Qullamaggie [Modified] | FractalystWhat's the purpose of this strategy?

The strategy aims to identify high-probability breakout setups in trending markets, inspired by Kristjan "Qullamaggie" Kullamägi’s approach.

It focuses on capturing explosive price moves after periods of consolidation, using technical criteria like moving averages, breakouts, trailing stop-loss and momentum confirmation.

Ideal for swing traders seeking to ride strong trends while managing risk.

----

How does the strategy work?

The strategy follows a systematic process to capture high-momentum breakouts:

Pre-Breakout Criteria:

Prior Price Surge: Identifies stocks that have rallied 30-100%+ in recent month(s), signaling strong underlying momentum (per Qullamaggie’s volatility expansion principles).

Consolidation Phase: Looks for a tightening price range (e.g., flag, pennant, or tight base), indicating a potential "coiling" before continuation.

Trend Confirmation: Uses moving averages (e.g., 20/50/200 EMA) to ensure the stock is trading above key averages on the daily chart, confirming an uptrend.

Price Break: Enters when price clears the consolidation high with conviction.

Risk Management:

Initial Stop Loss: Placed below the consolidation low or a recent swing point to limit downside.

Break-Even Adjustment: Moves stop loss to breakeven once the trade reaches 1.5x risk-to-reward (RR), securing a "free trade" while letting winners run.

Trailing Stop (Unique Edge):

Market Structure Trailing: Instead of trailing via moving averages, the stop is dynamically adjusted using structural invalidation level. This adapts to price action, allowing the trade to stay open during volatile retracements while locking in gains as new structure forms.

Why This Matters: Most strategies use rigid trailing stops (e.g., below the 10EMA), which often exit prematurely in choppy markets. By trailing based on structure, this strategy avoids "noise" and captures larger trends, directly boosting overall returns.

----

What markets or timeframes is this suited for?

This is a long-only strategy designed for trending markets, and it performs best in:

Markets: Stocks (especially high-growth, liquid equities), cryptocurrencies (major pairs with strong volatility), commodities (e.g., oil, gold), and futures (index/commodity futures).

Timeframes: Primarily daily charts for swing trades (1-30 day holds), though weekly charts can help confirm broader trends.

Key Advantage: The TradingView script allows instant backtesting with adjustable parameters

You can:

- Test historical performance across multiple markets to identify which assets align best with the strategy.

- Optimize settings (e.g., trailing stop sensitivity, moving averages etc.) to match a market’s volatility profile.

Build a diversified portfolio by filtering for markets that show consistent profitability in backtests.

For example, you might discover cryptos require tighter trailing stops due to volatility, while stocks thrive with wider structural stops. The script automates this analysis, letting you to trade confidently.

----

What indicators or tools does the strategy use?

The strategy combines customizable technical tools with strict anti-lookahead safeguards:

Core Indicators:

Moving Averages: Adjustable periods (e.g., 20/50/200 EMA or SMA) and timeframes (daily/weekly) to confirm trend alignment. Users can test combinations (e.g., 10EMA vs. 20EMA) to optimize for specific markets.

Breakout Parameters:

Consolidation Length: Adjustable window to define the "tightness" of the pre-breakout pattern.

Entry Models: Flexible entry logics (Breakouts and fractals)

Anti-Lookahead Design:

All calculations (e.g., moving averages, consolidation ranges, volume averages) use only closed/confirmed data available at the time of the signal.

----

How do I manage risk with this strategy?

The strategy prioritizes customizable risk controls to align with your trading style and account size:

User-Defined Risk Inputs:

Risk Per Trade: Set a % of Equity (e.g., 1-2%) to determine position size. The strategy auto-calculates shares/contracts to match your selected risk per trade.

Flexibility: Choose between fixed risk or equity-based scaling.

The script adjusts position sizing dynamically based on your selection.

Pyramiding Feature:

Customizable Entries: Adjust the number of pyramiding trades allowed (e.g., 1-3 additional positions) in the strategy settings. Each new entry is triggered only if the prior trade hits its 1.5x RR target and the trend remains intact.

Risk-Scaled Additions: New positions use profits from prior trades, compounding gains without increasing initial risk.

Risk-Free Trade Mechanic:

Once a trade reaches 1.5x RR, the stop loss is moved to breakeven, eliminating downside risk.

The strategy then opens a new position (if pyramiding is enabled) using a portion of the locked-in profit. This "snowballs" winners while keeping total capital exposure stable.

Impact on Net Profit & Drawdown:

Net Profit Boost: Pyramiding lets you ride multi-leg trends aggressively. For example, a 100% runner could generate 2-3x more profit vs. a single-entry approach.

Controlled Drawdowns: Since new positions are funded by profits (not initial capital), max drawdown stays anchored to your original risk per trade (e.g., 1-2% of account). Even if later entries fail, the breakeven stop on prior trades protects overall equity.

Why This Works: Most strategies either over-leverage (increasing drawdowns) or exit too early. By recycling profits into new positions only after securing risk-free capital, this approach mimics hedge fund "scaling in" tactics while staying retail-trader friendly.

----

How does the strategy identify market structure for its trailing stoploss?

The strategy identifies market structure by utilizing an efficient logic with for loops to pinpoint the first swing candle that features a pivot of 2. This marks the beginning of the break of structure, where the market's previous trend or pattern is considered invalidated or changed.

----

What are the underlying calculations?

The underlying calculations involve:

Identifying Swing Points: The strategy looks for swing highs (marked with blue Xs) and swing lows (marked with red Xs). A swing high is identified when a candle's high is higher than the highs of the candles before and after it. Conversely, a swing low is when a candle's low is lower than the lows of the candles before and after it.

Break of Structure (BOS):

Bullish BOS: This occurs when the price breaks above the swing high level of the previous structure, indicating a potential shift to a bullish trend.

Bearish BOS: This happens when the price breaks below the swing low level of the previous structure, signaling a potential shift to a bearish trend.

Structural Liquidity and Invalidation:

Structural Liquidity: After a break of structure, liquidity levels are updated to the first swing high in a bullish BOS or the first swing low in a bearish BOS.

Structural Invalidation: If the price moves back to the level of the first swing low before the bullish BOS or the first swing high before the bearish BOS, it invalidates the break of structure, suggesting a potential reversal or continuation of the previous trend.

This method provides users with a technical approach to filter market regimes, offering an advantage by minimizing the risk of overfitting to historical data, which is often a concern with traditional indicators like moving averages.

By focusing on identifying pivotal swing points and the subsequent breaks of structure, the strategy maintains a balance between sensitivity to market changes and robustness against historical data anomalies, ensuring a more adaptable and potentially more reliable market analysis tool.

----

What entry criteria are used in this script?

The script uses two entry models for trading decisions: BreakOut and Fractal.

Underlying Calculations:

Breakout: The script records the most recent swing high by storing it in a variable. When the price closes above this recorded level, and all other predefined conditions are satisfied, the script triggers a breakout entry. This approach is considered conservative because it waits for the price to confirm a breakout above the previous high before entering a trade. As shown in the image, as soon as the price closes above the new candle (first tick), the long entry gets taken. The stop-loss is initially set and then moved to break-even once the price moves in favor of the trade.

Fractal: This method involves identifying a swing low with a period of 2, which means it looks for a low point where the price is lower than the two candles before and after it. Once this pattern is detected, the script executes the trade. This is an aggressive approach since it doesn't wait for further price confirmation. In the image, this is represented by the 'Fractal 2' label where the script identifies and acts on the swing low pattern.

----

What type of stop-loss identification method are used in this strategy?

This strategy employs two types of stop-loss methods: Initial Stop-loss and Trailing Stop-Loss.

Underlying Calculations:

Initial Stop-loss:

ATR Based: The strategy uses the Average True Range (ATR) to set an initial stop-loss, which helps in accounting for market volatility without predicting price direction.

Calculation:

- First, the True Range (TR) is calculated for each period, which is the greatest of:

- Current Period High - Current Period Low

- Absolute Value of Current Period High - Previous Period Close

- Absolute Value of Current Period Low - Previous Period Close

- The ATR is then the moving average of these TR values over a specified period, typically 14 periods by default. This ATR value can be used to set the stop-loss at a distance from the entry price that reflects the current market volatility.

Swing Low Based:

For this method, the stop-loss is set based on the most recent swing low identified in the market structure analysis. This approach uses the lowest point of the recent price action as a reference for setting the stop-loss.

