Smart Money Concepts + Liquidity Voids [LuxAlgo]Liqudiy levels, smart mone concepts, and liquidity voids

Cari dalam skrip untuk "liquidity"

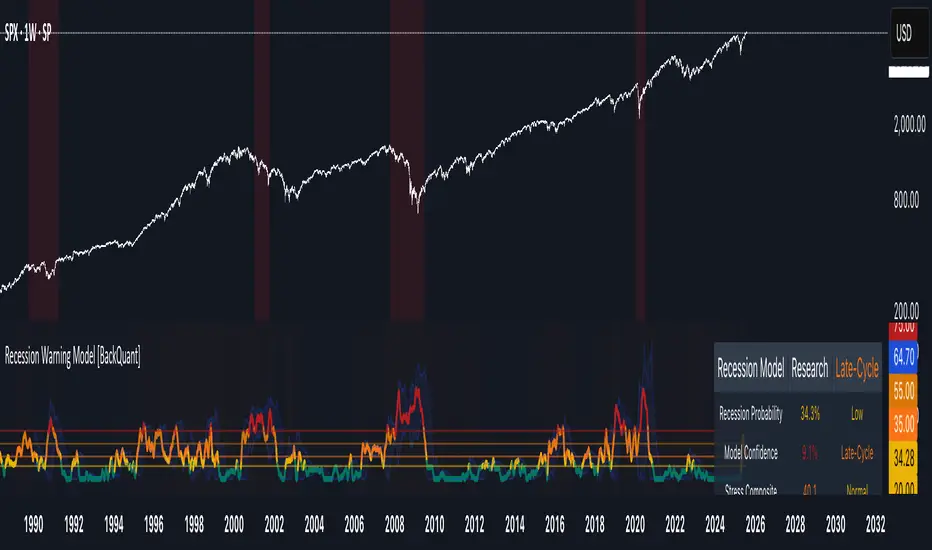

Recession Warning Model [BackQuant]Recession Warning Model

Overview

The Recession Warning Model (RWM) is a Pine Script® indicator designed to estimate the probability of an economic recession by integrating multiple macroeconomic, market sentiment, and labor market indicators. It combines over a dozen data series into a transparent, adaptive, and actionable tool for traders, portfolio managers, and researchers. The model provides customizable complexity levels, display modes, and data processing options to accommodate various analytical requirements while ensuring robustness through dynamic weighting and regime-aware adjustments.

Purpose

The RWM fulfills the need for a concise yet comprehensive tool to monitor recession risk. Unlike approaches relying on a single metric, such as yield-curve inversion, or extensive economic reports, it consolidates multiple data sources into a single probability output. The model identifies active indicators, their confidence levels, and the current economic regime, enabling users to anticipate downturns and adjust strategies accordingly.

Core Features

- Indicator Families : Incorporates 13 indicators across five categories: Yield, Labor, Sentiment, Production, and Financial Stress.

- Dynamic Weighting : Adjusts indicator weights based on recent predictive accuracy, constrained within user-defined boundaries.

- Leading and Coincident Split : Separates early-warning (leading) and confirmatory (coincident) signals, with adjustable weighting (default 60/40 mix).

- Economic Regime Sensitivity : Modulates output sensitivity based on market conditions (Expansion, Late-Cycle, Stress, Crisis), using a composite of VIX, yield-curve, financial conditions, and credit spreads.

- Display Options : Supports four modes—Probability (0-100%), Binary (four risk bins), Lead/Coincident, and Ensemble (blended probability).

- Confidence Intervals : Reflects model stability, widening during high volatility or conflicting signals.

- Alerts : Configurable thresholds (Watch, Caution, Warning, Alert) with persistence filters to minimize false signals.

- Data Export : Enables CSV output for probabilities, signals, and regimes, facilitating external analysis in Python or R.

Model Complexity Levels

Users can select from four tiers to balance simplicity and depth:

1. Essential : Focuses on three core indicators—yield-curve spread, jobless claims, and unemployment change—for minimalistic monitoring.

2. Standard : Expands to nine indicators, adding consumer confidence, PMI, VIX, S&P 500 trend, money supply vs. GDP, and the Sahm Rule.

3. Professional : Includes all 13 indicators, incorporating financial conditions, credit spreads, JOLTS vacancies, and wage growth.

4. Research : Unlocks all indicators plus experimental settings for advanced users.

Key Indicators

Below is a summary of the 13 indicators, their data sources, and economic significance:

- Yield-Curve Spread : Difference between 10-year and 3-month Treasury yields. Negative spreads signal banking sector stress.

