Liquidity Sweeps (Improved)this is improved version of liqudity sweep and alert thois is my third attempt

Cari dalam skrip untuk "liquidity"

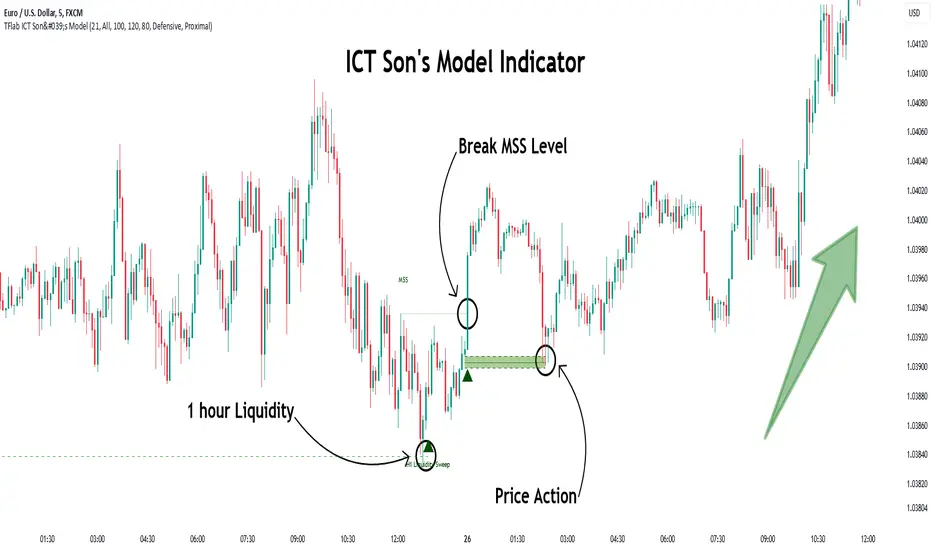

Multi-Timeframe Sweep IndicatorsLiquidity Sweeps: Identify when price sweeps stops above/below key levels

Breakout Confirmation: Confirm breakouts across multiple timeframes

Entry Timing: Use lower timeframe sweeps for precise entries

Risk Management: Higher timeframe sweeps may indicate stronger moves

The indicator works best when combined with other analysis techniques like support/resistance levels, volume analysis, and market structure.

Liquidity+FVG+OB Strategy (v6)How the strategy works (summary)

Entry Long when a Bullish FVG is detected (optionally requires a recent Bullish OB).

Entry Short when a Bearish FVG is detected (optionally requires a recent Bearish OB).

Stop Loss and Take Profit are placed using ATR multiples (configurable).

Position sizing is fixed contract/lot size (configurable).

You can require OB confirmation (within ob_confirm_window bars).

Alerts still exist and visuals are preserved.

Volume-Weighted Price MovementThe Volume-Weighted Price Movement (VWPM) indicator is an easy to read technical analysis tool that analyses how volume and price movement work together to drive market momentum.

How It Works

The VWPM indicator tracks two primary components:

Bullish Movement (green line): Measures the upward price movement weighted by volume. When price closes above the open, this component calculates how much buying pressure exists by multiplying the price change (close - open) by the volume of that period.

Bearish Movement (red line): Measures the downward price movement weighted by volume. When price closes below the open, this component calculates how much selling pressure exists by multiplying the price change (open - close) by the volume of that period.

Bull-Bear Difference (lime/orange line): Shows the net momentum by subtracting bearish movement from bullish movement, providing an at-a-glance view of which force is dominant.

The VWPM integrates volume data to identify whether price movements are backed by significant participation. A large price move with low volume carries less weight than the same move with high volume, providing a more accurate reflection of market strength.

A shorter lookback period makes the indicator more responsive to recent price action, while a longer period smooths out market noise for trend identification.

Interpretation

Bullish Signals

When the green line (bull movement) rises and stays above the red line

When the Bull-Bear Difference line crosses above zero and maintains positive momentum

Divergence between price making lower lows but the bull line making higher lows (hidden strength)

Bearish Signals

When the red line (bear movement) rises and stays above the green line

When the Bull-Bear Difference line crosses below zero and maintains negative momentum

Divergence between price making higher highs but the bull line making lower highs (hidden weakness)

open source, if anyone makes the script better please let me know :)

Liquidity Levels [LuxAlgo]The Peak Activity Levels indicator displays support and resistance levels from prices accompanied by significant volume. The indicator includes a histogram returning the frequency of closing prices falling between two parallel levels, each bin shows the number of bullish candles within the levels.

1. Settings

Length: Lookback for the detection of volume peaks.

Number Of Levels: Determines the number of levels to display.

Levels Color Mode: Determines how the levels should be colored. "Relative" will color the levels based on their location relative to the current price. "Random" will apply a random color to each level. "Fixed" will use a single color for each level.

Levels Style: Style of the displayed levels. Styles include solid, dashed, and dotted.

1.1 Histogram

Show Histogram: Determines whether to display the histogram or not.

Histogram Window: Lookback period of the histogram calculation.

Bins Colors: Control the color of the histogram bins.

2. Usage

The indicator can be used to display ready-to-use support and resistance. These are constructed from peaks in volume. When a peak occurs, we take the price where this peak occurred and use it as the value for our level.

If one of the levels was previously tested, we can hypothesize that the level might be used as support/resistance in the future. Additional analysis using volume can be done in order to confirm a potential bounce.

The histogram can return various information to the user. It can show if the price stayed within two levels for a long time and if the price within two levels was mostly made of bullish or bearish candles.

In the chart above, we can see that over the most recent 200 bars (determined by Histogram Window) 68 closing prices fall between levels A and B, with 27 bars being bullish.

Additionally, the width of a bin and its length can sometimes give information about the volatility of a specific price variation. If a bin is very wide but short (a low number of closing prices fallen within the levels) then we can conclude a most of the movement was done on a short amount of time.

Supertrend Advance Pullback StrategyHandbook for the Supertrend Advance Strategy

1. Introduction

Purpose of the Handbook:

The main purpose of this handbook is to serve as a comprehensive guide for traders and investors who are looking to explore and harness the potential of the Supertrend Advance Strategy. In the rapidly changing financial market, having the right tools and strategies at one's disposal is crucial. Whether you're a beginner hoping to dive into the world of trading or a seasoned investor aiming to optimize and diversify your portfolio, this handbook offers the insights and methodologies you need. By the end of this guide, readers should have a clear understanding of how the Supertrend Advance Strategy works, its benefits, potential pitfalls, and practical application in various trading scenarios.

Overview of the Supertrend Advance Pullback Strategy:

At its core, the Supertrend Advance Strategy is an evolution of the popular Supertrend Indicator. Designed to generate buy and sell signals in trending markets, the Supertrend Indicator has been a favorite tool for many traders around the world. The Advance Strategy, however, builds upon this foundation by introducing enhanced mechanisms, filters, and methodologies to increase precision and reduce false signals.

1. Basic Concept:

The Supertrend Advance Strategy relies on a combination of price action and volatility to determine the potential trend direction. By assessing the average true range (ATR) in conjunction with specific price points, this strategy aims to highlight the potential starting and ending points of market trends.

2. Methodology:

Unlike the traditional Supertrend Indicator, which primarily focuses on closing prices and ATR, the Advance Strategy integrates other critical market variables, such as volume, momentum oscillators, and perhaps even fundamental data, to validate its signals. This multidimensional approach ensures that the generated signals are more reliable and are less prone to market noise.

3. Benefits:

One of the main benefits of the Supertrend Advance Strategy is its ability to filter out false breakouts and minor price fluctuations, which can often lead to premature exits or entries in the market. By waiting for a confluence of factors to align, traders using this advanced strategy can increase their chances of entering or exiting trades at optimal points.

4. Practical Applications:

The Supertrend Advance Strategy can be applied across various timeframes, from intraday trading to swing trading and even long-term investment scenarios. Furthermore, its flexible nature allows it to be tailored to different asset classes, be it stocks, commodities, forex, or cryptocurrencies.

In the subsequent sections of this handbook, we will delve deeper into the intricacies of this strategy, offering step-by-step guidelines on its application, case studies, and tips for maximizing its efficacy in the volatile world of trading.

