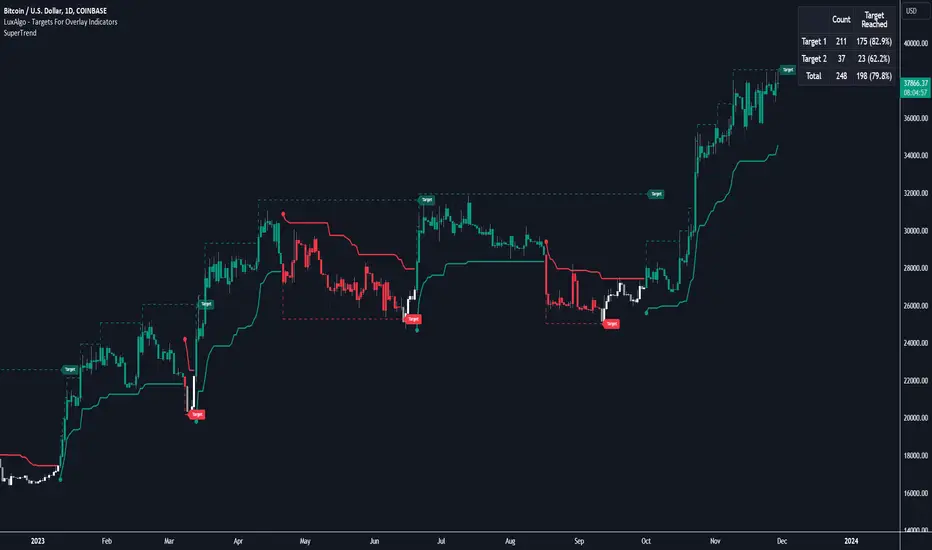

Targets For Overlay Indicators [LuxAlgo]The Targets For Overlay Indicators is a useful utility tool able to display targets during crossings made between the price and external indicators on the user chart. Users can display a series of two targets, one for crossover events and another one for crossunder event.

Alerts are included for the occurrence of a new target as well as for reached targets.

🔶 USAGE

In order for targets to be displayed users need to select an appropriate input source from the "Source" drop-down input setting. In the example above we apply the indicator to a volatility stop.

This can also easily be done by adding the "Targets For Overlay Indicators" script on the VStop indicator directly.

Targets can help users determine the price limit where the price might start deviating from an indication given by one or multiple indicators. In the context of trading, targets can help secure profits/reduce losses of a trade, as such this tool can be useful to evaluate/determine user take profits/stop losses.

Due to these essentially being horizontal levels, they can also serve as potential support/resistances, with breakouts potentially confirming new trends.

Users might be interested in obtaining new targets once one is reached, this can be done by enabling "New Target When Reached" in the target logic setting section, resulting in more frequent targets.

Lastly, users can restrict new target creation until current ones are reached. This can result in fewer and longer-term targets, with a higher reach rate.

🔹 Examples

The indicator can be applied to many overlay indicators that naturally produce crosses with the price, such as moving average, trailing stops, bands...etc.

Users can use trailing stops such as the SuperTrend or VStop to more easily create clean targets. Do note that certain SuperTrend scripts separate the upper and lower extremities of the SuperTrend into two different plot, which cannot be used with this tool, you may use the provided SuperTrend script below to have a compatible version with our tool:

//@version=5

indicator("SuperTrend", overlay = true)

factor = input.float(3, 'Factor', minval = 0)

atrLen = input.int(10, 'ATR Length', minval = 1)

= ta.supertrend(factor, atrLen)

plot(spt, 'SuperTrend', dir != dir ? na : dir < 0 ? #089981 : #f23645, 2)

plot(spt, 'Circles', dir > dir ? #f23645 : dir < dir ? #089981 : na, 3, plot.style_circles)

Using moving averages can produce more targets than other overlay indicators.

Users can apply the tool twice when using bands or any overlay indicator returning two outputs, using crossover targets for obtaining targets using the upper band as source and crossunder targets for targets using the lower band. We can also use the Trendlines with breaks indicator as example:

🔹 Dashboard

A dashboard is displayed on the top right of the chart, displaying the amount, reach rate of targets 1/2, and total amount.

This dashboard can be useful to evaluate the selected target distances relative to the selected conditions, with a higher reach rate suggesting the distance of the targets from the price allows them to be reached.

🔶 SETTINGS

Source: Indicator source used to create targets. Targets are created when the closing price crosses the specified source.

Show Target Labels: Display target labels on the chart.

Candle Coloring: Apply candle coloring based on the most recent active target.

🔹 Target

Crossover and Crossunder targets use the same settings below:

Show Target: Determines if the target is displayed or not.

Above Price Target: If selected, will create targets above the closing price.

Wait Until Reached: When enabled will not create a new target until an existing one is reached.

New Target When Reached: Will create a new target when an existing one is reached.

Evaluate Wicks: Will use high/low prices to determine if a target is reached. Unselecting this setting will use the closing price.

Target Distance From Price: Controls the distance of a target from the price. Can be determined in currencies/points, percentages, ATR multiples, or ticks.

Cari dalam skrip untuk "one一季度财报"

Dual_MACD_trendingINFO:

This indicator is useful for trending assets, as my preference is for low-frequency trading, thus using BTCUSD on 1D/1W chart

In the current implementation I find two possible use cases for the indicator:

- as a stand-alone indicator on the chart which can also fire alerts that can help to determine if we want to manually enter/exit trades based on the signals from it (1D/1W is good for non-automated trading)

- can be used to connect to the Signal input of the TTS (TempalteTradingStrategy) by jason5480 in order to backtest it, thus effectively turning it into a strategy (instructions below in TTS CONNECTIVITY section)

Trading period can be selected from the indicator itself to limit to more interesting periods.

Arrow indications are drawn on the chart to indicate the trading conditions met in the script - light green for HTF crossover, dark green for LTF crossover and orange for LTF crossunder.

Note that the indicator performs best in trending assets and markets, and it is advisable to use additional indicators to filter the trading conditions when market/asset is expected to move sideways.

DETAILS:

It uses a couple of MACD indicators - one from the current timeframe and one from a higher timeframe, as the crossover/crossunder cases of the MACD line and the signal line indicate the potential entry/exit points.

The strategy has the following flow:

- If the weekly MACD is positive (MACD line is over the signal line) we have a trading window.

- If we have a trading window, we buy when the daily macd line crosses AND closes above the signal line.

- If we are in a position, we await the daily MACD to cross AND close under the signal line, and only then place a stop loss under the wick of that closing candle.

The user can select both the higher (HTF) and lower (LTF) timeframes. Preferably the lower timeframe should be the one that the Chart is on for better visualization.

If one to decide to use the indicator as a strategy, it implements the following buy and sell criterias, which are feed to the TTS, but can be also manually managed via adding alerts from this indicator.

Since usually the LTF is preceeding the crossover compared to the HTF, then my interpretation of the strategy and flow that it follows is allowing two different ways to enter a trade:

- crossover (and bar close) of the macd over the signal line in the HIGH TIMEFRAME (no need to look at the LOWER TIMEFRMAE)

- crossover (and bar close) of the macd over the signal line in the LOW TIMEFRAME, as in this case we need to check also that the macd line is over the signal line for the HIGH TIMEFRAME as well (like a regime filter)

The exit of the trade is based on the lower timeframe MACD only, as we create a stop loss equal to the lower wick of the bar, once the macd line crosses below the signal line on that timeframe

SETTINGS:

All of the indicator's settings are for the vanilla/general case.

User can set all of the MACD parameters for both the higher and lower (current) timeframes, currently left to default of the MACD stand-alone indicator itself.

The start-end date is a time filter that can be extermely usefull when backtesting different time periods.

TTS SETTINGS (NEEDED IF USED TO BACKTEST WITH TTS)

The TempalteTradingStrategy is a strategy script developed in Pine by jason5480, which I recommend for quick turn-around of testing different ideas on a proven and tested framework

I cannot give enough credit to the developer for the efforts put in building of the infrastructure, so I advice everyone that wants to use it first to get familiar with the concept and by checking

by checking jason5480's profile www.tradingview.com

The TTS itself is extremely functional and have a lot of properties, so its functionality is beyond the scope of the current script -

Again, I strongly recommend to be thoroughly epxlored by everyone that plans on using it.