- Jobless Claims : Four-week moving average of unemployment claims. Sustained increases indicate rising layoffs.

- Unemployment Change : Three-month change in unemployment rate. Sharp rises often precede recessions.

- Sahm Rule : Triggers when unemployment rises 0.5% above its 12-month low, a reliable recession indicator.

- Consumer Confidence : University of Michigan survey. Declines reflect household pessimism, impacting spending.

- PMI : Purchasing Managers’ Index. Values below 50 indicate manufacturing contraction.

- VIX : CBOE Volatility Index. Elevated levels suggest market anticipation of economic distress.

- S&P 500 Growth : Weekly moving average trend. Declines reduce wealth effects, curbing consumption.

- M2 + GDP Trend : Monitors money supply and real GDP. Simultaneous declines signal credit contraction.

- NFCI : Chicago Fed’s National Financial Conditions Index. Positive values indicate tighter conditions.

- Credit Spreads : Proxy for corporate bond spreads using 10-year vs. 2-year Treasury yields. Widening spreads reflect stress.

- JOLTS Vacancies : Job openings data. Significant drops precede hiring slowdowns.

- Wage Growth : Year-over-year change in average hourly earnings. Late-cycle spikes often signal economic overheating.

Data Processing

- Rate of Change (ROC) : Optionally applied to capture momentum in data series (default: 21-bar period).

- Z-Score Normalization : Standardizes indicators to a common scale (default: 252-bar lookback).

- Smoothing : Applies a short moving average to final signals (default: 5-bar period) to reduce noise.

- Binary Signals : Generated for each indicator (e.g., yield-curve inverted or PMI below 50) based on thresholds or Z-score deviations.

Probability Calculation

1. Each indicator’s binary signal is weighted according to user settings or dynamic performance.

2. Weights are normalized to sum to 100% across active indicators.

3. Leading and coincident signals are aggregated separately (if split mode is enabled) and combined using the specified mix.

4. The probability is adjusted by a regime multiplier, amplifying risk during Stress or Crisis regimes.

5. Optional smoothing ensures stable outputs.

Display and Visualization

- Probability Mode : Plots a continuous 0-100% recession probability with color gradients and confidence bands.

- Binary Mode : Categorizes risk into four levels (Minimal, Watch, Caution, Alert) for simplified dashboards.

- Lead/Coincident Mode : Displays leading and coincident probabilities separately to track signal divergence.

- Ensemble Mode : Averages traditional and split probabilities for a balanced view.

- Regime Background : Color-coded overlays (green for Expansion, orange for Late-Cycle, amber for Stress, red for Crisis).

- Analytics Table : Optional dashboard showing probability, confidence, regime, and top indicator statuses.

Practical Applications

- Asset Allocation : Adjust equity or bond exposures based on sustained probability increases.

- Risk Management : Hedge portfolios with VIX futures or options during regime shifts to Stress or Crisis.

- Sector Rotation : Shift toward defensive sectors when coincident signals rise above 50%.

- Trading Filters : Disable short-term strategies during high-risk regimes.

- Event Timing : Scale positions ahead of high-impact data releases when probability and VIX are elevated.

Configuration Guidelines

- Enable ROC and Z-score for consistent indicator comparison unless raw data is preferred.

- Use dynamic weighting with at least one economic cycle of data for optimal performance.

- Monitor stress composite scores above 80 alongside probabilities above 70 for critical risk signals.

- Adjust adaptation speed (default: 0.1) to 0.2 during Crisis regimes for faster indicator prioritization.

- Combine RWM with complementary tools (e.g., liquidity metrics) for intraday or short-term trading.

Limitations

- Macro indicators lag intraday market moves, making RWM better suited for strategic rather than tactical trading.

- Historical data availability may constrain dynamic weighting on shorter timeframes.

- Model accuracy depends on the quality and timeliness of economic data feeds.

Final Note

The Recession Warning Model provides a disciplined framework for monitoring economic downturn risks. By integrating diverse indicators with transparent weighting and regime-aware adjustments, it empowers users to make informed decisions in portfolio management, risk hedging, or macroeconomic research. Regular review of model outputs alongside market-specific tools ensures its effective application across varying market conditions.

Order Blocks v2Order Blocks v2 – Smart OB Detection with Time & FVG Filters

Order Blocks v2 is an advanced tool designed to identify potential institutional footprints in the market by dynamically plotting bullish and bearish order blocks.

This indicator refines classic OB logic by combining:

Fractal-based break conditions

Time-level filtering (Power of 3)

Optional Fair Value Gap (FVG) confirmation

Real-time plotting and auto-invalidation

Perfect for traders using ICT, Smart Money, or algorithmic timing models like Hopplipka.

