Professional GBP/JPY Analysis ToolThe foundation of professional trading begins with analyzing individual currencies first, not just currency pairs. By understanding the relative strength of each currency in the pair, traders can anticipate potential market moves with greater accuracy.

This indicator simplifies that process by:

Analyzing Individual Currency Strength:

The strength of GBP is calculated by averaging its performance across seven major GBP currency pairs:

GBP/EUR

GBP/USD

GBP/CAD

GBP/CHF

GBP/AUD

GBP/NZD

GBP/JPY

The strength of JPY is calculated by averaging its performance across seven major JPY currency pairs:

JPY/USD

JPY/CAD

JPY/EUR

JPY/GBP

JPY/AUD

JPY/NZD

JPY/CHF

The values are normalized to allow direct comparison on the same scale.

Identifying Correlation Between GBP and JPY:

The histogram displays the correlation between GBP and JPY strength:

Positive Correlation (Green): Both GBP and JPY are trending up or down together, indicating a less strong trend. This is a market condition to avoid, as both currencies are strengthening or weakening simultaneously.

Negative Correlation (Red): One currency is strong while the other is weak, indicating a stronger trend in GBP/JPY. This scenario presents a better trading opportunity, as you are trading one strong currency against one weak currency, amplifying the potential for a clearer price movement in GBP/JPY.

Visualizing Long/Short Bias:

GBP Strength > JPY Strength: Bullish bias for GBP/JPY (green background).

JPY Strength > GBP Strength: Bearish bias for GBP/JPY (red background).

This indicator equips traders with a deeper understanding of GBP/JPY dynamics by first breaking down the individual currencies. With insights into currency strength, their correlation, and the optimal conditions for trading, it provides a solid foundation for making informed trading decisions.

How to Use:

Check the Histogram for Correlation:

Wait for the histogram to be red. This indicates that GBP and JPY are moving in opposite directions, signaling a stronger trend where you're trading a strong currency against a weak one—a more favorable setup.

Align with Background Color for Confirmation:

Wait for the background color to match your trade plan:

Green Background: Confirms a bullish bias, supporting long positions on the GBP/JPY pair.

Red Background: Confirms a bearish bias, supporting short positions on the GBP/JPY pair.

By following these steps, you can identify stronger trade opportunities and align them with your strategy.

Cari dalam skrip untuk "one一季度财报"

Multi-Band Comparison (Uptrend)Multi-Band Comparison

Overview:

The Multi-Band Comparison indicator is engineered to reveal critical levels of support and resistance in strong uptrends. In a healthy upward market, the price action will adhere closely to the 95th percentile line (the Upper Quantile Band), effectively “riding” it. This indicator combines a modified Bollinger Band (set at one standard deviation), quantile analysis (95% and 5% levels), and power‑law math to display a dynamic picture of market structure—highlighting a “golden channel” and robust support areas.

Key Components & Calculations:

The Golden Channel: Upper Bollinger Band & Upper Std Dev Band of the Upper Quantile

Upper Bollinger Band:

Calculation:

boll_upper=SMA(close,length)+(boll_mult×stdev)

boll_upper=SMA(close,length)+(boll_mult×stdev) Here, the 20-period SMA is used along with one standard deviation of the close, where the multiplier (boll_mult) is 1.0.

Role in an Uptrend:

In a healthy uptrend, price rides near the 95th percentile line. When price crosses above this Upper Bollinger Band, it confirms strong bullish momentum.

Upper Std Dev Band of the Upper Quantile (95th Percentile) Band:

Calculation:

quant_upper_std_up=quant_upper+stdev

quant_upper_std_up=quant_upper+stdev The Upper Quantile Band, quant_upperquant_upper, is calculated as the 95th percentile of recent price data. Adding one standard deviation creates an extension that accounts for normal volatility around this extreme level.

The Golden Channel:

When the price crosses above the Upper Bollinger Band, the Upper Std Dev Band of the Upper Quantile immediately shifts to gold (yellow) and remains gold until price falls below the Bollinger level. Together, these two lines form the “golden channel”—a visual hallmark of a healthy uptrend where the price reliably hugs the 95th percentile level.

Upper Power‑Law Band

Calculation:

The Upper Power‑Law Band is derived in two steps:

Determine the Extreme Return Factor:

power_upper=Percentile(returns,95%)

power_upper=Percentile(returns,95%) where returns are computed as:

returns=closeclose −1.

returns=close close−1.

Scale the Current Price:

power_upper_band=close×(1+power_upper)

power_upper_band=close×(1+power_upper)

Rationale and Correlation:

By focusing on the upper 5% of returns (reflecting “fat tails”), the Upper Power‑Law Band captures extreme but statistically expected movements. In an uptrend, its value often converges with the Upper Std Dev Band of the Upper Quantile because both measures reflect heightened volatility and extreme price levels. When the Upper Power‑Law Band exceeds the Upper Std Dev Band, it can signal a temporary overextension.

Upper Quantile Band (95% Percentile)

Calculation:

quant_upper=Percentile(price,95%)

quant_upper=Percentile(price,95%) This level represents where 95% of past price data falls below, and in a robust uptrend the price action practically rides this line.

Color Logic:

Its color shifts from a neutral (blackish) tone to a vibrant, bullish hue when the Upper Power‑Law Band crosses above it—signaling extra strength in the trend.

Lower Quantile and Its Support

Lower Quantile Band (5% Percentile):

Calculation:

quant_lower=Percentile(price,5%)

quant_lower=Percentile(price,5%)

Behavior:

In a healthy uptrend, price remains well above the Lower Quantile Band. It turns red only when price touches or crosses it, serving as a warning signal. Under normal conditions it remains bright green, indicating the market is not nearing these extreme lows.

Lower Std Dev Band of the Lower Quantile:

This line is calculated by subtracting one standard deviation from quant_lowerquant_lower and typically serves as absolute support in nearly all conditions (except during gap or near-gap moves). Its consistent role as support provides traders with a robust level to monitor.

How to Use the Indicator:

Golden Channel and Trend Confirmation:

As price rides the Upper Quantile (95th percentile) perfectly in a healthy uptrend, the Upper Bollinger Band (1 stdev above SMA) and the Upper Std Dev Band of the Upper Quantile form a “golden channel” once price crosses above the Bollinger level. When this occurs, the Upper Std Dev Band remains gold until price dips back below the Bollinger Band. This visual cue reinforces trend strength.

Power‑Law Insights:

The Upper Power‑Law Band, which is based on extreme (95th percentile) returns, tends to align with the Upper Std Dev Band. This convergence reinforces that extreme, yet statistically expected, price moves are occurring—indicating that even though the price rides the 95th percentile, it can only stretch so far before a correction or consolidation.

Support Indicators:

Primary and Secondary Support in Uptrends:

The Upper Bollinger Band and the Lower Std Dev Band of the Upper Quantile act as support zones for minor retracements in the uptrend.

Absolute Support:

The Lower Std Dev Band of the Lower Quantile serves as an almost invariable support area under most market conditions.

Conclusion:

The Multi-Band Comparison indicator unifies advanced statistical techniques to offer a clear view of uptrend structure. In a healthy bull market, price action rides the 95th percentile line with precision, and when the Upper Bollinger Band is breached, the corresponding Upper Std Dev Band turns gold to form a “golden channel.” This, combined with the Power‑Law analysis that captures extreme moves, and the robust lower support levels, provides traders with powerful, multi-dimensional insights for managing entries, exits, and risk.

Disclaimer:

Trading involves risk. This indicator is for educational purposes only and does not constitute financial advice. Always perform your own analysis before making trading decisions.

Volume EquilibriumThe intent behind this indicator is to provide comprehensive information relating to volume compared to multiple timeframes. This indicator allows one to see what the market 'theoretically' sees as 'fair-value' whilst also allowing one to gauge where the price of a stock is headed.

Volume Equilibrium

The main indicator finds the difference between buying volume and selling volume, under the basic presumption that more buying volume indicates greater bullish sentiment and vice versa.

Buying Volume = volume when close price is higher than open price.

Selling Volume = volume when close price is lower than open price.

Volume Balance = Cumulative Buying Volume − Cumulative Selling Volume

Volume Balance is then expressed as a percentage by dividing by total volume

This indicator is composed of three different lengths of the same indicator. Short, Mid, and Long term representations of Volume Equilibrium. The difference between the mid and long term are highlighted so to make it easy to see where volume is going relative to a longer time frame.

