AllinStrategy v5.0 ::: Allin® MarketEnergy™You need two indicators for it to work: AllinTension 5.0 and AllinStrategy 5.0 and use them in synergy.

They measure and gather information and then present them in an intuitive way for better opportunity spotting and a better and quicker decision making about buy or sell entries in certain markets.

In works with crypto, stock, fiat and futures market.

I will explain how it works o a page but as a thumb rule: the more GREEN you see turning up like an energy the more LONG situation is and the more RED you see turning up like en energy the more SHORT the situation is.

The best thing about a product of mine is that it can be backtested. Results of backtesting yields up to 85% of accuracy and risk-reward ratio up to 5X or more.

Indicator - AllinTension 5.0

This indicator will enable you to actually feel the market on several levels. Exploiting informations from different timeframes and different oscillators with different setting and average them out.

With this indicator you will either confirm the sensed direction or you will skip the opportunity because signals are not properly aligned. To be able to resist FOMO is really crucial here. Opportunities are in abundance. There will be more. A lot more. Really.

How to read it and properly use it?

For more in depth understanding on how it works and proper usage of it. There is lot of information on the page.

Strategy: AllinStrategy 5.0

This strategy indicator is used as a backtesting platform for different types of various settings for a selected pair.

Backtesting means you can test each TimeFrame (best 1-9min) with various AllinTension indicator settings. You will get a result for profitability in the last period (but it is not that important anything but for maybe feeling bad you missed it), success rate in percent (anything above 70% is good enough) and you have to watch the ratio of the max dropdown and average trade size (least acceptable is -5x, better is 2x or less).

So you will learn which strategy (TF and indicator setting) has steadily preformed best while being profitable in the past and assume it will do that in the same manner with same accuracy in the future. It sometimes changes so you need to preform rutine testing after some bigger market movements.

With this you will find the best preforming TImeFrame for each window. You will adjust settings for each window differently to diversify view on the market. My personal best setting are for the first window 4-16-64, second window 3-9-27, third window 2-8-32 and forth last window 5-20-80.

So ALLinStrategy is a visual representation of the market and the most important thing, it includes a feature "Strategy Tester" to backtest chosen strategy. The results may surprise you and they can all be proven!:) So what do you do in this case? :):)

But to really understand the market and given signals from this Strategy, you will need indicator ALLinTension or you are going blindfolded guess trading.

How to read it and properly use it?

For more in depth understanding on how it works and proper usage of it There is lot of information on the page.

For strategy to work you first have to find profitable and accurate enough TF (more than 70% should do the trick)and indicator settings (there are some favourites) and apply it to your executing strategy.

Cari dalam skrip untuk "profit"

QuantCat Mom Finder Strategy (1H)QuantCat Momentum Finder Strategy

This strategy is designed to be used on the 1 hour time frame, on all x/btc pairs.

The beautiful thing is it plots the take profit, and stoploss for you for each entry- where I would say use the stoploss for sure and feel with water with how the price action is looking when in profit.

In this strategy, I actually implemented my own trading style into building the strategy. Having to replicate my own trading strategy into an algorithm, I can't make it exactly perfect to how I would trade, but what I can do is try and program the parameters that give it the absolute best chance of making a big move with a small drawdown- which replicates part of my momentum trading style. Here I am using RSI, MACD, EMA and trend filtering values to find moments where there has been a momentum change to play the rest of the move. It only picks the best entries.

There is always a 3-4 R/R move on average with with these trades, meaning 1 in 4 only need to hit to be a break even trader- where most of these strategies have about 35% hit rate.

The stoploss is so crucial to minimise any damage from huge unexpected candles, the strategies can just be used for entries as well, you don't have to stick to the exact formula- of the long and short system, but this by itself is profitable.

The system nets positive results on

-ETH/BTC

-LTC/BTC

-XRP/BTC

-ADA/BTC

-NEO/BTC etc.

We also have a free 15M strategy available too.

You can join our discord server to get live alerts for the strategy as well as speak to our devs! Link in signature below!!!

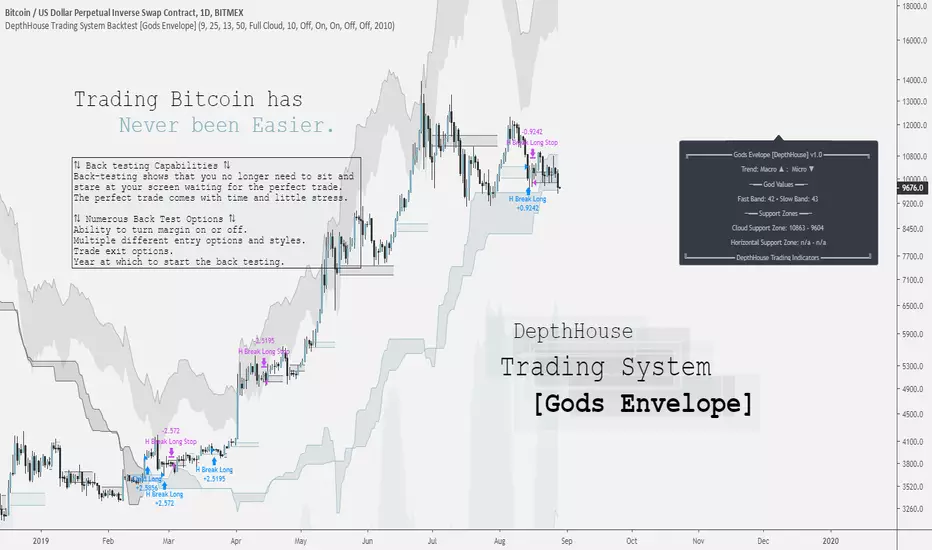

DepthHouse Trading System [Gods Envelope] Backtest StrategyCreated for Bitcoin!

