Quasimodo Pattern Strategy Back Test [TradingFinder] QM Trading🔵 Introduction

The QM pattern, also known as the Quasimodo pattern, is one of the popular patterns in price action, and it is often used by technical analysts. The QM pattern is used to identify trend reversals and provides a very good risk-to-reward ratio. One of the advantages of the QM pattern is its high frequency and visibility in charts.

Additionally, due to its strength, it is highly profitable, and as mentioned, its risk-to-reward ratio is very good. The QM pattern is highly popular among traders in supply and demand, and traders also use this pattern.

The Price Action QM pattern, like other Price Action patterns, has two types: Bullish QM and Bearish QM patterns. To identify this pattern, you need to be familiar with its types to recognize it.

🔵 Identifying the QM Pattern

🟣 Bullish QM

In the bullish QM pattern, as you can see in the image below, an LL and HH are formed. As you can see, the neckline is marked as a dashed line. When the price reaches this range, it will start its upward movement.

🟣 Bearish QM

The Price Action QM pattern also has a bearish pattern. As you can see in the image below, initially, an HH and LL are formed. The neckline in this image is the dashed line, and when the LL is formed, the price reaches this neckline. However, it cannot pass it, and the downward trend resumes.

🔵 How to Use

The Quasimodo pattern is one of the clearest structures used to identify market reversals. It is built around the concept of a structural break followed by a pullback into an area of trapped liquidity. Instead of relying on lagging indicators, this pattern focuses purely on price action and how the market reacts after exhausting one side of liquidity. When understood correctly, it provides traders with precise entry points at the transition between trend phases.

🟣 Bullish Quasimodo

A bullish Quasimodo forms after a clear downtrend when sellers start losing control. The market continues to make lower lows until a sudden higher high appears, signaling that buyers are entering with strength. Price then pulls back to retest the previous low, creating what is known as the Quasimodo low.

This area often becomes the final trap for sellers before the market shifts upward. A visible rejection or displacement from this zone confirms bullish momentum. Traders usually place entries near this level, stops below the low, and targets at previous highs or the next resistance zone. Combining the setup with demand zones or Fair Value Gaps increases its accuracy.

🟣 Bearish Quasimodo

A bearish Quasimodo forms near the top of an uptrend when buyers begin to lose strength. The market continues to make higher highs until a sudden lower low breaks the bullish structure, showing that selling pressure is entering the market. Price then retraces upward to retest the previous high, forming the Quasimodo high, where breakout buyers are often trapped.

Once rejection appears at this level, it indicates a likely reversal. Traders can enter short near this area, with stop-losses placed above the high and targets near the next support or previous lows. The setup gains more reliability when aligned with supply zones, SMT divergence, or bearish Fair Value Gaps.

🔵 Setting

Pivot Period : You can use this parameter to use your desired period to identify the QM pattern. By default, this parameter is set to the number 5.

Take Profit Mode : You can choose your desired Take Profit in three ways. Based on the logic of the QM strategy, you can select two Take Profit levels, TP1 and TP2. You can also choose your take profit based on the Reward to Risk ratio. You must enter your desired R/R in the Reward to Risk Ratio parameter.

Stop Loss Refine : The loss limit of the QM strategy is based on its logic on the Head pattern. You can refine it using the ATR Refine option to prevent Stop Hunt. You can enter your desired coefficient in the Stop Loss ATR Adjustment Coefficient parameter.

Reward to Risk Ratio : If you set Take Profit Mode to R/R, you must enter your desired R/R here. For example, if your loss limit is 10 pips and you set R/R to 2, your take profit will be reached when the price is 20 pips away from your entry point.

Stop Loss ATR Adjustment Coefficient : If you set Stop Loss Refine to ATR Refine, you must adjust your loss limit coefficient here. For example, if your buy position's loss limit is at the price of 1000, and your ATR is 10, if you set Stop Loss ATR Adjustment Coefficient to 2, your loss limit will be at the price of 980.

Entry Level Validity : Determines how long the Entry level remains valid. The higher the level, the longer the entry level will remain valid. By default it is 2 and it can be set between 2 and 15.

🔵 Results

The following examples show the backtest results of the Quasimodo (QM) strategy in action. Each image is based on specific settings for the symbol, timeframe, and input parameters, illustrating how the QM logic can generate signals under different market conditions. The detailed configuration for each backtest is also displayed on the image.

⚠ Important Note : Even with identical settings and the same symbol, results may vary slightly across different brokers due to data feed variations and pricing differences.

Default Properties of Backtests :

OANDA:XAUUSD | TimeFrame: 5min | Duration: 1 Year :

BINANCE:BTCUSD | TimeFrame: 5min | Duration: 1 Year :

CAPITALCOM:US30 | TimeFrame: 5min | Duration: 1 Year :

NASDAQ:QQQ | TimeFrame: 5min | Duration: 5 Year :

OANDA:EURUSD | TimeFrame: 5min | Duration: 5 Year :

PEPPERSTONE:US500 | TimeFrame: 5min | Duration: 5 Year :

Cari dalam skrip untuk "liquidity"

Game Theory Trading StrategyGame Theory Trading Strategy: Explanation and Working Logic

This Pine Script (version 5) code implements a trading strategy named "Game Theory Trading Strategy" in TradingView. Unlike the previous indicator, this is a full-fledged strategy with automated entry/exit rules, risk management, and backtesting capabilities. It uses Game Theory principles to analyze market behavior, focusing on herd behavior, institutional flows, liquidity traps, and Nash equilibrium to generate buy (long) and sell (short) signals. Below, I'll explain the strategy's purpose, working logic, key components, and usage tips in detail.

1. General Description

Purpose: The strategy identifies high-probability trading opportunities by combining Game Theory concepts (herd behavior, contrarian signals, Nash equilibrium) with technical analysis (RSI, volume, momentum). It aims to exploit market inefficiencies caused by retail herd behavior, institutional flows, and liquidity traps. The strategy is designed for automated trading with defined risk management (stop-loss/take-profit) and position sizing based on market conditions.

Key Features:

Herd Behavior Detection: Identifies retail panic buying/selling using RSI and volume spikes.

Liquidity Traps: Detects stop-loss hunting zones where price breaks recent highs/lows but reverses.

Institutional Flow Analysis: Tracks high-volume institutional activity via Accumulation/Distribution and volume spikes.

Nash Equilibrium: Uses statistical price bands to assess whether the market is in equilibrium or deviated (overbought/oversold).

Risk Management: Configurable stop-loss (SL) and take-profit (TP) percentages, dynamic position sizing based on Game Theory (minimax principle).

Visualization: Displays Nash bands, signals, background colors, and two tables (Game Theory status and backtest results).

Backtesting: Tracks performance metrics like win rate, profit factor, max drawdown, and Sharpe ratio.

Strategy Settings:

Initial capital: $10,000.

Pyramiding: Up to 3 positions.

Position size: 10% of equity (default_qty_value=10).

Configurable inputs for RSI, volume, liquidity, institutional flow, Nash equilibrium, and risk management.

Warning: This is a strategy, not just an indicator. It executes trades automatically in TradingView's Strategy Tester. Always backtest thoroughly and use proper risk management before live trading.

2. Working Logic (Step by Step)

The strategy processes each bar (candle) to generate signals, manage positions, and update performance metrics. Here's how it works:

a. Input Parameters

The inputs are grouped for clarity:

Herd Behavior (🐑):

RSI Period (14): For overbought/oversold detection.

Volume MA Period (20): To calculate average volume for spike detection.

Herd Threshold (2.0): Volume multiplier for detecting herd activity.

Liquidity Analysis (💧):

Liquidity Lookback (50): Bars to check for recent highs/lows.

Liquidity Sensitivity (1.5): Volume multiplier for trap detection.

Institutional Flow (🏦):

Institutional Volume Multiplier (2.5): For detecting large volume spikes.

Institutional MA Period (21): For Accumulation/Distribution smoothing.

Nash Equilibrium (⚖️):

Nash Period (100): For calculating price mean and standard deviation.

Nash Deviation (0.02): Multiplier for equilibrium bands.

Risk Management (🛡️):

Use Stop-Loss (true): Enables SL at 2% below/above entry price.

Use Take-Profit (true): Enables TP at 5% above/below entry price.

b. Herd Behavior Detection

RSI (14): Checks for extreme conditions:

Overbought: RSI > 70 (potential herd buying).

Oversold: RSI < 30 (potential herd selling).

Volume Spike: Volume > SMA(20) x 2.0 (herd_threshold).

Momentum: Price change over 10 bars (close - close ) compared to its SMA(20).

Herd Signals:

Herd Buying: RSI > 70 + volume spike + positive momentum = Retail buying frenzy (red background).

