New Age US ORB═════════════════════════════════════════════════════════════

NEW AGE US ORB

Opening Range Breakout Strategy with Neon Glow Effect

═════════════════════════════════════════════════════════════

🔒 INVITE-ONLY ACCESS

This script requires an invitation to use.

To request access, please send me a private message.

═════════════════════════════════════════════════════════════

🎯 OVERVIEW

The New Age US ORB is a clean, professional Opening Range Breakout (ORB) strategy with a futuristic visual style featuring dynamic neon glow effects.

Designed for Crypto (BTC/USD) and Indices (US100, US30, SPX) trading.

Best results on 5-minute or 15-minute chart with Regular Candles.

The strategy captures the first 15 minutes of US market activity (9:30-9:45 NY) and trades breakouts in the direction of the initial move.

💎 WHAT MAKES THIS UNIQUE

Unlike standard ORB indicators, this strategy combines:

• Proprietary 3-layer Neon Glow visualization for enhanced box visibility

• Integrated US Session backgrounds for market context

• Smart Session Filter to avoid low-probability late entries

• Separate Long/Short TP management for asymmetric markets

• Automatic EOD position closure for overnight risk control

• Daily trade limiter to prevent overtrading

• Global Timezone Support - works correctly for traders worldwide

This combination of visual design and risk management features is not available in standard ORB scripts.

Trade Smarter, not Harder.

📦 WHAT IS ORB?

The Opening Range Breakout (ORB) strategy is based on the concept that the first 15 minutes of the US market session often sets the tone for the rest of the day. The High and Low established during this period act as key support/resistance levels.

• Price breaks ABOVE ORB High → Bullish momentum (LONG)

• Price breaks BELOW ORB Low → Bearish momentum (SHORT)

⚡ KEY FEATURES

📦 ORB BOX VISUALIZATION

• Automatically captures High/Low of 9:30-9:45 NY candle

• Dynamic color change:

→ Cyan: Price ABOVE ORB High (Bullish)

→ Red: Price BELOW ORB Low (Bearish)

• Extends throughout the trading session

✨ NEON GLOW EFFECT

• 3-layer glow effect around the ORB box

• Layered borders (8px → 5px → 3px) with gradient transparency

• Creates futuristic, high-visibility appearance

• Toggle on/off in settings

🕐 US SESSION BACKGROUNDS

• US Open (9:30-11:30 NY) - Blue

• Lunch Break (11:30-13:30 NY) - Orange

• Afternoon (13:30-16:00 NY) - Green

• Visual reference only - helps identify optimal trading windows

⏱️ SESSION FILTER

• Configurable trading window (default: until 11:50 NY)

• Prevents late entries when momentum fades

• EOD auto-close in YOUR selected timezone (default: 21:45)

🎚️ RISK MANAGEMENT

• ORB Box Stop Loss: SL at opposite ORB level + buffer

• Separate Take Profit settings for Long/Short

• Points or Percentage mode

• Daily trade limit (default: 6 trades max)

📊 INFO DASHBOARD

• Real-time status panel (top right)

• Shows: Timezone, Status, Session, Direction, Trades, SL/TP, EOD, ORB levels

⚙️ SETTINGS

TIMEZONE

└── Your Timezone: Select from 12 global timezones (Default: Europe/Zurich)

Available: UTC, New York, Chicago, Los Angeles, London, Berlin,

Zurich, Paris, Tokyo, Hong Kong, Singapore, Sydney

ORB BOX (9:30-9:45 NY)

├── Show ORB Box: true/false

└── Neon Glow Effect: true/false

US SESSION BACKGROUNDS

├── Show Session Background: true/false

├── US Open Color (9:30-11:30)

├── Lunch Color (11:30-13:30)

└── Afternoon Color (13:30-16:00)

SESSION FILTER

├── Enable Session Filter: true/false

├── Session End Hour (NY): 0-23

└── Session End Minute (NY): 0-59

DAILY CLOSE (Your Timezone)

├── Enable Daily Close: true/false

├── EOD Hour: 0-23

└── EOD Minute: 0-59

TRADE LIMITS

├── Enable Daily Limit: true/false

└── Max Trades per Day: 1-10

STOP LOSS

├── Enable ORB Box SL: true/false

└── SL Buffer: Points distance from ORB level

TAKE PROFIT - LONG

├── Enable TP Long: true/false

├── Mode: Points / Percent

├── TP Long Points: Distance in points

└── TP Long Percent: Distance in %

TAKE PROFIT - SHORT

├── Enable TP Short: true/false

├── Mode: Points / Percent

├── TP Short Points: Distance in points

└── TP Short Percent: Distance in %

COLORS

├── Bullish: Default #00ffbb (Cyan)

└── Bearish: Default #ff1100 (Red)

📈 HOW TO USE

1. Apply to BTC/USD or US100 on 5min or 15min timeframe

2. Use Regular Candles for realistic results

3. Go to Strategy Properties → Enable ☑️ "Recalculate On Bar Close"

4. Select your Timezone in settings (for correct EOD close time)

5. Wait for ORB box to complete (9:45 NY)

6. Strategy enters automatically on breakout:

→ LONG when price closes above ORB High

→ SHORT when price closes below ORB Low

7. Manage risk with ORB Box SL and TP settings

8. All positions close at EOD time (in your timezone)

🔔 ALERTS

• LONG Entry - Breakout above ORB High

• SHORT Entry - Breakout below ORB Low

• EOD Close - End of day position close

💡 BEST PRACTICES

• Most effective during US Open session (9:30-11:30 NY)

• Avoid Lunch session (11:30-13:30) - lower volatility

• ORB levels act as support/resistance all day

• Wider TP for trending days, tighter for ranging markets

• Use session filter to avoid late, low-probability entries

═════════════════════════════════════════════════════════════

© AL_R4D1 - New Age Style Trading Tools

═════════════════════════════════════════════════════════════

Cari dalam skrip untuk "range"

S&D Light+ Enhanced# S&D Light+ Enhanced - Supply & Demand Zone Trading Strategy

## 📊 Overview

**S&D Light+ Enhanced** is an advanced Supply and Demand zone identification and trading strategy that combines institutional order flow concepts with smart money techniques. This strategy automatically identifies high-probability reversal zones based on Break of Structure (BOS), momentum analysis, and first retest principles.

## 🎯 Key Features

### Smart Zone Detection

- **Automatic Supply & Demand Zone Identification** - Detects institutional zones where price is likely to react

- **Multi-Candle Momentum Analysis** - Validates zones with configurable momentum requirements

- **Break of Structure (BOS) Confirmation** - Ensures zones are created only after significant structure breaks

- **Quality Filters** - Minimum zone size and ATR-based filtering to eliminate weak zones

### Advanced Zone Management

- **Customizable Zone Display** - Choose between Geometric or Volume-Weighted midlines

- **First Retest Logic** - Option to trade only the first touch of each zone for higher probability setups

- **Zone Capacity Control** - Maintains a clean chart by limiting stored zones per type

- **Visual Zone Status** - Automatically marks consumed zones with faded midlines

### Risk Management

- **Dynamic Stop Loss** - Positioned beyond zone boundaries with adjustable buffer

- **Risk-Reward Ratio Control** - Customizable R:R for consistent risk management

- **Entry Spacing** - Minimum bars between signals prevents overtrading

- **Position Sizing** - Built-in percentage of equity allocation

## 🔧 How It Works

### Zone Creation Logic

**Supply Zones (Selling Pressure):**

1. Strong momentum downward movement (configurable body-to-range ratio)

2. Identified bullish base candle (where institutions accumulated shorts)

3. Break of Structure downward (price breaks below recent swing low)

4. Zone created at the base candle's high/low range

**Demand Zones (Buying Pressure):**

1. Strong momentum upward movement

2. Identified bearish base candle (where institutions accumulated longs)

3. Break of Structure upward (price breaks above recent swing high)

4. Zone created at the base candle's high/low range

### Entry Conditions

**Long Entry:**

- Price retests a demand zone (touches top of zone)

- Rejection confirmed (close above zone)

- Zone hasn't been used (if "first retest only" enabled)

- Minimum bars since last entry respected

**Short Entry:**

- Price retests a supply zone (touches bottom of zone)

- Rejection confirmed (close below zone)

- Zone hasn't been used (if "first retest only" enabled)

- Minimum bars since last entry respected

## ⚙️ Customizable Parameters

### Display Settings

- **Show Zones** - Toggle zone visualization on/off

- **Max Stored Zones** - Control number of active zones (1-50 per type)

- **Color Customization** - Adjust supply/demand colors and transparency

### Zone Quality Filters

- **Momentum Body Fraction** - Minimum body size for momentum candles (0.1-0.9)

- **Min Momentum Candles** - Number of consecutive momentum candles required (1-5)

- **Big Candle Body Fraction** - Alternative single-candle momentum threshold (0.5-0.95)

- **Min Zone Size %** - Minimum zone height as percentage of price (0.01-5.0%)

### BOS Configuration

- **Swing Length** - Lookback period for structure identification (3-20)

