Breakout Trend Trading Strategy - V1Strategy in nutshell:

This strategy is made to be used in daily time-frames. Works better on trending instruments where volume is available. Hence, this is more suitable for trending shares rather than currencies, commodities and indexes where volume data is either not present or not reliable.

Breakout signifies the continuation of trend. Hence, trade in the direction of breakouts. Breakouts are calculated based on high volume and price movement in a day. This will be combined with few other conditions to generate buy and sell signals along with stop and compound targets. Supertrend is used for trend bias. Our buy and sell targets do not directly depend on the bias. But, entry criteria in opposite trend is made much difficult than that of trend direction. Further explanation of method and input parameters are explained below.

Backtesting parameters :

Capital and position sizing : Capital and position sizing parameters are set to test investing 2000 wholly on certain stock without compounding.

Initial Capital : 2000

Order Size : 100% of equity

Pyramiding : 1

ExitOnSignal : If unchecked exit is triggered solely on trailing stop

Trade Direction : Long, Short or All. Short condition is riskier than long conditions and often results in losses as per my observation. On most of the stocks trending up, strategy will not generate any short signals. This is achieved by comparing yearly high lows to previous two years to decide whether to allow short or long entries.

allowImmediateCompound : Applicable only if compounding/pyramiding is enabled in trade. If checked allows to place compounding orders immediately. If unchecked, it waits for stopline to cross order price before placing next compound.

Display Mode :

Targets : Whenever breakout happens, show marker for upTarget and downTarget

TargetChannel : Show up target and downtarget as a channel

Target With Stop : Along with targets, show also stop levels for breakouts

Up Channel : Channel created from UpTarget and respective stops

Down Channel : Channel created from DownTarget and respective stops

ShowTrailingStop : Shows trailing stop and compound lines when there is a trading position.

ShowTargetLevels : Shows Buy Sell target levels along with stop and compound lines. Trades are done as market orders. Hence, target levels are displayed after strategy makes the trade. Since only one order allowed per side without compounding, target, stop and compound levels are shown sometimes even without trade being made. These can be considered as entry levels if there is no existing position.

ShowPreviousLevels : Shows previous buy/sell target levels. When enabled, layout can look messy.

StopMultiplyer: To Set trailing stop loss.

BacktestYears: Number of years to include in backtest

So far my test cases are:

Positive : AAPL, AMZN, TSLA, RUN, VRT, ASX:APT

Negative Test Cases: WPL, WHC, NHC, WOW, COL, NAB (All ASX stocks)

Special test case: WDI

Negative test cases still show losses in backtesting. I have attempted including many conditions to eliminate or reduce the loss. But, further efforts has resulted in reduction in profits in positive cases as well. Still experimenting. Will update whenever I find improvements. Comments and suggestions welcome :)

Cari dalam skrip untuk "order"

The Maker StrategyDESCRIPTION

The Maker Strategy is a trend-following system built around exponential moving averages (EMAs). By analyzing the alignment of multiple EMAs, the strategy identifies strong bullish or bearish momentum and generates precise entry signals. This method is designed to capture sustained trends while filtering out sideways or noisy market conditions.

USER INPUTS :

• EMA 1 Length (Default: 30)

• EMA 2 Length (Default: 35)

• EMA 3 Length (Default: 40)

• EMA 4 Length (Default: 45)

• EMA 5 Length (Default: 50)

• EMA 6 Length (Default: 60)

LONG CONDITION :

A long signal is triggered when all EMAs are perfectly aligned in ascending order:

EMA1 > EMA2 > EMA3 > EMA4 > EMA5 > EMA6

SHORT CONDITION :

A short signal is triggered when all EMAs are perfectly aligned in descending order:

EMA1 < EMA2 < EMA3 < EMA4 < EMA5 < EMA6

WHY IT IS UNIQUE:

Unlike traditional EMA crossover systems that rely on just 2 or 3 moving averages, The Maker Strategy uses 6 EMAs in sequence. This ensures that trades are only taken when there is clear and strong market momentum. The approach minimizes false signals in ranging markets and focuses on capturing trends with higher probability setups.

HOW USER CAN BENEFIT FROM IT :

• Clear entry alerts for both long and short positions.

• Visual confirmation through candle coloring and EMA band fills.

• Works on multiple timeframes and instruments (stocks, forex, crypto, indices).

• Helps traders stay on the right side of the trend while avoiding whipsaws.

• A simple yet effective tool for those who want a disciplined, rules-based strategy.

Aetherium Institutional Market Resonance EngineAetherium Institutional Market Resonance Engine (AIMRE)

A Three-Pillar Framework for Decoding Institutional Activity

🎓 THEORETICAL FOUNDATION

The Aetherium Institutional Market Resonance Engine (AIMRE) is a multi-faceted analysis system designed to move beyond conventional indicators and decode the market's underlying structure as dictated by institutional capital flow. Its philosophy is built on a singular premise: significant market moves are preceded by a convergence of context , location , and timing . Aetherium quantifies these three dimensions through a revolutionary three-pillar architecture.

This system is not a simple combination of indicators; it is an integrated engine where each pillar's analysis feeds into a central logic core. A signal is only generated when all three pillars achieve a state of resonance, indicating a high-probability alignment between market organization, key liquidity levels, and cyclical momentum.

⚡ THE THREE-PILLAR ARCHITECTURE

1. 🌌 PILLAR I: THE COHERENCE ENGINE (THE 'CONTEXT')

Purpose: To measure the degree of organization within the market. This pillar answers the question: " Is the market acting with a unified purpose, or is it chaotic and random? "

Conceptual Framework: Institutional campaigns (accumulation or distribution) create a non-random, organized market environment. Retail-driven or directionless markets are characterized by "noise" and chaos. The Coherence Engine acts as a filter to ensure we only engage when institutional players are actively steering the market.

Formulaic Concept:

Coherence = f(Dominance, Synchronization)

Dominance Factor: Calculates the absolute difference between smoothed buying pressure (volume-weighted bullish candles) and smoothed selling pressure (volume-weighted bearish candles), normalized by total pressure. A high value signifies a clear winner between buyers and sellers.

Synchronization Factor: Measures the correlation between the streams of buying and selling pressure over the analysis window. A high positive correlation indicates synchronized, directional activity, while a negative correlation suggests choppy, conflicting action.

The final Coherence score (0-100) represents the percentage of market organization. A high score is a prerequisite for any signal, filtering out unpredictable market conditions.

2. 💎 PILLAR II: HARMONIC LIQUIDITY MATRIX (THE 'LOCATION')

Purpose: To identify and map high-impact institutional footprints. This pillar answers the question: " Where have institutions previously committed significant capital? "

Conceptual Framework: Large institutional orders leave indelible marks on the market in the form of anomalous volume spikes at specific price levels. These are not random occurrences but are areas of intense historical interest. The Harmonic Liquidity Matrix finds these footprints and consolidates them into actionable support and resistance zones called "Harmonic Nodes."

Algorithmic Process:

Footprint Identification: The engine scans the historical lookback period for candles where volume > average_volume * Institutional_Volume_Filter. This identifies statistically significant volume events.

Node Creation: A raw node is created at the mean price of the identified candle.

Dynamic Clustering: The engine uses an ATR-based proximity algorithm. If a new footprint is identified within Node_Clustering_Distance (ATR) of an existing Harmonic Node, it is merged. The node's price is volume-weighted, and its magnitude is increased. This prevents chart clutter and consolidates nearby institutional orders into a single, more significant level.

Node Decay: Nodes that are older than the Institutional_Liquidity_Scanback period are automatically removed from the chart, ensuring the analysis remains relevant to recent market dynamics.

3. 🌊 PILLAR III: CYCLICAL RESONANCE MATRIX (THE 'TIMING')

Purpose: To identify the market's dominant rhythm and its current phase. This pillar answers the question: " Is the market's immediate energy flowing up or down? "

Conceptual Framework: Markets move in waves and cycles of varying lengths. Trading in harmony with the current cyclical phase dramatically increases the probability of success. Aetherium employs a simplified wavelet analysis concept to decompose price action into short, medium, and long-term cycles.