Herd Selling: RSI < 30 + volume spike + negative momentum = Retail selling panic (green background).

c. Liquidity Trap Detection

Recent Highs/Lows: Calculated over 50 bars (liquidity_lookback).

Psychological Levels: Nearest round numbers (e.g., $100, $110) as potential stop-loss zones.

Trap Conditions:

Up Trap: Price breaks recent high, closes below it, with a volume spike (volume > SMA x 1.5).

Down Trap: Price breaks recent low, closes above it, with a volume spike.

Visualization: Traps are marked with small red/green crosses above/below bars.

d. Institutional Flow Analysis

Volume Check: Volume > SMA(20) x 2.5 (inst_volume_mult) = Institutional activity.

Accumulation/Distribution (AD):

Formula: ((close - low) - (high - close)) / (high - low) * volume, cumulated over time.

Smoothed with SMA(21) (inst_ma_length).

Accumulation: AD > MA + high volume = Institutions buying.

Distribution: AD < MA + high volume = Institutions selling.

Smart Money Index: (close - open) / (high - low) * volume, smoothed with SMA(20). Positive = Smart money buying.

e. Nash Equilibrium

Calculation:

Price mean: SMA(100) (nash_period).

Standard deviation: stdev(100).

Upper Nash: Mean + StdDev x 0.02 (nash_deviation).

Lower Nash: Mean - StdDev x 0.02.

Conditions:

Near Equilibrium: Price between upper and lower Nash bands (stable market).

Above Nash: Price > upper band (overbought, sell potential).

Below Nash: Price < lower band (oversold, buy potential).

Visualization: Orange line (mean), red/green lines (upper/lower bands).

f. Game Theory Signals

The strategy generates three types of signals, combined into long/short triggers:

Contrarian Signals:

Buy: Herd selling + (accumulation or down trap) = Go against retail panic.

Sell: Herd buying + (distribution or up trap).

Momentum Signals:

Buy: Below Nash + positive smart money + no herd buying.

Sell: Above Nash + negative smart money + no herd selling.

Nash Reversion Signals:

Buy: Below Nash + rising close (close > close ) + volume > MA.

Sell: Above Nash + falling close + volume > MA.

Final Signals:

Long Signal: Contrarian buy OR momentum buy OR Nash reversion buy.

Short Signal: Contrarian sell OR momentum sell OR Nash reversion sell.

g. Position Management

Position Sizing (Minimax Principle):

Default: 1.0 (10% of equity).

In Nash equilibrium: Reduced to 0.5 (conservative).

During institutional volume: Increased to 1.5 (aggressive).

Entries:

Long: If long_signal is true and no existing long position (strategy.position_size <= 0).

Short: If short_signal is true and no existing short position (strategy.position_size >= 0).

Exits:

Stop-Loss: If use_sl=true, set at 2% below/above entry price.

Take-Profit: If use_tp=true, set at 5% above/below entry price.

Pyramiding: Up to 3 concurrent positions allowed.

h. Visualization

Nash Bands: Orange (mean), red (upper), green (lower).

Background Colors:

Herd buying: Red (90% transparency).

Herd selling: Green.

Institutional volume: Blue.

Signals:

Contrarian buy/sell: Green/red triangles below/above bars.

Liquidity traps: Red/green crosses above/below bars.

Tables:

Game Theory Table (Top-Right):

Herd Behavior: Buying frenzy, selling panic, or normal.

Institutional Flow: Accumulation, distribution, or neutral.

Nash Equilibrium: In equilibrium, above, or below.

Liquidity Status: Trap detected or safe.

Position Suggestion: Long (green), Short (red), or Wait (gray).

Backtest Table (Bottom-Right):

Total Trades: Number of closed trades.

Win Rate: Percentage of winning trades.

Net Profit/Loss: In USD, colored green/red.

Profit Factor: Gross profit / gross loss.

Max Drawdown: Peak-to-trough equity drop (%).

Win/Loss Trades: Number of winning/losing trades.

Risk/Reward Ratio: Simplified Sharpe ratio (returns / drawdown).

Avg Win/Loss Ratio: Average win per trade / average loss per trade.

Last Update: Current time.

i. Backtesting Metrics

Tracks:

Total trades, winning/losing trades.

Win rate (%).

Net profit ($).

Profit factor (gross profit / gross loss).

Max drawdown (%).

Simplified Sharpe ratio (returns / drawdown).

Average win/loss ratio.

Updates metrics on each closed trade.

Displays a label on the last bar with backtest period, total trades, win rate, and net profit.

j. Alerts

No explicit alertconditions defined, but you can add them for long_signal and short_signal (e.g., alertcondition(long_signal, "GT Long Entry", "Long Signal Detected!")).

Use TradingView's alert system with Strategy Tester outputs.

3. Usage Tips

Timeframe: Best for H1-D1 timeframes. Shorter frames (M1-M15) may produce noisy signals.

Settings:

Risk Management: Adjust sl_percent (e.g., 1% for volatile markets) and tp_percent (e.g., 3% for scalping).

Herd Threshold: Increase to 2.5 for stricter herd detection in choppy markets.

Liquidity Lookback: Reduce to 20 for faster markets (e.g., crypto).

Nash Period: Increase to 200 for longer-term analysis.

Backtesting:

Use TradingView's Strategy Tester to evaluate performance.

Check win rate (>50%), profit factor (>1.5), and max drawdown (<20%) for viability.

Test on different assets/timeframes to ensure robustness.

Live Trading:

Start with a demo account.

Combine with other indicators (e.g., EMAs, support/resistance) for confirmation.

Monitor liquidity traps and institutional flow for context.

Risk Management:

Always use SL/TP to limit losses.

Adjust position_size for risk tolerance (e.g., 5% of equity for conservative trading).

Avoid over-leveraging (pyramiding=3 can amplify risk).

Troubleshooting:

If no trades are executed, check signal conditions (e.g., lower herd_threshold or liquidity_sensitivity).

Ensure sufficient historical data for Nash and liquidity calculations.

If tables overlap, adjust position.top_right/bottom_right coordinates.

4. Key Differences from the Previous Indicator

Indicator vs. Strategy: The previous code was an indicator (VP + Game Theory Integrated Strategy) focused on visualization and alerts. This is a strategy with automated entries/exits and backtesting.

Volume Profile: Absent in this strategy, making it lighter but less focused on high-volume zones.

Wick Analysis: Not included here, unlike the previous indicator's heavy reliance on wick patterns.

Backtesting: This strategy includes detailed performance metrics and a backtest table, absent in the indicator.

Simpler Signals: Focuses on Game Theory signals (contrarian, momentum, Nash reversion) without the "Power/Ultra Power" hierarchy.

Risk Management: Explicit SL/TP and dynamic position sizing, not present in the indicator.

5. Conclusion

The "Game Theory Trading Strategy" is a sophisticated system leveraging herd behavior, institutional flows, liquidity traps, and Nash equilibrium to trade market inefficiencies. It’s designed for traders who understand Game Theory principles and want automated execution with robust risk management. However, it requires thorough backtesting and parameter optimization for specific markets (e.g., forex, crypto, stocks). The backtest table and visual aids make it easy to monitor performance, but always combine with other analysis tools and proper capital management.

If you need help with backtesting, adding alerts, or optimizing parameters, let me know!

Strategy Builder v1.0.0 [BigBeluga]🔵 OVERVIEW

The Strategy Builder combines advanced price-action logic, smart-money concepts, and volatility-adaptive momentum signals to automate high-quality entries and exits across any market. It blends trend recognition, market structure shifts, order block reactions, imbalance (FVG) signals, liquidity sweeps, candlestick confirmations, and oscillator-powered divergences into one cohesive engine.

Whether used as a full automation workflow or as a structured confirmation framework, this strategy provides a disciplined, rules-driven method to trade with logic — not emotion.

🔵 BACKTEST WINDOW CONTROL

This module allows you to restrict strategy execution to a specific historical period.

Ideal for performance isolation, regime testing, and forward-walk validation.

Limit Backtest Window

Enabling this option activates custom date filters for the backtest engine.

Start — Define the starting date & time for backtesting

End — Define the ending date & time for backtesting

Only trades and signals inside this window are executed

Reduces computation load on large datasets

Useful for testing specific market environments (e.g., bull cycles, crash periods, sideways regimes)

🔵 SIGNAL GLOSSARY (Advanced Technical Explanation)

Traders can build long and short setups using up to 6 configurable entry conditions for each direction.

Every condition can be set as Bullish or Bearish and mapped to any signal source — allowing deep customization

Below is the full internal logic overview of every signal available in the Strategy Builder.