In the nutshell it is a script that can be feed with buy/sell signals from an external indicator script and based on many configuration options it can determine how to execute the trades.

The TTS has many settings that can be applied, so below I will cover only the ones that differ from the default ones, at least according to my testing - do your own research, you may find something even better :)

The current/latest version that I've been using as of writing and testing this script is TTSv48

Settings which differ from the default ones:

- from - False (time filter is from the indicator script itself)

- Deal Conditions Mode - External (take enter/exit conditions from an external script)

- 🔌Signal 🛈➡ - Dual_MACD: 🔌Signal to TTSv48 (this is the output from the indicator script, according to the TTS convention)

- Sat/Sun - true (for crypto, in order to trade 24/7)

- Order Type - STOP (perform stop order)

- Distance Method - HHLL (HigherHighLowerLow - in order to set the SL according to the strategy definition from above)

The next are just personal preferenes, you can feel free to experiment according to your trading style

- Take Profit Targets - 0 (either 100% in or out, no incremental stepping in or out of positions)

- Dist Mul|Len Long/Short- 10 (make sure that we don't close on profitable trades by any reason)

- Quantity Method - EQUITY (personal backtesting preference is to consider each backtest as a separate portfolio, so determine the position size by 100% of the allocated equity size)

- Equity % - 100 (note above)

EXAMPLES:

If used as a stand-alone indicator, the green arrows on the bottom will represent:

- light green - MACD line crossover signal line in the HTF

- darker green - MACD line crossover signal line in the LTF

- orange - MACD line crossunder signal line in the LTF

I recommend enabling the alerts from the script to cover those cases.

If used as an input to the TTS, we'll get more decorations on the chart from the TTS itself.

In the example below we open a trade on the next day of LTF crossover, then a few days later a crossunder in the LTF occurs, so we set a SL at the low of the wick of this day. Few days later the price doesn't recover and hits that SL, so the position is closed.

Renko StrategyRENKO STRATEGY

CAUTION : This strategy must be applied to a candlestick chart (not a Renko chart).

INTRODUCTION :

The Traditional Renko chart has been reproduced and is plotted according to the evolution of the price. It will enable us to receive buy or sell signals and follow major trends. This is a medium/long term strategy and depends a lot on the box size chosen in the parameters. There's also a money management method allowing us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RENKO CHART :

Renko chart construction methodology :

The user must first choose the box size. The minimum is 0.00001 and there is no maximum. The default is 10. The user must then choose the source that will define the data on which the calculations will be based (high, low, open, close). By default, close is selected. The first candle on the chart is used to draw the first box with its high and low.

Each time the price changes by the amount of the box size relative to the high or low of the last box, a new box is added above or below the previous one. If price variations are less than the box size, the same box is added next to the previous one. If price variations are N (integer number) times greater than box size, N boxes are added above or below the previous one. Each box added above the previous one is a green box, while each box added below the previous one is a red box.

Conditions for drawing a green box above the previous one :

(source - high_of_the_last_box) / box_size > 1

Condition for drawing a red box below the previous one :

(low_of_the_last_box - source) / box_size > 1

If neither condition is triggered, the same box is drawn next to the previous one.

Example :

The last candle has drawn a box with low 12 and high 14. The box size is therefore 2. The strategy will look at the value of the close each time a candle ends. The current candle closes with a close equal to 15.5. As the variation from the previous high is only 1.5 (which is less than the box size), the same box is added next to the previous one. The next candle closes at 16.2. The price variation is therefore 2.2 compared with the previous high. We can now add a new green box just above the previous one, with a low of 14 and a high of 16. The same process applies if the candle's close is at least one box size below the low of the last box. In this case, a new red box is placed below the previous one.

PARAMETERS :

Source : Allows you to specify which data will be taken into account by the strategy when performing calculations. The default is close.

Box size : Size of Renko graph boxes. This is a very important parameter to choose carefully, as it has a strong impact on the strategy's performance. Defaults to 10.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. The default is 400, meaning that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test all possible box sizes to find out which one generates the highest return on BITSTAMP:LTCUSD while limiting the drawdown. This strategy is the most optimal with a box size equal to 5.08 in 8h timeframe.

BUY AND SHORT SIGNALS :

As the aim of this strategy is to follow major trends based on price movements, we need to be on the right side of price fluctuation. We trade every box reversal, i.e. we are LONG when the boxes are green indicating an uptrend and SHORT when they are red indicating a downtrend.

RISK MANAGEMENT :

This strategy can incur losses. The size of the box is decisive, as it is used to plot the RENKO chart and thus trigger buy or sell signals. It's also what allows us to manage risk. For every trade, we risk a maximum amount equal to 2 times the size of the box, i.e. :(5.08*2*nb_contract)/trade_value.

MONEY MANAGEMENT :

The fixed ratio method has been used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy not only increases our performance, but also our drawdown.

Enjoy the strategy and don't forget to take the trade :)

Supertrend x4 w/ Cloud FillSuperTrend is one of the most common ATR based trailing stop indicators.

The average true range (ATR) plays an important role in 'Supertrend' as the indicator uses ATR to calculate its value. The ATR indicator signals the degree of price volatility. In this version you can change the ATR calculation method from the settings. Default method is RMA, when the alternative method is SMA.

The indicator is easy to use and gives an accurate reading about an ongoing trend. It is constructed with two parameters, namely period and multiplier.

The implementation of 4 supertrends and cloud fills allows for a better overall picture of the higher and lower timeframe trend one is trading a particular security in.

The default values used while constructing a supertrend indicator is 10 for average true range or trading period.

The key aspect what differentiates this indicator is the Multiplier. The multiplier is based on how much bigger of a range you want to capture. In our case by default, it starts with 2.636 and 3.336 for Set 1 & Set 2 respectively giving a narrow band range or Short Term (ST) timeframe visual. On the other hand, the multipliers for Set 3 & Set 4 goes up to 9.736 and 8.536 for the multiplier respectively giving a large band range or Long Term (LT) timeframe visual.

A ‘Supertrend’ indicator can be used on equities, futures or forex, or even crypto markets and also on minutes, hourly, daily, and weekly charts as well, but generally, it fails in a sideways-moving market. That's why with this implementation it enables one to stay out of the market if they choose to do so when the market is ranging.

This Supertrend indicator is modelled around trends and areas of interest versus buy and sell signals. Therefore, to better understand this indicator, one must calibrate it to one's need first, which means day trader (shorter timeframe) vs swing trader (longer time frame), and then understand how it can be utilized to improve your entries, exits, risk and position sizing.

Example:

In this chart shown above using SPX500:OANDA, 15R Time Frame, we can see that there is at any give time 1 to 4 clouds/bands of Supertrends. These four are called Set 1, Set 2, Set 3 and Set 4 in the indicator. Set's 1 & 2 are considered short term, whereas Set's 3 & 4 are considered long term. The term short and long are subjective based on one's trading style. For instance, if a person is a 1min chart trader, which would be short term, to get an idea of the trend you would have to look at a longer time frame like a 5min for instance. Similarly, in this cases the timeframes = Multiplier value that you set.

Optional Ideas:

+ Apply some basic EMA/SMA indicator script of your choice for easier understanding of the trend or to allow smooth transition to using this indicator.

+ Split the chart into two vertical layouts and applying this same script coupled with xdecow's 2 WWV candle painting script on both the layouts. Now you can use the left side of the chart to show all bearish move candles only (make the bullish candles transparent) and do the opposite for the right side of the chart. This way you enhance focus to just stick to one side at a given time.

Credits:

This indicator is a derivative of the fine work done originally by KivancOzbilgic

Here is the source to his original indicator: ).

Disclaimer:

This indicator and tip is for educational and entertainment purposes only. This not does constitute to financial advice of any sort.

Strategy Myth-Busting #12 - OSGFC+SuperTrend - [MYN]This is part of a new series we are calling "Strategy Myth-Busting" where we take open public manual trading strategies and automate them. The goal is to not only validate the authenticity of the claims but to provide an automated version for traders who wish to trade autonomously.

Our 12th one is an automated version of the "The Most Powerful Tradingview Buy Sell Signal Indicator " strategy from "Power of Trading" who doesn't make any official claims but watching how he trades with this, it on the surface looked promising. The strategy author uses this on the 15 min strategy on mostly FOREX. Unfortunately as indicated by the backtest results below, we were not able to substantiate any good positive trading metrics from this, be it Profit, Markdown, Num Of Trades etc. This does seem to do okay with some entries but perhaps adding another indicator to this to filter out more noise might make it better. At least how this strategy is presented now, this is not something I recommend anyone use.