Algorithmic Process:

Cycle Decomposition: The engine calculates three oscillators based on the difference between pairs of Exponential Moving Averages (e.g., EMA8-EMA13 for short cycle, EMA21-EMA34 for medium cycle).

Energy Measurement: The 'energy' of each cycle is determined by its recent volatility (standard deviation). The cycle with the highest energy is designated as the "Dominant Cycle."

Phase Analysis: The engine determines if the dominant cycles are in a bullish phase (rising from a trough) or a bearish phase (falling from a peak).

Cycle Sync: The highest conviction timing signals occur when multiple cycles (e.g., short and medium) are synchronized in the same direction, indicating broad-based momentum.

🔧 COMPREHENSIVE INPUT SYSTEM

Pillar I: Market Coherence Engine

Coherence Analysis Window (10-50, Default: 21): The lookback period for the Coherence Engine.

Lower Values (10-15): Highly responsive to rapid shifts in market control. Ideal for scalping but can be sensitive to noise.

Balanced (20-30): Excellent for day trading, capturing the ebb and flow of institutional sessions.

Higher Values (35-50): Smoother, more stable reading. Best for swing trading and identifying long-term institutional campaigns.

Coherence Activation Level (50-90%, Default: 70%): The minimum market organization required to enable signal generation.

Strict (80-90%): Only allows signals in extremely clear, powerful trends. Fewer, but potentially higher quality signals.

Standard (65-75%): A robust filter that effectively removes choppy conditions while capturing most valid institutional moves.

Lenient (50-60%): Allows signals in less-organized markets. Can be useful in ranging markets but may increase false signals.

Pillar II: Harmonic Liquidity Matrix

Institutional Liquidity Scanback (100-400, Default: 200): How far back the engine looks for institutional footprints.

Short (100-150): Focuses on recent institutional activity, providing highly relevant, immediate levels.

Long (300-400): Identifies major, long-term structural levels. These nodes are often extremely powerful but may be less frequent.

Institutional Volume Filter (1.3-3.0, Default: 1.8): The multiplier for detecting a volume spike.

High (2.5-3.0): Only registers climactic, undeniable institutional volume. Fewer, but more significant nodes.

Low (1.3-1.7): More sensitive, identifying smaller but still relevant institutional interest.

Node Clustering Distance (0.2-0.8 ATR, Default: 0.4): The ATR-based distance for merging nearby nodes.

High (0.6-0.8): Creates wider, more consolidated zones of liquidity.

Low (0.2-0.3): Creates more numerous, precise, and distinct levels.

Pillar III: Cyclical Resonance Matrix

Cycle Resonance Analysis (30-100, Default: 50): The lookback for determining cycle energy and dominance.

Short (30-40): Tunes the engine to faster, shorter-term market rhythms. Best for scalping.

Long (70-100): Aligns the timing component with the larger primary trend. Best for swing trading.

Institutional Signal Architecture

Signal Quality Mode (Professional, Elite, Supreme): Controls the strictness of the three-pillar confluence.

Professional: Loosest setting. May generate signals if two of the three pillars are in strong alignment. Increases signal frequency.

Elite: Balanced setting. Requires a clear, unambiguous resonance of all three pillars. The recommended default.

Supreme: Most stringent. Requires perfect alignment of all three pillars, with each pillar exhibiting exceptionally strong readings (e.g., coherence > 85%). The highest conviction signals.

Signal Spacing Control (5-25, Default: 10): The minimum bars between signals to prevent clutter and redundant alerts.

🎨 ADVANCED VISUAL SYSTEM

The visual architecture of Aetherium is designed not merely for aesthetics, but to provide an intuitive, at-a-glance understanding of the complex data being processed.

Harmonic Liquidity Nodes: The core visual element. Displayed as multi-layered, semi-transparent horizontal boxes.

Magnitude Visualization: The height and opacity of a node's "glow" are proportional to its volume magnitude. More significant nodes appear brighter and larger, instantly drawing the eye to key levels.

Color Coding: Standard nodes are blue/purple, while exceptionally high-magnitude nodes are highlighted in an accent color to denote critical importance.

🌌 Quantum Resonance Field: A dynamic background gradient that visualizes the overall market environment.

Color: Shifts from cool blues/purples (low coherence) to energetic greens/cyans (high coherence and organization), providing instant context.

Intensity: The brightness and opacity of the field are influenced by total market energy (a composite of coherence, momentum, and volume), making powerful market states visually apparent.

💎 Crystalline Lattice Matrix: A geometric web of lines projected from a central moving average.

Mathematical Basis: Levels are projected using multiples of the Golden Ratio (Phi ≈ 1.618) and the ATR. This visualizes the natural harmonic and fractal structure of the market. It is not arbitrary but is based on mathematical principles of market geometry.

🧠 Synaptic Flow Network: A dynamic particle system visualizing the engine's "thought process."

Node Density & Activation: The number of particles and their brightness/color are tied directly to the Market Coherence score. In high-coherence states, the network becomes a dense, bright, and organized web. In chaotic states, it becomes sparse and dim.

⚡ Institutional Energy Waves: Flowing sine waves that visualize market volatility and rhythm.

Amplitude & Speed: The height and speed of the waves are directly influenced by the ATR and volume, providing a feel for market energy.

📊 INSTITUTIONAL CONTROL MATRIX (DASHBOARD)

The dashboard is the central command console, providing a real-time, quantitative summary of each pillar's status.

Header: Displays the script title and version.

Coherence Engine Section:

State: Displays a qualitative assessment of market organization: ◉ PHASE LOCK (High Coherence), ◎ ORGANIZING (Moderate Coherence), or ○ CHAOTIC (Low Coherence). Color-coded for immediate recognition.

Power: Shows the precise Coherence percentage and a directional arrow (↗ or ↘) indicating if organization is increasing or decreasing.

Liquidity Matrix Section:

Nodes: Displays the total number of active Harmonic Liquidity Nodes currently being tracked.

Target: Shows the price level of the nearest significant Harmonic Node to the current price, representing the most immediate institutional level of interest.

Cycle Matrix Section:

Cycle: Identifies the currently dominant market cycle (e.g., "MID ") based on cycle energy.

Sync: Indicates the alignment of the cyclical forces: ▲ BULLISH , ▼ BEARISH , or ◆ DIVERGENT . This is the core timing confirmation.

Signal Status Section:

A unified status bar that provides the final verdict of the engine. It will display "QUANTUM SCAN" during neutral periods, or announce the tier and direction of an active signal (e.g., "◉ TIER 1 BUY ◉" ), highlighted with the appropriate color.

🎯 SIGNAL GENERATION LOGIC

Aetherium's signal logic is built on the principle of strict, non-negotiable confluence.

Condition 1: Context (Coherence Filter): The Market Coherence must be above the Coherence Activation Level. No signals can be generated in a chaotic market.

Condition 2: Location (Liquidity Node Interaction): Price must be actively interacting with a significant Harmonic Liquidity Node.

For a Buy Signal: Price must be rejecting the Node from below (testing it as support).

For a Sell Signal: Price must be rejecting the Node from above (testing it as resistance).

Condition 3: Timing (Cycle Alignment): The Cyclical Resonance Matrix must confirm that the dominant cycles are synchronized with the intended trade direction.

Signal Tiering: The Signal Quality Mode input determines how strictly these three conditions must be met. 'Supreme' mode, for example, might require not only that the conditions are met, but that the Market Coherence is exceptionally high and the interaction with the Node is accompanied by a significant volume spike.

Signal Spacing: A final filter ensures that signals are spaced by a minimum number of bars, preventing over-alerting in a single move.

🚀 ADVANCED TRADING STRATEGIES

The Primary Confluence Strategy: The intended use of the system. Wait for a Tier 1 (Elite/Supreme) or Tier 2 (Professional/Elite) signal to appear on the chart. This represents the alignment of all three pillars. Enter after the signal bar closes, with a stop-loss placed logically on the other side of the Harmonic Node that triggered the signal.

The Coherence Context Strategy: Use the Coherence Engine as a standalone market filter. When Coherence is high (>70%), favor trend-following strategies. When Coherence is low (<50%), avoid new directional trades or favor range-bound strategies. A sharp drop in Coherence during a trend can be an early warning of a trend's exhaustion.

