTRODUCTION TO THE MACD-v ✅

=======================================

I created the MACD-v in 2015,

as a way to deal with the limitations

of well known indicators like the Stochastic, RSI, MACD.

I decided to publicly share a very small part of my research

in the form of a research paper I wrote in 2022,

titled "MACD-v: Volatility Normalised Momentum".

That paper was awarded twice:

1. The "Charles H. Dow" Award (2022),

for outstanding research in Technical Analysis,

by the Chartered Market Technicians Association (CMTA)

2. The "Founders" Award (2022),

for advances in Active Investment Management,

by the National Association of Active Investment Managers (NAAIM)

=======================================

===================================================

❌ 2. WHY CREATE THE MACD-v ?

THE LIMITATIONS OF CONVENTIONAL MOMENTUM INDICATORS

====================================================

Technical Analysis indicators focused on momentum,

come in two general categories,

each with its own set of limitations:

(i) Range Bound Oscillators (RSI, Stochastics, etc)

These usually have a scaling of 0-100,

and thus have the advantage of having normalised readings,

that are comparable across time and securities.

However they have the following limitations (among others):

1. Skewing effect of steep trends

2. Indicator values do not adjust with and reflect true momentum

(indicator values are capped to 100)

(ii) Unbound Oscillators (MACD, RoC, etc)

These are boundless indicators,

and can expand with the market,

without being limited by a 0-100 scaling,

and thus have the advantage of really measuring momentum.

They have the main following limitations (among others):

1. Subjectivity of overbought / oversold levels

2. Not comparable across time

3. Not comparable across securities

=======================================

=======================================

💡 3. THE SOLUTION TO SOLVE THESE LIMITATIONS

=======================================

In order to deal with these limitations,

I decided to create an indicator,

that would be the "Best of two worlds".

A unique & hybrid indicator,

that would have objective normalised readings

(similar to Range Bound Oscillators - RSI)

but would also be able to have no upper/lower boundaries

(similar to Unbound Oscillators - MACD).

This would be achieved by "normalising" a boundless oscillator (MACD)

=======================================

==================================================

⛔ 4. DEEP DIVE INTO THE 5 LIMITATIONS OF THE MACD

==================================================

A Bloomberg study found that the MACD

is the most popular indicator after the RSI,

but the MACD has 5 BIG limitations.

Limitation 1: MACD values are not comparable across Time

The raw MACD values shift

as the underlying security's absolute value changes across time,

making historical comparisons obsolete

e.g S&P 500 maximum MACD was 1.56 in 1957-1971,

but reached 86.31 in 2019-2021 - not indicating 55x stronger momentum,

but simply different price levels.

Limitation 2: MACD values are not comparable across Assets

Traditional MACD cannot compare momentum between different assets.

S&P 500 MACD of 65 versus EUR/USD MACD of -0.5

reflects absolute price differences, not momentum differences

Limitation 3: MACD values cannot be Systematically Classified

Due to limitations #1 & #2, it is not possible to create

a momentum level classification scale

where one can define "fast", "slow", "overbought", "oversold" momentum

making systematic analysis impossible

Limitation 4: MACD Signal Line gives false crossovers in low-momentum ranges

In range-bound, low momentum environments,

most of the MACD signal line crossovers are false (noise)

Since there is no objective momentum classification system (limitation #3),

it is not possible to filter these signals out,

by avoiding them when momentum is low

Limitation 5: MACD Signal Line gives late crossovers in high momentum regimes.

Signal lag in strong trends not good at timing the turning point

— In high-momentum moves, MACD crossovers may come late.

Since there is no objective momentum classification system (limitation #3),

it is not possible to filter these signals out,

by avoiding them when momentum is high

===================================================================

===================================================================

🏆 5. MACD-v : THE SOLUTION TO THE LIMITATIONS OF THE MACD , RSI, etc

====================================================================

MACD-v is a volatility normalised momentum indicator.

It remedies these 5 limitations of the classic MACD,

while creating a tool with unique properties.

Formula: × 100

MACD-V enhances the classic MACD by normalizing for volatility,

transforming price-dependent readings into standardized momentum values.

This resolves key limitations of traditional MACD and adds significant analytical power.

Core Advantages of MACD-V

Advantage 1: Time-Based Stability

MACD-V values are consistent and comparable over time.

A reading of 100 has the same meaning today as it did in the past

(unlike traditional MACD which is influenced by changes in price and volatility over time)

Advantage 2: Cross-Market Comparability

MACD-V provides universal scaling.

Readings (e.g., ±50) apply consistently across all asset classes—stocks,

bonds, commodities, or currencies,

allowing traders to compare momentum across markets reliably.