As you journey through this handbook, we encourage you to approach the Supertrend Advance Strategy with an open mind, testing and tweaking it as per your personal trading style and risk appetite. The ultimate goal is not just to provide you with a new tool but to empower you with a holistic strategy that can enhance your trading endeavors.

2. Getting Started

Navigating the financial markets can be a daunting task without the right tools. This section is dedicated to helping you set up the Supertrend Advance Strategy on one of the most popular charting platforms, TradingView. By following the steps below, you'll be able to integrate this strategy into your charts and start leveraging its insights in no time.

Setting up on TradingView:

TradingView is a web-based platform that offers a wide range of charting tools, social networking, and market data. Before you can apply the Supertrend Advance Strategy, you'll first need a TradingView account. If you haven't set one up yet, here's how:

1. Account Creation:

• Visit TradingView's official website.

• Click on the "Join for free" or "Sign up" button.

• Follow the registration process, providing the necessary details and setting up your login credentials.

2. Navigating the Dashboard:

• Once logged in, you'll be taken to your dashboard. Here, you'll see a variety of tools, including watchlists, alerts, and the main charting window.

• To begin charting, type in the name or ticker of the asset you're interested in the search bar at the top.

3. Configuring Chart Settings:

• Before integrating the Supertrend Advance Strategy, familiarize yourself with the chart settings. This can be accessed by clicking the 'gear' icon on the top right of the chart window.

• Adjust the chart type, time intervals, and other display settings to your preference.

Integrating the Strategy into a Chart:

Now that you're set up on TradingView, it's time to integrate the Supertrend Advance Strategy.

1. Accessing the Pine Script Editor:

• Located at the top-center of your screen, you'll find the "Pine Editor" tab. Click on it.

• This is where custom strategies and indicators are scripted or imported.

2. Loading the Supertrend Advance Strategy Script:

• Depending on whether you have the script or need to find it, there are two paths:

• If you have the script: Copy the Supertrend Advance Strategy script, and then paste it into the Pine Editor.

• If searching for the script: Click on the “Indicators” icon (looks like a flame) at the top of your screen, and then type “Supertrend Advance Strategy” in the search bar. If available, it will show up in the list. Simply click to add it to your chart.

3. Applying the Strategy:

• After pasting or selecting the Supertrend Advance Strategy in the Pine Editor, click on the “Add to Chart” button located at the top of the editor. This will overlay the strategy onto your main chart window.

4. Configuring Strategy Settings:

• Once the strategy is on your chart, you'll notice a small settings ('gear') icon next to its name in the top-left of the chart window. Click on this to access settings.

• Here, you can adjust various parameters of the Supertrend Advance Strategy to better fit your trading style or the specific asset you're analyzing.

5. Interpreting Signals:

• With the strategy applied, you'll now see buy/sell signals represented on your chart. Take time to familiarize yourself with how these look and behave over various timeframes and market conditions.

3. Strategy Overview

What is the Supertrend Advance Strategy?

The Supertrend Advance Strategy is a refined version of the classic Supertrend Indicator, which was developed to aid traders in spotting market trends. The strategy utilizes a combination of data points, including average true range (ATR) and price momentum, to generate buy and sell signals.

In essence, the Supertrend Advance Strategy can be visualized as a line that moves with the price. When the price is above the Supertrend line, it indicates an uptrend and suggests a potential buy position. Conversely, when the price is below the Supertrend line, it hints at a downtrend, suggesting a potential selling point.

Strategy Goals and Objectives:

1. Trend Identification: At the core of the Supertrend Advance Strategy is the goal to efficiently and consistently identify prevailing market trends. By recognizing these trends, traders can position themselves to capitalize on price movements in their favor.

2. Reducing Noise: Financial markets are often inundated with 'noise' - short-term price fluctuations that can mislead traders. The Supertrend Advance Strategy aims to filter out this noise, allowing for clearer decision-making.

3. Enhancing Risk Management: With clear buy and sell signals, traders can set more precise stop-loss and take-profit points. This leads to better risk management and potentially improved profitability.

4. Versatility: While primarily used for trend identification, the strategy can be integrated with other technical tools and indicators to create a comprehensive trading system.

Type of Assets/Markets to Apply the Strategy:

1. Equities: The Supertrend Advance Strategy is highly popular among stock traders. Its ability to capture long-term trends makes it particularly useful for those trading individual stocks or equity indices.

2. Forex: Given the 24-hour nature of the Forex market and its propensity for trends, the Supertrend Advance Strategy is a valuable tool for currency traders.

3. Commodities: Whether it's gold, oil, or agricultural products, commodities often move in extended trends. The strategy can help in identifying and capitalizing on these movements.

4. Cryptocurrencies: The volatile nature of cryptocurrencies means they can have pronounced trends. The Supertrend Advance Strategy can aid crypto traders in navigating these often tumultuous waters.

5. Futures & Options: Traders and investors in derivative markets can utilize the strategy to make more informed decisions about contract entries and exits.

It's important to note that while the Supertrend Advance Strategy can be applied across various assets and markets, its effectiveness might vary based on market conditions, timeframe, and the specific characteristics of the asset in question. As always, it's recommended to use the strategy in conjunction with other analytical tools and to backtest its effectiveness in specific scenarios before committing to trades.

4. Input Settings

Understanding and correctly configuring input settings is crucial for optimizing the Supertrend Advance Strategy for any specific market or asset. These settings, when tweaked correctly, can drastically impact the strategy's performance.

Grouping Inputs:

Before diving into individual input settings, it's important to group similar inputs. Grouping can simplify the user interface, making it easier to adjust settings related to a specific function or indicator.

Strategy Choice:

This input allows traders to select from various strategies that incorporate the Supertrend indicator. Options might include "Supertrend with RSI," "Supertrend with MACD," etc. By choosing a strategy, the associated input settings for that strategy become available.

Supertrend Settings:

1. Multiplier: Typically, a default value of 3 is used. This multiplier is used in the ATR calculation. Increasing it makes the Supertrend line further from prices, while decreasing it brings the line closer.

2. Period: The number of bars used in the ATR calculation. A common default is 7.

EMA Settings (Exponential Moving Average):

1. Period: Defines the number of previous bars used to calculate the EMA. Common periods are 9, 21, 50, and 200.

2. Source: Allows traders to choose which price (Open, Close, High, Low) to use in the EMA calculation.

RSI Settings (Relative Strength Index):

1. Length: Determines how many periods are used for RSI calculation. The standard setting is 14.

2. Overbought Level: The threshold at which the asset is considered overbought, typically set at 70.

3. Oversold Level: The threshold at which the asset is considered oversold, often at 30.

MACD Settings (Moving Average Convergence Divergence):

1. Short Period: The shorter EMA, usually set to 12.

2. Long Period: The longer EMA, commonly set to 26.

3. Signal Period: Defines the EMA of the MACD line, typically set at 9.

CCI Settings (Commodity Channel Index):

1. Period: The number of bars used in the CCI calculation, often set to 20.

2. Overbought Level: Typically set at +100, denoting overbought conditions.

3. Oversold Level: Usually set at -100, indicating oversold conditions.

SL/TP Settings (Stop Loss/Take Profit):

1. SL Multiplier: Defines the multiplier for the average true range (ATR) to set the stop loss.

2. TP Multiplier: Defines the multiplier for the average true range (ATR) to set the take profit.

Filtering Conditions:

This section allows traders to set conditions to filter out certain signals. For example, one might only want to take buy signals when the RSI is below 30, ensuring they buy during oversold conditions.

Trade Direction and Backtest Period:

1. Trade Direction: Allows traders to specify whether they want to take long trades, short trades, or both.

2. Backtest Period: Specifies the time range for backtesting the strategy. Traders can choose from options like 'Last 6 months,' 'Last 1 year,' etc.

It's essential to remember that while default settings are provided for many of these tools, optimal settings can vary based on the market, timeframe, and trading style. Always backtest new settings on historical data to gauge their potential efficacy.

5. Understanding Strategy Conditions

Developing an understanding of the conditions set within a trading strategy is essential for traders to maximize its potential. Here, we delve deep into the logic behind these conditions, using the Supertrend Advance Strategy as our focal point.