Trailing Stop-Loss:

The strategy uses structural liquidity and structural invalidation levels across multiple timeframes to adjust the stop-loss once the trade is profitable. This method involves:

Detecting Structural Liquidity: After a break of structure, the liquidity levels are updated to the first swing high in a bullish scenario or the first swing low in a bearish scenario. These levels serve as potential areas where the price might find support or resistance, allowing the stop-loss to trail the price movement.

Detecting Structural Invalidation: If the price returns to the level of the first swing low before a bullish break of structure or the first swing high before a bearish break of structure, it suggests the trend might be reversing or invalidating, prompting the adjustment of the stop-loss to lock in profits or minimize losses.

By using these methods, the strategy dynamically adjusts the initial stop-loss based on market volatility, helping to protect against adverse price movements while allowing for enough room for trades to develop. The ATR-based stop-loss adapts to the current market conditions by considering the volatility, ensuring that the stop-loss is not too tight during volatile periods, which could lead to premature exits, nor too loose during calm markets, which might result in larger losses. Similarly, the swing low based stop-loss provides a logical exit point if the market structure changes unfavorably.

Each market behaves differently across various timeframes, and it is essential to test different parameters and optimizations to find out which trailing stop-loss method gives you the desired results and performance. This involves backtesting the strategy with different settings for the ATR period, the distance from the swing low, and how the trailing stop-loss reacts to structural liquidity and invalidation levels.

Through this process, you can tailor the strategy to perform optimally in different market environments, ensuring that the stop-loss mechanism supports the trade's longevity while safeguarding against significant drawdowns.

----

What type of break-even method is used in this strategy? What are the underlying calculations?

Moves the initial stop-loss to the entry price when the price reaches a certain RR ratio.

Calculation:

Break-even level = Entry Price + (Initial Risk * RR Ratio)

----

What tables are available in this script?

- Summary: Provides a general overview, displaying key performance parameters such as Net Profit, Profit Factor, Max Drawdown, Average Trade, Closed Trades and more.

Total Commission: Displays the cumulative commissions incurred from all trades executed within the selected backtesting window. This value is derived by summing the commission fees for each trade on your chart.

Average Commission: Represents the average commission per trade, calculated by dividing the Total Commission by the total number of closed trades. This metric is crucial for assessing the impact of trading costs on overall profitability.

Avg Trade: The sum of money gained or lost by the average trade generated by a strategy. Calculated by dividing the Net Profit by the overall number of closed trades. An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.

MaxDD: Displays the largest drawdown of losses, i.e., the maximum possible loss that the strategy could have incurred among all of the trades it has made. This value is calculated separately for every bar that the strategy spends with an open position.

Profit Factor: The amount of money a trading strategy made for every unit of money it lost (in the selected currency). This value is calculated by dividing gross profits by gross losses.

Avg RR: This is calculated by dividing the average winning trade by the average losing trade. This field is not a very meaningful value by itself because it does not take into account the ratio of the number of winning vs losing trades, and strategies can have different approaches to profitability. A strategy may trade at every possibility in order to capture many small profits, yet have an average losing trade greater than the average winning trade. The higher this value is, the better, but it should be considered together with the percentage of winning trades and the net profit.

Winrate: The percentage of winning trades generated by a strategy. Calculated by dividing the number of winning trades by the total number of closed trades generated by a strategy. Percent profitable is not a very reliable measure by itself. A strategy could have many small winning trades, making the percent profitable high with a small average winning trade, or a few big winning trades accounting for a low percent profitable and a big average winning trade. Most mean-reversion successful strategies have a percent profitability of 40-80% but are profitable due to risk management control.

BE Trades: Number of break-even trades, excluding commission/slippage.

Losing Trades: The total number of losing trades generated by the strategy.

Winning Trades: The total number of winning trades generated by the strategy.

Total Trades: Total number of taken traders visible your charts.

Net Profit: The overall profit or loss (in the selected currency) achieved by the trading strategy in the test period. The value is the sum of all values from the Profit column (on the List of Trades tab), taking into account the sign.

- Monthly: Displays performance data on a month-by-month basis, allowing users to analyze performance trends over each month and year.

- Weekly: Displays performance data on a week-by-week basis, helping users to understand weekly performance variations.

- UI Table: A user-friendly table that allows users to view and save the selected strategy parameters from user inputs. This table enables easy access to key settings and configurations, providing a straightforward solution for saving strategy parameters by simply taking a screenshot with Alt + S or ⌥ + S.

User-input styles and customizations:

Please note that all background colors in the style are disabled by default to enhance visualization.

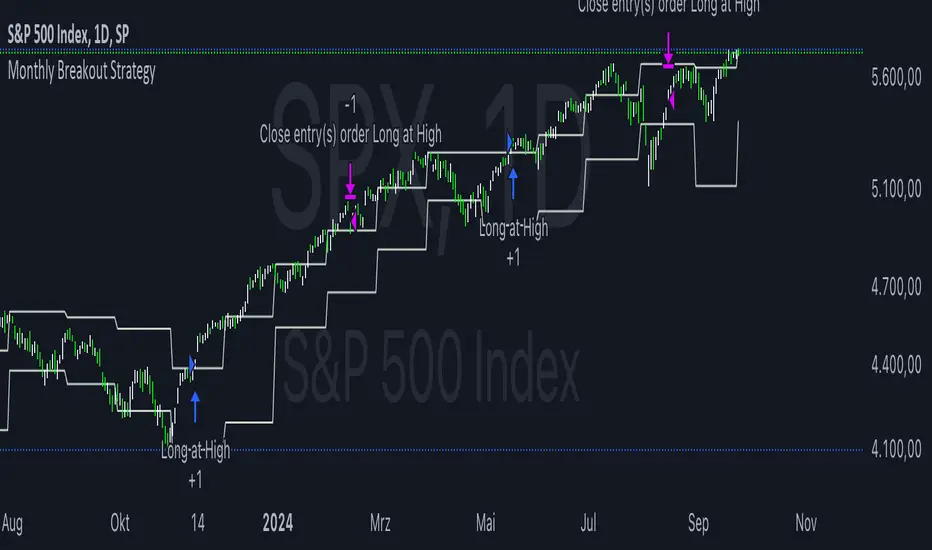

How to Use This Strategy to Create a Profitable Edge and Systems?

Choose Your Strategy mode:

- Decide whether you are creating an investing strategy or a trading strategy.

Select a Market:

- Choose a one-sided market such as stocks, indices, or cryptocurrencies.

Historical Data:

- Ensure the historical data covers at least 10 years of price action for robust backtesting.

Timeframe Selection:

- Choose the timeframe you are comfortable trading with. It is strongly recommended to use a timeframe above 15 minutes to minimize the impact of commissions/slippage on your profits.

Set Commission and Slippage:

- Properly set the commission and slippage in the strategy properties according to your broker/prop firm specifications.

Parameter Optimization:

- Use trial and error to test different parameters until you find the performance results you are looking for in the summary table or, preferably, through deep backtesting using the strategy tester.

Trade Count:

- Ensure the number of trades is 200 or more; the higher, the better for statistical significance.

Positive Average Trade:

- Make sure the average trade is above zero.

(An important value since it must be large enough to cover the commission and slippage costs of trading the strategy and still bring a profit.)

Performance Metrics:

- Look for a high profit factor, and net profit with minimum drawdown.

- Ideally, aim for a drawdown under 20-30%, depending on your risk tolerance.

Refinement and Optimization:

- Try out different markets and timeframes.

- Continue working on refining your edge using the available filters and components to further optimize your strategy.

What Makes This Strategy Unique?

This strategy combines flexibility, smart risk management, and momentum focus in a way that’s rare and practical:

1. Adapts to Any Market Rhythm

Works on daily, weekly, or intraday charts without code changes.

Uses two entry types: classic breakouts (like trending stocks) or fractal patterns (to avoid false starts).

2. Smarter Stop-Loss System

No rigid rules: Stops adjust based on price structure (e.g., new “higher lows”), not fixed percentages.

Avoids whipsaws: Tightens stops only when the trend strengthens, not in choppy markets.

3. Safe Profit-Boosting Pyramiding

Adds new positions only after prior trades are risk-free (stops moved above breakeven).

Scales up using locked-in profits, not new capital, to grow gains safely.

4. Built-In Momentum Check

Tracks 1/3/6-month price growth to spotlight stocks with strong, lasting momentum.

Terms and Conditions | Disclaimer

Our charting tools are provided for informational and educational purposes only and should not be construed as financial, investment, or trading advice. They are not intended to forecast market movements or offer specific recommendations. Users should understand that past performance does not guarantee future results and should not base financial decisions solely on historical data.