Advantage 3: Objective Momentum Classification

MACD-V includes a defined 5-range momentum lifecycle

with standardized thresholds (e.g., -150 to +150).

This offers an objective framework for analyzing market conditions

and supports integration with broader models.

Advantage 4: False Signal Reduction in Low-Momentum Regimes

MACD-V introduces a "neutral zone" (typically -50 to +50)

to filter out these low-probability signals.

Advantage 5: Improved Signal Timing in High-Momentum Regimes

MACD-V identifies extremely strong trends,

allowing for more precise entry and exit points.

Advantage 6: Trend-Adaptive Scaling

Unlike bounded oscillators like RSI or Stochastic,

MACD-V dynamically expands with trend strength,

providing clearer momentum insights without artificial limits.

Advantage 7: Enhanced Divergence Detection

MACD-V offers more reliable divergence signals

by avoiding distortion at extreme levels,

a common flaw in bounded indicators (RSI, etc)

====================================================================

=======================================

⚒️ 5. HOW TO USE THE MACD-v: 7 CORE PATTERNS

HOW TO USE THE MACD-v Histogram: 2 CORE PATTERNS

=======================================

>>>>>> BASIC USE (RANGE RULES) <<<<<<

The MACD-v has 7 Core Patterns (Ranges) :

1. Risk Range (Overbought)

Condition: MACD-V > Signal Line and MACD-V > +150

Interpretation: Extremely strong bullish momentum—potential exhaustion or reversal zone.

2. Retracing

Condition: MACD-V < Signal Line and MACD-V > -50

Interpretation: Mild pullback within a bullish trend.

3. Rundown

Condition: MACD-V < Signal Line and -50 > MACD-V > -150

Interpretation: Momentum is weakening—bearish pressure building.

4. Risk Range (Oversold)

Condition: MACD-V < Signal Line and MACD-V < -150

Interpretation: Extreme bearish momentum—potential for reversal or capitulation.

5. Rebounding

Condition: MACD-V > Signal Line and MACD-V > -150

Interpretation: Bullish recovery from oversold or weak conditions.

6. Rallying

Condition: MACD-V > Signal Line and MACD-V > +50

Interpretation: Strengthening bullish trend—momentum accelerating.

7. Ranging (Neutral Zone)

Condition: MACD-V remains between -50 and +50 for 20+ bars

Interpretation: Sideways market—low conviction and momentum.

The MACD-v Histogram has 2 Core Patterns (Ranges) :

1. Risk (Overbought)

Condition: Histogram > +40

Interpretation: Short-term bullish momentum is stretched—possible overextension or reversal risk.

2. Risk (Oversold)

Condition: Histogram < -40

Interpretation: Short-term bearish momentum is stretched—potential for rebound or reversal.

=======================================

=======================================

📈 6. ADVANCED PATTERNS WITH MACD-v

=======================================

Thanks to its volatility normalization,

the MACD-V framework enables the development

of a wide range of advanced pattern recognition setups,

trading signals, and strategic models.

These patterns go beyond basic crossovers,

offering deeper insight into momentum structure,

regime shifts, and high-probability trade setups.

These are not part of this script

=======================================

===========================================================

⚙️ 7. FUNCTIONALITY - HOW TO ADD THE INDICATORS TO YOUR CHART

===========================================================

The script allows you to see :

1. MACD-v

The indicator with the ranges (150,50,0,-50,-150)

and colour coded according to its 7 basic patterns

2. MACD-v Histogram

The indicator The indicator with the ranges (40,0,-40)

and colour coded according to its 2 basic ranges / patterns

3. MACD-v Heatmap

You can see the MACD-v in a Multiple Timeframe basis,

using a colour-coded Heatmap

Note that lowest timeframe in the heatmap must be the one on the chart

i.e. if you see the daily chart, then the Heatmap will be Daily, Weekly, Monthly

4. MACD-v Dashboard

You can see the MACD-v for 7 markets,

in a multiple timeframe basis

=======================================

=======================================

🤝 CONTRIBUTIONS 🤝

=======================================

I would like to thank the following people:

1. Mike Christensen for coding the indicator

@TradersPostInc, @Mik3Christ3ns3n,

2. @Indicator-Jones For allowing me to use his Scanner

3. @Daveatt For allowing me to use his heatmap

=======================================

=======================================

⚠️ LEGAL - Usage and Attribution Notice ⚠️

=======================================

Use of this Script is permitted

for personal or non-commercial purposes,

including implementation by coders and TradingView users.

However, any form of paid redistribution,

resale, or commercial exploitation is strictly prohibited.

Proper attribution to the original author is expected and appreciated,

in order to acknowledge the source

and maintain the integrity of the original work.