HOW TO USE:

At 0 ---> Equilibrium ---> Equal Buying/Selling Volume

Above 0 ---> More buying Volume

Below 0 ---> More selling Volume

Using theory, it is assumed that the price is at a 'fair-value' when the buying/selling volume is at 0. This is of course relative to the respective timeframe of your choosing. More weight given to larger timeframes.

Volume Histogram

It is a basic volume chart that represents the total volume though has highlighted bars so to indicate buying(green) and selling(red) volume. This allows one to see what the indicator is based off of.

Open-Close Oscillator(not needed)

Calculates the average open-close for a selected timeframe and then provides the current closing price relative to that average open-close. Very simply put, values below 0 indicate bearish and values above 0 generally indicate bullishness. This indicator is for a quick reference of price action relative to volume.

Another way to use this indicator, though unique, is to analyze the separate open-close lines themselves. Using the open-close bands, bullishness is defined as increasing closing prices and bearish as decreasing closing prices. So, in regard to this indicator, bear sessions can be indicated by the opening line being below the closing line and bull sessions as the opening line being above. Use the 'flip' of these lines to your advantage, they are very helpful at capturing long continuous sentiment.

This indicator is composed of great information though I still think it best to use many different indicators to help you with your trades.

NOTE: Be aware of what we are trying to analyze, Volume. This means that one should also look out for divergences to capture early indications of reversals. This indicator can be leveraged greatly.

SMT Divergence ICT 01 [TradingFinder] Smart Money Technique🔵 Introduction

SMT Divergence (short for Smart Money Technique Divergence) is a trading technique in the ICT Concepts methodology that focuses on identifying divergences between two positively correlated assets in financial markets.

These divergences occur when two assets that should move in the same direction move in opposite directions. Identifying these divergences can help traders spot potential reversal points and trend changes.

Bullish and Bearish divergences are clearly visible when an asset forms a new high or low, and the correlated asset fails to do so. This technique is applicable in markets like Forex, stocks, and cryptocurrencies, and can be used as a valid signal for deciding when to enter or exit trades.

Bullish SMT Divergence : This type of divergence occurs when one asset forms a higher low while the correlated asset forms a lower low. This divergence is typically a sign of weakness in the downtrend and can act as a signal for a trend reversal to the upside.

Bearish SMT Divergence : This type of divergence occurs when one asset forms a higher high while the correlated asset forms a lower high. This divergence usually indicates weakness in the uptrend and can act as a signal for a trend reversal to the downside.

🔵 How to Use

SMT Divergence is an analytical technique that identifies divergences between two correlated assets in financial markets.

This technique is used when two assets that should move in the same direction move in opposite directions.

Identifying these divergences can help you pinpoint reversal points and trend changes in the market.

🟣 Bullish SMT Divergence

This divergence occurs when one asset forms a higher low while the correlated asset forms a lower low. This divergence indicates weakness in the downtrend and can signal a potential price reversal to the upside.

In this case, when the correlated asset is forming a lower low, and the main asset is moving lower but the correlated asset fails to continue the downward trend, there is a high probability of a trend reversal to the upside.

🟣 Bearish SMT Divergence

Bearish divergence occurs when one asset forms a higher high while the correlated asset forms a lower high. This type of divergence indicates weakness in the uptrend and can signal a potential trend reversal to the downside.

When the correlated asset fails to make a new high, this divergence may be a sign of a trend reversal to the downside.

🟣 Confirming Signals with Correlation

To improve the accuracy of the signals, use assets with strong correlation. Forex pairs like OANDA:EURUSD and OANDA:GBPUSD , or cryptocurrencies like COINBASE:BTCUSD and COINBASE:ETHUSD , or commodities such as gold ( FX:XAUUSD ) and silver ( FX:XAGUSD ) typically have significant correlation. Identifying divergences between these assets can provide a strong signal for a trend change.

🔵 Settings

Second Symbol : This setting allows you to select another asset for comparison with the primary asset. By default, "XAUUSD" (Gold) is set as the second symbol, but you can change it to any currency pair, stock, or cryptocurrency. For example, you can choose currency pairs like EUR/USD or GBP/USD to identify divergences between these two assets.

Divergence Fractal Periods : This parameter defines the number of past candles to consider when identifying divergences. The default value is 2, but you can change it to suit your preferences. This setting allows you to detect divergences more accurately by selecting a greater number of candles.

Bullish Divergence Line : Displays a line showing bullish divergence from the lows.

Bearish Divergence Line : Displays a line showing bearish divergence from the highs.

Bullish Divergence Label : Displays the "+SMT" label for bullish divergences.

Bearish Divergence Label : Displays the "-SMT" label for bearish divergences.

🔵 Conclusion

SMT Divergence is an effective tool for identifying trend changes and reversal points in financial markets based on identifying divergences between two correlated assets. This technique helps traders receive more accurate signals for market entry and exit by analyzing bullish and bearish divergences.

Identifying these divergences can provide opportunities to capitalize on trend changes in Forex, stocks, and cryptocurrency markets. Using SMT Divergence along with risk management and confirming signals with other technical analysis tools can improve the accuracy of trading decisions and reduce risks from sudden market changes.

Moment-Based Adaptive DetectionMBAD (Moment-Based Adaptive Detection) : a method applicable to a wide range of purposes, like outlier or novelty detection, that requires building a sensible interval/set of thresholds. Unlike other methods that are static and rely on optimizations that inevitably lead to underfitting/overfitting, it dynamically adapts to your data distribution without any optimizations, MLE, or stuff, and provides a set of data-driven adaptive thresholds, based on closed-form solution with O(n) algo complexity.

1.5 years ago, when I was still living in Versailles at my friend's house not knowing what was gonna happen in my life tomorrow, I made a damn right decision not to give up on one idea and to actually R&D it and see what’s up. It allowed me to create this one.

The Method Explained

I’ve been wandering about z-values, why exactly 6 sigmas, why 95%? Who decided that? Why would you supersede your opinion on data? Based on what? Your ego?

Then I consciously noticed a couple of things:

1) In control theory & anomaly detection, the popular threshold is 3 sigmas (yet nobody can firmly say why xD). If your data is Laplace, 3 sigmas is not enough; you’re gonna catch too many values, so it needs a higher sigma.

2) Yet strangely, the normal distribution has kurtosis of 3, and 6 for Laplace.

3) Kurtosis is a standardized moment, a moment scaled by stdev, so it means "X amount of something measured in stdevs."

4) You generate synthetic data, you check on real data (market data in my case, I am a quant after all), and you see on both that:

lower extension = mean - standard deviation * kurtosis ≈ data minimum

upper extension = mean + standard deviation * kurtosis ≈ data maximum

Why not simply use max/min?

- Lower info gain: We're not using all info available in all data points to estimate max/min; we just pick the current higher and lower values. Lol, it’s the same as dropping exponential smoothing with alpha = 0 on stationary data & calling it a day.

You can’t update the estimates of min and max when new data arrives containing info about the matter. All you can do is just extend min and max horizontally, so you're not using new info arriving inside new data.

- Mixing order and non-order statistics is a bad idea; we're losing integrity and coherence. That's why I don't like the Hurst exponent btw (and yes, I came up with better metrics of my own).

- Max & min are not even true order statistics, unlike a percentile (finding which requires sorting, which requires multiple passes over your data). To find min or max, you just need to do one traversal over your data. Then with or without any weighting, 100th percentile will equal max. So unlike a weighted percentile, you can’t do weighted max. Then while you can always check max and min of a geometric shape, now try to calculate the 56th percentile of a pentagram hehe.

TL;DR max & min are rather topological characteristics of data, just as the difference between starting and ending points. Not much to do with statistics.

Now the second part of the ballet is to work with data asymmetry:

1) Skewness is also scaled by stdev -> so it must represent a shift from the data midrange measured in stdevs -> given asymmetric data, we can include this info in our models. Unlike kurtosis, skewness has a sign, so we add it to both thresholds:

lower extension = mean - standard deviation * kurtosis + standard deviation * skewness

upper extension = mean + standard deviation * kurtosis + standard deviation * skewness

2) Now our method will work with skewed data as well, omg, ain’t it cool?