Built-in components, features, and functionalities of our charting tools are the intellectual property of @Fractalyst Unauthorized use, reproduction, or distribution of these proprietary elements is prohibited.

- By continuing to use our charting tools, the user acknowledges and accepts the Terms and Conditions outlined in this legal disclaimer and agrees to respect our intellectual property rights and comply with all applicable laws and regulations.

Cari dalam skrip untuk "momentum"

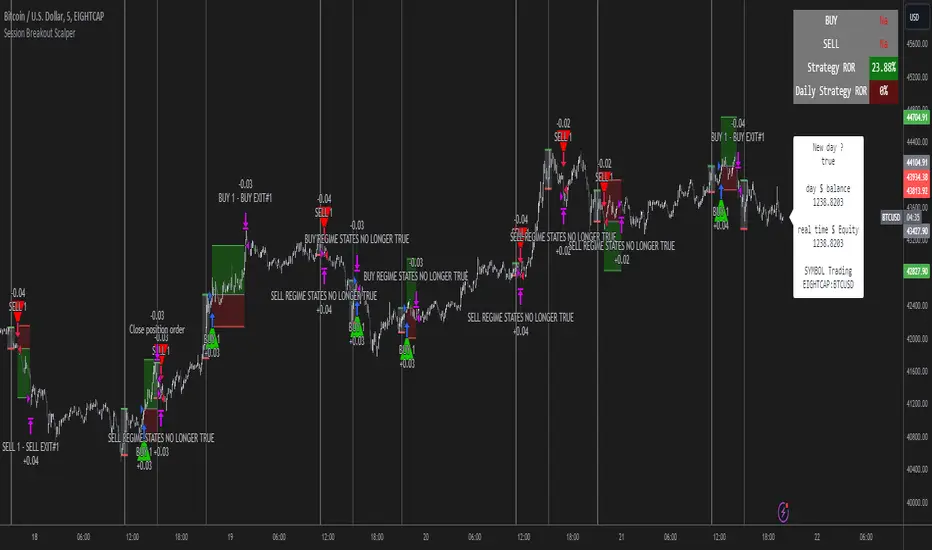

Scalping Strategy Signal v2 by [INFINITYTRADER]Overview

This Pine Script (v6) implements a scalping strategy that uses higher timeframe data (default: 4H) to generate entry and exit signals, originally designed for the 15-minute timeframe with an option for 30-minute charts. The "Scalping Strategy Signal v2 by " integrates moving averages, RSI, volume, ATR, and candlestick patterns to identify trading opportunities. It features adjustable risk management with ATR-based stop-loss, take-profit, and trailing stops, plus dynamic position sizing based on user-set capital. Trades trigger only on the higher timeframe candle close (e.g., 4H) to limit activity within the same period. This closed-source script offers a structured scalping approach, blending multiple entry methods and risk controls for adaptability across market conditions.

What Makes It Unique

Unlike typical scalping scripts relying on single-indicator triggers (e.g., RSI alone or basic MA crossovers), this strategy combines four distinct entry methods—standard MA crossovers, RSI-based momentum shifts, trend-following shorts, and candlestick pattern logic—evaluated on a 4H timeframe for confirmation. This multi-layered design, paired with re-entry logic after losses and a mix of manual, ATR-based, and trailing exits, aims to balance trade frequency and reliability. The higher timeframe filter adds precision not commonly found in simpler scalping tools, while the 30-minute option enhances consistency by reducing noise.

How It Works

Timeframe Logic

Runs on a base timeframe (designed for 15-minute charts, with a 30-minute option) while pulling data from a user-chosen higher timeframe (default: 4H) for signal accuracy.

Limits entries to the close of each 4H candle, ensuring one trade per period to avoid over-trading in volatile conditions.

Indicators and Data

Moving Averages : Employs 21-period and 50-period simple moving averages on the higher timeframe to detect trends and signal entries/exits.

Volume : Requires volume to exceed 70% of its 20-period average on the higher timeframe for momentum confirmation.

RSI : Uses a 14-period RSI for overbought/oversold filtering and a 6-period RSI for precise entry timing.

ATR : Applies a 14-period Average True Range on the higher timeframe to set adaptive stop-loss and take-profit levels.

Candlestick Patterns : Analyzes consecutive green or red 4H bars for trend continuation signals.

Why These Indicators

The blend of moving averages, RSI, volume, ATR, and candlestick patterns forms a robust scalping framework. Moving averages establish trend context, RSI filters momentum and avoids extremes, volume confirms market activity, ATR adjusts risk to volatility, and candlestick patterns enhance entry timing with price action insights. Together, they target small, frequent moves in flat or trending markets, with the 4H filter reducing false signals common in lower-timeframe scalping.

Entry Conditions

Four entry methods are evaluated at the 4H candle close:

Standard Long Entry: Price crosses above the 21-period moving average, volume exceeds 70% of its 20-period average, and the 1H 14-period RSI is below 70—confirms uptrend momentum.

Special Long Entry: The 6-period RSI crosses above 23, price is more than 1.5 times the ATR from the 21-period moving average, and price exceeds its prior close—targets oversold bounces with a stop-loss at the 4H candle’s low.

Short Entries:

- RSI-Based: The 6-period RSI crosses below 68 with volume support—catches overbought pullbacks.

- Trend-Based: Price crosses below the 21-period moving average, volume is above 70% of its average, and the 1H 14-period RSI is above 30—confirms downtrends.

Red/Green Bar Logic: Two consecutive green 4H bars for longs or red 4H bars for shorts—uses candlestick patterns for continuation, with a tight stop-loss from the base timeframe candle.

Re-Entry Logic

Long : After a losing special long, triggers when the 6-period RSI crosses 27 and price crosses the 21-period moving average.

Short : After a losing short, triggers when the 6-period RSI crosses 50 and price crosses below the 21-period moving average.

Purpose: Offers recovery opportunities with stricter conditions.

Exit Conditions

Manual Exits: Longs close if the 21-period MA crosses below the 50-period MA or the 1H 14-period RSI exceeds 68; shorts close if the 21-period MA crosses above the 50-period MA or RSI drops below 25.

ATR-Based TP/SL: Stop-loss is entry price ± ATR × 1.5 (default); take-profit is ± ATR × 4 (default), checked at 4H close.

Trailing Stop: Adjusts ±6x ATR from peak/trough, closing if price retraces within 1x ATR.

Special/Tight SL: Special longs exit if price opens below the 4H candle’s low; 4th method entries use the base timeframe candle’s low/high, checked every bar.

Position Sizing

Bases trade value on user-set capital (default: 100 USDT), dividing by the higher timeframe close price for dynamic sizing.

Visualization

Displays a table at the bottom-right with current/previous signals, TP/SL levels, equity, trading pair, and trade size—color-coded for clarity (green for buy, red for sell).

Inputs

Initial Capital (USDT): Sets trade value (default: 100, min: 1).

ATR Stop-Loss Multiplier: Adjusts SL distance (default: 1.5, min: 1).

ATR Take-Profit Multiplier: Adjusts TP distance (default: 4, min: 1).

Higher Timeframe: Selects analysis timeframe (options: 1m, 5m, 15m, 30m, 1H, 4H, D, W; default: 4H).

Usage Notes

Intended Timeframe: Designed for 15-minute charts with 4H confirmation for precision and frequency; 30-minute charts improve consistency by reducing noise.

Backtesting: Adjust ATR multipliers and capital to match your asset’s volatility and risk tolerance.

Risk Management: Combines manual, ATR, and trailing exits—monitor to avoid overexposure.

Limitations: 4H candle-close dependency may delay entries in fast markets; RSI/volume filters can reduce trades in low-momentum periods.

Backtest Observations

Tested on BTC/USDT (4H higher timeframe, default settings: Initial Capital: 100 USDT, ATR SL: 1.5x, ATR TP: 4x) across market conditions, comparing 15-minute and 30-minute charts:

Bull Market (Jul 2023 - Dec 2023):

15-Minute: 277 long, 219 short; Win Rate: 42.74%; P&L: 108%; Drawdown: 1.99%; Profit Factor: 3.074.

30-Minute: 257 long, 215 short; Win Rate: 49.58%; P&L: 116.85%; Drawdown: 2.34%; Profit Factor: 3.14.

Notes: Moving average crossovers and green bar patterns suited this bullish phase; 30-minute improved win rate and P&L by filtering weaker signals.