Basic Logic Behind Conditions:

Every strategy is built around a set of conditions that provide buy or sell signals. The conditions are based on mathematical or statistical methods and are rooted in the study of historical price data. The fundamental idea is to recognize patterns or behaviors that have been profitable in the past and might be profitable in the future.

Buy and Sell Conditions:

1. Buy Conditions: Usually formulated around bullish signals or indicators suggesting upward price momentum.

2. Sell Conditions: Centered on bearish signals or indicators indicating downward price momentum.

Simple Strategy:

The simple strategy could involve using just the Supertrend indicator. Here:

• Buy: When price closes above the Supertrend line.

• Sell: When price closes below the Supertrend line.

Pullback Strategy:

This strategy capitalizes on price retracements:

• Buy: When the price retraces to the Supertrend line after a bullish signal and is supported by another bullish indicator.

• Sell: When the price retraces to the Supertrend line after a bearish signal and is confirmed by another bearish indicator.

Indicators Used:

EMA (Exponential Moving Average):

• Logic: EMA gives more weight to recent prices, making it more responsive to current price movements. A shorter-period EMA crossing above a longer-period EMA can be a bullish sign, while the opposite is bearish.

RSI (Relative Strength Index):

• Logic: RSI measures the magnitude of recent price changes to analyze overbought or oversold conditions. Values above 70 are typically considered overbought, and values below 30 are considered oversold.

MACD (Moving Average Convergence Divergence):

• Logic: MACD assesses the relationship between two EMAs of a security’s price. The MACD line crossing above the signal line can be a bullish signal, while crossing below can be bearish.

CCI (Commodity Channel Index):

• Logic: CCI compares a security's average price change with its average price variation. A CCI value above +100 may mean the price is overbought, while below -100 might signify an oversold condition.

And others...

As the strategy expands or contracts, more indicators might be added or removed. The crucial point is to understand the core logic behind each, ensuring they align with the strategy's objectives.

Logic Behind Each Indicator:

1. EMA: Emphasizes recent price movements; provides dynamic support and resistance levels.

2. RSI: Indicates overbought and oversold conditions based on recent price changes.

3. MACD: Showcases momentum and direction of a trend by comparing two EMAs.

4. CCI: Measures the difference between a security's price change and its average price change.

Understanding strategy conditions is not just about knowing when to buy or sell but also about comprehending the underlying market dynamics that those conditions represent. As you familiarize yourself with each condition and indicator, you'll be better prepared to adapt and evolve with the ever-changing financial markets.

6. Trade Execution and Management

Trade execution and management are crucial aspects of any trading strategy. Efficient execution can significantly impact profitability, while effective management can preserve capital during adverse market conditions. In this section, we'll explore the nuances of position entry, exit strategies, and various Stop Loss (SL) and Take Profit (TP) methodologies within the Supertrend Advance Strategy.

Position Entry:

Effective trade entry revolves around:

1. Timing: Enter at a point where the risk-reward ratio is favorable. This often corresponds to confirmatory signals from multiple indicators.

2. Volume Analysis: Ensure there's adequate volume to support the movement. Volume can validate the strength of a signal.

3. Confirmation: Use multiple indicators or chart patterns to confirm the entry point. For instance, a buy signal from the Supertrend indicator can be confirmed with a bullish MACD crossover.

Position Exit Strategies:

A successful exit strategy will lock in profits and minimize losses. Here are some strategies:

1. Fixed Time Exit: Exiting after a predetermined period.

2. Percentage-based Profit Target: Exiting after a certain percentage gain.

3. Indicator-based Exit: Exiting when an indicator gives an opposing signal.

Percentage-based SL/TP:

• Stop Loss (SL): Set a fixed percentage below the entry price to limit potential losses.

• Example: A 2% SL on an entry at $100 would trigger a sell at $98.

• Take Profit (TP): Set a fixed percentage above the entry price to lock in gains.

• Example: A 5% TP on an entry at $100 would trigger a sell at $105.

Supertrend-based SL/TP:

• Stop Loss (SL): Position the SL at the Supertrend line. If the price breaches this line, it could indicate a trend reversal.

• Take Profit (TP): One could set the TP at a point where the Supertrend line flattens or turns, indicating a possible slowdown in momentum.

Swing high/low-based SL/TP:

• Stop Loss (SL): For a long position, set the SL just below the recent swing low. For a short position, set it just above the recent swing high.

• Take Profit (TP): For a long position, set the TP near a recent swing high or resistance. For a short position, near a swing low or support.

And other methods...

1. Trailing Stop Loss: This dynamic SL adjusts with the price movement, locking in profits as the trade moves in your favor.

2. Multiple Take Profits: Divide the position into segments and set multiple TP levels, securing profits in stages.

3. Opposite Signal Exit: Exit when another reliable indicator gives an opposite signal.

Trade execution and management are as much an art as they are a science. They require a blend of analytical skill, discipline, and intuition. Regularly reviewing and refining your strategies, especially in light of changing market conditions, is crucial to maintaining consistent trading performance.

7. Visual Representations

Visual tools are essential for traders, as they simplify complex data into an easily interpretable format. Properly analyzing and understanding the plots on a chart can provide actionable insights and a more intuitive grasp of market conditions. In this section, we’ll delve into various visual representations used in the Supertrend Advance Strategy and their significance.

Understanding Plots on the Chart:

Charts are the primary visual aids for traders. The arrangement of data points, lines, and colors on them tell a story about the market's past, present, and potential future moves.

1. Data Points: These represent individual price actions over a specific timeframe. For instance, a daily chart will have data points showing the opening, closing, high, and low prices for each day.

2. Colors: Used to indicate the nature of price movement. Commonly, green is used for bullish (upward) moves and red for bearish (downward) moves.

Trend Lines:

Trend lines are straight lines drawn on a chart that connect a series of price points. Their significance:

1. Uptrend Line: Drawn along the lows, representing support. A break below might indicate a trend reversal.

2. Downtrend Line: Drawn along the highs, indicating resistance. A break above might suggest the start of a bullish trend.

Filled Areas:

These represent a range between two values on a chart, usually shaded or colored. For instance:

1. Bollinger Bands: The area between the upper and lower band is filled, giving a visual representation of volatility.

2. Volume Profile: Can show a filled area representing the amount of trading activity at different price levels.

Stop Loss and Take Profit Lines:

These are horizontal lines representing pre-determined exit points for trades.

1. Stop Loss Line: Indicates the level at which a trade will be automatically closed to limit losses. Positioned according to the trader's risk tolerance.

2. Take Profit Line: Denotes the target level to lock in profits. Set according to potential resistance (for long trades) or support (for short trades) or other technical factors.

Trailing Stop Lines:

A trailing stop is a dynamic form of stop loss that moves with the price. On a chart:

1. For Long Trades: Starts below the entry price and moves up with the price but remains static if the price falls, ensuring profits are locked in.

2. For Short Trades: Starts above the entry price and moves down with the price but remains static if the price rises.

Visual representations offer traders a clear, organized view of market dynamics. Familiarity with these tools ensures that traders can quickly and accurately interpret chart data, leading to more informed decision-making. Always ensure that the visual aids used resonate with your trading style and strategy for the best results.

8. Backtesting

Backtesting is a fundamental process in strategy development, enabling traders to evaluate the efficacy of their strategy using historical data. It provides a snapshot of how the strategy would have performed in past market conditions, offering insights into its potential strengths and vulnerabilities. In this section, we'll explore the intricacies of setting up and analyzing backtest results and the caveats one must be aware of.

Setting Up Backtest Period:

1. Duration: Determine the timeframe for the backtest. It should be long enough to capture various market conditions (bullish, bearish, sideways). For instance, if you're testing a daily strategy, consider a period of several years.

2. Data Quality: Ensure the data source is reliable, offering high-resolution and clean data. This is vital to get accurate backtest results.

3. Segmentation: Instead of a continuous period, sometimes it's helpful to backtest over distinct market phases, like a particular bear or bull market, to see how the strategy holds up in different environments.

Analyzing Backtest Results:

1. Performance Metrics: Examine metrics like the total return, annualized return, maximum drawdown, Sharpe ratio, and others to gauge the strategy's efficiency.

2. Win Rate: It's the ratio of winning trades to total trades. A high win rate doesn't always signify a good strategy; it should be evaluated in conjunction with other metrics.