🧠 What the indicator does

Detects order blocks after break of bullish/bearish fractals

Supports 3-bar or 5-bar fractal structures

Allows OB detection based on close breaks or high/low breaks

Optionally confirms OBs only if followed by a Fair Value Gap within N candles

Filters OBs based on specific time levels (3, 7, 11, 14) — core anchors in many algorithmic models

Automatically deletes invalidated OBs once price closes through the zone

⚙️ How it works

The indicator:

Tracks local fractal highs/lows

Once a fractal is broken by price, it backtracks to identify the best OB candle (highest bullish or lowest bearish)

Validates the level by checking:

OB type logic (close or HL break)

Time stamp match with algorithmic time anchors (e.g. 3, 7, 11, 14 – known from the Power of 3 concept)

Optional FVG confirmation after OB

Plots OB zones as lines (body or wick-based) and removes them if invalidated by a candle close

This ensures traders see only valid, active levels — removing noise from broken or out-of-context zones.

🔧 Customization

Choose 3-bar or 5-bar fractals

OB detection type: close break or HL break

Enable/disable OBs only on times 3, 7, 11, 14 (Hopplipka style)

Optional: require nearby FVG for validation

Line style: solid, dashed, or dotted

Adjust OB length, width, color, and use body or wick for OB height

🚀 How to use it

Add the script to your chart

Choose your preferred OB detection mode and filters

Use plotted OB zones to:

Anticipate price rejections and reversals

Validate Smart Money or ICT-based entry zones

Align setups with algorithmic time sequences (3, 7, 11, 14)

Filter out invalid OBs automatically, keeping your chart clean

The tool is useful on any timeframe but performs best when combined with a liquidity-based or time-anchored trading model.

💡 What makes it original

Combines fractal logic with OB confirmation and time anchors

Implements time-based filtering inspired by Hopplipka’s interpretation of the "Power of 3"

Allows OB validation via optional FVG follow-up — rarely available in public indicators

Auto-cleans invalidated OBs to reduce clutter

Designed to reflect market structure logic used by institutions and algorithms

💬 Why it’s worth using

Order Blocks v2 simplifies one of the most nuanced parts of SMC: identifying clean and high-probability OBs.

It removes subjectivity, adds clear timing logic, and integrates optional confluence tools — like FVG.

For traders serious about algorithmic-level structure and clean setups, this tool delivers both logic and clarity.

⚠️ Important

This indicator:

Is not a signal generator or financial advice tool

Is intended for experienced traders using OB/SMC/time-based logic

Does not predict market direction — it provides visual structural levels only

ryantrad3s session highs and lowsThis indicator allows you find London Session and Asia Session highs and lows without marking them yourself. This indicator can also help you find good draws on liquidity for the day and potential highs and lows you can target during that trading day. I recommend trading NQ and ES with this indicator because that's what I seen it work best with. The blue lines are London Session high and low and the red lines are Asia Session high and low. Hope this can save you time marking out your chart before market open.

Smarter Money Concepts - MTF IFVGs [PhenLabs]📊 Smarter Money Concepts - MTF IFVG

Version: PineScript™ v6

📌 Description

This multi-timeframe indicator identifies Inverse Fair Value Gaps (IFVGs) and their inversions across simultaneous chart intervals, helping traders spot liquidity voids and potential reversal zones. By analyzing price action through the lens of institutional order flow patterns, it solves the problem of manual gap tracking across timeframes while incorporating volatility-adjusted parameters and psychological level analysis for higher-probability setups.

🚀 Points of Innovation

• Multi-Timeframe Engine - Simultaneous analysis of 3 higher timeframes

• Adaptive Parameters - Auto-adjusts to market volatility conditions

• Quality Scoring System - Ranks gaps using RVI strength and size metrics

• Inversion Tracking - Monitors failed gaps for counter-trend signals

• Render Optimization - Prevents chart clutter with smart gap management

🔧 Core Components

FVG Detection Logic: Identifies gaps using customizable price source (Close/Wick)

Inversion Tracker: Manages failed gaps and generates counter signals

Multi-Timeframe Engine: Processes 3 independent higher timeframe analyses

Dashboard System: Real-time display of active gaps across all timeframes

🔥 Key Features

• Volatility-adjusted gap size filters (ATR-based)

• Customizable timeframe confluence analysis

• Color-coded quality scoring

• Non-repainting inversion signals

• Mobile-optimized visual rendering

🎨 Visualization

• Colored Boxes: Translucent zones show active gaps (green/bullish, red/bearish)