- **ATR Length** - Period for volatility measurement (1-50)

- **BOS Required Break** - ATR multiplier for valid structure break (0.1-3.0)

### Midline Options

- **None** - No midline displayed

- **Geometric** - Simple average of zone top/bottom

- **CenterVolume** - Volume-weighted center based on highest volume bar in window

### Risk Management

- **SL Buffer %** - Additional space beyond zone boundary (0-5%)

- **Take Profit RR** - Risk-reward ratio for target placement (0.5-10x)

### Entry Rules

- **Only 1st Retest per Zone** - Trade zones only once for higher quality

- **Min Bars Between Entries** - Prevent overtrading (1-20 bars)

## 📈 Recommended Settings

### Conservative (Lower Frequency, Higher Quality)

```

Momentum Body Fraction: 0.30

Min Momentum Candles: 2-3

BOS Required Break: 0.8-1.0

Min Zone Size: 0.15-0.20%

Only 1st Retest: Enabled

```

### Balanced (Default)

```

Momentum Body Fraction: 0.28

Min Momentum Candles: 2

BOS Required Break: 0.7

Min Zone Size: 0.12%

Only 1st Retest: Enabled

```

### Aggressive (Higher Frequency, More Signals)

```

Momentum Body Fraction: 0.20-0.25

Min Momentum Candles: 1-2

BOS Required Break: 0.4-0.5

Min Zone Size: 0.08-0.10%

Only 1st Retest: Disabled

```

## 🎨 Visual Elements

- **Red Boxes** - Supply zones (potential selling areas)

- **Green Boxes** - Demand zones (potential buying areas)

- **Dotted Midlines** - Center of each zone (fades when zone is used)

- **Debug Triangles** - Shows when zone creation conditions are met

- Red triangle down = Supply zone created

- Green triangle up = Demand zone created

## 📊 Best Practices

1. **Use on Higher Timeframes** - 1H, 4H, and Daily charts work best for institutional zones

2. **Combine with Trend** - Trade zones in direction of overall market structure

3. **Wait for Confirmation** - Don't enter immediately at zone touch; wait for rejection

4. **Adjust for Market Volatility** - Increase BOS multiplier in choppy markets

5. **Monitor Zone Quality** - Fresh zones typically have higher success rates

6. **Backtest Your Settings** - Optimize parameters for your specific market and timeframe

## ⚠️ Risk Disclaimer

This strategy is for educational and informational purposes only. Past performance does not guarantee future results. Always:

- Use proper position sizing

- Set appropriate stop losses

- Test thoroughly before live trading

- Consider market conditions and overall trend

- Never risk more than you can afford to lose

## 🔍 Data Window Information

The strategy provides real-time metrics visible in the data window:

- Supply Zones Count

- Demand Zones Count

- ATR Value

- Momentum Signals (Up/Down)

- BOS Signals (Up/Down)

## 📝 Version History

**v1.0 - Enhanced Edition**

- Improved BOS detection logic

- Extended base candle search range

- Added comprehensive input validation

- Enhanced visual feedback system

- Robust array bounds checking

- Debug signals for troubleshooting

## 💡 Tips for Optimization

- **Trending Markets**: Lower momentum requirements, tighter BOS filters

- **Ranging Markets**: Increase zone size minimum, enable first retest only

- **Volatile Assets**: Increase ATR multiplier and SL buffer

- **Lower Timeframes**: Reduce swing length, increase min bars between entries

- **Higher Timeframes**: Increase swing length, relax momentum requirements

---

**Created with focus on institutional order flow, smart money concepts, and practical risk management.**

*Happy Trading! 📈*

AI ALGO [Ganesh]Core Strategy Components\

1. EMA (Exponential Moving Average) SystemThe strategy uses three EMAs to identify trend direction:

EMA 48 (longer-term trend)

EMA 2 (short-term momentum)

EMA 21 (medium-term trend)

How it works:

Bullish trend: When price is above EMA 21 (green cloud)

Bearish trend: When price is below EMA 21 (red cloud)

EMA Cloud: The area between EMA 2 and EMA 48/21 provides visual trend confirmation

Optional higher timeframe (HTF) analysis for multi-timeframe confirmation

2. DEMA ATR (Double EMA + Average True Range)

This is a dynamic support/resistance indicator that adapts to volatility:Components:

DEMA (Double Exponential Moving Average): Smooths price action with less lag

ATR Bands: Creates upper and lower bands based on volatility (ATR × 1.7 factor)

Signal Generation:

Green line: Uptrend (DEMA ATR rising)

Red line: Downtrend (DEMA ATR falling)

Acts as a trailing stop-loss level that adjusts with market volatility

3. Smart Trail System (Fibonacci-Based)

An advanced trailing stop system using modified true range calculations:Key Features:

Calculates true range using Wilder's smoothing method

Creates Fibonacci retracement levels (61.8%, 78.6%, 88.6%) from the trail line

Adaptive stop-loss: Adjusts based on ATR factor (4.2) and smoothing (4)

Trend Detection:

Bullish: Price > Trailing line (blue zones)

Bearish: Price < Trailing line (red zones)

The Fibonacci zones show potential support/resistance areas

4. ZigZag Indicator Identifies significant swing highs and lows:

Length parameter: 13 (sensitivity control)

Labels: Higher Highs (HH), Lower Lows (LL), etc.

Helps identify trend reversals and key pivot points

5. Support & Resistance Levels

Strength-based S/R: Identifies horizontal support/resistance zones

Zone width: Adjustable percentage-based zones

High/Low zones: Marks significant price levels

Trading LogicEntry Conditions (Implied)The strategy likely enters trades when:Long Entry:

Price crosses above DEMA ATR (green)

Price is above EMA 21 (bullish EMA cloud)

Smart Trail confirms uptrend

Price bounces from Fibonacci support levels

Short Entry:

Price crosses below DEMA ATR (red)

Price is below EMA 21 (bearish EMA cloud)

Smart Trail confirms downtrend

Price rejects from Fibonacci resistance levels

Exit/Stop-Loss Strategy

Trailing stops: Using Smart Trail Fibonacci levels

Dynamic stops: DEMA ATR line acts as a moving stop-loss

Risk management: Position sizing at 50% of equity per trade

Dashboard Features1. Weekly Performance Table

Tracks trades per day of the week

Shows win/loss statistics

Calculates win rate percentage

2. Monthly Performance Table

Monthly P&L breakdown

Yearly performance summary

Color-coded returns (green = profit, red = loss)

Strategy Parameters

Initial Capital: $5,000

Commission: 0.02% per trade

Position Size: 50% of equity

Pyramiding: Disabled (no adding to positions)

Calculation: On bar close (not tick-by-tick)

Visual Elements

EMA clouds: Green (bullish) / Red (bearish)

DEMA ATR line: Dynamic support/resistance

Smart Trail zones: Fibonacci-based colored bands

ZigZag lines: Swing high/low connections

S/R zones: Horizontal support/resistance areas

Strategy Philosophy

This is a trend-following strategy with dynamic risk management that:

Uses multiple timeframes for confirmation

Adapts to volatility through ATR-based indicators

Provides clear visual cues for trend direction

Includes comprehensive performance tracking

Combines momentum (EMAs) with volatility (ATR) for robust signals

The strategy works best in trending markets and uses the Fibonacci trail system to maximize profits while protecting against reversals with adaptive stop-losses.

QuantBot StrategyAutomated opening range breakout strategy for futures and intraday trading. Identifies the initial trading range and executes trades on breakouts with multiple confluence filters.

Key Features:

Opening Range Detection: Automatically identifies and tracks the opening range

Multi-Filter Entry System: Optional confluence filters to improve entry quality

Flexible Profit Targets: Dynamic targets based on recent volatility, or fixed tick/dollar targets

Advanced Position Management: Add to positions at key levels; partial profit-taking with trailing runners

Risk Controls: Multiple stop loss methods, maximum trade limits, and distance filters

Time-Based Filters: Configurable trading hours and days, with optional holiday blackouts

Visual Indicators: Displays trend lines, bands, and range levels on your chart

Designed for disciplined, systematic trading with customizable risk management and position sizing.

SmartMoneyConcept ProFlow StrategySmartMoneyConcept ProFlow is a complete SMC-based algo built for trending markets and clean volatility phases – especially on crypto pairs like BTC, ETH and perpetual futures.

It combines:

• Smart Money swing structure (BOS / CHoCH)

• Dynamic Support & Resistance levels

• Order Block–style gap detection

• Volatility normalization (ATR / Range / BBWidth)

• SuperTrend trend filter

• ATR & Volume-based exits, TP lock and session control

The goal: fewer random trades, more focused entries when structure + volatility + trend are in sync.

1. Core Idea

Smart Structure Levels (S/R)

– The strategy builds dynamic support/resistance using swing highs/lows.

– Breakouts above resistance or below support, with enough volatility (filter), become primary trade signals.

BOS / CHoCH Engine

– Tracks Break of Structure (BOS) and Change of Character (CHoCH).

– BOS up/down help define the current trend bias.

– CHoCH highlights potential reversals after a confirmed BOS in the opposite direction.