*All testing has been done on the 1 Day time frame of BTC USD pairs.

Use at your own risk.

DepthHouse Trading System Basics

The Cloud:

The cloud is used in a very similar manner as the ichimoku cloud. A complete cross above or below the represents a macro trend change. The cloud then could be used as dynamic support and resistance zones.

By default there is no smoothing to the full cloud. If you wish to add smoothing, you can change the ‘Trend Base On’ option to ‘Modded Cloud Average’ to add price action and smoothing into the cloud’s calculations. The Modded Cloud can then be used in the same manner as the Full Cloud. Generally, the Full Cloud is more forgiving and has less Macro Trend changes. By default, this option is turned off. The support or resistance zone created will be shown on the info panel on the right.

Horizontal Levels:

A Horizonal zone is generated each time there is a micro level trend change. For example, as soon as a positive micro trend change occurs a green horizontal level will be plotted.

These levels then can be used as temporary support and resistance zones. The Horizontal Break Trading Strategy is entirely based on these levels. These levels are also shown on the info panel on the right.

The Envelope Itself: (by default this is off)

By selecting the Overbought and Oversold Ranges option, a cloud envelope will appear around the price action. This envelope represents the overbought and oversold ranges. If the price action should go into these zones, the info panel on the right will show ‘CAUTION’ beside the God Values as this signals that the pair is either overbought or oversold.

The God Values:

The God values are listed on the info panel on the right. These are the values created by the Godmode indicator. Generally, below 20 or above 80 it signals for caution as the price action has overextended itself.

The Back-Test Strategy Options:

⇅ - Child Fomo Positioning:

Child Fomo Positioning strategy is entirely based on the macro trend change with the center cloud. As soon as there is a complete candle close above or below the cloud and a trend change takes place. The back-test places a market order as soon as the next candle opens. By default, it then will not close this position until the price action fully crosses the cloud once again.

⇅ - Horizontal Break Trading:

Horizontal Break Trading Strategy is entirely based on the horizontal levels generated and the macro trend direction. For example, say the Macro Trend is up, and a green, positive horizontal level is formed. As soon as a complete candle closes above the upper level of the positive zone, a limit order is placed in hope that the price action comes back down and retests, filling the order. This long will not close then until a negative level is formed. As soon as a negative level is formed a stop/loss order is placed on the lower level of the horizontal support zone. It will then do the opposite in a bearish trend, and margin trading is turned on.

⇅ - Parent Positions :

Parent Positioning Strategy is based on the overall trend and the center cloud levels. This strategy has limit orders waiting on the level of the cloud that is closest to the price action. Therefore, using this strategy alone, the back-test system waits for the trend to be confirmed, and then follows the price action with limit orders waiting on the cloud to be retested. By default this order does not close until a Marco trend change occurs.

⇅ - Take 50% Partial Profits:

This options allows the back-test to take 50% profit or loss when one of the two options occur.

Horizontal Break: This would close 50% of the position in the same manner it would close a trade using the horizontal break trading system.

God Values: Once the price action enters the oversold or overbought clouds, it would then place a close order as soon as the price action exits the cloud.

⟲ - Backtest Year Start Date :

Start year of the back-testing. If set to ex. 2017, the back-test will not calculate any trades that took place before Jan. 1 of 2017.

⚖ - Margin Trading :

By default, margin trading is turned off. Simply switch this option to on the enable ‘Short Trading’ into the strategy back-test.

Notes: If you are back testing multiple strategies at the same time, you must increase the pyramiding to correspond to the number or strategies.

My Favorite Settings:

Margin = Off

Pyramiding = 2 [Settings → Properties → Pyramiding → 2 orders

Child Fomo Positioning = On

Horizontal Break Trading = On

Everything else off 😊

DISCLAIMER: Past performance does not guarantee future results.

Use at your own risk.

QuantCat 1H Momentum Strategy [Crypto]**NOTE: IF YOU DO NOT OWN TRADINGVIEW PRO YOUR STRATEGIES WILL TAKE DATA FROM A SMALLER SAMPLE SIZE, AND THUS GIVE LESS ACCURATE BACKTESTING RESULTS TO THE ONES WE SHOW (LINKS WITH STEP 3) AND OPTIMISED OUR STRATEGIES WITH**

QuantCat 15M Crypto Trend Strategy

This strategy will allow you to absolutely smash the Crypto/BTC pairs with a high hit rate and incredible risk/reward. We have optimised this strategy to work best for the x/BTC pairs on the 1H minute time frame. There are 7 pairs that we optimised the strategy to work for. There are a few main steps are as follows to use the strategy in it's most efficient manner-

1. Recommended % of equity per trade = 10-50%.

2. 1H Minute time frame needs to be applied (obvious, we know).