3) Hold up, but what about 5th and 6th moments (hyperskewness & hyperkurtosis)? They should represent something meaningful as well.

4) Perhaps if extensions represent current estimated extremums, what goes beyond? Limits, beyond which we expect data not to be able to pass given the current underlying process generating the data?

When you extend this logic to higher-order moments, i.e., hyperskewness & hyperkurtosis (5th and 6th moments), they measure asymmetry and shape of distribution tails, not its core as previous moments -> makes no sense to mix 4th and 3rd moments (skewness and kurtosis) with 5th & 6th, so we get:

lower limit = mean - standard deviation * hyperkurtosis + standard deviation * hyperskewness

upper limit = mean + standard deviation * hyperkurtosis + standard deviation * hyperskewness

While extensions model your data’s natural extremums based on current info residing in the data without relying on order statistics, limits model your data's maximum possible and minimum possible values based on current info residing in your data. If a new data point trespasses limits, it means that a significant change in the data-generating process has happened, for sure, not probably—a confirmed structural break.

And finally we use time and volume weighting to include order & process intensity information in our model.

I can't stress it enough: despite the popularity of these non-weighted methods applied in mainstream open-access time series modeling, it doesn’t make ANY sense to use non-weighted calculations on time series data . Time = sequence, it matters. If you reverse your time series horizontally, your means, percentiles, whatever, will stay the same. Basically, your calculations will give the same results on different data. When you do it, you disregard the order of data that does have order naturally. Does it make any sense to you? It also concerns regressions applied on time series as well, because even despite the slope being opposite on your reversed data, the centroid (through which your regression line always comes through) will be the same. It also might concern Fourier (yes, you can do weighted Fourier) and even MA and AR models—might, because I ain’t researched it extensively yet.

I still can’t believe it’s nowhere online in open access. No chance I’m the first one who got it. It’s literally in front of everyone’s eyes for centuries—why no one tells about it?

How to use

That’s easy: can be applied to any, even non-stationary and/or heteroscedastic time series to automatically detect novelties, outliers, anomalies, structural breaks, etc. In terms of quant trading, you can try using extensions for mean reversion trades and limits for emergency exits, for example. The market-making application is kinda obvious as well.

The only parameter the model has is length, and it should NOT be optimized but picked consciously based on the process/system you’re applying it to and based on the task. However, this part is not about sharing info & an open-access instrument with the world. This is about using dem instruments to do actual business, and we can’t talk about it.

∞

Mean Price

^^ Plotting switched to Line.

This method of financial time series (aka bars) downsampling is literally, naturally, and thankfully the best you can do in terms of maximizing info gain. You can finally chill and feed it to your studies & eyes, and probably use nothing else anymore.

(HL2 and occ3 also have use cases, but other aggregation methods? Not really, even if they do, the use cases are ‘very’ specific). Tho in order to understand why, you gotta read the following wall, or just believe me telling you, ‘I put it on my momma’.

The true story about trading volumes and why this is all a big misdirection

Actually, you don’t need to be a quant to get there. All you gotta do is stop blindly following other people’s contextual (at best) solutions, eg OC2 aggregation xD, and start using your own brain to figure things out.

Every individual trade (basically an imprint on 1D price space that emerges when market orders hit the order book) has several features like: price, time, volume, AND direction (Up if a market buy order hits the asks, Down if a market sell order hits the bids). Now, the last two features—volume and direction—can be effectively combined into one (by multiplying volume by 1 or -1), and this is probably how every order matching engine should output data. If we’re not considering size/direction, we’re leaving data behind. Moreover, trades aren’t just one-price dots all the time. One trade can consume liquidity on several levels of the order book, so a single trade can be several ticks big on the price axis.

You may think now that there are no zero-volume ticks. Well, yes and no. It depends on how you design an exchange and whether you allow intra-spread trades/mid-spread trades (now try to Google it). Intra-spread trades could happen if implemented when a matching engine receives both buy and sell orders at the same microsecond period. This way, you can match the orders with each other at a better price for both parties without even hitting the book and consuming liquidity. Also, if orders have different sizes, the remaining part of the bigger order can be sent to the order book. Basically, this type of trade can be treated as an OTC trade, having zero volume because we never actually hit the book—there’s no imprint. Another reason why it makes sense is when we think about volume as an impact or imbalance act, and how the medium (order book in our case) responds to it, providing information. OTC and mid-spread trades are not aggressive sells or buys; they’re neutral ticks, so to say. However huge they are, sometimes many blocks on NYSE, they don’t move the price because there’s no impact on the medium (again, which is the order book)—they’re not providing information.

... Now, we need to aggregate these trades into, let’s say, 1-hour bars (remember that a trade can have either positive or negative volume). We either don’t want to do it, or we don’t have this kind of information. What we can do is take already aggregated OHLC bars and extract all the info from them. Given the market is fractal, bars & trades gotta have the same set of features:

- Highest & lowest ticks (high & low) <- by price;

- First & last ticks (open & close) <- by time;

- Biggest and smallest ticks <- by volume.*

*e.g., in the array ,

2323: biggest trade,

-1212: smallest trade.

Now, in our world, somehow nobody started to care about the biggest and smallest trades and their inclusion in OHLC data, while this is actually natural. It’s the same way as it’s done with high & low and open & close: we choose the minimum and maximum value of a given feature/axis within the aggregation period.

So, we don’t have these 2 values: biggest and smallest ticks. The best we can do is infer them, and given the fact the biggest and smallest ticks can be located with the same probability everywhere, all we can do is predict them in the middle of the bar, both in time and price axes. That’s why you can see two HL2’s in each of the 3 formulas in the code.

So, summed up absolute volumes that you see in almost every trading platform are actually just a derivative metric, something that I call Type 2 time series in my own (proprietary ‘for now’) methods. It doesn’t have much to do with market orders hitting the non-uniform medium (aka order book); it’s more like a statistic. Still wanna use VWAP? Ok, but you gotta understand you’re weighting Type 1 (natural) time series by Type 2 (synthetic) ones.

How to combine all the data in the right way (khmm khhm ‘order’)

Now, since we have 6 values for each bar, let’s see what information we have about them, what we don’t have, and what we can do about it:

- Open and close: we got both when and where (time (order) and price);

- High and low: we got where, but we don’t know when;

- Biggest & smallest trades: we know shit, we infer it the way it was described before.'

By using the location of the close & open prices relative to the high & low prices, we can make educated guesses about whether high or low was made first in a given bar. It’s not perfect, but it’s ultimately all we can do—this is the very last bit of info we can extract from the data we have.

There are 2 methods for inferring volume delta (which I call simply volume) that are presented everywhere, even here on TradingView. Funny thing is, this is actually 2 parts of the 1 method. I wonder how many folks see through it xD. The same method can be used for both inferring volume delta AND making educated guesses whether high or low was made first.

Imagine and/or find the cases on your charts to understand faster:

* Close > open means we have an up bar and probably the volume is positive, and probably high was made later than low.

* Close < open means we have a down bar and probably the volume is negative, and probably low was made later than high.

Now that’s the point when you see that these 2 mentioned methods are actually parts of the 1 method:

If close = open, we still have another clue: distance from open/close pair to high (HC), and distance from open/close pair to low (LC):

* HC < LC, probably high was made later.

* HC > LC, probably low was made later.

And only if close = open and HC = LC, only in this case we have no clue whether high or low was made earlier within a bar. We simply don’t have any more information to even guess. This bar is called a neutral bar.

At this point, we have both time (order) and price info for each of our 6 values. Now, we have to solve another weighted average problem, and that’s it. We’ll weight prices according to the order we’ve guessed. In the neutral bar case, open has a weight of 1, close has a weight of 3, and both high and low have weights of 2 since we can’t infer which one was made first. In all cases, biggest and smallest ticks are modeled with HL2 and weighted like they’re located in the middle of the bar in a time sense.

P.S.: I’ve also included a "robust" method where all the bars are treated like neutral ones. I’ve used it before; obviously, it has lesser info gain -> works a bit worse.

High/Low Location Frequency [LuxAlgo]The High/Low Location Frequency tool provides users with probabilities of tops and bottoms at user-defined periods, along with advanced filters that offer deep and objective market information about the likelihood of a top or bottom in the market.

