Candle Ribbon [UkutaLabs]The Candle Ribbon is a powerful trading tool that creates a strong ribbon that indicates market strength. This ribbon is created using three moving averages that use the candle values (high, low, open and close) as its input values.

The center most MA will also be colored green, red or grey depending on whether or not its direction aligns with current market strength.

The outer band lines act as range indicators, plotted above and below the center ribbon, which represent volatility boundaries for price action.

█ USAGE

The Candle Ribbon is created using a series of three moving averages that uses values from the candle as its inputs. The user has the ability to select whether the moving averages are EMAs or SMAs, as well as the ability to control the period of the moving averages.

If the moving average calculated using the Candle Open is below the moving average calculated using the Candle Close, the ribbon will be colored green, indicating a bullish trend. If the moving average calculated using the Candle Open is above the moving average calculated using the Candle Open, the ribbon will be colored red, indicating a bearish trend.

This indicator also uses a series of hidden EMAs to determine market strength. If these EMAs do not align with the direction of the Candle Ribbon, the middle MA will instead be colored grey, indicating uncertainty in the market, as well as a possible reversal.

█ SETTINGS

Configuration

• Moving Average Type: Determines whether or not the Candle Moving Averages will be drawn as EMAs or SMAs.

• Moving Average Period: Determines the period of the Candle Moving Averages.

Moving Average

• Moving Average Input: Determines the input values for the hidden EMAs.

Cari dalam skrip untuk "moving averages"

SyakDan FX (Clear Version)**SyakDan FX (Clear Version) - Indicator Description**

### Overview:

SyakDan FX (Clear Version) is a comprehensive TradingView indicator designed for account management, trend identification, and automated trading signals. This script utilizes multiple moving averages, ATR-based stop-loss calculations, and Fibonacci-based pivot points to assist traders in making informed trading decisions.

### Features:

1. **Account Management Calculation:**

- The indicator dynamically adapts to the current timeframe.

- Customizable moving average (MA) types, including EMA, SMA, WMA, and HMA.

- ATR-based trailing stop and volatility assessment.

2. **Moving Averages & Trend Identification:**

- Configurable EMA lengths for three different moving averages.

- Dynamic selection of MA types (SMA, EMA, WMA, HMA) for flexibility.

- Different EMA lengths for low and high timeframes.

- Automatic detection of EMA crossovers and trend changes.

3. **Entry, Stop-Loss, and Take-Profit Calculation:**

- Enables automatic calculation of entry, stop-loss, and take-profit levels.

- ATR-based stop-loss placement.

- Multi-level take-profit targets (TP1, TP2, TP3, and Max TP).

- Visual representation of SL/TP levels using dynamic lines and labels.

4. **Alerts & Notifications:**

- Alerts for EMA crossovers (Buy & Sell signals).

- Additional alerts when EMA 2 crosses EMA 3, indicating strong signals.

5. **Pivot Point Calculations:**

- Calculates daily and weekly pivot points using Fibonacci and traditional methods.

- Helps traders identify key support and resistance levels.

### How It Works:

- The indicator plots three customizable moving averages on the chart.

- It detects crossovers between these moving averages to identify potential buy and sell signals.

- ATR (Average True Range) is used to set dynamic stop-loss and take-profit levels.

- Traders can enable or disable automatic SL/TP plotting.

- Alerts notify users when key trade signals occur.

- Fibonacci and traditional pivot points provide additional confluence for trading decisions.

### Customization Options:

- **MA Type Selection:** Choose from SMA, EMA, WMA, or HMA for each moving average.

- **EMA Length Adjustments:** Modify the lengths for short-term and long-term trends.

- **SL/TP Settings:** Enable or disable SL/TP plotting and customize their multipliers.

- **Alert Preferences:** Enable or disable alerts for trend crossovers.

### Ideal Usage:

- Traders using trend-following strategies based on moving averages.

- Those who want automated SL/TP placement for risk management.

- Anyone looking to integrate pivot points into their trading decisions.

This indicator provides a clean, structured approach to trading with automated analysis, reducing the need for manual calculations while offering strong risk management tools.

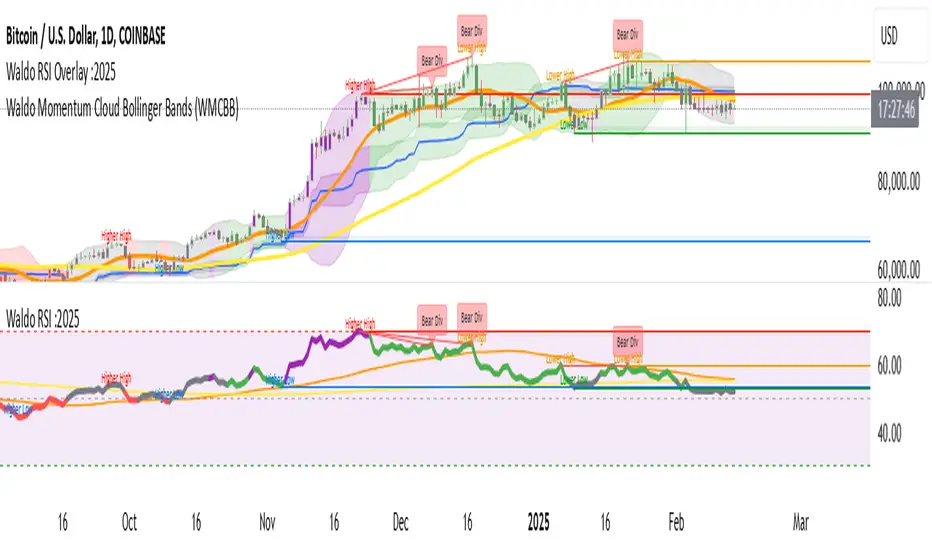

Waldo RSI :oWaldo RSI :o Indicator Guide

The Waldo RSI :o indicator is designed to complement the "Waldo RSI Overlay :o" by providing an RSI-based analysis on TradingView, focusing on macro shifts in market trends. Here's a comprehensive guide on how to use this indicator:

Key Features:

RSI Settings:

RSI Source: Choose from ON RSI, ON HIGH, ON LOW, ON CLOSE, or ON OPEN to determine how RSI calculates pivots.

RSI Settings:

Source: Default is (H+L)/2, but you can select any price for RSI calculation.

Length: Default RSI length is 7, which can be adjusted for sensitivity.

Trend Lines:

Show Trend Lines: Option to display trend lines based on RSI pivot points.

Zigzag Length: Determines pivot point sensitivity.

Confirm Length: Validates pivot points (default is 3).

Colors: Customize colors for Higher Highs (HH), Lower Highs (LH), Higher Lows (HL), and Lower Lows (LL) on the RSI.

Label Size and Line Width: Adjust the appearance of labels and lines.

Divergences:

Classic Divergences:

Show Classic Div: Toggle to reveal divergences where RSI and price move in opposite directions.

Colors: Set different colors for bullish and bearish divergence indicators.

Transparency and Line Width: Control the visual impact of divergence signals.

Hidden Divergences:

Similar settings for identifying hidden divergences, suggest trend continuation.

Breakout/Breakdown:

Show Breakout/Breakdown: Generates signals for RSI breakouts or breakdowns, used by "Waldo RSI Overlay :o" for visual chart signals.

Overbought/Oversold Zones:

Show Overbought and OverSold Zones: Highlights when RSI goes above 70 (overbought) or below 30 (oversold).

Moving Averages on RSI:

The default Moving Average (MA) settings are tailored to capture macro shifts in market trends:

Show Moving Averages: Option to overlay two MAs on the RSI for trend confirmation:

Fast RSI MA:

RSI Period: 50 (this is the period over which the RSI is calculated).

MA Length: 50 (the number of periods used for the moving average of the RSI).

Slow RSI MA:

RSI Period: 50 (same as fast for consistency in RSI calculation).

MA Length: 200 (longer term for capturing broader trends).

Crossover Signals: The RSI changes color from red to green based on these moving average crossovers:

When the Fast MA (50 period) crosses above the Slow MA (200 period), the RSI turns green, indicating potential bullish conditions or momentum shift.

Conversely, when the Fast MA crosses below the Slow MA, the RSI turns red, suggesting bearish conditions or a shift back towards a downtrend.

This 50-period RSI crossover setting is used to identify overall macro shifts in the market, providing a clear visual cue for traders looking at longer-term trends.

Ghost Lines (Optional):

Ghost Lines: Option to limit how far RSI trend lines extend, helping to keep the chart less cluttered.

How to Use the Indicator:

Setup:

Configure RSI by choosing the source and setting the length to match your trading style.

Set the zigzag and confirm lengths for appropriate pivot detection.

Trend Analysis:

Monitor the RSI for trend changes using the colored trend lines and labels.

Divergence Detection:

Look for RSI and price divergences to anticipate potential reversals or continuations.