3. Pairs we used to optimise and backtest the strategy should ideally be used when using the strategy-

ETH/BTC - prntscr.com

XRP/BTC - prntscr.com

LTC/BTC - prntscr.com

BNB/BTC - prntscr.com

ADA/BTC - prntscr.com

NEO/BTC - prntscr.com

EOS/BTC - prntscr.com

We have a list of Visual and Technical features that are implemented into our strategy to make sure it is easy to use, consistent and giving it the highest chance of being profitable.

Visual Features

Colored Candles- aesthetics to notify you of an alert.

Stop Loss Horizontal Line- a red line to show you where the stop-loss has been placed.

Take Profit Line- horizontal line to show your where you take profits

Technical Features

Trend filtering- Our algorithm prevents signals being created in sideways periods to mitigate the chance of fake outs and larger run ups.

Momentum confirmation- Every time a position is entered; strict conditions have been met to maximize the chance of predicting the right move.

If you have discord alerts access, be sure to watch out in the discord for entries!

CS Buy/Sell Strategy (read the description)Get Buy/Sell signals and check their profitability in the Strategy Tester.

This script has been tested for the crypto space (Bitcoin, Ethereum, etc.) but works for other assets, as well.

I recommend to apply strategy tests on different time-frames (usually daily and 4hr work best) and go with the most profitable ones.

In the settings you have the ability to test the strategy using from - to dates to narrow down best profitable trade periods.

In order to add this strategy to your chart, click on "Add to favorite scripts" and in then, in your chart, go to Indicator and add it from your favorites.

If you have questions, please send me a message.

There is also a Long/Short focused script available with the ability to set alerts (requires an invite). If you want to add it. Just send me a message to get an invite:

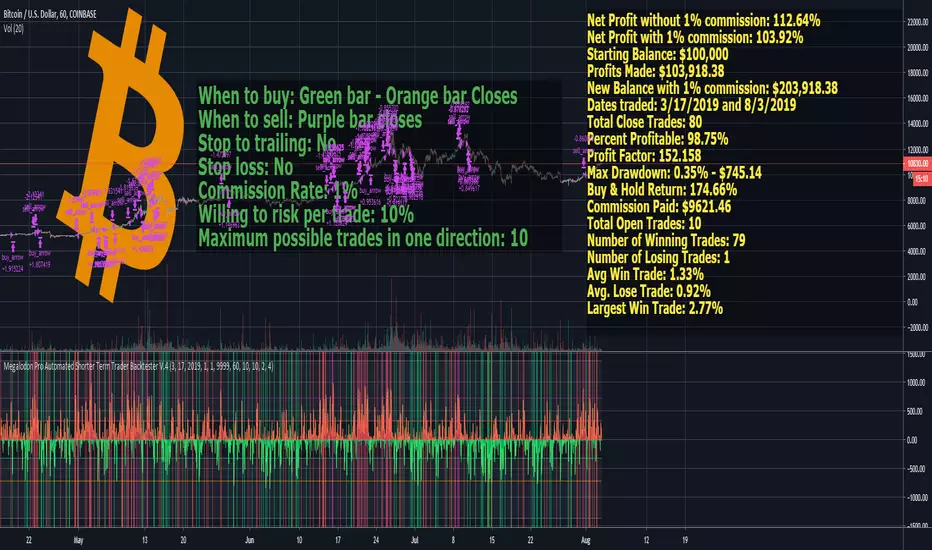

Megalodon Pro Automated Shorter Term Trader BacktesterSTRATEGY

When to buy: Green bar - Orange bar Closes

When to sell: Purple bar closes

Stop to trailing: No

Stop loss: No

Commission Rate: 1%

Willing to risk per trade: 10%

Maximum possible trades in one direction: 10

RESULTS

Net Profit without 1% commission: 112.64%

Net Profit with 1% commission: 103.92%

Starting Balance: $100,000

Profits Made: $103,918.38

New Balance with 1% commission: $203,918.38

Dates traded: 3/17/2019 and 8/3/2019

Total Close Trades: 80

Percent Profitable: 98.75%

Profit Factor: 152.158

Max Drawdown: 0.35% - $745.14

Buy & Hold Return: 174.66%

Commission Paid: $9621.46

Total Open Trades: 10

Number of Winning Trades: 79

Number of Losing Trades: 1

Avg Win Trade: 1.33%

Avg. Lose Trade: 0.92%

Largest Win Trade: 2.77%

Let me know what you guys think about the results?

Due to the tradingview's limitations on providing the shorter time frame price data, we had to provide a 60 minute time frame backtesting results.

The shorter time frames including 1 minute and 15 minutes backtesting results are way more accurate and precise than 60 minutes time frame results.

Megalodon Trading

Enlightening the Modern Investors

TrendMaster Gold, v. 6.2xTrendMaster Gold

The ultimate refinement of last year’s TrendMaster system, TrendMaster Gold takes deep pattern recognition to a new level tracking over 20 indicators triggering seven decision gates to trade in a Renko-smoothed charting environment. Optimized for higher returns over a wider range of instruments (see returns below), you are invited to trial this market-mirroring engine. Subscribers receive full breakdown for fine-tuning results to their market favorites while avoiding bot traps. Reach out by message to get your free trial. We are always available for questions, comments, and suggestions. There’s always room for improvement.