This strategy uses a combination of 2 open-source public indicators:

SuperTrend by TradingView Internal

One-Sided Gaussian Filter w/ Channels By Loxx

The SuperTrend indicator and the One-Sided Gaussian Filter complement each other by providing a more complete and accurate picture of market trends. The SuperTrend indicator is used to identify trends. It does this by calculating a moving average of the underlying securities price and then comparing the current price to the moving average. When the current price is above the moving average, the trend is considered bullish, and when it is below, the trend is considered bearish.

The One-Sided Gaussian Filter is a mathematical tool that is used to smooth out fluctuations in financial data. It does this by removing random noise from the data, making it easier to identify patterns and trends.

When the SuperTrend indicator is used in conjunction with the One-Sided Gaussian Filter, the smoothed price data generated by the filter is used as the input for the SuperTrend calculation. This provides a more accurate representation of market trends and helps to eliminate false signals generated by short-term price movements. As a result, the SuperTrend indicator is able to more accurately identify the underlying trend in the market and provide traders with a cleaner and more reliable signal to act upon.

In summary, the SuperTrend indicator and the One-Sided Gaussian Filter complement each other by providing a more accurate and reliable representation of market trends, resulting in improved performance for traders.

If you know of or have a strategy you want to see myth-busted or just have an idea for one, please feel free to message me.

Trading Rules

15 min candles

FOREX or Crypto

Stop loss at swing high/low | 1.5 risk/ratio

Long Condition

SuperTrend and OSGFC generate buy signal

Close Buy on Gaussian generating a sell signal

Short Condition

SuperTrend and OSGFC generate sell signal

Close Buy on Gaussian generating a buy signal

theme_presetsStyle Made Easy with 175 Reversable light/dark themes

Built on to of my theme engine, so any tools built with one

will work with the other.

getTheme(_input)

Get a theme by name. (see lib for copy/paste list)

Parameters:

_input : string Name of Theme to use.

apathy()

Theme preset -> "Apathy"

Returns: Theme object

apprentice()

Theme preset -> "Apprentice"

Returns: Theme object

ashes()

Theme preset -> "Ashes"

Returns: Theme object

atelier_cave()

Theme preset -> "Atelier Cave"

Returns: Theme object

atelier_dune()

Theme preset -> "Atelier Dune"

Returns: Theme object

atelier_estuary()

Theme preset -> "Atelier Estuary"

Returns: Theme object

atelier_forest()

Theme preset -> "Atelier Forest"

Returns: Theme object

atelier_heath()

Theme preset -> "Atelier Heath"

Returns: Theme object

atelier_lakeside()

Theme preset -> "Atelier Lakeside"

Returns: Theme object

atelier_plateau()

Theme preset -> "Atelier Plateau"

Returns: Theme object

atelier_savanna()

Theme preset -> "Atelier Savanna"

Returns: Theme object

atelier_seaside()

Theme preset -> "Atelier Seaside"

Returns: Theme object

atelier_sulphurpool()

Theme preset -> "Atelier Sulphurpool"

Returns: Theme object

atlas()

Theme preset -> "Atlas"

Returns: Theme object

ayu()

Theme preset -> "Ayu"

Returns: Theme object

ayu_mirage()

Theme preset -> "Ayu Mirage"

Returns: Theme object

bespin()

Theme preset -> "Bespin"

Returns: Theme object

black_metal()

Theme preset -> "Black Metal"

Returns: Theme object

black_metal_bathory()

Theme preset -> "Black Metal (bathory)"

Returns: Theme object

black_metal_burzum()

Theme preset -> "Black Metal (burzum)"

Returns: Theme object

black_metal_funeral()

Theme preset -> "Black Metal (dark Funeral)"

Returns: Theme object

black_metal_gorgoroth()

Theme preset -> "Black Metal (gorgoroth)"

Returns: Theme object

black_metal_immortal()

Theme preset -> "Black Metal (immortal)"

Returns: Theme object

black_metal_khold()

Theme preset -> "Black Metal (khold)"

Returns: Theme object

black_metal_marduk()

Theme preset -> "Black Metal (marduk)"

Returns: Theme object

black_metal_mayhem()

Theme preset -> "Black Metal (mayhem)"

Returns: Theme object

black_metal_nile()

Theme preset -> "Black Metal (nile)"

Returns: Theme object

black_metal_venom()

Theme preset -> "Black Metal (venom)"

Returns: Theme object

blue_forest()

Theme preset -> "Blue Forest"

Returns: Theme object

blueish()

Theme preset -> "Blueish"

Returns: Theme object

brewer()

Theme preset -> "Brewer"

Returns: Theme object

bright()

Theme preset -> "Bright"

Returns: Theme object

brogrammer()

Theme preset -> "Brogrammer"

Returns: Theme object

brush_trees()

Theme preset -> "Brush Trees"

Returns: Theme object

catppuccin()

Theme preset -> "Catppuccin"

Returns: Theme object

chalk()

Theme preset -> "Chalk"

Returns: Theme object

circus()

Theme preset -> "Circus"

Returns: Theme object

classic()

Theme preset -> "Classic"

Returns: Theme object

clrs()

Theme preset -> "Colors"

Returns: Theme object

codeschool()

Theme preset -> "Codeschool"

Returns: Theme object

cupcake()

Theme preset -> "Cupcake"

Returns: Theme object

cupertino()

Theme preset -> "Cupertino"

Returns: Theme object

da_one_black()

Theme preset -> "Da One Black"

Returns: Theme object

da_one_gray()

Theme preset -> "Da One Gray"

Returns: Theme object

da_one_ocean()

Theme preset -> "Da One Ocean"

Returns: Theme object

da_one_paper()

Theme preset -> "Da One Paper"

Returns: Theme object

da_one_sea()

Theme preset -> "Da One Sea"

Returns: Theme object

da_one_white()

Theme preset -> "Da One White"

Returns: Theme object

danqing()

Theme preset -> "Danqing"

Returns: Theme object

darcula()

Theme preset -> "Darcula"

Returns: Theme object

dark_violet()

Theme preset -> "Dark Violet"

Returns: Theme object

darkmoss()

Theme preset -> "Darkmoss"

Returns: Theme object

darktooth()

Theme preset -> "Darktooth"

Returns: Theme object

decaf()

Theme preset -> "Decaf"

Returns: Theme object

dirtysea()

Theme preset -> "Dirtysea"

Returns: Theme object

dracula()

Theme preset -> "Dracula"

Returns: Theme object

edge()

Theme preset -> "Edge"

Returns: Theme object

eighties()

Theme preset -> "Eighties"

Returns: Theme object

embers()

Theme preset -> "Embers"

Returns: Theme object

emil()

Theme preset -> "Emil"

Returns: Theme object

equilibrium()

Theme preset -> "Equilibrium"

Returns: Theme object

equilibrium_gray()

Theme preset -> "Equilibrium Gray"

Returns: Theme object

espresso()

Theme preset -> "Espresso"

Returns: Theme object

eva()

Theme preset -> "Eva"

Returns: Theme object

everforest()

Theme preset -> "Everforest"

Returns: Theme object

flat()

Theme preset -> "Flat"

Returns: Theme object

framer()

Theme preset -> "Framer"

Returns: Theme object

fruit_soda()

Theme preset -> "Fruit Soda"

Returns: Theme object

gigavolt()

Theme preset -> "Gigavolt"

Returns: Theme object

github()

Theme preset -> "Github"

Returns: Theme object

google()

Theme preset -> "Google"

Returns: Theme object

gotham()

Theme preset -> "Gotham"

Returns: Theme object

grayscale()

Theme preset -> "Grayscale"

Returns: Theme object

green_screen()

Theme preset -> "Green Screen"

Returns: Theme object

gruber()

Theme preset -> "Gruber"

Returns: Theme object

gruvbox_hard()

Theme preset -> "Gruvbox Dark, Hard"

Returns: Theme object

gruvbox_medium()

Theme preset -> "Gruvbox Dark, Medium"

Returns: Theme object

gruvbox_pale()

Theme preset -> "Gruvbox Dark, Pale"

Returns: Theme object

gruvbox_soft()