Failure to comply with these terms,

or to take corrective action within 48 hours of notification,

will result in a formal report to TradingView’s moderation team,

and will actively pursue account suspension and removal of the infringing script(s).

Continued violations may result in further legal action, as deemed necessary.

=======================================

=======================================

⚠️ DISCLAIMER ⚠️

=======================================

This indicator is For Educational Purposes Only (F.E.P.O.).

I am just Teaching by Example (T.B.E.)

It does not constitute investment advice.

There are no guarantees in trading - except one.

You will have losses in trading.

I can guarantee you that with 100% certainty.

The author is not responsible for any financial losses

or trading decisions made based on this indicator. 🙏

Always perform your own analysis and use proper risk management. 🛡️

=======================================

DTR & ATR with live zonesThis indicator is designed to help traders gauge the day's volatility in real-time. It compares the current Daily True Range (DTR)—the distance between the session's high and low—to the historical Average True Range (ATR).

The main purpose is to project potential price levels where the market might reach based on its average volatility. These levels (100% ATR, 150%, 200%, etc.) can be used as price targets. For instance, if you're in a long trade, you might consider taking partial or full profits as the price approaches these upper ATR extension levels. The indicator is highly customisable, allowing you to control the appearance of the ATR lines, zones, and labels to fit your charting preferences.

Core Concepts: ATR and DTR

To use this indicator effectively, it's important to understand its two main components:

Average True Range (ATR): This is a classic technical analysis indicator that measures market volatility. It calculates the average range of price movement over a specific period (e.g., 14 days). A higher ATR means the price is, on average, moving more, while a low ATR indicates less volatility. This script uses a higher timeframe ATR (e.g., Daily) to establish a stable volatility baseline for the current trading day.

Daily True Range (DTR): This is simply the difference between the current trading session's highest high and lowest low (session high - session low). It tells you how much the price has actually moved so far today.

The indicator's logic revolves around comparing the live, unfolding DTR to the historical, baseline ATR. An on-screen table conveniently shows this comparison as a percentage, to show how volatile the day has been.

How It Works: The Dynamic & Locked Mechanism

The most clever part of this indicator is how it draws the ATR levels. It operates in two distinct phases during the trading session:

Phase 1: Dynamic Expansion (Before DTR meets ATR)

At the start of the session, the DTR is small. The indicator calculates the remaining range needed to "complete" the 100% ATR level (difference = avg_atr - dtr). It then adds this remaining amount to the session high and subtracts it from the session low. This creates a "floating" 100% ATR range that expands dynamically as the session high or low is extended.

Phase 2: The Lock-in (After DTR meets or exceeds ATR)

Once the day's range (DTR) becomes equal to or greater than the avg_atr, the day has met its "expected" volatility. At this point, the levels lock in place. The indicator intelligently determines the anchor point for the locked range.

Once this primary 100% ATR range is established (either dynamically or locked), the script projects the other levels (150%, 200%, 250%, and 300%) by adding or subtracting multiples of the avg_atr from this base.

How to Use It for Trading

The primary use of this indicator is to set logical, volatility-based price targets.

Setting Profit Targets: If you enter a long position, the upper ATR levels (100%, 150%, 200%) serve as excellent areas to consider taking profits. A move to the 200% or 250% level often signifies an overextended or "exhaustion" move, making it a high-probability exit zone. For short positions, the lower ATR levels serve the same purpose.

Assessing Intraday Momentum: The on-screen table tells you how much of the expected daily range has been used. If it's early in the session and the DTR is only at 30% of the ATR, you can anticipate more significant price movement is likely to come. Conversely, if the DTR is already at 150% of ATR, the bulk of the day's move may already be complete.

Mean Reversion Signals: If the price pushes to an extreme level (e.g., 250% ATR) and shows signs of stalling (e.g., bearish divergence on an oscillator), it could signal a potential reversal or pullback, offering an opportunity for a counter-trend trade.

Key Settings

ATR Length & Smoothing Type: These settings control how the baseline ATR is calculated. The default 14 period and RMA smoothing are standard, but you can adjust them to your preference.

Session Settings: This is crucial. You must set the Market Session and Time Zone to match the primary trading hours of the asset you are analysing (e.g., "0930-1600" for the NYSE session).

Show Lines / Show Labels / Show Zones: The script gives you full control over the visual display. You can toggle each ATR level's lines, labels, and background zones individually to avoid a cluttered chart and focus only on the levels that matter to your strategy.

GRG/RGR Signal, MA, Ranges and PivotsThis indicator is a combination of several indicators.