Bear Market (Jan 2022 - Jun 2022):

15-Minute: 262 long, 211 short; Win Rate: 44.4%; P&L: 239.80%; Drawdown: 3.74%; Profit Factor: 3.419.

30-Minute: 250 long, 200 short; Win Rate: 52.22%; P&L: 258.77%; Drawdown: 5.34%; Profit Factor: 3.461.

Notes: Red bar patterns and RSI shorts thrived in the downtrend; 30-minute cut choppy reversals for better consistency.

Flat Market (Jan 2021 - Jun 2021):

15-Minute: 280 long, 208 short; Win Rate: 51.84%; P&L: 340.33%; Drawdown: 9.59%; Profit Factor: 2.924.

30-Minute: 270 long, 209 short; Win Rate: 55.11%; P&L: 315.42%; Drawdown: 7.21%; Profit Factor: 2.598.

Notes: High trade frequency and P&L showed strength in ranges; 30-minute lowered drawdown for better risk control.

Results reflect historical performance on BTC/USDT with default settings—users should test on their assets and timeframes. Past performance does not guarantee future results and is shared only to illustrate the strategy’s behavior.

Why It Works Well in Flat Markets

A "flat market" lacks strong directional trends, with price oscillating around moving averages, as in Jan 2021 - Jun 2021 for BTC/USDT. This strategy excels here because its crossover-based entries trigger frequently in tight ranges. In trending markets, an exit might not be followed by a new entry without a pullback, but flat markets produce multiple crossovers, enabling more trades. ATR-based TP/SL and trailing stops capture these small swings, while RSI and volume filters ensure momentum, driving high P&L and win rates.

Technical Details

Built in Pine Script v6 for TradingView compatibility.

Prevents overlapping trades with long/short checks.

Handles edge cases like zero division and auto-detects the trading pair’s base currency (e.g., BTC from BTCUSDT).

This strategy suits scalpers seeking structured entries and risk management. Test on 15-minute or 30-minute charts to match your style and market conditions.

QuantJazz Turbine Trader BETA v1.17QuantJazz Turbine Trader BETA v1.17 - Strategy Introduction and User Guide

Strategy Introduction

Welcome to the QuantJazz Turbine Trader BETA v1.17, a comprehensive trading strategy designed for TradingView. This strategy is built upon oscillator principles, drawing inspiration from the Turbo Oscillator by RedRox, and incorporates multiple technical analysis concepts including RSI, MFI, Stochastic oscillators, divergence detection, and an optional FRAMA (Fractal Adaptive Moving Average) filter.

The Turbine Trader aims to provide traders with a flexible toolkit for identifying potential entry and exit points in the market. It presents information through a main signal line oscillator, a histogram, and various visual cues like dots, triangles, and divergence lines directly on the indicator panel. The strategy component allows users to define specific conditions based on these visual signals to trigger automated long or short trades within the TradingView environment.

This guide provides an overview of the strategy's components, settings, and usage. Please remember that this is a BETA version (v1.17). While developed with care, it may contain bugs or behave unexpectedly.

LEGAL DISCLAIMER: QuantJazz makes no claims about the fitness or profitability of this tool. Trading involves significant risk, and you may lose all of your invested capital. All trading decisions made using this strategy are solely at the user's discretion and responsibility. Past performance is not indicative of future results. Always conduct thorough backtesting and risk assessment before deploying any trading strategy with real capital.

This work is licensed under Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International.

Core Concepts and Visual Elements

The Turbine Trader indicator displays several components in its own panel below the main price chart:

1. Signal Line (Avg & Avg2): This is the primary oscillator. It's a composite indicator derived from RSI, MFI (Money Flow Index), and Stochastic calculations, smoothed using an EMA (Exponential Moving Average).

Avg: The faster smoothed signal line.

Avg2: The slower smoothed signal line.

Color Coding: The space between Avg and Avg2 is filled. The color (Neon Blue/gColor or Neon Purple/rColor) indicates the trend based on the relationship between Avg and Avg2. Blue suggests bullish momentum (Avg > Avg2), while Purple suggests bearish momentum (Avg2 > Avg).

Zero Line Crosses: Crossovers of the Avg line with the zero level can indicate shifts in momentum.

2. Histogram (resMfi): This histogram is based on smoothed and transformed MFI calculations (Fast MFI and Slow MFI).

Color Coding: Bars are colored Neon Blue (histColorUp) when above zero, suggesting bullish pressure, and Neon Purple (histColorDn) when below zero, suggesting bearish pressure. Transparency is applied.

Zero Line Crosses: Crossovers of the histogram with the zero level can signal potential shifts in money flow.

3. Reversal Points (Dots): Dots appear on the Signal Line (specifically on Avg2) when the color changes (i.e., Avg crosses Avg2).

Small Dots: Appear when a reversal occurs while the oscillator is in an "extreme" zone (below -60 for bullish reversals, above +60 for bearish reversals).

Large Dots: Appear when a reversal occurs outside of these extreme zones.

Colors: Blue (gRdColor) for bullish reversals (Avg crossing above Avg2), Purple (rRdColor) for bearish reversals (Avg crossing below Avg2).

4. Take Profit (TP) Signals (Triangles): Small triangles appear above (+120) or below (-120) the zero line.

Bearish Triangle (Down, Purple rTpColor): Suggests a potential exit point for long positions or an entry point for short positions, based on the oscillator losing upward momentum above the 50 level.

Bullish Triangle (Up, Blue gTpColor): Suggests a potential exit point for short positions or an entry point for long positions, based on the oscillator losing downward momentum below the -50 level.

5. Divergence Lines: The strategy automatically detects and draws potential regular and hidden divergences between the price action (highs/lows) and the Signal Line (Avg).

Regular Bullish Divergence (White bullDivColor line, ⊚︎ label): Price makes a lower low, but the oscillator makes a higher low. Suggests potential bottoming.

Regular Bearish Divergence (White bearDivColor line, ⊚︎ label): Price makes a higher high, but the oscillator makes a lower high. Suggests potential topping.

Hidden Bullish Divergence (bullHidDivColor line, ⊚︎ label): Price makes a higher low, but the oscillator makes a lower low. Suggests potential continuation of an uptrend.

Hidden Bearish Divergence (bearHidDivColor line, ⊚︎ label): Price makes a lower high, but the oscillator makes a higher high. Suggests potential continuation of a downtrend.

Delete Broken Divergence Lines: If enabled, newer divergence lines originating from a similar point will replace older ones.

6. Status Line: A visual bar at the top (95 to 105) and bottom (-95 to -105) of the indicator panel. Its color intensity reflects the confluence of signals:

Score Calculation: +1 if Avg > Avg2, +1 if Avg > 0, +1 if Histogram > 0.

Top Bar (Bullish): Bright Blue (gStatColor) if score is 3, Faded Blue if score is 2, Black otherwise.

Bottom Bar (Bearish): Bright Purple (rStatColor) if score is 0, Faded Purple if score is 1, Black otherwise.

Strategy Settings Explained

The strategy's behavior is controlled via the settings panel (gear icon).

1. Date Range:

Start Date, End Date: Define the period for backtesting. Trades will only occur within this range.

2. Optional Webhook Configuration: (For Automation)

3C Email Token, 3C Bot ID: Enter your 3Commas API credentials if you plan to automate trading using webhooks. The strategy generates JSON alert messages compatible with 3Commas. You can go ahead and just leave the text field as defaulted, "TOKEN HERE" / "BOT ID HERE" if not using any bot automations at this time. You can always come back later and automate it. More info can be made available from QuantJazz should you need automation assistance with custom indicators and trading strategies.

3. 🚀 Signal Line:

Turn On/Off: Show or hide the main signal lines (Avg, Avg2).

gColor, rColor: Set the colors for bullish and bearish signal line states.

Length (RSI): The lookback period for the internal RSI calculation. Default is 2.

Smooth (EMA): The smoothing period for the EMAs applied to the composite signal. Default is 9.

RSI Source: The price source used for RSI calculation (default: close).

4. 📊 Histogram:

Turn On/Off: Show or hide the histogram.

histColorUp, histColorDn: Set the colors for positive and negative histogram bars.

Length (MFI): The base lookback period for MFI calculations. Default is 5. Fast and Slow MFI lengths are derived from this.

Smooth: Smoothing period for the final histogram output. Default is 1 (minimal smoothing).

5.💡 Other:

Show Divergence Line: Toggle visibility of regular divergence lines.

bullDivColor, bearDivColor: Colors for regular divergence lines.

Show Hidden Divergence: Toggle visibility of hidden divergence lines.

bullHidDivColor, bearHidDivColor: Colors for hidden divergence lines.