Breakout/Breakdown:

Use these signals in conjunction with "Waldo RSI Overlay :o" for price action confirmation.

Overbought/Oversold:

Identify when the market might be due for a correction or continued momentum.

Moving Averages:

Focus on the color changes in RSI to understand macro trend shifts with the default 50/200 period setup.

Ghost Lines:

Enable for a cleaner chart if you don't need trend lines extending indefinitely.

Usage Tips:

Combine with other indicators for confirmation, as no single tool is foolproof.

Adjust settings to suit different market conditions or trading timeframes.

Use in tandem with "Waldo RSI Overlay :o" for a full trading signal system.

Remember, trading involves significant risk, and historical data does not guarantee future performance. Use this indicator as part of a broader trading strategy.

Buy/Sell IndicatorBuy/Sell Indicator

Overview

The Buy/Sell Indicator is designed to help traders identify potential entry and exit points in the market using a combination of Simple Moving Averages (SMA) and the Relative Strength Index (RSI). This indicator plots buy and sell signals directly on the chart, making it easier to make informed trading decisions.

Inputs

Fast MA Length: The period for the fast-moving average. Default is 9.

Slow MA Length: The period for the slow-moving average. Default is 21.

RSI Length: The period for the RSI calculation. Default is 14.

RSI Overbought Level: The RSI level considered overbought. Default is 70.

RSI Oversold Level: The RSI level considered oversold. Default is 30.

How It Works

Moving Averages:

The indicator calculates two SMAs: a fast-moving average (fastMA) and a slow-moving average (slowMA).

The fast MA reacts more quickly to price changes, while the slow MA reacts more slowly.

RSI:

The RSI is calculated to measure the momentum of price movements.

It helps identify overbought and oversold conditions in the market.

Buy and Sell Conditions:

Buy Signal: A buy signal is generated when the fast MA crosses above the slow MA and the RSI is below the overbought level.

Sell Signal: A sell signal is generated when the fast MA crosses below the slow MA and the RSI is above the oversold level.

Plotting

Buy Signals: Displayed as green labels below the bars where the buy condition is met.

Sell Signals: Displayed as red labels above the bars where the sell condition is met.

Moving Averages: The fast MA is plotted in blue, and the slow MA is plotted in orange.

Heiken Ashi Ribbon [UkutaLabs]█ OVERVIEW

The Heiken Ashi Ribbon is a powerful trading tool that creates a strong ribbon that indicates market strength. This ribbon is created using four moving averages that use Heiken Ashi values (high, low, open and close) as its input values.

The ribbon will also be colored green, red or grey depending on whether or not its direction aligns with current market strength.

█ USAGE

The Heiken Ashi Ribbon is created using a series of four moving averages that uses values from the Heiken Ashi bars as its inputs. The user has the ability to select whether the moving averages are EMAs or SMAs, as well as the ability to control the period of the moving averages.

If the moving average calculated using the Heiken Ashi Open is below the moving average calculated using the Heiken Ashi Close, the ribbon will be colored green, indicating a bullish trend. If the moving average calculated using the Heiken Ashi Open is above the moving average calculated using the Heiken Ashi Open, the ribbon will be colored red, indicating a bearish trend.

This indicator also uses a series of hidden EMAs to determine market strength. If these EMAs do not align with the direction of the Heiken Ashi Ribbon, the Ribbon will instead be colored grey, indicating uncertainty in the market, as well as a possible reversal.

█ SETTINGS

Configuration

• Moving Average Type: Determines whether or not the Heiken Ashi Moving Averages will be drawn as EMAs or SMAs.

• Moving Average Period: Determines the period of the Heiken Ashi Moving Averages.

Moving Average

• Moving Average Input: Determines the input values for the hidden EMAs.

Doji Hunter█ OVERVIEW

This script is built to search for 8 different Doji candlestick patterns in markets and makes them appear on screen with bar coloring and creating color-coded labels/shapes. It will identify the following variants based upon user input for various rules to abide by:

Gapping Up

Gapping Down

Gravestone

Dragonfly

Long-Legged

Rickshaw Man

Northern (Doji in uptrend)

Southern (Doji in downtrend)

Note: for the remainder of this description, the types for inputs will be marked by italic text.

█ OPTIONS

This script features a wide range of options available to the user to modify how it functions. The first set of inputs dictate how the trend analysis is done with moving averages. The second and third sets of inputs dictate specific rules for how Doji candles are analyzed and the colors used for when they appear.

█ INPUTS (short)

1 — Moving Average Rules:

The Northern and Southern Doji variants require some trend analysis which will be done by Moving Averages. The inputs in this section change various things about the moving average(s) to be used. In the second section of inputs, there is one boolean option that will nullify the need for trend detection and consolidates the Northern and Southern Doji variants into one.

2/3 — Doji Rules and Colors:

The next two sections of inputs correspond to the various rules that dictate how various doji variants will be analyzed, as well as the colors that correspond to each variant. The colors will also apply to each of the labels/shapes used.

4 — Diagnostics:

The last boolean will allow the user to see extra detail with regards to how and when dojis are detected. Note: This is not a part of any prior section and is simply included as a last functional item to the list of all inputs.

An example of multiple labels being shown on screen for various types of Dojis (DJI 1D chart):

█ INPUTS (extended)

1 — Moving Average Rules:

This section consists of 10 different inputs specific to the rules on how the moving average functions for trend analysis.

"Trend Rule" ( string list) determines which Moving Average will be used for trend detection. It has 3 options: "MA 1", "MA 2", or "BOTH". The second input "Trend Source" determines which OHLC (or combination) value to use in comparison to either MA 1 or MA 2 (EX: Trend Rule -> "MA 1" and Trend Source -> "close": if close > MA 1 -> uptrend, downtrend otherwise). If "BOTH" is selected then "Trend Source" is ignored and added nuance in the script ensures that the shorter MA being above the longer MA yields an uptrend (downtrend otherwise).

The next 8 inputs focus on 4 different parts of both MA 1 and 2.

Length ( integer(s) )

Color

Switch between SMA/EMA ( boolean(s) )

Source for MA

Note: Additional attention to detail has been made here as trend direction is ignored if "BOTH" is selected for the MA Rules and the lengths of both Moving Averages are set to be the same.

2/3 — Doji Rules and Colors:

The next two sections include 19 inputs that are related to how this script will analyze and identify the different variants of Doji candles.

"Identify Pattern On Close" ( boolean ) modifies which candles are to be used for determining when Doji candles are recognized. This changes an offset used for historical reference on some global variables which will force the script to only identify patterns after the current candle has closed.

"Doji Body Tolerance" ( float ) tells the script the maximum % the candle body may be of the high-low range to be considered a Doji candle.

"Doji Wick Sample" ( integer ) defines how many prior candles to sample from in calculating the current average upper and lower wick sizes.

"Simplify Northern/Southern Dojis" ( boolean ) makes this script ignore trend direction for Doji detection and consolidates Northern and Southern Dojis into being recognized as the same. This has an added effect of removing the plotted moving averages from the screen.

"Northern/Southern Display" ( string list ) that has multiple options for how Northern and Southern Dojis will be displayed on screen. Because of how labels may be extremely taxing on TradingView's servers to display, the default setting is "shapes" where Northern and Southern (N/S) Dojis will be marked with a colored triangle at the top of the candle. If "Simplify Northern/Southern Dojis" is true, all N/S Dojis will be marked with an x-cross instead. Other options include "labels" which enables the use of labels accompanied by their respective tooltip and color, or "none" where N/S Dojis will be only noticeable by their changed barcolor.

"Allow Gravestone/Dragonfly Shadows" ( boolean ) allows a bit of additional nuance to the definition of Gravestone or Dragonfly Dojis with small shadows.

"Gravestone/Dragonfly Shadow Tolerance" ( float ) defines the maximum % that the lower wick/upper wick (respectively) may be relative to the high-low range for Gravestone or Dragonfly Dojis to still be considered valid.

"Doji Long Wick Setting" ( string list) is a list of settings for three different ways of confirming if a Doji is Long-Legged. The settings are "one", "two", and "average". These define how many wick lengths of a candle need to exceed the calculated average wick lengths (EX: "both" -> upper wick length > upper wick average and lower wick length > lower wick average). The "average" setting will combine the lengths of both wicks and both prior wick averages, divide both of these sums by 2 and compare them instead.

"Doji Long Wick Tolerance" ( float ) defines how large compared to the averages that wick lengths need to be in order for them to be considered "Long-Legged" (EX: 1.50 -> upper/lower wick needs to exceed 150% the average of previous upper/lower wicks).

"Rickshaw Man Body Placement Tolerance" ( float ) defines how close to the high-low range's midpoint the candle body's midpoint needs to be in order for it to be considered a Rickshaw Man Doji candle instead.