Signals are based on trend models, volatility structures, liquidity logic, oscillator behavior, and market structure mapping.

Trend Signals (Low-Lag Trend Engine)

Uses a proprietary low-lag baseline + momentum gradient model to detect directional bias.

Trend Signal — Momentum breaks above/below adaptive trend baseline.

Trend Signal+ — Stronger trend confirmation using volatility-weighted momentum.

Trend Signal Any — Triggers when any bullish/bearish trend signal appears.

SmartBand & Retests (Adaptive Volatility Bands)

Dynamic envelope that contracts/expands with volatility & trend strength.

SmartBand Retest — Price retests dynamic band and rejects, confirming continuation.

ActionWave Signals (Impulse-Pullback Engine)

Tracks wave behavior, acceleration and deceleration in price.

ActionWave — Detects directional impulse strength vs pullback weakness.

ActionWave Cross — Momentum acceleration threshold crossed → trend ignition.

Magnet Signals (Liquidity Gravity + Mean Reversion Bias)

Detects zones where price is being drawn due to liquidity voids or imbalance.

Magnet — Trend and liquidity pressure align, creating directional “pull.”

MagnetBar Low Momentum — Low-volatility compression → pre-breakout condition.

Flow Trend (Directional Flow State + ATR Envelope)

Higher-timeframe bias confirmation + dynamic volatility filter.

FlowTrend — Confirms major directional bias (uptrend or downtrend).

FlowTrend Retest — Price tests HTF flow band and rejects → trend resume.

Voltix (Volatility Expansion Pulse)

Detects regime shift from quiet accumulation → trending expansion.

Voltix — Breakout volatility signature, trend acceleration trigger.

Candlestick Pattern (Algorithmic Price Action Recognition)

Auto-recognizes meaningful reversal or continuation candle formations.

Candlestick Pattern — Confirms momentum reversal/continuation via candle logic.

OrderBlock Logic (Institutional Footprint System)

Institutional demand/supply zone tracking with mitigation logic.

Order Block Touch — Price taps institutional zone → reaction filter.

Order Block Break — OB invalidation → institutional flow shift.

Market Structure Engine (Swing Logic + Volume Confirmation)

Tracks major swing breaks and structural reversals.

BoS — Break of Structure in trend direction (continuation bias).

ChoCh — Change of Character — early reversal marker.

Fair Value Gaps (Imbalance & Volume Displacement)

Identifies inefficiencies caused by rapid displacement moves.

FVG Created — Price leaves inefficiency behind.

FVG Retest — Price returns to rebalance inefficiency → reaction zone.

Liquidity Events (Stop-Run & Reversal Logic)

Detects stop-hunt events and liquidity sweeps.

SFP — Swing failure & wick sweep → reversal confirmation.

Liquidity Created — New equal highs/lows form liquidity pool.

Liquidity Grab — Sweep through liquidity line followed by rejection.

Support / Resistance Break Logic

Adaptive zone recognition + momentum confirmation.

Support/Resistance Cross — Zone decisively broken → structural shift.

Pattern Breakouts (Market Geometry Engine)

Tracks breakout from compression & expansion formations.

Channel Break — Channel breakout → trend acceleration.

Wedge Break — Break from contraction wedge → burst of momentum.

Session Logic (Opening Range Behavior)

Session-based volatility trigger.

Session Break — Break above/below session opening range.

Momentum / Reversal Oscillator Suite

Oscillator-driven exhaustion & reversal signals.

Nautilus Signals — Momentum reversal signature (oscillator shift).

Nautilus Peak — Momentum peak → exhaustion risk.

OverSold/Overbought ❖ — Extreme exhaustion zones → reversal setup.

DipX Signals ✦ — Dip buy / Dip sell timing, micro-reversal engine.

Advanced Divergence Engine

Momentum/price disagreement layer with multi-trigger confirmation.

Normal Divergence — Classic divergence reversal.

Hidden Divergence — Trend continuation divergence.

Multiple Divergence — Multiple divergence confirmations stacked → high confidence.

🔧 Adjustable Signal Logic

Some signals in this system can be additionally refined through the strategy settings panel.

This allows traders to tune internal behavior for different market regimes, assets, and volatility conditions.

🔵 LONG / SHORT EXIT CONDITIONS

This section allows you to automate exits using the same advanced market conditions available for entries.

Each exit rule consists of:

Toggle — Enable/disable individual exit rule.

Direction Filter — Trigger exit only if selected market bias appears (Bullish/Bearish).

Signal Type — Choose which market event triggers the exit (same list as entry conditions).

When the active conditions are met, the strategy automatically closes the current position — ensuring emotion-free risk management and systematic trade control.

🔵 TAKE PROFIT & STOP LOSS SYSTEM

This strategy builder provides a fully dynamic risk-management engine designed for both systematic traders and discretionary confirmation users.

Take Profit Logic

Scale out of trades progressively or exit fully using algorithmic TP levels.

Up to 3 Take-Profit targets available

Choose TP calculation method:

• ATR-based distance (volatility-adaptive targets)

• %-based distance (fixed percentage from entry)

Define Size — ATR multiplier or % value

Custom Exit Size per TP (e.g., 25% / 25% / 50%)

Visual TP plotting on chart for clarity

Stop Loss Logic

Automated protection logic for every trade.

Two SL Modes:

• Fixed Stop Loss — static SL from entry

• Trailing Stop Loss — SL follows price as trade progresses

Distance options:

• ATR multiplier (adapts to volatility)

• %-based from entry (fixed distance)

SL dynamically draws on chart for transparency

Trailing SL behavior:

Follows price only in profitable direction

Never moves against the trade

Locks profits as trend develops

🔵 Strategy Dashboard

A compact on-chart performance dashboard is included to help monitor live trade status and backtest results in real time.

It displays key metrics:

Start Capital — Initial account balance used in simulation.

Position Size — % of capital allocated per trade based on user settings (It changes if the trade hits take profits, when more than one take profit is selected).

Current Trade — Shows active trade direction (Long / Short) and real-time % return from entry.

Closed Trades — Counter of completed positions, useful for reading sample size during testing.

🔵 CONCLUSION

The Strategy Builder brings together a powerful suite of smart-money and momentum-driven signals, allowing traders to automate robust trade logic built on modern market structure concepts. With access to trend filters, order blocks, liquidity events, divergence signals, volatility cues, and session-based triggers, it provides a deeply adaptive trade engine capable of fitting many market environments.

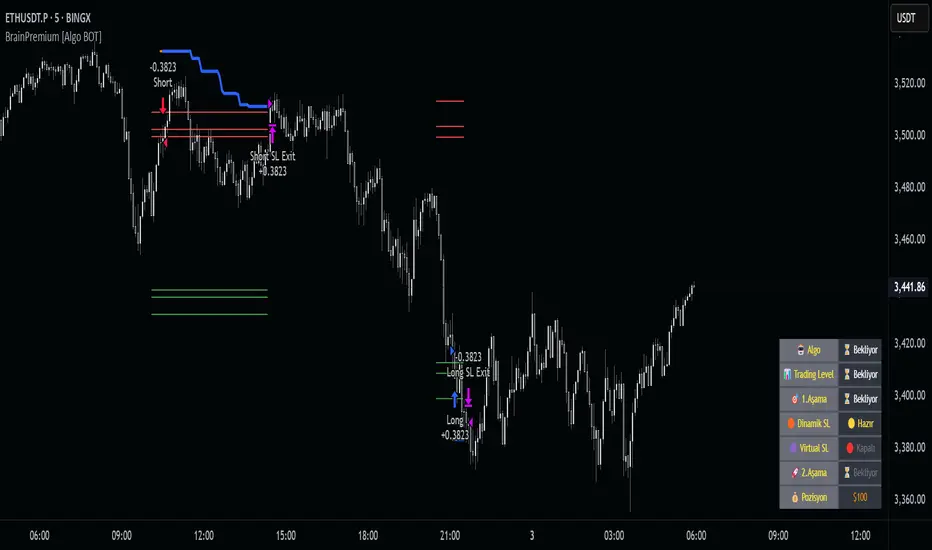

Brain Premium [ALGO]💡 Brain Premium ALGO

Brainpremium ALGO is a strategy algorithm that analyzes a two-phase regional liquidity structure and only opens positions on price breakouts occurring within these liquidity zones.

This system is developed based on the market experience of manual traders and automatically executes trade decisions using AI-like rules and specific triggers.

💡 Two-Phase Liquidity-Based Entry Strategy

This strategy operates by detecting liquidity sweep zones and confirmed reversal signals:

🔹 Phase 1 – Liquidity Sweep:

Price is expected to sweep areas where equal highs/lows or liquidity clusters exist. These zones are considered potential reversal levels.