Order Block Gap Logic

– Detects displacement candles with gaps (based on ATR) to approximate OB-style “impulsive moves”.

– Bullish gaps can add confluence for long entries, bearish gaps for shorts.

Volatility-Aware Entries

– Uses normalized volatility (via ATR, Range or BBWidth).

– Filters out breakouts in dead, low-vol environments and focuses on moves with real expansion.

2. Trend & Risk Management Stack

SuperTrend Filter

– Optional “Only With SuperTrend Direction” to restrict entries to the current ST trend.

– ST flips can also force exits if you want to exit as soon as the main trend changes.

ATR-Based Stops & Trails

– ATR distance check to avoid ultra-tight stops that get chopped instantly.

– Three modes:

• StopOnly – classic fixed ATR stop.

• TrailOnly – trailing ATR-style stop.

• StopAndTrail – initial fixed stop that later trails with price.

Volume-Based Exits (Optional)

– Exit on extremely low volume (move losing participation).

– Or on opposite volume spikes (strong counter-pressure against your position).

– Or use Both for a more active volume management.

TP Lock Logic

– When unrealized profit reaches a chosen value, the position is closed and a “lock” can be applied.

– Use this lock to:

• block same-direction re-entries for that side, or

• allow them again depending on your preference.

3. Anti-Churn & Session Control

Anti-Churn Controls

– Minimum bars between entries.

– Cooldown after an ATR exit.

– Limit of max entries per bar.

Session Filter

– Restrict trading to a specific hourly window (e.g. main market session).

– Option to force close positions outside your active session.

– Handy for intraday traders who don’t want overnight or low-liquidity exposure.

4. SmartMoney Preset Modes

Preset Mode:

• EtherFlux – more flexible, for general breakout & volatility trading.

• SmartMoney – SMC-focused preset:

– Adjusted length, volatility filter and ATR settings.

– Option to disable exits from the strategy side (for manual risk control).

Switching presets automatically tunes multiple internal parameters so you don’t have to micromanage every input each time.

5. Visual Layer

This script has a complete visual suite to help you “read the tape”:

– Bar Colors by position and SuperTrend bias.

– Support / Resistance dots and lines (stepline style).

– Order Block markers (bullish / bearish gap labels).

– BOS / CHoCH labels to track structure shifts in real-time.

– Liquidation Zones (visual only)

• Approximate long and short liquidation areas based on assumed leverage.

• Shaded zones on the chart for quick liquidity map.

– Status Labels

• Session status (ACTIVE / OFF / DISABLED).

• Current position (LONG / SHORT / FLAT).

• TP Lock status (longs locked / shorts locked / no lock).

All visuals are designed for dark charts but also work on light themes with minor tweaks.

6. Quick Input Guide

• Levels Period & Volatility Filter – main structure sensitivity and breakout quality.

• Volatility Method – ATR / Range / BBWidth normalization for the vol filter.

• ATR Stop & Management – core risk rules: ATR multiplier, stop/trail mode, min ATR distance.

• SuperTrend Settings – trend bias and ST-flip exits.

• SmartMoney Preset – quick switch between EtherFlux and SmartMoney tuning.

• Volume Exits – low volume / opposite spike / both.

• Session Filter – hour-based trading window + optional forced flat outside session.

• Follow-Signal Mode – flip from long→short or short→long when signal reverses (signal-based rotation).

• TP Lock – secure profits at a fixed amount and optionally block same-direction re-entries.

• Liq Zones – visual only, for liquidity map (no direct trade logic).

How to Use (My Suggestion)

Start on 15m–4H charts for liquid pairs (BTC, ETH, majors).

Choose your preset:

– EtherFlux for more general breakout + vol trading.

– SmartMoney if you want stricter SMC behaviour.

Turn on SuperTrend + ATR stops for cleaner risk management.

Forward-test in replay / paper trading before using real capital.

Use the visual BOS/CHoCH + Liq Zones as context , not as blind signals.

Important

This is a backtest & research tool . It is not financial advice and does not guarantee profits. Always combine it with your own risk management, position sizing, and forward-testing before going live. Trading leveraged products and crypto can result in partial or full loss of capital.

Absorption PROOF - Absorption PRO (Clean & Smart)Ultra-clean, high-precision absorption reversal strategy.Detects institutional buying/selling pressure using volume-weighted delta proxy and VWAP deviation zones.Smart RSI + early-session range filter automatically separates valid range-bound reversals from trend exhaustion.Green/Red circles → High-probability entries (fully tradable)

Small crosses + colored zones → Rejected signals (avoid)

Blue dotted lines → Session range ±100% deviation levels (optional)

By default: only signals and rejection zones displayed — zero clutter.Minimalist, professional, and deadly accurate on futures & forex (1m–15m).Less noise. Better trades.

Crypto Grid 2025+ Long Only (Asym TP)Crypto Grid 2025+ Long Only (Asymmetric Take-Profit) is a long-only mean-reversion grid strategy designed for intraday cryptocurrency trading.

The core idea is to accumulate long positions as price moves downward within a locally defined price range and to exit positions on upward retracements.

The strategy automatically builds a multi-level grid between the highest and lowest price over a user-defined lookback period (“range length”). Each grid level acts as a potential entry point when price crosses it from above.

Key Features

1. Long-only grid logic

The strategy opens long positions only, progressively increasing exposure as price moves into lower grid levels.

2. Asymmetric take-profit mechanism

Instead of taking profit strictly at the next grid level, the strategy allows targeting multiple levels above the entry point. This increases the average profit per winning trade and shifts the reward-to-risk profile toward larger, less frequent wins.

3. Optional partial take-profit

A portion of each trade can be closed at the nearest grid level, while the remainder is held for a more distant asymmetric target. This balances consistency and profit potential.

4. Volume-based market filter

Entries can be restricted to periods of healthy market activity by requiring volume to exceed a moving-average baseline.

5. Capital-scaled position sizing

Position size is determined by risk percentage, grid spacing, and a dynamic sizing mode (original / conservative / aggressive).

6. Built-in risk controls

global stop below the lower boundary of the range,

global take-profit above the upper boundary,

automatic shutdown after a configurable loss-streak.

Market Philosophy

This strategy belongs to the mean-reversion family: it expects short-term overshoots to revert back toward mid-range liquidity zones.

It is not trend-following.

It performs best in choppy, range-bound, or slow-grinding markets — especially on liquid crypto pairs.

Recommended Use Cases

Short timeframes (1–15 minutes)

High-liquidity crypto pairs

Sideways or rotational price action

Exchanges with low fees (due to higher order count)

Not Intended For

Strong trending markets without pullbacks

Assets with thin order books

Use with leverage without additional risk controls

Summary

Crypto Grid 2025+ Long Only (Asymmetric TP) is a refined grid-based mean-reversion strategy optimized for modern crypto markets. Its asymmetric take-profit framework is specifically engineered to reduce the classical issue of “small wins and large occasional losses” found in traditional grid systems, giving it a more favorable long-term trade distribution.

STRATEGY 1 │ Red Dragon │ Model 1 │ Pro │ [Titans_Invest]The Red Dragon Model 1 is a fully automated trading strategy designed to operate BTC/USDT.P on the 4-hour chart with precision, stability, and consistency. It was built to deliver reliable behavior even during strong market movements, maintaining operational discipline and avoiding abrupt variations that could interfere with the trader’s decision-making.

Its core is based on a professionally engineered logical structure that combines trend filters, confirmation criteria, and balanced risk management. Every component was designed to work in an integrated way, eliminating noise, avoiding unnecessary trades, and protecting capital in critical moments. There are no secret mechanisms or hidden logic: everything is built to be objective, clean, and efficient.

Even though it is based on professional quantitative engineering, Red Dragon Model 1 remains extremely simple to operate. All logic is clearly displayed and fully accessible within TradingView itself, making it easy to understand for both beginners and experienced traders. The structure is organized so that any user can quickly view entry conditions, exit criteria, additional filters, adjustable parameters, and the full mechanics behind the strategy’s behavior.

In addition, the architecture was built to minimize unnecessary complexity. Parameters are straightforward, intuitive, and operate in a balanced way without requiring deep adjustments or advanced knowledge. Traders have full freedom to analyze the strategy, understand the logic, and make personal adaptations if desired—always with total transparency inside TradingView.

The strategy was also designed to deliver consistent operational behavior over the long term. Its confirmation criteria reduce impulsive trades; its filters isolate noise; and its overall logic prioritizes high-quality entries in structured market movements. The goal is to provide a stable, clear, and repeatable flow—essential characteristics for any medium-term quantitative approach.

Combining clarity, professional structure, and ease of use, Red Dragon Model 1 offers a solid foundation both for users who want a ready-to-use automated strategy and for those looking to study quantitative models in greater depth.

This entire project was built with extreme dedication, backed by more than 14,000 hours of hands-on experience in Pine Script, continuously refining patterns, techniques, and structures until reaching its current level of maturity. Every line of code reflects this long process of improvement, resulting in a strategy that unites professional engineering, transparency, accessibility, and reliable execution.