The remaining 9 inputs define the colors to use for differentiating between all Doji variants this script will recognize.

█ USAGE

My hope for this script is that users find this easy to use/understand and will tinker with the input values to better identify Doji candlesticks across a wide range of markets.

Suggestions for changes in the future are welcome.

Ichimoku Wave Oscillator with Custom MAIchimoku Wave Oscillator with Custom MA - Pine Script Description

This script uses various types of moving averages (MA) to implement the concept of Ichimoku wave theory for wave analysis. The user can select from SMA, EMA, WMA, TEMA, SMMA to visualize the difference between short-term, medium-term, and long-term waves, while identifying potential buy and sell signals at crossover points.

Key Features:

MA Type Selection:

The user can select from SMA (Simple Moving Average), EMA (Exponential Moving Average), WMA (Weighted Moving Average), TEMA (Triple Exponential Moving Average), and SMMA (Smoothed Moving Average) to calculate the waves. This script is unique in that it combines TEMA and SMMA, distinguishing it from other simple moving average-based indicators.

TEMA (Triple Exponential Moving Average): Best suited for capturing short-term trends with quick responsiveness.

SMMA (Smoothed Moving Average): Useful for identifying long-term trends with minimal noise, providing more stable signals.

Wave Calculations:

The script calculates three waves: Wave 9-17, Wave 17-26, and Wave 9-26, each of which analyzes different time horizons.

Wave 9-17 (blue): Primarily used for analyzing short-term trends, ideal for detecting quick changes.

Wave 17-26 (red): Used to analyze medium-term trends, providing a more stable market direction.

Wave 9-26 (green): Represents long-term trends, suitable for understanding broader trend shifts.

Baseline (0 Line):

Each wave is visualized around the 0 line, where waves above the line indicate an uptrend and waves below the line indicate a downtrend. This allows for easy identification of trend reversals.

Crossover Signals:

CrossUp: When Wave 9-17 (short-term wave) crosses Wave 17-26 (medium-term wave) upward, it is considered a buy signal, indicating a potential upward trend shift.

CrossDown: When Wave 9-17 (short-term wave) crosses Wave 17-26 downward, it is considered a sell signal, indicating a potential downward trend shift.

Background Color for Signal:

The script visually highlights the signals with background colors. When a buy signal occurs, the background turns green, and when a sell signal occurs, the background turns red. This makes it easier to spot reversal points.

Calculation Method:

The script calculates the difference between moving averages to display the wave oscillation. Wave 9-17, Wave 17-26, and Wave 9-26 represent the difference between the moving averages for different time periods, allowing for analysis of short-term, medium-term, and long-term trends.

Wave 9-17 = MA(9) - MA(17): Represents the difference between the short-term moving averages.

Wave 17-26 = MA(17) - MA(26): Represents the difference between medium-term moving averages.

Wave 9-26 = MA(9) - MA(26): Provides insight into the long-term trend.

This calculation method effectively visualizes the oscillation of waves and helps identify trend reversals at crossover points.

Uniqueness of the Script:

Unlike other moving average-based indicators, this script combines TEMA (Triple Exponential Moving Average) and SMMA (Smoothed Moving Average) to capture both short-term sensitivity and long-term stability in trends. This duality makes the script more versatile for different market conditions.

TEMA is ideal for short-term traders who need quick signals, while SMMA is useful for long-term investors seeking stability and noise reduction. By combining these two, this script provides a more refined analysis of trend changes across various timeframes.

How to Use:

This script is effective for trend analysis and reversal detection. By visualizing the crossover points between the waves, users can spot potential buy and sell signals to make more informed trading decisions.

Scalping strategies can rely on Wave 9-17 to detect quick trend changes, while those looking for medium-term trends can analyze signals from Wave 17-26.

For a broader market overview, Wave 9-26 helps users understand the long-term market trend.

This script is built on the concept of wave theory to anticipate trend changes, making it suitable for various timeframes and strategies. The user can tailor the characteristics of the waves by selecting different MA types, allowing for flexible application across different trading strategies.

Ichimoku Wave Oscillator with Custom MA - Pine Script 설명

이 스크립트는 다양한 이동 평균(MA) 유형을 활용하여 일목 파동론의 개념을 기반으로 파동 분석을 시도하는 지표입니다. 사용자는 SMA, EMA, WMA, TEMA, SMMA 중 원하는 이동 평균을 선택할 수 있으며, 이를 통해 단기, 중기, 장기 파동 간의 차이를 시각화하고, 교차점에서 상승 및 하락 신호를 포착할 수 있습니다.

주요 기능:

이동 평균(MA) 유형 선택:

사용자는 SMA(단순 이동 평균), EMA(지수 이동 평균), WMA(가중 이동 평균), TEMA(삼중 지수 이동 평균), SMMA(평활 이동 평균) 중 하나를 선택하여 파동을 계산할 수 있습니다. 이 스크립트는 TEMA와 SMMA의 독창적인 조합을 통해 기존의 단순한 이동 평균 지표와 차별화됩니다.

TEMA(삼중 지수 이동 평균): 빠른 반응으로 단기 트렌드를 포착하는 데 적합합니다.

SMMA(평활 이동 평균): 장기적인 추세를 파악하는 데 유용하며, 노이즈를 최소화하여 안정적인 신호를 제공합니다.

파동(Wave) 계산:

이 스크립트는 Wave 9-17, Wave 17-26, Wave 9-26의 세 가지 파동을 계산하여 각각 단기, 중기, 장기 추세를 분석합니다.

Wave 9-17 (파란색): 주로 단기 추세를 분석하는 데 사용되며, 빠른 추세 변화를 포착하는 데 유용합니다.

Wave 17-26 (빨간색): 중기 추세를 분석하는 데 사용되며, 좀 더 안정적인 시장 흐름을 보여줍니다.

Wave 9-26 (녹색): 장기 추세를 나타내며, 큰 흐름의 방향성을 파악하는 데 적합합니다.

기준선(0 라인):

각 파동은 0 라인을 기준으로 변동성을 시각화합니다. 0 위에 있는 파동은 상승세, 0 아래에 있는 파동은 하락세를 나타내며, 이를 통해 추세의 전환을 쉽게 확인할 수 있습니다.

파동 교차 신호:

CrossUp: Wave 9-17(단기 파동)이 Wave 17-26(중기 파동)을 상향 교차할 때, 상승 신호로 간주됩니다. 이는 단기적인 추세 변화가 발생할 수 있음을 의미합니다.

CrossDown: Wave 9-17(단기 파동)이 Wave 17-26(중기 파동)을 하향 교차할 때, 하락 신호로 해석됩니다. 이는 시장이 약세로 돌아설 가능성을 나타냅니다.

배경 색상 표시:

교차 신호가 발생할 때, 상승 신호는 녹색 배경, 하락 신호는 빨간색 배경으로 시각적으로 강조되어 사용자가 신호를 쉽게 인식할 수 있습니다.

계산 방식:

이 스크립트는 이동 평균 간의 차이를 계산하여 각 파동의 변동성을 나타냅니다. Wave 9-17, Wave 17-26, Wave 9-26은 각각 설정된 주기의 이동 평균(MA)의 차이를 통해, 시장의 단기, 중기, 장기 추세 변화를 시각적으로 표현합니다.

Wave 9-17 = MA(9) - MA(17): 단기 추세의 차이를 나타냅니다.

Wave 17-26 = MA(17) - MA(26): 중기 추세의 차이를 나타냅니다.

Wave 9-26 = MA(9) - MA(26): 장기적인 추세 방향을 파악할 수 있습니다.

이러한 계산 방식은 파동의 변동성을 파악하는 데 유용하며, 추세의 교차점을 통해 상승/하락 신호를 잡아냅니다.

스크립트의 독창성:

이 스크립트는 기존의 이동 평균 기반 지표들과 달리, TEMA(삼중 지수 이동 평균)와 SMMA(평활 이동 평균)을 함께 사용하여 짧은 주기와 긴 주기의 트렌드를 동시에 파악할 수 있도록 설계되었습니다. 이를 통해 단기 트렌드의 민감한 변화와 장기 트렌드의 안정성을 모두 반영합니다.

TEMA는 단기 트레이더에게 빠르고 민첩한 신호를 제공하며, SMMA는 장기 투자자에게 보다 안정적이고 긴 호흡의 트렌드를 파악하는 데 유리합니다. 두 지표의 결합으로, 다양한 시장 환경에서 추세의 변화를 더 정교하게 분석할 수 있습니다.

사용 방법:

이 스크립트는 추세 분석과 변곡점 포착에 효과적입니다. 각 파동 간의 교차점을 시각적으로 확인하고, 상승 또는 하락 신호를 포착하여 매매 시점 결정을 도울 수 있습니다.