3. Risk/Reward: Understand the average profit versus the average loss per trade. A strategy might have a low win rate but still be profitable if the average gain far exceeds the average loss.

4. Drawdown Analysis: Review the periods of losses the strategy could incur and how long it takes, on average, to recover.

9. Tips and Best Practices

Successful trading requires more than just knowing how a strategy works. It necessitates an understanding of when to apply it, how to adjust it to varying market conditions, and the wisdom to recognize and avoid common pitfalls. This section offers insightful tips and best practices to enhance the application of the Supertrend Advance Strategy.

When to Use the Strategy:

1. Market Conditions: Ideally, employ the Supertrend Advance Strategy during trending market conditions. This strategy thrives when there are clear upward or downward trends. It might be less effective during consolidative or sideways markets.

2. News Events: Be cautious around significant news events, as they can cause extreme volatility. It might be wise to avoid trading immediately before and after high-impact news.

3. Liquidity: Ensure you are trading in assets/markets with sufficient liquidity. High liquidity ensures that the price movements are more reflective of genuine market sentiment and not due to thin volume.

Adjusting Settings for Different Markets/Timeframes:

1. Markets: Each market (stocks, forex, commodities) has its own characteristics. It's essential to adjust the strategy's parameters to align with the market's volatility and liquidity.

2. Timeframes: Shorter timeframes (like 1-minute or 5-minute charts) tend to have more noise. You might need to adjust the settings to filter out false signals. Conversely, for longer timeframes (like daily or weekly charts), you might need to be more responsive to genuine trend changes.

3. Customization: Regularly review and tweak the strategy's settings. Periodic adjustments can ensure the strategy remains optimized for the current market conditions.

10. Frequently Asked Questions (FAQs)

Given the complexities and nuances of the Supertrend Advance Strategy, it's only natural for traders, both new and seasoned, to have questions. This section addresses some of the most commonly asked questions regarding the strategy.

1. What exactly is the Supertrend Advance Strategy?

The Supertrend Advance Strategy is an evolved version of the traditional Supertrend indicator. It's designed to provide clearer buy and sell signals by incorporating additional indicators like EMA, RSI, MACD, CCI, etc. The strategy aims to capitalize on market trends while minimizing false signals.

2. Can I use the Supertrend Advance Strategy for all asset types?

Yes, the strategy can be applied to various asset types like stocks, forex, commodities, and cryptocurrencies. However, it's crucial to adjust the settings accordingly to suit the specific characteristics and volatility of each asset type.

3. Is this strategy suitable for day trading?

Absolutely! The Supertrend Advance Strategy can be adjusted to suit various timeframes, making it versatile for both day trading and long-term trading. Remember to fine-tune the settings to align with the timeframe you're trading on.

4. How do I deal with false signals?

No strategy is immune to false signals. However, by combining the Supertrend with other indicators and adhering to strict risk management protocols, you can minimize the impact of false signals. Always use stop-loss orders and consider filtering trades with additional confirmation signals.

5. Do I need any prior trading experience to use this strategy?

While the Supertrend Advance Strategy is designed to be user-friendly, having a foundational understanding of trading and market analysis can greatly enhance your ability to employ the strategy effectively. If you're a beginner, consider pairing the strategy with further education and practice on demo accounts.

6. How often should I review and adjust the strategy settings?

There's no one-size-fits-all answer. Some traders adjust settings weekly, while others might do it monthly. The key is to remain responsive to changing market conditions. Regular backtesting can give insights into potential required adjustments.

7. Can the Supertrend Advance Strategy be automated?

Yes, many traders use algorithmic trading platforms to automate their strategies, including the Supertrend Advance Strategy. However, always monitor automated systems regularly to ensure they're operating as intended.

8. Are there any markets or conditions where the strategy shouldn't be used?

The strategy might generate more false signals in markets that are consolidative or range-bound. During significant news events or times of unexpected high volatility, it's advisable to tread with caution or stay out of the market.

9. How important is backtesting with this strategy?

Backtesting is crucial as it allows traders to understand how the strategy would have performed in the past, offering insights into potential profitability and areas of improvement. Always backtest any new setting or tweak before applying it to live trades.

10. What if the strategy isn't working for me?

No strategy guarantees consistent profits. If it's not working for you, consider reviewing your settings, seeking expert advice, or complementing the Supertrend Advance Strategy with other analysis methods. Remember, continuous learning and adaptation are the keys to trading success.

Other comments

Value of combining several indicators in this script and how they work together

Diversification of Signals: Just as diversifying an investment portfolio can reduce risk, using multiple indicators can offer varied perspectives on potential price movements. Each indicator can capture a different facet of the market, ensuring that traders are not overly reliant on a single data point.

Confirmation & Reduced False Signals: A common challenge with many indicators is the potential for false signals. By requiring confirmation from multiple indicators before acting, the chances of acting on a false signal can be significantly reduced.

Flexibility Across Market Conditions: Different indicators might perform better under different market conditions. For example, while moving averages might excel in trending markets, oscillators like RSI might be more useful during sideways or range-bound conditions. A mashup strategy can potentially adapt better to varying market scenarios.

Comprehensive Analysis: With multiple indicators, traders can gauge trend strength, momentum, volatility, and potential market reversals all at once, providing a holistic view of the market.

How do the different indicators in the Supertrend Advance Strategy work together?

Supertrend: This is primarily a trend-following indicator. It provides traders with buy and sell signals based on the volatility of the price. When combined with other indicators, it can filter out noise and give more weight to strong, confirmed trends.

EMA (Exponential Moving Average): EMA gives more weight to recent price data. It can be used to identify the direction and strength of a trend. When the price is above the EMA, it's generally considered bullish, and vice versa.

RSI (Relative Strength Index): An oscillator that measures the magnitude of recent price changes to evaluate overbought or oversold conditions. By cross-referencing with other indicators like EMA or MACD, traders can spot potential reversals or confirmations of a trend.

MACD (Moving Average Convergence Divergence): This indicator identifies changes in the strength, direction, momentum, and duration of a trend in a stock's price. When the MACD line crosses above the signal line, it can be a bullish sign, and when it crosses below, it can be bearish. Pairing MACD with Supertrend can provide dual confirmation of a trend.

CCI (Commodity Channel Index): Initially developed for commodities, CCI can indicate overbought or oversold conditions. It can be used in conjunction with other indicators to determine entry and exit points.

In essence, the synergy of these indicators provides a balanced, comprehensive approach to trading. Each indicator offers its unique lens into market conditions, and when they align, it can be a powerful indication of a trading opportunity. This combination not only reduces the potential drawbacks of each individual indicator but leverages their strengths, aiming for more consistent and informed trading decisions.

Backtesting and Default Settings

• This indicator has been optimized to be applied for 1 hour-charts. However, the underlying principles of this strategy are supply and demand in the financial markets and the strategy can be applied to all timeframes. Daytraders can use the 1min- or 5min charts, swing-traders can use the daily charts.

• This strategy has been designed to identify the most promising, highest probability entries and trades for each stock or other financial security.

• The combination of the qualifiers results in a highly selective strategy which only considers the most promising swing-trading entries. As a result, you will normally only find a low number of trades for each stock or other financial security per year in case you apply this strategy for the daily charts. Shorter timeframes will result in a higher number of trades / year.

• Consequently, traders need to apply this strategy for a full watchlist rather than just one financial security.

• Default properties: RSI on (length 14, RSI buy level 50, sell level 50), EMA, RSI, MACD on, type of strategy pullback, SL/TP type: ATR (length 10, factor 3), trade direction both, quantity 5, take profit swing hl 5.1, highest / lowest lookback 2, enable ATR trail (ATR length 10, SL ATR multiplier 1.4, TP multiplier 2.1, lookback = 4, trade direction = both).

SOFR Spread (proxy: FEDFUNDS - US03MY)📊 SOFR Spread (Proxy: FEDFUNDS - US03MY) – Monitoring USD Money Market Liquidity

In 2008, the spread exhibits a sharp vertical spike, signaling a severe liquidity dislocation: investors rushed into short-term U.S. Treasuries, pushing their yields down dramatically, while the FEDFUNDS rate remained relatively high.