🔶 MAIN FEATURES

• Fully automated and robust: Operates without manual intervention, ideal for traders seeking consistency and stability. It delivers reliable performance even in volatile markets thanks to the solid quantitative engineering behind the system.

• Multiple layers of confirmation: Combines 10 key technical indicators with 15 adaptive filters to avoid false signals. It only triggers entries when all trend, market strength, and contextual criteria align.

• Configurable and adaptable filters: Each of the 15 filters can be enabled, disabled, or adjusted by the user, allowing the creation of personalized statistical models for different assets and timeframes. This flexibility gives full freedom to optimize the strategy according to individual preferences.

• Clear and accessible logic: All entry and exit conditions are explicitly shown within the TradingView parameters. The strategy has no hidden components—any user can quickly analyze and understand each part of the system.

• Integrated exclusive tools: Includes complete backtest tables (desktop and mobile versions) with annualized statistics, along with real-time entry conditions displayed directly on the chart. These tools help monitor the strategy across devices and track performance and risk metrics.

• No repaint: All signals are static and do not change after being plotted. This ensures the trader can trust every entry shown without worrying about indicators rewriting past values.

🔷 ENTRY CONDITIONS & RISK MANAGEMENT

Red Dragon Model 1 triggers buy (long) or sell (short) signals only when all configured conditions are satisfied. For example:

• Volume:

• The system only trades when current volume exceeds the volume moving average multiplied by a user-defined factor, indicating meaningful market participation.

• RSI:

• Confirms bullish bias when RSI crosses above its moving average, and bearish bias when crossing below.

• ADX:

• Enters long when +DI is above –DI with ADX above a defined threshold, indicating directional strength to the upside (and the opposite conditions for shorts).

• Other indicators (MACD, SAR, Ichimoku, Support/Resistance, etc.)

Each one must confirm the expected direction before a final signal is allowed.

When all bullish criteria are met simultaneously, the system enters Long; when all criteria indicate a bearish environment, the system enters Short.

In addition, the strategy uses fixed Take Profit and Stop Loss targets for risk control:

Currently: TP around 1.5% and SL around 2.0% per trade, ensuring consistent and transparent risk management on every position.

⚙️ INDICATORS

__________________________________________________________

1) 🔊 Volume: Avoids trading on flat charts.

2) 🍟 MACD: Tracks momentum through moving averages.

3) 🧲 RSI: Indicates overbought or oversold conditions.

4) 🅰️ ADX: Measures trend strength and potential entry points.

5) 🥊 SAR: Identifies changes in price direction.

6) ☁️ Cloud: Accurately detects changes in market trends.

7) 🌡️ R/F: Improves trend visualization and helps avoid pitfalls.

8) 📐 S/R: Fixed support and resistance levels.

9)╭╯MA: Moving Averages.

10) 🔮 LR: Forecasting using Linear Regression.

__________________________________________________________

🟢 ENTRY CONDITIONS 🔴

__________________________________________________________

IF all conditions are 🟢 = 📈 Long

IF all conditions are 🔴 = 📉 Short

__________________________________________________________

🚨 CURRENT TRIGGER SIGNAL 🚨

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🟢 ALL ENTRY CONDITIONS AVAILABLE 🔴

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult) and (close) > (open)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult) and (close) < (open)

🍟 MACD

🟢 LONG = (MACD) > (Signal Smoothing)

🔴 SHORT = (MACD) < (Signal Smoothing)

🧲 RSI

🟢 LONG = (RSI) < (Upper)

🔴 SHORT = (RSI) > (Lower)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🅰️ ADX

🟢 LONG = (+DI) > (-DI) and (ADX) > (Treshold)

🔴 SHORT = (+DI) < (-DI) and (ADX) > (Treshold)

🥊 SAR

🟢 LONG = (close) > (SAR)

🔴 SHORT = (close) < (SAR)

☁️ Cloud

🟢 LONG = (Cloud A) > (Cloud B)

🔴 SHORT = (Cloud A) < (Cloud B)

☁️ Cloud

🟢 LONG = (Kama) > (Kama )

🔴 SHORT = (Kama) < (Kama )

🌡️ R/F

🟢 LONG = (high) > (UP Range) and (upward) > (0)

🔴 SHORT = (low) < (DOWN Range) and (downward) > (0)

🌡️ R/F

🟢 LONG = (high) > (UP Range)

🔴 SHORT = (low) < (DOWN Range)

📐 S/R

🟢 LONG = (close) > (Resistance)

🔴 SHORT = (close) < (Support)

╭╯MA2️⃣

🟢 LONG = (Cyan Bar MA2️⃣)

🔴 SHORT = (Red Bar MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (close) > (MA2️⃣)

🔴 SHORT = (close) < (MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (Positive MA2️⃣)

🔴 SHORT = (Negative MA2️⃣)

__________________________________________________________

🎯 TP / SL 🛑

__________________________________________________________

🎯 TP: 1.5 %

🛑 SL: 2.0 %

__________________________________________________________

🪄 UNIQUE FEATURES OF THIS STRATEGY

____________________________________

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

_____________________________

𝄜 BACKTEST / PERFORMANCE 𝄜

_____________________________

• Net Profit: +634.47%, Maximum Drawdown: -18.44%.

🪙 PAIR / TIMEFRAME ⏳

🪙 PAIR: BINANCE:BTCUSDT.P

⏳ TIME: 4 hours (240m)

✅ ON ☑️ OFF

✅ LONG

✅ SHORT

🎯 TP / SL 🛑

🎯 TP: 1.5 (%)

🛑 SL: 2.0 (%)

⚙️ CAPITAL MANAGEMENT

💸 Initial Capital: 10000 $ (TradingView)

💲 Order Size: 10 % (Of Equity)

🚀 Leverage: 10 x (Exchange)

💩 Commission: 0.03 % (Exchange)

📆 BACKTEST

🗓️ Start: Setember 24, 2019

🗓️ End: November 21, 2025

🗓️ Days: 2250

🗓️ Yers: 6.17

🗓️ Bars: 13502

📊 PERFORMANCE

💲 Net Profit: + 63446.89 $

🟢 Net Profit: + 634.47 %

💲 DrawDown Maximum: - 10727.48 $

🔴 DrawDown Maximum: - 18.44 %

🟢 Total Closed Trades: 1042

🟡 Percent Profitable: 63.92 %

🟡 Profit Factor: 1.247

💲 Avg Trade: + 60.89 $

⏱️ Avg # Bars in Trades

🕯️ Avg # Bars: 4

⏳ Avg # Hrs: 15

✔️ Trades Winning: 666

❌ Trades Losing: 376

✔️ Maximum Consecutive Wins: 11

❌ Maximum Consecutive Losses: 7

📺 Live Performance : br.tradingview.com

• Use this strategy on the recommended pair and timeframe above to replicate the tested results.

• Feel free to experiment and explore other settings, assets, and timeframes.

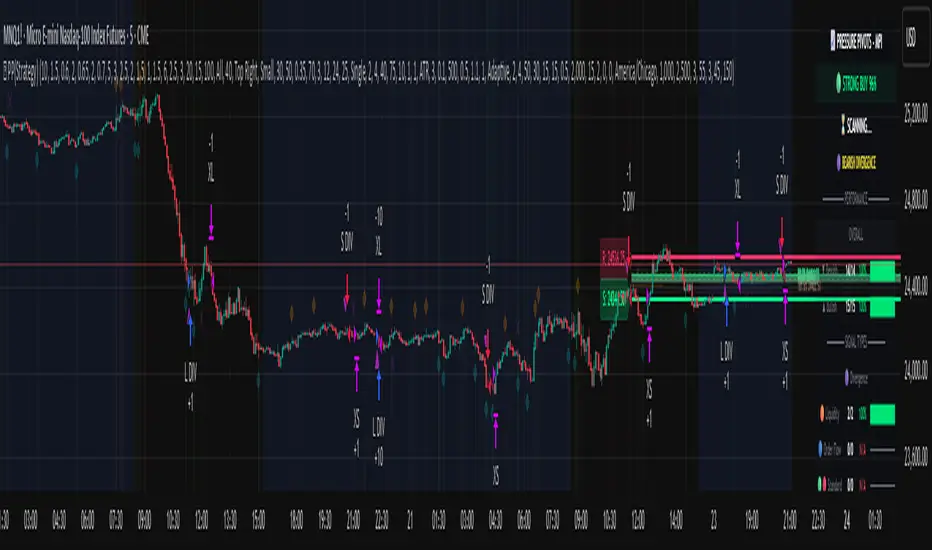

Pressure Pivots - MPI (Strategy)⇋ PRESSURE PIVOTS — MARKET PRESSURE INDEX STRATEGY

A comprehensive reversal trading system that combines order flow pressure analysis, multi-factor confluence detection, and adaptive machine learning to identify high-probability turning points in liquid markets.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

CORE INNOVATION: MARKET PRESSURE INDEX (MPI)

Traditional indicators measure price movement. The Market Pressure Index measures the force behind the movement.