• Midline Plot: Dashed gray line marks gap midpoint for price targets

• Inversion Markers: Intense colors show failed gaps (dark red/bullish failure, bright green/bearish failure)

• HTF Differentiation: Higher timeframe gaps shown in blue/teal hues

📖 Usage Guidelines

Multi-Timeframe Settings

• Higher Timeframe 1

Default: 30 | Range: Any > Chart TF | Controls primary confluence timeframe

• Show All Timeframes

Default: True | Toggles multi-TF gap displays

Gap Settings

• Source

Default: Close | Options: | Determines gap measurement method

• RVI Period

Default: 14 | Range: 1-50 | Sets momentum confirmation sensitivity

• RVI Value

Default 0.1 | 0 to see all IFVGs | Increase min RVI to see the most powerful IFVGs

✅ Best Use Cases

• Identifying confluence across timeframes

• Spotting institutional order blocks

• High-probability reversal trading

• Trend continuation confirmation

• Volatility breakout setups

⚠️ Limitations

• Repaints historical gap zones

• Requires understanding of FVG concepts

• Higher timeframe data latency

• Quality scores rely on RVI/ATR settings

💡 What Makes This Unique

First FVG indicator with true multi-timeframe processing

Adaptive parameters that auto-adjust to volatility

Quantifiable quality scoring system

Professional-grade dashboard with HTF tracking

🔬 How It Works

Gap Detection: Identifies FVGs using price relationships and RVI confirmation

Inversion Tracking: Monitors price breaches to flag failed gaps

Quality Assessment: Scores gaps based on size, momentum, and location

Adaptive Filtering: Adjusts parameters using ATR-based volatility analysis

Multi-TF Synthesis: Correlates gaps across user-selected timeframes

Visual Rendering: Displays only relevant, active gaps to prevent clutter

💡 Note:

Start with default settings and gradually adjust parameters after observing market interactions. Focus on gaps with quality scores above 7 that align with higher timeframe trends. Combine with price action at psychological levels for highest-probability setups. Remember that higher timeframe gaps generally carry more significance than current chart gaps.

MACD Liquidity Tracker SystemMACD Liquidity Tracker System

🔹 Enhanced MACD with candle coloring, entry markers, and customizable signal logic.

🧠 Features:

This tool combines a color-coded MACD histogram with signal-based candle colors and small shape markers (🔼🔽) for clear market momentum and entry visualization.

📊 Visuals:

MACD Histogram (Sub-panel):

4 dynamic colors to show momentum direction:

🔹 Bright Blue = MACD > 0 & rising (strong bullish)

🔹 Dark Blue = MACD > 0 & falling (weakening bullish)

🔹 Bright Magenta = MACD < 0 & falling (strong bearish)

🔹 Dark Magenta = MACD < 0 & rising (weakening bearish)

Price Candles (Main Chart):

🔹 Bright Blue = Active Long signal

🔹 Bright Magenta = Active Short signal

Entry Markers:

🔼 Blue triangle (below candle) = Start of Long

🔽 Magenta triangle (above candle) = Start of Short

⚙️ System Types (select in settings):

Normal:

🔹 Long = MACD > 0

🔹 Short = MACD < 0

Fast: (Based on histogram color)

🔹 Long = Bright Blue OR Dark Magenta

🔹 Short = Dark Blue OR Bright Magenta

Safe:

🔹 Long = Only Bright Blue

🔹 Short = All other colors

🔔 Alerts:

Alerts trigger only on the first bar of a new Long/Short signal.

Easy to set up using TradingView’s alert system.

📌 How to Use:

Add the indicator to your chart

Open settings and select a System Type

Adjust MACD parameters if needed

Use histogram color + candle color for momentum and signal confirmation

Set alerts for clean entries if desired

💡 Ideal for traders seeking visual clarity and flexible MACD-based strategies.