Node-to-Node Trading: In a high-coherence environment, use the Harmonic Liquidity Nodes as both entry points and profit targets. For example, after a BUY signal is generated at one Node, the next Node above it becomes a logical first profit target.

⚖️ RESPONSIBLE USAGE AND LIMITATIONS

Decision Support, Not a Crystal Ball: Aetherium is an advanced decision-support tool. It is designed to identify high-probability conditions based on a model of institutional behavior. It does not predict the future.

Risk Management is Paramount: No indicator can replace a sound risk management plan. Always use appropriate position sizing and stop-losses. The signals provided are probabilistic, not certainties.

Past Performance Disclaimer: The market models used in this script are based on historical data. While robust, there is no guarantee that these patterns will persist in the future. Market conditions can and do change.

Not a "Set and Forget" System: The indicator performs best when its user understands the concepts behind the three pillars. Use the dashboard and visual cues to build a comprehensive view of the market before acting on a signal.

Backtesting is Essential: Before applying this tool to live trading, it is crucial to backtest and forward-test it on your preferred instruments and timeframes to understand its unique behavior and characteristics.

🔮 CONCLUSION

The Aetherium Institutional Market Resonance Engine represents a paradigm shift from single-variable analysis to a holistic, multi-pillar framework. By quantifying the abstract concepts of market context, location, and timing into a unified, logical system, it provides traders with an unprecedented lens into the mechanics of institutional market operations.

It is not merely an indicator, but a complete analytical engine designed to foster a deeper understanding of market dynamics. By focusing on the core principles of institutional order flow, Aetherium empowers traders to filter out market noise, identify key structural levels, and time their entries in harmony with the market's underlying rhythm.

"In all chaos there is a cosmos, in all disorder a secret order." - Carl Jung

— Dskyz, Trade with insight. Trade with confluence. Trade with Aetherium.

KEMAD | QuantumResearchQuantumResearch KEMAD Indicator

The QuantumResearch KEMAD Indicator is a sophisticated trend-following and volatility-based tool designed for traders who demand precision in detecting market trends and price reversals. By leveraging advanced techniques implemented in PineScript, this indicator integrates a Kalman filter, an Exponential Moving Average (EMA), and dynamic ATR-based deviation bands to produce clear, actionable trading signals.

1. Overview

The KEMAD Indicator aims to:

Reduce Market Noise: Employ a Kalman filter to smooth price data.

Identify Trends: Use an EMA of the filtered price to define the prevailing market direction.

Set Dynamic Thresholds: Adjust breakout levels with ATR-based deviation bands.

Generate Signals: Provide clear long and short trading signals along with intuitive visual cues.

2. How It Works

A. Kalman Filter Smoothing

Purpose: The Kalman filter refines the selected price source (e.g., close price) by reducing short-term fluctuations, thus offering a clearer view of the underlying price movement.

Customization: Users can adjust key parameters such as:

Process Noise: Controls the filter’s sensitivity to recent changes.

Measurement Noise: Determines how responsive the filter is to incoming price data.

Filter Order: Sets the number of data points considered in the smoothing process.

B. EMA-Based Trend Detection

Primary Trend EMA: A 25-period EMA is applied to the Kalman-filtered price, serving as the core trend indicator.

Signal Mechanism:

Long Signal: Triggered when the price exceeds the EMA plus an ATR-based upper deviation.

Short Signal: Triggered when the price falls below the EMA minus an ATR-based lower deviation.

C. ATR Deviation Bands

ATR Utilization: The Average True Range (ATR) is computed (default length of 21) to assess market volatility.

Dynamic Thresholds:

Upper Deviation: Calculated by adding 1.5× ATR to the EMA (for long signals).

Lower Deviation: Calculated by subtracting 1.1× ATR from the EMA (for short signals).

These bands adapt to current volatility, ensuring that signal thresholds are both dynamic and market-sensitive.

3. Visual Representation

The indicator’s design emphasizes clarity and ease of use:

Color-Coded Bar Signals:

Green Bars: Indicate bullish conditions when a long signal is active.

Red Bars: Indicate bearish conditions when a short signal is active.

Trend Confirmation Line: A 54-period EMA is plotted to further validate trend direction. Its color dynamically changes to reflect the active trend.

Background Fill: The space between a calculated price midpoint (typically the average of high and low) and the EMA is filled, visually emphasizing the prevailing market trend.

4. Customization & Parameters

The KEMAD Indicator is highly configurable, allowing traders to tailor the tool to their specific trading strategies and market conditions:

ATR Settings:

ATR Length: Default is 21; adjusts sensitivity to market volatility.

EMA Settings:

Trend EMA Length: Default is 25; smooths price action for trend detection.

Confirmation EMA Length: Default is 54; aids in confirming the trend.

Kalman Filter Parameters:

Process Noise: Default is 0.01.

Measurement Noise: Default is 3.0.

Filter Order: Default is 5.

Deviation Multipliers:

Long Signal Multiplier: Default is 1.5× ATR.

Short Signal Multiplier: Default is 1.1× ATR.

Appearance: Eight customizable color themes are available to suit individual visual preferences.

5. Trading Applications

The versatility of the KEMAD Indicator makes it suitable for various trading strategies:

Trend Following: It helps identify and ride sustained bullish or bearish trends by filtering out market noise.

Breakout Trading: Detects when prices move beyond the ATR-based deviation bands, signaling potential breakout opportunities.

Reversal Detection: Alerts traders to potential trend reversals when price crosses the dynamically smoothed EMA.

Risk Management: Offers clearly defined entry and exit points, based on volatility-adjusted thresholds, enhancing trade precision and risk control.

6. Final Thoughts

The QuantumResearch KEMAD Indicator represents a unique blend of advanced filtering (via the Kalman filter), robust trend analysis (using EMAs), and dynamic volatility assessment (through ATR deviation bands).

Its PineScript implementation allows for a high degree of customization, making it an invaluable tool for traders looking to reduce noise, accurately detect trends, and manage risk effectively.

Whether used for trend following, breakout strategies, or reversal detection, the KEMAD Indicator is designed to adapt to varying market conditions and trading styles.

Important Disclaimer: Past data does not predict future behavior. This indicator is provided for informational purposes only; no indicator or strategy can guarantee future results. Always perform thorough analysis and use proper risk management before trading.

PitchforkLibrary "Pitchfork"

Pitchfork class

method tostring(this)

Converts PitchforkTypes/Fork object to string representation

Namespace types: Fork

Parameters:

this (Fork) : PitchforkTypes/Fork object

Returns: string representation of PitchforkTypes/Fork

method tostring(this)

Converts Array of PitchforkTypes/Fork object to string representation

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/Fork object

Returns: string representation of PitchforkTypes/Fork array

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/PitchforkProperties object to string representation

Namespace types: PitchforkProperties

Parameters:

this (PitchforkProperties) : PitchforkTypes/PitchforkProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/PitchforkProperties

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/PitchforkDrawingProperties object to string representation

Namespace types: PitchforkDrawingProperties

Parameters:

this (PitchforkDrawingProperties) : PitchforkTypes/PitchforkDrawingProperties object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/PitchforkDrawingProperties

method tostring(this, sortKeys, sortOrder)

Converts PitchforkTypes/Pitchfork object to string representation

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

Returns: string representation of PitchforkTypes/Pitchfork

method createDrawing(this)

Creates PitchforkTypes/PitchforkDrawing from PitchforkTypes/Pitchfork object

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

Returns: PitchforkTypes/PitchforkDrawing object created

method createDrawing(this)

Creates PitchforkTypes/PitchforkDrawing array from PitchforkTypes/Pitchfork array of objects