🔶 USAGE

There are four different time periods that traders can select for analysis of probabilities:

HOUR OF DAY: Probability of occurrence of top and bottom prices for each hour of the day

DAY OF WEEK: Probability of occurrence of top and bottom prices for each day of the week

DAY OF MONTH: Probability of occurrence of top and bottom prices for each day of the month

MONTH OF YEAR: Probability of occurrence of top and bottom prices for each month

The data is displayed as a dashboard, which users can position according to their preferences. The dashboard includes useful information in the header, such as the number of periods and the date from which the data is gathered. Additionally, users can enable active filters to customize their view. The probabilities are displayed in one, two, or three columns, depending on the number of elements.

🔹 Advanced Filters

Advanced Filters allow traders to exclude specific data from the results. They can choose to use none or all filters simultaneously, inputting a list of numbers separated by spaces or commas. However, it is not possible to use both separators on the same filter.

The tool is equipped with five advanced filters:

HOURS OF DAY: The permitted range is from 0 to 23.

DAYS OF WEEK: The permitted range is from 1 to 7.

DAYS OF MONTH: The permitted range is from 1 to 31.

MONTHS: The permitted range is from 1 to 12.

YEARS: The permitted range is from 1000 to 2999.

It should be noted that the DAYS OF WEEK advanced filter has been designed for use with tickers that trade every day, such as those trading in the crypto market. In such cases, the numbers displayed will range from 1 (Sunday) to 7 (Saturday). Conversely, for tickers that do not trade over the weekend, the numbers will range from 1 (Monday) to 5 (Friday).

To illustrate the application of this filter, we will exclude results for Mondays and Tuesdays, the first five days of each month, January and February, and the years 2020, 2021, and 2022. Let us review the results:

DAYS OF WEEK: `2,3` or `2 3` (for crypto) or `1,2` or `1 2` (for the rest)

DAYS OF MONTH: `1,2,3,4,5` or `1 2 3 4 5`

MONTHS: `1,2` or `1 2`

YEARS: `2020,2021,2022` or `2020 2021 2022`

🔹 High Probability Lines

The tool enables traders to identify the next period with the highest probability of a top (red) and/or bottom (green) on the chart, marked with two horizontal lines indicating the location of these periods.

🔹 Top/Bottom Labels and Periods Highlight

The tool is capable of indicating on the chart the upper and lower limits of each selected period, as well as the commencement of each new period, thus providing traders with a convenient reference point.

🔶 SETTINGS

Period: Select how many bars (hours, days, or months) will be used to gather data from, max value as default.

Execution Window: Select how many bars (hours, days, or months) will be used to gather data from

🔹 Advanced Filters

Hours of day: Filter which hours of the day are excluded from the data, it accepts a list of hours from 0 to 23 separated by commas or spaces, users can not mix commas or spaces as a separator, must choose one

Days of week: Filter which days of the week are excluded from the data, it accepts a list of days from 1 to 5 for tickers not trading weekends, or from 1 to 7 for tickers trading all week, users can choose between commas or spaces as a separator, but can not mix them on the same filter.

Days of month: Filter which days of the month are excluded from the data, it accepts a list of days from 1 to 31, users can choose between commas or spaces as separator, but can not mix them on the same filter.

Months: Filter months to exclude from data. Accepts months from 1 to 12. Choose one separator: comma or space.

Years: Filter years to exclude from data. Accepts years from 1000 to 2999. Choose one separator: comma or space.

🔹 Dashboard

Dashboard Location: Select both the vertical and horizontal parameters for the desired location of the dashboard.

Dashboard Size: Select size for dashboard.

🔹 Style

High Probability Top Line: Enable/disable `High Probability Top` vertical line and choose color

High Probability Bottom Line: Enable/disable `High Probability Bottom` vertical line and choose color

Top Label: Enable/disable period top labels, choose color and size.

Bottom Label: Enable/disable period bottom labels, choose color and size.

Highlight Period Changes: Enable/disable vertical highlight at start of period

Quick scan for drift🙏🏻

ML based algorading is all about detecting any kind of non-randomness & exploiting it, kinda speculative stuff, not my way, but still...

Drift is one of the patterns that can be exploited, because pure random walks & noise aint got no drift.

This is an efficient method to quickly scan tons of timeseries on the go & detect the ones with drift by simply checking wherther drift < -0.5 or drift > 0.5. The code can be further optimized both in general and for specific needs, but I left it like dat for clarity so you can understand how it works in a minute not in an hour

^^ proving 0.5 and -0.5 are natural limits with no need to optimize anything, we simply put the metric on random noise and see it sits in between -0.5 and 0.5

You can simply take this one and never check anything again if you require numerous live scans on the go. The metric is purely geometrical, no connection to stats, TSA, DSA or whatever. I've tested numerous formulas involving other scaling techniques, drift estimates etc (even made a recursive algo that had a great potential to be written about in a paper, but not this time I gues lol), this one has the highest info gain aka info content.

The timeseries filtered by this lil metric can be further analyzed & modelled with more sophisticated tools.

Live Long and Prosper

P.S.: there's no such thing as polynomial trend/drift, it's alwasy linear, these curves you see are just really long cycles

P.S.: does cheer still work on TV? @admin

Flashtrader´s Statistical BandwidthsThe vast majority of traders exclusively concern

themselves with trend-following in all its facets. Scoring

points with trends on a regular basis is a difficult task

since prices do not constantly move in one direction

or another. In the case of the DAX future, for example,

only about 30 per cent of all trading days in a year are

trend days. And of these, there are x percent long ones

and x per cent short ones. Catching the very days when

prices rise or fall from the opening to the close is a major

challenge for a trader who also needs to have previously

recognised the corresponding direction.

However, there are also other ways of profit-taking

every day – for example, by using the mean reversion

strategy. The idea behind this is the fact that prices reach

a high and a low every day – but very rarely close at the

high or the low. This means that prices always move

away from these extreme points and the closing price is

somewhere in between. A profitable trading strategy can

be developed out of this.

But how can you know where the high and the low

will be tomorrow? Is it possible for you to know this in

advance? No – because no one can predict the future. Or

can they? At least it can be statistically determined how

high or low prices could go tomorrow. There is a high

degree of probability that one of the two possibilities

will materialise. It will then be necessary to act.

Calculation

Classic pivot points for the following day are calculated

from the high, low and closing price. But does it really

make sense to use such a mix? I don’t think so and

use a different calculation for this strategy. In a first step,

only the differences between the start and the high or low

are calculated on a daily basis. To avoid being dependent

on individual days and outliers, it is advisable to calculate,

in a second step, the average of these differences over

the past five days. Finally, this average will then be added

at the opening price of the current trading day for the

upper statistical bandwidth and subtracted for the lower

bandwidth.

upper bandwidth = oSTB (violet dashed line in the chart)

lower bandwidth = uSTB (violet dashedline in the chart)

The second interesting question is, if the previous day's high has been exceeded, how much further can the price rise from a mathematical/statistical point of view?

These calculated previous day highs expansions are shown as red dashed lines

Previous day's high expansion = VTHA

Previous day's low expansion = VTTA

For further orientation, the previous day's high (VTH) and the previous day's low (VTT) are shown in light blue dashed lines

And as a supplement, the previous day's close in the DAX Future at 10:00 p.m. VTSA in violet solid lines and the previous day's close in the cash register at 5:30 p.m. VTSN in yellow solid lines

Reaching the calculated extreme values does not mean that the trend has to change immediately, but there is at least temporary exhaustion potential with which you can earn a few points every day in the area of scalping.

Example for cheap entry long:

Example for cheap entry short:

Deutsch:

Die Masse der Trader beschäftigt sich ausschließlich mit Trendfolge in all ihren Facetten. Mit Trends regelmäßig zu punkten ist ein schwieriges Unterfangen, da die Kurse nicht ständig in die eine oder andere Richtung laufen. Beim DAX-Future zum Beispiel sind von allen Börsentagen im Jahr lediglich zirka 30 Prozent Trendtage. Davon sind dann auch noch x Prozent Long und x Prozent Short. Hier genau die Tage abzupassen, an denen die Kurse von Börsenbeginn bis zum Schluss steigen beziehungsweise fallen, ist eine große Herausforderung – wobei der Trader zuvor noch die entsprechende Richtung erkannt haben muss. Es gibt jedoch auch noch andere Methoden täglich Gewinne mitzunehmen, zum Beispiel mit der Mean-Reversion-Strategie (Mittelwertumkehr).