How MPI Works:

Every bar tells two stories through volume distribution:

• Buy Pressure: Volume × (Close - Low) / (High - Low)

• Sell Pressure: Volume × (High - Close) / (High - Low)

• Net Pressure: Buy Pressure - Sell Pressure

This raw pressure is then normalized against baseline activity to create the bounded MPI (-1.0 to +1.0):

• Smooth Pressure: EMA(Net Pressure, period)

• Baseline Activity: SMA(|Net Pressure|, period × 2)

• MPI: (Smooth Pressure / Baseline) × Sensitivity

What MPI Reveals:

MPI > +0.7: Extreme buy pressure → Exhaustion potential

MPI = +0.2 to +0.7: Healthy bullish momentum

MPI = -0.2 to +0.2: Neutral/balanced pressure

MPI = -0.7 to -0.2: Healthy bearish momentum

MPI < -0.7: Extreme sell pressure → Exhaustion potential

Why It Works:

Two bars can both move 10 points, but if one closes at the high on high volume (aggressive buying) and the other closes mid-range on average volume (weak buying), only MPI distinguishes between sustainable momentum and exhaustion. This volume-weighted pressure analysis reveals conviction behind price moves—the key to timing reversals.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SEVEN-FACTOR CONFLUENCE SYSTEM

MPI extremes alone aren't enough. The system requires multiple independent confirmations through weighted scoring:

1. DIVERGENCE (Weight: 3.0) — Premium Signal Type: DIV

Price makes new high but MPI makes lower high (or inverse for bullish)

• Detection: Tracks pivots with 5-bar lookback, compares price vs MPI at pivot points

• Signal: Purple triangles, highest weight (pressure weakening while price extends)

2. LIQUIDITY SWEEP (Weight: 2.5) — Premium Signal Type: LIQ

Price breaks swing high/low within 0.3 ATR then reverses

• Detection: Break within tolerance + close back through level

• Signal: Orange triangles, second-highest weight (stop hunt reversal)

3. ORDER FLOW IMBALANCE (Weight: 2.0) — Premium Signal Type: OF

Aggressive buying/selling 50% above normal

• Detection: EMA(aggressive volume) vs SMA(imbalance) threshold

• Signal: Aqua triangles, institutional positioning

4. VELOCITY EXHAUSTION (Weight: 1.5)

Parabolic move (2+ ATRs in 3 bars) + extreme MPI

• Detection: |3-bar price change / ATR| > threshold + MPI > ±0.5

• Indicates: Momentum deceleration, blow-off top/bottom

5. WICK REJECTION (Weight: 1.5)

Single bar: wick > 60% of range, or sequence: 2 bars with 40% + 30% wicks

• Detection: Shooting stars (bearish) or hammers (bullish)

• Indicates: Intrabar rejection, battle won by opposing side

6. VOLUME SPIKE (Weight: 1.0)

Volume > 20-bar average × multiplier (default: 2.0x)

• Detection: Participation surge confirmation

• Lowest weight: Can be manipulated, better as confirmation

7. POSITION FACTOR (Weight: 1.0)

At 10-bar highest (bearish) or lowest (bullish)

• Detection: Structural positioning for reversal

• Base requirement: Must be at extreme to score

Scoring Logic:

Premium Signals (DIV/LIQ/OF): Must score ≥6.0 (default premiumThreshold)

Standard Signals (STD): Must score ≥4.0 (default standardThreshold)

Example Scoring:

Divergence (3.0) + Liquidity Sweep (2.5) + Volume (1.0) = 6.5 → FIRES (DIV signal)

Recent High (1.0) + Wick (1.5) + Volume (1.0) + Velocity (1.5) = 5.0 → FIRES (STD signal)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ADAPTIVE LEARNING ENGINE

Unlike static strategies, this system learns from every trade and optimizes itself.

Performance Tracking:

Every trade records:

• Entry Score: Confluence level at entry

• Signal Type: DIV / LIQ / OF / STD

• Win/Loss: Boolean outcome

• R-Multiple: (Exit - Entry) / (Entry - Stop)

• MAE: Maximum Adverse Excursion (worst drawdown)

• MFE: Maximum Favorable Excursion (best profit reached)

Three Adaptive Parameters:

1. Signal Threshold Adaptation

If Win Rate < Target (45%): RAISE threshold → fewer signals, better quality

If Win Rate > Target + 10% AND good R: LOWER threshold → more signals, profitable

2. Stop Distance Adaptation

If Avg MAE > 0.85 AND WR < 50%: WIDEN stops → reduce premature exits

If Avg MAE < 0.4 AND WR > 55%: TIGHTEN stops → reduce risk

3. Target Distance Adaptation

If Avg MFE > Target × 1.5: EXTEND targets → capture more of runners

If Avg MFE < Target × 0.7: SHORTEN targets → take profits faster

Signal Type Filtering:

The system tracks performance by type (DIV/LIQ/OF/STD):

• If Type WR < 40% AND Avg R < 0.8: Type DISABLED

• If Type WR ≥ 40% OR Avg R ≥ 0.8: Type RE-ENABLED

Example: If OF signals consistently lose while DIV signals win, system automatically stops taking OF signals and focuses on DIV.

Warmup Period:

First 30 trades (default) gather baseline data with relaxed thresholds. After warmup, full adaptation activates.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

COMPLETE POSITION MANAGEMENT

Dynamic Position Sizing:

Base Contracts = (Equity × Risk%) / (Stop Distance × Point Value)

Then multiplied by:

• Score Bonus: Up to +50% for highest-scoring signals

• Signal Type Bonus: DIV signals +50%, LIQ signals +30%

• Streak Multiplier: After 3 losses: 50% reduction, After 3 wins: 25% increase

Example: High-scoring DIV signal on winning streak = 3-4× larger position than weak STD signal on losing streak

Entry Modes:

Single Entry: Full size at once, exit at TP2 (or partial at TP1)

Tiered Entry: 40% at TP1 (2R), 60% at TP2 (4R adaptive)

Stop Management (3 Modes):

Structural: Beyond recent 20-bar swing high/low + buffer

ATR: Fixed ATR multiplier (default: 2.0 ATR, then adapts)

Hybrid: Attempt structural, fallback to ATR if invalid

Plus:

• Breakeven: Move stop to entry ± 1 tick when 1R reached

• Trailing: Activate when 1.5R reached, trail 0.8R behind price

• Max Loss Override: Cap dollar risk regardless of calculation

Target Management:

Fixed Mode: TP1 = 2R, TP2 = 4R

Adaptive Mode: TP1 = 2R fixed, TP2 adapts based on MFE analysis

Partial Exits: Default 50% at TP1, remainder at TP2 or trailing stop

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

COMPREHENSIVE RISK CONTROLS

Daily Limits:

• Max Daily Loss: $2,000 default → HALT trading

• Max Daily Trades: 15 default → prevent overtrading

• Max Concurrent: 2 positions → limit correlation risk

Session Controls:

• Trading Hours: Specify start/end times + timezone

• Weekend Block: Optional (avoid crypto weekend volatility)

Prop Firm Protection (Live Trading Only):

• Daily Loss Limit: Stricter of general or prop limit ($1,000 default)

• Trailing Drawdown: Tracks high water mark, HALTS if breach ($2,500 default)

• Reset on Reload: Optional high water mark reset

Liquidity Filter (Optional):

• Time-Based: Avoid first/last X minutes of session

• Volume-Based: Require minimum volume ratio (0.5× average default)

Market Regime Filter (Optional):

• ADX-Based: Only trade when ADX > threshold (trending)

• Block: Consolidation (ADX < 20) or Transitional regimes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

REAL-TIME DASHBOARD

MPI Gauge Section:

Shows current pressure: 🟢 STRONG BUY (+0.5 to +1.0), 🟩 BUY PRESSURE (+0.2 to +0.5), ⚪ NEUTRAL (-0.2 to +0.2), 🟥 SELL PRESSURE (-0.5 to -0.2), 🔴 STRONG SELL (-1.0 to -0.5)

Signal Status Section:

• Active Signals: "🔴 DIV SELL" (purple background), "🟢 LIQ BUY" (orange), "🔵 OF SELL" (aqua), "🟢 STD BUY" (green)

• Warnings: "⚠️ BEAR WARNING" / "⚠️ BULL WARNING" (yellow) — setup forming, not full signal

• Scanning: "⏳ SCANNING..." (gray) — no signal active

• Confidence Bar: Visual score display "██████░░░░" showing confluence strength

Divergence Indicator:

"🟣 BEARISH DIVERGENCE" or "🟡 BULLISH DIVERGENCE" when detected

Performance Statistics:

• Overall Win Rate: Wins/Total with visual bar (lime ≥70%, yellow 50-70%, red <50%)

• Directional: Bearish vs Bullish win rates separately

• By Signal Type: DIV / LIQ / OF / STD individual performance tracking

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

KEY PARAMETERS EXPLAINED

🎯 Pressure Engine:

• MPI Period (5-50, default: 14): Smoothing period — lower for scalping, higher for position trading

• MPI Sensitivity (0.5-5.0, default: 1.5): Amplification — lower compresses range, higher more extremes