Namespace types: array

Parameters:

this (array) : array of PitchforkTypes/Pitchfork object

Returns: array of PitchforkTypes/PitchforkDrawing object created

method draw(this)

draws from PitchforkTypes/PitchforkDrawing object

Namespace types: PitchforkDrawing

Parameters:

this (PitchforkDrawing) : PitchforkTypes/PitchforkDrawing object

Returns: PitchforkTypes/PitchforkDrawing object drawn

method delete(this)

deletes PitchforkTypes/PitchforkDrawing object

Namespace types: PitchforkDrawing

Parameters:

this (PitchforkDrawing) : PitchforkTypes/PitchforkDrawing object

Returns: PitchforkTypes/PitchforkDrawing object deleted

method delete(this)

deletes underlying drawing of PitchforkTypes/Pitchfork object

Namespace types: Pitchfork

Parameters:

this (Pitchfork) : PitchforkTypes/Pitchfork object

Returns: PitchforkTypes/Pitchfork object deleted

method delete(this)

deletes array of PitchforkTypes/PitchforkDrawing objects

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/PitchforkDrawing object

Returns: Array of PitchforkTypes/PitchforkDrawing object deleted

method delete(this)

deletes underlying drawing in array of PitchforkTypes/Pitchfork objects

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/Pitchfork object

Returns: Array of PitchforkTypes/Pitchfork object deleted

method clear(this)

deletes array of PitchforkTypes/PitchforkDrawing objects and clears the array

Namespace types: array

Parameters:

this (array) : Array of PitchforkTypes/PitchforkDrawing object

Returns: void

method clear(this)

deletes array of PitchforkTypes/Pitchfork objects and clears the array

Namespace types: array

Parameters:

this (array) : Array of Pitchfork/Pitchfork object

Returns: void

PitchforkDrawingProperties

Pitchfork Drawing Properties object

Fields:

extend (series bool) : If set to true, forks are extended towards right. Default is true

fill (series bool) : Fill forklines with transparent color. Default is true

fillTransparency (series int) : Transparency at which fills are made. Only considered when fill is set. Default is 80

forceCommonColor (series bool) : Force use of common color for forks and fills. Default is false

commonColor (series color) : common fill color. Used only if ratio specific fill colors are not available or if forceCommonColor is set to true.

PitchforkDrawing

Pitchfork drawing components

Fields:

medianLine (Line type from Trendoscope/Drawing/2) : Median line of the pitchfork

baseLine (Line type from Trendoscope/Drawing/2) : Base line of the pitchfork

forkLines (array type from Trendoscope/Drawing/2) : fork lines of the pitchfork

linefills (array type from Trendoscope/Drawing/2) : Linefills between forks

Fork

Fork object property

Fields:

ratio (series float) : Fork ratio

forkColor (series color) : color of fork. Default is blue

include (series bool) : flag to include the fork in drawing. Default is true

PitchforkProperties

Pitchfork Properties

Fields:

forks (array) : Array of Fork objects

type (series string) : Pitchfork type. Supported values are "regular", "schiff", "mschiff", Default is regular

inside (series bool) : Flag to identify if to draw inside fork. If set to true, inside fork will be drawn

Pitchfork

Pitchfork object

Fields:

a (chart.point) : Pivot Point A of pitchfork

b (chart.point) : Pivot Point B of pitchfork

c (chart.point) : Pivot Point C of pitchfork

properties (PitchforkProperties) : PitchforkProperties object which determines type and composition of pitchfork

dProperties (PitchforkDrawingProperties) : Drawing properties for pitchfork

lProperties (LineProperties type from Trendoscope/Drawing/2) : Common line properties for Pitchfork lines

drawing (PitchforkDrawing) : PitchforkDrawing object

Mean Price

^^ Plotting switched to Line.

This method of financial time series (aka bars) downsampling is literally, naturally, and thankfully the best you can do in terms of maximizing info gain. You can finally chill and feed it to your studies & eyes, and probably use nothing else anymore.

(HL2 and occ3 also have use cases, but other aggregation methods? Not really, even if they do, the use cases are ‘very’ specific). Tho in order to understand why, you gotta read the following wall, or just believe me telling you, ‘I put it on my momma’.

The true story about trading volumes and why this is all a big misdirection

Actually, you don’t need to be a quant to get there. All you gotta do is stop blindly following other people’s contextual (at best) solutions, eg OC2 aggregation xD, and start using your own brain to figure things out.

Every individual trade (basically an imprint on 1D price space that emerges when market orders hit the order book) has several features like: price, time, volume, AND direction (Up if a market buy order hits the asks, Down if a market sell order hits the bids). Now, the last two features—volume and direction—can be effectively combined into one (by multiplying volume by 1 or -1), and this is probably how every order matching engine should output data. If we’re not considering size/direction, we’re leaving data behind. Moreover, trades aren’t just one-price dots all the time. One trade can consume liquidity on several levels of the order book, so a single trade can be several ticks big on the price axis.

You may think now that there are no zero-volume ticks. Well, yes and no. It depends on how you design an exchange and whether you allow intra-spread trades/mid-spread trades (now try to Google it). Intra-spread trades could happen if implemented when a matching engine receives both buy and sell orders at the same microsecond period. This way, you can match the orders with each other at a better price for both parties without even hitting the book and consuming liquidity. Also, if orders have different sizes, the remaining part of the bigger order can be sent to the order book. Basically, this type of trade can be treated as an OTC trade, having zero volume because we never actually hit the book—there’s no imprint. Another reason why it makes sense is when we think about volume as an impact or imbalance act, and how the medium (order book in our case) responds to it, providing information. OTC and mid-spread trades are not aggressive sells or buys; they’re neutral ticks, so to say. However huge they are, sometimes many blocks on NYSE, they don’t move the price because there’s no impact on the medium (again, which is the order book)—they’re not providing information.

... Now, we need to aggregate these trades into, let’s say, 1-hour bars (remember that a trade can have either positive or negative volume). We either don’t want to do it, or we don’t have this kind of information. What we can do is take already aggregated OHLC bars and extract all the info from them. Given the market is fractal, bars & trades gotta have the same set of features:

- Highest & lowest ticks (high & low) <- by price;

- First & last ticks (open & close) <- by time;

- Biggest and smallest ticks <- by volume.*

*e.g., in the array ,

2323: biggest trade,

-1212: smallest trade.

Now, in our world, somehow nobody started to care about the biggest and smallest trades and their inclusion in OHLC data, while this is actually natural. It’s the same way as it’s done with high & low and open & close: we choose the minimum and maximum value of a given feature/axis within the aggregation period.

So, we don’t have these 2 values: biggest and smallest ticks. The best we can do is infer them, and given the fact the biggest and smallest ticks can be located with the same probability everywhere, all we can do is predict them in the middle of the bar, both in time and price axes. That’s why you can see two HL2’s in each of the 3 formulas in the code.

So, summed up absolute volumes that you see in almost every trading platform are actually just a derivative metric, something that I call Type 2 time series in my own (proprietary ‘for now’) methods. It doesn’t have much to do with market orders hitting the non-uniform medium (aka order book); it’s more like a statistic. Still wanna use VWAP? Ok, but you gotta understand you’re weighting Type 1 (natural) time series by Type 2 (synthetic) ones.

How to combine all the data in the right way (khmm khhm ‘order’)

Now, since we have 6 values for each bar, let’s see what information we have about them, what we don’t have, and what we can do about it:

- Open and close: we got both when and where (time (order) and price);

- High and low: we got where, but we don’t know when;

- Biggest & smallest trades: we know shit, we infer it the way it was described before.'

By using the location of the close & open prices relative to the high & low prices, we can make educated guesses about whether high or low was made first in a given bar. It’s not perfect, but it’s ultimately all we can do—this is the very last bit of info we can extract from the data we have.

There are 2 methods for inferring volume delta (which I call simply volume) that are presented everywhere, even here on TradingView. Funny thing is, this is actually 2 parts of the 1 method. I wonder how many folks see through it xD. The same method can be used for both inferring volume delta AND making educated guesses whether high or low was made first.

Imagine and/or find the cases on your charts to understand faster:

* Close > open means we have an up bar and probably the volume is positive, and probably high was made later than low.

* Close < open means we have a down bar and probably the volume is negative, and probably low was made later than high.

Now that’s the point when you see that these 2 mentioned methods are actually parts of the 1 method:

If close = open, we still have another clue: distance from open/close pair to high (HC), and distance from open/close pair to low (LC):

* HC < LC, probably high was made later.

* HC > LC, probably low was made later.

And only if close = open and HC = LC, only in this case we have no clue whether high or low was made earlier within a bar. We simply don’t have any more information to even guess. This bar is called a neutral bar.