Show Status Line: Toggle visibility of the top/bottom status bars.

gStatColor, rStatColor: Colors for the status line bars.

Show TP Signal: Toggle visibility of the TP triangles.

gTpColor, rTpColor: Colors for the TP triangles.

Show Reversal points: Toggle visibility of the small/large dots on the signal line.

gRdColor, rRdColor: Colors for the reversal dots.

Delete Broken Divergence Lines: Enable/disable automatic cleanup of older divergence lines.

6. ⚙️ Strategy Inputs: (CRITICAL for Trade Logic)

This section defines which visual signals trigger trades. Each signal (Small/Large Dots, TP Triangles, Bright Bars, Signal/Histogram Crosses, Signal/Histogram Max/Min, Divergences) has a dropdown menu:

Long: This signal can trigger a long entry.

Short: This signal can trigger a short entry.

Disabled: This signal will not trigger any entry.

Must Be True Checkbox: If checked for a specific signal, that signal's condition must be met for any trade (long or short, depending on the dropdown selection for that signal) to be considered. Multiple "Must Be True" conditions act as AND logic – all must be true simultaneously.

How it Works:

The strategy first checks if all conditions marked as "Must Be True" (for the relevant trade direction - long or short) are met.

If all "Must Be True" conditions are met, it then checks if at least one of the conditions not marked as "Must Be True" (and set to "Long" or "Short" respectively) is also met.

If both steps pass, and other filters (like Date Range, FRAMA) allow, an entry order is placed.

Example: If "Large Bullish Dot" is set to "Long" and "Must Be True" is checked, AND "Bullish Divergence" is set to "Long" but "Must Be True" is not checked: A long entry requires BOTH the Large Bullish Dot AND the Bullish Divergence to occur simultaneously. If "Large Bullish Dot" was "Long" but not "Must Be True", then EITHER a Large Bullish Dot OR a Bullish Divergence could trigger a long entry (assuming no other "Must Be True" conditions are active).

Note: By default, the strategy is configured for long-only trades (strategy.risk.allow_entry_in(strategy.direction.long)). To enable short trades, you would need to comment out or remove this line in the Pine Script code and configure the "Strategy Inputs" accordingly.

7. 💰 Take Profit Settings:

Take Profit 1/2/3 (%): The percentage above the entry price (for longs) or below (for shorts) where each TP level is set. (e.g., 1.0 means 1% profit).

TP1/2/3 Percentage: The percentage of the currently open position to close when the corresponding TP level is hit. The percentages should ideally sum to 100% if you intend to close the entire position across the TPs.

Trailing Stop (%): The percentage below the highest high (for longs) or above the lowest low (for shorts) reached after the activation threshold, where the stop loss will trail.

Trailing Stop Activation (%): The minimum profit percentage the trade must reach before the trailing stop becomes active.

Re-entry Delay (Bars): The minimum number of bars to wait after a TP is hit before considering a re-entry. Default is 1 (allows immediate re-entry on the next bar if conditions met).

Re-entry Price Offset (%): The percentage the price must move beyond the previous TP level before a re-entry is allowed. This prevents immediate re-entry if the price hovers around the TP level.

8. 📈 FRAMA Filter: (Optional Trend Filter)

Use FRAMA Filter: Enable or disable the filter.

FRAMA Source, FRAMA Period, FRAMA Fast MA, FRAMA Slow MA: Parameters for the FRAMA calculation. Defaults provided are common starting points.

FRAMA Filter Type:

FRAMA > previous bars: Allows trades only if FRAMA is significantly above its recent average (defined by FRAMA Percentage and FRAMA Lookback). Typically used to confirm strong upward trends for longs.

FRAMA < price: Allows trades only if FRAMA is below the current price (framaSource). Can act as a baseline trend filter.

FRAMA Percentage (X), FRAMA Lookback (Y): Used only for the FRAMA > previous bars filter type.

How it Affects Trades: If Use FRAMA Filter is enabled:

Long entries require the FRAMA filter condition to be true.

Short entries require the FRAMA filter condition to be false (as currently coded, this acts as an inverse filter for shorts if enabled).

How to Use the Strategy

1. Apply to Chart: Open your desired chart on TradingView. Click "Indicators", find "QuantJazz Turbine Trader BETA v1.17" (you might need to add it via Invite-only scripts or if published publicly), and add it to your chart. The oscillator appears below the price chart, and the strategy tester panel opens at the bottom.

2. Configure Strategy Properties: In the Pine Script code itself (or potentially via the UI if supported), adjust the strategy() function parameters like initial_capital, default_qty_value, commission_value, slippage, etc., to match your account, broker fees, and risk settings. The user preferences provided (e.g., 1000 initial capital, 0.1% commission) are examples. Remember use_bar_magnifier is false by default in v1.17.

3. Configure Inputs (Settings Panel):

Set the Date Range for backtesting.

Crucially, configure the ⚙️ Strategy Inputs. Decide which signals should trigger entries and whether they are mandatory ("Must Be True"). Start simply, perhaps enabling only one or two signals initially, and test thoroughly. Remember the default long-only setting unless you modify the code.

Set up your 💰 Take Profit Settings, including TP levels, position size percentages for each TP, and the trailing stop parameters. Decide if you want to use the re-entry feature.

Decide whether to use the 📈 FRAMA Filter and configure its parameters if enabled.

Adjust visual elements (🚀 Signal Line, 📊 Histogram, 💡 Other) as needed for clarity.

4. Backtest: Use the Strategy Tester panel in TradingView. Analyze the performance metrics (Net Profit, Max Drawdown, Profit Factor, Win Rate, Trade List) across different assets, timeframes, and setting configurations. Pay close attention to how different "Strategy Inputs" combinations perform.

5. Refine: Based on backtesting results, adjust the input settings, TP/SL strategy, and signal combinations to optimize performance for your chosen market and timeframe, while being mindful of overfitting.

6. Automation (Optional): If using 3Commas or a similar platform:

Enter your 3C Email Token and 3C Bot ID in the settings.

Create alerts in TradingView (right-click on the chart or use the Alert panel).

Set the Condition to "QuantJazz Turbine Trader BETA v1.17".

In the "Message" box, paste the corresponding placeholder, which will pass the message in JSON from our custom code to TradingView to pass through your webhook: {{strategy.order.alert_message}}.

In the next tab, configure the Webhook URL provided by your automation platform. Put a Whale sound, while you're at it! 🐳

When an alert triggers, TradingView will send the pre-formatted JSON message from the strategy code to your webhook URL.

Final Notes

The QuantJazz Turbine Trader BETA v1.17 offers a wide range of customizable signals and strategy logic. Its effectiveness heavily depends on proper configuration and thorough backtesting specific to the traded asset and timeframe. Start with the default settings, understand each component, and methodically test different combinations of signals and parameters. Remember the inherent risks of trading and never invest capital you cannot afford to lose.

Bull Flag (9:30-12:00 Only) [One-Liner Fix]🚀 Bull Flag Breakout Strategy | Intraday Momentum (9:30-12:00) 🔥📈

💡 Designed for Intraday Traders who love momentum breakouts and want to automate Bull Flag setups with volume confirmation! This strategy detects strong bullish moves, measures pullbacks, and triggers trades when the first candle makes a new high—ensuring maximum momentum.

⸻

🏆 Why This Strategy?

✅ Bull Flag Pattern Automation – No need to manually spot pullbacks! 🎯

✅ Smart Volume Confirmation – Only enter trades when breakout volume is strong! 📊

✅ Morning Session Focused (9:30 - 12:00 EST) – Trade when momentum is at its peak! ⏰

✅ Customizable ATR & Risk Settings – Adjust pullback %, stop-loss, and take-profit! 🛠️

✅ Backtest-Friendly – See how the strategy performs over time! 🔍

⸻

🎯 How It Works

📌 Step 1: Detects a Bullish Impulse Bar

🔹 Large green candle 🚀

🔹 Candle range > ATR multiplier

🔹 Volume > Average volume threshold

📌 Step 2: Confirms a Valid Pullback

🔸 Pullback must stay within % range of the impulse move 📉

🔸 If the pullback is too deep or takes too long, the setup is ignored ⛔

📌 Step 3: First Candle to Make a New High 📈

🔹 When a candle breaks the previous high and volume confirms, go long! 💰

🔹 Stop-Loss set at pullback low

🔹 Take-Profit at Risk:Reward (R:R) Target 🎯

⸻

🔥 Best For

💎 Scalpers & Day Traders – Capture short-term breakout momentum! ⚡

📊 Backtesters – Optimize ATR, volume, and pullback rules for best performance! 🧪

⏳ Morning Momentum Traders – Focus on 9:30-12:00 AM EST for higher probability setups!