🔹 Phase 2 – Confirmed Entry:

After liquidity is swept, entries are triggered only by confirmed reversal signals such as structural breaks, inside bars, or breakouts in the opposite direction.

✅ Entries are triggered only when liquidity and reversal confirmation occur simultaneously.

🎯 This approach targets high-probability, low-risk trades.

⚙️ Key Features

🔍 Dynamic Liquidity Detection — Automatically identifies liquidity zones.

🧩 Modular Entry Options (1–2–3) — Allows opening positions via different strategy paths.

🛡️ Dynamic Stop Loss System — Stop Loss adjusts as price moves favorably.

📈 Advanced Risk Management — Adjustable Take Profit, Stop Loss, leverage, balance, and mode.

🔔 JSON Alert Support — Connects to platforms like BingX via webhook.

🧾 Information Panel — Displays real-time trade data and strategy status.

📊 Backtest & Default Settings

Strategy tests are conducted with realistic and sustainable parameters:

Parameter Value

Trading Balance: $100 (%10 of total wallet)

Leverage: 10x

Stop Loss: 1%

Take Profit Type : High TP (optional: Low and Risky also available)

Entry Option 1 (optional: 2 and 3 also available)

Mode: NORMAL

Commission 0.05%

Dynamic Stop Loss: Enabled

Timeframe: 5 minute

Pair ETH/USDT

Duration: 30 days

🧭 Usage Instructions

Add Brain Premium ALGO to your TradingView chart.

Set position size, leverage, and SL/TP levels from the settings panel.

Select entry option (1, 2, or 3).

Activate backtesting and alert systems to monitor the strategy.

⚠️ Disclaimer

This strategy is not financial advice. Past performance does not guarantee future results. Trade only with capital you can afford to risk and always test thoroughly in a demo environment first.

3Commas Multicoin Scalper PRO [SwissAlgo]Introduction

Are you tired of tracking dozens of cryptocurrency charts and placing orders manually on your Exchange?

The 3Commas Multicoin Scalper PRO is an automated trading system designed to simultaneously identify and execute potential trading setups on multiple cryptocurrencies on your preferred Exchange (Binance, Bybit, OKX, Gate.io, Bitget) via 3Commas integration.

It analyzes price action, volume, momentum, volatility, and trend patterns across 180+ USDT Perpetual coins divided into 17 crypto categories , providing real-time signals directly to your 3Commas bots for automated trade execution. This indicator aims to identify potential trend-following and contrarian setups in both bull and bear markets.

-------------------------------------

What it Does

The 3Commas Multicoin Scalper PRO is a technical analysis tool that monitors multiple cryptocurrency pairs simultaneously and connects with 3Commas for signal delivery and execution.

Here's how the strategy works:

🔶 Technical Analysis : Analyzes price action, volume, momentum, volatility, and trend patterns across multiple USDT Perpetual Futures contracts simultaneously.

🔶 Pattern Detection : Identifies specific candle patterns and technical confluences that suggest potential trading setups across all USDT.P contracts of the selected categories

🔶 Signal Generation : When technical criteria are met at bar close, the indicator creates deal-start signals for the relevant pairs.

🔶 3Commas Integration : Packages these signals and delivers them to 3Commas through TradingView alerts, allowing 3Commas bots to receive specific pair information ('Deal-Start' signals).

🔶 Category Management : Each TradingView alert monitors an entire category (approximately 11 pairs), allowing selective activation of different crypto categories.

🔶 Visual Feedback : Provides color-coded candles and backgrounds to visualize technical conditions, with optional pivot points and trend visualization.

Candle types:

Signals:

-------------------------------------

Quick Start Guide

1. Setup 3Commas Bots : Configure two DCA bots in 3Commas (All USDT pairs) - one for LONG positions and one for SHORT positions.

2. Define Trading Parameters : Set your budget for each trade and adjust your preferred sensitivity within the indicator settings.

3. Create Category Alerts : Set up one TradingView alert for each crypto category you want to trade.

That's it! Once configured, the system automatically sends signals to your 3Commas bots when predefined trading setups are detected across coins in your selected/activated categories. The indicator scans all coins at bar close (for example, every hour on the 1H timeframe) and triggers trade execution only for those showing technical confluences.

Important : The more categories you activate by setting TradingView alerts, the more signals your 3Commas bots will receive. Consider your total capital when enabling multiple categories. More details about the setup process are provided below (see paragraph "Detailed Setup & Configuration")

-------------------------------------

Built-in Backtesting

The 3Commas Multicoin Scalper PRO includes backtesting visualization for each coin. When viewing any USDT Perpetual pair on your chart, you can visualize how the strategy would have performed historically on that specific asset.

Color-coded candles and signal markers show past trading setups, helping you evaluate which coins responded best to the strategy. This built-in backtesting capability can support your selection of assets/categories to trade before deploying real capital.

As backtesting results are hypothetical and do not guarantee future performance, your research and analysis are essential for selecting the crypto categories/coins to trade.

The default strategy settings are: Start Capital 1.000$, leverage 25X, Commissions 0.1% (average Taker Fee on Exchanges for average users), Order Amount 200$ for Longs/150$ for Shorts, Slippage 4

-------------------------------------

Key Features

🔶 Multi-Exchange Support : Compatible with BINANCE, BYBIT, BITGET, GATEIO, and OKX USDT Perpetual markets (USDT.P)

🔶 Wide Asset Coverage : Simultaneously analyzes 180+ cryptocurrencies across 17 specialized crypto categories

🔶 Custom Category Option : Create your watchlist with up to 10 custom USDT Perpetual pairs

🔶 3Commas Integration : Seamlessly connects with 3Commas bots to automate trade entries and exits

🔶 Dual Strategy Approach : Identifies both "trend following" and "contrarian" potential setups

🔶 Confluence-Based Signals : Uses a combination of multiple technical factors - price spikes, price momentum, volume spikes, volume momentum, trend analysis, and volatility spikes - to generate potential trading setups

🔶 Risk Management : Adjustable sensitivity/risk levels, leverage settings, and budget allocation for each trade

🔶 Visual Indicators : Color-coded candles and trading signals provide visual feedback on market conditions

🔶 Trend Indication : Background colors showing ongoing uptrends/downtrends

🔶 Pivot Points & Daily Open : Optional display of pivot points and daily open price for additional context

🔶 Liquidity Analysis : Optional display of high/low liquidity timeframes throughout the trading week

🔶 Trade Control : Configurable limit for the maximum number of signals sent to 3Commas for execution (per bar close and category)

Available Exchanges

Categories

Custom Category

Trend following/contrarian signals

-------------------------------------

Methodology

The 3Commas Multicoin Scalper PRO utilizes a multi-faceted approach to identify potential trading setups:

1. Price Action Analysis : Detects abnormal price movements by comparing the current candle's range to historical averages and standard deviations, helping identify potential "pump and dump" scenarios or new-trends start

2. Price Momentum : Evaluates the relative strength of bullish vs. bearish price movements over time, indicating the build-up of buying or selling pressure.

3. Volume Analysis: Identifies unusual volume spikes by comparing current volume to historical averages, signaling strong market interest in a particular direction.

4. Volume Momentum : Measures the ratio of bullish to bearish volume, revealing the dominance of buyers or sellers over time.

5. Trend Analysis : Combines EMA slopes, RSI, and Stochastic RSI to determine overall trend direction and strength.

6. Volatility : Monitors the ATR (Average True Range) to detect periods of increased market volatility, which may indicate potential breakouts or reversals

7. Candle Wick Analysis : Evaluates upper and lower wick percentages to detect potential rejection patterns and reversals.

8. Pivot Point Analysis : Uses pivot points (PP, R1-R3, S1-S3) for identifying key support/resistance areas and potential breakout/breakdown levels.

9. Daily Open Reference: Analyzes price action relative to the daily open for potential setups related to price movement vs. the opening price

10. Market Timing/Liquidity : Evaluates high/low liquidity periods, specific days/times of heightened risk, and potential market manipulation timeframes.

11. Boost Factors : Applies additional weight to certain confluence patterns to adjust global scores

These factors are combined into a "Global Score" ranging from -1 to +1 , applied at bar close to the newly formed candles.

Scores above predefined thresholds (configurable via the Sensitivity Settings) indicate strong bullish or bearish conditions and trigger signals based on predefined patterns. The indicator then applies additional filters to generate specific "Trend Following" and "Contrarian" trading signals. The identified signals are packaged and sent to 3Commas for execution.

Pivot Points

Daily open

Market Trend

Liquidity patterns by weekday

-------------------------------------

Who This Strategy Is For?