스캘핑 전략에서는 Wave 9-17을 주로 참고하여 빠르게 추세 변화를 잡아내고, 중기 추세를 참고하고 싶은 경우 Wave 17-26을 사용해 신호를 분석할 수 있습니다.

장기적인 시장 흐름을 파악하고자 할 때는 Wave 9-26을 통해 큰 트렌드를 확인할 수 있습니다.

이 스크립트는 파동 이론의 개념을 기반으로 시장의 추세 변화를 예측하는 데 유용하며, 다양한 시간대와 전략에 맞추어 사용할 수 있습니다. 특히, 사용자가 선택한 MA 유형에 따라 파동의 특성을 변화시킬 수 있어, 여러 매매 전략에 유연하게 대응할 수 있습니다.

Pi Cycle Top & Bottom Indicator [InvestorUnknown]The Pi Cycle Top & Bottom Indicator is designed for long-term cycle analysis, particularly useful for detecting significant market tops and bottoms in assets like Bitcoin. By comparing the behavior of two moving averages, one with a shorter period (default 111) and the other with a longer period (default 350), the indicator helps investors identify potential turning points in the market.

Key Features:

Dual Moving Average System:

The indicator uses two moving averages (MA) to create a cyclic oscillator. The shorter moving average (Short Length MA) is more reactive to recent price changes, while the longer moving average (Long Length MA) smooths out long-term trends. Users can select between:

Simple Moving Average (SMA): A straightforward average of closing prices.

Exponential Moving Average (EMA): Places more weight on recent prices, making it more responsive to market changes.

Oscillator Mode Options:

The Pi Cycle Indicator offers two modes of oscillation to better suit different analysis styles:

RAW Mode: This mode calculates the raw ratio of the Short MA to the Long MA, offering a simple comparison of the two averages.

LOG(X) Mode: In this mode, the oscillator takes the natural logarithm of the Short MA to Long MA ratio. This transformation compresses extreme values and highlights relative changes more effectively, making it particularly useful for spotting shifts in long-term trends.

Cyclical Analysis:

The core of the Pi Cycle Indicator is its ability to visualize the relationship between the two moving averages. The ratio of the Short MA to the Long MA is plotted as an oscillator. When the oscillator crosses above or below a baseline (which is 1 for RAW mode and 0 for LOG(X) mode), it signals potential market turning points.

Visual Representation:

The indicator provides a clear visual display of market conditions:

Orange Line: Represents the Pi Cycle Oscillator, which shows the relationship between the short and long moving averages.

Gray Baseline: A reference line that dynamically adjusts based on the oscillator mode. Crosses above or below this line help indicate possible trend reversals.

Shaded Areas: Color-filled areas between the oscillator and the baseline, which are shaded green when the market is bullish (oscillator above baseline) and red when bearish (oscillator below baseline). This provides a visual cue to assist in identifying potential market tops and bottoms.

Use Cases:

The Pi Cycle Top & Bottom Indicator is primarily used in long-term market analysis, such as Bitcoin cycles, to identify significant tops and bottoms. These moments often coincide with large cyclical shifts, making it valuable for those aiming to enter or exit positions at key moments in the market cycle.

By analyzing the interaction between short-term and long-term trends, investors can gain insight into broader market dynamics and make more informed decisions regarding entry and exit points. The ability to switch between moving average types (SMA/EMA) and oscillator modes (RAW/LOG) adds flexibility for adapting to different market environments.

Multi-Timeframe MA Levels█ OVERVIEW

This Pine Script is an indicator for displaying multiple moving average (MA) levels from several timeframes on your TradingView charts. At the Realtime Bar (the right-most bar on your chart), it draws a line where the various moving averages currently are.

For example, it will show you where the 8 EMA on the 5 minute timeframe is on your 1-minute timeframe chart.

It derives its look and function from "Lepelle's Key Levels" and focuses on visualizing various moving averages to complement this indicator.

█ FEATURES

1 — Multi-Timeframe Analysis:

• The script allows traders to view moving averages from different timeframes on a single chart.

This multi-timeframe approach helps identify significant levels and trends that might not be apparent when looking at a single timeframe.

2 — Customization and Flexibility:

• Extensive input options for customizing the appearance of the lines (width, style, color) and labels (size, position, distance from price).

This ensures that the indicator can be tailored to individual preferences and charting styles.

3 — Multiple Moving Averages:

• Support for various types of moving averages (8 EMA, 21 EMA, 50 SMA, 100 SMA, 200 SMA).

Each moving average can be individually enabled or disabled for specific timeframes,

providing a flexible tool for technical analysis.

█ SETTINGS

Inputs for Styling:

• Controls the appearance of the lines and labels.

• Includes options for line width, line style, text size, distance from the candlesticks, label position,

and whether to hide prices or use shorthand notation.

Moving Averages Settings:

• Inputs to select different moving averages (8 EMA, 21 EMA, 50 SMA, 100 SMA, 200 SMA) and their corresponding colors.

• Boolean inputs to enable or disable these moving averages on various timeframes (2 min, 5 min, hourly, daily).

█ SUMMARY

In essence, this script provides a comprehensive tool for technical analysis by combining multi-timeframe moving averages into a single, customizable, and user-friendly indicator. It enhances traders' ability to make informed decisions by providing clear visual representations of key moving average levels across different timeframes.

═════════════════════════════════════════════════════════════

█ LIMITATIONS

This script is best used with a short timeframe such as 1-minute or lower because of the limitations of Multi-Timeframe scripts. Basically, the alternate timeframes in use should always be higher than the chart timeframe.

═════════════════════════════════════════════════════════════

█ NOTES

This indicator is intended to complement and be used with "Lepelle's Key Levels" indicator.

In that indictor settings, I recommend turning off the 5 Daily timeframe moving average levels in that script, if using this one.

═════════════════════════════════════════════════════════════

TASC 2024.05 Ultimate Channels and Ultimate Bands█ OVERVIEW

This script, inspired by the "Ultimate Channels and Ultimate Bands" article from the May 2024 edition of TASC's Traders' Tips , showcases the application of the UltimateSmoother by John Ehlers as a lag-reduced alternative to moving averages in indicators based on Keltner channels and Bollinger Bands®.

█ CONCEPTS

The UltimateSmoother , developed by John Ehlers, is a digital smoothing filter that provides minimal lag compared to many conventional smoothing filters, e.g., moving averages . Since this filter can provide a viable replacement for moving averages with reduced lag, it can potentially find broader applications in various technical indicators that utilize such averages.

This script explores its use as the smoothing filter in Keltner channels and Bollinger Bands® calculations, which traditionally rely on moving averages. By substituting averages with the UltimateSmoother function, the resulting channels or bands respond more quickly to fluctuations with substantially reduced lag.

Users can customize the script by selecting between the Ultimate channel or Ultimate bands and adjusting their parameters, including lookback lengths and band/channel width multipliers, to fine-tune the results.

█ CALCULATIONS

The calculations the Ultimate channels and Ultimate bands use closely resemble those of their conventional counterparts.

Ultimate channel:

Apply the Ultimate smoother to the `close` time series to establish the basis (center) value.

Calculate the smooth true range (STR) by applying the UltimateSmoother function with a user-specified length instead of a rolling moving average, thus replacing the conventional average true range (ATR). Users can adjust the final STR value using the "Width multiplier" input in the script's settings.

Calculate the upper channel value by adding the multiplied STR to the basis calculated in the first step, and calculate the lower channel value by subtracting the multiplied STR from the basis.

Ultimate bands:

Apply the Ultimate smoother to the `close` time series to establish the basis (center) value.

Calculate the width of the bands by finding the square root of the average of individual squared deviations over the specified length, then multiplying the result by the "Width multiplier" input value.

Calculate the upper band by adding the resulting width to the basis from the first step, and calculate the lower band by subtracting the width from the basis.

Goertzel Adaptive JMA T3Hello Fellas,

The Goertzel Adaptive JMA T3 is a powerful indicator that combines my own created Goertzel adaptive length with Jurik and T3 Moving Averages. The primary intention of the indicator is to demonstrate the new adaptive length algorithm by applying it on bleeding-edge MAs.

It is useable like any moving average, and the new Goertzel adaptive length algorithm can be used to make own indicators Goertzel adaptive.

Used Adaptive Length Algorithms

Normalized Goertzel Power: This uses the normalized power of the Goertzel algorithm to compute an adaptive length without the special operations, like detrending, Ehlers uses for his DFT adaptive length.

Ehlers Mod: This uses the Goertzel algorithm instead of the DFT, originally used by Ehlers, to compute a modified version of his original approach, which sticks as close as possible to the original approach.

Scoring System

The scoring system determines if bars are red or green and collects them.

Then, it goes through all collected red and green bars and checks how big they are and if they are above or below the selected MA. It is positive when green bars are under MA or when red bars are above MA.

Then, it accumulates the size for all positive green bars and for all positive red bars. The same happens for negative green and red bars.