Hintergrund ist die Tatsache, dass die Kurse jeden Tag ein Hoch und ein Tief erreichen – aber sehr selten am Hoch oder am Tief schließen. Das bedeutet, dass die Preise sich immer wie der von diesen Extrempunkten wegbewegen und der Schlusskurs irgendwo dazwischen liegt. Hieraus lässt sich eine profitable Handelsstrategie entwickeln. Aber woher kannst Du wissen, wo morgen das Hoch und das Tief sein wird? Kannst Du das vorher schon wissen? Nein – denn niemand kann die Zukunft vorhersagen. Oder doch? Statistisch lässt sich zumindest bestimmen, wie hoch und wie tief die Kurse morgen steigen oder fallen könnten. Eine Seite wird mit sehr hoher Wahrscheinlichkeit ein treffen. Dann gilt es zu handeln.

Berechnung Klassischer Pivot-Punkte für den folgenden Tag werden aus Hoch, Tief und Schlusskurs berechnet. Aber ist es wirklich sinnvoll, einen solchen Mix zu verwenden? Ich finde das nicht und verwenden für diese Strategie eine andere Berechnung. Im ersten Schritt werden täglich die Differenzen nur vom Start bis zum Hoch beziehungsweise Tief errechnet. Um nicht von einzelnen Tagen und Ausreißern abhängig zu sein, empfiehlt es sich, in einem zweiten Schritt den Durchschnitt dieser Differenzen über die letzten fünf Tage zu errechnen. Zuletzt wird dann dieser Durchschnitt zum Eröffnungskurs des aktuellen Handelstages für die obere statistische Bandbreite addiert und für die untere Bandbreite subtrahiert.

Obere statistische Bandbreite = oSTB (violette gestrichelte Linie im Chart)

Untere statistische Bandbreite = uSTB (violette gestrichelte Linie im Chart)

Die zweite interessante Frage ist, wenn das Vortageshoch überschritten wurde, wie weit kann der Kurs dann noch steigen aus mathematisch/statistischer Sicht?

Diese berechneten Vortagesextremausdehnungen sind als rote gestrichelte Linien dargestellt

Vortageshochausdehnung = VTHA

Vortagestiefausdehnung = VTTA

Für die weitere Orientierung sind die Vortageshochs (VTH) und die Vortagestiefs (VTT) als hellblaue gestrichelte Linien abgebildet.

Als Ergänzung wird noch der Vortages Schluss im Dax Future um 22:00 Uhr VTSA mit einer violetten durchgezogenen Linie und der Kassamarktschluss um 17:30 Uhr mit einer gelben durchgezogenen Linie gezeigt.

Das Erreichen der berechneten Extremwerte bedeutet nicht, das der Trend sofort drehen muss, aber es sind zumindest temporäre Erschöpfungspotentiale mit denen sich im Bereich scalping täglich einige Punkte verdienen lassen.

Beispiel für günstigen Einstieg Long:

Beispiel für günstigen Einstieg Short:

LV Stock QualityCritical financial and technical values are listed in the table.

PIOTROSKI_F_SCORE (expect. >5) -> The Piotroski score is a discrete score between zero and nine that reflects nine criteria used to determine the strength of a firm's financial position. The Piotroski score is used to determine the best value stocks, with nine being the best and zero being the worst. Having a score bigger than 5 is a good sign for the strength of a firm's financial position

ROE (expect. >11) --> Return on equity (ROE) is a measure of a company's financial performance. It is calculated by dividing net income by shareholders' equity. Because shareholders' equity is equal to a company’s assets minus its debt, ROE is a way of showing a company's return on net assets. A “good” ROE will depend on the company’s industry and competitors.

EPS_GROWTH (expect. >11) --> This indicator is calculated as the percentage change in Basic earnings per share for one year. This indicator reflects the growth rate of a company's basic profit per share outstanding for one year. It is calculated based using only common shares. An increase in EPS growth may signal that a company is becoming more profitable and efficient in its operations. A decline in EPS growth may signal that a company is spending more or losing business share. EPS growth should be viewed alongside other metrics like revenue and costs.

CURRENT_RATIO (expect. >1.25) --> The current ratio measures a company’s ability to pay current, or short-term, liabilities (debt and payables) with its current, or short-term, assets (cash, inventory, and receivables). Current ratios over 1.00 indicate that a company's current assets are greater than its current liabilities, meaning it could more easily pay of short-term debts.

OPERATING_MARGIN(expect. >11) --> The operating margin measures how much profit a company makes on a dollar of sales after paying for variable costs of production, such as wages and raw materials, but before paying interest or tax.

RETURN_CAPITAL (expect. >11) --> Return of capital (ROC) is a payment that an investor receives as a portion of their original investment and that is not considered income or capital gains from the investment.

ALTMAN_Z_SCORE (expect. >1.8) --> The Altman Z-score is the output of a credit-strength test that gauges a publicly traded manufacturing company's likelihood of bankruptcy. An Altman Z-score close to 0 suggests a company might be headed for bankruptcy, while a score closer to 3 suggests a company is in solid financial positioning.

REVENUE_GROWTH (expect. >11) --> Quarterly revenue growth is an increase in a company's sales in one quarter compared to sales of a different quarter. Comparing a company's financials from one period to another gives a clear picture of its revenue growth rate and can help investors identify the catalyst for such growth.

SUSTAINABLE_GROWTH (expect. >11) --> The sustainable growth rate (SGR) is the maximum rate of growth that a company or social enterprise can sustain without having to finance growth with additional equity or debt. In other words, it is the rate at which the company can grow while using its own internal revenue without borrowing from outside sources.

DEBT TO INCOME (expect. <0.4) --> A debt-to-income (DTI) ratio is a financial metric used by lenders to determine your borrowing risk. Your DTI ratio represents the total amount of debt you owe compared to the total amount of money you earn each month.

NORMALIZED ATR (expect. <8, W) --> The Normalized Average True Range (Normalized ATR) is an indicator used to measure market volatility by normalizing the average true range values. It does this by dividing the Average True Range (ATR) by the asset's closing price, converting it into a percentage. This normalization allows for the comparison of volatility levels across different securities or market conditions, regardless of the asset's price levels. The Normalized ATR helps traders to adjust their strategies based on relative volatility, rather than absolute price movements.

INDEX expect. EMA10>EMA20 --> it is expected to have EMA 10 > EMA 20 in weekly basis graph. It is known that having a strong trend in index will also increases chance of strong trend on stock levels. You need to select INDEX Market of stock via settings.

M. RELATIVE STRENGTH expect. MRS>1 --> Stan Weinstein uses the Mansfield RS indicator as another relative strength indicator. The indicator measures the variation in the 52-week ratio of stock and market.

VOLUME CHANGE (expect. >30) --> Having an increase on volume comparing to previous week can be a good sign if it occurs at the same time of breakout.

PRICE CHANGE (expect. >5 and <20) --> Having an increase on price comparing to previous week can be a good sign if it occurs at the same time of breakout.

It is better to look on weekly basis graphs.

Momentum Nexus Oscillator [UAlgo]The "Momentum Nexus Oscillator " indicator is a comprehensive momentum-based tool designed to provide traders with visual cues on market conditions using multiple oscillators. By combining four popular technical indicators—RSI (Relative Strength Index), VZO (Volume Zone Oscillator), MFI (Money Flow Index), and CCI (Commodity Channel Index)—this heatmap offers a holistic view of the market's momentum.

The indicator plots two lines: one representing the current chart’s combined momentum score and the other representing a higher timeframe’s (HTF) score, if enabled. Through smooth gradient color transitions and easy-to-read signals, the Momentum Nexus Heatmap allows traders to easily identify potential trend reversals or continuation patterns.

Traders can use this tool to detect overbought or oversold conditions, helping them anticipate possible long or short trade opportunities. The option to use a higher timeframe enhances the flexibility of the indicator for longer-term trend analysis.

🔶 Key Features

Multi-Oscillator Approach: Combines four popular momentum oscillators (RSI, VZO, MFI, and CCI) to generate a weighted score, providing a comprehensive picture of market momentum.