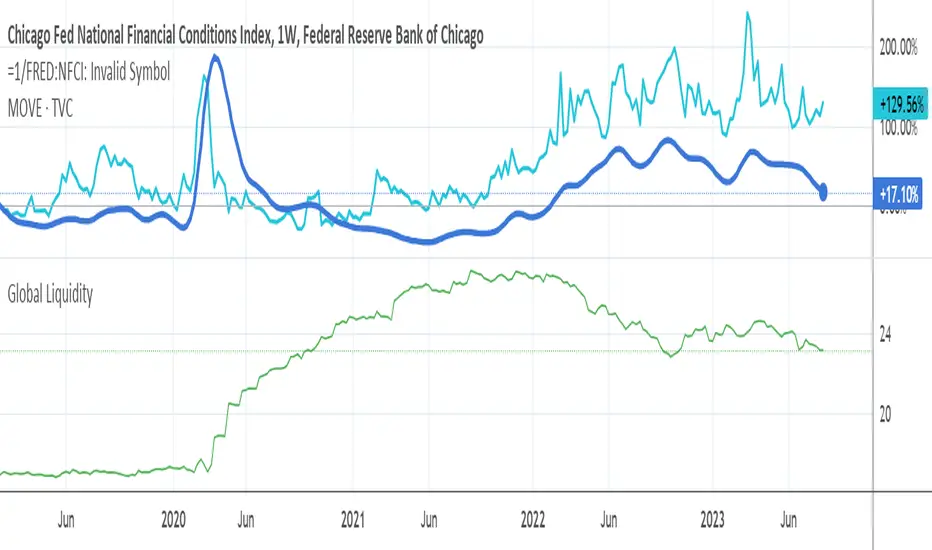

Global Liquidity Indicator in USDThis indicator aggregates the total central bank balance sheets and M2 money supply for the USA, Canada, China, European Union, Japan, and the UK, converting all values to USD and normalizing them to trillions for easy visualization. It plots three lines: Total Balance Sheet, Total M2, and Combined Total, providing a comprehensive view of global liquidity trends.

Key Features:

Dynamic Coloring: Customize line colors based on direction—green for upward trends, red for downward (or any colors you choose), with independent on/off toggles for each line.

Real-Time Currency Conversion: Uses live forex rates (e.g., USD/CNY, USD/EUR) for accurate USD conversions.

Bitcoin Liquidity Breakout with ICT StrategiesBitcoin Liquidity Breakout with ICT Strategies

a one of many scripts developed by our engineers .

Check the results for yourself

Pivot Liquidity Sweep + SignalsCore Functionalities:

Sweep Signals:

The indicator identifies sweeps of liquidity by detecting when price exceeds recent pivot highs (swing highs) or pivot lows (swing lows) and then reverses direction. It draws attention to these scenarios by labeling them on the chart.

For bullish sweep signals, the entry point is the closing price of the sweep candle, with the stop loss placed at the highest point between the sweep candle and the previous candle.

For bearish sweeps, the entry point is similarly identified, with the stop loss being the lowest price of the sweep candle and the candle before it. The profit target is dynamically set to the low or high of the closest valid pivot depending on the direction of the trade.

Rejection Signals:

Rejection signals are identified when price attempts to break a pivot high or low but fails, causing a rejection.

Bullish rejections involve price trying to break a pivot low but closing back above it, indicating potential for a bounce.

Bearish rejections follow a similar pattern, with price attempting to break a pivot high but failing to hold above it, signaling a potential bearish move.

High-Precision Intrabar Data:

The "Intrabar Precision" feature allows the indicator to use lower timeframe data to accurately plot sweeps and rejections, providing traders with precise entry and exit points.

The intrabar settings are particularly useful for traders looking for high-precision trades, such as scalpers who want to capture small yet consistent moves.

ATR and Percentage-Based Filters:

The indicator allows for customizable filters to ensure signals meet certain thresholds before being validated. Traders can use ATR (Average True Range) or percentage-based conditions to filter out low-quality signals, ensuring that the trades captured have enough volatility or price movement potential.

Dashboard:

The built-in dashboard provides a quick overview of trades executed using the indicator, displaying metrics such as the total number of sweep and rejection trades, their success rates, and total profit in points.

The dashboard is color-coded for easy reading and offers traders insights into the overall performance of their strategy, helping with ongoing evaluation and optimization.

Labeling and Alerts:

Every time a sweep or rejection signal is detected, the indicator automatically labels the chart to help traders quickly identify the trading opportunities.

Alerts are also generated for each trading signal, providing the trader with real-time notifications, which can be useful for those who are not constantly monitoring their charts.

Stop Loss and Target Adaptation:

The stop loss levels are adjusted dynamically based on the recent pivot points, and the target profit is derived from valid subsequent pivot levels to ensure realistic and efficient trade exits.

Custom Opening Price Levels (PO3)This indicator is designed to assist the trader in identifying the Power of Three through the opens of the candles.

-------------------------

The PO3 is a concept introduced by ICT. First, you need to have a directional bias for the month or the specific candle in question. It should be of high time frame (HTF BIAS).

At the open of the specific candle, the market will generate interest in the direction opposite to the HTF BIAS, accumulating positions. It will then manipulate the positions of less informed traders to generate the necessary liquidity to fill informed operators positions.

Finally, positions are distributed in favor of the bias.