Finally, it calculates the score by ((positiveGreenBars + positiveRedBars) / (negativeGreenBars + negativeRedBars)) * 100 with the scale 0–100.

Signals

Is the price above MA? -> bullish market

Is the price below MA? -> bearish market

Usage

Adjust the settings to reach the highest score, and enjoy an outstanding adaptive MA.

It should be useable on all timeframes. It is recommended to use the indicator on the timeframe where you can get the highest score.

Now, follows a bunch of knowledge for people who don't know about the concepts used here.

T3

The T3 moving average, short for "Tim Tillson's Triple Exponential Moving Average," is a technical indicator used in financial markets and technical analysis to smooth out price data over a specific period. It was developed by Tim Tillson, a software project manager at Hewlett-Packard, with expertise in Mathematics and Computer Science.

The T3 moving average is an enhancement of the traditional Exponential Moving Average (EMA) and aims to overcome some of its limitations. The primary goal of the T3 moving average is to provide a smoother representation of price trends while minimizing lag compared to other moving averages like Simple Moving Average (SMA), Weighted Moving Average (WMA), or EMA.

To compute the T3 moving average, it involves a triple smoothing process using exponential moving averages. Here's how it works:

Calculate the first exponential moving average (EMA1) of the price data over a specific period 'n.'

Calculate the second exponential moving average (EMA2) of EMA1 using the same period 'n.'

Calculate the third exponential moving average (EMA3) of EMA2 using the same period 'n.'

The formula for the T3 moving average is as follows:

T3 = 3 * (EMA1) - 3 * (EMA2) + (EMA3)

By applying this triple smoothing process, the T3 moving average is intended to offer reduced noise and improved responsiveness to price trends. It achieves this by incorporating multiple time frames of the exponential moving averages, resulting in a more accurate representation of the underlying price action.

JMA

The Jurik Moving Average (JMA) is a technical indicator used in trading to predict price direction. Developed by Mark Jurik, it’s a type of weighted moving average that gives more weight to recent market data rather than past historical data.

JMA is known for its superior noise elimination. It’s a causal, nonlinear, and adaptive filter, meaning it responds to changes in price action without introducing unnecessary lag. This makes JMA a world-class moving average that tracks and smooths price charts or any market-related time series with surprising agility.

In comparison to other moving averages, such as the Exponential Moving Average (EMA), JMA is known to track fast price movement more accurately. This allows traders to apply their strategies to a more accurate picture of price action.

Goertzel Algorithm

The Goertzel algorithm is a technique in digital signal processing (DSP) for efficient evaluation of individual terms of the Discrete Fourier Transform (DFT). It's particularly useful when you need to compute a small number of selected frequency components. Unlike direct DFT calculations, the Goertzel algorithm applies a single real-valued coefficient at each iteration, using real-valued arithmetic for real-valued input sequences. This makes it more numerically efficient when computing a small number of selected frequency components¹.

Discrete Fourier Transform

The Discrete Fourier Transform (DFT) is a mathematical technique used in signal processing to convert a finite sequence of equally-spaced samples of a function into a same-length sequence of equally-spaced samples of the discrete-time Fourier transform (DTFT), which is a complex-valued function of frequency . The DFT provides a frequency domain representation of the original input sequence .

Usage of DFT/Goertzel In Adaptive Length Algorithms

Adaptive length algorithms are automated trading systems that can dynamically adjust their parameters in response to real-time market data. This adaptability enables them to optimize their trading strategies as market conditions fluctuate. Both the Goertzel algorithm and DFT can be used in these algorithms to analyze market data and detect cycles or patterns, which can then be used to adjust the parameters of the trading strategy.

The Goertzel algorithm is more efficient than the DFT when you need to compute a small number of selected frequency components. However, for covering a full spectrum, the Goertzel algorithm has a higher order of complexity than fast Fourier transform (FFT) algorithms.

I hope this can help you somehow.

Thanks for reading, and keep it up.

Best regards,

simwai

---

Credits to:

@ClassicScott

@yatrader2

@cheatcountry

@loxx

Market Smith IndicatorsMarket Smith has a collection of tools that are useful for identifying stocks. On their charts they have a 21/50/200 day moving averages, high and low pivot points, a relative strength line, and a relative strength rating. This script contains indicators for the following:

21/50/200 Day Moving Averages

High and Low pivot points

A Relative Strength line

A Relative Strength rating

21/50/200 Day Moving Averages

The 21/50/200 Day moving averages are simple moving averages. They are visible in any chart increment but to use them properly you need to set you charts to be by day. Labels will appear on the right of the lines to show that they are representative of 21/50/200 day moving averages.

High and Low pivot points

The High and Low pivot points are green for high pivot points and red for low points. They are show in the Market Smith style with the numbers simply above the pivot points.

Relative Strength line

The Relative Strength line is a line that shows the strength of the stock compared to the S&P 500. In this case we utilize the SPX ticker to compare the stock to. This line is almost identical to the Market Smith tool and is an excellent tool to determine how a stock is doing compared to the market. When movements in the stock and shown with sideways trending of the RS line that means that the stock is following the market. When a stock is outperforming the market the RS line will follow.

Relative Strength rating

Thank you to ©Fred6724 for the RS Rating inspiration. They wrote excellent open source code for a RS Rating comparable to Market Smith. As the RS Rating in Market Smith is not open source it is difficult to know exactly how it is being calculated. After simplifying Fred's code and building upon a few ideas I had I compared the RS Rating to multiple Market Smith Ratings. The rating is close but often off by multiple points. If there is anyone who has a better idea on how to get this rating or how to improve on the code please send me a PM or fork this project. This rating is a good indicator to see how a certain stock compares to other stocks in the market. In Market Smith they are able to utilize their database to compare it to all other stocks. Since we do not have access to the same tools we are only able to compare it to the percentage of stocks above the 200, 150, 100, 50, and 20 day moving average.

Using these tools together are a small fraction what make people like Bill O'neill and Jim Roppel so successful. I plan on updating the RS Rating as I continue to work on this project so if there is anyone who has ideas then please send me a PM. Ultimately the goal of this project is to have a solution that is identical to Market Smith.

Adaptive Candlestick Pattern Recognition System█ INTRODUCTION

Nearly three years in the making, intermittently worked on in the few spare hours of weekends and time off, this is a passion project I undertook to flesh out my skills as a computer programmer. This script currently recognizes 85 different candlestick patterns ranging from one to five candles in length. It also performs statistical analysis on those patterns to determine prior performance and changes the coloration of those patterns based on that performance. In searching TradingView's script library for scripts similar to this one, I had found a handful. However, when I reviewed the ones which were open source, I did not see many that truly captured the power of PineScrypt or leveraged the way it works to create efficient and reliable code; one of the main driving factors for releasing this 5,000+ line behemoth open sourced.

Please take the time to review this description and source code to utilize this script to its fullest potential.

█ CONCEPTS

This script covers the following topics: Candlestick Theory, Trend Direction, Higher Timeframes, Price Analysis, Statistic Analysis, and Code Design.

Candlestick Theory - This script focuses solely on the concept of Candlestick Theory: arrangements of candlesticks may form certain patterns that can potentially influence the future price action of assets which experience those patterns. A full list of patterns (grouped by pattern length) will be in its own section of this description. This script contains two modes of operation for identifying candlestick patterns, 'CLASSIC' and 'BREAKOUT'.

CLASSIC: In this mode, candlestick patterns will be identified whenever they appear. The user has a wide variety of inputs to manipulate that can change how certain patterns are identified and even enable alerts to notify themselves when these patterns appear. Each pattern selected to appear will have their Profit or Loss (P/L) calculated starting from the first candle open succeeding the pattern to a candle close specified some number of candles ahead. These P/L calculations are then collected for each pattern, and split among partitions of prior price action of the asset the script is currently applied to (more on that in Higher Timeframes ).

BREAKOUT: In this mode, P/L calculations are held off until a breakout direction has been confirmed. The user may specify the number of candles ahead of a pattern's appearance (from one to five) that a pattern has to confirm a breakout in either an upward or downward direction. A breakout is constituted when there is a candle following the appearance of the pattern that closes above/at the highest high of the pattern, or below/at its lowest low. Only then will percent return calculations be performed for the pattern that's been identified, and these percent returns are broken up not only by the partition they had appeared in but also by the breakout direction itself. Patterns which do not breakout in either direction will be ignored, along with having their labels deleted.

In both of these modes, patterns may be overridden. Overrides occur when a smaller pattern has been detected and ends up becoming one (or more) of the candles of a larger pattern. A key example of this would be the Bearish Engulfing and the Three Outside Down patterns. A Three Outside Down necessitates a Bearish Engulfing as the first two candles in it, while the third candle closes lower. When a pattern is overridden, the return for that pattern will no longer be tracked. Overrides will not occur if the tail end of a larger pattern occurs at the beginning of a smaller pattern (Ex: a Bullish Engulfing occurs on the third candle of a Three Outside Down and the candle immediately following that pattern, the Three Outside Down pattern will not be overridden).