Theme preset -> "Gruvbox Dark, Soft"

Returns: Theme object

gruvbox_material_hard()

Theme preset -> "Gruvbox Material Dark, Hard"

Returns: Theme object

gruvbox_material_medium()

Theme preset -> "Gruvbox Material Dark, Medium"

Returns: Theme object

gruvbox_material_soft()

Theme preset -> "Gruvbox Material Dark, Soft"

Returns: Theme object

hardcore()

Theme preset -> "Hardcore"

Returns: Theme object

harmonic16()

Theme preset -> "Harmonic16"

Returns: Theme object

heetch()

Theme preset -> "Heetch"

Returns: Theme object

helios()

Theme preset -> "Helios"

Returns: Theme object

hopscotch()

Theme preset -> "Hopscotch"

Returns: Theme object

horizon()

Theme preset -> "Horizon"

Returns: Theme object

horizon_terminal()

Theme preset -> "Horizon Terminal"

Returns: Theme object

humanoid()

Theme preset -> "Humanoid"

Returns: Theme object

ia()

Theme preset -> "Ia"

Returns: Theme object

icy()

Theme preset -> "Icy"

Returns: Theme object

ir_black()

Theme preset -> "Ir Black"

Returns: Theme object

isotope()

Theme preset -> "Isotope"

Returns: Theme object

kanagawa()

Theme preset -> "Kanagawa"

Returns: Theme object

katy()

Theme preset -> "Katy"

Returns: Theme object

kimber()

Theme preset -> "Kimber"

Returns: Theme object

lime()

Theme preset -> "Lime"

Returns: Theme object

london_tube()

Theme preset -> "London Tube"

Returns: Theme object

macintosh()

Theme preset -> "Macintosh"

Returns: Theme object

marrakesh()

Theme preset -> "Marrakesh"

Returns: Theme object

materia()

Theme preset -> "Materia"

Returns: Theme object

material()

Theme preset -> "Material"

Returns: Theme object

materialdarker()

Theme preset -> "Material Darker"

Returns: Theme object

material_palenight()

Theme preset -> "Material Palenight"

Returns: Theme object

material_vivid()

Theme preset -> "Material Vivid"

Returns: Theme object

mellow_purple()

Theme preset -> "Mellow Purple"

Returns: Theme object

mocha()

Theme preset -> "Mocha"

Returns: Theme object

monokai()

Theme preset -> "Monokai"

Returns: Theme object

Nebula()

Theme preset -> "Nebula"

Returns: Theme object

nord()

Theme preset -> "Nord"

Returns: Theme object

nova()

Theme preset -> "Nova"

Returns: Theme object

ocean()

Theme preset -> "Ocean"

Returns: Theme object

oceanicnext()

Theme preset -> "Oceanicnext"

Returns: Theme object

onedark()

Theme preset -> "Onedark"

Returns: Theme object

outrun()

Theme preset -> "Outrun"

Returns: Theme object

pandora()

Theme preset -> "Pandora"

Returns: Theme object

papercolor()

Theme preset -> "Papercolor"

Returns: Theme object

paraiso()

Theme preset -> "Paraiso"

Returns: Theme object

pasque()

Theme preset -> "Pasque"

Returns: Theme object

phd()

Theme preset -> "Phd"

Returns: Theme object

pico()

Theme preset -> "Pico"

Returns: Theme object

pinky()

Theme preset -> "Pinky"

Returns: Theme object

pop()

Theme preset -> "Pop"

Returns: Theme object

porple()

Theme preset -> "Porple"

Returns: Theme object

primer()

Theme preset -> "Primer"

Returns: Theme object

purpledream()

Theme preset -> "Purpledream"

Returns: Theme object

qualia()

Theme preset -> "Qualia"

Returns: Theme object

railscasts()

Theme preset -> "Railscasts"

Returns: Theme object

rebecca()

Theme preset -> "Rebecca"

Returns: Theme object

rose_pine()

Theme preset -> "Rosé Pine"

Returns: Theme object

rose_pine_dawn()

Theme preset -> "Rosé Pine Dawn"

Returns: Theme object

rose_pine_moon()

Theme preset -> "Rosé Pine Moon"

Returns: Theme object

sagelight()

Theme preset -> "Sagelight"

Returns: Theme object

sakura()

Theme preset -> "Sakura"

Returns: Theme object

sandcastle()

Theme preset -> "Sandcastle"

Returns: Theme object

seti_ui()

Theme preset -> "Seti Ui"

Returns: Theme object

shades_of_purple()

Theme preset -> "Shades Of Purple"

Returns: Theme object

shadesmear()

Theme preset -> "Shadesmear"

Returns: Theme object

shapeshifter()

Theme preset -> "Shapeshifter"

Returns: Theme object

silk()

Theme preset -> "Silk"

Returns: Theme object

snazzy()

Theme preset -> "Snazzy"

Returns: Theme object

solar_flare()

Theme preset -> "Solar Flare"

Returns: Theme object

solarized()

Theme preset -> "Solarized"

Returns: Theme object

spaceduck()

Theme preset -> "Spaceduck"

Returns: Theme object

spacemacs()

Theme preset -> "Spacemacs"

Returns: Theme object

stella()

Theme preset -> "Stella"

Returns: Theme object

still_alive()

Theme preset -> "Still Alive"

Returns: Theme object

summercamp()

Theme preset -> "Summercamp"

Returns: Theme object

summerfruit()

Theme preset -> "Summerfruit"

Returns: Theme object

synth_midnight_terminal()

Theme preset -> "Synth Midnight Terminal"

Returns: Theme object

tango()

Theme preset -> "Tango"

Returns: Theme object

tender()

Theme preset -> "Tender"

Returns: Theme object

tokyo_city()

Theme preset -> "Tokyo City"

Returns: Theme object

tokyo_city_terminal()

Theme preset -> "Tokyo City Terminal"

Returns: Theme object

tokyo_night()

Theme preset -> "Tokyo Night"

Returns: Theme object

tokyo_night_storm()

Theme preset -> "Tokyo Night Storm"

Returns: Theme object

tokyo_night_terminal()

Theme preset -> "Tokyo Night Terminal"

Returns: Theme object

tokyo_night_terminal_storm()

Theme preset -> "Tokyo Night Terminal Storm"

Returns: Theme object

tokyodark()

Theme preset -> "Tokyodark"

Returns: Theme object

tokyodark_terminal()

Theme preset -> "Tokyodark Terminal"

Returns: Theme object

tomorrow()

Theme preset -> "Tomorrow"

Returns: Theme object

tomorrow_night()

Theme preset -> "Tomorrow Night"

Returns: Theme object

tomorrow_night_eighties()

Theme preset -> "Tomorrow Night Eighties"

Returns: Theme object

twilight()

Theme preset -> "Twilight"

Returns: Theme object

unikitty()

Theme preset -> "Unikitty"

Returns: Theme object

unikitty_reversible()

Theme preset -> "Unikitty Reversible"

Returns: Theme object

uwunicorn()

Theme preset -> "Uwunicorn"

Returns: Theme object

vice()

Theme preset -> "Vice"

Returns: Theme object

vulcan()

Theme preset -> "Vulcan"

Returns: Theme object

windows_10()

Theme preset -> "Windows 10"

Returns: Theme object

windows_95()

Theme preset -> "Windows 95"

Returns: Theme object

windows_high_contrast()

Theme preset -> "Windows High Contrast"

Returns: Theme object

windows_nt()

Theme preset -> "Windows Nt"

Returns: Theme object

woodland()

Theme preset -> "Woodland"

Returns: Theme object

xcode_dusk()

Theme preset -> "Xcode Dusk"

Returns: Theme object

VWMA/SMA 3Commas BotThis strategy utilizes two pairs of different Moving Averages, two Volume-Weighted Moving Averages (VWMA) and two Simple Moving Averages (SMA).

There is a FAST and SLOW version of each VWMA and SMA.

The concept behind this strategy is that volume is not taken into account when calculating a Simple Moving Average.

Simple Moving Averages are often used to determine the dominant direction of price movement and to help a trader look past any short-term volatility or 'noise' from price movement, and instead determine the OVERALL direction of price movement so that one can trade in that direction (trend-following) or look for opportunities to trade AGAINST that direction (fading).