-------------------------

The PO3 is a phenomenon that repeats across all timeframes. This indicator is highly customizable and allows the user to choose from a range of timeframes: 3 months, 1 month, 1 week, 1 day, and 3 hours. The indicator displays the last 3 opens for the selected period.

-------------------------

The script is open-source, so feel free to add more timeframes or open levels if you have coding skills.

Market Structure Volume Distribution [LuxAlgo]The Market Structure Volume Distribution tool allows traders to identify the strength behind breaks of market structure at defined price ranges to measure de correlation of forces between bulls and bears visually and easily.

🔶 USAGE

This tool has three main features: market structure highlighting, grid levels, and volume profile. Each feature is covered more in depth below:

🔹 Market Structure

The basic unit of market structure is a swing point, the period of the swing point is user-defined, so traders can identify longer-term market structures. Price breaking a prior swing point will confirm the occurrence of a market structure.

The tool will plot a line after a market structure is confirmed, by default the lines on bullish MS will be green (indicative of an uptrend), and red in case of bearish MS (indicative of a downtrend).

🔹 Grid Levels

The Grid visually divides the price range contained inside the tool execution window, into equal size rows, the number of rows is user-defined so users can divide the full price range up to 100 rows.

The main objective of this feature is to help identify the execution window and the limits of each row in the volume profile so traders can know in a simple look what BoMS belongs to each row.

There is however another use for the grid, by dividing the range into equal-sized parts, this feature provides automatic support and resistance levels as good as any other.

Grid provides a visual help to know what our execution window is and to associate MS with their rows in the profile. It can provide S/R levels too.

🔹 Volume Profile

The volume profile feature shows in a visually easy way the volume behind each MS aggregated by rows and divided into buy and sell volume to spot the differences in a simple look.

This tool allows users to spot the liquidity associated with the event of a market structure in a specific price range, allowing users to know which price areas where associated with the most trading activity during the occurrence of a market structutre.

🔶 SETTINGS

🔹 Data Gathering

Execute on all visible range: Activate this to use all visible bars on the calculations. This disables the use of the next parameter "Execute on the last N bars". Default false.

Execute on the last N bars: Use last N bars on the calculations. To use this parameter "Execute on all visible range" must be disabled. Values from 20 to 5000, default 500.

Pivot Length: How many bars will be used to confirm a pivot. The bigger this parameter is the fewer breaks of structure will detect. Values from 1, default 2

🔹 Profile

Profile Rows: Number of rows in the volume profile. Values from 2 to 100, default 10.

Profile Width: Maximum width of the volume profile. Values from 25 to 500, default 200.

Profile Mode: How the volume will be displayed on each row. "TOTAL VOLUME" will aggregate buy & sell volume per row, "BUY&SELL VOLUME" will separate the buy volume from the sell volume on each row. Default BUY&SELL VOLUME.

🔹 Style

Buy Color: This is the color for the buy volume on the profile when the "BUY&SELL VOLUME" mode is activated. Default green.

Sell Color: This is the color for the sell volume on the profile when the "BUY&SELL VOLUME" mode is activated. Default red.

Show dotted grid levels: Show dotted inner grid levels. Default true.

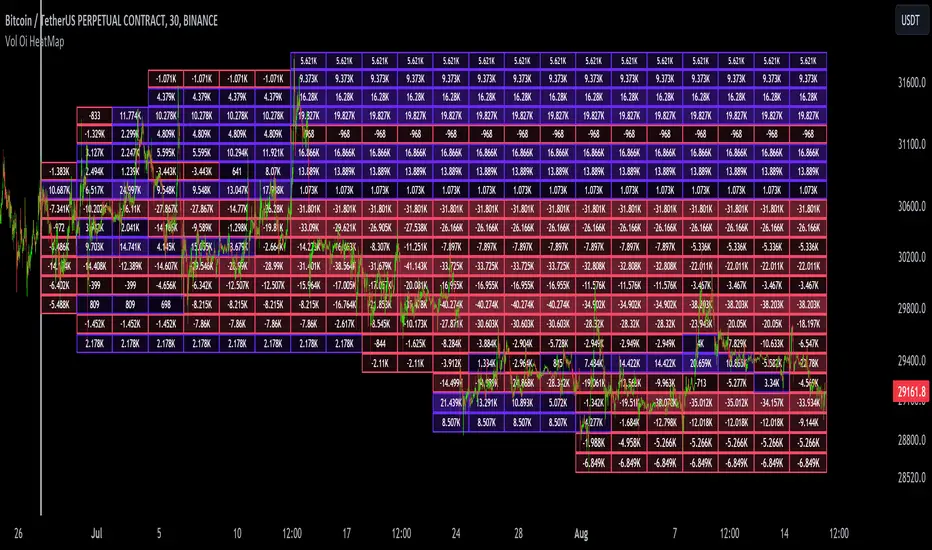

Dynamic Liquidity Map [Kioseff Trading]Hello!