Important Functionality Note: These patterns are only searched for at the most recently closed candle, not on the currently closing candle, which creates an offset of one for this script's execution. (SEE LIMITATIONS)

Trend Direction - Many of the patterns require a trend direction prior to their appearance. Noting TradingView's own publication of candlestick patterns, I utilize a similar method for determining trend direction. Moving Averages are used to determine which trend is currently taking place for candlestick patterns to be sought out. The user has access to two Moving Averages which they may individually modify the following for each: Moving Average type (list of 9), their length, width, source values, and all variables associated with two special Moving Averages (Least Squares and Arnaud Legoux).

There are 3 settings for these Moving Averages, the first two switch between the two Moving Averages, and the third uses both. When using individual Moving Averages, the user may select a 'price point' to compare against the Moving Average (default is close). This price point is compared to the Moving Average at the candles prior to the appearance of candle patterns. Meaning: The close compared to the Moving Average two candles behind determines the trend direction used for Candlestick Analysis of one candle patterns; three candles behind for two candle patterns and so on. If the selected price point is above the Moving Average, then the current trend is an 'uptrend', 'downtrend' otherwise.

The third setting using both Moving Averages will compare the lengths of each, and trend direction is determined by the shorter Moving Average compared to the longer one. If the shorter Moving Average is above the longer, then the current trend is an 'uptrend', 'downtrend' otherwise. If the lengths of the Moving Averages are the same, or both Moving Averages are Symmetrical, then MA1 will be used by default. (SEE LIMITATIONS)

Higher Timeframes - This script employs the use of Higher Timeframes with a few request.security calls. The purpose of these calls is strictly for the partitioning of an asset's chart, splitting the returns of patterns into three separate groups. The four inputs in control of this partitioning split the chart based on: A given resolution to grab values from, the length of time in that resolution, and 'Upper' and 'Lower Limits' which split the trading range provided by that length of time in that resolution that forms three separate groups. The default values for these four inputs will partition the current chart by the yearly high-low range where: the 'Upper' partition is the top 20% of that trading range, the 'Middle' partition is 80% to 33% of the trading range, and the 'Lower' partition covers the trading range within 33% of the yearly low.

Patterns which are identified by this script will have their returns grouped together based on which partition they had appeared in. For example, a Bullish Engulfing which occurs within a third of the yearly low will have its return placed separately from a Bullish Engulfing that occurred within 20% of the yearly high. The idea is that certain patterns may perform better or worse depending on when they had occurred during an asset's trading range.

Price Analysis - Price Analysis is a major part of this script's functionality as it can fundamentally change how patterns are shown to the user. The settings related to Price Analysis include setting the number of candles ahead of a pattern's appearance to determine the return of that pattern. In 'BREAKOUT' mode, an additional setting allows the user to specify where the P/L calculation will begin for a pattern that had appeared and confirmed. (SEE LIMITATIONS)

The calculation for percent returns of patterns is illustrated with the following pseudo-code (CLASSIC mode, this is a simplified version of the actual code):

type patternObj

int ID

int partition

type returnsArray

float returns

// No pattern found = na returned

patternObj TEST_VAL = f_FindPattern()

priorTestVal = TEST_VAL

if not na( priorTestVal )

pnlMatrixRow = priorTestVal.ID

pnlMatrixCol = priorTestVal.partition

matrixReturn = matrix.get(PERCENT_RETURNS, pnlMatrixRow, pnlMatrixCol)

percentReturn = ( (close - open ) / open ) * 100%

array.push(matrixReturn.returns, percentReturn)

Statistic Analysis - This script uses Pine's built-in array functions to conduct the Statistic Analysis for patterns. When a pattern is found and its P/L calculation is complete, its return is added to a 'Return Array' User-Defined-Type that contains numerous fields which retain information on a pattern's prior performance. The actual UDT is as follows:

type returnArray

float returns = na

int size = 0

float avg = 0

float median = 0

float stdDev = 0

int polarities = na

All values within this UDT will be updated when a return is added to it (some based on user input). The array.avg , array.median and array.stdev will be ran and saved into their respective fields after a return is placed in the 'returns' array. The 'polarities' integer array is what will be changed based on user input. The user specifies two different percentages that declare 'Positive' and 'Negative' returns for patterns. When a pattern returns above, below, or in between these two values, different indices of this array will be incremented to reflect the kind of return that pattern had just experienced.

These values (plus the full name, partition the pattern occurred in, and a 95% confidence interval of expected returns) will be displayed to the user on the tooltip of the labels that identify patterns. Simply scroll over the pattern label to view each of these values.

Code Design - Overall this script is as much of an art piece as it is functional. Its design features numerous depictions of ASCII Art that illustrate what is being attempted by the functions that identify patterns, and an incalculable amount of time was spent rewriting portions of code to improve its efficiency. Admittedly, this final version is nearly 1,000 lines shorter than a previous version (one which took nearly 30 seconds after compilation to run, and didn't do nearly half of what this version does). The use of UDTs, especially the 'patternObj' one crafted and redesigned from the Hikkake Hunter 2.0 I published last month, played a significant role in making this script run efficiently. There is a slight rigidity in some of this code mainly around pattern IDs which are responsible for displaying the abbreviation for patterns (as well as the full names under the tooltips, and the matrix row position for holding returns), as each is hard-coded to correspond to that pattern.

However, one thing I would like to mention is the extensive use of global variables for pattern detection. Many scripts I had looked over for ideas on how to identify candlestick patterns had the same idea; break the pattern into a set of logical 'true/false' statements derived from historically referencing candle OHLC values. Some scripts which identified upwards of 20 to 30 patterns would reference Pine's built-in OHLC values for each pattern individually, potentially requesting information from TradingView's servers numerous times that could easily be saved into a variable for re-use and only requested once per candle (what this script does).

█ FEATURES

This script features a massive amount of switches, options, floating point values, detection settings, and methods for identifying/tailoring pattern appearances. All modifiable inputs for patterns are grouped together based on the number of candles they contain. Other inputs (like those for statistics settings and coloration) are grouped separately and presented in a way I believe makes the most sense.

Not mentioned above is the coloration settings. One of the aims of this script was to make patterns visually signify their behavior to the user when they are identified. Each pattern has its own collection of returns which are analyzed and compared to the inputs of the user. The user may choose the colors for bullish, neutral, and bearish patterns. They may also choose the minimum number of patterns needed to occur before assigning a color to that pattern based on its behavior; a color for patterns that have not met this minimum number of occurrences yet, and a color for patterns that are still processing in BREAKOUT mode.

There are also an additional three settings which alter the color scheme for patterns: Statistic Point-of-Reference, Adaptive coloring, and Hard Limiting. The Statistic Point-of-Reference decides which value (average or median) will be compared against the 'Negative' and 'Positive Return Tolerance'(s) to guide the coloration of the patterns (or for Adaptive Coloring, the generation of a color gradient).

Adaptive Coloring will have this script produce a gradient that patterns will be colored along. The more bullish or bearish a pattern is, the further along the gradient those patterns will be colored starting from the 'Neutral' color (hard lined at the value of 0%: values above this will be colored bullish, bearish otherwise). When Adaptive Coloring is enabled, this script will request the highest and lowest values (these being the Statistic Point-of-Reference) from the matrix containing all returns and rewrite global variables tied to the negative and positive return tolerances. This means that all patterns identified will be compared with each other to determine bullish/bearishness in Adaptive Coloring.

Hard Limiting will prevent these global variables from being rewritten, so patterns whose Statistic Point-of-Reference exceed the return tolerances will be fully colored the bullish or bearish colors instead of a generated gradient color. (SEE LIMITATIONS)

Apart from the Candle Detection Modes (CLASSIC and BREAKOUT), there's an additional two inputs which modify how this script behaves grouped under a "MASTER DETECTION SETTINGS" tab. These two "Pattern Detection Settings" are 'SWITCHBOARD' and 'TARGET MODE'.

SWITCHBOARD: Every single pattern has a switch that is associated with its detection. When a switch is enabled, the code which searches for that pattern will be run. With the Pattern Detection Setting set to this, all patterns that have their switches enabled will be sought out and shown.

TARGET MODE: There is an additional setting which operates on top of 'SWITCHBOARD' that singles out an individual pattern the user specifies through a drop down list. The names of every pattern recognized by this script will be present along with an identifier that shows the number of candles in that pattern (Ex: " (# candles)"). All patterns enabled in the switchboard will still have their returns measured, but only the pattern selected from the "Target Pattern" list will be shown. (SEE LIMITATIONS)

The vast majority of other features are held in the one, two, and three candle pattern sections.