This behavior indicates extreme systemic stress in the interbank lending market, preceding massive Federal Reserve interventions such as rate cuts, emergency liquidity operations, and the launch of quantitative easing (QE).

Description:

This indicator plots the spread between the Effective Federal Funds Rate (FEDFUNDS) and the 3-Month US Treasury Bill yield (US03MY), used here as a proxy for the SOFR spread.

It serves as a simple yet powerful tool to detect liquidity dislocations and stress signals in the US short-term funding markets.

Interpretation:

🔴 Spread > 0.20% → Possible liquidity stress: elevated repo rates, cash shortage, interbank distrust.

🟡 Spread ≈ 0% → Normal market conditions, balanced liquidity.

🟢 Spread < 0% → Excess liquidity: strong demand for T-Bills, “flight to safety”, or distortion due to expansionary monetary policy.

Ideal for:

Monitoring Fed policy impact

Anticipating market-wide liquidity squeezes

Correlation with DXY, SPX, VIX, MOVE Index, and risk sentiment

🧠 Note: As SOFR is not directly available on TradingView, FEDFUNDS is used as a reliable proxy, closely tracking the same trends in most macro conditions.

Payday Anomaly StrategyThe "Payday Effect" refers to a predictable anomaly in financial markets where stock returns exhibit significant fluctuations around specific pay periods. Typically, these are associated with the beginning, middle, or end of the month when many investors receive wages and salaries. This influx of funds, often directed automatically into retirement accounts or investment portfolios (such as 401(k) plans in the United States), temporarily increases the demand for equities. This phenomenon has been linked to a cycle where stock prices rise disproportionately on and around payday periods due to increased buy-side liquidity.

Academic research on the payday effect suggests that this pattern is tied to systematic cash flows into financial markets, primarily driven by employee retirement and savings plans. The regularity of these cash infusions creates a calendar-based pattern that can be exploited in trading strategies. Studies show that returns on days around typical payroll dates tend to be above average, and this pattern remains observable across various time periods and regions.

The rationale behind the payday effect is rooted in the behavioral tendencies of investors, specifically the automatic reinvestment mechanisms used in retirement funds, which align with monthly or semi-monthly salary payments. This regular injection of funds can cause market microstructure effects where stock prices temporarily increase, only to stabilize or reverse after the funds have been invested. Consequently, the payday effect provides traders with a potentially profitable opportunity by predicting these inflows.

Scientific Bibliography on the Payday Effect

Ma, A., & Pratt, W. R. (2017). Payday Anomaly: The Market Impact of Semi-Monthly Pay Periods. Social Science Research Network (SSRN).

This study provides a comprehensive analysis of the payday effect, exploring how returns tend to peak around payroll periods due to semi-monthly cash flows. The paper discusses how systematic inflows impact returns, leading to predictable stock performance patterns on specific days of the month.

Lakonishok, J., & Smidt, S. (1988). Are Seasonal Anomalies Real? A Ninety-Year Perspective. The Review of Financial Studies, 1(4), 403-425.

This foundational study explores calendar anomalies, including the payday effect. By examining data over nearly a century, the authors establish a framework for understanding seasonal and monthly patterns in stock returns, which provides historical support for the payday effect.

Owen, S., & Rabinovitch, R. (1983). On the Predictability of Common Stock Returns: A Step Beyond the Random Walk Hypothesis. Journal of Business Finance & Accounting, 10(3), 379-396.

This paper investigates predictability in stock returns beyond random fluctuations. It considers payday effects among various calendar anomalies, arguing that certain dates yield predictable returns due to regular cash inflows.

Loughran, T., & Schultz, P. (2005). Liquidity: Urban versus Rural Firms. Journal of Financial Economics, 78(2), 341-374.

While primarily focused on liquidity, this study provides insight into how cash flows, such as those from semi-monthly paychecks, influence liquidity levels and consequently impact stock prices around predictable pay dates.

Ariel, R. A. (1990). High Stock Returns Before Holidays: Existence and Evidence on Possible Causes. The Journal of Finance, 45(5), 1611-1626.

Ariel’s work highlights stock return patterns tied to certain dates, including paydays. Although the study focuses on pre-holiday returns, it suggests broader implications of predictable investment timing, reinforcing the calendar-based effects seen with payday anomalies.

Summary

Research on the payday effect highlights a repeating pattern in stock market returns driven by scheduled payroll investments. This cyclical increase in stock demand aligns with behavioral finance insights and market microstructure theories, offering a valuable basis for trading strategies focused on the beginning, middle, and end of each month.

VWAP Flow ParmezanThe "Official Bank Flow VWAP" is a comprehensive trading suite designed for institutional Forex traders.

This indicator solves the problem of chart clutter by combining two critical components of liquidity: Price (Value) and Time (Sessions). It is specifically optimized for EUR/USD and GBP/USD on intraday timeframes (M5, M15), helping you identify high-probability setups where "Fair Value" meets "Volatility."

Key Features

1. Multi-Timeframe VWAP Hierarchy Unlike standard indicators, this tool visualizes the interaction between three distinct timeframes:

Daily VWAP (Dynamic Color): Your primary trend filter. Green when Bullish (Price > VWAP), Red when Bearish (Price < VWAP).

Weekly VWAP (Orange Dots): Represents the medium-term balance. Acts as a magnet for mean reversion mid-week.

Monthly VWAP (Purple Line): The institutional "line in the sand." Major support/resistance level.

2. Standard Deviation Bands (Market Balance) The indicator plots SD1 and SD2 bands around the Daily VWAP:

Inner Zone (SD1): Represents the "Fair Value" area.

Outer Bands (SD2): Represents overbought/oversold conditions. Useful for identifying mean reversion plays back to the center.

3. Official Exchange Sessions (Time) Forget confusing "killzones." This tool highlights the Official Open times for major exchanges, adjusted for Daylight Savings via New York time:

London Open (08:00 LDN): The start of European volume.

New York Open (08:00 NY): The injection of US liquidity.

London Close/Fix: The daily overlap close, often marking trend reversals.

Note: Sessions are visualized with non-intrusive black "shadow" backgrounds to keep your chart clean.

4. "Ghost" Levels (Previous VWAP) A unique feature that plots the closing VWAP level of the previous day. Institutional algorithms often target these "untested" levels as Take Profit targets or liquidity pools.

How to Use

Trend Following: If Price is above the Daily VWAP (Green) during the London Open, look for Long entries targeting the SD1/SD2 upper bands.

Mean Reversion: If Price hits the SD2 Band while far away from the Weekly VWAP, look for a reversal back to the mean.

Confluence: The strongest signals occur when price touches a key VWAP level (e.g., Weekly VWAP) specifically during the highlighted Session Start times.

Settings

Timezone: Defaults to America/New_York to automatically handle DST shifts for London/NY opens.

Visuals: Fully customizable colors and transparency. Default is set to a "Dark Mode" friendly professional palette.

Linear Trajectory & Volume StructureThe Linear Trajectory & Volume Structure indicator is a comprehensive trend-following system designed to identify market direction, volatility-adjusted channels, and high-probability entry points. Unlike standard Moving Averages, this tool utilizes Linear Regression logic to calculate the "best fit" trajectory of price, encased within volatility bands (ATR) to filter out market noise.

It integrates three core analytical components into a single interface:

Trend Engine: A Linear Regression Curve to determine the mean trajectory.

Volume Verification: Filters signals to ensure price movement is backed by market participation.

Market Structure: Identifies previous high-volume supply and demand zones for support and resistance analysis.

2. Core Components and Logic

The Trajectory Engine

The backbone of the system is a Linear Regression calculation. This statistical method fits a straight line through recent price data points to determine the current slope and direction.

The Baseline: Represents the "fair value" or mean trajectory of the asset.

The Cloud: Calculated using Average True Range (ATR). It expands during high volatility and contracts during consolidation.

Trend Definition:

Bullish: Price breaks above the Upper Deviation Band.

Bearish: Price breaks below the Lower Deviation Band.

Neutral/Chop: Price remains inside the cloud.

Smart Volume Filter

The indicator includes a toggleable volume filter. When enabled, the script calculates a Simple Moving Average (SMA) of the volume.

High Volume: Current volume is greater than the Volume SMA.

Signal Validation: Reversal signals and structure zones are only generated if High Volume is present, reducing the likelihood of trading false breakouts on low liquidity.