At this point, we have both time (order) and price info for each of our 6 values. Now, we have to solve another weighted average problem, and that’s it. We’ll weight prices according to the order we’ve guessed. In the neutral bar case, open has a weight of 1, close has a weight of 3, and both high and low have weights of 2 since we can’t infer which one was made first. In all cases, biggest and smallest ticks are modeled with HL2 and weighted like they’re located in the middle of the bar in a time sense.

P.S.: I’ve also included a "robust" method where all the bars are treated like neutral ones. I’ve used it before; obviously, it has lesser info gain -> works a bit worse.

Strategy: Candlestick Wick Analysis with Volume Conditions

This strategy focuses on analyzing the wicks (or shadows) of candlesticks to identify potential trading opportunities based on candlestick structure and volume. Based on these criteria, it places stop orders at the extremities of the wicks when certain conditions are met, thus increasing the chances of capturing significant price movements.

Trading Criteria

Volume Conditions:

The strategy checks if the volume of the current candle is higher than that of the previous three candles. This ensures that the observed price movement is supported by significant volume, increasing the probability that the price will continue in the same direction.

Wick Analysis:

Upper Wick:

If the upper wick of a candle represents more than 90% of its body size and is longer than the lower wick, this indicates that the price tested a resistance level before pulling back.

Order Placement: In this case, a Buy Stop order is placed at the upper extremity of the wick. This means that if the price rises back to this level, the order will be triggered, and the trader will take a buy position.

SL Management: A stop-loss is then placed below the lowest point of the same candle. This protects the trader by limiting losses if the price falls back after the order is triggered.

Lower Wick:

If the lower wick of a candle is longer than the upper wick and represents more than 90% of its body size, this indicates that the price tested a support level before rising.

Order Placement: In this case, a Sell Stop order is placed at the lower extremity of the wick. Thus, if the price drops back to this level, the order will be triggered, and the trader will take a sell position.

SL Management: A stop-loss is then placed above the highest point of the same candle. This ensures risk management by limiting losses if the price rebounds upward after the order is triggered.

Strategy Advantages

Responsiveness to Price Movements: The strategy is designed to detect significant price movements based on the market's reaction around support and resistance levels. By placing stop orders directly at the wick extremities, it allows capturing strong movements in the direction indicated by the candles.

Securing Positions: Using stop-losses positioned just above or below key levels (wicks) provides better risk management. If the market doesn't move as expected, the position is automatically closed with a limited loss.

Clear Visual Indicators: Symbols are displayed on the chart at the points where orders have been placed, making it easier to understand trading decisions. This helps to quickly identify the support or resistance levels tested by the price, as well as potential entry points.

Conclusion

The strategy is based on the idea that large wicks signal areas where buyers or sellers have tested significant price levels before temporarily retreating. By placing stop orders at the extremities of these wicks, the strategy allows capturing price movements when they confirm, while limiting risks through strategically placed stop-losses. It thus offers a balanced approach between capturing potential profit and managing risk.

This description emphasizes the idea of capturing significant market movements with stop orders while providing a clear explanation of the logic and risk management. It’s tailored for publication on TradingView and highlights the robustness of the strategy.

Liquidity VisualizerThe "Liquidity Visualizer" indicator is designed to help traders visualize potential areas of liquidity on a price chart. In trading, liquidity often accumulates around key levels where market participants have placed their stop orders or pending orders. These levels are commonly found at significant highs and lows, where traders tend to set their stop-losses or take-profit orders. The indicator aims to highlight these areas by drawing unbroken lines that extend indefinitely until breached by the price action.

Specifically, this indicator identifies and marks pivot highs and pivot lows, which are price levels where a trend changes direction. When a pivot high or pivot low is formed, it is represented on the chart with a horizontal line that continues to extend until the price touches or surpasses that level. The line remains in place as long as the level remains unbroken, which means there is potential liquidity still resting at that level.

The concept behind this indicator is that liquidity is likely to be resting at unbroken pivot points. These levels are areas where stop-loss orders or pending buy/sell orders may have accumulated, making them attractive zones for large market participants, such as institutions, to target. By visualizing these unbroken levels, traders can gain insight into where liquidity might be concentrated and where potential price reversals or significant movements could occur as liquidity is taken out.

The indicator helps traders make more informed decisions by showing them key price levels that may attract significant market activity. For instance, if a trader sees multiple unbroken pivot high lines above the current price, they might infer that there is a cluster of liquidity in that area, which could lead to a price spike as those levels are breached. Similarly, unbroken pivot lows may indicate areas where downside liquidity is concentrated.

In summary, this indicator acts as a "liquidity visualizer," providing traders with a clear, visual representation of potential liquidity resting at significant pivot points. This information can be valuable for understanding where price might be drawn to, and where large movements might occur as liquidity is targeted and removed by market participants.

Grid TraderGrid Trader Indicator ( GTx ):

Overview

The Grid Trader Indicator is a tool that helps traders visualize key levels within a specified trading range. The indicator plots accumulation and distribution levels, an entry level, an exit level, and a midpoint. This guide will help you understand how to use the indicator and its features for effective grid trading.

Basics of Trading Range, Grid Buy, and Grid Sell

Trading Range

A trading range is the horizontal price movement between a defined upper ( resistance ) and lower ( support ) level over a period of time. When a security trades within a range, it repeatedly moves between these two levels without trending upwards or downwards significantly. Traders often use the trading range to identify potential buy and sell points:

Upper Level (Resistance): This is the price level at which selling pressure overcomes buying pressure, preventing the price from rising further.

Lower Level (Support): This is the price level at which buying pressure overcomes selling pressure, preventing the price from falling further.

Grid Trading Strategy

Grid trading is a type of trading strategy that involves placing buy and sell orders at predefined intervals around a set price. It aims to profit from the natural market volatility by buying low and selling high in a range-bound market. The strategy divides the trading range into several grid levels where orders are placed.

Grid Buy

Grid buy orders are placed at intervals below the current price . When the price drops to these levels, buy orders are triggered . This strategy ensures that the trader buys more as the price falls, potentially lowering the average purchase price .

Grid Sell

Grid sell orders are placed at intervals above the current price . When the price rises to these levels, sell orders are triggered . This ensures that the trader sells portions of their holdings as the price increases, potentially securing profits at higher levels .

Key Points of Grid Trading

Grid Size : The interval between each buy and sell order. This can be constant (e.g., $2 intervals) or variable based on certain conditions.

Accumulation Range : The lower part of the trading range where buy orders are placed.

Distribution Range : The upper part of the trading range where sell orders are placed.

Midpoint : The average price of the entry and exit levels, often used as a reference point for balance.

As the price moves up and down within this range, your buy orders will be triggered as the price drops and your sell orders will be triggered as the price rises. This allows you to accumulate more of the asset at lower prices and sell portions at higher prices, profiting from the price oscillations within the defined range. Grid trading can be particularly effective in a sideways market where there is no clear long-term trend. However, it requires careful monitoring and adjustment of grid levels based on market conditions to minimize risks and maximize returns .

Configuring the Indicator :

Once the indicator is added, you will see a settings icon next to it. Click on it to open the settings menu.

Adjust the Upper Level , Lower Level , Entry Level , and Exit Level to match your trading strategy and market conditions.

Set the Levels Visibility to control how many bars back the levels will be plotted.

Interpreting the Levels :

Accumulation Levels : These are plotted below the entry level and are potential buy zones. They are labeled as Accumulation Level 1, 2, and 3.

Distribution Levels : These are plotted above the exit level and are potential sell zones. They are labeled as Distribution Level 1, 2, and 3.

Upper Level : Marked in fuchsia, indicating the top boundary of the trading range.

Exit Level : Marked in yellow, indicating the level at which you plan to exit trades.

Midpoint : Marked in white, indicating the average of the entry and exit levels.

Entry Level : Marked in yellow, indicating the level at which you plan to enter trades.

Lower Level : Marked in aqua, indicating the bottom boundary of the trading range.

By visualizing key levels, you can make informed decisions on where to place buy and sell orders, potentially maximizing your trading profits through systematic grid trading.