For one-candle patterns, there are:

3 — Settings related to defining 'Tall' candles:

The number of candles to sample for previous candle-size averages.

The type of comparison done for 'Tall' Candles: Settings are 'RANGE' and 'BODY'.

The 'Tolerance' for tall candles, specifying what percent of the 'average' size candles must exceed to be considered 'Tall'.

When 'Tall Candle Setting' is set to RANGE, the high-low ranges are what the current candle range will be compared against to determine if a candle is 'Tall'. Otherwise the candle bodies (absolute value of the close - open) will be compared instead. (SEE LIMITATIONS)

Hammer Tolerance - How large a 'discarded wick' may be before it disqualifies a candle from being a 'Hammer'.

Discarded wicks are compared to the size of the Hammer's candle body and are dependent upon the body's center position. Hammer bodies closer to the high of the candle will have the upper wick used as its 'discarded wick', otherwise the lower wick is used.

9 — Doji Settings, some pulled from an old Doji Hunter I made a while back:

Doji Tolerance - How large the body of a candle may be compared to the range to be considered a 'Doji'.

Ignore N/S Dojis - Turns off Trend Direction for non-special Dojis.

GS/DF Doji Settings - 2 Inputs that enable and specify how large wicks that typically disqualify Dojis from being 'Gravestone' or 'Dragonfly' Dojis may be.

4 Settings related to 'Long Wick Doji' candles detailed below.

A Tolerance for 'Rickshaw Man' Dojis specifying how close the center of the body must be to the range to be valid.

The 4 settings the user may modify for 'Long Legged' Dojis are: A Sample Base for determining the previous average of wicks, a Sample Length specifying how far back to look for these averages, a Behavior Setting to define how 'Long Legged' Dojis are recognized, and a tolerance to specify how large in comparison to the prior wicks a Doji's wicks must be to be considered 'Long Legged'.

The 'Sample Base' list has two settings:

RANGE: The wicks of prior candles are compared to their candle ranges and the 'wick averages' will be what the average percent of ranges were in the sample.

WICKS: The size of the wicks themselves are averaged and returned for comparing against the current wicks of a Doji.

The 'Behavior' list has three settings:

ONE: Only one wick length needs to exceed the average by the tolerance for a Doji to be considered 'Long Legged'.

BOTH: Both wick lengths need to exceed the average of the tolerance of their respective wicks (upper wicks are compared to upper wicks, lower wicks compared to lower) to be considered 'Long Legged'.

AVG: Both wicks and the averages of the previous wicks are added together, divided by two, and compared. If the 'average' of the current wicks exceeds this combined average of prior wicks by the tolerance, then this would constitute a valid 'Long Legged' Doji. (For Dojis in general - SEE LIMITATIONS)

The final input is one related to candle patterns which require a Marubozu candle in them. The two settings for this input are 'INCLUSIVE' and 'EXCLUSIVE'. If INCLUSIVE is selected, any opening/closing variant of Marubozu candles will be allowed in the patterns that require them.

For two-candle patterns, there are:

2 — Settings which define 'Engulfing' parameters:

Engulfing Setting - Two options, RANGE or BODY which sets up how one candle may 'engulf' the previous.

Inclusive Engulfing - Boolean which enables if 'engulfing' candles can be equal to the values needed to 'engulf' the prior candle.

For the 'Engulfing Setting':

RANGE: If the second candle's high-low range completely covers the high-low range of the prior candle, this is recognized as 'engulfing'.

BODY: If the second candle's open-close completely covers the open-close of the previous candle, this is recognized as 'engulfing'. (SEE LIMITATIONS)

4 — Booleans specifying different settings for a few patterns:

One which allows for 'opens within body' patterns to let the second candle's open/close values match the prior candles' open/close.

One which forces 'Kicking' patterns to have a gap if the Marubozu setting is set to 'INCLUSIVE'.

And Two which dictate if the individual candles in 'Stomach' patterns need to be 'Tall'.

8 — Floating point values which affect 11 different patterns:

One which determines the distance the close of the first candle in a 'Hammer Inverted' pattern must be to the low to be considered valid.

One which affects how close the opens/closes need to be for all 'Lines' patterns (Bull/Bear Meeting/Separating Lines).

One that allows some leeway with the 'Matching Low' pattern (gives a small range the second candle close may be within instead of needing to match the previous close).

Three tolerances for On Neck/In Neck patterns (2 and 1 respectively).

A tolerance for the Thrusting pattern which give a range the close the second candle may be between the midpoint and close of the first to be considered 'valid'.

A tolerance for the two Tweezers patterns that specifies how close the highs and lows of the patterns need to be to each other to be 'valid'.

The first On Neck tolerance specifies how large the lower wick of the first candle may be (as a % of that candle's range) before the pattern is invalidated. The second tolerance specifies how far up the lower wick to the close the second candle's close may be for this pattern. The third tolerance for the In Neck pattern determines how far into the body of the first candle the second may close to be 'valid'.

For the remaining patterns (3, 4, and 5 candles), there are:

3 — Settings for the Deliberation pattern:

A boolean which forces the open of the third candle to gap above the close of the second.

A tolerance which changes the proximity of the third candle's open to the second candle's close in this pattern.

A tolerance that sets the maximum size the third candle may be compared to the average of the first two candles.

One boolean value for the Two Crows patterns (standard and Upside Gapping) that forces the first two candles in the patterns to completely gap if disabled (candle 1's close < candle 2's low).

10 — Floating point values for the remaining patterns:

One tolerance for defining how much the size of each candle in the Identical Black Crows pattern may deviate from the average of themselves to be considered valid.

One tolerance for setting how close the opens/closes of certain three candle patterns may be to each other's opens/closes.*

Three floating point values that affect the Three Stars in the South pattern.

One tolerance for the Side-by-Side patterns - looks at the second and third candle closes.

One tolerance for the Stick Sandwich pattern - looks at the first and third candle closes.

A floating value that sizes the Concealing Baby Swallow pattern's 3rd candle wick.

Two values for the Ladder Bottom pattern which define a range that the third candle's wick size may be.

* This affects the Three Black Crows (non-identical) and Three White Soldiers patterns, each require the opens and closes of every candle to be near each other.

The first tolerance of the Three Stars in the South pattern affects the first candle body's center position, and defines where it must be above to be considered valid. The second tolerance specifies how close the second candle must be to this same position, as well as the deviation the ratio the candle body to its range may be in comparison to the first candle. The third restricts how large the second candle range may be in comparison to the first (prevents this pattern from being recognized if the second candle is similar to the first but larger).

The last two floating point values define upper and lower limits to the wick size of a Ladder Bottom's fourth candle to be considered valid.

█ HOW TO USE

While there are many moving parts to this script, I attempted to set the default values with what I believed may help identify the most patterns within reasonable definitions. When this script is applied to a chart, the Candle Detection Mode (along with the BREAKOUT settings) and all candle switches must be confirmed before patterns are displayed. All switches are on by default, so this gives the user an opportunity to pick which patterns to identify first before playing around in the settings.

All of the settings/inputs described above are meant for experimentation. I encourage the user to tweak these values at will to find which set ups work best for whichever charts they decide to apply these patterns to.

Refer to the patterns themselves during experimentation. The statistic information provided on the tooltips of the patterns are meant to help guide input decisions. The breadth of candlestick theory is deep, and this was an attempt at capturing what I could in its sea of information.

█ LIMITATIONS

DISCLAIMER: While it may seem a bit paradoxical that this script aims to use past performance to potentially measure future results, past performance is not indicative of future results . Markets are highly adaptive and often unpredictable. This script is meant as an informational tool to show how patterns may behave. There is no guarantee that confidence intervals (or any other metric measured with this script) are accurate to the performance of patterns; caution must be exercised with all patterns identified regardless of how much information regarding prior performance is available.

Candlestick Theory - In the name, Candlestick Theory is a theory , and all theories come with their own limits. Some patterns identified by this script may be completely useless/unprofitable/unpredictable regardless of whatever combination of settings are used to identify them. However, if I truly believed this theory had no merit, this script would not exist. It is important to understand that this is a tool meant to be utilized with an array of others to procure positive (or negative, looking at you, short sellers ) results when navigating the complex world of finance.

To address the functionality note however, this script has an offset of 1 by default. Patterns will not be identified on the currently closing candle, only on the candle which has most recently closed. Attempting to have this script do both (offset by one or identify on close) lead to more trouble than it was worth. I personally just want users to be aware that patterns will not be identified immediately when they appear.

Trend Direction - Moving Averages - There is a small quirk with how MA settings will be adjusted if the user inputs two moving averages of the same length when the "MA Setting" is set to 'BOTH'. If Moving Averages have the same length, this script will default to only using MA 1 regardless of if the types of Moving Averages are different . I will experiment in the future to alleviate/reduce this restriction.