Volume Structure (Smart Liquidity)

The script automatically plots Support (Demand) and Resistance (Supply) boxes based on pivot points.

Creation: A box is drawn only if a pivot high or low is formed with High Volume (if the volume filter is active).

Mitigation: The boxes extend to the right. If price breaks through a zone, the box turns gray to indicate the level has been breached.

3. Signal Guide

Trend Reversals (Buy/Sell Labels)

These are the primary signals indicating a potential change in the macro trend.

BUY Signal: Appears when price closes above the upper volatility band after previously being in a downtrend.

SELL Signal: Appears when price closes below the lower volatility band after previously being in an uptrend.

Pullbacks (Small Circles)

These are continuation signals, useful for adding to positions or entering an existing trend.

Long Pullback: The trend is Bullish, but price dips momentarily below the baseline (into the "discount" area) and closes back above it.

Short Pullback: The trend is Bearish, but price rallies momentarily above the baseline (into the "premium" area) and closes back below it.

4. Configuration and Settings

Trend Engine Settings

Trajectory Length: The lookback period for the Linear Regression. This is the most critical setting for tuning sensitivity.

Channel Multiplier: Controls the width of the cloud.

1.0: Aggressive. Results in narrower bands and earlier signals, but more false positives.

1.5: Balanced (Default).

2.0+: Conservative. Creates a wide channel, filtering out significant noise but delaying entry signals.

Signal Logic

Show Trend Reversals: Toggles the main Buy/Sell labels.

Show Pullbacks: Toggles the re-entry circle signals.

Smart Volume Filter: If checked, signals require above-average volume. Unchecking this yields more signals but removes the volume confirmation requirement.

Volume Structure

Show Smart Liquidity: Toggles the Support/Resistance boxes.

Structure Lookback: Defines how many bars constitute a pivot. Higher numbers identify only major market structures.

Max Active Zones: Limits the number of boxes on the chart to prevent clutter.

5. Timeframe Optimization Guide

To maximize the effectiveness of the Linear Trajectory, you must adjust the Trajectory Length input based on your trading style and timeframe.

Scalping (1-Minute to 5-Minute Charts)

Recommended Length: 20 to 30

Multiplier: 1.2 to 1.5

Logic: Fast-moving markets require a shorter lookback to react quickly to micro-trend changes.

Day Trading (15-Minute to 1-Hour Charts)

Recommended Length: 55 (Default)

Multiplier: 1.5

Logic: A balance between responsiveness and noise filtering. The default setting of 55 is standard for identifying intraday sessions.

Swing Trading (4-Hour to Daily Charts)

Recommended Length: 89 to 100

Multiplier: 1.8 to 2.0

Logic: Swing trading requires filtering out intraday noise. A longer length ensures you stay in the trade during minor retracements.

6. Dashboard (HUD) Interpretation

The Head-Up Display (HUD) provides a summary of the current market state without needing to analyze the chart visually.

Bias: Displays the current trend direction (BULLISH or BEARISH).

Momentum:

ACCELERATING: Price is moving away from the baseline (strong trend).

WEAKENING: Price is compressing toward the baseline (potential consolidation or reversal).

Volume: Indicates if the current candle's volume is HIGH or LOW relative to the average.

Disclaimer

*Trading cryptocurrencies, stocks, forex, and other financial instruments involves a high level of risk and may not be suitable for all investors. This indicator is a technical analysis tool provided for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a guarantee of profit. Past performance of any trading system or methodology is not necessarily indicative of future results.

CANDLE RANGE THEORY (H1 Only)Hello traders.

This indicator identifies CRT candles

-Each candle is a range.

-Each candle has its own po3.

-Focus on specific times of the day. By recognizing the importance of time and price, we can capture high-quality trades. Together with HTF PD array, Look for 4-hour candles forming at specific times of the day. (1am - 5am - 9am EST)

-After the 1st candle, wait for the 2nd candle to clear the high/low of the 1st candle and then close inside the 1st candle range at a specific time (1-5-9) and look for entries in the LTF

Why choose 1 5 9 hours EST?

### **1. 1:00 AM (EST)**

- **Trading Session:** This is the time between the Tokyo (Asian) session and the Sydney (Australian) session. The Asian market is very active.

- **Characteristics:**

- Liquidity: Moderate, as only the Asian market is active.

- Volatility: Pairs involving JPY (Japanese Yen), AUD (Australian Dollar), and NZD (New Zealand Dollar) tend to have higher volatility.

- Trading Opportunities: Suitable for traders who like to trade trends or news in the Asian region.

- **Note:** Volatility may be lower than the London or New York session.

### **2. 5:00 AM (EST)**

- **Trading Session:** This is the time near the end of the Tokyo session and the London (European) session is about to open.

- **Characteristics:**

- Liquidity: Starts to increase due to the preparation of the European market.

- Volatility: This is the time between two trading sessions, there can be strong fluctuations, especially in major currency pairs such as EUR/USD, GBP/USD.

- Trading opportunities: Suitable for breakout trading strategies when liquidity increases.

- **Note:** The overlap between Tokyo and London can cause sudden fluctuations.

### **3. 9:00 AM (EST)**

- **Trading sessions:** This time is within the London session and near the beginning of the New York session.

- **Characteristics:**

- Liquidity: Very high, as this is the period between the two largest sessions – London and New York.

- Volatility: Extremely strong, especially for major currency pairs such as EUR/USD, GBP/USD, USD/JPY.

- Trading opportunities: Suitable for both news trading and trend trading, as this is the time when a lot of economic data is released (usually from the US or the European region).

- **Note:** High volatility can bring big profits, but also comes with high risks.

### **Summary of effects:**

- **1 AM (EST):** Moderate volatility, focusing on Asian currency pairs.

- **5 AM (EST):** Increased liquidity and volatility, suitable for breakout trading.

- **9 AM (EST):** High volatility and high liquidity, the best time for Forex trading.

==> How to trade, when the high/low of CRT is swept, move to LTF to wait for confirmation to enter the order

Only sell at high level and buy at discount price.

Find CE at specific important time. Trading CRT with HTF direction has better win rate.

The more inside bars, the higher the probability.

Place a partial and Move breakeven at 50% range.

Do a backtest and post your chart.

Fair Value Gap [by Oberlunar]Fair Value Gap

This indicator is designed to identify and display Fair Value Gaps (FVG) on the price chart. Fair Value Gaps are areas between candles where the price lacks continuity, leaving a "gap" that can serve as a reference point for price retracements. These zones are often considered important by traders as they represent market imbalances that tend to be "mitigated" (i.e., filled or tested) over time.

Purpose of Publication

This indicator addresses a common gap in FVG indicators. Most existing FVG indicators do not visually distinguish between mitigated (touched) FVGs and those that remain intact. With this indicator:

Mitigated FVGs are clearly displayed with distinct colors, allowing traders to identify which zones have been partially or fully filled by the price.

Unmitigated FVGs remain prominent, representing potential points of interest.

Key Features

Identification of Fair Value Gaps:

A Bullish FVG (upward gap) forms when the high of the three previous candles (candle -3) is lower than the low of the next candle (candle -1).

A Bearish FVG (downward gap) forms when the low of the three previous candles (candle -3) is higher than the high of the next candle (candle -1).

Dynamic Coloring:

Unmitigated FVGs are highlighted with specific colors: green for Bullish and red for Bearish gaps.

When an FVG is "touched" by the price (i.e., mitigated), the color changes:

Yellow-green for mitigated Bullish FVGs.

Purple for mitigated Bearish FVGs.

Handling Mitigated FVGs:

When an FVG is touched by the price, it is visually updated with a different color.

An option can be enabled to "shrink" the mitigated zone, adjusting the box to reflect the remaining untested portion of the gap.

Customization:

Configure the maximum number of FVGs to display on the chart.

Set specific colors for mitigated and unmitigated FVGs.

Choose whether to automatically shrink mitigated zones.

How to Identify Support and Resistance Levels

Support:

Bullish FVGs represent potential support levels, as they indicate areas where the price might return to seek liquidity or fill the imbalance.

An FVG that is repeatedly touched without being fully filled becomes a significant support zone.