By comparing the different movements of a Volume-Weighted Moving Average against a Simple Moving Average of the same length, a trader can get a better picture of what price movements are actually significant, helping to reduce false signals that might occur from only using Simple Moving Averages.

The practical applications of this strategy are identifying dominant directional trends. These can be found when the Volume Weighted Moving Average is moving in the same direction as the Simple Moving Average, and ideally, tracking above it.

This would indicate that there is sufficient volume supporting an uptrend or downtrend, and thus gives traders additional confirmation to potentially look for a trade in that direction.

One can initially look for the Fast VWMA to track above the Fast SMA as your initial sign of bullish confirmation (reversed for downtrending markets). Then, when the Fast VWMA crosses over the Slow SMA, one can determine additional trend strength. Finally, when the Slow VWMA crosses over the Slow SMA, one can determine that the trend is truly strong.

Traders can choose to look for trade entries at either of those triggers, depending on risk tolerance and risk appetite.

Furthermore, this strategy can be used to identify divergence or weakness in trending movements. This is very helpful for identifying potential areas to exit one's trade or even look for counter-trend trades (reversals).

These moments occur when the Volume-Weighted Moving Average, either fast or slow, begins to trade in the opposite direction as their Simple Moving Average counterpart.

For instance, if price has been trending upwards for awhile, and the Fast VWMA begins to trade underneath the Fast SMA, this is an indication that volume is beginning to falter. Uptrends need appropriate volume to continue moving with momentum, so when we see volume begin to falter, it can be a potential sign of an upcoming reversal in trend.

Depending on how quickly one wants to enter into a movement, one could look for crosses of the Fast VWMA under/over the Fast SMA, crosses of the Fast VWMA over/under the Slow SMA, or crosses over/under of the Slow VWMA and the Slow SMA.

This concept was originally published here on TradingView by ProfitProgrammers.

Here is a link to his original indicator script:

I have added onto this concept by:

converting the original indicator into a strategy tester for backtesting

adding the ability to conveniently test long or short strategies, or both

adding the ability to calculate dynamic position sizes

adding the ability to calculate dynamic stop losses and take profit levels using the Average True Range

adding the ability to exit trades based on overbought/oversold crosses of the Stochastic RSI

conveniently switch between different thresholds or speeds of the Moving Average crosses to test different strategies on different asset classes

easily hook this strategy up to 3Commas for automation via their DCA bot feature

Full credit to ProfitProgrammers for the original concept and idea.

Any feedback or suggestions are greatly appreciated.

Signs of the Times [LucF]█ OVERVIEW

This oscillator calculates the directional strength of bars using a primitive weighing mechanism based on a small number of what I consider to be fundamental properties of a bar. It does not consider the amplitude of price movements, so can be used as a complement to momentum-based oscillators. It thus belongs to the same family of indicators as my Bar Balance , Volume Ticks , Efficient work , Volume Buoyancy or my Delta Volume indicators.

█ CONCEPTS

The calculations underlying Signs of the Times (SOTT) use a simple, oft-explored concept: measure bar attributes, assign a weight to them, and aggregate results to provide an evaluation of a bar's directional strength. Bull and bear weights are added independently, then subtracted and divided by the maximum possible weight, so the final calculation looks like this:

(up - dn) / weightRange

SOTT has a zero centerline and oscillates between +1 and -1. Ten elementary properties are evaluated. Most carry a weight of one, a few are doubly weighted. All properties are evaluated using only the current bar's values or by comparing its values to those of the preceding bar. The bull conditions follow; their inverse applies to bear conditions:

Weight of 1

• Bar's close is greater than the bar's open (bar is considered to be of "up" polarity)

• Rising open

• Rising high

• Rising low

• Rising close

• Bar is up and its body size is greater than that of the previous bar

• Bar is up and its body size is greater than the combined size of wicks

Weight of 2

• Gap to the upside

• Efficient Work when it is positive

• Bar is up and volume is greater than that of the previous bar (this only kicks in if volume is actually available on the chart's data feed)

Except for the Efficient Work weight, which is a +1 to -1 float value multiplied by 2, all weights are discrete; either zero or the full weight of 1 or 2 is generated. This will cause any gap, for example, to generate a weight of +2 or -2, regardless of the gap's size. That is the reason why the oscillator is oblivious to the amplitude of price movements.

You can see the code used to calculate SOTT in my ta library 's `sott()` function.

█ HOW TO USE THE INDICATOR

No videos explain this indicator and none are planned; reading this description or the script's code is the only way to understand what Signs of the Times does.

Load the indicator on an active chart (see here if you don't know how).

The default configuration displays:

• An Arnaud-Legoux moving average of length 20 of the instant SOTT value. This is the signal line.

• A fill between the MA and the centerline.

• Levels at arbitrary values of +0.3 and -0.3.

• A channel between the signal line and its MA (a simple MA of length 20), which can be one of four colors:

• Bull (green): The signal line is above its MA.

• Strong bull (lime): The bull condition is fulfilled and the signal line is above the centerline.

• Bear (red): The signal line is below its MA.

• Strong bear (pink): The bear condition is fulfilled and the signal line is below the centerline.

The script's "Inputs" tab allows you to:

• Choose a higher timeframe to calculate the indicator's values. This can be useful to get a wider perspective of the indicator's values.

If you elect to use a higher timeframe, make sure that your chart's timeframe is always lower than the higher timeframe you specified,

as calculating on a timeframe lower than the chart's does not make much sense because the indicator is then displaying only the value of the last intrabar in the chart bar.

• Specify the type of MA used to produce the signal line. Use a length of 1 or the Data Window to see the instant value of SOTT. It is quite noisy, thus the need to average it.

• Specify the type of MA applied to the signal line. The idea here is to provide context to the signal.

• Control the display and colors of the lines and fills.

The first pane of this publication's chart shows the default setup. The second one shows only a monochrome signal line.

Using the "Style" tab of the indicator's settings, you can change the type and width of the lines, and the level values.

█ INTERPRETATION

Remember that Signs of the Times evaluates directional bar strength — not price movement. Its highs and lows do not reflect price, but the strength of chart bars. The fact that SOTT knows nothing of how far price moves or of trends is easy to forget. As such, I think SOTT is best used as a confirmation tool. Chart movements may appear to be easy to read when looking at historical bars, but when you have to make go-no-go decisions on the last bar, the landscape often becomes murkier. By providing a quantitative evaluation of the strength of the last few bars, which is not always easily discernible by simply looking at them, SOTT aims to help you decide if the short-term past favors the bets you are considering. Can SOTT predict the future? Of course not.

While SOTT uses completely different calculations than classical momentum oscillators, its profile shares many of their characteristics. This could lead one to infer that directional bar strength correlates with price movement, which could in turn lead one to conclude that indicators such as this one are useless, or that they can be useful tools to confirm momentum oscillators or other models of price movement. The call is, of course, up to you. You can try, for example, to compare a Wilder MA of SOTT to an RSI of the same length.

One key difference with momentum oscillators is that SOTT is much less sensitive to large price movements. The default Arnaud-Legoux MA used for the signal line makes it quite active; you can use a more quiet SMA or EMA if you prefer to tone it down.

In systems where it can be useful to only enter or exit on short-term strength, an average of SOTT values over the last 3 to 5 bars can be used as a more quiet filter than a momentum oscillator would.

█ NOTES

My publications often go through a long gestation period where I use them on my charts or in systems before deciding if they are worth a publication. With an incubation period of more than three years, Signs of the Times holds the record. The properties SOTT currently evaluates result from the systematic elimination of contaminants over that lengthy period of time. It was long because of my usual, slow gear, but also because I had to try countless combinations of conditions before realizing that, contrary to my intuition, best results were achieved by:

• Keeping the number of evaluated properties to the absolute minimum.

• Limiting the evaluation's scope to the current and preceding bar.

• Choosing properties that, in my view, were unmistakably indicative of bullish/bearish conditions.

Repainting

As most oscillators, the indicator provides live realtime values that will recalculate with chart updates. It will thus repaint in real time, but not on historical values. To learn more about repainting, see the Pine Script™ User Manual's page on the subject .

LibraryCOTLibrary "LibraryCOT"

This library provides tools to help Pine programmers fetch Commitment of Traders (COT) data for futures.

rootToCFTCCode(root)

Accepts a futures root and returns the relevant CFTC code.

Parameters:

root : Root prefix of the future's symbol, e.g. "ZC" for "ZC1!"" or "ZCU2021".