⸻

🚨 Important Notes

🔹 This strategy is not financial advice! 📜

🔹 Always backtest & paper trade before using real money! 📉📈

🔹 Volatility varies – Customize settings based on your trading style! 🔧

🚀 Like this script? Give it a try & let us know how it works for you! 🔥👊

⸻

IU BBB(Big Body Bar) StrategyDESCRIPTION

The IU BBB (Big Body Bar) Strategy is a price action-based trading strategy that identifies high-momentum candles with significantly larger body sizes compared to the average. It enters trades when a strong bullish or bearish move occurs and manages risk using an ATR-based trailing stop-loss system.

USER INPUTS:

- Big Body Threshold – Defines how many times larger the candle body should be compared to the average body ( default is 4 ).

- ATR Length – The period for the Average True Range (ATR) used in the trailing stop-loss calculation ( default is 14 ).

- ATR Factor – Multiplier for ATR to determine the trailing stop distance ( default is 2 ).

LONG CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is higher than the opening price (bullish candle).

SHORT CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is lower than the opening price (bearish candle).

LONG EXIT:

- ATR-based trailing stop-loss dynamically adjusts, locking in profits as the price moves higher.

SHORT EXIT:

- ATR-based trailing stop-loss dynamically adjusts, securing profits as the price moves lower.

WHY IT IS UNIQUE:

- Unlike traditional momentum strategies, this system adapts to volatility by filtering trades based on relative candle size.

- It incorporates an ATR-based trailing stop-loss, ensuring risk management and profit protection.

- The strategy avoids choppy market conditions by only trading when significant momentum is present.

HOW USERS CAN BENEFIT FROM IT:

- Catch Strong Price Moves – The strategy helps traders enter trades when the market shows decisive momentum.

- Effective Risk Management – The ATR-based trailing stop ensures that winning trades remain profitable.

- Works Across Markets – Can be applied to stocks, forex, crypto, and indices with proper optimization.

- Fully Customizable – Users can adjust sensitivity settings to match their trading style and time frame.

Pure Price Action StrategyTest Price Action Strategy from Lux Pure Price Action Indicator

How This Strategy Works:

Recognizing Trends & Reversals:

Break of Structure (BOS): A bullish signal indicating a trend continuation.

Market Structure Shift (MSS): A bearish signal indicating a potential reversal.

Analyzing Market Momentum:

It uses recent highs and lows to confirm whether the price is making higher highs (bullish) or lower lows (bearish).

Customizing Visualization Styles:

Buy signals (BUY Signal) are plotted as green upward arrows.

Sell signals (SELL Signal) are plotted as red downward arrows.

Stop-Loss (SL) & Take-Profit (TP): Configurable via percentage input.

Sniper Trade Pro (ES 15-Min) - Topstep Optimized🔹 Overview

Sniper Trade Pro is an advanced algorithmic trading strategy designed specifically for E-mini S&P 500 (ES) Futures on the 15-minute timeframe. This strategy is optimized for Topstep 50K evaluations, incorporating strict risk management to comply with their max $1,000 daily loss limit while maintaining a high probability of success.

It uses a multi-confirmation approach, integrating:

✅ Money Flow Divergence (MFD) → To track liquidity imbalances and institutional accumulation/distribution.

✅ Trend Confirmation (EMA + VWAP) → To identify strong trend direction and avoid choppy markets.

✅ ADX Strength Filter → To ensure entries only occur in trending conditions, avoiding weak setups.

✅ Break-Even & Dynamic Stop-Losses → To reduce drawdowns and protect profits dynamically.

This script automatically generates Buy and Sell signals and provides built-in risk management for automated trading execution through TradingView Webhooks.

🔹 How Does This Strategy Work?

📌 1. Trend Confirmation (EMA + VWAP)

The strategy uses:

✔ 9-EMA & 21-EMA: Fast-moving averages to detect short-term momentum.

✔ VWAP (Volume-Weighted Average Price): Ensures trades align with institutional volume flow.

How it works:

Bullish Condition: 9-EMA above 21-EMA AND price above VWAP → Confirms buy trend.

Bearish Condition: 9-EMA below 21-EMA AND price below VWAP → Confirms sell trend.

📌 2. Liquidity & Money Flow Divergence (MFD)

This indicator measures liquidity shifts by tracking momentum changes in price and volume.

✔ MFD Calculation:

Uses Exponential Moving Average (EMA) of Momentum (MOM) to detect changes in buying/selling pressure.

If MFD is above its moving average, it signals liquidity inflows → bullish strength.

If MFD is below its moving average, it signals liquidity outflows → bearish weakness.

Why is this important?

Detects when Smart Money is accumulating or distributing before major moves.

Filters out false breakouts by confirming momentum strength before entry.

📌 3. Trade Entry Triggers (Candlestick Patterns & ADX Filter)

To avoid random entries, the strategy waits for specific candlestick confirmations with ADX trend strength:

✔ Bullish Entry (Buy Signal) → Requires:

Bullish Engulfing Candle (Reversal confirmation)

ADX > 20 (Ensures strong trending conditions)

MFD above its moving average (Liquidity inflows)

9-EMA > 21-EMA & price above VWAP (Trend confirmation)

✔ Bearish Entry (Sell Signal) → Requires:

Bearish Engulfing Candle (Reversal confirmation)

ADX > 20 (Ensures strong trending conditions)

MFD below its moving average (Liquidity outflows)

9-EMA < 21-EMA & price below VWAP (Trend confirmation)

📌 4. Risk Management & Profit Protection

This strategy is built with strict risk management to maintain low drawdowns and maximize profits:

✔ Dynamic Position Sizing → Automatically adjusts trade size to risk a fixed $400 per trade.

✔ Adaptive Stop-Losses → Uses ATR-based stop-loss (0.8x ATR) to adapt to market volatility.

✔ Take-Profit Targets → Fixed at 2x ATR for a Risk:Reward ratio of 2:1.

✔ Break-Even Protection → Moves stop-loss to entry once price moves 1x ATR in profit, locking in gains.

✔ Max Daily Loss Limit (-$1,000) → Stops trading if total losses exceed $1,000, complying with Topstep rules.

Balance of Power for US30 4H [PineIndicators]The Balance of Power (BoP) Strategy is a momentum-based trading system for the US30 index on a 4-hour timeframe. It measures the strength of buyers versus sellers in each candle using the Balance of Power (BoP) indicator and executes trades based on predefined threshold crossovers. The strategy includes dynamic position sizing, adjustable leverage, and visual trade tracking.

⚙️ Core Strategy Mechanics

Positive values indicate buying strength.

Negative values indicate selling strength.

Values close to 1 suggest strong bullish momentum.

Values close to -1 indicate strong bearish pressure.

The strategy uses fixed threshold crossovers to determine trade entries and exits.

📌 Trade Logic

Entry Conditions

Long Entry: When BoP crosses above 0.8, signaling strong buying pressure.

Exit Conditions

Position Close: When BoP crosses below -0.8, indicating a shift to selling pressure.

This threshold-based system filters out low-confidence signals and focuses on high-momentum shifts.

📏 Position Sizing & Leverage

Leverage: Adjustable by the user (default = 5x).

Risk Management: Position size adapts dynamically based on equity fluctuations.

📊 Trade Visualization & History Tracking

Trade Markers:

"Buy" labels appear when a long position is opened.

"Close" labels appear when a position is exited.

Trade History Boxes:

Green for profitable trades.

Red for losing trades.

These elements provide clear visual tracking of past trade execution.

⚡ Usage & Customization

1️⃣ Apply the script to a US30 4H chart in TradingView.

2️⃣ Adjust leverage settings as needed.

3️⃣ Review trade signals and historical performance with visual markers.

4️⃣ Enable backtesting to evaluate past performance.

This strategy is designed for momentum-based trading and is best suited for volatile market conditions.

TSI Long/Short for BTC 2HThe TSI Long/Short for BTC 2H strategy is an advanced trend-following system designed specifically for trading Bitcoin (BTC) on a 2-hour timeframe. It leverages the True Strength Index (TSI) to identify momentum shifts and executes both long and short trades in response to dynamic market conditions.

Unlike traditional moving average-based strategies, this script uses a double-smoothed momentum calculation, enhancing signal accuracy and reducing noise. It incorporates automated position sizing, customizable leverage, and real-time performance tracking, ensuring a structured and adaptable trading approach.