Resistance:

Bearish FVGs represent potential resistance levels, indicating zones where the price might stall or reverse direction.

Why a Repeatedly Mitigated FVG is Significant

When an FVG is touched or mitigated multiple times, it means the market recognizes that area as significant. This can happen for several reasons:

Accumulation or Distribution: Institutional traders may use these zones to accumulate or distribute positions without causing excessive market movement.

Presence of Liquidity: FVGs often represent areas with pending orders (stop-losses, limit orders), and the price revisits these zones to seek liquidity.

Market Equilibrium: When an FVG is repeatedly filled, it indicates the market's attempt to balance a demand-supply imbalance. This makes the zone an important level to monitor for potential breakouts or reversals.

Smart Money Concepts by WeloTradesThe "Smart Money Concepts by WeloTrades" indicator is designed to offer traders a comprehensive tool that integrates multiple advanced features to aid in market analysis. By combining order blocks, liquidity levels, fair value gaps, trendlines, and market structure analysis, the indicator provides a holistic approach to understanding market dynamics and making informed trading decisions.

Components and Their Integration:

Order Blocks and Breaker Blocks Detection

Functionality: Order blocks represent areas where significant buying or selling occurred, creating potential support or resistance zones. Breaker blocks signal potential reversals.

Integration: By detecting and visualizing these blocks, the indicator helps traders identify key levels where price might react, aiding in entry and exit decisions. The customizable settings allow traders to adjust the visibility and parameters to suit their specific trading strategy.

Liquidity Levels Analysis

Functionality: Liquidity levels indicate zones where significant price movements can occur due to the presence of large orders. These are areas where smart money might be executing trades.

Integration: By tracking these high-probability liquidity areas, traders can anticipate potential price movements. Customizable display limits and mitigation strategies ensure that the information is tailored to the trader’s needs, providing precise and actionable insights.

Fair Value Gaps (FVG)

Functionality: Fair value gaps highlight areas where there is an imbalance between buyers and sellers. These gaps often represent potential trading opportunities.

Integration: The ability to identify and analyze FVGs helps traders spot potential entries based on market inefficiencies. The touch and break detection functionalities provide further refinement, enhancing the precision of trading signals.

Trendlines

Functionality: Trendlines help in identifying the direction of the market and potential reversal points. The additional trendline adds a layer of confirmation for breaks or retests.

Integration: Automatically drawn trendlines assist traders in visualizing market trends and making decisions about potential entries and exits. The additional trendline for stronger confirmation reduces the risk of false signals, providing more reliable trading opportunities.

Market Structure Analysis

Functionality: Understanding market structure is crucial for identifying key support and resistance levels and overall market dynamics. This component displays internal, external, and composite market structures.

Integration: By automatically highlighting shifts in market structure, the indicator helps traders recognize important levels and potential changes in market direction. This analysis is critical for strategic planning and execution in trading.

Customizable Alerts

Functionality: Alerts ensure that traders do not miss significant market events, such as the formation or breach of order blocks, liquidity levels, and trendline interactions.

Integration: Customizable alerts enhance the user experience by providing timely notifications of key events. This feature ensures that traders can act quickly and efficiently, leveraging the insights provided by the indicator.

Interactive Visualization

Functionality: Customizable visual aspects of the indicator allow traders to tailor the display to their preferences and trading style.

Integration: This feature enhances user engagement and usability, making it easier for traders to interpret the data and make informed decisions. Personalization options like colors, styles, and display formats improve the overall effectiveness of the indicator.

How Components Work Together

Comprehensive Market Analysis

Each component of the indicator addresses a different aspect of market analysis. Order blocks and liquidity levels highlight potential support and resistance zones, while fair value gaps and trendlines provide additional context for potential entries and exits. Market structure analysis ties everything together by offering a broad view of market dynamics.

Synergistic Insights

The integration of multiple features allows for cross-validation of trading signals. For instance, an order block coinciding with a high-probability liquidity level and a fair value gap can provide a stronger signal than any of these features alone. This synergy enhances the reliability of the insights and trading signals generated by the indicator.

Enhanced Decision Making

By combining these advanced features into a single tool, traders are equipped with a powerful resource for making informed decisions. The customizable alerts and interactive visualization further support this by ensuring that traders can act quickly on the insights provided.

Order Blocks ( OB) & Breaker Blocks (BB) Visuals:

📝 OB Input Settings

📊 Timeframe #1

TF #1🕑: Enable or disable Timeframe 1.

What it is: A boolean input to toggle the use of the first timeframe.

What it does: Enables or disables Timeframe 1 for the OB settings.

How to use it: Check or uncheck the box to enable or disable.

📊 Timeframe 1 Selection

Timeframe #1🕑: Select the timeframe for Timeframe 1.

What it is: A dropdown to select the desired timeframe.

What it does: Sets the timeframe for Timeframe 1.

How to use it: Choose a timeframe from the dropdown list.

📊 Timeframe #2

TF #2🕑: Enable or disable Timeframe 2.

What it is: A boolean input to toggle the use of the second timeframe.

What it does: Enables or disables Timeframe 2 for the OB settings.

How to use it: Check or uncheck the box to enable or disable.

📊 Timeframe 2 Selection

Timeframe #2🕑: Select the timeframe for Timeframe 2.

What it is: A dropdown to select the desired timeframe.

What it does: Sets the timeframe for Timeframe 2.

How to use it: Choose a timeframe from the dropdown list.

Additional Info: Higher TF Chart & Lower TF Setting / Lower TF Chart & Higher TF Setting.

📏 Show OBs

OB (Length)📏: Toggle the display of Order Blocks.

What it is: A boolean input to enable or disable the display of Order Blocks.

What it does: Shows or hides Order Blocks based on the selected swing length.

How to use it: Check or uncheck the box to enable or disable.

📏 Swing Length Option

Swing Length Option: Select the swing length option.

What it is: A dropdown to choose between SHORT, MID, LONG, or CUSTOM.

What it does: Sets the length of swings for Order Blocks.

How to use it: Choose an option from the dropdown.

Additional Info: Default lengths are SHORT=10, MID=28, LONG=50.

🔧 Custom Swing Length

🔧custom: Specify a custom swing length.

What it is: An integer input for setting a custom swing length.

What it does: Overrides the default swing lengths if set to CUSTOM.

How to use it: Enter a custom integer value (only shown when CUSTOM is selected).

📛 Show BBs

BB (Method)📛: Toggle the display of Breaker Blocks.

What it is: A boolean input to enable or disable the display of Breaker Blocks.

What it does: Shows or hides Breaker Blocks.

How to use it: Check or uncheck the box to enable or disable.

📛 OB End Method

OB End Method: Select the method for determining the end of a Breaker Block.

What it is: A dropdown to choose between Wick and Close.

What it does: Sets the criteria for when a Breaker Block is considered mitigated.

How to use it: Choose an option from the dropdown.

Additional Info: Wicks: OB is mitigated when the price wicks through the OB Level. Close: OB is mitigated when the closing price is within the OB Level.

🔍 Max Bullish Zones

🔍Max Bullish: Set the maximum number of Bullish Order Blocks to display.

What it is: A dropdown to select the maximum number of Bullish Order Blocks.

What it does: Limits the number of Bullish Order Blocks shown on the chart.

How to use it: Choose a value from the dropdown (1-10).

🔍 Max Bearish Zones

🔍Max Bearish: Set the maximum number of Bearish Order Blocks to display.

What it is: A dropdown to select the maximum number of Bearish Order Blocks.

What it does: Limits the number of Bearish Order Blocks shown on the chart.

How to use it: Choose a value from the dropdown (1-10).

🟩 Bullish OB Color

Bullish OB Color: Set the color for Bullish Order Blocks.

What it is: A color picker to set the color of Bullish Order Blocks.

What it does: Changes the color of Bullish Order Blocks on the chart.

How to use it: Select a color from the color picker.

🟥 Bearish OB Color

Bearish OB Color: Set the color for Bearish Order Blocks.

What it is: A color picker to set the color of Bearish Order Blocks.

What it does: Changes the color of Bearish Order Blocks on the chart.

How to use it: Select a color from the color picker.

🔧 OB & BB Range

↔ OB & BB Range: Select the range option for OB and BB.

What it is: A dropdown to choose between RANGE and CUSTOM.