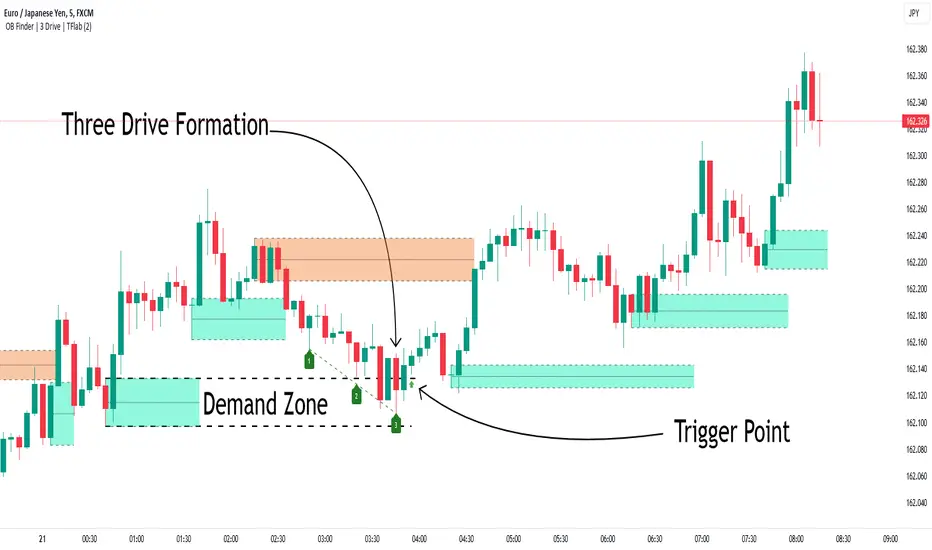

Smart Money Setup 04 [TradingFinder] Three Drive (Harmonic) + OB🔵 Introduction

The "Three Drive" pattern is a well-known formation in technical analysis, recognized for its ability to signal potential trend reversals in price action. Within the realm of trading, particularly in the context of "Reversal Patterns," the Three Drive pattern holds significance as a reliable indicator of shifts in market sentiment.

🟣 Bullish 3 Drive

This pattern typically manifests at a price bottom, where a sequence of lower lows suggests a prevailing negative trend. However, within the structure of the Three Drive pattern, a notable occurrence unfolds.

The second low breaches the range of the first low, followed by the third low surpassing the range of the second low. These penetrations signify a diminishing selling pressure and an emerging buying interest.

Traders often await the confirmation of the third low surpassing the second low as an entry point, with price targets set at the highs formed within the Three Drive pattern.

🟣 Bearish 3 Drive

Conversely, the Bearish Three Drive pattern emerges at a price top, characterized by a sequence of higher highs indicating an upward trend. Yet, amidst this apparent bullish momentum, a shift occurs.

The second high breaks beyond the range of the first high, succeeded by the third high exceeding the range of the second high. These breaches signify a waning buying strength and a resurgence in selling pressure.

Entry into a trade is often executed after the confirmation of the third high surpassing the second high, with targets set at the lows formed within the Three Drive pattern.

Importance :

Understanding the Three Drive pattern's significance extends beyond mere technical analysis. It bears resemblance to other established patterns, such as the Harmonic Pattern and Ending Diagonal within the Elliott Wave Theory.

Recognizing these parallels aids traders in comprehending broader market dynamics and potential price movements.

🔵 Formation of 3 Drive in Order Block Zone

The convergence of the Three Drive pattern with the concept of the Order Block Zone introduces a nuanced layer to traders' analytical approach.

In "Price Action" methodology, Order Blocks represent areas on the price chart where significant market players, such as institutional traders, have executed notable orders.

These zones often act as barriers, with price encountering resistance or support upon reaching them.

When the Three Drive pattern forms within an Order Block Zone, it signifies a confluence of market dynamics.

The completion of the pattern within this zone suggests a potential reversal in the prevailing trend, augmented by the presence of significant institutional orders.

Traders incorporate these Order Blocks into their analysis to identify probable levels where price may change direction, enhancing the reliability of their trading decisions.

🔵 How to Use :

To effectively utilize the Three Drive pattern within the Order Block Zone, traders seek alignment between the completion of the pattern and the presence of significant Order Blocks.

This convergence enhances the reliability of the pattern's signals, increasing the likelihood of successful trade outcomes.

Bullish Three Drive in Demand Zone :

Bearish Three Drive in Supply Zone :

Settings :

You can set your desired "Pivot Period" via settings for the indicator to identify setups based on it.

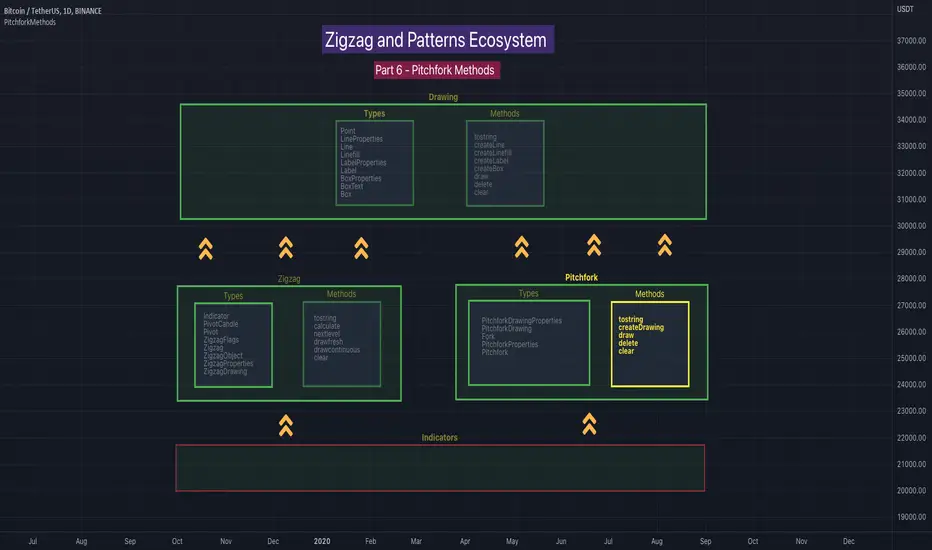

ZigzagLibrary "Zigzag"

Zigzag related user defined types. Depends on DrawingTypes library for basic types

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts ZigzagTypes/Pivot object to string representation

Namespace types: Pivot

Parameters:

this (Pivot) : ZigzagTypes/Pivot

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (string ) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of ZigzagTypes/Pivot

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts Array of Pivot objects to string representation

Namespace types: Pivot

Parameters:

this (Pivot ) : Pivot object array

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (string ) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of Pivot object array

method tostring(this)

Converts ZigzagFlags object to string representation

Namespace types: ZigzagFlags

Parameters:

this (ZigzagFlags) : ZigzagFlags object

Returns: string representation of ZigzagFlags

method tostring(this, sortKeys, sortOrder, includeKeys)

Converts ZigzagTypes/Zigzag object to string representation

Namespace types: Zigzag

Parameters:

this (Zigzag) : ZigzagTypes/Zigzagobject

sortKeys (bool) : If set to true, string output is sorted by keys.

sortOrder (int) : Applicable only if sortKeys is set to true. Positive number will sort them in ascending order whreas negative numer will sort them in descending order. Passing 0 will not sort the keys

includeKeys (string ) : Array of string containing selective keys. Optional parmaeter. If not provided, all the keys are considered

Returns: string representation of ZigzagTypes/Zigzag

method calculate(this, ohlc, indicators, indicatorNames)

Calculate zigzag based on input values and indicator values

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

ohlc (float ) : Array containing OHLC values. Can also have custom values for which zigzag to be calculated

indicators (matrix) : Array of indicator values

indicatorNames (string ) : Array of indicator names for which values are present. Size of indicators array should be equal to that of indicatorNames

Returns: current Zigzag object

method calculate(this)

Calculate zigzag based on properties embedded within Zigzag object

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

Returns: current Zigzag object

method nextlevel(this)

Calculate Next Level Zigzag based on the current calculated zigzag object

Namespace types: Zigzag

Parameters:

this (Zigzag) : Zigzag object

Returns: Next Level Zigzag object

method clear(this)

Clears zigzag drawings array

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing ) : array

Returns: void

method drawplain(this)

draws fresh zigzag based on properties embedded in ZigzagDrawing object without trying to calculate