The 3Commas Multicoin Scalper PRO may benefit:

Crypto Traders seeking to automate their trading across multiple coins simultaneously

3Commas Users looking to enhance their bot performance with advanced technical signals

Busy Traders who want to monitor many market opportunities without constant chart-watching

Multi-strategy traders interested in both trend-following and reversal trading approaches

Traders of Various Experience Levels from intermediate traders wanting to save time to advanced traders seeking to scale their operations

Perpetual Futures Traders on major exchanges (Binance, Bybit, OKX, Gate.io, Bitget)

Swing and Scalp Traders seeking to identify short to medium-term profit opportunities

-------------------------------------

Visual Indicators

The indicator provides visual feedback through:

1. Candlestick Colors :

* Lime: Strong bullish candle (High positive score)

* Blue: Moderate bullish candle (Medium positive score)

* Red: Strong bearish candle (High negative score)

* Purple: Moderate bearish candle (Medium negative score)

* Pale Green/Red: Mild bullish/bearish candle

2. Signal Markers :

* ↗: Trend Following Long signal

* ↘: Trend Following Short signal

* ⤴: Contrarian Long signal

* ⤵: Contrarian Short signal

3. Optional Elements :

* Pivot Points: Daily support/resistance levels (R1-R3, S1-S3, PP)

* Daily Open: Reference price level for the current trading day

* Trend Background: Color-coded background suggesting potential ongoing uptrend/downtrend

* Liquidity Highlighting: Background colors indicating typical high/low market liquidity periods

4. TradingView Strategy Plots and Backtesting Data : Standard performance metrics showing entry/exit points, equity curves, and trade statistics, based on the signals generated by the script.

-------------------------------------

Detailed Setup & Configuration

The indicator features a user-friendly input panel organized in sequential steps to guide you through the complete setup process. Tooltips for each step provide additional information to help you understand the actions required to get the strategy running.

Informative tables provide additional details and instructions for critical setup steps such as 3Commas bot configuration and TradingView alert creation (to activate trading on specific categories).

1. Choose Exchange, Crypto Category & Sensitivity

* Select your USDT Perpetual Exchange (BINANCE, BYBIT, BITGET, GATEIO, or OKX) - i.e. the same Exchange connected in your 3Commas account

* Browse and choose your preferred crypto category, or define your watchlist

* Choose from three sensitivity levels: Default, Aggressive, or Test Mode (test mode is designed to generate way more signals, a potentially helpful feature when you are testing the indicator and alerts)

2. Setup 3Commas Bots and integrate them with the algo

* Create both LONG and SHORT DCA Bots in 3Commas

* Configure bots to accept signals for 'All USDT Pairs' with "TradingView Custom Signal" as deal start condition

* Enter your Bot IDs and Email Token in the indicator settings

* Set a maximum budget for LONG and SHORT trades

* Choose whether to allow LONG trades, SHORT trades, or both, according to your preference and market analysis

* Set maximum trades per bar/category (i.e. the max. number of simultaneous signals that the algo may send to your 3Commas bots for execution at every bar close - every hour if you set the 1H timeframe)

* Access the detailed setup guide table for step-by-step 3Commas configuration instructions

3Commas integration

3. Choose Visuals

* Toggle various optional visual elements to add to the chart: category metrics, fired alerts, coin metrics, daily open, pivot points

* Select a color theme: Dark or Light

4. Activate Trading via Alerts

* Create TradingView alerts for each category you want to trade

* Set alert condition to "3Commas Multicoin Scalper" with "Any alert() function call"

* Set the content of the message filed to: {{Message}}, deleting the default content shown in this text field, to enable proper 3Commas integration (any other text than {{Message}}, would break the delivery trading signals from Tradingview to 3Commas)

* View the alerts setup instruction table for visual guidance on this critical step

Alerts

Fired Alerts

Important Configuration Notes

Ensure that the TradingView chart's exchange matches your selected exchange in the indicator settings and your 3Commas bot settings.

You must configure the same leverage in both the script and your 3Commas bots

Your 3Commas bots must be configured for All USDT pairs

You must enter the exact Bot IDs and Email Token from 3Commas (these remain confidential - no one, including us, has access to them)

If you activate multiple categories without sufficient capital, 3Commas will display " insufficient funds " errors - align your available capital with the number of categories you activate (each deal will use the budget amount specified in user inputs)

You are free to set your Take Profit % / trailing on 3Commas

We recommend not to use DCA orders (i.e. set the number of DCA orders at zero)

Legend of symbols

-------------------------------------

FAQs

General Questions

❓ Q: What is Global Score? A: The Global Score serves as a foundation for signal generation. When a candle's score exceeds certain thresholds (defined by your Risk Level setting), it becomes a candidate for signal generation. However, not all high-scoring candles generate trading signals - the indicator applies additional pattern recognition and contextual filters. For example, a strongly positive score (lime candle) in an established uptrend may trigger a "Trend Following" signal, while a strongly negative score (red candle) in a downtrend might generate a "Trend Following Short" signal. Similarly, contrarian signals are generated when specific reversal patterns occur alongside appropriate Global Score values, often involving wick analysis and pivot point interactions. This multi-layer approach helps filter out false positives and identify higher-probability trading setups.

❓ Q: What's the difference between "Trend following" and "Contrarian" signals in the script? A: "Trend Following" signals follow the identified trends while "Contrarian" signals anticipate potential trend reversals.

❓ Q: Why can't I configure all the parameters? A: We've designed the solution to be plug-and-play to prevent users from getting lost in endless configurations. The preset values have been tested against their trade-offs in terms of financial performance, average trade duration, and risk levels.

❓ Q: Why don't I see any signals on my chart? A: Make sure you're viewing a USDT Perpetual pair from your selected exchange that belongs to the crypto category you've chosen to analyze. For example, if you've selected the "Top Major Coins" category with Binance as your exchange, you need to view a chart of one of those specific pairs (like BINANCE:BTCUSDT.P) to see signals. If you switch exchanges, for example from Binance to Bybit, you need to pull a Bybit pair on the chart to see backtesting data and signals.

❓ Q: Does this indicator guarantee profits? A: No. Trading cryptocurrencies involves significant risk, and past performance is not indicative of future results. This indicator is a tool to help you identify potential trading setups, but it does not and cannot guarantee profits.

❓ Q: Does this indicator repaint or use lookahead bias? A: No. All trading signals generated by this indicator are based only on completed price data and do not repaint. The system is designed to ensure that backtesting results reflect as closely as possible what you should experience in live trading.

While reference levels like pivot points are kept stable throughout the day using lookahead on, the actual buy and sell signals are calculated using only historical data (lookahead off) that would have been available at that moment in time. This ensures reliability and consistency between backtesting and real-time trading performance.

Technical Setup

❓ Q: What exchanges are supported? A: The strategy supports BINANCE, BYBIT, BITGET, GATEIO, and OKX USDT Perpetual markets (i.e. all the Exchanges you can connect to your 3Commas account for USDT Perpetual trading, excluding Coinbase Perpetual that offers UDSC pairs, instead of USDT).

❓ Q: What timeframe should I use? A: The indicator is optimized for the 1-hour (1H) timeframe but may run on any timeframe.

❓ Q: How many coins can I trade at once? A: You can trade all coins within each selected category (up to 11 coins per category in standard categories). You can activate multiple categories by setting up multiple alerts.

❓ Q: How many alerts do I need to set up? A: You need to set up one alert for each crypto category you want to trade. For example, if you want to trade both the "Top Major Coins" and the "DeFi" categories, you'll need to create two separate alerts, one for each category. We recommend starting with one category, testing the results carefully, monitoring performance daily, and perhaps activating additional categories in a second stage.

❓ Q: Are there any specific risk management features built into the indicator? A: Yes, the indicator includes risk management features: adjustable maximum trades per hour/category, the ability to enable/disable long or short signals depending on market conditions, customizable trade size for both long and short positions, and different sensitivity/risk level settings.

❓ Q: What happens if 3Commas can't execute a signal? A: If 3Commas cannot execute a signal (due to insufficient funds, bot offline, etc.), the trade will be skipped. The indicator will continue sending signals for other valid setups, but it doesn't retry failed signals.

❓ Q: Can I run this indicator on multiple charts at once? A: Yes, but it's not necessary. The indicator analyzes all coins in your selected categories regardless of which chart you apply it to. For optimal resource usage, apply it to a single chart of a USDT Perpetual pair from your selected exchange. To stop trading a category delete the alert created for that category.

❓ Q: How frequently does the indicator scan for new signals? A: The indicator scans all coins in your selected categories at the close of each bar (every hour if you selected the 1H timeframe).