Dynamic Color Heatmap: Utilizes a smooth gradient transition between bullish and bearish colors, reflecting market momentum across different thresholds.

Higher Timeframe (HTF) Compatibility: Includes an optional higher timeframe input that displays a separate score line based on the same momentum metrics, allowing for multi-timeframe analysis.

Customizable Parameters: Adjustable RSI, VZO, MFI, and CCI lengths, as well as overbought and oversold levels, to match the trader’s strategy or preference.

Signal Alerts: Built-in alert conditions for both the current chart and higher timeframe scores, notifying traders when long or short entry signals are triggered.

Buy/Sell Signals: Displays visual signals (▲ and ▼) on the chart when combined scores reach overbought or oversold levels, providing clear entry cues.

User-Friendly Visualization: The heatmap is separated into four sections representing each indicator, providing a transparent view of how each contributes to the overall momentum score.

🔶 Interpreting Indicator:

Combined Score

The indicator generates a combined score by weighing the individual contributions of RSI, VZO, MFI, and CCI. This score ranges from 0 to 100 and is plotted as a line on the chart. Lower values suggest potential oversold conditions, while higher values indicate overbought conditions.

Color Heatmap

The indicator divides the combined score into four distinct sections, each representing one of the underlying momentum oscillators (RSI, VZO, MFI, and CCI). Bullish (greenish) colors indicate upward momentum, while bearish (grayish) colors suggest downward momentum.

Long/Short Signals

When the combined score drops below the oversold threshold (default is 26), a long signal (▲) is displayed on the chart, indicating a potential buying opportunity.

When the combined score exceeds the overbought threshold (default is 74), a short signal (▼) is shown, signaling a potential sell or short opportunity.

Higher Timeframe Analysis

If enabled, the indicator also plots a line representing the combined score for a higher timeframe. This can be used to align lower timeframe trades with the broader trend of a higher timeframe, providing added confirmation.

Signals for long and short entries are also plotted for the higher timeframe when its combined score reaches overbought or oversold levels.

🔶Purpose of Using Multiple Technical Indicators

The combination of RSI, VZO, MFI, and CCI in the Momentum Nexus Heatmap provides a comprehensive approach to analyzing market momentum by leveraging the unique strengths of each indicator. This multi-indicator method minimizes the limitations of using just one tool, resulting in more reliable signals and a clearer understanding of market conditions.

RSI (Relative Strength Index)

RSI contributes by measuring the strength and speed of recent price movements. It helps identify overbought or oversold levels, signaling potential trend reversals or corrections. Its simplicity and effectiveness make it one of the most widely used indicators in technical analysis, contributing to momentum assessment in a straightforward manner.

VZO (Volume Zone Oscillator)

VZO adds the critical element of volume to the analysis. By assessing whether price movements are supported by significant volume, VZO distinguishes between price changes that are driven by real market conviction and those that might be short-lived. It helps validate the strength of a trend or alert the trader to potential weakness when price moves are unsupported by volume.

MFI (Money Flow Index)

MFI enhances the analysis by combining price and volume to gauge money flow into and out of an asset. This indicator provides insight into the participation of large players in the market, showing if money is pouring into or exiting the asset. MFI acts as a volume-weighted version of RSI, giving more weight to volume shifts and helping traders understand the sustainability of price trends.

CCI (Commodity Channel Index)

CCI contributes by measuring how far the price deviates from its statistical average. This helps in identifying extreme conditions where the market might be overextended in either direction. CCI is especially useful for spotting trend reversals or continuations, particularly during market extremes, and for identifying divergence signals.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Autotable█ OVERVIEW

The library allows to automatically draw a table based on a string or float matrix (or both) controlling all of the parameters of the table (including merging cells) with parameter matrices (like, e.g. matrix of cell colors).

All things you would normally do with table.new() and table.cell() are now possible using respective parameters of library's main function, autotable() (as explained further below).

Headers can be supplied as arrays.

Merging of the cells is controlled with a special matrix of "L" and "U" values which instruct a cell to merged with the cell to the left or upwards (please see examples in the script and in this description).

█ USAGE EXAMPLES

The simplest and most straightforward:

mxF = matrix.new(3,3, 3.14)

mxF.autotable(bgcolor = color.rgb(249, 209, 29)) // displays float matrix as a table in the top right corner with defalult settings

mxS = matrix.new(3,3,"PI")

// displays string matrix as a table in the top right corner with defalult settings

mxS.autotable(Ypos = "bottom", Xpos = "right", bgcolor = #b4d400)

// displays matrix displaying a string value over a float value in each cell

mxS.autotable(mxF, Ypos = "middle", Xpos = "center", bgcolor = color.gray, text_color = #86f62a)

Draws this:

Tables with headers:

if barstate.islast

mxF = matrix.new(3,3, 3.14)

mxS = matrix.new(3,3,"PI")

arColHeaders = array.from("Col1", "Col2", "Col3")

arRowHeaders = array.from("Row1", "Row2", "Row3")

// float matrix with col headers

mxF.autotable(

bgcolor = #fdfd6b

, arColHeaders = arColHeaders

)

// string matrix with row headers

mxS.autotable(arRowHeaders = arRowHeaders, Ypos = "bottom", Xpos = "right", bgcolor = #b4d400)

// string/float matrix with both row and column headers

mxS.autotable(mxF

, Ypos = "middle", Xpos = "center"

, arRowHeaders = arRowHeaders

, arColHeaders = arColHeaders

, cornerBgClr = #707070, cornerTitle = "Corner\ncell", cornerTxtClr = #ffdc13

, bgcolor = color.gray, text_color = #86f62a

)

Draws this:

█ FUNCTIONS

One main function is autotable() which has only one required argument mxValS, a string matrix.

Please see below the description of all of the function parameters:

The table:

tbl (table) (Optional) If supplied, this table will be deleted.

The data:

mxValS (matrix ) (Required) Cell text values

mxValF (matrix) (Optional) Numerical part of cell text values. Is concatenated to the mxValS values via `string_float_separator` string (default "\n")

Table properties, have same effect as in table.new() :

defaultBgColor (color) (Optional) bgcolor to be used if mxBgColor is not supplied

Ypos (string) (Optional) "top", "bottom" or "center"

Xpos (string) (Optional) "left", "right", or "center"

frame_color (color) (Optional) frame_color like in table.new()

frame_width (int) (Optional) frame_width like in table.new()

border_color (color) (Optional) border_color like in table.new()

border_width (int) (Optional) border_width like in table.new()

force_overlay (simple bool) (Optional) If true draws table on main pane.

Cell parameters, have same effect as in table.cell() ):

mxBgColor (matrix) (Optional) like bgcolor argument in table.cell()

mxTextColor (matrix) (Optional) like text_color argument in table.cell()

mxTt (matrix) (Optional) like tooltip argument in table.cell()

mxWidth (matrix) (Optional) like width argument in table.cell()

mxHeight (matrix) (Optional) like height argument in table.cell()

mxHalign (matrix) (Optional) like text_halign argument in table.cell()

mxValign (matrix) (Optional) like text_valign argument in table.cell()

mxTextSize (matrix) (Optional) like text_size argument in table.cell()

mxFontFamily (matrix) (Optional) like text_font_family argument in table.cell()

Other table properties:

tableWidth (float) (Optional) Overrides table width if cell widths are non zero. E.g. if there are four columns and cell widths are 20 (either as set via cellW or via mxWidth) then if tableWidth is set to e.g. 50 then cell widths will be 50 * (20 / 80), where 80 is 20*4 = total width of all cells. Works simialar for widths set via mxWidth - determines max sum of widths across all cloumns of mxWidth and adjusts cell widths proportionally to it. If cell widths are 0 (i.e. auto-adjust) tableWidth has no effect.

tableHeight (float) (Optional) Overrides table height if cell heights are non zero. E.g. if there are four rows and cell heights are 20 (either as set via cellH or via mxHeight) then if tableHeigh is set to e.g. 50 then cell heights will be 50 * (20 / 80), where 80 is 20*4 = total height of all cells. Works simialar for heights set via mxHeight - determines max sum of heights across all cloumns of mxHeight and adjusts cell heights proportionally to it. If cell heights are 0 (i.e. auto-adjust) tableHeight has no effect.