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

Returns: ZigzagDrawing object

method drawfresh(this, ohlc, indicators, indicatorNames)

draws fresh zigzag based on properties embedded in ZigzagDrawing object

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

ohlc (float ) : values on which the zigzag needs to be calculated and drawn. If not set will use regular OHLC

indicators (matrix) : Array of indicator values

indicatorNames (string ) : Array of indicator names for which values are present. Size of indicators array should be equal to that of indicatorNames

Returns: ZigzagDrawing object

method drawcontinuous(this, ohlc, indicators, indicatorNames)

draws zigzag based on the zigzagmatrix input

Namespace types: ZigzagDrawing

Parameters:

this (ZigzagDrawing) : ZigzagDrawing object

ohlc (float ) : values on which the zigzag needs to be calculated and drawn. If not set will use regular OHLC

indicators (matrix) : Array of indicator values

indicatorNames (string ) : Array of indicator names for which values are present. Size of indicators array should be equal to that of indicatorNames

Returns:

method getPrices(pivots)

Namespace types: Pivot

Parameters:

pivots (Pivot )

method getBars(pivots)

Namespace types: Pivot

Parameters:

pivots (Pivot )

Indicator

Indicator is collection of indicator values applied on high, low and close

Fields:

indicatorHigh (series float) : Indicator Value applied on High

indicatorLow (series float) : Indicator Value applied on Low

PivotCandle

PivotCandle represents data of the candle which forms either pivot High or pivot low or both

Fields:

_high (series float) : High price of candle forming the pivot

_low (series float) : Low price of candle forming the pivot

length (series int) : Pivot length

pHighBar (series int) : represents number of bar back the pivot High occurred.

pLowBar (series int) : represents number of bar back the pivot Low occurred.

pHigh (series float) : Pivot High Price

pLow (series float) : Pivot Low Price

indicators (Indicator ) : Array of Indicators - allows to add multiple

Pivot

Pivot refers to zigzag pivot. Each pivot can contain various data

Fields:

point (chart.point) : pivot point coordinates

dir (series int) : direction of the pivot. Valid values are 1, -1, 2, -2

level (series int) : is used for multi level zigzags. For single level, it will always be 0

componentIndex (series int) : is the lower level zigzag array index for given pivot. Used only in multi level Zigzag Pivots

subComponents (series int) : is the number of sub waves per each zigzag wave. Only applicable for multi level zigzags

microComponents (series int) : is the number of base zigzag components in a zigzag wave

ratio (series float) : Price Ratio based on previous two pivots

sizeRatio (series float)

subPivots (Pivot )

indicatorNames (string ) : Names of the indicators applied on zigzag

indicatorValues (float ) : Values of the indicators applied on zigzag

indicatorRatios (float ) : Ratios of the indicators applied on zigzag based on previous 2 pivots

ZigzagFlags

Flags required for drawing zigzag. Only used internally in zigzag calculation. Should not set the values explicitly

Fields:

newPivot (series bool) : true if the calculation resulted in new pivot

doublePivot (series bool) : true if the calculation resulted in two pivots on same bar

updateLastPivot (series bool) : true if new pivot calculated replaces the old one.

Zigzag

Zigzag object which contains whole zigzag calculation parameters and pivots

Fields:

length (series int) : Zigzag length. Default value is 5

numberOfPivots (series int) : max number of pivots to hold in the calculation. Default value is 20

offset (series int) : Bar offset to be considered for calculation of zigzag. Default is 0 - which means calculation is done based on the latest bar.

level (series int) : Zigzag calculation level - used in multi level recursive zigzags

zigzagPivots (Pivot ) : array which holds the last n pivots calculated.

flags (ZigzagFlags) : ZigzagFlags object which is required for continuous drawing of zigzag lines.

ZigzagObject

Zigzag Drawing Object

Fields:

zigzagLine (series line) : Line joining two pivots

zigzagLabel (series label) : Label which can be used for drawing the values, ratios, directions etc.

ZigzagProperties

Object which holds properties of zigzag drawing. To be used along with ZigzagDrawing

Fields:

lineColor (series color) : Zigzag line color. Default is color.blue

lineWidth (series int) : Zigzag line width. Default is 1

lineStyle (series string) : Zigzag line style. Default is line.style_solid.

showLabel (series bool) : If set, the drawing will show labels on each pivot. Default is false

textColor (series color) : Text color of the labels. Only applicable if showLabel is set to true.

maxObjects (series int) : Max number of zigzag lines to display. Default is 300

xloc (series string) : Time/Bar reference to be used for zigzag drawing. Default is Time - xloc.bar_time.

ZigzagDrawing

Object which holds complete zigzag drawing objects and properties.

Fields:

zigzag (Zigzag) : Zigzag object which holds the calculations.

properties (ZigzagProperties) : ZigzagProperties object which is used for setting the display styles of zigzag

drawings (ZigzagObject ) : array which contains lines and labels of zigzag drawing.

Goertzel Cycle Composite Wave [Loxx]As the financial markets become increasingly complex and data-driven, traders and analysts must leverage powerful tools to gain insights and make informed decisions. One such tool is the Goertzel Cycle Composite Wave indicator, a sophisticated technical analysis indicator that helps identify cyclical patterns in financial data. This powerful tool is capable of detecting cyclical patterns in financial data, helping traders to make better predictions and optimize their trading strategies. With its unique combination of mathematical algorithms and advanced charting capabilities, this indicator has the potential to revolutionize the way we approach financial modeling and trading.

*** To decrease the load time of this indicator, only XX many bars back will render to the chart. You can control this value with the setting "Number of Bars to Render". This doesn't have anything to do with repainting or the indicator being endpointed***

█ Brief Overview of the Goertzel Cycle Composite Wave

The Goertzel Cycle Composite Wave is a sophisticated technical analysis tool that utilizes the Goertzel algorithm to analyze and visualize cyclical components within a financial time series. By identifying these cycles and their characteristics, the indicator aims to provide valuable insights into the market's underlying price movements, which could potentially be used for making informed trading decisions.

The Goertzel Cycle Composite Wave is considered a non-repainting and endpointed indicator. This means that once a value has been calculated for a specific bar, that value will not change in subsequent bars, and the indicator is designed to have a clear start and end point. This is an important characteristic for indicators used in technical analysis, as it allows traders to make informed decisions based on historical data without the risk of hindsight bias or future changes in the indicator's values. This means traders can use this indicator trading purposes.

The repainting version of this indicator with forecasting, cycle selection/elimination options, and data output table can be found here:

Goertzel Browser

The primary purpose of this indicator is to:

1. Detect and analyze the dominant cycles present in the price data.

2. Reconstruct and visualize the composite wave based on the detected cycles.

To achieve this, the indicator performs several tasks:

1. Detrending the price data: The indicator preprocesses the price data using various detrending techniques, such as Hodrick-Prescott filters, zero-lag moving averages, and linear regression, to remove the underlying trend and focus on the cyclical components.

2. Applying the Goertzel algorithm: The indicator applies the Goertzel algorithm to the detrended price data, identifying the dominant cycles and their characteristics, such as amplitude, phase, and cycle strength.

3. Constructing the composite wave: The indicator reconstructs the composite wave by combining the detected cycles, either by using a user-defined list of cycles or by selecting the top N cycles based on their amplitude or cycle strength.

4. Visualizing the composite wave: The indicator plots the composite wave, using solid lines for the cycles. The color of the lines indicates whether the wave is increasing or decreasing.

This indicator is a powerful tool that employs the Goertzel algorithm to analyze and visualize the cyclical components within a financial time series. By providing insights into the underlying price movements, the indicator aims to assist traders in making more informed decisions.

█ What is the Goertzel Algorithm?

The Goertzel algorithm, named after Gerald Goertzel, is a digital signal processing technique that is used to efficiently compute individual terms of the Discrete Fourier Transform (DFT). It was first introduced in 1958, and since then, it has found various applications in the fields of engineering, mathematics, and physics.

The Goertzel algorithm is primarily used to detect specific frequency components within a digital signal, making it particularly useful in applications where only a few frequency components are of interest. The algorithm is computationally efficient, as it requires fewer calculations than the Fast Fourier Transform (FFT) when detecting a small number of frequency components. This efficiency makes the Goertzel algorithm a popular choice in applications such as:

1. Telecommunications: The Goertzel algorithm is used for decoding Dual-Tone Multi-Frequency (DTMF) signals, which are the tones generated when pressing buttons on a telephone keypad. By identifying specific frequency components, the algorithm can accurately determine which button has been pressed.