Results Chart

The backtests below show 1-year returns against a Buy and Hold (B+H) approach for 40 of the world’s top traded instruments (as measured by price volume or similar indicator). The TrendMaster system was run on the top 10 instruments in each of four major markets: Equities, ETFs, Cryptocurrencies, and Forex. All tests were on a 30min chart, set to Renko “Traditional” blocks (because TradingView does not support realtime alerts from ATR-based charts). Block size was set proportionately to price to give the instrument positive results, but there was no “cherry-picking”. (In fact, changing time frames would have produced even better returns in some cases, but it seemed best to use a consistent measure.) Subscribers to the system receive a full, step-by-step breakdown on how to customize the parameters to get the best from their favorite markets.

(For each instrument, you see listed its Symbol (name), Profit % (annual return using TrendMaster Gold), Winning Trade % (being “right”), ProfitFactor (Ratio of money won to money lost), Max Draw Down % (point of worst % loss during the year), and B+H (how much the asset would have returned with no trades, via "buy-and-hold" )...)

TrendMaster Gold

Settings: 30 min, Traditional Renko box, over 1 year (June 1, 2018 - June 1, 2019)

EQUITIES

Symbol Profit % Trade % PF Max DrDn B + H

AMZN 2,212 62 6.6 3 7

AAPL 158 49 3.7 5 5

TSLA 8,263 57 5 6 -38

FB 179 47 3 8 -7

BABA 247 56 3.4 9 -23

BYND 348 67 17.9 6 140

MSFT 224 58 6.8 3 28

AMD 171 50 2.6 13 0

NFLX 2,132 55 5.2 11 -5

BA 560 54 4.9 3 97

ETFs

Symbol Profit % Trade % PF Max DrDn B + H

SPY 275 64 5.5 3 4

QQQ 865 62 6.1 3 5

EEM 278 60 5.3 2 0

IWM 783 61 6.1 2 -3

HYG 21 51 2.7 1 0.5

EWZ 798 58 5.6 5 26

LQD 12 54 2 1 6

EFA 121 61 4.5 2 -7

FXI 391 63 5.4 3 -15

XLF 200 58 3.4 5 -3

CRYPTOCURRENCIES

Symbol Profit % Trade % PF Max DrDn B + H

BTC/USD 3 million 55 4.7 8 -8

ETH/USD 2 million 52 4.9 21 -54

XRP/USD 6 million 52 4 13 -16.6

LTC/USD 222,000 54 3 13 13

BCH/USD 380,000 54 4.6 28 -5

EOS/USD 147,000 55 2.7 20 13

BNB/USDT 2 million 54 4.4 14 143

BSV/USD 334,000 65 18 5 -8

XLM/USD 34 million 51 2.8 12 34

ADA/USD 48,000 64 7 6 3

FOREX PAIRS

Symbol Profit % Trade % PF Max DrDn B + H

EUR/USD 13 41 1.3 5 -4

USD/JPY 3 37 1.1 4 -1

AUD/USD 24 43 1.4 4 10

USD/CAD 20 43 1.7 4 3

GBP/USD 36 46 1.8 2 -5

NZD/USD 21 47 1.6 2 -6

GBP/JPY 40 42 1.6 2 -6

EUR/JPY 18 54 3.2 2 -5

AUD/JPY 47 44 1.8 5 -10

EUR/GBP 17 46 1.7 4 0.1

[astropark - Premium] Long-Short V3-FOREX [Strategy]This indicator is not holy grail , but it is an amazing trend finder and works nicely between 3m and 1W timeframes on FOREX :)))

With this indicator you can enjoy its trading signal and backtest the strategy.

In order to check how much you could have been profitable with this script if you started trading from a specific timestamp, please use this nice website to get the integer number representing in seconds the date-time you want to start from: www.unixtimestamp.com

If you want to set alerts on both buy, sell, take profit and stop-loss signals you must use the following not-strategy indicator version:

HOW TO USE THIS INDICATOR

Buy/Long when you see a green "B" label on the chart at best price you can, you have time till next candle's open price , trying to buy as low as possible near the green cloud or below it. Green cloud acts like a moving support for price, so use it for more buys/longs. The bigger the cloud, the stronger the bull-trend and so the support.

Sell/Short when you see a red "S" label on the chart at best price you can, you have time till next candle's open price , trying to sell as high as possible near the red cloud or over it. Red cloud acts like a moving resistance for price, so use it for more sells/shorts. The bigger the cloud, the stronger the bear-trend and so the resistance.

This indicator suggests some TP (Take Profit) for both longs (in green color) and shorts (in red color): you can start (at least partially!) closing the current trade (eventually you start new longs/shorts at cloud touch if you are a bold trader!).

Keep in mind that the lower the timeframe you work on, the easier is the trend to change rapidly, so always set a -2% / -5% stop-loss on trades and follow the trend with a nice trailing stop strategy.

Of course, as said at the beginning, this indicator suggests some TPs (Take Profits) for both longs (in green color) and shorts (in red color) operations: when you see a TP, you can start (at least partially!) taking profits over the current trade and move stop-loss higher (at least at break-even).

This is a premium indicator , so send me a private message in order to get access to this script.