It is a combination of two of my indicators which I solely use for trading

1. EMA 10-20-50-200, Pivots and Previous Day/Week/Month range

2. 3/4-Bar GRG / RGR Pattern (Conditional 4th Candle)

You can use them individually if you already have some of them or just use this one. Belive me when I say, this is all you need, along with market structure knowlege and even if you don’t have that, this indicator has been doing wonders for me. This is all I use. I do not use anything else.

**Note - Do checkout the indicators individually as I have added valuable information in the comment section.

It contains the following,

1. 10 EMA/SMA - configurable

2. 20 EMA/SMA - configurable

3. 50 EMA/SMA - configurable

4. 200 EMA/SMA - configurable

5. Previous Day's Range - configurable

6. Previous Week's Range - configurable

7. Previous Month's Range - configurable

8. Pivots - configurable

9. Buy Sell Signal - configurable

The Moving Averages

It is a very important combination and using it correctly with price action will strengthen your entries and exits.

The ema's or sma's added are the most powerful ones and they do definitely act as support and resistance.

The Daily/Weekly/Monthly Ranges

The Daily/Weekly/Monthly ranges are extremely important for any trader and should be used for targets and reversals.

Pivots

Pivots can provide support and resistance level. R5 and S5 can be used to check for over stretched conditions. You can customise them however you like. It is a full pivot indicator.

It is defaulted to show R5 and S5 only to reduce noise in the chart but it can be customised.

The 3/4 RGR or GRG Signal Generator

Combined with a 3/4 RGR or GRG setup can be all a trader needs.

You don't need complex strategies and SMC concepts to trade. Simple EMAs, ranges and RGR/GRG setup is the most winning combination.

This indicator can be used to identify the Green-Red-Green or Red-Green-Red pattern.

It is a price action indicator where a price action which identifies the defeat of buyers and sellers.

If the buyers comprehensively defeat the sellers then the price moves up and if the sellers defeat the buyers then the price moves down.

In my trading experience this is what defines the price movement.

It is a 3 or 4 candle pattern, beyond that i.e, 5 or more candles could mean a very sideways market and unnecessary signal generation.

How does it work?

Upside/Green signal

1. Say candle 1 is Green, which means buyers stepped in, then candle 2 is Red or a Doji, that means sellers brought the price down. Then if candle 3 is forming to be Green and breaks the closing of the 1st candle and opening of the 2nd candle, then a green arrow will appear and that is the place where you want to take your trade.

2. Here the buyers defeated the sellers.

3. Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

4. Important - We need to enter the trade as soon as the price moves above the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close. Ignore wicks.

5. But for a more optimised entry I have added an option to use candle’s highs and lows instead of open and close. This reduces lot of noise and provides us with more precise entry. This setting is turned on by default.

6. I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

7. I call it the +-+ or GRG pattern or Green-Red-Green or Buyer-Seller-Buyer or Seller defeated or just Buyer pattern.

8. Stop loss can be candle 2's mid for safe traders (that includes me) or candle 2's body low for risky traders.

9. Back testing suggests that body low will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Downside/Red signal

1. Say candle 1 is Red, which means sellers stepped in, then candle 2 is Green or a Doji, that means buyers took the price up. Then if candle 3 is forming to be Red and breaks the closing of the 1st candle and opening of the 2nd candle then a Red arrow will appear and that is the place where you want to take your trade.

2. Sometimes candle 3 falls short but candle 4 breaks candle 1's closing and candle 2's opening price. We can enter on candle 4.

3. We need to enter the trade as soon as the price moves below the candle 1 and 2's body and should not wait for the 3rd or 4th candle to close.

4. But for a more optimised entry I have added an option to use candle’s highs and lows instead of open and close. This reduces lot of noise and provides us with more precise entry. This setting is turned on by default.

5. I have restricted it to 4 candles and that is all that is needed. More than that is a longer sideways market.

6. I call it the -+- or RGR pattern or Red-Green-Red or Seller-Buyer-Seller or Buyer defeated or just Seller pattern.

7. Stop loss can be candle 2's mid for safe traders ( that includes me) or candle 2's body high for risky traders.

8. Back testing suggests that body high will be useless and result in more points in loss because for the bigger move this point will not be touched, so why not get out faster.

Combining Indicators and Signal

Combining these indicators with GRG/RGR signal can be very powerful and can provide big moves.

1. MA crossover and Signal - This is very powerful and provides a very big move. Trades can be held for longer. If after taking the trade we notice that the MA crossover has happened then trades can be held for higher targets.

2. Pivots and Signal - Pivots and add a support or resistance point. Take profits on these points. R5/S5 are over streched conditions so we can start looking for reversal signals and ignore other signals

3. Intraday Range - first 1, 5, 15 min of the day - Sideways days is when price will stay in these ranges. You can take profits at these ranges or if the range is broken and we get a signal, then it can mean that the direction will be sustained.