🔍 Detection:

• Wick Threshold (0.3-0.9, default: 0.6): Minimum wick-to-range ratio for rejection

• Volume Spike (1.2-3.0x, default: 2.0): Multiplier above average for spike

• Aggressive Ratio (0.5-0.9, default: 0.65): Close position in range for aggressive orders

• Velocity Threshold (1.0-5.0 ATR, default: 2.0): ATR-normalized move for exhaustion

• MPI Extreme (0.5-0.95, default: 0.7): Level considered overbought/oversold

⚖️ Weights:

• Divergence: 3.0 (highest — pressure weakening)

• Liquidity: 2.5 (second — stop hunts)

• Order Flow: 2.0 (institutional positioning)

• Velocity: 1.5 (momentum exhaustion)

• Wick: 1.5 (rejection patterns)

• Volume: 1.0 (lowest — can be manipulated)

🎚️ Thresholds:

• Premium (4.0-15.0, default: 6.0): Score for DIV/LIQ/OF signals

• Standard (2.0-8.0, default: 4.0): Score for STD signals

• Warning Confluence (1-4, default: 2): Factors for yellow diamond warnings

🧬 Adaptive:

• Enable (true/false, default: true): Master learning switch

• Warmup Trades (5-100, default: 30): Data collection before adaptation

• Lookback (20-200, default: 50): Recent trades for performance calculation

• Adapt Speed (0.05-0.50, default: 0.15): Parameter adjustment rate

• Target Win Rate (30-70%, default: 45%): Optimization goal

• Target R-Multiple (0.5-5.0, default: 1.5): Risk/reward goal

💼 Position:

• Base Risk (0.1-10.0%, default: 1.5%): Equity risked per trade

• Max Contracts (1-100, default: 10): Hard position limit

• DIV Bonus (1.0-3.0x, default: 1.5): Size multiplier for divergence signals

• LIQ Bonus (1.0-3.0x, default: 1.3): Size multiplier for liquidity signals

🛡️ Stops:

• Mode (Structural/ATR/Hybrid, default: ATR): Stop placement method

• ATR Multiplier (0.5-5.0, default: 2.0): Stop distance in ATRs (adapts)

• Breakeven at (0.3-3.0R, default: 1.0R): When to move stop to entry

• Trail Trigger (0.5-5.0R, default: 1.5R): When to activate trailing

• Trail Offset (0.3-3.0R, default: 0.8R): Distance behind price

🎯 Targets:

• Mode (Fixed/Adaptive, default: Fixed): Target placement method

• TP1 (0.5-10.0R, default: 2.0R): First target for partial exit

• TP2 (1.0-15.0R, default: 4.0R): Final target (adapts in adaptive mode)

• Partial % (0-100%, default: 50%): Position percentage to exit at TP1

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

PROFESSIONAL USAGE PROTOCOL

Phase 1: Paper Trading (Weeks 1-4)

• Setup: Default settings, all adaptive features ON, 0.5% base risk

• Goal: 30+ trades for warmup, observe MPI behavior and signal frequency

• Adjust: MPI sensitivity if stuck near neutral or always at extremes

• Threshold: Raise/lower if too many/few signals

Phase 2: Micro Live (Weeks 5-8)

• Requirements: WR >43%, at least one type >55%, Avg R >0.8

• Setup: 10-25% intended size, 0.5-1.0% risk, 1 position max

• Focus: Execution quality, match dashboard performance

• Journal: Screenshot every signal, track outcomes

Phase 3: Full Scale (Month 3+)

• Requirements: WR >45% over 50+ trades, Avg R >1.2, drawdown <15%

• Progression: Months 3-4 (1.0-1.5% risk), 5-6 (1.5-2.0%), 7+ (1.5-2.5%)

• Maintenance: Weekly dashboard review, monthly deep analysis

• Warnings: Reduce size if WR drops >10%, consecutive losses >7, or drawdown >20%

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DEVELOPMENT INSIGHTS

The Pressure Insight: Emerged from analyzing intrabar volume distribution. Within every candlestick, volume accumulates at different price levels. MPI deconstructs this to reveal conviction behind moves.

The Confluence Challenge: Early versions using MPI extremes alone achieved only 42% win rate. The seven-factor confluence system emerged from testing which combinations produced reliable reversals. Divergence + liquidity sweep became the strongest setup (68% win rate in isolation).

The Adaptive Breakthrough: Per-signal-type performance tracking revealed DIV signals winning at 71% while OF signals languished at 38%. Adaptive filtering disabled weak types automatically, recovering win rate from 39% to 54% during the 2022 volatility spike.

The Position Sizing Revelation: Dynamic sizing based on signal quality and recent performance increased Sharpe ratio from 1.2 to 1.9 while decreasing max drawdown from 18% to 12% over 500 trades. Bigger positions on better signals = geometric edge amplification.

The Risk Control Lesson: Testing with $50K accounts revealed catastrophic failure modes: daily loss cascades, overtrading commission bleed, weekend gap blowouts. Multi-layer controls (daily limits, concurrent caps, prop firm protection) became essential.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

LIMITATIONS & ASSUMPTIONS

What This Is NOT:

• NOT a Holy Grail: Typical performance 52-58% WR, 1.3-1.8 avg R, probabilistic edge

• NOT Predictive: Identifies high-probability conditions, doesn't forecast prices

• NOT Market-Agnostic: Best on liquid auction-driven markets (futures, forex, major crypto)

• NOT Hands-Off: Requires oversight for news events, gaps, system anomalies

• NOT Immune to Regime Changes: Adaptive engine helps but cannot predict black swans

Critical Assumptions:

1. Volume reflects intent (valid for regulated markets, violated by wash trading)

2. Pressure extremes mean-revert (true in ranging/exhaustion, fails in paradigm shifts)

3. Stop hunts exist (valid in liquid markets, less in thin/random walk periods)

4. Past patterns persist (valid in stable regimes, fails when structure fundamentally changes)

Works Best On: Major futures (ES, NQ, CL), liquid forex pairs (EUR/USD, GBP/USD), large-cap stocks, BTC

Performs Poorly On: Low-volume stocks, illiquid crypto pairs, news-driven headline events

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

RISK DISCLOSURE

Trading futures, forex, and leveraged instruments involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. This strategy is provided for educational purposes only and should not be construed as financial advice.

The adaptive engine learns from historical data—there is no guarantee that past relationships will persist. Market conditions change, volatility regimes shift, and black swan events occur. No strategy can eliminate the risk of loss.

Users must validate performance on their specific instruments and timeframes before risking capital. The developer makes no warranties regarding profitability or suitability. Users assume all responsibility for trading decisions and outcomes.

"The market doesn't care about your indicators. It only cares about pressure—who's willing to pay more, who's desperate to sell. Find the exhaustion. Trade the reversal. Let the system learn the rest."

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

STRATEGY 1 │ Red Dragon │ Model 1 │ [Titans_Invest]The Red Dragon Model 1 is a fully automated trading strategy designed to operate BTC/USDT.P on the 4-hour chart with precision, stability, and consistency. It was built to deliver reliable behavior even during strong market movements, maintaining operational discipline and avoiding abrupt variations that could interfere with the trader’s decision-making.

Its core is based on a professionally engineered logical structure that combines trend filters, confirmation criteria, and balanced risk management. Every component was designed to work in an integrated way, eliminating noise, avoiding unnecessary trades, and protecting capital in critical moments. There are no secret mechanisms or hidden logic: everything is built to be objective, clean, and efficient.

Even though it is based on professional quantitative engineering, Red Dragon Model 1 remains extremely simple to operate. All logic is clearly displayed and fully accessible within TradingView itself, making it easy to understand for both beginners and experienced traders. The structure is organized so that any user can quickly view entry conditions, exit criteria, additional filters, adjustable parameters, and the full mechanics behind the strategy’s behavior.

In addition, the architecture was built to minimize unnecessary complexity. Parameters are straightforward, intuitive, and operate in a balanced way without requiring deep adjustments or advanced knowledge. Traders have full freedom to analyze the strategy, understand the logic, and make personal adaptations if desired—always with total transparency inside TradingView.

The strategy was also designed to deliver consistent operational behavior over the long term. Its confirmation criteria reduce impulsive trades; its filters isolate noise; and its overall logic prioritizes high-quality entries in structured market movements. The goal is to provide a stable, clear, and repeatable flow—essential characteristics for any medium-term quantitative approach.

Combining clarity, professional structure, and ease of use, Red Dragon Model 1 offers a solid foundation both for users who want a ready-to-use automated strategy and for those looking to study quantitative models in greater depth.

This entire project was built with extreme dedication, backed by more than 14,000 hours of hands-on experience in Pine Script, continuously refining patterns, techniques, and structures until reaching its current level of maturity. Every line of code reflects this long process of improvement, resulting in a strategy that unites professional engineering, transparency, accessibility, and reliable execution.

🔶 MAIN FEATURES

• Fully automated and robust: Operates without manual intervention, ideal for traders seeking consistency and stability. It delivers reliable performance even in volatile markets thanks to the solid quantitative engineering behind the system.