Returns: The part of a COT ticker corresponding to `root`, or "" if no CFTC code exists for the `root`.

currencyToCFTCCode(curr)

Converts a currency string to its corresponding CFTC code.

Parameters:

curr : Currency code, e.g., "USD" for US Dollar.

Returns: The corresponding to the currency, if one exists.

optionsToTicker(includeOptions)

Returns the part of a COT ticker using the `includeOptions` value supplied, which determines whether options data is to be included.

Parameters:

includeOptions : A "bool" value: 'true' if the symbol should include options and 'false' otherwise.

Returns: The part of a COT ticker: "FO" for data that includes options and "F" for data that doesn't.

metricNameAndDirectionToTicker(metricName, metricDirection)

Returns a string corresponding to a metric name and direction, which is one component required to build a valid COT ticker ID.

Parameters:

metricName : One of the metric names listed in this library's chart. Invalid values will cause a runtime error.

metricDirection : Metric direction. Possible values are: "Long", "Short", "Spreading", and "No direction". Valid values vary with metrics. Invalid values will cause a runtime error.

Returns: The part of a COT ticker ID string, e.g., "OI_OLD" for "Open Interest" and "No direction", or "TC_L" for "Traders Commercial" and "Long".

typeToTicker(metricType)

Converts a metric type into one component required to build a valid COT ticker ID. See the "Old and Other Futures" section of the CFTC's Explanatory Notes for details on types.

Parameters:

metricType : Metric type. Accepted values are: "All", "Old", "Other".

Returns: The part of a COT ticker.

convertRootToCOTCode(mode, convertToCOT)

Depending on the `mode`, returns a CFTC code using the chart's symbol or its currency information when `convertToCOT = true`. Otherwise, returns the symbol's root or currency information. If no COT data exists, a runtime error is generated.

Parameters:

mode : A string determining how the function will work. Valid values are:

"Root": the function extracts the futures symbol root (e.g. "ES" in "ESH2020") and looks for its CFTC code.

"Base currency": the function extracts the first currency in a pair (e.g. "EUR" in "EURUSD") and looks for its CFTC code.

"Currency": the function extracts the quote currency ("JPY" for "TSE:9984" or "USDJPY") and looks for its CFTC code.

"Auto": the function tries the first three modes (Root -> Base Currency -> Currency) until a match is found.

convertToCOT : "bool" value that, when `true`, causes the function to return a CFTC code. Otherwise, the root or currency information is returned. Optional. The default is `true`.

Returns: If `convertToCOT` is `true`, the part of a COT ticker ID string. If `convertToCOT` is `false`, the root or currency extracted from the current symbol.

COTTickerid(COTType, CTFCCode, includeOptions, metricName, metricDirection, metricType)

Returns a valid TradingView ticker for the COT symbol with specified parameters.

Parameters:

COTType : A string with the type of the report requested with the ticker, one of the following: "Legacy", "Disaggregated", "Financial".

CTFCCode : The for the asset, e.g., wheat futures (root "ZW") have the code "001602".

includeOptions : A boolean value. 'true' if the symbol should include options and 'false' otherwise.

metricName : One of the metric names listed in this library's chart.

metricDirection : Direction of the metric, one of the following: "Long", "Short", "Spreading", "No direction".

metricType : Type of the metric. Possible values: "All", "Old", and "Other".

Returns: A ticker ID string usable with `request.security()` to fetch the specified Commitment of Traders data.

R-squared Adaptive T3 Ribbon Filled Simple [Loxx]R-squared Adaptive T3 Ribbon Filled Simple is a T3 ribbons indicator that uses a special implementation of T3 that is R-squared adaptive.

What is the T3 moving average?

Better Moving Averages Tim Tillson

November 1, 1998

Tim Tillson is a software project manager at Hewlett-Packard, with degrees in Mathematics and Computer Science. He has privately traded options and equities for 15 years.

Introduction

"Digital filtering includes the process of smoothing, predicting, differentiating, integrating, separation of signals, and removal of noise from a signal. Thus many people who do such things are actually using digital filters without realizing that they are; being unacquainted with the theory, they neither understand what they have done nor the possibilities of what they might have done."

This quote from R. W. Hamming applies to the vast majority of indicators in technical analysis . Moving averages, be they simple, weighted, or exponential, are lowpass filters; low frequency components in the signal pass through with little attenuation, while high frequencies are severely reduced.

"Oscillator" type indicators (such as MACD , Momentum, Relative Strength Index ) are another type of digital filter called a differentiator.

Tushar Chande has observed that many popular oscillators are highly correlated, which is sensible because they are trying to measure the rate of change of the underlying time series, i.e., are trying to be the first and second derivatives we all learned about in Calculus.

We use moving averages (lowpass filters) in technical analysis to remove the random noise from a time series, to discern the underlying trend or to determine prices at which we will take action. A perfect moving average would have two attributes:

It would be smooth, not sensitive to random noise in the underlying time series. Another way of saying this is that its derivative would not spuriously alternate between positive and negative values.

It would not lag behind the time series it is computed from. Lag, of course, produces late buy or sell signals that kill profits.

The only way one can compute a perfect moving average is to have knowledge of the future, and if we had that, we would buy one lottery ticket a week rather than trade!

Having said this, we can still improve on the conventional simple, weighted, or exponential moving averages. Here's how:

Two Interesting Moving Averages

We will examine two benchmark moving averages based on Linear Regression analysis.

In both cases, a Linear Regression line of length n is fitted to price data.

I call the first moving average ILRS, which stands for Integral of Linear Regression Slope. One simply integrates the slope of a linear regression line as it is successively fitted in a moving window of length n across the data, with the constant of integration being a simple moving average of the first n points. Put another way, the derivative of ILRS is the linear regression slope. Note that ILRS is not the same as a SMA ( simple moving average ) of length n, which is actually the midpoint of the linear regression line as it moves across the data.

We can measure the lag of moving averages with respect to a linear trend by computing how they behave when the input is a line with unit slope. Both SMA (n) and ILRS(n) have lag of n/2, but ILRS is much smoother than SMA .

Our second benchmark moving average is well known, called EPMA or End Point Moving Average. It is the endpoint of the linear regression line of length n as it is fitted across the data. EPMA hugs the data more closely than a simple or exponential moving average of the same length. The price we pay for this is that it is much noisier (less smooth) than ILRS, and it also has the annoying property that it overshoots the data when linear trends are present.

However, EPMA has a lag of 0 with respect to linear input! This makes sense because a linear regression line will fit linear input perfectly, and the endpoint of the LR line will be on the input line.

These two moving averages frame the tradeoffs that we are facing. On one extreme we have ILRS, which is very smooth and has considerable phase lag. EPMA has 0 phase lag, but is too noisy and overshoots. We would like to construct a better moving average which is as smooth as ILRS, but runs closer to where EPMA lies, without the overshoot.

A easy way to attempt this is to split the difference, i.e. use (ILRS(n)+EPMA(n))/2. This will give us a moving average (call it IE /2) which runs in between the two, has phase lag of n/4 but still inherits considerable noise from EPMA. IE /2 is inspirational, however. Can we build something that is comparable, but smoother? Figure 1 shows ILRS, EPMA, and IE /2.

Filter Techniques

Any thoughtful student of filter theory (or resolute experimenter) will have noticed that you can improve the smoothness of a filter by running it through itself multiple times, at the cost of increasing phase lag.

There is a complementary technique (called twicing by J.W. Tukey) which can be used to improve phase lag. If L stands for the operation of running data through a low pass filter, then twicing can be described by:

L' = L(time series) + L(time series - L(time series))

That is, we add a moving average of the difference between the input and the moving average to the moving average. This is algebraically equivalent to:

2L-L(L)

This is the Double Exponential Moving Average or DEMA , popularized by Patrick Mulloy in TASAC (January/February 1994).

In our taxonomy, DEMA has some phase lag (although it exponentially approaches 0) and is somewhat noisy, comparable to IE /2 indicator.

We will use these two techniques to construct our better moving average, after we explore the first one a little more closely.

Fixing Overshoot

An n-day EMA has smoothing constant alpha=2/(n+1) and a lag of (n-1)/2.

Thus EMA (3) has lag 1, and EMA (11) has lag 5. Figure 2 shows that, if I am willing to incur 5 days of lag, I get a smoother moving average if I run EMA (3) through itself 5 times than if I just take EMA (11) once.