4. Previous Day/Week/Month Ranges - These can be used as Take Profit points if the price is moving towards them after getting the signal. If the range is broken and we get a signal then it can be a strong signal. They can also be used as reversal points if a strong signal is generated.

Important Settings

1. Include 4th Candle Confirmation - You can enable or disable the 4th candle signal to avoid the noise, but at times I have noticed that the 4th candle gives a very strong signal or I can say that the strong signal falls on the 4th candle. This is mostly a coincidence.

2. Bars to check (default 10) - You can also configure how many previous bars should the signal be generated for. 10 to 30 is good enough. To backtest increase it to 2000 or 5000 for example.

3. Use Candle High/Low for confirmation instead of Candle Open/Close - More optimized entry and noise reduction. This option is now defaulted to false.

4. Show Green-Red-Green (bull) signals - Show only bull entries. Useful when I have a predefined view i.e, I know market is going to go up today.

5. Show Red-Green-Red (bear) signals - Show only bear entries. Useful when I have a predefined view i.e, I know market is going to go down today.

6. 3rd candle should be a Strong candle before considering 4th candle - This will enforce additional logic in 4 candle setup that the 3rd candle is the candle in our direction of breakout. This means something like GRGG is mandatory, which is still the default behaviour. If disabled, the 3rd candle can be any candle and 4th candle will act as our breakout candle. This behaviour has led to breakouts and breakdowns as times, hence I added this as a separate feature. Vice-versa for a RGGR.

For a 4 candle setup till now we were expecting GRGG or RGRR but we can let the system ignore the 3rd candle completely if needed.

This will result in additional signals.

7. Three intraday ranges added for index and stock traders - 1 min, 5 min and 15 min ranges will be displayed. These are disabled by default except 15 min. These are very important ranges and in sideways days the price will usually move within the 15 min. A breakout of this range and a positive signal can be a very powerful setup.

Safe traders can avoid taking a trade in this range as it can lead to fakeouts.

The line style, width, color and opacity are configurable.

Pointers/Golden Rules

1. If after taking the trade, the next candle moves in your direction and closes strong bullish or bearish, then move SL to break even and after that you can trail it.

2. If a upside trade hits SL and immediately a down side trade signal is generated on the next candle then take it. Vice versa is true.

3. Trades need to be taken on previous 2 candle's body high or low combined and not the wicks.

4. The most losses a trader takes is on a sideways day and because in our strategy the stop loss is so small that even on a sideways day we'll get out with a little profit or worst break even.

5. Hold trades for longer targets and don't panic.

6. If last 3-4 days have been sideways then there is a good probability that today will be trending so we can hold our trade for longer targets. Inverse is true when the market has been trending for 2-3 days then volatility followed by sideways is coming (DOW theory). Target to hold the trade for whole day and not exit till the day closes.

7. In general avoid trading in the middle of the day for index and stocks. Divide the day into 3 parts and avoid the middle.

8. Use Support/Resistance, 10, 20, 50, 200 EMA/SMA, Gaps, Whole/Round numbers(very imp) for identifying targets.

9. Trail your SL.

10. For indexes I would use 5 min and 15 min timeframe and at times 10 mins.

11. For commodities and crypto we can use higher timeframe as well. Look for signals during volatile time durations and avoid trading the whole day. Signal usually gives good targets on those times.

12. If a GRG or RGR pattern appears on a daily timeframe then this is our time to go big.

13. Minimum Risk to Reward should be 1:2 and for longer targets can be 1:4 to 1:10.

14. Trade with small lot size. Money management will happen automatically.

15. With small lot size and correct Risk-Reward we can be very profitable. Don't trade with big lot size.

16. Stay in the market for longer and collect points not money.

17. Very imp - Watch market and learn to generate a market view.

18. Very imp - Only 3 type of candles are needed in trading -

Strong Bullish (Big Green candle), Strong Bearish (Big Red candle),

Hammer (it is Strong Bullish), Inverse Hammer (it is Strong Bearish)

and Doji (indecision or confusion).

If on daily timeframe I see Strong Bullish candle previous day then I am biased to the upside the next day, if I see Strong Bearish candle the previous day then I am biased to the downside the next day, if I see Doji on the previous day then I am cautious the next day, if there are back to back Dojis forming in daily or weekly then I am preparing for big move so time to go big once I get the signal.