2. Audio processing: The algorithm can be used to detect specific pitches or harmonics in an audio signal, making it useful in applications like pitch detection and tuning musical instruments.

3. Vibration analysis: In the field of mechanical engineering, the Goertzel algorithm can be applied to analyze vibrations in rotating machinery, helping to identify faulty components or signs of wear.

4. Power system analysis: The algorithm can be used to measure harmonic content in power systems, allowing engineers to assess power quality and detect potential issues.

The Goertzel algorithm is used in these applications because it offers several advantages over other methods, such as the FFT:

1. Computational efficiency: The Goertzel algorithm requires fewer calculations when detecting a small number of frequency components, making it more computationally efficient than the FFT in these cases.

2. Real-time analysis: The algorithm can be implemented in a streaming fashion, allowing for real-time analysis of signals, which is crucial in applications like telecommunications and audio processing.

3. Memory efficiency: The Goertzel algorithm requires less memory than the FFT, as it only computes the frequency components of interest.

4. Precision: The algorithm is less susceptible to numerical errors compared to the FFT, ensuring more accurate results in applications where precision is essential.

The Goertzel algorithm is an efficient digital signal processing technique that is primarily used to detect specific frequency components within a signal. Its computational efficiency, real-time capabilities, and precision make it an attractive choice for various applications, including telecommunications, audio processing, vibration analysis, and power system analysis. The algorithm has been widely adopted since its introduction in 1958 and continues to be an essential tool in the fields of engineering, mathematics, and physics.

█ Goertzel Algorithm in Quantitative Finance: In-Depth Analysis and Applications

The Goertzel algorithm, initially designed for signal processing in telecommunications, has gained significant traction in the financial industry due to its efficient frequency detection capabilities. In quantitative finance, the Goertzel algorithm has been utilized for uncovering hidden market cycles, developing data-driven trading strategies, and optimizing risk management. This section delves deeper into the applications of the Goertzel algorithm in finance, particularly within the context of quantitative trading and analysis.

Unveiling Hidden Market Cycles:

Market cycles are prevalent in financial markets and arise from various factors, such as economic conditions, investor psychology, and market participant behavior. The Goertzel algorithm's ability to detect and isolate specific frequencies in price data helps trader analysts identify hidden market cycles that may otherwise go unnoticed. By examining the amplitude, phase, and periodicity of each cycle, traders can better understand the underlying market structure and dynamics, enabling them to develop more informed and effective trading strategies.

Developing Quantitative Trading Strategies:

The Goertzel algorithm's versatility allows traders to incorporate its insights into a wide range of trading strategies. By identifying the dominant market cycles in a financial instrument's price data, traders can create data-driven strategies that capitalize on the cyclical nature of markets.

For instance, a trader may develop a mean-reversion strategy that takes advantage of the identified cycles. By establishing positions when the price deviates from the predicted cycle, the trader can profit from the subsequent reversion to the cycle's mean. Similarly, a momentum-based strategy could be designed to exploit the persistence of a dominant cycle by entering positions that align with the cycle's direction.

Enhancing Risk Management:

The Goertzel algorithm plays a vital role in risk management for quantitative strategies. By analyzing the cyclical components of a financial instrument's price data, traders can gain insights into the potential risks associated with their trading strategies.

By monitoring the amplitude and phase of dominant cycles, a trader can detect changes in market dynamics that may pose risks to their positions. For example, a sudden increase in amplitude may indicate heightened volatility, prompting the trader to adjust position sizing or employ hedging techniques to protect their portfolio. Additionally, changes in phase alignment could signal a potential shift in market sentiment, necessitating adjustments to the trading strategy.

Expanding Quantitative Toolkits:

Traders can augment the Goertzel algorithm's insights by combining it with other quantitative techniques, creating a more comprehensive and sophisticated analysis framework. For example, machine learning algorithms, such as neural networks or support vector machines, could be trained on features extracted from the Goertzel algorithm to predict future price movements more accurately.

Furthermore, the Goertzel algorithm can be integrated with other technical analysis tools, such as moving averages or oscillators, to enhance their effectiveness. By applying these tools to the identified cycles, traders can generate more robust and reliable trading signals.

The Goertzel algorithm offers invaluable benefits to quantitative finance practitioners by uncovering hidden market cycles, aiding in the development of data-driven trading strategies, and improving risk management. By leveraging the insights provided by the Goertzel algorithm and integrating it with other quantitative techniques, traders can gain a deeper understanding of market dynamics and devise more effective trading strategies.

█ Indicator Inputs

src: This is the source data for the analysis, typically the closing price of the financial instrument.

detrendornot: This input determines the method used for detrending the source data. Detrending is the process of removing the underlying trend from the data to focus on the cyclical components.

The available options are:

hpsmthdt: Detrend using Hodrick-Prescott filter centered moving average.

zlagsmthdt: Detrend using zero-lag moving average centered moving average.

logZlagRegression: Detrend using logarithmic zero-lag linear regression.

hpsmth: Detrend using Hodrick-Prescott filter.

zlagsmth: Detrend using zero-lag moving average.

DT_HPper1 and DT_HPper2: These inputs define the period range for the Hodrick-Prescott filter centered moving average when detrendornot is set to hpsmthdt.

DT_ZLper1 and DT_ZLper2: These inputs define the period range for the zero-lag moving average centered moving average when detrendornot is set to zlagsmthdt.

DT_RegZLsmoothPer: This input defines the period for the zero-lag moving average used in logarithmic zero-lag linear regression when detrendornot is set to logZlagRegression.

HPsmoothPer: This input defines the period for the Hodrick-Prescott filter when detrendornot is set to hpsmth.

ZLMAsmoothPer: This input defines the period for the zero-lag moving average when detrendornot is set to zlagsmth.

MaxPer: This input sets the maximum period for the Goertzel algorithm to search for cycles.

squaredAmp: This boolean input determines whether the amplitude should be squared in the Goertzel algorithm.

useAddition: This boolean input determines whether the Goertzel algorithm should use addition for combining the cycles.

useCosine: This boolean input determines whether the Goertzel algorithm should use cosine waves instead of sine waves.

UseCycleStrength: This boolean input determines whether the Goertzel algorithm should compute the cycle strength, which is a normalized measure of the cycle's amplitude.

WindowSizePast: These inputs define the window size for the composite wave.

FilterBartels: This boolean input determines whether Bartel's test should be applied to filter out non-significant cycles.

BartNoCycles: This input sets the number of cycles to be used in Bartel's test.

BartSmoothPer: This input sets the period for the moving average used in Bartel's test.

BartSigLimit: This input sets the significance limit for Bartel's test, below which cycles are considered insignificant.

SortBartels: This boolean input determines whether the cycles should be sorted by their Bartel's test results.

StartAtCycle: This input determines the starting index for selecting the top N cycles when UseCycleList is set to false. This allows you to skip a certain number of cycles from the top before selecting the desired number of cycles.

UseTopCycles: This input sets the number of top cycles to use for constructing the composite wave when UseCycleList is set to false. The cycles are ranked based on their amplitudes or cycle strengths, depending on the UseCycleStrength input.

SubtractNoise: This boolean input determines whether to subtract the noise (remaining cycles) from the composite wave. If set to true, the composite wave will only include the top N cycles specified by UseTopCycles.

█ Exploring Auxiliary Functions

The following functions demonstrate advanced techniques for analyzing financial markets, including zero-lag moving averages, Bartels probability, detrending, and Hodrick-Prescott filtering. This section examines each function in detail, explaining their purpose, methodology, and applications in finance. We will examine how each function contributes to the overall performance and effectiveness of the indicator and how they work together to create a powerful analytical tool.

Zero-Lag Moving Average:

The zero-lag moving average function is designed to minimize the lag typically associated with moving averages. This is achieved through a two-step weighted linear regression process that emphasizes more recent data points. The function calculates a linearly weighted moving average (LWMA) on the input data and then applies another LWMA on the result. By doing this, the function creates a moving average that closely follows the price action, reducing the lag and improving the responsiveness of the indicator.