Just a quick/fun project here: "Dynamic Heatmap".

This script draws a volume delta or open interest delta heatmap for the asset on your chart.

The adjective "Dynamic" is used for two reasons (:

1: Self-Adjusting Lower Timeframe Data

The script requests ~10 lower timeframe volume and open interest data sets.

When using the fixed range feature the script will, beginning at the start time, check the ~10 requested lower timeframes to see which of the lower timeframes has available data.

The script will always use the lowest timeframe available during the calculation period. As time continues, the script will continue to check if new lower timeframe data (lower than the currently used lowest timeframe) is available. This process repeats until bar time is close enough to the current time that 1-minute data can be retrieved.

The image above exemplifies the process.

Incrementally lower timeframe data will be used as it becomes available.

1: Fixed range capabilities

The script features a "fixed range" tool, where you can manually set a start time (or drag & drop a bar on the chart) to determine the interval the heatmap covers.

From the start date, the script will calculate the calculate the sub-intervals necessary to draw a rows x columns heatmap. Consequently, setting the start time further back will draw a heat map with larger rows x columns, whereas, a start time closer to the current bar time will draw a more "precise" heatmap with smaller rows x columns.

Additionally, the heatmap can be calculated using open interest data.

The image above shows the heatmap displaying open interest delta.

The image above shows alternative settings for the heatmap.

Delta values have been hidden alongside grid border colors. These settings can be replicated to achieve a more "traditional" feel for the heatmap.

Thanks for checking this out!

HTF Liquidity Dashboard [TFO]The purpose of this indicator is to server as a multi-symbol scanner that indicates when user-defined symbols have exceeded their previous Day/Week/Month highs and lows.

By default, the dashboard will use a compact view where the green ✔ means that price has swept and is currently exceeding the level of interest, the red ❌ implies that price swept the level but reversed back into the original range, and - indicates that the level hasn't been reached. However, the dashboard text can be toggled to show the numerical values of the highs and lows instead of these compact strings, as shown in the following image.

These levels may be shown and customized on the current chart as well via the Show Levels option. By default, levels from the selected timeframes will initially be plotted as black, and will change to red once traded through. Users can optionally increase the Session Limit parameter to show more than one previous high/low on their chart, for each selected timeframe.

Optionally, we can also plot labels to show when any of the user-defined symbols have exceeded their respective highs and lows, for any of the selected timeframes. Alerts can be created for these events as well; simply select the desired symbols and timeframes, create a new alert using this indicator, and you should be alerted when highs and lows are traded through. Note: if you encounter any issues with duplicate alerts, try deleting the alert, navigating to a lower timeframe such as the 1m, and making a new alert.

Nexus Blast Trading Strategy [Kaspricci]Nexus Blast Trading Strategy - Kaspricci

This indicator shows the different sessions during the day (London session, New York AM session, New York PM session and Asian session) by adding vertical lines and draws horizontal lines for the high and low during each session. Furthermore those lines turn red once the price has taken this high or low. Blue lines indicate liquidity not yet taken.

On top the indicator draws boxes of different color to indicate bullish and bearish Fair Value Gaps (FVG).

Happy to receive your feedback. Please leave a comment for bugs as well as ideas for improvement.

General Settings

Time Zone - used for marking sessions and end of day.

Sessions

Sessions - start and end time for each session based on set time zone

Number of Days back - for how many days in the past the startegy will draw strategy highs and lows. Theres is a maximum of 50 days defined.

FVG Settings

Threshold in Ticks - you can hide very small FVGs by increasing this threshold

FVG Colors - colors used for the bearish and bullish FVG box

This script is for educational purposes only! It is not meant to be a financial advice.

PS: The former strategy script was removed by TV, as it would violate several rules according to them.

Central Bank LiquidityCentral Bank Liquidity = Total value of the assets of all Federal Reserve Banks - Overnight Reverse Repurchase Agreements (RRP) - The Treasury General Account (TGA)

TradingView ticker arithmetic: FRED:WALCL-FRED:WTREGEN-FRED:RRPONTSYD

Market Structure and Liquidity IndicatorThis indicator tracks the market structure by identifying the highest high and lowest low. It then calculates the area of interest by taking the average of these levels. Additionally, it calculates liquidity by dividing the volume by the range between the highest high and lowest low.