19. Most Important Candlestick pattern - Bullish and Bearish Engulfing

20. The only Chart patterns I need -

a) Falling Wedge/Channel Bullish Pattern Uptrend or Bull Flag - Buying - Forming over a couple days for intraday and forming over a couple of weeks for swing

b) Falling Wedge/Channel Bullish Pattern Downtrend or Falling Channel - Buying

c) Rising Wedge Bearish Pattern Uptrend or Rising Channel - Selling

d) Rising Wedge Bearish Pattern Downtrend or Bear flag - Selling

e) Head and Shoulder - Over a longer period not for intraday. In 15 min takes few days and for swing 1hr or 4h or daily can take few days

f) M and W pattern - Reversal Patterns - They form within the above 4 patterns, usually resulting in the break of trend line

21. How Gaps work -

a) Small Gap up in Uptrend - Market can fill the gap and reverse. The perception is that people are buying. If previous day candle was Strong Bullish then market view is up.

b) Big Gap up in Uptrend - Not news driven - Profit booking will come but may not fill the entire gap

c) Big Gap up in Uptrend - News driven, war related, tax, interest rate - Market can keep going up without stopping.

c) Flat opening in Uptrend - Big chance of market going up. If previous day candle was Strong Bullish then view is upwards, if it was Doji then still upwards.

d) Gap down in Uptrend - Market is surprised. After going down initially it can go up

e) Small Gap down in Downtrend - Market can fill the gap and keep moving down. If previous day candle was Strong Bearish then view is still down.

f) Flat opening in Downtrend - View is down, short today.

g) Big Gap down in Downtrend - Profit booking and foolish buying will come but market view is still down.

h) Gap down with News - Volatility, sideways then down.

i) Gap Up in Downtrend - Can move up - Price can move up during 2/3rd of the day and End of the day revert and close in red.

22. Go big on bearish days for option traders. Puts are better bought and Calls are better sold.

23. Cluster of green signals can lead to bigger move on the upside and vice versa for red signals.

24. Most of this is what I learned from successful traders (from the top 2%) only the indicator is mine.

Smart Money Concept v1Smart Money Concept Indicator – Visual Interpretation Guide

What Happens When Liquidity Lines Are Broken

🟩 Green Line Broken (Buy-Side Liquidity Pool Swept)

- Indicates price has dipped below a previous swing low where sell stops are likely placed.

- Market Makers may be triggering these stops to accumulate long positions.

- Often followed by a bullish reversal.

- Trader Actions:

• Look for a bullish candle close after the sweep.

• Confirm with nearby Bullish Order Block or Fair Value Gap.

• Consider entering a Buy trade (SLH entry).

- If price continues falling: Indicates trend continuation and invalidation of the buy-side liquidity zone.

🟥 Red Line Broken (Sell-Side Liquidity Pool Swept)

- Indicates price has moved above a previous swing high where buy stops are likely placed.

- Market Makers may be triggering these stops to accumulate short positions.

- Often followed by a bearish reversal.

- Trader Actions:

• Look for a bearish candle close after the sweep.

• Confirm with nearby Bearish Order Block or Fair Value Gap.

• Consider entering a Sell trade (SLH entry).

- If price continues rising: Indicates trend continuation and invalidation of the sell-side liquidity zone.

Chart-Based Interpretation of Green Line Breaks

In the provided DOGE/USD 15-minute chart image:

- Green lines represent buy-side liquidity zones.

- If these lines are broken:

• It may be a stop hunt before a bullish continuation.

• Or a false Break of Structure (BOS) leading to deeper retracement.

- Confirmation is needed from candle structure and nearby OB/FVG zones.

Is the Pink Zone a Valid Bullish Order Block?

To validate the pink zone as a Bullish OB:

- It should be formed by a strong down-close candle followed by a bullish move.

- Price should have rallied from this zone previously.

- If price is now retesting it and showing bullish reaction, it confirms validity.

- If formed during low volume or price never rallied from it, it may not be valid.

Smart Money Concept - Liquidity Line Breaks Explained

This document explains how traders should interpret the breaking of green (buy-side) and red (sell-side) liquidity lines when using the Smart Money Concept indicator. These lines represent key liquidity pools where stop orders are likely placed.

🟩 Green Line Broken (Buy-Side Liquidity Pool Swept)

When the green line is broken, it indicates:

• - Price has dipped below a previous swing low where sell stops were likely placed.

• - Market Makers have triggered those stops to accumulate long positions.

• - This is often followed by a bullish reversal.

Trader Actions:

• - Look for a bullish candle close after the sweep.

• - Confirm with a nearby Bullish Order Block or Fair Value Gap.

• - Consider entering a Buy trade (SLH entry).

🟥 Red Line Broken (Sell-Side Liquidity Pool Swept)

When the red line is broken, it indicates:

• - Price has moved above a previous swing high where buy stops were likely placed.

• - Market Makers have triggered those stops to accumulate short positions.

• - This is often followed by a bearish reversal.

Trader Actions:

• - Look for a bearish candle close after the sweep.