3Commas Integration

❓ Q: Do I need a 3Commas account? A: Yes, a 3Commas account with active DCA bots (both LONG and SHORT) is required for automated trade execution. A paid subscription is needed, as multipair Bots and multiple simultaneous deals are involved.

❓ Q: How do I set the leverage? A: Set the leverage identically in both the indicator settings and your 3Commas DCA bots (the max supported leverage is 50x). Always be careful about leverage, as it amplifies both profits and losses.

❓ Q: Where do I find my 3Commas Bot IDs and Email Token? A: Open your 3Commas DCA bot and scroll to the "Messages" section. You'll find the Bot ID and Email Token within any message (e.g., "Start Deal").

Display Settings

❓ Q: What does the Sensitivity setting do? A: It adjusts the sensitivity of signal generation. "Default" provides a balanced approach with moderate signal frequency. "Aggressive" lowers the thresholds for signal generation, potentially increasing trade frequency but may include more noise. "Test Mode" is the most sensitive setting, useful for testing alert configurations but not recommended for live trading. Higher risk levels may generate more signals but with potentially lower average quality, while lower risk levels produce fewer but potentially better signals.

❓ Q: What does "Show fired alerts" do? A: The "Show fired alerts" option displays a label on your chart showing which signals have been fired and sent to 3Commas during the most recent candle closes. This visual indicator helps you confirm that your alerts are working properly and shows which coins from your selected category have triggered signals. It's useful when setting up and testing the system, allowing you to verify that signals are being sent to 3Commas as expected and their frequency over time.

❓ Q: What does "Show coin/token metrics" do? A: This toggle displays detailed technical metrics for the specific coin/token currently shown on your chart. When enabled, it shows statistics for the last closed candle for that coin.

❓ Q: What does "Show most liquid days/times" do? A: This toggle displays color-coded background highlighting to indicate periods of varying market liquidity throughout the trading week. Green backgrounds show generally higher liquidity periods (typically weekday trading hours), yellow highlights potentially manipulative periods (often Sunday/Monday overnight), and gray indicates low liquidity periods (when major markets are closed or during late hours).

⚠️ Disclaimer

This indicator is for informational and educational purposes only and does not constitute financial advice. Trading cryptocurrencies involves significant risk, including the potential loss of all invested capital, and past performance is not indicative of future results.

Always conduct your own thorough research (DYOR) and understand the risks involved before making any trading decisions. Trading with leverage significantly amplifies both potential profits and losses - exercise extreme caution when using leverage and never risk more than you can afford to lose.

The Bot ID and Email Token information are transmitted directly from TradingView to 3Commas via secure connections. No third party or entity will ever have access to this data (including the Author). Do not share your 3Commas credentials with anyone.

This indicator is not affiliated with, endorsed by, or sponsored by TradingView or 3Commas.

Destroyer LifeDestroyer Life Strategy - High-Frequency Long & Short Trading

Overview:

The Destroyer Life strategy is an advanced cryptocurrency trading algorithm designed for high-frequency execution on the 15-second timeframe. It combines CRT (Candle Range Trend) and Turtle Soup trading logic with multi-timeframe analysis to optimize entries and exits for both long and short trades. This strategy is specifically optimized for high-volatility crypto pairs, such as SOL/USD on MEXC, ensuring precise execution with minimal drawdown.

Key Features:

15-Second Timeframe Execution: Optimized for ultra-short-term trading.

Long & Short Strategy: Simultaneously identifies profitable buy and sell opportunities.

CRT & Turtle Soup Logic: Leverages price action patterns for enhanced trade accuracy.

Higher Timeframe Analysis (HTF): Incorporates liquidity zones, fair value gaps (FVG), and breaker blocks for context-aware trading.

Dynamic Position Sizing: Uses an adjustable leverage multiplier for risk-controlled trade sizing.

Commission Optimization: Ensures profitability even with trading fees.

Strict Risk Management: Implements exit conditions based on liquidity structure and trend reversals.

Strategy Performance (Backtested on SOL/USD - MEXC):

Overall Profitability: ~80% win rate in backtesting.

Net Profit: $3,151.12 (6.30% ROI).

Gross Profit: $3,795.68 (7.59%).

Gross Loss: $644.56 (1.29%).

Long Trades Profit: $1,459.05 (2.92%).

Short Trades Profit: $1,692.07 (3.38%).

Commission Paid: $924.82.

Minimum Trade Holding Period: 1-minute cooldown between trades.

Trading Logic:

Entry Conditions:

Long Trades: Triggered when the price enters a liquidity void and aligns with higher timeframe bullish bias.

Short Trades: Triggered when price approaches a resistance level with bearish higher timeframe confluence.

CRT & Turtle Soup Patterns: Identifies reversals by analyzing breakout and fake-out structures.

Exit Conditions:

Long Positions Close: Upon price exceeding a 3.88% profit threshold or reversing below an HTF structure.

Short Positions Close: Upon reaching a similar 3.88% threshold or showing strong bullish signals.

Dynamic Position Sizing:

Uses a leverage-based calculation that adapts trade size based on volatility.

Liquidity Awareness:

Tracks Mitigation Blocks (MB), Fair Value Gaps (FVG), Buy/Sell-Side Liquidity (BSL/SSL) to determine optimal execution.

Best Use Cases:

Scalpers & High-Frequency Traders: Those looking for rapid trade execution with short holding periods.

Crypto Traders Focused on Low Timeframes: Optimized for 15-second price action.

Traders Utilizing Liquidity Concepts: Built to exploit liquidity traps and inefficiencies.

Risks & Considerations:

High-Frequency Execution Requires Low Latency: Ensure your broker or exchange supports fast order execution.

Backtested Results May Vary: Real-time performance depends on market conditions.

Commission & Fees Impact Profits: Consider exchanges with low fees to maximize strategy efficiency.

Final Thoughts:

The Destroyer Life Strategy is designed for serious traders looking to take advantage of high-volatility markets with a structured, liquidity-based approach. By combining price action, liquidity concepts, and adaptive risk management, it provides a solid framework for executing high-probability trades on crypto markets.

🚀 Ready to take your trading to the next level? Try Destroyer Life today and dominate the markets!

Flux Charts - PAT Automation💎 GENERAL OVERVIEW

The PAT Automation is a powerful and versatile tool designed to help traders rigorously test their trading strategies against historical market data. With an array of advanced settings, traders can fine-tune their strategies, assess performance, and identify key improvements before deploying in live trading environments. This backtester offers a wide range of configurable settings, explained within this write-up.

Features of the PAT Automation:

Step By Step : Configure your strategy step by step, which will allow you to have OR & AND logic in your strategies.

Highly Configurable : Offers multiple parameters for fine-tuning trade entry and exit conditions.

Multi-Timeframe Analysis : Allows traders to analyze multiple timeframes simultaneously for enhanced accuracy.

Provides advanced stop-loss, take-profit, and break-even settings.

Incorporates volume-based conditions, liquidity grabs , order blocks , market structures and fair value gaps for refined strategy execution.

🚩 UNIQUENESS

The PAT Automation stands out from conventional backtesting tools due to its unparalleled flexibility, precision, and advanced trading logic integration. Key factors that make it unique include:

✅ Comprehensive Strategy Customization – Unlike traditional backtesters that offer basic entry and exit conditions, PAT Automation provides a highly detailed parameter set, allowing traders to fine-tune their strategies with precision.

✅ Multi-Timeframe Price Action Features – This is the first-ever tool that allows traders to backtest price action with multi-timeframe features such as Fair Value Gaps (FVGs), Inversion Fair Value Gaps (IFVGs), Order Blocks & Breaker Blocks.

✅ Customizable Take-Profit Conditions – Offers various methods to set take-profit exits, including using core features from price action, and fixed exits like ATR, % change or price change, enabling traders to tailor their exit strategies to specific market behaviors.

✅ Customizable Stop-Loss Conditions – Provides several ways to set up stop losses, including using concepts from price action and trailing stops or fixed exits like ATR, % change or price change, allowing for dynamic risk management tailored to individual strategies.

✅ Integration of External Indicators – Allows the inclusion of other indicators or data sources from TradingView for creating strategy conditions, enabling traders to enhance their strategies with additional insights and data points.

By integrating these advanced features, PAT Automation ensures that traders can rigorously test and optimize their strategies with great accuracy and efficiency.

📌 HOW DOES IT WORK?

The first setting you will want to set it the pyramiding setting. This setting controls the number of simultaneous trades in the same direction allowed in the strategy. For example, if you set it to 1, only one trade can be active in any time, and the second trade will not be entered unless the first one is exited. If it is set to 2, the script will handle both of them at the same time. Note that you should enter the same value to this pyramiding setting, and the pyramiding setting in the "Properties" tab of the script for this to work.