🔹 What Makes This Strategy Unique?

Unlike simple crossover strategies or generic trend-following approaches, this system utilizes a customized True Strength Index (TSI) methodology that dynamically adjusts to market conditions.

🔸 True Strength Index (TSI) Filtering – The script refines the TSI by applying double exponential smoothing, filtering out weak signals and capturing high-confidence momentum shifts.

🔸 Adaptive Entry & Exit Logic – Instead of fixed thresholds, it compares the TSI value against a dynamically determined high/low range from the past 100 bars to confirm trade signals.

🔸 Leverage & Risk Optimization – Position sizing is dynamically adjusted based on account equity and leverage settings, ensuring controlled risk exposure.

🔸 Performance Monitoring System – A built-in performance tracking table allows traders to evaluate monthly and yearly results directly on the chart.

📊 Core Strategy Components

1️⃣ Momentum-Based Trade Execution

The strategy generates long and short trade signals based on the following conditions:

✅ Long Entry Condition – A buy signal is triggered when the TSI crosses above its 100-bar highest value (previously set), confirming bullish momentum.

✅ Short Entry Condition – A sell signal is generated when the TSI crosses below its 100-bar lowest value (previously set), indicating bearish pressure.

Each trade execution is fully automated, reducing emotional decision-making and improving trading discipline.

2️⃣ Position Sizing & Leverage Control

Risk management is a key focus of this strategy:

🔹 Dynamic Position Sizing – The script calculates position size based on:

Account Equity – Ensuring trade sizes adjust dynamically with capital fluctuations.

Leverage Multiplier – Allows traders to customize risk exposure via an adjustable leverage setting.

🔹 No Fixed Stop-Loss – The strategy relies on reversals to exit trades, meaning each position is closed when the opposite signal appears.

This design ensures maximum capital efficiency while adapting to market conditions in real time.

3️⃣ Performance Visualization & Tracking

Understanding historical performance is crucial for refining strategies. The script includes:

📌 Real-Time Trade Markers – Buy and sell signals are visually displayed on the chart for easy reference.

📌 Performance Metrics Table – Tracks monthly and yearly returns in percentage form, helping traders assess profitability over time.

📌 Trade History Visualization – Completed trades are displayed with color-coded boxes (green for long trades, red for short trades), visually representing profit/loss dynamics.

📢 Why Use This Strategy?

✔ Advanced Momentum Detection – Uses a double-smoothed TSI for more accurate trend signals.

✔ Fully Automated Trading – Removes emotional bias and enforces discipline.

✔ Customizable Risk Management – Adjust leverage and position sizing to suit your risk profile.

✔ Comprehensive Performance Tracking – Integrated reporting system provides clear insights into past trades.

This strategy is ideal for Bitcoin traders looking for a structured, high-probability system that adapts to both bullish and bearish trends on the 2-hour timeframe.

📌 How to Use: Simply add the script to your 2H BTC chart, configure your leverage settings, and let the system handle trade execution and tracking! 🚀

FRAMA-LRO📌 FRAMA × LRO Auto-Trading Strategy - Adaptive Trend & Momentum System

Overview

This Pine Script provides an automated trading strategy that combines FRAMA (Fractal Adaptive Moving Average) and LRO (Linear Regression Oscillator) to enhance trend detection and momentum analysis. Unlike traditional moving averages, FRAMA dynamically adjusts to price volatility, while LRO effectively measures momentum for high-precision entries.

📌 Key Features

1. Dynamic Trend & Momentum Synergy

FRAMA: Detects price trends by adjusting to market conditions using fractal dimensions.

LRO: Filters trades based on linear regression slope momentum.

Breakout Confirmation: Entry is validated when price breaks FRAMA bands with LRO support.

2. Realistic Backtesting Settings

Initial Capital: $5,000 (more in line with retail traders).

Risk Management: 5% equity per trade.

Slippage & Commission: Adjusted to realistic values (1 pip slippage, 94 pips spread per trade).

Backtest Data: Covers at least 100 trades for statistical significance.

3. Clear Trade Logic

Long Entry: Price breaks above FRAMA upper band & LRO > 0.

Short Entry: Price breaks below FRAMA lower band & LRO < 0.

Stop-Loss: Dynamic ATR-based calculation.

Take-Profit: Fixed risk-reward ratio (1:2).

📌 How It Works

The system identifies trend strength with FRAMA, then confirms momentum shifts with LRO before executing trades. This ensures higher accuracy and filters false breakouts.

📌 Visual Aids for Clarity

Color-Coded Candles:

🟢 Uptrend (LRO > 0)

🔵 Downtrend (LRO < 0)

⚪ Neutral (LRO ≈ 0)

Chart Annotations: Clearly marked trade signals for easy reference.

📌 Risk Management & Automation

Fully automated execution of entries, stop-loss, and take-profit.

ATR-based volatility adaptation for dynamic SL adjustments.

Customizable parameters (period, volatility settings, risk percentage).

📌 Originality & Enhancements

This script is not just a combination of FRAMA & LRO, but an optimized system designed to:

Improve signal accuracy using adaptive trend detection.

Eliminate noise with LRO-based momentum filtering.

Implement dynamic risk management via ATR-based SL.

Influences & Acknowledgments

This strategy builds on methodologies inspired by ChartPrime and BigBeluga, refining their concepts for a systematic approach.

📌 Disclaimer

This script is for educational purposes only. Past performance does not guarantee future results. Always manage risk appropriately.

Volatility-Adjusted Rate of Change (VARC) ModelThe Volatility-Adjusted Rate of Change (VARC) Model is a dynamic trading strategy designed to identify potential market opportunities by incorporating volatility and skewness data. The model relies on the CBOE Skew Index (CBOE:SKEW) and adjusts the traditional Rate of Change (ROC) indicator based on market volatility, offering a more refined approach to trading based on price momentum.

1. CBOE Skew Index (SKEW) and ROC Calculation

At its core, the VARC model uses the CBOE Skew Index as a measure of market sentiment. The SKEW index represents the perceived risk of extreme negative movements in the S&P 500, providing insight into the balance of risks in the market (CBOE, 2021). This sentiment-based index is often used by traders and analysts to gauge the likelihood of a market downturn.

The Rate of Change (ROC) is applied to the Skew Index, calculated over a specified lookback period (rocLength = 29). The ROC measures the percentage change in price from one period to another and is widely used to gauge the momentum of an asset (Chande & Kroll, 1994). In the VARC model, the ROC of the Skew Index is employed to assess shifts in market sentiment that may signal turning points or potential volatility.

2. Volatility Adjustment

Volatility plays a significant role in market behavior and risk management. The VARC model uses a volatility-adjusted threshold to dynamically adjust the sensitivity of the trading signals. This is achieved by calculating the standard deviation of the ROC over a defined volatility lookback period (volatilityLookback = 20) and applying a volatility multiplier (volatilityMultiplier = 1.5). These parameters define upper and lower thresholds for trade entry and exit.

The model adjusts the sensitivity of the ROC signals based on market volatility, ensuring that the strategy adapts to changing market conditions. When volatility is high, the thresholds are widened, allowing the model to filter out noise and avoid unnecessary trades. Conversely, during periods of low volatility, the thresholds tighten, enabling the model to capture smaller price movements.

3. Entry and Exit Conditions

The VARC model generates trading signals based on the behavior of the ROC relative to the dynamically adjusted volatility thresholds. A long position is initiated when the ROC crosses below the lower threshold, indicating that the market is becoming oversold or showing signs of excessive pessimism. The position is closed when the ROC exceeds the upper threshold, signaling a potential reversal or a return to normal market conditions. These entry and exit conditions are defined as follows:

• Long Condition: The ROC is below the lower threshold (roc < dynamicThresholdLow).

• Exit Condition: The ROC is above the upper threshold (roc > dynamicThresholdHigh).

This approach provides a systematic method for entering and exiting positions based on volatility-adjusted momentum, helping traders to capitalize on shifts in market sentiment.

4. Visualization and Signal Highlighting

The model includes several visual aids to help traders interpret the signals. The ROC, dynamic thresholds, and a zero line are plotted on the chart to provide a clear representation of market momentum and the current trading range. Furthermore, a background color is used to highlight periods when a position is open, visually reinforcing the model’s decisions.