• - Confirm with a nearby Bearish Order Block or Fair Value Gap.

• - Consider entering a Sell trade (SLH entry).

📌 Additional Notes

• - If price continues beyond the liquidity line without reversal, it may indicate a trend continuation rather than a stop hunt.

• - Always confirm with Higher Time Frame bias, Institutional Order Flow, and price reaction at the zone.

BayesStack RSI [CHE]BayesStack RSI — Stacked RSI with Bayesian outcome stats and gradient visualization

Summary

BayesStack RSI builds a four-length RSI stack and evaluates it with a simple Bayesian success model over a rolling window. It highlights bull and bear stack regimes, colors price with magnitude-based gradients, and reports per-regime counts, wins, and estimated win rate in a compact table. Signals seek to be more robust through explicit ordering tolerance, optional midline gating, and outcome evaluation that waits for events to mature by a fixed horizon. The design focuses on readable structure, conservative confirmation, and actionable context rather than raw oscillator flips.

Motivation: Why this design?

Classical RSI signals flip frequently in volatile phases and drift in calm regimes. Pure threshold rules often misclassify shallow pullbacks and stacked momentum phases. The core idea here is ordered, spaced RSI layers combined with outcome tracking. By requiring a consistent order with a tolerance and optionally gating by the midline, regime identification becomes clearer. A horizon-based maturation check and smoothed win-rate estimate provide pragmatic feedback about how often a given stack has recently worked.

What’s different vs. standard approaches?

Reference baseline: Traditional single-length RSI with overbought and oversold rules or simple crossovers.

Architecture differences:

Four fixed RSI lengths with strict ordering and a spacing tolerance.

Optional requirement that all RSI values stay above or below the midline for bull or bear regimes.

Outcome evaluation after a fixed horizon, then rolling counts and a prior-smoothed win rate.

Dispersion measurement across the four RSIs with a percent-rank diagnostic.

Gradient coloring of candles and wicks driven by stack magnitude.

A last-bar statistics table with counts, wins, win rate, dispersion, and priors.

Practical effect: Charts emphasize sustained momentum alignment instead of single-length crosses. Users see when regimes start, how strong alignment is, and how that regime has recently performed for the chosen horizon.

How it works (technical)

The script computes RSI on four lengths and forms a “stack” when they are strictly ordered with at least the chosen tolerance between adjacent lengths. A bull stack requires a descending set from long to short with positive spacing. A bear stack requires the opposite. Optional gating further requires all RSI values to sit above or below the midline.

For evaluation, each detected stack is checked again after the horizon has fully elapsed. A bull event is a success if price is higher than it was at event time after the horizon has passed. A bear event succeeds if price is lower under the same rule. Rolling sums over the training window track counts and successes; a pair of priors stabilizes the win-rate estimate when sample sizes are small.

Dispersion across the four RSIs is measured and converted to a percent rank over a configurable window. Gradients for bars and wicks are normalized over a lookback, then shaped by gamma controls to emphasize strong regimes. A statistics table is created once and updated on the last bar to minimize overhead. Overlay markers and wick coloring are rendered to the price chart even though the indicator runs in a separate pane.

Parameter Guide

Source — Input series for RSI. Default: close. Tips: Use typical price or hlc3 for smoother behavior.

Overbought / Oversold — Guide levels for context. Defaults: seventy and thirty. Bounds: fifty to one hundred, zero to fifty. Tips: Narrow the band for faster feedback.

Stacking tolerance (epsilon) — Minimum spacing between adjacent RSIs to qualify as a stack. Default: zero point twenty-five RSI points. Trade-off: Higher values reduce false stacks but delay entries.

Horizon H — Bars ahead for outcome evaluation. Default: three. Trade-off: Longer horizons reduce noise but delay success attribution.

Rolling window — Lookback for counts and wins. Default: five hundred. Trade-off: Longer windows stabilize the win rate but adapt more slowly.

Alpha prior / Beta prior — Priors used to stabilize the win-rate estimate. Defaults: one and one. Trade-off: Larger priors reduce variance with sparse samples.

Show RSI 8/13/21/34 — Toggle raw RSI lines. Default: on.

Show consensus RSI — Weighted combination of the four RSIs. Default: on.

Show OB/OS zones — Draw overbought, oversold, and midline. Default: on.

Background regime — Pane background tint during bull or bear stacks. Default: on.

Overlay regime markers — Entry markers on price when a stack forms. Default: on.

Show statistics table — Last-bar table with counts, wins, win rate, dispersion, priors, and window. Default: on.

Bull requires all above fifty / Bear requires all below fifty — Midline gate. Defaults: both on. Trade-off: Stricter regimes, fewer but cleaner signals.