For deep backtesting, you can set "Max Distance To Last Bar" to "Unlimited". If you encounter any memory issues, try decreasing this setting to a lower value.

You can enable and set a backtesting window that will limit the entries to between the start date & end date.

Then, you can enter your desired settings to Price Action features like FVGs, IFVGs, Order Blocks, Breaker Blocks, Liquidity Grabs, Market Structures, EQH & EQL and Volume Imbalances. You can also enable and set up to 3 timeframes, which you can use later on when customizing your strategies enter / exit conditions.

Entry Conditions

From the "Long Conditions" or the "Short Conditions" groups, you can set your position entry conditions. For settings like "initial capital" or "order size", you can open the "Properties" tab, where these are handled.

The PAT Automation can use the following conditions for entry conditions :

1. Order Block (OB)

Detection: Triggered when an Order Block forms or is detected

Retest: Triggered when price retests an Order Block. A retest is confirmed when a candle enters an Order Block and closes outside of it.

Retracement: Triggered when price touches an Order Block

Break: Triggered when an Order Block is invalidated by candle close or wick, depending on the user's input.

2. Breaker Block (BB)

Detection: Triggered when a Breaker Block forms or is detected

Retest: Triggered when price retests a Breaker Block. A retest is confirmed when a candle enters a Breaker Block and closes outside of it.

Retracement: Triggered when price touches a Breaker Block

Break: Triggered when a Breaker Block is invalidated by candle close or wick, depending on the user's input.

3. Fair Value Gap (FVG)

Detection: Triggered when an FVG forms or is detected

Retest: Triggered when price retests an FVG. A retest is confirmed when a candle enters an FVG and closes outside of it.

Retracement: Triggered when price touches an FVG

Break: Triggered when an FVG is invalidated by candle close or wick, depending on the user's input.

4. Inversion Fair Value Gap (IFVG)

Detection: Triggered when an IFVG forms or is detected

Retest: Triggered when price retests an IFVG. A retest is confirmed when a candle enters an IFVG and closes outside of it.

Retracement: Triggered when price touches an IFVG

Break: Triggered when an IFVG is invalidated by candle close or wick, depending on the user's input.

5. Break of Structure (BOS)

Detection: Triggered when a BOS forms or is detected

6. Change of Character (CHoCH)

Detection: Triggered when a CHoCH forms or is detected

7. Change of Character Plus (CHoCH+)

Detection: Triggered when a CHoCH+ forms or is detected

8. Volume Imbalance (VI)

Detection: Triggered when a Volume Imbalance forms or is detected

9. Equal High (EQH)

Detection: Triggered when an EQH is detected

10. Equal Low (EQL)

Detection: Triggered when an EQL is detected

11. Buyside Liquidity Grab

Detection: Triggered when a liquidity grab occurs at Buyside Liquidity (BSL).

12. Sellside Liquidity Grab

Detection: Triggered when a liquidity grab occurs at Sellside Liquidity (SSL).

🕒 TIMEFRAME CONDITIONS

The PAT Automation supports Multi-Timeframe (MTF) features, just like the Price Action Toolkit. When setting an entry condition, you can also choose the timeframe.

To set up MTF conditions, navigate to the 'Timeframes' section in the settings, select your desired timeframes, and enable them. You can choose up to three timeframes.

Once you've selected your timeframes, you can use them in your strategy. When setting long and short entry / exit conditions, you can choose from Timeframe 1, Timeframe 2, or Timeframe 3.

External Conditions

Users can use external indicators on the chart to set entry conditions.

The second dropdown in the external condition settings allows you to choose a conditional operator to compare external outputs. Available options include:

Less Than or Equal To: <=

Less Than: <

Equal To: =

Greater Than: >

Greater Than or Equal To: >=

The position entry conditions work like this ;

Each side has 5 Price Action conditions and 1 Source condition. Each condition can be enabled or disabled using the checkbox on the left side.

For Price Action Conditions, you can set a direction: "Any", "Bullish" or "Bearish".

Then a Price Action Feature, like "FVG" or "Order Block".

The last part of our constructed condition is the alert type, which you can select between "Detection", "Retest", "Retracement" or "Break".

Now you should have a constructed condition, which should look like "Bullish Order Block Retest".

You can select which timeframe should this condition work on from Timeframe 1, 2 or 3. If you select "Any Timeframe", the condition will work for all timeframes.

Lastly select the step of this condition from 1 to 6.

The Source Condition

The last condition on each side is a source condition that is different from the others. Using this condition, you can create your own logic using other indicators' outputs on your chart. For example, suppose that you have an EMA indicator in your chart. You can have the source condition to something like "EMA > high".

The Step System

Each condition has a step number, and conditions are in topological order based on them.

The conditions are executed step by step. This means the condition with step 2 cannot be executed before the condition with step 1 is executed.

Conditions with the same step numbers have "OR" logic. This means that if you have 2 conditions with step 3, the condition with step 4 can trigger after only one of the step 3 conditions is executed.

➕ OTHER ENTRY FEATURES

The PAT Automation allows traders to choose when to execute trades and when not to execute trades.

1. Only Take Trades

This setting lets users specify the time period when their strategy can open or execute trades.

2. Don't Take Trades

This setting lets users specify time periods when their strategy can't open or execute trades.

↩️ EXIT CONDITIONS

1. Exit on Opposite Signal

When enabled, a long position will close when short entry conditions are met, and a short position will close when long entry conditions are met.

2. Exit on Session End

When enabled, positions will be closed at the end of the trading session.

📈 TAKE PROFIT CONDITIONS

There are several methods available for setting take profit exits and conditions.

1. Entry Condition TP

Users can use entry conditions as triggers for take-profit exits. This setting can be found under the long and short exit conditions.

2. Fixed TP

Users can set a fixed TP for exits. This setting can be found under the long and short exit conditions. Users can choose between the following:

Price: This method triggers a TP exit when price reaches a specified level. For example, if you set the Price TP to 10 and buy NASDAQ:TSLA at $190, the trade will automatically exit when the price reaches $200 ($190 + $10).

Ticks: This method triggers a TP exit when price moves a specified number of ticks.

Percentage (%): This method triggers a TP exit when price moves a specified percentage.

ATR: This method triggers a TP exit based on a specified multiple of the Average True Range (ATR).

📉 STOP LOSS CONDITIONS

There are several methods available for setting stop-loss exits and conditions.

1. Entry Condition SL

Users can use entry conditions as triggers for stop-loss exits. This setting can be found under the long and short exit conditions.

2. Fixed SL

Users can set a fixed SL for exits. This setting can be found under the long and short exit conditions. Users can choose between the following:

Price: This method triggers a SL exit when price reaches a specified level. For example, if you set the Price SL to 10 and buy NASDAQ:TSLA at $200, the trade will automatically exit when the price reaches $190 ($200 - $10).

Ticks: This method triggers a SL exit when price moves a specified number of ticks.

Percentage (%): This method triggers a SL exit when price moves a specified percentage.

ATR: This method triggers a SL exit based on a specified multiple of the Average True Range (ATR).

3. Trailing Stop

An explanation & example for the trailing stop feature is present on the write-up within the next section.

Exit conditions have the same logic of constructing conditions like the entry ones. You can construct a Take-Profit Condition & a Stop-Loss Condition. Note that the Take-Profit condition will only work if the position is in profit, regardless of if it's triggered or not. The same applies for the Stop-Loss condition, meaning that it will only work if the position is in loss.

You can also set a Fixed TP & Fixed SL based on the price movement after the position is entered. You have options like "Price", "Ticks", "%", or "Average True Range". For example, you can set a Fixed TP like "5%", and the position will be entered once it moves 5% up in a long position.

Trailing Stop

For the Fixed SL, you also have a "Trailing" stop option, which you can set it's activation level as well. The Trailing stop activation level and it's value are expressed in ticks. Check this scenerio for an example :

We have a ticker with a tick value of $1. Our Trailing Stop is set to 10 ticks and activation level is set to 30 ticks.

We buy 1 contract when the price is $100.

When the price becomes $110, we are in $10 (10 ticks) profit and the trailing stop is now activated.

The current price our stop's on is $110 - $30 (30 ticks), which is the level of $80.

The trailing stop will only move if the price moves up the highest high the price has been after we entered the position.

Let's suppose that price moves up $40 right after our trailing stop is activated. The price will now be $150, and our trailing stop will sit on $150 - $30 (30 ticks) = $120.

If the price is down the $120 level, our stop loss will be triggered.

There is also a "Hard SL" option designed for a backup stop-loss when trailing stops are enabled. You can enable & set this option and if the price goes down before our trailing stop even activates, the position will be exited.