What it does: Sets how far the OB or BB should extend.

How to use it: Choose an option from the dropdown.

Additional Info: RANGE = Current price, CUSTOM = Adjustable Range.

🔧 Custom OB & BB Range

🔧Custom: Specify a custom range for OB and BB.

What it is: An integer input for setting a custom range.

What it does: Defines how far the OB or BB should go, based on a custom value.

How to use it: Enter a custom integer value (range: 1000-500000).

💬 Text Options

💬Text Options: Set text size and color for OB and BB.

What it is: A dropdown to select text size and a color picker to choose text color.

What it does: Changes the size and color of the text displayed for OB and BB.

How to use it: Select a size from the dropdown and a color from the color picker.

💬 Show Timeframe OB

Text: Toggle to display the timeframe of OB.

What it is: A boolean input to show or hide the timeframe text for OB.

What it does: Displays the timeframe information for Order Blocks on the chart.

How to use it: Check or uncheck the box to enable or disable.

💬 Show Volume

Volume: Toggle to display the volume of OB.

What it is: A boolean input to show or hide the volume information for Order Blocks.

What it does: Displays the volume information for Order Blocks on the chart.

How to use it: Check or uncheck the box to enable or disable.

Additional Info:

What it represents: The volume displayed represents the total trading volume that occurred during the formation of the Order Block. This can indicate the level of participation or interest in that price level.

How it's calculated: The volume is the sum of all traded volumes within the candles that form the Order Block.

What it means: Higher volume at an Order Block level may suggest stronger support or resistance. It shows the amount of trading activity and can be an indicator of the potential strength or validity of the Order Block.

Why it's shown: To give traders an idea of the market participation and to help assess the strength of the Order Block.

💬 Show Percentage

%: Toggle to display the percentage of OB.

What it is: A boolean input to show or hide the percentage information for Order Blocks.

What it does: Displays the percentage information for Order Blocks on the chart.

How to use it: Check or uncheck the box to enable or disable.

Additional Info:

What it represents: The percentage displayed usually represents the proportion of price movement relative to the Order Block.

How it's calculated: This can be the percentage move from the start to the end of the Order Block or the retracement level that price has reached relative to the Order Block's range.

What it means: It helps traders understand the extent of price movement within the Order Block and can indicate the significance of the price level.

Why it's shown: To provide a clearer understanding of the price dynamics and the importance of the Order Block within the overall price movement.

Additional Information

Volume Example: If an Order Block forms over three candles with volumes of 100, 150, and 200, the total volume displayed for that Order Block would be 450.

Percentage Example: If the price moves from 100 to 110 within an Order Block, and the total range of the Order Block is from 100 to 120, the percentage shown might be 50% (since the price has moved halfway through the Order Block's range).

Liquidity Levels visuals:

📊 Liquidity Levels Input Settings

📊 Current Timeframe

TF #1🕑: Enable or disable the current timeframe.

What it is: A boolean input to toggle the use of the current timeframe.

What it does: Enables or disables the display of liquidity levels for the current timeframe.

How to use it: Check or uncheck the box to enable or disable.

📊 Higher Timeframe

Higher Timeframe: Select the higher timeframe for liquidity levels.

What it is: A dropdown to select the desired higher timeframe.

What it does: Sets the higher timeframe for liquidity levels.

How to use it: Choose a timeframe from the dropdown list.

📏 Liquidity Length Option

📏Liquidity Length: Select the length for liquidity levels.

What it is: A dropdown to choose between SHORT, MID, LONG, or CUSTOM.

What it does: Sets the length of swings for liquidity levels.

How to use it: Choose an option from the dropdown.

Additional Info: Default lengths are SHORT=10, MID=28, LONG=50.

🔧 Custom Liquidity Length

🔧custom: Specify a custom length for liquidity levels.

What it is: An integer input for setting a custom swing length.

What it does: Overrides the default liquidity lengths if set to CUSTOM.

How to use it: Enter a custom integer value (only shown when CUSTOM is selected).

📛 Mitigation Method

📛Mitigation (Method): Select the method for determining the mitigation of liquidity levels.

What it is: A dropdown to choose between Close and Wick.

What it does: Sets the criteria for when a liquidity level is considered mitigated.

How to use it: Choose an option from the dropdown.

Additional Info:

Wick: Level is mitigated when the price wicks through the level.

Close: Level is mitigated when the closing price is within the level.

📛 Display Mitigated Levels

-: Select to display or hide mitigated levels.

What it is: A dropdown to choose between Remove and Show.

What it does: Displays or hides mitigated liquidity levels.

How to use it: Choose an option from the dropdown.

Additional Info:

Remove: Hide mitigated levels.

Show: Display mitigated levels.

🔍 Max Buy Side Liquidity

🔍Max Buy Side Liquidity: Set the maximum number of Buy Side Liquidity Levels to display.

What it is: An integer input to set the maximum number of Buy Side Liquidity Levels.

What it does: Limits the number of Buy Side Liquidity Levels shown on the chart.

How to use it: Enter a value between 0 and 50.

🟦 Buy Side Liquidity Color

Buy Side Liquidity Color: Set the color for Buy Side Liquidity Levels.

What it is: A color picker to set the color of Buy Side Liquidity Levels.

What it does: Changes the color of Buy Side Liquidity Levels on the chart.

How to use it: Select a color from the color picker.

Additional Info:

Tooltip: Set the maximum number of Buy Side Liquidity Levels to display. Default: 5, Min: 1, Max: 50.

If liquidity levels are not displayed as expected, try increasing the max count.

🔍 Max Sell Side Liquidity

🔍Max Sell Side Liquidity: Set the maximum number of Sell Side Liquidity Levels to display.

What it is: An integer input to set the maximum number of Sell Side Liquidity Levels.

What it does: Limits the number of Sell Side Liquidity Levels shown on the chart.

How to use it: Enter a value between 0 and 50.

🟥 Sell Side Liquidity Color

Sell Side Liquidity Color: Set the color for Sell Side Liquidity Levels.

What it is: A color picker to set the color of Sell Side Liquidity Levels.

What it does: Changes the color of Sell Side Liquidity Levels on the chart.

How to use it: Select a color from the color picker.

Additional Info:

Tooltip: Set the maximum number of Sell Side Liquidity Levels to display. Default: 5, Min: 1, Max: 50.

If liquidity levels are not displayed as expected, try increasing the max count.

✂ Box Style (Height)

✂ Box Style (↕): Set the box height style for liquidity levels.

What it is: A float input to set the height of the boxes.

What it does: Adjusts the height of the boxes displaying liquidity levels.

How to use it: Enter a value between -50 and 50.

Additional Info: Default value is -5.

📏 Box Length

b: Set the box length of liquidity levels.

What it is: An integer input to set the length of the boxes.

What it does: Adjusts the length of the boxes displaying liquidity levels.

How to use it: Enter a value between 0 and 500.

Additional Info: Default value is 20.

⏭ Extend Liquidity Levels

Extend ⏭: Toggle to extend liquidity levels beyond the current range.

What it is: A boolean input to enable or disable the extension of liquidity levels.

What it does: Extends liquidity levels beyond their default range.

How to use it: Check or uncheck the box to enable or disable.

Additional Info: Extend liquidity levels beyond the current range.

💬 Text Options

💬 Text Options: Set text size and color for liquidity levels.

What it is: A dropdown to select text size and a color picker to choose text color.

What it does: Changes the size and color of the text displayed for liquidity levels.

How to use it: Select a size from the dropdown and a color from the color picker.

💬 Show Text

Text: Toggle to display text for liquidity levels.

What it is: A boolean input to show or hide the text for liquidity levels.

What it does: Displays the text information for liquidity levels on the chart.

How to use it: Check or uncheck the box to enable or disable.

💬 Show Volume

Volume: Toggle to display the volume of liquidity levels.

What it is: A boolean input to show or hide the volume information for liquidity levels.

What it does: Displays the volume information for liquidity levels on the chart.

How to use it: Check or uncheck the box to enable or disable.

Additional Info:

What it represents: The volume displayed represents the total trading volume that occurred during the formation of the liquidity level. This can indicate the level of participation or interest in that price level.

How it's calculated: The volume is the sum of all traded volumes within the candles that form the liquidity level.