Do you like my free scripts? Offer me a coffee, a beer, a pizza or whatever :)

BTC jar: 1K5kuYQPEqoNo6GRmJbHWMPmqwKM5S3oRR

ETH jar: 0x091b541a6dd6fe08c4e7bd909baafb2fce9b975e

LTC jar: LSVoAChsZrVsvbNyUfdpxtFpDAUSaUTUig

XRP jar: (XRP deposit tag) 103997763 (XRP deposit address) rEb8TK3gBgk5auZkwc6sHnwrGVJH8DuaLh

PS: Do you need a customization or do you need a dev who implements your strategy? send me a private message ;-)

[astropark - Premium] Long-Short Strategy V3This indicator is not holy grail , but it is an amazing trend finder and works nicely between 3m and 1W timeframes :)))

With this indicator you can enjoy its trading signal and backtest the strategy.

In order to check how much you could have been profitable with this script if you started trading from a specific timestamp, please use this nice website to get the integer number representing in seconds the date-time you want to start from: www.unixtimestamp.com

If you want to set alerts on both buy, sell, take profit and stop-loss signals you must use this not-strategy indicator version

HOW TO USE THIS INDICATOR

Buy/Long when you see a green "B" label on the chart at best price you can, you have time till next candle's open price , trying to buy as low as possible near the green cloud or below it. Green cloud acts like a moving support for price, so use it for more buys/longs. The bigger the cloud, the stronger the bull-trend and so the support.

Sell/Short when you see a red "S" label on the chart at best price you can, you have time till next candle's open price , trying to sell as high as possible near the red cloud or over it. Red cloud acts like a moving resistance for price, so use it for more sells/shorts. The bigger the cloud, the stronger the bear-trend and so the resistance.

This indicator suggests some TP (Take Profit) for both longs (in green color) and shorts (in red color): you can start (at least partially!) closing the current trade (eventually you start new longs/shorts at cloud touch if you are a bold trader!).

Keep in mind that the lower the timeframe you work on, the easier is the trend to change rapidly, so always set a -2% / -5% stop-loss on trades and follow the trend with a nice trailing stop strategy.

Of course, as said at the beginning, this indicator suggests some TPs (Take Profits) for both longs (in green color) and shorts (in red color) operations: when you see a TP, you can start (at least partially!) taking profits over the current trade and move stop-loss higher (at least at break-even).

This is a premium indicator , so send me a private message in order to get access to this script.

Do you like my free scripts? Offer me a coffee, a beer, a pizza or whatever :)

BTC jar: 1K5kuYQPEqoNo6GRmJbHWMPmqwKM5S3oRR

ETH jar: 0x091b541a6dd6fe08c4e7bd909baafb2fce9b975e

LTC jar: LSVoAChsZrVsvbNyUfdpxtFpDAUSaUTUig

XRP jar: (XRP deposit tag) 103997763 (XRP deposit address) rEb8TK3gBgk5auZkwc6sHnwrGVJH8DuaLh

PS: Do you need a customization or do you need a dev who implements your strategy? send me a private message ;-)

Buy The Dip - Does It Work?Buying the dip has become a meme in crypto, but does it actually work?

Using this script you can find out.

The dip is defined here as the average true range multiplied by a number of your choosing (dipness input) and subtracted from the low.

When price crosses under the dip level, a long is initiated. The long is then closed using a timestop (default value 20 bars), no fancy exits here.

A general rule for buying the dip should be to be more passive in a bull market and aggressive in a bear market.

Same goes for all counter trend trading.

Heres a few other examples of dip buying statistics using the H4 timeframe:

50% profitable, 1.692 Profit Factor

BINANCE:PIVXBTC

56.52% profitable, 1.254 Profit Factor

BINANCE:KMDBTC

27.27% Profitable, 0.257 Profit Factor... yikes!

BINANCE:BTSBTC

73.33% Profitable, 13.627 Profit Factor... o.O

BINANCE:MANABTC

-- Ultimate Crypto Trading Strategy -- Backtesting version** This is the backtesting (strategy) version of the ~ Ultimate Crypto Trading Strategy ~ script in TradingView. **

~ Ultimate Crypto Trading Strategy ~

֎ Trading system script on @tradingview that brings the easiest approach to trading with a high profitability rate

֎ Optimized for crypto markets, to catch trend movements as soon as possible and maximize profitability

֎ Sell & Buy alerts, Safeguard mode, Take Profits alerts, auto resistance-support and always adding new features!

֎ Customizable settings.

֎ Users Discord community for learning, sharing and direct support

֎ Ultimate Crypto Trading Strategy Tutorial Video: www.youtube.com www.youtube.com

֎ Safeguard feature (match multiple timeframes signals) explained: youtu.be youtu.be

If you’d like to test the trading script in TradingView, I can give you access to a 10 days trial.

Please send me a message in tradingview and I’ll activate it right away.

Thank you!

Megalodon Pro Automated Trader BackTester

Why Megalodon?

We believe that enlightening others is an incredible way to make this world a better place. That's why we created the tools you need to stop worrying about your investments and focus on what really matters in your life.

What is Megalodon?

Megalodon uses Artificial Intelligence that combines 574 back-tested indicators and 2674 back-tested setups, simultaneously.

Megalodon works with any kind of asset , market state and time frame .

What is the win rate?

Megalodon is extremely accurate and offers insane profits as long as the fundamental analysis is done right .

Backtesting results can be found on our social media or down below .