You can also move stop-loss to the break-even (entry price of the position) after a certain profit is achieved using the last setting of the exit conditions. Note that for this to work, you will need to have a Fixed SL set-up.

➕ OTHER EXIT FEATURES

1. Move Stop Loss to Breakeven

This setting allows the strategy to automatically move the SL to Breakeven (BE) when the position is in profit by a certain amount. Users can choose between the following:

Price: This method moves the SL to BE when price reaches a specified level.

Ticks: This method moves the SL to BE when price moves a specified number of ticks.

Percentage (%): This method moves the SL to BE when price moves a specified percentage.

ATR: This method moves the SL to BE when price moves a specified multiple of the Average True Range (ATR).

Example Entry Scenario

To give an example , check this scenario; out conditions are :

LONG CONDITIONS

Bullish Order Block Detection, Step 1

Bullish CHoCH Detection, Step 2

Bullish Volume Imbalance Detection, Step 2

Bullish IFVG Retest, Step 3

First, the strategy needs to detect a Bullish Order Block in order to start working.

After it's detected, now it's looking for either a CHoCH, or a Volume Imbalance to proceed to the next step, the reason for this is that they both have the same step number.

After one of them is detected, the strategy will consistently check all IFVGs for a retest. If the retest occurs, a long position will be entered.

⏰ ALERTS

This indicator uses TradingView's strategy alert system. All entries and exits will be sent as an alert if configured. It's possible to further customize these alerts to your liking. For more information check TradingView's strategy alert customization page: www.tradingview.com

⚙️ SETTINGS

1. Backtesting Settings

Pyramiding: Controls the number of simultaneous trades allowed in the strategy. This setting must have the same value that is entered on the script's properties tab on the settings pane.

Max Distance to Last Bar: Determines the depth of historical data used to prevent memory overload.

Enable Custom Backtesting Period: Restricts backtesting to a specific date range.

Start & End Time Configuration: Define precise start and end dates for historical analysis.

2. Fair Value Gaps Settings

Zone Invalidation: Select between "Wick" and "Close" invalidation.

Filtering: Choose between "Average Range" and "Volume Threshold".

FVG Sensitivity: Ranges from Extreme to Low to detect FVGs with varying strictness.

Allow Gaps: Enables analysis on tickers that have different open-close price gaps.

3. Inversion Fair Value Gaps Settings

Zone Invalidation: Choose between "Wick" and "Close".

4. Order Block Settings

Swing Length: Adjusts the minimum number of bars required for OB formation.

Zone Invalidation Method: Select between "Wick" and "Close".

5. Breaker Block Settings

Zone Invalidation: Set invalidation method as "Wick" or "Close".

6. Liquidity Grabs Settings

Pivot Length: Adjusts the number of bars used to detect liquidity grabs.

Wick-Body Ratio: Defines the proportion of wick-to-body size for liquidity grab detection.

7. Multi-Timeframe Analysis

Enable Up to Three Timeframes: Select and analyze trades across multiple timeframes.

8. Market Structures

Swing Length: Defines the number of bars required for structure shifts.

Includes BOS, CHoCH, CHoCH+ Detection.

9. Equal Highs & Lows

ATR Multiplier: Defines the sensitivity of equal highs/lows detection.

10. Volume Imbalances

Gap Size Sensitivity: Ranges from "Ultra" to "Low".

Disable Overnight Gaps: Filters out volume imbalances occurring due to overnight gaps.

11. Entry Conditions for Long & Short Trades

Multiple Conditions (1-6): Configure up to six independent conditions per trade direction.

Condition Types: Options include Detection, Retest, Retracement, and Break.

Timeframe Specification: Choose between "Any Timeframe", "Timeframe 1", "Timeframe 2", or "Timeframe 3".

Trade Execution Filters: Restrict trades within specific trading sessions.

12. Exit Conditions for Long & Short Trades

Exit on Opposite Signal: Automatically exit trades upon opposite trade conditions.

Exit on Session End: Closes all positions at the end of the trading session.

Multiple Take-Profit (TP) and Stop-Loss (SL) Configurations:

TP/SL based on % move, ATR, Ticks, or Fixed Price.

Hard SL option for additional risk control.

Move SL to BE (Break Even) after a certain profit threshold.

Briss Thorn XtremeStrategy Description: Briss Thorn Xtreme

The Briss Thorn Xtreme is an innovative trading strategy designed to identify and capitalize on opportunities in the forex market through advanced technical analysis and dynamic risk management. This strategy combines calculations based on RSI and ATR with time and day filters, providing customized signals and real-time alerts via Discord. Ideal for traders seeking a structured and highly customizable methodology, Briss Thorn Xtreme integrates enhanced visual tools for efficient trade management.

Key Features:

RSI and ATR-Based Signals: Utilizes smoothed RSI and ATR calculations to identify trends and measure volatility, allowing for more precise detection of buy and sell opportunities.

Dynamic Stop-Loss (SL) and Take-Profit (TP) Levels: Automatically calculates SL and TP levels based on market volatility, dynamically adjusting to optimize risk management.

Advanced Discord Integration: Sends detailed alerts to your Discord channel, including information such as the asset, signal time, entry price, and SL/TP levels, facilitating real-time decision-making.

Complete Customization: Allows users to adjust key parameters such as RSI periods, smoothing factors, liquidity thresholds, trading schedules, and operation days, adapting to different trading styles and market conditions.

Enhanced Chart Visualization: Includes visual elements like candle color changes based on trend, colored boxes for SL and TP, and a summary table of recent trades, enabling quick market interpretation.

Day and Time Operation Filters: Enables selection of specific days of the week and time slots during which signals are generated, optimizing market exposure and avoiding periods of low liquidity or unwanted high volatility.

Trade Summary: Displays a summary of the last three trades directly on the chart, indicating whether TP or SL was reached, aiding in strategy performance evaluation.

Customizable Alert Messages: Allows customization of messages sent to Discord for buy and sell signals, tailoring them to your specific preferences and requirements.

Additional Visual Tools: Highlights the operational range on the chart during permitted trading hours and colors candles based on the current trend (bullish, bearish, or neutral), enhancing visibility and decision-making.

How the Strategy Works:

Technical Indicators Calculation:

- RSI (Relative Strength Index) : Calculates RSI with a defined period and smooths it using an Exponential Moving Average (EMA) to obtain a more stable and reliable signal.

- ATR (Average True Range) : Calculates ATR adjusted by a rapid liquidity factor to measure the current market volatility, thereby determining the strength of the trend.

Generating Buy and Sell Signals:

- Buy Signal: A buy signal is generated when the liquidity index surpasses the short liquidity level, indicating potential accumulation and an upward trend.

- Sell Signal: A sell signal is generated when the liquidity index falls below the long liquidity level, indicating potential distribution and a downward trend.

- Operation Conditions: Signals are only generated on selected days and times, avoiding periods of low liquidity or unwanted high volatility.

Dynamic SL and TP Levels Calculation:

- Stop-Loss (SL) and Take-Profit (TP): SL and TP levels are calculated based on the entry price and a defined number of ticks, automatically adjusting to market volatility to optimize risk management.

- SL and TP Visualization: Colored boxes are drawn on the chart for a clear visual reference of SL and TP levels, facilitating trade management.

Automatic Execution and Alerts:

- Order Execution: Upon signal generation, the strategy automatically executes a market order (buy or sell).

- Discord Alerts: Detailed alerts are sent to the configured Discord channel, providing essential information for swift decision-making, including asset, signal time, entry price, current volatility (ATR), and trend direction.

Trade Management and Monitoring:

- Trade Summary: A table on the chart displays a summary of the last three trades (Today, Yesterday, Day Before Yesterday), indicating whether TP or SL was reached, allowing real-time performance evaluation.

- Automatic Trade Closure: The strategy automatically closes trades upon reaching the established SL or TP levels, ensuring efficient risk management and preventing excessive losses.

Additional Visualization:

- Candle Coloring by Trend: Candles are colored based on the current trend (bullish, bearish, or neutral), facilitating quick identification of market direction.

- Operational Range Highlighting: The chart background is colored during permitted trading hours, highlighting active periods of the strategy and enhancing trade visibility.

---

Strategy Properties (Important)

This backtest is conducted on M17 EURUSD using the following backtesting properties:

Initial Capital: $1000

Order Size: 1% of capital

Commission: $0.20 per order

Slippage: 1 tick

Pyramiding: 1 order

Price Verification for Limit Orders: 0 ticks

Recalculate on Order Execution: Enabled

Recalculate on Every Tick: Enabled

Recalculate After Order Execution: Enabled

Bar Magnifier for Backtesting Precision: Enabled