defaultTxtColor (color) (Optional) text_color to be used if mxTextColor is not supplied

text_size (string) (Optional) text_size to be used if mxTextSize is not supplied

font_family (string) (Optional) cell text_font_family value to be used if a value in mxFontFamily is no supplied

cellW (float) (Optional) cell width to be used if a value in mxWidth is no supplied

cellH (float) (Optional) cell height to be used if a value in mxHeight is no supplied

halign (string) (Optional) cell text_halign value to be used if a value in mxHalign is no supplied

valign (string) (Optional) cell text_valign value to be used if a value in mxValign is no supplied

Headers parameters:

arColTitles (array) (Optional) Array of column titles. If not na a header row is added.

arRowTitles (array) (Optional) Array of row titles. If not na a header column is added.

cornerTitle (string) (Optional) If both row and column titles are supplied allows to set the value of the corner cell.

colTitlesBgColor (color) (Optional) bgcolor for header row

colTitlesTxtColor (color) (Optional) text_color for header row

rowTitlesBgColor (color) (Optional) bgcolor for header column

rowTitlesTxtColor (color) (Optional) text_color for header column

cornerBgClr (color) (Optional) bgcolor for the corner cell

cornerTxtClr (color) (Optional) text_color for the corner cell

Cell merge parameters:

mxMerge (matrix) (Optional) A matrix determining how cells will be merged. "L" - cell merges to the left, "U" - upwards.

mergeAllColTitles (bool) (Optional) Allows to print a table title instead of column headers, merging all header row cells and leaving just the value of the first cell. For more flexible options use matrix arguments leaving header/row arguments na.

mergeAllRowTitles (bool) (Optional) Allows to print one text value merging all header row cells and leaving just the value of the first cell. For more flexible options use matrix arguments leaving header/row arguments na.

Format:

string_float_separator (string) (Optional) A string used to separate string and float parts of cell values (mxValS and mxValF). Default is "\n"

format (string) (Optional) format string like in str.format() used to format numerical values

nz (string) (Optional) Determines how na numerical values are displayed.

The only other available function is autotable(string,... ) with a string parameter instead of string and float matrices which draws a one cell table.

█ SAMPLE USE

E.g., CSVParser library demo uses Autotable's for generating complex tables with merged cells.

█ CREDITS

The library was inspired by @kaigouthro's matrixautotable . A true master. Many thanks to him for his creative, beautiful and very helpful libraries.

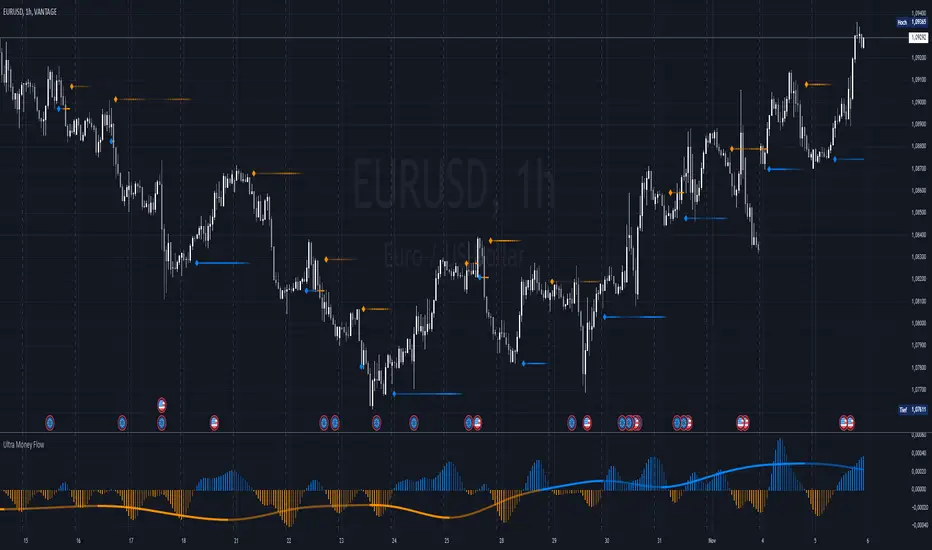

Ultra Money FlowIntroduction

The Ultra Money Flow script is a technical indicator for analyzing stock trends. It highlights buying and selling power, helping you identify bullish (rising) or bearish (falling) market trends.

Detailed Description

The Ultra Money Flow script calculates and visually displays two main components: Fast and Slow money flow. These components represent short-term and long-term trends, respectively.

Here's how it works:

.........

Inputs

You can adjust the speed of analysis (Fast Length and Slow Length) and the type of smoothing applied (e.g., Simple Moving Average, Exponential Moving Average).

Choose colors for visualizing the trends, with blue for bullish (positive) and orange for bearish (negative) movements.

.....

Money Flow Calculation

The script analyzes price changes (delta) over specified periods.

It separates upward price movements (buying power) from downward ones (selling power).

It then calculates the difference between these powers for both Fast and Slow components.

The types of smoothing methods range from traditional ones like the Simple Moving Average (SMA) to advanced ones like the Double Expotential Moving Average (DEMA) or the Triple Exponential Moving Average (TEMA) or the Recursive Moving Average (RMA) or the Weigthend Moving Average (WMA) or the Volume Weigthend Moving Average (VWMA) or Hull Moving Average (HMA).

Very Special ones are the Triple Weigthend Moving Average (TWMA) wich created RedKTrader .

I created the Multi Weigthend Moving Average (MWMA) wich is a simple signal line to the TWMA.

.....

Divergence

This indicator can show divergence by comparing the direction of price movements with the indicator value.

If the price and the indicator move in opposite directions, you can use these signals to help decide when to buy or sell.

.....

Auto Scaling

The script adjusts its calculations based on the time frame you are viewing, whether it's minutes, hours, or days, ensuring accurate representation across different time scales.

.....

Plotting

The script plots the Fast component as a histogram and the Slow component as a line, using the chosen colors to indicate bullish or bearish trends.

The thickness and transparency of these plots give additional clues about the strength of the trend.

.........

By using this indicator, traders can easily spot shifts in buying and selling power, allowing for better-informed decisions in the market.

Special Thanks

I use the TWMA-Function created from RedKTrader to smooth the values.

Special thanks to him for creating and sharing this function!

Descriptive Backtesting Framework (DBF)As the name suggests, this is a backtesting framework made to offer full backtesting functionality to any custom indicator in a visually descriptive way.

Any trade taken will be very clear to visualize on the chart and the equity line will be updated live allowing us to use the REPLAY feature to view the strategy performing in real time.

Stops and Targets will also get draw on the chart with labels and tooltips and there will be a table on the top right corner displaying lots of descriptive metrics to measure your strategy's performance.

IF YOU DECIDE TO USE THIS FRAMEWORK, PLEASE READ **EVERYTHING** BELOW

HOW TO USE IT

Step 1 - Insert Your Strategy Indicators:

Inside this framework's code, right at the beginning, you will find a dedicated section where you can manually insert any set of indicators you desire.

Just replace the example code in there with your own strategy indicators.

Step 2 - Specify The Conditions To Take Trades:

After that, there will be another section where you need to specify your strategy's conditions to enter and exit trades.

When met, those conditions will fire the trading signals to the trading engine inside the framework.

If you don't wish to use some of the available signals, please just assign false to the signal.

DO NOT DELETE THE SIGNAL VARIABLES

Step 3 - Specify Entry/Exit Prices, Stops & Targets:

Finally you'll reach the last section where you'll be able to specify entry/exit prices as well as add stops and targets.

On most cases, it's easier and more reliable to just use the close price to enter and exit trades.

If you decide to use the open price instead, please remember to change step 2 so that trades are taken on the open price of the next candle and not the present one to avoid the look ahead bias.

Stops and targets can be set in any way you want.

Also, please don't forget to update the spread. If your broker uses commissions instead of spreads or a combination of both, you'll need to manually incorporate those costs in this step.

And that's it! That's all you have to do.

Below this section you'll now see a sign warning you about not making any changes to the code below.

From here on, the framework will take care of executing the trades and calculating the performance metrics for you and making sure all calculations are consistent.

VISUAL FEATURES:

Price candles get painted according to the current trade.

They will be blue during long trades, purple on shorts and white when no trade is on.