How to use Megalodon Pro Automated Trader?

Simply, orange rectangles are buy signals and purple rectangles are sell signals .

Green clouds show buy signals and red clouds show sell signals.

Yellow line shows the difference between buy and sell counts.

How to set alarms on Megalodon Pro Automated Trader?

Click on Alert, select Megalodon Pro Automated Trader and click on Buy-Signal or Sell-Signal. More details can be found on our social media.

You may also watch our Megalodon Investing Tutorials on Youtube for more information.

How to purchase?

Megalodon is totally FREE .

You may upgrade to Megalodon Pro for the most important features , including automizing your trading on any asset profitably, setting up alarms to get notified , joining to our VIP telegram channel to get daily updates and our VIP telegram group to interact with the community. Simply go to our website on our TradingView page for learning more and joining us for free.

Some of the backtesting results are:

BTC/USD for longer time frame trading in the bear market for the last year.

APPLE for longer time frame trading in the bull market for the last 10 years.

EURO/USD for day trading in the neutral market for the last month.

BTC/USD for day trading in the bull market for the last 15 days.

APPLE for day trading in the neutral market for the last 2 days and 6 hours.

Stochastic & MACD Strategy Ver 1.0This strategy is inspired by ChartArt and jasonluk28.

The following input changes from the initial ChartArt version to achieve higher stability and profit:

Fast MA Len:11

Slow MA len: 24

Stoch Len: 20

No difference is found in minor changes (+-10) lv. of overbought/oversold

It works above 40% winning rate in Heng Heng Index, Shanghai Composite, Dow Jones Industrial Averge, S&P 500 NASDAQ, VT (World Total Market) and in 15 mins chart

Profit: above ~10 to 30% in less than 1year backtest for most major indice of China and US and ~62% in Heng Seng Index (Hong Kong) & 40.5% in SZSE Composite (Shen Zhen)

P.S. Profit: 700 (Tencent) +150.5%, 939 (CCB) +66.5%, 1299 (AIA) +45%, 2628 (CLIC) +41%, 1 (CK Hutchison) +31%

NFLX +82.5%, BABA +55.5%, AMZN +44%, GOOG +38%, MCD +24.5%

However, Loss in FB -19% , AMD -38.5%

Not suitable for stocks with great influences in News or Events ???

TEMA Strategy 1 (Updated)This is just a test strategy using TEMA ( Triple Exponential Moving Average ).

Test Detail

Symbol: BTCUSD

Interval: 1H

Initial Capital: $1000

Investment: 100% Equity

Results (on BTCUSD -2.31% - Bitfinex)

I had to chunk the months because of the order limit (1000)

(all months start at 1st, 00:00 AND finish at last date, 23:59 )

Timeframe: 2017 August - 2017 Nov

Profit: 21.9%

Max Drawdown: 83.94%

Timeframe: 2017 Dec - 2018 Feb

Profit: 446.32%

Max Drawdown: 46.54%

Timeframe: 2018 Mar - 2018 Jul

Profit: 288.87%

Max Drawdown: 51.49%

To fix:

Too many orders, potentially reduce order counts by increasing max loss (100~200 orders/month) \u2028

High Max Drawdown, need to fix that

Looks like orders are created and terminated very quickly, need to look into that

Still figuring things out

PPSignal MTFSystem Algorithm Ppsignal Versin MTF. based on historical price probabilities . We recommend use financial stock, bond, crypts, indices, futures and Forex market ( GBPUSD -0.09% , EURUSD -0.02% , USDJPY 0.28% , USDCAD 0.09% , AUDUSD -0.02% , USOIL -0.05% , XAUUSD -0.06% , SOYUSD -1.22% , DXY 0.07% , SPY 0.12% , SP1! 0.40% , bitcoin -0.02% ) with defined trends above 50 or 100 and 200 simple moving averages idem if you want trade downtrend financial assets.

Use projections and retracements Fibonacci, MACD and RSI or Stoch oscillator and figures charters Head and shoulder, triangles and double bottom , double top , etc.

This system will notify you of the probability of success. The profit will be defined for yourself and according to your investor profile.

There are stocks and other assets with high returns but the system does not know exactly. Check in the Strategy tester section and then net profit.

We have other tools that support to PPsignal system, we will publish them shortly.

Define system parameters

As it is a system that is based on past data we recommend using the most historical data weekly (W) but you an use day historical data or 3 o 2 hs.

Candle color: you can choose if you want a trend color for candles or not, in the chart propieties menu detach the border option.

PPsignal it's a very simple system with which you will have a great support when it is a good time for enter in the marker and out.

we await your comments.

With this new version you can change the period and time and find a better percent profitable.

Eng. Oscar Alejandro Peruchena

Quants Mathematical and Market Analyst

RSI Buy/sell signal with TP_SL_TL_15min by rajistaRSI Buy/sell signal with TakeProfit_Stop loss_Trailing_SL script -can be used on any altcoin/btc pair on the 15min chart .

This script can be used for backtesting pupose and also to give buy/sell signals based on the settings provided by you.

Benefits of the script:

1> Fully customizable script according to your trade setups.

2> The script incorporates Take-profit, Stop-loss & Trailing SL.

3> Cuts your losses significantly, in comparision to a script without TP, SL & TL strategies.