5. Conclusion

The VARC model offers a robust framework for trading by combining momentum (through the ROC) with a volatility-adjusted approach that refines trade signals based on market conditions. The use of the CBOE Skew Index adds an additional layer of market sentiment analysis, providing context to the ROC values. This volatility-adaptive strategy offers traders a more nuanced way to navigate the markets, making it suitable for both short-term and longer-term trading horizons.

References:

• CBOE. (2021). CBOE Skew Index (SKEW). Chicago Board Options Exchange. Retrieved from www.cboe.com

• Chande, T., & Kroll, J. (1994). The New Technical Trader: Boost Your Profit by Plugging into the Latest Indicators. Wiley.

This model can be particularly useful in volatile markets, where traditional fixed thresholds may not perform as well. By adjusting the thresholds dynamically based on the underlying volatility, the VARC model offers a more flexible and responsive approach to market trading.

Bullish Reversal Bar Strategy [Skyrexio]Overview

Bullish Reversal Bar Strategy leverages the combination of candlestick pattern Bullish Reversal Bar (description in Methodology and Justification of Methodology), Williams Alligator indicator and Williams Fractals to create the high probability setups. Candlestick pattern is used for the entering into trade, while the combination of Williams Alligator and Fractals is used for the trend approximation as close condition. Strategy uses only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator or the candlestick pattern invalidation to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Trend Trade Filter: strategy uses Alligator and Fractal combination as high probability trend filter.

Methodology

The strategy opens long trade when the following price met the conditions:

1.Current candle's high shall be below the Williams Alligator's lines (Jaw, Lips, Teeth)(all details in "Justification of Methodology" paragraph)

2.Price shall create the candlestick pattern "Bullish Reversal Bar". Optionally if MFI and AO filters are enabled current candle shall have the decreasing AO and at least one of three recent bars shall have the squat state on the MFI (all details in "Justification of Methodology" paragraph)

3.If price breaks through the high of the candle marked as the "Bullish Reversal Bar" the long trade is open at the price one tick above the candle's high

4.Initial stop loss is placed at the Bullish Reversal Bar's candle's low

5.If price hit the Bullish Reversal Bar's low before hitting the entry price potential trade is cancelled

6.If trade is active and initial stop loss has not been hit, trade is closed when the combination of Alligator and Williams Fractals shall consider current trend change from upward to downward.

Strategy settings

In the inputs window user can setup strategy setting:

Enable MFI (if true trades are filtered using Market Facilitation Index (MFI) condition all details in "Justification of Methodology" paragraph), by default = false)

Enable AO (if true trades are filtered using Awesome Oscillator (AO) condition all details in "Justification of Methodology" paragraph), by default = false)

Justification of Methodology

Let's explore the key concepts of this strategy and understand how they work together. The first and key concept is the Bullish Reversal Bar candlestick pattern. This is just the single bar pattern. The rules are simple:

Candle shall be closed in it's upper half

High of this candle shall be below all three Alligator's lines (Jaw, Lips, Teeth)

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

Fractals, another tool by Bill Williams, help identify potential reversal points on a price chart. A fractal forms over at least five consecutive bars, with the middle bar showing either:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often use fractals alongside other indicators to confirm trends or reversals, enhancing decision-making accuracy.

How do these tools work together in this strategy? Let’s consider an example of an uptrend.

When the price breaks above an up fractal, it signals a potential bullish trend. This occurs because the up fractal represents a shift in market behavior, where a temporary high was formed due to selling pressure. If the price revisits this level and breaks through, it suggests the market sentiment has turned bullish.

The breakout must occur above the Alligator’s teeth line to confirm the trend. A breakout below the teeth is considered invalid, and the downtrend might still persist. Conversely, in a downtrend, the same logic applies with down fractals.

How we can use all these indicators in this strategy? This strategy is a counter trend one. Candle's high shall be below all Alligator's lines. During this market stage the bullish reversal bar candlestick pattern shall be printed. This bar during the downtrend is a high probability setup for the potential reversal to the upside: bulls were able to close the price in the upper half of a candle. The breaking of its high is a high probability signal that trend change is confirmed and script opens long trade. If market continues going down and break down the bullish reversal bar's low potential trend change has been invalidated and strategy close long trade.

If market really reversed and started moving to the upside strategy waits for the trend change form the downtrend to the uptrend according to approximation of Alligator and Fractals combination. If this change happens strategy close the trade. This approach helps to stay in the long trade while the uptrend continuation is likely and close it if there is a high probability of the uptrend finish.

Optionally users can enable MFI and AO filters. First of all, let's briefly explain what are these two indicators. The Awesome Oscillator (AO), created by Bill Williams, is a momentum-based indicator that evaluates market momentum by comparing recent price activity to a broader historical context. It assists traders in identifying potential trend reversals and gauging trend strength.

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

This indicator is filtering signals in the following way: if current AO bar is decreasing this candle can be interpreted as a bullish reversal bar. This logic is applicable because initially this strategy is a trend reversal, it is searching for the high probability setup against the current trend. Decreasing AO is the additional high probability filter of a downtrend.

Let's briefly look what is MFI. The Market Facilitation Index (MFI) is a technical indicator that measures the price movement per unit of volume, helping traders gauge the efficiency of price movement in relation to trading volume. Here's how you can calculate it:

MFI = (High−Low)/Volume

MFI can be used in combination with volume, so we can divide 4 states. Bill Williams introduced these to help traders interpret the interaction between volume and price movement. Here’s a quick summary:

Green Window (Increased MFI & Increased Volume): Indicates strong momentum with both price and volume increasing. Often a sign of trend continuation, as both buying and selling interest are rising.

Fake Window (Increased MFI & Decreased Volume): Shows that price is moving but with lower volume, suggesting weak support for the trend. This can signal a potential end of the current trend.

Squat Window (Decreased MFI & Increased Volume): Shows high volume but little price movement, indicating a tug-of-war between buyers and sellers. This often precedes a breakout as the pressure builds.

Fade Window (Decreased MFI & Decreased Volume): Indicates a lack of interest from both buyers and sellers, leading to lower momentum. This typically happens in range-bound markets and may signal consolidation before a new move.

For our purposes we are interested in squat bars. This is the sign that volume cannot move the price easily. This type of bar increases the probability of trend reversal. In this indicator we added to enable the MFI filter of reversal bars. If potential reversal bar or two preceding bars have squat state this bar can be interpret as a reversal one.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.12.31. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -5.29%

Maximum Single Profit: +29.99%

Net Profit: +5472.66 USDT (+54.73%)

Total Trades: 103 (33.98% win rate)

Profit Factor: 1.634

Maximum Accumulated Loss: 1231.15 USDT (-8.32%)

Average Profit per Trade: 53.13 USDT (+0.94%)

Average Trade Duration: 76 hours

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h ETH/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

Up Gap Strategy with DelayThis strategy, titled “Up Gap Strategy with Delay,” is based on identifying up gaps in the price action of an asset. A gap is defined as the percentage difference between the current bar’s open price and the previous bar’s close price. The strategy triggers a long position if the gap exceeds a user-defined threshold and includes a delay period before entering the position. After entering, the position is held for a set number of periods before being closed.

Key Features:

1. Gap Threshold: The strategy defines an up gap when the gap size exceeds a specified threshold (in percentage terms). The gap threshold is an input parameter that allows customization based on the user’s preference.

2. Delay Period: After the gap occurs, the strategy waits for a delay period before initiating a long position. This delay can help mitigate any short-term volatility that might occur immediately after the gap.

3. Holding Period: Once the position is entered, it is held for a user-defined number of periods (holdingPeriods). This is to capture the potential post-gap trend continuation, as gaps often indicate strong directional momentum.

4. Gap Plotting: The strategy visually plots up gaps on the chart by placing a green label beneath the bar where the gap condition is met. Additionally, the background color turns green to highlight up-gap occurrences.

5. Exit Condition: The position is exited after the defined holding period. The strategy ensures that the position is closed after this time, regardless of whether the price is in profit or loss.

Scientific Background:

The gap theory has been widely studied in financial literature and is based on the premise that gaps in price often represent areas of significant support or resistance. According to research by Kaufman (2002), gaps in price action can be indicators of future price direction, particularly when they occur after a period of consolidation or a trend reversal. Moreover, Gaps and their Implications in Technical Analysis (Murphy, 1999) highlights that gaps can reflect imbalances between supply and demand, leading to high momentum and potential price continuation or reversal.

In trading strategies, utilizing gaps with specific conditions, such as delay and holding periods, can enhance the ability to capture significant price moves. The strategy’s delay period helps avoid potential market noise immediately after the gap, while the holding period seeks to capitalize on the price continuation that often follows gap formation.