When the framework receives the signals to start or close a trade, it will display those signals as shapes on the upper and lower limits of the chart:

DIAMOND: represents a signal to open a trade, the trade direction is represented by the shape's color;

CROSS: means a stop loss was triggered;

FLAG: means a take profit was triggered;

CIRCLE: means an exit trade signal was fired;

Hovering the mouse over the trade labels will reveal:

Asset Quantity;

Entry/Exit Prices;

Stops & Targets;

Trade Profit;

Profit As Percentage Of Trade Volume;

**Please note that there's a limit as to how many labels can be drawn on the chart at once.**

If you which to see labels from the beginning of the chart, you'll probably need to use the replay feature.

PERFORMANCE TABLE:

The performance table displays several performance metrics to evaluate the strategy.

All the performance metrics here are calculated by the framework. It does not uses the oficial pine script strategy tester.

All metrics are calculated in real time. If using the replay feature, they will be updated up to the last played bar.

Here are the available metrics and their definition:

INITIAL EQUITY: the initial amount of money we had when the strategy started, obviously...;

CURRENT EQUITY: the amount of money we have now. If using the replay feature, it will show the current equity up to the last bar played. The number on it's right side shows how many times our equity has been multiplied from it's initial value;

TRADE COUNT: how many trades were taken;

WIN COUNT: how many of those trades were wins. The percentage at the right side is the strategy WIN RATE;

AVG GAIN PER TRADE: the average percentage gain per trade. Very small values can indicate a fragile strategy that can behave in unexpected ways under high volatility conditions;

AVG GAIN PER WIN: the average percentage gain of trades that were profitable;

AVG GAIN PER LOSS: the average percentage loss on trades that were not profitable;

EQUITY MAX DD: the maximum drawdown experienced by our equity during the entire strategy backtest;

TRADE MAX DD: the maximum drawdown experienced by our equity after one single trade;

AVG MONTHLY RETURN: the compound monthly return that our strategy was able to create during the backtested period;

AVG ANNUAL RETURN: this is the strategy's CAGR (compound annual growth rate);

ELAPSED MONTHS: number of months since the backtest started;

RISK/REWARD RATIO: shows how profitable the strategy is for the amount of risk it takes. Values above 1 are very good (and rare). This is calculated as follows: (Avg Annual Return) / mod(Equity Max DD). Where mod() is the same as math.abs();

AVAILABLE SETTINGS:

SPREAD: specify your broker's asset spread

ENABLE LONGS / SHORTS: you can keep both enable or chose to take trades in only one direction

MINIMUM BARS CLOSED: to avoid trading before indicators such as a slow moving average have had time to populate, you can manually set the number of bars to wait before allowing trades.

INITIAL EQUITY: you can specify your starting equity

EXPOSURE: is the percentage of equity you wish to risk per trade. When using stops, the strategy will automatically calculate your position size to match the exposure with the stop distance. If you are not using stops then your trade volume will be the percentage of equity specified here. 100 means you'll enter trades with all your equity and 200 means you'll use a 2x leverage.

MAX LEVERAGE ALLOWED: In some situations a short stop distance can create huge levels of leverage. If you want to limit leverage to a maximum value you can set it here.

SEVERAL PLOTTING OPTIONS: You'll be able to specify which of the framework visuals you wish to see drawn on the chart.

FRAMEWORK **LIMITATIONS**:

When stop and target are both triggered in the same candle, this framework isn't able to enter faster timeframes to check which one was triggered first, so it will take the pessimistic assumption and annul the take profit signal;

This framework doesn't support pyramiding;

This framework doesn't support both long and short positions to be active at the same time. So for example, if a short signal is received while a long trade is open, the framework will close the long trade and then open a short trade;

FINAL CONSIDERATIONS:

I've been using this framework for a good time and I find it's better to use and easier to analyze a strategy's performance then relying on the oficial pine script strategy tester. However, I CANNOT GUARANTEE IT TO BE BUG FREE.

**PLEASE PERFORM A MANUAL BACKTEST BEFORE USING ANY STRATEGY WITH REAL MONEY**

Price Action Smart Money Concepts [BigBeluga]THE SMART MONEY CONCEPTS Toolkit

The Smart Money Concepts [ BigBeluga ] is a comprehensive toolkit built around the principles of "smart money" behavior, which refers to the actions and strategies of institutional investors.

The Smart Money Concepts Toolkit brings together a suite of advanced indicators that are all interconnected and built around a unified concept: understanding and trading like institutional investors, or "smart money." These indicators are not just randomly chosen tools; they are features of a single overarching framework, which is why having them all in one place creates such a powerful system.

This all-in-one toolkit provides the user with a unique experience by automating most of the basic and advanced concepts on the chart, saving them time and improving their trading ideas.

Real-time market structure analysis simplifies complex trends by pinpointing key support, resistance, and breakout levels.

Advanced order block analysis leverages detailed volume data to pinpoint high-demand zones, revealing internal market sentiment and predicting potential reversals. This analysis utilizes bid/ask zones to provide supply/demand insights, empowering informed trading decisions.

Imbalance Concepts (FVG and Breakers) allows traders to identify potential market weaknesses and areas where price might be attracted to fill the gap, creating opportunities for entry and exit.

Swing failure patterns help traders identify potential entry points and rejection zones based on price swings.

Liquidity Concepts, our advanced liquidity algorithm, pinpoints high-impact events, allowing you to predict market shifts, strong price reactions, and potential stop-loss hunting zones. This gives traders an edge to make informed trading decisions based on liquidity dynamics.

🔵 FEATURES

The indicator has quite a lot of features that are provided below:

Swing market structure

Internal market structure

Mapping structure

Adjustable market structure

Strong/Weak H&L

Sweep

Volumetric Order block / Breakers

Fair Value Gaps / Breakers (multi-timeframe)

Swing Failure Patterns (multi-timeframe)

Deviation area

Equal H&L

Liquidity Prints

Buyside & Sellside

Sweep Area

Highs and Lows (multi-timeframe)

🔵 BASIC DEMONSTRATION OF ALL FEATURES

1. MARKET STRUCTURE

The preceding image illustrates the market structure functionality within the Smart Money Concepts indicator.

➤ Solid lines: These represent the core indicator's internal structure, forming the foundation for most other components. They visually depict the overall market direction and identify major reversal points marked by significant price movements (denoted as 'x').

➤ Internal Structure: These represent an alternative internal structure with the potential to drive more rapid market shifts. This is particularly relevant when a significant gap exists in the established swing structure, specifically between the Break of Structure (BOS) and the most recent Change of High/Low (CHoCH). Identifying these formations can offer opportunities for quicker entries and potential short-term reversals.

➤ Sweeps (x): These signify potential turning points in the market where liquidity is removed from the structure. This suggests a possible trend reversal and presents crucial entry opportunities. Sweeps are identified within both swing and internal structures, providing valuable insights for informed trading decisions.

➤ Mapping structure: A tool that automatically identifies and connects significant price highs and lows, creating a zig-zag pattern. It visualizes market structure, highlights trends, support/resistance levels, and potential breakouts. Helps traders quickly grasp price action patterns and make informed decisions.

➤ Color-coded candles based on market structure: These colors visually represent the underlying market structure, making it easier for traders to quickly identify trends.

➤ Extreme H&L: It visualizes market structure with extreme high and lows, which gives perspective for macro Market Structure.

2. VOLUMETRIC ORDER BLOCKS

Order blocks are specific areas on a financial chart where significant buying or selling activity has occurred. These are not just simple zones; they contain valuable information about market dynamics. Within each of these order blocks, volume bars represent the actual buying and selling activity that took place. These volume bars offer deeper insights into the strength of the order block by showing how much buying or selling power is concentrated in that specific zone.

Additionally, these order blocks can be transformed into Breaker Blocks. When an order block fails—meaning the price breaks through this zone without reversing—it becomes a breaker block. Breaker blocks are particularly useful for trading breakouts, as they signal that the market has shifted beyond a previously established zone, offering opportunities for traders to enter in the direction of the breakout.

Here's a breakdown:

➤ Bear Order Blocks (Red): These are zones where a lot of selling happened. Traders see these areas as places where sellers were strong, pushing the price down. When the price returns to these zones, it might face resistance and drop again.

➤ Bull Order Blocks (Green): These are zones where a lot of buying happened. Traders see these areas as places where buyers were strong, pushing the price up. When the price returns to these zones, it might find support and rise again.