Price Analysis - BREAKOUT mode - With how identifying patterns with a look-ahead confirmation works, the percent returns for patterns that break out in either direction will be calculated on the same candle regardless of if P/L Offset is set to 'FROM CONFIRMATION' or 'FROM APPEARANCE'. This same issue is present in the Hikkake Hunter script mentioned earlier. This does not mean the P/L calculations are incorrect , the offset for the calculation is set by the number of candles required to confirm the pattern if 'FROM APPEARANCE' is selected. It just means that these two different P/L calculations will complete at the same time independent of the setting that's been selected.

Adaptive Coloring/Hard Limiting - Hard Limiting is only used with Adaptive Coloring and has no effect outside of it. If Hard Limiting is used, it is recommended to increase the 'Positive' and 'Negative' return tolerance values as a pattern's bullish/bearishness may be disproportionately represented with the gradient generated under a hard limit.

TARGET MODE - This mode will break rules regarding patterns that are overridden on purpose. If a pattern selected in TARGET mode would have otherwise been absorbed by a larger pattern, it will have that pattern's percent return calculated; potentially leading to duplicate returns being included in the matrix of all returns recognized by this script.

'Tall' Candle Setting - This is a wide-reaching setting, as approximately 30 different patterns or so rely on defining 'Tall' candles. Changing how 'Tall' candles are defined whether by the tolerance value those candles need to exceed or by the values of the candle used for the baseline comparison (RANGE/BODY) can wildly affect how this script functions under certain conditions. Refer to the tooltip of these settings for more information on which specific patterns are affected by this.

Doji Settings - There are roughly 10 or so two to three candle patterns which have Dojis as a part of them. If all Dojis are disabled, it will prevent some of these larger patterns from being recognized. This is a dependency issue that I may address in the future.

'Engulfing' Setting - Functionally, the two 'Engulfing' settings are quite different. Because of this, the 'RANGE' setting may cause certain patterns that would otherwise be valid under textbook and online references/definitions to not be recognized as such (like the Upside Gap Two Crows or Three Outside down).

█ PATTERN LIST

This script recognizes 85 patterns upon initial release. I am open to adding additional patterns to it in the future and any comments/suggestions are appreciated. It recognizes:

15 — 1 Candle Patterns

4 Hammer type patterns: Regular Hammer, Takuri Line, Shooting Star, and Hanging Man

9 Doji Candles: Regular Dojis, Northern/Southern Dojis, Gravestone/Dragonfly Dojis, Gapping Up/Down Dojis, and Long-Legged/Rickshaw Man Dojis

White/Black Long Days

32 — 2 Candle Patterns

4 Engulfing type patterns: Bullish/Bearish Engulfing and Last Engulfing Top/Bottom

Dark Cloud Cover

Bullish/Bearish Doji Star patterns

Hammer Inverted

Bullish/Bearish Haramis + Cross variants

Homing Pigeon

Bullish/Bearish Kicking

4 Lines type patterns: Bullish/Bearish Meeting/Separating Lines

Matching Low

On/In Neck patterns

Piercing pattern

Shooting Star (2 Lines)

Above/Below Stomach patterns

Thrusting

Tweezers Top/Bottom patterns

Two Black Gapping

Rising/Falling Window patterns

29 — 3 Candle Patterns

Bullish/Bearish Abandoned Baby patterns

Advance Block

Collapsing Doji Star

Deliberation

Upside/Downside Gap Three Methods patterns

Three Inside/Outside Up/Down patterns (4 total)

Bullish/Bearish Side-by-Side patterns

Morning/Evening Star patterns + Doji variants

Stick Sandwich

Downside/Upside Tasuki Gap patterns

Three Black Crows + Identical variation

Three White Soldiers

Three Stars in the South

Bullish/Bearish Tri-Star patterns

Two Crows + Upside Gap variant

Unique Three River Bottom

3 — 4 Candle Patterns

Concealing Baby Swallow

Bullish/Bearish Three Line Strike patterns

6 — 5 Candle Patterns

Bullish/Bearish Breakaway patterns

Ladder Bottom

Mat Hold

Rising/Falling Three Methods patterns

█ WORKS CITED

Because of the amount of time needed to complete this script, I am unable to provide exact dates for when some of these references were used. I will also not provide every single reference, as citing a reference for each individual pattern and the place it was reviewed would lead to a bibliography larger than this script and its description combined. There were five major resources I used when building this script, one book, two websites (for various different reasons including patterns, moving averages, and various other articles of information), various scripts from TradingView's public library (including TradingView's own source code for *all* candle patterns ), and PineScrypt's reference manual.

Bulkowski, Thomas N. Encyclopedia of Candlestick Patterns . Hoboken, New Jersey: John Wiley & Sons Inc., 2008. E-book (google books).

Various. Numerous webpages. CandleScanner . 2023. online. Accessed 2020 - 2023.

Various. Numerous webpages. Investopedia . 2023. online. Accessed 2020 - 2023.

█ AKNOWLEDGEMENTS

I want to take the time here to thank all of my friends and family, both online and in real life, for the support they've given me over the last few years in this endeavor. My pets who tried their hardest to keep me from completing it. And work for the grit to continue pushing through until this script's completion.

This belongs to me just as much as it does anyone else. Whether you are an institutional trader, gold bug hedging against the dollar, retail ape who got in on a squeeze, or just parents trying to grow their retirement/save for the kids. This belongs to everyone.

Private Beta for new features to be tested can be found here .

Vires In Numeris

Moving Average Compendium RefurbishedThis is my effort to bring together in a single script the widest range of moving averages possible.

I aggregated the calculation of averages within a library.

For more information about the library follow the link:

Basically this indicator is the visual result of this library.

You can choose the moving average and the script updates the chart as per the type.

The unique parameters of certain moving averages remain at their default values.

To have a rainbow of moving averages I also made an indicator:

Available moving averages:

AARMA = 'Adaptive Autonomous Recursive Moving Average'

ADEMA = '* Alpha-Decreasing Exponential Moving Average'

AHMA = 'Ahrens Moving Average'

ALMA = 'Arnaud Legoux Moving Average'

ALSMA = 'Adaptive Least Squares'

AUTOL = 'Auto-Line'

CMA = 'Corrective Moving average'

CORMA = 'Correlation Moving Average Price'

COVWEMA = 'Coefficient of Variation Weighted Exponential Moving Average'

COVWMA = 'Coefficient of Variation Weighted Moving Average'

DEMA = 'Double Exponential Moving Average'

DONCHIAN = 'Donchian Middle Channel'

EDMA = 'Exponentially Deviating Moving Average'

EDSMA = 'Ehlers Dynamic Smoothed Moving Average'

EFRAMA = '* Ehlrs Modified Fractal Adaptive Moving Average'

EHMA = 'Exponential Hull Moving Average'

EMA = 'Exponential Moving Average'

EPMA = 'End Point Moving Average'

ETMA = 'Exponential Triangular Moving Average'

EVWMA = 'Elastic Volume Weighted Moving Average'

FAMA = 'Following Adaptive Moving Average'

FIBOWMA = 'Fibonacci Weighted Moving Average'

FISHLSMA = 'Fisher Least Squares Moving Average'

FRAMA = 'Fractal Adaptive Moving Average'

GMA = 'Geometric Moving Average'

HKAMA = 'Hilbert based Kaufman\'s Adaptive Moving Average'

HMA = 'Hull Moving Average'

JURIK = 'Jurik Moving Average'

KAMA = 'Kaufman\'s Adaptive Moving Average'

LC_LSMA = '1LC-LSMA (1 line code lsma with 3 functions)'

LEOMA = 'Leo Moving Average'

LINWMA = 'Linear Weighted Moving Average'

LSMA = 'Least Squares Moving Average'

MAMA = 'MESA Adaptive Moving Average'

MCMA = 'McNicholl Moving Average'

MEDIAN = 'Median'

REGMA = 'Regularized Exponential Moving Average'

REMA = 'Range EMA'

REPMA = 'Repulsion Moving Average'

RMA = 'Relative Moving Average'

RSIMA = 'RSI Moving average'

RVWAP = '* Rolling VWAP'

SMA = 'Simple Moving Average'

SMMA = 'Smoothed Moving Average'

SRWMA = 'Square Root Weighted Moving Average'

SW_MA = 'Sine-Weighted Moving Average'

SWMA = '* Symmetrically Weighted Moving Average'

TEMA = 'Triple Exponential Moving Average'

THMA = 'Triple Hull Moving Average'

TREMA = 'Triangular Exponential Moving Average'

TRSMA = 'Triangular Simple Moving Average'

TT3 = 'Tillson T3'

VAMA = 'Volatility Adjusted Moving Average'

VIDYA = 'Variable Index Dynamic Average'

VWAP = '* VWAP'

VWMA = 'Volume-weighted Moving Average'