• Multiple layers of confirmation: Combines 10 key technical indicators with 15 adaptive filters to avoid false signals. It only triggers entries when all trend, market strength, and contextual criteria align.

• Configurable and adaptable filters: Each of the 15 filters can be enabled, disabled, or adjusted by the user, allowing the creation of personalized statistical models for different assets and timeframes. This flexibility gives full freedom to optimize the strategy according to individual preferences.

• Clear and accessible logic: All entry and exit conditions are explicitly shown within the TradingView parameters. The strategy has no hidden components—any user can quickly analyze and understand each part of the system.

• Integrated exclusive tools: Includes complete backtest tables (desktop and mobile versions) with annualized statistics, along with real-time entry conditions displayed directly on the chart. These tools help monitor the strategy across devices and track performance and risk metrics.

• No repaint: All signals are static and do not change after being plotted. This ensures the trader can trust every entry shown without worrying about indicators rewriting past values.

🔷 ENTRY CONDITIONS & RISK MANAGEMENT

Red Dragon Model 1 triggers buy (long) or sell (short) signals only when all configured conditions are satisfied. For example:

• Volume:

• The system only trades when current volume exceeds the volume moving average multiplied by a user-defined factor, indicating meaningful market participation.

• RSI:

• Confirms bullish bias when RSI crosses above its moving average, and bearish bias when crossing below.

• ADX:

• Enters long when +DI is above –DI with ADX above a defined threshold, indicating directional strength to the upside (and the opposite conditions for shorts).

• Other indicators (MACD, SAR, Ichimoku, Support/Resistance, etc.)

Each one must confirm the expected direction before a final signal is allowed.

When all bullish criteria are met simultaneously, the system enters Long; when all criteria indicate a bearish environment, the system enters Short.

In addition, the strategy uses fixed Take Profit and Stop Loss targets for risk control:

Currently: TP around 1.5% and SL around 2.0% per trade, ensuring consistent and transparent risk management on every position.

⚙️ INDICATORS

__________________________________________________________

1) 🔊 Volume: Avoids trading on flat charts.

2) 🍟 MACD: Tracks momentum through moving averages.

3) 🧲 RSI: Indicates overbought or oversold conditions.

4) 🅰️ ADX: Measures trend strength and potential entry points.

5) 🥊 SAR: Identifies changes in price direction.

6) ☁️ Cloud: Accurately detects changes in market trends.

7) 🌡️ R/F: Improves trend visualization and helps avoid pitfalls.

8) 📐 S/R: Fixed support and resistance levels.

9)╭╯MA: Moving Averages.

10) 🔮 LR: Forecasting using Linear Regression.

__________________________________________________________

🟢 ENTRY CONDITIONS 🔴

__________________________________________________________

IF all conditions are 🟢 = 📈 Long

IF all conditions are 🔴 = 📉 Short

__________________________________________________________

🚨 CURRENT TRIGGER SIGNAL 🚨

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🟢 ALL ENTRY CONDITIONS AVAILABLE 🔴

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult) and (close) > (open)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult) and (close) < (open)

🍟 MACD

🟢 LONG = (MACD) > (Signal Smoothing)

🔴 SHORT = (MACD) < (Signal Smoothing)

🧲 RSI

🟢 LONG = (RSI) < (Upper)

🔴 SHORT = (RSI) > (Lower)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🅰️ ADX

🟢 LONG = (+DI) > (-DI) and (ADX) > (Treshold)

🔴 SHORT = (+DI) < (-DI) and (ADX) > (Treshold)

🥊 SAR

🟢 LONG = (close) > (SAR)

🔴 SHORT = (close) < (SAR)

☁️ Cloud

🟢 LONG = (Cloud A) > (Cloud B)

🔴 SHORT = (Cloud A) < (Cloud B)

☁️ Cloud

🟢 LONG = (Kama) > (Kama )

🔴 SHORT = (Kama) < (Kama )

🌡️ R/F

🟢 LONG = (high) > (UP Range) and (upward) > (0)

🔴 SHORT = (low) < (DOWN Range) and (downward) > (0)

🌡️ R/F

🟢 LONG = (high) > (UP Range)

🔴 SHORT = (low) < (DOWN Range)

📐 S/R

🟢 LONG = (close) > (Resistance)

🔴 SHORT = (close) < (Support)

╭╯MA2️⃣

🟢 LONG = (Cyan Bar MA2️⃣)

🔴 SHORT = (Red Bar MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (close) > (MA2️⃣)

🔴 SHORT = (close) < (MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (Positive MA2️⃣)

🔴 SHORT = (Negative MA2️⃣)

__________________________________________________________

🎯 TP / SL 🛑

__________________________________________________________

🎯 TP: 1.5 %

🛑 SL: 2.0 %

__________________________________________________________

🪄 UNIQUE FEATURES OF THIS STRATEGY

____________________________________

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

_____________________________

𝄜 BACKTEST / PERFORMANCE 𝄜

_____________________________

• Net Profit: +634.47%, Maximum Drawdown: -18.44%.

🪙 PAIR / TIMEFRAME ⏳

🪙 PAIR: BINANCE:BTCUSDT.P

⏳ TIME: 4 hours (240m)

✅ ON ☑️ OFF

✅ LONG

✅ SHORT

🎯 TP / SL 🛑

🎯 TP: 1.5 (%)

🛑 SL: 2.0 (%)

⚙️ CAPITAL MANAGEMENT

💸 Initial Capital: 10000 $ (TradingView)

💲 Order Size: 10 % (Of Equity)

🚀 Leverage: 10 x (Exchange)

💩 Commission: 0.03 % (Exchange)

📆 BACKTEST

🗓️ Start: Setember 24, 2019

🗓️ End: November 21, 2025

🗓️ Days: 2250

🗓️ Yers: 6.17

🗓️ Bars: 13502

📊 PERFORMANCE

💲 Net Profit: + 63446.89 $

🟢 Net Profit: + 634.47 %

💲 DrawDown Maximum: - 10727.48 $

🔴 DrawDown Maximum: - 18.44 %

🟢 Total Closed Trades: 1042

🟡 Percent Profitable: 63.92 %

🟡 Profit Factor: 1.247

💲 Avg Trade: + 60.89 $

⏱️ Avg # Bars in Trades

🕯️ Avg # Bars: 4

⏳ Avg # Hrs: 15

✔️ Trades Winning: 666

❌ Trades Losing: 376

✔️ Maximum Consecutive Wins: 11

❌ Maximum Consecutive Losses: 7

📺 Live Performance : br.tradingview.com

• Use this strategy on the recommended pair and timeframe above to replicate the tested results.

• Feel free to experiment and explore other settings, assets, and timeframes.

CongTrader Strategy V1📈 CongTrader Strategy V1 — Official Overview

CongTrader Strategy V1 is a precision-built algorithm designed for intraday and swing traders who want a structured, rules-driven approach to capturing directional momentum while avoiding low-quality market conditions.

This strategy combines volatility-based logic, trend confirmation filters, and a market-conditioning engine to produce high-probability long and short signals with strictly candle-close confirmed entries (no intrabar repainting).

🔍 Core Philosophy

Modern markets move in bursts of volatility that are often preceded by subtle shifts in momentum and structure.

CongTrader V1 is engineered to:

identify emerging directional pressure early

filter out noise, consolidation, and choppy environments

only execute when multiple conditions align

maintain consistent, disciplined trade management

The result is a strategy that aims to trade quality over quantity, focusing on clear, structured setups rather than impulsive, intrabar signals.

🧠 Key Components (High-Level Explanation)

1️⃣ Directional Signal Engine (Trigger System)

The strategy uses a custom momentum-oscillation model to detect potential turning points and trend continuations.

This engine smooths price action, measures pressure extremes, and generates trigger crossovers that signal potential long or short opportunities.

(The exact formula and coefficients are proprietary and not displayed.)

2️⃣ ATR-Based Risk Management

Each trade is automatically paired with:

a volatility-adaptive stop loss, and

a volatility-adaptive profit target

This allows the strategy to adjust position management dynamically based on current market movement rather than fixed pip or dollar distances.

3️⃣ Trend Confirmation Filter (EMA)

A long-term EMA trend filter prevents counter-trend entries by ensuring:

Long positions trade only above trend

Short positions trade only below trend

This keeps signals aligned with higher-timeframe momentum.

4️⃣ VWAP Institutional Bias Filter

VWAP is used as a dynamic market fair-value reference.

The strategy only trades when price action shows favorable positioning relative to VWAP—helping avoid false moves and mean-reversion traps.

5️⃣ Range & Volatility Filter

A volatility/range filter avoids entering during tight consolidations.

If the market is not moving or lacks range expansion, the strategy waits patiently.

This significantly reduces chop and whipsaw trades.

6️⃣ RTH (Regular Trading Hours) Protection

Optionally limits trades to regular exchange hours for traders who avoid low-liquidity overnight sessions.