4> Based on RSI Overbought/Oversold levels, which can also be customizable.

5> Doesn't take too many trades in a day, thereby decreasing commission paid to exchanges & hence enhances the overall profit.

Here's how, you can fully customize the script, according to your strategy, once you have been provided access:

( To gain access to the script just hit the like/comment in the #tradingview published article & i'll grant access based on your tradingview userid )

You can add this script to your charts in 15min timeframe, like adding any other simple indicator.

Once you have added the script, just hit the settings button to fully customize the script according to your strategy and plan, that you have, for your trade setup.

Take profit, Stop loss, Trailing Stop loss values can be entered in satoshis from the setting panel.

RSI Overbought & Oversold values can also be entered according to your trading setup.

Like in below example , i have put the following values as default

Test date is set as 1 May 2018

Take profit=1000, stop loss=5, Trailing SL=40

RSI Overbought=70, Oversold=20

" Above mentioned values are default values and may not be profitable in every condition, you have to backtest the strategy by changing these values and then see the results of given values under the Strategy tester tab- located at bottom of your #tradingview chart. "

Lets see how the scipt is able to make these awesome gains:

Suppose your script enters a trade(buys Verge) when #Verge is at 800sats

Then the bot will close the trade(sell Verge) when either of these things happen:

a> Verge surges to 1800 sats, then the script will close trade by Taking profit

b>Verge increases to 850 only, but the RSI value in 15min chart has gone above 70 (Overbought-default value) then scipt will close trade.

c>Verge decreases to 995 sats, then script will close trade by Stop loss hit.

d>Verge surges to 840 but then again drops slightly to 835, script will again close trade by Trailing SL hit.

Initial capital is set to 10 btc

Make sure to check the performance summary tab below and overview of the script running on #XVGBTC since 1 May 2018-Till date

Profit -11.6% while running script

Where Buy and hold return for verge in the same period is:

- to get an instant notification, once i publish a script or a trading analysis/trade-setup , which will always be available for free for everyone!!!

Can you cheat a back test? Things to look out for...I have seen a lot of people selling strategies for large amounts of money. But please be careful. In this I am going to show a strategy that says it makes 9 trillion % profit and is 100% of the time profitable.

If someone was trying to sell you this, alarm bells should be ringing. I have managed to get very good results without cheating, as you can see in all our other strategies where the figures you see are real.

How to cheat a back test

You can not really cheat it, but if you play around with the figures you can drastically improve the results.

First you need to get a good strategy with over 95% time profitable and a good net profit (this is the hard part)

Then simply click on the gear icon of that strategy, go to the property tab, set initial capital to 1000 and increase the order size to 10000000000000000.

Its that simple

Most strategies work on either 1000 or 10,000 initial capital. Its the order size that should be 1 to get more realistic results.

All our other strategies use 1000 for initial capital and 1 for order size.

Please note when back testing you should always enter the commission of that exchange, I like to use 0.3%.

Hope this helps, please let me know your thoughts.

If you would like to be kept up to date please FOLLOW us and try our indicators and strategies here: uk.tradingview.com

If you like it please click the LIKE button.

XPloRR MA-Buy ATR-Trailing-Stop Long Term Strategy Beating B&HXPloRR MA-Buy ATR-MA-Trailing-Stop Strategy

Long term MA Trailing Stop strategy to beat Buy&Hold strategy

None of the strategies that I tested can beat the long term Buy&Hold strategy. That's the reason why I wrote this strategy.

Purpose: beat Buy&Hold strategy with around 10 trades. 100% capitalize sold trade into new trade.

My buy strategy is triggered by the EMA(blue) crossing over the SMA curve(orange).

My sell strategy is triggered by another EMA(lime) of the close value crossing the trailing stop(green) value.

The trailing stop value(green) is set to a multiple of the ATR(15) value.

ATR(15) is the SMA(15) value of the difference between high and low values.

Every stock has it's own "DNA", so first thing to do is find the right parameters to get the best strategy values voor EMA, SMA and Trailing Stop.

Then keep using these parameter for future buy/sell signals only for that particular stock.

Do the same for other stocks.

Here are the parameters:

Exponential MA: buy trigger when crossing over the SMA value (use values between 11-50)

Simple MA: buy trigger when EMA crosses over the SMA value (use values between 20 and 200)

Stop EMA: sell trigger when Stop EMA of close value crosses under the trailing stop value (use values between 8 and 16)

Trailing Stop #ATR: defines the trailing stop value as a multiple of the ATR(15) value

Example parameters for different stocks (Start capital: 1000, Order=100% of equity, Period 1/1/2005 to now):

BAR(Barco): EMA=11, SMA=82, StopEMA=12, Stop#ATR=9

Buy&HoldProfit: 45.82%, NetProfit: 294.7%, #Trades:8, %Profit:62.5%, ProfitFactor: 12.539

AAPL(Apple): EMA=12, SMA=45, StopEMA=12, Stop#ATR=6

Buy&HoldProfit: 2925.86%, NetProfit: 4035.92%, #Trades:10, %Profit:60%, ProfitFactor: 6.36

BEKB(Bekaert): EMA=12, SMA=42, StopEMA=12, Stop#ATR=7

Buy&HoldProfit: 81.11%, NetProfit: 521.37%, #Trades:10, %Profit:60%, ProfitFactor: 2.617

SOLB(Solvay): EMA=12, SMA=63, StopEMA=11, Stop#ATR=8

Buy&HoldProfit: 43.61%, NetProfit: 151.4%, #Trades:8, %Profit:75%, ProfitFactor: 3.794

PHIA(Philips): EMA=11, SMA=80, StopEMA=8, Stop#ATR=10

Buy&HoldProfit: 56.79%, NetProfit: 198.46%, #Trades:6, %Profit:83.33%, ProfitFactor: 23.07

I am very curious to see the parameters for your stocks and please make suggestions to improve this strategy.