Enable gradient barcolor / wick coloring — Gradient visuals mapped to stack magnitude. Defaults: on. Trade-off: Clearer regime strength vs. extra rendering cost.

Collection period — Normalization window for gradients. Default: one hundred. Trade-off: Shorter values react faster but fluctuate more.

Gamma bars and shapes / Gamma plots — Curve shaping for gradients. Defaults: zero point seven and zero point eight. Trade-off: Higher values compress weak signals and emphasize strong ones.

Gradient and wick transparency — Visual opacity controls. Defaults: zero.

Up/Down colors (dark and neon) — Gradient endpoints. Defaults: green and red pairs.

Fallback neutral candles — Directional coloring when gradients are off. Default: off.

Show last candles — Limit for gradient squares rendering. Default: three hundred thirty-three.

Dispersion percent-rank length / High and Low thresholds — Window and cutoffs for dispersion diagnostics. Defaults: two hundred fifty, eighty, and twenty.

Table X/Y, Dark theme, Text size — Table anchor, theme, and typography. Defaults: right, top, dark, small.

Reading & Interpretation

RSI stack lines: Alignment and spacing convey regime quality. Wider spacing suggests stronger alignment.

Consensus RSI: A single line that summarizes the four lengths; use as a smoother reference.

Zones: Overbought, oversold, and midline provide context rather than standalone triggers.

Background tint: Indicates active bull or bear stack.

Markers: “Bull Stack Enter” or “Bear Stack Enter” appears when the stack first forms.

Gradients: Brighter tones suggest stronger stack magnitude; dull tones suggest weak alignment.

Table: Count and Wins show sample size and successes over the window. P(win) is a prior-stabilized estimate. Dispersion percent rank near the high threshold flags stretched alignment; near the low threshold flags tight clustering.

Practical Workflows & Combinations

Trend following: Enter only on new stack markers aligned with structure such as higher highs and higher lows for bull, or lower lows and lower highs for bear. Use the consensus RSI to avoid chasing into overbought or oversold extremes.

Exits and stops: Consider reducing exposure when dispersion percent rank reaches the high threshold or when the stack loses ordering. Use the table’s P(win) as a context check rather than a direct signal.

Multi-asset and multi-timeframe: Defaults travel well on liquid assets from intraday to daily. Combine with higher-timeframe structure or moving averages for regime confirmation. The script itself does not fetch higher-timeframe data.

Behavior, Constraints & Performance

Repaint and confirmation: Stack markers evaluate on the live bar and can flip until close. Alert behavior follows TradingView settings. Outcome evaluation uses matured events and does not look into the future.

HTF and security: Not used. Repaint paths from higher-timeframe aggregation are avoided by design.

Resources: max bars back is two thousand. The script uses rolling sums, percent rank, gradient rendering, and a last-bar table update. Shapes and colored wicks add draw overhead.

Known limits: Lag can appear after sharp turns. Very small windows can overfit recent noise. P(win) is sensitive to sample size and priors. Dispersion normalization depends on the collection period.

Sensible Defaults & Quick Tuning

Start with the shipped defaults.

Too many flips: Increase stacking tolerance, enable midline gates, or lengthen the collection period.

Too sluggish: Reduce stacking tolerance, shorten the collection period, or relax midline gates.

Sparse samples: Extend the rolling window or increase priors to stabilize P(win).

Visual overload: Disable gradient squares or wick coloring, or raise transparency.

What this indicator is—and isn’t

This is a visualization and context layer for RSI stack regimes with simple outcome statistics. It is not a complete trading system, not predictive, and not a signal generator on its own. Use it with market structure, risk controls, and position management that fit your process.

Metadata

- Pine version: v6

- Overlay: false (price overlays are drawn via forced overlay where applicable)

- Primary outputs: Four RSI lines, consensus line, OB/OS guides, background tint, entry markers, gradient bars and wicks, statistics table

- Inputs with defaults: See Parameter Guide

- Metrics and functions used: RSI, rolling sums, percent rank, dispersion across RSI set, gradient color mapping, table rendering, alerts

- Special techniques: Ordered RSI stacking with tolerance, optional midline gating, horizon-based outcome maturation, prior-stabilized win rate, gradient normalization with gamma shaping

- Performance and constraints: max bars back two thousand, rendering of shapes and table on last bar, no higher-timeframe data, no security calls

- Recommended use-cases: Regime confirmation, momentum alignment, post-entry management with dispersion and recent outcome context

- Compatibility: Works across assets and timeframes that support RSI

- Limitations and risks: Sensitive to parameter choices and market regime changes; not a standalone strategy

- Diagnostics: Statistics table, dispersion percent rank, gradient intensity

Disclaimer