⏳ Candle-Close Entry Confirmation (No Repainting)

All entries are strictly confirmed after the bar closes, which means:

No intrabar fakeouts

No signal disappearance

No repainting

Cleaner, more realistic backtesting

This ensures the strategy behaves the same in backtests and in live charts.

🎯 Trade Logic Summary

A trade is only taken when:

✔ A directional trigger signal occurs

✔ Price meets VWAP bias conditions

✔ Price aligns with the long-term trend

✔ Sufficient volatility/range is present

✔ (Optional) Within regular trading hours

✔ The candle has fully confirmed

Every trade is managed automatically with ATR-based stop loss and take profit placement.

📊 Who This Strategy Is For

CongTrader V1 works well for:

Intraday traders (1–15m)

Swing traders (30m–4h)

Momentum and trend-followers

Algorithmic traders looking for disciplined, rules-based entries

Traders who want cleaner signals and less noise

Anyone who wants to avoid low-quality, choppy markets

🔔 Alerts Included

Built-in alerts notify you instantly when conditions for long or short entries are met, making it suitable for:

Manual execution

Automated trading systems

Signal services

🧩 Important Note

This strategy is designed for educational purposes and is not financial advice. Performance may vary depending on market conditions, broker feed, and instrument volatility. Always backtest thoroughly and use risk management.

SP500 Session Gap Fade StrategySummary in one paragraph

SPX Session Gap Fade is an intraday gap fade strategy for index futures, designed around regular cash sessions on five minute charts. It helps you participate only when there is a full overnight or pre session gap and a valid intraday session window, instead of trading every open. The original part is the gap distance engine which anchors both stop and optional target to the previous session reference close at a configurable flat time, so every trade’s risk scales with the actual gap size rather than a fixed tick stop.

Scope and intent

• Markets. Primarily index futures such as ES, NQ, YM, and liquid index CFDs that exhibit overnight gaps and regular cash hours.

• Timeframes. Intraday timeframes from one minute to fifteen minutes. Default usage is five minute bars.

• Default demo used in the publication. Symbol CME:ES1! on a five minute chart.

• Purpose. Provide a simple, transparent way to trade opening gaps with a session anchored risk model and forced flat exit so you are not holding into the last part of the session.

• Limits. This is a strategy. Orders are simulated on standard candles only.

Originality and usefulness

• Unique concept or fusion. The core novelty is the combination of a strict “full gap” entry condition with a session anchored reference close and a gap distance based TP and SL engine. The stop and optional target are symmetric multiples of the actual gap distance from the previous session’s flat close, rather than fixed ticks.

• Failure mode it addresses. Fixed sized stops do not scale when gaps are unusually small or unusually large, which can either under risk or over risk the account. The session flat logic also reduces the chance of holding residual positions into late session liquidity and news.

• Testability. All key pieces are explicit in the Inputs: session window, minutes before session end, whether to use gap exits, whether TP or SL are active, and whether to allow candle based closes and forced flat. You can toggle each component and see how it changes entries and exits.

• Portable yardstick. The main unit is the absolute price gap between the entry bar open and the previous session reference close. tp_mult and sl_mult are multiples of that gap, which makes the risk model portable across contracts and volatility regimes.

Method overview in plain language

The strategy first defines a trading session using exchange time, for example 08:30 to 15:30 for ES day hours. It also defines a “flat” time a fixed number of minutes before session end. At the flat bar, any open position is closed and the bar’s close price is stored as the reference close for the next session. Inside the session, the strategy looks for a full gap bar relative to the prior bar: a gap down where today’s high is below yesterday’s low, or a gap up where today’s low is above yesterday’s high. A full gap down generates a long entry; a full gap up generates a short entry. If the gap risk engine is enabled and a valid reference close exists, the strategy measures the distance between the entry bar open and that reference close. It then sets a stop and optional target as configurable multiples of that gap distance and manages them with strategy.exit. Additional exits can be triggered by a candle color flip or by the forced flat time.

Base measures

• Range basis. The main unit is the absolute difference between the current entry bar open and the stored reference close from the previous session flat bar. That value is used as a “gap unit” and scaled by tp_mult and sl_mult to build the target and stop.

Components

• Component one: Gap Direction. Detects full gap up or full gap down by comparing the current high and low to the previous bar’s high and low. Gap down signals a long fade, gap up signals a short fade. There is no smoothing; it is a strict structural condition.

• Component two: Session Window. Only allows entries when the current time is within the configured session window. It also defines a flat time before the session end where positions are forced flat and the reference close is updated.

• Component three: Gap Distance Risk Engine. Computes the absolute distance between the entry open and the stored reference close. The stop and optional target are placed as entry ± gap_distance × multiplier so that risk scales with gap size.

• Optional component: Candle Exit. If enabled, a bullish bar closes short positions and a bearish bar closes long positions, which can shorten holding time when price reverses quickly inside the session.

• Session windows. Session logic uses the exchange time of the chart symbol. When changing symbols or venues, verify that the session time string still matches the new instrument’s cash hours.

Fusion rule

All gates are hard conditions rather than weighted scores. A trade can only open if the session window is active and the full gap condition is true. The gap distance engine only activates if a valid reference close exists and use_gap_risk is on. TP and SL are controlled by separate booleans so you can use SL only, TP only, or both. Long and short are symmetric by construction: long trades fade full gap downs, short trades fade full gap ups with mirrored TP and SL logic.

Signal rule

• Long entry. Inside the active session, when the current bar shows a full gap down relative to the previous bar (current high below prior low), the strategy opens a long position. If the gap risk engine is active, it places a gap based stop below the entry and an optional target above it.

• Short entry. Inside the active session, when the current bar shows a full gap up relative to the previous bar (current low above prior high), the strategy opens a short position. If the gap risk engine is active, it places a gap based stop above the entry and an optional target below it.

• Forced flat. At the configured flat time before session end, any open position is closed and the close price of that bar becomes the new reference close for the following session.

• Candle based exit. If enabled, a bearish bar closes longs, and a bullish bar closes shorts, regardless of where TP or SL sit, as long as a position is open.

What you will see on the chart

• Markers on entry bars. Standard strategy entry markers labeled “long” and “short” on the gap bars where trades open.

• Exit markers. Standard exit markers on bars where either the gap stop or target are hit, or where a candle exit or forced flat close occurs. Exit IDs “long_gap” and “short_gap” label gap based exits.

• Reference levels. Horizontal lines for the current long TP, long SL, short TP, and short SL while a position is open and the gap engine is enabled. They update when a new trade opens and disappear when flat.

• Session background. This version does not add background shading for the session; session logic runs internally based on time.

• No on chart table. All decisions are visible through orders and exit levels. Use the Strategy Tester for performance metrics.

Inputs with guidance

Session Settings

• Trading session (sess). Session window in exchange time. Typical value uses the regular cash session for each contract, for example “0830-1530” for ES. Adjust if your broker or symbol uses different hours.

• Minutes before session end to force exit (flat_before_min). Minutes before the session end where positions are forced flat and the reference close is stored. Typical range is 15 to 120. Raising it closes trades earlier in the day; lowering it allows trades later in the session.

Gap Risk

• Enable gap based TP/SL (use_gap_risk). Master switch for the gap distance exit engine. Turning it off keeps entries and forced flat logic but removes automatic TP and SL placement.

• Use TP limit from gap (use_gap_tp). Enables gap based profit targets. Typical values are true for structured exits or false if you want to manage exits manually and only keep a stop.

• Use SL stop from gap (use_gap_sl). Enables gap based stop losses. This should normally remain true so that each trade has a defined initial risk in ticks.

• TP multiplier of gap distance (tp_mult). Multiplier applied to the gap distance for the target. Typical range is 0.5 to 2.0. Raising it places the target further away and reduces hit frequency.

• SL multiplier of gap distance (sl_mult). Multiplier applied to the gap distance for the stop. Typical range is 0.5 to 2.0. Raising it widens the stop and increases risk per trade; lowering it tightens the stop and may increase the number of small losses.

Exit Controls

• Exit with candle logic (use_candle_exit). If true, closes shorts on bullish candles and longs on bearish candles. Useful when you want to react to intraday reversal bars even if TP or SL have not been reached.

• Force flat before session end (use_forced_flat). If true, guarantees you are flat by the configured flat time and updates the reference close. Turn this off only if you understand the impact on overnight risk.

Filters

There is no separate trend or volatility filter in this version. All trades depend on the presence of a full gap bar inside the session. If you need extra filtering such as ATR, volume, or higher timeframe bias, they should be added explicitly and documented in your own fork.

Usage recipes

Intraday conservative gap fade

• Timeframe. Five minute chart on ES regular session.

• Gap risk. use_gap_risk = true, use_gap_tp = true, use_gap_sl = true.

• Multipliers. tp_mult around 0.7 to 1.0 and sl_mult around 1.0.

• Exits. use_candle_exit = false, use_forced_flat = true. Focus on the structured TP and SL around the gap.

Intraday aggressive gap fade

• Timeframe. Five minute chart.

• Gap risk. use_gap_risk = true, use_gap_tp = false, use_gap_sl = true.

• Multipliers. sl_mult around 0.7 to 1.0.