Aurum15 - http://tvautotrader.comAurum15 - tvautotrader.com

Initial version of strategy, basing on market condition and price movement according to MA's, closing on RSI overbought value.

Exit position are configurable by RSI (default rsi(open,29) > 70), designed for 15 minutes charts

It creates very long trades (above 300 bars per trade) but is very profitable.

Tested at:

USOIL - 66% profitable, 15 trades since 2017-09-04

LTCUSD - 75% profitable, 20 trades since 2017-10-02

XRPUSD - 87.5% profitable, 8 trades since 2017-10-02

IOTUSD - 77% profitable, 9 trades since 2017-10-02

This strat is not for sale yet, I need to make futher tests in more sideways market.

Upgraded XAUUSD 30m only Strategy V2.0So i've been fiddling around with this once more

The result is increased net profit, same time frame as previous strategy, more drawdown, but that comes with the net profit.

1 pip = 1$

Pyramiding of 3 orders.

Commission included.

More trades

Profitability rate is about the same.

MACDouble + RSI (rec. 15min-2hr intrv) Uses two sets of MACD plus an RSI to either long or short. All three indicators trigger buy/sell as one (ie it's not 'IF MACD1 OR MACD2 OR RSI > 1 = buy", its more like "IF 1 AND 2 AND RSI=buy", all 3 match required for trigger)

The MACD inputs should be tweaked depending on timeframe and what you are trading. If you are doing 1, 3, 5 min or real frequent trading then 21/44/20 and 32/66/29 or other high value MACDs should be considered. If you are doing longer intervals like 2, 3, 4hr then consider 9/19/9 and 21/44/20 for MACDs (experiment! I picked these example #s randomly).

Ideal usage for the MACD sets is to have MACD2 inputs at around 1.5x, 2x, or 3x MACD1's inputs.

Other settings to consider: try having fastlength1=macdlength1 and then (fastlength2 = macdlength2 - 2). Like 10/26/10 and 23/48/20. This seems to increase net profit since it is more likely to trigger before major price moves, but may decrease profitable trade %. Conversely, consider FL1=MCDL1 and FL2 = MCDL2 + (FL2 * 0.5). Example: 10/26/10 and 22/48/30 this can increase profitable trade %, though may cost some net profit.

Feel free to message me with suggestions or questions.

MACD, backtest 2015+ only, cut in half and doubledThis is only a slight modification to the existing "MACD Strategy" strategy plugin!

found the default MACD strategy to be lacking, although impressive for its simplicity. I added "year>2014" to the IF buy/sell conditions so it will only backtest from 2015 and beyond ** .

I also had a problem with the standard MACD trading late, per se. To that end I modified the inputs for fast/slow/signal to double. Example: my defaults are 10, 21, 10 so I put 20, 42, 20 in. This has the effect of making a 30min interval the same as 1 hour at 10,21,10. So if you want to backtest at 4hr, you would set your time interval to 2hr on the main chart. This is a handy way to make shorter time periods more useful even regardless of strategy/testing, since you can view 15min with alot less noise but a better response.

Used on BTCCNY OKcoin, with the chart set at 45 min (so really 90min in the strategy) this gave me a percent profitable of 42% and a profit factor of 1.998 on 189 trades.

Personally, I like to set the length/signals to 30,63,30. Meaning you need to triple the time, it allows for much better use of shorter time periods and the backtests are remarkably profitable. (i.e. 15min chart view = 45min on script, 30min= 1.5hr on script)

** If you want more specific time periods you need to try plugging in different bar values: replace "year" with "n" and "2014" with "5500". The bars are based on unix time I believe so you will need to play around with the number for n, with n being the numbers of bars.

Outsidebar vs Insidebar, Illusion Strategy (by ChartArt)WARNING: This strategy does not work! Please don't trade with this strategy

I'm sharing this strategy for the following three educational reasons:

1. You can easily find 100% strategies, but if they only seem to work 100% on one asset, they actually don't work at all. Therefore never backtest your strategy only on one asset, especially forward testing is useless, because it tends to repeat the old patterns. Your strategy has to work on as many different assets as possible.

2. The pyramiding of orders can have an impact on the strategy. In this case if you manually change the strategy settings by increasing it from 1 to 100 pyramiding orders changes the percent profitable on "UKOIL" monthly from 100% to 90% profitable. On other assets you can see very different results. Allowing much more pyramiding orders in this case results in opening orders where the background color highlights appear.

3. The Tradingview backtest beta version currently does not close the last open trade during the backtest. In this case going long on "UKOIL" near the top in 2011 as this strategy did would result in a big loss in 2015. But since the trade is still open and not canceled out by a new short order it still appears as if this strategy works 100% profitable. Which it doesn't.