This suggests that if EPMA and DEMA have 0 or low lag, why not run fast versions (eg DEMA (3)) through themselves many times to achieve a smooth result? The problem is that multiple runs though these filters increase their tendency to overshoot the data, giving an unusable result. This is because the amplitude response of DEMA and EPMA is greater than 1 at certain frequencies, giving a gain of much greater than 1 at these frequencies when run though themselves multiple times. Figure 3 shows DEMA (7) and EPMA(7) run through themselves 3 times. DEMA^3 has serious overshoot, and EPMA^3 is terrible.

The solution to the overshoot problem is to recall what we are doing with twicing:

DEMA (n) = EMA (n) + EMA (time series - EMA (n))

The second term is adding, in effect, a smooth version of the derivative to the EMA to achieve DEMA . The derivative term determines how hot the moving average's response to linear trends will be. We need to simply turn down the volume to achieve our basic building block:

EMA (n) + EMA (time series - EMA (n))*.7;

This is algebraically the same as:

EMA (n)*1.7-EMA( EMA (n))*.7;

I have chosen .7 as my volume factor, but the general formula (which I call "Generalized Dema") is:

GD (n,v) = EMA (n)*(1+v)-EMA( EMA (n))*v,

Where v ranges between 0 and 1. When v=0, GD is just an EMA , and when v=1, GD is DEMA . In between, GD is a cooler DEMA . By using a value for v less than 1 (I like .7), we cure the multiple DEMA overshoot problem, at the cost of accepting some additional phase delay. Now we can run GD through itself multiple times to define a new, smoother moving average T3 that does not overshoot the data:

T3(n) = GD ( GD ( GD (n)))

In filter theory parlance, T3 is a six-pole non-linear Kalman filter. Kalman filters are ones which use the error (in this case (time series - EMA (n)) to correct themselves. In Technical Analysis , these are called Adaptive Moving Averages; they track the time series more aggressively when it is making large moves.

What is R-squared Adaptive?

One tool available in forecasting the trendiness of the breakout is the coefficient of determination ( R-squared ), a statistical measurement.

The R-squared indicates linear strength between the security's price (the Y - axis) and time (the X - axis). The R-squared is the percentage of squared error that the linear regression can eliminate if it were used as the predictor instead of the mean value. If the R-squared were 0.99, then the linear regression would eliminate 99% of the error for prediction versus predicting closing prices using a simple moving average .

R-squared is used here to derive a T3 factor used to modify price before passing price through a six-pole non-linear Kalman filter.

Included:

Alerts

Signals

Loxx's Expanded Source Types

T3 Volatility Quality Index (VQI) w/ DSL & Pips Filtering [Loxx]T3 Volatility Quality Index (VQI) w/ DSL & Pips Filtering is a VQI indicator that uses T3 smoothing and discontinued signal lines to determine breakouts and breakdowns. This also allows filtering by pips.***

What is the Volatility Quality Index ( VQI )?

The idea behind the volatility quality index is to point out the difference between bad and good volatility in order to identify better trade opportunities in the market. This forex indicator works using the True Range algorithm in combination with the open, close, high and low prices.

What are DSL Discontinued Signal Line?

A lot of indicators are using signal lines in order to determine the trend (or some desired state of the indicator) easier. The idea of the signal line is easy : comparing the value to it's smoothed (slightly lagging) state, the idea of current momentum/state is made.

Discontinued signal line is inheriting that simple signal line idea and it is extending it : instead of having one signal line, more lines depending on the current value of the indicator.

"Signal" line is calculated the following way :

When a certain level is crossed into the desired direction, the EMA of that value is calculated for the desired signal line

When that level is crossed into the opposite direction, the previous "signal" line value is simply "inherited" and it becomes a kind of a level

This way it becomes a combination of signal lines and levels that are trying to combine both the good from both methods.

In simple terms, DSL uses the concept of a signal line and betters it by inheriting the previous signal line's value & makes it a level.

What is the T3 moving average?

Better Moving Averages Tim Tillson

November 1, 1998

Tim Tillson is a software project manager at Hewlett-Packard, with degrees in Mathematics and Computer Science. He has privately traded options and equities for 15 years.

Introduction

"Digital filtering includes the process of smoothing, predicting, differentiating, integrating, separation of signals, and removal of noise from a signal. Thus many people who do such things are actually using digital filters without realizing that they are; being unacquainted with the theory, they neither understand what they have done nor the possibilities of what they might have done."

This quote from R. W. Hamming applies to the vast majority of indicators in technical analysis . Moving averages, be they simple, weighted, or exponential, are lowpass filters; low frequency components in the signal pass through with little attenuation, while high frequencies are severely reduced.

"Oscillator" type indicators (such as MACD , Momentum, Relative Strength Index ) are another type of digital filter called a differentiator.

Tushar Chande has observed that many popular oscillators are highly correlated, which is sensible because they are trying to measure the rate of change of the underlying time series, i.e., are trying to be the first and second derivatives we all learned about in Calculus.

We use moving averages (lowpass filters) in technical analysis to remove the random noise from a time series, to discern the underlying trend or to determine prices at which we will take action. A perfect moving average would have two attributes:

It would be smooth, not sensitive to random noise in the underlying time series. Another way of saying this is that its derivative would not spuriously alternate between positive and negative values.

It would not lag behind the time series it is computed from. Lag, of course, produces late buy or sell signals that kill profits.

The only way one can compute a perfect moving average is to have knowledge of the future, and if we had that, we would buy one lottery ticket a week rather than trade!

Having said this, we can still improve on the conventional simple, weighted, or exponential moving averages. Here's how:

Two Interesting Moving Averages

We will examine two benchmark moving averages based on Linear Regression analysis.

In both cases, a Linear Regression line of length n is fitted to price data.

I call the first moving average ILRS, which stands for Integral of Linear Regression Slope. One simply integrates the slope of a linear regression line as it is successively fitted in a moving window of length n across the data, with the constant of integration being a simple moving average of the first n points. Put another way, the derivative of ILRS is the linear regression slope. Note that ILRS is not the same as a SMA ( simple moving average ) of length n, which is actually the midpoint of the linear regression line as it moves across the data.

We can measure the lag of moving averages with respect to a linear trend by computing how they behave when the input is a line with unit slope. Both SMA (n) and ILRS(n) have lag of n/2, but ILRS is much smoother than SMA .

Our second benchmark moving average is well known, called EPMA or End Point Moving Average. It is the endpoint of the linear regression line of length n as it is fitted across the data. EPMA hugs the data more closely than a simple or exponential moving average of the same length. The price we pay for this is that it is much noisier (less smooth) than ILRS, and it also has the annoying property that it overshoots the data when linear trends are present.

However, EPMA has a lag of 0 with respect to linear input! This makes sense because a linear regression line will fit linear input perfectly, and the endpoint of the LR line will be on the input line.

These two moving averages frame the tradeoffs that we are facing. On one extreme we have ILRS, which is very smooth and has considerable phase lag. EPMA has 0 phase lag, but is too noisy and overshoots. We would like to construct a better moving average which is as smooth as ILRS, but runs closer to where EPMA lies, without the overshoot.

A easy way to attempt this is to split the difference, i.e. use (ILRS(n)+EPMA(n))/2. This will give us a moving average (call it IE /2) which runs in between the two, has phase lag of n/4 but still inherits considerable noise from EPMA. IE /2 is inspirational, however. Can we build something that is comparable, but smoother? Figure 1 shows ILRS, EPMA, and IE /2.

Filter Techniques

Any thoughtful student of filter theory (or resolute experimenter) will have noticed that you can improve the smoothness of a filter by running it through itself multiple times, at the cost of increasing phase lag.

There is a complementary technique (called twicing by J.W. Tukey) which can be used to improve phase lag. If L stands for the operation of running data through a low pass filter, then twicing can be described by:

L' = L(time series) + L(time series - L(time series))

That is, we add a moving average of the difference between the input and the moving average to the moving average. This is algebraically equivalent to:

2L-L(L)

This is the Double Exponential Moving Average or DEMA , popularized by Patrick Mulloy in TASAC (January/February 1994).

In our taxonomy, DEMA has some phase lag (although it exponentially approaches 0) and is somewhat noisy, comparable to IE /2 indicator.