Please note that this is a basic example, and you can modify and enhance it according to your specific requirements and trading strategy. Remember to thoroughly backtest and validate any trading strategy or indicator before using it in live trading.

Global LiquidityPlots the sum of the balance sheets of the world's major central banks - FED, ECB, BoE, PBoC, BOJ, India and Switzerland - in a currency of your choice. Defaults to USD.

Also shows FED net liquidity (balance sheet - tga - rrp) for comparison. Uses a configurable multiplier to make the two lines viewable on the same price scale.

Traders Reality Vector Candle ZonesVector Candle Zone indicator displays areas of unrecovered liquidity based on PVSRA with override option for the chart symbol.

Developed for TradersReality by infernixx with library conversion by peshocore

SPX and Federal Net Liquidity differenceScript for applying Federal Net Liquidity to the SPX post-2020 monetary policy. Original indicator from jlb05013 with adjustments to make it more readable and usable. When the indicator is above 250 the SPX is overbought and when it's below -250 the SPX is oversold.

It's not perfect, I'm just publishing because I didn't see it already out there.

ICT Index Futures Session LinesICT Index Futures Session Lines

Description:

The script is based on one of ICT's concepts on trading Index Futures. The script lays out the daily range from an intraday basis.

Range:

00:00 - New York Midnight

08:30 – New York Open (News events come out)

12:00/13:00 - New York Lunch (No trade time period)

13:30 - (Algorithm)

16:30 - Close

* The open, high and low lines are plotted from 00:00 to 08:30

How To Use:

You will need to check the daily bias. Prior to 8:30 you are to look for previous swing points where liquidity may exist. During the open you want to see if a high or low is taken out, and then wait for an energetic break/displacement for a potential FVG/imbalance retracement entry.

Strategy is for LTF (1 to 15m)

Default time zone is set to America/New_York (UTC New York), so lines will be plotted correctly regardless of user’s local UTC chart setting.

Ticker SummaryTicker Summary provides at-a-glance summary information about a ticker near the current bar on the chart:

P/E ratio

Fwd P/E ratio

PEG ratio

Floating shares vs. total shares outstanding

% of trading volume that was short over the last 3 days

Average True Range (ATR) over last 14 days

There are a few less common items of information:

How many ATR multiples the ATR is extended over the last 10 bars. This gives an idea of how far the stock is currently extended.

"R-frequency", explained below.

An optional "ATR Reticule" is shown near the price. This is useful for traders that use ATR as a guideline for price targets and stop losses. On the left is the # of ATRs the stock is currently above the session open. On the right is the # of ATRs the stock is extended above the 10-bar moving average.

R-frequency: a measure of liquidity relevant to your own trading size. It is the frequency at which 1-R of your trading account is traded for a stock. Formula:

(1-R worth of shares) / (average dollar value traded per second), where:

"1-R worth of shares" is how many shares you would buy for a stop loss of -1 ATR, with max risk dollar value based on the Balance and Max Risk % indicator options.

"Average dollar value traded per second" is the 14-day average of (avg(high, low and close) * daily volume)

R-frequency of a second or less is very liquid. If the value is higher (for example, over 60 seconds) the stock is less liquid and you may have some trouble filling limit orders quickly.

Volumetric colored candles with matching pivot point linesCandles are split into 10 categories based on their volume, and can be changed in the options. By default and in the images, white is very high volume, reds are high volume, yellows are medium volume, greens are low and dark-grey is very low.

Adjustments for scale are included in the options. The Magnitude option is a 10x multiplier, so 1=10, 2=100, 3=1000, etc., up to 9. There is also a Multiplier selection option where 1=1, 2=2, 3=3, 4=4, etc.

To attenuate for a given chart, these multipliers will need to be changed. In general, all white means you need to increase the Magnitude and all dark-grey means you need to decrease the magnitude. Somewhere between those two, the Multiplier can be used for further calibration. All this color coating is relational, like a spectrum. As you adjust you will see them maintaining their proportions as the candles switch color (ex. green become yellow while yellow becomes red).

I have also included pivot lines that follow the same logic for color coding. Two options exist for adjusting the pivot high and pivot low points respectively. They do not always correspond to the exact color of the candle producing them, but they should be a rough average (ie. red and green bars making yellow lines). They make for good indicators of how much liquidity may be at a certain support/resistance level. The lines can also be turned off altogether.

If your candles aren't looking right, go to settings of both regular candles and heikin-ashi, and uncheck both border and wick.

I still have some code to clean up and I plan on expanding upon this study. If you like my work consider tipping!