We will use these two techniques to construct our better moving average, after we explore the first one a little more closely.

Fixing Overshoot

An n-day EMA has smoothing constant alpha=2/(n+1) and a lag of (n-1)/2.

Thus EMA (3) has lag 1, and EMA (11) has lag 5. Figure 2 shows that, if I am willing to incur 5 days of lag, I get a smoother moving average if I run EMA (3) through itself 5 times than if I just take EMA (11) once.

This suggests that if EPMA and DEMA have 0 or low lag, why not run fast versions (eg DEMA (3)) through themselves many times to achieve a smooth result? The problem is that multiple runs though these filters increase their tendency to overshoot the data, giving an unusable result. This is because the amplitude response of DEMA and EPMA is greater than 1 at certain frequencies, giving a gain of much greater than 1 at these frequencies when run though themselves multiple times. Figure 3 shows DEMA (7) and EPMA(7) run through themselves 3 times. DEMA^3 has serious overshoot, and EPMA^3 is terrible.

The solution to the overshoot problem is to recall what we are doing with twicing:

DEMA (n) = EMA (n) + EMA (time series - EMA (n))

The second term is adding, in effect, a smooth version of the derivative to the EMA to achieve DEMA . The derivative term determines how hot the moving average's response to linear trends will be. We need to simply turn down the volume to achieve our basic building block:

EMA (n) + EMA (time series - EMA (n))*.7;

This is algebraically the same as:

EMA (n)*1.7-EMA( EMA (n))*.7;

I have chosen .7 as my volume factor, but the general formula (which I call "Generalized Dema") is:

GD (n,v) = EMA (n)*(1+v)-EMA( EMA (n))*v,

Where v ranges between 0 and 1. When v=0, GD is just an EMA , and when v=1, GD is DEMA . In between, GD is a cooler DEMA . By using a value for v less than 1 (I like .7), we cure the multiple DEMA overshoot problem, at the cost of accepting some additional phase delay. Now we can run GD through itself multiple times to define a new, smoother moving average T3 that does not overshoot the data:

T3(n) = GD ( GD ( GD (n)))

In filter theory parlance, T3 is a six-pole non-linear Kalman filter. Kalman filters are ones which use the error (in this case (time series - EMA (n)) to correct themselves. In Technical Analysis , these are called Adaptive Moving Averages; they track the time series more aggressively when it is making large moves.

Included

Signals

Alerts

Related indicators

Zero-line Volatility Quality Index (VQI)

Volatility Quality Index w/ Pips Filtering

Variety Moving Average Waddah Attar Explosion (WAE)

***This indicator is tuned to Forex. If you want to make it useful for other tickers, you must change the pip filtering value to match the asset. This means that for BTC, for example, you likely need to use a value of 10,000 or more for pips filter.

R-squared Adaptive T3 w/ DSL [Loxx]R-squared Adaptive T3 w/ DSL is the following T3 indicator but with Discontinued Signal Lines added to reduce noise and thereby increase signal accuracy. This adaptation makes this indicator lower TF scalp friendly.

What is R-squared Adaptive?

One tool available in forecasting the trendiness of the breakout is the coefficient of determination ( R-squared ), a statistical measurement.

The R-squared indicates linear strength between the security's price (the Y - axis) and time (the X - axis). The R-squared is the percentage of squared error that the linear regression can eliminate if it were used as the predictor instead of the mean value. If the R-squared were 0.99, then the linear regression would eliminate 99% of the error for prediction versus predicting closing prices using a simple moving average .

R-squared is used here to derive a T3 factor used to modify price before passing price through a six-pole non-linear Kalman filter.

What is the T3 moving average?

Better Moving Averages Tim Tillson

November 1, 1998

Tim Tillson is a software project manager at Hewlett-Packard, with degrees in Mathematics and Computer Science. He has privately traded options and equities for 15 years.

Introduction

"Digital filtering includes the process of smoothing, predicting, differentiating, integrating, separation of signals, and removal of noise from a signal. Thus many people who do such things are actually using digital filters without realizing that they are; being unacquainted with the theory, they neither understand what they have done nor the possibilities of what they might have done."

This quote from R. W. Hamming applies to the vast majority of indicators in technical analysis . Moving averages, be they simple, weighted, or exponential, are lowpass filters; low frequency components in the signal pass through with little attenuation, while high frequencies are severely reduced.

"Oscillator" type indicators (such as MACD , Momentum, Relative Strength Index ) are another type of digital filter called a differentiator.

Tushar Chande has observed that many popular oscillators are highly correlated, which is sensible because they are trying to measure the rate of change of the underlying time series, i.e., are trying to be the first and second derivatives we all learned about in Calculus.

We use moving averages (lowpass filters) in technical analysis to remove the random noise from a time series, to discern the underlying trend or to determine prices at which we will take action. A perfect moving average would have two attributes:

It would be smooth, not sensitive to random noise in the underlying time series. Another way of saying this is that its derivative would not spuriously alternate between positive and negative values.

It would not lag behind the time series it is computed from. Lag, of course, produces late buy or sell signals that kill profits.

The only way one can compute a perfect moving average is to have knowledge of the future, and if we had that, we would buy one lottery ticket a week rather than trade!

Having said this, we can still improve on the conventional simple, weighted, or exponential moving averages. Here's how:

Two Interesting Moving Averages

We will examine two benchmark moving averages based on Linear Regression analysis.

In both cases, a Linear Regression line of length n is fitted to price data.

I call the first moving average ILRS, which stands for Integral of Linear Regression Slope. One simply integrates the slope of a linear regression line as it is successively fitted in a moving window of length n across the data, with the constant of integration being a simple moving average of the first n points. Put another way, the derivative of ILRS is the linear regression slope. Note that ILRS is not the same as a SMA ( simple moving average ) of length n, which is actually the midpoint of the linear regression line as it moves across the data.

We can measure the lag of moving averages with respect to a linear trend by computing how they behave when the input is a line with unit slope. Both SMA (n) and ILRS(n) have lag of n/2, but ILRS is much smoother than SMA .

Our second benchmark moving average is well known, called EPMA or End Point Moving Average. It is the endpoint of the linear regression line of length n as it is fitted across the data. EPMA hugs the data more closely than a simple or exponential moving average of the same length. The price we pay for this is that it is much noisier (less smooth) than ILRS, and it also has the annoying property that it overshoots the data when linear trends are present.

However, EPMA has a lag of 0 with respect to linear input! This makes sense because a linear regression line will fit linear input perfectly, and the endpoint of the LR line will be on the input line.

These two moving averages frame the tradeoffs that we are facing. On one extreme we have ILRS, which is very smooth and has considerable phase lag. EPMA has 0 phase lag, but is too noisy and overshoots. We would like to construct a better moving average which is as smooth as ILRS, but runs closer to where EPMA lies, without the overshoot.

A easy way to attempt this is to split the difference, i.e. use (ILRS(n)+EPMA(n))/2. This will give us a moving average (call it IE /2) which runs in between the two, has phase lag of n/4 but still inherits considerable noise from EPMA. IE /2 is inspirational, however. Can we build something that is comparable, but smoother? Figure 1 shows ILRS, EPMA, and IE /2.

Filter Techniques

Any thoughtful student of filter theory (or resolute experimenter) will have noticed that you can improve the smoothness of a filter by running it through itself multiple times, at the cost of increasing phase lag.

There is a complementary technique (called twicing by J.W. Tukey) which can be used to improve phase lag. If L stands for the operation of running data through a low pass filter, then twicing can be described by:

L' = L(time series) + L(time series - L(time series))

That is, we add a moving average of the difference between the input and the moving average to the moving average. This is algebraically equivalent to:

2L-L(L)

This is the Double Exponential Moving Average or DEMA , popularized by Patrick Mulloy in TASAC (January/February 1994).

In our taxonomy, DEMA has some phase lag (although it exponentially approaches 0) and is somewhat noisy, comparable to IE /2 indicator.

We will use these two techniques to construct our better moving average, after we explore the first one a little more closely.

Fixing Overshoot

An n-day EMA has smoothing constant alpha=2/(n+1) and a lag of (n-1)/2.

Thus EMA (3) has lag 1, and EMA (11) has lag 5. Figure 2 shows that, if I am willing to incur 5 days of lag, I get a smoother moving average if I run EMA (3) through itself 5 times than if I just take EMA (11) once.